Embed Size (px)

Citation preview

Please see pages 17-20 for Important Disclosures 1

Na

tio

na

l S

ec

urit

ies

Re

se

arc

h Established 1947, Member FINRA/SIPC

Technology

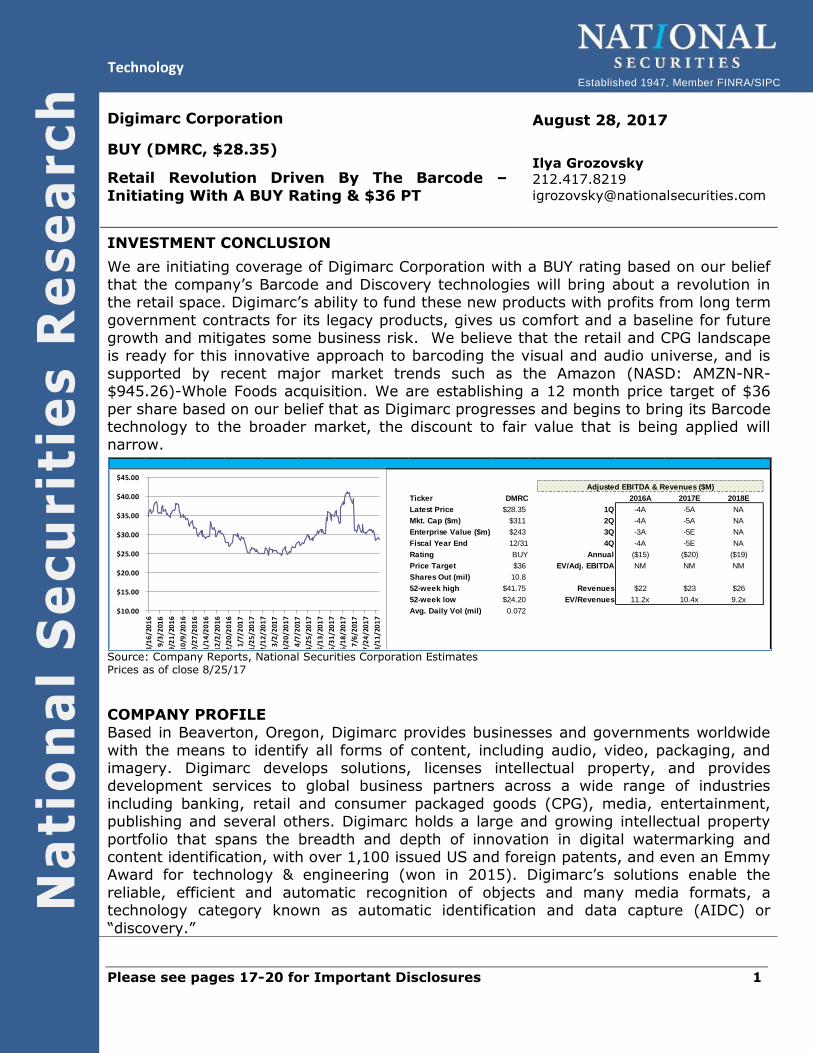

Digimarc Corporation August 28, 2017

Ilya Grozovsky

212.417.8219

BUY (DMRC, $28.35)

Retail Revolution Driven By The Barcode –

Initiating With A BUY Rating & $36 PT

INVESTMENT CONCLUSION

We are initiating coverage of Digimarc Corporation with a BUY rating based on our belief

that the company’s Barcode and Discovery technologies will bring about a revolution in the retail space. Digimarc’s ability to fund these new products with profits from long term

government contracts for its legacy products, gives us comfort and a baseline for future growth and mitigates some business risk. We believe that the retail and CPG landscape is ready for this innovative approach to barcoding the visual and audio universe, and is

supported by recent major market trends such as the Amazon (NASD: AMZN-NR-$945.26)-Whole Foods acquisition. We are establishing a 12 month price target of $36

per share based on our belief that as Digimarc progresses and begins to bring its Barcode technology to the broader market, the discount to fair value that is being applied will narrow.

Source: Company Reports, National Securities Corporation Estimates Prices as of close 8/25/17

COMPANY PROFILE

Based in Beaverton, Oregon, Digimarc provides businesses and governments worldwide

with the means to identify all forms of content, including audio, video, packaging, and imagery. Digimarc develops solutions, licenses intellectual property, and provides development services to global business partners across a wide range of industries

including banking, retail and consumer packaged goods (CPG), media, entertainment, publishing and several others. Digimarc holds a large and growing intellectual property

portfolio that spans the breadth and depth of innovation in digital watermarking and content identification, with over 1,100 issued US and foreign patents, and even an Emmy Award for technology & engineering (won in 2015). Digimarc’s solutions enable the

reliable, efficient and automatic recognition of objects and many media formats, a technology category known as automatic identification and data capture (AIDC) or

“discovery.”

Ticker DMRC 2016A 2017E 2018E

Latest Price $28.35 1Q -4A -5A NA

Mkt. Cap ($m) $311 2Q -4A -5A NA

Enterprise Value ($m) $243 3Q -3A -5E NA

Fiscal Year End 12/31 4Q -4A -5E NA

Rating BUY Annual ($15) ($20) ($19)

Price Target $36 EV/Adj. EBITDA NM NM NM

Shares Out (mil) 10.8

52-week high $41.75 Revenues $22 $23 $26

52-week low $24.20 EV/Revenues 11.2x 10.4x 9.2x

Avg. Daily Vol (mil) 0.072

Adjusted EBITDA & Revenues ($M)

$10.00

$15.00

$20.00

$25.00

$30.00

$35.00

$40.00

$45.00

8/1

6/2

01

6

9/3

/201

6

9/2

1/2

01

6

10

/9/2

01

6

10

/27

/20

16

11

/14

/20

16

12

/2/2

01

6

12

/20

/20

16

1/7

/201

7

1/2

5/2

01

7

2/1

2/2

01

7

3/2

/201

7

3/2

0/2

01

7

4/7

/201

7

4/2

5/2

01

7

5/1

3/2

01

7

5/3

1/2

01

7

6/1

8/2

01

7

7/6

/201

7

7/2

4/2

01

7

8/1

1/2

01

7

National Securities Corporation Technology

August 28, 2017 2

Digimarc Corporation participates in the watermarking space, providing protective technologies primarily to central banks. However, Digimarc is investing in barcode and discovery technologies as it plans a significant push into the retail and space and into

consumer packaged goods (CPG), which comprise short lifespan products that are typically purchased multiple times, as opposed to durable goods which last.

Implications of Amazon Whole Foods Acquisition. We believe that the June 16, 2017 announcement that Amazon is buying Whole Foods has created an expectation that Digimarc’s Barcode and SDK technologies will be the new “norm” of grocery shopping, expediting check

out and enhancing the shopping experience. Hot deal pipeline. Digimarc has made clear during previous earnings calls that it is in the

process of negotiating several deals with CPG providers that management was not able to disclose at the time. It is expected that some of these will be completed and publicized leading to a further expansion of market share for Digimarc’s product. Along with the announcement

of a growing partnership with WalMart, Digimarc is engaged in conversations with the top 10/10 major retailers.

International expansion has potential for driving increased revenue growth. Digimarc has announced in 2016 its partnership with GS1 in Germany, which will provide for greater global adoption of Digimarc’s barcode and SDK technologies in Europe. Digimarc has also

partnered with Dai Nippon Printing Co., Ltd. (DNP), SATO Corporation (SATO) and Monic Corporation (Monic) to form a Study Group, "Shopping for the Future," aimed at creating a market in Japan, in order to address the dramatic change in demographics there and how this

will affect the retail industry. Dependence on small group of customers for majority of revenue stream. A small

number of customers account for a substantial portion of Digimarc’s revenue. Therefore, we believe that the loss of any large contract could significantly disrupt the business. We believe that as Digimarc will continue to depend on this small number of customers, it will act on this

pressure to expand to different sectors over the coming years. Potential for augmented/virtual reality applications for marketing. Digimarc’s

barcoding and scanning technologies can provide visual identities that may be accessed through augmented/virtual reality platforms, such as Oculus goggles, Google Glass, Snapchat Spectacles, and others. We believe Digimarc can play a key role in this augmented reality by

providing unique visual access to products and advertisements.

We are initiating coverage of Digimarc with a BUY rating. We are initiating coverage of

Digimarc Corporation with a BUY rating based on our belief that the company’s Barcode and

Discovery technologies will bring about a revolution in the retail space. This, coupled with the unique financing structure of the company that allows it to rely on long term government contracts to fund its development of these new products over the next several years, make

this a strong stock from our perspective.

We are establishing a 12 month price target of $36 based on our DCF analysis. We

are establishing a 12 month price target of $36 per share based on our belief that as Digimarc progresses and begins to bring its Barcode technology to the broader market, the discount to

fair value that is being applied will narrow.

National Securities Corporation Technology

August 28, 2017 3

MARKET OPPORTUNITY

We believe that the current conditions for growth in Digimarc’s market share can be assessed by understanding a few different trends today. This positive investment climate

can be broken down into three themes, namely changes in retail market adoption; the potential for technological collaboration with new markets such as data analysis for entertainment and marketing; and the opportunities inherent in Digimarc’s recent moves

towards global expansion.

