Embed Size (px)

Citation preview

DOCUMENT RESUME

ED 203 151 CE 029 293

TITLEINSTITUTIONPUB DATENOTE

Personal Finance Education Guide.Oregon state Dept. of Education, Salem.8180p.

EDRS PRICE MF01/PC04 Plus Postage.DESCRIPTOPS Adult Education: Behavioral Obiectives: Competence:

*Consumer Economics: *Consumer Education: *ConsumerProtection.: Credit (Pinancel: Economics: Emplovment:Tncome: Instructional Saterials: Learning Activf..tion:Legislation: Marketing: *Money Management;Purchasing

IDENTIFIERS *Consumer Skills: *Personal Finance Training

ABSTRACTThis guide is intended to assist curriculua planners

and classroom teachers in designing and implementing personal financeinstruction c meet a variety of student needs, interests, andabilities. It is organized under five concept areas: employment andincome, money manageeent, credit, purchase of goods and services, andrights and responsibilities in the marketplace. Each concept areacontains several subconcepts. Under each subconcept the goals arelisted at three levels of progressively greeter complexity along withsasple indicators of student performance. Classroom activities areaccompanied by an outline of program content. Topics covered in thefive concept areas include obtaining a lob: 'meting responsibilitiesfor iob success: employment law: financial security and employment:financial planning: banking and recordkeeping: savings; investments:let:Pa documents: insurance: taxation: credit availability, use,selection, and problems: consumer credit laws: factors affectingconsumer purchases: role of advertising: guidelines for shoppers: theU.S. economic system: rights and responsibilities of consumers andsellers: fraudulent and deceptive practices: sources of consumerassistance: and consumer legislation. (MNI

***********************************************************************Peproductions supplied by ?'DRS are the best that can be made

from the original document.***********************************************************************

111rlreN rePN044_

.NOL.L.1

PERSONAL FINANCEEDUCATION GUIDE

Spring 1981

Verne A. DuncanState Superintendent of

Public Instruction

Oregon Department of Education700 Pringle Parkway SE

Salem, Oregon 97310

U.S DEPARTMENT OF HEALTH.E DUCATION &WELFAREN ATIONAL INSTITUTE OF

EDUCATION

"PERMISSION TO REPRODUCE THISMATERIAL HAS BEEN GRANTED BY

THIS DOCUMENT HAS SEEN REPRO- S. J. Cava.-()DUCE EXACTLY AS RECEIVED FROMTHE PERSON OR ORGANIZATION ORIGIN-ATING IT POINTS OF VIEW OR OPINIONSSTATED DO NOT NECESSARILY REPRE-SENT OFFICIAL NATIONAL INSTITUTE Of TO THE EDUCATIONAL RESOURCESEDUCATION POSIT ION OR POLICY 1) INFORMATION CENTER (ERIC)."

L.

Federal law prohibits discrimination on the basis of race, color or national origin (Title VI of the Civil Rights Act of 1964); sex(Title IX of the Educational Amendments of 1972 and Title II of the Vocational Education Amendments of 1976); or handicap(Section 504 of the Rehabilitation Act of 1973) in educational programs and activities which receive federal assistance. Oregonlaws prohibiting discrimination include ORS 659.150 and 659.030. The State Board of Education, furthermore, has adoptedOregon Administrative Rules regarding equal opportunity and nondiscrimination: OARs 581-21-045 through -049 and OAR581-22-505.

It is the policy of the State Board of Education and a priority of the Oregon Depirtment of Education to ensure equalopportunity in all educational programs and activities and in employment. The Department provides assistance as neededthroughout the state's educational system concerning issues of equal opportunity, and has designated the following asresponsible for coordinating the Department's efforts:

Title IIVocational Education Equal Opportunity SpecialistTitle VIEqual Education and Legal SpecialistTitle IXAssociate Superintendent, Educational Program Audit Division and Equal Education and Legal SpecialistSection 504Specialist for Speech, Language and Hearing, Special Education Section

Inquiries may be addressed to the Oregon Department of Education, 700 Pringle Parkway SE, Salem 97310 or to the RegionalOffice for Civil Rights, Region X, 1321 Second Avenue, Seattle 98101.

Copyright 1981

3559219815000 3

it

contents

Foreword v

Acknowledgments vii

Introduction 1

Implementation 7

Assessment 11

Employment and Income 13

Obtaining a Job 14Meeting Responsibilities for Job Success 16

Employment Organizations 18Employment LawFederal and State 20

Money Management 23

Financial Security and Employment 24Financial Planning 26Banking and Recordkeeping 28Savings 30Investments 32

Insurance 34

Legal Documents 36Taxation 38

Credit 41

Availability and Use 42Credit Selection 44Credit Problems 46Consumer Credit Laws 48

Purchase of Goods and Services 51

Factors Affecting Consumer Purchases 52Role of Advertising 56Guidelines for Shoppers 58Making Specific Purchases 62

Rights and Responsibilities in the Marketplace 67

The U S Economic System 68Rights and Responsibilities of Consumers and Sellers 70Fraudulent and Deceptive Practices 72Sources of Consumer Assistance.. 74Consumer Legislation 76

111

foreword

Since the costs of transportation, utilities, housing and food continue to escalate at an unprecedentedrate, students must be able to make informed choices in managing their personal resources. For thisreason, the study of personal finance is of vital interest to everyone.

This Personal Finance Education Guide is intended to help students develop a framework forand "standing the day to day marketplace economy. The guide, as part of the ongoing effort to achieveexcellence in education, is designed so that teachers may tailor instructi m according to student needsand abilities. In this way, they will help students satisfy immediate needs, while encouraging theinvestigation of the more complex and subtle issues of consumer decisions.

The development of this guide represents the combined efforts of business, labor and others. Whilethey find themselves to be competitors in the marketplace, together they developed a documentspeaking to the diversity which is characteristic of the economy. It is this kind of involvement andcooperation, the community working together, that helps to achieve an L11 nnce for excellence ineducationproviding students with the best that education has to offer.

