Embed Size (px)

Citation preview

Injury Manual

Division 6 – Table of Contents 1

Division 6 - Table of Contents

Division 6 6.0 Permanent Impairment Benefits 6.1 Summary Information

6.1.1 Introduction to Permanent Impairment Benefits

What is a permanent impairment? Important Terms and Definitions Conceptual Framework

6.1.2 Summary of Division 6 Legislation

Summary of Section 152 - Permanent impairment benefit Summary of Section 153 - When beneficiary dies Summary of Section 154 - Evaluation of permanent impairment Summary of Section 155 - Calculation of lump sum benefit Summary of Section 155.1 - Interest on permanent impairment benefit 6.1.3 Summary of Part V Regulations Summary of Section 36 of the Regulations –

Compensation for permanent impairment based on Appendix B Summary of Section 37 of the Regulations - Evaluation of impairment to symmetrical parts of the body Summary of Section 38 of the Regulations - Application of section 37 Summary of Section 39 of the Regulations - Percentage fixed for deficit existing before the accident Summary of Section 40 of the Regulations - Computation of more than one permanent impairment Summary of Section 41 of the Regulations -

Section 40 not to be applied to percentage based on enhancement factor Summary of Section 42 of the Regulations -

Enhancement factor to be added after computation of combined value impairment rating Appendix B – Schedule of Permanent Impairments Appendix C – Combined Value Impairment Rating Table

6.2 Lump Sum Benefits

6.2.1 Calculation of lump sum benefits When permanent impairment is assessed and calculated

Timing of PI assessments and calculations Evaluation of permanent impairment Permanent impairment maximum benefit amounts Minimum permanent impairment benefit Customer to receive PI benefit amounts based on accident year How a permanent impairment calculation is completed When certain impairments are not in Appendix B Calculating Multiple Impairments

Combined Value Impairment Rating Table How to use the Combined Value Impairment Rating Table Examples

Injury Manual

Division 6 – Table of Contents 2

PI percentages with fractions Enhancement Factor

Evaluation of impairment to symmetrical parts of the body Enhancement factor does not apply to all areas of the body Applying the enhancement factor

6.2.2 Interim PI Payments and PJI Interim assessment and payment of PI at the one-year anniversary date

Preparing the file in advance of the one-year anniversary date If the customer is almost fully recovered nearing the one-year anniversary date

Estimated PI benefit paid at a rate of 60% Interest on permanent impairment benefit Calculation of the interim PI payment and PJI Decision letters not required on interim payments Preparing the file for an interim PI assessment 6.2.3 Final PI Payments and PJI Final assessment when customer is at maximum medical improvement

Final payment of PI for remaining balance Interest on permanent impairment benefit Calculation of final PI payment and PJI Overpayments not recovered Decision letter required on final PI payment Preparing the file for a final assessment of PI

6.2.4 Appendix B – Schedule of Permanent Impairments Use of Appendix B – Schedule of Permanent Impairments Conceptual Framework

Rating an Impairment Adding impairments within a subdivision Combined value impairment rating Non-facial disfigurement and scarring to be computed last using combined value rating Percentage within each subdivision or division rounded to nearest percentage

General information Important terms and definitions

6.2.5 Catastrophic Injury and Impairment Catastrophic permanent impairment When payment for catastrophic injury may be made Medical consultants to determine if customer sustained a catastrophic injury Maximum benefit amount for catastrophic PI Examples

6.2.6 When beneficiary dies When beneficiary dies When permanent impairment and death benefits are payable

Customer dies from accident-related injuries and PI has not already been paid Customer dies from cause unrelated to the accident and PI has not already been paid Customer dies from accident-related injuries and PI has already been paid

Injury Manual

Division 6 – Table of Contents 3

6.3 Permanent impairment policies, procedures, and information

6.3.1 Preparing a File for Assessment of PI Role of the medical consultant Medical consultant assessment reports When to assess permanent impairment

Interim PI payment and PJI at one-year anniversary date Final PI payment and PJI at MMI Medical information must demonstrate that the customer has reached MMI When to assess PI for scarring

Checklist for sending files to the medical consultants Information required to assess PI

Scarring Other permanent impairment Additional information that may be required in the assessment of permanent impairment

Scarring measurements and photographs Instructions for Customers Instructions for PIRs

Requesting scarring photos and measurements Range of Motion

How range of motion loss is measured When to request range of motion measurements Requesting range of motion measurements General instructions for using range of motion forms Instruction for PIRs upon receipt of range of motion forms

6.3.2 Processing a Lump Sum PI Payment Payment of permanent impairment procedure Using the appropriate guide letter Pro-rating permanent impairment Using the PI pro-rate calculator Payment to the Public Guardian and Trustee for minors or mentally incompetent adults

Public Guardian and Trustee contact information Correspondence with the Public Guardian and Trustee

If permanent impairment benefits are not payable

6.3.3 Denial of Permanent Impairment When permanent impairment benefits not payable Investigation of accident circumstances

Proving the customer is more than 50% at fault RCMP or Police Information Weather conditions Single-vehicle accidents Examples of evidence required to determine liability

Obtaining information immediately following the accident Blood Alcohol Concentration readings

Injury Manual

Division 6 – Table of Contents 4

Toxicology Analysis

Denial of permanent impairment based on evidence of impairment Toxicology analysis report Preparing the file for toxicology analysis Written requests for toxicology analysis should include Sample written request to forensic expert

Evidence required to deny coverage Information to obtain and document on file Denial of Coverage Procedure Appeals for denial of permanent impairment Sharing toxicology and blood alcohol concentration information

6.3.4 Other Related Policies, Procedures, and Information Information obtained at the time of the initial interview

Scarring information Other information

Baby teeth Corrective surgery for scarring Documenting concussion PI not subject to garnishment

Injury Manual

6.1.1 – Introduction to Permanent Impairment 1

6.1.1 Introduction to Permanent Impairment (6.1.1-01/2017)

Effective January 1, 2017

Purpose Provides a basic overview, summary and introduction to all permanent impairment (PI) concepts.

Act 152-155.1 Division 6 - Permanent Impairment Benefits

Regulations 36-42 Appendix B

Part VI – Permanent Impairment Benefits Schedule of Permanent Impairments

What is Permanent Impairment?

What is permanent impairment? Permanent impairment includes a permanent anatomical or physiological deficit, a permanent

disfigurement, a permanent acquired brain injury or any other prescribed permanent impairment (Act, ss 2(1)(gg)). ° A permanent impairment is not a disability.

° Impairment is considered permanent when a condition has reached maximum medical improvement

(MMI) and no further treatment will improve the condition.

° A permanent impairment is measurable.

° Permanent impairments are specifically described in Appendix B – Schedule of Permanent Impairments of the regulations.

° Pain does not form part of SGI’s assessment of a permanent impairment. Pain is subjective and cannot be validated or measured objectively.

° Soft tissue injuries (e.g., whiplash injuries) are not considered a permanent impairment.

Important Terms & Definitions

Important Terms and Definitions: Act: Permanent impairment includes a permanent anatomical or physiological deficit, a permanent

disfigurement, a permanent acquired brain injury or any other prescribed permanent impairment (Act, ss 2(1)(gg)).

Injury Manual

6.1.1 – Introduction to Permanent Impairment 2

Regulations: Catastrophic injury means (Regulations, ss 2(1)(c)): paraplegia or quadriplegia amputation resulting in two or more impairments total loss of functional vision resulting in an impairment of 80% or more of the entire visual system functional alteration of the brain (Division 2, Subdivision 1, Parts 4.6, 4.7, 4.8 of the Schedule of

Permanent Impairments) resulting in a combined impairment of 50% or more a total impairment of 80% or more calculated using the combined value impairment rating table based

on a combination of a list of specific permanent impairments Note: Please reference the regulations for further clarity and specificity with respect to the definition of a catastrophic injury and the application of Appendix B – Schedule of Permanent Impairments. Appendix B – Schedule of Permanent Impairments: Disability is defined as an alteration of an individual’s capacity to meet personal, social, or occupational

demands. While not all cases of impairment lead to disability, only in the case of impairment can disability develop. Disability usually refers to a specific activity or task the individual cannot accomplish. A disability arises out of the interaction between impairment and external requirements.

Impairment is defined as a loss, loss of use, or derangement of any body part, organ system, or organ function. A medical impairment can develop from an illness or injury.

Permanent impairment is an impairment that has become static or has stabilized during a period of time sufficient to allow optimal tissue repair and one that is unlikely to change significantly with further therapy. This time period is referred to as Maximum Medical Improvement (MMI). MMI does not preclude follow-up, maintenance or palliative care or an alteration of the medical condition with the passage of time.

Conceptual Framework

Conceptual Framework Rating an impairment: To rate impairment, it is necessary to weigh the relative functional importance of various structures of

the human body in relation to the function of the whole person. Through ad hoc proceedings, such values, expressed as a percentage of the whole person’s function, have been assigned to the various physical and psychological impairments with international acceptance. All impairment ratings listed in this manual are “whole person” impairments.

When calculating an impairment rating for an injured person who has more than one impairment, the following process must be used unless otherwise noted:

Adding impairments within a subdivision: ° When calculating an injured person’s total impairment rating, the impairments within each

Subdivision of a particular Division (or if a Division has no separate Subdivision, the impairments within the Parts of a Division) are added together first.

Injury Manual

6.1.1 – Introduction to Permanent Impairment 3

Combined value impairment rating:

° If a customer has more than one impairment, the percentage of the most severe impairment must be computed on the basis of 100% and the percentage of the other impairments, starting with the highest, must be computed in accordance with Appendix C. The percentage of an impairment pursuant to Division 12, Subdivision 2 (i.e., non-facial disfigurement and scarring), however, must be computed last.