With regard to retail market adoption, Digimarc’s stock saw a significant rally in response to the announcement of Amazon’s acquisition of Whole Foods on June 16, 2017. This enthusiasm for Digimarc is linked to the expectation that Digimarc’s Barcode and SDK

technologies will be the new “norm” of grocery shopping with Amazon and others, expediting check out and enhancing the shopping experience. Though this initial

enthusiasm for Digimarc -- in light of the Amazon/Whole Foods acquisition -- has subsided, and there is no evidence of Digimarc working with Amazon before or after the June 2017 announcement, the excitement surrounding Digimarc in light of the deal clearly

suggests that there is an expectation of wider market adoption for advanced scanning/reading checkout systems to compete in the new age of shopping. Whether or

not Digimarc develops a direct relationship with Amazon/Whole Foods, there will be many other grocery and CPG players who would benefit from Digimarc’s products in light of

Amazon’s appetite for innovation and growing share in this marketplace. In addition to the expectation of increased market adoption of Digimarc’s barcode and

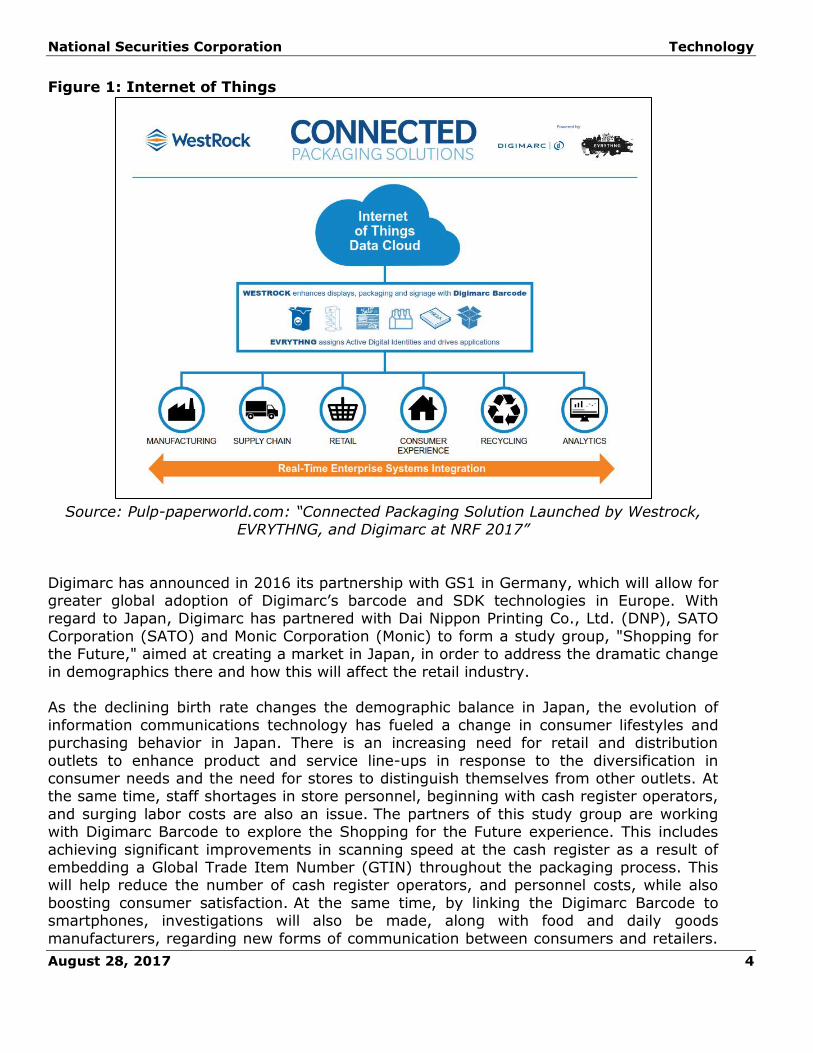

scanning technologies, we believe there is significant potential to advance the precision of data gathering techniques for analytical applications in the entertainment and retail

marketing industries. Currently, Digimarc maintains a relationship with companies WestRock and EVRYTHNG, who support analytical applications of Digimarc’s licensed software (see Figure 1 below). With regard to entertainment: According to a report

published by the Ericsson ConsumerLab in 2016, titled “TV and Media 2016,” the average American spends 1.3 years of their life time looking for which movies and shows to watch,

and likely more than that to decide which music to listen to. This challenge can be met with a combination of scanning technologies and predictive analytics that listen to and watch what you listen to and watch, which can streamline the decision-making process of

selecting a movie or song. This creates the potential for greater adoption of Digimarc’s audio/visual technologies.

In addition to streamlining consumers’ entertainment selection process, there is the potential for Digimarc’s barcoding and scanning technologies to provide visual identities

that may be accessed through augmented/virtual reality platforms, such as Oculus goggles, Google Glass, Snapchat Spectacles, or other visual enhancers that allow users to

scan their surroundings and see beyond the “naked eye.” We believe Digimarc can play a key role in this augmented reality by providing identities to store-front products or other public advertising that could be accessed through such collaborations between Digimarc

and augmented/virtual reality platforms.

Beyond the retail and technological perspectives, we believe Digimarc will soon benefit from its recent moves towards global expansion, namely in Germany and Japan.

National Securities Corporation Technology

August 28, 2017 4

Figure 1: Internet of Things

Source: Pulp-paperworld.com: “Connected Packaging Solution Launched by Westrock,

EVRYTHNG, and Digimarc at NRF 2017”

Digimarc has announced in 2016 its partnership with GS1 in Germany, which will allow for greater global adoption of Digimarc’s barcode and SDK technologies in Europe. With regard to Japan, Digimarc has partnered with Dai Nippon Printing Co., Ltd. (DNP), SATO

Corporation (SATO) and Monic Corporation (Monic) to form a study group, "Shopping for the Future," aimed at creating a market in Japan, in order to address the dramatic change

in demographics there and how this will affect the retail industry. As the declining birth rate changes the demographic balance in Japan, the evolution of

information communications technology has fueled a change in consumer lifestyles and purchasing behavior in Japan. There is an increasing need for retail and distribution

outlets to enhance product and service line-ups in response to the diversification in consumer needs and the need for stores to distinguish themselves from other outlets. At the same time, staff shortages in store personnel, beginning with cash register operators,

and surging labor costs are also an issue. The partners of this study group are working with Digimarc Barcode to explore the Shopping for the Future experience. This includes

achieving significant improvements in scanning speed at the cash register as a result of embedding a Global Trade Item Number (GTIN) throughout the packaging process. This will help reduce the number of cash register operators, and personnel costs, while also

boosting consumer satisfaction. At the same time, by linking the Digimarc Barcode to smartphones, investigations will also be made, along with food and daily goods

manufacturers, regarding new forms of communication between consumers and retailers.

National Securities Corporation Technology

August 28, 2017 5

As this research is still ongoing, we believe that the results will further advance Digimarc’s market share in Japan.

Between expected growth in retail adoption, the potential for technological collaborations with augmented reality and entertainment selection analysis, growing relationships with

the all of the top retails including WalMart, and the bold steps towards market expansion in Europe and Asia, we believe Digimarc will have the ability to diversify its client base while taking a lead in these evolving arenas.

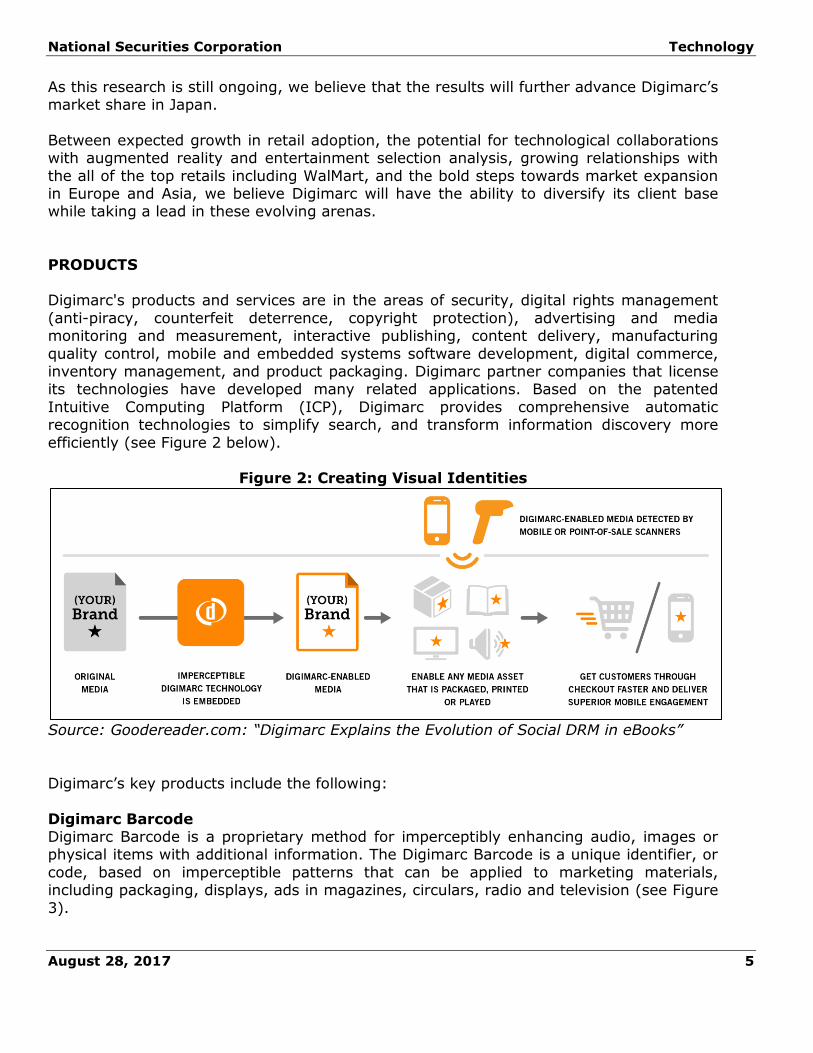

PRODUCTS Digimarc's products and services are in the areas of security, digital rights management

(anti-piracy, counterfeit deterrence, copyright protection), advertising and media monitoring and measurement, interactive publishing, content delivery, manufacturing

quality control, mobile and embedded systems software development, digital commerce, inventory management, and product packaging. Digimarc partner companies that license its technologies have developed many related applications. Based on the patented

Intuitive Computing Platform (ICP), Digimarc provides comprehensive automatic recognition technologies to simplify search, and transform information discovery more

efficiently (see Figure 2 below).

