Embed Size (px)

Citation preview

Disclosure of Account Information

(REVISED - JANUARY 2018)

200846053-010.qxp_200846053-010 10/26/17 11:33 AM Page 1

200846053-010.qxp_200846053-010 10/26/17 11:33 AM Page 2

TABLE OF CONTENTSGENERAL TERMS AND CONDITIONS OF YOUR ACCOUNT...............5Important Information About Procedures for

Opening a New Account................................................5Agreement ........................................................................5Bylaws..............................................................................6Liability ............................................................................6Deposits ...........................................................................7Withdrawals ......................................................................8Ownership of Account and Beneficiary Designation ...............9Pay On Death ..................................................................10Stop Payments ................................................................10Telephone Transfers .........................................................11Amendments and Termination...........................................11Notices ...........................................................................12Change in Terms Notice....................................................13Statements .....................................................................13Account Transfer..............................................................14Direct Deposits ................................................................14Temporary Account Agreement ..........................................14Right to Repayment of Indebtedness .................................14Authorized Signer (Individual Accounts Only) .....................15Restrictive Legends or Indorsements..................................15Pledges...........................................................................16Check Processing.............................................................16Indorsements ..................................................................16Death or Incompetence ....................................................17Fiduciary Accounts ..........................................................17Credit Verification ............................................................17Legal Actions Affecting Your Account.................................18Security ..........................................................................18Telephonic Instructions ....................................................19Monitoring and Recording Telephone Calls

and Consent to Receive Communications......................19Claim of Loss ..................................................................19Early Withdrawal Penalties (and involuntary withdrawals).....20Address or Name Changes ................................................20Resolving Account Disputes ..............................................20Waiver of Notices.............................................................20ACH and Wire Transfers ....................................................21Unclaimed Property Notice ...............................................21Remotely Created Checks .................................................21Checking Account Organization .........................................21FUNDS AVAILABILITY POLICY ...............................................22LONGER DELAYS MAY APPLY................................................23SPECIAL RULES FOR NEW ACCOUNTS....................................23DEPOSITS AT AUTOMATED TELLER MACHINES.........................24SUBSTITUTE CHECKS AND YOUR RIGHTS ...............................24

200846053-010.qxp_200846053-010 10/26/17 11:33 AM Page 3

ELECTRONIC FUND TRANSFERS ............................................25Electronic Funds Transfers Initiated by Third Parties ...........25Telephone TellerSM Transfers..............................................26ATM Transfers..................................................................27Types of ATM Card Point-of-Sale Transactions .....................27Types of Visa® Debit Card Point-of-Sale Transactions ..........27Visa®/Mastercard Foreign Transaction Fee..........................28Advisory Against Illegal Use ..............................................29Non-Visa Debit Transaction Processing...............................29Golden 1 OnlineSM Online Transfers ...................................30FEES ...............................................................................30DOCUMENTATION ..............................................................31PREAUTHORIZED PAYMENTS................................................31FINANCIAL INSTITUTION’S LIABILITY .....................................32CONFIDENTIALITY ..............................................................32UNAUTHORIZED TRANSFERS................................................32ERROR RESOLUTION NOTICE ................................................33NOTICE OF ATM/NIGHT DEPOSIT FACILITY

USER PRECAUTIONS .....................................................34WITHDRAWALS FROM YOUR ACCOUNT ..................................36Your Available Balance .....................................................36Operation of Account and Order of Posting .........................37Authorization Holds for Debit Card Transactions..................37INSUFFICIENT FUNDS - Overdrafts and Returned Items..............38General...........................................................................38Insufficient Funds - Overdrafts and Returned Items ............39Optional Overdraft Protection Services ...............................39Courtesy Pay (Including Courtesy Pay for Everyday

Debit Card Transactions) .............................................40Always a Discretionary Program.........................................42The Responsibility is Yours ...............................................42TRUTH-IN-SAVINGS DISCLOSURE..........................................43Regular Savings Account ..................................................43FlexSavingsSM Account .....................................................44Youth Savings Account .....................................................44Money Market Savings Account .........................................45IRA Savings Account........................................................46Santa SaverSM Savings Account .........................................47Collateral Account............................................................47Premium CheckingSM Account ...........................................48Free Checking Account.....................................................49Student Checking Account................................................49SmartStart CheckingSM Account.........................................49New Generation CheckingSM Account .................................50Golden 1 Freedom CheckingSM Account..............................50Term-Savings Certificate Account ......................................50Term-Savings IRA Certificate Account ................................5212-Month Term-Savings IRA Certificate Account.................53COMMON FEATURES...........................................................55

200846053-010.qxp_200846053-010 10/26/17 11:33 AM Page 4

5

GENERAL TERMS AND CONDITIONS OF YOUR ACCOUNT

IMPORTANT INFORMATION ABOUT PROCEDURES FOR OPENING ANEW ACCOUNT - To help the government fight the funding ofterrorism and money laundering activities, federal law requires allfinancial institutions to obtain, verify, and record information thatidentifies each person who opens an account.

What this means for you: When you open an account, we will ask foryour name, address, date of birth, and other information that willallow us to identify you. We may also ask to see your driver's licenseor other identifying documents.

Request Additional Information: We may from time to time requestadditional information from you to protect your account and oursystems from fraud or other problems.

This information may include new signature cards and otherdocumentation. You agree to assist us by promptly complying withany such request.

Additionally you agree to hold us harmless for refusing to pay orrelease funds, or take any other action relating to your accountwhere the refusal is based on your failure to provide thedocumentation or signatures requested by us.

AGREEMENT - To the extent that the terms contained in thisdisclosure are different than those in any other previous agreementor terms of account, this disclosure shall control and be deemed tomodify such other agreements or terms of account. This document,along with any other documents we give you pertaining to youraccount(s), is a contract that establishes rules which control youraccount(s) with us. Please read this carefully and retain it for futurereference. If you sign the signature card or open or continue to usethe account, you agree to these rules. You will receive a separateschedule of rates, qualifying balances, and fees if they are notincluded in this document. If you have any questions, please call us.

This agreement is subject to applicable federal laws, the laws of thestate of California and other applicable rules such as the operatingletters of the Federal Reserve Banks and payment processing systemrules (except to the extent that this agreement can and does varysuch rules or laws). The body of state and federal law that governsour relationship with you, however, is too large and complex to bereproduced here. The purpose of this document is to:

(1) summarize some laws that apply to common transactions;

(2) establish rules to cover transactions or events which the lawdoes not regulate;

(3) establish rules for certain transactions or events which thelaw regulates but permits variation by agreement; and

(4) give you disclosures of some of our policies to which youmay be entitled or in which you may be interested.

200846053-010.qxp_200846053-010 10/26/17 11:33 AM Page 5

6

If any provision of this document is found to be unenforceableaccording to its terms, all remaining provisions will continue in fullforce and effect. We may permit some variations from our standardagreement, but we must agree to any variation in writing either onthe signature card for your account or in some other document.Nothing in this document is intended to vary our duty to act in goodfaith and with ordinary care when required by law.

As used in this document the words “we,” “our,” “us”, and “creditunion” mean Golden 1 Credit Union and the words “you” and“your” mean the account holder(s) and anyone else with theauthority to deposit, withdraw, or exercise control over the funds inthe account. However, this agreement does not intend, and theterms “you” and “your” should not be interpreted, to expand anindividual’s responsibility for an organization’s liability. If thisaccount is owned by a corporation, partnership or other organization,individual liability is determined by the laws generally applicable tothat type of organization. The headings in this document are forconvenience or reference only and will not govern the interpretationof the provisions. Unless it would be inconsistent to do so, wordsand phrases used in this document should be construed so thesingular includes the plural and the plural includes the singular.

