Embed Size (px)

Citation preview

Investment and Foreign Exchange operation of Islami Bank Bangladesh Limited (IBBL)

1

Table of Contents:

LIST OF ILUSTRATIONLIST OF ILUSTRATION..............................................................................................................................................................................................................55EEXECUTIVEXECUTIVE S SUMMARYUMMARY....................................................................................................................................................................................................................66ACKNOWLEDGEMENTACKNOWLEDGEMENT............................................................................................................................................................................................................77CHAPTER ONE: INTRODUCTION:CHAPTER ONE: INTRODUCTION:....................................................................................................................................................................88

1.1 PURPOSE........................................................................................................................81.2 SCOPE:............................................................................................................................81.3 BACKGROUND.............................................................................................................91.4 METHODS OF DATA COLLECTION........................................................................101.5 LIMITATION OF THE STUDY:.................................................................................11

CHAPTER TWO: PROFILE OF IBBLCHAPTER TWO: PROFILE OF IBBL............................................................................................................................................................1212 2.1 INTRODUCTION:2.1 INTRODUCTION:..........................................................................................................................................................................................................1212

2.2 DEFINITION OF ISLSMIIC BANK:...........................................................................122.3 Historical Background of IBBL:...................................................................................12

CHAPTERFOUR: FOREIGN EXCHANGE OPERATIONCHAPTERFOUR: FOREIGN EXCHANGE OPERATION........................................................................................4949OF IBBLOF IBBL..................................................................................................................................................................................................................................................................4949

4.2 FOREIGN EXCHANGE:..............................................................................................494.3 Functions of Foreign Exchange Department:................................................................50Exports:................................................................................................................................50

2

LIST OF ILUSTRATION

3

EEXECUTIVEXECUTIVE S SUMMARYUMMARY

Islamic banking is relatively a new concept in the world. Before the inception of Islamic

banking phenomenon, banks were institutes to be avoided by the millions of Muslims.

Keeping aloof themselves from banking, Muslims began to loss their market in the world

economy. As the competition the business world became more and more severe,

businesspersons had no alternative banking premises and many of them were getting

involved in the traditional banking. However, the traditional banking is based on interest,

which is fully prohibited in Islam. To overcome this problem, Muslim scholars, philosophers,

economists etc. were thinking to establish a new interest-free banking structure right from the

1940’s. At last, they succeeded to formulate an appropriate Islamic banking structure. Many

previous studies have been done in this regard. Islam is a complete code of life. It does not

allow anything to be done in unislamic. So Islamic banks do not give more importance only

on earning profit but also try to ensure social welfare in terms of its activities. Collecting

foreign remittance is one of the important functions of the Islamic Bank. It is one type of a

social activity and other side important source of bank’s income. Foreign remittance account

is conducted based on profitability and safety of funds. One of the main objectives of

collection of foreign remittances is to build up strong economic position of the country and

other is increase profitability of the bank. Bank has several scheme for non-residents

Bangladeshi and it always try to collect remittance of those people by easier way that is

helpful for those people and benefit for Bangladesh government. IBBL has representatives in

different countries to motivate non-residents Bangladeshi to open account and send their

income as they save. Therefore, IBBL plays an important role to improve foreign remittance

of the country. It will also participate for different development programmed and build up of

social infrastructure, which is a part of state’s planning. Bank also uses their collecting

money with the participation of govt. for creating more employment opportunities.

Foreign remittance increase bank’s reserve and ultimate result is increase of Bangladesh

Bank reserve and supporting to strong economic position of the country. All of the

investment activities of the banks are conducted based on Islamic shariah. I tried to show the

role of IBBL to improve foreign remittance and improve the economic condition of the

country.

4

ACKNOWLEDGEMENTIt is a great honor for me to submit this report to my respected internee supervisor and

madam associate professor Ms.Samina M.Saifuddin. At first I want to convey my thanks and

gratitude to her for assigning me to prepare internship report entitled, “Investment and

Foreign Exchange operation of IBBL”, that help me to gather practical knowledge about the

Investment and Foreign Exchange operation of IBBL.

It would not be possible for me to complete this report, but for her help. Her continuous and

enthusiastic monitoring has motivated me to reach my goal on time and with efficiency. My

debt to her can only be gratefully acknowledged but can never be compensated.

Last but not least thanks to Md. Kawsar Ul Alam, Vice President, Mohammead Akhter

Hossen, Senior principal Officer, Md. Omar Faruk, principal Officer, Roizul Islam, Assistant

Officer, Arifur Rahman, Officer, and other officials of IBBL for their comments &

assistance. I express my deepest sense of regards and gratitude to them.

5

CHAPTER ONE: INTRODUCTION:

1.1 PURPOSE

Every activity is directed to achieve some specific purpose. This Internship Report also serves some specific purposes. The main purposes of this study are mentioned below:

To understand and analyze the Islamic Banking system of Bangladesh and its policies

& regulations.

To understand and analyze foreign exchange mechanism of Islami bank.

To understand and analyze foreign remittance role of IBBL and also contribution to

the economy.

To make possible suggestions and recommendations for increasing foreign

remittances through Islami bank Bangladesh Ltd.

To know how to make investment by IBBL under different modes

1.2 SCOPE:

The scope of this report is analytical. This report mainly focuses on the investment and foreign exchange operation of IBBL This report covers the details discussion of investment operation of IBBL. Import & Export business procedures of IBBL are also discussed in this report. Foreign remittance policies of IBBL are discussed herewith. Various statistical data are shown in this report.

This report does not cover the General Banking activities of IBBL, Social activities of IBBL

etc.

1.3 BACKGROUND

For an expanding economy, a developed and efficient banking system is indispensable.

Among others, it helps transfer of financial resources from surplus units to deficit units and,

6

hence, helps accelerate the pace of development by securing uninterrupted supply of

financial resources to people engaged in numerous economic activities. The tremendous

development that the world economy has experienced in the last few decades was contributed

by several factors among which, growing institutional supply of loan able funds must have

played the pivotal role. The role of banking is comparable to what an artery system does in

the human body. Both commercial banks and other development financial institutions

provide short-term, medium-term, and long-term credits to businessmen and entrepreneurs

who usually take the lead in ventures of economic development. Institutional supply of credit

has been made possible by a system of financial intermediation organized in a way where

conventional banks collect small savings from the public by offering them a fixed rate of

interest and advancing the loan able funds out of the deposited money to enterprising clients

charging relatively higher rates of interest.

The margin between these two rates is the bank's income. In addition, banks also provide

many other services to the public for which it receives service charges. For millions of

Muslims, traditional banks are institutions to be avoided. Islam is a religion, which keeps

believers from the teller's window. Their Islamic beliefs prevent them from dealings that

involve usury or interest (Riba). Yet Muslims need banking services as much as anyone and

for many purposes: to finance new business ventures, to buy a house, to buy a car, to

facilitate capital investment, to undertake trading activities, and to offer a safe place for

savings. For Muslims are not averse to legitimate profit as Islam encourages people to use

money in Islamic legitimate ventures, not just to keep their funds idle.

However, in this fast moving world, more than 1400 years after the Prophet (Sm), can

Muslims find room for the principles of their religion? The answer comes with the fact that a

global network of Islamic banks, investment houses and other financial institutions has

started to take shape based on the principles of Islamic finance laid down in the Quran and

the Prophet's traditions 14 centuries ago.

Islamic Banking beyond the traditional banking system will serve the purpose of Islamic

ideology of ‘complete code of life’. One could conclude that Islam has many universal values

in common with the west. As Islam believes the earlier scriptures in its original form were

from the same God (Allah), this is not surprising. However, the specific prohibition of

7

interest and establishment of the zakat tax, and the status of law on gambling, uncertain

contracts etc. which are prohibitions and not moral exhortations, implies that the objectives

of banking in Islam is different from conventional and even to a certain extent social and

environmental investment. Thus, there is a need for an Islamic investment system and foreign

exchange operation in the Banking arena.

1.4 METHODS OF DATA COLLECTION

The study is performed based on the information extracted from different sources

collected by using a specific methodology. This report is analytical in nature. The

methodology is

Population: All the Branches of IBBL located in everywhere in Bangladesh has been taken

into consideration as population.

Sample: Islami Bank Bangladesh Ltd, Corporate office & Islami Bank Training centre

Data collection: The data are collected from both primary and secondary sources:

Primary Sources:

Face to Face conversation with the respective officers and staffs.

Interviewing officers and staffs.

Sharing practical knowledge of officials.

Relevant file study provided by the officers concerned.

In-depth study of selected cases.

Secondary Sources:

Annual Report of IBBL

Audit Reports

Website

Relevant books, Research papers, Newspapers and Journals.

Internet and various study selected reports.

8

1.5 LIMITATION OF THE STUDY:

High degree of involvement regarding collection of information, review of literature and

analysis of information requires for any kind of research work. This study has suffered from

certain constraints noted below:

Unpublished data have not considered for the study.

The depth of the analysis has been limited to the extent of information collected

from different sources.

Last of all, this study has been conducted within a limited time. So, time

constraint has played a key role for the whole study.

Lack of co-operation of the respondents.

CHAPTER TWO: PROFILE OF IBBL

2.1 INTRODUCTION:

Islami bank Bangladesh Limited (IBBL) was established in 1983 with a view to conducting

its banking activities based on the principle of Islamic Shariah. In 1987 Oriental Bank (Al-

9

Baraka Bank) Bangladesh Limited the second Islamic Bank was established. There are seven

Islamic Banks in Bangladesh. These are:

Islamic Bank Bangladesh Limited (1983)

Social Invested Bank Limited (1995)

Al Faisal Bank Limited (1995),

Al-Arafah Islamic Bank Limited (1995)

Shahajalal Bank Ltd.

Exim Bank Ltd (two branches).

Also Prime Bank Ltd. Dhaka Ltd., Southeast Bank Ltd., Premier Bank Ltd. And some other

Banks are thinking about the opening of Islamic Branches

2.2 DEFINITION OF ISLSMIIC BANK:

According to Organization of Islamic Conference (OIC), “Islamic bank is a financial

institution whose statutes, rules and procedures expressly state its commitment to the

principles of Islamic Shariah and to the banning of the receipt and payment of interest on any

of its operations.”

According to Dr. Ziauddin Ahmed “Islamic Bank is essentially a normative concept and could be defined as conduct of banking in consonance with the ethos of the value system of Islam.

