Embed Size (px)

Citation preview

Australian HealthcareA digital perspective

Disruption, innovation and the new ecosystems for care and prevention

Caitlin Francis

April 2016

Page 3

Our Agenda

Digital disruption: What do we mean by digital disruption?

The digital customer: Why is digital changing expectations?

Participatory health: A new model to deliver care and outcomes

Digital health: What is ‘digital health’?

Digital health:

What is ‘digital health’?

Page 5

Digital is the defining mega-trend of our time

Page 6

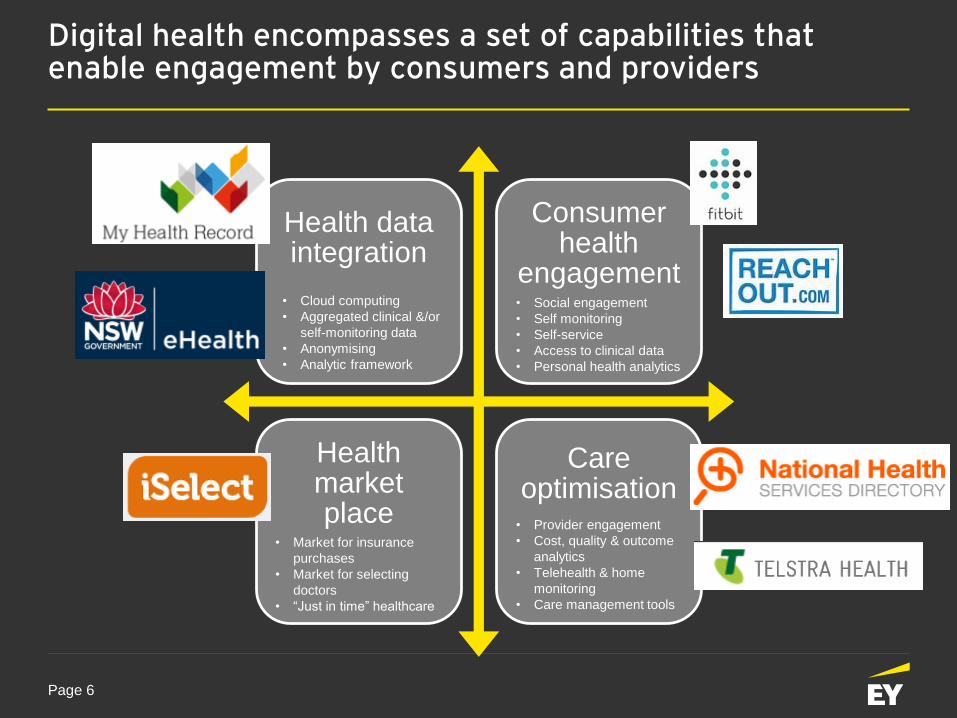

Health data integration

Consumer health

engagement

Health market place

Care optimisation

Digital health encompasses a set of capabilities thatenable engagement by consumers and providers

• Social engagement

• Self monitoring

• Self-service

• Access to clinical data

• Personal health analytics

• Cloud computing

• Aggregated clinical &/or

self-monitoring data

• Anonymising

• Analytic framework

• Provider engagement

• Cost, quality & outcome

analytics

• Telehealth & home

monitoring

• Care management tools

• Market for insurance

purchases

• Market for selecting

doctors

• “Just in time” healthcare

Page 7

Healthcare has lagged behind other industries in its progress towards digital enablement (mobile, cloud, big data & social)