Figure 2: Creating Visual Identities

Source: Goodereader.com: “Digimarc Explains the Evolution of Social DRM in eBooks”

Digimarc’s key products include the following:

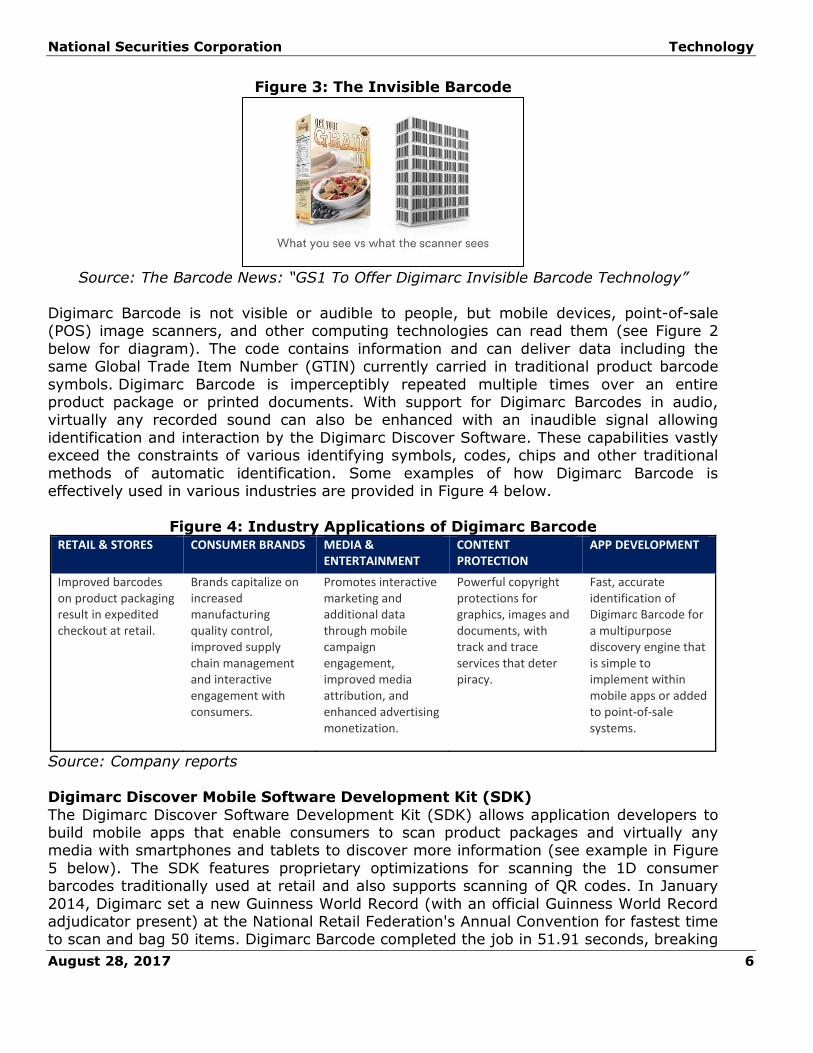

Digimarc Barcode Digimarc Barcode is a proprietary method for imperceptibly enhancing audio, images or physical items with additional information. The Digimarc Barcode is a unique identifier, or

code, based on imperceptible patterns that can be applied to marketing materials, including packaging, displays, ads in magazines, circulars, radio and television (see Figure

3).

National Securities Corporation Technology

August 28, 2017 6

Figure 3: The Invisible Barcode

Source: The Barcode News: “GS1 To Offer Digimarc Invisible Barcode Technology”

Digimarc Barcode is not visible or audible to people, but mobile devices, point-of-sale (POS) image scanners, and other computing technologies can read them (see Figure 2

below for diagram). The code contains information and can deliver data including the same Global Trade Item Number (GTIN) currently carried in traditional product barcode

symbols. Digimarc Barcode is imperceptibly repeated multiple times over an entire product package or printed documents. With support for Digimarc Barcodes in audio, virtually any recorded sound can also be enhanced with an inaudible signal allowing

identification and interaction by the Digimarc Discover Software. These capabilities vastly exceed the constraints of various identifying symbols, codes, chips and other traditional

methods of automatic identification. Some examples of how Digimarc Barcode is effectively used in various industries are provided in Figure 4 below.

Figure 4: Industry Applications of Digimarc Barcode

RETAIL & STORES CONSUMER BRANDS MEDIA & ENTERTAINMENT

CONTENT PROTECTION

APP DEVELOPMENT

Improved barcodes on product packaging result in expedited checkout at retail.

Brands capitalize on increased manufacturing quality control, improved supply chain management and interactive engagement with consumers.

Promotes interactive marketing and additional data through mobile campaign engagement, improved media attribution, and enhanced advertising monetization.

Powerful copyright protections for graphics, images and documents, with track and trace services that deter piracy.

Fast, accurate identification of Digimarc Barcode for a multipurpose discovery engine that is simple to implement within mobile apps or added to point-of-sale systems.

Source: Company reports

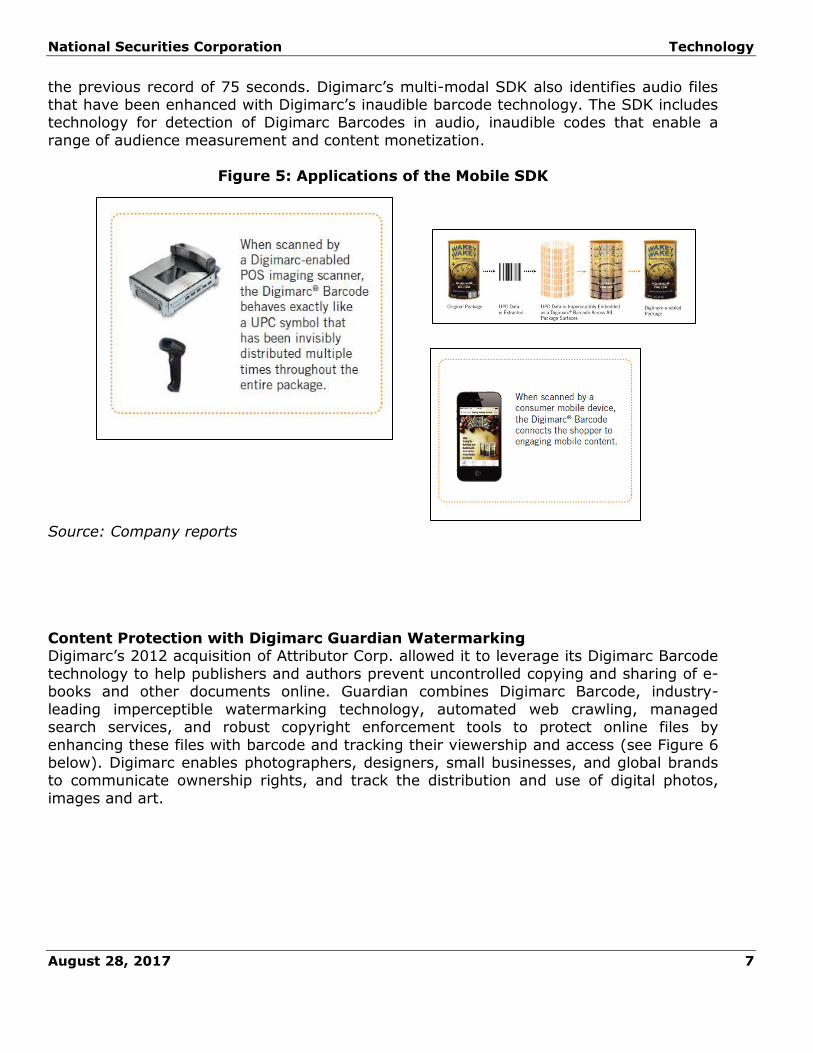

Digimarc Discover Mobile Software Development Kit (SDK)

The Digimarc Discover Software Development Kit (SDK) allows application developers to build mobile apps that enable consumers to scan product packages and virtually any media with smartphones and tablets to discover more information (see example in Figure

5 below). The SDK features proprietary optimizations for scanning the 1D consumer barcodes traditionally used at retail and also supports scanning of QR codes. In January

2014, Digimarc set a new Guinness World Record (with an official Guinness World Record adjudicator present) at the National Retail Federation's Annual Convention for fastest time to scan and bag 50 items. Digimarc Barcode completed the job in 51.91 seconds, breaking

National Securities Corporation Technology

August 28, 2017 7

the previous record of 75 seconds. Digimarc’s multi-modal SDK also identifies audio files that have been enhanced with Digimarc’s inaudible barcode technology. The SDK includes technology for detection of Digimarc Barcodes in audio, inaudible codes that enable a

range of audience measurement and content monetization.

Figure 5: Applications of the Mobile SDK

Source: Company reports

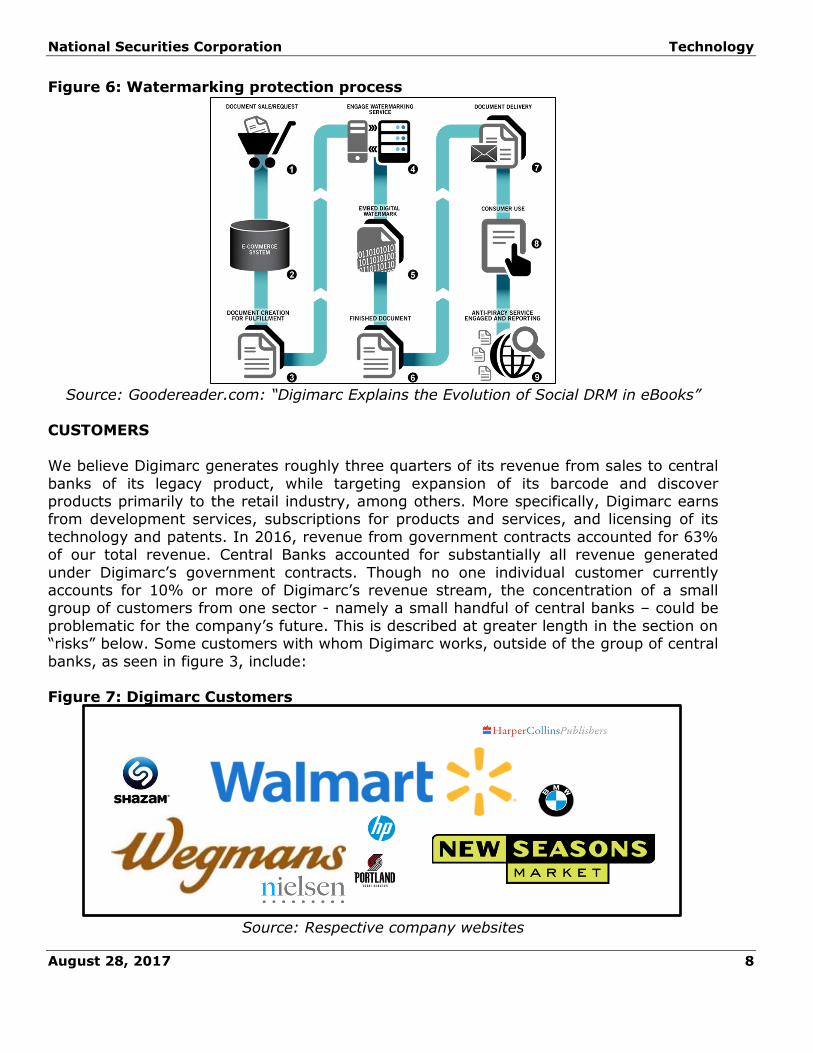

Content Protection with Digimarc Guardian Watermarking Digimarc’s 2012 acquisition of Attributor Corp. allowed it to leverage its Digimarc Barcode

