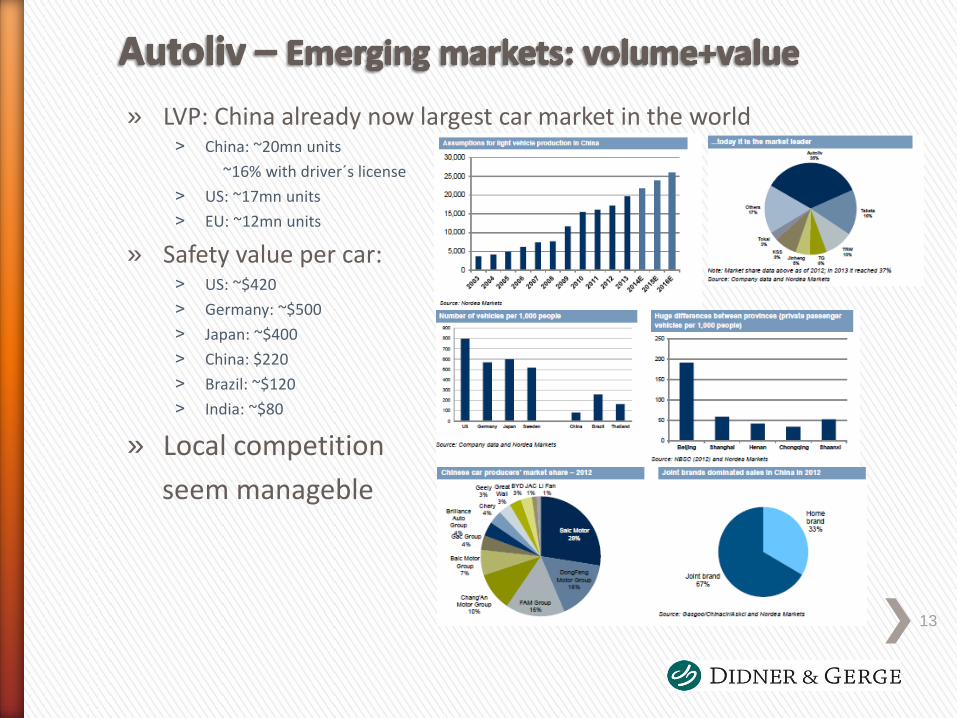

Embed Size (px)

