Embed Size (px)

Citation preview

,

Discussion: The Financial Channel of WageRigidity

Benjamin Schoefer

Claudio Michelacci, CSEF-EIEF-SITE Conference

,

Important questions

Why do firms reduce hiring in recessions and unemploymentincrease ?

Does wage rigidity in existing matches (as opposed to newmatches) matter?

Should wages be counter-cyclical or pro-cyclical to smoothaggregate cyclical fluctuations?

Large literature. Here an interesting, new, nice, and simpletwist based on the financial channel of wage rigidity

Wage contracts are like debt-contracts.

During recessions, firms revenue falls and rigid wages makefirm cash flows fall more. If firms are financially constrained,rigid wages exacerbate firm financial constraint and force firmto cut hiring more.

,

Important questions

Why do firms reduce hiring in recessions and unemploymentincrease ?

Does wage rigidity in existing matches (as opposed to newmatches) matter?

Should wages be counter-cyclical or pro-cyclical to smoothaggregate cyclical fluctuations?

Large literature. Here an interesting, new, nice, and simpletwist based on the financial channel of wage rigidity

Wage contracts are like debt-contracts.

During recessions, firms revenue falls and rigid wages makefirm cash flows fall more. If firms are financially constrained,rigid wages exacerbate firm financial constraint and force firmto cut hiring more.

,

Important questions

Why do firms reduce hiring in recessions and unemploymentincrease ?

Does wage rigidity in existing matches (as opposed to newmatches) matter?

Should wages be counter-cyclical or pro-cyclical to smoothaggregate cyclical fluctuations?

Large literature. Here an interesting, new, nice, and simpletwist based on the financial channel of wage rigidity

Wage contracts are like debt-contracts.

During recessions, firms revenue falls and rigid wages makefirm cash flows fall more. If firms are financially constrained,rigid wages exacerbate firm financial constraint and force firmto cut hiring more.

,

Methodology and some key resultsSome empirical evidence and a quantitative model.

Firm level evidence Firms with higher internal funds at thestart of the recession tend to experience smaller reductions inemployment

Industry level evidence High labor share industries tend tohave more pro-cyclical employment

DMP quantitative model Using a DMP model (with sometwists), show that the mechanism could be quantitativelyimportant

Key important point An increase in the procyclicality ofwages would be welfare improving and would stabilizeaggregate fluctuations.Workers should provide more financing to firms in recessions

First reaction: A bit too much and somewhat unfocused, but it isa good start!

,

Methodology and some key resultsSome empirical evidence and a quantitative model.

Firm level evidence Firms with higher internal funds at thestart of the recession tend to experience smaller reductions inemployment

Industry level evidence High labor share industries tend tohave more pro-cyclical employment

DMP quantitative model Using a DMP model (with sometwists), show that the mechanism could be quantitativelyimportant

Key important point An increase in the procyclicality ofwages would be welfare improving and would stabilizeaggregate fluctuations.Workers should provide more financing to firms in recessions

First reaction: A bit too much and somewhat unfocused, but it isa good start!

,

Methodology and some key resultsSome empirical evidence and a quantitative model.

Firm level evidence Firms with higher internal funds at thestart of the recession tend to experience smaller reductions inemployment

Industry level evidence High labor share industries tend tohave more pro-cyclical employment

DMP quantitative model Using a DMP model (with sometwists), show that the mechanism could be quantitativelyimportant

Key important point An increase in the procyclicality ofwages would be welfare improving and would stabilizeaggregate fluctuations.Workers should provide more financing to firms in recessions

First reaction: A bit too much and somewhat unfocused, but it isa good start!

,

Methodology and some key resultsSome empirical evidence and a quantitative model.

Firm level evidence Firms with higher internal funds at thestart of the recession tend to experience smaller reductions inemployment

Industry level evidence High labor share industries tend tohave more pro-cyclical employment

DMP quantitative model Using a DMP model (with sometwists), show that the mechanism could be quantitativelyimportant

Key important point An increase in the procyclicality ofwages would be welfare improving and would stabilizeaggregate fluctuations.Workers should provide more financing to firms in recessions

First reaction: A bit too much and somewhat unfocused, but it isa good start!

