Embed Size (px)

Citation preview

DMA/Winterberry Group

Quarterly Business Review

Current Economic Trends in Direct and Digital Marketing

Second Quarter of 2013

2

About Direct Marketing Association (DMA) The Direct Marketing Association (www.the‐dma.org) is the world’s largest trade association dedicated to advancing and protecting responsible data‐driven marketing. Founded in 1917, DMA represents thousands of companies and nonprofit organizations that use and support data‐driven marketing practices and techniques. In 2012, marketers — commercial and nonprofit —will spend $168.5 billion on direct marketing, which accounts for 52.7 percent of all ad expenditures in the United States. Measured against total US sales, these advertising expenditures will generate approximately $2.05 trillion in incremental sales. In 2012, direct marketing accounts for 8.7 percent of total US gross domestic product and produces 1.3 million direct marketing employees in the US. Their collective sales efforts directly support 7.9 million other jobs, accounting for a total of 9.2 million US jobs. DMA Mission: To advance and protect responsible data‐driven marketing. All rights reserved. No part of this publication may be reproduced, stored in a retrieval system, or transmitted, in any form or by any means, electronic, mechanical, photocopying, recording, or otherwise without the prior written permission of the copyright owner.

DISCLAIMER: DMA does not make any warranties, express or implied, as to results to be obtained from the use of this report data. In no event shall DMA, its affiliates, or any other entity involved in providing the data herein have any liability for lost profits or for indirect, special, punitive, or consequential damages, or any liability to any third party arising out of the use of this data, even if advised of the possibility of such damages or liability. All disclaimers herein shall not be applicable to liability that cannot be waived under State or Federal law.

PRINTED IN THE UNITED STATES OF AMERICA

3

Winterberry Group is a unique strategic consulting firm that supports the growth of advertising, marketing, media and information organizations. Our services include: Corporate Strategy: The Opportunity Mapping strategic development process helps clients prioritize their available customer, channel and capability growth options, informed by a synthesis of market insights and intensive internal analysis. Market Intelligence: Comprehensive industry trend, vertical market and value chain research provides in‐depth analysis of customers, market developments and potential opportunities as a precursor to any growth or transaction strategy. Marketing System Optimization and Alignment: Process mapping, marketplace benchmarking and holistic system engineering efforts are grounded in deep industry insights and “real‐world” understandings—with a focus on helping advertisers, marketers and publishers better leverage their core assets. Mergers & Acquisitions Due Diligence Support Services: Company assessments and industry landscape reports provide insight into trends, forecasts and comparative transaction data needed for reliable financial model inputs, supporting the needs of strategic and financial acquirers to make informed investment decisions and lay the foundation for value‐focused ownership. For more information, please visit www.winterberrygroup.com.

4

Table of Contents

METHODOLOGY……………………………………..………………………………………………….……………….4

EXECUTIVE SUMMARY…………………………………………………………………………..…………….………5

I. DATA‐DRIVEN MARKETING (DDM) SPENDING………………………...……………….……….7

II. REVENUE GENERATED FROM DDM ACTIVITY……………………………………………………9

III. PROFITABILITY…………………………………………………………………………………………………11

IV. STAFFING…………………………………………………………………………………………………………13

V. MEDIA MIX AND ACTIVITY……………………………………………………………………………….15

VI. FACTORS AFFECTING DDM ACTIVITY……………………………………………………………….17

5

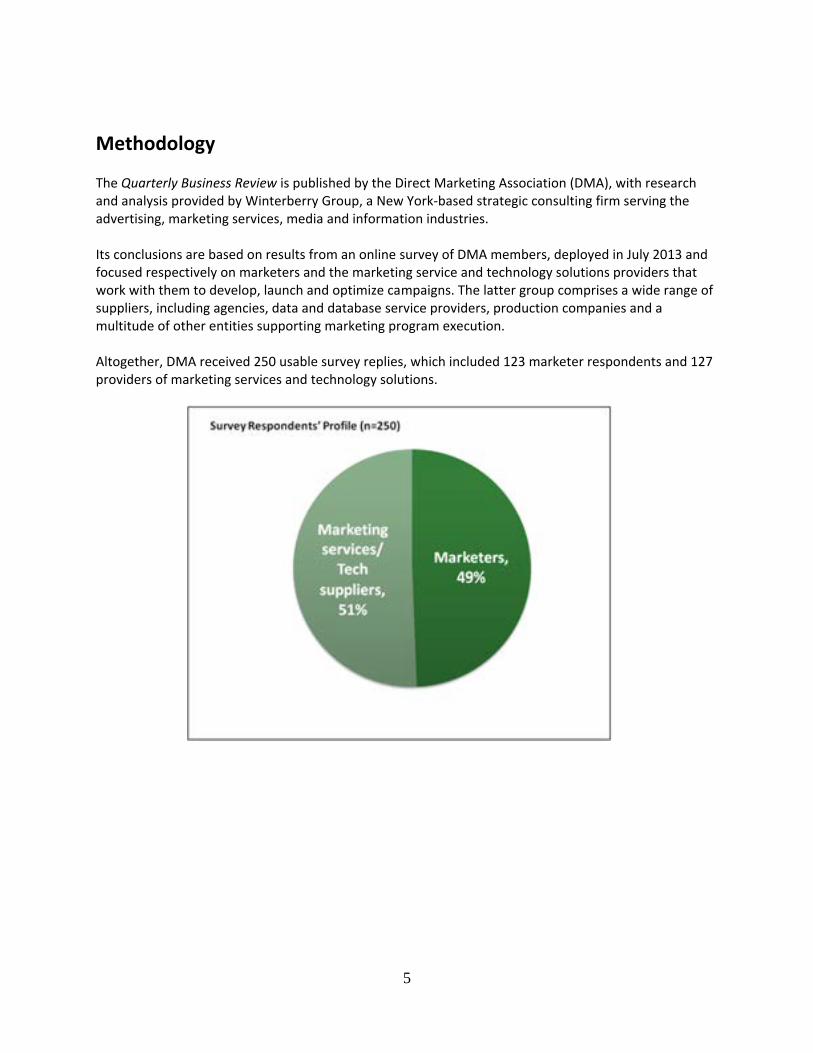

Methodology The Quarterly Business Review is published by the Direct Marketing Association (DMA), with research and analysis provided by Winterberry Group, a New York‐based strategic consulting firm serving the advertising, marketing services, media and information industries. Its conclusions are based on results from an online survey of DMA members, deployed in July 2013 and focused respectively on marketers and the marketing service and technology solutions providers that work with them to develop, launch and optimize campaigns. The latter group comprises a wide range of suppliers, including agencies, data and database service providers, production companies and a multitude of other entities supporting marketing program execution. Altogether, DMA received 250 usable survey replies, which included 123 marketer respondents and 127 providers of marketing services and technology solutions.