Citation preview

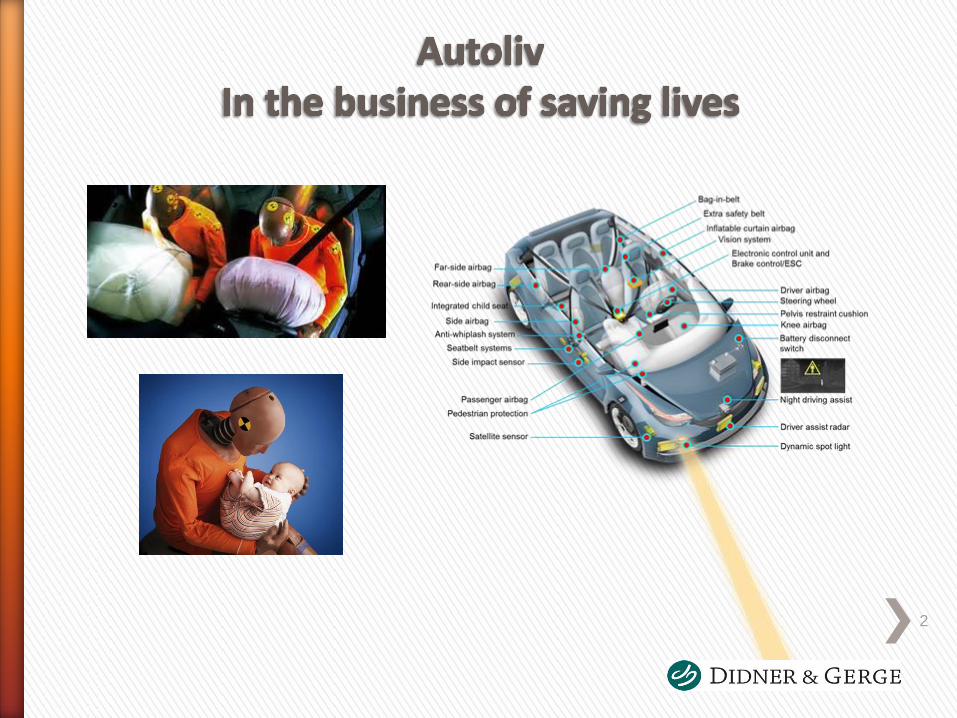

Active investing – it makes a difference

Henrik Andersson

2

3

Outstanding business

Are these companies really…

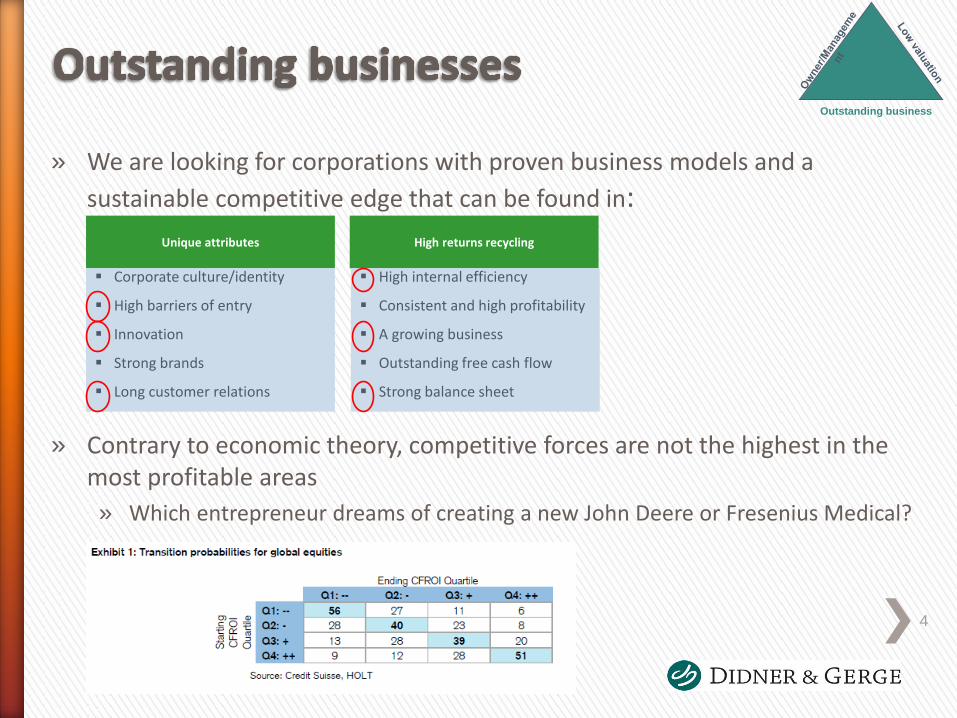

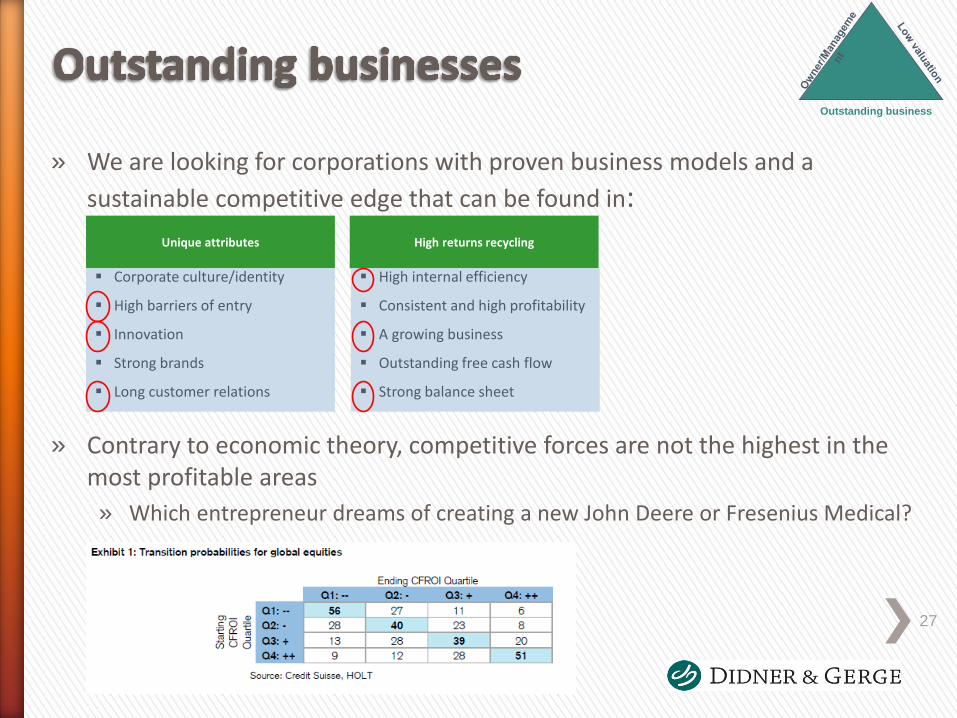

» We are looking for corporations with proven business models and a

sustainable competitive edge that can be found in:

» Contrary to economic theory, competitive forces are not the highest in the

most profitable areas

» Which entrepreneur dreams of creating a new John Deere or Fresenius Medical?

Unique attributes

Corporate culture/identity

High barriers of entry

Innovation

Strong brands

Long customer relations

High returns recycling

High internal efficiency

Consistent and high profitability

A growing business

Outstanding free cash flow

Strong balance sheet

4

Outstanding business

5

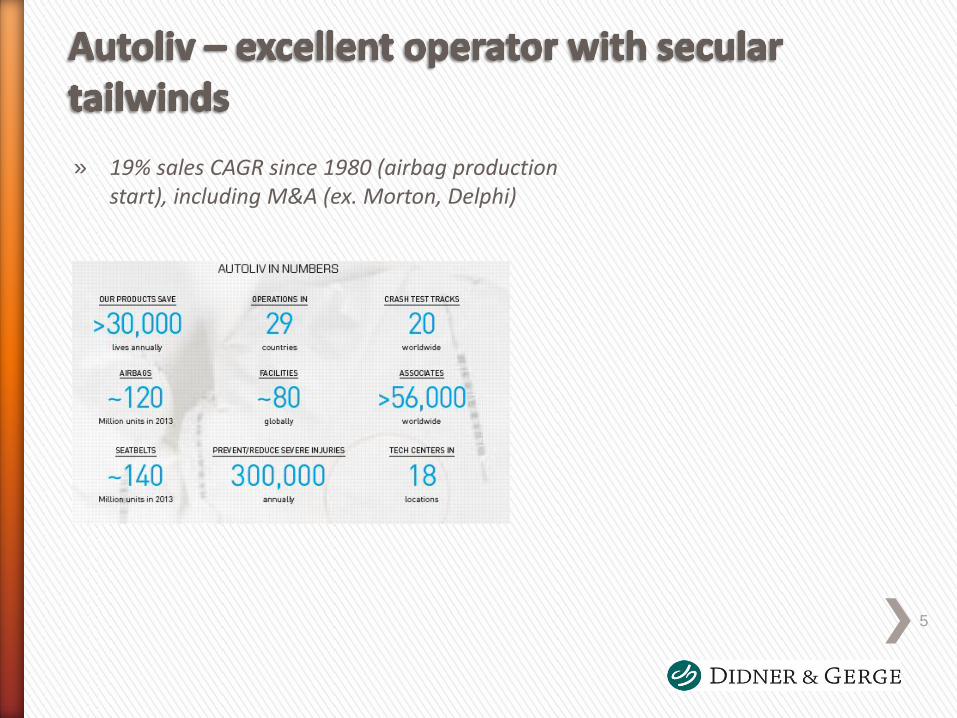

» 19% sales CAGR since 1980 (airbag production start), including M&A (ex. Morton, Delphi)

