Embed Size (px)

Citation preview

Document of

The World Bank

FOR OFFICIAL USE ONLY

Report No: 74108-MG

RESTRUCTURING PAPER

ON A PROPOSED PROJECT RESTRUCTURING

OF

ACGF - MADAGASCAR FINANCIAL SERVICES PROJECT (TF-092098)

Approved on June 5, 2008

TO THE REPUBLIC OF MADAGASCAR

December 11, 2012

Finance and Private Sector Development Africa Region This document has a restricted distribution and may be used by recipients only in the performance of their official duties. Its contents may not otherwise be disclosed without World Bank authorization.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

ABBREVIATIONS AND ACRONYMS

ACGF Africa Catalytic Growth Fund AfD Agence française de Développement (French Development Agency) AGEPASEF Association pour la Gestion du Programme d’Appui aux Services Financiers

(Financial services project implementing entity) APIMF Association Professionnelle des Institutions de Microfinance (Microfinance

Institutions Professional Association) BCM Banque Centrale de Madagascar (Central Bank of Madagascar) BDS Business development services BOA Bank of Africa CRM Centrale des Risques de la Microfinance (Credit bureau) CSBF Commission de Supervision Bancaire et Financière (Banking Commission) ELA Exclusion List of Activities ESMF Environmental and Social Management Framework GDP Gross Domestic Product GoM Government of Madagascar ICR Implementation Completion and Results Report IDA International Development Association IFC International Finance Corporation ISN Interim strategy note MFB Ministry of Finance and Budget MFI Microfinance institution MIS Management information system MoF Ministry of Finance MSME Micro, small and medium enterprise NPL Non-performing loan PPCG Partial portfolio credit guarantee PCU Project coordination unit PIE Project implementation entity PDO Project development objective PFI Participating financial institution ROA Return on assets ROE Return on equity RSF Risk Sharing Facility RVP Regional Vice President TA Technical assistance

Regional Vice President: Makhtar Diop Country Director: Haleh Bridi Sector Manager: Irina Astrakhan

Task Team Leader: Josiane V. Raveloarison

REPUBLIC OF MADAGASCAR ACGF - MADAGASCAR FINANCIAL SERVICES PROJECT

P109607 CONTENTS

A. SUMMARY ............................................................................................................... 1

B. PROJECT STATUS ................................................................................................. 1

C. PROPOSED CHANGES .......................................................................................... 2

Annex 1: Results Framework and Monitoring ........................................................... 16

Annex 2: Implementation Schedule ............................................................................. 23

Annex 3: OP 8.30 Compliance Review ......................................................................... 24

Restructuring Status: Draft Restructuring Type: Level one Last modified on date : 12/11/2012

1. Basic Information Project ID & Name P109607: MG-ACGF Financial Services (FY08) Country Madagascar Task Team Leader Josiane V. Raveloarison Sector Manager/Director Irina Astrakhan Country Director Haleh Z. Bridi Original Board Approval Date 06/05/2008 Original Closing Date: 12/31/2012 Current Closing Date 12/31/2012 Proposed Closing Date [if applicable] 12/31/2016 EA Category C-Not Required Revised EA Category FI – Financial Intermediary Assessment EA Completion Date Revised EA Completion Date

2. Revised Financing Plan (US$m) Source Original Revised ACGF 15.00 15.00 BORR 0.00 0.00 Total 15.00 15.00

3. Borrower

Organization Department Location Ministry of Finance and Budget (MFB)

Madagascar

4. Implementing Agency

Organization Department Location Agence d’ Exécution du Projet d’Appui aux Services Financiers (AGEPASEF)

Madagascar

5. Disbursement Estimates (US$m) Actual amount disbursed as of 09/30/2012 0.52

Fiscal Year Annual Cumulative 2011-2012 0.00 0.52 2013 1.11 1.63 2014 6.48 8.11 2015 4.70 12.81 2016 1.74 14.55 2017 0.45 15.00 Total 15.00

6. Policy Exceptions and Safeguard Policies Does the restructured project require any exceptions to Bank policies? N Do the restructured projects trigger any new safeguard policies? If yes, please select from the checklist below and update ISDS accordingly before submitting the package.

Y

Safeguard Policy Last Rating Proposed Environmental Assessment (OD 4.01) X Natural Habitats (OP 4.04) Forestry (OP 4.36) Pest Management (OP 4.09) Physical Cultural Resources (OP 4.11) Indigenous Peoples (OD 4.20) Involuntary Resettlement (OP 4.12) Safety of Dams (OP 4.37) Projects in International Waterways (OP 7.50) Projects in Disputed Areas (OP 7.60)

7a. Project Development Objectives/Outcomes Original/Current Project Development Objectives/Outcomes The objective of the Project is to assist the Recipient in increasing access to sustainable financial services, particularly by micro, small and medium enterprises, and households in Madagascar through the improvement of competition and diversification in the financial sector.

7b. Revised Project Development Objectives/Outcomes The objective of the Project is to assist the Recipient in increasing access to sustainable financial services, particularly by micro, small and medium enterprises and households in Madagascar.

1

ACGF - MADAGASCAR FINANCIAL SERVICES PROJECT (P109607) RESTRUCTURING PAPER

A. SUMMARY 1. This restructuring paper seeks your approval to proceed with changes to the Madagascar Financial Services Project (P109607). On February 21, 2012 the Board discussed an Interim Strategy Note (ISN) for Madagascar to guide engagement during FY12-13. The proposed restructuring is consistent with the ISN’s approach to restructure the World Bank’s portfolio. 2. The proposed changes would focus support for a smaller number of large activities that have a bigger impact on access to micro, small and medium enterprise (MSME) finance and on the microfinance sector and withdraw support for activities that the Project is unable to implement under the current political situation or that require policy decisions or legislative reforms.

3. The restructuring would amend the Project’s documents by: (i) revising the Project Development Objective (PDO); (ii) revising planned activities and reallocating resources accordingly; (iii) extending the project closing date from December 31, 2012 to December 31, 2016 to accommodate completion of project activities being financed under this project, with corresponding changes in implementation and disbursement projections; (iv) reallocating funds across disbursement categories and change in the categories; and (v) revising the Results Framework to be coherent with the restructured components and activities. The government has agreed on an action plan (Annex 2). This will be a Level I restructuring. Also, this project is financed under a child trust fund, part of the overall ACGF Trust Fund (TF092098) whose end-disbursement date of April 30, 2014 is extended to December 31, 2017. The Bank project team is confident that with these changes the revised PDO is achievable.

4. In the context of the restructuring an innovative partial portfolio credit guarantee (PPCG) will be put in place through a Malagasy Fund set up for this purpose and managed by a Malagasy financial institution licensed by the bank supervisor. The Funds will be capitalized by the Grant and subject to close monitoring, even after the project closing to ensure appropriate use of resources.

B. PROJECT STATUS 5. The Project, which is financed by a US$15 million grant from the Africa Catalytic Growth Fund (ACGF) became effective on November 28, 2008, immediately before the 2009 political crisis. Cumulative disbursements now stand at US$0.52 million, which reflect the fact that activities have not yet started. All the project activities have been put on hold due to the political crisis and which halted disbursements in the context of OP/BP 7.30. The Project is currently rated Moderately Unsatisfactory for both implementation progress (IP) and progress towards achieving PDO. In both cases the ratings represent an increase from the previous unsatisfactory ratings. In the case of the PDO rating, the increase is due to the substantial progress made over this last semester (June-December 2012) in project restructuring that

2

increases the likelihood for the project to achieve its development objectives once project implementation starts. In the case of the IP, the improvement in rating is due to the fact that the Project Implementation Entity (PIE) has actively participated in the three back-to-back restructuring missions and is closely working with the Bank team on the restructuring. With the Level 1 Restructuring, it is expected to bring project performance to satisfactory levels. Implementation of project activities will start as soon as the restructuring package is approved and disbursements should pick up accordingly. After the extension and as many activities fall into place, it is expected that the project rating will be upgraded at least to Moderately Satisfactory. The team is comforted by the quality and intensity of preparatory activities that have been undertaken by the PIE. C. PROPOSED CHANGES Project Development Objective 6. The proposed PDO is amended to make it leaner and simpler and will permit to have fewer but better focused activities. The proposed PDO and accompanying activities fit within the framework of the World Bank’s Interim Strategy Note (ISN).

Original PDO in the Grant Agreement Proposed revised PDO

The objective of the Project is to assist the Recipient in increasing access to sustainable financial services, particularly by micro, small and medium enterprises, and households in Madagascar through the improvement of competition and diversification in the financial sector.

