Embed Size (px)

Citation preview

7/27/2019 Dmp3e Ch06 Solutions 01.26.10 Final

http://slidepdf.com/reader/full/dmp3e-ch06-solutions-012610-final 1/39

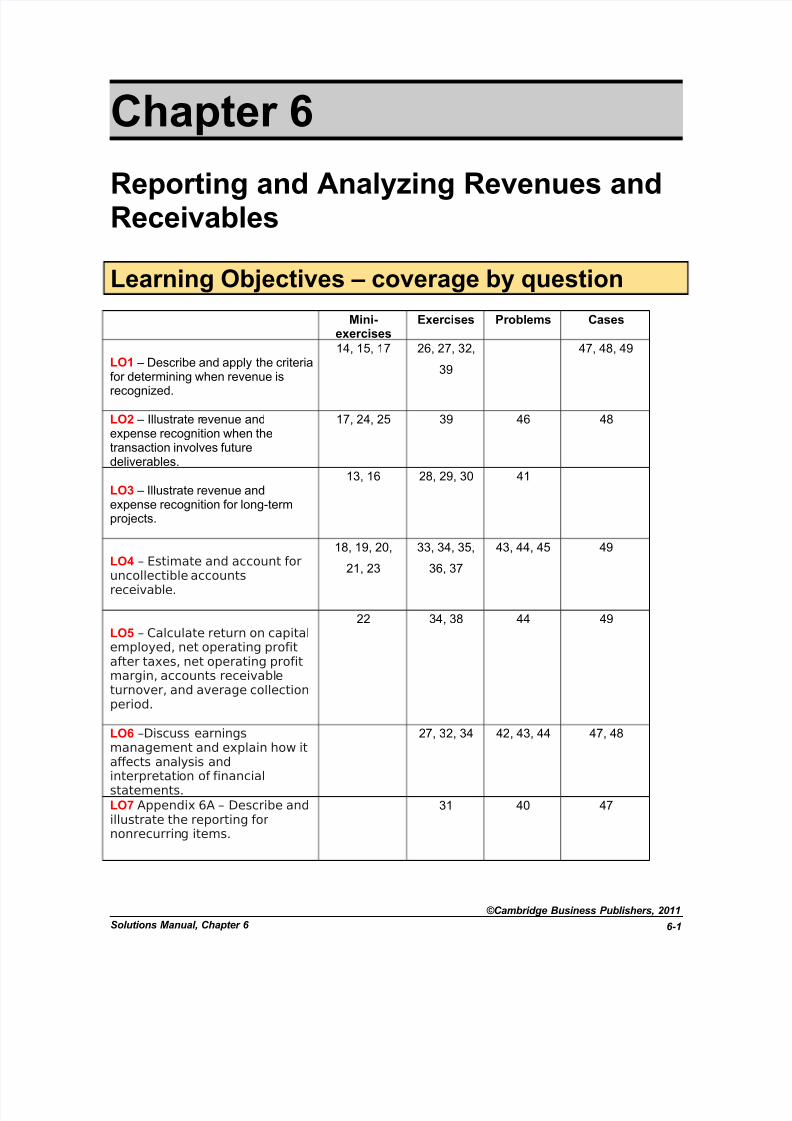

Chapter 6

Reporting and Analyzing Revenues andReceivables

Learning Objectives – coverage by question

Mini-exercises

Exercises Problems Cases

LO1 – Describe and apply the criteria

for determining when revenue isrecognized.

14, 15, 17 26, 27, 32,

39

47, 48, 49

LO2 – Illustrate revenue andexpense recognition when thetransaction involves futuredeliverables.

17, 24, 25 39 46 48

LO3 – Illustrate revenue andexpense recognition for long-termprojects.

13, 16 28, 29, 30 41

LO4 – Estimate and account foruncollectible accountsreceivable.

18, 19, 20,

21, 23

33, 34, 35,

36, 37

43, 44, 45 49

LO5 – Calculate return on capitalemployed, net operating profitafter taxes, net operating profitmargin, accounts receivableturnover, and average collectionperiod.

22 34, 38 44 49

LO6 –Discuss earnings

management and explain how itaffects analysis andinterpretation of financialstatements.

27, 32, 34 42, 43, 44 47, 48

LO7 Appendix 6A – Describe andillustrate the reporting fornonrecurring items.

31 40 47

©Cambridge Business Publishers, 2011

Solutions Manual, Chapter 6 6-1

7/27/2019 Dmp3e Ch06 Solutions 01.26.10 Final

http://slidepdf.com/reader/full/dmp3e-ch06-solutions-012610-final 2/39

7/27/2019 Dmp3e Ch06 Solutions 01.26.10 Final

http://slidepdf.com/reader/full/dmp3e-ch06-solutions-012610-final 3/39

Q6-5. Earnings management may be motivated by a desire to reach or exceedpreviously stated earnings targets, to meet analysts’ expectations, or tomaintain steady growth in earnings from year to year. This desire toachieve income goals may be motivated by the need to avoid violatingcovenants in loan indentures or to maximize incentive-basedcompensation.

The tactics used to manage income involve transaction timing (recognizinga gain or loss) and estimations that increase (or decrease) income toachieve a target.

Q6-6. Pro forma income adjusts GAAP income to eliminate (and sometimes add)various items that the company believes do not reflect its core operations.Such pro forma disclosures are only reported in earnings and pressreleases and are not part of the published 10-Ks or other annual reportsprovided for shareholders. The SEC requires that GAAP income bereported together with pro forma income. Yet, companies often report their GAAP income at the very end of the earnings or press release, thus

obfuscating their comparison and focusing attention on the pro formaincome.

It is because of this potential to confuse the reader about the true financialperformance of the company that the SEC has become concerned. Also,pro forma numbers are not subject to accepted standards (and, thus, weobserve differing definitions across companies), are not subject to usualaudit tests, and are subject to considerable management latitude in what isand is not included and how items are measured.

Q6-7. Estimates are necessary in order to accurately measure and report incomeon a timely basis. For example, in order to record periodic depreciation of

long-lived assets, one must estimate the useful life of the asset. Estimatesallow accountants to match revenues and expenses incurred in differentperiods. For example, accountants estimate warranty costs so that thewarranty expense is matched against the corresponding sales revenue. If the accounting process waited until no estimates were necessary, therewould be a significant delay in the reporting of financial results.

Q6-8. When analysts publish earnings forecasts, these forecasts become abenchmark against which some investors evaluate the company’sperformance. A company that fails to meet analysts’ forecasts may suffer astock price decline, even though earnings are higher than previous years’earnings and overall performance is good. Consequently, management

may feel pressure to meet or slightly exceed analysts’ forecasts of earnings.

©Cambridge Business Publishers, 2011

Solutions Manual, Chapter 6 6-3

7/27/2019 Dmp3e Ch06 Solutions 01.26.10 Final

http://slidepdf.com/reader/full/dmp3e-ch06-solutions-012610-final 4/39

Q6-9. Bad debts expense is recorded in the income statement when theallowance for uncollectible accounts is increased. If a companyoverestimates the allowance account, net income will be understated onthe income statement and accounts receivable (net of the allowanceaccount) will be underestimated on the balance sheet. In future periods,such a company will not need to add as much to its allowance account

since it is already overestimated from that prior period (or, it can reversethe existing excess allowance balance). As a result, future net income willbe higher.On the other hand, if a company underestimates its allowance account,then current net income will be overstated. In future periods, however, netincome will be understated as the company must add to the allowanceaccount and report higher bad debts expense.

Q6-10. There are several possible explanations for a decrease in the allowanceaccount. First, after an aging of accounts receivable, Wallace Company mayhave determined that a smaller percentage of its receivables are past due.Wallace Company may have changed its credit policy such that it isattracting lower-risk customers than in the past. Second, experience mayhave indicated that the percentages used to estimate uncollectibles was toohigh in previous years. By correcting the estimated percentage of defaults,the estimated uncollectibles would end up lower than in past years. Third,Wallace Company may be managing earnings. By lowering estimateduncollectibles, the company can increase current earnings, but may end upreporting a loss in a future year when write-offs exceed the balance in theallowance account.

Q6-11. Minimizing uncollectible accounts is not necessarily the best objective for managing accounts receivable. That objective could be accomplished by not

offering to sell to customers on credit. The purpose of offering credit tocustomers is to increase sales and profits. Losses from uncollectibleaccounts are a cost of doing business. As long as the benefit (greater contribution to profits due to increased sales) exceeds the cost (increasedlosses due to uncollectibles) then a higher-risk credit policy which increasesthe amount of uncollectible accounts would be a more profitable policy.

Q6-12. The number of defaults tends to rise and fall with the economy. For example,in a recession, customers are more likely to default and companies takelonger, on average, to pay their bills than during a healthy economy. Thiswould result in higher estimated uncollectibles if the estimates are based onan aging of accounts receivable.

For many companies, sales revenue also tends to decline during a recession.If estimated uncollectibles are estimated as a percentage of sales, then theestimate would tend to fall in a recession. This is contrary to the increase inthe number of defaults that occurs during a recession. Therefore, thepercentage of sales approach is not as sensitive to changing economicconditions as is accounts receivable aging.

©Cambridge Business Publishers, 2011

Financial Accounting, 3rd Edition6-4

7/27/2019 Dmp3e Ch06 Solutions 01.26.10 Final

http://slidepdf.com/reader/full/dmp3e-ch06-solutions-012610-final 5/39

MINI EXERCISES

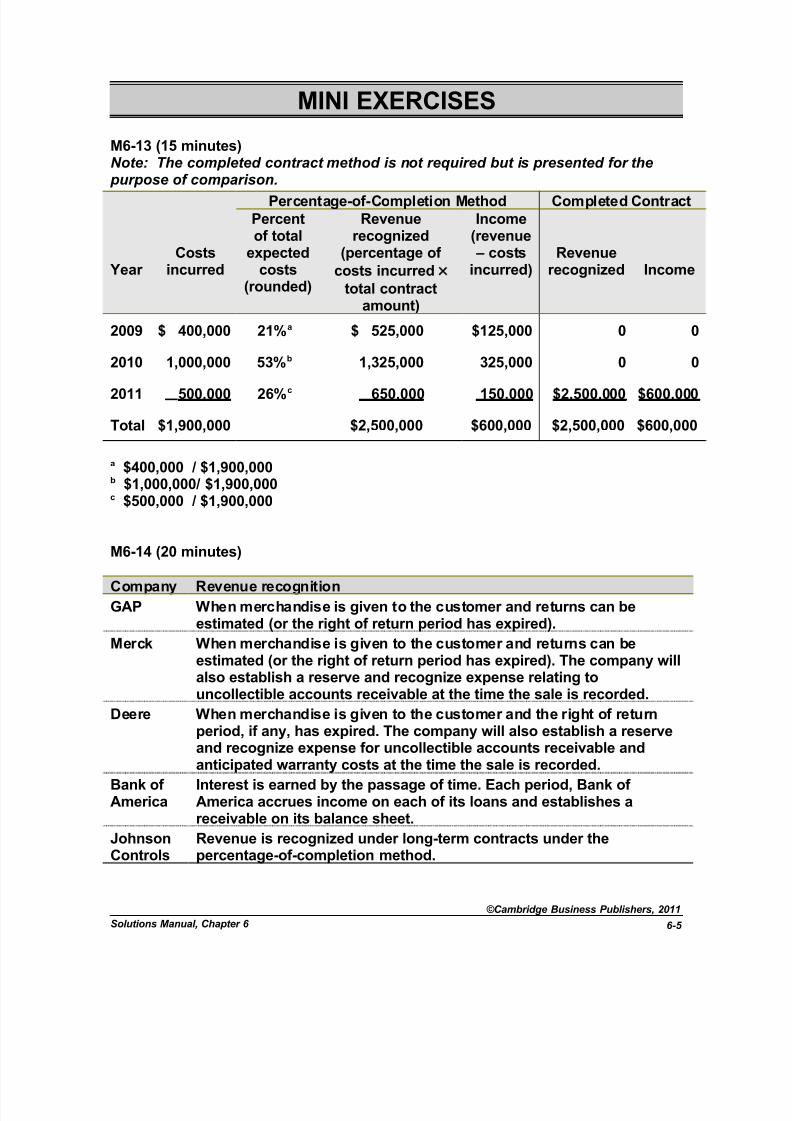

M6-13 (15 minutes)Note: The completed contract method is not required but is presented for the

purpose of comparison.Percentage-of-Completion Method Completed Contract

Year Costs

incurred

Percentof total

expectedcosts

(rounded)

Revenuerecognized

(percentage of costs incurred ×

total contractamount)

Income(revenue – costsincurred)

Revenuerecognized Income

2009 $ 400,000 21%a $ 525,000 $125,000 0 0

2010 1,000,000 53%b 1,325,000 325,000 0 0

2011 500,000 26%c 650,000 150,000 $2,500,000 $600,000

Total $1,900,000 $2,500,000 $600,000 $2,500,000 $600,000

a $400,000 / $1,900,000b $1,000,000/ $1,900,000c $500,000 / $1,900,000

M6-14 (20 minutes)

Company Revenue recognition

GAP When merchandise is given to the customer and returns can beestimated (or the right of return period has expired).

Merck When merchandise is given to the customer and returns can beestimated (or the right of return period has expired). The company willalso establish a reserve and recognize expense relating touncollectible accounts receivable at the time the sale is recorded.

Deere When merchandise is given to the customer and the right of returnperiod, if any, has expired. The company will also establish a reserve

and recognize expense for uncollectible accounts receivable andanticipated warranty costs at the time the sale is recorded.

Bank of America

Interest is earned by the passage of time. Each period, Bank of America accrues income on each of its loans and establishes areceivable on its balance sheet.

JohnsonControls

Revenue is recognized under long-term contracts under thepercentage-of-completion method.

©Cambridge Business Publishers, 2011

Solutions Manual, Chapter 6 6-5

7/27/2019 Dmp3e Ch06 Solutions 01.26.10 Final

http://slidepdf.com/reader/full/dmp3e-ch06-solutions-012610-final 6/39

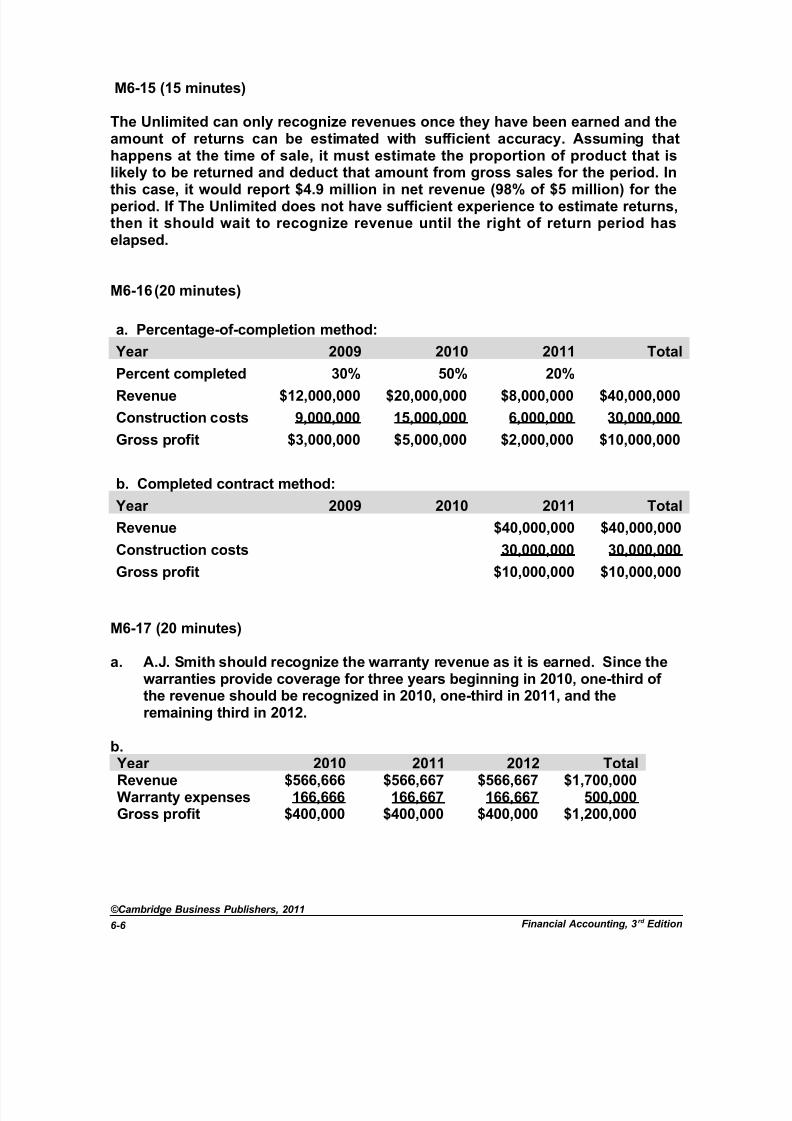

M6-15 (15 minutes)

The Unlimited can only recognize revenues once they have been earned and theamount of returns can be estimated with sufficient accuracy. Assuming thathappens at the time of sale, it must estimate the proportion of product that islikely to be returned and deduct that amount from gross sales for the period. In

this case, it would report $4.9 million in net revenue (98% of $5 million) for theperiod. If The Unlimited does not have sufficient experience to estimate returns,then it should wait to recognize revenue until the right of return period haselapsed.