Percentage within each subdivision or division rounded up to nearest percentage: ° Before using Appendix C, the percentage of impairment within each subdivision or Division must be

rounded up to the nearest percentage (subsection 40(3) of the regulations).

Injury Manual

6.1.2 – Summary of Division 6 Legislation 1

6.1.2 Summary of Division 6 Legislation (6.1.2-01/2017)

Effective January 1, 2017

Purpose Provides a detailed overview of the relevant sections of the Act pertaining to the administration of permanent impairment (PI) benefits.

Act 152-155.1 Division 6 – Permanent Impairment Benefits

Summary of Section 152

Permanent impairment benefit (Act, s 152): A customer who suffers a permanent impairment because of the accident is entitled to a lump-sum

benefit for the permanent impairment.

Summary of Section 153

When beneficiary dies (Act, s 153): A lump-sum benefit pursuant to this Division is not payable if the customer dies of a cause related to the

accident. If the customer dies of a cause unrelated to the accident and, on the date of his or her death, the

customer is suffering a permanent impairment arising out of the accident, SGI shall: ° Estimate the amount of the lump-sum benefit that it would have awarded to the customer respecting

the permanent impairment if the customer had not died; and ° Pay that lump-sum benefit to the customer’s estate.

Summary of Section 154

Evaluation of permanent impairment (Act, s 154): SGI shall evaluate a customer’s permanent impairment as a percentage that is determined on the basis

of the prescribed schedule of permanent impairments. If a customer’s permanent impairment is not listed on the prescribed schedule of permanent

impairments, SGI shall determine a percentage for the permanent impairment using the prescribed schedule as a guide.

Summary of Section 155

Calculation of lump-sum benefit (Act, s 155): If a customer suffers a permanent impairment, SGI shall calculate the lump-sum benefit in the manner

set out in this section. The amount of a lump-sum benefit is the amount PI calculated in accordance with the following formula:

PI = $192,561 x P

Where P is the percentage determined pursuant to section 154.

Injury Manual

6.1.2 – Summary of Division 6 Legislation 2

If the customer is determined to have suffered a permanent impairment that includes a catastrophic injury, the amount of the lump-sum benefit for a permanent impairment payable pursuant to this Division is the amount CPI calculated in accordance with the following formula:

CPI = $235,186 x P

Where P is the percentage determined pursuant to section 154.

The minimum amount of a lump-sum benefit for a permanent impairment pursuant to this section is

$770 (2016), and the maximum amount is: ° $192,561 (2016) for a customer who has suffered a permanent impairment; and ° $235,186 (2016) for a customer who has suffered a permanent impairment that includes a

catastrophic injury.

Note: All amounts shown above are in 2016 dollars. The base number to be used when performing these calculations is the benefit amount in place for the year in which the accident occurred.

Summary of Section 155.1

Interest on permanent impairment benefit (Act, s 155.1): SGI shall pay to the customer interest in accordance with the regulations on the amount of the

customer’s permanent impairment benefit computed from the day of the accident to the day on which the benefit is paid.

Injury Manual

6.1.3 – Summary of Part VI Regulations 1

6.1.3 Summary of Part VI Regulations (6.1.3-01/2017)

Effective January 1, 2017

Purpose Provides a detailed overview of the relevant sections of the regulations pertaining to the administration of permanent impairment (PI) benefits.

Regulations 36-42

Appendix B Appendix C

Part VI – Permanent Impairment Benefits Schedule of Permanent Impairments Combined Value Impairment Rating

Summary of Section 36 of the Regulations

Compensation for permanent impairment based on Appendix B (Regulations, s 36): Compensation for permanent impairments is to be determined on the basis of Appendix B.

Summary of Section 37 of the Regulations

Evaluation of impairment to symmetrical parts of the body (Regulations, s 37): Where a permanent anatomical or physiological deficit resulting from an accident impairs symmetrical

parts of the body, or impairs a part of the body that is symmetrical to a part of the body that was permanently impaired before the accident, the percentage of the permanent impairment for that deficit for the purposes of Division 6 of the Act is determined in accordance with the following formula:

P = PB + (TB x 0.25)

Where:

° P is the percentage to be used pursuant to Division 6 of the Act ° PB is the percentage attributed to the deficit arising from the accident ° TB is the total percentage of anatomical or physiological deficits impairing the more severely impaired

symmetrical part of the customer’s body

Summary of Section 38 of the Regulations

Application of section 37 (Regulations, s 38): Section 37 does not apply to an anatomical or physiological deficit that: ° affects an internal organ ° affects an organ controlling vision, balance or hearing ° results from an injury to the central nervous system

Summary of Section 39 of the Regulations

Percentage fixed for deficit existing before accident (Regulations, s 39): For the purposes of section 37, the percentage of an anatomical or physiological deficit existing before

an accident is to be determined using Appendix B or, if the anatomical or physiological deficit does not appear in Appendix B, by using Appendix B as a guideline.

Injury Manual

6.1.3 – Summary of Part VI Regulations 2

Summary of Section 40 of the Regulations

Computation of more than one permanent impairment (Regulations, s 40): In calculating the percentage of permanent impairment to be assigned to a customer who has more than

one impairment: ° The impairments within each subdivision of a particular Division in Appendix B are to be added

together; or

° If a Division in Appendix B has no separate subdivision, the impairments within the parts of a Division are to be added together.

If a customer has more than one impairment, the percentage of the most severe impairment must be

computed on the basis of 100% and the percentage of the other impairments, starting with the highest, must be computed in accordance with the Combined Value Impairment Rating Table as found in Appendix C.

For the purpose of combining more than one impairment, the percentage of an impairment pursuant to Division 12, Subdivision 2 (i.e., non-facial scarring or disfigurement) of the Schedule of Permanent Impairments must be computed last. Please note that this is an exception to the normal application of combined values according to Appendix C.

Before using the Combined Value Impairment Rating Table, SGI shall round up to the nearest percentage

of impairment within each subdivision or Division, as the case may be, to the nearest percentage.

Summary of Section 41 of the Regulations

Section 40 not to be applied to percentage based on enhancement factor (Regulations, s 41): Section 40 does not apply to the percentage obtained by applying the enhancement factor mentioned in

section 37.

Summary of Section 42 of the Regulations

Enhancement factor to be added after computation of combined value impairment rating (Regulations, s 42): Where sections 36 to 40 apply to a customer, the percentage resulting from the enhancement factor

mentioned in section 37 is added to the other percentages of deficits after the combined value impairment rating has been computed pursuant to section 40.

Appendix B Appendix B – Schedule of Permanent Impairments:

The prescribed schedule is found in the regulations under Appendix B – Schedule of Permanent Impairments. Appendix B is a detailed schedule of percentages for different areas of the body. The medical information on file is reviewed by medical consultants to provide an assessment of the customer’s permanent impairment. Note: Medical consultants who review customer medical files are physicians (i.e., licensed practitioners).

Injury Manual

6.1.3 – Summary of Part VI Regulations 3

Appendix C Combined Value Impairment Rating: The Combined Value Impairment Rating Table is used to combine two or more impairments if a person

has an impairment in more than one subdivision as set out in Appendix B. The values are derived from the formula:

A +[ B (1 – A)] = combined value of A and B

Where: A and B are the decimal equivalents of the impairment ratings.

In the chart all values are expressed as percentages. To combine any two impairment values, locate the larger of the values on the side of the chart and read along that row until you come to the column indicated by the smaller value at the bottom of the chart. At the intersection of the row and the column is the combined value.

Note: Please see Appendix C to view the Combined Value Impairment Rating Table.

Injury Manual

6.2.1 – Calculation of Lump Sum Benefits 1

6.2.1 Calculation of Lump Sum Benefits (6.2.1-01/2017)

Effective January 1, 2017

Purpose Provides a detailed overview of the Act, the regulations, and SGI’s policies and procedures with respect the assessment and calculation of a permanent impairment (PI) benefit

Act 152-155.1 Division 6 – Permanent Impairment Benefits

Regulations 36-42 Appendix B Appendix C

Part VI – Permanent Impairment Benefits Schedule of Permanent Impairments Combined Value Impairment Rating

When PI is assessed and calculated

When permanent impairment (PI) is assessed and calculated: A lump sum PI benefit is assessed when a customer suffers a permanent impairment because of the

accident. Timing of PI assessments and calculations: Interim PI payment and PJI at the one-year anniversary date - An interim assessment, calculation, and

payment of the customer’s PI benefit is completed on or about the one-year anniversary date of the accident including pre-judgment interest (PJI).

Final PI payment and PJI at Maximum medical improvement (MMI) - A final assessment, calculation,

and payment of the customer’s PI benefit is completed when the customer has reached MMI including pre-judgment interest.

Note: For additional information please see 6.2.2 – Interim PI Payments and PJI and 6.2.3 – Final PI Payments and PJI.

Evaluation of PI

Evaluation of permanent impairment (Act, s 154): SGI evaluates the customer’s permanent impairment as a percentage that is determined on the basis of

the prescribed schedule of permanent impairments (i.e., Appendix B).

If a customer’s permanent impairment is not listed on the prescribed schedule of permanent impairments, SGI shall determine a percentage for the permanent impairment using the prescribed schedule as a guide.

