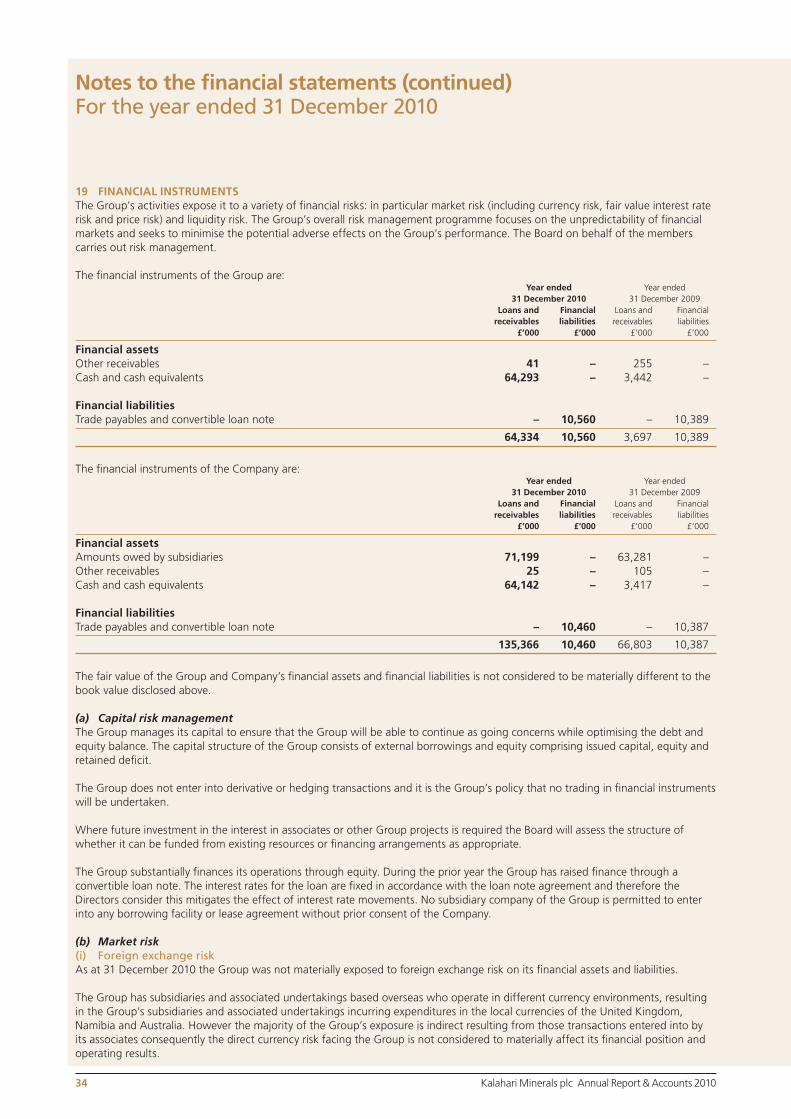

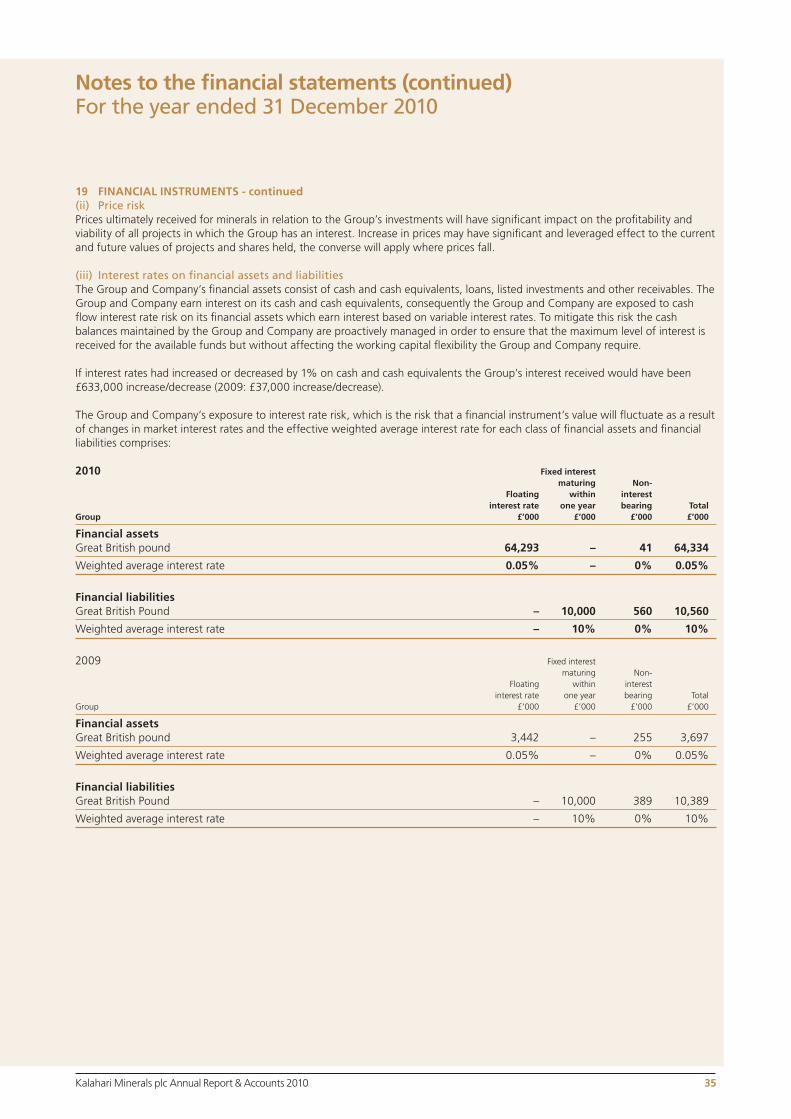

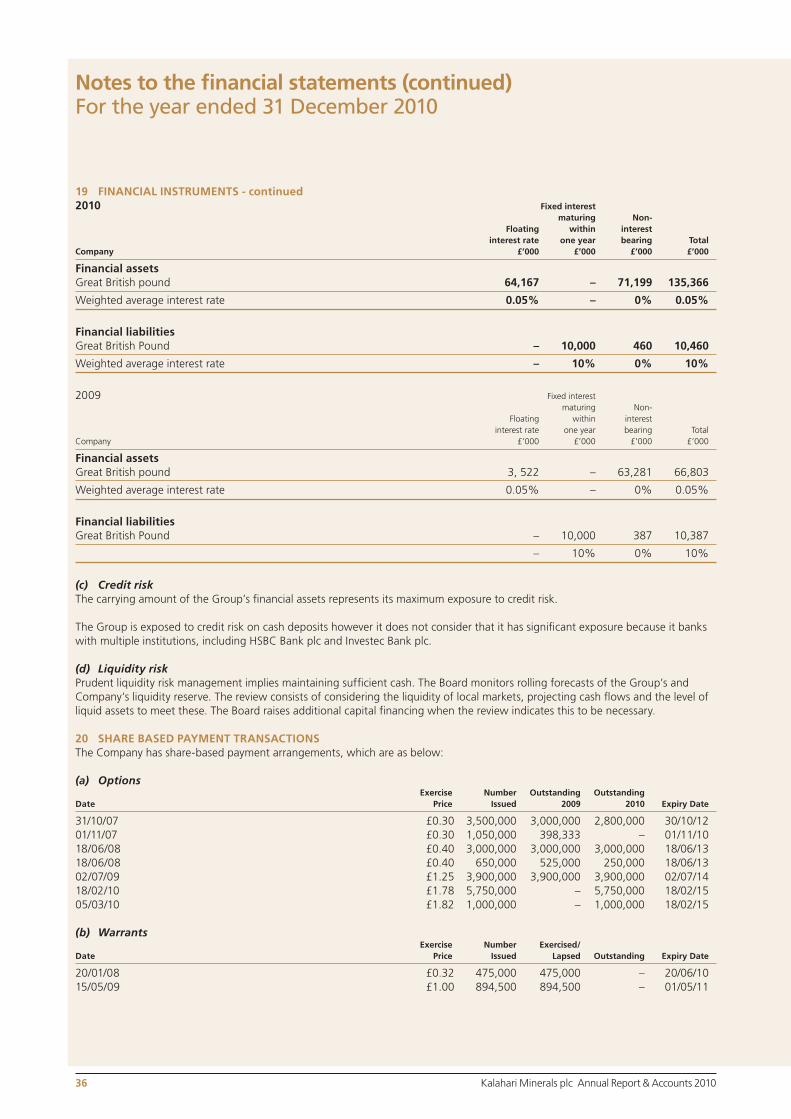

Embed Size (px)

Citation preview

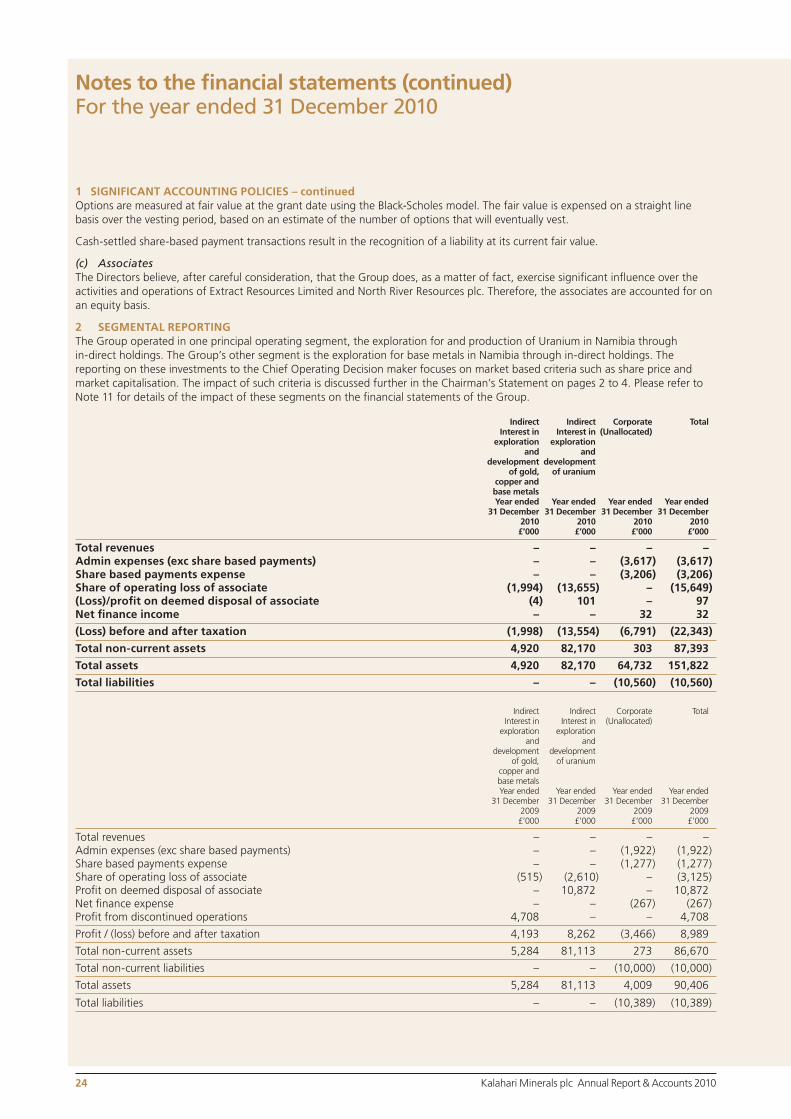

Discovering and DevelopingNamibia’s Potential

Annual Report and FinancialStatements for the year ended31 December 2010

Our Performance01 Highlights02 Chairman’s Statement06 Directors, Officers and Advisers07 Report of the Directors11 Report of the Independent Auditors12 Consolidated Statement of Comprehensive Income13 Consolidated Statement of Financial Position14 Company Statement of Financial Position15 Consolidated Statement of Changes in Equity16 Company Statement of Changes in Equity17 Consolidated Statement of Cash Flows18 Company Statement of Cash Flows19 Notes to the Financial Statements

Mark Hohnen, Executive Chairman

“Kalahari Minerals is an AIM and NSX listed resource company with uranium, gold and base metal interests in Namibia. Its key value driver is its significant stake in Extract Resources Limited, owners of the world class Husab Uranium Project. Husab is moving into its production phase ahead of establishing one of the largest uranium mines globally.”