,

Methodology and some key resultsSome empirical evidence and a quantitative model.

Firm level evidence Firms with higher internal funds at thestart of the recession tend to experience smaller reductions inemployment

Industry level evidence High labor share industries tend tohave more pro-cyclical employment

DMP quantitative model Using a DMP model (with sometwists), show that the mechanism could be quantitativelyimportant

Key important point An increase in the procyclicality ofwages would be welfare improving and would stabilizeaggregate fluctuations.Workers should provide more financing to firms in recessions

First reaction: A bit too much and somewhat unfocused, but it isa good start!

,

Methodology and some key resultsSome empirical evidence and a quantitative model.

Firm level evidence Firms with higher internal funds at thestart of the recession tend to experience smaller reductions inemployment

Industry level evidence High labor share industries tend tohave more pro-cyclical employment

DMP quantitative model Using a DMP model (with sometwists), show that the mechanism could be quantitativelyimportant

Key important point An increase in the procyclicality ofwages would be welfare improving and would stabilizeaggregate fluctuations.Workers should provide more financing to firms in recessions

First reaction: A bit too much and somewhat unfocused, but it isa good start!

,

My discussion

A nice twist!

Comments on empirical evidence

Why wage rigidity?

Is the mechanism quantitatively important in the aggregateeconomy?

,

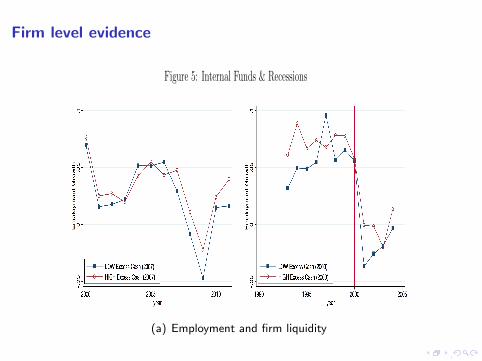

Firm level evidence

Figure 5: Internal Funds & Recessions

(a) 2007/08 Recession (b) 2001/02 Recession

Notes: Firms are cut above/below median of excess liquidity in pre-recession reference year(vertical line). Excess liquidity: residual of liquid over total assets regressed on size (totalasset deciles) & 2-digit SIC industry and interactions. Annual, weighted by pre-recessionlevels. Source: Compustat.

50

(a) Employment and firm liquidity

,

Industry level evidence

Figure 7: Industry-level Cyclicalities by Labor Share: Cash Flow, Employment, Investment.

(a) Recession event studies: Employment de-clines by labor share.

(b) Recession event studies: Cash flow declinesby labor share.

(c) Recession event studies: Capital expendi-ture declines by labor share.

(d) Industry cyclicalities: cash flow, employ-ment, capital expenditure.

Figure 8: See main text for construction of cyclicality measures (coefficient on detrended un-employment from industry-level regressions). Source: NBER-CES Manufacturing IndustryData Base, annual data, 1958-2009.

52

(a) Recessions and labor share

But is this evidence in favor of the financial channel of wagerigidity?