Injury Manual

6.2.1 – Calculation of Lump Sum Benefits 2

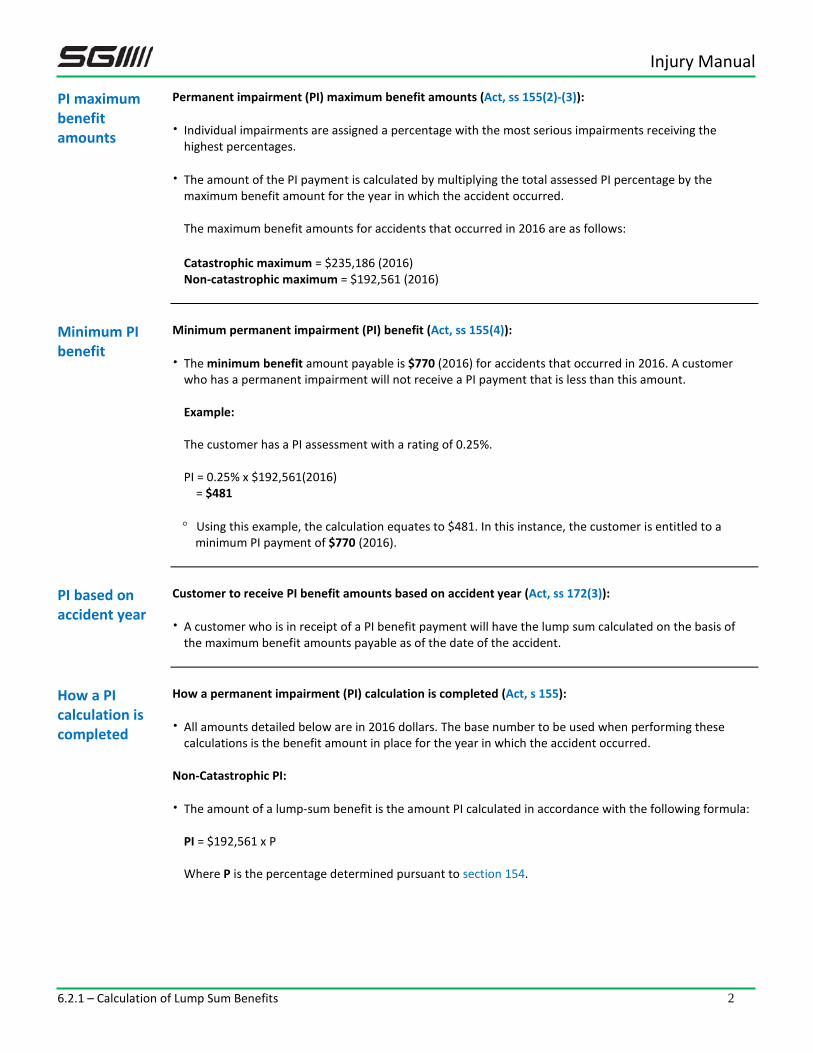

PI maximum benefit amounts

Permanent impairment (PI) maximum benefit amounts (Act, ss 155(2)-(3)): Individual impairments are assigned a percentage with the most serious impairments receiving the

highest percentages.

The amount of the PI payment is calculated by multiplying the total assessed PI percentage by the maximum benefit amount for the year in which the accident occurred. The maximum benefit amounts for accidents that occurred in 2016 are as follows:

Catastrophic maximum = $235,186 (2016) Non-catastrophic maximum = $192,561 (2016)

Minimum PI benefit

Minimum permanent impairment (PI) benefit (Act, ss 155(4)): The minimum benefit amount payable is $770 (2016) for accidents that occurred in 2016. A customer

who has a permanent impairment will not receive a PI payment that is less than this amount.

Example: The customer has a PI assessment with a rating of 0.25%.

PI = 0.25% x $192,561(2016) = $481

° Using this example, the calculation equates to $481. In this instance, the customer is entitled to a

minimum PI payment of $770 (2016).

PI based on accident year

Customer to receive PI benefit amounts based on accident year (Act, ss 172(3)):

A customer who is in receipt of a PI benefit payment will have the lump sum calculated on the basis of the maximum benefit amounts payable as of the date of the accident.

How a PI calculation is completed

How a permanent impairment (PI) calculation is completed (Act, s 155): All amounts detailed below are in 2016 dollars. The base number to be used when performing these

calculations is the benefit amount in place for the year in which the accident occurred. Non-Catastrophic PI: The amount of a lump-sum benefit is the amount PI calculated in accordance with the following formula:

PI = $192,561 x P

Where P is the percentage determined pursuant to section 154.

Injury Manual

6.2.1 – Calculation of Lump Sum Benefits 3

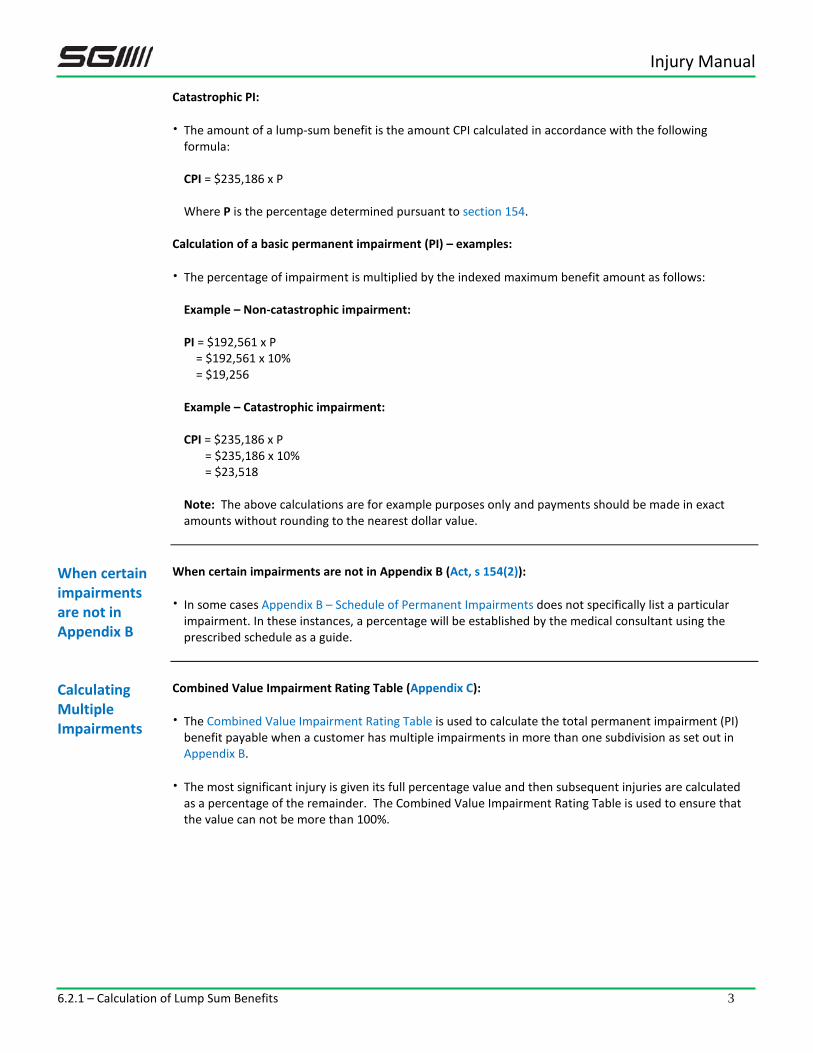

Catastrophic PI: The amount of a lump-sum benefit is the amount CPI calculated in accordance with the following

formula:

CPI = $235,186 x P

Where P is the percentage determined pursuant to section 154. Calculation of a basic permanent impairment (PI) – examples: The percentage of impairment is multiplied by the indexed maximum benefit amount as follows:

Example – Non-catastrophic impairment: PI = $192,561 x P = $192,561 x 10% = $19,256 Example – Catastrophic impairment: CPI = $235,186 x P = $235,186 x 10% = $23,518 Note: The above calculations are for example purposes only and payments should be made in exact amounts without rounding to the nearest dollar value.

When certain impairments are not in Appendix B

When certain impairments are not in Appendix B (Act, s 154(2)): In some cases Appendix B – Schedule of Permanent Impairments does not specifically list a particular

impairment. In these instances, a percentage will be established by the medical consultant using the prescribed schedule as a guide.

Calculating Multiple Impairments

Combined Value Impairment Rating Table (Appendix C): The Combined Value Impairment Rating Table is used to calculate the total permanent impairment (PI)

benefit payable when a customer has multiple impairments in more than one subdivision as set out in Appendix B.

The most significant injury is given its full percentage value and then subsequent injuries are calculated as a percentage of the remainder. The Combined Value Impairment Rating Table is used to ensure that the value can not be more than 100%.

Injury Manual

6.2.1 – Calculation of Lump Sum Benefits 4

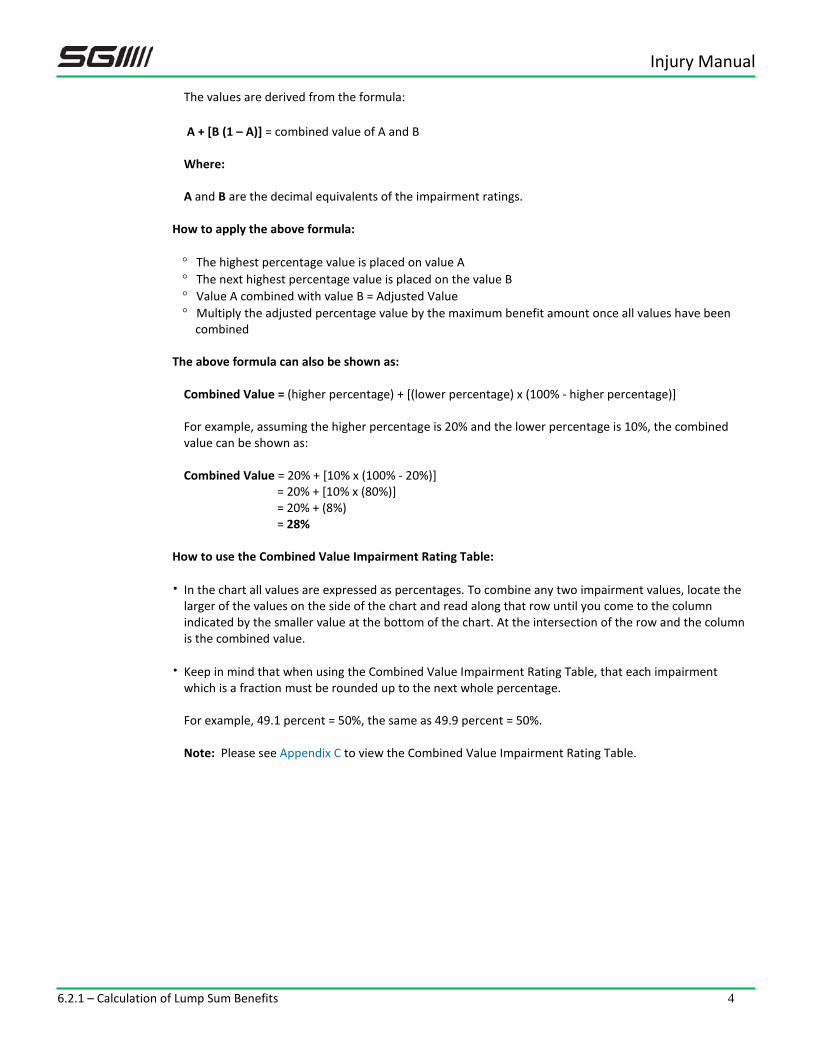

The values are derived from the formula:

A + [B (1 – A)] = combined value of A and B

Where:

A and B are the decimal equivalents of the impairment ratings. How to apply the above formula: ° The highest percentage value is placed on value A ° The next highest percentage value is placed on the value B ° Value A combined with value B = Adjusted Value ° Multiply the adjusted percentage value by the maximum benefit amount once all values have been

combined The above formula can also be shown as:

Combined Value = (higher percentage) + [(lower percentage) x (100% - higher percentage)]

For example, assuming the higher percentage is 20% and the lower percentage is 10%, the combined value can be shown as: Combined Value = 20% + [10% x (100% - 20%)] = 20% + [10% x (80%)] = 20% + (8%) = 28%

How to use the Combined Value Impairment Rating Table: In the chart all values are expressed as percentages. To combine any two impairment values, locate the

larger of the values on the side of the chart and read along that row until you come to the column indicated by the smaller value at the bottom of the chart. At the intersection of the row and the column is the combined value.

Keep in mind that when using the Combined Value Impairment Rating Table, that each impairment which is a fraction must be rounded up to the next whole percentage. For example, 49.1 percent = 50%, the same as 49.9 percent = 50%.

Note: Please see Appendix C to view the Combined Value Impairment Rating Table.

Injury Manual

6.2.1 – Calculation of Lump Sum Benefits 5

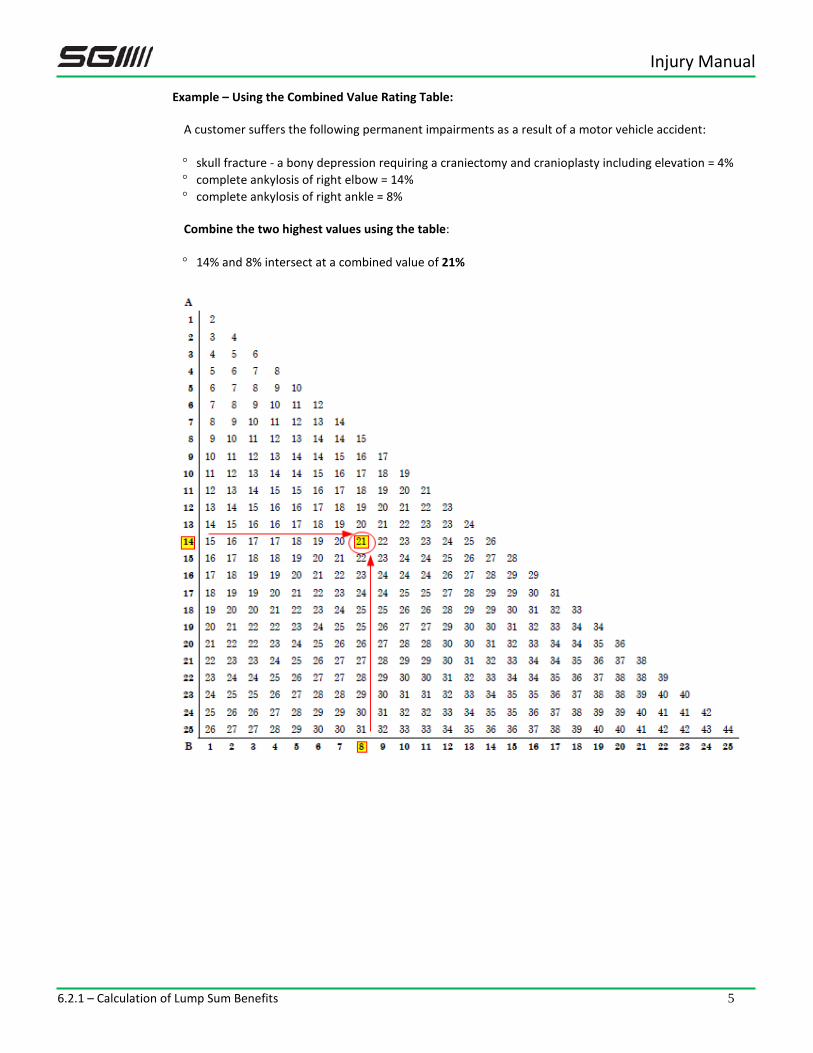

Example – Using the Combined Value Rating Table: A customer suffers the following permanent impairments as a result of a motor vehicle accident: ° skull fracture - a bony depression requiring a craniectomy and cranioplasty including elevation = 4% ° complete ankylosis of right elbow = 14% ° complete ankylosis of right ankle = 8%

Combine the two highest values using the table: ° 14% and 8% intersect at a combined value of 21%

Injury Manual

6.2.1 – Calculation of Lump Sum Benefits 6

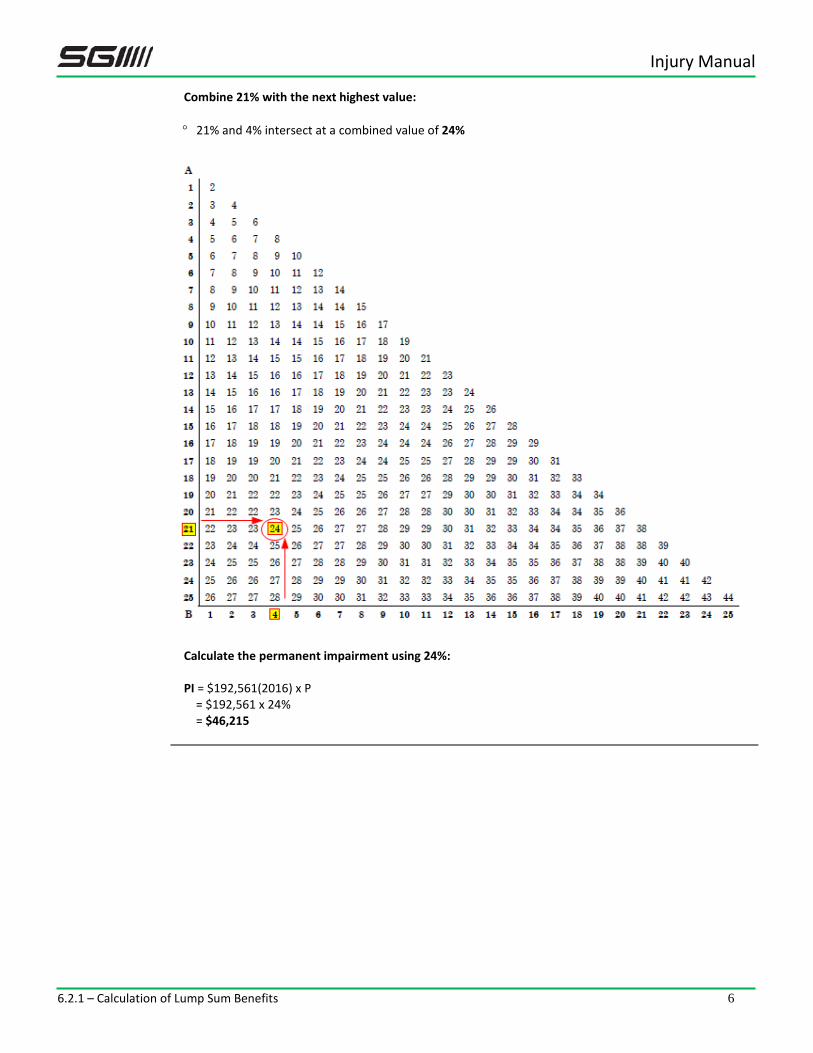

Combine 21% with the next highest value: ° 21% and 4% intersect at a combined value of 24%

Calculate the permanent impairment using 24%: PI = $192,561(2016) x P = $192,561 x 24% = $46,215

Injury Manual

6.2.1 – Calculation of Lump Sum Benefits 7

PI Percentages with Fractions

Permanent impairment (PI) percentages with fractions: Fractions of permanent impairment percentages are to be rounded up to the next whole percentage if

the customer has more than one impairment. In these instances, the Combined Value Rating Table is to be used.

Example - Rounding to the next whole percentage:

° 4.1% with 2% is rounded to 5% with 2%

Using the Combined Value Rating Table:

° When determining the total permanent impairment percentage, 5% and 2% intersect at a combined

value of 7%.

Calculating the PI benefit:

PI = 7% x $192,561(2016) = $13,479

Enhancement Factor

Enhancement Factor Evaluation of impairment to symmetrical parts of the body (Regulations, s 37): An enhancement factor is applied in instances where a permanent anatomical or physiological deficit

resulting from an accident impairs symmetrical parts of the body, or impairs a part of the body that is symmetrical to a part of the body that was permanently impaired before the accident.

