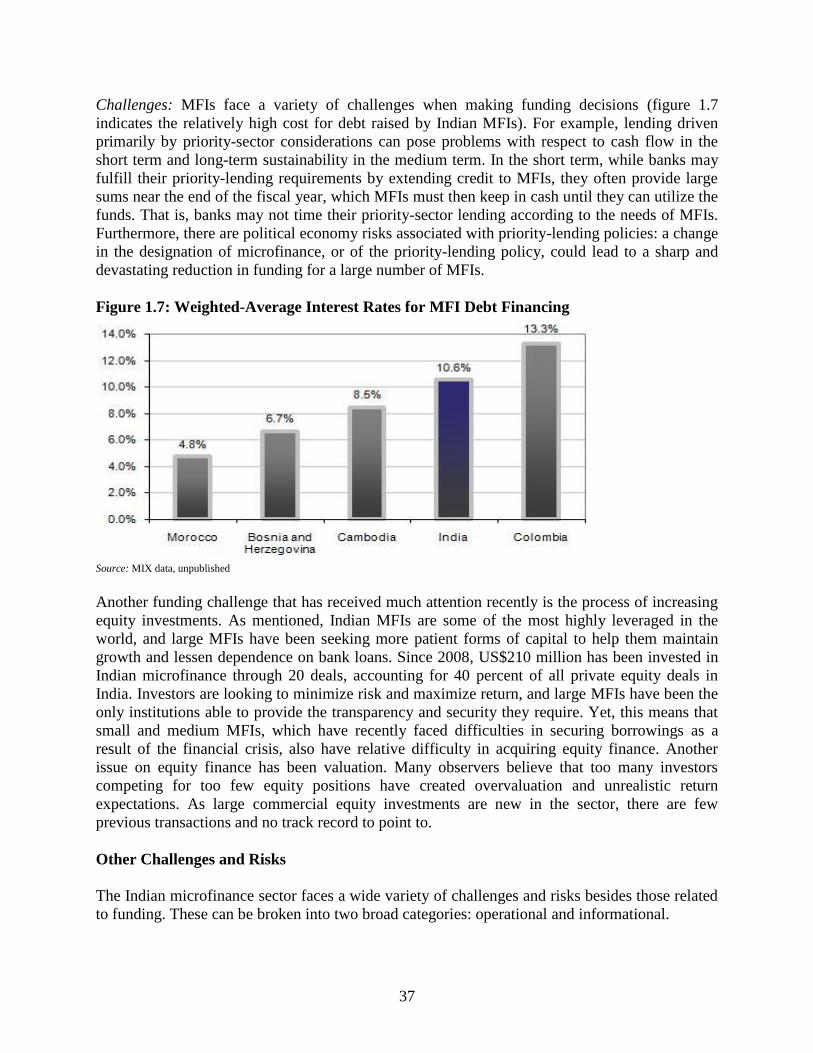

Embed Size (px)

Citation preview

Document of

The World Bank

FOR OFFICIAL USE ONLY

Report No: 50874-IN

PROJECT APPRAISAL DOCUMENT

ON A

PROPOSED CREDIT

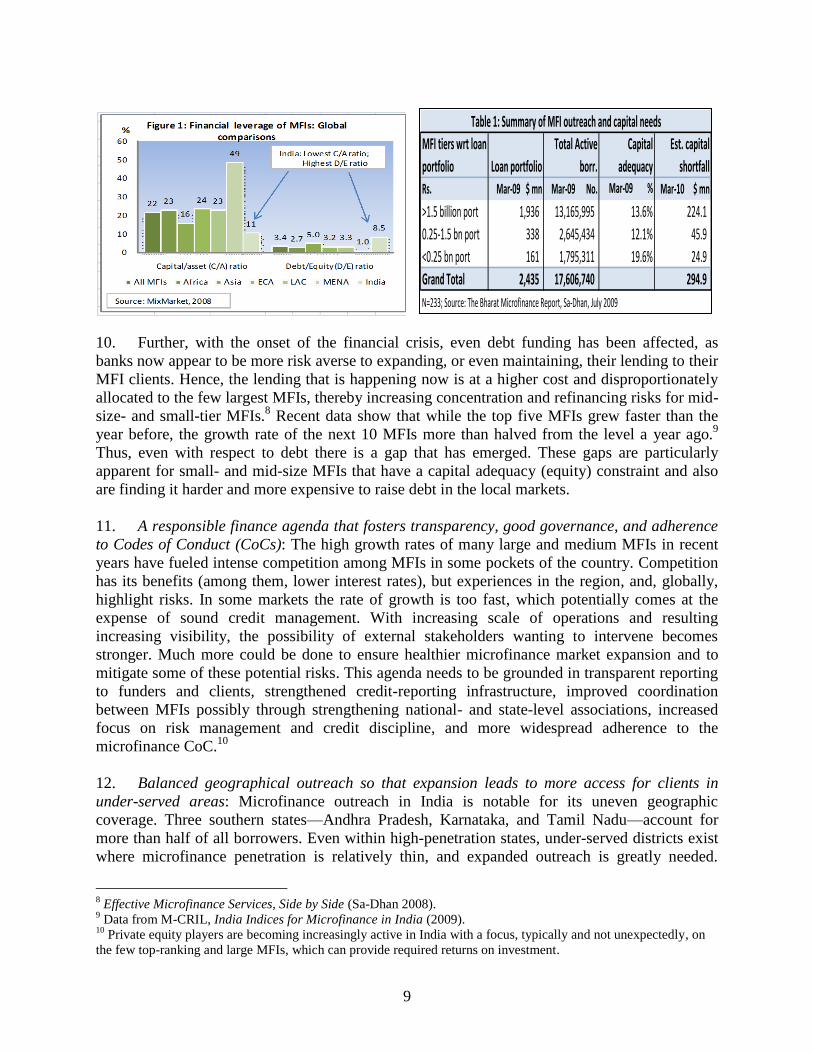

IN THE AMOUNT OF SDR 65.9 MILLION

(US$100 MILLION EQUIVALENT)

TO THE REPUBLIC OF INDIA

AND A PROPOSED LOAN

IN THE AMOUNT OF US$200 MILLION

TO THE SMALL INDUSTRIES DEVELOPMENT BANK OF INDIA

WITH A GUARANTEE OF THE REPUBLIC OF INDIA

FOR A

SCALING UP SUSTAINABLE AND RESPONSIBLE MICROFINANCE PROJECT

May 3, 2010

Poverty Reduction and Economic Management

Finance and Private Sector Development Department

South Asia Region

This document has a restricted distribution and may be used by recipients only in the performance of their official

duties. Its contents may not otherwise be disclosed without World Bank authorization.