,

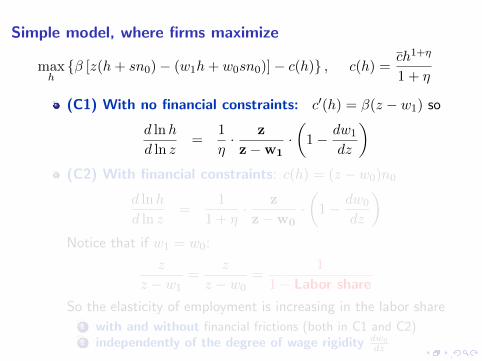

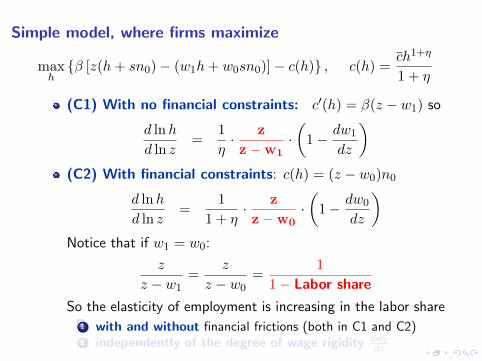

Simple model, where firms maximize

maxh{β [z(h+ sn0)− (w1h+ w0sn0)]− c(h)} , c(h) =

ch1+η

1 + η

(C1) With no financial constraints: c′(h) = β(z − w1) so

d lnh

d ln z=

1

η· z

z−w1·(1− dw1

dz

)(C2) With financial constraints: c(h) = (z − w0)n0

d lnh

d ln z=

1

1 + η· z

z−w0·(1− dw0

dz

)Notice that if w1 = w0:

z

z − w1=

z

z − w0=

1

1− Labor share

So the elasticity of employment is increasing in the labor share1 with and without financial frictions (both in C1 and C2)2 independently of the degree of wage rigidity dw0

dz

,

Simple model, where firms maximize

maxh{β [z(h+ sn0)− (w1h+ w0sn0)]− c(h)} , c(h) =

ch1+η

1 + η

(C1) With no financial constraints: c′(h) = β(z − w1) so

d lnh

d ln z=

1

η· z

z−w1·(1− dw1

dz

)(C2) With financial constraints: c(h) = (z − w0)n0

d lnh

d ln z=

1

1 + η· z

z−w0·(1− dw0

dz

)Notice that if w1 = w0:

z

z − w1=

z

z − w0=

1

1− Labor share

So the elasticity of employment is increasing in the labor share1 with and without financial frictions (both in C1 and C2)2 independently of the degree of wage rigidity dw0

dz

,

Simple model, where firms maximize

maxh{β [z(h+ sn0)− (w1h+ w0sn0)]− c(h)} , c(h) =

ch1+η

1 + η

(C1) With no financial constraints: c′(h) = β(z − w1) so

d lnh

d ln z=

1

η· z

z−w1·(1− dw1

dz

)(C2) With financial constraints: c(h) = (z − w0)n0

d lnh

d ln z=

1

1 + η· z

z−w0·(1− dw0

dz

)Notice that if w1 = w0:

z

z − w1=

z

z − w0=

1

1− Labor share

So the elasticity of employment is increasing in the labor share1 with and without financial frictions (both in C1 and C2)2 independently of the degree of wage rigidity dw0

dz

,

Simple model, where firms maximize

maxh{β [z(h+ sn0)− (w1h+ w0sn0)]− c(h)} , c(h) =

ch1+η

1 + η

(C1) With no financial constraints: c′(h) = β(z − w1) so

d lnh

d ln z=

1

η· z

z−w1·(1− dw1

dz

)(C2) With financial constraints: c(h) = (z − w0)n0

d lnh

d ln z=

1

1 + η· z

z−w0·(1− dw0

dz

)Notice that if w1 = w0:

z

z − w1=

z

z − w0=

1

1− Labor share

So the elasticity of employment is increasing in the labor share1 with and without financial frictions (both in C1 and C2)2 independently of the degree of wage rigidity dw0

dz

,

Why wage rigidity?

1 In search models wages are just a way of splitting the surplusgenerated by employment relations

2 How this surplus is split is irrelevant and it has no welfareconsequences from the point of view of the two partiesinvolved (workers and firms).

3 Search models are a natural theoretical framework to modelwage rigidity because the Coase theorem applies

4 But here the Coase theorem is violated. Firms and workersleave some unexploited gains on the table. There are noexternalities and firms and workers know that their netsurplus would increase if they were to sign a wage contractwhere wages are procyclical

5 Why don’t they do it? What is the friction? This is a bitunsatisfactory.

,

Why wage rigidity?

1 In search models wages are just a way of splitting the surplusgenerated by employment relations

2 How this surplus is split is irrelevant and it has no welfareconsequences from the point of view of the two partiesinvolved (workers and firms).

3 Search models are a natural theoretical framework to modelwage rigidity because the Coase theorem applies

4 But here the Coase theorem is violated. Firms and workersleave some unexploited gains on the table. There are noexternalities and firms and workers know that their netsurplus would increase if they were to sign a wage contractwhere wages are procyclical

5 Why don’t they do it? What is the friction? This is a bitunsatisfactory.

,

Why wage rigidity?