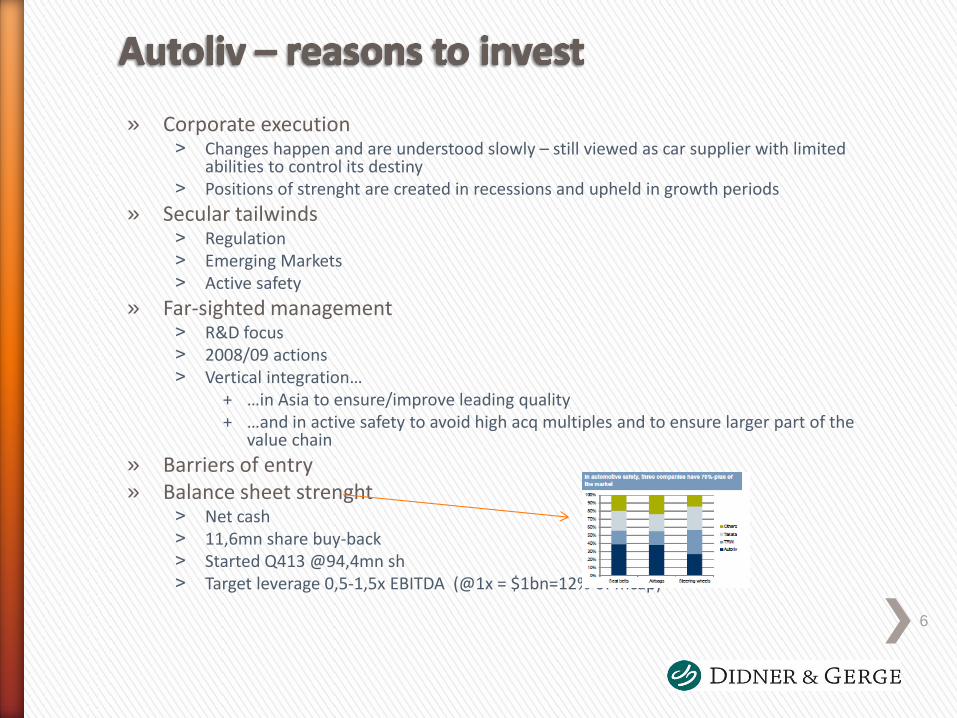

» Corporate execution ˃ Changes happen and are understood slowly – still viewed as car supplier with limited

abilities to control its destiny ˃ Positions of strenght are created in recessions and upheld in growth periods

» Secular tailwinds ˃ Regulation ˃ Emerging Markets ˃ Active safety

» Far-sighted management ˃ R&D focus ˃ 2008/09 actions ˃ Vertical integration…

+ …in Asia to ensure/improve leading quality + …and in active safety to avoid high acq multiples and to ensure larger part of the

value chain

» Barriers of entry » Balance sheet strenght

˃ Net cash ˃ 11,6mn share buy-back ˃ Started Q413 @94,4mn sh ˃ Target leverage 0,5-1,5x EBITDA (@1x = $1bn=12% of mcap)

6

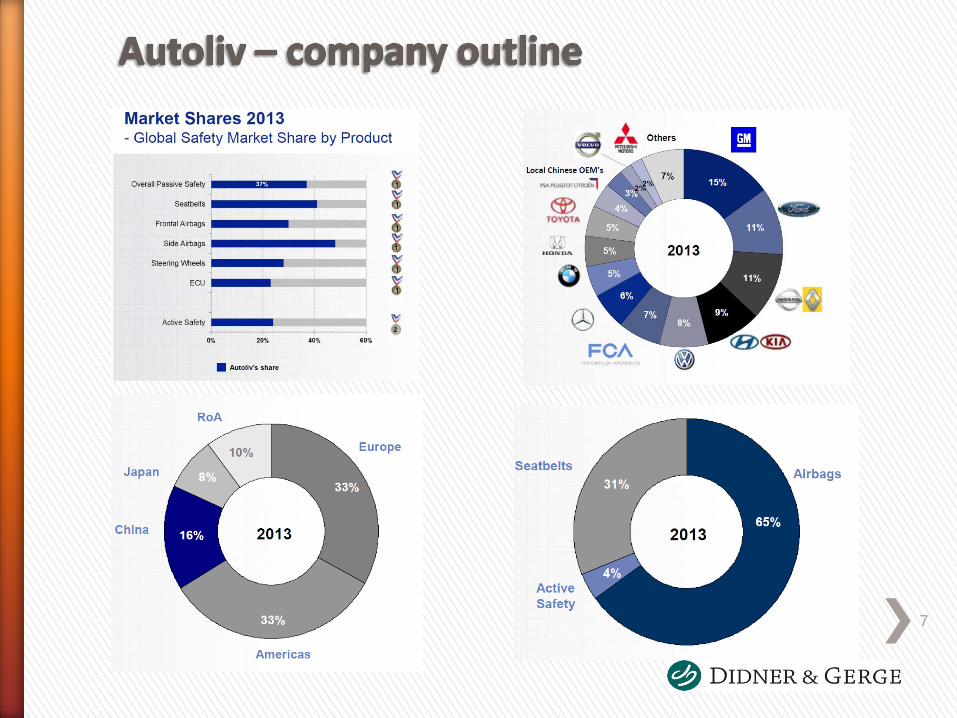

» xx

7

» 1953: Company founded by Lennart & Stig Lindblad as a repair shop

» 1956: First seatbelt launched (Renault, GM)

» 1968: Company name changed to Autoliv

» 1975: Autoliv acquired by Gränges, that

previously developed the seatbelt retractor

» 1980: Gränges/Autoliv becomes part of Electrolux

» 1980: Airbag production starts (after about a decade´s R&D)

» 1989: First JV in China (Nanjing, seatbelts)