Opportunistic Repeatable Managed

Telecommunications

Utilities

Banking and Finance

Federal Government

Ma

turi

ty

Transport and

Logistics

HealthMining

Time

Energy

Media & Entertainment

Insurance

Retail

Source: EY

Page 8

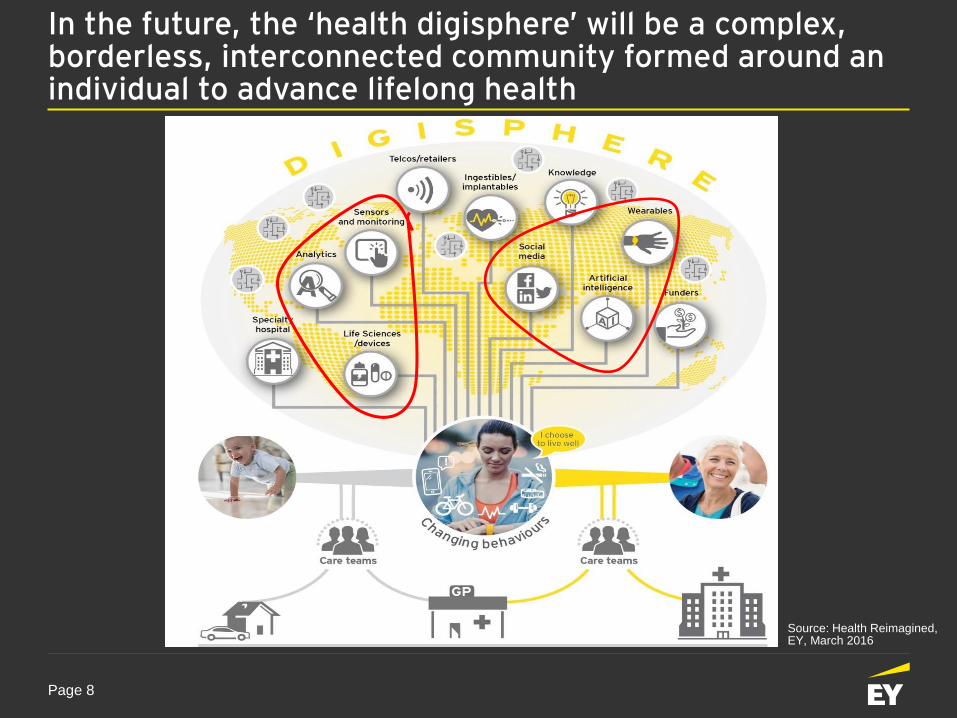

In the future, the ‘health digisphere’ will be a complex, borderless, interconnected community formed around an individual to advance lifelong health

Source: Health Reimagined, EY, March 2016

Digital health:

What do we mean by digital disruption?

Page 10

The secret to understanding digital is that the underlying business model and allocation of capital is being re-architected

The technology is a byproduct of the new business

Digital disruption is a business model change which creates opportunities and threats

Worlds largest taxi company owns no taxis

Largest accommodation provider owns no real estate

Largest phone companies owns no telco infrastructure

Most valuable retailer has no inventory

Most popular media owner creates no content

Fastest growing banks have no actual money

Worlds largest movie house owns no cinemas

Largest software vendors don’t write the Apps

Page 11

Digital disruption is changing what is possible in healthcare

Radically different approaches

to care

New/non-traditional players

enter through increasingly

permeable boundaries

Consumers have adopted the

‘digital life’ with enthusiasm

Social shifts towards sharing

economy, crowdsourcing

Generation of vast amounts of

personal data via ‘quantified

self’ and ‘Internet of Things’

(IoT)

Consumers expect mobile-

enabled solutions they enjoy in

travel, transport, financial

services & retail

Page 12

This disruption is being reflected in the range and number of new entrants/non-traditional players in the health sector

New entrants/

nontraditional players “Brilliant, connected healthcare for everyone”

Online services/online

patient communities “Live better, together! Making healthcare

better for everyone through sharing, support

and research”

Consumer engagement “Big data, better health. Smarter care starts

with your smartphone’”

Big data/

clinical/administration“The deep learning healthcare company

ushering in a new era of Data Driven

Medicine”

Telehealth/point of

care/New Science “Expert doctors online when you need them”