6

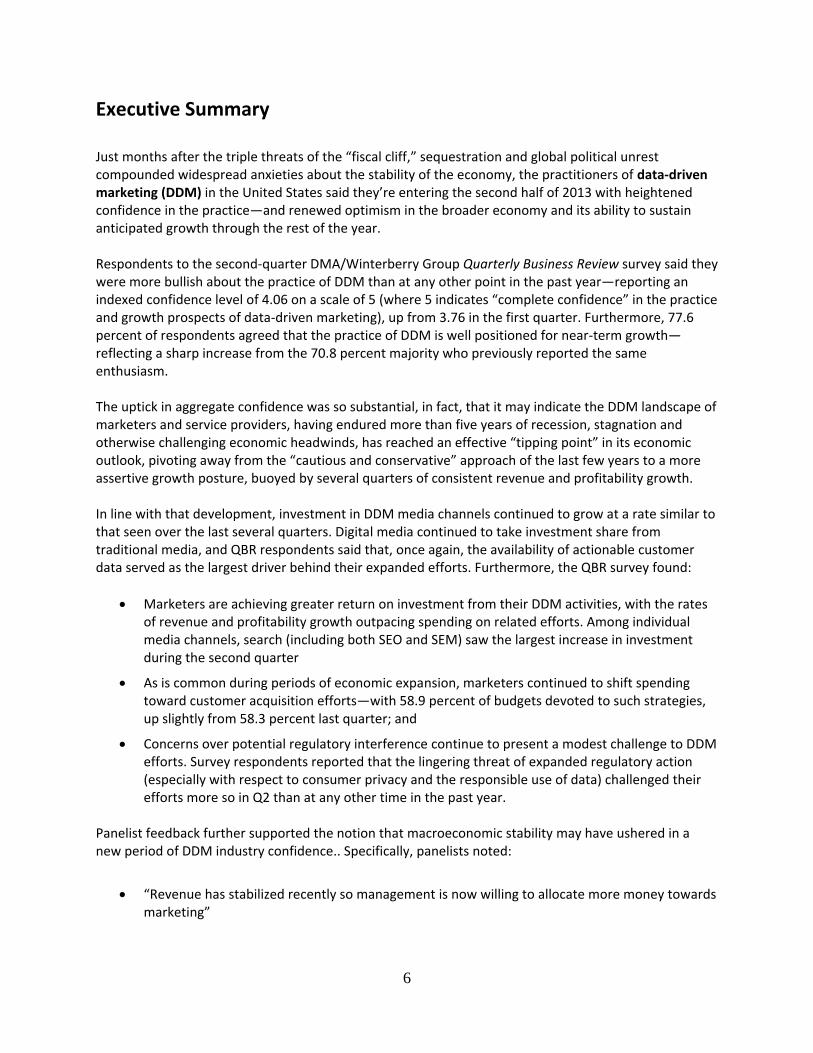

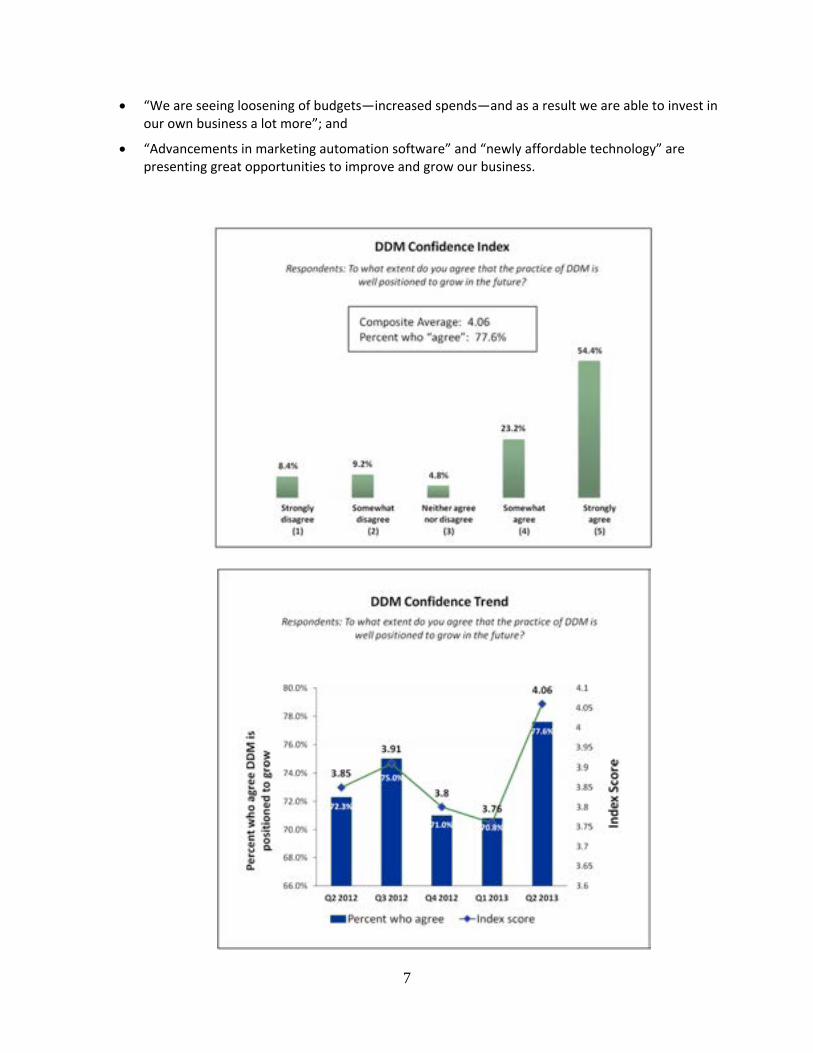

Executive Summary Just months after the triple threats of the “fiscal cliff,” sequestration and global political unrest compounded widespread anxieties about the stability of the economy, the practitioners of data‐driven marketing (DDM) in the United States said they’re entering the second half of 2013 with heightened confidence in the practice—and renewed optimism in the broader economy and its ability to sustain anticipated growth through the rest of the year. Respondents to the second‐quarter DMA/Winterberry Group Quarterly Business Review survey said they were more bullish about the practice of DDM than at any other point in the past year—reporting an indexed confidence level of 4.06 on a scale of 5 (where 5 indicates “complete confidence” in the practice and growth prospects of data‐driven marketing), up from 3.76 in the first quarter. Furthermore, 77.6 percent of respondents agreed that the practice of DDM is well positioned for near‐term growth—reflecting a sharp increase from the 70.8 percent majority who previously reported the same enthusiasm. The uptick in aggregate confidence was so substantial, in fact, that it may indicate the DDM landscape of marketers and service providers, having endured more than five years of recession, stagnation and otherwise challenging economic headwinds, has reached an effective “tipping point” in its economic outlook, pivoting away from the “cautious and conservative” approach of the last few years to a more assertive growth posture, buoyed by several quarters of consistent revenue and profitability growth. In line with that development, investment in DDM media channels continued to grow at a rate similar to that seen over the last several quarters. Digital media continued to take investment share from traditional media, and QBR respondents said that, once again, the availability of actionable customer data served as the largest driver behind their expanded efforts. Furthermore, the QBR survey found:

Marketers are achieving greater return on investment from their DDM activities, with the rates of revenue and profitability growth outpacing spending on related efforts. Among individual media channels, search (including both SEO and SEM) saw the largest increase in investment during the second quarter

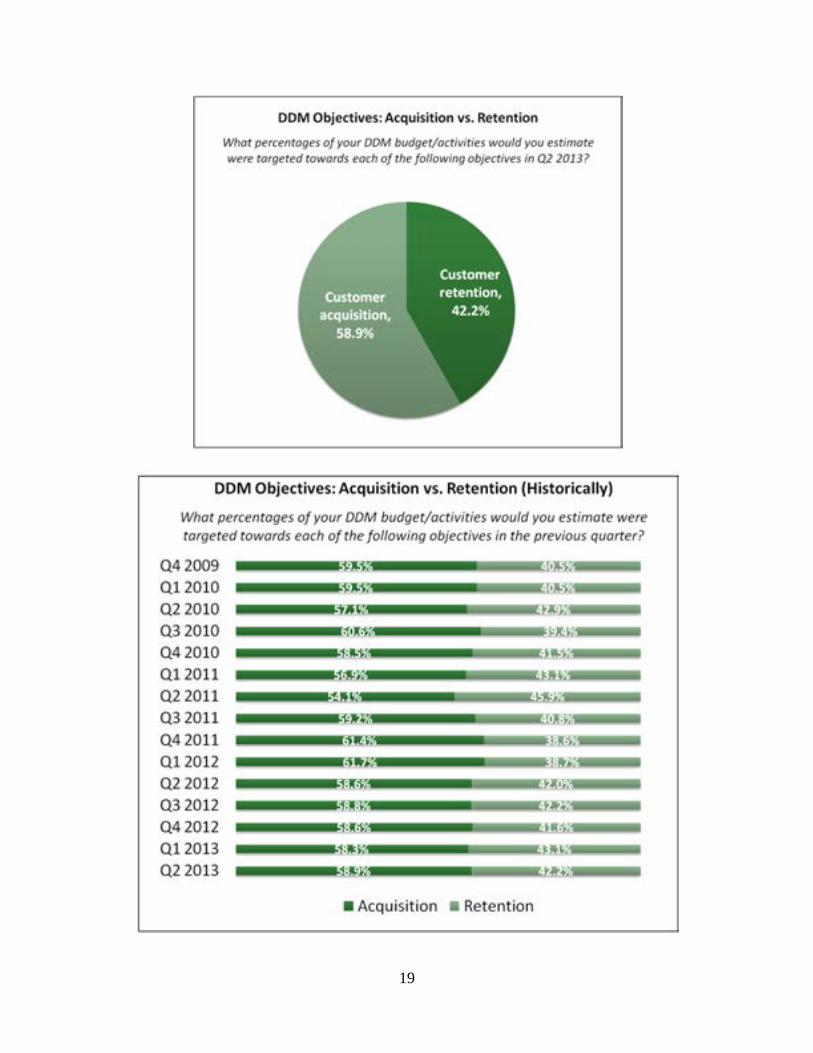

As is common during periods of economic expansion, marketers continued to shift spending toward customer acquisition efforts—with 58.9 percent of budgets devoted to such strategies, up slightly from 58.3 percent last quarter; and

Concerns over potential regulatory interference continue to present a modest challenge to DDM efforts. Survey respondents reported that the lingering threat of expanded regulatory action (especially with respect to consumer privacy and the responsible use of data) challenged their efforts more so in Q2 than at any other time in the past year.

Panelist feedback further supported the notion that macroeconomic stability may have ushered in a new period of DDM industry confidence.. Specifically, panelists noted:

“Revenue has stabilized recently so management is now willing to allocate more money towards marketing”

7

“We are seeing loosening of budgets—increased spends—and as a result we are able to invest in our own business a lot more”; and

“Advancements in marketing automation software” and “newly affordable technology” are presenting great opportunities to improve and grow our business.

8

I. Data‐Driven Marketing Spending

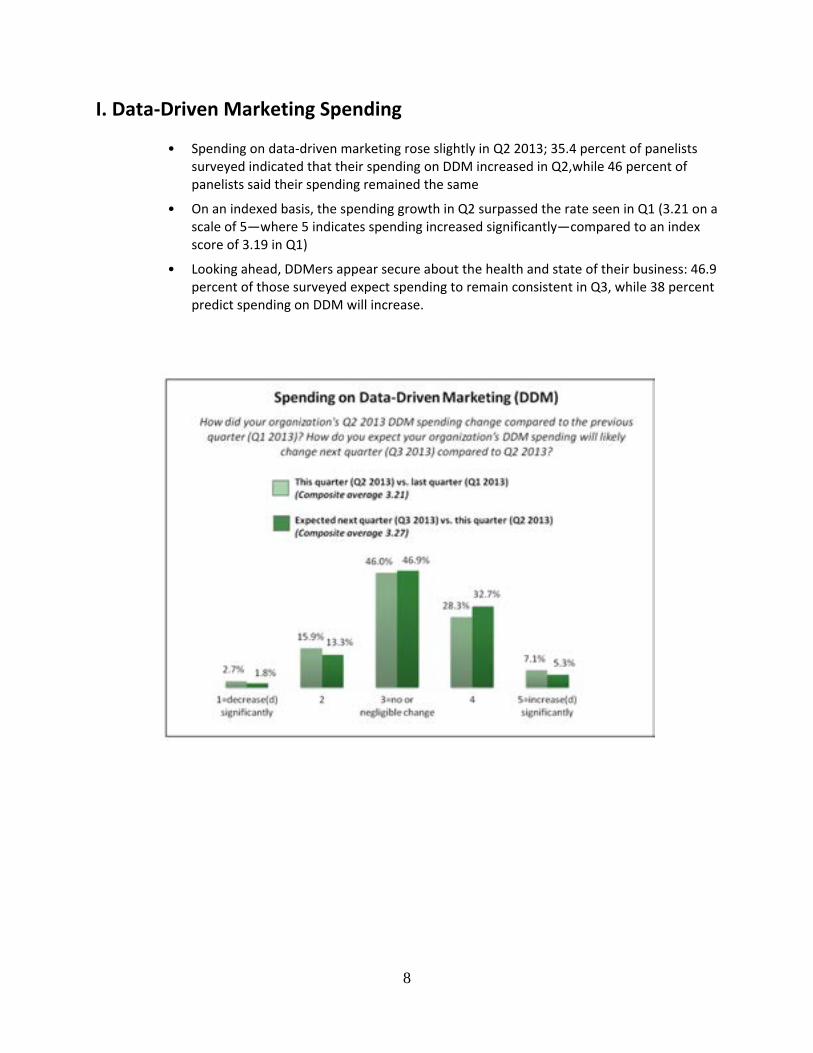

• Spending on data‐driven marketing rose slightly in Q2 2013; 35.4 percent of panelists surveyed indicated that their spending on DDM increased in Q2,while 46 percent of panelists said their spending remained the same