» 1993: Autoliv listed on Stockholm Stock Exchange

» 1994: Merger with Morton ASP, the leading NA and Asian player

» 2002: Visteon Restrain Electronics acquired

» 2008: Acquisition of Tyco´s radar business

» 2009: Acquisition of Delphi´s passive safety business

8

9

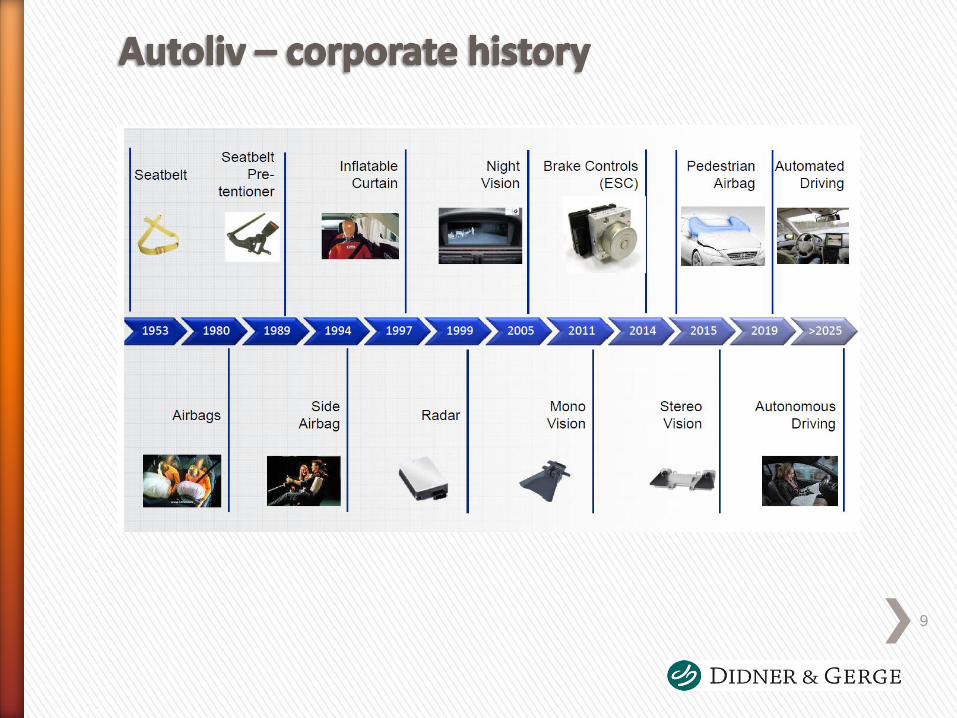

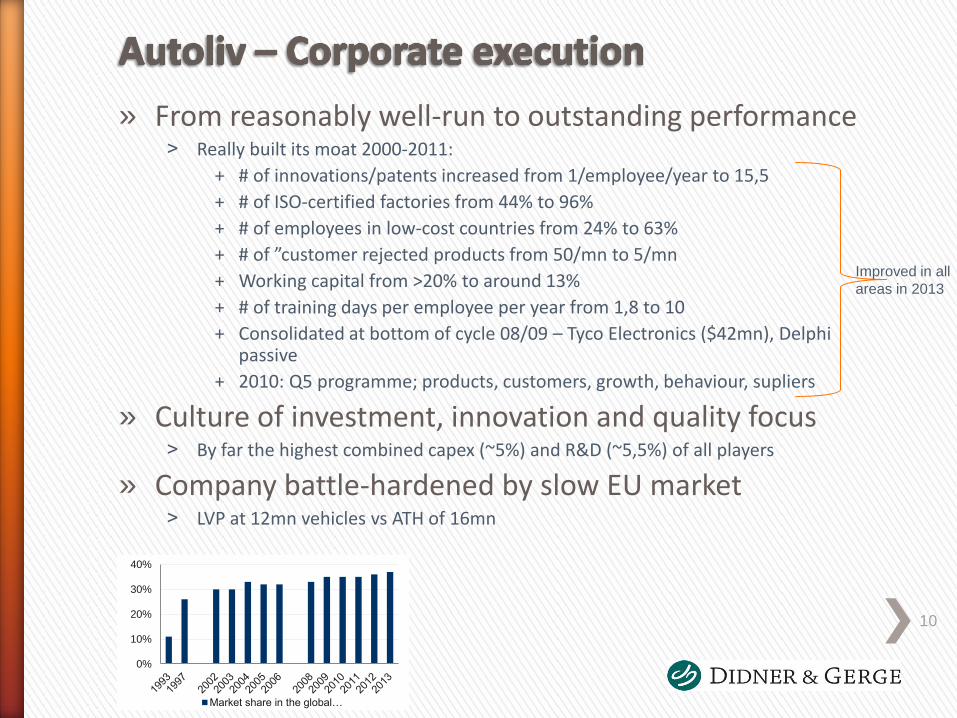

» From reasonably well-run to outstanding performance ˃ Really built its moat 2000-2011:

+ # of innovations/patents increased from 1/employee/year to 15,5

+ # of ISO-certified factories from 44% to 96%

+ # of employees in low-cost countries from 24% to 63%

+ # of ”customer rejected products from 50/mn to 5/mn

+ Working capital from >20% to around 13%

+ # of training days per employee per year from 1,8 to 10

+ Consolidated at bottom of cycle 08/09 – Tyco Electronics ($42mn), Delphi passive

+ 2010: Q5 programme; products, customers, growth, behaviour, supliers

» Culture of investment, innovation and quality focus ˃ By far the highest combined capex (~5%) and R&D (~5,5%) of all players

» Company battle-hardened by slow EU market ˃ LVP at 12mn vehicles vs ATH of 16mn

10

0%

10%

20%

30%

40%

Market share in the global…

Improved in all

areas in 2013

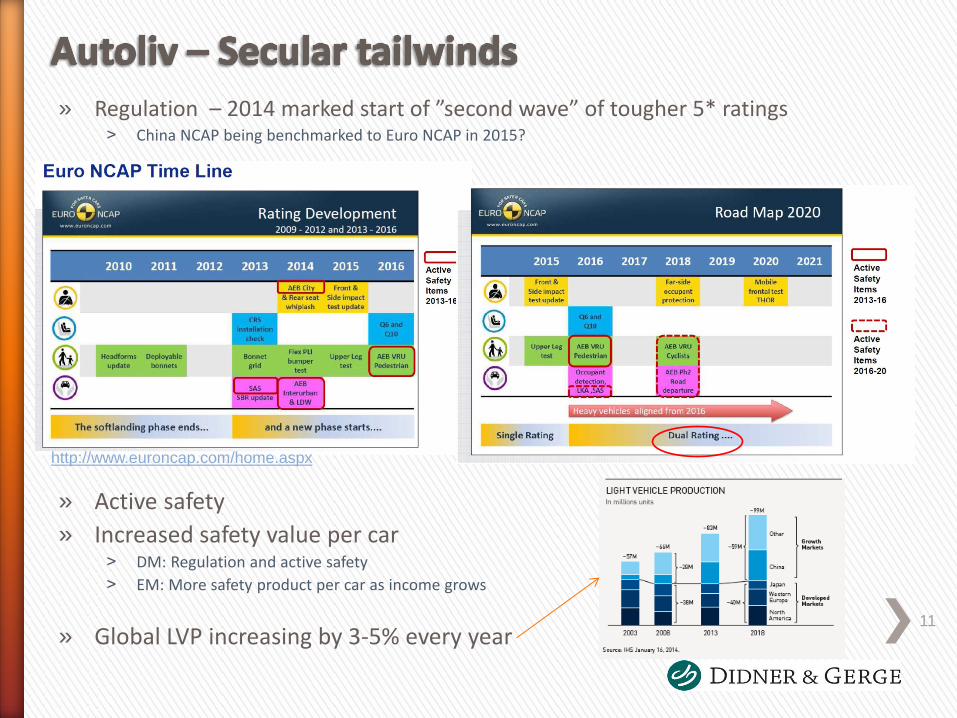

» Regulation – 2014 marked start of ”second wave” of tougher 5* ratings

˃ China NCAP being benchmarked to Euro NCAP in 2015?