The objective of the Project is to assist the Recipient in increasing access to sustainable financial services, particularly by micro, small and medium enterprises and households in Madagascar.

Results/indicators

7. The results framework presented in Annex 1 has been revised to take into account improved attribution of project outcomes to activities and components, improved measurability and data availability, and to include mandatory sector indicators.

Components

8. Within the framework of the World Bank’s Interim Strategy Note (ISN) and following GoM’s request dated October 16, 2012, the activities of the Project have been modified. The new activities are better focused to achieve the revised PDO; they build on lessons learned from the Bank and other donors’ past experiences, provide more synergies with projects in the country portfolio such as the Integrated Growth Poles project and promote donors’ partnership.

9. Some activities have been cancelled because they (a) would require policy decisions or legislative reforms; (b) would be outside the scope of the restructured project; and/or (c) would have no impact during the lifetime of the project even if political stability resumes.

3

10. All the other activities remain relevant to the achievement of the PDO. Moreover, they are scaled up and better focused. In that vein the two original components1 are restructured to focus on (i) increasing MSME access to finance and (ii) improving the capacity of microfinance institutions for greater outreach and sustainability. For these two restructured components, the project will finance the establishment of a guarantee fund, technical assistance and equipment purchase, which are provided under specific conditions and selected criteria.

Component 1: Increasing MSME access to finance 11. Under this component, the Project will finance: (i) a partial portfolio credit guarantee (PPCG) including capitalization of the Fund and the meeting fees for the members of its Board of Directors; (ii) audits of the Fund, participating financial institutions (PFIs) and the Fund manager; (iii) technical advisory services and training to PFIs and the Fund manager; (iv) legal assistance for the establishment of the PPCG Fund and the PPCG; and (v) a study on interest rates charged by banks and MFIs to MSMEs. (i) The partial portfolio credit guarantee

Characteristics of the PPCG

12. A PPCG for commercial bank and MFI loans to MSMEs will be put in place. This guarantee scheme takes into account the findings and recommendations of the review of a previous Risk Sharing Facility (RSF) implemented in June 2006 under the Madagascar Integrated Growth Poles Project as well as World Bank and IFC project implementation experience in this area. The RSF involved the International Development Association (IDA), the International Finance Corporation (IFC) and two banks, BNI-Crédit Lyonnais Madagascar and BFV-Société Générale. The review of the RSF noted that its main shortcoming was in a lack of sustainability, institutionalization, and ownership of the program. 13. The PPCG will cover 50 percent of the credit (principal plus interest), the participatory financial institutions (PFIs) assuming the other 50 percent. At the beginning, a multiplier of two will be applied to the capital of the fund (constituted by seed money plus reinvested profits). Combining the percentage guaranteed and the multiplier, the amount of credit guaranteed can be four times the amount of capital. The objective of this guarantee is to fill a noted gap2 in lending to MSME and thereby increases access to finance, an important contributor to growth and poverty reduction.

14. An important characteristic of the PPCG is its automatism simplifying the guaranteeing process. All credits originated by PFIs and falling within pre-defined eligibility criteria (size of the firm, sector of activity, maximum/minimum credit size, and credit term to maturity) will be automatically registered on the guarantee. The PFIs will perform analysis of the credit according to their own procedures. While the PPCG covers many sectors and short, medium and long term credit as well as overdrafts, it is expected that the portfolio guaranteed will be diversified and not

1 Third component: Project implementation and Monitoring and Evaluation remains unchanged. 2 Many factors explain this gap, such a lack of transparency of MSMEs, banks lack of familiarity with them, lack of banking services tailored to MSME needs, insufficient collateral, etc.

4

all credit will be short term. In order to ensure this outcome, benchmarks will concern the minimum percentage of medium to long term credit for investment purposes in the portfolio as well as the credits to industry and agriculture, as specified in the Procedures Manual. 15. It is expected that the credits benefitting from the PPCG will be credits to existing customers that have not borrowed from the PFI but have deposit accounts or to new customers. This will contribute to additionality. Quite often, a PFI will consider a client creditworthy but because of lack of sufficient collateral will not extend the credit. The PPCG is expected to compensate for insufficient collateral and, thus, increase access to financing. In this context, the funds provided by ACGF will be used to partially finance credit risk associated with bank or MFI lending.

16. The PPCG should be self-sustainable. The guarantee fees paid by the PFIs and the proceeds from the investment of the seed money should cover claims and operating expenses. At start, the guarantee fees are estimated at 2 percent of the amount guaranteed and the operating expenses will be capped. The Governmet of Madagascar (GoM) has indicated that after the closing of the project, the resources will remain within the Fund to continue its operations. The Bank will perform a closing assessment six months before the Closing Date, and if pre-determined benchmarks (see below) are met the remaining resources could stay within the Fund. This differs from the previous RSF, where at the end of the project, the IFC funds were withdrawn and the whole guarantee program came to a halt. To have a lasting impact on the development of MSMEs and by ricochet on growth, it is important that the program continue after the closing date of the project.

The institutional framework

17. The Fund will be established as an independent legal entity owned by the GoM. It will be managed by SOLIDIS, a Malagasy guarantee firm licensed by the Central Bank and supervised by the banking commission (CSBF). The fact that both the Fund and its manager are Malagasy will contribute to the ownership and the perpetuation of the program, contrary to the previous experience where IFC was the guarantee provider and its manager. The GoM will give all oversight powers and responsibility to a Board of Directors3 composed of a representative each from the Government, the bankers Association, as well as two members appointed intuitu personae for their technical knowledge of banking and guarantees. The GoM will appoint the Board of Directors on the basis of proposals made by the concerned parties. Board members will not receive any salary, but only a fee for their participation to the Board meetings. The Board will provide general oversight of the operations of the Board and particularly of the Fund manager. 18. SOLIDIS will be the exclusive manager of the Fund and its fiduciary agent, at the start of the project and for as long as its performance is satisfactory. The operations of the Fund and the role and obligations of Fund manager will be guided by Management Agreement of the Fund and the Procedures Manual. There will be a Management Agreement between the Fund and the Fund manager, and Guarantee Agreements between the Fund, represented by its Manager and the

3 The Fund manager will report to the Board and participate to the Board meetings but will not have voting power.

5

PFIs.4 The Fund does not have any staff. The Fund manager staff will monitor all operations of the Fund (registration of credits, analysis of claims, follow-up on recovery by PFIs). It will ensure that at any moment there is sufficient liquidity to pay claims within the prescribed period for honoring of claims. It will manage the investment of the Fund. The Fund manager will apply the upmost prudence and diligence in the management of the Fund’s investments and will receive dedicated technical assistance financed by the Project. The Procedures Manual will provide a list of eligible investment instruments.

19. Fees and investment proceeds are paid to the Fund. In turn, the Fund pays the Fund manager a management fee that has been agreed between the Fund manager and the Fund. At first with few guarantees, the Fund will register losses as the management fees will be larger than the guarantee fees, but with an increase in the volume of guarantees, the situation will be reversed.5

20. The PFI will undertake to place a certain volume of credits annually on the PPCG and to keep its non-performing portfolio at a maximum of 3 percent. If this limit is exceeded, the PFI will have a choice to pay a higher fee or be excluded from the PPCG. Similarly, if the PFI does not meet its commitment volume, it will be excluded from the PPCG.

21. An important element making the guarantee interesting is the rapidity of claim settlement. Once a credit has been deemed non performing, after being in arrears for 90 days, a claim will be submitted by the PFI to the Fund. If deemed receivable, the claim will be paid within 30 days. The PFI will be responsible for the recovery of the loan and the proceeds will be distributed pari-passu between the fund and the PFI. 22. On the basis of a screening done by the consultant report and the team’s technical appraisal, it was decided that at the beginning one PFI will benefit from the guarantee, Bank of Africa Madagascar (BOA). BOA, a private bank belonging to an important cross border group, has the largest branch network in the country and is looking at downscaling. It has expressed strong interest in the PPCG. A call for expression of interest for other banks meeting the same criteria as for BOA (prudential norms, good standing with the authorities and licensed by them, coverage of the country, activities in the MSME sector, strong expressed interest in the guarantee instrument) will be launched right after the Fund has started operations.

23. On the basis of the study on a RSF conducted by consultants in the context of the restructuring of the project, it can be estimated that the MSME credit portfolio of BOA could rise at an annual rate of 20 percent between 2012 and 2016. A similar percentage increase is expected from other banks that would join the PPCG after the call for expression of interest. Discussions with MSME confirm the existence of an unsatisfied demand for credit. Demand could be larger or smaller depending on the political and economic development of the country. As banks are over-liquid, availability of funds is not an issue for additional lending.