technology to help publishers and authors prevent uncontrolled copying and sharing of e-books and other documents online. Guardian combines Digimarc Barcode, industry-

leading imperceptible watermarking technology, automated web crawling, managed search services, and robust copyright enforcement tools to protect online files by

enhancing these files with barcode and tracking their viewership and access (see Figure 6 below). Digimarc enables photographers, designers, small businesses, and global brands to communicate ownership rights, and track the distribution and use of digital photos,

images and art.

National Securities Corporation Technology

August 28, 2017 8

Figure 6: Watermarking protection process

Source: Goodereader.com: “Digimarc Explains the Evolution of Social DRM in eBooks”

CUSTOMERS

We believe Digimarc generates roughly three quarters of its revenue from sales to central

banks of its legacy product, while targeting expansion of its barcode and discover products primarily to the retail industry, among others. More specifically, Digimarc earns from development services, subscriptions for products and services, and licensing of its

technology and patents. In 2016, revenue from government contracts accounted for 63% of our total revenue. Central Banks accounted for substantially all revenue generated

under Digimarc’s government contracts. Though no one individual customer currently accounts for 10% or more of Digimarc’s revenue stream, the concentration of a small group of customers from one sector - namely a small handful of central banks – could be

problematic for the company’s future. This is described at greater length in the section on “risks” below. Some customers with whom Digimarc works, outside of the group of central

banks, as seen in figure 3, include:

Figure 7: Digimarc Customers

Source: Respective company websites

National Securities Corporation Technology

August 28, 2017 9

COMPETITION

We believe that there are no individual dominant competitors in the various markets

where Digimarc competes. Though competition varies depending on the product or service, Digimarc primarily competes with non-digital watermarking technologies for the

budgets of the producers and distributors of media objects, documents, products and advertising. These alternatives include, among other things, encryption-based security systems and technologies and solutions based on fingerprinting, pattern recognition, and

traditional barcodes.

Some specific examples of these alternatives that we believe compete with applications of

Digimarc’s watermarking technologies include: (1) traditional anti-counterfeiting technologies designed to deter counterfeiting, including optically sensitive ink, magnetic threads and other materials used in the printing of currencies; (2) Image recognition—one

or several pre-specified or learned objects or object classes that can be recognized (such as Amazon Firefly or PTC Vuforia); (3) Radio frequency tags (embedding a chip that emits

a signal when in close proximity with a receiver); and (4) Barcodes or QR codes—data-carrying codes, typically visible in nature (but may be invisible if printed in particular types of inks). Digimarc maintains its competitive edge with its broad portfolio of

watermarking and barcoding patents.

RISKS

Competing with established companies, trying to disrupt existing entrenched relationships. We believe that while the Digimarc’s legacy watermarking business

remains strong, the company’s primary engines of growth—Digimarc Discover and Digimarc Barcode—are subject to the market forces common to other disruptive

technologies. The market is in early stages of development. The revenue model anticipates annual subscriptions are the primary source of income. If adoption takes longer than anticipated, operating losses will continue.

Dependence on clients promoting product to their customers in order to

encourage continued adoption. Digmarc’s success is largely dependent on a new generation of business partners supporting Digimarc Discover and Digimarc Barcode. The company has entered into agreements with numerous channel partners who offer

Digimarc Barcode services to national and store brand owners and consumer products suppliers. If channel partners are not successful in advocating and deploying Digimarc’s

technologies, the company may not be able to sustain profitable operations. Dependent on small group of customers. A small number of customers account for a substantial portion of Digimarc’s revenue. Therefore, we believe that the loss of any large contract could significantly disrupt the business. Five customers represented 73% of

Digimarc’s revenue last year. We believe that Digimarc will continue to depend on a small number of customers for a significant portion of its revenue for the foreseeable future.

National Securities Corporation Technology

August 28, 2017 10

Heavily dependent on patents and protecting against infringement. Digimarc depends in part on securing protection for proprietary technology and successfully licensing these technologies to third parties. To protect its intellectual property, Digimarc

relies on a combination of patents, copyrights, trademarks and trade secret rights, confidentiality procedures and licensing arrangements. Although Digimarc regularly

applies for patents to protect intellectual property, there is no guarantee that the company will secure protection for any particular technology it develops, or that it will successfully enforce intellectual property rights against any infringing third party, should

that scenario arise. This may negatively affect products and services provided to customers. International expansion exposes Digimarc to policy and regulatory complications. We believe Digimarc does not have an extensive infrastructure for

international business. The company generally depends on local or international business partners and subcontractors for performance of substantial portions of its business. These

factors may result in greater risk of performance problems if foreign government authorities terminate or delay the implementation of products and services. Security breach of sensitive materials that are protected by Digimarc products could endanger not only one customer, but potentially Digimarc’s reputation

across the market. The security systems used in Digimarc’s products and services may be circumvented or sabotaged by third parties, which could result in the disclosure of

sensitive information or private personal information or cause other business interruptions that could damage the company’s reputation in addition to disrupting business.

Challenge to quantify the Return on Investment (ROI) of new technologies. We believe that Digimarc faces the challenge of not being able to adequately measure the ROI

of its product for new customers. This poses the risk of failing to sell the company’s products effectively to customers who use related products effectively. With time, this challenge will be resolved as more data is collected on product usefulness, which can then

be translated precisely into ROI metrics for marketing and promotion to particular customers. MANAGEMENT

Bruce Davis, Chief Executive Officer and Chairman of the Board of Directors Bruce Davis serves as CEO of Digimarc since 1997, and help the position of Chairman of

the Board since 2002. Previously, Mr. Davis served as president of Prevue Networks, Inc. and of Titan Broadband Communications. He holds a law degree from Columbia Law School, a B.S. in accounting and psychology, and an M.A. in criminal justice, from the

State University of New York at Albany.

Robert P. Chamness, Chief Legal Officer and Secretary Robert P. Chamness serves as VP and General Counsel of Digimarc since 2002. Prior to joining Digimarc, Mr. Chamness held executive roles as president, COO and a director of

Concentrex Inc. and before that practiced law in San Francisco, Washington, D.C., and Indianapolis. He holds an A.B. from Wabash College and a law degree from the Indiana

University School of Law.

National Securities Corporation Technology

August 28, 2017 11

Charles Beck, Chief Financial Officer and Treasurer Charles Beck joined Digimarc as Controller in 2012 to oversee the company's finance and

accounting functions. Before joining Digimarc, Charles was a Senior Manager in the audit practice at KPMG LLP in Portland, Oregon. Mr. Beck holds a CPA, and received his B.A. in

business administration and his M.B.A. from the University of Portland. Mr. Beck recently completed the Stanford Graduate School of Business Executive Program for Growing Companies.

Joel Meyer, Executive Vice President IP, IP Legal

Joel Meyer serves as the Digimarc’s VP of Intellectual Property since September 2004. Prior to joining Digimarc 1999, Mr. Meyer practiced IP law. Mr. Meyer received a B.S. in Electrical and Computer Engineering from the University of Wisconsin, and a law degree

from the University of Wisconsin Law School.

Tony Rodriguez, Executive Vice President, Chief Technology Officer Tony Rodriguez serves as the leading software engineering, focused on the development and application of digital watermarking and other content identification technologies.

Before joining Digimarc, Mr. Rodriguez worked as a senior software engineer at Intel Architecture Labs. Mr. Rodriguez has a bachelor degree in electrical engineering from the

University of Washington and completed the AeA/Stanford Executive Institute program from Stanford Graduate School of Business.