Pub

lic D

iscl

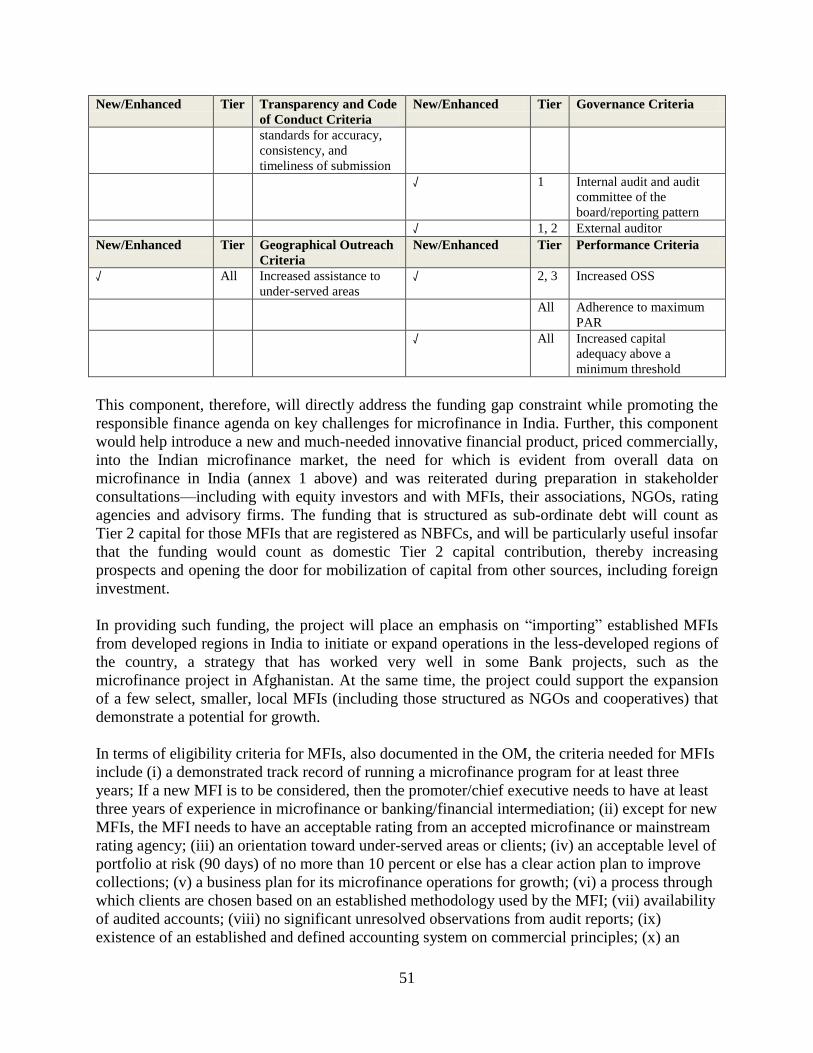

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

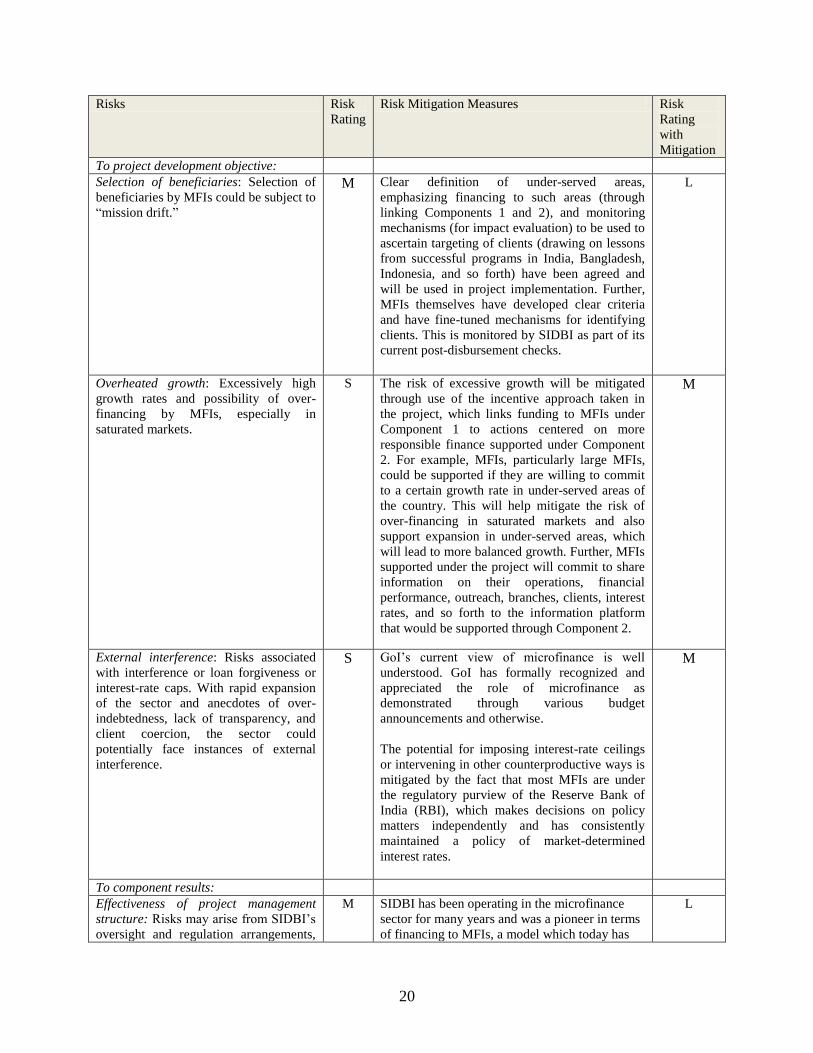

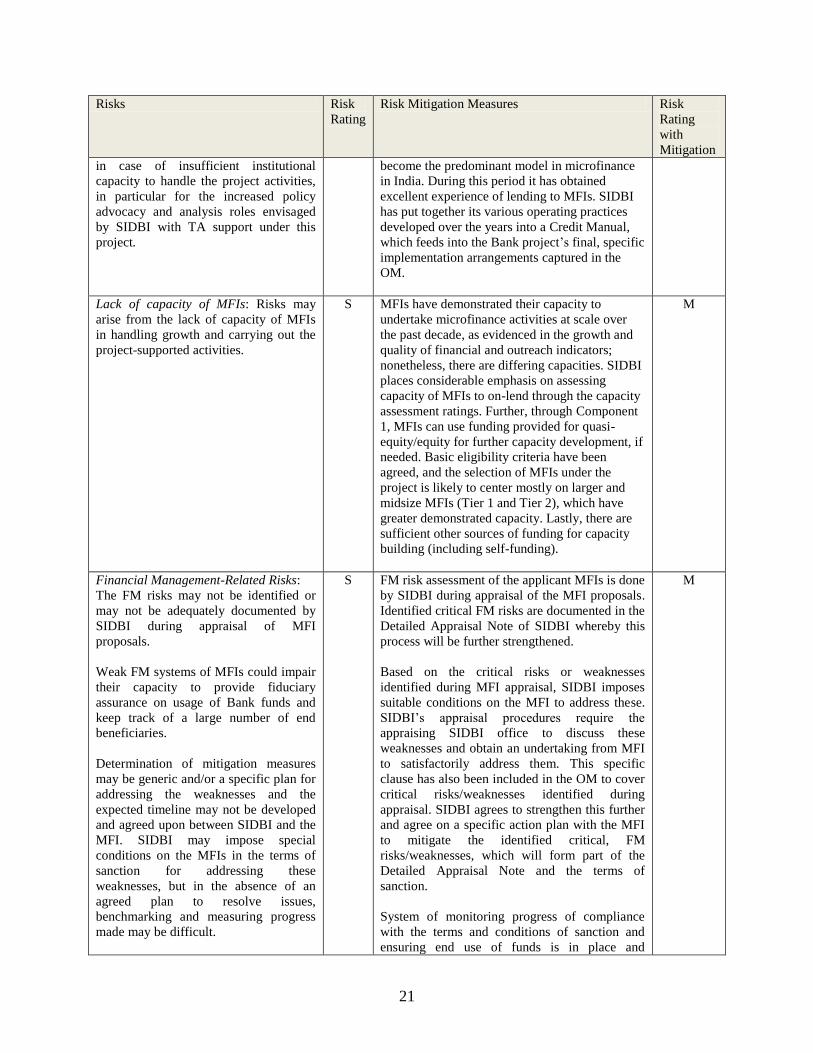

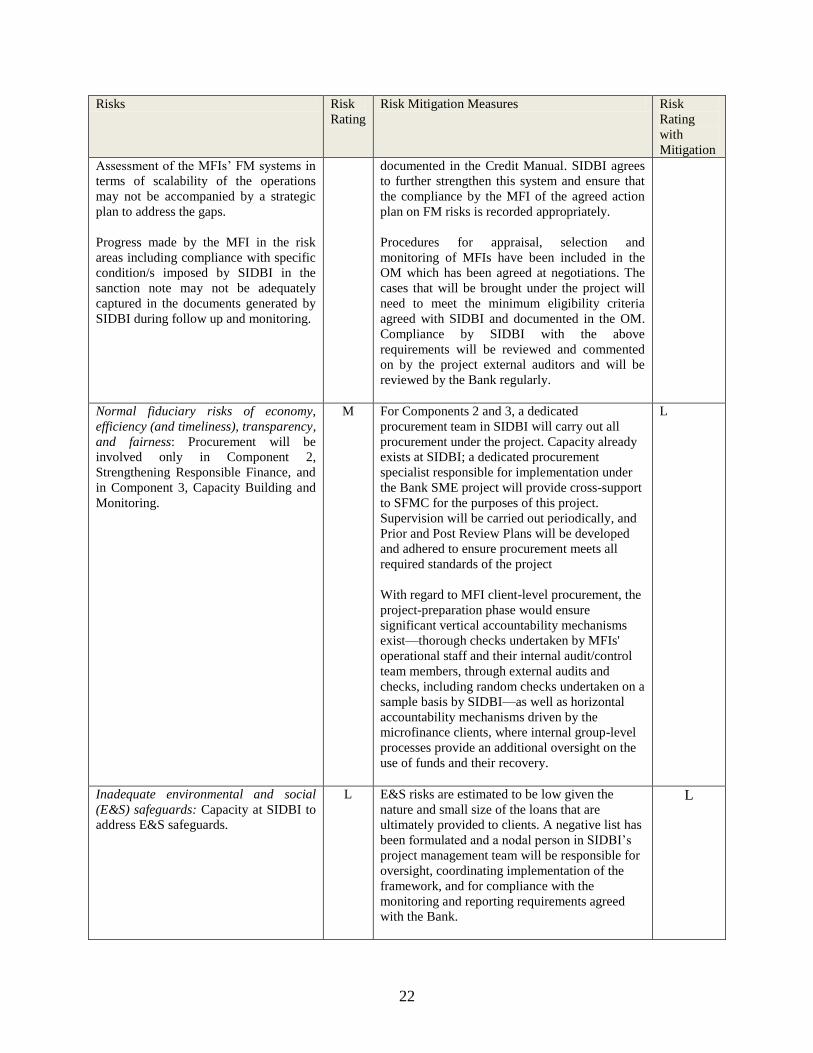

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

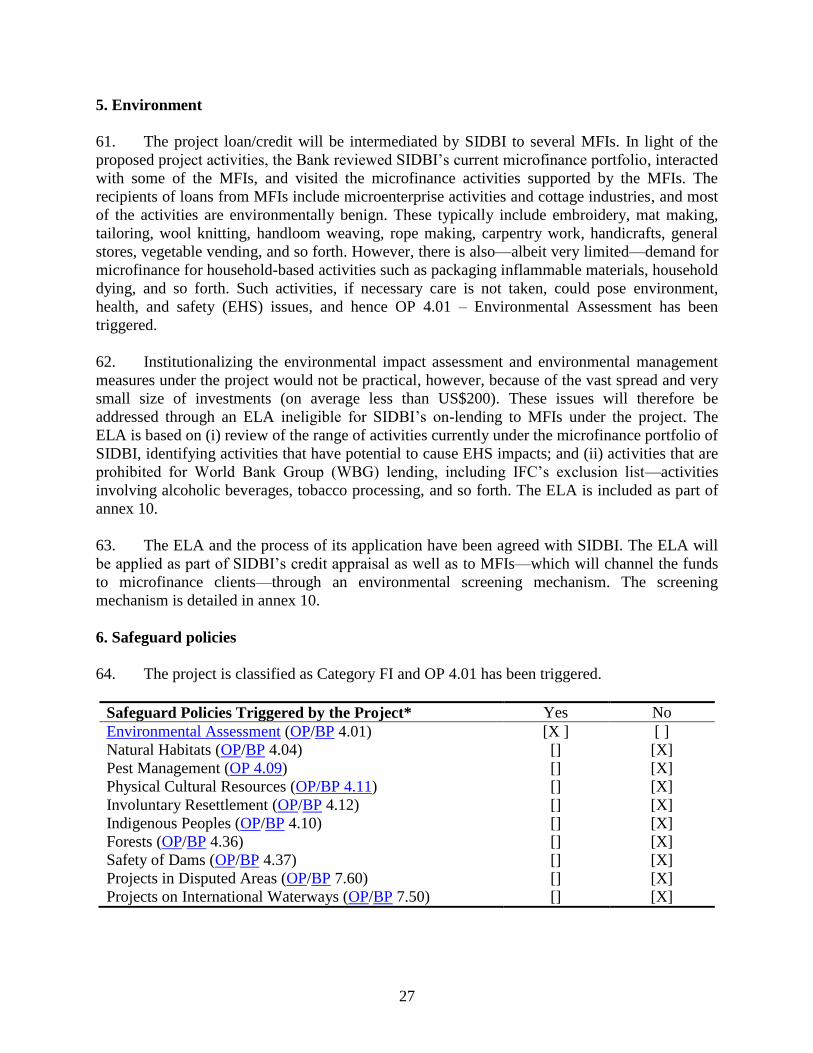

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

CURRENCY EQUIVALENTS

(Exchange Rate Effective March 31, 2010)

Currency Unit = Indian rupees (Rs)

Rs 45.14 = US$1

US$1.518 = SDR 1

FISCAL YEAR

April 1 – March 31

ABBREVIATIONS AND ACRONYMS

ACB

ADB

Audit Committee of the Board

Asian Development Bank

LIBOR

M&E

London Interbank Offer rate

Monitoring and Evaluation

AGM Assistant General Manager MFI Microfinance Institution

AML

ARCS

Anti-Money Laundering

Audit Reports Compliance System

MIS Management Information Services

CAS Country Strategy MISFA Microfinance Investment Support

Facility for Afghanistan

CDB China Development Bank MIV Microfinance Investment Vehicle

CGAP Consultative Group to Assist the Poor MIX Microfinance Information Exchange

CGM Chief General Manager MoF Ministry of Finance

CITES Convention on International Trade in

Endangered Species

MSME Micro, Small, and Medium Enterprises

CMD Chairman and Managing Director MTR Mid-Term Review

CoC Code of Conduct NABARD National Bank for Agriculture and

Rural Development

CRAR Capital to Risk-weighted Assets Ratio NBFC Nonbank Finance Company

CQS Consultant Qualification Services NCB National Competitive Bidding

DFID Department for International

Development, U.K.

NGO Non-Government Organization

DFS Department of Financial Services NMFSP National Micro Finance Support

Program

DGM Deputy General Manager NPA Non Performing Assets

DMD Deputy Managing Director NPL Non Performing Loans

DO

DPL

E&S

Development Objective

Development Policy Loan

Environmental and Social

OM

OSS

PAC

Operations Manual

Operational Self-Sufficiency

Project Advisory Committee

EHS Environment, Health, and Safety PAR Portfolio At Risk

ELA Exclusion List of Activities PCBs Polychlorinated Biphenyls

ESW Economic and Sector Work PKSF Palli-Karma Sahayak Foundation

FBS Fixed-Budget Selection PMD Project Management Department

FIL Financial Intermediary Loan PPAF Pakistan Poverty Alleviation Fund

FM Financial Management PSIG Poorest States Inclusive Growth

Program

FY Financial Year QCBS Quality and Cost-Based Selection

GAAP Governance and Accountability

Action Plan

QPR Quarterly Progress Report

GIS Global Information Services RBI Reserve Bank of India

GoI Government of India ROA Return On Assets

GM General Manager ROE Return On Equity

GTZ German Association for Technical

Cooperation

RTI Right to Information

IAD Internal Audit Department SFMC SIDBI Foundation for Micro-Credit

IBRD International Bank for Reconstruction

and Development

SHG Self-Help Group

ICB International competitive bidding SIDBI Small Industries Development Bank of

India

IDA International Development

Association

SME Small and Medium Enterprise

IDBI Industrial Development Bank of India SMFB Specialized Micro Finance Branch

IFAD International Fund for Agriculture

Development

TA Technical Assistance

IFC International Finance Corporation ToR Terms of Reference

IP Implementation Progress UC Utilization Certificate

IT Information Technology UNDB United Nations Development Business

IUFRs Interim Unaudited Financial Reports UPS Uninterrupted Power Supply

JBIC Japanese Bank for International

Cooperation

VSL Variable Spread Loan

KfW German Development Bank WAN Wide Area Network

KYC Know Your Customer WBG World Bank Group

LAN Local Area Network

LCS Least-Cost Selection

Vice President: Isabel Guerrero

Country Director: Roberto Zagha

Sector Director: Ernesto May

Sector Manager: Ivan Rossignol

Task Team Leaders: Niraj Verma and Mehnaz Safavian

INDIA:

SCALING UP SUSTAINABLE AND RESPONSIBLE MICROFINANCE PROJECT

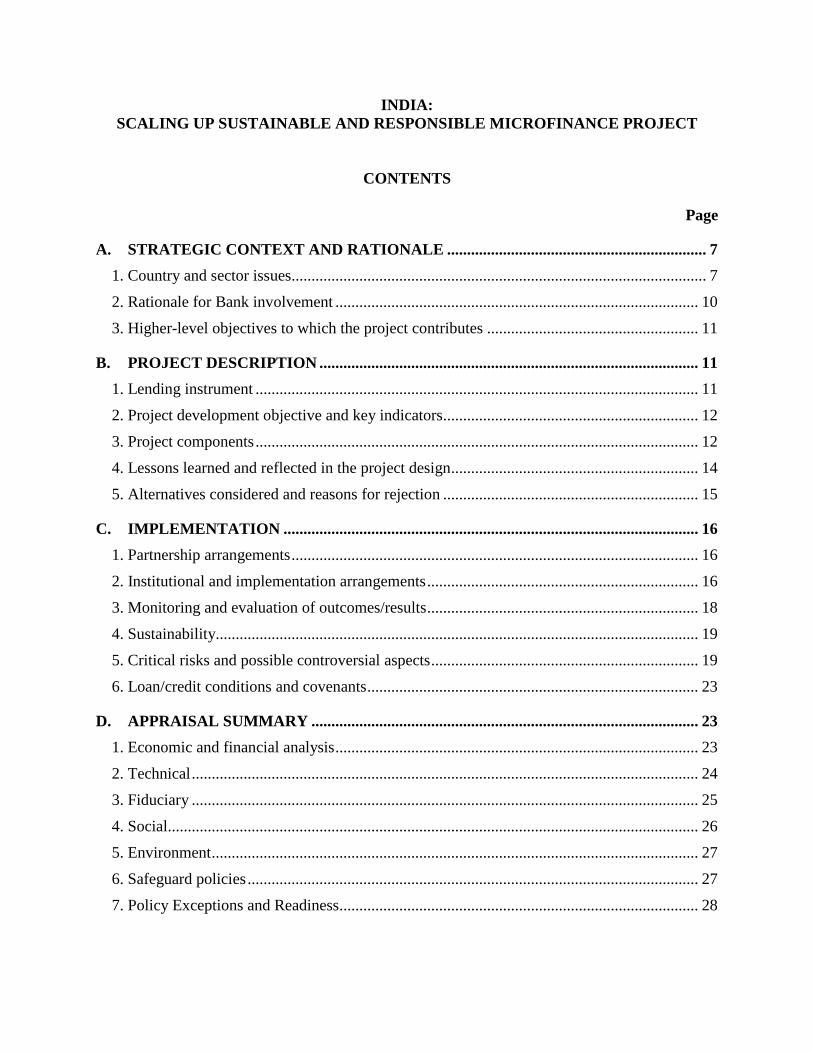

CONTENTS

Page

A. STRATEGIC CONTEXT AND RATIONALE ................................................................. 7

1. Country and sector issues........................................................................................................ 7

2. Rationale for Bank involvement ........................................................................................... 10

3. Higher-level objectives to which the project contributes ..................................................... 11

B. PROJECT DESCRIPTION ............................................................................................... 11

1. Lending instrument ............................................................................................................... 11

2. Project development objective and key indicators ................................................................ 12

3. Project components ............................................................................................................... 12

4. Lessons learned and reflected in the project design.............................................................. 14

5. Alternatives considered and reasons for rejection ................................................................ 15

C. IMPLEMENTATION ........................................................................................................ 16

1. Partnership arrangements ...................................................................................................... 16

2. Institutional and implementation arrangements .................................................................... 16

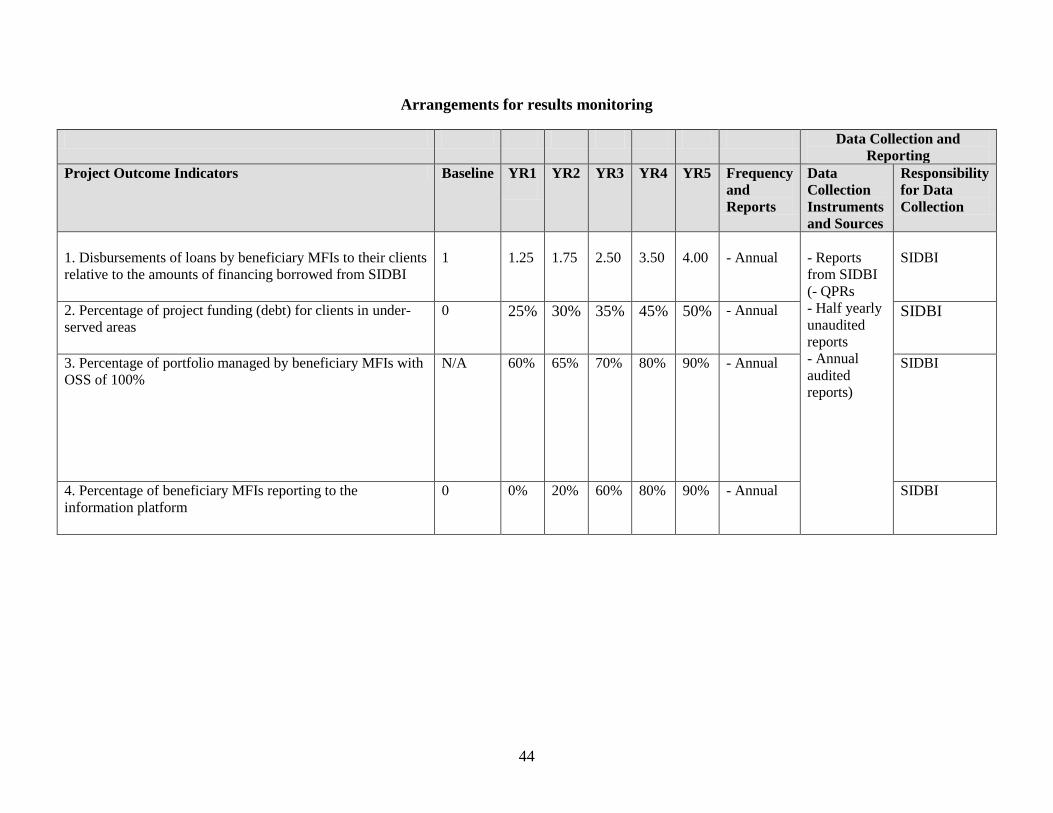

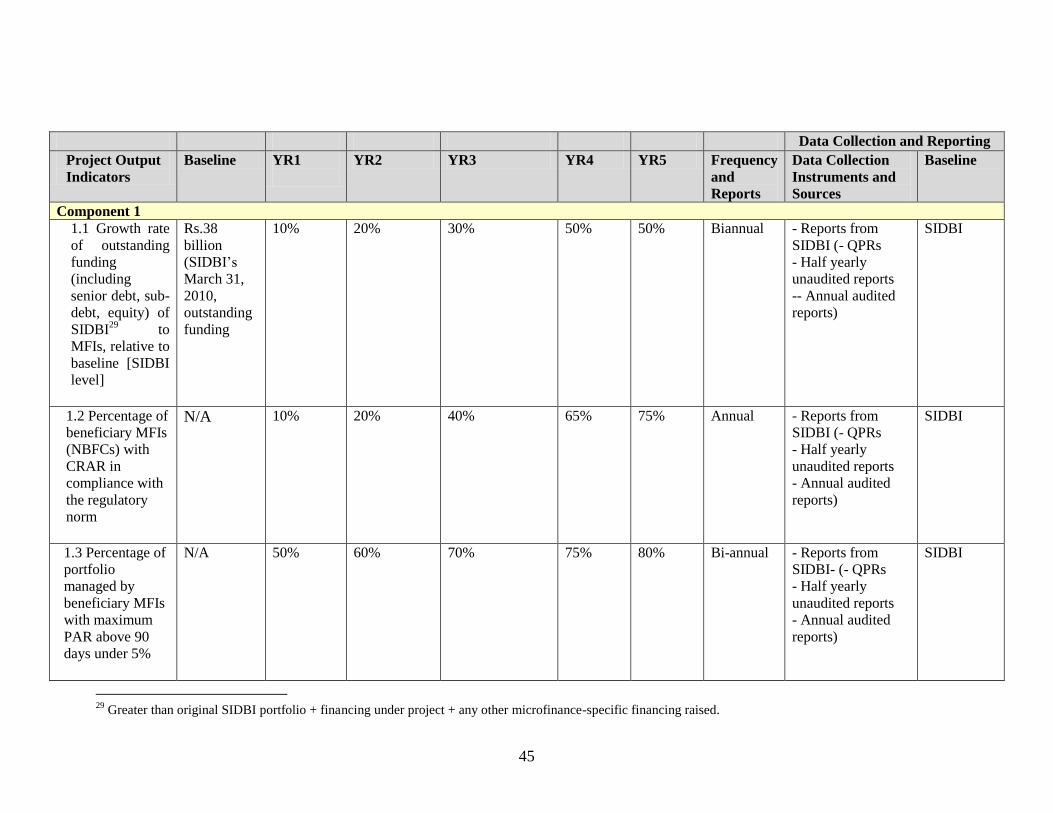

3. Monitoring and evaluation of outcomes/results .................................................................... 18

4. Sustainability......................................................................................................................... 19