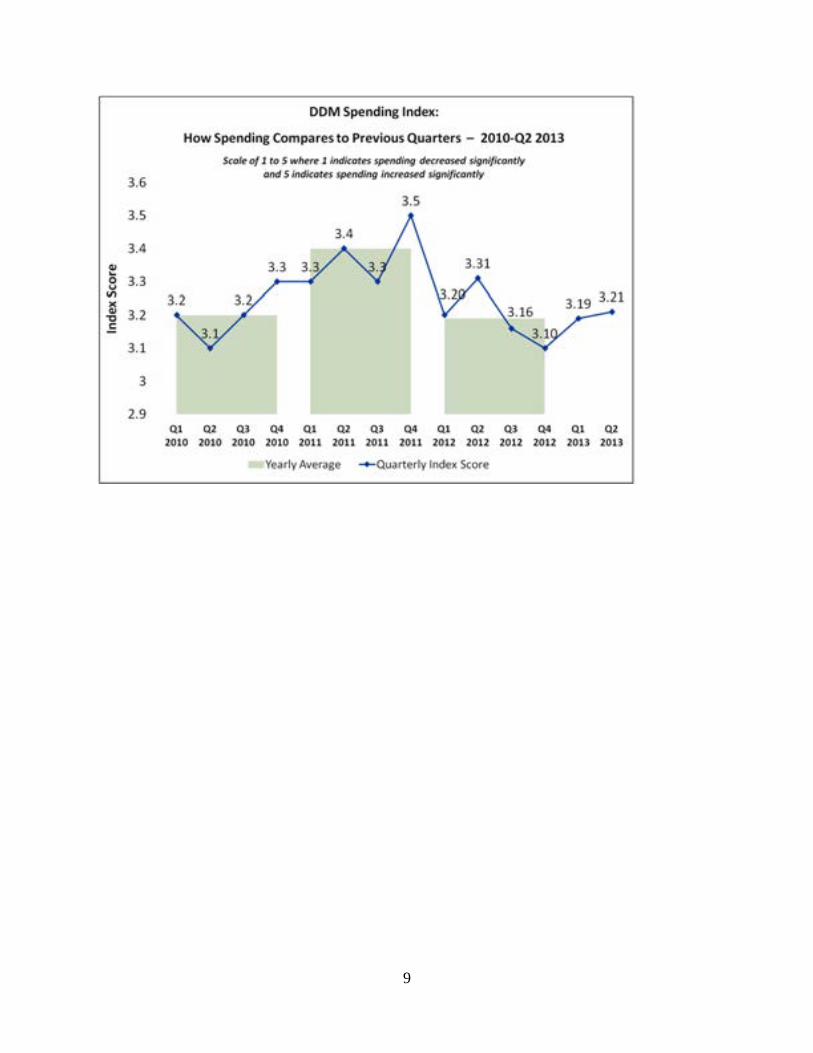

• On an indexed basis, the spending growth in Q2 surpassed the rate seen in Q1 (3.21 on a scale of 5—where 5 indicates spending increased significantly—compared to an index score of 3.19 in Q1)

• Looking ahead, DDMers appear secure about the health and state of their business: 46.9 percent of those surveyed expect spending to remain consistent in Q3, while 38 percent predict spending on DDM will increase.

9

10

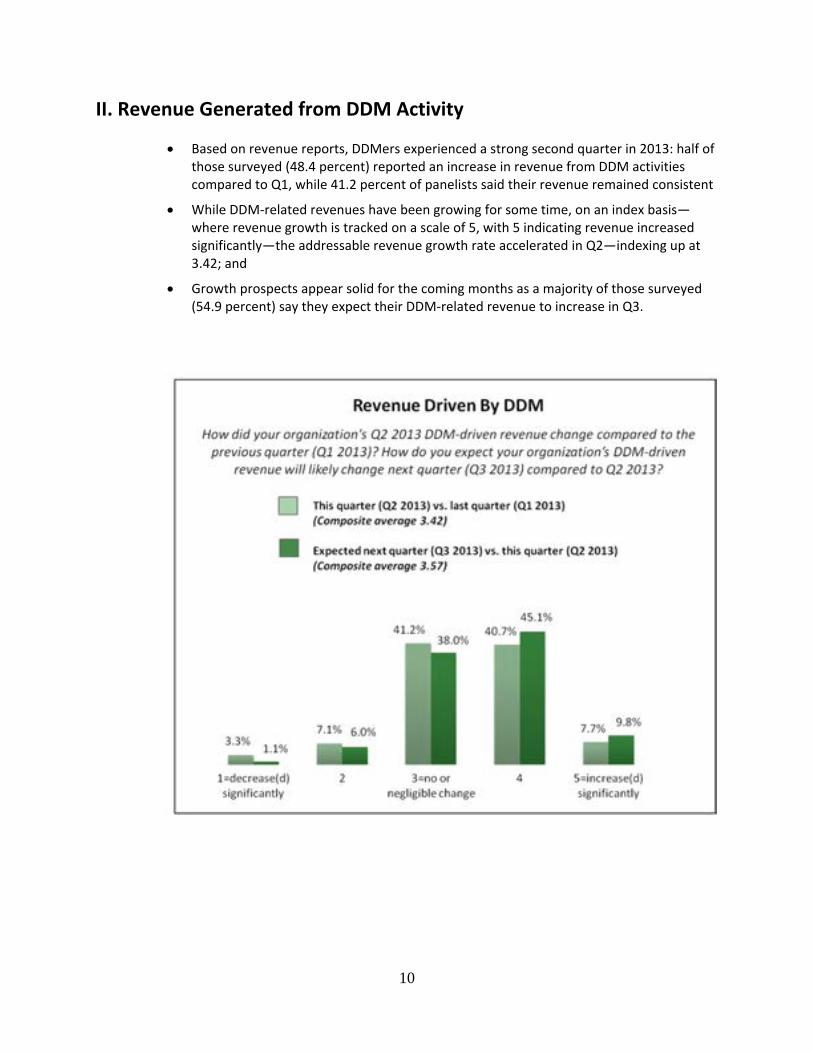

II. Revenue Generated from DDM Activity

Based on revenue reports, DDMers experienced a strong second quarter in 2013: half of those surveyed (48.4 percent) reported an increase in revenue from DDM activities compared to Q1, while 41.2 percent of panelists said their revenue remained consistent