2.3 Historical Background of IBBL:In August 1974, Bangladesh signed the Charter of Islamic Development Bank and committed

itself to reorganize its economic and financial system as per Islamic Shariah. In January

1981, the President of People’s Republic of Bangladesh While addressing the third Islamic

conference held at Mecca and Taif suggested “The Islamic countries should develop a

separate banking system of their own in order to facilitate their trade and commerce". This

statement of the president indicated favorable attitude of the government of the People’s

Republic of Bangladesh towards establishing Islamic banks and financial institution in the

country.

In early November 1980, Bangladesh bank, the country’s Central Bank, sent a representative

to study the working of several Islamic Banks abroad.

10

In November 1982, a delegation of IDB visited Bangladesh and showed keen interest to

participate in establishing a joint venture Islamic bank in the private sector. They found a lot

of work had already been done and Islamic banking was in a ready from for immediate

introduction. Two professional bodies of Islami Economics Research Bureau (IERB) and

Bangladesh Islami Bankers’ Association (BIBA) made significant contribution towards

introduction of Islami banking in the country.

They came forward to provide training of Islamic banking to top bankers and economists to

fill up the vacuum of leadership for the future Islami bank in Bangladesh. They also had

seminars, symposiums and workshops on Islami economic and banking throughout the

country to mobilize public opinion in favor of Islami banking. Their professional activities

were reinforced by a number of Muslim entrepreneurs working under the support of the then

Muslim Businessmen society (now reorganized as Industrialist & Businessmen Association).

The body concentrated mainly in mobilizing equity capital for the emerging Islami bank.

At last, the long drawn struggle to establish an Islami bank in Bangladesh become a reality

and Islami bank Bangladesh limited was established in march 1983 in which 19 Bangladeshi

national, 4 Bangladeshi institutions and 11 banks, financial institutions and government

bodies of the middle East and Europe including IDB and two eminent personalities of the

kingdom of Saudi Arabia joined hands to made the dream a reality.

Later, other Islami Banks, Islami Insurance Companies and Financial Institution were

established in the country. Some traditional banks opened Islamic banking branches in some

major cities.

2.4 Management of IBBL:A Board of Directors consists of 13 directors those are elected from the foreigners and local

shareholders. They provide policy guide lines to Islami Bank Bangladesh limited. The Board

of Directors forms an Executive Committee for smooth and efficient operations of the Bank

Executive Committee consists the members of the Board. Besides, a Management committee

consisting of the senior executives headed by the chief executive looks after the actual

operations of the Bank.

2.5 ORGANIZATIONAL STRUCTURE OF IBBL:

11

2.6 Mission of IBBL:To establish Islamic Banking through the introduction of a welfare oriented banking system

and also ensure equity and justice in the field of all economic activities, achieve balanced

growth and equitable development through diversified investment operations particularly in

12

Executive President (EP)

Deputy Executive President (DEP)

Executive Vice President ( EVP)

Senior Vice President (SVP)

Vice President (VP)

Senior Principal Officer (SPO)

Assistant Vice President (AVP)

Principal Officer (PO)

Senior Officer (SO)

Officer

Probationary Officer

Assistant Officer Grade - I

Assistant Officer Grade - II

Assistant Officer Grade - III

the priority sectors and less development areas of the country. To encourage socio-economic

uplift and financial services the low-income community particularly in the rural areas.

2.7 Vision of IBBL:Vision of IBBL is to always strive to achieve superior financial performance, be considered a

leading Islami Bank by reputation and performance.

Goal of IBBL is to establish and maintain the modern banking techniques, to ensure

the soundness and development if the financial system based on Islami principles and

to become the strong and efficient organization with highly motivated professionals,

working for the benefit of people, based upon accountability, transparency and

integrity in order to ensure the stability of financial systems.

IBBL will try to encourage saving in the form of direct investment.

IBBL will also try to encourage investment particularly in projects which are more

likely to higher employment.

2.8 FEATURES OF IBBLThe bank is committed to run all its activities as per Islami Shariah. IBBL through its steady

progress and continuous success has earned the reputation of being one of the leading

private sector banks of the country. The distinguishing feature s of IBBL is as follow:

All its activities are conducted on interest-free banking system according to

Islamic Shariah.

Establishment of participatory banking instead of banking on debtor-creditor

relationship.

Investment is made through different modes permitted under Islami Shariah

Investment income of the Bank is shared with the Mudaraba depositors according

to a ratio to ensure a reasonable fair rate of return on their depositors.

Its aims are to introduce a welfare-oriented banking system and also to establish

equity and justice in the field of all economic activities.

13

It extends Socio-economic and financial services to the poor, helpless and low-

income group of the people for their economic up liftmen particularly in the rural

areas.

It plays a vital role in human resource development and employment generation

particularly for the unemployed youths.

Its aim is to achieve balanced growth and equitable development of the country

through diversified investment operations particularly in the priority sectors and

in the less developed areas.

It extends co-operation to the poor, the helpless and the low-income group for

their economic development.

2.9 Functions of IBBL:

Islami Bank Bangladesh limited is performing the following functions:

To maintain all types of deposit accounts.

To make investment.

To handle foreign exchange business.

To extend other banking services.

To conduct social welfare activities through Islami Bank Foundation.

2.10 Capital of the IBBL:The authorized capital of the bank is Tk. 5000.00 million and paid up capital is Tk. 3456.00 million as on 31st December, 2006.

2.11 Equity:Total equity of the bank as on 31st December, 2006 was Tk 10,261.50 million.

CHAPTER THREE:

14

INVESTMENT ACTIVITIES OF IBBL

Conventional and Islamic bank operate to earn profit but they differ in the way of operation.

Islami Bank emphasises on the legitimate (Halal) business. On the other hand traditional

bank is not operated by the following rules and regulations approved by Islam that is the

most powerful contradiction between them. Islamic Bank does not invest in loans and fixed

interest securities. It can invest in ordinary share only while interest based bank can invest in

loans and different kinds of securities. Islami Bank establishes and participate projects with

its client as a partner and bears the risk along with the client on a proportionate basis. The

bank takes deposits and invests the same based on the profit-loss sharing. Bank go for the

investment mainly which are long term and profitable in nature. IBBL also give high

concentration on the investment that will generate more employment. As investment is one of

the most priority areas for the IBBL, so it needs to cautious in investment decision. To ensure

proper investment IBBL always go with in-depth study before making the investment.

The special feature of the investment policy of Islamic Banks is to invest based on profit-loss

sharing system in accordance with the tenets and principles of Islamic Shariah. Earning of

the profit is not the only motives and objectives of the Islamic Bank’s investment policy

rather emphasis is given in attaining social good and in creating employment opportunities.

3.1 Objectives and principles:

The objectives and principles of investment operations of the Bank are:

To invest fund strictly in accordance with the principles of Islamic Shariah.

To diversify its investment portfolio by size of investment portfolio by sectors (Public

&Private), by economic purpose, by securities and by geographical area including

industrial, commercial & agricultural.

15

To ensure mutual benefit both for the bank and the investment client by professional

appraisal of investment proposals, judicious sanction of investment, close and

constant supervision and monitoring thereof.

To make investment keeping the socio economic requirement of the country in view.

To increase the number of potential investors by making participatory and productive

investment.

To finance various development schemes for poverty alleviation, income and

employment generation with a view to accelerate sustainable socio-economic growth

and uplift of the society.

To invest in the form of goods and commodities rather than give out cash money to

the investment clients.

To encourage social uplift enterprises.

To ensure avoid all the investment forbidden by the Islami shariah.

The bank extends investment under the principles of Bai-murabaha, Bai-Muajjal, Hire

Purchase under Shirkatul Melk and Musharaka.

3.2 Investment policy of IBBL:Investment policy of Islamic Bank and non-Islamic bank are fully different. The investment policies of Islamic bank are:

Strict observance of Islamic Shariah principles.

Investment to national priority sectors.

Diversified investment portfolio: Diversification by size, sector, geographical area,

economic purpose, securities and mode of investment.

Preference to short-term Investments.

16

Preference to investment of small size.

To ensure safety & security of investments

To look profitability of investments.

To give support to government denationalization industrial program.

Investment to trade and commerce sector.

Investment to industrial sectors.

Investment to Foreign Trade (import & export).

Exploration of the possibility of investment in the existing Money & capital Market

and help organization of Islamic Money & Capital Market

3.3 Investment Strategy of IBBL:

Investment strategy of Islamic Bank and interest-based bank are contradictory. The

investment strategies of Islamic Bank are:

To check exodus of investment clients.

To induct new investment clients.

To induct good investment clients of other Banks.

To enhance existing limits of good investment clients.

Extension of investment transport sector.

Extension of investment to backward as well as forward linkage industries.

Extension of investment to real Estate Sector.

Extension of investment to Jute sector; particularly for trading and export purpose.

17

Strengthening supervision, control and monitoring mechanism.

Training and motivation of manpower to handle increased and diverse volume of

investment s.

To give due consideration to high risk, high return and low risk, low return

investment proposals.

Adaptation of modern technology

3.4 Steps in Investment Operations: Induction of client:

Preliminary discussion with the prospective client regarding his investment needs, business experience, viability of the project and Shariah permissibility of the assets the business and the uses of the assets.

Brief him on the salient features of Hire Purchase under Shirkatul Milk mode of Investment. Apprise, in particular, the usual terms and conditions under which the Bank made such investment. Discuss about Client’s equity participation and its immediate availability.

Look to the past performance of the Client, Check-up Head Office Current Investment Policy and Branch’s track record of Hire purchase under Shirkatul Melk Investment of the item(s).

If the Proposal is found permissible under Islamic principles and suitable, advise the Client to submit formal Application. If not found suitable, regret politely.

Request potential Client to open an Al-Wadeeah Current account. Let him maintain the Current account. Let him maintain the current Account satisfactorily for a reasonable period. (This will generally mean six month).

Application: Obtain application in triplicate from the client of F-167A and record the same in the

Investment Proposal Received and Disposal Register (B-53). Obtain and affix attested photograph(s) of the Proprietor /Partner/Directors/ Trustee/

Administrator on the top right hand corner of the application.

18

Processing and Appraisal: Check–up credit Restriction schedule of Bangladesh Bank and Head office current

investment policy guideline. Reject the proposal, if it conflicts with the existing credit restrictions of Bangladesh Bank and Head Office Policy Guidelines.

Visit the Business Establishment of the Client. Tally/briefly the securities, particulars, information and figures given in the Application form with the original Documents/Papers and are sanguine about its genuineness and correctness. Obtain additional information, particulars, and facts and figures, if required.

Talk to his business and important personalities of the locality to ascertain the honesty, integrity and business dealings of the Client.