For further information, contact Marian Kienzle, Specialist, Consumer Education and PersonalFinance, 378-3816, or toll free in Oregon 1-800-452-7813.

Verne A. DuncanState Superintendent ofPublic Instruction

v

acknowledgments

This guide was revised through the efforts of business and industry, government, and labor represent-atives working with classroom teachers and university staff. Their purpose was to provide current andaccurate information needed by the consumer to function responsibly in the marketplace.

Particularly helpful was research conducted by Margaret Stamps ("An Analysis of the Acceptance andthe Conceptual Clustering of Personal Finance Competencies as Identified by the Business Commu-nity and Personal Finance Teachers," Oregon State University, 1979), and by Gregory Breuner ("ASurvey of Personal Finance Curriculum in Oregon Secondary Schools," Oregon State University,1978).

Special thanks to the Personal Finance Advisory Committee members, the Economics Education TaskForce, the Personal Finance Cadre, and the Consumer Protection Division of the Oregon Departmentof Justice, for advising and assisting during the revision process.

6vii

introduction

Preparing students to participate successfully in the United States economic system is a vital part ofbasic education. This publication presents guidelines to help schools develop a curriculum in personalfinance which meets student and community needs.

Financial concerns of consumers and the relationship to basic economic concepts are the focus of thisPersonal Finance Education Guide. Personal finance is the area of study that relates those basicconcepts and practices to the financial concerns of consumers. Economics, by way of contrast, isdefined as the study of how limited resources are allocated to meet unlimited needs and wants. InOregon, students are required to study in both content areas in order to earn a diploma.

This guide is intended to assist curriculum planners and classroom teachers in designing andimplementing personal finance instruction which meets a variety of students' needs, interests andabilities. It is organized under five concept areas (with corresponding program goals): employment andincome, money management, credit, purchase of goods and services, rights and responsibilities in themarketplace. Within each concept area are several sections, or subconcepts. Under each subconcept,such as Financial Planning, Aix course goals are listed at three levels of progressively greatercomplexity along with sample indicators of student performance. Classroom activities are accom-panied by an outline of program content. In addition, the level that most students can be expected toattain is identified with an asterisk.

A bank of test items, now under development, provides the teacher with easy access to appropriatemeasures. Items are organized according to levels of difficulty.

Due to the rapidly changing nature of the subject, a separate personal finance resource list isavailable from the personal finance specialist at the Department of Education.

State Standards

Statewide goals for Oregon schools are presented in OAR 581-22-201:

(1) The Board, in response to the changing needs of Oregon learners, sets forth six goalsfor the public schools.

(2) Conceived and endorsed by Oregon citizens, the statewide goals are designed to assurethat every student in the elementary and secondary schools shall have the opportu-nity to learn to function effectively in six life roles: INDIVIDUAL, LEARNER,PRODUCER, CITIZEN, CONSUMER and FAMILY MEMBER. . . .

(3) The statewide goals shall be implemented through the district, program and coursegoals of each local school district. . . .

The State Board of Education's Standards for Oregon Schools contain certain requirements whichrelate directly to personal finance and economic education in Oregon. According to OAR 581-22-211:

Each school district shall maintain a coordinated K/1-12 instructional program based on:

(1) District goals adopted by the district school board and consistent with the goalsadopted by the State Board;

(2) Program goals consistent with goals adopted by the State Board;

1

(3) Competence requirements for graduation; and

(4) Course goals.

In addition, as partial fulfillment, of the state graduation requirements listed in OAR 581-22-316,students must earn one unit of credit in personal finance and economics. According to OAR 581 -22-102, a "unit of credit" is defined as "certification of a student's successful completion of classroom orequivalent work . . . in a course of at least 130 clock hours."

Goal-Based Planning

Goals give purpose and direction when planning activities and they provide a common language fordiscussing the merits of activities as they are carried out. As a reference for planning, districts usestate goals, district goals, program goals, course goals.

State goals describe what the Oregon Department of Education thinks a student ought to learn inpublic school. District goals describe what the local community and its schools think a student ought tolearn in school locally, and how such learning relates to state goals. Program goals describe what localcurriculum planners and teachers think a student ought to learn in personal finance and economiceducation and how such learning relates to district goals. Course goals describe what teachers think astudent ought to learn in personal finance and economics and how such learning relates to programgoals.

Competence Requirements

Competence is a separate but related part of goal-based planning. It is one of three graduationrequirements.* While districts plan and evaluate instruction by means of goals, minimum require-ments for graduation are based on credit, attendance and competence.

Competence means being capable, and students indicate competence by demonstrating their knowl-edge and skills. Districts verify student competence through the local list of indicators of competence(what many people have called "competencies").** Districts generally have developed indicators ofcompetence for the "consumer" in four areasreading, writing, mathematics and reasoning. Howev-er, the curriculum may be developed for all six by adding listening and speaking to the requiredcompetence areas.

*OAR 581-22-316**See Competence Guide list, Standards Guidelines: Competence Requirements (Salem: Oregon Department of Education.

1980), page 2.

2

For example, in personal finance:

INDIVIDUAL

STATE GOALS FOR OREGON LEARNERS

LEARNER PRODUCER CITIZEN CONSUMER

DISTRICT GOAL

Stude. its will know how the use ofpersonal resources affects and is af-fected by our economic system.

PROGRAM GOAL

Students will be able to make finan-cial decisions which contribute to fi-nancial stability and personal satis-faction.

COURSE GOALSSECONDARY

9-12

The student will be able to judge theimpact of financial planning onmoney management and economicsecurity.

FAMILYMEMBER

COMPETENCE REQUIREMENTS ANDRELATED INDICATORS

A Readeg, Following a reading assignment, distin-guish between fixed and flexible expenses.

B Writeeg, Describe ways financial planning helpsto budget resources.

C Matheg, Prepare budgets for different incomelevels, using percentages for variousexpenditures.