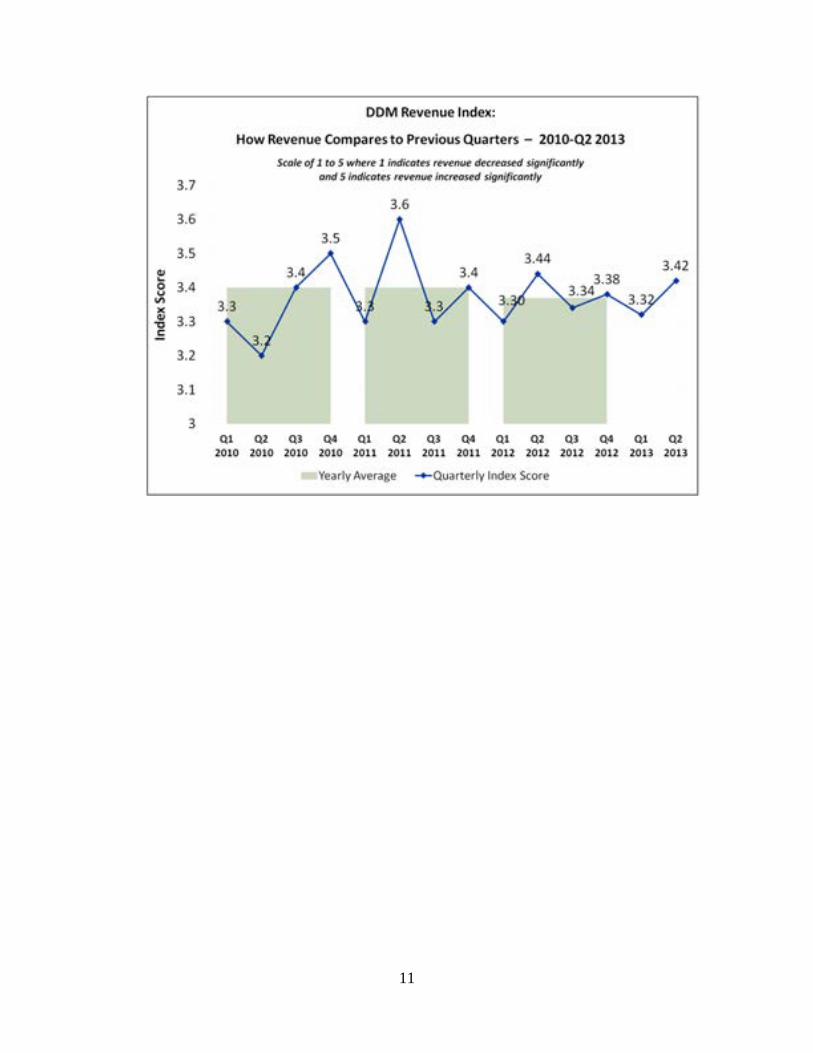

While DDM‐related revenues have been growing for some time, on an index basis—where revenue growth is tracked on a scale of 5, with 5 indicating revenue increased significantly—the addressable revenue growth rate accelerated in Q2—indexing up at 3.42; and

Growth prospects appear solid for the coming months as a majority of those surveyed (54.9 percent) say they expect their DDM‐related revenue to increase in Q3.