5. Critical risks and possible controversial aspects ................................................................... 19

6. Loan/credit conditions and covenants ................................................................................... 23

D. APPRAISAL SUMMARY ................................................................................................. 23

1. Economic and financial analysis ........................................................................................... 23

2. Technical ............................................................................................................................... 24

3. Fiduciary ............................................................................................................................... 25

4. Social..................................................................................................................................... 26

5. Environment .......................................................................................................................... 27

6. Safeguard policies ................................................................................................................. 27

7. Policy Exceptions and Readiness.......................................................................................... 28

2

Annex 1: Country and Sector or Program Background ......................................................... 29

Annex 2: Major Related Projects Financed by the Bank and/or other Agencies ................. 40

Annex 3: Results Framework and Monitoring ........................................................................ 42

Annex 4: Detailed Project Description ...................................................................................... 48

Annex 5: Project Costs ............................................................................................................... 55

Annex 6: Implementation Arrangements ................................................................................. 56

Annex 7: Financial Management and Disbursement Arrangements ..................................... 78

Annex 8: Procurement Arrangements ...................................................................................... 89

Annex 9: Economic and Financial Analysis ............................................................................. 97

Annex 10: Safeguard Policy Issues .......................................................................................... 102

Annex 11: Project Preparation and Supervision ................................................................... 105

Annex 12: Documents in the Project File ............................................................................... 107

Annex 13: Statement of Loans and Credits ............................................................................ 110

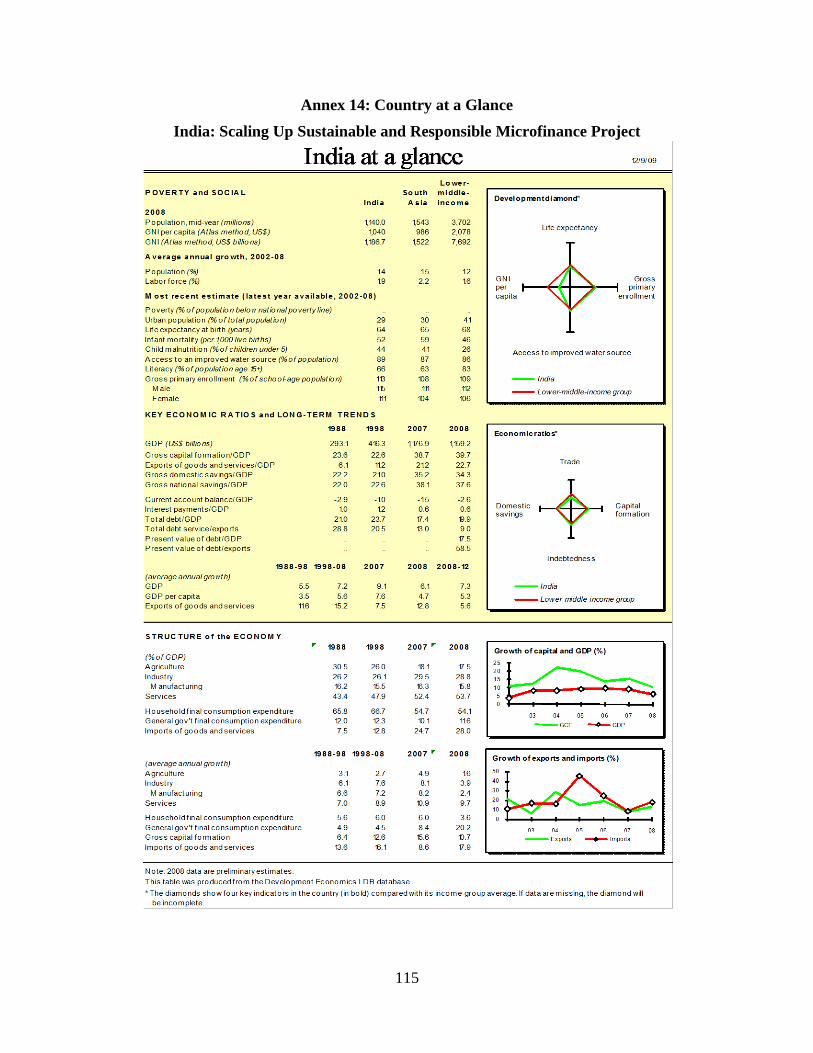

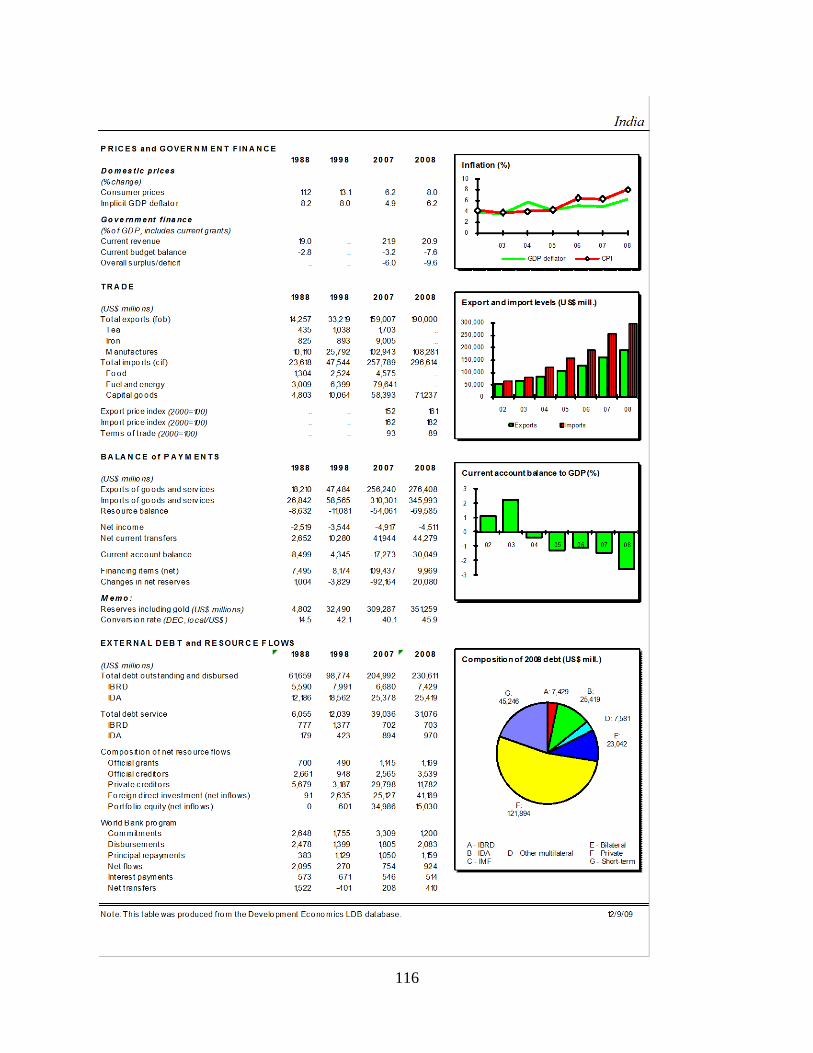

Annex 14: Country at a Glance ............................................................................................... 115

3

INDIA:

SCALING UP SUSTAINABLE AND RESPONSIBLE MICROFINANCE PROJECT

PROJECT APPRAISAL DOCUMENT (PAD)

SOUTH ASIA REGION

SASFP

Date: June 25, 2010 Team Leader: Niraj Verma, Mehnaz Safavian

Country Director: Roberto Zagha

Sector Manager/Director: Ivan Rossignol/

Ernesto May

Sectors:Micro- and SME Finance (100

percent)

Themes: Other financial and private sector

development; rural and non-farm development

Project ID: P119043 Environmental category: FI

Lending Instrument: Financial Intermediary

Loan (FIL)

Project Financing Data

[ x ] Loan [X] Credit [ ] Grant [ ] Guarantee [ ] Other:

For Loans/Credits/Others (US$m): 300.0

Total Bank financing (US$m.): 300.0

Proposed terms: IBRD flexible loan with variable spread with a 25 year maturity, including a

14.5-year grace period; for IDA, 35 years with 10 years‘ grace

Financing Plan (US$m)

Source Local Foreign Total

BORROWER/RECIPIENT 30.00 0.00 30.00

International Development Association

(IDA)

100.00 0.00 100.00

International Bank for Reconstruction and

Development (IBRD)

200.00 0.00 200.00

Total: 330.00 0.00 330.00

Borrower: Small Industries Development Bank of India (SIDBI) for IBRD and the Republic of

India, for IDA (to be channeled onward to SIDBI)

Responsible Agency: Department of Financial Services, Ministry of Finance, Government of

India, and SIDBI

Estimated disbursements (Bank FY/US$m)

FY 2011 2012 2013 2014 2015

Annual 70.0 80.0 80.0 50.0 20.0

Cumulative 70.0 150.0 230.0 280.0 300.0

Project Implementation Period: 5 years

Expected effectiveness date: June 30, 2010

4

Expected closing date: June 30, 2015

Does the project depart from the CAS in content or other significant respects?

Ref. PAD I.C. [ ]Yes [X] No

Does the project require any exceptions from Bank policies?

Ref. PAD IV.G. Have these been approved by Bank management?

[ ]Yes [X] No

[ ]Yes [X] No

Is approval for any policy exception sought from the Board? [ ]Yes [X] No

Does the project include any critical risks rated ―substantial‖ or ―high‖?

Ref. PAD III.E. []Yes [X] No

Does the project meet the Regional criteria for readiness for implementation?

Ref. PAD IV.G. [X]Yes [ ] No

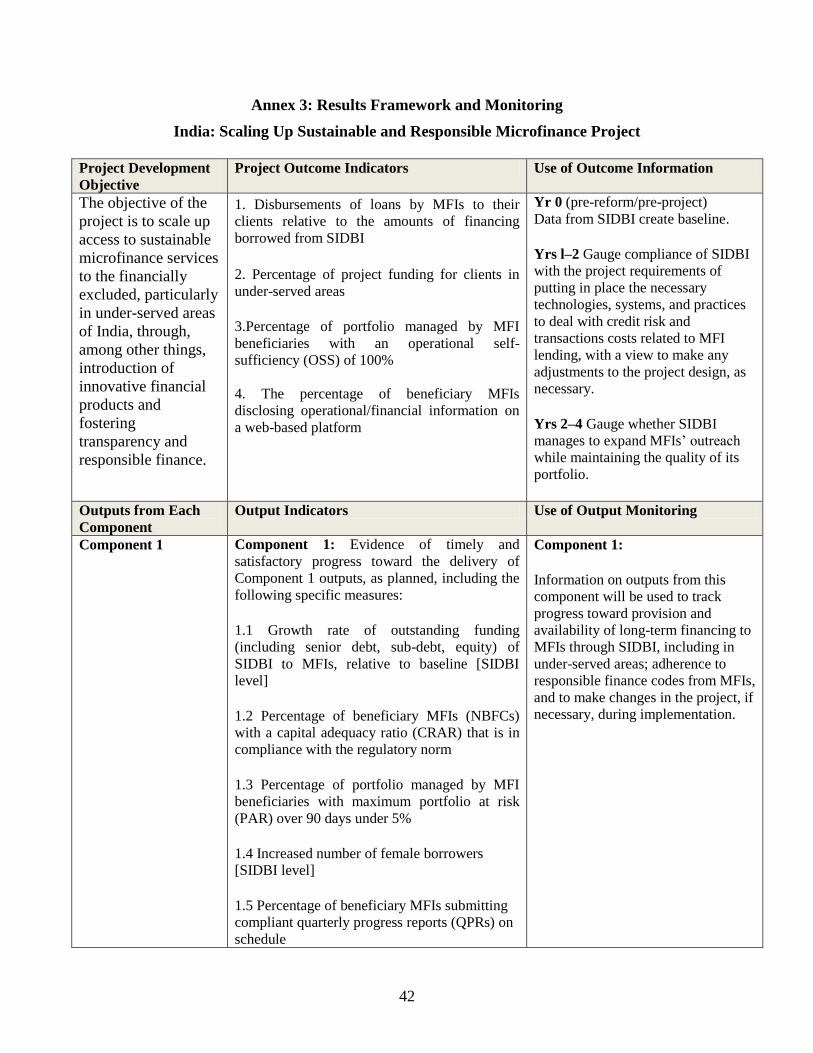

Project development objective Ref. PAD B.2, Technical Annex 3

The objective of the project is to scale up access to sustainable microfinance services to the

financially excluded, particularly in under-served areas of India, through, among other things,

introduction of innovative financial products and fostering transparency and responsible finance.

Progress towards the achievement of the project objective would be monitored using the

following indicators (refer also to annex 3):

Extent of outreach: Disbursements of loans by microfinance institutions (MFIs) to their

clients relative to the amounts of financing borrowed from SIDBI

Breadth of outreach: Measured by growth rates within under-served areas

Operational sustainability: Measured by operational self sufficiency (OSS)

Responsible Finance: Measured by the percentage of beneficiary MFIs disclosing

operational/ financial information on a web-based information platform

Project description Ref. PAD B.3, Technical Annex 4

Component 1: Scaling Up Funding Support for Microfinance Institutions (MFIs) (~US$290

million, plus US$30 million counterpart funding)

This component would provide funding for MFIs to scale up their operations. Funding from

SIDBI to MFIs is proposed to be structured as debt or quasi-equity, to support their operations

and growth, enhance their financial strength, and enable them to leverage and crowd-in private

commercial funds to on-lend larger amounts to the under-served. Limited equity support would

also be considered from SIDBI to MFIs. The total funding thus mobilized will enhance MFIs‘

ability to reach out to larger numbers of under-served segments of the population through

microfinance services. In particular, the quasi-equity/equity funding will also help address the

equity gap in Indian MFIs, while providing SIDBI with the leverage to promote the responsible

finance agenda among the MFIs funded by the project.