Welcome toKalahariMinerals plc

Kalahari Minerals plc Annual Report & Accounts 2010 1

Overview Financial Statements

HighlightsChairman’s StatementFinancial StatementsCompany Information

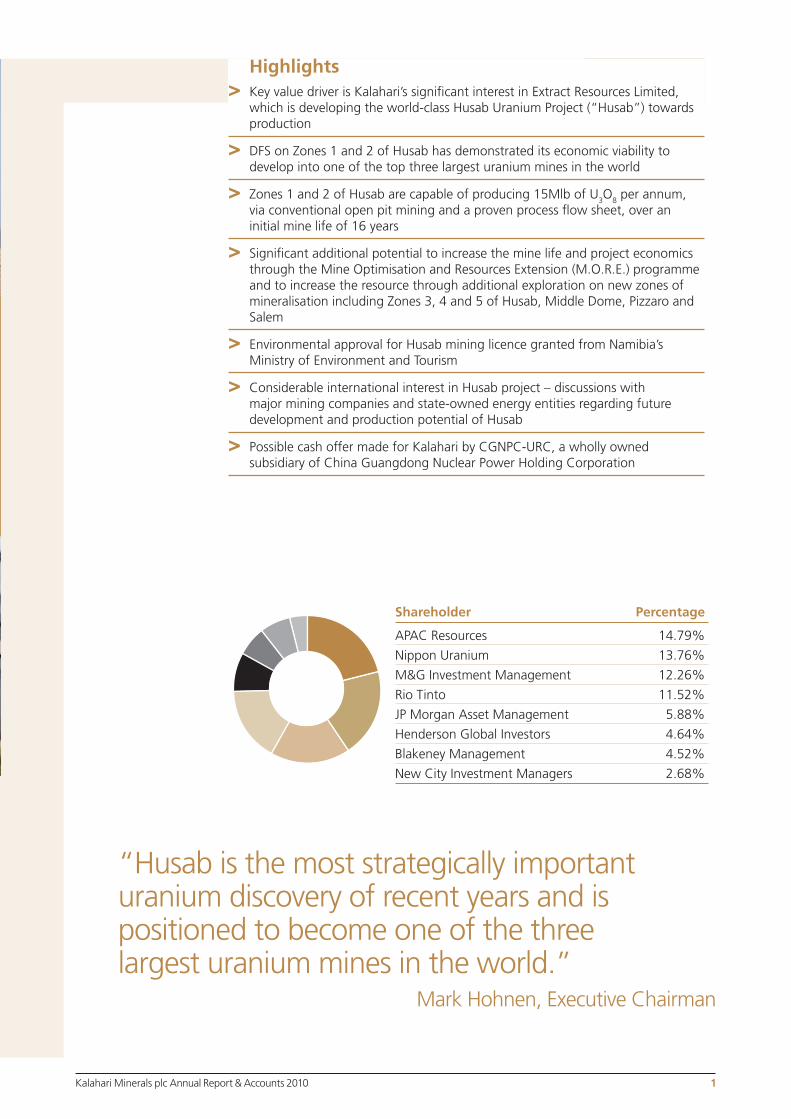

Highlights> Key value driver is Kalahari’s significant interest in Extract Resources Limited,

which is developing the world-class Husab Uranium Project (“Husab”) towards production

>DFS on Zones 1 and 2 of Husab has demonstrated its economic viability to develop into one of the top three largest uranium mines in the world

>Zones 1 and 2 of Husab are capable of producing 15Mlb of U3O8 per annum, via conventional open pit mining and a proven process flow sheet, over an initial mine life of 16 years

>Significant additional potential to increase the mine life and project economics through the Mine Optimisation and Resources Extension (M.O.R.E.) programme and to increase the resource through additional exploration on new zones of mineralisation including Zones 3, 4 and 5 of Husab, Middle Dome, Pizzaro and Salem

>Environmental approval for Husab mining licence granted from Namibia’s Ministry of Environment and Tourism

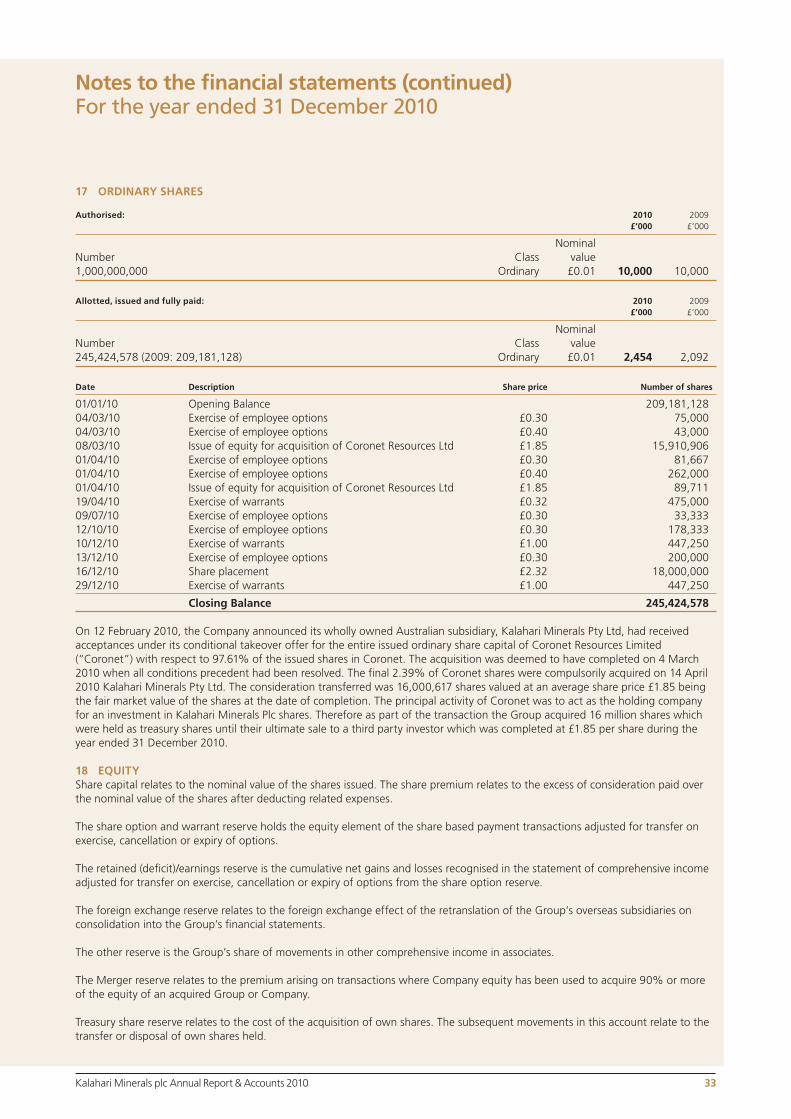

>Considerable international interest in Husab project – discussions with major mining companies and state-owned energy entities regarding future development and production potential of Husab

>Possible cash offer made for Kalahari by CGNPC-URC, a wholly owned subsidiary of China Guangdong Nuclear Power Holding Corporation

Shareholder Percentage

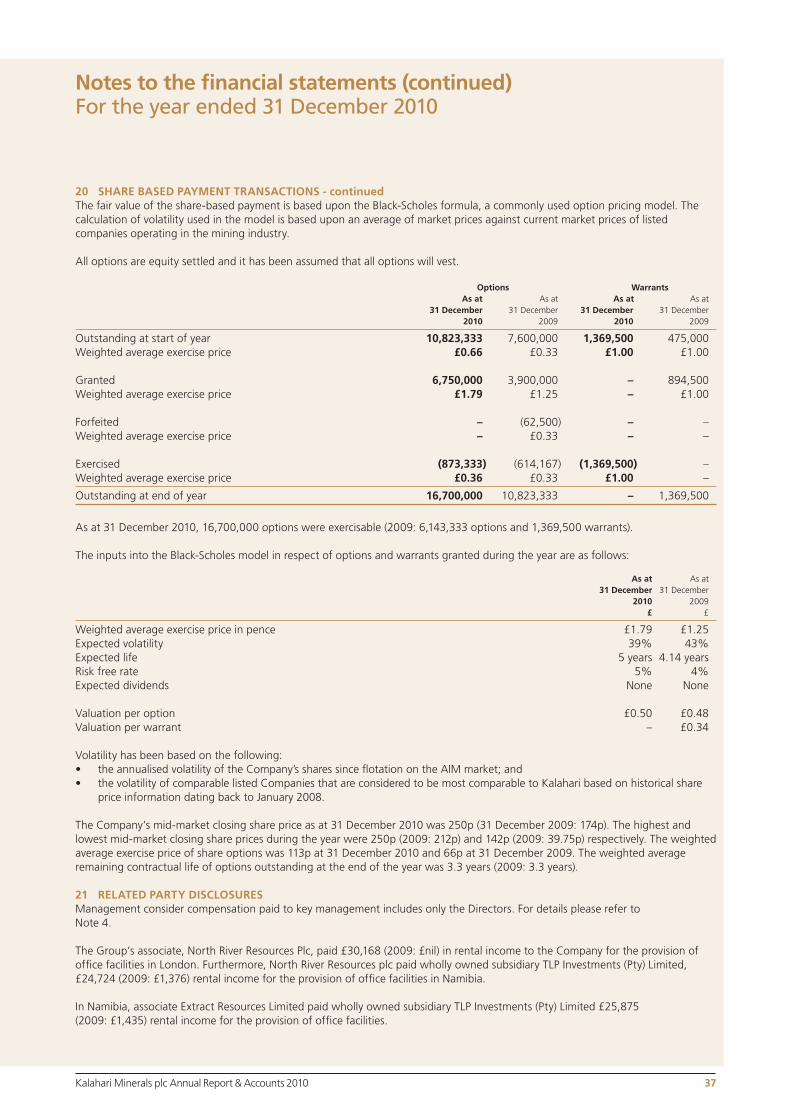

APAC Resources 14.79%

Nippon Uranium 13.76%

M&G Investment Management 12.26%

Rio Tinto 11.52%

JP Morgan Asset Management 5.88%

Henderson Global Investors 4.64%

Blakeney Management 4.52%

New City Investment Managers 2.68%

“Husab is the most strategically important uranium discovery of recent years and is positioned to become one of the three largest uranium mines in the world.”

Mark Hohnen, Executive Chairman

Kalahari Minerals plc Annual Report & Accounts 2010 1

Kalahari Minerals plc Annual Report & Accounts 20102

HighlightsChairman’s StatementFinancial StatementsCompany Information

Chairman’s Statement

“This has been a period of accelerated development and growth for Kalahari”

This has been a period of accelerated development and growth for Kalahari, as Extract Resources Limited (“Extract”), in which we have a 42.79% interest, approaches its production phase at the world-class Husab Uranium Project in Namibia (“Husab”). The rapid development of this strategic uranium project towards production has inevitably generated significant international interest, and we have held discussions with various multi-national mining and energy majors including Rio Tinto and Russian uranium miner AtomRedMetZoloto (“ARMZ”), in addition to government-owned energy entities and our strategic shareholder ITOCHU Corporation. The objective of these discussions has been to ensure that the value of the Husab project is maximised for the benefit of all stakeholders. This discussion process recently resulted in the announcement of a possible bid for Kalahari by CGNPC Uranium Resources Co., Ltd (“CGNPC-URC”), a state-owned enterprise in the People’s Republic of China.

The recent publication of the Definitive Feasibility Study (“DFS”) on Zones 1 and 2 of Husab further underpinned our confidence that Husab is the most exciting and strategically significant new uranium project globally, with the viability to become one of the top three largest uranium mines in the world. This is obviously a fantastic achievement, particularly when coupled with the fact that the DFS only covers Zones 1 and 2, and does not include the highly prospective new zones of mineralisation including Zones 3, 4 and 5, Pizzaro and Middle Dome. With this in mind, the full scope and potential for Husab to house multiple mining operations over a significantly extended mine life, can be truly appreciated. Husab is located in a politically stable and well established uranium mining region, and is importantly less than 50km from the deep water port at Walvis Bay. The combination of these important criteria, coupled with an increasing resource and reserve inventory, has underlined the Husab project’s status as a globally significant uranium project with considerable strategic value, and the Kalahari board has remained steadfast in its objective of ensuring that its value is maximised for all stakeholders.

In addition, our investment in AIM listed North River Resources plc (“North River”) continues to build value. North River has made a great deal of progress during the period, both in terms of developing its gold, copper and other base metals portfolio of assets in Namibia and securing joint venture agreements to rapidly advance its additional interests.

Husab Uranium ProjectDevelopment continues apace at the Husab Uranium Project, with Extract achieving several key milestones during the period. One important achievement was the release of an upgraded resource, in August 2010, which defined Husab as the fifth largest uranium deposit globally. The upgraded resource statement included an Indicated Resource of more than a quarter of a billion pounds of U3O8, a ten-fold increase in the Indicated Resource from the previous resource statement, and a 37% increase in the total Resource for Husab to 367Mlb U3O8. Importantly, this resource statement also included a Maiden Inferred Resource from Zones 3 and 4, with drilling continuing on site to extend and upgrade this 110Mlb Inferred Resource into higher confidence categories.

The most significant achievement in Extract’s development schedule was the publication of the DFS on Zones 1 and 2 of Husab post period end. The results of the DFS, which outlined the base case path to production, demonstrated the viability of transforming Zone 1 and 2 of Husab into one of the three largest uranium mines in the world, producing 15Mlb of U3O8 per annum, via conventional open pit mining and a proven process flow sheet, over an initial mine life of 16 years. This was a tremendous achievement for Extract, however it must be emphasised that this remains a base case, and Extract has initiated a Mine Optimisation and Resources Extension programme (“M.O.R.E.”) to increase the mine life and to investigate opportunities to add significant additional value through optimisation of the mine plan and process modifications, and to enhance the project’s expected mine life, operating and financial performance.

The M.O.R.E. process is in addition to continued exploratory work which continues on other zones within the project area, and this has delineated significant additional targets for follow-up work. Outstanding assay results released in September 2010 confirmed the existence of the emerging Zone 5, which remains open along strike and down dip, with intersections including 29 metres, grading 1,653ppm U3O8 from 279 metres. This intersection ranks within the top 2% for metal content within the current Husab database, confirming Zone 5 as a high priority exploration target. Further assay results from the wider Husab project area beyond the Rössing South Anticline, have also yielded further exceptional exploration zones, including the Middle Dome and Pizzaro targets. Importantly, the best intersection returned, of 20m @ 846 ppm U3O8 from the Middle Dome target, is the second highest grade-width intersection in the entire non-resource Husab exploration drilling database, underpinning the fantastic prospectivity of the entire Husab area and its ability to host multiple world class uranium deposits.