Consumer goods/

wearables“Fitbit activity index – we geek out about

workouts…tips for getting started and staying

motivated”

Page 13

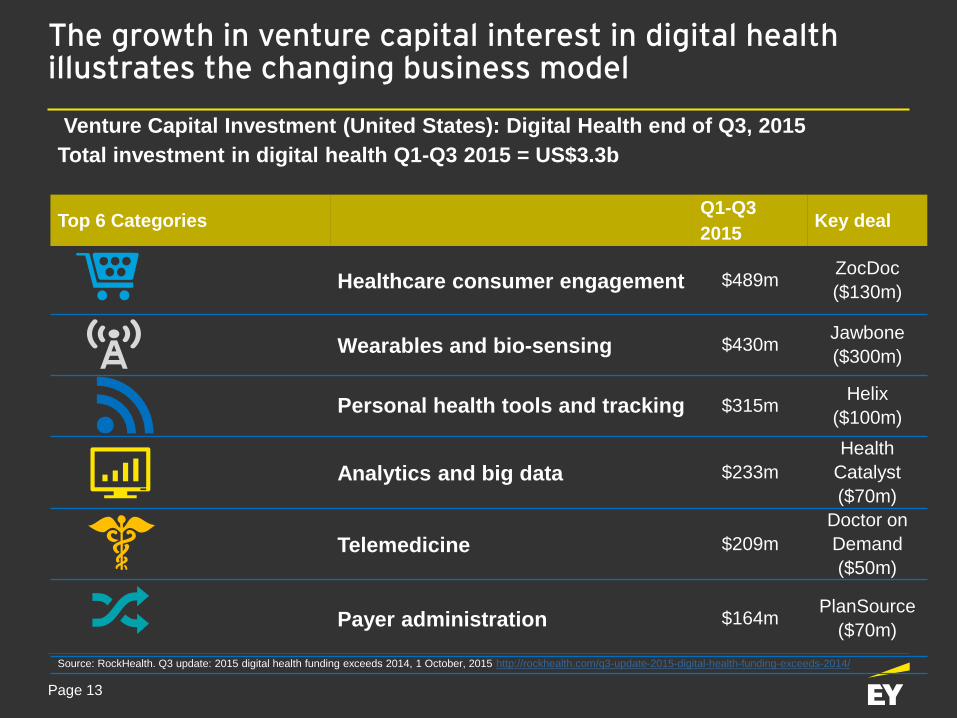

The growth in venture capital interest in digital health illustrates the changing business model

Venture Capital Investment (United States): Digital Health end of Q3, 2015

Total investment in digital health Q1-Q3 2015 = US$3.3b

Top 6 CategoriesQ1-Q3

2015Key deal

Healthcare consumer engagement $489m ZocDoc

($130m)

Wearables and bio-sensing $430mJawbone

($300m)

Personal health tools and tracking $315mHelix

($100m)

Analytics and big data $233m

Health

Catalyst

($70m)

Telemedicine $209m

Doctor on

Demand

($50m)

Payer administration $164mPlanSource

($70m)

Source: RockHealth. Q3 update: 2015 digital health funding exceeds 2014, 1 October, 2015 http://rockhealth.com/q3-update-2015-digital-health-funding-exceeds-2014/

The digital patient:Why digital changes customer (patient, provider) expectations?

“Put the user at the centre of everything you do”

