Embed Size (px)

Citation preview

HELPING YOU UNDERSTAND THE GOVERNMENT EMPLOYEE PENSION FUND

As a government employee you have access to comprehensive risk and retirement benefits with the Government Employee Pension Fund (GEPF). But does this mean you have enough risk cover and retirement savings should something happen? This brochure gives you details of what benefits you have, potential risk cover shortfalls and your options when retiring or leaving the fund.

It is divided into three sections: 1. Risk cover2. Retirement savings3. Leaving the GEPF (before normal retirement)

Each section will give you a summary of your benefits and questions to think about when making plans for your financial future.

To gain a better understanding of your benefits with the GEPF and any potential shortfalls, contact your Old Mutual personal financial adviser or your broker who can give you a tailor-made report of all your benefits with the GEPF.

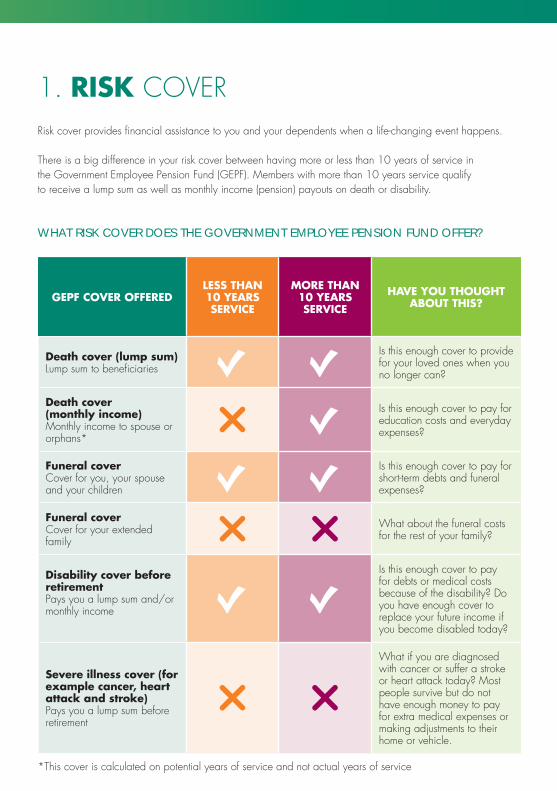

Risk cover provides financial assistance to you and your dependents when a life-changing event happens.

There is a big difference in your risk cover between having more or less than 10 years of service in the Government Employee Pension Fund (GEPF). Members with more than 10 years service qualify to receive a lump sum as well as monthly income (pension) payouts on death or disability.

WHAT RISK COVER DOES THE GOVERNMENT EMPLOYEE PENSION FUND OFFER?

GEPF COVER OFFEREDLESS THAN 10 YEARS SERVICE

MORE THAN 10 YEARS SERVICE

HAVE YOU THOUGHT ABOUT THIS?

Death cover (lump sum)Lump sum to beneficiaries Ç Ç

Is this enough cover to provide for your loved ones when you no longer can?

Death cover (monthly income)Monthly income to spouse or orphans*

I ÇIs this enough cover to pay for education costs and everyday expenses?

Funeral cover Cover for you, your spouse and your children Ç Ç

Is this enough cover to pay for short-term debts and funeral expenses?

Funeral cover Cover for your extended family I I What about the funeral costs

for the rest of your family?

Disability cover before retirementPays you a lump sum and/or monthly income Ç Ç

Is this enough cover to pay for debts or medical costs because of the disability? Do you have enough cover to replace your future income if you become disabled today?

Severe illness cover (for example cancer, heart attack and stroke) Pays you a lump sum before retirement

I I

What if you are diagnosed with cancer or suffer a stroke or heart attack today? Most people survive but do not have enough money to pay for extra medical expenses or making adjustments to their home or vehicle.

1. RISK COVER

*This cover is calculated on potential years of service and not actual years of service

What do these risk benefits cover?

Death before and after retirement: Pays out a taxable lump sum and/or monthly income to the surviving spouse, beneficiaries or estate. The amount payable is dependent on how long you were a member of the GEPF.

Funeral cover: Pays a taxable lump sum of R7 500 for you and your spouse and R3 000 for your children.

Spouse’s pension: Pays a taxable monthly income to your spouse or eligible life partner as a percentage of your income at date of death.

Orphan’s pension: Pays a taxable monthly income on your death to eligible orphans.

Disability cover: Pays out a taxable lump sum and/or monthly income if you become disabled due to medical reasons or forced discharge before retirement.

Your disability benefits – are you sure that it is enough? Your most important asset is you and your ability to earn an income. If you become disabled today, will your benefits from the GEPF be enough to replace your income? Can you and your family settle debts, make changes to your everyday life and pay for rehabilitation or frail care costs if there is a decrease in your monthly income? If your life is impacted by a disability event today, what will the difference in your income be before and after retirement?

Severe illness cover is not offered by the GEPF. Have you thought about what impact a severe illness such as cancer, stroke or a heart attack would have on your life and your family? How would you pay for additional medical expenses or settle your debt? After initial treatment, do you have funds to cover rehabilitation costs and give you the best chance at recovery?

Your spouse is not covered by the GEPF. Who will replace your spouse’s income if they become disabled and cannot work? If your spouse is running the household, who will do this if they no longer can? Will you have enough funds to cover debt, education fees for your children and everyday living expenses if your spouse had to die or become disabled today?

HAVE YOU THOUGHT ABOUT THIS?