M6-16(20 minutes)

a. Percentage-of-completion method:

Year 2009 2010 2011 Total

Percent completed 30% 50% 20%Revenue $12,000,000 $20,000,000 $8,000,000 $40,000,000

Construction costs 9,000,000 15,000,000 6,000,000 30,000,000

Gross profit $3,000,000 $5,000,000 $2,000,000 $10,000,000

b. Completed contract method:

Year 2009 2010 2011 Total

Revenue $40,000,000 $40,000,000

Construction costs 30,000,000 30,000,000

Gross profit $10,000,000 $10,000,000

M6-17 (20 minutes)

a. A.J. Smith should recognize the warranty revenue as it is earned. Since thewarranties provide coverage for three years beginning in 2010, one-third of the revenue should be recognized in 2010, one-third in 2011, and theremaining third in 2012.

b. Year 2010 2011 2012 TotalRevenue $566,666 $566,667 $566,667 $1,700,000Warranty expenses 166,666 166,667 166,667 500,000Gross profit $400,000 $400,000 $400,000 $1,200,000

©Cambridge Business Publishers, 2011

Financial Accounting, 3rd Edition6-6

7/27/2019 Dmp3e Ch06 Solutions 01.26.10 Final

http://slidepdf.com/reader/full/dmp3e-ch06-solutions-012610-final 7/39

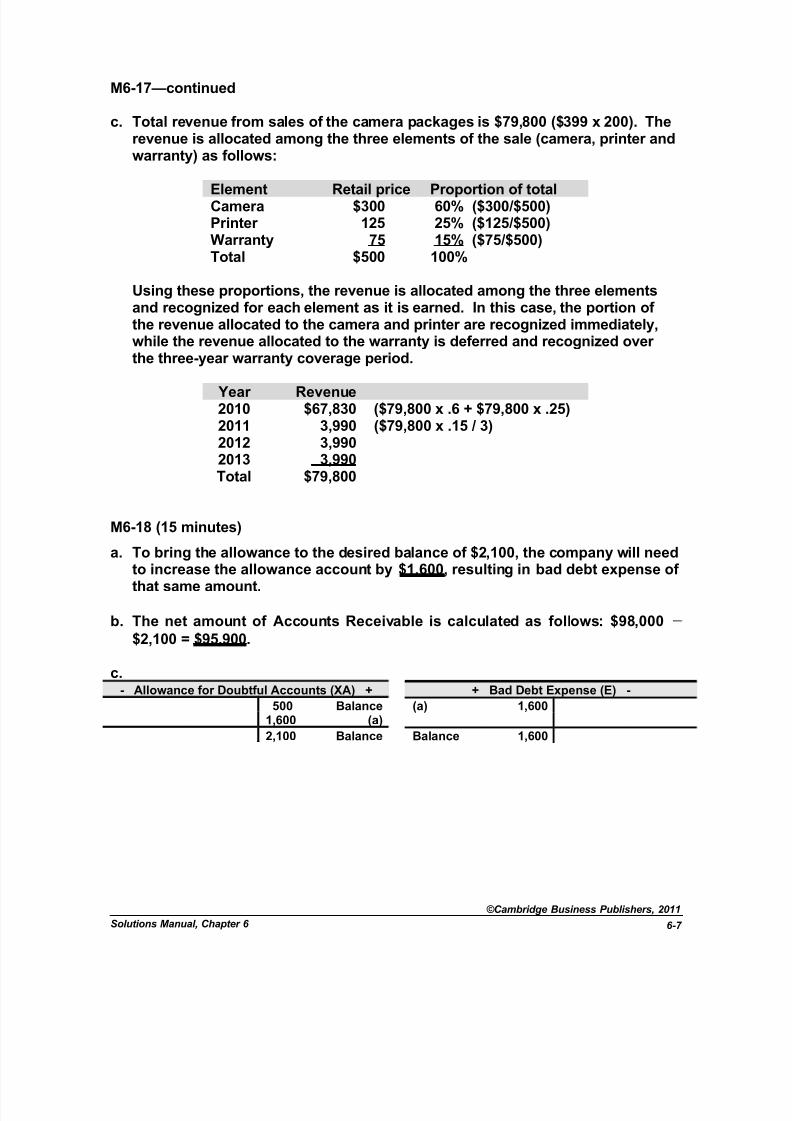

M6-17—continued

c. Total revenue from sales of the camera packages is $79,800 ($399 x 200). Therevenue is allocated among the three elements of the sale (camera, printer andwarranty) as follows:

Element Retail price Proportion of totalCamera $300 60% ($300/$500)Printer 125 25% ($125/$500)Warranty 75 15% ($75/$500)Total $500 100%

Using these proportions, the revenue is allocated among the three elementsand recognized for each element as it is earned. In this case, the portion of the revenue allocated to the camera and printer are recognized immediately,while the revenue allocated to the warranty is deferred and recognized over the three-year warranty coverage period.

Year Revenue2010 $67,830 ($79,800 x .6 + $79,800 x .25)2011 3,990 ($79,800 x .15 / 3)2012 3,9902013 3,990Total $79,800

M6-18 (15 minutes)

a. To bring the allowance to the desired balance of $2,100, the company will needto increase the allowance account by $1,600, resulting in bad debt expense of that same amount.

b. The net amount of Accounts Receivable is calculated as follows: $98,000 −$2,100 = $95,900.

c.- Allowance for Doubtful Accounts (XA) + + Bad Debt Expense (E) -

500 Balance (a) 1,6001,600 (a)

2,100 Balance Balance 1,600

©Cambridge Business Publishers, 2011

Solutions Manual, Chapter 6 6-7

7/27/2019 Dmp3e Ch06 Solutions 01.26.10 Final

http://slidepdf.com/reader/full/dmp3e-ch06-solutions-012610-final 8/39

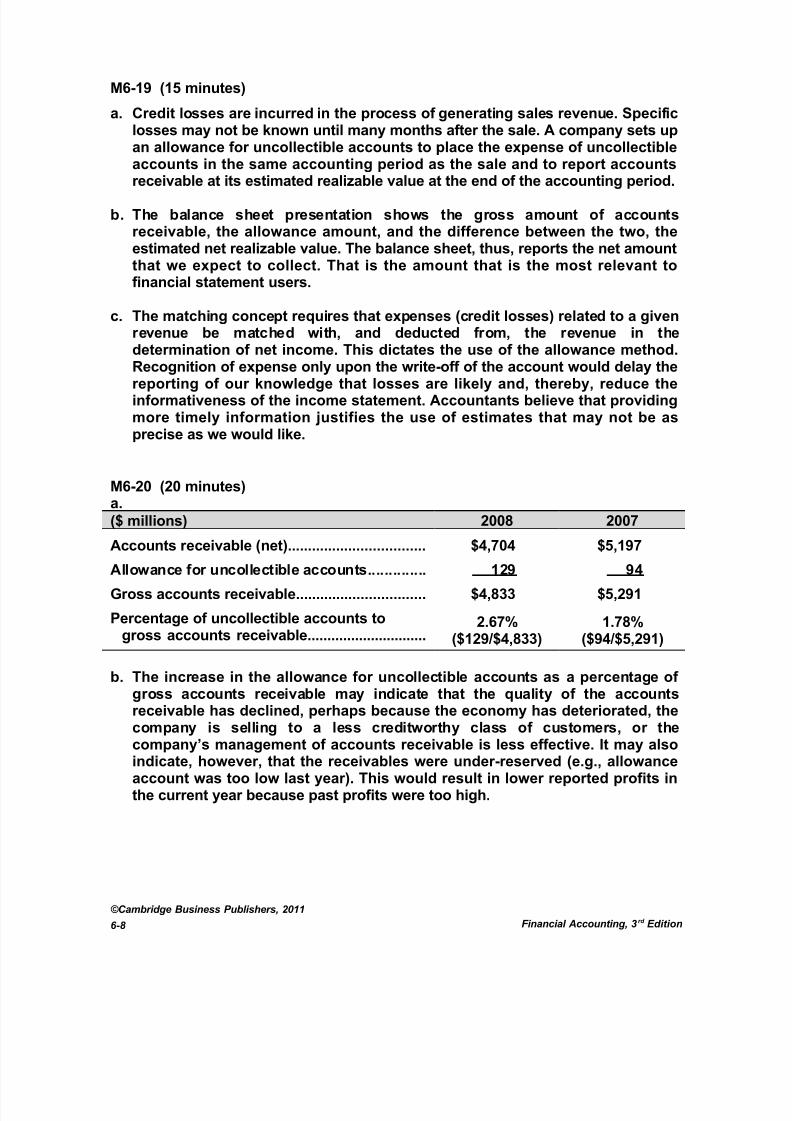

M6-19 (15 minutes)

a. Credit losses are incurred in the process of generating sales revenue. Specificlosses may not be known until many months after the sale. A company sets upan allowance for uncollectible accounts to place the expense of uncollectibleaccounts in the same accounting period as the sale and to report accounts

receivable at its estimated realizable value at the end of the accounting period.

b. The balance sheet presentation shows the gross amount of accountsreceivable, the allowance amount, and the difference between the two, theestimated net realizable value. The balance sheet, thus, reports the net amountthat we expect to collect. That is the amount that is the most relevant tofinancial statement users.

c. The matching concept requires that expenses (credit losses) related to a givenrevenue be matched with, and deducted from, the revenue in thedetermination of net income. This dictates the use of the allowance method.

Recognition of expense only upon the write-off of the account would delay thereporting of our knowledge that losses are likely and, thereby, reduce theinformativeness of the income statement. Accountants believe that providingmore timely information justifies the use of estimates that may not be asprecise as we would like.

M6-20 (20 minutes)a.($ millions) 2008 2007

Accounts receivable (net).................................. $4,704 $5,197

Allowance for uncollectible accounts.............. 129 94

Gross accounts receivable................................ $4,833 $5,291

Percentage of uncollectible accounts togross accounts receivable..............................

2.67%($129/$4,833)

1.78%($94/$5,291)

b. The increase in the allowance for uncollectible accounts as a percentage of gross accounts receivable may indicate that the quality of the accountsreceivable has declined, perhaps because the economy has deteriorated, thecompany is selling to a less creditworthy class of customers, or the

company’s management of accounts receivable is less effective. It may alsoindicate, however, that the receivables were under-reserved (e.g., allowanceaccount was too low last year). This would result in lower reported profits inthe current year because past profits were too high.

©Cambridge Business Publishers, 2011

Financial Accounting, 3rd Edition6-8

7/27/2019 Dmp3e Ch06 Solutions 01.26.10 Final

http://slidepdf.com/reader/full/dmp3e-ch06-solutions-012610-final 9/39

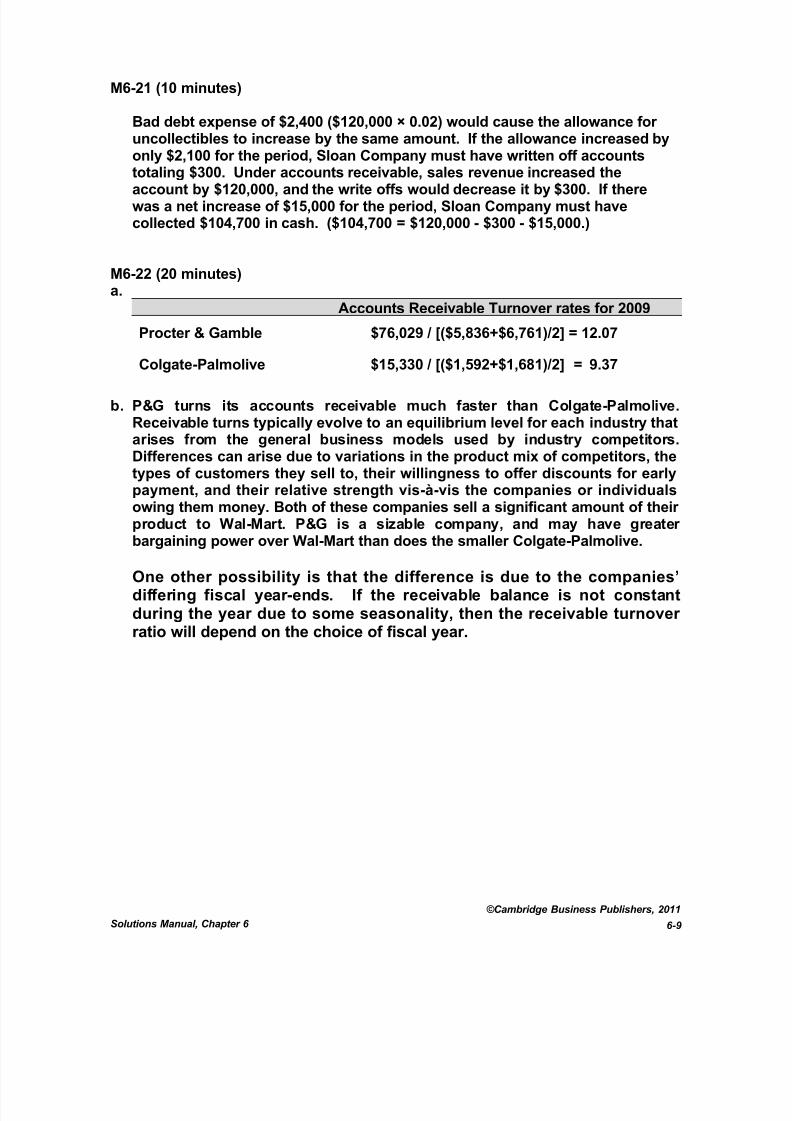

M6-21 (10 minutes)

Bad debt expense of $2,400 ($120,000 × 0.02) would cause the allowance for uncollectibles to increase by the same amount. If the allowance increased byonly $2,100 for the period, Sloan Company must have written off accountstotaling $300. Under accounts receivable, sales revenue increased the

account by $120,000, and the write offs would decrease it by $300. If therewas a net increase of $15,000 for the period, Sloan Company must havecollected $104,700 in cash. ($104,700 = $120,000 - $300 - $15,000.)

M6-22 (20 minutes)a.

Accounts Receivable Turnover rates for 2009

Procter & Gamble $76,029 / [($5,836+$6,761)/2] = 12.07

Colgate-Palmolive $15,330 / [($1,592+$1,681)/2] = 9.37

b. P&G turns its accounts receivable much faster than Colgate-Palmolive.Receivable turns typically evolve to an equilibrium level for each industry thatarises from the general business models used by industry competitors.Differences can arise due to variations in the product mix of competitors, thetypes of customers they sell to, their willingness to offer discounts for earlypayment, and their relative strength vis-à-vis the companies or individualsowing them money. Both of these companies sell a significant amount of their product to Wal-Mart. P&G is a sizable company, and may have greater bargaining power over Wal-Mart than does the smaller Colgate-Palmolive.