1 In search models wages are just a way of splitting the surplusgenerated by employment relations

2 How this surplus is split is irrelevant and it has no welfareconsequences from the point of view of the two partiesinvolved (workers and firms).

3 Search models are a natural theoretical framework to modelwage rigidity because the Coase theorem applies

4 But here the Coase theorem is violated. Firms and workersleave some unexploited gains on the table. There are noexternalities and firms and workers know that their netsurplus would increase if they were to sign a wage contractwhere wages are procyclical

5 Why don’t they do it? What is the friction? This is a bitunsatisfactory.

,

The important question: Should wage decrease more inrecessions?

Three views about wages over the cycle

1 Neoclassical view Wages are set optimally

2 The firm supply financial friction view (this paper) Inrecessions wages should fall to boost financial capacity offinancially constrained firms. Workers as financiers.

3 The aggregate demand view In recession wages shouldincrease to boost labor income and to sustain aggregatedemand.

Implicit assumption: Propensity to consume out of laborincome is higher than out of capital income.

Which force dominates depends on whether firms or householdsare relatively more financially constrained in recessions.

Important policy relevant question

,

The important question: Should wage decrease more inrecessions?

Three views about wages over the cycle

1 Neoclassical view Wages are set optimally

2 The firm supply financial friction view (this paper) Inrecessions wages should fall to boost financial capacity offinancially constrained firms. Workers as financiers.

3 The aggregate demand view In recession wages shouldincrease to boost labor income and to sustain aggregatedemand.

Implicit assumption: Propensity to consume out of laborincome is higher than out of capital income.

Which force dominates depends on whether firms or householdsare relatively more financially constrained in recessions.

Important policy relevant question

,

The important question: Should wage decrease more inrecessions?

Three views about wages over the cycle

1 Neoclassical view Wages are set optimally

2 The firm supply financial friction view (this paper) Inrecessions wages should fall to boost financial capacity offinancially constrained firms. Workers as financiers.

3 The aggregate demand view In recession wages shouldincrease to boost labor income and to sustain aggregatedemand.

Implicit assumption: Propensity to consume out of laborincome is higher than out of capital income.

Which force dominates depends on whether firms or householdsare relatively more financially constrained in recessions.

Important policy relevant question

,

The important question: Should wage decrease more inrecessions?

Three views about wages over the cycle

1 Neoclassical view Wages are set optimally

2 The firm supply financial friction view (this paper) Inrecessions wages should fall to boost financial capacity offinancially constrained firms. Workers as financiers.

3 The aggregate demand view In recession wages shouldincrease to boost labor income and to sustain aggregatedemand.

Implicit assumption: Propensity to consume out of laborincome is higher than out of capital income.

Which force dominates depends on whether firms or householdsare relatively more financially constrained in recessions.

Important policy relevant question

,

The important question: Should wage decrease more inrecessions?

Three views about wages over the cycle

1 Neoclassical view Wages are set optimally

2 The firm supply financial friction view (this paper) Inrecessions wages should fall to boost financial capacity offinancially constrained firms. Workers as financiers.

3 The aggregate demand view In recession wages shouldincrease to boost labor income and to sustain aggregatedemand.

Implicit assumption: Propensity to consume out of laborincome is higher than out of capital income.

Which force dominates depends on whether firms or householdsare relatively more financially constrained in recessions.

Important policy relevant question

,

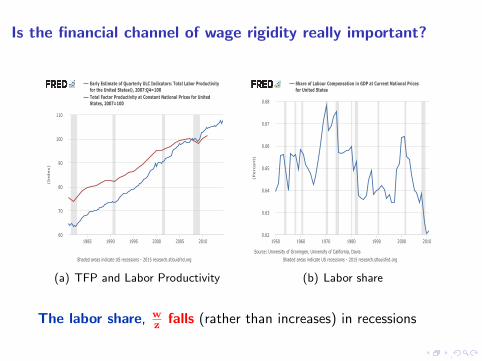

Is the financial channel of wage rigidity really important?