D Speakeg, In a presentation to the class, point outways in which financial planning helpsindividuals and families in specific situa-tions.

E Listeneg, Following a classroom presentation, liststeps in planning a budget.

F Reasoneg, Justify the need for financial planningin specific situations.

It is important that teachers providing personal finance and economics instruction be directlyinvolved in developing district, program and course goals so that their curriculum is coordinated withother subject areas.

When developing program and course goals, it should be pointed out that personal finance and

*These are sample performance indicators taken from 2.2 Financial Planning, page 26. Districts may adapt any of theperformance indicators as indicators of competence.

3

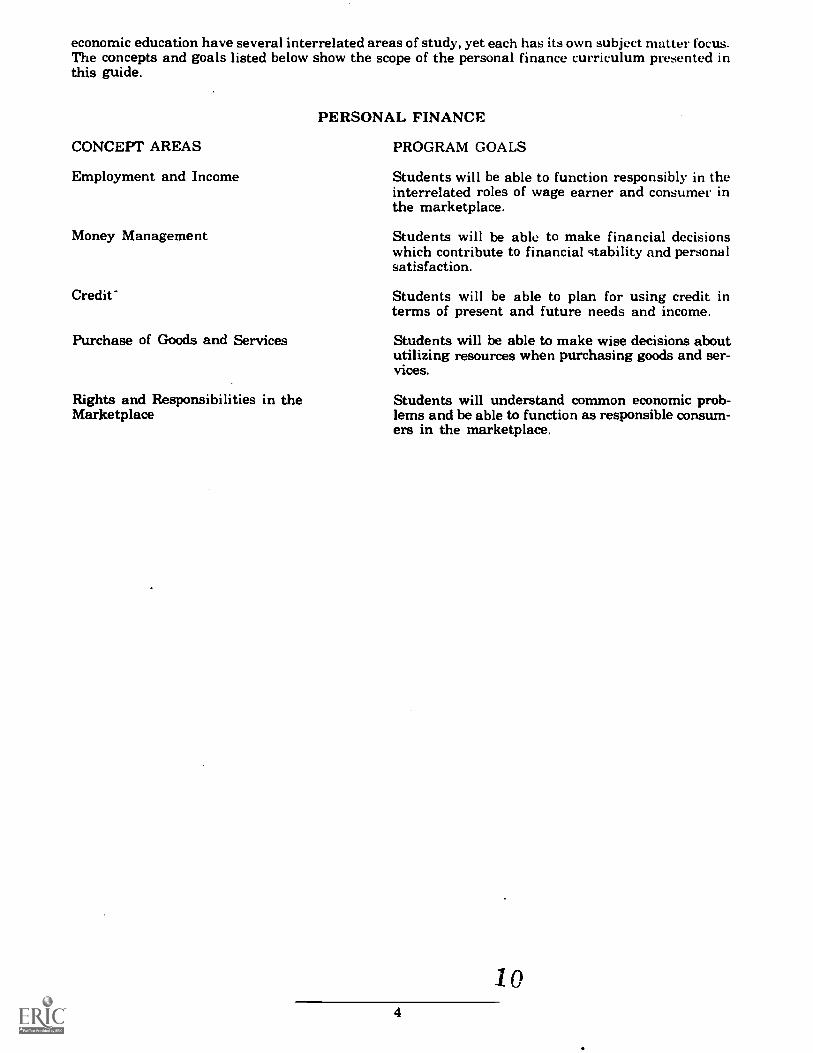

economic education have several interrelated areas of study, yet each has its own subject matter focus.The concepts and goals listed below show the scope of the personal finance curriculum presented inthis guide.

CONCEPT AREAS

Employment and Income

Money Management

Credit"

Purchase of Goods and Services

Rights and Responsibilities in theMarketplace

PERSONAL FINANCE

PROGRAM GOALS

Students will be able to function responsibly in theinterrelated roles of wage earner and consumer inthe marketplace.

Students will be able to make financial decisionswhich contribute to financial stability and personalsatisfaction.

Students will be able to plan for using credit interms of present and future needs and income.

Students will be able to make wise decisions aboututilizing resources when purchasing goods and ser-vices.

Students will understand common economic prob-lems and be able to function as responsible consum-ers in the marketplace.

104

The following table illustrates how personal finance reinforces various concepts in economics.

Personal Finance Curriculum Economic Concepts

cr)Z rx1 i5 xec.) 4 L.), w 0 2 o .i 2 . ....E 4., Cl)

1-4 1-2 cr-:°1-gi 0 E-' 0 °710,E-4 ow a <4r o 0:,.:42 E st.'zr=, z,;), oo-9, ce, zrxic iioz 0 uDalcd 2 °' 2 ozW 0 W

i tlt Q

c..) OCEI) Z

cd )

44 A

EMPLOYMENT AND INCOMEObtaining a Job 0 0Meeting Responsibilities for Job Success 0 0 XEmployment Organizations 0 0Employment LawsFederal and State 0 0

MONEY MANAGEMENTFinancial Security and Employment 0 X X XFinancial Planning X X X XBanking Services and Financial Records 0 Xsavings 0 X XInvestments 0 X XInsurance 0 XLegal Documents 0Taxation X 0 X

CREDIT

Credit Problems0

XCredit Selection

0Consumer Credit Laws 0

XCredit Availability and Use 1 0

PURCHASE OF GOODS AND SERVICESFactors Affecting Consumer Purchases X X X 0 XThe Role of Advertising 0 XGuidelines for Shoppers x o o xMaking Specific Purchases 0 X X

RIGHTS AND RESPONSIBILITIES IN THE MARKETPLACETheU S Economic System 0 X X 0 XRights and Responsibilities of the Consumers/Sellers X X X XFraudulent and Deceptive Practices 0Sources of Consumer Assistance 0 X 0Consumer Legislation X 0 0

0 - Indicates minor emphasis.X - Indicates major emphasis.

implementation

According to State Board of Education commentary on OAR 581-22-316: "Personal Finance andEconomics - Each student will study materials in both content areas . . . districts may develop variousofferings designed to meet the needs of students, but in all cases the content must be directlyidentified with personal finance and economics." This commentary was dev loped to further clarifyrule language as well as the Board's intent when adopting the rule.