BYLAWS - By signing the Application for Membership, you agree tobe governed by the Bylaws, rules, regulations, and practices ofGolden 1 Credit Union and any existing or future amendmentsthereto, and by the federal and state Laws applicable to creditunions. A copy of the Bylaws is available for inspection at thecorporate headquarters of Golden 1 Credit Union. Our right torequire you to give us notice of your intention to withdraw fundsfrom your account is described in the bylaws. Unless we have agreedotherwise, you are not entitled to receive any original item after it ispaid, although you may request that we send you an item(s) or acopy of an item(s). Dividends are based on current earnings andavailable earnings of the credit union, after providing for requiredreserves.

LIABILITY - You agree, for yourself (and the person or entity yourepresent if you sign as a representative of another) to the terms ofthis account and the schedule of charges. You authorize us todeduct these charges, without notice to you, directly from theaccount balance as accrued. You will pay any additional reasonablecharges for services you request which are not covered by thisagreement.

We may reopen your account if we receive a dishonored or returneditem that you are responsible for, such as a preauthorized debitinitiated on your account and not canceled prior to account closure,and you will have to repay any balance due arising from suchtransaction.Each of you also agrees to be jointly and severally (individually)liable for any account shortage resulting from charges or overdrafts,

200846053-010.qxp_200846053-010 10/26/17 11:33 AM Page 6

7

whether caused by you or another with access to this account. Thisliability is due immediately, and can be deducted directly from theaccount balance whenever sufficient funds are available. You haveno right to defer payment of this liability, and you are liableregardless of whether you signed the item or benefited from thecharge or overdraft.

You will be liable for our costs as well as for our reasonableattorneys’ fees, to the extent permitted by law, whether incurred as aresult of collection or in any other dispute involving your account.This includes, but is not limited to, disputes between you andanother joint owner; you and an authorized signer or similar party; ora third party claiming an interest in your account. This also includesany action that you or a third party takes regarding the account thatcauses us, in good faith, to seek the advice of an attorney, whetheror not we become involved in the dispute. All costs and attorneys’fees can be deducted from your account when they are incurred,without notice to you.

DEPOSITS - We will give only provisional credit until collection isfinal for any items, other than cash, we accept for deposit (includingitems drawn “on us”). Before settlement of any item becomes final,we act only as your agent, regardless of the form of indorsement orlack of indorsement on the item and even though we provide youprovisional credit for the item. We may reverse any provisional creditfor items that are lost, stolen, or returned. You are responsible forany loss that occurs if any item is returned to us for any reason,including if it is fraudulent, counterfeit or otherwise invalid,regardless of whether the amount of the item has been madeavailable for your use. Unless prohibited by law, we also reserve theright to charge back to your account the amount of any itemdeposited to your account or cashed for you which was initially paidby the payor bank and which is later returned to us due to anallegedly forged, unauthorized or missing indorsement, claim ofalteration, encoding error or other problem which in our judgmentjustifies reversal of credit. You authorize us to attempt to collectpreviously returned items without giving you notice, and inattempting to collect we may permit the payor bank to hold an itembeyond the midnight deadline. Actual credit for deposits of, orpayable in, foreign currency will be at the exchange rate in effect onfinal collection in U.S. dollars. We are not responsible fortransactions by mail or outside depository until we actually recordthem. If you deliver a deposit to us and you will not be present whenthe deposit is counted, you may provide us an itemized list of thedeposit (deposit slip). To process the deposit, we will verify andrecord the deposit, and credit the deposit to the account. If thereare any discrepancies between the amounts shown on the itemizedlist of the deposit and the amount we determine to be the actualdeposit, you will be entitled to credit only for the actual deposit asdetermined by us, regardless of what is stated on the itemizeddeposit slip. We will treat and record all transactions received after

200846053-010.qxp_200846053-010 10/26/17 11:33 AM Page 7

8

our “daily cutoff time” on a business day we are open, or receivedon a day we are not open for business, as if initiated on the nextbusiness day that we are open. At our option, we may take an itemfor collection rather than for deposit. If we accept a third-partycheck for deposit, we may require any third-party indorsers to verifyor guarantee their indorsements, or indorse in our presence.

WITHDRAWALS - Generally - Unless clearly indicated otherwise on the accountrecords, any of you, acting alone, who signs to open the account orhas authority to make withdrawals may withdraw or transfer all orany part of the account balance at any time. Each of you (until wereceive written notice to the contrary) authorizes each other personwho signs or has authority to make withdrawals to indorse any itempayable to you or your order for deposit to this account or any othertransaction with us.

Postdated checks - A postdated check is one which bears a datelater than the date on which the check is written. We may properlypay and charge your account for a postdated check even thoughpayment was made before the date of the check, unless we havereceived written notice of the postdating in time to have areasonable opportunity to act. Because we process checksmechanically, your notice will not be effective and we will not beliable for failing to honor your notice unless it precisely identifiesthe number, date, amount and payee of the item.

Checks and withdrawal rules - If you do not purchase your checkblanks from us, you must be certain that we approve the checkblanks you purchase. We may refuse any withdrawal or transferrequest which you attempt on forms not approved by us or by anymethod we do not specifically permit. We may refuse any withdrawalor transfer request which is greater in number than the frequencypermitted, or which is for an amount greater or less than anywithdrawal limitations. We will use the date the transaction iscompleted by us (as opposed to the date you initiate it) to apply thefrequency limitations. In addition, we may place limitations on theaccount until your identity is verified.

Even if we honor a nonconforming request, we are not required to doso later. If you violate the stated transaction limitations (if any), inour discretion we may close your account or reclassify it as atransaction account. If we reclassify your account, your account willbe subject to the fees and earnings rules of the new accountclassification.

If we are presented with an item drawn against your account thatwould be a “substitute check,” as defined by law, but for an error ordefect in the item introduced in the substitute check creationprocess, you agree that we may pay such item.

See the funds availability policy disclosure for information aboutwhen you can withdraw funds you deposit. For those accounts towhich our funds availability policy disclosure does not apply, you

200846053-010.qxp_200846053-010 10/26/17 11:33 AM Page 8

9

can ask us when you make a deposit when those funds will beavailable for withdrawal. An item may be returned after the fundsfrom the deposit of that item are made available for withdrawal. Inthat case, we will reverse the credit of the item. We may determinethe amount of available funds in your account for the purpose ofdeciding whether to return an item for insufficient funds at any timebetween the time we receive the item and when we return the itemor send a notice in lieu of return. We need only make onedetermination, but if we choose to make a subsequentdetermination, the account balance at the subsequent time willdetermine whether there are insufficient available funds.

Overdrafts - You understand that we may, at our discretion, honorwithdrawal requests that overdraw your account. However, the factthat we may honor withdrawal requests that overdraw the accountbalance does not obligate us to do so later. So you can NOT rely onus to pay overdrafts on your account regardless of how frequently orunder what circumstances we have paid overdrafts on your accountin the past. We can change our practice of paying overdrafts on youraccount without notice to you. You can ask us if we have otheraccount services that might be available to you where we commit topaying overdrafts under certain circumstances, such as an overdraftprotection line-of-credit or a plan to sweep funds from anotheraccount you have with us. You agree that we may charge fees foroverdrafts as permitted by law. For consumer accounts, we will notcharge fees for overdrafts caused by ATM withdrawals or one-timedebit card transactions if you have not opted-in to that service. Wemay use subsequent deposits, including direct deposits of socialsecurity or other government benefits, to cover such overdrafts andoverdraft fees.