Example: A customer may have an arm that was previously impaired due to a prior injury and now the function of the opposing arm has been affected by accident-related injuries.

Enhancement factor does not apply to all areas of the body (Regulations, s 38): The enhancement factor does not apply to all areas of the body and does not include an anatomical or

physiological deficit that: ° affects an internal organ ° affects an organ controlling vision, balance or hearing ° results from an injury to the central nervous system

The reason for this is that the enhancement factor for organs are built in to the method of calculating the alteration in function - in the case of impairment to the eyes, the entire visual system is affected, and that is what is measured in Appendix B. Deficits resulting from injury to the central nervous system already include considerations concerning how the impairment affects symmetrical parts of the body.

Injury Manual

6.2.1 – Calculation of Lump Sum Benefits 8

Applying the enhancement factor:

The percentage of the permanent impairment for that deficit for the purposes of Division 6 of the Act is determined in accordance with the following formula:

P = PB + (TB x 0.25)

Where:

° P is the percentage to be used pursuant to Division 6 of the Act ° PB is the percentage attributed to the deficit arising from the accident ° TB is the total percentage of anatomical or physiological deficits impairing the more severely impaired

symmetrical part of the customer’s body

Note: The enhancement factor (i.e., 0.25) is multiplied by the percentage attached to the most severe impairment, regardless of whether or not the most severe impairment existed prior to the accident.

Injury Manual

6.2.2 – Interim PI Payments and PJI 1

6.2.2 Interim PI Payments and PJI (6.2.2-01/2017)

Effective January 1, 2017

Purpose Provides a detailed explanation of SGI’s policies and procedures with respect to interim assessment and payment of permanent impairment (PI) and how pre-judgment interest (PJI) is applied.

Act 152

154 155 155.1

Permanent impairment benefit Evaluation of permanent impairment Calculation of lump sum benefit Interest on permanent impairment benefit

Regs 36-42 Part VI – Permanent Impairment Benefits

Interim assessment and payment of PI

Interim assessment and payment of PI at the one-year anniversary date: In the context of the unique facts of each customer’s file, an interim assessment and estimate of the

customer’s PI benefit is to be completed at or around the one-year anniversary date of the accident, with the interim payment of the customer’s lump sum PI benefit being issued as close as possible to the one-year anniversary date of the accident.

Preparing the file in advance of one-year anniversary date: The process of collecting medical information and preparing the customer’s file for review by the

medical consultants should start at approximately 10 months following the date of the accident.

The same procedures are to be followed when collecting medical information for both the interim assessment and the final assessment of the customer PI benefit.

If the customer is almost fully recovered nearing the one-year anniversary date:

If the customer is almost fully recovered or it is anticipated that full recovery will be achieved at or near

the one-year anniversary date of the accident, completing the assessment of the customer’s PI benefit can be delayed until the customer is at maximum medical improvement (MMI). Note: Consult with the PIR III or Adjuster III for direction in these circumstances and for assistance with making a decision whether to proceed with the interim assessment of the customer’s PI benefit.

Estimated PI benefit paid at 60%

Estimated PI benefit paid at a rate of 60%: The estimated PI benefit based on the medical consultant’s interim assessment report is to be paid at a

rate of 60%. This is to ensure that PI is accurately calculated, allowing provision for recovery between the interim calculation of PI and the final calculation of PI. To determine the amount of the interim payment, multiply the estimated PI benefit by 60%:

Interim PI payment = Estimated PI x 60%

Injury Manual

6.2.2 – Interim PI Payments and PJI 2

Interest on PI Interest on permanent impairment benefit (Act, s 155.1): SGI shall pay to the customer interest in accordance with the regulations on the amount of the

customer’s permanent impairment benefit computed from the day of the accident to the day on which the benefit is paid.

Calculation of interim PI payment and PJI

Calculation of the interim PI payment and pre-judgment interest (PJI): The calculation of the customer’s interim PI payment is completed in three steps as detailed below and

is to be completed using the PJI calculator which will automatically calculate the PJI payable for the period of time specified.

This can be shown as: 1. Interim PI payment = Estimated PI x 60% 2. PJI payment = Interim PI payment x PJI 3. Payment amount = Interim PI payment + PJI Payable

Example: If the estimated PI is equal to $100,000 the calculation of the interim PI payment and PJI would be as follows:

Interim PI payment

= Estimated PI x 60% = $100,000 x 60% = $60,000

PJI payment

= Interim PI payment x PJI = $60,000 x 1% = $600

Payment amount

= Interim PI payment + PJI payment = $60,000 + $600 = $60,600

Note: The above is a simplified example and is only intended to illustrate concepts concerning the administration of the interim PI payment and PJI on or about one-year anniversary date of the accident.

Injury Manual

6.2.2 – Interim PI Payments and PJI 3

Decision letters not required

Decision letters not required on interim payments: An informational letter is to be provided to the customer explaining the basis of the interim PI payment

and any prejudgment interest (PJI).

A decision letter is not required to accompany an interim payment as this payment is made by policy and is not a requirement under the Act. A decision letter is only provided to the customer upon issuing the customer’s final PI payment.

Provide an informational letter upon issuing the customer’s interim PI payment detailing the following

information: ° the interim PI payment ° the maximum benefit amount to be applied based on the accident year ° a copy of the medical consultant’s report ° the amount of the PJI paid

Note: Ensure to discuss the details of the interim payment and rationale for the payment with the customer.

Procedure Preparing the file for a interim assessment and payment of PI:

1. Request the required medical information and documentation required to assess PI:

Where applicable, request the required medical information, including: ° scarring information (i.e., photos and measurements) ° range of motion measurements

Follow the procedures outlined in 6.3.1 – Preparing a File for Assessment of PI. 2. Complete a Request for Review when sending the file to the medical consultants: Ensure to indicate in your request to the medical consultant that the file requires an assessment and

estimate for the interim payment of the customer’s permanent impairment. Once the medical consultant’s PI assessment report has been received, follow the procedures outlined in

6.3.2 – Processing a Lump Sum PI Payment.

Injury Manual

6.2.3 – Final PI Payments and PJI 1

6.2.3 Final PI Payments and PJI (6.2.3-01/2017)

Effective January 1, 2017

Purpose Provides a detailed explanation of SGI’s policies and procedures with respect to final assessment and payment of permanent impairment (PI) and how pre-judgment interest (PJI) is applied.

Act 152

154 155 155.1

Permanent impairment benefit Evaluation of permanent impairment Calculation of lump sum benefit Interest on permanent impairment benefit

Regulations 36-42 Part VI – Permanent Impairment Benefits

Final assessment and payment of PI

Final assessment when customer is at maximum medical improvement (MMI): The final assessment of the customer’s PI is completed once the customer reaches maximum medical

improvement (MMI). Final payment of PI for remaining balance: Once the medical consultant’s final assessment of the customer’s PI is complete, payment is made for

the balance owing to the customer (i.e., the difference between the final PI and the interim payment).

PJI from date of accident to date of payment

Interest on permanent impairment benefit (Act, s 155.1): SGI shall pay to the customer interest in accordance with the regulations on the amount of the

customer’s permanent impairment benefit computed from the day of the accident to the day on which the benefit is paid.

Calculation of final PI payment and PJI

Calculation of the final PI payment and PJI: The calculation of the customer’s final PI payment is completed in three steps as detailed below and is to

be completed using the PJI calculator which will automatically calculate the PJI payable for the period of time specified.

This can be shown as: 1. Final PI payment = final PI - interim PI payment 2. PJI payment = final PI payment x PJI 3. Payment amount = final PI payment + PJI payment

Injury Manual

6.2.3 – Final PI Payments and PJI 2

Example: If the interim PI payment (i.e., prior to PJI being applied) was $60,000 and the final assessed PI is $100,000, the calculation of the final PI payment and PJI would be as follows: Final PI payment

= final PI - interim PI payment = $100,000 - $60,000 = $40,000

PJI payment

= final PI payment x PJI = $40,000 x 1% = $400

Payment amount

= final PI payment + PJI payment = $40,000 + $400 = $40,400

Note: The above is a simplified example and is only intended to illustrate concepts concerning the administration of the final PI payment and PJI.

Overpayments not recovered

Overpayments not recovered: In the event that SGI has overpaid the customer based on the interim assessment report and estimated

PI, SGI does not recover the amount of any PI overpayment resulting from SGI’s interim assessment.

If SGI’s interim PI assessment exceeds the final PI assessment, SGI will not recover the overpayment; however, a written decision letter outlining the details of the customer’s final PI assessment is required.

Decision letter required

Decision letter required on final PI payment: A decision letter must be provided to the customer upon issuing the customer’s final PI payment

detailing the following information: ° the final assessed PI percentage ° the maximum benefit amount to be applied based on the accident year ° the amount of the interim PI payment previously paid ° the amount of the final assessed PI ° the amount of the final PI payment ° the amount of the PJI paid

Injury Manual

6.2.3 – Final PI Payments and PJI 3

Procedure Preparing the file for a final assessment of PI: 1. Request the required medical information and documentation required to assess PI:

Where applicable, request the required medical information including: ° scarring information (i.e., photos and measurements) ° range of motion measurements

Follow the procedures outlined in 6.3.1 – Preparing a File for Assessment of PI. 2. Complete a Request for Review when sending the file to the medical consultants: Ensure to indicate in your request to the medical consultant that the file requires a final assessment of

the customer’s permanent impairment. Once the medical consultant’s PI assessment report has been received, follow the procedures outlined in

6.3.2 – Processing a Lump Sum PI Payment.

Injury Manual

6.2.4 – Appendix B – Schedule of Permanent Impairments 1

6.2.4 Appendix B – Schedule of Permanent Impairments (6.2.4-01/2017)

Effective January 1, 2017

Purpose Provides general information concerning the application of Appendix B – Schedule of Permanent Impairments.