Request for Confidential Report of the Client from local bank branches is received. Confidential Reports should also be obtained from local Financial, Credit and Leasing

Institutions, if felt necessary. Obtain Report from Credit information Bureau (CIB) of Bangladesh Bank through Head

Office Investment division as per Circular issued by H.O from time to time in this regard. Obtain declaration of the client about his liability (both contingent and real) with other

Banks/financial Institutions/Leasing Companies etc. including any other branches of IBBL.

Obtain financial statement /Balance Sheet of the concerned application for last three consecutive. Accounting years for investment proposals of Tk. 50 lac and above or as per Head office instruction. This is to be furnished by all clients irrespective of their status.

Forward the documents, title deeds and other relevant papers to the approved lawyer of the Bank for examination and furnishing his opinion.

Obtain lawyer opinion as per clause no.7.18.2 (i) Please study the following carefully and note down the actual finding in the appraisal

from against each item. Whether the assets, which the client intends to, hire and purchase, are readily useable and

has constant and effective demand in the market. Whether the price of the asset is subject to frequent and violent changes. Whether the asset is non-fungible or has flow of services. Whether the quality and other specifications of the asset as desired by the Client can be

ensured. Whether the assets are available in the market and it is possible to

purchase/construct/manufacture/make the asset in time and the negotiable price/cost. Whether rental and sale price of the assets are payable by the Client at the agreed

specified future date is lump sum or by instilments as per proposal.

19

Whether Client & Bank’s equity ration is fixed to cover the price of the asset. Whether the project/deal is profitable to generate sufficient fund to pay the rent/sale price

by the Client within the deal period. Market price and cost price should be carefully studied by the Investment Committee of

the branch and properly recorded, verified and signed. For Hire Purchase under Shirkatul Melk Investment. (Other than the Schemes), prepare

Appraisal Report on F-167B.

Documentation:Before purchasing the asset/property by the Bank, obtain sufficient collateral securities as mentioned in the sanction advice along with the following charge documents properly executed i.e. duly filled in, signed, stamped, verified and witnessed where necessary:

Hire Purchase under Shirkatul Melk Sanction Advice deal-wise duly accepted by the client.

Hire Purchase under Shirkatul Melk Agreement (Deal-wise). Letter of Pledge (Deal-wise)/Mortgage Deed. Single party D.P. Not, if there is no guarantor. Double party D.P. Not, if there is guarantor (s) to be made by the Client in favor of

the guarantor and endorsed by the later to the Bank. D.P. Not Delivery letter. Letter of Hypothecation for the asset(s) and Client’s stock in Trade/work-in-process. Letter of Disclaimer, (if stored in Client’s/Party’s own/hired Godown. Insurance policy (If stored in Client’s/Party’s Godown/yard under Bank’s effective

control) duly recorded in insurance register. Letter of guarantee. Balance confirmation letter. Letter of installments. Letter of Disbursement.

If the investment is made collaterally secured by Mortgage of property, obtain the following documents:

In case equitable mortgage, Memorandum of Deposit of Title Deep (MDTD) signed by the owner of the property.

In case of Legal Mortgage, Registered Mortgage Deed should be obtained. Personal Guarantee of the owners of the property on.

20

Original Title Deeds with CS, RS, SA, Mutation Parcha, DCR of the property and Mutation record.

Up-to-date Rent Receipt. Non-encumbrance Certificate along with Search Fee Paid Receipt of the concerned

Registry/Sub-Registry office. Site plan (Map/Naksha) of the Mortgaged property. Valuation Certificate countersigned by the Manager certifying the Market value and

the Forced sale value. Legal opinion should be self-contained, without any ambiguity and clean in all

respects.Where the Investment is secured by pledge/Hypothecation of Stock-in-Trade, Machineries etc., also obtain the following Document:

Letter of Pledge asset & goods security, for Client’s stocks in Trade/work-in-Process etc. if any.

Letter of Hypothecation for Client’s stocks, stores, Work-in-Process etc. Legal Mortgage of Machineries with full details of each machinery

In case the investment Collaterally/ Additionally secured by Pledge of Shares of reputed Public Limited Company on Bank’s approved list and quoted in the Stock Exchange, the following additional documents are to be obtained:

Agreement for Pledge of share along with original share certificates (No share in the name of minor shall be accepted as security).

Blank Share Transfer Deed in Duplicate – on copy signed, dated and another copy signed and undated.

Share Delivery letter addressed to the Bank. Letter to the concerned Company to register Line in Bank’s favor. This notice shall

be sent be registered acknowledgement due post (registered A/D post) and confirmation of recording the Line shall be obtained from the concerned company.

Letter of authority in Bank’s favor duly signed by the shareholder.

In case of investment to Private or public Limited Company, obtain the following additional document:

Obtain certified copy of the Memorandum and Articles of Association of the company to ensure that the company has necessary power to borrow/avail investment from any Bank.

21

Resolution of the board Directors of the Company to avail Investment/Facility/Borrow, do Business with IBBL and authorizing the office bearers to execute necessary Documents.

Personal Guarantee of the Directors of the Company. If the investment is allowed on Hypothecation of assets. Certificate issued by the registrar of Joint Stock Companies under section 114 of The

Companies Act-1994 in respect of creation of charges. Copies of Memorandum and Articles of Association with the latest amendments A copy of the Certificate of Incorporation duly attested by the Incumbent-In-Charge

of the Branch. A copy of the certificate of commencement of Business duly attested by the

Incumbent-In-Charge of the Branch.

In case of investment to a trust organization obtain the following Document in addition to other charges Documents:

Copy of trust deed duly attested by a 1st class Gazette officer and verified by the incumbent-in-charge of the branch with the original copy. The Trust Deed must contain a clause authorizing the Trustees to do Business with banks and to avail investment facilities /borrow from banks.

Resolution of the Board of Trustees to do business with IBBL and avail investment/borrow from IBBL.

The charge documents and all other agreements shall be signed /executed by persons authorized by all the members of the board of Trustees, in Trustees are authorized to delegate their powers by the trust Deed; otherwise all the Trustees must sign/execute the charge documents and all other agreements.

Personal guarantee of all the members of the board of trustees must be obtained.

In case of investment to co-operative security, obtain the following documents also: Clearance from the register of co-operative societies for doing business and avail

faculties / investment from IBBL within the annual borrowing limit of the society. Litter to be issued to; the concerned registrar of co-operative societies under

registered A/D Mail informing about allowing investment /facility to the concerned society by the bank as per clearance accorded by him.

Personal guarantee of the office Bearers of the society if their personal capacity. A copy of the byelaws of the society duly certified by the registrar of the co-operative

societies.

22

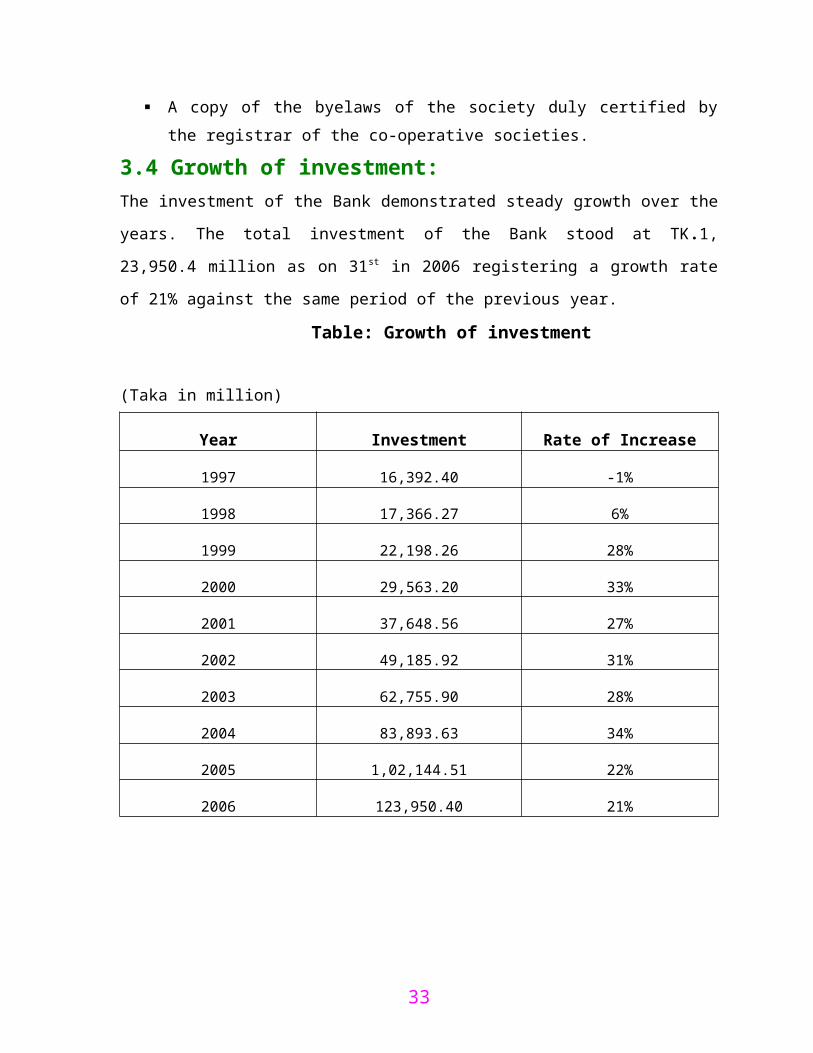

3.4 Growth of investment: The investment of the Bank demonstrated steady growth over the years. The total investment

of the Bank stood at TK.1, 23,950.4 million as on 31st in 2006 registering a growth rate of

21% against the same period of the previous year.

Table: Growth of investment

(Taka in million)

Year Investment Rate of Increase

1997 16,392.40 -1%

1998 17,366.27 6%

1999 22,198.26 28%

2000 29,563.20 33%

2001 37,648.56 27%

2002 49,185.92 31%

2003 62,755.90 28%

2004 83,893.63 34%

2005 1,02,144.51 22%

2006 123,950.40 21%

23

3.5 Investment Instrument of IBBL:

IBBL invests money in various sectors of the economy through different modes permitted by

Shariah and approved by the Bangladesh Bank. The modes of investment are discussed

bellow:

A. Profit & Loss Sharing Mode

Mudaraba: It is a form of partnership where one party provides the fund while the other

provide the expertise, labor and the letter referred to at the Mudaraba any profits accrued are

shared between the two parties on a pre –agreed basis, while capital loss in exclusively born

by the partner providing the capital.

Musharakah: The term Shirkat and Musharaka have been derived from Arabic words

“Shairkah” and “Sharika.” The word shirkah means a partnership between more than one

partner. Thus the ward “Musharaka” and “Shirkat” means a partnership established between

two or more partners for purpose of a commercial venture participate both in the capital and

management where the profit may be shared between the partners as per agreed upon ratio

and the loss. If any incurred, is to be borne by the partners at per capital Lequity ratio.