Kalahari Minerals plc Annual Report & Accounts 2010 3

Overview Financial Statements

HighlightsChairman’s StatementFinancial StatementsCompany Information

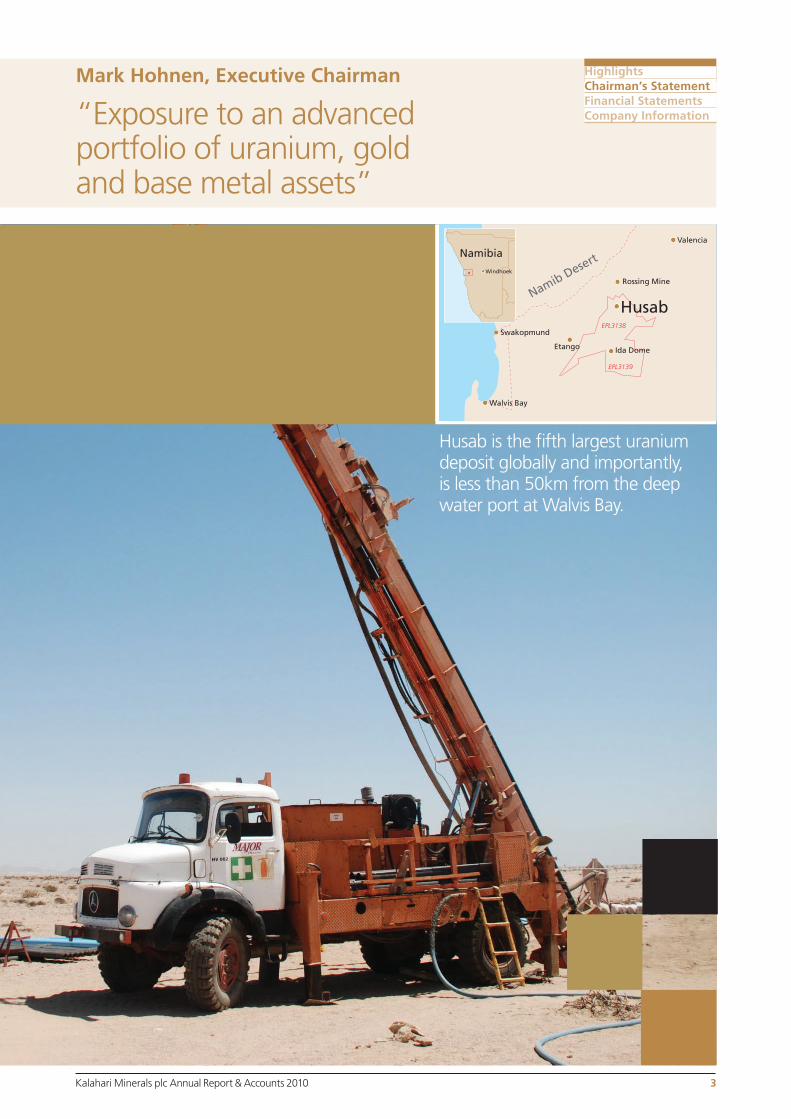

Mark Hohnen, Executive Chairman

“Exposure to an advanced portfolio of uranium, gold and base metal assets”

Walvis Bay

Swakopmund

Etango Ida Dome

Namib Desert

Rossing Mine

Valencia

HusabEPL3138

EPL3139

Namibia

Windhoek

Husab is the fifth largest uranium deposit globally and importantly, is less than 50km from the deep water port at Walvis Bay.

Kalahari Minerals plc Annual Report & Accounts 20104

HighlightsChairman’s StatementFinancial StatementsCompany Information

In line with Extract’s ambitious development schedule, environmental approval for the Husab mining licence was granted from Namibia’s Ministry of Environment and Tourism in January 2011. Obtaining this environmental approval was another significant step towards achieving production at Husab, and emphasises both the project’s environmental credentials and the support for its development from the Namibian Government. A two year extension for EPL 3138, which covers Husab, has also been granted and which enables Extract to continue its rapid exploration programme, focused on the newly delineated targets of Zones 3, 4 and 5 of Husab, Middle Dome, Salem and Pizzaro, in addition to further in-fill drilling at Zones 1 and 2.

North River Resources North River has had a particularly active year in terms of operations and corporate activity; development work is continuing on its copper, gold and base metals projects in Namibia, in addition to joint venture agreements with Baobab Resources plc and Jacana Resources Limited being signed in relation to its Mozambican assets. North River has also ventured into the nuclear fuels arena through its joint venture with Extract, and we look forward to North River announcing results from all of these joint venture relationships in the future.

In April 2011, North River announced a placing which raised £3 million. The funds raised in this placing will be used to accelerate North River’s development programme across its portfolio of assets in Namibia. Kalahari was not able to participate in this placing due to restrictions relating to the 4.2 announcement regarding CGNPC-URC’s possible offer for the Company.

North River remains focussed on the evaluation of potential acquisitions, but has stated that it will only enter into transactions which are clearly going to be value enhancing for its shareholders. It has assessed a great many potential acquisitions but, to date, none have made a compelling investment case. The board of North River will continue this process whilst increasing the level of exploration activity on its existing exploration properties.

Financial Overview• Increase of interest in associate Extract of 0.71% to

41.12% (as at 31 December 2009: 40.41%). The market value of this investment at reporting date is £617.7m (reporting date share price value £6.17 : A$9.40)

• Slight annual decrease of interest in associate North River of 0.16% to 44.73% (as at 31 December 2009: 44.89%). The market value of the investment in North River at reporting date is £10.5m (reporting date share price value £6.17)

• During the year the Company successfully raised net capital proceeds of £42.3m, which included a raising on 16 December 2011 of £41.1m (after expenses) by way of a placing of 18 million new ordinary shares of 1 pence each in the capital of the Company, at a price of 232 pence per placing share

• Since the year end, the Company has increased its interest in associate Extract from 41.12% to 42.79% (as at 31 March 2011) and its interest in North River was diluted to 38.03% following a

fundraising which Kalahari was unable to participate in due to its 4.2 announcement regarding CGNPC-URC’s possible offer for Kalahari.

Corporate OverviewDue to the large resource size, good grades and strategic location of Husab, we, as Extract’s largest shareholder, have received extensive interest from a number of international parties seeking to participate in the project’s development.

Our strategic shareholders ITOCHU Corporation, a major Japanese trading house with a long history in the uranium market, as well as operating in Namibia, has continued to have a positive and contributing role on our shareholder register. In addition, an expression of interest by ITOCHU in taking a more directional role in Husab’s development has been evaluated. In addition, due to the close proximity and obvious logistical synergies with Rio Tinto’s 69% owned Rössing Mine, careful consideration has been given to a potential partnership agreement with Rio Tinto and an announcement was made on 21 February 2011 outlining the rationale behind this.

However, as shareholders will be aware, on 7 March 2011, the Company announced a possible cash offer for Kalahari from CGNPC-URC (“the Possible Offer”), a wholly owned subsidiary of China Guangdong Nuclear Power Holding Corporation, a state owned nuclear fuel producer in the People’s Republic of China. The Possible Offer comprises 290 pence in cash for each ordinary share in Kalahari, valuing Kalahari’s fully diluted share capital, including shares attributable to options and convertible loan notes, at approximately £756 million. The Kalahari Board has considered the Possible Offer carefully, in the context of other opportunities available to the Company, and it believes this represents attractive value for shareholders. If made, the Possible Offer would enable Kalahari Shareholders to crystallise this value now, in cash.

The Possible Offer is subject to the satisfaction of certain pre-conditions, and the Company will keep shareholders updated as to the progress of this process. For more details on the Possible Offer, please refer to the announcement made on 7 March 2011, which is available on the Company’s website at www.kalahari-minerals.com.

OutlookThe overarching objective of the Kalahari Board remains in maximising the value of our interest in Extract and the Husab project, and the Company will update shareholders when appropriate on any developments in this regard.

I would like to take this opportunity to thank our investors for their continued support for Kalahari during this exciting time in the Company’s development and to my fellow Directors on the Board.

Mark HohnenExecutive Chairman12 April 2011

Chairman’s Statement continued

Kalahari Minerals plc Annual Report & Accounts 2010 5

Overview Financial Statements

HighlightsChairman’s StatementFinancial StatementsCompany Information

Kalahari Minerals plc Annual Report & Accounts 20106

Directors Mark Hohnen Executive Chairman Mr. Hohnen has been involved in the mineral business since the late 1970s. He has had extensive international business experience in a wide range of industries including mining and exploration, property, investment, software and agriculture. He has held a number of directorships in both public and private companies and was founding Chairman of Cape Mentelle and Cloudy Bay wines, as well as the oil and coal company Anglo Pacific Resources Plc.

Neil MacLachlan Executive Director Mr. MacLachlan has over 30 years experience in investment banking in Europe, South East Asia and Australia through his positions with the investment banking division of HSBC, as Deputy Chairman and CEO of Wardly Australia Ltd and as head of investment banking at James Capel and Co Ltd. He also has extensive mining industry experience, having held the position of Executive Vice President, Asia for Barrick Gold Corporation and directorship positions at Golden Prospect Plc, Ambrian Partners Ltd. Additionally, he was a founding director of Markham Associates, a corporate consultancy service focussed on smaller companies in the resource sector.

Glyn Tonge Non-executive Director Professor Tonge has international business, finance and management experience across a broad range of industries and for a number of years was a director of Baring Brothers & Co Ltd where he worked in corporate finance. He was until recently Pro Chancellor at Southampton Solent University. He is also a Fellow of the Royal Institution in London, a Fellow of the Society of Biology and a Fellow of the Royal Society of Medicine and also serves as a Non-executive Director of AIM listed North River Resources plc.

David de Jongh Weill Non-executive Director Mr. Weill started his professional career with Salomon Brothers in derivative products sales and trading before moving to develop international proprietary trading with Greenwich Capital Markets six years later. Focussing on private equity investment, predominantly in natural resource and media and technology companies, Mr Weill has considerable experience in proprietary trading in international financial markets, investment management, corporate finance, and corporate governance. Mr Weill is a founder and partner of Chiliogon Partners LLP.

Richard Lockwood Non-executive Director Mr. Lockwood has 50 years of experience in institutional investment, primarily with Hoare Govett in London and Australia and AMVESCAP, London. He is currently a Senior Fund Manager for City Natural Resources High Yield Trust, New City High Yield Fund, Geiger Counter Limited and Golden Prospect Precious Metals.

Sumihiro Kamino Non-executive Director Mr. Kamino’s position on the Board is designed to ensure that the strategic relationship between Kalahari and ITOCHU, Kalahari’s strategic investor with a circa 15% interest, is maximised to the benefit of all stakeholders. ITOCHU is a major Japanese trading house with a strong relationship with the Government of Japan.

Secretaries & Officers Duncan Craib Chief Financial Officer and Joint Company Secretary Mr. Craib qualified as a Chartered Accountant in Perth, Western Australia, and has subsequently held senior financial and management roles in both publically listed and private enterprises in Australia, Europe and Africa. He has extensive international business experience which is primarily focussed on mining and exploration activities. Mr. Craib became the full time CFO on 1 February 2011, having previously contracted his services while also serving as CFO to Universal Coal plc, as well as advising other listed entities.

Janis Sawyer Joint Company Secretary Ms. Sawyer qualified as a Chartered Account in England and is now a Fellow member of the Institute of Chartered Accountants in Australia, a Fellow member of the Australian Institute of Company Directors and an Associate Fellow of the Australian Institute of Management WA Ltd. Ms. Sawyer has acted as Company Secretary for numerous listed and unlisted Australian and UK based companies, operating in diverse industries, for in excess of 25 years.

Sadike Nepela General Manager Mr. Nepela is a graduate of the University of Witwatersrand, Johannesburg and has also studied at the University of Connecticut, West Hartford, USA. For a number of years he has served as an assistant to the Minister in the Namibian Ministry of Mines and Energy and most recently he has been the General Manager for Westport Resources, a subsidiary of Forsys Metals Corp. He is also a Fellow of the International Centre for Research and Training in Major Projects Management, Montreal, Canada.

Advisers Nominated Adviser Strand Hanson Limited 26 Mount Row London W1K 3SQ

Joint Broker Ambrian Partners Limited Old Change House 128 Queen Victoria Street London EC4V 4BJ

Joint Broker Mirabaud Securities LLP 21 St James’s Square London SW1Y 4JP

Financial AdviserAzure CapitalLevel 34Exchange Plaza2 The EsplanadePerth WA 6000Australia

Legal AdviserLawrence Graham LLP4 More London Riverside London SE1 2AE

Auditors BDO LLP 55 Baker Street London W1V 7EU

Registrars Computershare

Financial Public Relations St Brides Media and Finance Ltd Chaucer House 38 Bow Lane London EC4M 9AY

Registered Office Kalahari Minerals plc 1b, 38 Jermyn Street London SW1Y 6DN

Country of Incorporation England and Wales Registered number: 5294388

Directors, Officers and Advisers

Kalahari Minerals plc Annual Report & Accounts 2010 7

The Directors present their report with the financial statements of the Company and its subsidiaries (together, the “Group”) for the year ended 31 December 2010.