Regulations Appendix B Schedule of Permanent Impairments

Use of Appendix B

Use of Appendix B – Schedule of Permanent Impairments: Appendix B is used by SGI’s medical consultants when assessing a permanent impairment (PI)

percentage for a customer who suffers an impairment because of the accident. The percentage assessed by the medical consultant using Appendix B determines the customer’s entitlement and is used to calculate a lump sum PI benefit.

Note: Medical consultants who review customer medical files are physicians (i.e., licensed practitioners).

Conceptual Framework

Conceptual Framework Rating an impairment: To rate impairment, it is necessary to weigh the relative functional importance of various structures of

the human body in relation to the function of the whole person. Through ad hoc proceedings, such values, expressed as a percentage of the whole person’s function, have been assigned to the various physical and psychological impairments with international acceptance. All impairment ratings listed in this manual are “whole person” impairments.

When calculating an impairment rating for an injured customer who has more than one impairment, the following process must be used unless otherwise noted: Adding impairments within a subdivision: ° When calculating an injured customer’s total impairment rating, the impairments within each

Subdivision of a particular Division (or if a Division has no separate Subdivision, the impairments within the Parts of a Division) are added together first.

Combined value impairment rating:

° If a customer has more than one impairment, the percentage of the most severe impairment must be computed on the basis of 100% and the percentage of the other impairments, starting with the highest, must be computed in accordance with Appendix C. The percentage of an impairment pursuant to Division 12, Subdivision 2 (i.e., non-facial disfigurement and scarring), however, must be computed last.

Percentage within each subdivision or division rounded to nearest percentage: ° Before using Appendix C, the percentage of impairment within each subdivision or Division must be

rounded up to the nearest percentage.

Injury Manual

6.2.4 – Appendix B – Schedule of Permanent Impairments 2

General information

General information: Appendix B – Schedule of Permanent Impairments outlines numerous types of anatomical and

physiological deficits, as well as disfigurements and scarring for different areas of the body. The PI schedule is broken down by division according to individual areas or systems of the body and each

division is further broken down into subdivisions.

Each subdivision lists the individual impairments with a corresponding percentage (i.e., rating) based on the severity of the impairment.

The PI schedule is broken down and organized into the following divisions: Division 1: Musculoskeletal system Division 2: Central and peripheral nervous system Division 3: Maxillofacial system Division 4: Vision Division 5: Urogenital system and fetus Division 6: Respiratory system Division 7: The digestive tract system Division 8: Cardiovascular system Division 9: Endocrine system Division 10: The hematopoietic system Division 11: Vestibulocochlear apparatus Division 12: Skin

Note: Please see Appendix B – Schedule of Permanent Impairments in the regulations for additional detail with respect to the subdivisions and individual impairment ratings.

Important terms and definitions

Important terms and definitions: Disability is defined as an alteration of an individual’s capacity to meet personal, social, or occupational

demands. While not all cases of impairment lead to disability, only in the case of impairment can disability develop. Disability usually refers to a specific activity or task the individual cannot accomplish. A disability arises out of the interaction between impairment and external requirements.

Impairment is defined as a loss, loss of use, or derangement of any body part, organ system, or organ function. A medical impairment can develop from an illness or injury.

Permanent impairment is an impairment that has become static or has stabilized during a period of time sufficient to allow optimal tissue repair and one that is unlikely to change significantly with further therapy. This time period is referred to as Maximum Medical Improvement (MMI). MMI does not preclude follow-up, maintenance or palliative care or an alteration of the medical condition with the passage of time.

Note: For additional definitions contained in Appendix B – Schedule of Permanent Impairments, please reference definitions found at the beginning of each division.

Injury Manual

6.2.5 – Catastrophic Injury and Impairment 1

6.2.5 Catastrophic Injury and Impairment (6.2.5-01/2017)

Effective January 1, 2017

Purpose Provides an overview of the Act, the regulations, and SGI’s policies and procedures with respect to catastrophic injuries and impairment.

Act 152

154 155 173

Permanent impairment benefit Evaluation of permanent impairment Calculation of lump sum benefit When payment for catastrophic injury may be made

Regulations 2(1)(c) 36-42 Appendix B

Definition of catastrophic injury Part VI – Permanent Impairment Benefits Schedule of Permanent Impairment Benefits

Catastrophic PI Catastrophic Permanent Impairment (PI):

In order to qualify for the catastrophic PI benefit, the customer must fall within the definition of

catastrophic injury. Catastrophic injury means (Regulations, ss 2(1)(c)): paraplegia or quadriplegia amputation resulting in two or more impairments total loss of functional vision resulting in an impairment of 80% or more of the entire visual system functional alteration of the brain (Division 2, Subdivision 1, Parts 4.6, 4.7, 4.8 of the Schedule of

Permanent Impairments) resulting in a combined impairment of 50% or more a total impairment of 80% or more calculated using the combined value impairment rating table based

on a combination of a list of specific permanent impairments Note: Please reference the regulations for further clarity and specificity with respect to the definition of a catastrophic injury and the application of Appendix B – Schedule of Permanent Impairments.

Payment for Catastrophic Injury

When payment for catastrophic injury may be made (Act, s 173): If the nature of a customer’s injury prevents SGI from determining if the customer suffered a

catastrophic injury at the date of the accident, SGI is not obligated to pay the customer benefits on the basis of a catastrophic injury until the medical information indicates that the customer suffered a catastrophic injury.

When the medical information indicates that a customer suffered a catastrophic injury, SGI shall, if applicable:

° Pay benefits to the customer on the basis of a catastrophic injury; and ° Pay to the customer any additional benefit that would have been paid to him or her as if the

catastrophic injury assessment was made at the date of the accident together with interest pursuant to section 210.

Note: This section also has application to the payment of Division 4 – Income Replacement Benefits and Division 6 – Permanent Impairment Benefits for a customer who suffers a catastrophic injury.

Injury Manual

6.2.5 – Catastrophic Injury and Impairment 2

For additional information please see the following sections of the Act: Section 115 – IRB for catastrophic injury; Subsection 123(5) – IRB after studies for students with catastrophic injury; and Subsection 172(2) – Benefits payable from the first day after the accident for catastrophic injury.

Medical consultants review

Medical consultants to determine if customer sustained a catastrophic injury: The medical consultants will determine whether a customer has been catastrophically injured as a result

of a motor vehicle accident in accordance with the regulations. In some cases it will be clear that the customer meets this definition, while in other cases it will take longer to make a determination. For example, if the customer is a quadriplegic from the motor vehicle accident, the medical consultant will be able to readily determine that the customer has suffered a catastrophic injury. If however, the customer sustained a brain injury, it may take more time to determine whether the brain injury falls within the definition of catastrophic injury pursuant to subsection 2(1)(c)(iv) of the regulations.

In order to pay a catastrophic permanent impairment benefit injuries sustained must fall within the definition of catastrophic injury.

Maximum benefit amount

Maximum benefit amount for catastrophic PI: Once the medical consultant has determined that the customer sustained a catastrophic injury, the

customer will be entitled to a PI benefit based on a higher maximum benefit amount. The maximum benefit amount for accidents that occurred in 2016 is as follows:

Catastrophic PI - $235,186 (2016)

Examples Example 1:

A customer receives the following PI ratings: 65% - amputation of right arm 45% - brain injury (as defined in subsection 2(1)(c)(iv) of the regulations) Using the Combined Value Impairment Rating Table: ° Combine 65% with 45% = 81%

Calculating the PI benefit:

PI = 81% x $235,186(2016)

= $190,501

Note: This customer would qualify under the definition of catastrophic injury (subsection 2(1)(c)(v) of the regulations) with a combination of impairments of 80% or more.

Injury Manual

6.2.5 – Catastrophic Injury and Impairment 3

Example 2: (note the difference) A customer receives the following PI ratings: 65% - amputation of right arm 45% - scarring (legs) Using the Combined Value Impairment Rating Table: ° Combine 65% with 45% = 81%

Calculating the PI benefit:

PI = 81% x $192,561(2016)

= $155,974 Note: Scarring is not considered within the definition of catastrophic injury and impairment resulting in the customer receiving the non-catastrophic maximum of $192,561 (2016) the customer should be paid based on the non- catastrophic maximum of $192,561 (2016).

Injury Manual

6.2.6 – When Beneficiary Dies 1

6.2.6 When Beneficiary Dies (6.2.6-01/2017)

Effective January 1, 2017

Purpose Provides information on the Act, and SGI’s policies and procedures with respect to when a beneficiary dies in relation to permanent impairment (PI).

Act 153 When beneficiary dies

When beneficiary dies

When beneficiary dies (Act, s 153): A lump-sum benefit pursuant to this Division is not payable if the customer dies of a cause related to the

accident. If the customer dies of a cause unrelated to the accident and, on the date of his or her death, the

customer is suffering a permanent impairment arising out of the accident, SGI shall: ° Estimate the amount of the lump-sum benefit that it would have awarded to the customer respecting

the permanent impairment if the customer had not died; and ° Pay that lump-sum benefit to the customer’s estate.

When PI and death benefits are payable

When permanent impairment and death benefits are payable: Permanent Impairment benefits are distinct from death benefits. Permanent impairment is payable to a

customer to compensate them for a permanent physical or mental impairment and scarring or disfigurement from the accident, whereas death benefits are payable to the deceased’s family.

Customer dies from accident-related injuries and PI has not already been paid: If a customer dies from accident-related injuries and a permanent impairment benefit has not already

been paid, the benefit is not payable following their death. In these cases, only death benefits are payable.

Example: A customer suffers a severe brain injury resulting in death 45 days after the accident. SGI would not pay any permanent impairment benefits, but would pay death benefits.