One other possibility is that the difference is due to the companies’differing fiscal year-ends. If the receivable balance is not constantduring the year due to some seasonality, then the receivable turnover ratio will depend on the choice of fiscal year.

©Cambridge Business Publishers, 2011

Solutions Manual, Chapter 6 6-9

7/27/2019 Dmp3e Ch06 Solutions 01.26.10 Final

http://slidepdf.com/reader/full/dmp3e-ch06-solutions-012610-final 10/39

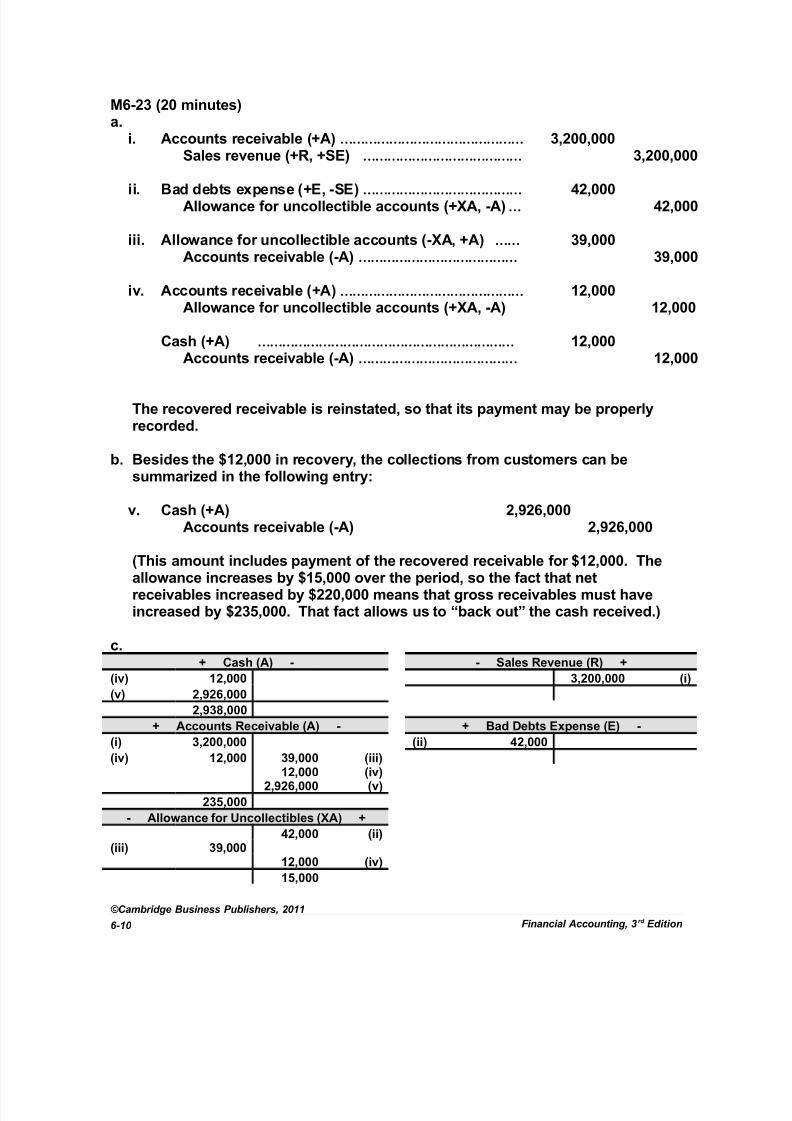

M6-23 (20 minutes)a.

i. Accounts receivable (+A)……………………………………… 3,200,000Sales revenue (+R, +SE) ………………………………… 3,200,000

ii. Bad debts expense (+E, -SE)………………………………… 42,000Allowance for uncollectible accounts (+XA, -A)… 42,000

iii. Allowance for uncollectible accounts (-XA, +A) …… 39,000Accounts receivable (-A)………………………………… 39,000

iv. Accounts receivable (+A)……………………………………… 12,000Allowance for uncollectible accounts (+XA, -A) 12,000

Cash (+A) ……………………………………………………… 12,000Accounts receivable (-A)………………………………… 12,000

The recovered receivable is reinstated, so that its payment may be properlyrecorded.

b. Besides the $12,000 in recovery, the collections from customers can besummarized in the following entry:

v. Cash (+A) 2,926,000Accounts receivable (-A) 2,926,000

(This amount includes payment of the recovered receivable for $12,000. Theallowance increases by $15,000 over the period, so the fact that netreceivables increased by $220,000 means that gross receivables must haveincreased by $235,000. That fact allows us to “back out” the cash received.)

c.+ Cash (A) - - Sales Revenue (R) +

(iv) 12,000 3,200,000 (i)

(v) 2,926,000

2,938,000

+ Accounts Receivable (A) - + Bad Debts Expense (E) -

(i) 3,200,000 (ii) 42,000(iv) 12,000 39,000 (iii)12,000 (iv)

2,926,000 (v)

235,000

- Allowance for Uncollectibles (XA) +

42,000 (ii)(iii) 39,000

12,000 (iv)

15,000

©Cambridge Business Publishers, 2011

Financial Accounting, 3rd Edition6-10

7/27/2019 Dmp3e Ch06 Solutions 01.26.10 Final

http://slidepdf.com/reader/full/dmp3e-ch06-solutions-012610-final 11/39

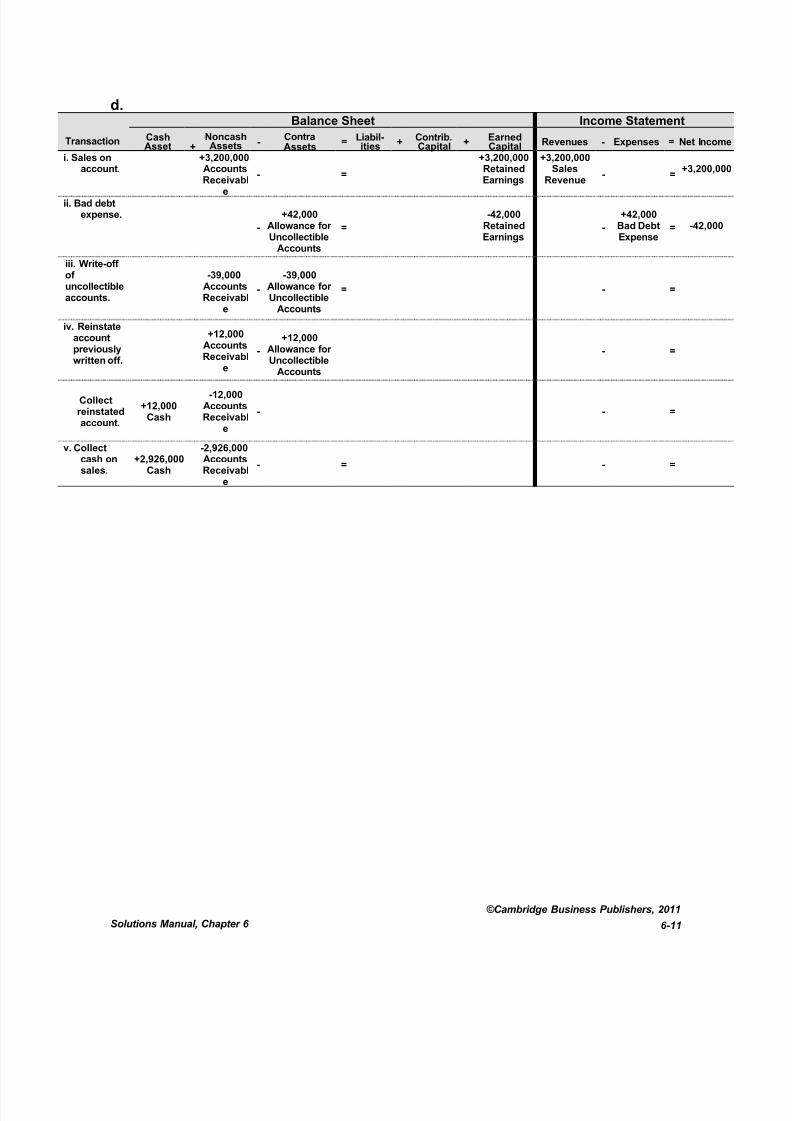

d.Balance Sheet Income Statement

Transaction CashAsset +

NoncashAssets -

ContraAssets

= Liabil-ities + Contrib.

Capital + EarnedCapital Revenues - Expenses = Net Incom

i. Sales onaccount.

+3,200,000AccountsReceivabl

e

- =

+3,200,000RetainedEarnings

+3,200,000Sales

Revenue- =

+3,200,00

ii. Bad debtexpense.

-

+42,000Allowance for Uncollectible

Accounts

=

-42,000RetainedEarnings

-

+42,000Bad DebtExpense

= -42,000

iii. Write-off of uncollectibleaccounts.

-39,000AccountsReceivabl

e

-

-39,000Allowance for Uncollectible

Accounts

= - =

iv. Reinstateaccountpreviouslywritten off.

+12,000AccountsReceivabl

e

-

+12,000Allowance for Uncollectible

Accounts

- =

Collectreinstatedaccount.

+12,000Cash

-12,000AccountsReceivabl

e

- - =

v. Collectcash onsales.

+2,926,000Cash

-2,926,000AccountsReceivabl

e

- = - =

©Cambridge Business Publishers, 2011

Solutions Manual, Chapter 6 6-11

7/27/2019 Dmp3e Ch06 Solutions 01.26.10 Final

http://slidepdf.com/reader/full/dmp3e-ch06-solutions-012610-final 12/39

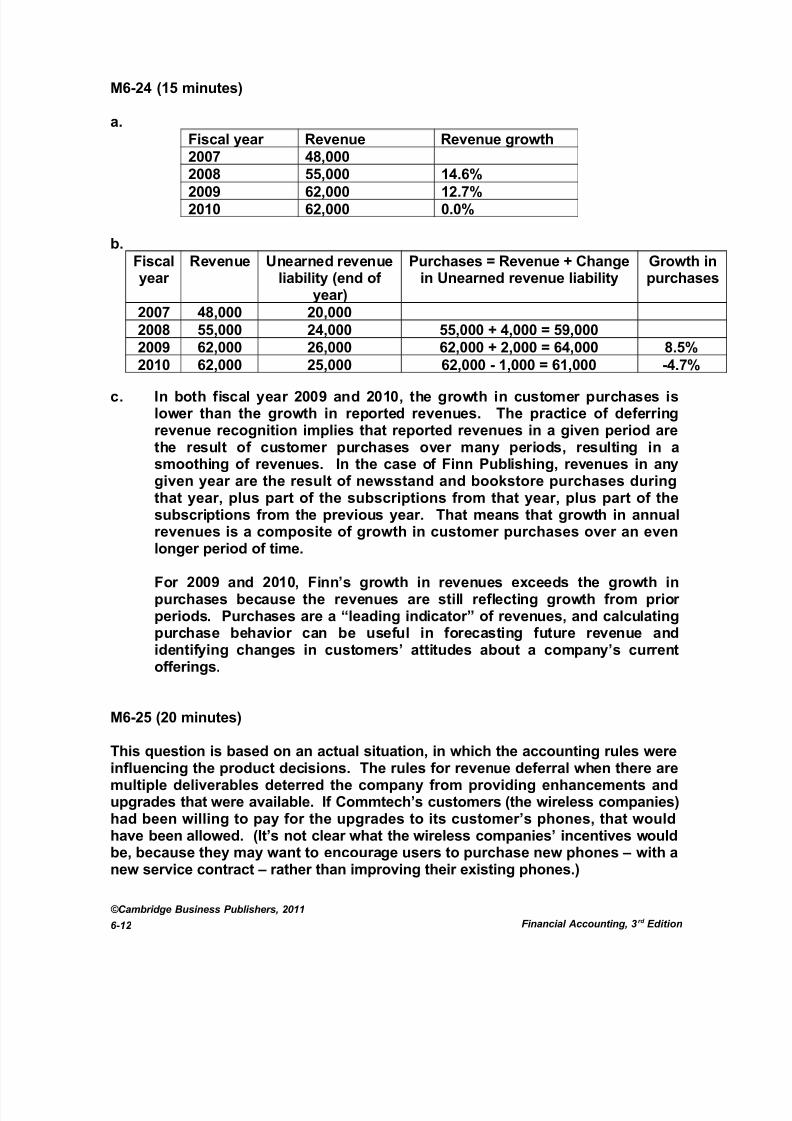

M6-24 (15 minutes)

a.Fiscal year Revenue Revenue growth2007 48,0002008 55,000 14.6%

2009 62,000 12.7%2010 62,000 0.0%

b.Fiscalyear

Revenue Unearned revenueliability (end of

year)

Purchases = Revenue + Changein Unearned revenue liability

Growth inpurchases

2007 48,000 20,0002008 55,000 24,000 55,000 + 4,000 = 59,0002009 62,000 26,000 62,000 + 2,000 = 64,000 8.5%2010 62,000 25,000 62,000 - 1,000 = 61,000 -4.7%

c. In both fiscal year 2009 and 2010, the growth in customer purchases islower than the growth in reported revenues. The practice of deferringrevenue recognition implies that reported revenues in a given period arethe result of customer purchases over many periods, resulting in asmoothing of revenues. In the case of Finn Publishing, revenues in anygiven year are the result of newsstand and bookstore purchases duringthat year, plus part of the subscriptions from that year, plus part of thesubscriptions from the previous year. That means that growth in annualrevenues is a composite of growth in customer purchases over an evenlonger period of time.

For 2009 and 2010, Finn’s growth in revenues exceeds the growth inpurchases because the revenues are still reflecting growth from prior periods. Purchases are a “leading indicator” of revenues, and calculatingpurchase behavior can be useful in forecasting future revenue andidentifying changes in customers’ attitudes about a company’s currentofferings.

M6-25 (20 minutes)

This question is based on an actual situation, in which the accounting rules wereinfluencing the product decisions. The rules for revenue deferral when there aremultiple deliverables deterred the company from providing enhancements andupgrades that were available. If Commtech’s customers (the wireless companies)had been willing to pay for the upgrades to its customer’s phones, that wouldhave been allowed. (It’s not clear what the wireless companies’ incentives wouldbe, because they may want to encourage users to purchase new phones – with anew service contract – rather than improving their existing phones.)

©Cambridge Business Publishers, 2011

Financial Accounting, 3rd Edition6-12

7/27/2019 Dmp3e Ch06 Solutions 01.26.10 Final

http://slidepdf.com/reader/full/dmp3e-ch06-solutions-012610-final 13/39

M6-25—continued.

The question can generate a discussion about whether accounting should drivedecisions. Whether it should or not, it does, so the question should evolve intowhat top management should do about this type of situation. Does the situationdescribed in the problem require some managerial action, or not. Is the company

foregoing sales because of its accounting? Within Commtech, the finance staff was skeptical of marketing’s predictions that the upgrades and enhancementswould increase the sales of existing phone models. If the upgrades andenhancements are delivered, Commtech will have to change its accounting for revenue, with a resulting decrease in near-term profitability. How might thecompany communicate that change in a way that the investing public willunderstand as a net benefit to the company?