4 Notes on the content of these documents can be found in the project file. 5 If SOLIDIS ceases to be the Fund manager for a reason or another, the Board of Directors will hire a new manager in a transparent manner calling upon a respected international firm to conduct the hiring process.

6

24. At mid-term review to be held at the end of 2014, if the volume of guarantees extended is well below expectations,6 or the benchmarks with respect to the kind of credits (diversification of term and sector) are not met, the advisability of continuing the guarantee program will be assessed and funds could be reallocated to other activities of the project.

Disbursement arrangements for the PPCG 25. A balance of the funds provided by ACGF will be used as seed money to capitalize the Fund. The resources will be given to AGEPASEF which will transfer them into a bank account opened in the name of the Fund, but with the Fund manager’s signature. Under operational policy 6.00 the World Bank may finance from loan proceeds expenditures that are productive. The seed money for the PPCG will allow the fund to issue a portfolio guarantee. The guarantee fund to be credible and inspire confidence to the PFIs needs some capital reserves to demonstrate ability to pay-out potential claims. Given the multiplier of two and the 50 percent guarantee, the fund needs to hold funds equal to one quarter of the amount of credit guaranteed. Against this backdrop, up-front disbursement of ACGF resources is critical to get the guarantee operations started. The guarantee will increase MSMEs access to finance and allow them to expand their operations. In turn this will contribute to growth in Madagascar. The grant to the Fund is not expected to have any impact on the Borrower’s fiscal sustainability. This is the only payment the Borrower will make to the Fund. There will be no further subsidies from the GoM to the Fund. The original grant is fully funded by a grant from ACGF. In addition as discussed above and in Annex 3, the oversight arrangements are deemed satisfactory. Therefore, the provision of seed money to the Fund constitutes a clear productive purpose and hence meets the requirements of Operational Policy 6.00.

Figure 1: Set-up of the partial portfolio credit guarantee

6 This would be the case, for instance, if only the advance of 1 million dollars has been disbursed and other payments have not been called.

Fund (managed by

SOLIDIS)

PARTICIPATING FINANCIAL

INSTITUTIONS (PFIs)

that meet eligibility criteria MSMEs

Loans Grant Guarantees ACGF - TF

US$4 million

PIE

Grant

TA to SOLIDIS TA to PFIs

7

26. While the agreement between the Government and the Bank calls for total seed money of US$4 million for the guarantee Fund, the disbursement will be made in stages. A first advance of US$1 million will be made. The million dollars could support guaranteed credit of US$4 million (it covers 50 percent of the credit risk and uses a multiplier of two). Before the complete amount of guaranteed credit supported by the first installment is registered7 in the PPCG guaranteed portfolio, the Fund manager will call for the disbursement of the second tranche of US$1 million. The lead time will ensure that the guarantee process will not be interrupted while waiting for the disbursement of the second tranche. The application for the disbursement will be accompanied by the list of credits constituting the portfolio guaranteed for each PFI, realized with the US$1 million. De facto ACGF is disbursing against the purchase of financial services (i.e. guarantees). This process will be repeated until the full US$4 million has been disbursed.

27. The disbursement of the first one million dollars will not take place until the procedure manual and management agreements mentioned above are finalized and signed, and the Board of Directors has been appointed. These have to be completed six months from project effectiveness.

Arrangements to maintain the Fund in operation after closing of the Project

28. Six months before the Closing Date, a special implementation support mission shall review and assess the operations of the Fund and verify, on the basis of the most recent audit and of its direct review, that the Fund is managed in line with international best practices and that the resources put by ACGF in the guarantee fund were used for the intended purposes (i.e. that MSMEs in various sectors obtained short, medium and long term credit). On the basis of this Closing Assessment, the US$4 million may remain with the Fund and the guarantee mechanism will continue after the closing of the project. 29. In making the Closing Assessment, the following factors will be considered: (i) the governance arrangements for the Fund are satisfactory to the Association; (ii) the financial management system of the Fund is satisfactory to the Association; (iii) the Fund is operating in accordance with the applicable legal provisions and the Financing Agreement; (iv) the Fund in the opinion of the Association, has sufficient resources for the continued operation of the guarantee scheme; (v) the Fund’s audit reports are unqualified; and (vi) any other factors considered relevant by the Association. The goal will be to ensure that the Fund is complying with international best practices for credit guarantees and that it has robust fiduciary management and governance systems that make it sustainable in the long run. As part of the Closing Assessment, the Bank will require the Fund and its manager to prepare (not later than six months before the end of the project) a plan (“the Plan”) designed to ensure the continued achievement of the Fund’s objectives, and its continued operation. The Fund will, after closing date, continue to make annual audited financial statements publically available within one month of receipt of such reports from the auditors. Bank staff will have the right to conduct on-sight supervision as it sees fit, after the closing of the project. 30. If the Closing Assessment (or the Plan) is, in the opinion of the Bank, unsatisfactory, the Fund shall repay into the Grant Account for cancellation an amount equal to the proceeds of the Grant provided by the Bank to the Fund. The repayment may be staggered overtime to avoid

7 For instance as soon as US$3 million have been registered.

8

disruptions to outstanding guarantees. After Project closing and until the Grant is paid in full, the Fund would maintain a strong and effective governance structure, and the strong oversight arrangements discussed in the above paragraph, such as the periodic publication of audited financial statements. (ii) Audits of the Fund, the Fund manager and PFIs

31. Semi-annual external audits of the Fund, the Fund manager and the PFIs will be conducted by a reputable international auditor to ensure that the PPCG is well managed, that the resources disbursed by ACGF are used to support guarantees for credits falling within the qualifications criteria, that all such credits extended by the PFI are registered under the guarantee and that the PFIs do their best efforts in recovering the bad credits.

(iii) Technical advisory services to assist the Fund manager and the PFIs

32. Technical assistance to SOLIDIS, the Fund manager, will be provided on: (a) the management of a portfolio guarantee fund; (b) the conduct of due diligence of PFIs; (c) the assessment of fees to be charged to the banks benefitting from the guarantee; and (d) the drafting of legal documents. A resident technical adviser will be provided to SOLIDIS for two years, with the possibility of an extension. The involvement of SOLIDIS in the guarantee scheme will contribute to the institutionalization and perpetuation of the guarantee. Indeed, it would be expected that at the end of the project, SOLIDIS will continue to manage the PPCG having benefitted from a transfer of knowledge and capacity building. 33. Mandatory resident technical assistance to the PFIs will contribute to: (a) the establishment of a special MSME department;8 (b) the marketing of the new products for MSMEs; (c) the analysis and monitoring loans to MSMEs; and (d) the management of the PPCG in interaction with the Fund manager. Experience has shown that this kind of technical assistance is essential to increase the institutions’ capacity to lend to MSMEs. A PCG is an added incentive and a catalyst for such lending.

OP 8.30

34. The team has conducted a technical appraisal of the guarantee, SOLIDIS and BOA and concluded that the guarantee and SOLIDIS, subject to project technical assistance, meet the technical requirements of OP 8.30 Compliance Review.9 (iv) Provision of legal assistance for the establishment of the PCG Fund and the PPCG 35. The project will finance a legal consultant to assist with the drafting of legal documents

8 The beneficiary financial institutions will make a commitment to set up a special MSME department/unit and allocate dedicated staff members to MSME lending. 9 Annex 3 presenting the OP 8.30 Compliance Review has been cleared by FFIMS.

9

(v) Study on interest rates charged by banks and MFIs to MSMEs

36. The Project will finance the conduct of a study to outline the factors contributing to the level of interest rates charged on credit by MFIs and banks to MSMEs. The high level of interest rates is an important factor contributing to the low level of MSME lending – and thereby potentially constraining the pool of SME loans benefitting from the PPCG. A study was conducted in 2008 by the microfinance institutions association (APIMF) supported by several donors. It needs to be updated and extended to commercial banks. The new study should shed light on the interest rates determination process within MFIs and commercial banks and on the actions that can be taken to impact on the factors behind the rate of interest so as to lower the cost of credit. This is a much needed complement to the PPCG.