60

70

80

90

100

110

1985 1990 1995 2000 2005 2010

ShadedareasindicateUSrecessions-2015research.stlouisfed.org

EarlyEstimateofQuarterlyULCIndicators:TotalLaborProductivityfortheUnitedStates©,2007:Q4=100TotalFactorProductivityatConstantNationalPricesforUnitedStates,2007=100

(Index)

(a) TFP and Labor Productivity

0.62

0.63

0.64

0.65

0.66

0.67

0.68

1950 1960 1970 1980 1990 2000 2010

ShadedareasindicateUSrecessions-2015research.stlouisfed.org

Source:UniversityofGroningen,UniversityofCalifornia,Davis

ShareofLabourCompensationinGDPatCurrentNationalPricesforUnitedStates

(Percent)

(b) Labor share

The labor share, wz falls (rather than increases) in recessions

,

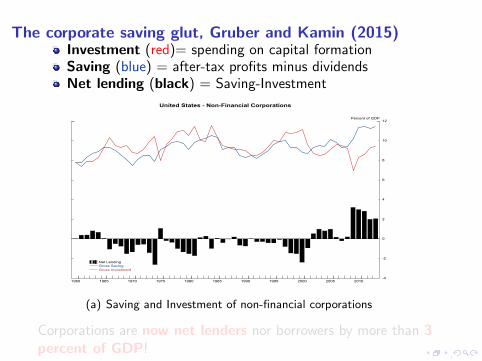

The corporate saving glut, Gruber and Kamin (2015)Investment (red)= spending on capital formationSaving (blue) = after-tax profits minus dividendsNet lending (black) = Saving-Investment

Figure 1

United States - Non-Financial Corporations

-4

-2

0

2

4

6

8

10

12

1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010

Percent of GDP

Net LendingGross SavingGross Investment

(a) Saving and Investment of non-financial corporations

Corporations are now net lenders nor borrowers by more than 3percent of GDP!

,

The corporate saving glut, Gruber and Kamin (2015)Investment (red)= spending on capital formationSaving (blue) = after-tax profits minus dividendsNet lending (black) = Saving-Investment

Figure 1

United States - Non-Financial Corporations

-4

-2

0

2

4

6

8

10

12

1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010

Percent of GDP

Net LendingGross SavingGross Investment

(a) Saving and Investment of non-financial corporations

Corporations are now net lenders nor borrowers by more than 3percent of GDP!

,

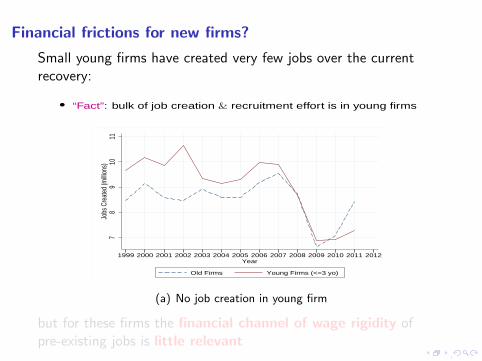

Financial frictions for new firms?

Small young firms have created very few jobs over the currentrecovery:Mechanism

• “Fact”: bulk of job creation & recruitment effort is in young firms7

89

1011

Jobs

Cre

ated

(milli

ons)

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012Year

Old Firms Young Firms (<=3 yo)

Gavazza-Mongey-Violante, ”What Shifts the Beveridge Curve?” p. 5 /14(a) No job creation in young firm

but for these firms the financial channel of wage rigidity ofpre-existing jobs is little relevant

,

Financial frictions for new firms?