©Cambridge Business Publishers, 2011

Solutions Manual, Chapter 6 6-13

7/27/2019 Dmp3e Ch06 Solutions 01.26.10 Final

http://slidepdf.com/reader/full/dmp3e-ch06-solutions-012610-final 14/39

EXERCISES

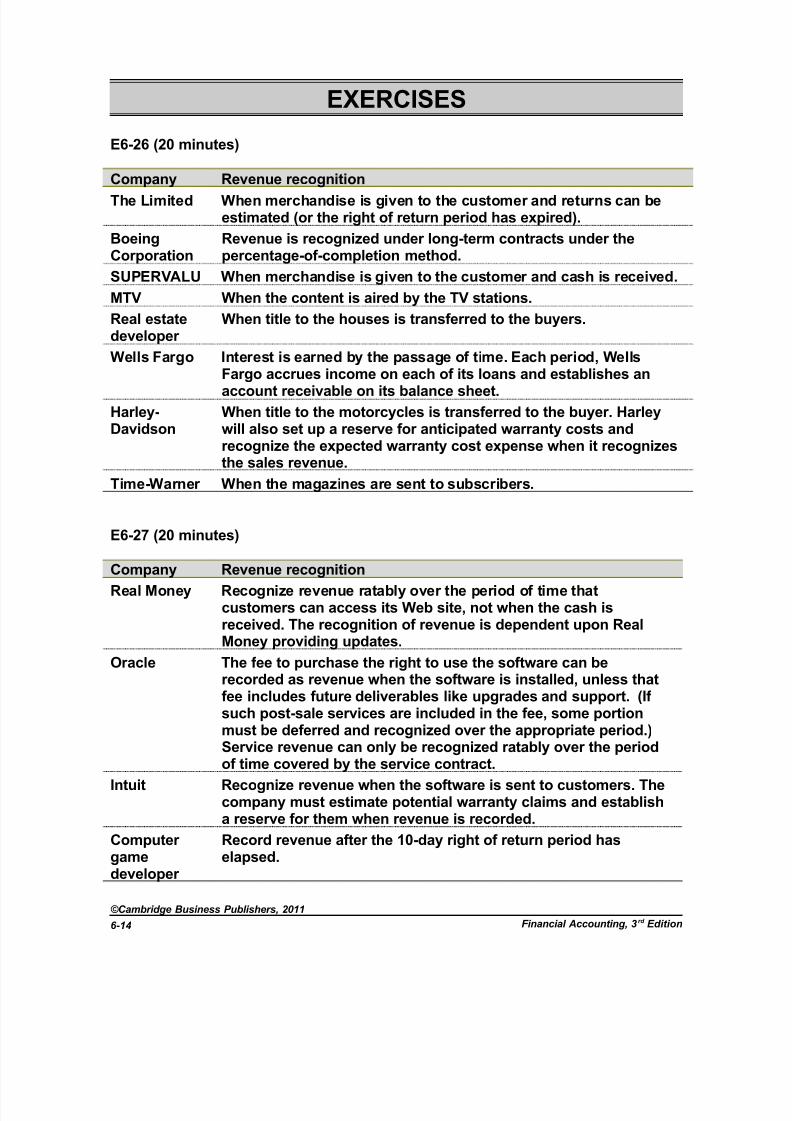

E6-26 (20 minutes)

Company Revenue recognitionThe Limited When merchandise is given to the customer and returns can be

estimated (or the right of return period has expired).

BoeingCorporation

Revenue is recognized under long-term contracts under thepercentage-of-completion method.

SUPERVALU When merchandise is given to the customer and cash is received.

MTV When the content is aired by the TV stations.

Real estatedeveloper

When title to the houses is transferred to the buyers.

Wells Fargo Interest is earned by the passage of time. Each period, Wells

Fargo accrues income on each of its loans and establishes anaccount receivable on its balance sheet.

Harley-Davidson

When title to the motorcycles is transferred to the buyer. Harleywill also set up a reserve for anticipated warranty costs andrecognize the expected warranty cost expense when it recognizesthe sales revenue.

Time-Warner When the magazines are sent to subscribers.

E6-27 (20 minutes)

Company Revenue recognition

Real Money Recognize revenue ratably over the period of time thatcustomers can access its Web site, not when the cash isreceived. The recognition of revenue is dependent upon RealMoney providing updates.

Oracle The fee to purchase the right to use the software can berecorded as revenue when the software is installed, unless thatfee includes future deliverables like upgrades and support. (If such post-sale services are included in the fee, some portionmust be deferred and recognized over the appropriate period.)

Service revenue can only be recognized ratably over the periodof time covered by the service contract.

Intuit Recognize revenue when the software is sent to customers. Thecompany must estimate potential warranty claims and establisha reserve for them when revenue is recorded.

Computer gamedeveloper

Record revenue after the 10-day right of return period haselapsed.

©Cambridge Business Publishers, 2011

Financial Accounting, 3rd Edition6-14

7/27/2019 Dmp3e Ch06 Solutions 01.26.10 Final

http://slidepdf.com/reader/full/dmp3e-ch06-solutions-012610-final 15/39

©Cambridge Business Publishers, 2011

Solutions Manual, Chapter 6 6-15

7/27/2019 Dmp3e Ch06 Solutions 01.26.10 Final

http://slidepdf.com/reader/full/dmp3e-ch06-solutions-012610-final 16/39

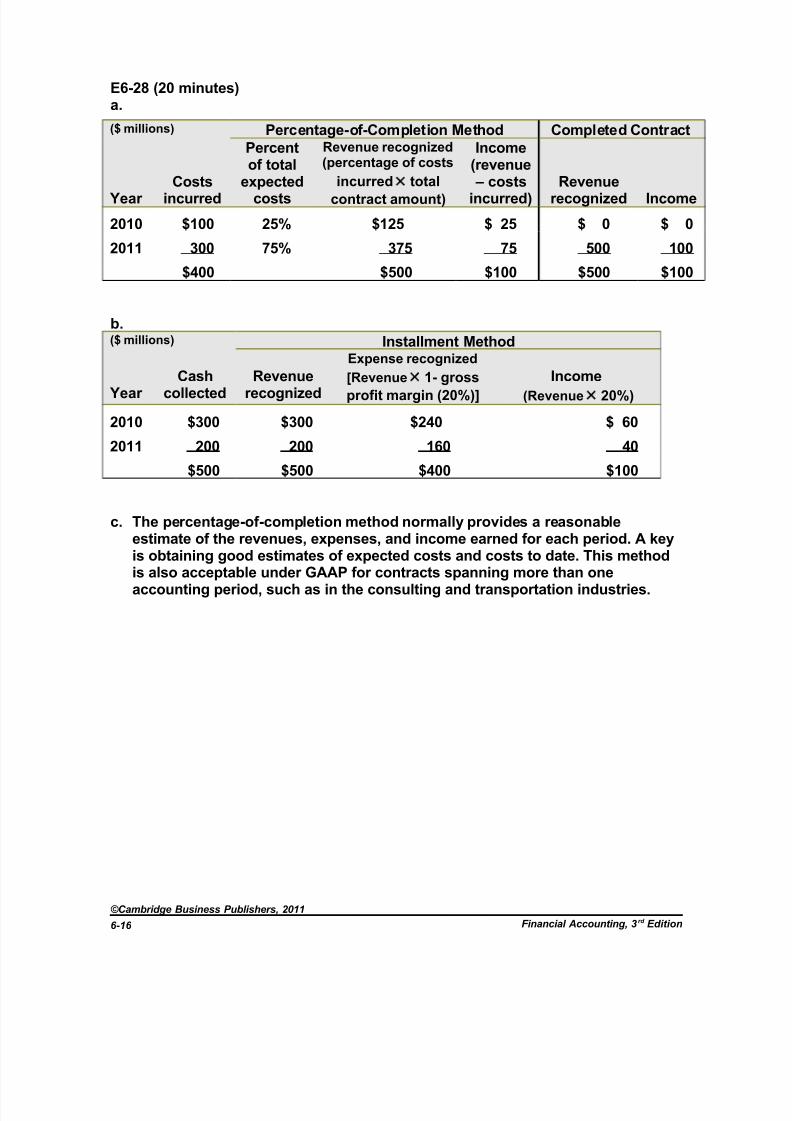

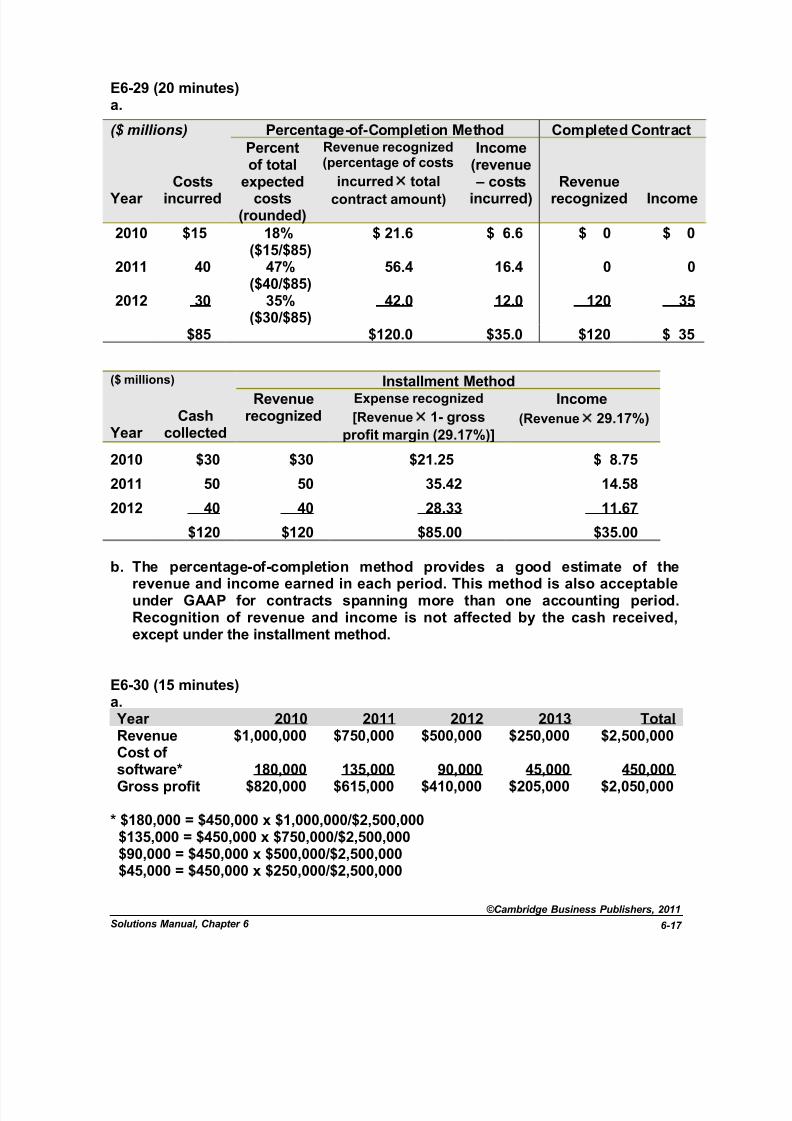

E6-28 (20 minutes)a.

($ millions) Percentage-of-Completion Method Completed Contract

Year Costsincurred

Percentof total

expectedcosts

Revenue recognized(percentage of costs

incurred×

totalcontract amount)

Income(revenue

– costsincurred) Revenuerecognized Income

2010 $100 25% $125 $ 25 $ 0 $ 0

2011 300 75% 375 75 500 100

$400 $500 $100 $500 $100

b.($ millions) Installment Method

Year Cash

collectedRevenue

recognized

Expense recognized

[Revenue × 1- grossprofit margin (20%)]

Income(Revenue × 20%)

2010 $300 $300 $240 $ 60

2011 200 200 160 40

$500 $500 $400 $100

c. The percentage-of-completion method normally provides a reasonableestimate of the revenues, expenses, and income earned for each period. A key

is obtaining good estimates of expected costs and costs to date. This methodis also acceptable under GAAP for contracts spanning more than oneaccounting period, such as in the consulting and transportation industries.

©Cambridge Business Publishers, 2011

Financial Accounting, 3rd Edition6-16

7/27/2019 Dmp3e Ch06 Solutions 01.26.10 Final

http://slidepdf.com/reader/full/dmp3e-ch06-solutions-012610-final 17/39

7/27/2019 Dmp3e Ch06 Solutions 01.26.10 Final

http://slidepdf.com/reader/full/dmp3e-ch06-solutions-012610-final 18/39

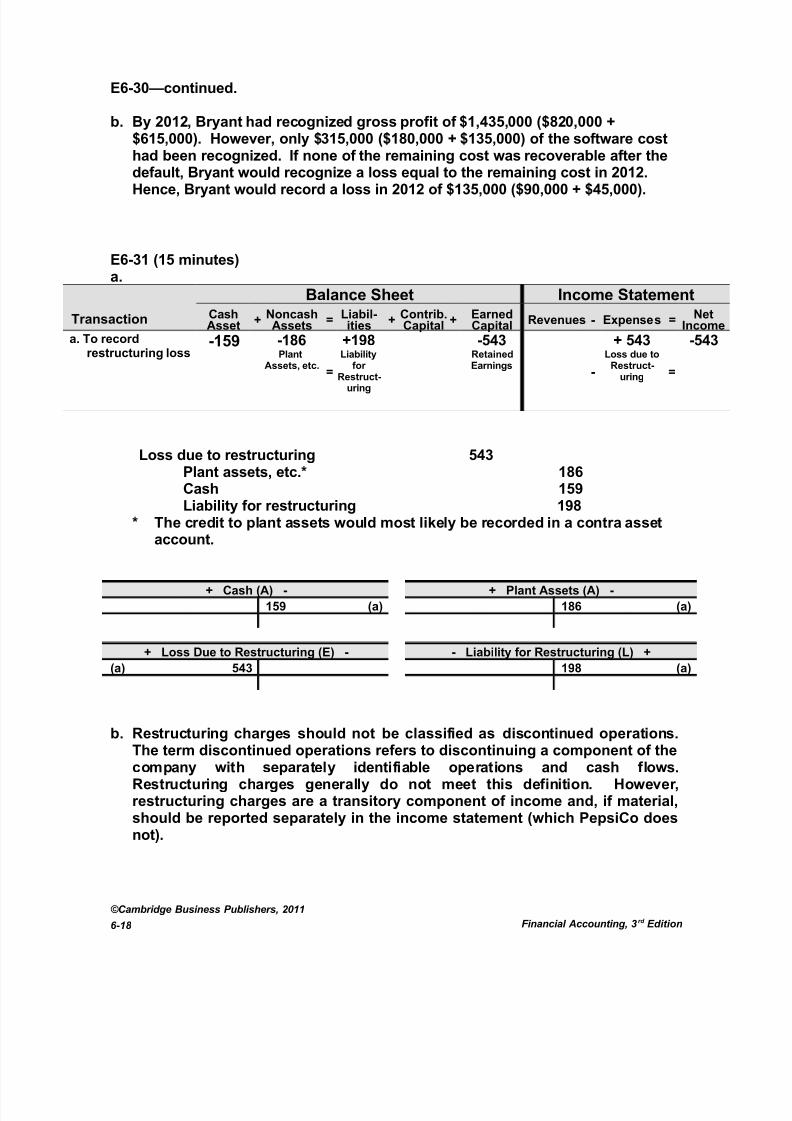

E6-30—continued.

b. By 2012, Bryant had recognized gross profit of $1,435,000 ($820,000 +$615,000). However, only $315,000 ($180,000 + $135,000) of the software costhad been recognized. If none of the remaining cost was recoverable after thedefault, Bryant would recognize a loss equal to the remaining cost in 2012.

Hence, Bryant would record a loss in 2012 of $135,000 ($90,000 + $45,000).

E6-31 (15 minutes)a.

Balance Sheet Income Statement

Transaction CashAsset + Noncash

Assets = Liabil-ities + Contrib.

Capital + EarnedCapital Revenues - Expenses = Net

Incomea. To record

restructuring loss-159 -186

PlantAssets, etc.

=

+198Liability

for

Restruct-uring

-543RetainedEarnings

-

+ 543Loss due to

Restruct-

uring =

-543

Loss due to restructuring 543Plant assets, etc.*Cash

186159

Liability for restructuring 198* The credit to plant assets would most likely be recorded in a contra asset

account.

+ Cash (A) - + Plant Assets (A) -

159 (a) 186 (a)

+ Loss Due to Restructuring (E) - - Liability for Restructuring (L) +

(a) 543 198 (a)

b. Restructuring charges should not be classified as discontinued operations.

The term discontinued operations refers to discontinuing a component of thecompany with separately identifiable operations and cash flows.Restructuring charges generally do not meet this definition. However,restructuring charges are a transitory component of income and, if material,should be reported separately in the income statement (which PepsiCo doesnot).