Component 2: Improving the capacity of MFIs for greater outreach and sustainability

37. As its implementation completion report (ICR of September 2011) confirms, the Microfinance project (P052186) has demonstrated a substantial increase in access to financial services for the low-income population. However, there is a need for continued support to the microfinance sector in Madagascar because the gains attained so far remain fragile and, in the absence of a continued donors’ support, the sector’s performance could deteriorate. On the other hand, there is excellent potential for the sector to consolidate its recent strides and achieve even greater results. That requires the World Bank’s (and other donors’) continued engagement which is what this component is setting out to do. Hence, all of the microfinance activities in the original project will be maintained but scaled up and better focused. They form the new Component 2 of the project. Changes will consist of: (i) Strengthening supervision of MFIs by the regulatory authority (CSBF). Currently,

many MFIs are operating without a license; on-site inspections present many weaknesses; poor databases impact negatively on the quality of supervision; mobile banking operations lack a good regulatory framework. The Project will contribute to strengthen the supervision of micro finance institutions by financing the following interventions: a. Identification of MFIs operating without a license: a survey will be conducted by

CSBF with the assistance of district authorities. This survey will enable to map all the MFIs operating in the country and identify those operating without a license. If needed, CSBF could use the services of a private firm, with project financing, to complete the work done with internal resources. MFIs operating without a license will be invited to submit a licensing request within six months. CSBF agreed that MFIs that have not conformed to this request or whose application has been denied should be closed. More generally, new MFIs should not be allowed to start operations before having received a license.

b. Facilitating the MFIs licensing process: the Project will finance the establishment of information centers within the territorial representations of the Central Bank. These centers will provide all the necessary forms to apply for a license and will inform on the procedure. The project may fund minor works to refurbish premises, purchase of equipment and printing of forms and other materials.

10

c. Strengthening of MFIs on-site inspections by CSBF: the Project will facilitate the involvement of the ten territorial representations of the Central Bank in on-site MFIs inspections by funding the related mission costs. In parallel, new inspectors will be hired by CSBF. This will contribute to increase the frequency and the quality of inspections.

d. Technical assistance for a new regulatory text on mobile banking and agent

banking: the Project will fund a consultant to assist CSBF with the drafting of the new regulation on mobile and agent banking that will be introduced through a circular issued by the Central Bank.10 To this date, a clause in the banking law on the intermediaries in banking operation has been used to govern “mobile banking”. Such an approach has a limited scope and does not provide the needed flexibility. Thus, a specific regulatory framework established by a circular will protect the users without stifling the development of mobile and agent banking.

e. Improving the efficiency of the Centrale des Risques (CRM): the Project will

provide technical support to the CRM by improving links between the MFIs and the CRM and by building a “bridge” between the CRM for banks and that for MFIs.11

f. Establishing a comprehensive database for supervision: the Project will finance

the set up (i.e. hardware and software) of a centralized database in CSBF allowing combining in a single database all the information on banks and MFIs through easy computerized treatment of data. In particular, there is a need to establish an informational link between on and off site supervisions.

g. Training of CSBF staff in banking and MFI supervision: the Project will provide

technical assistance for providing training and building the capacity of CSBF staff in banking and MFI supervision. Trainings will help CSBF staff to adopt risk-based supervision approaches and will allow staff to be abreast of latest developments. Such training is key to maintain a high quality supervision of banks and MFIs.

(ii) Reinforcing the MFIs. Assistance to MFIs will focus on: (a) strengthening the capacity of MFIs through training to be provided through their professional association, APIMF; (b) modernizing their MIS systems accompanied by the establishment of a communications system between the individual units, the regional centers and the central union; and (c) providing support to MFIs to operate in target areas. The three sub-components are independent and any MFI can benefit from one, two or all of them. MIS modernization and incentives to operate in target areas are new interventions compared to the original project.

10 The circular is applicable without any other institution or Government’s decision. 11 Support for the establishment of credit information bureau – with the purpose of positive information sharing – will be considered in due course, possibly by using alternative sources of funding (e.g. FIRST-funded projects).

11

(a) Training to MFIs: the Project will finance dedicated training courses to be provided through APIMF12 on a range of relevant topics for supporting the operations of MFIs across the country. This is an essential element for strengthening MFIs’ capacity, outreach and sustainability.

(b) Modernizing MIS and communication systems for MFIs: the Project will finance

the establishment of automated MIS, to be possibly accompanied by an efficient, rapid and secure communications system between the individual units, the regional units and the central union of each MFI. Modernizing MIS would require covering consultant fees (for the computerization plan, the development of bidding documents, and procedure manuals), purchase of hardware and acquisition of software (including installation, establishing the parameters of the system, and follow-up technical assistance) and training of relevant staff in the use of the new MIS. Supporting communication systems would require to cover consultant fees (for an initial needs assessment) and the cost of a contract with a supplier (which may include equipment - routers, solar panels and a service contract as well as training of staff). In both cases, it will be advantageous to regroup the needs of several MFIs to possibly benefit from economies of scale from the suppliers as well as better service following the installation. MIS would use the same “trunk” software with some adaptations tailored to specific needs.

Recipients of project assistance for MIS and communications systems will be chosen on the basis of a call for expression of interest. However, assistance will be restricted to MFIs that have positive net worth, meet CSBF prudential requirements and have good prospects for achieving long term sustainability. Priority may be given to MFIs which operate or intend to operate in target regions13. To ensure the internal capacity to absorb the assistance, modernization of MIS and communications systems must be part of the MFIs business plan with an implementation calendar corresponding to their capacities. The project implementation entity (PIE) will confirm with MFI management the capacity to absorb the reforms. More MFIs could be reached if other donors would agree to accompany the Bank. Discussions with donors support the sector have been initiated. In many cases, modernization of the MIS will accompany an internal reorganization to improve efficiency. The MFI will have to present and agree to an organizational plan. Procedures manuals will be written. This reorganization and computerization will improve the gamut and quality of services offered and thus will increase the number of clients (individuals, MSMEs, rural enterprises, etc.).

(c) Support to MFIs to extend their activities. The Project will provide funding, in the

form of a grant, to support, on a cost-sharing basis, the opening of new MFI

12 This was already part of the original project. 13 Target regions may be defined as those where there are few MFIs or as those where other World Bank projects such as the Integrated Growth Poles Project intervene.

12

branch and sub-branch offices in areas where there are few institutions or in areas of intervention of other Bank projects (the Anosy Region is an example). Such grants are only for licensed MFIs and may be used to cover minor works, equipment, staff training and even salaries during the initial period of functioning. This one-time support is needed to attract, in the nearest future, qualified MFIs to target regions. It is expected that the overall-socio economic benefits of extending activities of MFIs in these areas far exceed the cost of the grant, which should be seen as a transparent, non-discriminatory and capped one-time incentive. The Project Implementation Entity (PIE) will have the responsibility of monitoring the actual use of the grant support for the establishment of new branches.

Safeguards 38. The proposed project will not finance a specific set of pre-identified investments. A guarantee will apply to a portfolio of loans extended by PFIs to MSME; the onlent funds will be mobilized by the PFIs themselves. No specific sector has been identified and PFIs will lend at market conditions. Partial coverage of the credit risks on loans to MSMEs, could possibly pose environment, health and safety issues and hence OP 4.01 (Environmental Assessment) has been triggered. 39. The project has been re-classified as Category FI and the World Bank Operational Policy on Environmental Assessment (OP 4.01) is triggered. As sub-projects/activities to be financed under the credit of local banks for partial guarantee have not yet been identified during the project preparation, an Environmental and Social Management Framework (ESMF) has been prepared for the Project. The ESMF will set forth the principles and guidelines to be followed by the borrowers to comply with the requirements of the triggered policy. It includes a mechanism to review and conduct an environmental screening to avoid and mitigate the environmental and social impacts risks of potential subprojects eligible for financing by the participating financial institutions that have access to the partial guarantee. 40. Two stages of environmental screening process have been adopted by the project to avoid and minimize environmental and social issues.

The first level of screening will be addressed through an Exclusion List of Activities (ELA). This is a list of sub-projects/activities that are ineligible for access by the local banks to the project’s partial guarantee The key steps and due diligence to identify ELA and ineligible activities include the following: (i) a detailed review of range of activities classified as Category A, according to World Bank OP 4.01; (ii) all activities/subprojects that could trigger World Bank OP 4.12 on Involuntary Resettlement and OP 4.04 on Natural Habitats; and (iii) activities that are prohibited for World Bank Group lending, including IFC’s exclusion list.

In the second level of screening are the activities or subprojects presented by PFIs that could be eligible for access to the project’s partial guarantee of the project fund. The key steps and due diligence to identify eligible activities included the following: (i) activities classified as Category B, according to World Bank OP 4.01, where the proposed subproject/activity presented by the PFIs to be registered under the PPCG has received

13

an environmental license delivered by the Malagasy Environmental Authority (National Office of Environment) and implemented in a manner satisfactory to the Environmental and Social Management Plan (ESMP) that would be prepared for each subproject, and monitored by the Malagasy Environmental Authority; (ii) activities classified as Category C according to World Bank OP 4.01(i.e. negligible or no environmental and social impacts).