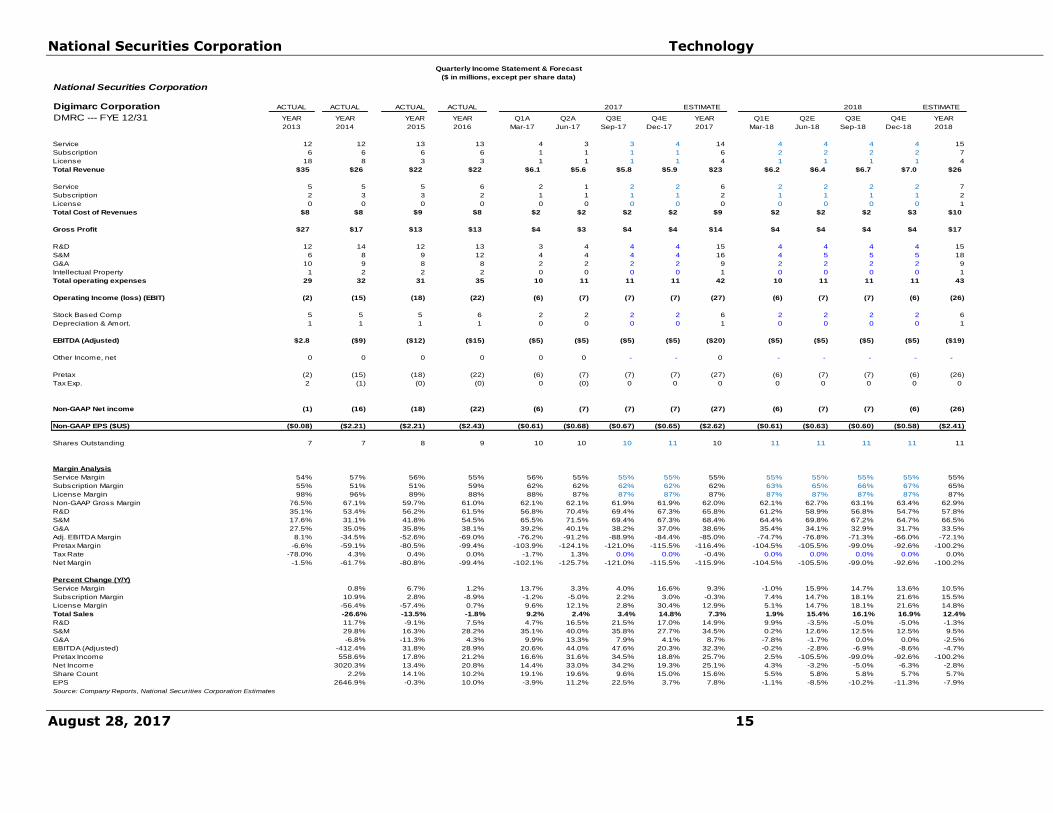

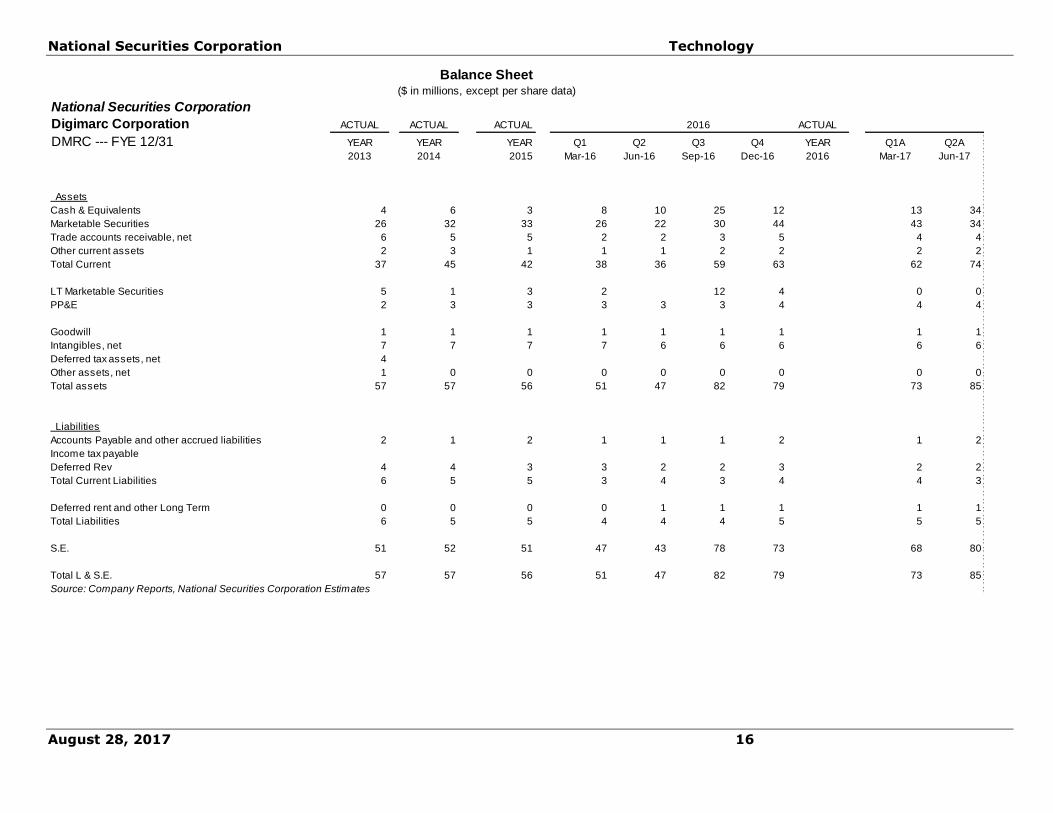

FINANCIALS

Digimarc’s revenue is driven by a combination of services, subscriptions and licensing of its proprietary technologies. Services primarily include development to support customer

adoption of Digimarc products. Subscriptions include revenue derived from anti-piracy and copyright protection, and licensing revenue is derived from royalties from Digimarc’s

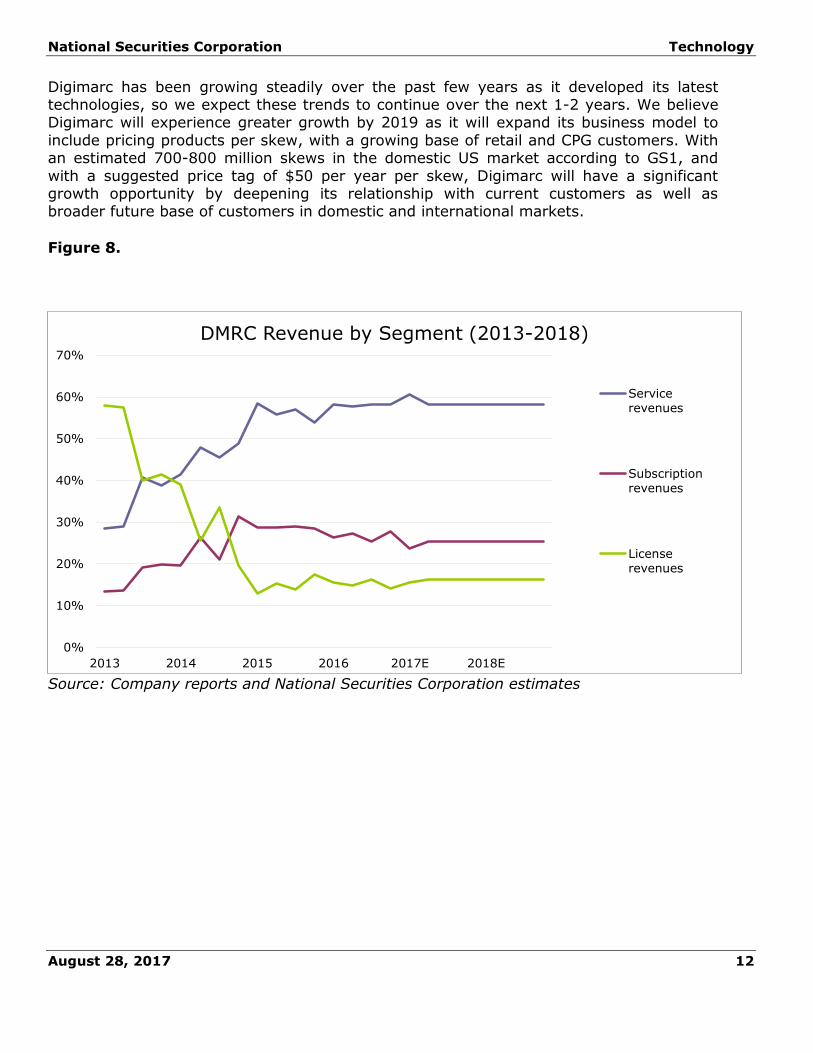

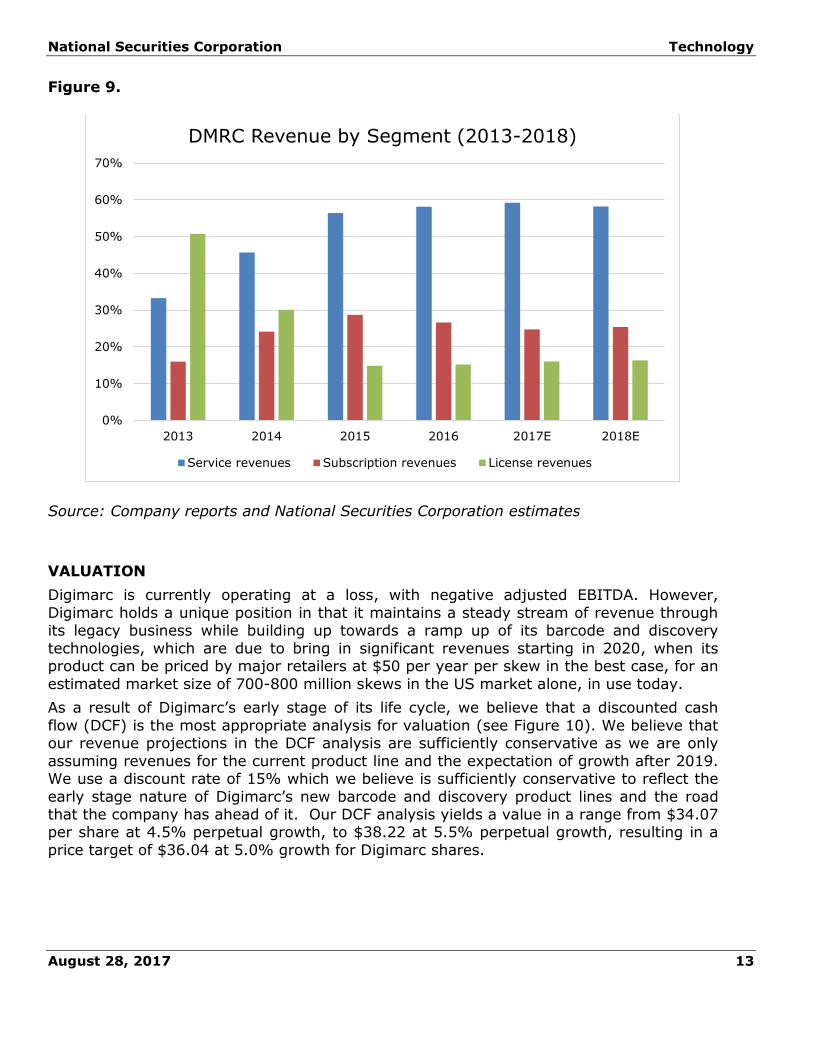

technologies and patents. In terms of the revenue mix, we have seen a clear trend of Services taking the dominant

spot with 58% of the revenue mix, up from an average of 33% at year-end 2013. In this time, licensing has taken a significantly reduced part of the revenue mix (see diagram

below). We expect 2017 annual revenue of $23.4mm and 2018 annual revenue of $26.3mm, with an expected year over year growth of 7% and 12%, respectively, which

includes expected 3-5% growth from the central bank business (which accounts for three quarters of Digmarc’s annual revenue). We believe Digimarc will see a steady gross margin in the low 60% range. we expect gross margin in 2017 of 62%, and gross margin

of 62.9% in 2018. We expect an increase in operating expenses to reflect Digimarc’s pursuit of deeper relations with its domestic customers while embarking on its global

expansion. We expect operating expenses of $41.8m in 2017 and $42.9m in 2018, up from $35.2m in 2016. In 2016, Digimarc saw a continued negative trend for adjusted EBITDA with a loss of $15mm in 2016. We believe however, that Digimarc’s adjusted

EBITDA will eventually turn upward with expected loss of $20mm in 2017 followed by $19mm in 2018.