11

12

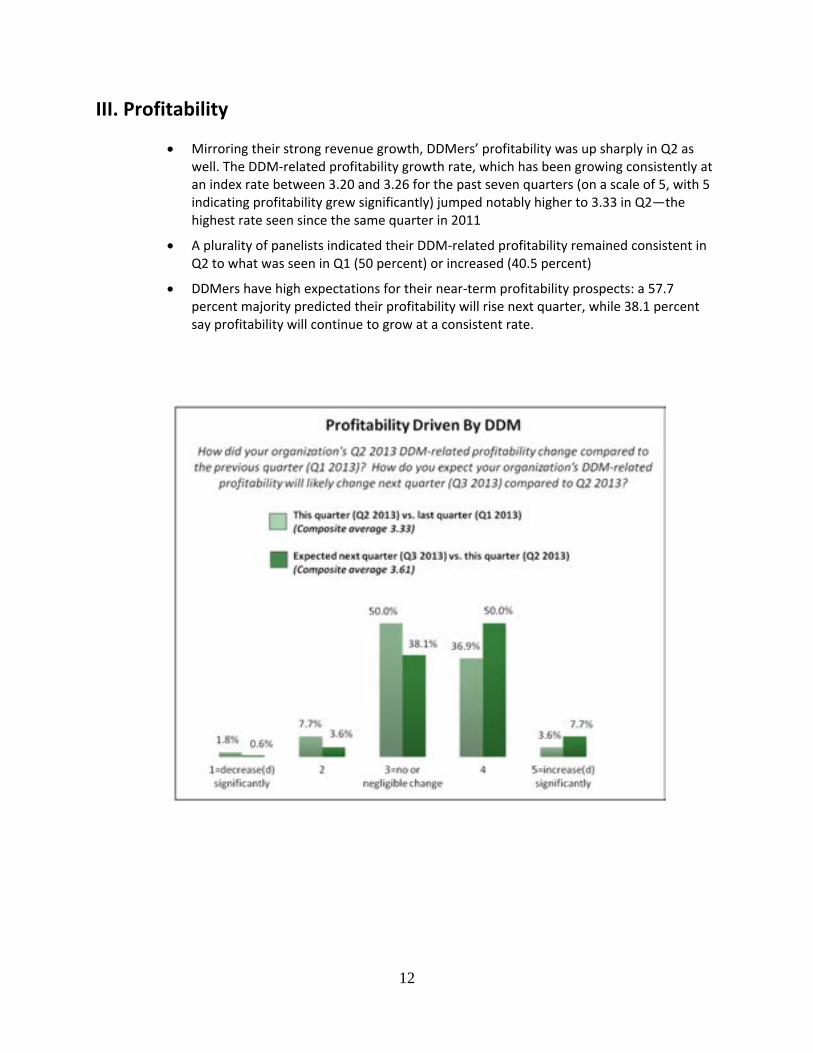

III. Profitability

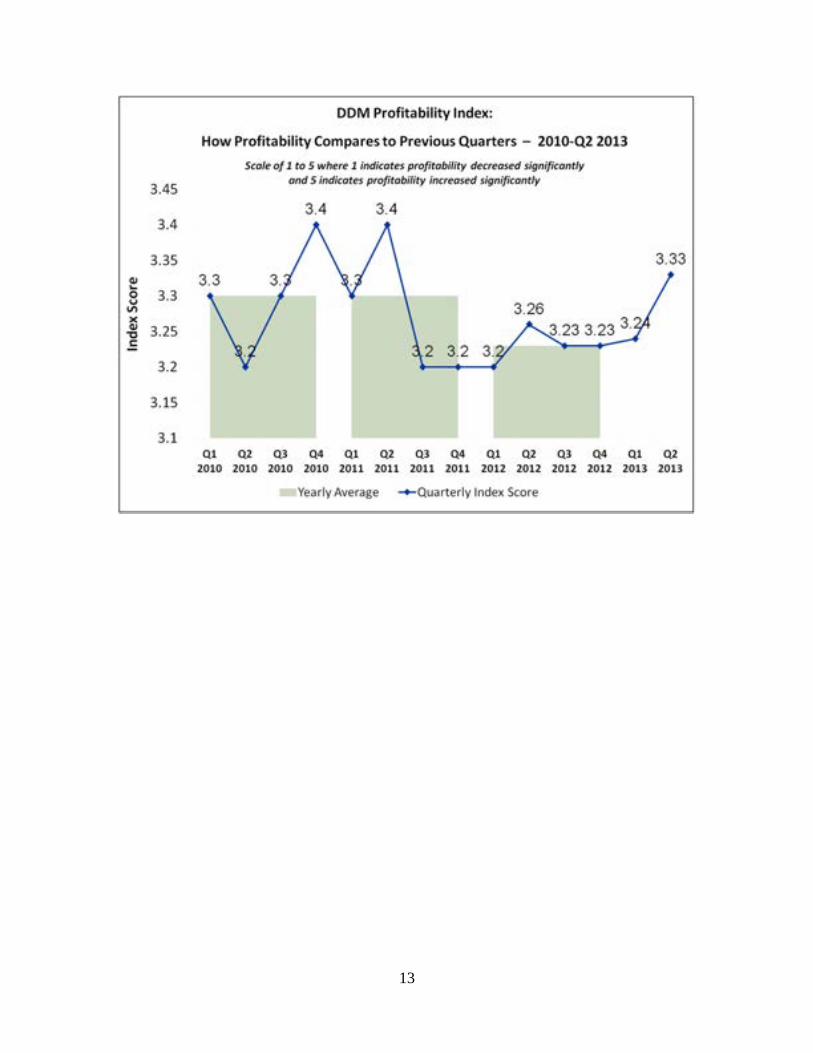

Mirroring their strong revenue growth, DDMers’ profitability was up sharply in Q2 as well. The DDM‐related profitability growth rate, which has been growing consistently at an index rate between 3.20 and 3.26 for the past seven quarters (on a scale of 5, with 5 indicating profitability grew significantly) jumped notably higher to 3.33 in Q2—the highest rate seen since the same quarter in 2011

A plurality of panelists indicated their DDM‐related profitability remained consistent in Q2 to what was seen in Q1 (50 percent) or increased (40.5 percent)

DDMers have high expectations for their near‐term profitability prospects: a 57.7 percent majority predicted their profitability will rise next quarter, while 38.1 percent say profitability will continue to grow at a consistent rate.