41. The World Bank will assist and train the Project Coordination Unit and SOLIDIS, a Malagasy guarantee firm licensed by the Central Bank of Madagascar, to build up their capacity on the management of environmental and social risks described in the ESM. The ESMF includes the screening of activities concerned by the request of partial guarantee and their classification into ineligible or eligible activities. For the PFIs, completion of this training will be a pre-condition to launch the activities on the provision of guarantee fund. Institutional arrangements

42. Project implementation will remain under the leadership of the Ministry of Finance and Budget (MFB). The MFB will pass the funds of the financing onto the PIE for the implementation of the Project. The PIE staff, headed by a project coordinator, will be responsible for the day-to-day project management of the overall project. The PIE will be responsible for the implementation of all the project components and assume fiduciary responsibilities for the project. The Steering Committee (SC), the administrative body of the PIE, will remain responsible for overall project oversight. Its roles are the same as described in the PAD but its composition will be limited to four members to assure effectiveness and efficiency. Strategic guidance will be the responsibility of the PIE’s General Assembly. The Project Operational Manual will incorporate these changes. Financing

Table 1: Project Costs

Components / Activities Costs (US$ million)

Current Proposed Current Proposed

Component 1 Improving Financial Sector Infrastructure and Environment

2.00

Sub-component 1.1 Enabling financial sector infrastructure

1.00

1.1. Improving the legal and regulatory environment

0.70

1.2. Establishing a financial sector infrastructure

0.30

Sub-component 1.2 Strengthening supervision of the financial sector

1.00

Component 2 Improving the diversity of financial institutions and products

10.30

2.1. Increasing access to SME finance

Component 1 Increasing MSME access to finance

5.50 5.80

2.2. Increasing access to microfinance

Component 2 Improving the capacity of MFIs for greater outreach and sustainability

3.50 6.30

14

Components / Activities Costs (US$ million)

Current Proposed Current Proposed

2.3. Developing financial products and instruments

2.1. Strengthening supervision of MFIs (CSBF)

1.30 0.70

2.2. Reinforcing the MFIs 5.60 Component 3 Project Implementation and Monitoring and Evaluation

Component 3 Project implementation and M&E

1.50 2.70

3.1. Coordination and implementation

3.1. Coordination and Implementation 0.96 2.4014

3.2. Monitoring and evaluation 3.2. Monitoring and evaluation 0.54 0.30

Unallocated Unallocated 1,20 0.20 Total Project Costs 15.00 15.00

Disbursement arrangements 43. For the implementation of the project, there will be one designated account for the PIE: Denominated in United States Dollars (US$), disbursements from the ACGF grant will be deposited on this account in a commercial bank to finance all the project activities. Designated account A for the Central Bank will be closed. Reallocations

Table 2: Reallocations

14 Of which US$0.6 million disbursed.

Category of Expenditure Allocation (in US$ 000s)

% of Financing

Current Revised Current Revised Current Revised (1) Goods, consultant’ services, and training under subcomponent 1 (b) of the project

1,000,000 0 100%

(2) Goods, consultant’ services, and training under the project other than Part 1(b)

5,650,000 20,000 100% 100%

(3) Goods and services under Matching grants

(3) Goods and services for matching grants under Part 2(iii) of the project

3,850,000 1,200,000 100% 100%

(4) Operating cost (4) Operating cost 800,000 1,650,000 100% 100% (5) Risk sharing facility 2,500,000 0 100% (6) Unallocated 1,200,000 180,000 100% 100% (7) Initial

contribution to the PPCG Fund

0 4,000,000 100%

(8)Minor works, goods, consultant services under the project other than Parts 1(i) and 2(ii)

0 7,950,000 100%

Total amount 15,000,000 15,000,000 100% 100%

15

Closing date 44. The proposed extension is necessary to allow for completion of activities under the project. The lifespan of the original project was four and half years. All the project activities have been put on hold partially due to the political crisis which halted disbursement in the context of OP/BP 7.30, but also because of persistent weaknesses observed at the PIE until November 2011. The project will be re-launched in earnest once the restructuring has been approved. Thus a four year extension appears reasonable to allow for a reasonable time to complete all activities. This will be the first extension of the project. Implementation schedule

45. The revised proposed implementation plan is elaborated in Annex 2.

16

Annex 1: Results Framework and Monitoring

ACGF – Madagascar Financial Services Project

Project Development Objective: To increase access to sustainable financial services, particularly to micro, small and medium enterprises (MSMEs) and households in Madagascar. This will be achieved through improving competition and diversification in the sector by providing technical assistance, capacity building, and matching grants to financial actors and stakeholders. Revised Project Development Objective: To increase access to sustainable financial services, particularly by micro, small and medium enterprises (MSMEs) and households in Madagascar.

PDO Level Results Indicators C

ore

D=Dropped C=Continue N=New R=Revised

Unit of Measure

Baseline15

Cumulative Target Values

Frequency

Data Source/ Methodology

Responsibility for Data Collection

2013

2014

2015

2016

Indicator One: Credit extended to MSMEs by participating financial institutions

D

Indicator Two: Number of accounts at licensed financial institutions (banks or microfinance institutions) (of which held by women)

D

Indicator One: Outstanding loans -MSMEs

N

MGA million

3,000,000

3,600,000

4,800,000

6,000,000

7,500,000

Quarterly

Central Bank/ Banks/Survey

PIE

Indicator Two: Outstanding loans– MFIs

N MGA million

250,000

280,000

300,000

350,000

400,000

Quarterly

Central Bank/ Banks/Survey

PIE

Indicator Three: Percentage of outstanding loans to women - MFIs

N %

NA

48%

49%

50%

52%

Annual

MFIs/Survey

PIE

15 Baseline data refers to progress to date (2012) and to be verified and confirmed during the first six months of project implementation.

17

INTERMEDIATE RESULTS

Intermediate Indicators

Cor

e

D=Dropped C=Continue N=New R=Revised

Unit of Measure

Baseline

Cumulative Target Values Frequency

Data Source/ Methodology

Responsibility for Data Collection

2013

2014

2015

2016

Intermediate Result (Component One): Legislation and regulatory framework for implementation of secured transactions law, housing finance as well as pensions and insurance formulated and adopted

Revised Intermediate Result (Component One): MSMEs access to commercial banks credits improved

Intermediate Result indicator One: Appropriate legal and regulatory framework for implementation of the law on secured transactions (loi sur les voies d’exécution) adopted by end 2010

D

Intermediate Result indicator Two: Appropriate legal framework (including amended civil procedures for foreclosures) for housing finance adopted by end of project

D

Intermediate Result indicator Three: Legislation on private pensions harmonized and adopted by end of project

D

Intermediate Result indicator Four: Updated legal and regulatory framework for insurance adopted by end of project

D

Intermediate Result indicator One: Outstanding loans to MSMEs by participating financial institutions

N

MGA million

0

To be est.

To be est.

To be est.

To be est.

Quarterly

PFIs/PIE reports

PIE

Intermediate Result indicator Two: Portfolio at Risk - MSME - of participating financial institutions

N

%

NA

To be est.

To be est.

To be est.

To be est.

Quarterly

PFIs/PIE reports

PIE

18

INTERMEDIATE RESULTS

Intermediate Indicators

Cor

e

D=Dropped C=Continue N=New R=Revised

Unit of Measure

Baseline

Cumulative Target Values Frequency

Data Source/ Methodology

Responsibility for Data Collection

2013

2014

2015

2016

Intermediate Result (Component One): The Central Bank credit information system established and operational; and legal obstacles to the establishment of a private credit bureau/registry removed

Revised Intermediate Result (Component One): Increased technical capacity of partner institutions in MSME lending

Intermediate Result indicator One: Increase in depth of credit information index by end of project

D

Intermediate Result indicator One: Dedicated MSME lending departments established in each of the participating financial institutions

N

Yes/No

No

No

Yes

Yes

Yes

Annual

PFIs/PIE Report/Audit of MFI report

PIE

Intermediate Result indicator Two: Number of loans introduced in the PPCG fund by partner financial institutions

N

Number

0

To be est.

To be est.

To be est.

To be est.