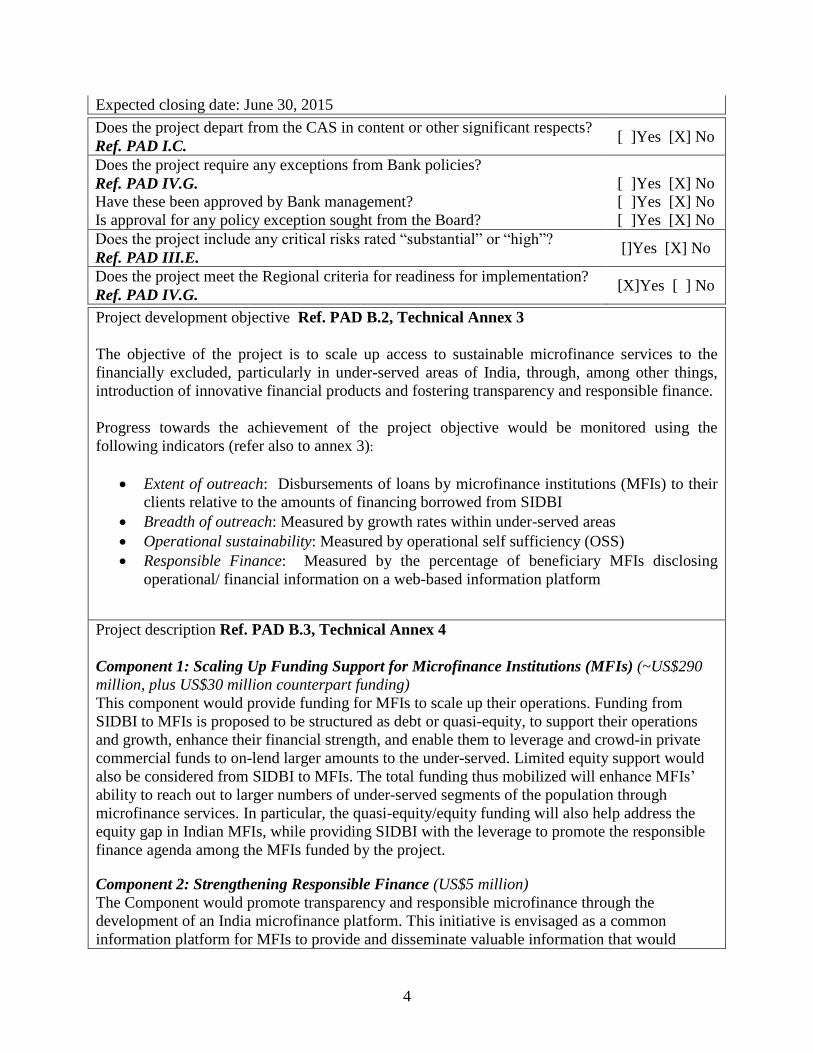

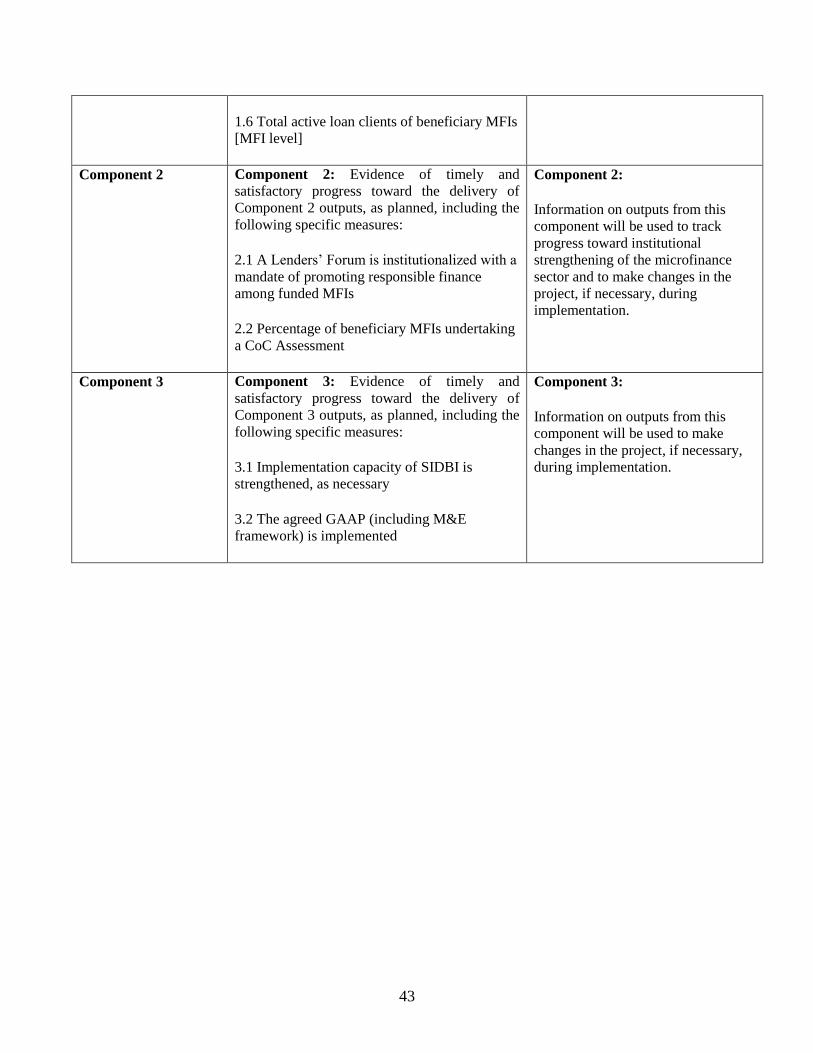

Component 2: Strengthening Responsible Finance (US$5 million)

The Component would promote transparency and responsible microfinance through the

development of an India microfinance platform. This initiative is envisaged as a common

information platform for MFIs to provide and disseminate valuable information that would

5

inform policymakers, MFI managers and funders (similar, but broader and deeper than the

information available on the MixMarket – which is the leading global microfinance information

database provider - including through potential collaboration with MixMarket in India). As part

of the responsible finance initiative, SIDBI will seek to bring together a Lenders‘ Forum

comprising key MFI funders to agree on common actions which could include those on

transparency and good governance by MFIs. Additionally, once the Unique Identification (UID)

initiative of the GoI is ready for implementation, the forum will encourage MFIs to participate

and support the roll-out of this initiative, given its significant potential to improve transparency

and credit information. The Component could also potentially support the development and

piloting of a Code of Conduct (CoC) Assessment, which could serve as an innovative rating tool

measuring performance of MFIs as pertaining to their CoC adherence. Component 2 will be

cross linked with Component 1, such that MFIs accessing Component 1 will need to commit to

data sharing on the common information platform and possibly other responsible finance

initiatives defined in the Operations Manual (OM).

Component 3: Capacity Building and Monitoring Component (US$5 million)

This component would provide implementation support, which would include support to SIDBI

for (i) implementing the project, including operating expenses and costs of the monitoring work

(defined in annex 3 and elsewhere); (ii) commissioning an impact evaluation exercise (to be

carried out through an external research agency); and (iii) SIDBI‘s own capacity building. This

component would also include support for a communication strategy to help ensure the benefits

from this intervention are shared with the wider microfinance sector.

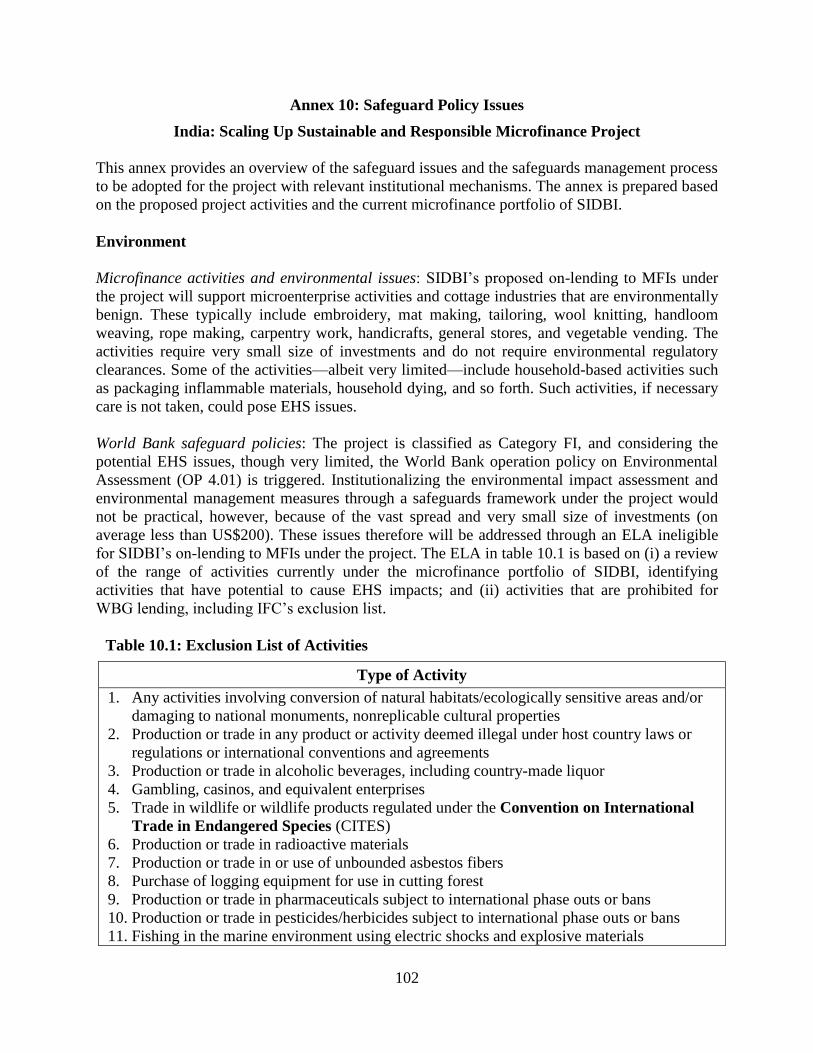

Which safeguard policies are triggered, if any? Ref. PAD D.5, Technical Annex 10

The project has been assigned an environmental screening category ―FI.‖ The following

safeguard policies are triggered: Environmental Assessment OP 4.01

Significant, non-standard conditions, if any, for:

Board presentation: None

Loan/credit effectiveness: June 2010

The condition for effectiveness will be that the Subsidiary Agreement has been executed on

behalf of India and SIDBI, and all conditions precedent to its effectiveness or to the right of the

SIDBI to make withdrawals under it (other than the effectiveness of the Loan Agreement and the

Financing Agreement) have been fulfilled.

Covenants applicable to project implementation are as follows:

i. SIDBI shall maintain an adequate organizational structure with functions, powers,

staff, and resources necessary for project implementation.

ii. SIDBI shall implement the project in accordance with the provisions of the OM

for the project.

iii. SIDBI shall monitor progress of the project in accordance with indicators

satisfactory to the Bank.

iv. The midterm review (MTR) of the project shall be carried out by December 31,

2012.

6

v. SIDBI‘s on-lending activities to MFIs under the project shall be carried out in

accordance with the agreed Exclusion List of Activities (ELA), and SIDBI will

ensure that the microfinance activities under the project comply with the ELA.

7

A. STRATEGIC CONTEXT AND RATIONALE

1. Country and sector issues

1. The Indian financial sector has witnessed reforms since the early 1990s resulting in

improved financial performance and stability during this period. These reforms—including

interest rate deregulation, capital market development (particularly equity and government bond

markets), and opening up of the banking and insurance sectors—have facilitated increased

competitiveness in banking through the entry of new private domestic and foreign players,

introduction of new technology and products, and deepening of India‘s financial system.

2. Notwithstanding a stable, dynamic, and growing financial sector, increasing access to

finance for millions of India’s financially under-served segments remains a challenge. This

challenge has further been accentuated by the financial crisis, during which—despite stable

policies, increasing efficiency, strong factor endowments, and a dynamic financial market—

India‘s economic growth slowed from 9.7 percent in 2006–07 to 5–6 percent in the second half

of 2008–09, accompanied by a slowdown in credit growth.1

3. In recent years there have been numerous initiatives to improve access to finance to

financially under-served segments. Among these initiatives is the Government of India (GoI)

program to support the revitalization of the rural credit cooperatives,2 initiatives to increase

access to finance for small and medium enterprises (SMEs),3 and supporting infrastructure

finance,4 introducing enabling guidelines to support financial inclusion by, for example, opening

no-frills savings accounts for under-served clients, provisions to expand the outreach of micro-

insurance, and the use of banking correspondents to increase access.

4. However, despite these measures, access to financial services for India’s poor still

remains a key development challenge, as a significant part of the population is under-served by

the formal banking sector.5 While India has a well-developed banking system and there has been

significant progress in banking sector reforms, performance, and stability, two-thirds of the

population is still estimated to have only limited or no access to financial services. Given the

large demand, in addition to the measures described above, there is a need for multiple

approaches and mechanisms to provide basic financial services to all Indians. Among such

initiatives is the use and support of microfinance initiatives that can help to deepen the

penetration of financial services among the poor and under-served.

5. The microfinance sector, which bridges the ―access gap‖ by providing thrift, credit, and

other customized financial services to the under-served, with the aim to help raise incomes and

improve living standards, has been growing exponentially in India. Smaller initiatives in

1 Supported by the Bank-funded Banking Sector Support Loan (US$2 billion) that provides budgetary support to the

government for supporting capital infusion into banks, partly as a precautionary shield and partly to prevent lack of

capital from constraining good quality credit growth. 2 Supported by a Bank project on Strengthening India‘s Rural Credit Cooperatives (US$600 million).

3 Supported by a Bank project on SME Financing and Development (US$120 million) topped up recently with

additional financing in the amount of US$400 million. 4 Supported by the Bank‘s loan to the India Infrastructure Finance Company (US$1.195 billion).

5 India: Scaling Up Access to Finance for India’s Rural Poor (World Bank 2004, 2006).

8

microfinance in India date back to the 1970s, but the sector really started gaining a foothold in

the late 1990s (see also annex 1). Facilitated by a benign approach toward regulation since 1997,

and with a focus on the southern states, microfinance institutions (MFIs) have been scaling up

rapidly in recent years, although from a small base. Growth in loans outstanding to clients—now

mostly accounted for by MFIs structured as regulated nonbank finance companies—has been at

rates in excess of 65 percent per year over the past three years, and stood at around US$2.5

billion at the end of financial year (FY) 2009.

6. This growth has contributed to reducing the gap between the unmet demand for and

supply of financial services for under-served households and microenterprises. Recent analysis

indicates that access to microfinance in India has contributed to the reduction in vulnerability of

poor households through asset creation, increased incomes, higher savings and employment, and

empowerment of women clientele.6

7. However, two overarching challenges remain: (i) a large unmet demand for financial

services by India’s under-served segments, particularly in states where market penetration has

been extremely low; and (ii) rapid expansion, which introduces the dual challenge of

maintaining good-quality growth while promoting responsible finance among MFIs.

Conservative estimates from Sa-Dhan, the main network of MFIs, indicate an unmet credit

demand among potential microfinance clients at Rs 80,000 crores (US$17.7 billion). Rapid

expansion, however, can lead to funding gaps, potentially erode credit discipline, and introduce

risky market behavior. This could result in external interference in the sector, which could

threaten short- and medium-term sustainability.

Key Issues:

8. Scaling up microfinance and promoting responsible and balanced growth relies on

tackling three key issues facing the microfinance industry in India:

9. Appropriate financing that tackles the growing equity gap and the need for more patient

debt instruments: The fast-paced growth of Indian microfinance has been largely driven by

commercial bank debt to MFIs. The share of debt in total funding of MFIs exceeds 80 percent,

most of which is sourced from commercial banks at commercial rates. As a result, the fast debt-

funded growth—without sources and amounts of equity growing at a commensurate pace—has

led to a situation where many Indian MFIs face a severe shortage of equity capital, limiting their

ability to take on more debt and increase lending outreach to more clients (figure 1 and table 1

below). A recent International Finance Corporation (IFC)–Intellecap study estimates that even

with conservative assumptions, the minimum equity/quasi-equity amount needed is US$1.3

billion over the next four years.7 Bank projections show that even with conservative growth

assumptions, there is a need of US$294 million in equity funds immediately. Furthermore, with

such capital structure constraints, MFIs have less of an incentive to focus on under-served areas,

as this will increase their cost, which in turn will have a negative impact on the capital adequacy.

6 Assessing Development Impact of Microfinance Programs is a national study of Indian microfinance households

commissioned by SIDBI, in collaboration with the Department for International Development (DFID), September

2008. 7 Inverting the Pyramid (Intellecap and IFC 2008).

9

MFI tiers wrt loan

portfolio Loan portfolio

Total Active

borr.

Capital

adequacy

Est. capital

shortfall

Rs. Mar-09 $ mn Mar-09 No. Mar-09 % Mar-10 $ mn

>1.5 billion port 1,936 13,165,995 13.6% 224.1

0.25-1.5 bn port 338 2,645,434 12.1% 45.9

<0.25 bn port 161 1,795,311 19.6% 24.9

Grand Total 2,435 17,606,740 294.9

N=233; Source: The Bharat Microfinance Report, Sa-Dhan, July 2009

Table 1: Summary of MFI outreach and capital needs

10. Further, with the onset of the financial crisis, even debt funding has been affected, as

banks now appear to be more risk averse to expanding, or even maintaining, their lending to their

MFI clients. Hence, the lending that is happening now is at a higher cost and disproportionately

allocated to the few largest MFIs, thereby increasing concentration and refinancing risks for mid-

size- and small-tier MFIs.8 Recent data show that while the top five MFIs grew faster than the

year before, the growth rate of the next 10 MFIs more than halved from the level a year ago.9

Thus, even with respect to debt there is a gap that has emerged. These gaps are particularly

apparent for small- and mid-size MFIs that have a capital adequacy (equity) constraint and also

are finding it harder and more expensive to raise debt in the local markets.

11. A responsible finance agenda that fosters transparency, good governance, and adherence

to Codes of Conduct (CoCs): The high growth rates of many large and medium MFIs in recent

years have fueled intense competition among MFIs in some pockets of the country. Competition

has its benefits (among them, lower interest rates), but experiences in the region, and, globally,

highlight risks. In some markets the rate of growth is too fast, which potentially comes at the

expense of sound credit management. With increasing scale of operations and resulting

increasing visibility, the possibility of external stakeholders wanting to intervene becomes

stronger. Much more could be done to ensure healthier microfinance market expansion and to

mitigate some of these potential risks. This agenda needs to be grounded in transparent reporting

to funders and clients, strengthened credit-reporting infrastructure, improved coordination

between MFIs possibly through strengthening national- and state-level associations, increased

focus on risk management and credit discipline, and more widespread adherence to the

microfinance CoC.10

12. Balanced geographical outreach so that expansion leads to more access for clients in

under-served areas: Microfinance outreach in India is notable for its uneven geographic

coverage. Three southern states—Andhra Pradesh, Karnataka, and Tamil Nadu—account for

more than half of all borrowers. Even within high-penetration states, under-served districts exist

where microfinance penetration is relatively thin, and expanded outreach is greatly needed.

8 Effective Microfinance Services, Side by Side (Sa-Dhan 2008).

9 Data from M-CRIL, India Indices for Microfinance in India (2009).

10 Private equity players are becoming increasingly active in India with a focus, typically and not unexpectedly, on

the few top-ranking and large MFIs, which can provide required returns on investment.