REVIEW OF THE BUSINESSThe results for the year and financial position of the Group and Company are as shown in the annexed financial statements.

The principal activity of the Group and Company in the year under review continued to be that of minerals exploration and development, as well as holding strategic interests in a number of other significant base metal assets.

The function of the business review is to provide a balanced and comprehensive review of the Group’s and Company’s performance and development during the year and its position at the year end. The review also covers the principal risks and uncertainties faced by the Group. A detailed review of the business and its operations in the year is given in the Chairman’s Statement on pages 2 to 4.

Principal risks and uncertaintiesThe management of the business and the execution of the Group’s strategy are subject to a number of risks.

Risks are formally reviewed by the Kalahari board (the “Board”) and appropriate processes put in place to monitor and mitigate them. If more than one event occurs, it is possible that the overall effect of such events would compound the possible adverse effects on the Group.

Business risks are discussed at Board meetings and, if considered material, further investigated to lower or remove the perceived risk. The key business risks affecting the Group are set out below:

Liquidity riskThe Group manages its cash and borrowing requirements centrally to maximise interest and investment income and minimise interest expense, whilst ensuring that the Group has sufficient liquid resources to meet the operating needs of its business.

Interest rate riskThe Group has interest bearing borrowings in the form of a Convertible Loan Note, which incurs a fixed interest charge of 10% per annum and is therefore only exposed to fair value interest rate risk on its fixed rate deposits. Strategic riskSignificant and increasing competition exists for mineral acquisition opportunities throughout the world. As a result of this competition, the Group may be unable to acquire rights to exploit additional attractive mining properties on terms it considers acceptable. Accordingly, there can be no assurance that the Group will acquire any interest in additional operations or strategic investments that would yield reserves or result in commercial mining operations. The Group expects to undertake sufficient due diligence where warranted to help ensure opportunities are subjected to proper evaluation.

Report of the directorsFor the year ended 31 December 2010

Commercial riskThe mining industry is competitive and there is no assurance that, even if commercial quantities of minerals are discovered by the Group or its strategic partners, a profitable market will exist for the sale of such minerals. There can be no assurance that the quality of the minerals of its strategic partners can be mined at a profit. Factors beyond the control of the Group and its strategic partners may affect the marketability of any minerals discovered. Mineral prices are subject to volatile price changes from a variety of factors including international economic and political trends, expectations of inflation, global and regional demand, currency exchange fluctuations, interest rates and global or regional consumption patterns, speculative activities and increased production due to improved mining and production methods. Ultimately, the Group and its strategic partners expect that all projects will be the subject of sufficient feasibility analysis to ensure a reasonable level of confidence appropriate to the circumstances under consideration.

Operational riskMining operations are subject to hazards normally encountered in exploration, development and production. Although it is intended to take adequate precautions to minimise risk, there is a possibility of a material adverse impact on the Group’s strategic partners’ operations and financial results. The Group will monitor its strategic partners’ development and maintenance of policies appropriate to the stage of development of its various projects and interests.

Staffing and Key Personnel RisksRecruiting and retaining qualified personnel is critical to the Group’s success. The number of persons skilled in the acquisition, exploration and development of mining properties is limited and competition for such persons is intense. While the Group has good relations with its employees, these relations may be impacted by changes in the scheme of labour relations which may be introduced by the relevant governmental authorities. Adverse changes in such legislation may have a material adverse effect on the Group’s business, results of operations and financial condition. Staff are encouraged to discuss with Management matters of interest to the employees and subjects affecting day-to-day operations of the Group.

Speculative Nature of Mineral Exploration and DevelopmentDevelopment of the Group’s strategic partners’ mineral exploration properties is contingent upon obtaining satisfactory exploration results. Mineral exploration and development involves substantial expenses and a high degree of risk, which even a combination of experience, knowledge and careful evaluation may not be able to adequately mitigate. The degree of risk increases substantially when properties are in the exploration phase as opposed to the development phase.

The discovery of mineral deposits is dependent upon a number of factors including the technical skill of the exploration personnel involved. The commercial viability of a mineral deposit, once discovered, is also dependent upon a number of factors, including the size, grade and proximity to infrastructure, metal prices and government regulations, including regulations relating to royalties, allowable production, importing and exporting of minerals, and environmental protection. In addition, several years can elapse from the initial phase of drilling until commercial operations are commenced.

Kalahari Minerals plc Annual Report & Accounts 20108

Political StabilityThe Group’s strategic partners’ projects in Namibia may be subject to the effect of political changes, war and civil conflict, changes in government policy, lack of law enforcement and labour unrest and the creation of new laws. These changes (which may include new or modified taxes or other government levies as well as other legislation) may impact on the profitability and viability of properties.

Uninsurable RisksThe Group may become subject to liability for accidents, pollution and other hazards against which it cannot insure or against which it may elect not to insure because of premium costs or for other reasons, such as in amounts, which exceed policy limits.

Security of TenureThe Group will investigate the rights to explore and extract minerals from its strategic partners’ material properties and, to the best of its knowledge, those rights are expected to be in good standing. No assurance can be given, however, that the Group and its strategic partners will be able to secure the grant or the renewal of existing mineral rights and tenures on terms satisfactory to it, or that governments in the jurisdictions in which the Group and its strategic partners operate will not revoke or significantly alter such rights or tenures or that such rights or tenures will not be challenged or impugned by third parties, including local governments or other claimants. Although the Group is not currently aware of any existing title uncertainties with respect to any of its or those of its strategic partners’ material properties, there is no assurance that such uncertainties will not result in future losses or additional expenditures, which could have an adverse impact on the Group’s future cash flows, earnings, results of operations and financial condition.

Government RegulationsThe Group’s activities and those of its strategic partners’ are subject to extensive laws and regulations controlling not only the mining of and exploration for mineral properties, but also the possible effects of such activities upon the environment and upon the interests of indigenous people. Permits from a variety of regulatory authorities are required for many aspects of mine operations and reclamation. Future legislation and regulations could cause additional expense, capital expenditures, restrictions and delays, the extent of which cannot be predicted.

Environmental legislation is evolving in a manner which will require stricter standards and enforcement, increased fines and penalties for non-compliance, more stringent environmental assessments of proposed projects and a heightened degree of responsibility for companies and their officers, directors and employees.

There is no assurance that future changes in environmental regulation, if any, will not adversely affect the Group and its strategic partners’ operations. Environmental and employee health and safety laws and regulations have tended to become more stringent over time. Any changes in such laws or in the environmental conditions at the Group and its strategic partners’ properties could have a material adverse effect on the Group’s financial condition, cash flows or results of operations.

Failure to comply with applicable environmental and health and safety laws can result in injunctions, damages, suspension or revocation of licenses and the imposition of penalties. There can be no assurance that the Group has been or will be at all times in complete compliance with such laws, regulations and permits, or that the costs of complying with current and future environmental and health and safety laws and permits will not adversely affect the Group’s business, results of operations, financial condition or prospects.

Key performance indicatorsThe Board monitors progress on the overall Group strategy and the individual strategic elements by reference to its key performance indicators as follows: 2010 2009 £’000 £’000

Market value of investment in associates at year end Extract Resources Limited 617,658 454,486North River Resources plc 10,533 8,319Operating loss (6,823) (3,199)Net assets 141,262 80,017Cash at year end 64,293 3,442Share price at reporting dates 250p 174p

The increase in net assets is attributable to the share issues in the period, which have been applied to increase the holding in Extract Resources Limited and also increased our year end cash balance. Extract Resources Limited is listed on the Australian Stock Exchange and the Namibian Stock Exchange. North River Resources plc is listed on AIM. The loss for the year was as anticipated by the Directors and is therefore in line with Management’s expectations.

Environmental responsibilityThe Group recognises that the activities of its strategic partners require them to have regard to the potential impact that they may have on the environment. Where exploration works are carried out, care is taken to limit the amount of disturbance and where any such works are required they are carried out as and when required.

The BoardAs at 31 December 2010, the Board was comprised of six Directors, being one Executive Chairman, Mark Hohnen, and five Non-Executive Directors, being Glyn Tonge, Neil MacLachlan, David Weill, Richard Lockwood and Takashi Yasuda. Post year end, Mr. MacLachlan has been appointed as Executive Director of the Company. In addition, Mr. Sumihiro Kamino has been appointed as a Non-executive Director to the Board, replacing Mr. Takashi Yasuda as ITOCHU’s nominated representative. Accordingly, Mr. Yasuda resigned from the Board with immediate effect. The composition of the Board reflects a wealth of minerals exploration and development experience.

The Board ordinarily meets on a quarterly basis and also as and when required, providing effective leadership and overall management of the Group’s affairs through the schedule of matters reserved for its decision. These include the approval of the budget and business plan, major capital or investment expenditure, acquisitions and disposals, risk management

Kalahari Minerals plc Annual Report & Accounts 2010 9

policies and the approval of the financial statements. Formal agendas, papers and reports are sent to the Directors in a timely manner, prior to the Board meetings. The Board delegates certain responsibilities to Board committees, which have terms of reference as listed below.

All Directors have access to the advice of the Company Secretary who is responsible for ensuring that all Board procedures are followed. Any Director may take independent professional advice at the Company’s expense in the furtherance of his duties.

The remuneration committeeAs at 31 December 2010, the remuneration committee comprised of Glyn Tonge (Chairman), Neil MacLachlan and David Weill. The committee is responsible for reviewing the performance of the Directors and for setting the framework and Board policy for the scale and structure of their remuneration taking into account all factors which it shall deem necessary. The remuneration packages applicable to the Board and employees are reviewed annually and terms and conditions documented in formal employment contracts. The remuneration committee will also determine allocations of share options and is responsible for setting up any performance criteria in relation to the exercise of options granted under any share option schemes adopted by the Group.

The audit committeeAs at 31 December 2010, the audit committee comprised of David Weill (Chairman), Neil Maclachlan and Glyn Tonge. The committee monitors the integrity of the Company’s annual and interim financial statements. The Committee also monitors and reviews the effectiveness of the Management and the external auditors on accounting and internal control matters, recommending the appointment of and reviewing the fees of the external auditors.

EmployeesStaff numbers (excluding Directors) remain at 1 (2009: 1) employee.

DividendsNo dividends will be distributed for the year ended 31 December 2010 (2009: £nil).

Policy on payment of creditorsThe Group and Company’s policy is to settle terms of payment with suppliers when agreeing terms of business, to ensure that the suppliers are aware of the terms of payment and to abide by them. The Group and Company settle its trade payables in accordance with this policy. Trade payables of the Group are usually paid upon demand or within 30 days of recognition (2009: upon demand or within 30 days of recognition).

Charitable and political contributionsDuring the year, the Group made no charitable or political contributions (2009: £nil).

Financial instrumentsThe Group’s use of financial instruments is described in Note 19.

Events after the reporting datePlease refer to Note 23 of the financial statements.

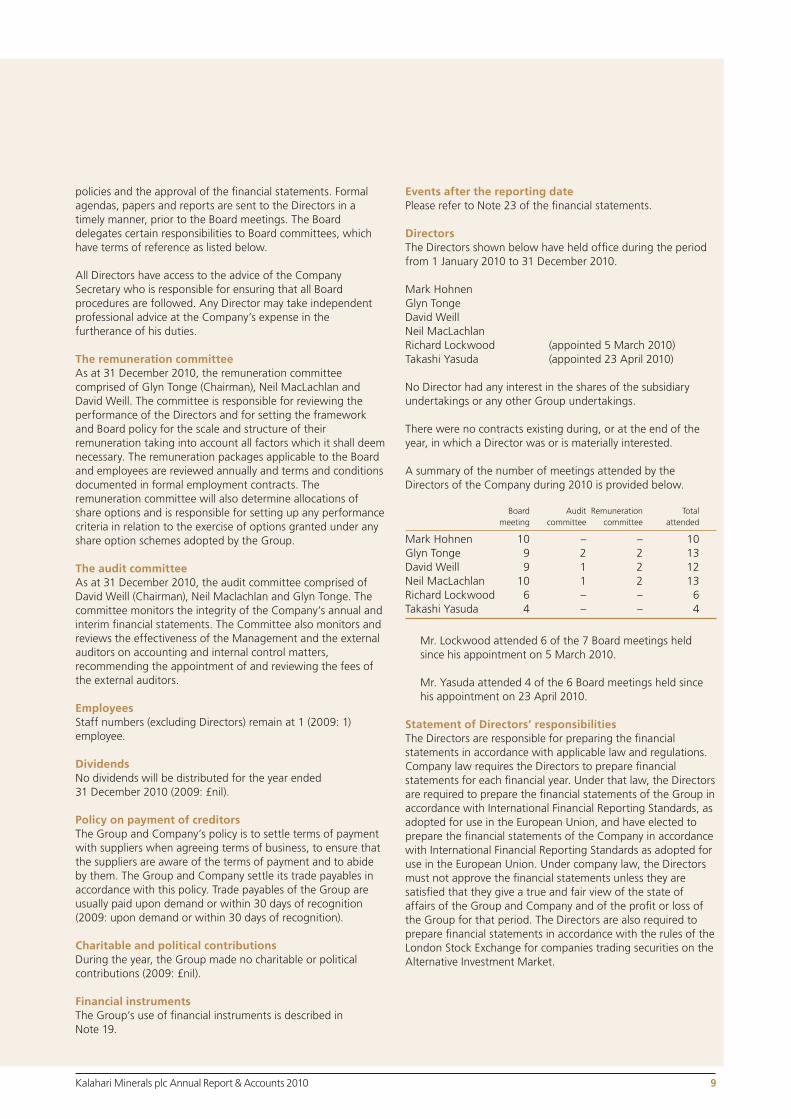

DirectorsThe Directors shown below have held office during the period from 1 January 2010 to 31 December 2010.