Quarterly

PFIs/PIE Report/Audit of MFI report

PIE

Intermediate Result indicator Three: PFI meet main prudential norms and regularly provide audited financial statements

N

Yes

Yes

Yes

Yes

Yes

Yes

Quarterly

BCM reports

PIE

Intermediate Result indicator Four: Internal audit , risk management of the Fund Manager improved

N

Yes

Unsatisfactory

Yes

Yes

Yes

Yes

Semestrial

Audit of Fund

PIE

Intermediate Result indicator Five: Fund Manager profitable

N

Yes

No

No

Yes

Yes

Yes Semestrial

Audit of Fund

PIE

Intermediate Result indicator Six: Claims on guaranteed portfolio less than 3%

Yes

Does not apply

NA

Yes

Yes

Yes

Semestrial

Audit of Fund

PIE

19

INTERMEDIATE RESULTS

Intermediate Indicators

Cor

e

D=Dropped C=Continue N=New R=Revised

Unit of Measure

Baseline

Cumulative Target Values Frequency

Data Source/ Methodology

Responsibility for Data Collection

2013

2014

2015

2016

Intermediate Result (Component One): The capacity of the Central Bank/Banking Commission (CSBF) or other designated supervisory authority to monitor, regulate and supervise the financial sector is strengthened

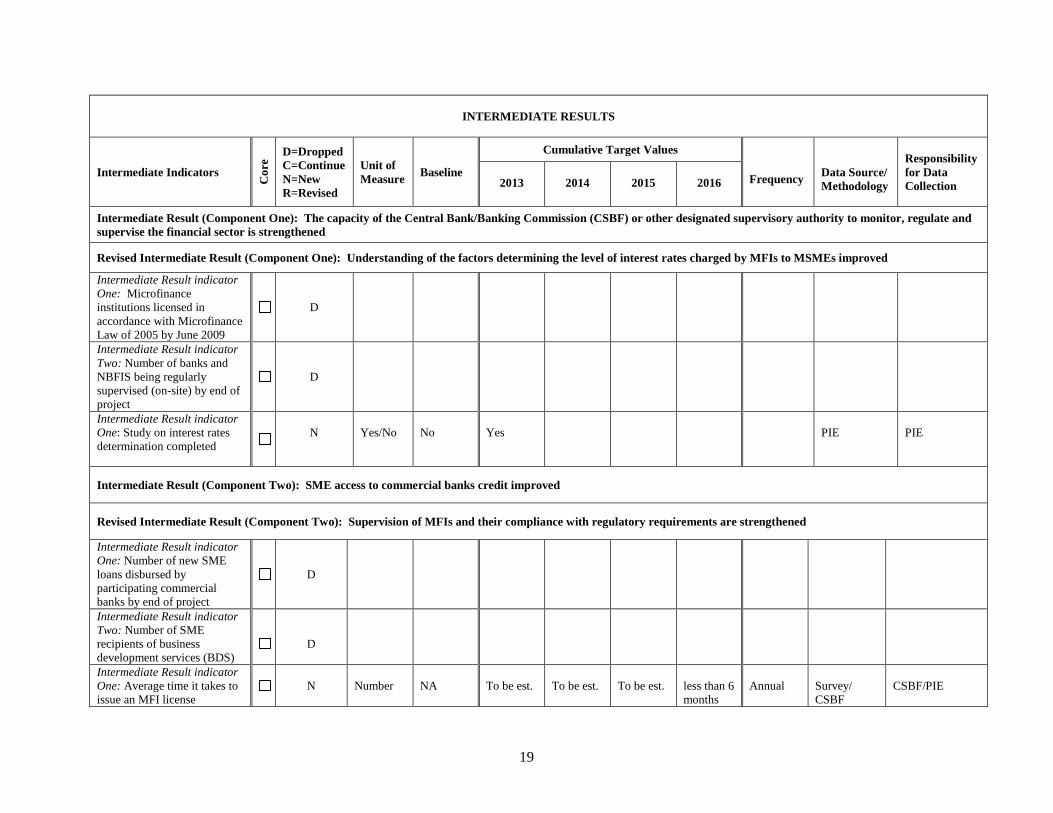

Revised Intermediate Result (Component One): Understanding of the factors determining the level of interest rates charged by MFIs to MSMEs improved

Intermediate Result indicator One: Microfinance institutions licensed in accordance with Microfinance Law of 2005 by June 2009

D

Intermediate Result indicator Two: Number of banks and NBFIS being regularly supervised (on-site) by end of project

D

Intermediate Result indicator One: Study on interest rates determination completed

N

Yes/No

No

Yes

PIE

PIE

Intermediate Result (Component Two): SME access to commercial banks credit improved

Revised Intermediate Result (Component Two): Supervision of MFIs and their compliance with regulatory requirements are strengthened

Intermediate Result indicator One: Number of new SME loans disbursed by participating commercial banks by end of project

D

Intermediate Result indicator Two: Number of SME recipients of business development services (BDS)

D

Intermediate Result indicator One: Average time it takes to issue an MFI license

N Number

NA

To be est.

To be est.

To be est.

less than 6 months

Annual

Survey/ CSBF

CSBF/PIE

20

INTERMEDIATE RESULTS

Intermediate Indicators

Cor

e

D=Dropped C=Continue N=New R=Revised

Unit of Measure

Baseline

Cumulative Target Values Frequency

Data Source/ Methodology

Responsibility for Data Collection

2013

2014

2015

2016

Intermediate Result indicator Two: Number of enquiries issued through single application window in regional branches of CSBF

N

Number To be est. To be est. To be est. To be est. To be est.

Annual

CSBF

CSBF/PIE

Intermediate Result indicator Three: Number of MFIs inspected (on-site) by CSBF at minimum every two years per MFI

N

Number

6

16

16

18

18

Annual

CSBF

CSBF/ PIE

Intermediate Result indicator Four: Number of enquiries from MFIs to Centrale des Risques increases

N

Number

7

13

23

33

33

Annual

CSBF

CSBF/ PIE

Intermediate Result indicator Five: A mobile banking framework is issued

N

Yes/No

No

No

Yes

CSBF

PIE

Intermediate Result (Component Two): Capacity of MFIs and their Apex organization

Revised Intermediate Result (Component Two): Capacity of MFIs to provide access to financial services is increased

Intermediate Result indicator One: Number of MFIs in compliance with licensing requirements

D

Intermediate Result indicator Two: Number of financially self- sufficient MFIs by end of project

D

Intermediate Result indicator Three: Number of microfinance clients by gender by end of project

D

21

INTERMEDIATE RESULTS

Intermediate Indicators

Cor

e

D=Dropped C=Continue N=New R=Revised

Unit of Measure

Baseline

Cumulative Target Values Frequency

Data Source/ Methodology

Responsibility for Data Collection

2013

2014

2015

2016

Intermediate Result indicator One: Outstanding loans to MSMEs by participating financial institutions

N

MGA million

To be est. To be est. To be est. To be est. To be est.