» Active safety

» Increased safety value per car ˃ DM: Regulation and active safety

˃ EM: More safety product per car as income grows

» Global LVP increasing by 3-5% every year

11

http://www.euroncap.com/home.aspx

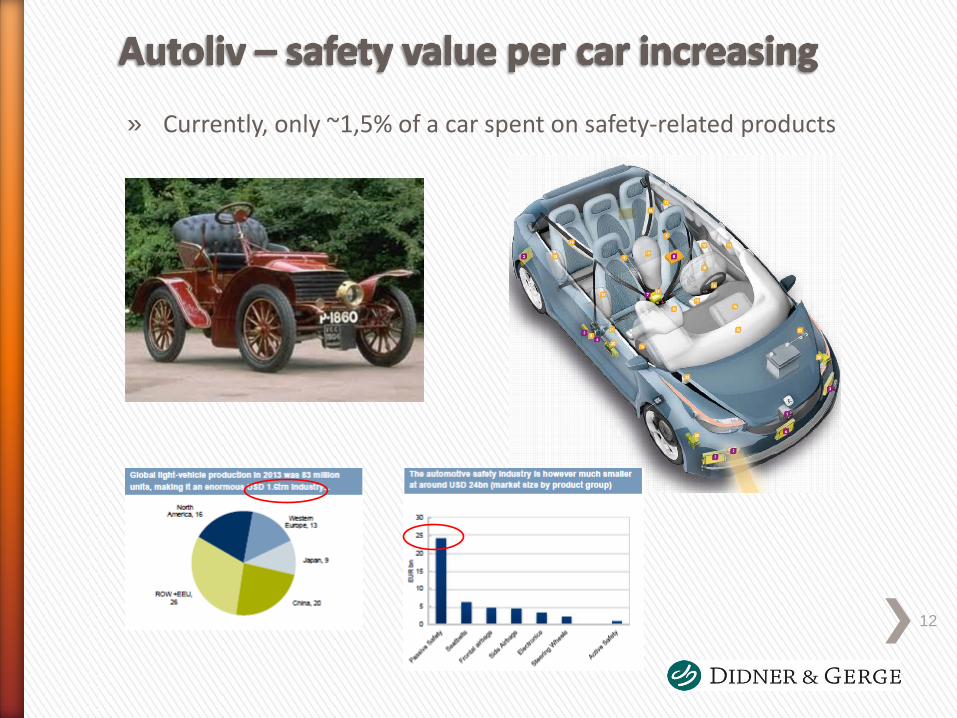

» Currently, only ~1,5% of a car spent on safety-related products

12

» LVP: China already now largest car market in the world ˃ China: ~20mn units

~16% with driver´s license

˃ US: ~17mn units

˃ EU: ~12mn units

» Safety value per car: ˃ US: ~$420

˃ Germany: ~$500

˃ Japan: ~$400

˃ China: $220

˃ Brazil: ~$120

˃ India: ~$80

» Local competition

seem manageble

13

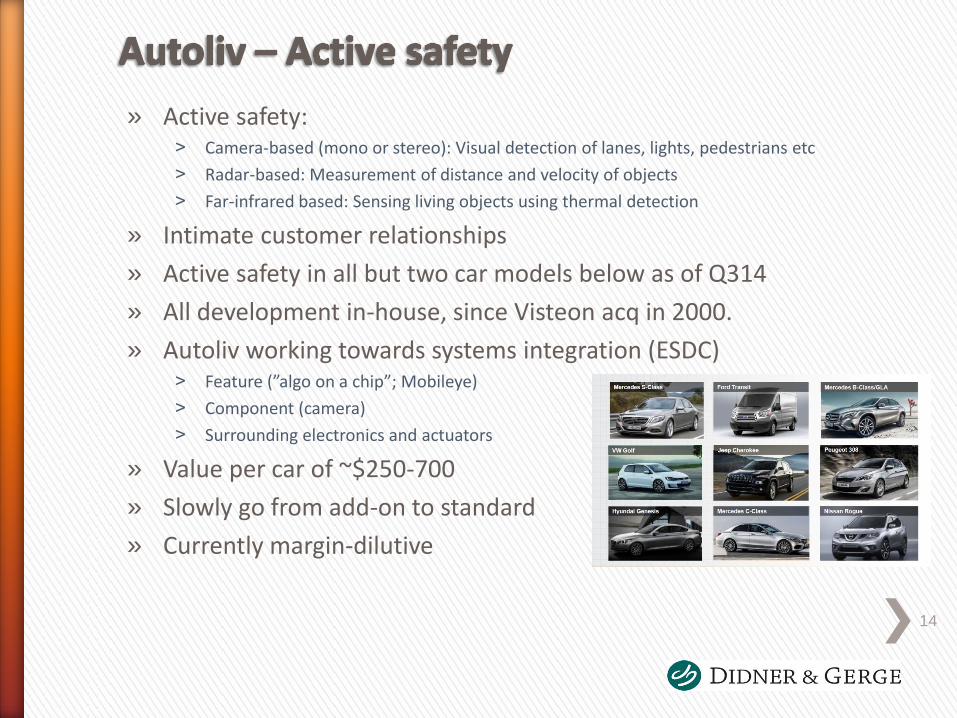

» Active safety: ˃ Camera-based (mono or stereo): Visual detection of lanes, lights, pedestrians etc

˃ Radar-based: Measurement of distance and velocity of objects

˃ Far-infrared based: Sensing living objects using thermal detection

» Intimate customer relationships

» Active safety in all but two car models below as of Q314

» All development in-house, since Visteon acq in 2000.

» Autoliv working towards systems integration (ESDC) ˃ Feature (”algo on a chip”; Mobileye)

˃ Component (camera)