Mark HohnenGlyn TongeDavid Weill Neil MacLachlanRichard Lockwood (appointed 5 March 2010)Takashi Yasuda (appointed 23 April 2010)

No Director had any interest in the shares of the subsidiary undertakings or any other Group undertakings.

There were no contracts existing during, or at the end of the year, in which a Director was or is materially interested.

A summary of the number of meetings attended by the Directors of the Company during 2010 is provided below.

Board Audit Remuneration Total meeting committee committee attended

Mark Hohnen 10 – – 10Glyn Tonge 9 2 2 13David Weill 9 1 2 12Neil MacLachlan 10 1 2 13Richard Lockwood 6 – – 6Takashi Yasuda 4 – – 4

Mr. Lockwood attended 6 of the 7 Board meetings held since his appointment on 5 March 2010.

Mr. Yasuda attended 4 of the 6 Board meetings held since his appointment on 23 April 2010.

Statement of Directors’ responsibilitiesThe Directors are responsible for preparing the financial statements in accordance with applicable law and regulations. Company law requires the Directors to prepare financial statements for each financial year. Under that law, the Directors are required to prepare the financial statements of the Group in accordance with International Financial Reporting Standards, as adopted for use in the European Union, and have elected to prepare the financial statements of the Company in accordance with International Financial Reporting Standards as adopted for use in the European Union. Under company law, the Directors must not approve the financial statements unless they are satisfied that they give a true and fair view of the state of affairs of the Group and Company and of the profit or loss of the Group for that period. The Directors are also required to prepare financial statements in accordance with the rules of the London Stock Exchange for companies trading securities on the Alternative Investment Market.

Kalahari Minerals plc Annual Report & Accounts 201010

In preparing these financial statements, the Directors are required to:

• select suitable accounting policies and then apply them consistently;

• make judgements and accounting estimates that are reasonable and prudent;

• state whether they have been prepared in accordance with IFRSs as adopted by the European Union, subject to any material departures disclosed and explained in the financial statements; and

• prepare the financial statements on the going concern basis unless it is inappropriate to presume that the Group and Company will continue in business.

The Directors are responsible for keeping proper accounting records which disclose with reasonable accuracy at any time the financial position of the Group and Company and to enable them to ensure that the financial statements comply with the Companies Act 2006. They are also responsible for safeguarding the assets of the Group and Company and hence for taking reasonable steps for the prevention and detection of fraud and other irregularities.

The Directors are responsible for ensuring the annual report and the financial statements are made available on a website. Financial statements are published on the Company’s website in accordance with legislation in the United Kingdom governing the preparation and dissemination of financial statements, which may vary from legislation in other jurisdictions. The maintenance and integrity of the Company’s website is the responsibility of the Directors. The Directors’ responsibility also extends to the ongoing integrity of the financial statements contained therein.

Directors’ indemnitySubject to the conditions set out in the Companies Act 2006, the Company has arranged appropriate Directors’ and Officers’ insurance to indemnify the Directors against liability in respect of proceedings brought by third parties. Such provisions remain in force at the date of this report.

AuditorsBDO LLP have expressed their willingness to continue in office and a resolution to reappoint them will be proposed at the Annual General Meeting.

Directors’ statement as to disclosure of information to auditorsThe Directors who were members of the Board at the time of approving the Directors’ report are listed on page 6. Having made enquiries of fellow Directors, each of these Directors confirms that:

• to the best of each Director’s knowledge and belief, there is no information relevant to the preparation of their report of which the Company’s auditors are unaware; and

• each Director has taken all the steps a Director might reasonably be expected to take to make themselves aware of any information needed by the Group’s auditors for the purpose of their audit.

Annual general meetingThe notice of the Annual General Meeting is attached at the end of the annual report. Full details of the business to be considered at the meeting can be found in the notice.

ON BEHALF OF THE BOARD:

Mark Hohnen – ChairmanDate: 12 April 2011

Kalahari Minerals plc Annual Report & Accounts 2010 11

We have audited the financial statements of Kalahari Minerals plc for the year ended 31 December 2010, which comprise the Consolidated Statement of Comprehensive Income, the Consolidated and Company Statements of Financial Position, the Consolidated and Company Statements of Changes in Equity, the Consolidated and Company Statements of Cash Flows and the related notes. The financial reporting framework that has been applied in their preparation is applicable law and International Financial Reporting Standards (IFRS), as adopted by the European Union, and, as regards the parent company financial statements, as applied in accordance with the provisions of the Companies Act 2006.

This report is made solely to the Company’s shareholders, as a body, in accordance with Chapter 3 of Part 16 of the Companies Act 2006. Our audit work has been undertaken so that we might state to the Company’s shareholders those matters we are required to state to them in an auditors’ report and for no other purpose. To the fullest extent permitted by law, we do not accept or assume responsibility to anyone other than the Company and the Company’s members as a body, for our audit work, for this report, or for the opinions we have formed.

Respective responsibilities of Directors and auditorsAs explained more fully in the statement of Directors’ responsibilities, the Directors are responsible for the preparation of the financial statements and for being satisfied that they give a true and fair view. Our responsibility is to audit and express an opinion on the financial statements in accordance with applicable law and International Standards on Auditing (UK and Ireland). Those standards require us to comply with the Auditing Practices Board’s (APB’s) Ethical Standards for Auditors.

Scope of the audit of the financial statementsA description of the scope of an audit of financial statements is provided on the APB’s website at www.frc.org.uk/apb/scope/private.cfm.

Opinion on financial statementsIn our opinion:

• the financial statements give a true and fair view of the state of the Group’s and the Parent Company’s affairs as at 31 December 2010 and of the Group’s loss for the year then ended;

• the Group financial statements have been properly prepared in accordance with IFRSs as adopted by the European Union;• the Parent Company’s financial statements have been properly prepared in accordance with IFRSs as adopted by the European

Union and as applied in accordance with the provisions of the Companies Act 2006; and • the financial statements have been prepared in accordance with the requirements of the Companies Act 2006.

Opinion on other matters prescribed by the Companies Act 2006In our opinion the information given in the Directors’ report for the financial year for which the financial statements are prepared is consistent with the financial statements.

Matters on which we are required to report by exceptionWe have nothing to report in respect of the following matters where the Companies Act 2006 requires us to report to you if, in our opinion:

• adequate accounting records have not been kept by the Parent Company, or returns adequate for our audit have not been received from branches not visited by us; or

• the Parent Company financial statements are not in agreement with the accounting records and returns; or• certain disclosures of Directors’ remuneration specified by law are not made; or• we have not received all the information and explanations we require for our audit.

Scott Knight (Senior Statutory Auditor) For and on behalf of BDO LLP, Statutory AuditorLondonUK12 April 2011

BDO LLP is a limited liability partnership registered in England and Wales (with registered number OC305127).

Report of the independent auditorsFor the year ended 31 December 2010

Kalahari Minerals plc Annual Report & Accounts 201012

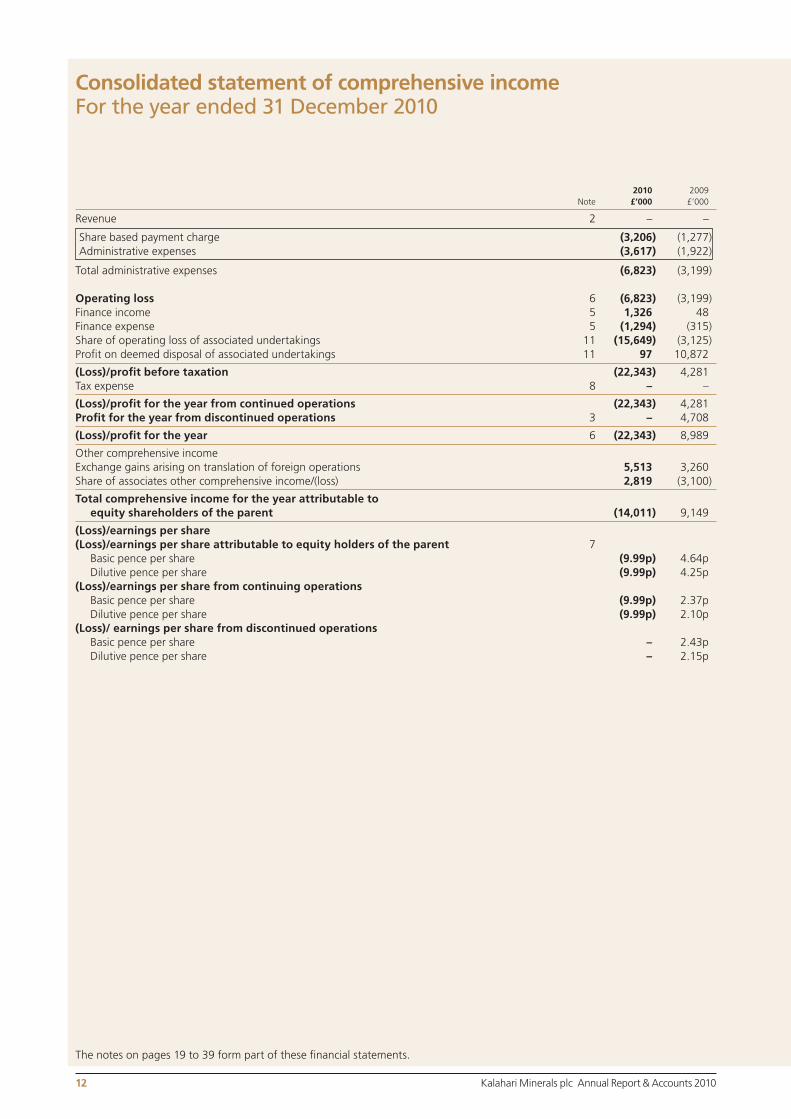

2010 2009 Note £’000 £’000

Revenue 2 – –

Share based payment charge (3,206) (1,277)Administrative expenses (3,617) (1,922)

Total administrative expenses (6,823) (3,199)

Operating loss 6 (6,823) (3,199)Finance income 5 1,326 48Finance expense 5 (1,294) (315)Share of operating loss of associated undertakings 11 (15,649) (3,125)Profit on deemed disposal of associated undertakings 11 97 10,872

(Loss)/profit before taxation (22,343) 4,281Tax expense 8 – –

(Loss)/profit for the year from continued operations (22,343) 4,281Profit for the year from discontinued operations 3 – 4,708

(Loss)/profit for the year 6 (22,343) 8,989

Other comprehensive income Exchange gains arising on translation of foreign operations 5,513 3,260Share of associates other comprehensive income/(loss) 2,819 (3,100)

Total comprehensive income for the year attributable toequity shareholders of the parent (14,011) 9,149

(Loss)/earnings per share (Loss)/earnings per share attributable to equity holders of the parent 7

Basic pence per share (9.99p) 4.64pDilutive pence per share (9.99p) 4.25p

(Loss)/earnings per share from continuing operations Basic pence per share (9.99p) 2.37pDilutive pence per share (9.99p) 2.10p

(Loss)/ earnings per share from discontinued operations Basic pence per share – 2.43pDilutive pence per share – 2.15p

Consolidated statement of comprehensive incomeFor the year ended 31 December 2010

The notes on pages 19 to 39 form part of these financial statements.