Quarterly

MFI reports/ CNMF

PIE

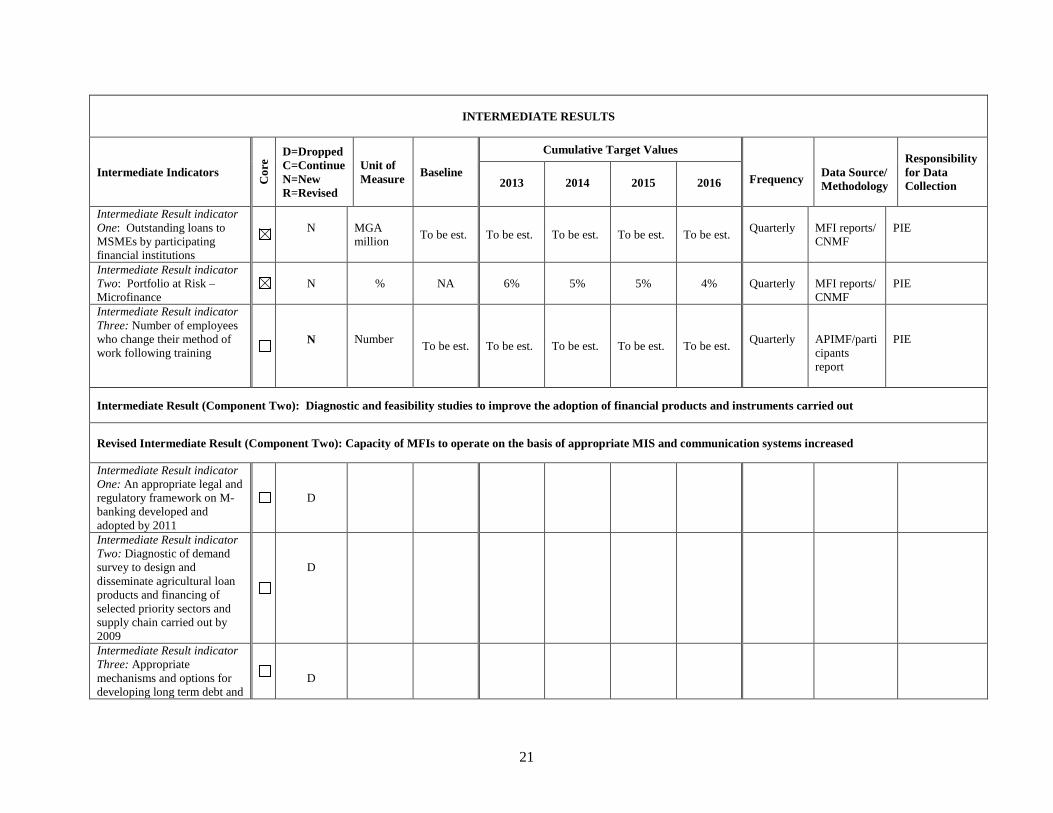

Intermediate Result indicator Two: Portfolio at Risk – Microfinance

N

%

NA

6%

5%

5%

4%

Quarterly

MFI reports/ CNMF

PIE

Intermediate Result indicator Three: Number of employees who change their method of work following training

N

Number

To be est. To be est. To be est. To be est. To be est.

Quarterly

APIMF/participants report

PIE

Intermediate Result (Component Two): Diagnostic and feasibility studies to improve the adoption of financial products and instruments carried out

Revised Intermediate Result (Component Two): Capacity of MFIs to operate on the basis of appropriate MIS and communication systems increased

Intermediate Result indicator One: An appropriate legal and regulatory framework on M-banking developed and adopted by 2011

D

Intermediate Result indicator Two: Diagnostic of demand survey to design and disseminate agricultural loan products and financing of selected priority sectors and supply chain carried out by 2009

D

Intermediate Result indicator Three: Appropriate mechanisms and options for developing long term debt and

D

22

INTERMEDIATE RESULTS

Intermediate Indicators

Cor

e

D=Dropped C=Continue N=New R=Revised

Unit of Measure

Baseline

Cumulative Target Values Frequency

Data Source/ Methodology

Responsibility for Data Collection

2013

2014

2015

2016

equity market have been identified Intermediate Result indicator Four: FinScope or similar demand survey on access to financial services is carried out

D

Intermediate Result indicator One: Number of MFIs supported by the project using an automated MIS

N

Number

To be est.

To be est.

To be est.

To be est.

To be est.

Annual

MFI reports/ CNMF

PIE

Intermediate Result (Component Two): None

Revised Intermediate Result (Component Two): MFIs extended their activities in target areas (i.e. areas where there are few MFIs compared to the national average per region or areas of intervention of other World Bank projects)

Intermediate Result indicator One: Outstanding loans by participating MFIs in target areas

N

Number

To be est.

To be est.

To be est.

To be est.

To be est.

Quarterly

MFI reports/ CNMF

PIE

23

Annex 2: Implementation Schedule16

Madagascar: ACGF – Madagascar Financial Services Project COMPONENTS SUBCOMPONENTS MAIN ACTIVITIES

2013 2014 2015 2016 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

1.Increasing MSME access to finance

1.1. Provision of guarantee fund

Implementation of the program

1.2.TAand training to partner banks and guarantee fund manager

TA and training to PFIs TA and training to guarantee fund manager

1.3.Audits of partner banks and guarantee fund manager

Selection of auditors and conduct audits

1.4. Legal assistance for drafting contractual agreements

Support to PCU for establishing contractual agreements

1.5.Study on interest rates

Selection of consultant and conduct study on interest rates determination

2. Improving the capacity of micro-finance institutions for greater outreach and sustainability

2.1.Strengthening supervision of MFIs by CSBF

Support for participation of territorial representations in inspection missions

Survey of all MFIs across the country Establishment of information centers for licensing in territorial representations of the Central Bank

TA for drafting regulatory text on mobile banking

Support to Centrale des risques Training of CSBF staff Database of financial institutions

2.2.Reinforcing the MFIs

Training of MFIS through APIMF Modernizing MIS (TA for computerization plan, procurement, manual, purchase of software/ hardware, training of staff, implementation)

Support to MFIs to extend their activities

3.Project implementation and M&E

3.1.Coordination and implementation

PCU Operation costs (incl. external audits)

3.2.Monitoring and evaluation

Missions conducted by PIE TA for mid-term review and ICR

16 Calendar year.

24

Annex 3:17 OP 8.30 Compliance Review

Madagascar: ACGF – Financial Services Project 1. This annex summarizes the outcome of a review of a proposed grant, in the amount of US$4 million, to a guarantee fund, to be managed by SOLIDIS, in support of the provision of a partial portfolio credit guarantee (PPCG) to participating financial institutions (PFIs) to mitigate their credit risks on loans to micro, small and medium enterprises (MSMEs). This assessment is to evaluate the state of compliance of this activity with the requirements of OP 8.30. 2. The team has conducted a technical appraisal of the guarantee and SOLIDIS and concluded that the guarantee and SOLIDIS subject to project technical assistance meet the technical requirements of OP 8.30 Compliance Review and are qualified to implement the project. The Project 3. The grant is a subcomponent of the global project whose objective is to enhance MSME access to finance through the provision of partial credit guarantees to participating financial institutions to mitigate their credit risks on loans to MSMEs. The Bank is not financing sub-projects linked to the credits but is partially financing the credit risk of the PFI. OP 8.30 Considerations 4. Objective. The objective of the Project is to assist the Recipient in increasing access to sustainable financial services, particularly by micro, small and medium enterprises, and households in Madagascar. This objective is consistent with OP 8.30. 5. The PPCG scheme and SOLIDIS. A guarantee fund will be established and provided with seed money by ACGF. It will be managed from the outset by SOLIDIS and as long as its performance is satisfactory. The fund will be separated from the other activities of SOLIDIS. It will have its own Board of Directors. As the PFIs will assess all credits included in the PPCG, SOLIDIS’ management role will be mainly to monitor the registration of credits, receive and analyze the claims and authorize the payment of claims, monitor the loan recovery by participating banks and manage the investments of the fund. The procedure manual will list eligible investment instruments. 6. Established in 2008 as a limited liability corporation and operational since 2010, SOLIDIS is the strongest of two credit guarantee institutions licensed in Madagascar. The private shareholders invested MGA 250 million (equivalent to approximately US$125,000), while the French development agency (AfD) provided another MGA 750 million of quasi equity. Total capital therefore is equivalent to US$500,000.

17 This Annex has been cleared by FFMS.

25

7. SOLIDIS has obtained a license from the Central Bank of Madagascar and is supervised by it; it is in full compliance with all relevant regulation. The institution has eight employees (General Manager, three clientele agents, two credit analysts and two financial management specialists). Employees are dynamic relatively young people, well trained and recruited from local banks or MFIs. SOLIDIS currently provides advice to small businesses in preparing a financing request and elaborating financial statements and offers a 50 percent individual guarantee on credits granted by banks to these businesses. 8. The intention of this process is to make the customer bankable. Due to the experience and know-how of the SOLIDIS staff, the borrower is supposed to approach the bank or the micro-finance institution with all the required information. The prospective borrower is accompanied by SOLIDIS in establishing his or her contact with the bank. 9. On the weak side, SOLIDIS is a young institution with limited track record. While SOLIDIS was able to conclude guarantee agreements with a large number of financial institutions, none of them had a large number of files guaranteed by SOLIDIS. SOLIDIS has extended 34 guarantees with nine institutions (banks and MFIs) for a total amount of MGA 902 million (US$450 000) supporting total credits of MGA 1,805 million (or US$902,000). 10. SOLIDIS does not have much specific guarantee know-how yet. The French development agency (AfD) has been financing a TA grant under which a French consultant carried out a number of missions to establish certain policies and procedures. During the preparation missions, however, it became clear that the institution does not have strong risk management systems and capabilities. Portfolio reporting is made in a very narrow approach with Microsoft Excel. Technical assistance will be provided to strengthen SOLIDIS. 11. On the other hand, among its strengths the shareholders and management are very entrepreneurial, dynamic, and keen to improve the institution and eager to learn. SOLIDIS is very well capitalized. Being a new institution, it is still in loss making position, which can easily be absorbed by a large capital base. SOLIDIS management has provided the team with a plan to reach profitability within two years. It should be noted that the guarantee fund will not be financially impacted by the financial situation of SOLIDIS. As indicated earlier, the fund is separated from the other operations of SOLIDIS. 12. Technical assistance to SOLIDIS, used to implement the institutional development plan, will be provided on: (a) the management of a portfolio guarantee, including the management of claims; (b) the functioning of SOLIDIS, including procedures, risk management, internal controls; (c) the conduct of due diligence of participating banks; (d) the assessment of fees to be charged to the banks benefitting from the guarantee; (e) the drafting of legal documents, and (f) the training of staff. A resident technical assistant will be provided to SOLIDIS for two years, with the possibility of an extension. The involvement of SOLIDIS in the guarantee scheme will contribute to the institutionalization and perpetuation of the guarantee. Indeed, it is expected that at the end of the project, SOLIDIS will continue to manage the PPCG having benefitted from a transfer of knowledge and capacity building.