13

14

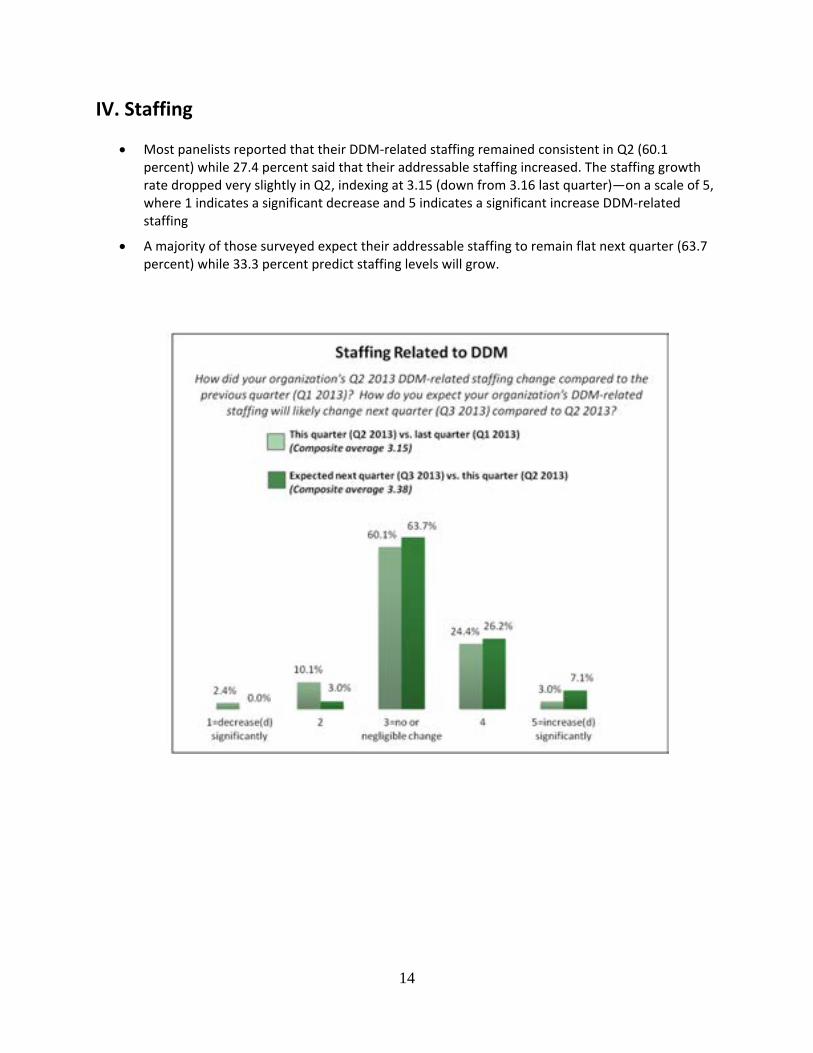

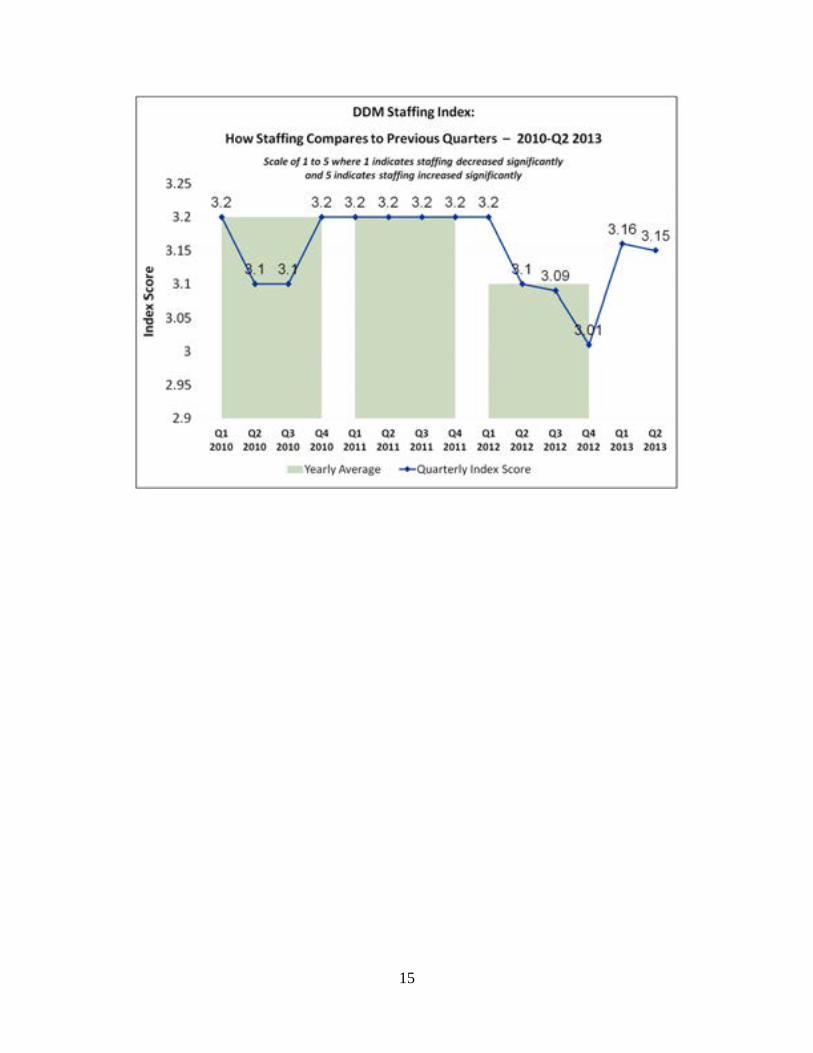

IV. Staffing

Most panelists reported that their DDM‐related staffing remained consistent in Q2 (60.1 percent) while 27.4 percent said that their addressable staffing increased. The staffing growth rate dropped very slightly in Q2, indexing at 3.15 (down from 3.16 last quarter)—on a scale of 5, where 1 indicates a significant decrease and 5 indicates a significant increase DDM‐related staffing

A majority of those surveyed expect their addressable staffing to remain flat next quarter (63.7 percent) while 33.3 percent predict staffing levels will grow.