National Securities Corporation Technology

August 28, 2017 12

Digimarc has been growing steadily over the past few years as it developed its latest technologies, so we expect these trends to continue over the next 1-2 years. We believe Digimarc will experience greater growth by 2019 as it will expand its business model to

include pricing products per skew, with a growing base of retail and CPG customers. With an estimated 700-800 million skews in the domestic US market according to GS1, and

with a suggested price tag of $50 per year per skew, Digimarc will have a significant growth opportunity by deepening its relationship with current customers as well as broader future base of customers in domestic and international markets.

Figure 8.

Source: Company reports and National Securities Corporation estimates

0%

10%

20%

30%

40%

50%

60%

70%

2013 2014 2015 2016 2017E 2018E

DMRC Revenue by Segment (2013-2018)

Servicerevenues

Subscriptionrevenues

Licenserevenues

National Securities Corporation Technology

August 28, 2017 13

Figure 9.

Source: Company reports and National Securities Corporation estimates

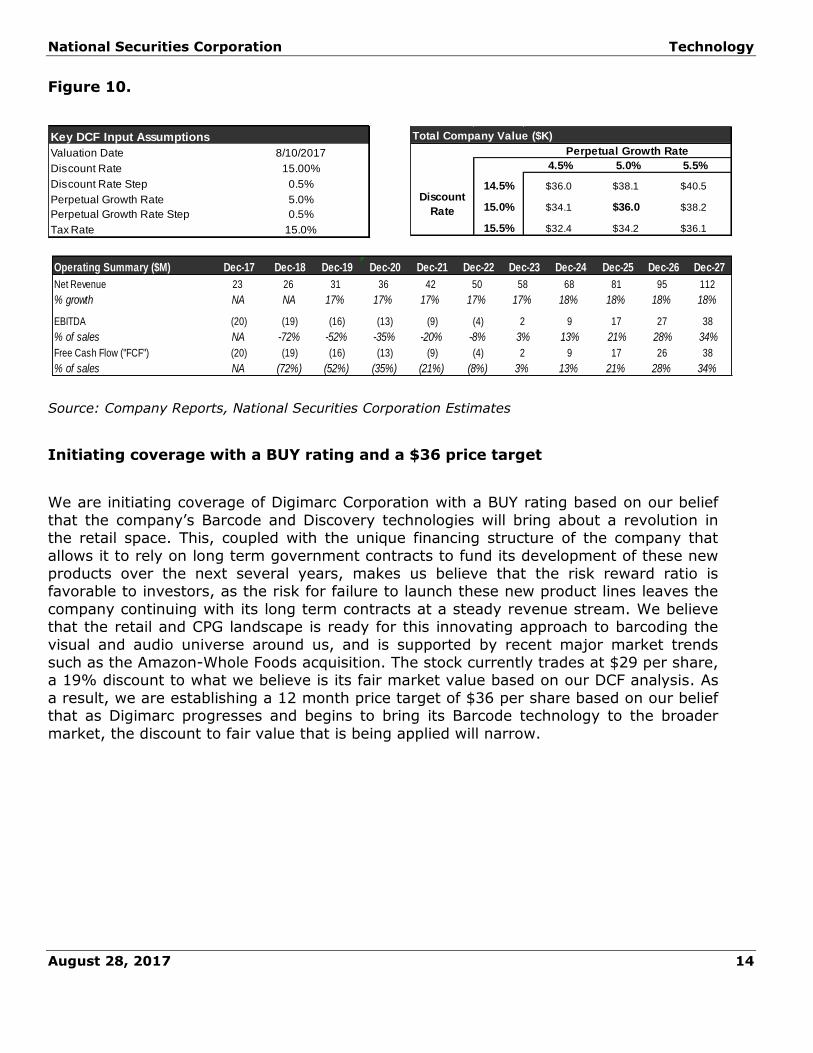

VALUATION

Digimarc is currently operating at a loss, with negative adjusted EBITDA. However,

Digimarc holds a unique position in that it maintains a steady stream of revenue through its legacy business while building up towards a ramp up of its barcode and discovery

technologies, which are due to bring in significant revenues starting in 2020, when its product can be priced by major retailers at $50 per year per skew in the best case, for an

estimated market size of 700-800 million skews in the US market alone, in use today.

As a result of Digimarc’s early stage of its life cycle, we believe that a discounted cash

flow (DCF) is the most appropriate analysis for valuation (see Figure 10). We believe that our revenue projections in the DCF analysis are sufficiently conservative as we are only

assuming revenues for the current product line and the expectation of growth after 2019. We use a discount rate of 15% which we believe is sufficiently conservative to reflect the

early stage nature of Digimarc’s new barcode and discovery product lines and the road that the company has ahead of it. Our DCF analysis yields a value in a range from $34.07 per share at 4.5% perpetual growth, to $38.22 at 5.5% perpetual growth, resulting in a

price target of $36.04 at 5.0% growth for Digimarc shares.

0%

10%

20%

30%

40%

50%

60%

70%

2013 2014 2015 2016 2017E 2018E

DMRC Revenue by Segment (2013-2018)

Service revenues Subscription revenues License revenues

National Securities Corporation Technology

August 28, 2017 14

Figure 10.

Source: Company Reports, National Securities Corporation Estimates

Initiating coverage with a BUY rating and a $36 price target

We are initiating coverage of Digimarc Corporation with a BUY rating based on our belief

that the company’s Barcode and Discovery technologies will bring about a revolution in the retail space. This, coupled with the unique financing structure of the company that

allows it to rely on long term government contracts to fund its development of these new products over the next several years, makes us believe that the risk reward ratio is favorable to investors, as the risk for failure to launch these new product lines leaves the

company continuing with its long term contracts at a steady revenue stream. We believe that the retail and CPG landscape is ready for this innovating approach to barcoding the

visual and audio universe around us, and is supported by recent major market trends such as the Amazon-Whole Foods acquisition. The stock currently trades at $29 per share, a 19% discount to what we believe is its fair market value based on our DCF analysis. As

a result, we are establishing a 12 month price target of $36 per share based on our belief that as Digimarc progresses and begins to bring its Barcode technology to the broader

market, the discount to fair value that is being applied will narrow.

Key DCF Input Assumptions

Valuation Date 8/10/2017

Discount Rate 15.00%

Discount Rate Step 0.5%

Perpetual Growth Rate 5.0%

Perpetual Growth Rate Step 0.5%

Tax Rate 15.0%

Total Company Value ($K)

4.5% 5.0% 5.5%

14.5% $36.0 $38.1 $40.5

15.0% $34.1 $36.0 $38.2

15.5% $32.4 $34.2 $36.1

Perpetual Growth Rate

Discount

Rate

Operating Summary ($M) Dec-17 Dec-18 Dec-19 Dec-20 Dec-21 Dec-22 Dec-23 Dec-24 Dec-25 Dec-26 Dec-27

Net Revenue 23 26 31 36 42 50 58 68 81 95 112

% growth NA NA 17% 17% 17% 17% 17% 18% 18% 18% 18%

EBITDA (20) (19) (16) (13) (9) (4) 2 9 17 27 38

% of sales NA -72% -52% -35% -20% -8% 3% 13% 21% 28% 34%

Free Cash Flow ("FCF") (20) (19) (16) (13) (9) (4) 2 9 17 26 38

% of sales NA (72%) (52%) (35%) (21%) (8%) 3% 13% 21% 28% 34%

National Securities Corporation Technology

August 28, 2017 15

National Securities Corporation

Digimarc Corporation ACTUAL ACTUAL ACTUAL ACTUAL 2017 ESTIMATE 2018 ESTIMATE

DMRC --- FYE 12/31 YEAR YEAR YEAR YEAR Q1A Q2A Q3E Q4E YEAR Q1E Q2E Q3E Q4E YEAR

2013 2014 2015 2016 Mar-17 Jun-17 Sep-17 Dec-17 2017 Mar-18 Jun-18 Sep-18 Dec-18 2018

Service 12 12 13 13 4 3 3 4 14 4 4 4 4 15

Subscription 6 6 6 6 1 1 1 1 6 2 2 2 2 7

License 18 8 3 3 1 1 1 1 4 1 1 1 1 4

Total Revenue $35 $26 $22 $22 $6.1 $5.6 $5.8 $5.9 $23 $6.2 $6.4 $6.7 $7.0 $26

Service 5 5 5 6 2 1 2 2 6 2 2 2 2 7

Subscription 2 3 3 2 1 1 1 1 2 1 1 1 1 2

License 0 0 0 0 0 0 0 0 0 0 0 0 0 1

Total Cost of Revenues $8 $8 $9 $8 $2 $2 $2 $2 $9 $2 $2 $2 $3 $10

Gross Profit $27 $17 $13 $13 $4 $3 $4 $4 $14 $4 $4 $4 $4 $17

R&D 12 14 12 13 3 4 4 4 15 4 4 4 4 15

S&M 6 8 9 12 4 4 4 4 16 4 5 5 5 18

G&A 10 9 8 8 2 2 2 2 9 2 2 2 2 9

Intellectual Property 1 2 2 2 0 0 0 0 1 0 0 0 0 1

Total operating expenses 29 32 31 35 10 11 11 11 42 10 11 11 11 43

Operating Income (loss) (EBIT) (2) (15) (18) (22) (6) (7) (7) (7) (27) (6) (7) (7) (6) (26)