Multiple signatures, electronic check conversion, and similartransactions - An electronic check conversion transaction is atransaction where a check or similar item is converted into anelectronic fund transfer as defined in the Electronic Fund Transfersregulation. In these types of transactions the check or similar item iseither removed from circulation (truncated) or given back to you. Asa result, we have no opportunity to review the check to examine thesignatures on the item. You agree that, as to these or any items as towhich we have no opportunity to examine the signatures, youacknowledge that multiple signatures are not allowed forwithdrawals on any accounts with this credit union.

OWNERSHIP OF ACCOUNT AND BENEFICIARY DESIGNATION -You agree that the shares purchased for this account shall be heldindividually, in joint tenancy, or as trustee and co-trustee with theperson or persons named on the membership application, if any(excluding IRA funds). We do not offer business accounts at thistime. You further agree that Golden 1 Credit Union is authorized torecognize any of the signatures subscribed on the membershipapplication in the payment of funds or the transaction of anybusiness for this account.

200846053-010.qxp_200846053-010 10/26/17 11:33 AM Page 9

10

IRA owners understand that periodic IRA statements will becombined with the periodic statement for all other accounts openedpursuant to the membership application and that information aboutthe IRA will therefore be disclosed to all of the persons named onthe membership application. If you wish to have the IRA statementprovided exclusively to the IRA owner, you must establish a separateIRA account.

These rules apply to this account depending on the form ofownership and beneficiary designation, if any, specified on theaccount records. We make no representations as to theappropriateness or effect of the ownership and beneficiarydesignations, except as they determine to whom we pay the accountfunds. As used in this agreement “party” means a person who, bythe terms of the account, has a present right, subject to request, topayment from a multiple-party account other than as an agent.

Individual Account - This account is in the name of one person.

Joint Account - This account or certificate is owned by the namedparties. Upon the death of any of them, ownership passes to thesurvivor(s).

PAY ON DEATH Account with Single Party - This account orcertificate is owned by the named party. Upon the death of thatparty, ownership passes to the named pay-on-death payee(s).

PAY ON DEATH Account with Multiple Parties - This account orcertificate is owned by the named parties. Upon the death of any ofthem, ownership passes to the survivor(s). Upon the death of all ofthem, ownership passes to the named pay-on-death payee(s).

Totten Trust Account - (subject to this form) - If two or more of youcreate this account, you own the account jointly with survivorship.Beneficiaries cannot withdraw unless: (1) all persons creating theaccount die, and (2) the beneficiary is then living. If two or morebeneficiaries are named and survive the death of all personscreating the account, such beneficiaries will own this account inequal shares, without right of survivorship. The person(s) creatingthis account type reserves the right to: (1) change beneficiaries, (2)change account types, and (3) withdraw all or part of the accountfunds at any time.

Trust Account Subject to Separate Agreement - We will abide bythe terms of any separate agreement which clearly pertains to thisaccount and which you file with us. Any additional consistent termsstated on this form will also apply.

STOP PAYMENTS - Unless otherwise provided, the rules in thissection cover stopping payment of items such as checks and drafts.Rules for stopping payment of other types of transfers of funds, suchas consumer electronic fund transfers, may be established by law orour policy. If we have not disclosed these rules to you elsewhere, youmay ask us about those rules.

200846053-010.qxp_200846053-010 10/26/17 11:33 AM Page 10

11

We may accept an order to stop payment on any item from any oneof you. You must make any stop-payment order in the mannerrequired by law and we must receive it in time to give us areasonable opportunity to act on it before our stop-payment cutofftime. Because stop-payment orders are handled by computers, to beeffective, your stop-payment order must precisely identify thenumber, date, and amount of the item, and the payee. You may stoppayment on any item drawn on your account whether you sign theitem or not. Generally, if your stop-payment order is given to us inwriting it is effective for six months. Your order will lapse after thattime if you do not renew the order in writing before the end of thesix-month period. We are not obligated to notify you when a stop-payment order expires. A release of the stop-payment request maybe made only by the person who initiated the stop-payment order.

If you stop payment on an item and we incur any damages orexpenses because of the stop payment, you agree to indemnify usfor those damages or expenses, including attorneys’ fees. You assignto us all rights against the payee or any other holder of the item. Youagree to cooperate with us in any legal actions that we may takeagainst such persons. You should be aware that anyone holding theitem may be entitled to enforce payment against you despite thestop-payment order.

Our stop-payment cutoff time is one hour after the opening of thenext banking day after the banking day on which we receive theitem. Additional limitations on our obligation to stop payment areprovided by law (e.g., we paid the item in cash or we certified theitem).

TELEPHONE TRANSFERS - A telephone transfer of funds from thisaccount to another account with us, if otherwise arranged for orpermitted, may be made by the same persons and under the sameconditions generally applicable to withdrawals made in writing.Unless a different limitation is disclosed in writing, we restrict thenumber of transfers from a savings account to another account or tothird parties, to a maximum of six per month (less the number of“preauthorized transfers” during the month). Other account transferrestrictions may be described elsewhere.

AMENDMENTS AND TERMINATION - We may change our bylawsand any term of this agreement. Rules governing changes in ratesare provided separately in the Truth-in-Savings disclosure or inanother document. For other changes we will give you reasonablenotice in writing or by any other method permitted by law. If we havenotified you of a change in any term of your account and youcontinue to have your account after the effective date of the change,you have agreed to the new term(s).

We may close this account if your membership in the credit unionterminates, or by giving reasonable notice to you and tender of theaccount balance personally or by mail. Items presented for paymentafter the account is closed may be dishonored. When you close your

200846053-010.qxp_200846053-010 10/26/17 11:33 AM Page 11

12

account, you are responsible for leaving enough money in the account to cover any outstanding items and charges to be paid from the account. Reasonable notice depends on the circumstances, and in some cases such as when we cannot verify your identity or we suspect fraud, it might be reasonable for us to give you notice after the change or account closure becomes effective. For instance, if we suspect fraudulent activity with respect to your account, we might immediately freeze or close your account and then give you notice.

You must not use or try to use your account or any of our products and services for any unlawful transactions. You also must not engage in any activities that abuse our products or services or are deemed by us to be unusual, fraudulent, dishonest or deceptive. You agree not to use your personal account for business related activity. You also agree not to engage in conduct that poses a threat to the health, safety, and welfare of our employees and/or other members, including violent or threatening behavior, or interfere with our employees carrying out their duties or functions.

If we have reason to believe that you violated the terms of this Agreement, for example, by using your personal account for business transactions or engaging in unlawful, unusual or fraudulent activities, we may, at our option, restrict or suspend your access to any or all products or member services or close your account. We may also restrict or suspend your access to any of our products or services upon giving you notice reasonable under the circumstances when you become delinquent in your obligations to the credit union or cause a loss to the credit union. In such case, we may also deny your subsequent application for any new product or service that would allow you to obtain further credit from the credit union or cause the credit union a further loss. Restrictions or suspensions of accounts, products and services will be reasonably related to the nature of your conduct, and will apply to joint owners and authorized users. Our good faith determination whether a particular transaction is permissible under this Agreement shall be conclusive.

You may be expelled from membership for any reason allowed by applicable law, including failure to comply with the credit union’s bylaws, conviction of a criminal offense, causing a loss to the credit union or otherwise failing to carry out your contracts, agreements, or obligations with the credit union, conducting yourself in a threatening or abusive manner to our employees and/or other members, or willfully destroying or damaging credit union property. If you are expelled, you may not be a fiduciary or a joint account owner on another account.