Small young firms have created very few jobs over the currentrecovery:Mechanism

• “Fact”: bulk of job creation & recruitment effort is in young firms7

89

1011

Jobs

Cre

ated

(milli

ons)

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012Year

Old Firms Young Firms (<=3 yo)

Gavazza-Mongey-Violante, ”What Shifts the Beveridge Curve?” p. 5 /14(a) No job creation in young firm

but for these firms the financial channel of wage rigidity ofpre-existing jobs is little relevant

,

Household debt and Employment in the US

MSMSMSMSMSMSMSMSMSMSMSMSWVWVWVWVWVWVWVWVWVWVWVWVOKOKOKOKOKOKOKOKOKOKOKOK

LALALALALALALALALALALALA

NDNDNDNDNDNDNDNDNDNDNDND

WYWYWYWYWYWYWYWYWYWYWYWY

ARARARARARARARARARARARARKSKSKSKSKSKSKSKSKSKSKSKS

PAPAPAPAPAPAPAPAPAPAPAPAIAIAIAIAIAIAIAIAIAIAIAIATXTXTXTXTXTXTXTXTXTXTXTXNENENENENENENENENENENENE

KYKYKYKYKYKYKYKYKYKYKYKY

ALALALALALALALALALALALAL

MOMOMOMOMOMOMOMOMOMOMOMOWIWIWIWIWIWIWIWIWIWIWIWIOHOHOHOHOHOHOHOHOHOHOHOHININININININININININININ

TNTNTNTNTNTNTNTNTNTNTNTN

VTVTVTVTVTVTVTVTVTVTVTVT

SDSDSDSDSDSDSDSDSDSDSDSD

NYNYNYNYNYNYNYNYNYNYNYNY

CTCTCTCTCTCTCTCTCTCTCTCTMEMEMEMEMEMEMEMEMEMEMEME

SCSCSCSCSCSCSCSCSCSCSCSC

DCDCDCDCDCDCDCDCDCDCDCDC

MIMIMIMIMIMIMIMIMIMIMIMINMNMNMNMNMNMNMNMNMNMNMNM

MTMTMTMTMTMTMTMTMTMTMTMT

NCNCNCNCNCNCNCNCNCNCNCNC

ILILILILILILILILILILILILNJNJNJNJNJNJNJNJNJNJNJNJMAMAMAMAMAMAMAMAMAMAMAMANHNHNHNHNHNHNHNHNHNHNHNH

RIRIRIRIRIRIRIRIRIRIRIRI

DEDEDEDEDEDEDEDEDEDEDEDE

AKAKAKAKAKAKAKAKAKAKAKAK

MNMNMNMNMNMNMNMNMNMNMNMN

IDIDIDIDIDIDIDIDIDIDIDID

VAVAVAVAVAVAVAVAVAVAVAVA

GAGAGAGAGAGAGAGAGAGAGAGA

FLFLFLFLFLFLFLFLFLFLFLFL

ORORORORORORORORORORORORWAWAWAWAWAWAWAWAWAWAWAWA

MDMDMDMDMDMDMDMDMDMDMDMD

HIHIHIHIHIHIHIHIHIHIHIHI

COCOCOCOCOCOCOCOCOCOCOCOUTUTUTUTUTUTUTUTUTUTUTUT

AZAZAZAZAZAZAZAZAZAZAZAZ

NVNVNVNVNVNVNVNVNVNVNVNV

CACACACACACACACACACACACA

−.0

8−

.06

−.0

4−

.02

0L

og

−(W

)Ch

an

ge

in

Em

plo

ym

en

t o

ve

r 2

00

7−

20

09

.5 1 1.5 2Household Debt over Income in 2007

Correlation: −.73

Services

(a) Employment and debt

MSWV

OKLA

ND

WYARKS

PA

IATX

NEKYAL

MOWIOHINTNVT

SD

NYCT

ME

SC

DC

MI

NM

MTNC

ILNJMANH

RI

DE

AK

MN IDVA

GA

FL

ORWA

MD

HI

CO

UT

AZ

NV

CA

−.4

−.3

−.2

−.1

0.1

Log−

Change H

om

e P

rices 2

007−

2009

.5 1 1.5 2Household Debt over Income in 2007

Correlation: −.8

(b) Asset prices and debt

Household rather than firm debt seem to matter

,

Conclusions

Nice paper

Skeptical about the relevance of the mechanism in theaggregate at least in the US. I am not convinced thatreducing wages in recessions to boost financial capacity of USfirms is a good idea, at least in the current US GreatRecession. Because

1 Labor share has fallen rather than increased

2 It is unlikely that US corporations were financially constrained

3 Financial frictions might have played a role for newly createdfirms, but for these firms the channel is unlikely to be relevant

4 Substantial evidence that households were financiallyconstrained due to high pre-existing debt. In this casesustaining labor income is crucial to sustain consumption andaggregate demand.