©Cambridge Business Publishers, 2011

Financial Accounting, 3rd Edition6-18

7/27/2019 Dmp3e Ch06 Solutions 01.26.10 Final

http://slidepdf.com/reader/full/dmp3e-ch06-solutions-012610-final 19/39

7/27/2019 Dmp3e Ch06 Solutions 01.26.10 Final

http://slidepdf.com/reader/full/dmp3e-ch06-solutions-012610-final 20/39

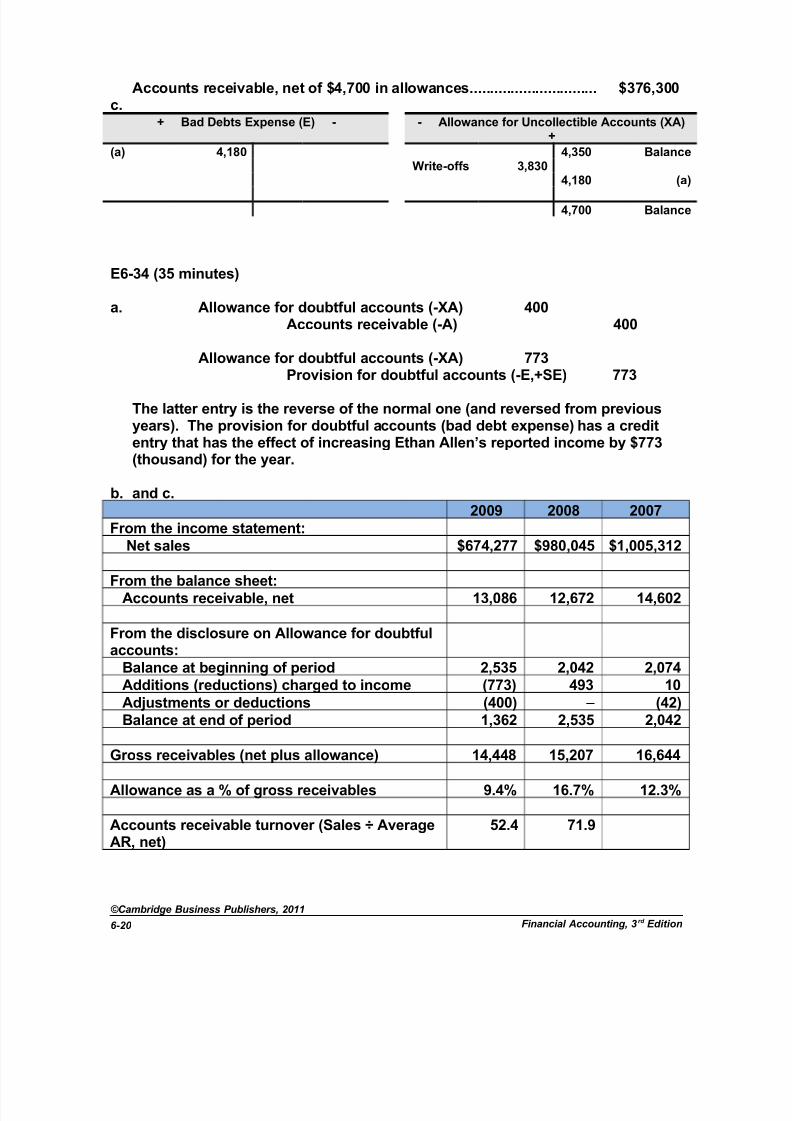

Accounts receivable, net of $4,700 in allowances............................... $376,300c.

+ Bad Debts Expense (E) - - Allowance for Uncollectible Accounts (XA)+

(a) 4,180 4,350 BalanceWrite-offs 3,830

4,180 (a)

4,700 Balance

E6-34 (35 minutes)

a. Allowance for doubtful accounts (-XA) 400Accounts receivable (-A) 400

Allowance for doubtful accounts (-XA) 773

Provision for doubtful accounts (-E,+SE) 773

The latter entry is the reverse of the normal one (and reversed from previousyears). The provision for doubtful accounts (bad debt expense) has a creditentry that has the effect of increasing Ethan Allen’s reported income by $773(thousand) for the year.

b. and c.2009 2008 2007

From the income statement:Net sales $674,277 $980,045 $1,005,312

From the balance sheet:Accounts receivable, net 13,086 12,672 14,602

From the disclosure on Allowance for doubtfulaccounts:

Balance at beginning of period 2,535 2,042 2,074Additions (reductions) charged to income (773) 493 10Adjustments or deductions (400) – (42)Balance at end of period 1,362 2,535 2,042

Gross receivables (net plus allowance) 14,448 15,207 16,644

Allowance as a % of gross receivables 9.4% 16.7% 12.3%

Accounts receivable turnover (Sales ÷ AverageAR, net)

52.4 71.9

©Cambridge Business Publishers, 2011

Financial Accounting, 3rd Edition6-20

7/27/2019 Dmp3e Ch06 Solutions 01.26.10 Final

http://slidepdf.com/reader/full/dmp3e-ch06-solutions-012610-final 21/39

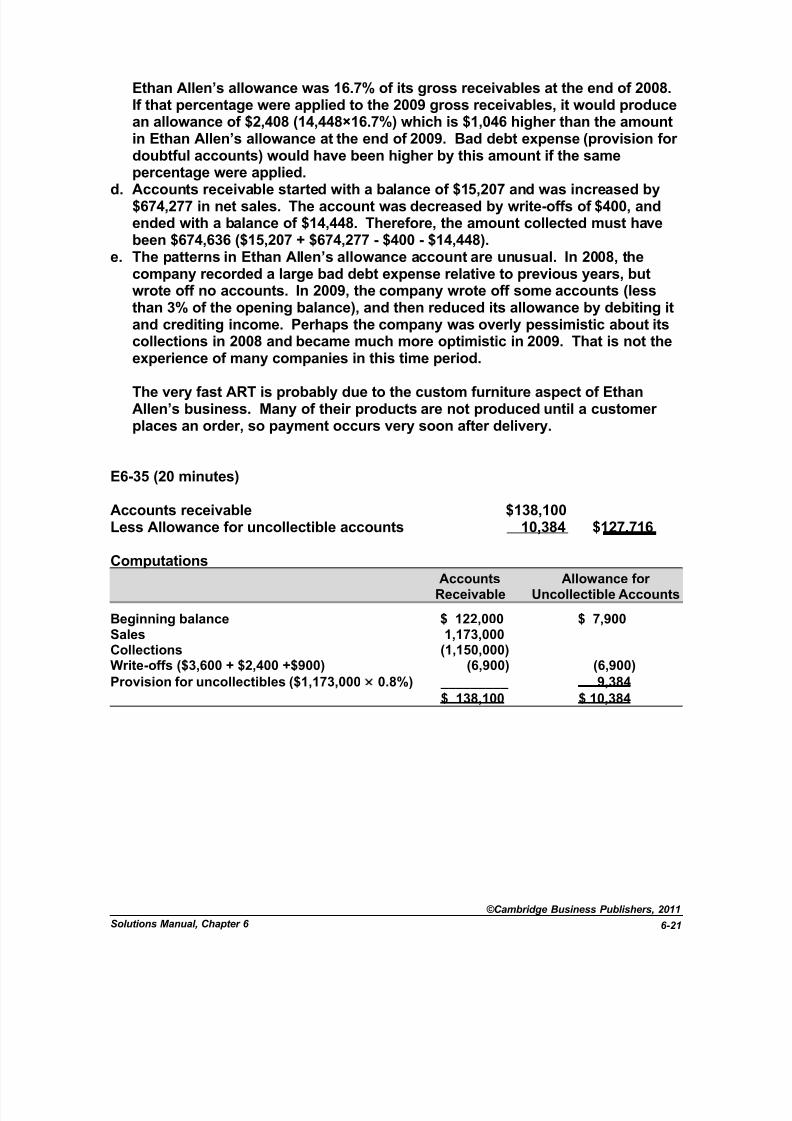

Ethan Allen’s allowance was 16.7% of its gross receivables at the end of 2008.If that percentage were applied to the 2009 gross receivables, it would producean allowance of $2,408 (14,448×16.7%) which is $1,046 higher than the amountin Ethan Allen’s allowance at the end of 2009. Bad debt expense (provision for doubtful accounts) would have been higher by this amount if the samepercentage were applied.

d. Accounts receivable started with a balance of $15,207 and was increased by$674,277 in net sales. The account was decreased by write-offs of $400, andended with a balance of $14,448. Therefore, the amount collected must havebeen $674,636 ($15,207 + $674,277 - $400 - $14,448).

e. The patterns in Ethan Allen’s allowance account are unusual. In 2008, thecompany recorded a large bad debt expense relative to previous years, butwrote off no accounts. In 2009, the company wrote off some accounts (lessthan 3% of the opening balance), and then reduced its allowance by debiting itand crediting income. Perhaps the company was overly pessimistic about itscollections in 2008 and became much more optimistic in 2009. That is not theexperience of many companies in this time period.

The very fast ART is probably due to the custom furniture aspect of EthanAllen’s business. Many of their products are not produced until a customer places an order, so payment occurs very soon after delivery.

E6-35 (20 minutes)

Accounts receivable $138,100Less Allowance for uncollectible accounts 10,384 $127,716

Computations Accounts Allowance for Receivable Uncollectible Accounts

Beginning balance $ 122,000 $ 7,900Sales 1,173,000Collections (1,150,000)Write-offs ($3,600 + $2,400 +$900) (6,900) (6,900)Provision for uncollectibles ($1,173,000 × 0.8%) _________ 9,384

$ 138,100 $ 10,384

©Cambridge Business Publishers, 2011

Solutions Manual, Chapter 6 6-21

7/27/2019 Dmp3e Ch06 Solutions 01.26.10 Final

http://slidepdf.com/reader/full/dmp3e-ch06-solutions-012610-final 22/39

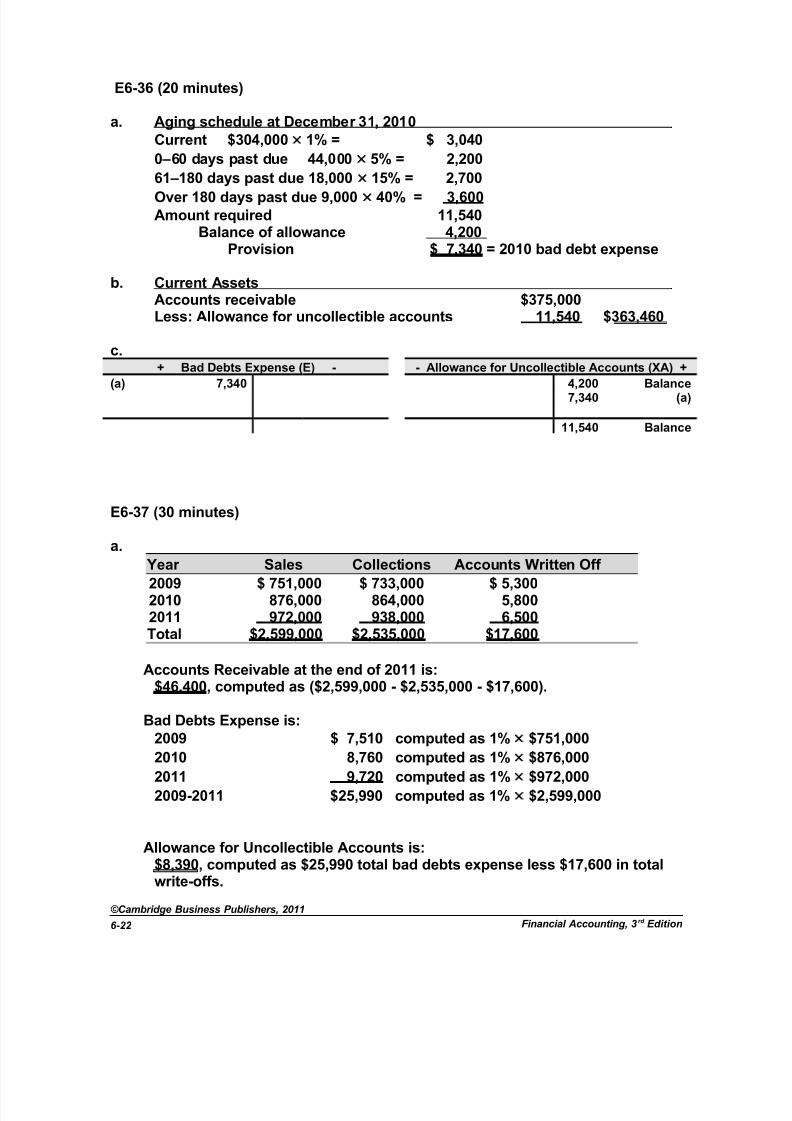

E6-36 (20 minutes)

a. Aging schedule at December 31, 2010Current $304,000 × 1% = $ 3,040

0–60 days past due 44,000 × 5% = 2,200

61–180 days past due 18,000 × 15% = 2,700

Over 180 days past due 9,000 × 40% = 3,600Amount required 11,540

Balance of allowance 4,200Provision $ 7,340 = 2010 bad debt expense

b. Current AssetsAccounts receivable $375,000Less: Allowance for uncollectible accounts 11,540 $363,460

c.

+ Bad Debts Expense (E) - - Allowance for Uncollectible Accounts (XA) +(a) 7,340 4,200 Balance7,340 (a)

11,540 Balance

E6-37 (30 minutes)

a.

Year Sales Collections Accounts Written Off 2009 $ 751,000 $ 733,000 $ 5,3002010 876,000 864,000 5,8002011 972,000 938,000 6,500Total $2,599,000 $2,535,000 $17,600

Accounts Receivable at the end of 2011 is:$46,400, computed as ($2,599,000 - $2,535,000 - $17,600).

Bad Debts Expense is:2009 $ 7,510 computed as 1% × $751,000

2010 8,760 computed as 1% × $876,000

2011 9,720 computed as 1% × $972,000

2009-2011 $25,990 computed as 1% × $2,599,000

Allowance for Uncollectible Accounts is:$8,390, computed as $25,990 total bad debts expense less $17,600 in totalwrite-offs.

©Cambridge Business Publishers, 2011

Financial Accounting, 3rd Edition6-22

7/27/2019 Dmp3e Ch06 Solutions 01.26.10 Final

http://slidepdf.com/reader/full/dmp3e-ch06-solutions-012610-final 23/39

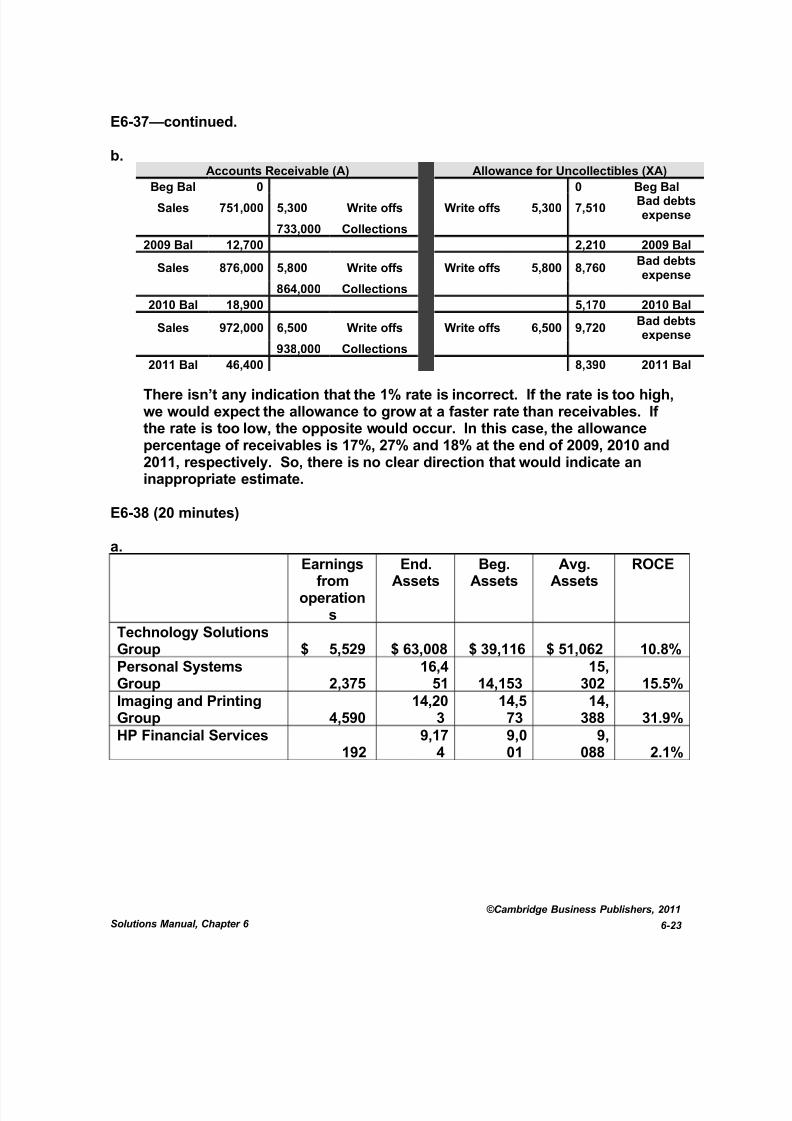

E6-37—continued.

b.Accounts Receivable (A) Allowance for Uncollectibles (XA)

Beg Bal 0 0 Beg Bal

Sales 751,000 5,300 Write offs Write offs 5,300 7,510Bad debtsexpense

733,000 Collections

2009 Bal 12,700 2,210 2009 Bal

Sales 876,000 5,800 Write offs Write offs 5,800 8,760Bad debtsexpense

864,000 Collections

2010 Bal 18,900 5,170 2010 Bal

Sales 972,000 6,500 Write offs Write offs 6,500 9,720Bad debtsexpense

938,000 Collections

2011 Bal 46,400 8,390 2011 Bal

There isn’t any indication that the 1% rate is incorrect. If the rate is too high,we would expect the allowance to grow at a faster rate than receivables. If the rate is too low, the opposite would occur. In this case, the allowancepercentage of receivables is 17%, 27% and 18% at the end of 2009, 2010 and2011, respectively. So, there is no clear direction that would indicate aninappropriate estimate.