NOTICES - Any written notice you give us is effective when we actually receive it, and it must be given to us according to the specific delivery instructions provided elsewhere, if any. We must receive it in time to have a reasonable opportunity to act on it. If the notice is regarding a check or other item, you must give us sufficient information to be able to identify the check or item, including the

200846053-010.qxp_200846053-010 10/26/17 11:33 AM Page 12

13

precise check or item number, amount, date and payee. Writtennotice we give you is effective when it is deposited in the UnitedStates Mail with proper postage and addressed to your mailingaddress we have on file. Notice to any of you is notice to all of you.

CHANGE IN TERMS NOTICE - You will be notified of a change interms to this disclosure when such notice is required by law.

STATEMENTS - Your duty to report unauthorized signatures,alterations and forgeries - You must examine your statement ofaccount with “reasonable promptness.” If you discover (orreasonably should have discovered) any unauthorized signatures oralterations, you must promptly notify us of the relevant facts. Asbetween you and us, if you fail to perform either of these duties, youwill have to either share the loss with us, or bear the loss entirelyyourself (depending on whether we used ordinary care and, if not,whether we contributed to the loss). The loss could be not only withrespect to items on the statement but other items with unauthorizedsignatures or alterations by the same wrongdoer.

You agree that the time you have to examine your statement andreport to us will depend on the circumstances, but will not, in anycircumstance, exceed a total of 30 days from when the statement isfirst sent or made available to you.

You further agree that if you fail to report any unauthorizedsignatures, alterations or forgeries in your account within 60 days ofwhen we first send or make the statement available, you cannotassert a claim against us on any items in that statement, and asbetween you and us the loss will be entirely yours. This 60-daylimitation is without regard to whether we used ordinary care. Thelimitation in this paragraph is in addition to that contained in thefirst paragraph of this section.

Your duty to report other errors - In addition to your duty to reviewyour statements for unauthorized signatures, alterations andforgeries, you agree to examine your statement with reasonablepromptness for any other error - such as an encoding error. Inaddition, if you receive or we make available either your items orimages of your items, you must examine them for any unauthorizedor missing indorsements or any other problems. You agree that thetime you have to examine your statement and items and report to uswill depend on the circumstances. However, this time period shallnot exceed 60 days. Failure to examine your statement and itemsand report any errors to us within 60 days of when we first send ormake the statement available precludes you from asserting a claimagainst us for any errors on items identified in that statement and asbetween you and us the loss will be entirely yours.

Errors relating to electronic fund transfers or substitute checks -For information on errors relating to electronic fund transfers (e.g.,computer, debit card or ATM transactions) refer to your ElectronicFund Transfers disclosure and the sections on consumer liability and

200846053-010.qxp_200846053-010 10/26/17 11:33 AM Page 13

14

error resolution. For information on errors relating to a substitutecheck you received, refer to your disclosure entitled SubstituteChecks and Your Rights.

ACCOUNT TRANSFER - This account may not be transferred orassigned without our prior written consent.

DIRECT DEPOSITS - If we are required for any reason to reimbursethe federal government for all or any portion of a benefit paymentthat was directly deposited into your account, you authorize us todeduct the amount of our liability to the federal government fromthe account or from any other account you have with us, withoutprior notice and at any time, except as prohibited by law. We mayalso use any other legal remedy to recover the amount of ourliability.

TEMPORARY ACCOUNT AGREEMENT - If the accountdocumentation indicates that this is a temporary accountagreement, each person who signs to open the account or hasauthority to make withdrawals (except as indicated to the contrary)may transact business on this account. However, we may at sometime in the future restrict or prohibit further use of this account ifyou fail to comply with the requirements we have imposed within areasonable time.

RIGHT TO REPAYMENT OF INDEBTEDNESS - You each agree thatwe may (without prior notice and when permitted by law) chargeagainst and deduct from this account any due and payable debt anyof you owe us now or in the future. If this account is owned by oneor more of you as individuals, we may set off any funds in theaccount against a due and payable debt a partnership owes us nowor in the future, to the extent of your liability as a partner for thepartnership debt. If your debt arises from a promissory note, thenthe amount of the due and payable debt will be the full amount wehave demanded, as entitled under the terms of the note, and thisamount may include any portion of the balance for which we haveproperly accelerated the due date.

In addition to these contract rights, we may also have rights under a“statutory lien.” A “lien” on property is a creditor’s right to obtainownership of the property in the event a debtor defaults on a debt. A“statutory lien” is one created by federal or state statute. If federalor state law provides us with a statutory lien, then we are authorizedto apply, without prior notice, your shares and dividends to any debtyou owe us, in accord with the statutory lien.

Neither our contract rights nor rights under a statutory lien apply tothis account if prohibited by law. For example, neither our contractrights nor rights under a statutory lien apply to this account if: (a) itis an Individual Retirement Account or similar tax-deferred account,or (b) the debt is created by a consumer credit transaction under acredit card plan (but this does not affect our rights under anyconsensual security interest), or (c) the debtor’s right of withdrawalarises only in a representative capacity, or (d) setoff is prohibited by

200846053-010.qxp_200846053-010 10/26/17 11:33 AM Page 14

15

the Military Lending Act or its implementing regulations. We will notbe liable for the dishonor of any check or draft when the dishonoroccurs because we charge and deduct an amount you owe us fromyour account. You agree to hold us harmless from any claim arisingas a result of our exercise of our right to repayment.

You agree to pledge all shares, payments on shares, dividends onshares, and deposits (excluding IRA accounts or other accounts tothe extent that applicable law precludes the pledge of suchaccounts) in all joint and individual accounts held by you, which youhave now or in the future with Golden 1 Credit Union, as security forall your obligations with Golden 1 Credit Union. These obligationsinclude but are not limited to principal, interest, late charges,finance charges, costs, and expenses, including attorney’s fees. Youauthorize Golden 1 Credit Union, without further notice, to applyany and all shares, payments, dividends and deposits to thepayment of each obligation if you should default. You agree thatGolden 1 Credit Union’s lien is independent of any securityagreement you may sign, and Golden 1 Credit Union may enforce itslien in any manner, at any time allowed by law. You agree that youown any shares pledged and that there are no liens against themother than Golden 1 Credit Union’s.

AUTHORIZED SIGNER (Individual Accounts Only) - A singleindividual is the owner. The authorized signer is merely designatedto conduct transactions on the owner’s behalf. The owner does notgive up any rights to act on the account, and the authorized signermay not in any manner affect the rights of the owner orbeneficiaries, if any, other than by withdrawing funds from theaccount. The owner is responsible for any transactions of theauthorized signer. We undertake no obligation to monitortransactions to determine that they are on the owner’s behalf.

The owner may terminate the authorization at any time, and theauthorization is automatically terminated by the death of the owner.However, we may continue to honor the transactions of theauthorized signer until: (a) we have received written notice or haveactual knowledge of the termination of authority, and (b) we have areasonable opportunity to act on that notice or knowledge. We mayrefuse to accept the designation of an authorized signer.

RESTRICTIVE LEGENDS OR INDORSEMENTS - The automatedprocessing of the large volume of checks we receive prevents usfrom inspecting or looking for restrictive legends, restrictiveindorsements or other special instructions on every check. Examplesof restrictive legends placed on checks are “must be presentedwithin 90 days” or “not valid for more than $1,000.00.” Thepayee’s signature accompanied by the words “for deposit only” is anexample of a restrictive indorsement. For this reason, we are notrequired to honor any restrictive legend or indorsement or otherspecial instruction placed on checks you write unless we haveagreed in writing to the restriction or instruction. Unless we have

200846053-010.qxp_200846053-010 10/26/17 11:33 AM Page 15

16

agreed in writing, we are not responsible for any losses, claims,damages, or expenses that result from your placement of theserestrictions or instructions on your checks.