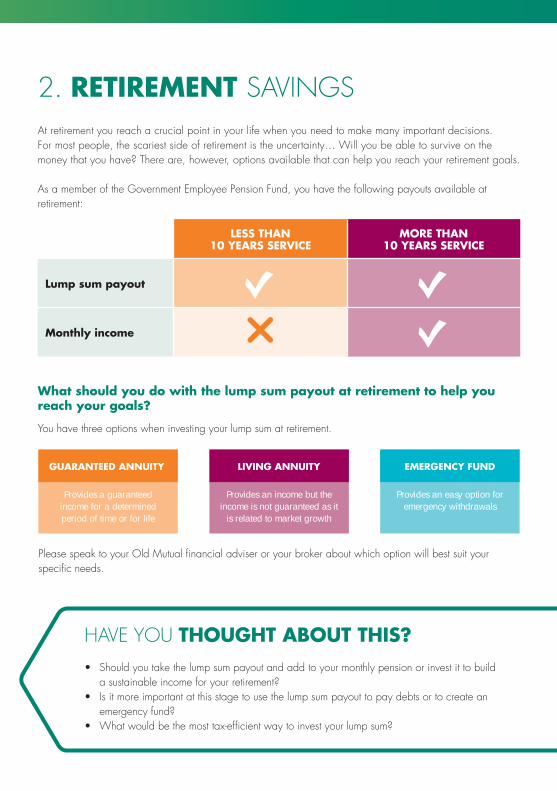

At retirement you reach a crucial point in your life when you need to make many important decisions. For most people, the scariest side of retirement is the uncertainty… Will you be able to survive on the money that you have? There are, however, options available that can help you reach your retirement goals.

As a member of the Government Employee Pension Fund, you have the following payouts available at retirement:

LESS THAN 10 YEARS SERVICE

MORE THAN 10 YEARS SERVICE

Lump sum payout Ç ÇMonthly income I Ç

What should you do with the lump sum payout at retirement to help you reach your goals?

You have three options when investing your lump sum at retirement.

2. RETIREMENT SAVINGS

HAVE YOU THOUGHT ABOUT THIS? • Should you take the lump sum payout and add to your monthly pension or invest it to build

a sustainable income for your retirement? • Is it more important at this stage to use the lump sum payout to pay debts or to create an

emergency fund? • What would be the most tax-efficient way to invest your lump sum?

GUARANTEED ANNUITY

Provides a guaranteed income for a determined period of time or for life

LIVING ANNUITY

Provides an income but the income is not guaranteed as it

is related to market growth

EMERGENCY FUND

Provides an easy option for emergency withdrawals

Please speak to your Old Mutual financial adviser or your broker about which option will best suit your specific needs.

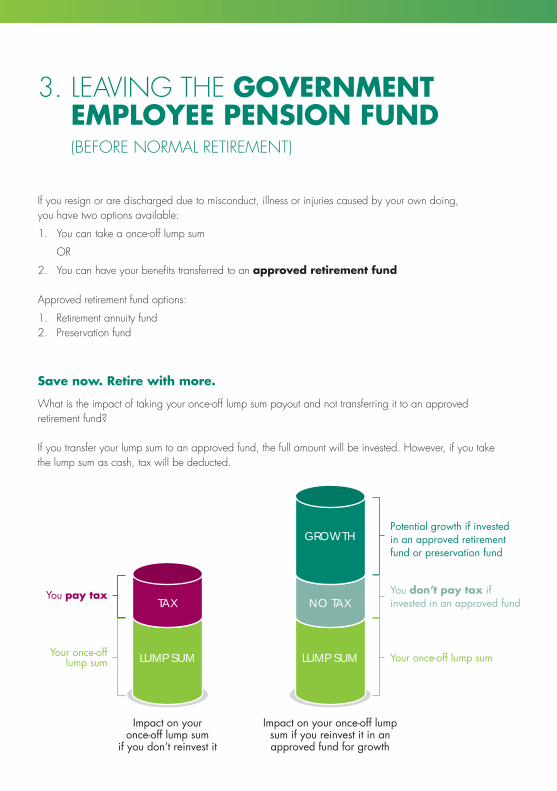

If you resign or are discharged due to misconduct, illness or injuries caused by your own doing, you have two options available:

1. You can take a once-off lump sum

OR

2. You can have your benefits transferred to an approved retirement fund

Approved retirement fund options:

1. Retirement annuity fund2. Preservation fund

Save now. Retire with more.

What is the impact of taking your once-off lump sum payout and not transferring it to an approved retirement fund?

If you transfer your lump sum to an approved fund, the full amount will be invested. However, if you take the lump sum as cash, tax will be deducted.

3. LEAVING THE GOVERNMENT EMPLOYEE PENSION FUND (BEFORE NORMAL RETIREMENT)

Potential growth if invested in an approved retirement fund or preservation fund

You don’t pay tax if invested in an approved fund

Your once-off lump sum

Impact on your once-off lump sum

if you don’t reinvest it

You pay tax

Your once-off lump sum

TAX NO TAX

Impact on your once-off lump sum if you reinvest it in an approved fund for growth

LUMP SUM LUMP SUM

GROWTH

HAVE YOU THOUGHT ABOUT THIS?• If you take the once-off lump sum payout and spend it now, will you have enough money

for you and your family at retirement? • What other investment vehicle besides a retirement annuity or preservation fund will

allow your funds to grow without being taxed on the growth? • If you use your retirement funds to start a business, what protection will you have against

potential insolvency?

To gain a better understanding of your benefits with the GEPF and any potential

shortfalls, speak to your Old Mutual personal financial adviser or your broker who can give you a tailor-made report of all your benefits with the GEPF.

Old Mutual is a Licensed Financial Services Provider.

hero, O

M77

3320

1