B. Bai Mode

Bai-Murabaha: Bai-murabaha may be defined as a contract between a buyer and a seller

under which the sells certain specific goods (permissible under Islamic Shariah and the law

of the land) to the buyer at a cost plus agreed profit payable in cash or on any fixed future

data in lump sum or by installments. The marked up profit may be fixed in lump sum or in

percentage of the cost price of the goods.

Bai-Muajjal: Bai-Muajjal may be defined as a contract between a buyer and seller under

which the seller sells certain specific goods permissible under Islamic Shariah and law of

the country to the buyer at an agreed fixed price payable at a certain fixed future date in

lump sum or within a fixed period by him as per order and specification of the buyer.

Bai-Salam: Bai-Salam may be defined as a contract between a buyer and a seller under

which the seller in advance in the certain commodity/products permissible under Islamic

Shariah and the law of the land to the Buyer at an agreed price payable on execution of the

24

said contract and the commodity products to the buyer at a future time in exchange of an

advance price fully paid on the spot

Istishna’a: Istishna’a is a contract between a manufacturer/seller and a buyer under which the

Manufacturer/seller sells specific product(s) after having manufactured, permissible under

Islamic Shariah and Law of the Country after having manufactured at an agreed price

payable in advance or by installments within a fixed period or on/within a fixed future date

on the basis of the order placed by the buyer.

C. Rent Sharing Mode:

Ijarah (Lease): The term Ijarah has been derived from the Arabic words Ajr and Ujrat, which

means consideration, return, wages or rent. This is really the exchange value or

consideration; return wages font of service of an asset. Ijarah has been defined as a contract

between two parties, the Hiree andHirer where the Hirer enjoys or reaps a specific service or

benefit againsta specified consideration or rent from the asset owned by the Hiree .to a Hirer

against fixed rent or rentals hires out a certain asset for a specified period.

Ijarah wa Iqtina (Hire Purchase): This term refers to a mode of financing adopted by Islami

banks. It is a contract under which the Islami Bank Finance equipment, building, or other

facility for the client against an agreed rental together with an undertaking from the client to

purchase the equipment or the facility. The rental as well as the purchase price is fixed in

such a manner that the bank gets back its principal sum along with some profit which is

usually determined in advance.

Hire Purchase under Shirkatul Melk: Hire Purchase under Shirkatul Melk is a Special type of

contract that has been developed through practice. Actually, it is a synthesis of three contacts:

i) Shirkatul Melk: Shirkat means partnership. Shirkatul Melk means share in ownership.

When two or more persons supply equity, purchase an asset, own the same jointly, and share

the benefit as per agreement and bear the loss in proportion to their respective equity, the

contract is calledShirkatul Melk contract.

25

ii) Ijarah: The term Ijarah has been derived from the Arabic words (Air) and (Ujrat) which

means consideration, return, wages or rent. This is really the exchange value or

consideration, return, wages, rent of service f an asset. Ijarah has been defined as a contract

between two parties, the Hiree and Hirer where the Hirer enjoys or reaps a specific service or

benefit against a specified consideration or rent from the asset owned by the Hiree. It is a hire

agreement under which the Hiree to a Hirer against fixed rent or rentals hires out a certain

asset for a specified period.

iii) Sale: This is a sale contract between a buyer and a seller under which the ownership of

certain goods or asset is transferred by seller to the buyer against agreed upon price paid / to

be paid by the buyer.

Thus, in Hire purchase under Shirkatul Melk mode both the Bank and the

Client supply equity in equal or unequal proportion for purchase of an asset like land,

building, and machinery, transport etc.

Mode wise investment:

26

Investment Sectors:

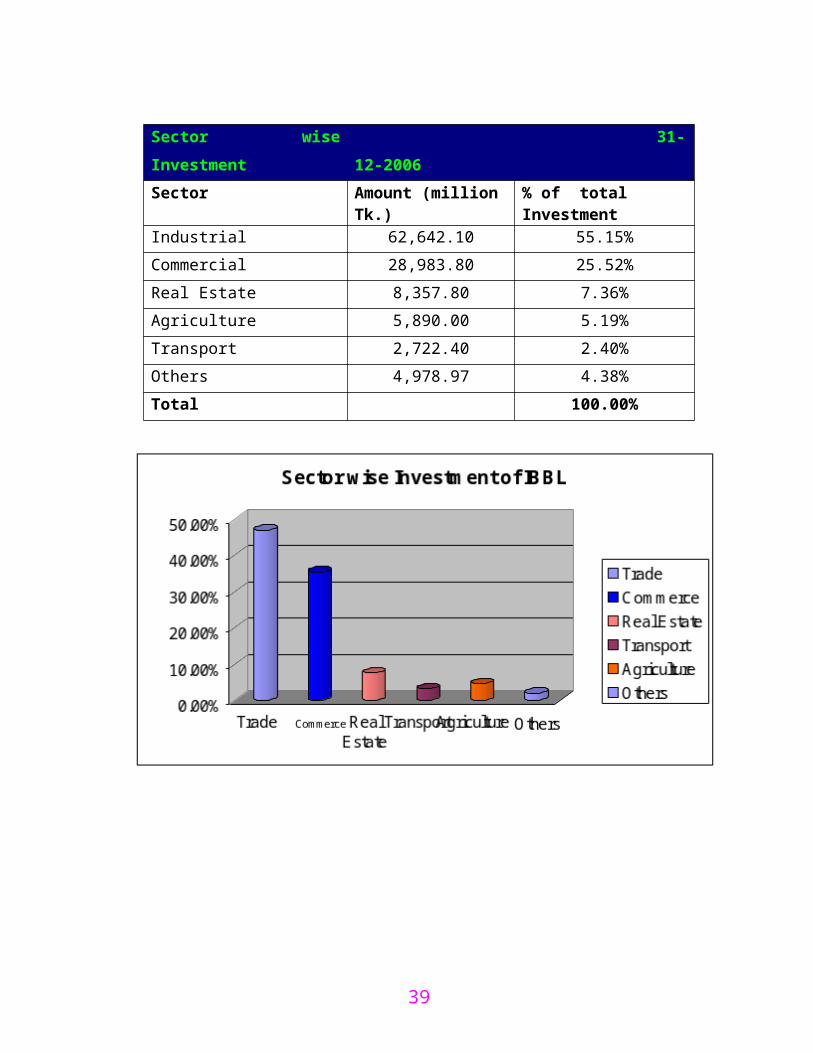

Sector wise Investment 31-12-2006Sector Amount (million Tk.) % of total InvestmentIndustrial 62,642.10 55.15%Commercial 28,983.80 25.52%Real Estate 8,357.80 7.36%Agriculture 5,890.00 5.19%Transport 2,722.40 2.40%Others 4,978.97 4.38%Total 100.00%

27

3.6 SPECIAL INVESTMENT SCHEMES OF IBBL:3.6.1 Household Durable Investment Scheme:In a developing country like Bangladesh people of middle and lower class especially service holders with limited income find it difficult to purchase articles like refrigerator, television, cot, Almirah, wadrobe, sofa-set, pressure cooker, sewing machine etc. which are part of modern and decent living. They cannot enhance the standard and quality of life to the desired level due to constrain of their limited income. Islami Bank Bangladesh Limited has, therefore, introduced Household Durables Investment Scheme that has already created great enthusiasm among the people and received tremendous response from them.

Eligibility:Interested permanent officials of the following organizations may apply for investment:

Government Organizations. Semi-Government Organizations and Autonomous Bodies. Banks and Financial Institutions. Armed Forces, BDR, Police and Ansars. Teachers of Universities, Government Colleges, School and Senior Madrashas. Officers of International Financial & Relief Organization. Officers of the multinational companies. Officers of the local established and renowned public limited companies. House Owners. Investment clients of IBBL. Deposit client of IBBL.

Mode of Recovery: The Bank’s investments and profit thereon shall be recovered in 24 monthly

installments within a period of 2 (two) years. The monthly installment shall be payable by the first week of every month. The first

installment shall be due for payment in the first week of the subsequent month of the disbursement/ delivery of goods/articles.

(Taka in million)Particulars 2001 2002 2003 2004 2005 2006

Household Durable Scheme865.9 886.79 910.91 878.76 782.09 878.76

28

4.6.2 Housing Investment SchemeOne of the basic human needs is to have a house to live in. A house is an abode of peace and happiness. Housing has now become an acute problem in the country, especially in the towns, cities and metropolis. With their limited income, it has become almost impossible on the part of the lower middle class, middle class and sometimes, even for upper middle class to solve their housing problem. To meet this basic human need, Isalmi Bank Bangladesh Limited is committed to contribute to this end to provide a peaceful and happy living. The Bank has introduced “Housing Investment Scheme” with the objective to ease and minimize the housing problem and assist service holders and professionals with limited income in materializing their dream of becoming owner of housing.

Eligibility: Initially the following categories of people shall be eligible to apply for availing investment facilities under this Scheme: Officials of the Defense Forces, Permanent Officials of Government, Semi-Government and Autonomous Organizations, Teachers of the established Universities, University Colleges & Medical Colleges etc.

Target Area:At the initial stage, the Scheme is being implemented in all divisional area

29

Trend of Household Durable Scheme

0

200

400

600

800

1000

2001 2002 2003 2004 2005 2006Year

T k. (i n m ill .)

Period of investment: The maximum period of investment shall be generally 15 years. Reasonable gestation period for construction be allowed considering the size of

construction and Bank’s investment.

Disbursement Procedure of Investment:Bank will pay the sanctioned money through Pay-Order directly or through investment client to the supplier of construction materials/owner of the built house. However, the following points shall be taken into consideration in disbursing the investment:

In case of purchase of apartment/flat/built house, the client shall have to deposit the equity money in the Branch of produce documentary evidence in support of his investment up to the satisfaction of the concerned Branch.

In case of construction of house on the client’s own land or for extension of the existing house, the valuation of the Bank as regards client’s investment shall be consideration final.

The client shall have to submit to the Bank, the construction plan approved by the competent authority and also the required permission to mortgage the property, where necessary.

The client must execute all necessary documents including mortgage deed and complete all necessary documentation formalities to avail the investment. Related documents of mortgage, agreement of sale and other documents must be vetted by the penal lawyer of the Bank.

Recovery of Bank’s Investment: The client shall have to pay the Bank’s dues by monthly installment immediately after the

expiry of the period of construction. The Bank shall realize the amount of monthly installment by depositing the cheque of a

particular month on the first week of every month. The client shall have to execute irrevocable power of attorney in favor of the Bank

authorizing the Bank to collect monthly rent from the tenants incase of failure of the client to pay the monthly installment.