PLEDGES - Each owner of this account may pledge all or any part ofthe funds in it for any purpose. Any pledge of this account must firstbe satisfied before the rights of any surviving account owner oraccount beneficiary become effective.

CHECK PROCESSING - We process items mechanically by relyingsolely on the information encoded in magnetic ink along the bottomof the items. This means that we do not individually examine all ofyour items to determine if the item is properly completed, signedand indorsed or to determine if it contains any information otherthan what is encoded in magnetic ink. You agree that we haveexercised ordinary care if our automated processing is consistentwith general banking practice, even though we do not inspect eachitem. Because we do not inspect each item, if you write a check tomultiple payees, we can properly pay the check regardless of thenumber of indorsements unless you notify us in writing that thecheck requires multiple indorsements. We must receive the notice intime for us to have a reasonable opportunity to act on it, and youmust tell us the precise date of the check, amount, check numberand payee. We are not responsible for any unauthorized signature oralteration that would not be identified by a reasonable inspection ofthe item. Using an automated process helps us keep costs down foryou and all account holders.

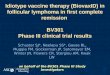

INDORSEMENTS - We may accept for deposit any item payable to youor your order, even if they are not indorsed by you. We may give cashback to any one of you. We may supply any missing indorsement(s)for any item we accept for deposit or collection, and you warrantthat all indorsements are genuine.

To ensure that your check or share draft is processed without delay,you must indorse it (sign it on the back) in a specific area. Yourentire indorsement (whether a signature or a stamp) along with anyother indorsement information (e.g. additional indorsements, IDinformation, driver’s license number, etc.) must fall within 11/2” ofthe “trailing edge” of a check. Indorsements must be made in blueor black ink, so that they are readable.

As you look at the front of a check, the “trailing edge” is the leftedge. When you flip the check over, be sure to keep all indorsementinformation within 11/2” of that edge.

200846053-010.qxp_200846053-010 10/26/17 11:33 AM Page 16

17

It is important that you confine the indorsement information to thisarea since the remaining blank space will be used by others in theprocessing of the check to place additional needed indorsementsand information. You agree that you will indemnify, defend, and holdus harmless for any loss, liability, damage or expense that occursbecause your indorsement, another indorsement or information youhave printed on the back of the check obscures our indorsement.These indorsement guidelines apply to both personal and businesschecks.DEATH OR INCOMPETENCE - You agree to notify us promptly if anyperson with a right to withdraw funds from your account(s) dies or isadjudicated (determined by the appropriate official) incompetent.We may continue to honor your checks, items, and instructionsuntil: (a) we know of your death or adjudication of incompetence,and (b) we have had a reasonable opportunity to act on thatknowledge. You agree that we may pay or certify checks drawn on orbefore the date of death or adjudication of incompetence for up toten (10) days after your death or adjudication of incompetenceunless ordered to stop payment by someone claiming an interest inthe account.FIDUCIARY ACCOUNTS - Accounts may be opened by a personacting in a fiduciary capacity. A fiduciary is someone who isappointed to act on behalf of and for the benefit of another. We arenot responsible for the actions of a fiduciary, including the misuseof funds. This account may be opened and maintained by a personor persons named as a trustee under a written trust agreement, or asexecutors, administrators, or conservators under court orders. Youunderstand that by merely opening such an account, we are notacting in the capacity of a trustee in connection with the trust nordo we undertake any obligation to monitor or enforce the terms ofthe trust or letters.CREDIT VERIFICATION - You agree that we may verify credit andemployment history by any necessary means, including preparationof a credit report by a credit reporting agency.

FRONT OF CHECK

Bank Nameand Location

A123456789A 7654

Pay to theorder of $

dollars

20NameAddress, City, State

7654

BACK OF CHECK

Memo

Keep your indorsementout of this area.

1 1/2"

TRAILING EDGE

YOUR INDORSEMENT MUSTBE WITHIN THIS AREA

200846053-010.qxp_200846053-010 10/26/17 11:33 AM Page 17

18

LEGAL ACTIONS AFFECTING YOUR ACCOUNT - If we are servedwith a subpoena, restraining order, writ of attachment or execution,levy, garnishment, search warrant, or similar order relating to youraccount (termed “legal action” in this section), we will comply withthat legal action. Or, in our discretion, we may freeze the assets inthe account and not allow any payments out of the account until afinal court determination regarding the legal action. We may dothese things even if the legal action involves less than all of you. Inthese cases, we will not have any liability to you if there areinsufficient funds to pay your items because we have withdrawnfunds from your account or in any way restricted access to yourfunds in accordance with the legal action. Any fees or expenses weincur in responding to any legal action (including, withoutlimitation, attorneys’ fees and our internal expenses) may becharged against your account. The list of fees applicable to youraccount(s) provided elsewhere may specify additional fees that wemay charge for certain legal actions.

SECURITY - It is your responsibility to protect the account numbersand electronic access devices (e.g., an ATM card) we provide you foryour account(s). Do not discuss, compare, or share informationabout your account number(s) with anyone unless you are willing togive them full use of your money. An account number can be usedby thieves to issue an electronic debit or to encode your number ona false demand draft which looks like and functions like anauthorized check. If you furnish your access device and grant actualauthority to make transfers to another person (a family member orcoworker, for example) who then exceeds that authority, you areliable for the transfers unless we have been notified that transfers bythat person are no longer authorized.

Your account number can also be used to electronically removemoney from your account, and payment can be made from youraccount even though you did not contact us directly and order thepayment.

You must also take precaution in safeguarding your blank checks.Notify us at once if you believe your checks have been lost or stolen.As between you and us, if you are negligent in safeguarding yourchecks, you must bear the loss entirely yourself or share the losswith us (we may have to share some of the loss if we failed to useordinary care and if we substantially contributed to the loss).

Except for consumer electronic funds transfers subject to RegulationE, you agree that if we offer you services appropriate for youraccount to help identify and limit fraud or other unauthorizedtransactions against your account, such as positive pay orcommercially reasonable security procedures, and you reject thoseservices, you will be responsible for any fraudulent or unauthorizedtransactions which could have been prevented by the services weoffered, unless we acted in bad faith or to the extent our negligencecontributed to the loss. If we offered you a commercially reasonablesecurity procedure which you reject, you agree that you are

200846053-010.qxp_200846053-010 10/26/17 11:33 AM Page 18

19

responsible for any payment order, whether authorized or not, thatwe accept in compliance with an alternative security procedure thatyou have selected.

TELEPHONIC INSTRUCTIONS - Unless required by law or we haveagreed otherwise in writing, we are not required to act uponinstructions you give us via facsimile transmission or leave by voicemail or on a telephone answering machine.

MONITORING AND RECORDING TELEPHONE CALLS AND CONSENTTO RECEIVE COMMUNICATIONS - We may monitor or record phonecalls for security reasons, to maintain a record and to ensure thatyou receive courteous and efficient service.

We may contact you from time to time by telephone, text messaging,email or mail in order to service your account or collect amounts youowe to us. We are permitted to use any address, telephone numberor email address you provide to us. You agree to provide accurateand current contact information and only give us telephone numbersand email addresses that belong to you. We may sendcommunications electronically, such as by email or text message,rather than by mail, unless the law requires otherwise.

When you give us a telephone number (including a cellular ormobile device number) or place a telephone call to us, you areproviding your express consent permitting us (and any party actingon our behalf) to contact you at that number about all of yourGolden 1 accounts. Your consent allows us to make live telephonecalls, send text messages, leave prerecorded or artificial voicemessages, and use automatic telephone dialing technology forinformational and account service purposes. For example, we mayplace such calls or texts to provide notices, investigate or preventfraud, or contact you about the amounts you owe to us. This expressconsent applies to each telephone number that you provide to usnow or in the future. Message and data rates may apply. You maychange your communication preferences at any time by anyreasonable means, including calling us at 1-877-723-3010,sending an email to [email protected], or writing to us atGolden 1 Credit Union, Attn: Member Care, P.O. Box 15966,Sacramento, CA 95852-0966.