26

13. In addition, bi-annual audits funded by the project will be conducted by external independent firms of the participating banks and SOLIDIS to ensure that the Fund is well managed, that the banks follow the rules for registering all qualified loans on the guarantee, do their best efforts to recover and split the net recovery proceeds 50-50 with the Fund. After the closing of the project, the audits will be paid by the Fund out of the commissions received. 14. The team believes that with the technical assistance provided by the project, SOLIDIS meets the requirements of OP 8.30, particularly as its implication is only as manager of the fund. 15. Design of PPCG products. Building on discussions with SOLIDIS and the participating banks, the PPCG will guarantee loans between US$500 and US$400,000 (with ceiling on the number of large loans). The loan duration can be between six months and five years. Eligible loan purposes are fixed assets, working capital and property. The guarantee will cover all sectors of economic activity, with the exception of a negative list. However, there will be ceilings on the amount of short term credit and trade credit and minima for investment credits. The purpose is to provide incentives for financing production and transformation, as well as rural areas and for investments, which will have the largest impact on growth and poverty reduction. 16. Financial terms of the PPCG. The financial terms of the PPCG have been reviewed by the team and are considered to be adequate. The PPCG covers 50 percent of the loan on a pari passu basis. A variable annual commission in relation to risk (as measured by the ratio of non-performing credits to total credits in the PPCG portfolio) will be charged. At first the commission will be set up at 2 percent for a portfolio with a non performing rate less than 3 percent. The commissions and returns on the investment of the capital will cover operational expenses and expected losses. 17. Processing of claims. On the basis of discussions with the participating institutions and SOLIDIS, all justified claims will be paid within 30 days on a first demand basis. The full amount of the guarantee (50 percent of the credit) will be paid. The bank will do its best efforts to recover the losses. Recovery proceeds, net of recovery costs, will be divided 50-50 between the bank and the Fund. 18. Internal controls and Financial Management. SOLIDIS internal control and financial management framework needs to be reinforced. This strengthening will be one of the mandates of the resident technical assistant. 19. Risk management. The risk management framework will also be strengthened by the resident technical assistant. It is expected that the non-performing loans (NPLs) on the PPCG will be lower than those on the individual guarantees provided by SOLIDIS. Experience shows that up-front capitalization (disbursement of funds) of the project funds into a reserve account is the most effective way in which this program can function. As with any risk sharing program, the financial intermediary providing credit coverage serving as a guarantor must have sufficient market credibility in terms of its available reserves for participating banks to accept its loan guarantees. For commercial banks to accept the guarantees of the program, funds must be

27

unencumbered and transparently available to back the guarantees.18 SOLIDIS will deposit part of the Fund reserves in the participating banks. 20. Policy Framework. This section will successively cover (a) the macroeconomic environment; (b) the financial sector framework; (c) the on-lending rate; (d) the interest rate regime in the country; and (e) the existence of a subsidy.

(a) A stable macroeconomic environment is critical of success as distorted or disturbed macroeconomic environment could undermine the realization of project objectives. The socio political crisis has impacted negatively on economic performance in 2009. Real growth in 2011 was estimated at around 2 percent up from 0.5 percent in 2010 and -4.1 percent in 2009. The modest uptick in gross domestic product (GDP) growth in 2011 was mainly boosted by some rebound in tourism, export from export processing zones and agri-business. GDP growth occurred largely in the tertiary sector and secondary sectors, also supported by investment in mining projects, while the primary sector continued to perform poorly with a negative growth rate. On average, inflation was stable in the 2008-11 periods, hovering around 9 percent, but has since decelerated with the temporary freeze in petroleum products prices, and the easing of supply-related tensions on rice prices. CPI inflation slowed to 6 percent year-on-year through mid-2012. Money growth reached 20 percent in 2011, compared to 9 percent in 2010, mainly due to increase in net foreign assets and credit to the government, and to a lesser extent, to credit to the economy. It is now easing with a slower rate of reserve accumulation, tight fiscal financing and a deceleration of growth in credit to the economy, down to 3.5 percent, mainly on account of lingering uncertainty in the economy and low credit demand. The Central Bank rate remained at 9.5 percent in 2009 and 2010, slightly positive in real terms, ensuring positive real deposit and lending rates. Interest rates on bank credit remains high at about 15 percent and microfinance rates are much higher. It is expected that the PCG will contribute to lower rates. The overall budget deficit rose at MGA 324 billion in 2011 (about 1.7 percent of GDP), up from MGA 196 billion in 2010 (1.1 percent of GDP), financed mainly from domestic treasury issues and some modest resumption of donor programs. Revenues stood at MGA 2,646 billion and total spending remained broadly in line with budget plans, with limited spending on public investment. As the political transition lingers, with limited donor support and muted economic performance, fiscal outcomes for 2012 should remain broadly in line with 2011. As regards external development, the trade deficit narrowed to US$941 million in 2011, from US$1,074 million in 2010, reflecting the pick-up in export processing

1818 IFC-IDA. Task Force Report: Review on the Use of IDA funds for Risk Sharing Facilities and Partial Credit

28

zones, tourism resumption and an exceptional cloves prices on the international market, while the completion of investment in large mining projects resulted in the slowing down of imports, offset by rising food and input materials import.

(b) OP 8.30 requires that a sound financial sector framework be in place. The

prospects for the success of a guarantee are significantly stronger if the project uses strong and capable PFIs and such intermediaries are usually found in a competitive, liberalized, well-supervised, and reasonably strong financial sectors.

The banking sector is showing stability, competitiveness and profitability. Sector growth resumed in 2010 following uncertainties linked to the crisis in 2009. In 2011, there were 11 banks, 7 financial establishments and 31 microfinance institutions (MFI). Total assets (banks, financial establishments and MFIs reached MGA 4 751 billion in 2010, a 7.4 percent increase from a year earlier. Deposits rose by 7 percent and credits by 10.3 percent. The number of bank agencies and MFIs increased by 11 in 2010 to reach 655, following a decrease of 11 in 2009.

With respect to banks only, total assets stood at MGA 5,083 billion (US$2 billion) at end 2011, a 12 percent increase from 2010, total deposits rose by a same amount to reach MGA 4,164 (US$1.8 billion); however total credit increased by only 4 percent to MGA 2,212 billion (US$1 billion). However, NPLs remain high with an average gross ratio around 12 percent. This is a result of the continuing impact of the crisis. On the positive side, provisioning rose to about 70 percent. Net worth stood at MGA 449.7 billion in 2011. The net banking product registered a 13 percent increase in 2011 to MGA 399 billion. The average Return on Assets (ROA) stood at of 1.8 percent and the Return on Equity (ROE) at 19.6 percent which are quite respectable. Only one bank had a negative net profit.

All banks are very liquid as witnessed by the large gap between credits and deposits. While deposit mobilization continued throughout the crisis, banks remain very prudent in their lending activities. The PCG is expected to contribute to an increase in bank lending to qualifying firms.

A majority of banks are subsidiary from foreign banks. The three largest banks have similar market shares. As part of the appraisal, the team has reviewed regulation and supervision of banks by the Central Bank of Madagascar (BCM). BCM sets forth a set of strong prudential standards, which have generally been met by banks and MFIs.

- Solvency: The BCM requires banks to have a minimum available net

worth of MGA 3 billion and financial establishments a minimum capital of MGA 1 billion. Both must maintain a minimum solvency ratio of 8 percent.

29

- Counterparty risks: Exposure risk on a single beneficiary is limited to 35 percent of available net worth.

Regulations also set forth adequate governance directives and internal control systems. The BCM carries out off-site and on-site inspections of banks and financial establishments.