Stock Based Comp 5 5 5 6 2 2 2 2 6 2 2 2 2 6

Depreciation & Amort. 1 1 1 1 0 0 0 0 1 0 0 0 0 1

EBITDA (Adjusted) $2.8 ($9) ($12) ($15) ($5) ($5) ($5) ($5) ($20) ($5) ($5) ($5) ($5) ($19)

Other Income, net 0 0 0 0 0 0 - - 0 - - - - -

Pretax (2) (15) (18) (22) (6) (7) (7) (7) (27) (6) (7) (7) (6) (26)

Tax Exp. 2 (1) (0) (0) 0 (0) 0 0 0 0 0 0 0 0

Non-GAAP Net income (1) (16) (18) (22) (6) (7) (7) (7) (27) (6) (7) (7) (6) (26)

Non-GAAP EPS ($US) ($0.08) ($2.21) ($2.21) ($2.43) ($0.61) ($0.68) ($0.67) ($0.65) ($2.62) ($0.61) ($0.63) ($0.60) ($0.58) ($2.41)

Shares Outstanding 7 7 8 9 10 10 10 11 10 11 11 11 11 11

Margin Analysis

Service Margin 54% 57% 56% 55% 56% 55% 55% 55% 55% 55% 55% 55% 55% 55%

Subscription Margin 55% 51% 51% 59% 62% 62% 62% 62% 62% 63% 65% 66% 67% 65%

License Margin 98% 96% 89% 88% 88% 87% 87% 87% 87% 87% 87% 87% 87% 87%

Non-GAAP Gross Margin 76.5% 67.1% 59.7% 61.0% 62.1% 62.1% 61.9% 61.9% 62.0% 62.1% 62.7% 63.1% 63.4% 62.9%

R&D 35.1% 53.4% 56.2% 61.5% 56.8% 70.4% 69.4% 67.3% 65.8% 61.2% 58.9% 56.8% 54.7% 57.8%

S&M 17.6% 31.1% 41.8% 54.5% 65.5% 71.5% 69.4% 67.3% 68.4% 64.4% 69.8% 67.2% 64.7% 66.5%

G&A 27.5% 35.0% 35.8% 38.1% 39.2% 40.1% 38.2% 37.0% 38.6% 35.4% 34.1% 32.9% 31.7% 33.5%

Adj. EBITDA Margin 8.1% -34.5% -52.6% -69.0% -76.2% -91.2% -88.9% -84.4% -85.0% -74.7% -76.8% -71.3% -66.0% -72.1%

Pretax Margin -6.6% -59.1% -80.5% -99.4% -103.9% -124.1% -121.0% -115.5% -116.4% -104.5% -105.5% -99.0% -92.6% -100.2%

Tax Rate -78.0% 4.3% 0.4% 0.0% -1.7% 1.3% 0.0% 0.0% -0.4% 0.0% 0.0% 0.0% 0.0% 0.0%

Net Margin -1.5% -61.7% -80.8% -99.4% -102.1% -125.7% -121.0% -115.5% -115.9% -104.5% -105.5% -99.0% -92.6% -100.2%

Percent Change (Y/Y)

Service Margin 0.8% 6.7% 1.2% 13.7% 3.3% 4.0% 16.6% 9.3% -1.0% 15.9% 14.7% 13.6% 10.5%

Subscription Margin 10.9% 2.8% -8.9% -1.2% -5.0% 2.2% 3.0% -0.3% 7.4% 14.7% 18.1% 21.6% 15.5%

License Margin -56.4% -57.4% 0.7% 9.6% 12.1% 2.8% 30.4% 12.9% 5.1% 14.7% 18.1% 21.6% 14.8%

Total Sales -26.6% -13.5% -1.8% 9.2% 2.4% 3.4% 14.8% 7.3% 1.9% 15.4% 16.1% 16.9% 12.4%

R&D 11.7% -9.1% 7.5% 4.7% 16.5% 21.5% 17.0% 14.9% 9.9% -3.5% -5.0% -5.0% -1.3%

S&M 29.8% 16.3% 28.2% 35.1% 40.0% 35.8% 27.7% 34.5% 0.2% 12.6% 12.5% 12.5% 9.5%

G&A -6.8% -11.3% 4.3% 9.9% 13.3% 7.9% 4.1% 8.7% -7.8% -1.7% 0.0% 0.0% -2.5%

EBITDA (Adjusted) -412.4% 31.8% 28.9% 20.6% 44.0% 47.6% 20.3% 32.3% -0.2% -2.8% -6.9% -8.6% -4.7%

Pretax Income 558.6% 17.8% 21.2% 16.6% 31.6% 34.5% 18.8% 25.7% 2.5% -105.5% -99.0% -92.6% -100.2%

Net Income 3020.3% 13.4% 20.8% 14.4% 33.0% 34.2% 19.3% 25.1% 4.3% -3.2% -5.0% -6.3% -2.8%

Share Count 2.2% 14.1% 10.2% 19.1% 19.6% 9.6% 15.0% 15.6% 5.5% 5.8% 5.8% 5.7% 5.7%

EPS 2646.9% -0.3% 10.0% -3.9% 11.2% 22.5% 3.7% 7.8% -1.1% -8.5% -10.2% -11.3% -7.9%

Source: Company Reports, National Securities Corporation Estimates

Quarterly Income Statement & Forecast

($ in millions, except per share data)

National Securities Corporation Technology

August 28, 2017 16

National Securities Corporation

Digimarc Corporation ACTUAL ACTUAL ACTUAL 2016 ACTUAL

DMRC --- FYE 12/31 YEAR YEAR YEAR Q1 Q2 Q3 Q4 YEAR Q1A Q2A

2013 2014 2015 Mar-16 Jun-16 Sep-16 Dec-16 2016 Mar-17 Jun-17

Assets

Cash & Equivalents 4 6 3 8 10 25 12 13 34

Marketable Securities 26 32 33 26 22 30 44 43 34

Trade accounts receivable, net 6 5 5 2 2 3 5 4 4

Other current assets 2 3 1 1 1 2 2 2 2

Total Current 37 45 42 38 36 59 63 62 74

LT Marketable Securities 5 1 3 2 12 4 0 0

PP&E 2 3 3 3 3 3 4 4 4

Goodwill 1 1 1 1 1 1 1 1 1

Intangibles, net 7 7 7 7 6 6 6 6 6

Deferred tax assets, net 4

Other assets, net 1 0 0 0 0 0 0 0 0

Total assets 57 57 56 51 47 82 79 73 85

Liabilities

Accounts Payable and other accrued liabilities 2 1 2 1 1 1 2 1 2

Income tax payable

Deferred Rev 4 4 3 3 2 2 3 2 2

Total Current Liabilities 6 5 5 3 4 3 4 4 3

Deferred rent and other Long Term 0 0 0 0 1 1 1 1 1

Total Liabilities 6 5 5 4 4 4 5 5 5

S.E. 51 52 51 47 43 78 73 68 80

Total L & S.E. 57 57 56 51 47 82 79 73 85

Source: Company Reports, National Securities Corporation Estimates

Balance Sheet($ in millions, except per share data)

National Securities Corporation Technology

August 28, 2017 17

IMPORTANT DISCLOSURES:

National Securities Corporation

200 Vesey Street, 25th Floor, New York, NY 10281

REG AC ANALYST CERTIFICATION

The research analyst named on this report, Ilya Grozovsky, certifies the following: (1) that all of the views expressed in this research report accurately reflect his personal views about any and all of the subject securities or issuers; and (2) that no part of his

compensation was, is, or will be directly or indirectly related to the specific recommendations or views expressed by him in this research report.

IMPORTANT DISCLOSURES

This publication does not constitute and should not be construed as an offer or the

solicitation of any transaction to buy or sell any securities or any instruments or any derivatives of the securities mentioned herein, or to participate in any particular trading strategies. Although the information contained herein has been obtained from recognized

services, and sources believed to be reliable, its accuracy or completeness cannot be guaranteed. Opinions, estimates or projections expressed in this report may make

assumptions regarding economic, industry, company and political considerations, and constitute current opinions, at the time of issuance, which are subject to change without notice.

This report is being furnished for informational purposes only, and on the condition that it will not form a primary basis for any investment decision. Any recommendation(s)

contained in this report is/are not intended to be, nor should it / they construed or inferred to be, investment advice, as such investments may not be suitable for all

investors. When preparing this report, no consideration to one’s investment objectives, risk tolerance and other individual factors was given; as such, as with all investments, purchase or sale of any securities mentioned herein may not be suitable for all investors.

By virtue of this publication, neither the Firm nor any of its employees shall be responsible for any investment decisions. Before committing funds to ANY investment, an investor

should seek professional advice. Any information relating to the tax status of financial instruments discussed herein is not intended to provide tax advice, or to be used by anyone to provide tax advice. Investors are urged to consult an independent tax

professional for advice concerning their particular circumstances. Past performance should not be taken as an indication or guarantee of future performance, and no representation

or warranty, either expressed or implied, is made regarding future performance.

National Securities Corporation (NSC) and its affiliated companies, shareholders, officers,

directors and / or employees (including persons involved with the preparation or issuance of this report) may, from time to time, have long or short positions in, and buy or sell the securities or derivatives (including options) thereof, of the companies mentioned herein.

One or more directors, officers, and / or employees of NSC and its affiliated companies, or independent contractors affiliated with NSC may be a director of the issuer of the

securities mentioned herein. NSC and / or its affiliated companies may have managed or

National Securities Corporation Technology

August 28, 2017 18

co-managed a public offering of, or acted as initial purchaser or placement agent for a private placement of any of the securities of any issuer mentioned in this report within the last three (3) years, or may, from time to time, perform investment banking or other

services for, or solicit investment banking business from any company mentioned in this report.

This research may be distributed by affiliated entities of National Securities Corporation (NSC). Affiliated entities of NSC may include, but are not limited to, finance Investments, Inc., National Asset Management and other subsidiaries of our parent company, National

Holdings Corporation.