Kalahari Minerals plc Annual Report & Accounts 2010 13

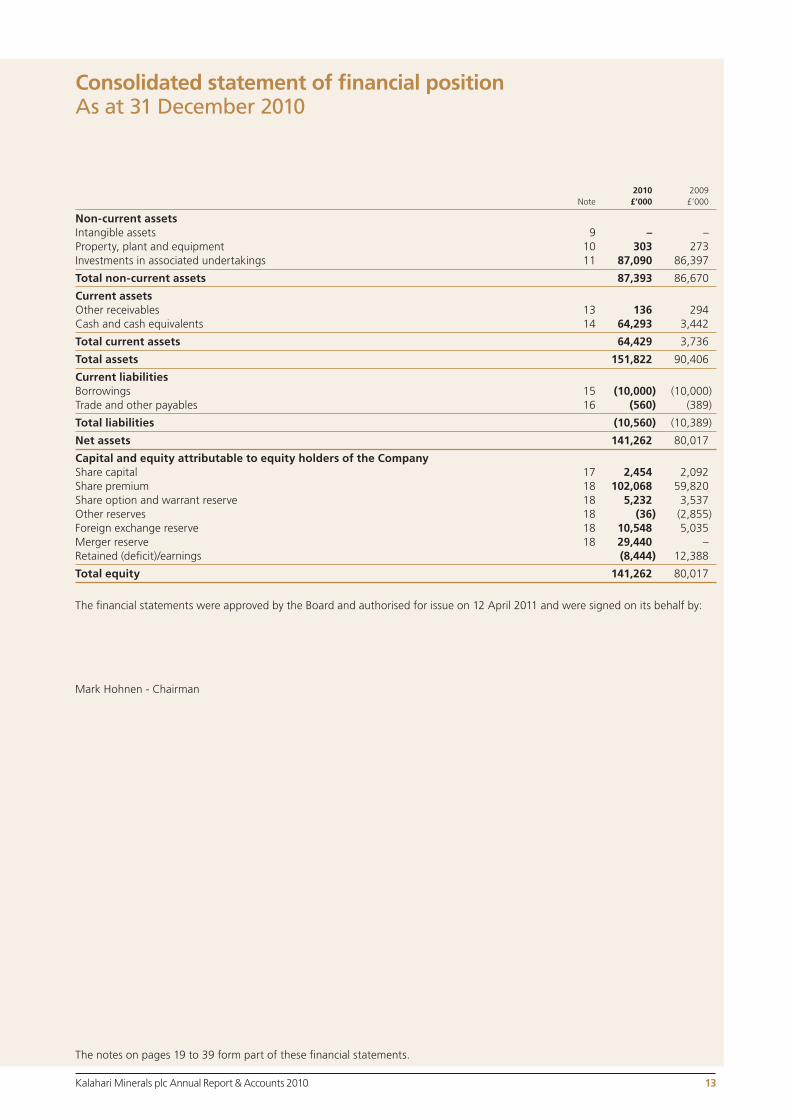

2010 2009 Note £’000 £’000

Non-current assets Intangible assets 9 – –Property, plant and equipment 10 303 273Investments in associated undertakings 11 87,090 86,397

Total non-current assets 87,393 86,670

Current assets Other receivables 13 136 294Cash and cash equivalents 14 64,293 3,442

Total current assets 64,429 3,736

Total assets 151,822 90,406

Current liabilitiesBorrowings 15 (10,000) (10,000)Trade and other payables 16 (560) (389)

Total liabilities (10,560) (10,389)

Net assets 141,262 80,017

Capital and equity attributable to equity holders of the Company Share capital 17 2,454 2,092Share premium 18 102,068 59,820Share option and warrant reserve 18 5,232 3,537Other reserves 18 (36) (2,855)Foreign exchange reserve 18 10,548 5,035Merger reserve 18 29,440 –Retained (deficit)/earnings (8,444) 12,388

Total equity 141,262 80,017

The financial statements were approved by the Board and authorised for issue on 12 April 2011 and were signed on its behalf by:

Mark Hohnen - Chairman

The notes on pages 19 to 39 form part of these financial statements.

Consolidated statement of financial positionAs at 31 December 2010

Kalahari Minerals plc Annual Report & Accounts 201014

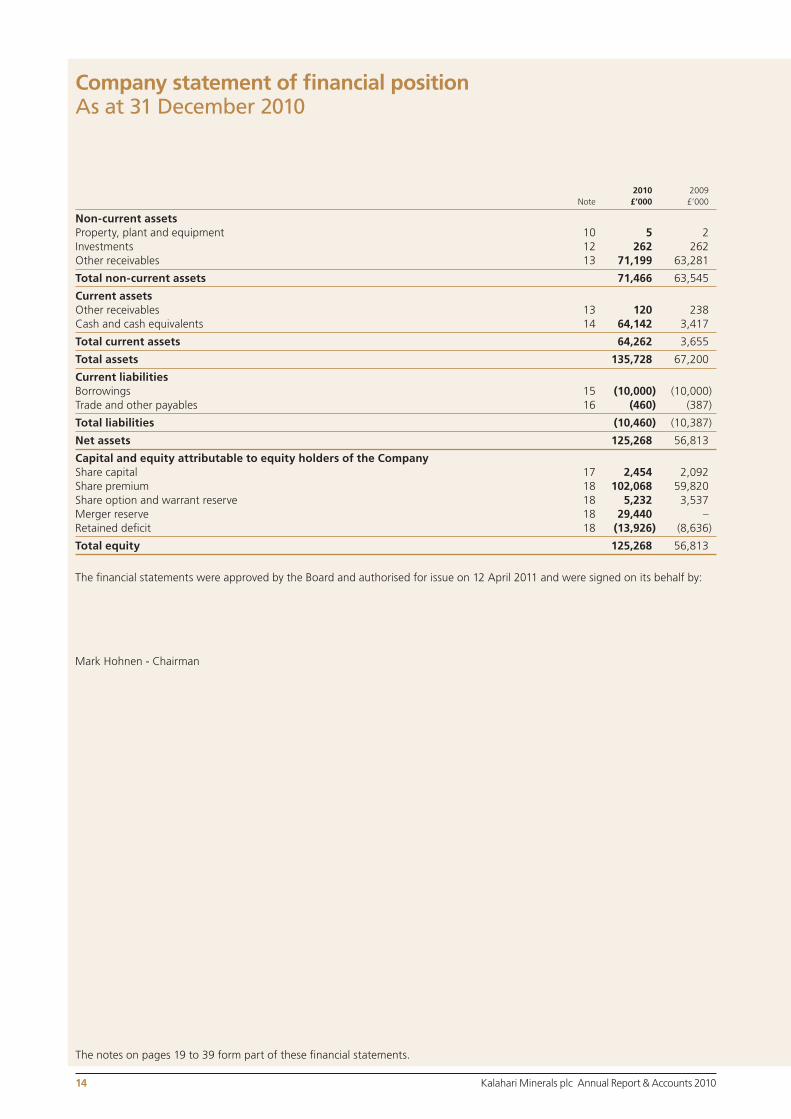

2010 2009 Note £’000 £’000

Non-current assetsProperty, plant and equipment 10 5 2Investments 12 262 262Other receivables 13 71,199 63,281

Total non-current assets 71,466 63,545

Current assetsOther receivables 13 120 238Cash and cash equivalents 14 64,142 3,417

Total current assets 64,262 3,655

Total assets 135,728 67,200

Current liabilities Borrowings 15 (10,000) (10,000)Trade and other payables 16 (460) (387)

Total liabilities (10,460) (10,387)

Net assets 125,268 56,813

Capital and equity attributable to equity holders of the Company Share capital 17 2,454 2,092Share premium 18 102,068 59,820Share option and warrant reserve 18 5,232 3,537Merger reserve 18 29,440 –Retained deficit 18 (13,926) (8,636)

Total equity 125,268 56,813

The financial statements were approved by the Board and authorised for issue on 12 April 2011 and were signed on its behalf by:

Mark Hohnen - Chairman

Company statement of financial positionAs at 31 December 2010

The notes on pages 19 to 39 form part of these financial statements.

Kalahari Minerals plc Annual Report & Accounts 2010 15

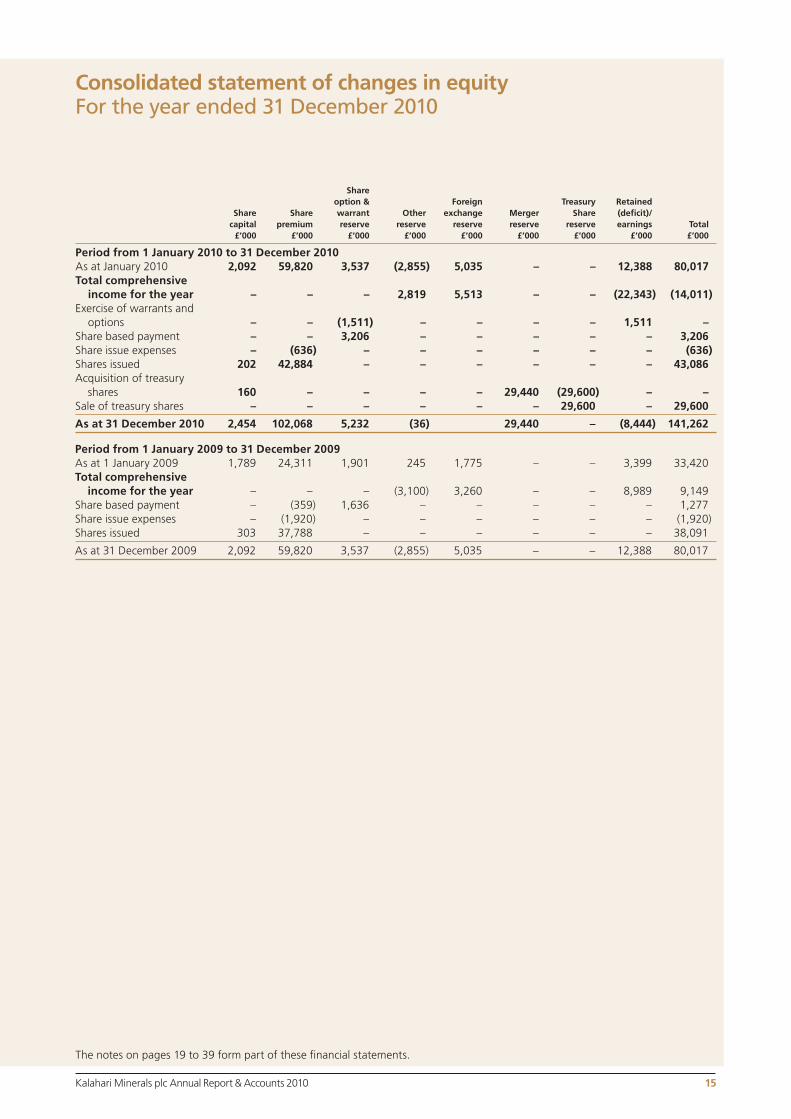

Share option & Foreign Treasury Retained Share Share warrant Other exchange Merger Share (deficit)/ capital premium reserve reserve reserve reserve reserve earnings Total £’000 £’000 £’000 £’000 £’000 £’000 £’000 £’000 £’000

Period from 1 January 2010 to 31 December 2010As at January 2010 2,092 59,820 3,537 (2,855) 5,035 – – 12,388 80,017Total comprehensive income for the year – – – 2,819 5,513 – – (22,343) (14,011)Exercise of warrants and options – – (1,511) – – – – 1,511 –Share based payment – – 3,206 – – – – – 3,206Share issue expenses – (636) – – – – – – (636)Shares issued 202 42,884 – – – – – – 43,086Acquisition of treasury shares 160 – – – – 29,440 (29,600) – –Sale of treasury shares – – – – – – 29,600 – 29,600

As at 31 December 2010 2,454 102,068 5,232 (36) 29,440 – (8,444) 141,262

Period from 1 January 2009 to 31 December 2009As at 1 January 2009 1,789 24,311 1,901 245 1,775 – – 3,399 33,420Total comprehensive income for the year – – – (3,100) 3,260 – – 8,989 9,149Share based payment – (359) 1,636 – – – – – 1,277Share issue expenses – (1,920) – – – – – – (1,920)Shares issued 303 37,788 – – – – – – 38,091

As at 31 December 2009 2,092 59,820 3,537 (2,855) 5,035 – – 12,388 80,017

Consolidated statement of changes in equityFor the year ended 31 December 2010

The notes on pages 19 to 39 form part of these financial statements.

Kalahari Minerals plc Annual Report & Accounts 201016

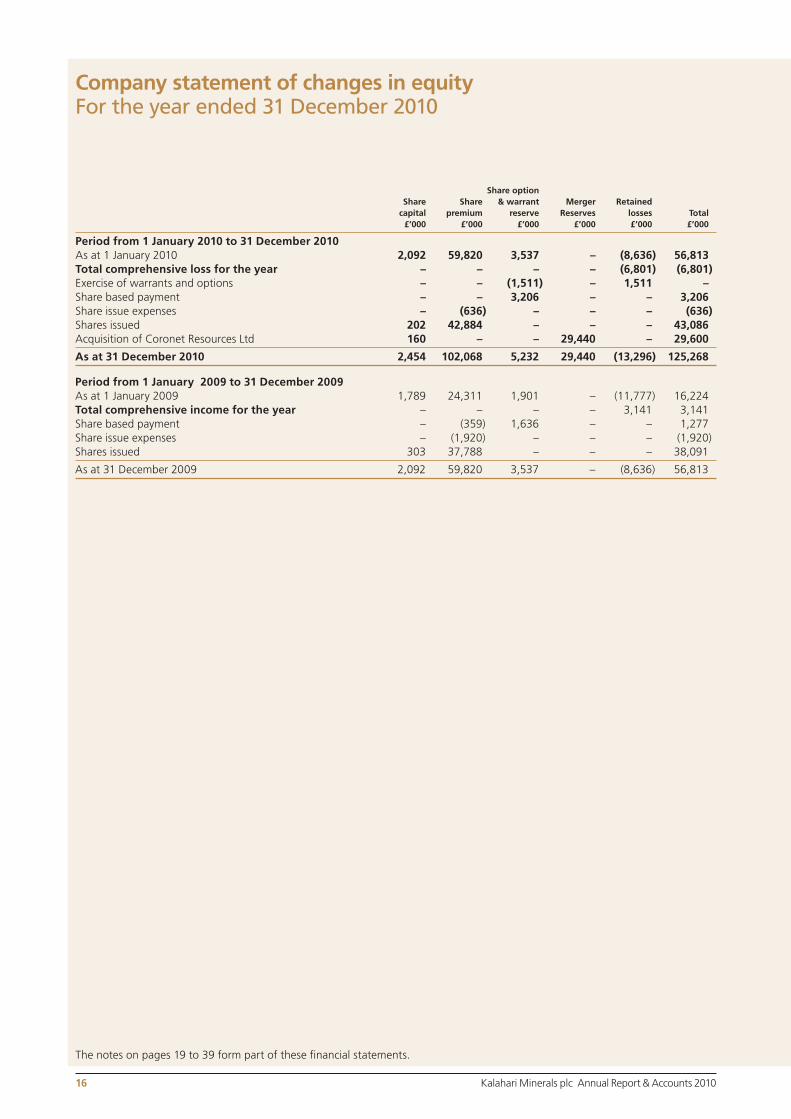

Share option Share Share & warrant Merger Retained capital premium reserve Reserves losses Total £’000 £’000 £’000 £’000 £’000 £’000

Period from 1 January 2010 to 31 December 2010As at 1 January 2010 2,092 59,820 3,537 – (8,636) 56,813Total comprehensive loss for the year – – – – (6,801) (6,801)Exercise of warrants and options – – (1,511) – 1,511 –Share based payment – – 3,206 – – 3,206Share issue expenses – (636) – – – (636)Shares issued 202 42,884 – – – 43,086Acquisition of Coronet Resources Ltd 160 – – 29,440 – 29,600

As at 31 December 2010 2,454 102,068 5,232 29,440 (13,296) 125,268

Period from 1 January 2009 to 31 December 2009As at 1 January 2009 1,789 24,311 1,901 – (11,777) 16,224Total comprehensive income for the year – – – – 3,141 3,141Share based payment – (359) 1,636 – – 1,277Share issue expenses – (1,920) – – – (1,920)Shares issued 303 37,788 – – – 38,091

As at 31 December 2009 2,092 59,820 3,537 – (8,636) 56,813

Company statement of changes in equityFor the year ended 31 December 2010

The notes on pages 19 to 39 form part of these financial statements.