˃ Surrounding electronics and actuators

» Value per car of ~$250-700

» Slowly go from add-on to standard

» Currently margin-dilutive

14

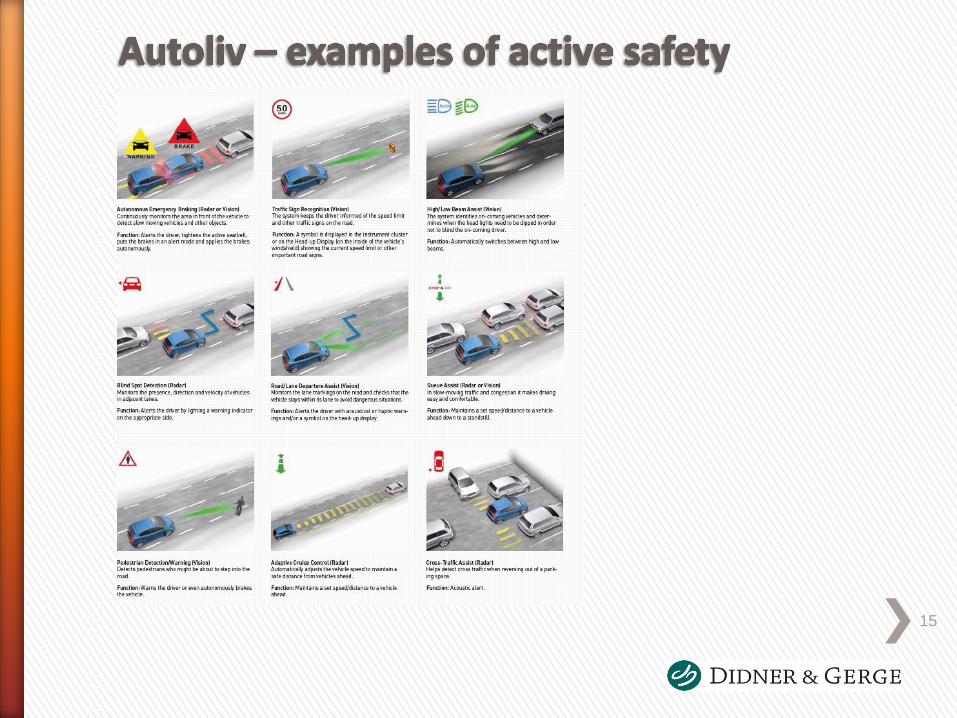

» XX

15

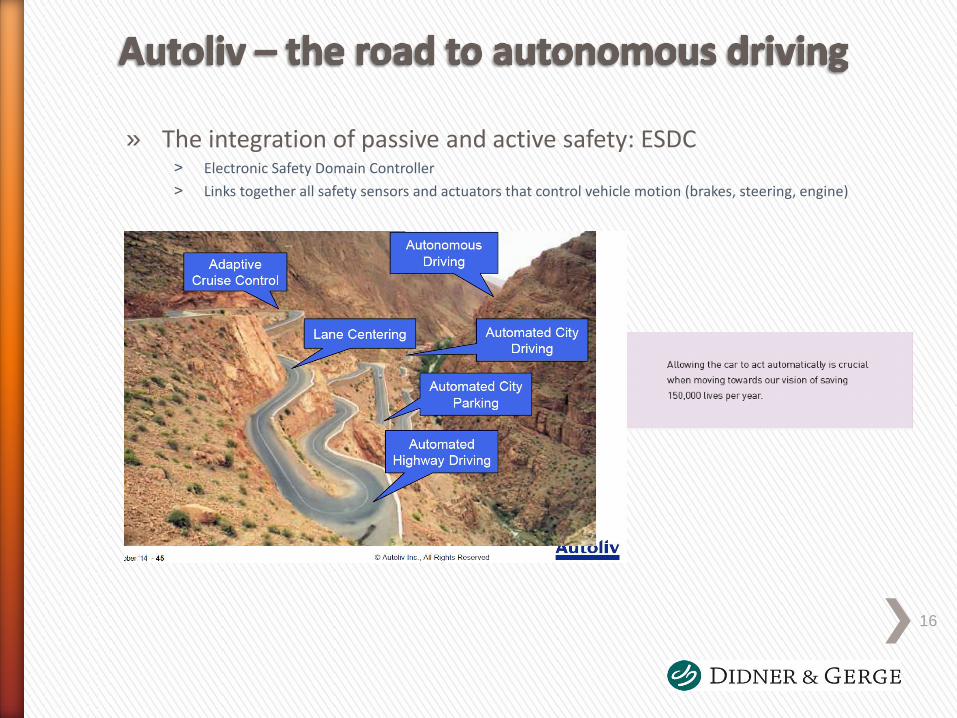

» The integration of passive and active safety: ESDC ˃ Electronic Safety Domain Controller

˃ Links together all safety sensors and actuators that control vehicle motion (brakes, steering, engine)