While the personal finance and economics requirement calls for study in both content areas, it does notdefine the amount or proportion of time for either. There are a number of ways to meet the creditrequirement. Personal finance could be integrated in varying degrees with economic education; eitherpersonal finance or economic education could be the major focus. Personal finance and economicscould be taught as a single course or a series of courses, or through separate courses.* Even whentaught as part of other instructional programs, such as business education, home economics,mathematics, and social studies, program goals and course goals must be developed for personalfinance and economics.

RECOMMENDED STEPS IN ESTABLISHING A PERSONAL FINANCE CURRICULUM

STEP 1 DETERMINE LOCAL DISTRICT NEEDS.

Review state standards and curriculum guidelines.

Establish community review process utilizing the serv:er.,- of:

advisory committees,curriculum committees,student, parent, teacher groups.

Analyze economic data, trends and needs in the local area.

Research resources available in the community.

Compile information about local needs as a basis for program development.

STEP 2 SECURE ADMINISTRATIVE AND SCHOOL BOARD SUPPORT.

Coordinate district goals for personal finance with program development at the schoollevel.

Determine course of study in light of total curriculum offerings:

*With the first approach, no specific subject endorsement for certification is required; with the latter, the economics teachermust hold a social studies endorsement.

7 2

program goals*,staff assignment and training,budgetary support,assessment and evaluation.

Assign administrative liaison to local school(s.

STEP 3 ASSIGN LOCAL SCHOOL COORDINATOR.

Designate a person responsible for coordination and establish responsibilities.

STEP 4 ANALYZE CURRENT OFFERINGS.

Review required and elective offerings with similar curriculum content.

Determine which offerings have a direct correlction in terms of content, such as CareerDevelopment.

Establish general guidelines for implementation model based on current offerings,staffing, facility availability, and district-level decisions.

STEP 5 IDENTIFY TEACHING STAFF.

Select staff who are interested in teaching personal finance and economics.

Utilize staff with certification endorsements in business education, home economics,mathematics or social studies, when possible.

STEP 6 DEVELOP CURRICULUM DESIGN.

Write plenned course statements, including course goals which are based on programgoals.

Establish implementation model, including the grade levellt at which it will be offered.

Determine performance requirements. activities and resources for the program.

Review the basic design to assure that individual student needs, interests and abilities areconsidered.

Develop options for students with special needs, including identifying materials andresources for independent study or research, and for bilingual students.

STEP 7 PROVIDE STAFF INSERVICE AND PROFESSIONAL GROWTH OPPORTUNITIES.

Establish a separate budget, including funds for professional growth opportunities, ifpossible.

Identify individual staff needs and interests through staff inservice.

Determine what inservice opportunities are already available.

Provide staff inservice and coordination opportunities,

Establish a procedure for training new stuff on an annual basis.

STEP 8 DEVELOP EVALUATION PROCEDURES.

Determine means for assessing individual student progress.

Experionco. hum mhown that it 101 prfuruble. for cliodriou 111 111W4114) *ondo *mu of ',nostrum 0(11111s for porsonssl (limner andormoom irs odurou Inn.

13$

Establish evaluation procedures for instruction, including analysis of curriculum develop-ment by staff on an annual basis.

STEP 9 IMPLEMENT INSTRUCTIONAL OFFERINGS.

Establish timeline for implementation or revision.

Coordinate implementation plans with the revie.% Lind acquisition of resources.

STEP 10 ESTABLISH RE-EVALUATION AND REVISION PROCEDURES.

Determine timeline and cycle for review and evalL

Coordinate re-evaluation and revision of design with other associated curriculum areasand in light of staff work load assignments.

Review instructional materials on a regularly-scheduled basis.