E6-38 (20 minutes)

a.

Earningsfrom

operations

End.Assets

Beg.Assets

Avg.Assets

ROCE

Technology SolutionsGroup $ 5,529 $ 63,008 $ 39,116 $ 51,062 10.8%Personal SystemsGroup 2,375

16,451 14,153

15,302 15.5%

Imaging and PrintingGroup 4,590

14,203

14,573

14,388 31.9%

HP Financial Services

192

9,17

4

9,0

01

9,

088 2.1%

©Cambridge Business Publishers, 2011

Solutions Manual, Chapter 6 6-23

7/27/2019 Dmp3e Ch06 Solutions 01.26.10 Final

http://slidepdf.com/reader/full/dmp3e-ch06-solutions-012610-final 24/39

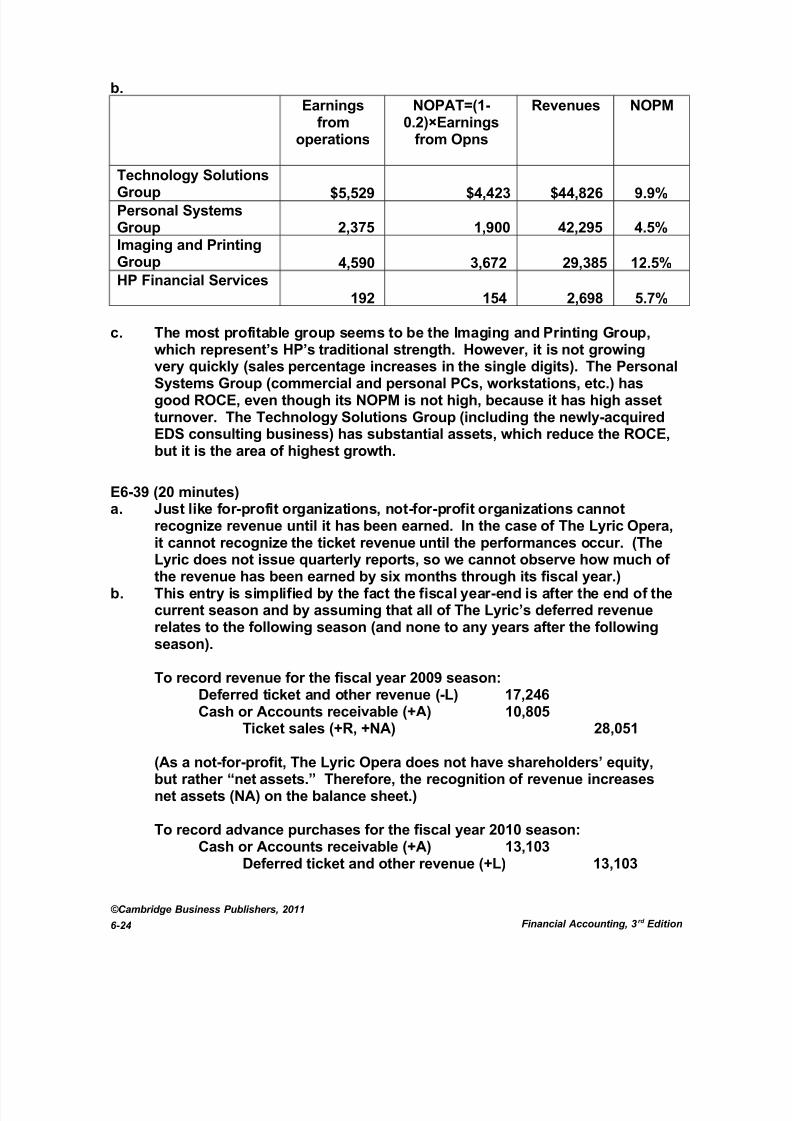

b.Earnings

fromoperations

NOPAT=(1-0.2)×Earnings

from Opns

Revenues NOPM

Technology SolutionsGroup $5,529 $4,423 $44,826 9.9%Personal SystemsGroup 2,375 1,900 42,295 4.5%Imaging and PrintingGroup 4,590 3,672 29,385 12.5%HP Financial Services

192 154 2,698 5.7%

c. The most profitable group seems to be the Imaging and Printing Group,which represent’s HP’s traditional strength. However, it is not growing

very quickly (sales percentage increases in the single digits). The PersonalSystems Group (commercial and personal PCs, workstations, etc.) hasgood ROCE, even though its NOPM is not high, because it has high assetturnover. The Technology Solutions Group (including the newly-acquiredEDS consulting business) has substantial assets, which reduce the ROCE,but it is the area of highest growth.

E6-39 (20 minutes)a. Just like for-profit organizations, not-for-profit organizations cannot

recognize revenue until it has been earned. In the case of The Lyric Opera,it cannot recognize the ticket revenue until the performances occur. (The

Lyric does not issue quarterly reports, so we cannot observe how much of the revenue has been earned by six months through its fiscal year.)

b. This entry is simplified by the fact the fiscal year-end is after the end of thecurrent season and by assuming that all of The Lyric’s deferred revenuerelates to the following season (and none to any years after the followingseason).

To record revenue for the fiscal year 2009 season:Deferred ticket and other revenue (-L) 17,246Cash or Accounts receivable (+A) 10,805

Ticket sales (+R, +NA) 28,051

(As a not-for-profit, The Lyric Opera does not have shareholders’ equity,but rather “net assets.” Therefore, the recognition of revenue increasesnet assets (NA) on the balance sheet.)

To record advance purchases for the fiscal year 2010 season:Cash or Accounts receivable (+A) 13,103

Deferred ticket and other revenue (+L) 13,103

©Cambridge Business Publishers, 2011

Financial Accounting, 3rd Edition6-24

7/27/2019 Dmp3e Ch06 Solutions 01.26.10 Final

http://slidepdf.com/reader/full/dmp3e-ch06-solutions-012610-final 25/39

c. It’s likely that the downturn in the economy caused some subscribers notto renew (or to wait until after April 30 to renew). It’s possible that thedecline in advance purchases is a statement about the opera selections for the 2009-10 season. However, the loyal subscriber base (and the desire tokeep one’s assigned seating) makes the economy a more likely cause.

d. The Lyric Opera usually operates at close to seating capacity. And, in a

typical year, approximately 60% of its seats are sold by the April 30thpreceding the season. So, the quantity of unsold seats will affect TheLyric’s marketing efforts for subscribers who have not yet renewed,outreach to new potential subscribers and promotions for individual ticketswhich go on sale shortly before the season. Those efforts can be scaledup or down depending on the experience with advance sales.

©Cambridge Business Publishers, 2011

Solutions Manual, Chapter 6 6-25

7/27/2019 Dmp3e Ch06 Solutions 01.26.10 Final

http://slidepdf.com/reader/full/dmp3e-ch06-solutions-012610-final 26/39

PROBLEMS

P6-40A (20 minutes)

a. The following items might be considered to be operating:

1. Net Sales, cost of sales, R&D expenses, and SG&A expenses are typicallydesignated as operating.

2. Amortization of intangible assets and restructuring charges would usually beconsidered to be operating under the assumptions that the acquisition thatgave rise to the intangible assets is included as part of operations, and thatthe restructuring did not involve discontinuation of distinct parts of thebusiness.

3. The asbestos-related credit would be considered to be operating since it isrelated to Dow Chemical’s operating activities. The same is true of thegoodwill impairment losses. (These items are both operating and transitory –see b.)

4. Purchased in-process research and development charges and Acquisition-related expenses are caused by the company’s investing activities, and wouldbe considered nonoperating.

5. Equity in earnings of nonconsolidated affiliates would be consideredoperating under the assumption that the affiliates are related to Dow’s coreoperations, which is typically the case.

6. Sundry income would generally be considered nonoperating in the absence of a footnote clearly indicating its connection to the operating activities of thecompany.

7. Interest income (expense) is considered nonoperating

8. Minority interests’ share in income is nonoperating as it relates to equity thatis nonoperating. Due to changes discussed in Chapter 12, Dow’s 2009 incomestatement will not show Minority interest in the determination of net income.

b. The following items might be identified as transitory items:

1. Purchased in-process research and development and Acquisition-related expenses – these are one-time (e.g., transitory) costs incurred in connectionwith the acquisition of another company and can properly be expensed under GAAP.

2. Asbestos-related credit – this is a reversal of a previous accrual for litigation

in connection with asbestos-related lawsuits. GAAP requires such an accrualif the loss is probable and can be reasonably estimated. Since it is a one-timeoccurrence, it can be considered to be a transitory item.

3. Goodwill impairment losses – this loss results from changes in expectationsof the performance of past acquisitions. It would be considered operating, buttransitory.

4. Restructuring charges – these relate to the company’s actions due to theeconomic decline in 2008 and the expectations that future performance will

©Cambridge Business Publishers, 2011

Financial Accounting, 3rd Edition6-26

7/27/2019 Dmp3e Ch06 Solutions 01.26.10 Final

http://slidepdf.com/reader/full/dmp3e-ch06-solutions-012610-final 27/39

not meet prior expectations. Restructuring costs are considered “specialitems,” meaning that individually they are transitory, but as a category, theyhappen frequently. (Dow had restructuring charges – from other causes – of $578 million and $591 million in 2007 and 2006, respectively.)

We would need to examine prior years’ income statements to discern if the other

categories in Dow’s income statement are to be considered transitory.

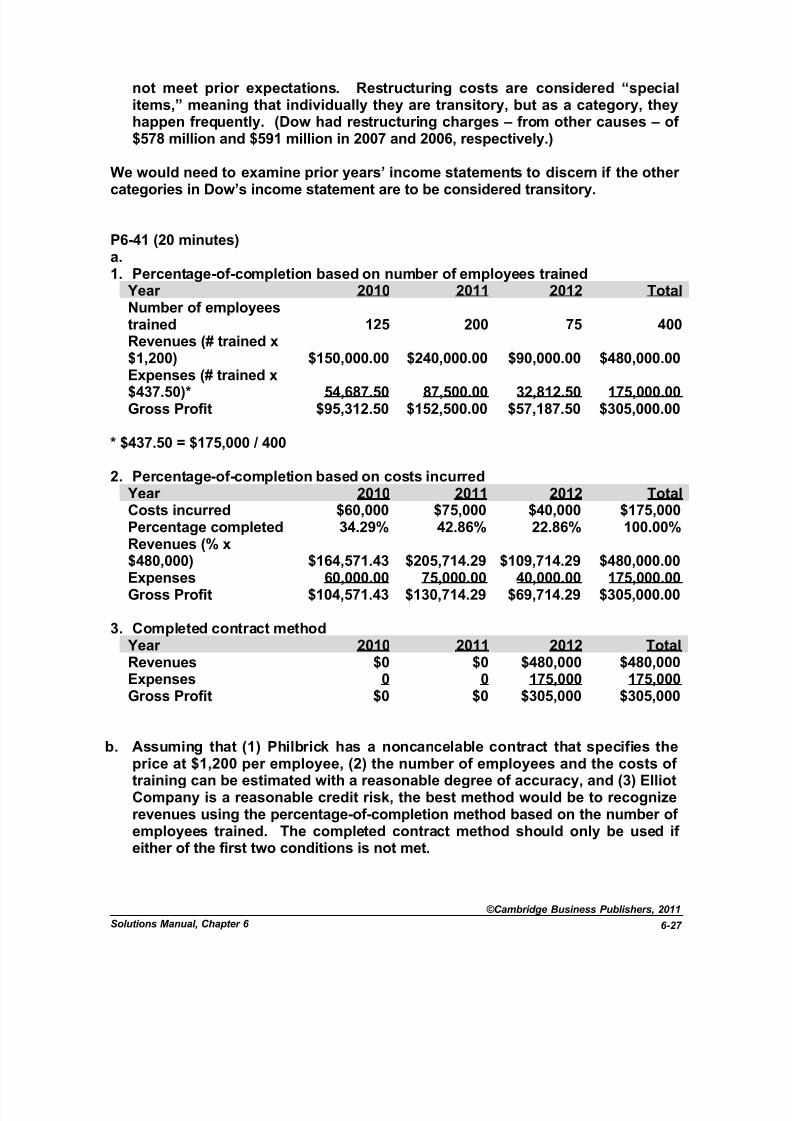

P6-41 (20 minutes)a.1. Percentage-of-completion based on number of employees trained

Year 2010 2011 2012 TotalNumber of employeestrained 125 200 75 400Revenues (# trained x$1,200) $150,000.00 $240,000.00 $90,000.00 $480,000.00

Expenses (# trained x$437.50)* 54,687.50 87,500.00 32,812.50 175,000.00Gross Profit $95,312.50 $152,500.00 $57,187.50 $305,000.00

* $437.50 = $175,000 / 400

2. Percentage-of-completion based on costs incurred Year 2010 2011 2012 TotalCosts incurred $60,000 $75,000 $40,000 $175,000Percentage completed 34.29% 42.86% 22.86% 100.00%Revenues (% x

$480,000) $164,571.43 $205,714.29 $109,714.29 $480,000.00Expenses 60,000.00 75,000.00 40,000.00 175,000.00Gross Profit $104,571.43 $130,714.29 $69,714.29 $305,000.00

3. Completed contract method Year 2010 2011 2012 TotalRevenues $0 $0 $480,000 $480,000Expenses 0 0 175,000 175,000Gross Profit $0 $0 $305,000 $305,000

b. Assuming that (1) Philbrick has a noncancelable contract that specifies theprice at $1,200 per employee, (2) the number of employees and the costs of training can be estimated with a reasonable degree of accuracy, and (3) ElliotCompany is a reasonable credit risk, the best method would be to recognizerevenues using the percentage-of-completion method based on the number of employees trained. The completed contract method should only be used if either of the first two conditions is not met.

©Cambridge Business Publishers, 2011

Solutions Manual, Chapter 6 6-27

7/27/2019 Dmp3e Ch06 Solutions 01.26.10 Final

http://slidepdf.com/reader/full/dmp3e-ch06-solutions-012610-final 28/39

P6-42 (15 minutes)

a. Management would have an incentive to shift $1 million of income from thecurrent period into next. This might be accomplished by delaying revenuerecognition or accelerating expenses. This would increase their bonus by$100,000 next year without decreasing the current bonus.

b. Management would have an incentive to shift $3 million of income from nextyear into income reported this year. This would increase the current year bonus by $300,000 without reducing next year’s bonus.

c. Management would have an incentive to shift income from the current year into next year. Even though this would reduce earnings this year, earningsare already so low that management does not expect to receive a bonus.Shifting earnings into a future period increases the bonus in that period.

d. These incentives for earnings management would be mitigated if the “kinks”

in the bonus formula were removed. Alternatively, some companies paybonuses based on a three-year moving average of earnings to minimize theimpact of earnings management.