Kalahari Minerals plc Annual Report & Accounts 2010 17

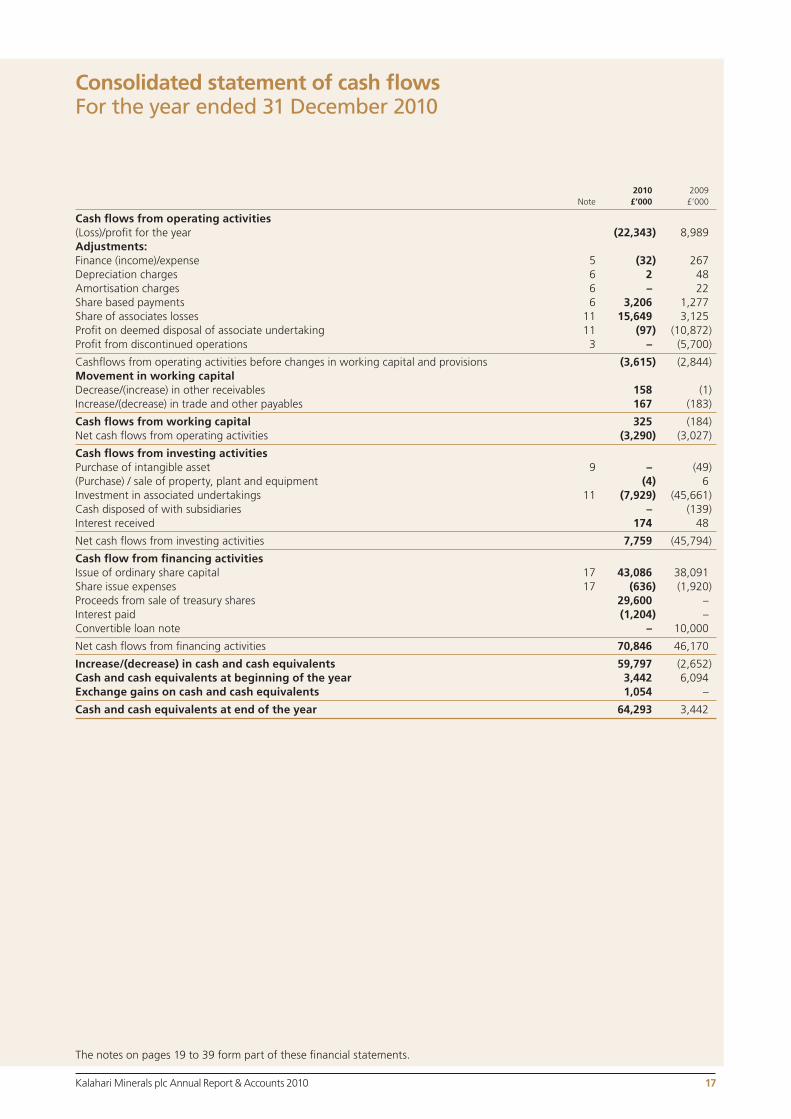

2010 2009 Note £’000 £’000

Cash flows from operating activities(Loss)/profit for the year (22,343) 8,989Adjustments:Finance (income)/expense 5 (32) 267Depreciation charges 6 2 48Amortisation charges 6 – 22Share based payments 6 3,206 1,277Share of associates losses 11 15,649 3,125Profit on deemed disposal of associate undertaking 11 (97) (10,872)Profit from discontinued operations 3 – (5,700)

Cashflows from operating activities before changes in working capital and provisions (3,615) (2,844)Movement in working capital Decrease/(increase) in other receivables 158 (1)Increase/(decrease) in trade and other payables 167 (183)

Cash flows from working capital 325 (184)Net cash flows from operating activities (3,290) (3,027)

Cash flows from investing activitiesPurchase of intangible asset 9 – (49)(Purchase) / sale of property, plant and equipment (4) 6Investment in associated undertakings 11 (7,929) (45,661)Cash disposed of with subsidiaries – (139)Interest received 174 48

Net cash flows from investing activities 7,759 (45,794)

Cash flow from financing activitiesIssue of ordinary share capital 17 43,086 38,091Share issue expenses 17 (636) (1,920)Proceeds from sale of treasury shares 29,600 –Interest paid (1,204) –Convertible loan note – 10,000

Net cash flows from financing activities 70,846 46,170

Increase/(decrease) in cash and cash equivalents 59,797 (2,652)Cash and cash equivalents at beginning of the year 3,442 6,094Exchange gains on cash and cash equivalents 1,054 –

Cash and cash equivalents at end of the year 64,293 3,442

Consolidated statement of cash flowsFor the year ended 31 December 2010

The notes on pages 19 to 39 form part of these financial statements.

Kalahari Minerals plc Annual Report & Accounts 201018

The notes on pages 19 to 39 form part of these financial statements.

2010 2009 Note £’000 £’000

Cash flows from operating activities(Loss)/profit for the year (6,801) 3,141Adjustments:Finance expense 68 315Depreciation charges 1 –Share based payments 3,206 1,277Profit/(Loss) on disposal of subsidiaries 3 – 832

Cashflows from operating activities before changes in working capital and provisions (3,526) 5,565

Movement in working capitalDecrease/(increase) in other receivables 13 118 (131)Increase in payables 16 (19) (232)

Cash flows from by operating activities 99 (363)

Net cash from operating activities (3,427) 5,202

Cash flows from investing activitiesPurchase of property, plant and equipment (4) (2)Sale of property, plant and equipment – 23Interest received 174 48Loans to group undertakings (21,682) (53,794)

Net cash flow from investing activities 21,852 (53,725)

Cash flow used in financing activities Issue of ordinary share capital 17 43,086 38,091Share issue expenses 17 (636) (1,920)Interest paid (1,204) –Convertible loan note – 10,000

Net cash flows from financing activities 41,246 46,170

Increase/(decrease) in cash and cash equivalents 59,671 (2,353)Cash and cash equivalents at beginning of the year 3,417 5,770Exchange gains on cash and cash equivalents 1,054 –

Cash and cash equivalents at end of the year 64,142 3,417

Company statement of cash flowsFor the year ended 31 December 2010

Kalahari Minerals plc Annual Report & Accounts 2010 19

1 SIGNIFICANT ACCOUNTING POLICIESGeneral information Kalahari Minerals plc is a public limited company which is quoted on AIM and NSX and domiciled in the UK. The address of the registered office is Level 1B, 38 Jermyn Street, London SW1Y 6DN. The registered number of the Company is 5294388.

Basis of preparationThe principal accounting policies adopted in the preparation of the financial statements are set out below. The policies have been consistently applied to all the years presented, unless otherwise stated. Both the Company financial statements and the Group financial statements have been prepared and approved by the Directors in accordance with International Financial Reporting Standards IFRS’s and IFRIC interpretations, issued by the International Accounting Standards Board (IASB) as endorsed for use in the EU (“Endorsed IFRSs”) and those parts of the Companies Act 2006 that are applicable to companies that prepare their financial statements under IFRS.

The Company has taken advantage of the exemption allowed under section 408 of the Companies Act 2006 and has not presented its own statement of comprehensive income in these financial statements. The Group loss for the year includes a loss after tax of £6.8 million (2009: profit after tax of £3.1 million), which is dealt with in the financial statements of the Company.

New IFRS issued by the IASB effective from 1 January 2010 and applied in these financial statements are as follows: Standard Date of adoption Impact on initial applicationIAS 27 Amendment – Consolidated and separate financial statements

1 July 2009 This amendment did not have any impact on the current, or prior year financial statements. Future transactions will be accounted for consistently with this amendment.

IFRS3 Revised – Business Combinations

1 July 2009 This amendment did not have any impact on the current, or prior year financial statements. Future transactions will be accounted for consistently with this amendment.

IAS 39 – Amendment – Financial Instruments: Recognition and Measurement: Eligible Hedged Items

1 July 2009 The amendment clarifies the principles for determining eligibility of hedged items.

The amendment did not have any impact on the current or prior years’ financial statements. Future transactions will be accounted for consistently with this amendment.

IFRS 2 – Amendment – Group Cash – settled Share-based Payment Transactions

1 January 2010 This is not relevant to the Group as it does not have any cash settled share based payment transactions.

Improvements to IFRSs (2009) Generally 1 January 2010 The improvements in this Amendment clarify the requirements of

IFRSs and eliminate inconsistencies within and between Standards. The improvements did not have any impact on the current or prior years’ financial statements.

IFRIC 17 – Distributions of Non-cash Assets to Owners

1 January 2010 The interpretation provides guidance on how to measure distribution of assets other than cash.

The application of this interpretation did not have any impact on the current or prior year’s financial statements. Future transactions will be accounted for consistently with this interpretation.

IFRIC 18 – Transfer of Assets from Customers

1 January 2010 The interpretation clarifies the treatment of agreements in which an entity receives from a customer an item of property that it must use to provide the customer with an on-going access to goods or services.

The application of this interpretation did not have any impact on the current or prior year’s financial statements. Future transactions will be accounted for consistently with this interpretation.

Notes to the financial statementsFor the year ended 31 December 2010

Kalahari Minerals plc Annual Report & Accounts 201020

1 SIGNIFICANT ACCOUNTING POLICIES – continuedIFRIC 9/IAS 39 – Amendment – Embedded Derivative

1 January 2010 The amendment clarifies the treatment of embedded derivatives in host contracts that are classified out of fair value through profit or loss.

The application of this interpretation did not have any impact on the current or prior year’s financial statements. Future transactions will be accounted for consistently with this interpretation.

IFRIC 16 Hedges of a Net Investment in a Foreign Operation

1 January 2010 The interpretation provides guidance for application of hedge accounting in foreign operations.

The application of this interpretation did not have any impact on the current or prior year’s financial statements. Future transactions will be accounted for consistently with this interpretation.

The following standards, interpretations and amendments issued by the IASB are not yet effective in 2010:

Standard Effective date DescriptionIAS 32 1 February 2010 Amendment - Classification of Right IssuesIFRIC 19 1 July 2010 Extinguishing Financial Liabilities with Equity InstrumentsIFRS 1 1 July 2010 Amendment - First Time Adoption of IFRSIAS 24 1 January 2011 Revised - Related Party DisclosuresIFRIC 14 1 January 2011 Amendment - IAS 19 Limit on a defined benefit assetIFRS 7 * 1 July 2011 Amendment - Transfer of financial assetsIFRS 1 * 1 July 2011 Severe Hyperinflation and Removal of Fixed Dates for First-time

Adopters 1 January 2011 Improvements to IFRSs (2010) *IAS 12 * 1 January 2012 Deferred Tax: Recovery of Underlying Assets IFRS 9 * 1 January 2013 Financial instruments

No other IFRS’s issued and adopted but not yet effective are expected to have an impact on the Group’s financial statements.

The Group have not yet assessed the impact of IFRS 9. Except for the amended disclosure requirements of IAS24 Revised the above new standards, amendments and interpretations are not expected to materially affect the Group’s reporting or reported numbers.

The Directors do not anticipate that the adoption of the other standards and interpretations listed above will have a material impact on the Company’s financial statements in the period of initial application.

* Not yet endorsed by European Union

Basis of consolidation(a) SubsidiariesSubsidiaries are entities that are directly or indirectly controlled by the Group. Control exists where the Group has the power to govern the financial and operating policies of the entity so as to obtain benefits from its activities. In assessing control, potential voting rights are taken into account. Subsidiaries are fully consolidated from the date on which control is transferred until the date that the control ceases.