9 14

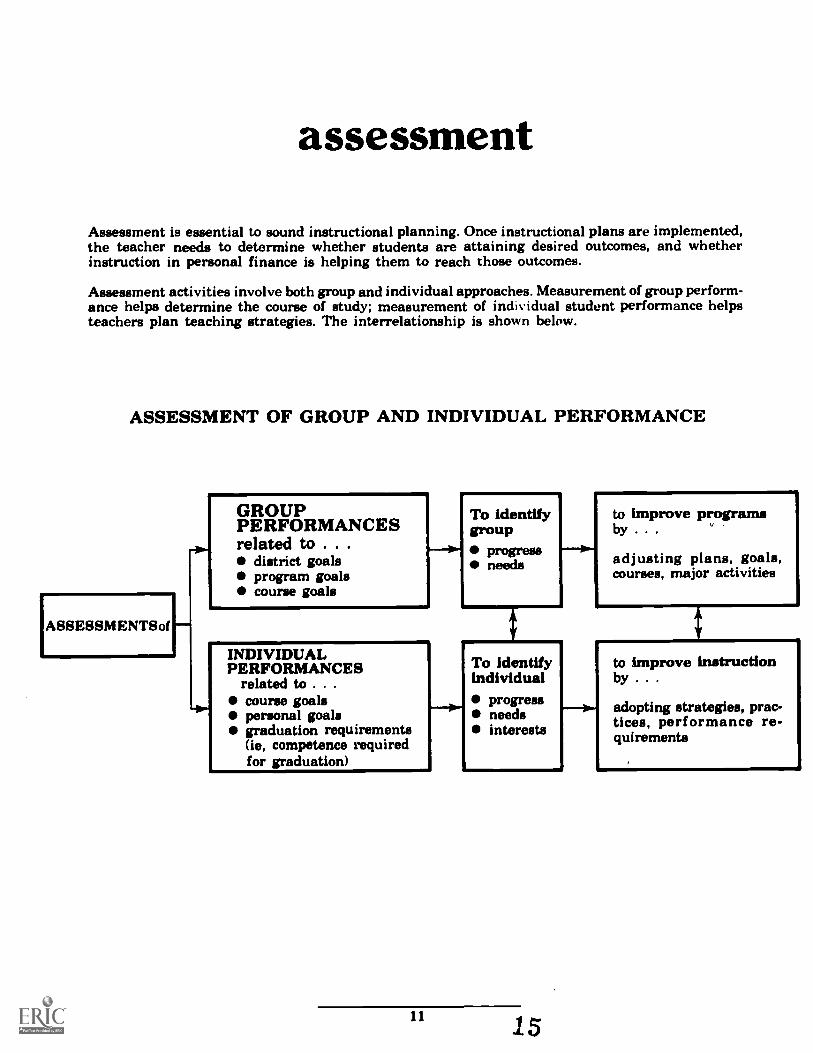

assessment

Assessment is essential to sound instructional planning. Once instructional plans are implemented,the teacher needs to determine whether students are attaining desired outcomes, and whetherinstruction in personal finance is helping them to reach those outcomes.

Assessment activities involve both group and individual approaches. Measurement of group perform-ance helps determine the course of study; measurement of individual student performance helpsteachers plan teaching strategies. The interrelationship is shown below.

ASSESSMENT OF GROUP AND INDIVIDUAL PERFORMANCE

ASSESSMENTS of

GROUPPERFORMANCESrelated to . . .

district goalsprogram goalscourse goals

-ow

INDIVIDUALPERFORMANCES

related to . . .

course goalspersonal goalsgraduation requirements(le, competence requiredfor graduation)

To identifygroup

progressneeds

.....1111.,

s

To identifyindividual

progressneedsinterests

to improve programsby . . .

adjusting plans, goals,courses, major activities

tto improve instructionby . . .

--40- adopting strategies, prac-tices, performance re-quirements

11 15

Under Goal-Based Planning, page 2 of this guide, goals were described as learning outcomes.Assessment should determine:

The extent to which students are attaining the outcomes the community and its schools havedesignated (district goal).

The extent to which students are attaining the outcomes teachers and curriculum planners havedesignated for the curriculum (program goal).

The extent to which students are attaining the outcomes teachers have designated for a course,such as Personal Finance I (course goal).

Furthermore, assessment of personal goals helps determine the extent to which the student isattaining those outcomes designated as of greatest personal importance, need, or interest. Identifica-tion of learning strengths and weaknesses in a student's performance helps determine factors whichenhance or inhibit attainment of desired outcomes.

Before assessment activities are conducted, clear goals and indicators describing student performancewhich can be accepted are necessary. Such statements guide assessment activities toward producinginformation that is useful in making curriculum decisions.

12

4

emp oymentand income

1.1 Obtaining a Job1.2 Meeting Responsibilities for Job Stvvess

1.3 Employee Organizations1.4 Employment Laws - Federal and State

employment and income

FIRST LEVEL

1.1 Obtaining a Job

STUDENTS WILL KNOW FACTORS WHICH IN-FLUENCE OPPORTUNITI}..2. FOR EMPLOYMENTAND INCOME.

List several factors which affect employmentopportunities and the potential for earning income.

List sources of information about job oppor-tunities and job requirements.

Describe grooming practices and dress stan-dards appropriate for a number of types of jobinterviews.

STUDENTS WILL COMPREHEND HOW VARIOUSFACTORS INFLUENCE OPPORTUNITIES FOREMPLOYMENT AND INCOME.

Explain factors affecting employability and in-come opportunities.Give examples of sources of information forspecific jobs.

Have students brainstorm factors affecting employ-ment opportunities; identify community resourcepeople for students to interview regarding the im-portance of such factors. Next, invite resource peopleto class to discuss job opportunities and the servicesprovided by such organizations as the state employ-ment office, private employment agencies, youthopportunity centers. As a class, discuss other waysjobs can be found.

Divide the class into groups for the purpose of estab-lishing mock employment agencies. Have each groupselect three or more occupations and compile infor-mation on: potential earning power, the skills and

training required, anticipated working conditions,and where jobs can be found. Next, ask each studentto research and list aptitudes, skills and personaltraits necessary for a specific job of a personal choice.

As a follow-up, invite a panel of local business peopleto class to discuss application forms, resumes andletters of application, on-the-job dress requirements,interview and testing procedures.

SECOND LEVEL

*STUDENTS WILL BE ABLE TO APPLY VARIOUSJOB SEARCH TECHNIQUES AND APPLICATIONTECHNIQUES TO SPECIFIC SITUATIONS.

Use local sources to determine employment po-tential in specific situations.

Write a letter of application.

Complete an application form.

Predict outcomes of several job interviews.

STUDENTS WILL BE ABLE TO ANALYZE THEIROWN POTENTIAL FOR EMPLOYMENT.

Relate how interests, abilities, training and ex-perience influence employability in specificsituations.

Select several careers which reflect personalinterests and abilities.

Have students review local newspaper "help wanted"listings and talk with people in the community aboutthe potential for employment locally; then ask eachstudent to prepare a list of potential jobs and investi-gate the skills and training required for those ofinterest personally.Ask each student to prepare a list of five questions

14 1 8

which a potential employer might ask a job applicantand then determine how best to provide such infor-mation through letters of application, resumes, inter-views, or recommendations.

Using a transparency, demonstrate for students howto complete an application form correctly. Have stu-dents complete application forms; comment or makeneeded corrections on an individual basis.

Discuss the elements of a good letter of application.Distribute copies of a sample letter and discuss as aclass. Have students write their own letters of appli-cation.

Show students a film about interviews and then havethem simulate various interview situations. Follow-ing each, discuss whether the applicant is likely toreceive the job. Point out both positive and negativeaspects of each interview. Have students repeat inter-views, including as many improvements as possible.