5 If relevant, firms and workers should have negotiated andagreed on that

,

Conclusions

Nice paper

Skeptical about the relevance of the mechanism in theaggregate at least in the US. I am not convinced thatreducing wages in recessions to boost financial capacity of USfirms is a good idea, at least in the current US GreatRecession. Because

1 Labor share has fallen rather than increased

2 It is unlikely that US corporations were financially constrained

3 Financial frictions might have played a role for newly createdfirms, but for these firms the channel is unlikely to be relevant

4 Substantial evidence that households were financiallyconstrained due to high pre-existing debt. In this casesustaining labor income is crucial to sustain consumption andaggregate demand.

5 If relevant, firms and workers should have negotiated andagreed on that

,

Conclusions

Nice paper

Skeptical about the relevance of the mechanism in theaggregate at least in the US. I am not convinced thatreducing wages in recessions to boost financial capacity of USfirms is a good idea, at least in the current US GreatRecession. Because

1 Labor share has fallen rather than increased

2 It is unlikely that US corporations were financially constrained

3 Financial frictions might have played a role for newly createdfirms, but for these firms the channel is unlikely to be relevant

4 Substantial evidence that households were financiallyconstrained due to high pre-existing debt. In this casesustaining labor income is crucial to sustain consumption andaggregate demand.

5 If relevant, firms and workers should have negotiated andagreed on that

,

Conclusions

Nice paper

Skeptical about the relevance of the mechanism in theaggregate at least in the US. I am not convinced thatreducing wages in recessions to boost financial capacity of USfirms is a good idea, at least in the current US GreatRecession. Because

1 Labor share has fallen rather than increased

2 It is unlikely that US corporations were financially constrained

3 Financial frictions might have played a role for newly createdfirms, but for these firms the channel is unlikely to be relevant

4 Substantial evidence that households were financiallyconstrained due to high pre-existing debt. In this casesustaining labor income is crucial to sustain consumption andaggregate demand.

5 If relevant, firms and workers should have negotiated andagreed on that

,

Conclusions

Nice paper

Skeptical about the relevance of the mechanism in theaggregate at least in the US. I am not convinced thatreducing wages in recessions to boost financial capacity of USfirms is a good idea, at least in the current US GreatRecession. Because

1 Labor share has fallen rather than increased

2 It is unlikely that US corporations were financially constrained

3 Financial frictions might have played a role for newly createdfirms, but for these firms the channel is unlikely to be relevant

4 Substantial evidence that households were financiallyconstrained due to high pre-existing debt. In this casesustaining labor income is crucial to sustain consumption andaggregate demand.

5 If relevant, firms and workers should have negotiated andagreed on that

,

Conclusions

Nice paper

Skeptical about the relevance of the mechanism in theaggregate at least in the US. I am not convinced thatreducing wages in recessions to boost financial capacity of USfirms is a good idea, at least in the current US GreatRecession. Because

1 Labor share has fallen rather than increased

2 It is unlikely that US corporations were financially constrained

3 Financial frictions might have played a role for newly createdfirms, but for these firms the channel is unlikely to be relevant

4 Substantial evidence that households were financiallyconstrained due to high pre-existing debt. In this casesustaining labor income is crucial to sustain consumption andaggregate demand.

5 If relevant, firms and workers should have negotiated andagreed on that

,

Conclusions

Nice paper

Skeptical about the relevance of the mechanism in theaggregate at least in the US. I am not convinced thatreducing wages in recessions to boost financial capacity of USfirms is a good idea, at least in the current US GreatRecession. Because

1 Labor share has fallen rather than increased

2 It is unlikely that US corporations were financially constrained

3 Financial frictions might have played a role for newly createdfirms, but for these firms the channel is unlikely to be relevant

4 Substantial evidence that households were financiallyconstrained due to high pre-existing debt. In this casesustaining labor income is crucial to sustain consumption andaggregate demand.

5 If relevant, firms and workers should have negotiated andagreed on that

,

A topical question.....

so keep working on it!