Page 15

Experience is the new currency for digital businesses

Page 16

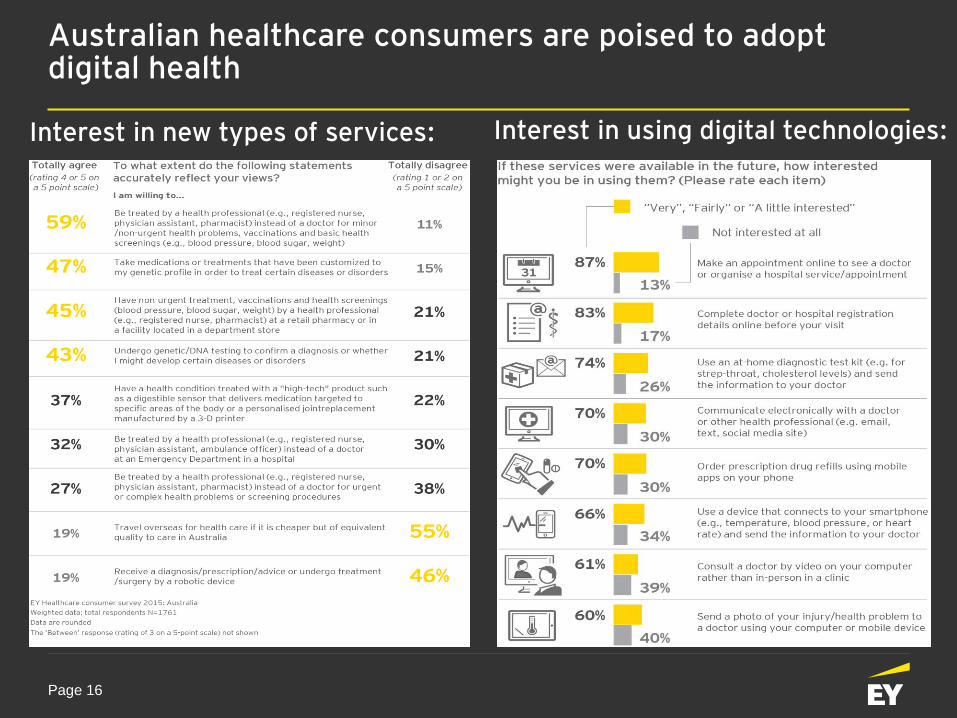

Interest in new types of services:

Australian healthcare consumers are poised to adopt digital health

Interest in using digital technologies:

Digital Health:A new model to deliver care and outcomes

Page 18

There are four irrefutable facts for the Healthcare and Life Sciences sectors which are shaping their development

1

2

3

Healthcare and Pharmaceuticals will continue to take an ever larger share of GDP – putting all payers under pressure

The merging of computational power with the health data and artificial intelligence will change the delivery of healthcare

R&D productivity and market access remains the sectors’ biggest challenges leading to increased consolidation and deconsolidation cycles

Information is driving patients, payers and healthcare providers to become Super Consumers – who are then determining the rate of change 4

Page 19

Sick-care Health-care

Blockbusters

Drugs

Personalised

Medicine

Disconnected

Healthcare

Connected

Healthcare

The pace of change is being governed by the “Shift to Digital”

“Uninformed”

Buyers/Users

Super

Consumers

Analogue Digital

Irrefutable Facts The Healthcare & Life Science Ecosystem Trends

Page 20

New entrants are betting on a new digital ‘participatory’ model in which maturing consumerism, technology and new social media platforms are key enablers

Page 21

Participatory Health is a future that’s underway

“The patient

will see you

now”

Page 22

EY report

“The future of

health insurance:

A roadmap

through change”.

2015

EY report

“Health reimagined:

a new participatory

health paradigm”.

2016

Recent and relevant EY publications

Ernst & Young

Assurance | Tax | Transactions | Advisory

About Ernst & YoungErnst & Young is a global leader in assurance, tax, transaction and advisory services. Worldwide, our 144,000 people are united by our shared values and an unwavering commitment to quality. We make a difference by helping our people, our clients and our wider communities achieve their potential.

For more information, please visit www.ey.com/au

© 2016 Ernst & Young Australia

Liability limited by a scheme approved under Professional Standards Legislation.

The information in this document and in any oral presentations made by Ernst & Young is confidential to Ernst & Young and should not be disclosed, used, or duplicated in whole or in part for any purpose.

This document (or any part of it) may not be copied or otherwise reproduced except with the written consent of Ernst & Young.