16

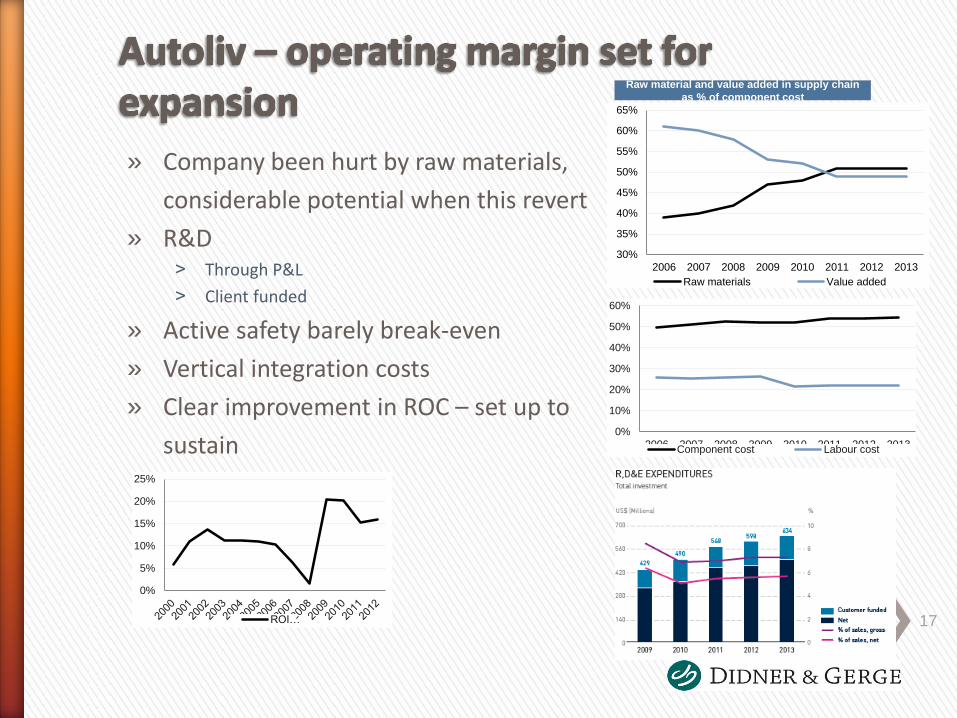

» Company been hurt by raw materials,

considerable potential when this revert

» R&D ˃ Through P&L

˃ Client funded

» Active safety barely break-even

» Vertical integration costs

» Clear improvement in ROC – set up to

sustain

17

30%

35%

40%

45%

50%

55%

60%

65%

2006 2007 2008 2009 2010 2011 2012 2013

Raw materials Value added

Raw material and value added in supply chain

as % of component cost

0%

10%

20%

30%

40%

50%

60%

2006 2007 2008 2009 2010 2011 2012 2013Component cost Labour cost

0%

5%

10%

15%

20%

25%

ROI…

» xx

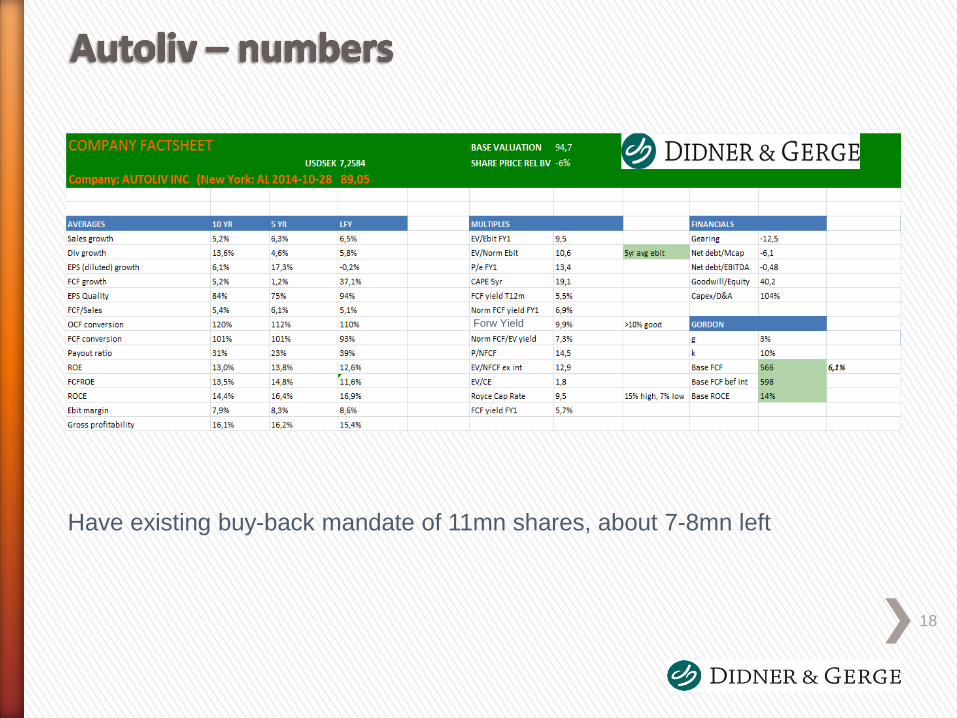

18

Forw Yield

Have existing buy-back mandate of 11mn shares, about 7-8mn left

We strive for a conservative, consistent, entry-price (our ”base”)

Establish a sustainable number across the business cycle

Could finance other ideas at 40-50% above BV

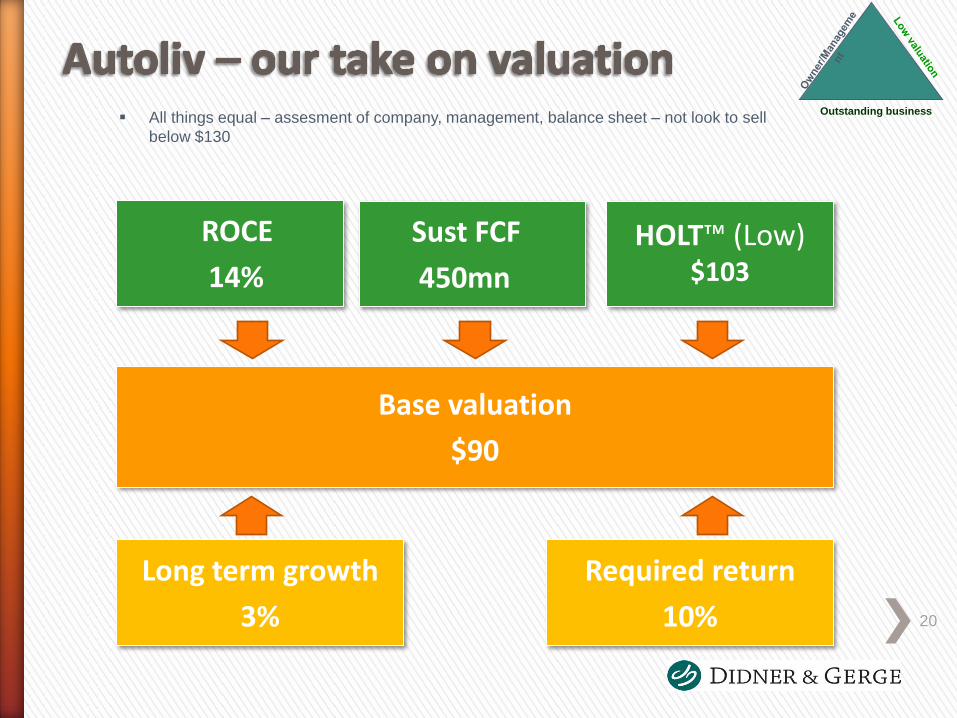

Return on capital

Sustainable free cash flow

HOLT™

Base valuation

Long term growth Required return 19

Outstanding business

ROCE

14%

Sust FCF

450mn

HOLT™ (Low) $103

Base valuation

$90

Long term growth

3%

Required return

10% 20

Outstanding business All things equal – assesment of company, management, balance sheet – not look to sell

below $130

» Slower short-term growth due to slowing Chinese car market

» Investment phase, both through P&L (R&D) and capex ˃ FCF 2014 significantly below last year´s level?

» Somewhat rigid margin structure, with GM at 20%

» Somewhat restrictive with financial information ˃ Do not disclose margins per geography

˃ Important car models?