10

Therefore, as microfinance continues to grow, it will be important to ensure this growth is

inclusive, with better geographical coverage to address the demand for financial services in

under-served states and districts.

2. Rationale for Bank involvement

13. The rationale for Bank involvement essentially revolves around three main issues: (i) the

contribution of the project to the goal of inclusive growth, consistent with the Country Strategy

(CAS); (ii) the long-term funding constraints that threaten continued and balanced growth of the

sector; and (iii) need for a stronger responsible finance agenda that is undertaken by the sector.

14. The World Bank Group‘s India CAS highlights the need for inclusive growth.

Microfinance, by addressing the financial service needs of under-served clients, is an important

tool for poverty reduction, private sector development, and inclusive growth. Economic and

sector work undertaken11

emphasizes the need for the development of the microfinance sector in

India. The Bank has also recently completed a microfinance strategy, Financing the Bottom of

the Pyramid: Microfinance Strategy for South Asia: FY2010–12. The strategy highlights the

Bank‘s comparative advantage in supporting the microfinance agenda in the region, including

working with apex institutions to crowd in commercial finance; increase standards, reporting,

and efficiency of MFIs; and ease crisis-related liquidity constraints. The Government of India

(GoI) recognizes that scaling up microfinance in a responsible and sustainable manner will

require diverse modalities for expanding the flow of financial services to the poor. Toward this

objective, the Small Industries Development Bank of India (SIDBI) is poised to take a more

active leadership role in growing the industry to meet the unmet demand for financial services.

SIDBI is the most prominent and influential apex organization for microfinance in India and

among the better-performing microfinance apexes globally. Support to strengthen SIDBI‘s

leadership role is well suited to the World Bank‘s country and regional microfinance strategies.

15. Secondly, the role of the Bank is justified on grounds of the market failure that exists with

respect to lack of appropriate funding instruments needed at this stage of development. As

mentioned above, Indian microfinance is faced with a situation where many Indian MFIs face a

severe shortage of equity capital, which limits their ability to take on more debt and increase

lending outreach to more clients. Availability of longer-term funding sources would help SIDBI

in introducing appropriate financial instruments that would contribute to strengthening the

balance sheets of the MFIs. The accumulated Bank know-how and lessons learned from previous

lending operations, both in India (for example, rural livelihoods projects, financial intermediary

loans to SIDBI directed to the financing and development of small and medium enterprises; see

annex 2 for more detail) and globally, provide useful experience to draw on. Additionally, the

project would support India in its response to the financial crisis, which has affected lending to

MFIs as observed by a slowdown in fresh disbursements to smaller and medium-size MFIs.

11

These include India: Scaling Up Access to Finance for India‘s Rural Poor‖ (World Bank 2004, 2006),

Microfinance in South Asia (World Bank 2006), India: Regulation of Microfinance (World Bank, CGAP 2006),

Inverting the Pyramid (Intellecap and IFC 2008), Bharat Microfinance Report (Sa-Dhan 2009), and Microfinance

India: State of the Sector Reports (Access Development Services 2006, 2007, 2008, 2009). For a more detailed list,

see annex 12.

11

16. Thirdly, microfinance in India has entered a phase of rapid growth, but as a younger

industry, it still has numerous vulnerabilities. High growth can erode credit discipline and can

potentially introduce risky market behaviors such as client over-indebtedness and poor risk

management. Timely leadership from SIDBI supported by the World Bank project to promote

more responsible finance, improve transparency, and add to new market information and

infrastructure can serve to mitigate these risks during this crucial period of expansion. Such

leadership can ensure that microfinance becomes a nationwide industry contributing to balanced

and inclusive growth across India.

3. Higher-level objectives to which the project contributes

17. The project is designed to support inclusive growth in India by supporting GoI and

SIDBI‘s efforts to scale up and promote responsible and balanced growth of microfinance.

Improved access to finance would work toward this objective by contributing to sustainable

income generation and productive asset creation, poverty reduction, and growth. These are

consistent with GoI‘s development priorities as reflected in the Eleventh Five-Year Plan as well

as the Bank‘s focus on inclusive growth reflected in the CAS.

18. The project is part of the Bank's program of targeted assistance to those without access to

financial services. The project addresses the lack of access of the under-served households to

financial services, an important constraint to improved productivity and incomes, particularly in

the aftermath of the global financial crisis that has affected MFIs and their clients. The project

would build on SIDBI‘s success of fostering and catalyzing growth and sustainability of the

sector since the mid-to-late 1990s, with a focus toward increasing financial outreach particularly

in under-served areas where microfinance penetration continues to be very low.

B. PROJECT DESCRIPTION

1. Lending instrument

19. The lending instrument is a financial intermediary loan (FIL) (as per the World Bank

Operational Manual Policy Directive OP 8.30), to be financed by a combination of the

International Development Association (IDA) and International Bank for Reconstruction and

Development (IBRD) resources, in one-third and two-third proportions, respectively, totaling

US$300 million (equivalent). For the IBRD component, SIDBI has opted for a variable spread,

denominated in U.S. dollars. The IBRD part will have a final maturity of 25 years, including a

grace period of 14.5 years. The variable lending rate consists of six-month London interbank

offered rate (LIBOR) and a variable spread. The charges include a front-end fee, apart from the

contractual spread. After factoring in the benefits of sub-LIBOR funding costs, including any

applicable loan charge waivers the expected disbursement profile of the project, and amortization

schedule, the all-inclusive (blended) cost based on forward LIBOR rates and the current variable

spread (as on April 26, 2010) is estimated at 3.40 percent.12

12

The current variable spread is LIBOR + 0.24%, or 0.74% at market rates as of April 26, 2010.

12

2. Project development objective and key indicators

20. The objective of the project is to scale up access to sustainable microfinance services to

the financially excluded, particularly in under-served areas of India, through, among other things,

the introduction of innovative financial products and fostering transparency and responsible

finance.

21. Progress towards the achievement of the project objective would be monitored using the

following indicators (refer also to annex 3):

Extent of outreach: Disbursements of loans by MFIs to their clients relative to the amounts of

financing borrowed from SIDBI

Breadth of outreach: Measured by growth rates within under-served areas

Operational sustainability: Measured by operational self sufficiency (OSS)

Responsible finance: Measured by the percentage of beneficiary MFIs disclosing

operational/ financial information on a Web-based information platform

3. Project components

22. The project will achieve its objective by: (i) supporting the expansion of financial

services, particularly in under-served states or under-served areas within states; and (ii)

facilitating responsible and sustainable growth through the provision of more patient capital,

including longer-term debt, equity and quasi-equity instruments with funding linked to

responsible finance actions (for example, actions on transparency, good governance, and CoC

adherence).

23. The project will use an incentive approach and link the three components (annex 5

provides the project costs) described below such that maximum additionality is attained, while

also addressing the key issues (see section A above) facing the Indian microfinance sector. The

incentive approach will involve the provision of appropriate financing instruments, access to

which would be conditional not just on satisfactory appraisal of the MFI based on a detailed

appraisal system (annexes 4 and 6 and the OM), but also based on case-by-case agreements with

MFIs on responsible finance or other actions on capacity improvement that they would need to

complete to ensure continued access to funding under the project. The incentive to be used will

be a commercially priced, but attractive funding product, such as a quasi-equity/subordinate

product, which is currently not available in the India market, but will help address equity-gap

issues for Indian MFIs. In return for access to this funding, the responsible finance or capacity-

building actions could include commitments to increase MFI portfolios in under-served areas,

adoption of improved governance practices, reporting to an information platform, initiating a

CoC Assessment, and adoption of improved accounting practices where relevant. Through this

link between a financing component and a responsible finance component, project funding will

seek to contribute to the objectives of promoting sustainable and more responsible finance.

13

Component 1. Scaling Up Funding Support for MFIs (~US$290 million plus US$30 million

counterpart funding)

24. This component would provide funding for MFIs to scale up their operations. Funding

from SIDBI to MFIs is proposed to be structured as debt or quasi-equity to support their

operations and growth, enhance their financial strength, and enable them to leverage and crowd

in private commercial funds to on-lend larger amounts to the under-served. Limited equity

support would also be considered from SIDBI to MFIs. The funding provided under this

component to MFIs would be on commercial terms. The total funding thus mobilized will

enhance MFIs‘ ability to reach out to larger numbers of under-served segments of the population

through microfinance services. In particular, the quasi-equity/equity funding will also help

address the equity gap in Indian MFIs, while providing SIDBI with the leverage to promote the

responsible finance agenda among the MFIs funded.

25. Two kinds of leverage would be sought to be derived from such funding:

(i) Financial leverage: Equity or quasi-equity would lead to 6-7 times leverage through

raising of additional debt which would contribute to significantly enhanced on-lending,

while a 4-5 year debt from SIDBI to MFIs would lead to a roll-over of around 3-4, in

terms of on-lending to final clients. Funding that is structured as quasi-equity or equity

will obtain leverage or crowding in through the MFIs raising additional debt and also

through future mobilization of additional equity. This will help create strong institutions

that are viable and able to attract and access the capital market and private sector

investors in the medium to long term, ensuring that their growth sustains beyond the

project period.

(ii) Responsible-finance leverage: As discussed above, funding to MFIs would be linked to

performance criteria and actions revolving around greater transparency, responsible

expansion, accountability, growth in under-served areas, disclosure, and good governance

in the microfinance sector, thereby contributing to a responsible finance initiative, an

activity supported under Component 2 of the project (see also annex 4).13

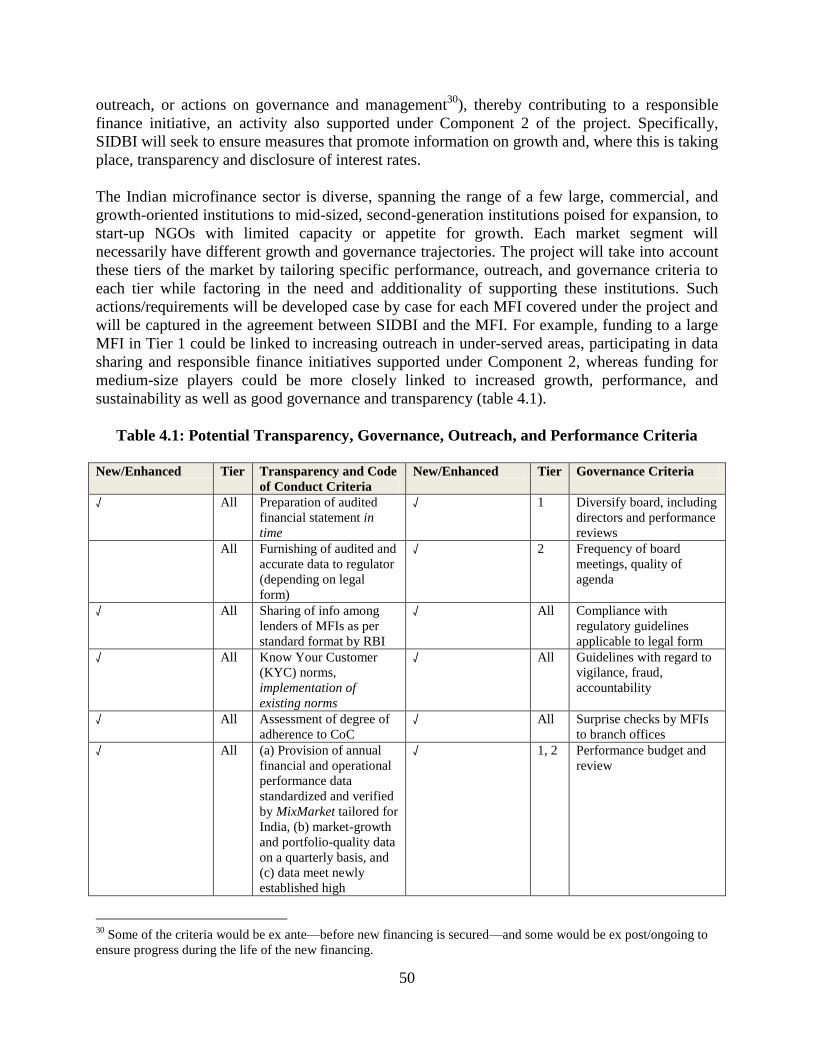

26. The Indian microfinance sector is diverse, spanning the range of a few large, commercial,

and growth-oriented institutions to midsized, second-generation institutions poised for

expansion, to start-up non-governmental organizations (NGOs), with limited capacity but an

appetite for growth. Each market segment will necessarily have different growth and governance

trajectories. The project takes into account these tiers of the market by tailoring specific

performance, outreach, and governance criteria to each tier while taking into account need and

additionality of supporting these institutions. For example, funding to a large MFI in Tier 1

would be linked to increasing outreach in under-served areas and participating in data sharing

and responsible finance initiatives supported under Component 2, whereas funding for medium-

size players would be more closely linked to increased growth, performance, and sustainability,

as well as good governance and transparency. The tiers and proposed performance criteria are

further discussed in annex 4.

13

Some of the criteria would be ex ante—before new financing is secured—and some would be ex post/ongoing to

ensure progress during the life of the new financing.

14

27. This component will directly address the funding gap constraint, promote the responsible

finance agenda, and support the continuation of a diverse range of institutions. Further, this

component would help introduce a new and much-needed innovative financial product, priced

commercially, into the Indian microfinance market, the need for which is evident from overall

data on microfinance in India (figure 1) and was reiterated during stakeholder consultations.14

In

providing such funding, the project will place an emphasis on ―importing‖ established MFIs

from developed regions in India to initiate or expand operations in the less-developed regions of

the country, a strategy that has worked very well in some Bank projects (for example, a

microfinance project in Afghanistan). At the same time, the project will support the expansion of

a few smaller MFIs (Tiers 2 and 3), including those structured as NGOs and cooperatives, that

demonstrate a potential for growth.

Component 2: Strengthening Responsible Finance (US$5 million)

28. This component would promote transparency and responsible microfinance through the

development of an India microfinance platform. This initiative would be envisaged as a common

information platform for MFIs to provide and disseminate valuable information that would

inform policy makers, MFI managers, and funders (similar, but broader and deeper than the

information available on the MixMarket,15

including through potential collaboration with Mix

Market in India). As part of the responsible finance initiative, SIDBI will seek to bring together a

Lenders‘ Forum comprising key MFI funders to agree on common actions, including those on

transparency and good governance by MFIs. Additionally, once the Unique Identification (UID)

initiative of the GoI is ready for implementation, the forum will encourage MFIs to participate

and support the roll-out of this initiative, given its significant potential to improve transparency

and credit information. This component could also potentially support the development and

piloting of a CoC Assessment, which could serve as an innovative tool for measuring

performance of MFIs as pertaining to their CoC adherence. This component will be cross-linked

with Component 1, such that MFIs accessing Component 1 will need to commit to data sharing

on the common information platform and possibly other responsible finance initiatives that are

defined as performance criteria in the OM.

Component 3: Capacity Building and Monitoring (US$5 million)

29. Implementation support would include support to SIDBI for (i) implementing the project,

including operating expenses and costs of the monitoring (defined in annex 3 and elsewhere); (ii)

commissioning an impact evaluation (to be carried out through an external research agency); and

(iii) SIDBI‘s own capacity building. This component would also include support for a

communication strategy to help ensure that benefits from this intervention are shared with the

wider microfinance sector.

4. Lessons learned and reflected in the project design

30. In designing this project, the Bank has leveraged its experience with similar initiatives

around the world (in Afghanistan, Bangladesh, Bosnia, Mexico, Pakistan, and Russia, to name a

14

Equity investors, MFIs, their associations, NGOs, rating agencies, and advisory firms. 15

MixMarket is the leading global information database (www.mixmarket.org), managed by the Microfinance

Information Exchange (the Mix, www.themix.org), which was founded by the Consultative Group to Assist the Poor

(CGAP, a multi-donor consortium housed in the World Bank and part of its Financial Sector Network).

15

few) and with livelihoods/poverty-reduction projects in India. Additionally, the Bank has

extensive experience working with apex institutions and has incorporated lessons learned and

good practices associated with this institutional mechanism. The new model of Bank support

relies on institutions that on-lend at or near commercial rates or take equity positions that help

crowd in private sector funding and foster continued commercialization. In this model, SIDBI

leverages its position to play a role in nurturing the development of sustainable microfinance

providers by setting minimum standards and performance targets around transparency and

governance as well as more efficient financial management and internal controls.

31. The preparation team for this project included the Consultative Group to Assist the Poor

(CGAP) and the International Finance Corporation (IFC). During implementation, close links

will be maintained with other initiatives. For example, the IFC‘s Technical Assistance Advisory

Services is undertaking a market assessment to identify optimal modalities and capacity-building

needs to design and implement a credit reporting platform shared among the MFI community.