Using a Needle -Sort of the Career Information Sys-tem (CIS), have students identify and list individualinterests and skills and job categories related to suchinterests and skills. From the list, have studentsselect several careers to explore in more detail.

THIRD LEVEL

STUDENTS WILL BE ABLE TO PROPOSE WAYSTO MEET CAREER GOALS.

Design a plan for meeting career goals.

Summarize the importance of factors which af-

feet the selection of careers in specific situa-tions.

STUDENTS WILL BE ABLE TO JUDGE THE ADE-QUACY OF JOBS IN TERMS OF FULFILLINGLONG-TERM CAREER GOALS.

Compare the potential of several occupations forreaching personal career goals.

Interpret the effect of training and experienceon long-term career goals.

Have each student select a successful person in his-tory with a job of interest to the student and write areport based on the following questions:

What career goals might this person have had?

How would such goals relate to your career goalstoday?

How did this person achieve those goals?

What factors could have influenced this person'schoice of careers and how did these factors helpthis person's achievement?

As a wrap-up, ask each student to outline and de-scribe how one can achieve individual career goals,based on research and the answers to the questionsabove.

Using earlier research on careers, ask students todecide which jobs meet their criteria. Investigatetraining opportunities and determine whether suchtraining would help attain long-term career goals.

Factors affecting employment op-portunities and income potentialPersonal characteristics

Mental and physical healthGrooming and personal cleanlinessAppropriate dress standards

Salable skills, talents, and experiencesSchool courses, grades, and atten-

danceHobbiesSkillsSummer and part-time job experi-

encesSports and extracurricular activities

Information on jobsOccupational Outlook HandbookCurrent articles about occupational

trendsOccupational Outlook QuarterlyPrivate and public agencies

State employment officesPrivate employment agenciesYouth employment servicesYouth corp agenciesCivil service agenciesApprenticeship board

Career Information System (CIS)Other

Newspaper want adsSchool counselorsCommunity businessesYellow pages of telephone bookFriends and relativesProfessional publications

Job requirementsDictionary of Occupational riflesOccupational Outlook HandbookCareer cluster guidesInterviews with employers and employeesCareer Information System (CIS)

Personal interviewPunctualityCourtesyGood grammarPerseveranceSelf-confidenceEnthusiasmProper attitudePoiseKnowledge of employer and the businessAppropriate dress and grooming

15

Alert, intelligent responsesOther

Credit recordRecord of civil actionsReferences

Procedures in applying for a jobPrepare personal data sheet (resume)Write letters of applicationObtain recommendationsObtain referencesFill out application formsTake testsObtain social security number and work

permit (1.4)

Factors influencing career selectionInterestsSkills and abilitiesPresent and future goalsJob requirementsEmployment oppor.unitiesJob locationJob securityPresent and potential IncomeRisk or adventureBenefitsWorking hours and conditions

1.2 Meeting Responsibilities for Job Success

FIRST LEVEL

STUDENTS WILL KNOW WHY MEETING EM-PLOYER AND EMPLOYEE RESPONSIBILITIESCAN LEAD TO SUCCESS ON THE JOB.

Identify responsibilities of employers to em-ployees.

Identify responsibilities of employees to employ-ers and to other employees.

*STUDENTS WILL COMPREHEND HOW EMPLOY-ERS AND EMPLOYEES MEET ON-THE-JOB RE-SPONSIBILITIES SUCCESSFULLY.

Explain how employer and employee attitudesinfluence success on the job.

Give examples of reasons for employee promo-tions.

Explain most frequent causes of employee ter-mination.

Write, visit, or invite persons from managementlevels of large companies to: discuss training andeducation programs for their employees; describecriteria used for employee evaluation (performanceratings); identify the most frequent causes of em-p1 iyee termination; discuss the basis for employeerromotions. As a follow-up, discuss performance rat-ing scales fur employees who are on probation prior totenured employment or who are being rated for sal-ary increases. Discuss various criteria used as a basisfor promotion (ie, merit, seniority, automatic).

Have students read several newspaper "help wanted"ads and determine to what extent, if any, the respon-sibilities of the employee or the employer are de-scribed. Next, ask each student to select one ad andlist the information provided including employer andemployee responsibilities and job advancement infor-mation which would be useful to know before accept-ing that particular job.

As a class, prepare a list of on-the-job "Do's" and"Don'ts" and discuss how these factors affect jobsuccess and advancement.

SECOND LEVEL

STUDENTS WILL BE ABLE TO APPLY TECH-NIQUES FOR MEETING JOB RESPONSIBILITIES

ACCORDING TO THE SPECIFIC SITUATION.

Modify a situation to improve potential for jobsuccess and advancement.

Relate attitudes to job success.

STUDENTS WILL BE ABLE TO ANALYZE INDI-VIDUAL RESPONSIBILITIES OF EMPLOYERSAND EMPLOYEES.

Discriminate between responsibilities of em-ployee and employer in a specific situation.

Outline ways employees have maintained goodworking relationships in given situations.

Divide the class into groups to investigate casestudies involving comments by employees and em-ployers, or among other employees. Develop a skitillustrating one of these situations, and have theclass suggest changes which might improve workingrelationships. Emphasize the importance of attitudeson the job.

Ask groups of students to review various hypotheticaljob situations which are unsatisfactory, and listexamples of employer and employee responsibilitieswhich are not being met. In addition, have them listother responsibilities which they feel should be ob-served, as well as how employees can maintain goodrelationships with other employees.

THIRD LEVEL

STUDENTS WILL BE ABLE TO RELATE HOWVARIOUS FACTORS CONTRIBUTE TO JOB SUC-CESS AND ADVANCEMENT.

Design a plan for upgrading skills for a specificoccupation.

Summarize experience or training needed foremployability or job advancement in varioussituations.

STUDENTS WILL BE ABLE TO JUDGE THEAPPROPRIATENESS OF EMPLOYER OR EM-PLOYEE ACTIONS.

Justify the use of specific criteria as the basisfor promotion.

Appraise how employee attitude influences jobsuccess in specific situations.