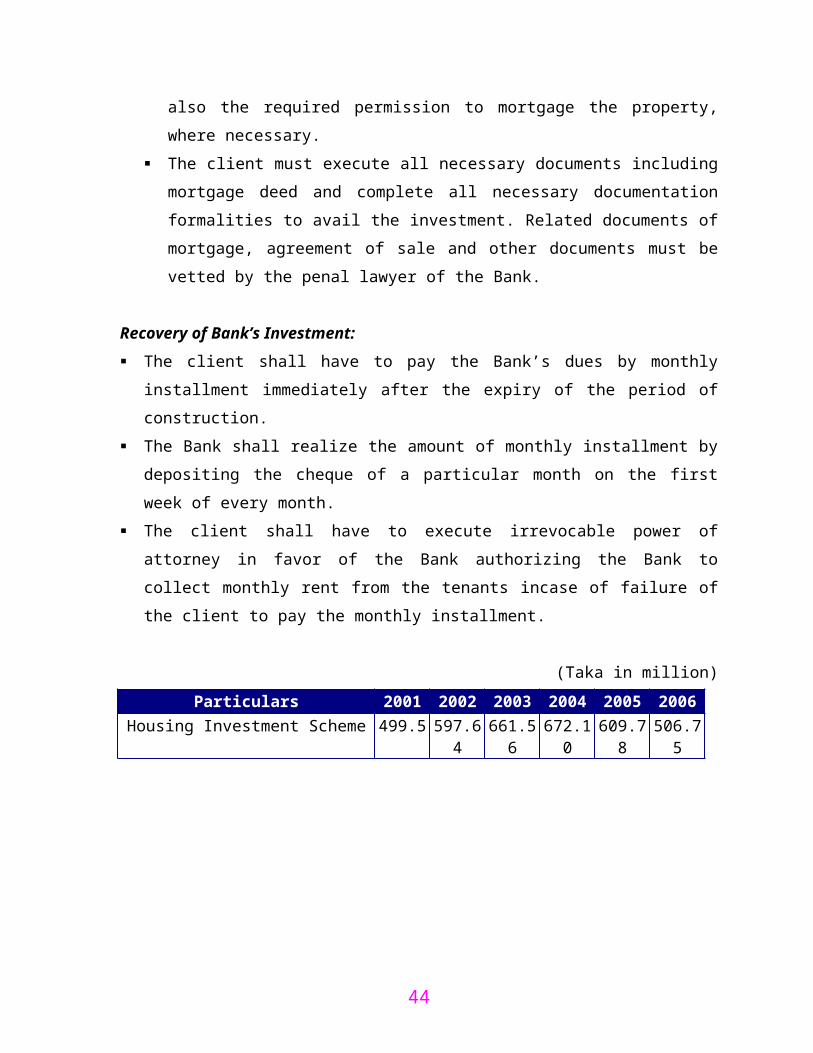

(Taka in million)Particulars 2001 2002 2003 2004 2005 2006

Housing Investment Scheme 499.5 597.64 661.56 672.10 609.78 506.75

30

Trend of Housing Investment Scheme

0100200300400500600700

1999 2000 2001 2002 2003

Year

TK(in

mill

ion)

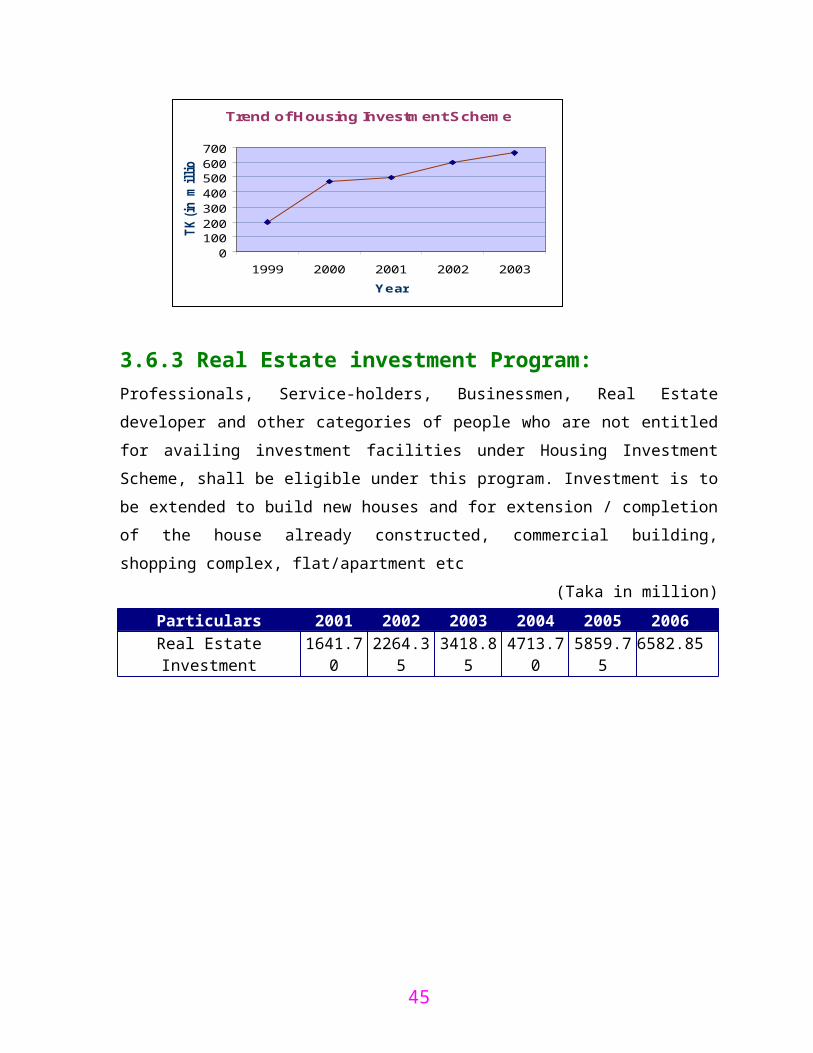

3.6.3 Real Estate investment Program:Professionals, Service-holders, Businessmen, Real Estate developer and other categories of people who are not entitled for availing investment facilities under Housing Investment Scheme, shall be eligible under this program. Investment is to be extended to build new houses and for extension / completion of the house already constructed, commercial building, shopping complex, flat/apartment etc

(Taka in million)Particulars 2001 2002 2003 2004 2005 2006

Real Estate Investment 1641.70 2264.35 3418.85 4713.70 5859.75 6582.85

Trend of Real Estate Investment

0

1000

2000

3000

4000

1999 2000 2001 2002 2003

Year

TK(in

mill

ion)

31

3.6.4 Transport investment ProgramThe role modern communication is most vital for the socio-economic growth and uplift of a developing country like Bangladesh. A sound and efficient communication network is the pre-requisite for sustained development through the expansion of trade, commerce and industry. In this backdrop the demand for road and water transport has increased manifold throughout the country. Moreover, the use of modern transports has increased keeping pace with the rise of standard of living of professionals. Considering all these facts, Islami Bank Bangladesh Limited has introduced ‘Transport Investment Scheme’ Under this scheme investment on easy terms is being extended to the existing successful businessmen in road and water transports and potential entrepreneurs in this sector for different types of road and water transport. Besides, Multinational companies, established business house and well to do officials and professionals can become owner of various kinds of transports through Hire Purchase under scheme.

Mode of Transports: Road Transports, Water Transport.. Target Group

Bus/Truck/Minibus Private car/Microbus/ Jeep Auto Rickshaw/ Tempo/ Pick-up van Ambulance. Water transport

.Period of Investment: Maximum 3 years from the date of delivery of the vehicle.

Mode of disbursement: Bank’s sanctioned amount shall be disbursed directly to the supplier of the vehicles. The client shall have to complete all documentation formalities including mortgage of

property before disbursement of the Bank’s investment. The cost of chassis and bodybuilding shall be taken into consideration in ascertaining

the price.Recovery of Bank’s Investment

The client shall have to repay the dues to the Bank in monthly installment stating immediately after the expiry of the gestation period fixed by the Bank.

The Bank shall collect the monthly installment of a particular month through encashment of the cheque in the first week of the concerned month.

If a client fails to pay 3 consecutive installments, the Bank can take back the possession of the vehicle from the client and sell or transfer it to another client.

32

(Taka in million)

Trend of Transport Investment Scheme

0

500

1000

1500

2000

2500

1999 2000 2001 2002 2003

Year

Tk.(i

n m

ill.)

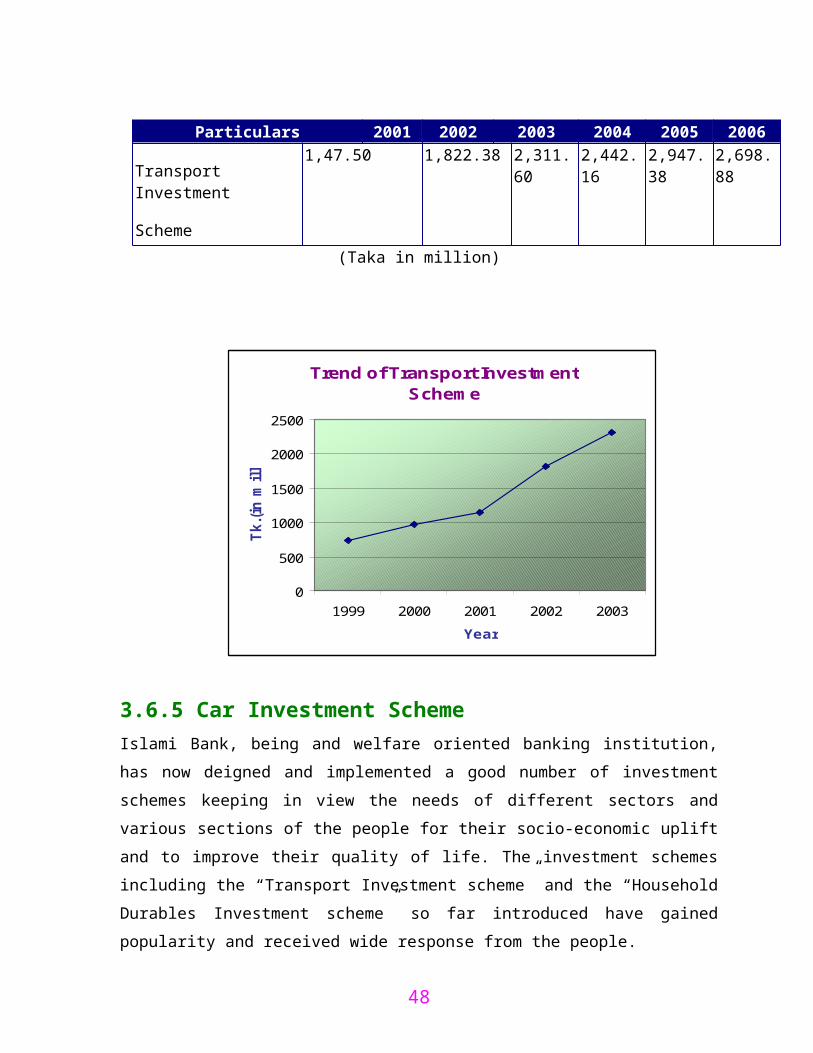

3.6.5 Car Investment SchemeIslami Bank, being and welfare oriented banking institution, has now deigned and implemented a good number of investment schemes keeping in view the needs of different sectors and various sections of the people for their socio-economic uplift and to improve their quality of life. The investment schemes including the “Transport Investment scheme” and the “Household Durables Investment scheme” so far introduced have gained popularity and received wide response from the people.