CLAIM OF LOSS - If you claim a credit or refund because of aforgery, alteration, or any other unauthorized withdrawal, youagree to cooperate with us in the investigation of the loss,including giving us an affidavit containing whatever reasonableinformation we require concerning your account, the transaction,and the circumstances surrounding the loss. You will notify lawenforcement authorities of any criminal act related to the claimof lost, missing, or stolen checks or unauthorized withdrawals.We will have a reasonable period of time to investigate the factsand circumstances surrounding any claim of loss. Unless wehave acted in bad faith, we will not be liable for special orconsequential damages, including loss of profits or opportunity,

200846053-010.qxp_200846053-010 10/26/17 11:33 AM Page 19

20

or for attorneys’ fees incurred by you. You agree not to give ormake available your password or credentials to any unauthorizedindividuals, and take reasonable precautions to safeguard yourcredentials and account information. If you disclose your accountnumber, card number, PIN, credentials, and/or any other meansto access your account to anyone, you assume all risks andlosses associated with such disclosure. This means that you areresponsible, to the extent permitted by law, for any transactionsand activities performed from your accounts by such person orentity, even those you did not intend them to make.

You agree that you will not waive any rights you have to recover yourloss against anyone who is obligated to repay, insure, or otherwisereimburse you for your loss. You will pursue your rights or, at ouroption, assign them to us so that we may pursue them. Our liabilitywill be reduced by the amount you recover or are entitled to recoverfrom these other sources.

EARLY WITHDRAWAL PENALTIES (and involuntary withdrawals) -We may impose early withdrawal penalties on a withdrawal from atime account even if you don’t initiate the withdrawal. For instance,the early withdrawal penalty may be imposed if the withdrawal iscaused by our setoff against funds in the account or as a result of anattachment or other legal process. We may close your account andimpose the early withdrawal penalty on the entire account balancein the event of a partial early withdrawal. See your notice of penaltyfor early withdrawals for additional information.

ADDRESS OR NAME CHANGES - You are responsible for notifying usof any change in your address or your name. Unless we agreeotherwise, change of address or name must be made in writing by atleast one of the account holders. Informing us of your address orname change on a check reorder form is not sufficient. We willattempt to communicate with you only by use of the most recentaddress you have provided to us. If provided elsewhere, we mayimpose a service fee if we attempt to locate you.

RESOLVING ACCOUNT DISPUTES - We may place an administrativehold on the funds in your account (refuse payment or withdrawal ofthe funds) if it becomes subject to a claim adverse to (1) your owninterest; (2) others claiming an interest as survivors or beneficiariesof your account; or (3) a claim arising by operation of law. The holdmay be placed for such period of time as we believe reasonablynecessary to allow a legal proceeding to determine the merits of theclaim or until we receive evidence satisfactory to us that the disputehas been resolved. We will not be liable for any items that aredishonored as a consequence of placing a hold on funds in youraccount for these reasons.

WAIVER OF NOTICES - To the extent permitted by law, you waiveany notice of non-payment, dishonor or protest regarding any itemscredited to or charged against your account. For example, if youdeposit a check and it is returned unpaid or we receive a notice of

200846053-010.qxp_200846053-010 10/26/17 11:33 AM Page 20

21

nonpayment, we do not have to notify you unless required by federalRegulation CC or other law.

ACH AND WIRE TRANSFERS - This agreement is subject to Article4A of the Uniform Commercial Code - Fund Transfers as adopted inthe state in which you have your account with us. If you originate afund transfer and you identify by name and number a beneficiaryfinancial institution, an intermediary financial institution or abeneficiary, we and every receiving or beneficiary financialinstitution may rely on the identifying number to make payment. Wemay rely on the number even if it identifies a financial institution,person or account other than the one named. You agree to be boundby automated clearing house association rules. These rules provide,among other things, that payments made to you, or originated byyou, are provisional until final settlement is made through a FederalReserve Bank or payment is otherwise made as provided in Article4A-403(a) of the Uniform Commercial Code. If we do not receivesuch payment, we are entitled to a refund from you in the amountcredited to your account and the party originating such payment willnot be considered to have paid the amount so credited. Creditentries may be made by ACH. If we receive a payment order tocredit an account you have with us by wire or ACH, we are notrequired to give you any notice of the payment order or credit.

UNCLAIMED PROPERTY NOTICE - Your property may be transferredto the appropriate state if no activity occurs in the account withinthe time period specified by state law.

REMOTELY CREATED CHECKS - Like any standard check or draft, aremotely created check (sometimes called a telecheck,preauthorized draft or demand draft) is a check or draft that can beused to withdraw money from an account. Unlike a typical check ordraft, however, a remotely created check is not issued by the payingbank and does not contain the signature of the account owner (or asignature purported to be the signature of the account owner). Inplace of a signature, the check usually has a statement that theowner authorized the check or has the owner’s name typed orprinted on the signature line.

You warrant and agree to the following for every remotely createdcheck we receive from you for deposit or collection: (1) you havereceived express and verifiable authorization to create the check inthe amount and to the payee that appears on the check; (2) you willmaintain proof of the authorization for at least 2 years from the dateof the authorization, and supply us the proof if we ask; and (3) if acheck is returned you owe us the amount of the check, regardless ofwhen the check is returned. We may take funds from your accountto pay the amount you owe us, and if there are insufficient funds inyour account, you still owe us the remaining balance.

CHECKING ACCOUNT ORGANIZATION - Your checking accountconsists of two subaccounts. One of these subaccounts is atransaction subaccount (e.g., a checking subaccount). You willtransact business on this subaccount as usual. The other is a

200846053-010.qxp_200846053-010 10/26/17 11:33 AM Page 21

22

nontransaction subaccount (e.g., a savings account). You cannotdirectly access the nontransaction savings subaccount, but youagree that we may automatically, and without a specific requestfrom you, initiate individual transfers of funds between subaccountsfrom time to time at no cost or effect to you. This accountorganization will not change the amount of NCUA insuranceavailable to you, your available balance, the information on yourperiodic statements, the dividend earnings (if this is a dividend-bearing account), or any other feature of your checking account. Youwill not see any difference between the way your account operatesand the way a traditionally organized account operates, but thisorganization makes us more efficient and helps us to keep costsdown.

FUNDS AVAILABILITY POLICYThis policy statement applies to all accounts.

Our policy is to make funds from your cash, check, and electronicdirect deposits available to you on the same day we receive yourdeposit. At that time, you can withdraw the funds in cash and we willuse the funds to pay transactions that you have authorized, subjectto certain exceptions described in this policy.

Please remember that even after we have made funds available toyou, and you have withdrawn the funds, you are still responsible forchecks you deposit that are returned to us unpaid and for any otherproblems involving your deposit. All deposits are subject toverification.

For determining the availability of your deposits, every day is abusiness day, except Saturdays, Sundays, and federal holidays. If youmake a deposit before closing on a business day that we are open,we will consider that day to be the day of your deposit. However, ifyou make a deposit after closing or on a day we are not open, we willconsider that the deposit was made on the next business day we areopen.

If you make a deposit at an ATM on a day that we are open, we willconsider that day to be the day of your deposit. However, if you makea deposit at an ATM on a day we are not open, we will consider thatthe deposit was made on the next business day we are open.