16 20

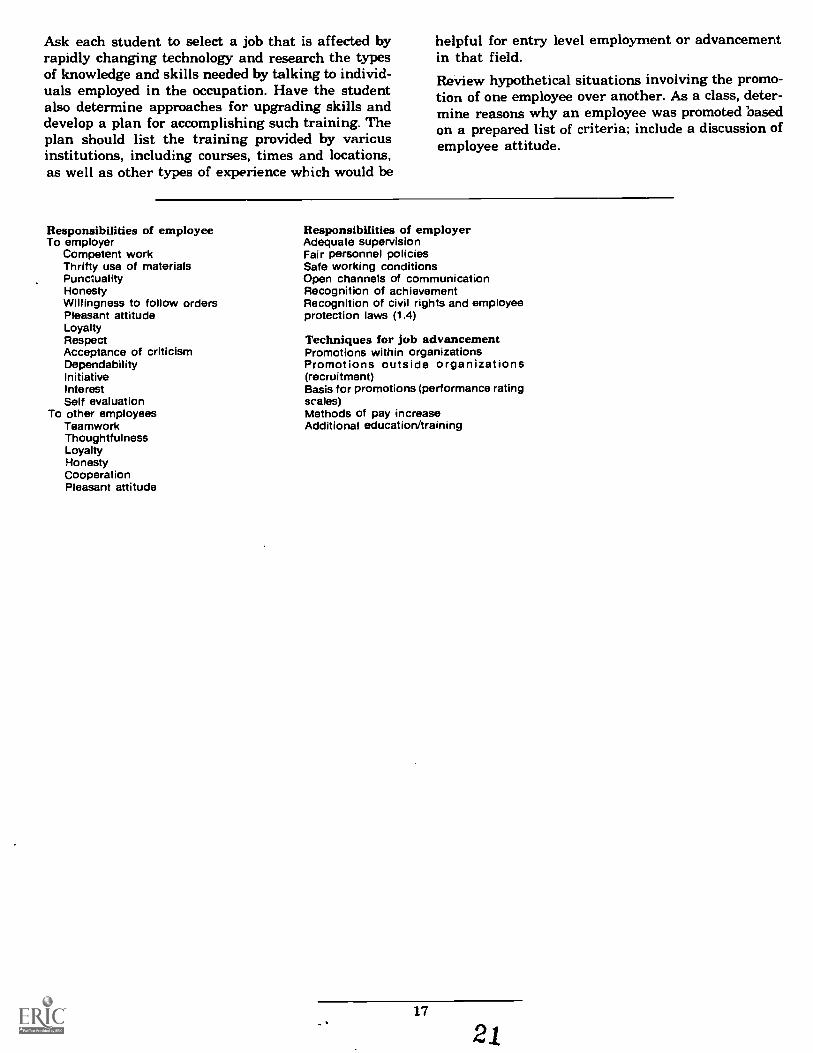

Ask each student to select a job that is affected byrapidly changing technology and research the typesof knowledge and skills needed by talking to individ-uals employed in the occupation. Have the studentalso determine approaches for upgrading skills anddevelop a plan for accomplishing such training. Theplan should list the training provided by varicusinstitutions, including courses, times and locations,as well as other types of experience which would be

helpful for entry level employment or advancementin that field.Review hypothetical situations involving the promo-tion of one employee over another. As a class, deter-mine reasons why an employee was promoted basedon a prepared list of criteria; include a discussion ofemployee attitude.

Responsibilities of employeeTo employer

Competent workThrifty use of materialsPunctualityHonestyWillingness to follow ordersPleasant attitudeLoyaltyRespectAcceptance of criticismDependabilityInitiativeInterestSelf evaluation

To other employeesTeamworkThoughtfulnessLoyaltyHonestyCooperationPleasant attitude

Responsibilities of employerAdequate supervisionFair personnel policiesSafe working conditionsOpen channels of communicationRecognition of achievementRecognition of civil rights and employeeprotection laws (1.4)

Techniques for job advancementPromotions within organizationsPromotions outside organizations(recruitment)Basis for promotions (performance ratingscales)Methods of pay increaseAdditional education/training

17

1.3 Employee Organizations

FIRST LEVEL

STUDENTS WILL KNOW HOW GROUPS OFEMPLOYEES CAN ORGANIZE TO INFLUENCEEMPLOYMENT CONDITIONS.

List the major purposes of labor unions.

List the major purposes of professional organi-zations.

*STUDENTS WILL COMPREHEND THE IMPACTOF EMPLOYEE ORGANIZATIONS AND UNIONSON THE EMPLOYEE.

Explain the purposes and expectations of aunion shop.

Give examples of services and benefits providedby professional organizations.

Invite union officials to class to discuss the purposesand expectations of a typical union shop; invite mem-bers of professional organizations to discuss servicesand benefits of professional organizations. After thepresentations, encourage questions and answersabout the functions of these organizations. As afollow-up, have students read about the developmentof union shops in the United States and discuss theoriginal purposes for which each was established.Have students interview union members to askwhether union shops have the same purposes today.

SECOND LEVEL

STUDENTS WILL BE ABLE TO APPLY KNOWL-EDGE OF UNIONS AND PROFESSIONAL OR-GANIZATIONS TO VARIOUS EMPLOYMENTSITUATIONS.

Show how membership in a union or profession-al organization influences employability or jobadvancement.

Relate the advantages and disadvantages of aunion shop to a nonunion shop.

STUDENTS WILL BE ABLE TO ANALYZE THEIMPACT OF UNION OR PROFESSIONAL MEM-BERSHIP ON EMPLOYMENT.

Point out the effect of the union movement onemployee conditions in specific situations.

Point out how professional organizations haveinfluenced professional standards.

Divide the class into groups, with each group repre-senting a specific occupation. Ask those groups whoseoccupations are represented by unions to investigatethe development of the union movement generallyand of the specific union that represents the occupa-tion, the pros and cons of unions and the specificunion, the wage scales and fringe benefits of unionand nonunion occupations, jobs available to teen-agers which involve unions and a comparison ofmonthly dues among such unions.