The project will closely coordinate with this initiative and possibly use the findings of the study

to feed into overall project implementation. A dialogue between IFC and SIDBI and potential

future collaboration have also been initiated and facilitated. The project is also highly

complementary to the IFC agenda, which focuses primarily on equity investments in

microfinance investment vehicles (which invest in MFIs).16

Component 1 funding will likely

expand the market for IFC and other investors looking at MFI investments through crowding in

from Tier 2 capital and stabilizing MFI balance sheets, making them more investor-worthy. The

responsible finance agenda has an enormous externality effect, where reputational risks are

lowered for the IFC, other investors, and the donor community.

32. The Bank has also started discussions and will continue to coordinate with the United

Kingdom‘s Department for International Development (DFID) as they implement the Poorest

States Inclusive Growth Program (PSIG). The Bank discussed the performance of the previous

DFID technical assistance (TA) project and also SIDBI‘s implementation of the SME project TA

component. In both cases, it is evident that SIDBI‘s capacity to deliver TA has developed

considerably. In any case, TA at the institutional level for MFIs would not be directly addressed

by the project; instead the project would leverage off the TA activities of programs such as the

PSIG that are being initiated through a consortium of institutions (including SIDBI) and would

focus much more on the simpler structure proposed by the project under Component 2.17

5. Alternatives considered and reasons for rejection

33. Regarding the choice of lending instrument, an FIL is deemed appropriate. The project is

designed to support SIDBI‘s funding to MFIs while assuming full credit risk. The project focuses

exclusively on the MFI sector, rather than supporting a broader range of financial intermediaries.

Although the project could have looked at other financial intermediaries for implementation,

given that the focus is on MFIs, which have steadily been growing in terms of becoming the

predominant players in the microfinance sector and that SIDBI is the main intermediary that

16

The project helped to initiate discussions between IFC-SIDBI. Potential linkages are being explored between IFC

and SIDBI in close coordination with the Bank. 17

The DFID PSIG plans to cover four states. The implementing agencies for PSIG are yet to be identified. Support

from IFC and CGAP could also be explored during implementation in providing MFI and sector capacity building.

16

lends to MFIs, the choice was natural. Although intermediaries such as banking correspondents

are not explicitly included, many MFIs are eligible to be banking correspondents. Also, there are

a number of ongoing initiatives (supported by the Bank and other donors) that support different

types of entities, such as rural cooperatives. Moreover, MFIs are now showing promise of being

able to deliver financial services on a much broader scale, and hence the project focuses on

MFIs.

34. A Development Policy Loan (DPL) instrument was also considered given the links

between the financing and the responsible finance policy actions. However, because the

implementing agency (SIDBI) is a corporate entity, the DPL instrument cannot be used.

C. IMPLEMENTATION

1. Partnership arrangements

35. The project is financed only by the Bank and funds from SIDBI, but there are several

other donors involved in the microfinance sector, including DFID, the Asian Development Bank

(ADB), and the German Development Bank (KfW). The Bank has consulted and made every

effort to ensure complementarities and close coordination will be facilitated by SIDBI, as it is an

implementing agency for most microfinance projects.

36. DFID‘s PSIG will be implemented by a consortium, in which SIDBI plays a critical role.

The design phase of the PSIG has been initiated, which will enable SIDBI to factor in the project

design and ensure maximum complementarities between the two projects. ADB‘s project focuses

on clients above the typical microfinance-client level in terms of loan size and will also be

implemented by SIDBI. The ADB project complements the Bank‘s project by focusing on clients

that are on the higher end of the spectrum of microfinance services. KfW is providing a line of

credit and some TA to SIDBI. This will support the traditional debt products that SIDBI has been

implementing and add funding to its main business line. KfW will also have a TA component

(around US$2.5 million) that will focus on capacity building, including supporting an

information platform that would allow SIDBI to interface with its MFI clients, developing a set

of benchmark indicators for performance monitoring, and supporting SIDBI in carrying out

systems and portfolio audits. All these activities are complementary to the Bank‘s project.

Efforts will be made to meet with donors during supervision missions to facilitate effective

coordination and communication during implementation.

2. Institutional and implementation arrangements

37. SIDBI, with its vast experience of microfinance in India, will be the implementing

agency for this project. Within SIDBI, the SIDBI Foundation for Micro-Credit (SFMC), which

has a dedicated and experienced microfinance team, will be responsible for implementation. The

current staffing of SFMC is around 45 officers, located in many locations. The central team is

based in Lucknow.

38. SIDBI is well placed to implement the project. It has been playing a catalytic role in

supporting the Indian microfinance sector particularly since 1999, when SFMC was launched.

Apart from being an important and responsive funder, SIDBI is also regarded as a leading

17

institution in the sector, as reflected in its involvement in the development of the broader sector

(for example, introduction of ratings and impact assessments, strengthening MFIs‘ capacity and

internal control systems) as well as in discussions of regulation-related issues. SIDBI‘s profile

has developed over the years and was facilitated through projects from 2000 to 2009 with the

International Fund for Agriculture Development (IFAD) and DFID. In both projects SIDBI was

the counterpart for the partners in the National Micro Finance Support Program (NMFSP).18

Given SIDBI‘s demonstrated capacity and track record in supporting the development of the

retail microfinance sector in India,19

the institution is ready to begin the second phase of the

development of the sector, which would address key issues listed above. SIDBI also makes for

an appropriate implementing counterpart for this project given its very good implementation

capacity, familiarity with development financing, and familiarity with Bank fiduciary and

safeguards requirements. SIDBI has done very well in implementing the World Bank‘s SME

Financing and Development Project (US$120 million), which has been recently scaled up

through additional financing (US$400 million).

39. SIDBI will be responsible for ensuring compliance of project activities to the fiduciary

arrangements for the project (annexes 7 and 8). To ensure that these functions are performed

efficiently and effectively, SIDBI will provide requisite additional staffing, where necessary.

Given its financial capacity and track record (see above and annex 9), SIDBI is well placed to

implement the project. Safeguards arrangements have been agreed with SIDBI (annex 10), and

SIDBI has the capacity to ensure compliance during implementation.

40. SIDBI is fully committed to enhancing transparency under the project. Besides the on-

demand disclosure of information, SIDBI has proposed to initiate proactive (suo moto)

disclosures that include the public disclosure of all key documents related to the project and,

more broadly, to its overall microfinance operations. SIDBI‘s website will highlight the project

(including project audit reports and financial management reports) and other microfinance-

focused activities. SIDBI intends to further enhance disclosures to fully comply with provisions

of the Right to Information (RTI) Act 2005 and will undertake capacity building of its staff,

including familiarization with RTI provisions through Component 3.

41. Components 2 and 3 may involve procurement of consultancies and training and goods.

Procurement will be undertaken by SIDBI in line with agreed procurement procedures for this

project (annex 8). For support in the implementation of Component 2, SIDBI will hire a firm

where required that can provide operational support for the responsible finance component. One

example of such support could revolve around supporting the information platform, where the

work would entail, among other things, collating and following up on data submission from

18

The main features of NMFSP were to provide customized, need-based packages of loans, grants, and to a lesser

extent, equity to partner MFIs to develop into large and sustainable institutions; capacity building of clients, MFIs,

and the sector; and capacity-assessment ratings and capacity-building needs assessments. All aspects of the program

were based on a market-driven, flexible approach for credit delivery with a focus on financial sustainability. The

program closed in March 2009 and reportedly received the highest rating possible from DFID‘s assessment of its

global microfinance program. 19 From the Forbes list of Top 100 MFIs, seven Indian institutions were included in the list—all of them partner

organizations of SIDBI—testifying to the high impact of SIDBI in supporting and nurturing the microfinance sector

in India.

18

MFIs, analyzing and cleaning the data and preparing comparative reports, maintaining the

website for disclosure of the information shared on the responsible finance initiative, developing

templates for reporting on this platform, and maintaining the platform.

42. An Operations Manual (OM) acceptable to the Bank has been prepared by SIDBI. The

OM includes, among other things, the agreed financial management (FM) and disbursement

arrangements; procurement arrangements; guidelines on Preventing and Combating Fraud and

Corruption in Projects Financed by IBRD Loans and IDA Credits (dated October 15, 2006); a

Governance and Accountability Action Plan (GAAP); and a detailed framework for the

continuous measurement and monitoring of outcomes (annex 3), a key element in ensuring

effective implementation.

43. Arrangements will be put in place to ensure adequate project supervision, covering

fiduciary and safeguards aspects, with semi-annual supervision missions. The supervision team

will draw on expertise from the Bank as well as external experts, where necessary. Meetings

with other concerned stakeholders engaged in microfinance, including donor agencies, will be

undertaken during supervision missions.

44. IBRD funds will flow to SIDBI, which will channel them for the project components.

IDA funding will flow to GoI, and from GoI to SIDBI for implementing project components.

Disbursements will be made on a reimbursement basis using interim unaudited financial reports

(IUFRs)—evidencing actual expenditures—prepared by SIDBI. IUFRs will be submitted on a

quarterly basis, but SIDBI would have the flexibility to seek reimbursement earlier than the

quarterly intervals by submitting reports for shorter periods. The disbursement percentage will be

a defined percentage of the gross expenditures as reported by SIDBI through the IUFRs.

Retroactive financing up to an amount of 20 percent of the total loan and credit amount may be

made available for all eligible expenditures in all components incurred after July 1, 2009. The

retroactive financing will be applied as follows: up to US$15 million will be drawn against the

IBRD loan and up to US$45 million equivalent will be drawn against the IDA credit.

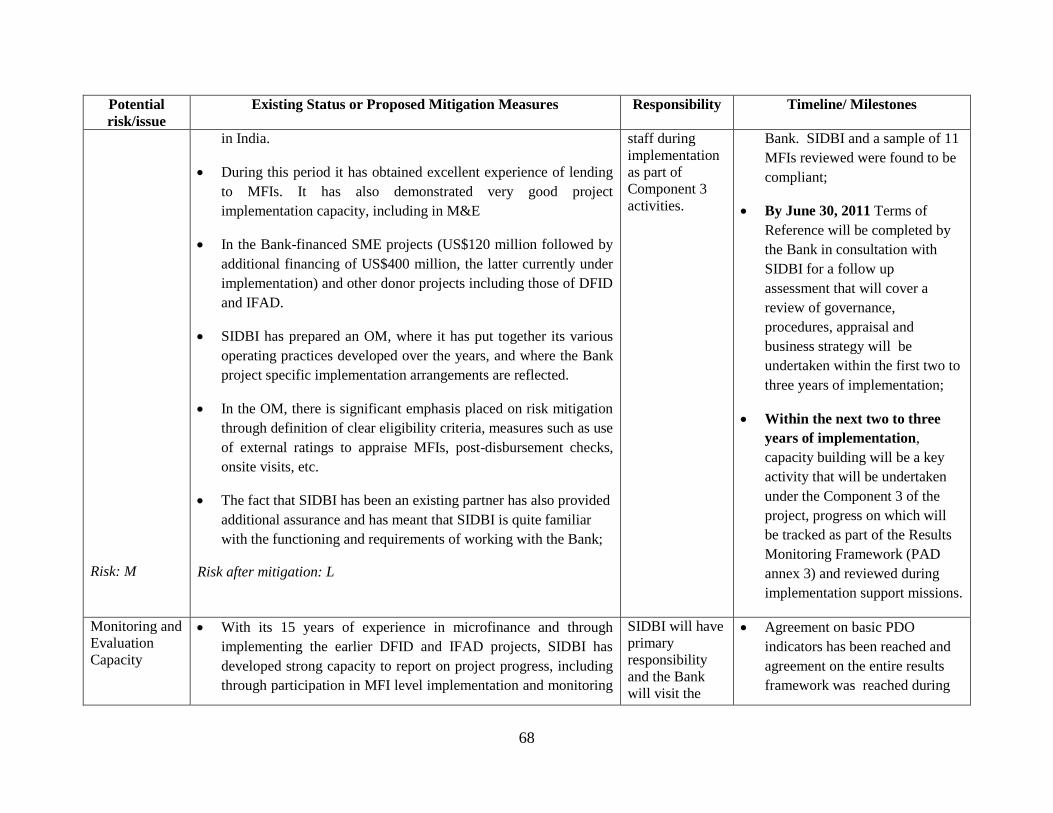

3. Monitoring and evaluation of outcomes/results

45. A strong monitoring and evaluation (M&E) framework to track inputs, outputs, and

outcomes in a systematic and timely fashion has been developed and agreed with SIDBI (annex

3). Project outcomes and outputs will be monitored through periodic reporting by SIDBI—which

has developed considerable capacity in monitoring through implementing the earlier DFID and

IFAD projects—and via project supervision using data from several sources, including (i)

reported data from SIDBI; (ii) data from MFIs; (iii) data collected by the agency that will be

responsible for the microfinance information platform; (iv) auditors; (v) Bank staff

implementation support missions; and (vi) the long-term impact assessment that will be

undertaken by an independent, external impact evaluation agency (under Component 3). The

Midterm Review (MTR) of the project will entail an update of an institutional assessment of

SIDBI/SFMC, including its management, its appraisal standards, and its portfolio and business

strategy for microfinance. Further, within the first two–three years of implementation, either as

part of the MTR or otherwise, an update of the corporate governance of SIDBI and a review of

governance issues in the project will be undertaken.

19

4. Sustainability

46. The sustainability of the project‘s outcomes, defined as scaling up sustainable and

responsible finance, will depend on how well the project is implemented by SIDBI in terms of

leveraging the funding component (Component 1) with the responsible finance component

(Component 2), while supporting SIDBI‘s capacity and project-implementation activities

(Component 3). Four factors bode well for ensuring sustainability of project outcomes: (i)

SIDBI‘s track record in the microfinance sector, in particular its pioneering role in Indian

microfinance and its successful implementation of past, large donor projects (DFID and IFAD);

(ii) SIDBI‘s commitment to the project structure with its incentive-based approach through links

between financing and responsible finance actions, as well as its commitment to implement this

project—as demonstrated by its active participation in the preparation of the project and

proactive approach to developing/researching the ideas that the project intends to support; (iii)

SIDBI‘s commitment to the microfinance sector as reflected in its annual reports, progress of

supporting the microfinance sector over time, and its business plan to increase staffing and focus

on this area over time; and (iv) GoI‘s strong commitment to promoting sustainable microfinance

and increasing the outreach of financial services to under-served areas/segments. GoI‘s

commitment is reflected in its various policy statements in support of the microfinance sector

and its support of this project.

47. Other factors that will have an impact on the sustainability of project outcomes relate to

the participation of other key stakeholders in supporting the project objectives. In particular,

participation of MFIs in Components 1 and 2 will be critical. This will be ensured through

linking access to funding in Component 1 to actions committed by each MFI under Component

2. Stakeholder consultations and individual meetings with MFIs have indicated that SIDBI—on

account of its position in the lending market and given the attractive long term funding, including

quasi-equity available under Component 1—will be able to derive sufficient leverage from

Component 1 in getting action on Component 2. The participation of other lenders in requiring

similar action as under Component 2 could also further bolster project sustainability, and the idea

of the Lenders‘ Forum in Component 2 will help facilitate this.