If we cash a check for you that is drawn on another bank, we maywithhold the availability of a corresponding amount of funds that arealready in your account. Those funds will be available at the timefunds from the check we cashed would have been available if youhad deposited it.

If we accept for deposit a check that is drawn on another bank, wemay make funds from the deposit available for withdrawalimmediately but delay your availability to withdraw a correspondingamount of funds that you have on deposit in another account with

200846053-010.qxp_200846053-010 10/26/17 11:33 AM Page 22

23

us. The funds in the other account would then not be available forwithdrawal until the time periods that are described elsewhere inthis disclosure for the type of check that you deposited.

LONGER DELAYS MAY APPLYCase-by-case delays. In some cases, we will not make all of thefunds that you deposit by check available to you on the same daywe receive your deposit. Depending on the type of check that youdeposit, funds may not be available until the second business dayafter the day of your deposit. The first $200 of your deposits,however, will be available on the same day.

If we are not going to make all of the funds from your depositavailable on the same day we receive your deposit, we will notify youat the time you make your deposit. We will also tell you when thefunds will be available. If your deposit is not made directly to one ofour employees, or if we decide to take this action after you have leftthe premises, we will mail you the notice by the day after we receiveyour deposit.

If you will need the funds from a deposit right away, you should askus when the funds will be available.

Safeguard exceptions. In addition, funds you deposit by check maybe delayed for a longer period under the following circumstances:

We believe a check you deposit will not be paid.

You deposit checks totaling more than $5,000 on any one day.

You redeposit a check that has been returned unpaid.

You have overdrawn your account repeatedly in the last six months.

There is an emergency, such as failure of computer orcommunications equipment.

We will notify you if we delay your ability to withdraw funds for any ofthese reasons, and we will tell you when the funds will be available.They will generally be available no later than the seventh business dayafter the day of your deposit.

SPECIAL RULES FOR NEW ACCOUNTSIf you are a new member, the following special rules will applyduring the first 30 days your account is open.

Funds from electronic direct deposits to your account will beavailable on the day we receive the deposit. Funds from deposits ofcash, wire transfers, and the first $5,000 of a day’s total deposits ofcashier’s, certified, teller’s, traveler’s, and federal, state and localgovernment checks will be available on the same day as the day ofyour deposit if the deposit meets certain conditions. For example,the checks must be payable to you (and you may have to use a

200846053-010.qxp_200846053-010 10/26/17 11:33 AM Page 23

24

special deposit slip). The excess over $5,000 will be available onthe ninth business day after the day of your deposit. If your depositof these checks (other than a U.S. Treasury check) is not made inperson to one of our employees, the first $5,000 will not beavailable until the second business day after the day of your deposit.

Funds from all other check deposits will be available on the ninthbusiness day after the day of your deposit.

DEPOSITS AT AUTOMATED TELLER MACHINESFunds from any deposits (cash or check) made at automated tellermachines (ATMs), whether we own and operate or not, may not beavailable until the second business day after the day of your deposit.All deposits are subject to verification.

All ATMs that we own or operate are identified as our machines.

SUBSTITUTE CHECKS AND YOUR RIGHTSWhat is a substitute check?

To make check processing faster, federal law permits financialinstitutions to replace original checks with “substitute checks.”These checks are similar in size to original checks with a slightlyreduced image of the front and back of the original check. The frontof a substitute check states: “This is a legal copy of your check. Youcan use it the same way you would use the original check.” You mayuse a substitute check as proof of payment just like the originalcheck.

Some or all of the checks that you receive back from us may besubstitute checks. This notice describes rights you have when youreceive substitute checks from us. The rights in this notice do notapply to original checks or to electronic debits to your account.However, you have rights under other law with respect to thosetransactions.

What are my rights regarding substitute checks?

In certain cases, federal law provides a special procedure that allowsyou to request a refund for losses you suffer if a substitute check isposted to your account (for example, if you think that we withdrewthe wrong amount from your account or that we withdrew moneyfrom your account more than once for the same check). The lossesyou may attempt to recover under this procedure may include theamount that was withdrawn from your account and fees that werecharged as a result of the withdrawal (for example, bounced checkfees).

The amount of your refund under this procedure is limited to theamount of your loss or the amount of the substitute check,whichever is less. You also are entitled to dividends on the amountof your refund if your account is a dividend-bearing account. If your

200846053-010.qxp_200846053-010 10/26/17 11:33 AM Page 24

25

loss exceeds the amount of the substitute check, you may be able torecover additional amounts under other law.

If you use this procedure, you may receive up to $2,500 of yourrefund (plus dividends if your account earns dividends) within 10business days after we received your claim and the remainder ofyour refund (plus dividends if your account earns dividends) notlater than 45 calendar days after we received your claim.

We may reverse the refund (including any dividends on the refund) ifwe later are able to demonstrate that the substitute check wascorrectly posted to your account.

How do I make a claim for a refund?

If you believe that you have suffered a loss relating to a substitutecheck that you received and that was posted to your account, pleasecontact us at:

GOLDEN 1 CREDIT UNIONP.O. BOX 15966

SACRAMENTO, CA 95852-09661-877-GOLDEN 1 or (1-877-465-3361)

You must contact us within 40 calendar days of the date that wemailed (or otherwise delivered by a means to which you agreed) thesubstitute check in question or the account statement showing thatthe substitute check was posted to your account, whichever is later.We will extend this time period if you were not able to make a timelyclaim because of extraordinary circumstances.

Your claim must include —

• A description of why you have suffered a loss (for example,you think the amount withdrawn was incorrect);

• An estimate of the amount of your loss;

• An explanation of why the substitute check you received isinsufficient to confirm that you suffered a loss; and

• A copy of the substitute check or the following informationto help us identify the substitute check: the check number,the amount of the check, the date of the check, and thename of the person to whom you wrote the check.

ELECTRONIC FUND TRANSFERSIndicated below are types of Electronic Fund Transfers we arecapable of handling, some of which may not apply to your account.Please read this disclosure carefully because it tells you your rightsand obligations for the transactions listed. You should keep thisnotice for future reference.

Electronic Funds Transfers Initiated By Third Parties. You mayauthorize a third party to initiate electronic fund transfers between

200846053-010.qxp_200846053-010 10/26/17 11:33 AM Page 25

26

your account and the third party’s account. These transfers to makeor receive payment may be one-time occurrences or may recur asdirected by you. These transfers may use the Automated ClearingHouse (ACH) or other payments network. Your authorization to thethird party to make these transfers can occur in a number of ways.For example, your authorization to convert a check or draft to anelectronic fund transfer or to electronically pay a returned check ordraft charge can occur when a merchant provides you with notice andyou go forward with the transaction (typically, at the point ofpurchase, a merchant will post a sign and print the notice on areceipt). In all cases, these third party transfers will require you toprovide the third party with your account number and credit unioninformation. This information can be found on your check or draft aswell as on a deposit or withdrawal slip. Thus, you should only provideyour credit union and account information (whether over the phone,the Internet, or via some other method) to trusted third parties whomyou have authorized to initiate these electronic fund transfers.Examples of these transfers include, but are not limited to:

• Preauthorized credits. You may make arrangements forcertain direct deposits to be accepted into your checking orsavings account(s).

• Preauthorized payments. You may make arrangements to paycertain recurring bills from your checking account(s).

• Electronic check or draft conversion. You may authorize amerchant or other payee to make a one-time electronicpayment from your checking or share draft account usinginformation from your check or draft to pay for purchases orpay bills.

• Electronic returned check or draft charge. You mayauthorize a merchant or other payee to initiate an electronicfunds transfer to collect a charge in the event a check or draftis returned for insufficient funds.