15

16

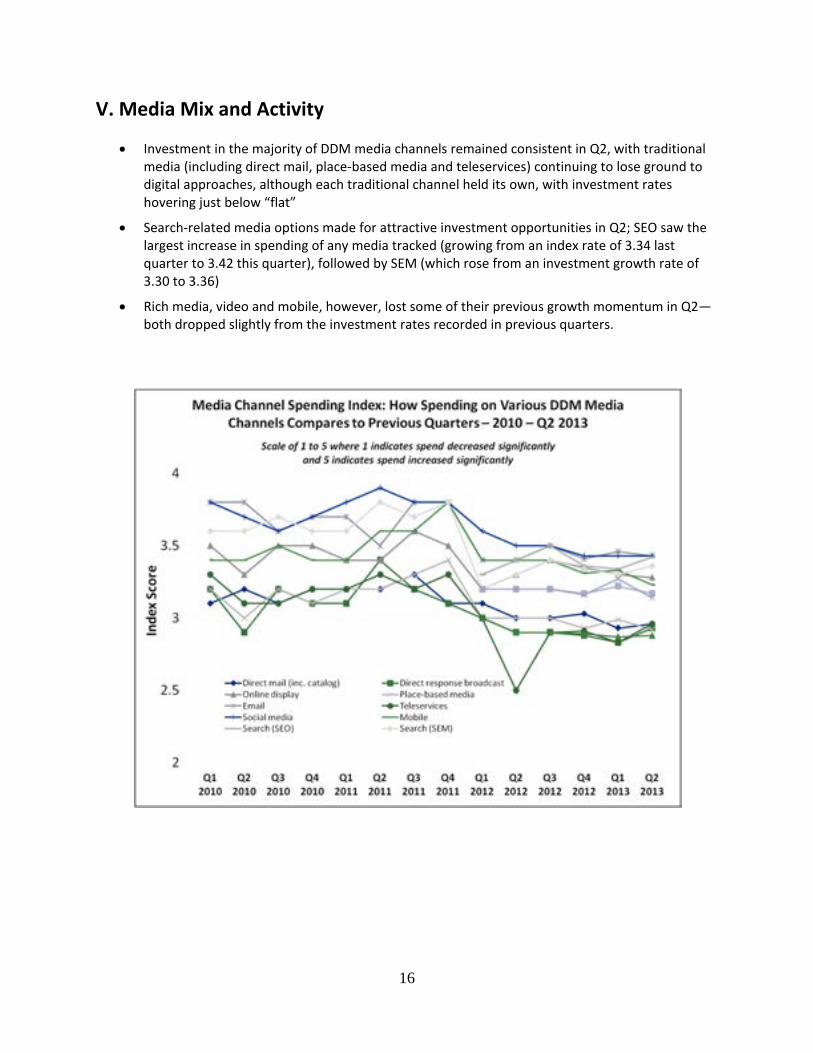

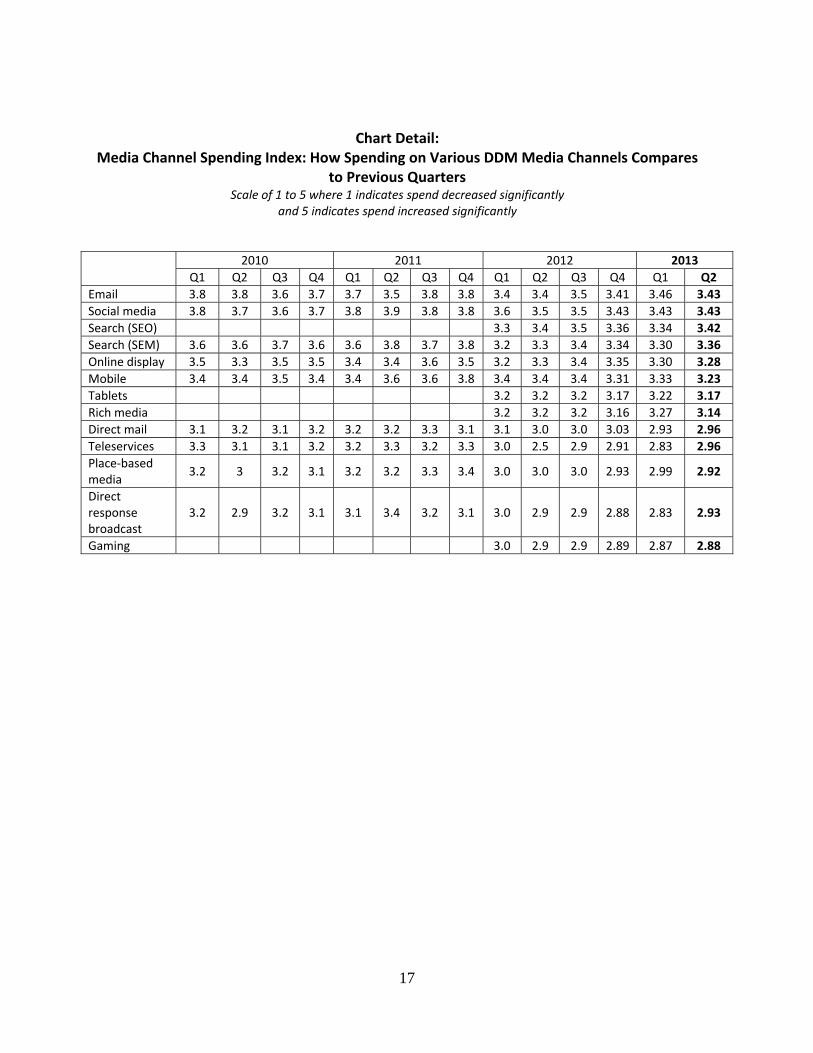

V. Media Mix and Activity

Investment in the majority of DDM media channels remained consistent in Q2, with traditional media (including direct mail, place‐based media and teleservices) continuing to lose ground to digital approaches, although each traditional channel held its own, with investment rates hovering just below “flat”

Search‐related media options made for attractive investment opportunities in Q2; SEO saw the largest increase in spending of any media tracked (growing from an index rate of 3.34 last quarter to 3.42 this quarter), followed by SEM (which rose from an investment growth rate of 3.30 to 3.36)

Rich media, video and mobile, however, lost some of their previous growth momentum in Q2—both dropped slightly from the investment rates recorded in previous quarters.

17

Chart Detail: Media Channel Spending Index: How Spending on Various DDM Media Channels Compares

to Previous Quarters Scale of 1 to 5 where 1 indicates spend decreased significantly

and 5 indicates spend increased significantly

2010 2011 2012 2013

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2

Email 3.8 3.8 3.6 3.7 3.7 3.5 3.8 3.8 3.4 3.4 3.5 3.41 3.46 3.43

Social media 3.8 3.7 3.6 3.7 3.8 3.9 3.8 3.8 3.6 3.5 3.5 3.43 3.43 3.43

Search (SEO) 3.3 3.4 3.5 3.36 3.34 3.42

Search (SEM) 3.6 3.6 3.7 3.6 3.6 3.8 3.7 3.8 3.2 3.3 3.4 3.34 3.30 3.36

Online display 3.5 3.3 3.5 3.5 3.4 3.4 3.6 3.5 3.2 3.3 3.4 3.35 3.30 3.28

Mobile 3.4 3.4 3.5 3.4 3.4 3.6 3.6 3.8 3.4 3.4 3.4 3.31 3.33 3.23

Tablets 3.2 3.2 3.2 3.17 3.22 3.17

Rich media 3.2 3.2 3.2 3.16 3.27 3.14

Direct mail 3.1 3.2 3.1 3.2 3.2 3.2 3.3 3.1 3.1 3.0 3.0 3.03 2.93 2.96

Teleservices 3.3 3.1 3.1 3.2 3.2 3.3 3.2 3.3 3.0 2.5 2.9 2.91 2.83 2.96

Place‐based media

3.2 3 3.2 3.1 3.2 3.2 3.3 3.4 3.0 3.0 3.0 2.93 2.99 2.92

Direct response broadcast

3.2 2.9 3.2 3.1 3.1 3.4 3.2 3.1 3.0 2.9 2.9 2.88 2.83 2.93

Gaming 3.0 2.9 2.9 2.89 2.87 2.88

18

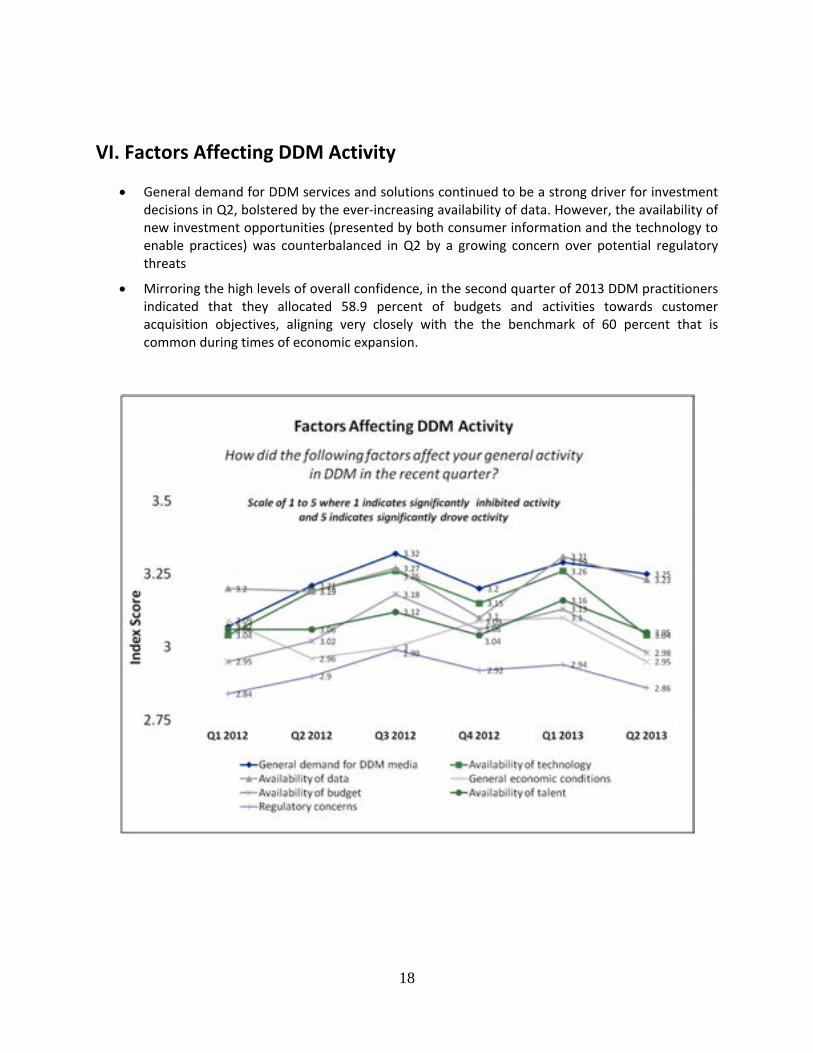

VI. Factors Affecting DDM Activity

General demand for DDM services and solutions continued to be a strong driver for investment decisions in Q2, bolstered by the ever‐increasing availability of data. However, the availability of new investment opportunities (presented by both consumer information and the technology to enable practices) was counterbalanced in Q2 by a growing concern over potential regulatory threats

Mirroring the high levels of overall confidence, in the second quarter of 2013 DDM practitioners indicated that they allocated 58.9 percent of budgets and activities towards customer acquisition objectives, aligning very closely with the the benchmark of 60 percent that is common during times of economic expansion.

19