This problem can provide an opportunity to discuss the “slippery slope” of earnings management. For example, management’s optimism about next year inpart b may not turn out to be warranted. Suppose next year’s “natural” earningsturns out to be $20 million instead of $24 million. Management’s action in thefirst year will have reduced next year’s $20 million to $17 million, and earningsmanagement would again be required to meet the target. And, if meeting thetarget in one year causes the next year’s target to increase, things can get out of

control very quickly.

©Cambridge Business Publishers, 2011

Financial Accounting, 3rd Edition6-28

7/27/2019 Dmp3e Ch06 Solutions 01.26.10 Final

http://slidepdf.com/reader/full/dmp3e-ch06-solutions-012610-final 29/39

P6-43 (30 minutes)

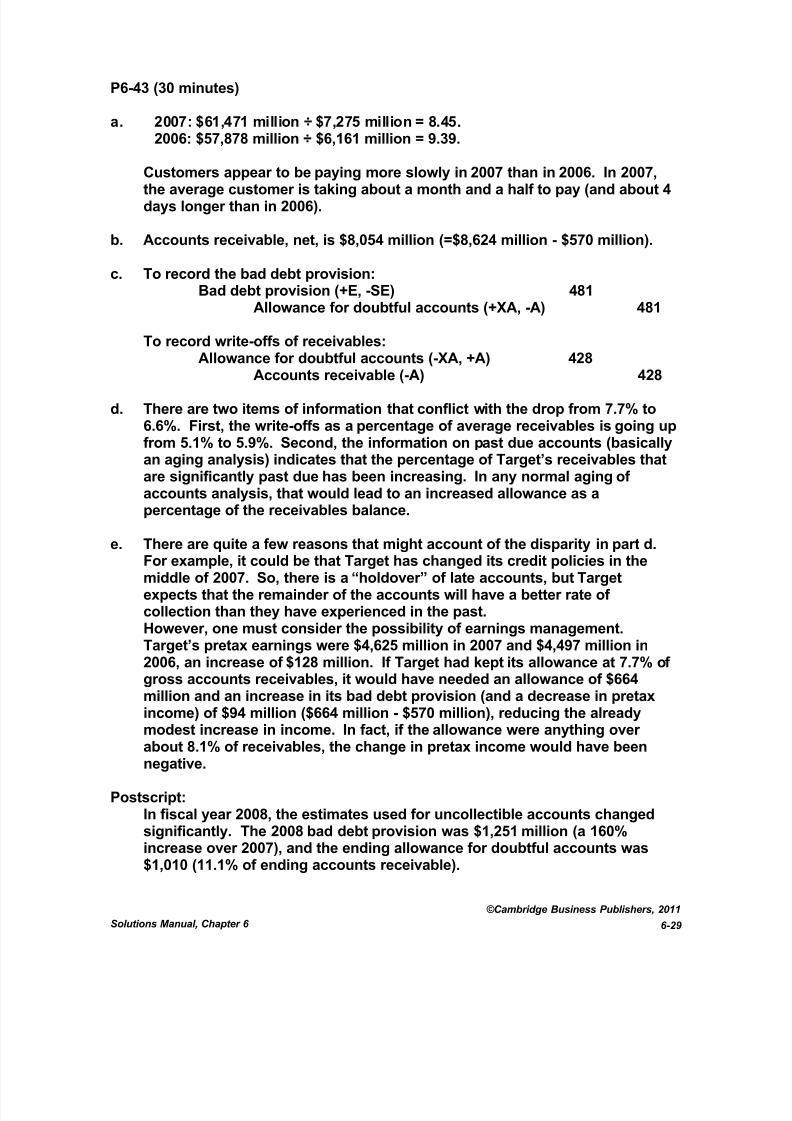

a. 2007: $61,471 million ÷ $7,275 million = 8.45.2006: $57,878 million ÷ $6,161 million = 9.39.

Customers appear to be paying more slowly in 2007 than in 2006. In 2007,

the average customer is taking about a month and a half to pay (and about 4days longer than in 2006).

b. Accounts receivable, net, is $8,054 million (=$8,624 million - $570 million).

c. To record the bad debt provision:Bad debt provision (+E, -SE) 481

Allowance for doubtful accounts (+XA, -A) 481

To record write-offs of receivables:Allowance for doubtful accounts (-XA, +A) 428

Accounts receivable (-A) 428

d. There are two items of information that conflict with the drop from 7.7% to6.6%. First, the write-offs as a percentage of average receivables is going upfrom 5.1% to 5.9%. Second, the information on past due accounts (basicallyan aging analysis) indicates that the percentage of Target’s receivables thatare significantly past due has been increasing. In any normal aging of accounts analysis, that would lead to an increased allowance as apercentage of the receivables balance.

e. There are quite a few reasons that might account of the disparity in part d.

For example, it could be that Target has changed its credit policies in themiddle of 2007. So, there is a “holdover” of late accounts, but Targetexpects that the remainder of the accounts will have a better rate of collection than they have experienced in the past.However, one must consider the possibility of earnings management.Target’s pretax earnings were $4,625 million in 2007 and $4,497 million in2006, an increase of $128 million. If Target had kept its allowance at 7.7% of gross accounts receivables, it would have needed an allowance of $664million and an increase in its bad debt provision (and a decrease in pretaxincome) of $94 million ($664 million - $570 million), reducing the alreadymodest increase in income. In fact, if the allowance were anything over

about 8.1% of receivables, the change in pretax income would have beennegative.

Postscript:In fiscal year 2008, the estimates used for uncollectible accounts changedsignificantly. The 2008 bad debt provision was $1,251 million (a 160%increase over 2007), and the ending allowance for doubtful accounts was$1,010 (11.1% of ending accounts receivable).

©Cambridge Business Publishers, 2011

Solutions Manual, Chapter 6 6-29

7/27/2019 Dmp3e Ch06 Solutions 01.26.10 Final

http://slidepdf.com/reader/full/dmp3e-ch06-solutions-012610-final 30/39

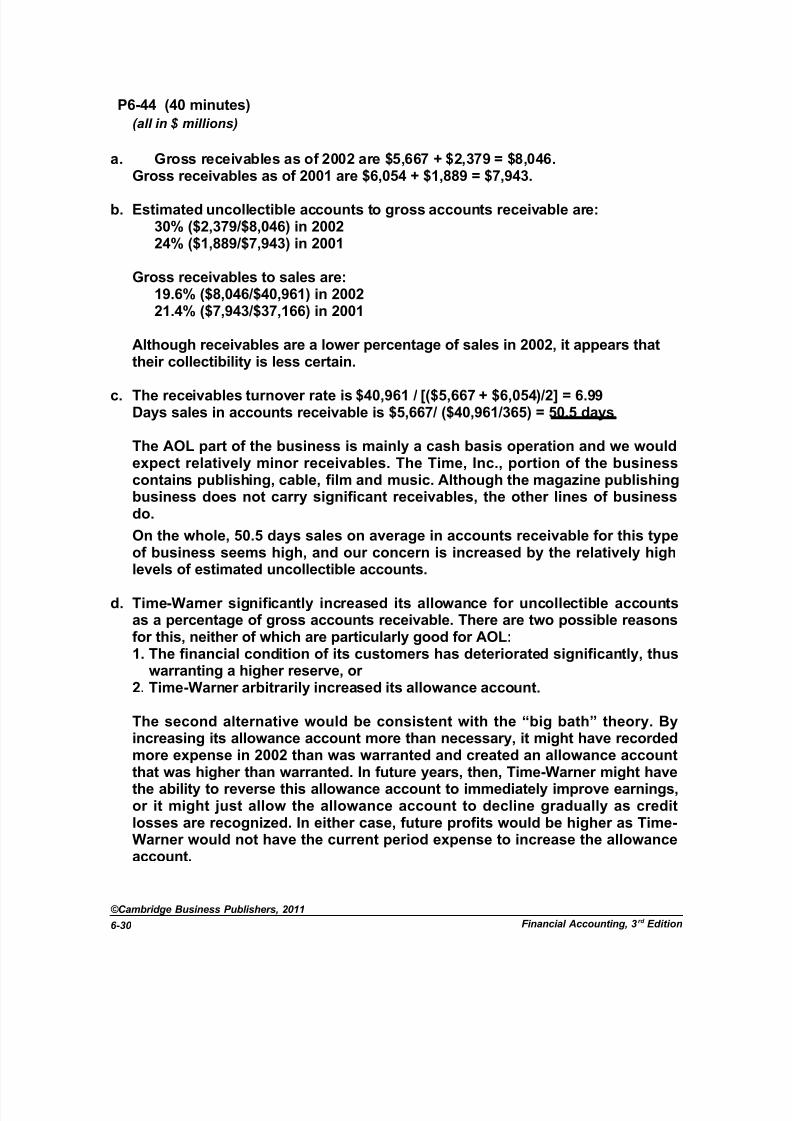

P6-44 (40 minutes)(all in $ millions)

a. Gross receivables as of 2002 are $5,667 + $2,379 = $8,046.Gross receivables as of 2001 are $6,054 + $1,889 = $7,943.

b. Estimated uncollectible accounts to gross accounts receivable are:30% ($2,379/$8,046) in 200224% ($1,889/$7,943) in 2001

Gross receivables to sales are:19.6% ($8,046/$40,961) in 200221.4% ($7,943/$37,166) in 2001

Although receivables are a lower percentage of sales in 2002, it appears thattheir collectibility is less certain.

c. The receivables turnover rate is $40,961 / [($5,667 + $6,054)/2] = 6.99Days sales in accounts receivable is $5,667/ ($40,961/365) = 50.5 days

The AOL part of the business is mainly a cash basis operation and we wouldexpect relatively minor receivables. The Time, Inc., portion of the businesscontains publishing, cable, film and music. Although the magazine publishingbusiness does not carry significant receivables, the other lines of businessdo.

On the whole, 50.5 days sales on average in accounts receivable for this typeof business seems high, and our concern is increased by the relatively highlevels of estimated uncollectible accounts.

d. Time-Warner significantly increased its allowance for uncollectible accountsas a percentage of gross accounts receivable. There are two possible reasonsfor this, neither of which are particularly good for AOL:1. The financial condition of its customers has deteriorated significantly, thus

warranting a higher reserve, or 2. Time-Warner arbitrarily increased its allowance account.

The second alternative would be consistent with the “big bath” theory. Byincreasing its allowance account more than necessary, it might have recordedmore expense in 2002 than was warranted and created an allowance accountthat was higher than warranted. In future years, then, Time-Warner might havethe ability to reverse this allowance account to immediately improve earnings,or it might just allow the allowance account to decline gradually as creditlosses are recognized. In either case, future profits would be higher as Time-Warner would not have the current period expense to increase the allowanceaccount.

©Cambridge Business Publishers, 2011

Financial Accounting, 3rd Edition6-30

7/27/2019 Dmp3e Ch06 Solutions 01.26.10 Final

http://slidepdf.com/reader/full/dmp3e-ch06-solutions-012610-final 31/39

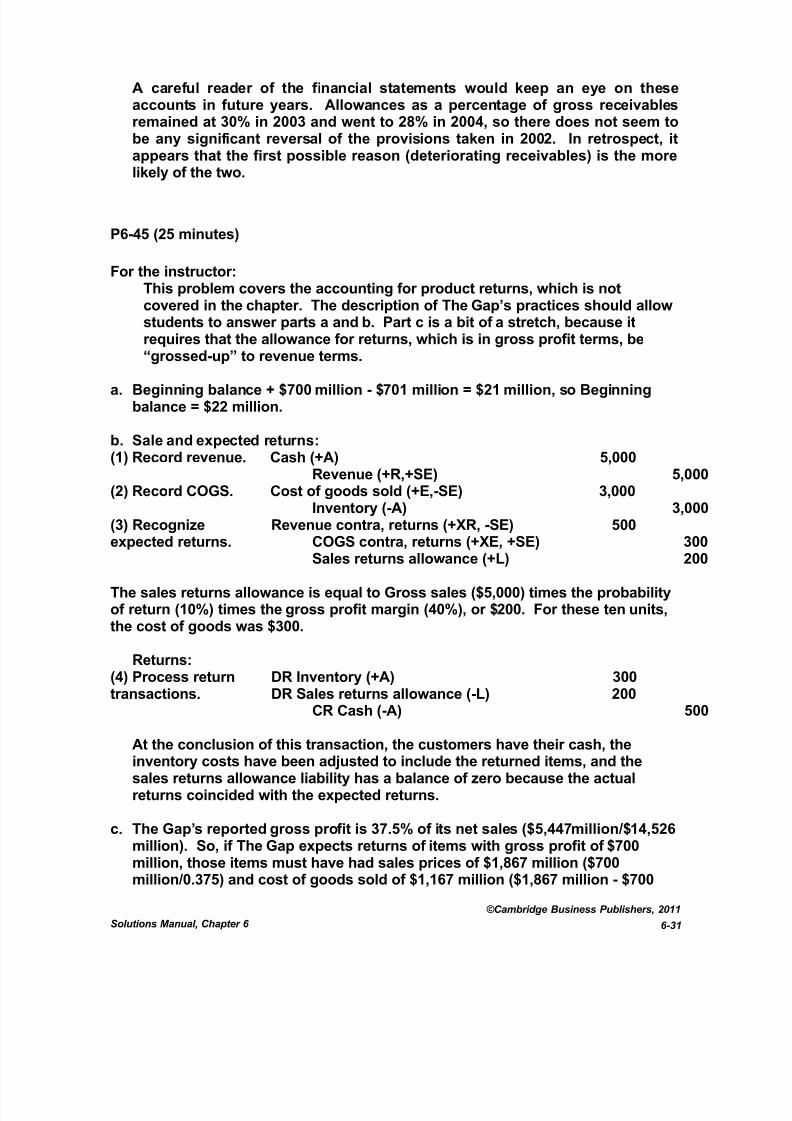

A careful reader of the financial statements would keep an eye on theseaccounts in future years. Allowances as a percentage of gross receivablesremained at 30% in 2003 and went to 28% in 2004, so there does not seem tobe any significant reversal of the provisions taken in 2002. In retrospect, itappears that the first possible reason (deteriorating receivables) is the morelikely of the two.

P6-45 (25 minutes)

For the instructor:This problem covers the accounting for product returns, which is notcovered in the chapter. The description of The Gap’s practices should allowstudents to answer parts a and b. Part c is a bit of a stretch, because itrequires that the allowance for returns, which is in gross profit terms, be“grossed-up” to revenue terms.

a. Beginning balance + $700 million - $701 million = $21 million, so Beginningbalance = $22 million.

b. Sale and expected returns:(1) Record revenue. Cash (+A) 5,000

Revenue (+R,+SE) 5,000(2) Record COGS. Cost of goods sold (+E,-SE) 3,000

Inventory (-A) 3,000(3) Recognizeexpected returns.

Revenue contra, returns (+XR, -SE) 500COGS contra, returns (+XE, +SE) 300

Sales returns allowance (+L) 200

The sales returns allowance is equal to Gross sales ($5,000) times the probabilityof return (10%) times the gross profit margin (40%), or $200. For these ten units,the cost of goods was $300.

Returns:(4) Process returntransactions.

DR Inventory (+A) 300DR Sales returns allowance (-L) 200

CR Cash (-A) 500

At the conclusion of this transaction, the customers have their cash, theinventory costs have been adjusted to include the returned items, and thesales returns allowance liability has a balance of zero because the actualreturns coincided with the expected returns.

c. The Gap’s reported gross profit is 37.5% of its net sales ($5,447million/$14,526million). So, if The Gap expects returns of items with gross profit of $700million, those items must have had sales prices of $1,867 million ($700million/0.375) and cost of goods sold of $1,167 million ($1,867 million - $700

©Cambridge Business Publishers, 2011

Solutions Manual, Chapter 6 6-31

7/27/2019 Dmp3e Ch06 Solutions 01.26.10 Final

http://slidepdf.com/reader/full/dmp3e-ch06-solutions-012610-final 32/39

million). The entry that would have reflected The Gap’s accounting for theseexpected returns is the following:

Recognize expectedreturns.