Telephone TellerSM Transfers - types of transfers - You may accessyour account by telephone 24 hours, 7 days a week at 1-877-GOLDEN1 (1-877-465-3361), Option 2 using your personal identificationnumber, a touch-tone phone and your account number(s), to:

• transfer funds from checking to checking

• transfer funds from checking to savings

• transfer funds from savings to checking

• transfer funds from savings to savings

• transfer funds from line of credit to checking

• transfer funds from line of credit to savings

• make payments from checking to loan accounts with us

• make payments from savings to loan accounts with us

• get information about:

200846053-010.qxp_200846053-010 10/26/17 11:33 AM Page 26

27

- the account balance of checking accounts

- the last five deposits to checking accounts

- the last five withdrawals from checking accounts

- the account balance of savings accounts

- the last five deposits to savings accounts

- the last five withdrawals from savings accounts

ATM Transfers - types of transfers and dollar limitations - You mayaccess your account(s) by ATM using your ATM card and personalidentification number (PIN) or Visa® Debit Card and personalidentification number (PIN), to:

• make deposits to checking account(s)

• make deposits to savings account(s)

• get cash withdrawals from checking account(s)

- dollar limitations will be disclosed in writing at cardissuance

• get cash withdrawals from savings account(s)

- dollar limitations will be disclosed in writing at cardissuance

• transfer funds from savings to checking account(s)

• transfer funds from checking to savings account(s)

• transfer funds from line of credit to checking account(s)

• transfer funds from line of credit to savings account(s)

• make payments from checking account(s) to consumer loanaccounts with us, except payments to credit cards

• get information about:

- the account balance of your checking account(s)

- the account balance of your savings accounts

Some of these services may not be available at all terminals.

Types of ATM Card Point-of-Sale Transactions - You may accessyour checking account(s) to purchase goods (in person), pay forservices (in person), get cash from a merchant, if the merchantpermits, or from a participating financial institution, and doanything that a participating merchant will accept.

Point-of-Sale Transactions - dollar limitations - Using your card:

• dollar limitations will be disclosed in writing at card issuance

Types of Visa® Debit Card Point-of-Sale Transactions - You mayaccess your checking account(s) to purchase goods (in person,

200846053-010.qxp_200846053-010 10/26/17 11:33 AM Page 27

28

online, or by phone), pay for services (in person, online, or byphone), get cash from a merchant, if the merchant permits, or froma participating financial institution, and do anything that aparticipating merchant will accept.

Point-of-Sale Transactions - dollar limitations - Using your card:

• dollar limitations will be disclosed in writing at card issuance

Visa®/Mastercard Foreign Transaction Fee

Transactions that you incur in foreign currencies will be posted toyour account in U.S. dollars. Foreign transactions are normallyconverted to U.S. dollars by the network processing the transaction,which may impose a fee for this service. Since conversion may occurafter the date of the transaction, the conversion rate in effect on theprocessing date may differ from the rate in effect on the transactiondate or posting date. You agree that the transaction amount asconverted by the network may be deducted from your account, aswell as any conversion charges which are imposed. You agree toaccept the converted amount in U.S. dollars.

Visa USA charges us a .8% International Service Assessment (ISA)on all international transactions, regardless of whether there is acurrency conversion. If there is a currency conversion, theInternational Service Assessment is 1% of the transaction. In eithercase, we pass this international transaction fee on to you. Thecurrency conversion rate used to determine the transaction amountin U.S. dollars is either (i) a rate selected by Visa from the range ofrates available in wholesale currency markets for the applicablecentral processing date, which rate may vary from the rate Visa itselfreceives, or (ii) the government-mandated rate in effect for theapplicable central processing date, in each instance in addition tothe VISA ISA fee.

Any time you complete a foreign transaction using your ATM or DebitCard through the Mastercard Network, such as through Cirrus® orMaestro®, for a transaction in a foreign country (excludingtransactions initiated in U.S. territories or at U.S. military bases inforeign countries), you will be assessed an Issuer Cross-borderAssessment fee (“ICA”). In addition, you will be assessed a CurrencyConversion Assessment fee (“CCA”) if the merchant settles in acurrency other than U.S. dollars. Therefore, if you perform atransaction outside of the U.S. and the transaction is in a foreigncurrency, you will be assessed both the ICA and the CCA fees.However, if the transaction is in U.S. dollars, then you will beassessed only the ICA fee. Currently, the ICA fee is 0.90% (90 basispoints) and the CCA fee is 0.20% (20 basis points). These fees areassessed by Mastercard to Golden 1 and passed on to members. Thecurrency conversion rate used to determine the transaction amountin U.S. dollars is either (i) a rate selected by Mastercard from therange of rates available in wholesale currency markets for theapplicable central processing date, which rate may vary from the

200846053-010.qxp_200846053-010 10/26/17 11:33 AM Page 28

29

rate Mastercard itself receives, or (ii) the government-mandated ratein effect for the applicable central processing date, in each instancein addition to the CCA fee.

Advisory Against Illegal Use. You agree not to use your card(s) forillegal gambling or other illegal purpose. Display of a payment cardlogo by, for example, an online merchant does not necessarily meanthat transactions are lawful in all jurisdictions in which thecardholder may be located.

In accordance with the requirements of the Unlawful InternetGambling Enforcement Act of 2006 and Regulation GG, thisnotification is to inform you that restricted transactions areprohibited from being processed through your account orrelationship with our institution. Restricted transactions aretransactions in which a person accepts credit, funds, instrumentsor other proceeds from another person in connection with unlawfulInternet gambling.

Please see your cardholder agreement for additional informationrelating to the use of your ATM Card and Visa® Debit Card.

Non-Visa Debit Transaction Processing. We have enabled non-Visadebit transaction processing. This means you may use your Debit Cardon a PIN-Debit Network* (a non-Visa network) without using a PIN.

The non-Visa debit network(s) for which such transactions areenabled are: Accel™ Network (© 2013 Fiserv, Inc. or its affiliates.Accel and the Accel logo are trademarks of Fiserv, Inc.).

Examples of the types of actions that you may be required to maketo initiate a Visa transaction on your ATM/Debit Card include signinga receipt, providing a card number over the phone or via theInternet, or swiping the card through a point-of-sale terminal.

Examples of the types of actions you may be required to make toinitiate a transaction on a PIN-Debit Network include initiating apayment directly with the biller (possibly via telephone, Internet, orkiosk locations), responding to a logo displayed at a payment siteand choosing to direct payment through that network, and havingyour identity verified using known information derived from anexisting relationship with you instead of through use of a PIN.

Examples of the types of actions you may be required to make toinitiate a transaction on the Accel Network include initiating apayment directly with the biller, possibly via telephone, Internet, orkiosk locations. Accel Network billers are required to display theAccel logo. Accel Network billers must also allow you to choose howyour payment is directed. Thus, you could see the Accel logo andchoose to direct your payment through the Accel Network. Inaddition, Accel Bill Payments are not authenticated with a PIN;instead the biller authenticates your identity using knowninformation derived from an existing relationship with you.

The provisions of your agreement with us relating only to Visatransactions are not applicable to non-Visa transactions. For

200846053-010.qxp_200846053-010 10/26/17 11:33 AM Page 29

30

example, the additional limits on liability (sometimes referred to asVisa's zero-liability program) and the streamlined error resolutionprocedures offered on Visa debit card transactions are notapplicable to transactions processed on a PIN-Debit Network.

*Visa Rules generally define PIN-Debit Network as a non-Visa debitnetwork that typically authenticates transactions by use of apersonal identification number (PIN) but that is not generally knownfor having a card program.