The purchase method of accounting is used to account for the acquisition of subsidiaries by the Group. Inter-company transactions, balances and unrealised gains on transactions between Group entities are eliminated.

(b) AssociatesAn associate is an entity over which the Group has significant influence and that is neither a subsidiary nor an interest in a joint venture. Significant influence is the power to participate in the financial and operating policy decisions of the investee but is not control or exert joint control over those policies.

In considering the degree of control the contractual ability to direct use of funding provided by the Group are taken into consideration.

Notes to the financial statements (continued)For the year ended 31 December 2010

Kalahari Minerals plc Annual Report & Accounts 2010 21

1 SIGNIFICANT ACCOUNTING POLICIES – continuedInvestments in associates are accounted for using the equity method of accounting and are initially recognised at cost plus any goodwill arising. Any premium paid for an associate above the fair value of the Group’s share of the identifiable assets, liabilities and contingent liabilities acquired is capitalised and included in the carrying amount of the associate. The carrying amount of investment in an associate is subject to impairment in the same way as described below.

The Group’s share of its associates’ post-acquisition profits or losses is recognised in the consolidated statement of comprehensive income, and its share of post-acquisition movements in equity is recognised in equity. The cumulative post-acquisition movements are adjusted against the carrying amount of the investment. When the Group’s share of losses in an associate equals or exceeds its interest in the associate no further losses are recognised.

Where annual financial statements for an associate are available which have a concurrent year end to that of the Group the information contained within the financial statements will be used to equity account for the associate. Where an associate has a financial year end which is not concurrent with that of the Group or is more than three months different to that of the Group but the associate prepares interim financial information which is publicly available this information, adjusted for any known circumstances, will be used to equity account for the associate.

Revenue recognition Revenue is measured at the fair value of consideration received or receivable from the sale of goods and services from the Group’s ordinary business activities. Revenue is stated net of discounts, sales and other taxes. There was no revenue received in the year.

Finance incomeRevenue from finance income is accrued on a timely basis using the effective interest method, which exactly discounts estimated future cash flows through the expected life of the financial asset, to which the finance income derived, to its net carrying value. The only interest received in the year was on cash held at bank.

ExpensesOperating expenses are recognised in the statement of comprehensive income upon utilisation of the service or at the date of their origin.

Continued and discontinued operationsThe results of operations during the year are included in the consolidated statement of comprehensive income up to the date of disposal.

Discontinued operations are presented in the statement of comprehensive income (including the comparative period) as a single line which comprises the post tax loss of the discontinued operation. Operations are classified as discontinued when the decision is made to dispose of the operation by the directors and the operations are actively marketed.

Intangible assets – exploration and evaluation assetsThe Group capitalises the fair value of the consideration paid for exploration and prospecting rights. All other costs incurred are expensed as they are incurred. The Group has taken into consideration the degree to which expenditure can be associated with finding specific mineral resources. The intangibles are amortised over the length of the mining licences and the amortisation expense is included within the Administration expenses line in the statement of comprehensive income.

Impairment of assets Where appropriate, the Group reviews the carrying amounts of its tangible assets, intangible assets and investments in associates to determine whether there is any indication that those assets have suffered an impairment loss.

If any such indication exists, the recoverable amount of the asset is estimated in order to determine the extent of theimpairment loss. Where it is not possible to estimate the recoverable amount of an individual asset, the Group estimates the recoverable amount of the cash-generating unit to which the asset belongs.

The recoverable amount is the higher of fair value less costs to sell and value in use. In assessing value in use, the estimated future cash flows are discounted to their present value using a pre-tax discount rate that reflects the current market assessments of the time value of money and the risks specific to the asset. If the recoverable amount of an asset (or cash-generating unit) is estimated to be less than its carrying amount, the carrying amount of the asset (cash generating unit) is reduced to its recoverable amount. An impairment loss is recognised immediately in the statement of comprehensive income, unless the relevant asset is carried at a revalued amount, in which case the impairment loss is treated as a revaluation decrease.

Where an impairment loss subsequently reverses, the carrying amount of the asset (cash-generating unit) is increased to the revised estimate of its recoverable amount, but so that the increased carrying amount does not exceed the carrying amount that would have been determined had no impairment loss been recognised for the asset (cash-generating unit) in prior years.

Notes to the financial statements (continued)For the year ended 31 December 2010

Kalahari Minerals plc Annual Report & Accounts 201022

1 SIGNIFICANT ACCOUNTING POLICIES – continuedProperty, plant and equipmentProperty, plant and equipment are stated at cost less accumulated depreciation and any recognised impairment loss. Depreciation is charged so as to write off the costs of assets, over their estimated useful lives, using the straight line method, on the following basis:

Leasehold land & buildings 50 yearsBuilding improvements 4 yearsFixtures & fittings 4 yearsPlant and machinery 4 yearsMotor vehicles 4 years

Financial instrumentsFinancial assets and financial liabilities are recognised on the statement of financial positions when the Company becomes a party to the contractual provisions of the instrument.

Financial assets and liabilities are initially recognised and subsequently measured based on their classification as “loans and receivables” or “other” financial liabilities.

The Company classifies its financial assets as loans and receivables. The classification depends on the purpose for which the financial assets were acquired. Management determines the classification of its financial assets at initial recognition.

Loans and ReceivablesLoans and receivables are non-derivative financial assets with fixed or determinable payments that are not quoted in an active market. They are included in current assets. The Company’s loans and receivables comprise of “Other receivables” and “cash and cash equivalents”. Other receivables are recognised initially at fair value and subsequently measured at amortised cost less provision for impairment.

Financial liabilitiesThe Group classifies its financial liabilities into categories depending on the purpose for which the liability was acquired. The Group has not classified any of its liabilities at fair value through profit and loss.

The Group’s accounting policy for each category is as follows:

Held at amortised cost: Trade payables and other short-term monetary liabilities are initially recognised at fair value and subsequently carried at amortised cost using the effective interest method.

Compound financial instruments: The Group’s convertible loan notes are classified as compound financial instruments and a separate accounting policy for Convertible Debt has been included below.

Convertible debtIn accordance with IAS 32 and IAS 39, the Company has classified the convertible debt in issue as a compound financial instrument. Accordingly, the Company presents as appropriate the liability and equity components separately on the statement of financial position. The classification of the liability and equity components is not reversed as a result of a change in the likelihood that the conversion option will be exercised. No gain or loss arises from initially recognising the components of the instrument separately. Interest on the debt element of the loan is accreted over the term of the loan. Costs associated with the raising of debt are set off against the gross value of monies received.

Share capitalFinancial instruments issued by the Group are treated as equity only to the extent that they do not meet the definition of a financial liability. The Group’s ordinary shares and unclassified ordinary shares are classed as equity instruments.

LeasesPayments made under operating leases are recognised in the statement of comprehensive income on a straight line basis over the term of the lease.

ProvisionsProvisions are recognised when the Group has a present obligation as a result of a past event and it is probable that the Group will be required to settle the obligation. Provisions are measured at the Directors’ best estimate of the expenditure required to settle that obligation at the reporting date and are discounted to present value where the effect is material.

Notes to the financial statements (continued)For the year ended 31 December 2010

Kalahari Minerals plc Annual Report & Accounts 2010 23

1 SIGNIFICANT ACCOUNTING POLICIES – continuedTaxationCurrent taxes are based on the results shown in the financial statements and are calculated according to local tax rules, using tax rates enacted or substantively enacted by the reporting date.

Deferred taxDeferred tax is calculated on the comprehensive basis using the statement of financial position liability method, which requires provision for temporary differences between the tax bases of assets and liabilities and their carrying amounts on the statement of financial position. Tax rates enacted at the statement of financial position date are used to determine the deferred tax balances. Deferred tax assets are recognised to the extent that it is probable that future taxable profit will be available against which the asset can be utilised. Deferred tax is applied to share-based payments in accordance with IAS 12 Income Taxes.

Foreign currenciesAssets and liabilities in foreign currencies are translated into sterling at the rates of exchange ruling at the reporting date. Transactions in foreign currencies are translated into sterling at the rate of exchange ruling at the date of transaction. Exchange differences are taken into account in arriving at the operating result. The Company translates its foreign operations using the closing rate method.

One of the requirements of IAS 21 – “The Effects of Changes in Foreign Exchange Rates” is that on disposal of a foreign operation, the cumulative amount of exchange differences previously recognised directly in equity for that foreign operation are to be transferred to the statement of comprehensive income as part of the profit or loss on disposal. The Company has adopted the exemption allowing these cumulative translation differences to be reset to zero at the transition date. If the Company had not taken this exemption, a different amount of net foreign exchange gains and losses would be transferred to the statement of comprehensive income on disposal of a foreign operation.

Monetary assets and liabilities for foreign operations are translated at the year end exchange rate and non-monetary assets are recorded at the exchange rate prevailing at the date of acquisition.

Exchange differences arising from the translation of the net assets of foreign operations are taken to the foreign exchange reserve. Other exchange differences are taken to the statement of comprehensive income.

Share-based paymentsThe Company has granted equity-settled options and warrants. The fair value of the incentive granted is recognised as an expense with a corresponding increase in equity. The fair value is measured at the grant date and spread over the period during which the employees or third parties become unconditionally entitled to the incentives. When identifiable, the fair value is determined by the value of the services provided. When a fair value for the services provided cannot be ascertained the fair value is measured by reference to the fair value of the equity instrument granted.

Judgements made in applying accounting policies and key sources of estimation uncertaintyThe significant judgements made by management in applying the Group’s accounting policies and the key sources of estimation were:

(a) Impairment of assetsIn formulating accounting policies the Directors are required to apply their judgment, and where necessary engage professional advisors, with regard to the following significant areas:

• Investments in associates.

These associates carrying values are subject to periodic review by the Directors.

On review, during the year, the Directors have noted no circumstances which would suggest that at this time any impairment is necessary given the market value of each investment. The situation will be closely monitored and adjustments made in future periods if there are indications that the assets held are not recoverable.

(b) Share-based payments In determining the fair value of equity settled share based payments and the related charge to the statement of comprehensive income, the Group must make assumptions about future events and market conditions. Judgement is made as to the likely number of shares that will vest, and the fair value of each award granted.

Notes to the financial statements (continued)For the year ended 31 December 2010

Kalahari Minerals plc Annual Report & Accounts 2010 25

3 PRIOR YEAR DISCONTINUED OPERATIONSOn 20 November 2009 the Company sold its interest in West Africa Gold Exploration (Namibia) (Pty) Ltd and Craton Diamonds (Pty) Ltd to North River Resources plc in exchange for 266,666,667 shares in North River. The income, expenses, assets and liabilities relating to this asset were reclassified as discontinued in the year ending 31 December 2009.

PROFIT ON DISCONTINUED OPERATIONS FOR THE PERIOD TO THE DATE OF DISPOSAL: 2009 £’000

Loss on discontinued operations (992)

Profit from selling discontinued operations after tax Sales proceeds, net of costs 5,879Pre-disposal carrying value 179

Profit on disposal of discontinued operations 5,700

Total profit from discontinued operations after tax 4,708

FINANCIAL INFORMATION RELATING TO THE NON-CURRENT ASSETS HELD FOR SALE: 2009 £’000

Cash disposed of: 139

Net assets disposed of: Intangible assets 63Property, plant and equipment 159Trade and other receivables 144Trade and other payables (326)

179

DISCONTINUED CASH FLOW MOVEMENTS:The statement of cash flows includes the following amounts relating to discontinued operations: 2009 £’000

Net cash from operating activities (810)

Net cash from investing activities (139)

4 DIRECTORS AND EMPLOYEES Group Group Company Company 2010 2009 2010 2009

Average number of Directors and employees are as follows: Directors 6 4 6 4Administration and operations 1 50 1 1

7 54 7 5

Group Group Company Company 2010 2009 2010 2009 £’000 £’000 £’000 £’000

Gross salaries 31 571 31 39Share based payments – employees – 21 – –

31 592 31 39

Director fees 298 241 298 241Share based payments – Directors 2,998 1,173 2,998 1,173

3,296 1,414 3,296 1,414

3,327 2,006 3,327 1,453

Notes to the financial statements (continued)For the year ended 31 December 2010

Kalahari Minerals plc Annual Report & Accounts 201026

4 DIRECTORS AND EMPLOYEES – continuedDirectors listed on page 6 are considered to be the key management. Their remuneration and interests in share options, as at 31 December 2010, are as follows:

Salary Salary Share Share 2010 2009 options options £’000 £’000 2010 2009

Executive Chairman – Mark Hohnen(*) 150 150 7,500,000 5,500,000Non-Executive Director – Glyn Tonge 38 35 2,750,000 1,750,000Non-Executive Director – David Weill 31 25 1,750,000 750,000Non-Executive Director – Neil MacLachlan 39 24 2,050,000 750,000Non-Executive Director – Richard Lockwood 26 – 1,000,000 –Non-Executive Director – Takashi Yasuda 14 – – –

298 234 15,050,000 8,750,000

All Directors’ remuneration is paid in cash in accordance with their contracts. In addition all Directors have received options to purchase Ordinary Shares of the Company at exercise prices that vary in accordance to the year of grant (see Note 20). The highest paid Director (*) was paid £150,000 in the year (2009: £150,000) and did not exercise any share options (2009: nil).

The Company provides limited Directors and Officers Liability Insurance, at a cost of approximately £20,738 (2009: £14,095). This cost is not included in the table above.