Car is considered as on essential mode of transport in the modern society, particularly by a section of the officials, business houses and business executives and established professionals for movement in discharging their duties and responsibilities punctually and efficiently. Many of these categories of people cannot purchase a car on payment of entire purchase value at a time out of their own sources. To meet this need Islami Bank has introduced the ‘Car Investment Scheme’ for the mid and high ranking officials of government and semi-government organizations, corporations, executive and directors of big business houses and

Particulars 2001 2002 2003 2004 2005 2006

Transport Investment

Scheme

1,47.50 1,822.38 2,311.60 2,442.16 2,947.38 2,698.88

33

companies and also for persons of different professional group on easy payment terms and conditions.

Eligibility Permanent senior officers/executives of the following organizations: Government Organizations, Semi-Government Organizations/Autonomous Bodies/Corporations, Banks, Commissioned Officer of Armed forces, BDR, Police and Ansars, Teachers of the Universities, Government Colleges, Executives/ Directors of big companies and business houses of repute, Members of all other professional groups having good income.

Client’s EquityMinimum 30% of the purchase cost of the vehicle. The amount of equity shall have to be deposited with the Bank before disbursement of Bank’s investment.Period of InvestmentPeriod of investment is maximum, 4 (four) years from the date of disbursement or delivery of the vehicle to the client, whichever is earlier.Mode of RecoveryDues to the Bank shall recover in the following manner:

In equal monthly installment along with monthly rent, The monthly installment shall be payable by the first week of every month. Post-dated cheques for the whole period of investment mentioning the amount of

monthly installment shall have to be deposit by the client. The amount of monthly installment shall not exceeded 50% of the total income of the

client The Branch shall have the right to take possession of the vehicle in case of failure of

the client to pay 3 (three) consecutive monthly installments.

(Taka in million) Particulars

2001 2002 2003 2004 2005 2006

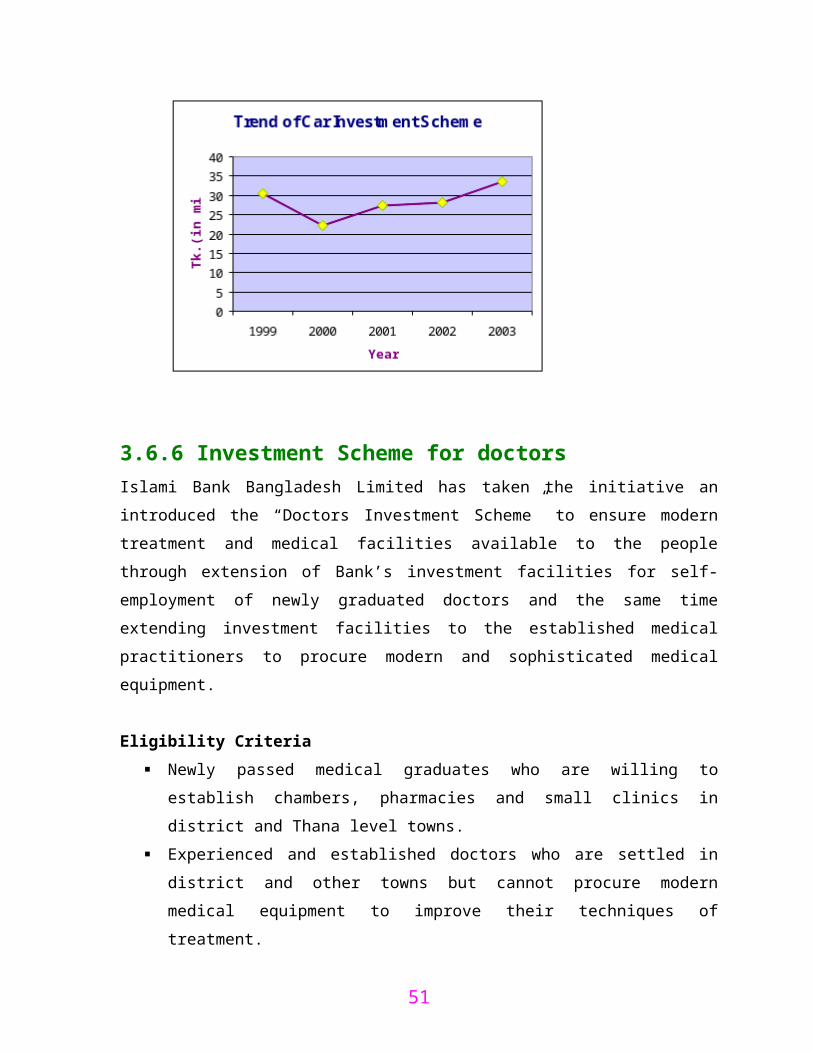

Car Investment Scheme 27.40 28.25 33.58 30.30 27.75 23.54

34

3.6.6 Investment Scheme for doctorsIslami Bank Bangladesh Limited has taken the initiative an introduced the “Doctors Investment Scheme” to ensure modern treatment and medical facilities available to the people through extension of Bank’s investment facilities for self-employment of newly graduated doctors and the same time extending investment facilities to the established medical practitioners to procure modern and sophisticated medical equipment.

Eligibility Criteria Newly passed medical graduates who are willing to establish chambers, pharmacies

and small clinics in district and Thana level towns. Experienced and established doctors who are settled in district and other towns but

cannot procure modern medical equipment to improve their techniques of treatment. Specialized and consulted physicians who are willing to procure latest and specialized

type of medical equipment. Newly passed medical graduates who are willing to from groups in order to establish

clinic. Priority is given to specialist and consultant physicians like dentists, child specialists,

and ophthalmologists etc.

35

Equity: Newly graduated doctors under self-employment scheme 10%, Established doctors 20%, Established Clinics 30%

Mode of repayment Investment of the Bank is to be repaid on monthly installment basis. Re-payment of the 1st installment will start after three months from the date of

investment. If the client fails to pay back three consecutive installments without any satisfactory

reasons, the bank may take possession and control of the machinery and equipment etc. supplied by the Bank.

(Taka in million) Particulars 2001 2002 2003 2004 2005 2006

Investment Scheme for Doctors 95.10 97.21 101.01 85.54 64.42 33.38

36

3.6.7 Small Business Investment Scheme The Bank, to make effective contribution in this respect, has taken-up a special program and introduced ‘Small Business Investment Scheme’ to make the small traders, entrepreneurs and neglected unemployment youth of urban and rural areas self-reliant by providing them required financial supportEligibility of the Clients

Investment clients must be permanent residents of the command area of the branch They must have valid trade license and shops or selling centers. Small business man and entrepreneurs, who has the shortage of fund/capital, will also

be eligible to avail investment facilities under the Scheme. Investment shall also be extended to those poor and asset-less unemployed youths,

especially those who have ability to run business. Besides the above categories, investment facilities under this Scheme shall also be

extended to small and cottage industries and service sector.

Sectors of Investment: Livestock, Fishery, Agro-processing, Manufacturing, Trading/shop keeping, Transport, Services, Agriculture Implements and Forestry.Mode of Investment

Hire purchases Shirkatul Meelk: For all kinds of machineries i.e. equipments & transport sector.

Bai-Muajjal-TR: For trading shop keeping, agro-processing and raw materials for manufacturing purposes.

Period of Investment: In case of HPSM: Maximum 24 months, In case of Bai-Muajjal-TR: Maximum 12 months.Client’s Equity: For HPSM Investment: Maximum 20% on cost price of the machineries/vehicles, For Bai–muajjal-TR: Nil. Recovery Procedure:

For HPSM investment: Monthly installment basis For Bai-Muajjal-TR: Monthly/Quarterly/Half-yearly installment/ lump-sum/ at a

time-within the date of expiry.

37

(Taka in million)Particulars 2001 2002 2003 2004 2005 2006

Small Business Investment Scheme

244.10 325.06 395.75 501.26 629.81 768.45

3.6.8 Agriculture Implements Investment SchemeIslami Bank Bangladesh Limited is a welfare oriented Bank. It can play positive and important role in the economic development, progress and uplift of the country by investing in the agriculture sector. The Bank has, therefore, introduced “ Agriculture Implements Investment Scheme” to provide power tillers, power pumps shallow tube wells, thrasher machine etc. on easy terms to the unemployed youths for self-employment and to the farms to help augment production in agricultural sector.Type of Agriculture Implements: Power tillers, Thrasher Machine, Any other agricultural implements proposed by the branch and which has local demand.Investment Area:Investments are allowed under this Scheme through all branches of the Bank expected the branches located in the metropolitan areas. The command area of the concerned branch is within 15 miles radius from its location.

38

Eligibility of Investment Clients: Educated or half-educated rural youths, educated or illiterate farmers and any person

may apply for investment facilities under this scheme. The applicant must be physically and mentally fit and willing to operate the machine

himself. Applicant must be a permanent resident of the concerned area and be willing to stay

and work there.Period of Investment: Two years Mode of Investment: Hire Purchase under Shirkatul Melk.Client’s Equity: Client shall have to pay 20% of the cost of agriculture implements/equipment as equity. Equity shall be 10% if the Bank undertakes any special project under the supervision of any registered NGO approved by the Bank. Repayment Producer: The investment shall have to be repaid in 4 installments within a year. The installment shall be fixed on the basis of the sowing/transplantation and harvesting seasons of the crop. The branch Manager shall decide both the amount and time of the repayment of installment.