Customer dies from cause unrelated to the accident and PI has not already been paid: Should the injured customer die from a cause unrelated to the accident, the lump sum permanent

impairment benefit will be paid to the injured person's estate. If the death is not accident related, the permanent impairment benefit is based on an estimate from the medical information available.

Injury Manual

6.2.6 – When Beneficiary Dies 2

Example: A customer sustains several lacerations as a result of being hit as a pedestrian. These lacerations cause permanent scarring. Four months following the motor vehicle accident the pedestrian dies of a heart attack unrelated to the accident. SGI would still assess what permanent impairment would have been paid for scarring and pay this amount to the estate.

Customer dies from accident-related injuries and PI has already been paid: If a customer dies from accident-related injuries and a permanent impairment benefit has already been

paid, death benefits are payable in addition to these amounts. In these cases, death benefits are calculated in the normal manner and are paid in full.

Injury Manual

6.3.1 – Preparing a File for Assessment of PI 1

6.3.1 Preparing a File for Assessment of Permanent Impairment (6.3.1-01/2017)

Effective January 1, 2017

Purpose Provides a detailed explanation of SGI’s policies and procedures with respect to preparing a customer’s claim file for assessment of permanent impairment (PI).

Act 154 Evaluation of permanent impairment

Regulations 36-42 Permanent Impairment Benefits

Role of the medical consultant

Role of the medical consultant: The medical consultant will assess the extent of an impairment and the entitlement to No Fault benefits

is assessed by the Personal Injury Representative (PIR). It is the PIR's responsibility to recognize and monitor cases where such payments may be required.

These decisions will not be made without having the permanent impairment (PI) assessed by a medical consultant. The consultant's role is not to make the decision, but to assess the extent of the PI.

Medical consultant assessment reports

Medical consultant assessment reports: The medical consultant’s report should accompany the written decision letter to the customer detailing

their entitlement to a PI benefit. Although the medical consultant’s reports are prepared for the PIRs to assist with adjudication of the

file, the PI assessment report is considered part of the medical file and is to be medically indexed.

When to Assess PI

When to assess permanent impairment (PI): Interim PI payment and PJI at the one-year anniversary date - An interim assessment, calculation, and

payment of the customer’s PI benefit is completed on or about the one-year anniversary date of the accident including pre-judgment interest (PJI).

Final PI payment and PJI at Maximum medical improvement (MMI) - A final assessment, calculation,

and payment of the customer’s PI benefit is completed when the customer has reached MMI including pre-judgment interest.

Note: For additional information please see 6.2.2 – Interim PI Payments and PJI and 6.2.3 – Final PI Payments and PJI. Medical information must demonstrate that the customer has reached MMI: In order to proceed with the final assessment and payment of permanent impairment (PI) benefits, the

medical information on file must demonstrate that the customer has reached maximum medical improvement (MMI).

Injury Manual

6.3.1 – Preparing a File for Assessment of PI 2

When to assess PI for scarring: If the customer has accident-related cuts, scrapes, lacerations, or surgical scarring, the scarring is to be

assessed: ° Approximately 10 months following the date of the accident for the interim assessment and payment

of PI; and

° Approximately 10 months from the date of the customer’s last accident-related surgery for the final assessment and payment of PI.

Note: Scarring requires a minimum of ten months for complete healing and maturation of the scar tissue.

Checklist for sending files to the medical consultants

Checklist for sending files to the medical consultants: Complete a Request for Review by the medical consultants detailing the following information: a brief summary of the file accident circumstances a list of accident-related injuries a list of pre-existing conditions if permanent impairment (PI) has previously been assessed specific questions relating to the request for review any other additional information that is relevant to the medical consultant’s review of the file

Note: Ensure that you detail the specific nature of the request when asking questions of the medical consultants. You may ask the medical consultant medical questions (e.g., which injuries or impairments are causally related to the motor vehicle accident?), but do not ask adjudication questions of the consultants.

Information required to assess PI

Information required to assess PI: The following information must be provided to the medical consultant where applicable: Scarring: location of scar (i.e., exact location) clear photos that are labeled (i.e., area of the body and which side it is located on) detailed and accurate measurements in centimetres Other permanent impairment: measurements detailed on the Range of Motion Charts for the specific joint or area of the body; hospital records; ambulance reports (i.e., required to document a loss of consciousness);

Injury Manual

6.3.1 – Preparing a File for Assessment of PI 3

Additional information that may be required in the assessment of permanent impairment:

police reports; clinical notes; consultation reports; diagnostics testing results (e.g., MRI results); etc. Note: Range of motion measurements must be completed by a physiotherapist or occupational therapist.

Scarring measurements and photographs

Scarring measurements and photographs: Scarring photos and measurements should be taken approximately 10 months following the date of the

accident. Scarring for any skin injury requires at least ten months for complete healing and maturation of the scar. Any submissions of photographs and scar measurements less than 10 months following the date of the accident are considered premature and not at maximum medical improvement.

Instructions for customers Photo and measurement specifications: The photos must be high quality. Photos must be clear and have high resolution. The photo clearly identifies where the scar starts and stops. Each photo is labeled as to the specific anatomical part of the body. A centimetre ruler is place in each photo.

Additional information: ° If a digital camera is used – the photo must have the appropriate date. ° Photos should be taken close-up. ° Ensure the quality and resolution of the photo prior to submission. ° For facial scarring – A photo of the entire face and close-ups of the scar itself. ° For scarring of a limb – A photo of the entire limb and close-ups of the scar itself. ° For other areas of the body – A photo of the entire anatomical region and close-ups of the scar itself.

The Permanent Impairment Description form completed by the customer’s practitioner detailing: ° scar location ° scar description ° scar type ° scar length ° scar width

Instructions for PIRs upon receipt of photos: Digital photos - Save in JPEG or JPG format and upload photos to the attachments on the claim file. Printed photos - Make sure they are stapled to the form entitled Photo Sheet. All photo sheets should be

medically indexed and placed in the customer’s medical file. Photos must be labeled - Ensure that each photo is appropriately labeled.

Injury Manual

6.3.1 – Preparing a File for Assessment of PI 4

Procedure Requesting scarring photos and measurements: 1. Contact the customer to advise of them of the request: Contact the customer to advise them of the request for scarring photos and measurements used to

assess their eligibility for a permanent impairment (PI) benefit. Ensure to explain the process of assessing PI in detail.

2. Send a request for the required photos and scarring information: Send a written request to the customer for the scarring photos and measurements entitled PI-Scarring

Information Request. The letter provides detailed instructions to customers outlining the requirements for scarring photos and measurements with the Permanent Impairment Description Form attached.

Range of Motion

Range of Motion How range of motion loss is measured: Range of motion loss is evaluated by measuring active range of motion with the aid of a measuring

device (e.g., goniometer or inclinometer) according to standardized position and technique (Division 1, Appendix B).

When to request range of motion measurements: Range of motion measurements should be requested at the following times: ° At approximately 10 months following the date of the accident for the interim assessment and

payment of the customer’s PI benefit; and

° When the customer has reached maximum medical improvement (MMI) for the final assessment and payment of the customer’s PI benefit.

Requesting range of motion measurements: 1. Contact the customer to advise of them of the request: Contact the customer to advise them of the request for range of motion measurements used to assess

their eligibility for a permanent impairment (PI) benefit. Ensure to explain the process of assessing range of motion.

2. Send a request for the range of motion measurements: Send a written request to the customer for range of motion measurements entitled PI-

ROM/Disfigurement. The letter provides detailed instructions to customers outlining the requirements for range of motion measurements.

Injury Manual

6.3.1 – Preparing a File for Assessment of PI 5

3. Attach the appropriate range of motion chart to the request: Attach the appropriate range of motion chart to the request. The nature of the customer’s injuries will

determine which charts are required.

Range of motion charts are available for the following joints:

° shoulder ° wrist ° elbow

° thumb ° fingers ° hip

° knee ° ankle ° big toe

° temporomandibular joint

General instructions for using range of motion forms: The range of motion forms must be completed by a physiotherapist (PT) or occupational therapist (OT). The customer can choose the PT or OT to complete the form. Each form outlines the procedure for completion. The PT sends the form to SGI once complete along with their invoice. Instructions for PIRs upon receipt of range of motion forms: Review the form to ensure that it has been fully completed. If the form is not complete, contact the PT or OT who performed the measurements. Return the form to the PT or OT for completion. Process the payment for the range of motion form upon completion. Medically index the range of motion form and place in the customer’s medical file.

Injury Manual

6.3.2 – Processing a Lump Sum PI Payment 1

6.3.2 Processing a Lump Sum PI Payment (6.3.2-01/2017)

Effective January 1, 2017

Purpose Provides a detailed explanation of SGI’s policies and procedures with respect to the payment of permanent impairment (PI) benefits.

Act 152-155.1 Division 6 – Permanent Impairment Benefits

Regulations 36-42 Part VI – Permanent Impairment Benefits

Procedure Payment of permanent impairment (PI):

1. Review the medical consultant’s PI assessment report: Review the medical consultant’s report and the PI percentages (i.e., ratings) assigned to all impairments. Review the applicable sections of Appendix B – Schedule of Permanent Impairments that correspond to

the impairment ratings in the report and prepare copies for the customer. Ensure the report is attached to file, is medically indexed and placed in the customer’s medical file. 2. Prepare an informational letter or decision letter outlining the customer’s entitlement: Prepare an informational letter or written decision using the letter entitled PI-Benefit Explanation or PI-

Catastrophic outlining SGI’s decision with respect to the customer’s entitlement to a permanent impairment benefit. Note: Only an informational letter is required at the time of the interim assessment and payment of PI.

The letter must include:

° Details concerning the medical consultant’s review of the PI benefit. ° An overview of information that was reviewed to determine the amount of the PI benefit. ° The total PI percentage assessed as it applies to the maximum benefit amount. ° How the calculation of the PI benefit works. ° The total amount of the PI benefit payment. ° Reference to the appropriate sections of the Act and regulations where necessary. ° The appeal option, if issuing a decision letter.