21

Active investing – it makes a difference

Appendix

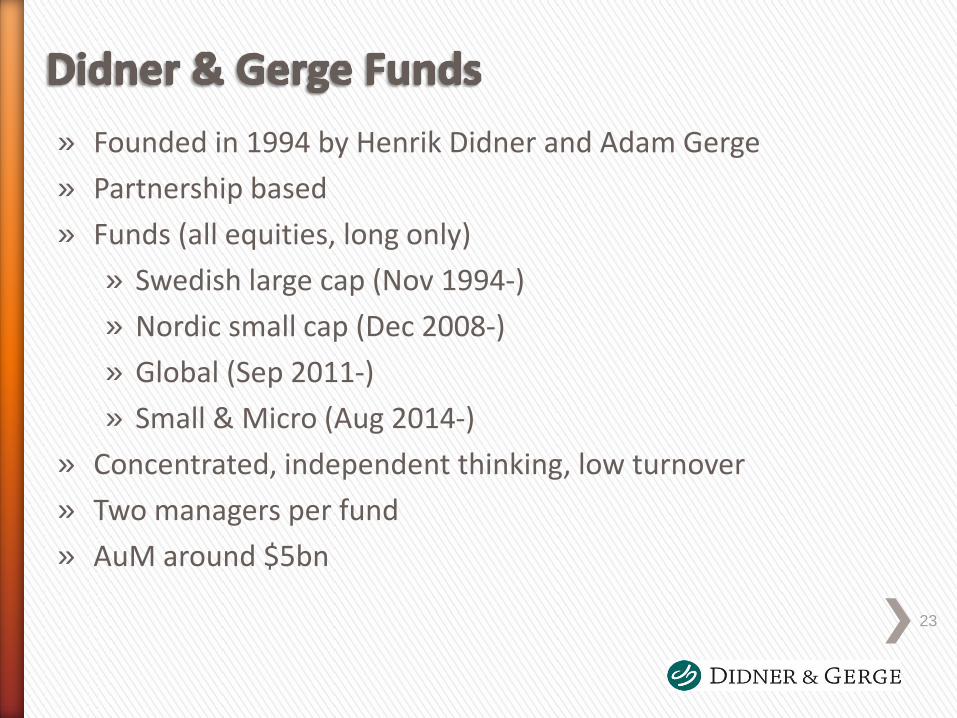

» Founded in 1994 by Henrik Didner and Adam Gerge

» Partnership based

» Funds (all equities, long only)

» Swedish large cap (Nov 1994-)

» Nordic small cap (Dec 2008-)

» Global (Sep 2011-)

» Small & Micro (Aug 2014-)

» Concentrated, independent thinking, low turnover

» Two managers per fund

» AuM around $5bn

23

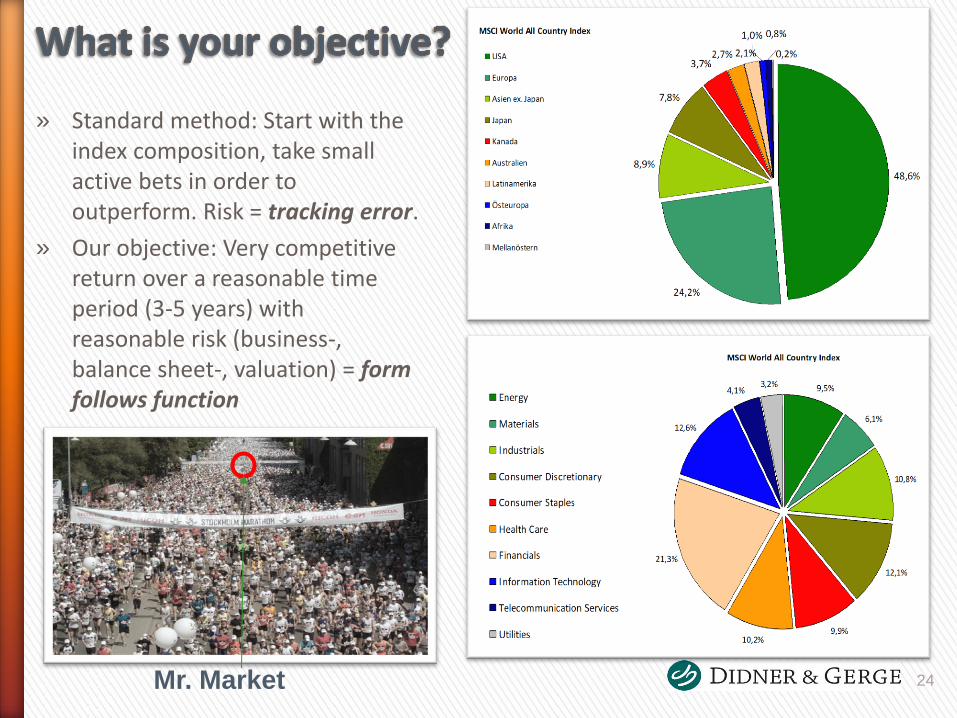

» Standard method: Start with the index composition, take small active bets in order to outperform. Risk = tracking error.

» Our objective: Very competitive return over a reasonable time period (3-5 years) with reasonable risk (business-, balance sheet-, valuation) = form follows function

Mr. Market 24

Outstanding business

”You´ve got to stand for something, otherwise you´ll fall for anything”

John C. Mellencamp

25

» ”Honey, what did you do at the office today?”

» ”Well dear, actually nothing.”

» ”But honey, weren´t you out looking for some alpha?”

26

» We are looking for corporations with proven business models and a

sustainable competitive edge that can be found in:

» Contrary to economic theory, competitive forces are not the highest in the

most profitable areas

» Which entrepreneur dreams of creating a new John Deere or Fresenius Medical?

Unique attributes

Corporate culture/identity

High barriers of entry

Innovation

Strong brands

Long customer relations

High returns recycling

High internal efficiency

Consistent and high profitability

A growing business

Outstanding free cash flow

Strong balance sheet

27

Outstanding business

» ”Not everything which can be measured counts, and not everything which counts can be measured”. Albert Einstein

» Corporate culture is often viewed as a ”soft” asset » Nonetheless, it is of crucial importance in most businesses

» Long-termism (Deere), discipline (Oaktree), honesty (Markel)

» Insurance companies, asset managers, consumer companies, industrials…

28

Outstanding business

» ”What we are looking for is honest and able management”. Warren Buffett

» ”Boards don´t look for dobermans, they look for cocker spaniels”. W Buffett

» An articulated vision of where they see the company in 5 years » Do they view shareholders as partners or minorities to manipulate?

» Evidence of sensible capital allocation

» Direct ownership

» A great mgmt team can lower the required return by 3%*

» Management meetings – not a requirement » According to a survey, 76% of investors meet management prior to investing

(source: Rivel Intelligence Council, Jan2014)

» According to the same study, investors want management to allocate a maximum of 10% of their time to investor meetings.

29

* According to a study by Richard Taffler, Warwick Business School, 2014

Outstanding business

Active investing – it makes a difference

![Religious Organizations Your Company. [Your Company] can help you… ˃ Welcome more members ˃ Increase attendance ˃ Get members involved ˃ Maintain lasting](https://img.pdfslide.net/doc/110x75/56649e0e5503460f94af82fd/religious-organizations-your-company-your-company-can-help-you-welcome.jpg)

![Real Estate Your Company. [Your Company] can help you… ˃ Reach new prospects more effectively ˃ Provide instant information and updates ˃ Sell more homes](https://img.pdfslide.net/doc/110x75/56649db65503460f94aa7b86/real-estate-your-company-your-company-can-help-you-reach-new-prospects.jpg)

![Retail Industry Your Company. [Your Company] can help you… ˃ Reel in more first-time shoppers ˃ Boost repeat customer visits ˃ Bring in shoppers during](https://img.pdfslide.net/doc/110x75/56649e4b5503460f94b4077e/retail-industry-your-company-your-company-can-help-you-reel-in-more.jpg)