(Taka in million)Particulars 2001 2002 2003 2004 2005 2006

Small Business Investment Scheme

244.10 325.06 395.75 501.26 629.81 768.45

39

4.3.9 Micro Industries Investment SchemeIslami Bank Bangladesh Ltd. has been appreciably participating in this direction by financing industrial sector. With a view to creating wider base for industries, the Bank has decided to launch “Micro Industries Investment Scheme” through its Branches. This scheme has been devised to cater to the investment needs of those persons who intend to set-up new micro industrial ventures or to restructure their old units by way of BMRE involving a total cost of Tk. 5.00 lac.This is intended mainly to create new jobs for the educated, skilled & semi skilled unemployed and also to encourage those who remain outside the purview of investment due to shortage of funds and insufficient collaterals. The scheme has been prepared with easy terms and conditions to encourage the small entrepreneurs, educated unemployed youths and skilled/semi skilled persons to come forward for establishment of micro industries commensurate with the local demand.

EligibilityThe eligibility criteria for the selection of the entrepreneurs under the scheme will be as under:

Engineering diploma or degree holders, or persons having diploma or certificate from any Technical/Vocational Training Institutes and willing to set up micro industries.

Educated unemployed youths having initiative and knowledge regarding the proposed industry.

Skilled and semi-skilled persons having practical knowledge and experience in industrial operations.

Persons already engaged in micro-industries as owners and willing for BMRE of their enterprises.

Wage earners who want to establish micro industries having work experience/training in the particular field of industry.

The proposed enterprise must be exclusively owned by Bangladeshi Nationals that use indigenous raw materials or imported raw materials not exceeding 25% of the total requirement of raw materials.

Defaulters and persons/enterprises having outstanding liabilities with other Banks and Financial Institutions will not be eligible for availing investment under the scheme.

Sectors of Investment

40

Different sectors including food and agriculture based industries, plastic & rubber industries, forestry and furniture industries, engineering industries, lather industries, chemical industries, textile industries, recycling industries, service industries, electrical accessories industries, computer technology industries, paper products industries, handicraft industries, fishery & livestock farming, hollow bricks, roof tiles and any other viable micro-industries have been identified for financing under the Scheme.Period of InvestmentCapital Machinery: 5(five) years including reasonable gestation period.Raw materials: One year from the date of 1st disbursement.Mode of InvestmentCapital Machinery: Hire-Purchase Shirkatul Melk (HPSM)Raw Materials: Bai-Muajjal.Recovery of Bank’s dues:

Hire Purchase: In monthly/fortnightly/weekly installment basis. Bai-Muajjal: In Lump sum at the end of the tenure of investment.

Command AreaInvestment under the Scheme shall be made within the 20 Km. radiuses from the branch.

(Taka in million)Particulars 2001 2002 2003 2004 2005 2006

Micro Industry Investment Scheme

6.30 6.63 10.10 17.18 10.21 6.24

41

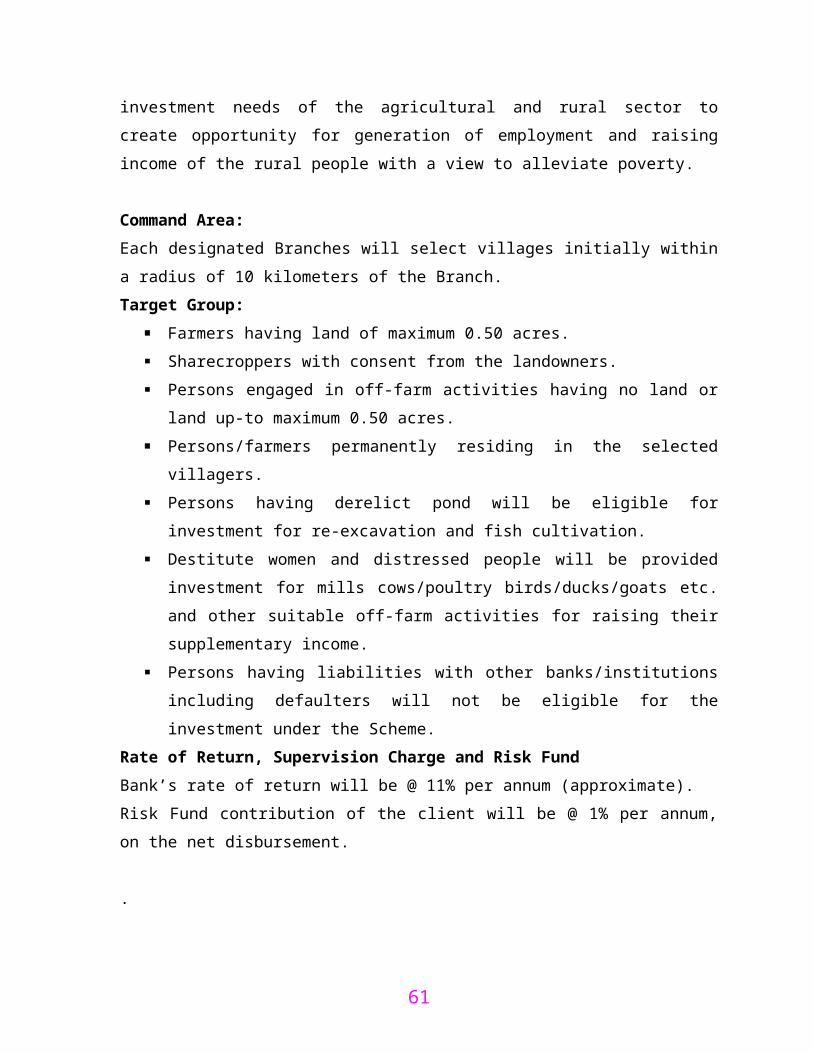

3.6.10 Rural development Scheme. Islami Bank Bangladesh Limited has been founded with the major objective of establishing Islamic economy for balanced economic growth by ensuring reduction of rural-urban disparity and equitable distribution of income. In view of the above, Branches of the Bank have been encouraged to invest their deposits in their respective areas and in particular for the economic uplift of the rural people.Accordingly, a Scheme in the name and style of ‘Rural Development Scheme’ has been introduced to cater tot eh investment needs of the agricultural and rural sector to create opportunity for generation of employment and raising income of the rural people with a view to alleviate poverty.

Command Area:Each designated Branches will select villages initially within a radius of 10 kilometers of the Branch. Target Group:

Farmers having land of maximum 0.50 acres. Sharecroppers with consent from the landowners. Persons engaged in off-farm activities having no land or land up-to maximum 0.50

acres. Persons/farmers permanently residing in the selected villagers. Persons having derelict pond will be eligible for investment for re-excavation and fish

cultivation. Destitute women and distressed people will be provided investment for mills

cows/poultry birds/ducks/goats etc. and other suitable off-farm activities for raising their supplementary income.

Persons having liabilities with other banks/institutions including defaulters will not be eligible for the investment under the Scheme.

Rate of Return, Supervision Charge and Risk FundBank’s rate of return will be @ 11% per annum (approximate).Risk Fund contribution of the client will be @ 1% per annum, on the net disbursement.

.

Sanction and Disbursement

42

On the basis of the list submitted by the field officer, the Investment Committee of the Branch will carefully scrutinize the applications and sanction the investment at the Branch level. The members of the Committee will consist of Manager, Project Officer and the field officer. After sanction of the investment the Branch will complete documentation formalities and then disburse the amount with the help of the Investment Officer and field officers. In the entire case Branch must ensure strict adherence tot eh banking and Shariah norms.

Modes of InvestmentThe Branch will select any of the following modes depending upon the sector and purpose of investment:

Bai-Muajjal TR Hire-Purchase under Shirkatul Melk (HPSM) or Leasing Mudaraba Musharaka Bai-Salam Murabaha TR

Recovery of InvestmentTo ensure recovery of investment in time, the Branch will determine the investments judiciously. Installments should be fixed in the following manner, keeping in view the income generation capacity of the investment and time thereof:

In case of off-farm activities installments should be fixed on weekly basis. In case of agricultural/crop production, installment should be fixed on quarterly basis

or on the basis of harvesting period of the crop in each of the investment area. A token installment may however be realized on weekly basis.

(Taka in million)Particulars 2001 2002 2003 2004 2005 2006

Rural Development Scheme 371.10 432.04 570.88 789.97 1,106.47 2,242.22

43

Table:(Tk.in million)

Investment in different schemesParticulars 2002 2003 2004 2005 2006

Rural Development Scheme 432.04 570.88 789.97 1,106.47 2,242.22House Durable Scheme 886.79 910.91 878.76 782.09 699.95Investment Scheme for Doctors 97.21 101.01 85.54 64.42 33.38Transport Investment Scheme 1,822.38 2311.6 2,442.16 2,947.38 2,698.88Car Investment Scheme 28.25 33.58 30.30 27.75 23.54Small Business Investment Scheme 325.06 395.75 501.26 629.81 786.45Micro-Industries Investment Scheme 6.63 10.1 17.18 10.21 6.24Agricultural Implements Investment Scheme

13.66 12.76 14.69 12.53 11.94

Housing Investment Scheme 597.64 661.56 672.10 609.78 506.75Real Estate Investment program 2264.35 3418.85 4,713.70 5,859.75 6,582.85Fig: Outstanding amount of investment as at the year end under different welfare Schemes are as under:

44

Sector wise distribution of investment as on December 31, 2006 vis-à-vis corresponding period of last year are given below:

Investment in Different Sector:

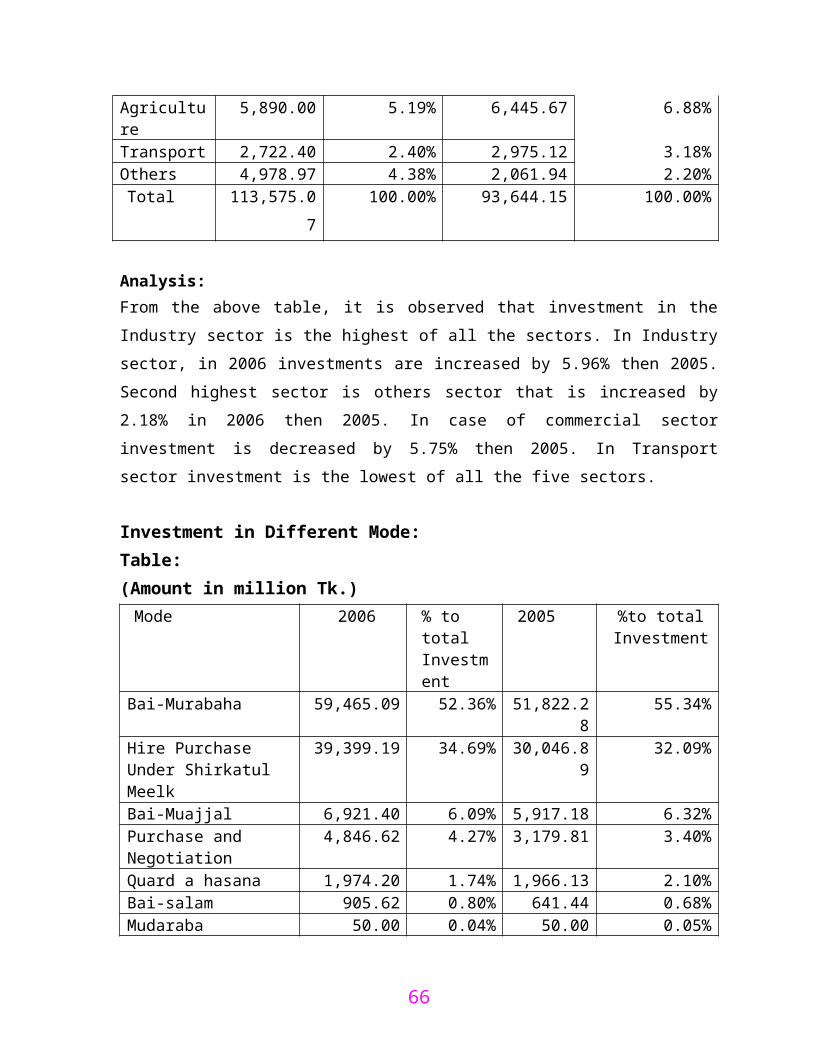

Table: (Tk in million)Sector 2006 % to total

Investment 2005 % to total

InvestmentIndustrial 62,642.10 55.15% 46,063.51 49.19%Commercial 28,983.80 25.52% 29,284.21 31.27%Real Estate 8,357.80 7.36% 6,813.70 7.28%Agriculture 5,890.00 5.19% 6,445.67 6.88%Transport 2,722.40 2.40% 2,975.12 3.18%Others 4,978.97 4.38% 2,061.94 2.20%Total 113,575.07 100.00% 93,644.15 100.00%

Analysis:From the above table, it is observed that investment in the Industry sector is the highest of all the sectors. In Industry sector, in 2006 investments are increased by 5.96% then 2005.

45

Second highest sector is others sector that is increased by 2.18% in 2006 then 2005. In case of commercial sector investment is decreased by 5.75% then 2005. In Transport sector investment is the lowest of all the five sectors.

Investment in Different Mode: Table: (Amount in million Tk.)

Mode 2006 % to total Investment

2005 %to total Investment

Bai-Murabaha 59,465.09 52.36% 51,822.28 55.34%Hire Purchase Under Shirkatul Meelk

39,399.19 34.69% 30,046.89 32.09%

Bai-Muajjal 6,921.40 6.09% 5,917.18 6.32%Purchase and Negotiation 4,846.62 4.27% 3,179.81 3.40% Quard a hasana 1,974.20 1.74% 1,966.13 2.10%Bai-salam 905.62 0.80% 641.44 0.68%Mudaraba 50.00 0.04% 50.00 0.05%Musharaka 12.95 0.01% 20.42 0.02%Total 113,575.07 100.00% 75,858.56 100.00%

Analysis: The above table shows that in 2006 Investment increased 2.60%

than 2005 under Hire purchase mode. 0.87% under Purchase & Negotiation mode,

remaining does not positively increased rather most of them are decreased.

.

46

CHAPTERFOUR: FOREIGN EXCHANGE OPERATION

OF IBBL

4.1 Introduction:

Foreign trade is a business activity, which transcends national boundaries. These may be

occurred between two parties or governments. Trades among nations are a common

occurrence and normally benefits both the exporter and importer in many countries

international trade accounts for more than 20 % of their national incomes.

Foreign trade can usually be justified on the principle of comparative advantage according to

this economic principle. It is economically profitable for a country to specialize in the

production of that commodity in which the producer country has the greater comparative

advantage and to allow the other country to produce that commodity in which it has the lesser

comparative advantage. It includes the spectrum of goods services, investment, technology

transfer etc. this trade among various countries pauses for close linkage between the parties

dealing with trade. The bank, which provides such transactional trade, demands a few of

goods from seller to buyer and of payment form buyer to seller. And this flow of goods and

payment are done through letter of credit (L/C).

4.2 FOREIGN EXCHANGE:

As more than one currency is involved in foreign trade, it gives rise to exchange of

currencies which is known as foreign exchange. The term “Foreign Exchange’ has three

principal meanings. Firstly, it is a term used referring to the currencies of the other countries

47

in terms of any single one currency. To a Bangladeshi, Dhaka, pound sterling etc. are foreign

currencies and as such foreign exchange. Secondly, the term also commonly refers to some

instruments used in international trade, such as bill of exchange. Drafts, Traveler cheek and

other means of international remittance. Thirdly, the term foreign exchange is also quite

often referred to the balance in foreign currencies held by a country. In terms of section 2(d)

of the foreign exchange regulations 1947, is adopted in Bangladesh. Foreign exchange means

foreign currency and includes any instrument drawn accepted made or issued under clause

(13) of article 16 of the Bangladesh Bank order 1972, all the deposits, credits and balances

payable in any foreign currency and draft check, letter of credit and bill of exchange

expressed or drawn in Bangladesh currency but payable in any foreign countries.

In exercise of the power conferred by section 3 of the foreign exchange regulation, 1947

Bangladesh Bank issues license to schedule Bank to deal with exchange. These banks are

known as Authorized Dealers. Licenses are also issued by Bangladesh Bank to person or

firms to exchange foreign currency instruments such as T.C. Currency notes and coins. They

are known as Authorized Money changers.

4.3 Functions of Foreign Exchange Department:

Exports:

Pre shipment advanced

Purchase of foreign bills

Negotiating of foreign bill.

Export guarantees

Advising / confirming letters – letters of credit

Advance for deferred payments exports

Advance against bills for collection

Imports: 1. Opening of letter of credit.

2. Advance bills.

3. Bills for collection.

4. Import loans and guarantees.

48

Remittances: Issue of DD, MT, TT etc.

Payment of DD, MT, TT etc.

Issue and enhancement of travelers check.

Sale and enhancement of foreign currency notes

4.4 THE MOST COMMONLY USED DOCUMENTS IN FOREIGN

EXCHANGE: Documentary Letter of Credit.

Bill of exchange.

Bill of Lading.

Commercial invoice.

Certificate of Origin of Goods.

Insurance Certificate.

Packing List.

Insurance Policy.

Pro- forma Invoice / Indent.

Master Receipt.

G.S.P Certificate.

DOCUMENTARY LETTER OF CREDIT:

In simple terms a documentary credit is a conditional bank undertaking of payment.

Expressed more fully, it is a written undertaking by a bank (issuing bank) given to seller

(beneficiary). At the request, and in accordance with the instructions of the buyer

(applicant) to effect payment (that is, by making a payment, or accepting or negotiating

bill of exchange) up to a stated sum of money, with in a prescribe time limit and against

stipulated documents.

The Customary Clauses Contain in an L/C is as followings:

A clause authorizing the beneficiary to draw bills of exchange up to a certain limit.

49

List of shipping documents, which are to accompany the bills.

Description of the goods to be shipped. An undertaking by the opening bank that bills

drawn in accordance with the conditions will be dully honored.

Instructions to the negotiating bank for obtaining reimbursement of payments under

the credit.

Parties involved in letter of Credit:

The parties to L/C are:

Importer/ buyer

Opening Bank / Issuing Bank

Exporter /seller / Beneficiary

Advising Bank /Notifying Bank

Negotiating bank

Confirming Bank

Paying /reimbursing bank

BILL OF LAFING:

A bill of lading is a document that is usually stipulated in a credit when the goods are

dispatched by sea. It is evidence of a contract of carriage, is a receipt for the goods, and is a

document of tile to the goods. It also constituted a document that is, or may be, needed to

support insurance.

The details on the bill of lading should include:

Description of the goods in general terms not inconsistent with in the credit.

Identify marks and numbers, if any

The name of the carrying vessel

Evidence that the goods have been loaded on board

The ports of ships of shipment and discharge

The names of shipper, consignee and name and address of the notifying party.

Whether freight has been paid or is payable at destination

The number of original bill of lading issued

The date of issuance

50

A bill of lading specifically stating that goods are loaded for ultimate destination specifically

mentioned in the credit.

COMMERCIAL INVOICE:

A Commercial invoice is the accounting document by which the seller charges the goods to

the buyer a commercial invoice normally includes the following information:

Date

Name and address of the buyer and seller

Order of contract number, quantity and description of the goods. Unit price and the

total price

Weight of the goods, number of the package, shipping marks and numbers.

Terms of delivery and payment

Shipment details

CERTIFICATE OF ORIGIN:

A certificate of origin is a signed statement providing evidence of the origin of the goods.

INSPECTION CERTIFICATE:

This is usually issued by an independent inspection company located in the exporting country

certifying or describing the quality, specification or other aspects of the goods, as called for

in the contract and the L/C. The inspection company is usually nominated by the buyer who

indicates the types of inspection what he/she wishes to undertake by the inspection company.

INSURANCE CERTIFICATE:

The insurance certificate document must:

Be specified in the credit;

Be covered the risk specified in the credit;

Be consistent with the other documents in its identification of the voyage and

description of the goods.

Unless otherwise specified in the credit it would:

51

Be a document issued and / or signed by an insurance company or its agent, or by

underwriters;

Be dated on or before the date of shipment as evidenced by the shipping documents;

Be for an amount at least equal to the CIF value of the goods and in the currency of

credit.

4.3 IMPORT:

Import is foreign goods and services purchased by consumers, Firms and government in

Bangladesh.

An importer must have Import Registration Certificate (IRC) given by Chief controller of

Import and Exports (CCI & L) to import any thing from other country.

To obtain IRC the following certificates are required: Trade license

Income tax certificate

Nationally certificate -

Banks solvency certificate

Asset certificate

Registration partnership deed (if any)

Memorandum and article of association

Certificate of incorporation (if any)

Rent receipt of the business premises

IMPORT PROCEDURE:

To import through Islami Bank Bangladesh Ltd a customer requires the following:

Bank Account

Import registration certificate

Tax paying identification number

Pro forma invoice/indent

Membership certificate

L/C application form duly attested

Insurance cover note with money receipt

Others

52

Importer’s application for L/C limit/margin:To have an import L/C limit, an application must submit to the department of RBL furnishing

the following information.

Full particulars of bank account.

Natural of business