The following information should accompany the written decision letter:

° a copy of the medical consultant’s assessment report ° a copy of the applicable sections of Appendix B – Schedule of Permanent Impairments ° the cheque issued to the customer for the amount of the lump sum PI benefit

Note: Use the appropriate guide letter to suit the payment of the customer’s PI benefit and modify the letter tailoring it to suit the customer’s circumstances.

3. Use the PI Pro-Rate Calculator: Use the PI Pro-rate Calculator to ensure that the correct amounts are apportioned for each type of

impairment. Please refer back to the section regarding pro-rating of permanent impairment.

Injury Manual

6.3.2 – Processing a Lump Sum PI Payment 2

4. Process the payment of the permanent impairment benefit: Process the payment of the customer’s benefit ensuring that the appropriate amounts are being paid for

each type of impairment, and redirect the cheque to the office to be enclosed with the customer’s decision letter.

The following information should be considered prior to making a payment for permanent impairment and should be documented in the approval note on the file: ° if the customer was the driver, passenger, or a pedestrian ° verification that coverage is in order (e.g., no charges for impairment) ° the loss year and maximum PI benefit amount being applied (e.g., $192,561 (2016)) ° a list of all areas of the body receiving a PI rating and corresponding percentages ° the corresponding sections of Appendix B for each impairment rating

5. Contact the customer to arrange a meeting: Contact the customer to arrange a meeting to fully explain SGI's decision regarding entitlement to, and

the payment of, the permanent impairment benefit.

Note: If the customer is unable to attend a meeting in person, the details of the lump sum PI benefit can be discussed over the phone.

6. Meet with the customer to explain the details of the permanent impairment benefit payment: If possible, meet in person with the customer to explain the details of the PI benefit payment; provide

them with the decision letter, and the lump sum PI benefit payment. Provide the customer with the following information:

° Details of the medical consultant’s review, including a copy of the assessment report. ° An overview of information that was reviewed to determine the amount of the PI benefit. ° A copy of the applicable sections of Appendix B – Schedule of Permanent Impairments. ° The total PI percentage assessed as it applies to the maximum benefit amount. ° How the lump sum PI benefit calculation works. ° The total amount of the lump sum PI benefit payment.

Summary of the above procedure: 1. Review the medical consultant’s PI assessment report. 2. Prepare a written decision letter outlining the customer’s entitlement. 3. Use the PI Pro-Rate Calculator. 4. Process the payment of the permanent impairment benefit. 5. Contact the customer to arrange a meeting. 6. Meet with the customer to explain the details of the permanent impairment benefit payment.

Injury Manual

6.3.2 – Processing a Lump Sum PI Payment 3

Using the appropriate guide letter

Using the appropriate guide letter: When issuing payment of the lump sum PI benefit the following guide letters should be used: PI – Benefit Explanation - Utilize this letter when your customer is over the age of 18 years and injuries

are non-catastrophic. PI – Benefit Minor-Advise Sent to Public Trustee - Send this letter to the parent or guardian of a

customer who is under 18 years of age as their PI benefit is paid in trust to the Public Guardian and Trustee.

PI – Catastrophic - Utilize this letter when your customer is over the age of 18 years and injuries are

catastrophic. PI – Catastrophic to Public Trustee - Utilize this letter when your customer is under the age of 18 years

and for adults who are mentally incompetent with respect to the handling of their own financial affairs and injuries are catastrophic.

PI – Explain Benefit to Public Trustee - Utilize this cover letter when you are paying PI benefit in trust to

the Public Guardian and Trustee. A copy of this letter should be sent to the parent or guardian of the minor or mentally incompetent adult, or their representative.

Pro-rating Pro-rating permanent impairment (PI):

When a PI payment involves multiple impairments, each individual impairment must be properly pro-

rated (i.e., apportioned) so that the appropriate amount is paid for each type of impairment. Example – Prorating PI:

The customers PI ratings are as follows: ° scarring 20% ° mild brain injury 10% ° loss of canine tooth 2% Total PI before using combined value rating table = 32%

Using the combined value rating table: ° Combine 20% with 10% = 28% ° Combine 28% with 2% = 29% Calculating the PI benefit: PI = 29% x $192,561(2016) = $55,843

Prorating the total payment amount using the original percentages: Scarring – 20% out of 32%: = 20/32 x $55,843 = $34,902 paid under Scarring

Injury Manual

6.3.2 – Processing a Lump Sum PI Payment 4

Mild brain injury – 10% out of 32%: = 10/32 x $55,843 = $17,451 paid under Mild Brain Injury

Loss of canine tooth – 2% out of 32% = 2/32 x $55,843 = $3,490 paid under Other

PI Pro-Rate Calculator

Using the PI pro-rate calculator: When pro-rating a permanent impairment benefit always use the PI-Pro-Rate Calculator to make pro-

rating easy and efficient. The following information must be entered into the form:

° if the lump sum PI payment is for catastrophic injuries ° the year that the accident occurred ° total percentage using combined values ° total percentage before using combined values and rounding ° all individual PI types ° all percentages corresponding to each type of PI before combined values

The PI Pro-Rate Calculator will automatically pro-rate and generate the appropriate values to be paid

under each type of impairment. Note: A copy of the finalized PI pro-calculation should accompany the lump-sum payment for approval.

Payment to the Public Guardian & Trustee

Payment to the Public Guardian and Trustee for minors or mentally incompetent adults: Payment of PI benefits to a minor or a mentally incompetent adult must be paid to the Public Guardian

and Trustee with the decision letter and payment attached. For example, a person for whom a certificate has been issued under The Public Guardian and Trustee Act or The Adult Guardianship and Co-Decision-Making Act, any PI benefit payments will be issued to the Public Guardian and Trustee.

Public Guardian and Trustee contact information:

Public Guardian and Trustee of Saskatchewan 1871 Smith Street Regina SK S4P 4W4 Phone: 306-787-5424

The Public Guardian and Trustee is mandated to receive funds for people under the age of 18 and adults

for whom the Public Guardian and Trustee has been appointed a property decision-maker.

Injury Manual

6.3.2 – Processing a Lump Sum PI Payment 5

Correspondence with the Public Guardian and Trustee: Advise the Public Guardian and Trustee's office in writing, indicating for whom the payment was made,

the amount, and the reasons for the payment using the cover letter entitled PI-Explain Benefit to Public Trustee.

If the Public Guardian and Trustee is providing instructions concerning the payment of benefits, SGI will

require a letter from that office detailing those payment instructions.

Issuing a payment in trust with cover letter: Include the following information in correspondence to the Public Guardian and Trustee: ° what the payment is for ° the name, address, and date of birth of the customer ° the name of the parent or legal guardian of the customer ° the contact person’s name, address, and telephone number where the minor or mentally incompetent

adult is currently residing ° a copy of the decision letter and medical consultant’s PI assessment report

If PI benefits are not payable

If permanent impairment (PI) benefits are not payable: If for some reason PI benefits are not payable (e.g., the impairment is not causally related to the motor

vehicle accident) after an assessment of the claim, apply the following: If payment is not in order:

° Contact the customer or arrange to meet with them to explain the rationale behind SGI’s decision. ° Document this discussion in your file notes. ° Send the customer a detailed decision letter outlining SGI’s decision. The decision letter must include:

° The reason(s) for SGI’s decision. ° Reference to the appropriate sections of the Act and regulations where necessary. ° The appeal option.

Injury Manual

6.3.3 – Denial of Permanent Impairment 1

6.3.3 Denial of Permanent Impairment (6.3.3-01/2017)

Effective January 1, 2017

Purpose Provides an explanation of the Act, and SGI’s policies and procedures with respect to the denial of permanent impairment when the customer is convicted of specified Criminal Code offences.

Act 175

177 When permanent impairment benefits not payable Beneficiary may appeal decision of insurer

When PI benefits not payable

When permanent impairment benefits not payable (Act, s 175) A customer is not entitled to any lump sum benefit for a permanent impairment pursuant to Division 6 to which the insured would otherwise be entitled if: 1. The customer is more than 50% responsible and was impaired: ° The customer is more than 50% responsible for the accident; and

The customer at the time of the accident: Was the operator, or had the care and control of a motor vehicle involved in the accident; and

Was under the influence of alcohol or drugs to such an extent that the insured was incapable for the

time being of having proper control of the motor vehicle; or 2. The customer is more than 50% responsible and is convicted: ° The customer has been convicted of a specified Criminal Code offence:

220 - The person’s criminal negligence causes death 221 - The person’s criminal negligence causes bodily harm 249.1(3) - Flight from a peace officer causes bodily harm or death 249.2 - The person’s criminal negligence causes death while street racing 249.3 - The person’s criminal negligence causes bodily harm while street racing 249.4 - Dangerous operation of a motor vehicle while street racing causes bodily harm or death 253(1)(a) - The person’s ability to operate the vehicle is impaired by alcohol or drug 253(1)(b) - The person’s blood alcohol content (BAC) exceeds the legal limit 254(5) - Failure or refusal to provide a sample without reasonable excuse 255(2) - Operation while impaired causing bodily harm 255(2.1) – BAC exceeds the legal limit, caused an accident resulting in bodily harm 255(2.2) – Failure or refusal to provide a sample, caused an accident resulting in bodily harm 255(3) – Operation while impaired causing the death 255(3.1) – BAC exceeds the legal limit, caused an accident resulting in death 255(3.2) – Failure or refusal to provide a sample, caused an accident resulting in death

Or an offence pursuant to a law of a state of the U.S. that is substantially similar to one of the offences noted above; or

Injury Manual

6.3.3 – Denial of Permanent Impairment 2