The securities mentioned in this document may not be eligible for sale in some states or

countries, nor be suitable for all types of investors; their value and the income they produce if any, may fluctuate and/or be adversely affected by exchange rates, interest

rates or other factors. Furthermore, NSC may follow emerging growth companies whose securities typically involve a higher degree of risk and more volatility than the securities of more established companies. This report does not take into account the particular

investment objectives, financial situation or needs of individual investors. Before acting on any advice or recommendation in this material, the investor should exercise independent

judgment as to whether it is suitable in light of his/her particular circumstances and, if necessary, seek professional advice. Past performance should not be taken as an indication or guarantee of future performance, and no representation or warranty, express

or implied, is made regarding future performance.

Additional information relative to securities, other financial products, or issuers discussed

in this report is available upon request. Neither this entire report, nor any part thereof, may be reproduced, copied or duplicated in any form or by any means without the prior written consent of National Securities Corporation. All rights reserved. NSC is a member of

both the Financial Industry Regulatory Authority (FINRA) and the Securities Investors Protection Corporation (SIPC).

For disclosures inquiries, please call us at 1-800-417-8000 and ask for your NSC representative, or write us at National Securities Corporation, Attn. Chris Testa or Glenn

Williams- Research Department, 200 Vesey Street, 25th Floor, New York, NY 10281, or visit our website at www.nationalsecurities.com

Research Disclosures Legend

Relevant Disclosures: 1

Affiliates of National Securities Corporation have a financial interest in the securities of the subject company as follows: long common stock.

1 National Securities (NSC) is a market-maker in the securities of the subject company

2 In the past twelve (12) month period, NSC and / or its affiliates have received compensation for investment banking for services from the subject company

3 In the past twelve (12) month period, NSC and / or its affiliates have received

compensation from the subject company for services other than those related to investment banking

National Securities Corporation Technology

August 28, 2017 19

4 In the past twelve (12) month period, NSC was a manager or a co-manager of a public offering of one or more of the securities of the issuer

5 In the past twelve (12) month period, NSC was a member of the selling group of

a public offering of the security (is) of the issuer 6 One or more directors, officers, and / or employees of NSC and / or its affiliated

companies is / are a director (s) of the issuer of the security which is the subject of this report

7 NSC and / or its affiliates expects to receive or intends to seek compensation for

investment banking services from the subject company at some point during the next three (3) months

8 A research analyst or a member of his / her household has a financial interest in the securities of the subject company as follows: a) long common stock; b) short common stock; c) long calls; d) short calls; e) long puts; f) short puts; g) long

rights; h) short rights; I) long warrants; j) short warrants; k) long futures; l) short futures; m) long preferred stock; n) short preferred stock

9 As of the end of the month immediately preceding the date of publication of this report or the end of the prior month if the publication is within ten (10) days following the end of the month, NSC and / or its affiliates beneficially owned one

percent (1%) or more of any class of common equity securities of the subject company.

10 Please see below for other relevant disclosures

Shares of this security may be sold to residents of all 50 states, Puerto Rico, Guam, the US Virgin Islands and the District of Columbia.

*Investment banking services provided in the previous 12 months

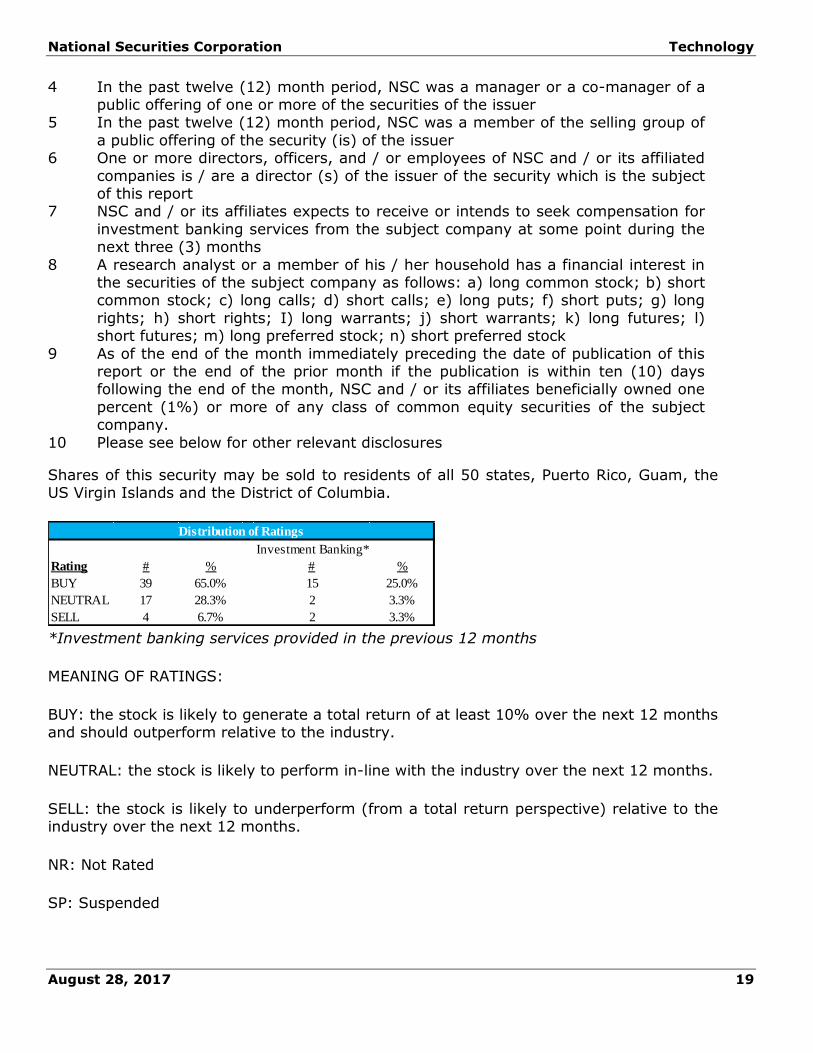

MEANING OF RATINGS:

BUY: the stock is likely to generate a total return of at least 10% over the next 12 months and should outperform relative to the industry.

NEUTRAL: the stock is likely to perform in-line with the industry over the next 12 months.

SELL: the stock is likely to underperform (from a total return perspective) relative to the industry over the next 12 months.

NR: Not Rated

SP: Suspended

Investment Banking*

Rating # % # %

BUY 39 65.0% 15 25.0%

NEUTRAL 17 28.3% 2 3.3%

SELL 4 6.7% 2 3.3%

Distribution of Ratings

National Securities Corporation Technology

August 28, 2017 20

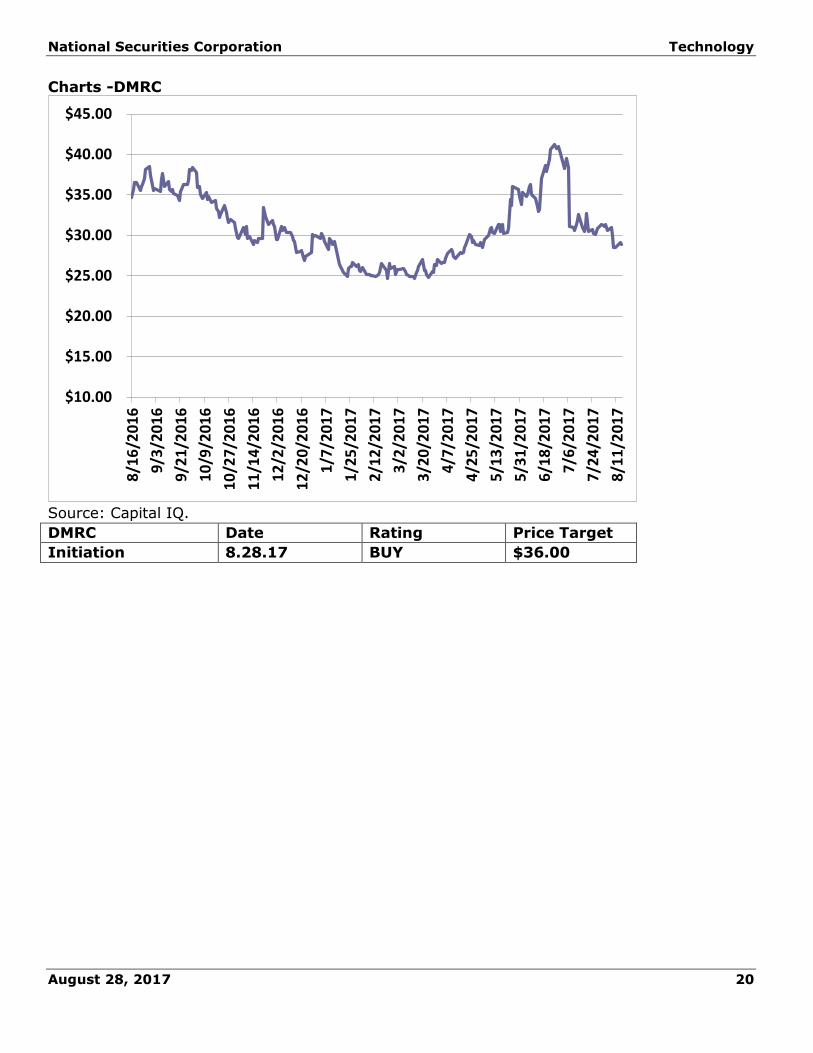

Charts -DMRC

Source: Capital IQ.

DMRC Date Rating Price Target

Initiation 8.28.17 BUY $36.00

$10.00

$15.00

$20.00

$25.00

$30.00

$35.00

$40.00

$45.008

/16

/20

16

9/3

/20

16

9/2

1/2

01

6

10

/9/2

01

6

10

/27

/20

16

11

/14

/20

16

12

/2/2

01

6

12

/20

/20

16

1/7

/20

17

1/2

5/2

01

7

2/1

2/2

01

7

3/2

/20

17

3/2

0/2

01

7

4/7

/20

17

4/2

5/2

01

7

5/1

3/2

01

7

5/3

1/2

01

7

6/1

8/2

01

7

7/6

/20

17

7/2

4/2

01

7

8/1

1/2

01

7