Revenue contra, returns (+XR, -SE) 1,867COGS contra, returns (+XE, +SE) 1,167Sales returns allowance (+L) 700

The Gap’s gross sales revenue would have been $16,393 million ($14,526million + $1,867 million), and its expected returns as a percentage of saleswould be 11.4% ($1,867 million/$16,393 million).

The size of the allowance for 2008 ($700 million) relative to the end-of-year return liability ($21 million) means that the vast majority of these productreturns occurred during the 2008 fiscal year, so it is more a reflection of actualexperience than of management’s estimates of future events.

d. Under these circumstances, The Gap doesn’t have to worry about accounting

for expected returns, because it has not satisfied the requirements for revenuerecognition. If the amount to be received (or in this case, the amount to bekept) is not yet “fixed or determinable,” the revenue should not be recognizeduntil it is.

P6-46 (25 minutes)

a.

Fiscal year ending March

31

Net revenue Growth rate

2005 3,129 –2006 2,951 -5.7%2007 3,091 4.7%2008 3,665 18.6%2009 4,212 14.9%

b.Fiscal year

endingMarch 31

Net

revenue

Deferred net

revenue (liability)

Purchases = Net

revenue + Change inDeferred net revenue

Growth

rate

2005 3,129 0 3,129 –2006 2,951 9 2,960 -5.4%2007 3,091 32 3,114 5.2%2008 3,665 387 4,020 29.1%2009 4,212 261 4,086 1.6%

©Cambridge Business Publishers, 2011

Financial Accounting, 3rd Edition6-32

7/27/2019 Dmp3e Ch06 Solutions 01.26.10 Final

http://slidepdf.com/reader/full/dmp3e-ch06-solutions-012610-final 33/39

When companies defer revenue, there is a lag between customers’ purchasesand the recognition of revenue on the income statement. In 2006, 2007 and2008, a growing portion of EA’s sales to customers were deferred, as therewas an increase in the rate of growth in purchases. So the growth in revenueswas less than the growth in customer purchases. However, the growth incustomer purchases for 2009 was not large – only 1.6%. The substantial

growth in revenue for 2009 is a vestige of the higher growth rates in previousyears (particularly 2008).

c. If customer purchases in 2009 are a leading indicator of customer purchasesin 2010, we would predict a substantial drop in revenue growth for 2010 over 2009.

©Cambridge Business Publishers, 2011

Solutions Manual, Chapter 6 6-33

7/27/2019 Dmp3e Ch06 Solutions 01.26.10 Final

http://slidepdf.com/reader/full/dmp3e-ch06-solutions-012610-final 34/39

CASES

C6-47A (60 minutes)

a. i. SALES – revenue is normally earned when title to the product passes to thecustomer who either purchases the product for cash or on credit terms.

ii. SERVICES, OUTSOURCING AND RENTALS – revenue from services is normallyearned as the service is performed, usually ratably over the period of theservice contract. The same applies to outsourcing and rentals.

iii. FINANCE INCOME – revenue from finance income (normally interest) is earnedwith the passage of time. For example, each period, Xerox accrues intereston its loans and leases.

b. i. Restructuring costs typically fall within two general categories. (1) Thewrite-off of assets, such as plant assets and goodwill, and (2) the accrual of liabilities for items, such as employee severance payments and exit costs.

ii. These restructuring costs result in expenses that are recorded in their respective current periods despite the fact that the corresponding impairedassets may not be formerly written off and the employees not paid their severance until future periods. In any event, most analysts treatrestructuring costs as transitory (one-time occurrences). Accordingly, theyshould impact the analysis, but are unlikely to impact the analysis to thedegree of more persistent items such as recurring revenues and expenses.

iii. Some companies report regularly recurring restructuring costs. In suchcases, many analysts treat these recurring costs as operating expensesand do not consider them to be transitory items. This treatment implies thatthese costs are less transitory and more persistent in nature.

In 2007, Xerox had a net credit on restructuring – the result of arestructuring provision of $35 million and a reversal of prior restructuringaccruals of $41 million.

c. Companies are not required to separately disclose revenue and expense itemsunless they are deemed to be material. If not separately disclosed, these itemsare aggregated with other items that are also deemed not to be material. Suchaggregation generally reduces the informativeness of income statements.More problematic is that revenues and expenses can be commingled in this“Other” category to yield a small number that further obscures the importanceof the individual items comprising this category.

©Cambridge Business Publishers, 2011

Financial Accounting, 3rd Edition6-34

7/27/2019 Dmp3e Ch06 Solutions 01.26.10 Final

http://slidepdf.com/reader/full/dmp3e-ch06-solutions-012610-final 35/39

In Xerox’s case, the significantly higher amount in Other expenses, net, is dueto a $774 million pretax charge for litigation losses. These would not beexpected to recur in future years.

d. The following items might be considered to be operating:

Sales and service, outsourcing and rental revenue would be consideredoperating; cost of sales, cost of service, outsourcing and rentals, R&D andengineering expenses, and SG&A expenses are typically designated asoperating.Restructuring and asset impairment charges would usually be considered tobe operating.Equity in earnings of unconsolidated affiliates would be considered operatingunder the assumption that the affiliates are related to Xerox’s core operations,which is typically the case.Finance income and equipment financing interest expense would be classifiedas operating, because financing customers’ purchases is one of Xerox’s lines

of business. However, it would be useful to consider it as a separate line of business for forecasting purposes.Other expenses would generally be considered nonoperating in the absenceof a footnote clearly indicating its connection to the operating activities of thecompany (such as the litigation losses described above).

The following items might be identified as transitory items:

If Xerox had income from discontinued operations or extraordinary items,those would be considered transitory. Those items did not appear in its 2006,2007 or 2008 income statement. The restructuring and impairment chargesappear regularly, but in varying amounts, and the MD&A reports that asignificant share of the Other expenses, net is due to litigation charges thatare probably transitory (but related to operations).

One other item that has transitory factors is the company’s income taxexpenses for the year. For reasons that will be discussed in Chapter 10,Xerox’s tax expense as a percentage of pretax income was (35.6%), 27.8% and202.6% in 2006, 2007 and 2008, respectively. Given that the U.S corporate taxrate is 35%, it is clear that there are some transitory effects going on in thisline item.

©Cambridge Business Publishers, 2011

Solutions Manual, Chapter 6 6-35

7/27/2019 Dmp3e Ch06 Solutions 01.26.10 Final

http://slidepdf.com/reader/full/dmp3e-ch06-solutions-012610-final 36/39

C6-48 (30 minutes)

a. When Dell sells other companies’ software products, it is often as part of amultiple-element sales agreement. For example, the customer may purchasehardware, software, and customer support for one price. This is an exampleof a bundled sale. Dell must allocate the sales price based on the relative fair

market value of each element. Revenue is recognized for each specificelement when it is clear that the element has been delivered and the revenueis earned.

There are at least two possibilities for earnings management here. First, Dellcould misallocate the sales price. By allocating more of the price to hardwareand less to software, Dell may be able to manage when earnings are reported.Second, Dell may be aggressive in applying the “earned and realizable”criteria to each element, thereby prematurely recognizing revenue.

From the information provided, it appears that Dell was recognizing revenue

on software “resales” at the time of sale. However, most software is not trulysold. Instead, the customer purchases a license to use the software. As aresult, Dell should have deferred part of the revenue and recognized it ratablyover the license period.

b. Extended warranties are typically sold separately from other products.Therefore, the revenue should be deferred and recognized ratably over thewarranty contract period. Dell employees were apparently recording revenueat the time of sale, or were recognizing the revenue over a shorter time periodthan the contract period. As a result, revenues and income were overstated.

c. It is common for managers to have performance targets based on revenuesand earnings. This provides an incentive for these employees to take actionsto accelerate revenue recognition when it appears that targets may not be met.On the other hand, in periods when revenues and earnings exceed the targets,managers may delay revenue recognition until a future period. In this way,they can “store up” revenues and earnings to meet future targets.

The key to preventing this type of abuse is the periodic audit of divisionalrevenues and earnings. In addition, businesses spend a large amount of resources trying to design incentive compensation plans that do notencourage this type of abuse.

©Cambridge Business Publishers, 2011

Financial Accounting, 3rd Edition6-36

7/27/2019 Dmp3e Ch06 Solutions 01.26.10 Final

http://slidepdf.com/reader/full/dmp3e-ch06-solutions-012610-final 37/39

C6-49 (45 minutes)

a.i. Bad debt expense (+E, -SE) 2,095,000

Allowance for doubtful accounts (+XA, -A) 2,095,000

ii. Allowance for doubtful accounts (-XA, +A) 1,562,000Accounts receivable (-A) 1,562,000

+ Accounts Receivable (A) ($000) - - Allowance for Doubtful Accounts (XA) ($000) +

Balance 110,069 3,609 BalanceSales 761,865 2,095 (i)

1,562 (ii) (ii) 1,562

Balance*

124,430 4,142 Balance

*This accounts receivable T-account above is incomplete; it is missing a credit for sales returns

and a credit for cash collections. Both are discussed and illustrated below.)

b. If sales returns are material in amount and can be estimated with a reasonabledegree of accuracy, they should be estimated just as bad debts are estimated.Sales revenue is debited for the estimated returns while an allowance for returns is credited. One important difference is that with sales returns (unlikebad debts) the customer returns the product to the company and it is oftenreturned to inventory. Hence, the amount of estimated returns is equal to theestimated gross profit on expected returns. Using Oakley’s gross profitmargin of 54.2% (= $412,751 / $761,865) the following entries would be

required in 2006:

iii. Sales revenue (est. sales returns) (-R, -SE) 7,547,000Allowance for returns (+XA, -A) 7,547,000

iv. Allowance for returns (-XA, +A) 6,993,000Inventory (+A) 5,909,000

Accounts receivable* (-A) 12,902,000

+ Accounts Receivable (A) ($000) - - Allowance for Returns (XA) ($000) +Balance 110,069 6,683 BalanceSales 761,865 1,562 (ii) 7,547 (iii)

12,902 (iv) (iv) 6,993733,040 Collections

Balance 124,430 7,237 Balance

* $6,993,000 / 0.542 = $12,902,000

©Cambridge Business Publishers, 2011

Solutions Manual, Chapter 6 6-37

7/27/2019 Dmp3e Ch06 Solutions 01.26.10 Final

http://slidepdf.com/reader/full/dmp3e-ch06-solutions-012610-final 38/39

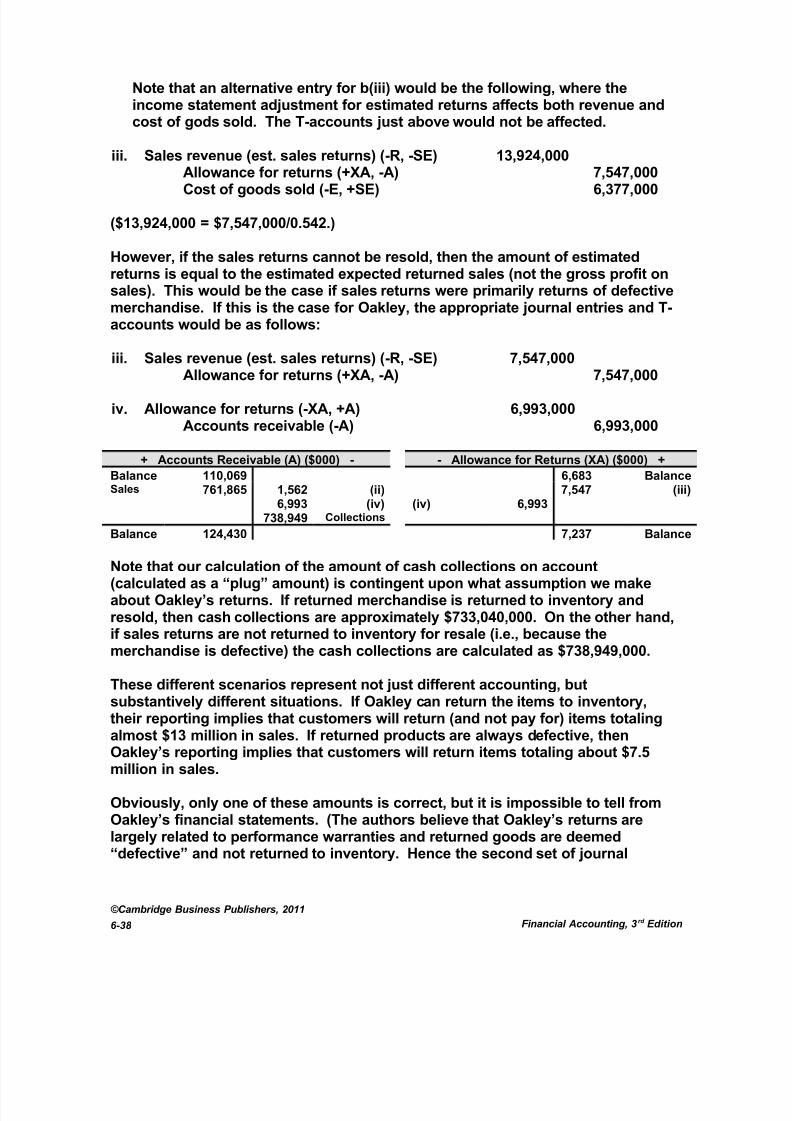

Note that an alternative entry for b(iii) would be the following, where theincome statement adjustment for estimated returns affects both revenue andcost of gods sold. The T-accounts just above would not be affected.

iii. Sales revenue (est. sales returns) (-R, -SE) 13,924,000Allowance for returns (+XA, -A) 7,547,000

Cost of goods sold (-E, +SE) 6,377,000

($13,924,000 = $7,547,000/0.542.)

However, if the sales returns cannot be resold, then the amount of estimatedreturns is equal to the estimated expected returned sales (not the gross profit onsales). This would be the case if sales returns were primarily returns of defectivemerchandise. If this is the case for Oakley, the appropriate journal entries and T-accounts would be as follows:

iii. Sales revenue (est. sales returns) (-R, -SE) 7,547,000

Allowance for returns (+XA, -A) 7,547,000

iv. Allowance for returns (-XA, +A) 6,993,000Accounts receivable (-A) 6,993,000

+ Accounts Receivable (A) ($000) - - Allowance for Returns (XA) ($000) +

Balance 110,069 6,683 BalanceSales 761,865 1,562 (ii) 7,547 (iii)

6,993 (iv) (iv) 6,993738,949 Collections

Balance 124,430 7,237 Balance

Note that our calculation of the amount of cash collections on account(calculated as a “plug” amount) is contingent upon what assumption we makeabout Oakley’s returns. If returned merchandise is returned to inventory andresold, then cash collections are approximately $733,040,000. On the other hand,if sales returns are not returned to inventory for resale (i.e., because themerchandise is defective) the cash collections are calculated as $738,949,000.

These different scenarios represent not just different accounting, butsubstantively different situations. If Oakley can return the items to inventory,their reporting implies that customers will return (and not pay for) items totalingalmost $13 million in sales. If returned products are always defective, then

Oakley’s reporting implies that customers will return items totaling about $7.5million in sales.

Obviously, only one of these amounts is correct, but it is impossible to tell fromOakley’s financial statements. (The authors believe that Oakley’s returns arelargely related to performance warranties and returned goods are deemed“defective” and not returned to inventory. Hence the second set of journal

©Cambridge Business Publishers, 2011

Financial Accounting, 3rd Edition6-38

7/27/2019 Dmp3e Ch06 Solutions 01.26.10 Final

http://slidepdf.com/reader/full/dmp3e-ch06-solutions-012610-final 39/39

entries would be correct.) The amount of cash collected is included in theaccounts receivable T-accounts above to be complete.

c. Accounts receivable turnover: $761,865 / [($109,168 + $99,430)/2] = 7.3 times.