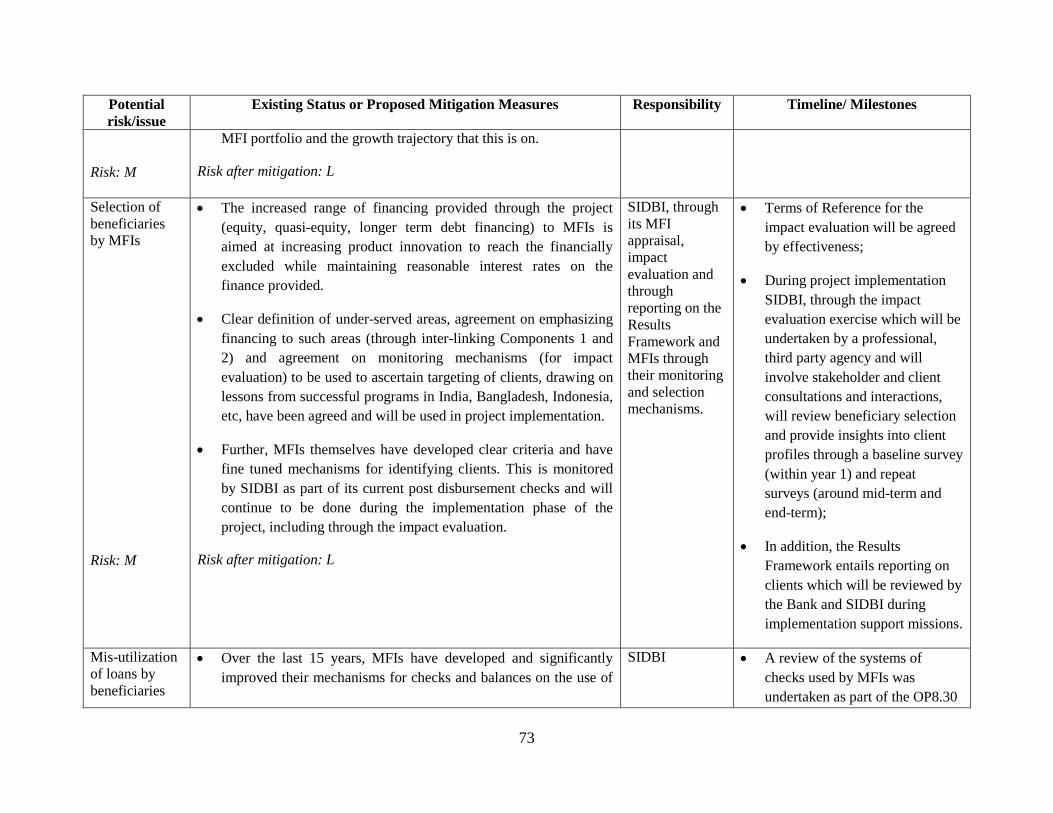

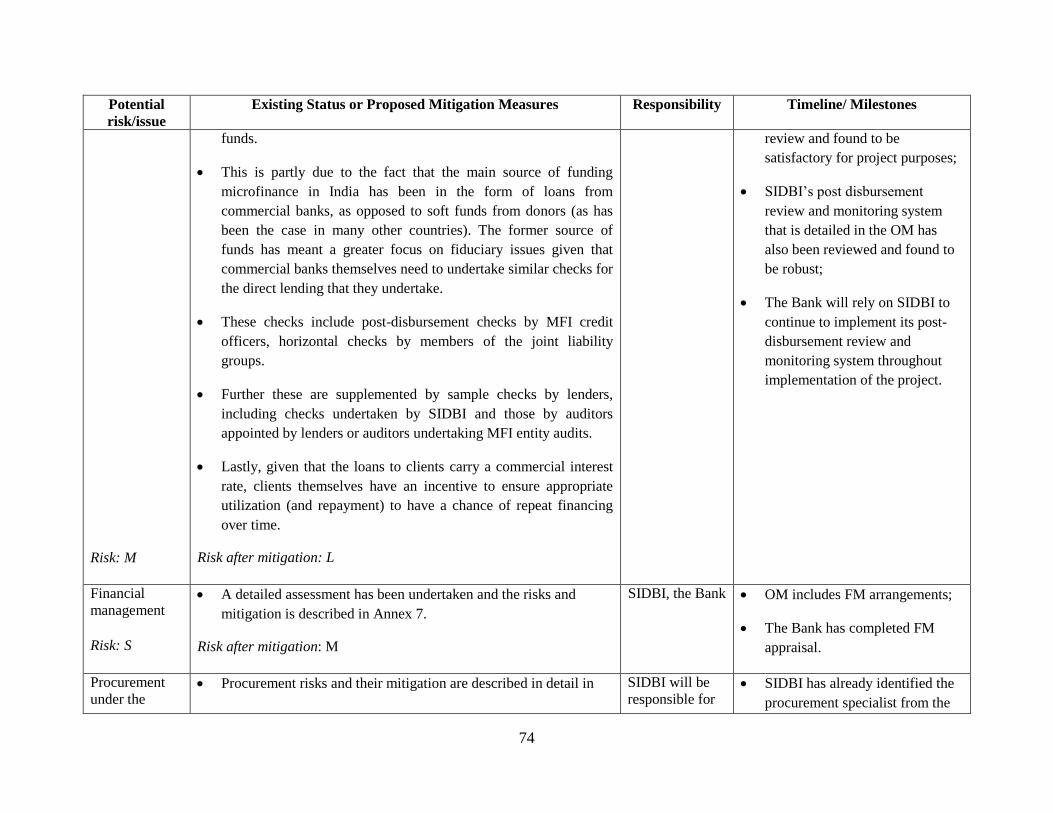

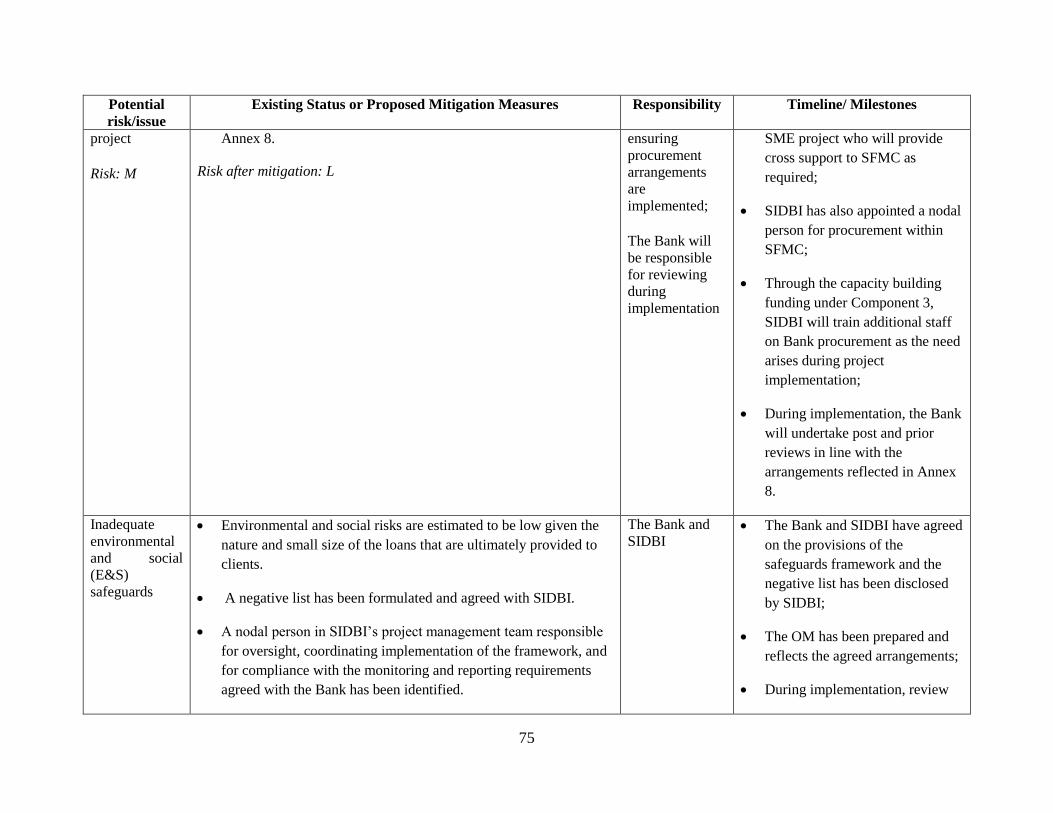

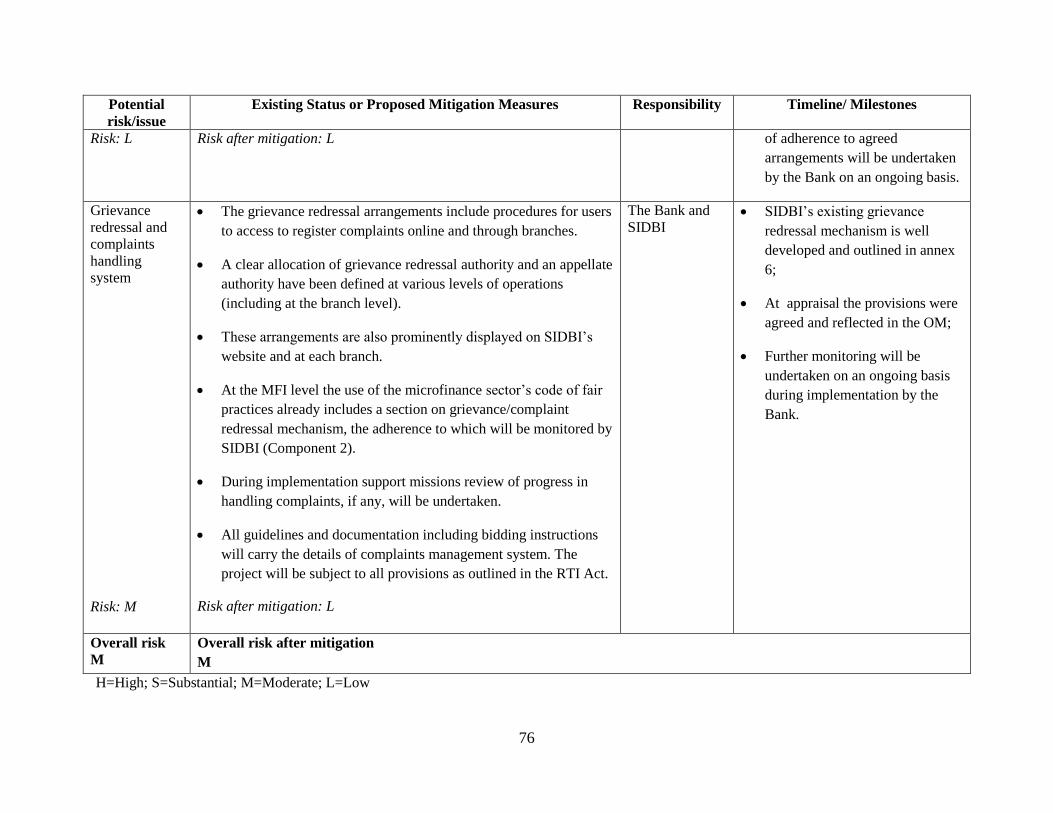

5. Critical risks and possible controversial aspects

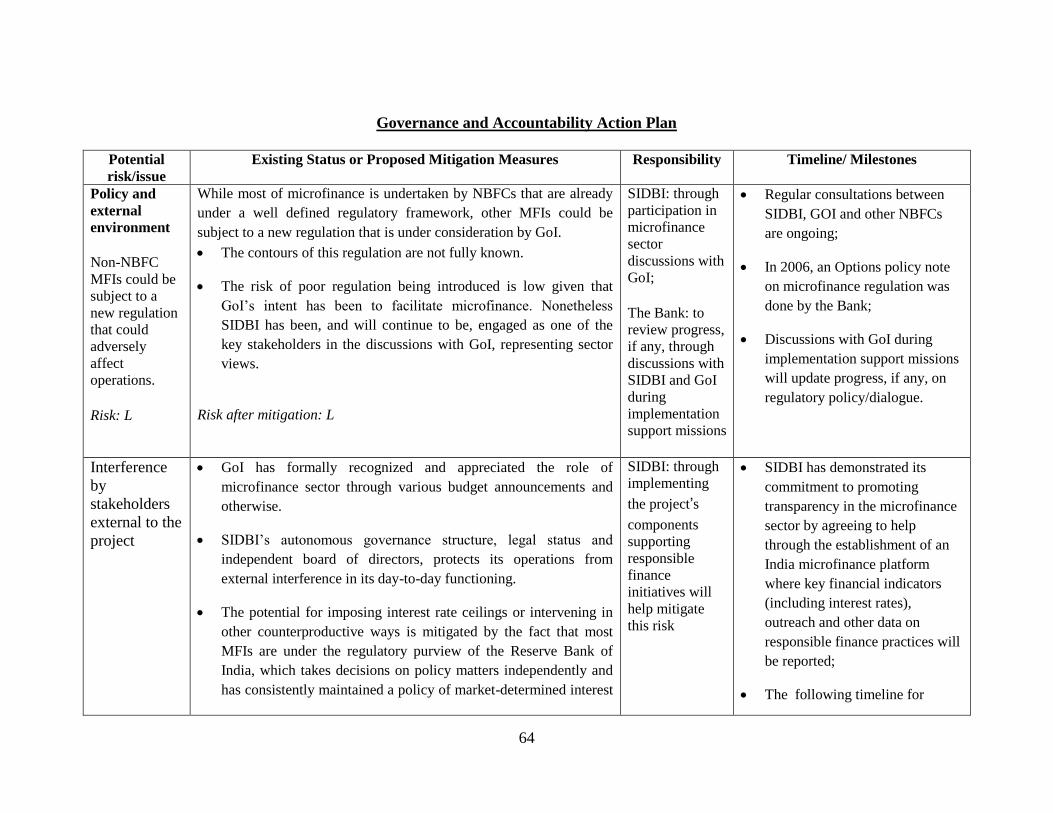

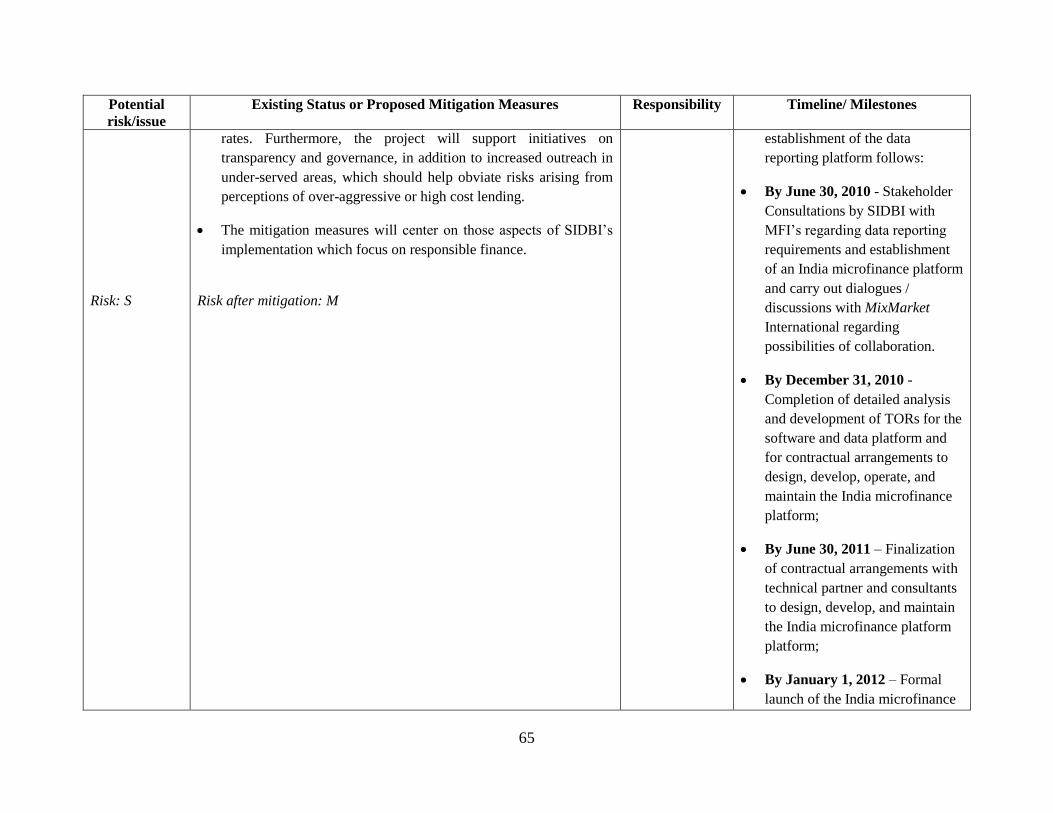

48. A detailed analysis of the potential risk areas and proposed or existing mitigation measures

was undertaken and is reflected in the GAAP (see annex 6; GAAP is also included in the OM). The

table below describes the potential risks, the degree of risks, the mitigation measures, and residual

risks. While overall risks are moderate, the following risks will need particular focus: (i) FM risks at

the MFI level; (ii) risks related to over-fast growth and lack of capacity of MFIs to handle this,

leading to fall in quality of lending by MFIs; and (iii) potential external interference in

microfinance. The GAAP includes mitigation measures and timelines/milestones for dealing with

these risks drawing significantly from Component 2, which focuses on responsible finance and

SIDBI‘s ongoing activities in the sector that help mitigate these risks. These risks will be reviewed

to determine how they may have changed during implementation and allow the team to focus

implementation support resources on the evolving risk areas.

20

Risks Risk

Rating

Risk Mitigation Measures Risk

Rating

with

Mitigation

To project development objective:

Selection of beneficiaries: Selection of

beneficiaries by MFIs could be subject to

―mission drift.‖

M Clear definition of under-served areas,

emphasizing financing to such areas (through

linking Components 1 and 2), and monitoring

mechanisms (for impact evaluation) to be used to

ascertain targeting of clients (drawing on lessons

from successful programs in India, Bangladesh,

Indonesia, and so forth) have been agreed and

will be used in project implementation. Further,

MFIs themselves have developed clear criteria

and have fine-tuned mechanisms for identifying

clients. This is monitored by SIDBI as part of its

current post-disbursement checks.

L

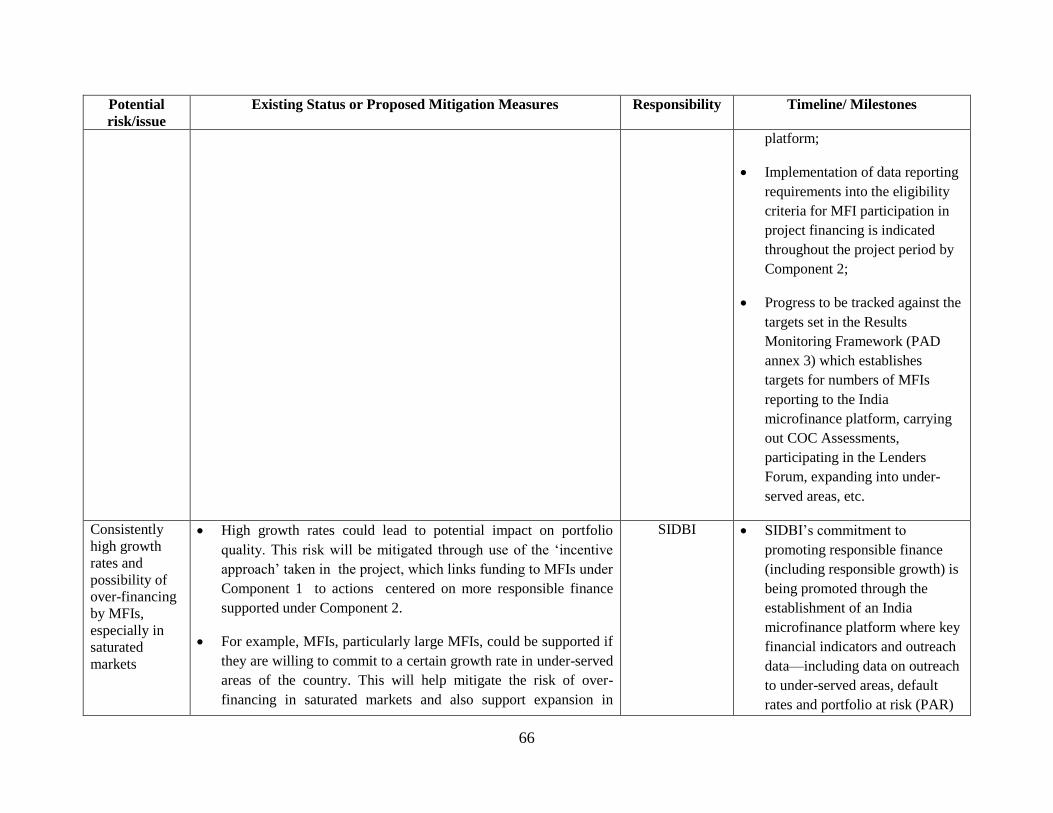

Overheated growth: Excessively high

growth rates and possibility of over-

financing by MFIs, especially in

saturated markets.

S

The risk of excessive growth will be mitigated

through use of the incentive approach taken in

the project, which links funding to MFIs under

Component 1 to actions centered on more

responsible finance supported under Component

2. For example, MFIs, particularly large MFIs,

could be supported if they are willing to commit

to a certain growth rate in under-served areas of

the country. This will help mitigate the risk of

over-financing in saturated markets and also

support expansion in under-served areas, which

will lead to more balanced growth. Further, MFIs

supported under the project will commit to share

information on their operations, financial

performance, outreach, branches, clients, interest

rates, and so forth to the information platform

that would be supported through Component 2.

M

External interference: Risks associated

with interference or loan forgiveness or

interest-rate caps. With rapid expansion

of the sector and anecdotes of over-

indebtedness, lack of transparency, and

client coercion, the sector could

potentially face instances of external

interference.

S GoI‘s current view of microfinance is well

understood. GoI has formally recognized and

appreciated the role of microfinance as

demonstrated through various budget

announcements and otherwise.

The potential for imposing interest-rate ceilings

or intervening in other counterproductive ways is

mitigated by the fact that most MFIs are under

the regulatory purview of the Reserve Bank of

India (RBI), which makes decisions on policy

matters independently and has consistently

maintained a policy of market-determined

interest rates.

M

To component results:

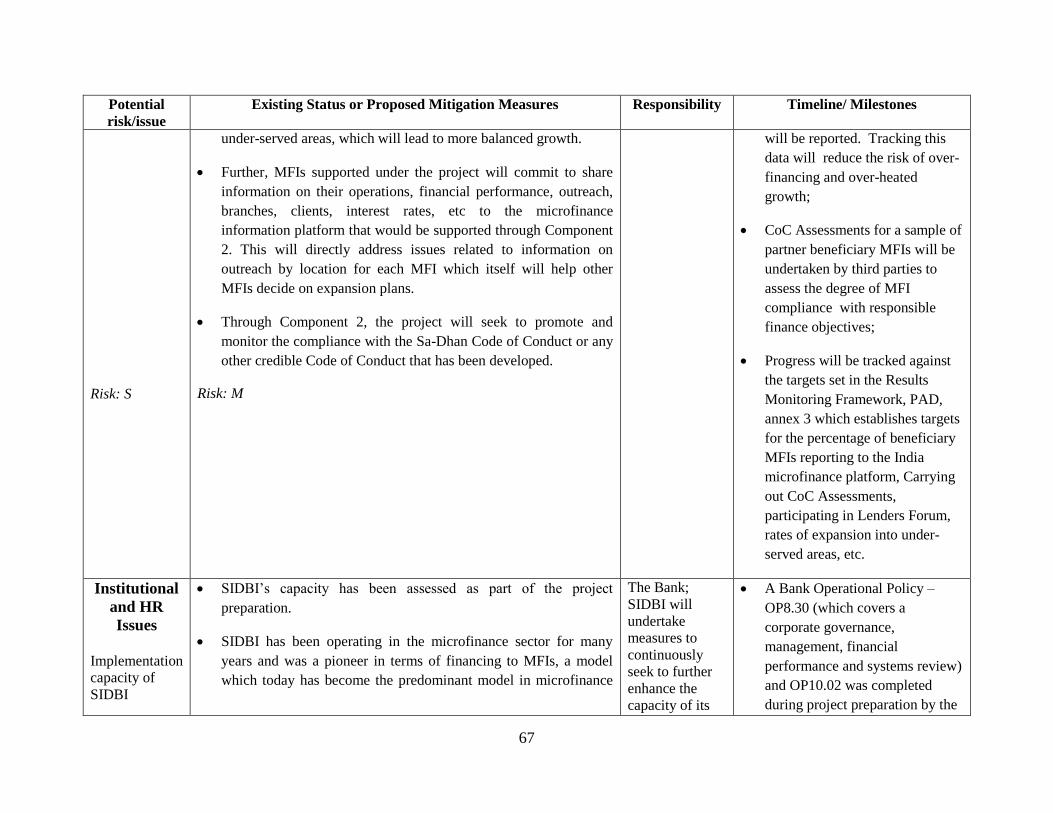

Effectiveness of project management

structure: Risks may arise from SIDBI‘s

oversight and regulation arrangements,

M SIDBI has been operating in the microfinance

sector for many years and was a pioneer in terms

of financing to MFIs, a model which today has

L

21

Risks Risk

Rating

Risk Mitigation Measures Risk

Rating

with

Mitigation

in case of insufficient institutional

capacity to handle the project activities,

in particular for the increased policy

advocacy and analysis roles envisaged

by SIDBI with TA support under this

project.

become the predominant model in microfinance

in India. During this period it has obtained

excellent experience of lending to MFIs. SIDBI

has put together its various operating practices

developed over the years into a Credit Manual,

which feeds into the Bank project‘s final, specific

implementation arrangements captured in the

OM.

Lack of capacity of MFIs: Risks may

arise from the lack of capacity of MFIs

in handling growth and carrying out the

project-supported activities.

S MFIs have demonstrated their capacity to

undertake microfinance activities at scale over

the past decade, as evidenced in the growth and

quality of financial and outreach indicators;

nonetheless, there are differing capacities. SIDBI

places considerable emphasis on assessing

capacity of MFIs to on-lend through the capacity

assessment ratings. Further, through Component

1, MFIs can use funding provided for quasi-

equity/equity for further capacity development, if

needed. Basic eligibility criteria have been

agreed, and the selection of MFIs under the

project is likely to center mostly on larger and

midsize MFIs (Tier 1 and Tier 2), which have

greater demonstrated capacity. Lastly, there are

sufficient other sources of funding for capacity

building (including self-funding).

M

Financial Management-Related Risks:

The FM risks may not be identified or

may not be adequately documented by

SIDBI during appraisal of MFI

proposals.

Weak FM systems of MFIs could impair

their capacity to provide fiduciary

assurance on usage of Bank funds and

keep track of a large number of end

beneficiaries.

Determination of mitigation measures

may be generic and/or a specific plan for

addressing the weaknesses and the

expected timeline may not be developed

and agreed upon between SIDBI and the

MFI. SIDBI may impose special

conditions on the MFIs in the terms of

sanction for addressing these

weaknesses, but in the absence of an

agreed plan to resolve issues,

benchmarking and measuring progress

made may be difficult.

S FM risk assessment of the applicant MFIs is done

by SIDBI during appraisal of the MFI proposals.

Identified critical FM risks are documented in the

Detailed Appraisal Note of SIDBI whereby this

process will be further strengthened.

Based on the critical risks or weaknesses

identified during MFI appraisal, SIDBI imposes

suitable conditions on the MFI to address these.

SIDBI‘s appraisal procedures require the

appraising SIDBI office to discuss these

weaknesses and obtain an undertaking from MFI

to satisfactorily address them. This specific

clause has also been included in the OM to cover

critical risks/weaknesses identified during

appraisal. SIDBI agrees to strengthen this further

and agree on a specific action plan with the MFI

to mitigate the identified critical, FM

risks/weaknesses, which will form part of the

Detailed Appraisal Note and the terms of

sanction.

System of monitoring progress of compliance

with the terms and conditions of sanction and

ensuring end use of funds is in place and

M

22

Risks Risk

Rating

Risk Mitigation Measures Risk

Rating

with

Mitigation

Assessment of the MFIs‘ FM systems in

terms of scalability of the operations

may not be accompanied by a strategic

plan to address the gaps.

Progress made by the MFI in the risk

areas including compliance with specific

condition/s imposed by SIDBI in the

sanction note may not be adequately

captured in the documents generated by

SIDBI during follow up and monitoring.

documented in the Credit Manual. SIDBI agrees

to further strengthen this system and ensure that

the compliance by the MFI of the agreed action

plan on FM risks is recorded appropriately.

Procedures for appraisal, selection and

monitoring of MFIs have been included in the

OM which has been agreed at negotiations. The

cases that will be brought under the project will

need to meet the minimum eligibility criteria

agreed with SIDBI and documented in the OM.

Compliance by SIDBI with the above

requirements will be reviewed and commented

on by the project external auditors and will be

reviewed by the Bank regularly.

Normal fiduciary risks of economy,

efficiency (and timeliness), transparency,

and fairness: Procurement will be

involved only in Component 2,

Strengthening Responsible Finance, and

in Component 3, Capacity Building and

Monitoring.

M For Components 2 and 3, a dedicated

procurement team in SIDBI will carry out all

procurement under the project. Capacity already

exists at SIDBI; a dedicated procurement

specialist responsible for implementation under

the Bank SME project will provide cross-support

to SFMC for the purposes of this project.

Supervision will be carried out periodically, and

Prior and Post Review Plans will be developed

and adhered to ensure procurement meets all

required standards of the project

With regard to MFI client-level procurement, the

project-preparation phase would ensure

significant vertical accountability mechanisms

exist—thorough checks undertaken by MFIs'

operational staff and their internal audit/control

team members, through external audits and

checks, including random checks undertaken on a

sample basis by SIDBI—as well as horizontal

accountability mechanisms driven by the

microfinance clients, where internal group-level

processes provide an additional oversight on the

use of funds and their recovery.

L

Inadequate environmental and social

(E&S) safeguards: Capacity at SIDBI to

address E&S safeguards.

L E&S risks are estimated to be low given the

nature and small size of the loans that are

ultimately provided to clients. A negative list has

been formulated and a nodal person in SIDBI‘s

project management team will be responsible for

oversight, coordinating implementation of the

framework, and for compliance with the

monitoring and reporting requirements agreed

with the Bank.

L

23

Risks Risk

Rating

Risk Mitigation Measures Risk

Rating

with

Mitigation

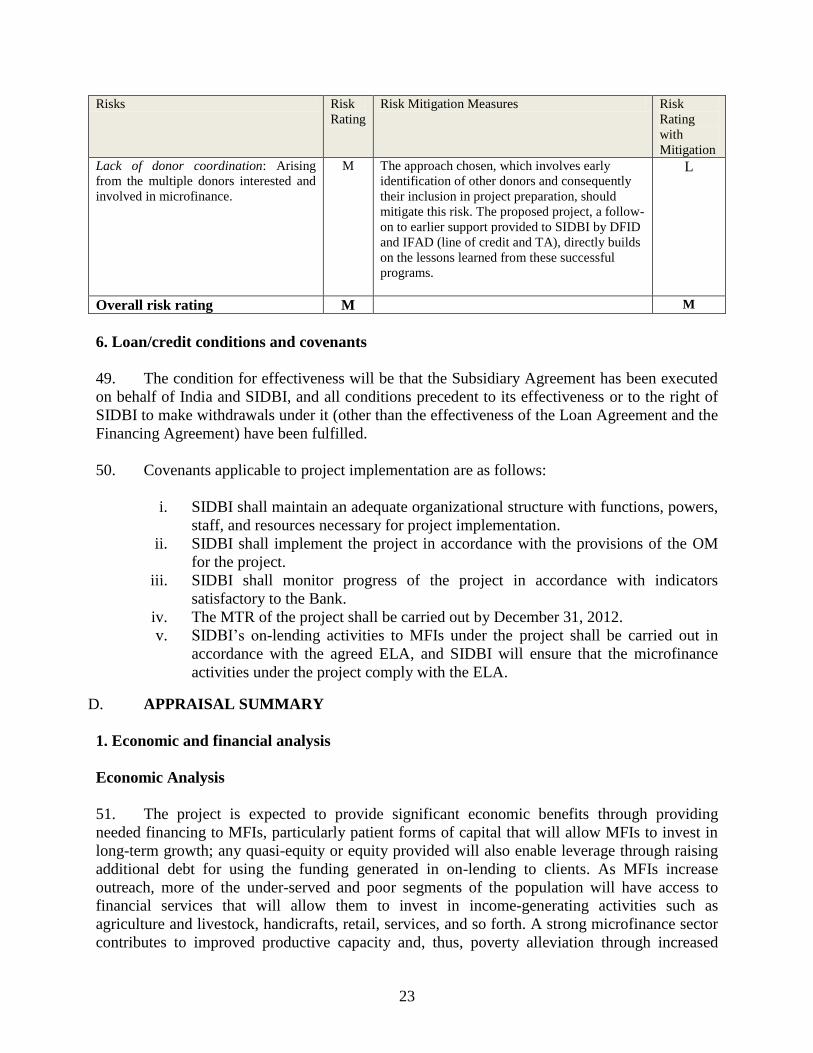

Lack of donor coordination: Arising

from the multiple donors interested and

involved in microfinance.

M The approach chosen, which involves early

identification of other donors and consequently

their inclusion in project preparation, should

mitigate this risk. The proposed project, a follow-

on to earlier support provided to SIDBI by DFID

and IFAD (line of credit and TA), directly builds

on the lessons learned from these successful

programs.

L

Overall risk rating M M

6. Loan/credit conditions and covenants

49. The condition for effectiveness will be that the Subsidiary Agreement has been executed

on behalf of India and SIDBI, and all conditions precedent to its effectiveness or to the right of

SIDBI to make withdrawals under it (other than the effectiveness of the Loan Agreement and the

Financing Agreement) have been fulfilled.

50. Covenants applicable to project implementation are as follows:

i. SIDBI shall maintain an adequate organizational structure with functions, powers,

staff, and resources necessary for project implementation.

ii. SIDBI shall implement the project in accordance with the provisions of the OM

for the project.

iii. SIDBI shall monitor progress of the project in accordance with indicators

satisfactory to the Bank.

iv. The MTR of the project shall be carried out by December 31, 2012.

v. SIDBI‘s on-lending activities to MFIs under the project shall be carried out in

accordance with the agreed ELA, and SIDBI will ensure that the microfinance

activities under the project comply with the ELA.

D. APPRAISAL SUMMARY

1. Economic and financial analysis

Economic Analysis

51. The project is expected to provide significant economic benefits through providing

needed financing to MFIs, particularly patient forms of capital that will allow MFIs to invest in