Have groups whose occupations are represented byprofessional organizations investigate the advan-tages and disadvantages of such organizations, thenumber and types of professional organizations avail-able in the community, and membership require-ments according to occupation. As a class, determinethose characteristics which unions and professionalorganizations hold in common as well as those whichare unique to each.

THIRD LEVEL

STUDENTS WILL BE ABLE TO RELATE KNOWL-EDGE OF UNIONS AND PROFESSIONAL OR-GANIZATIONS TO PERSONAL CAREER DECI-SIONS.

Explain how union membership and nonmem-bership could affect employees in specific occu-pations.

Summarize the economic and noneconomic ef-fects of union and professional organizationmembership in specific situations.

STUDENTS WILL BE ABLE TO JUDGE PERSON-ALLY THE VALUE OF UNION AND PROFES-SIONAL ORGANIZATION MEMBERSHIP.

Appraise reasons for membership and nonmem-bership in specific situations.

Support a personal decision regarding union orprofessional organization membership.

Utilizing previous research on general characteristicsof unions and professional organizations, have eachstudent select a specific union or organization forresearch. Through investigation, including reading

18 1)2

and interviews, determine the specific economic andnoneconomic benefits, membership benefits, and whymembership, if optional, is of benefit to the individ-ual employee.Have students research employee conditions prior tothe union movement and the growth of professionalorganizations. Speculate what employee conditions,including salaries and benefits, would be like at the

present time without the involvement of unions andorganizations. Ask groups of students to select issuesrelated to working conditions and trace the role ofunions and professional organizations historically inbringing about improved working conditions. Includea chronological sequence of events leading to workingconditions as they exist currently.

UnionsPurposes

Act as collective bargaining agents foremployees

Wages for regular work andovertime

Hours of workRequirements for employmentPensionsHealth, safety, and working

conditionsMethod of hiring and firingCases involving dischargeMethods of settling disputes

Provide job placement servicesEnforce labor agreementsSupport legislation affecting worker

Professional organizationsPurposes

Establish and maintain professionalstandards

Support legislation affecting theprofession

Encourage individual growth andadvancement

Improve working conditions andincome

Provide pension, retirement, andsupportive benefits

Keep membership up to date onresearch and technology

Negotiate with employer on terms ofemployment (restricted)

19

1.4 Employment Laws - Federal and State

FIRST LEVEL

STUDENTS WILL KNOW WHICH FEDERAL ANDSTATE LAWS AND REGULATIONS PROTECTEMPLOYERS AND EMPLOYEES.

List major employment laws and regulations.

Matcl: ws with agencies responsible for ad-minis each.

Describe employment laws or regulations whichaffect minors and their employers.

*STUDENTS WILL COMPREHEND THE EFFECTSOF EMPLOYMENT LAWS AND REGULATIONSON EMPLOYERS AND EMPLOYEES.

Explain how employment laws protect the em-ployee.

Give examples of laws or regulations which af-fect minors or their employers.

Explain why laws differ, depending on the occu-pation.

Have students answer the following questions:

Why are there laws for protecting employees?

Why are laws different for certain jobs?

Why do laws for employees who are minorsdiffer from laws for employees who are adults?

Why do laws for 14- and 15-year-old employeesdiffer from laws for 16- and 17-year-olds?

Invite representatives from the local Wage and HourDivision to class to discuss: how to obtain a workpermit, when a work permit is required, what types ofjobs are not regulated, what jobs are permissible foremployees of different ages, the work hours for em-ployees of different ages, and the jobs which employ-ees under 18 years of age are prohibited from holding.

Develop a list on the board of major federal and statelaws and regulations affecting employment. Havestudents use the telephone book and interview agen-cy or business representatives to determine whichagencies administer each law or regulation.

Invite an employer to class to discuss the laws andregulations under which employers must work andthe agency that is responsible for administering each.

SECOND LEVEL

STUDENTS WILL BE ABLE TO APPLY EMPLOY-MENT LAWS AND REGULATIONS TO SPECIFICSITUATIONS.

Show how laws differ according to age group orjob.

Relate current laws affecting minors to specificjob situations.

Write to an agency regarding a potential viola-tion of an employment law or regulation.

STUDENTS WILL BE ABLE TO ANALYZE HOWLEGISLATION HAS AFFECTED SPECIFIC EM-PLOYMENT CONDITIONS.

Illustrate how employment legislation related tominors differs from legislation for adults.

Identify how employment conditions havechanged as a result of federal and state legisla-tion.

Have students review current federal and state agen-cy publications dealing with the administration ofvarious laws or regulations, such as the "Employ-ment of Minors" pamphlet from the Oregon Bureauof Labor and Industries. Determine the status ofcurrent laws and regulations which affect employeeswho are minors. As a class, discuss differences amonglaws and regulations for various workers according toage and sex.

Have students investigate specific laws or regula-tions which affect employees who are minors in occu-pations in which they are interested. Determinewhether or not these laws or restrictions are based onhealth and safety concerns of young employees. Readabout the working conditions of young employees inthe early 1900's and discuss whether these conditionshave been affected by legislation.

Using a variety of occupations as examples, have

20 24

students identify special regulations or restrictionsfor employees who are minors which are not imposed/on other workers. Determine whether other claisifi=cations of workers, such as women, have special pro-tection through legislation. As a class, disciiss theadvantages and disadvantages of special legislation.

Invite an employer to class to explain how laws andregulations affect the employment of minors in cer-tain occupations. Discuss whether these laws benefityoung employees wishing to enter a specific occupa-tion.

Using a case situation, write hypothetical letters toagencies identifying potential violations of employ-ment laws or regulations and document complaintswith specific data and evidence. Read letters lin classand determine what action might be taken by agen-cies and whether employers would be involved. Dis-cuss the advantages of resolving problems with anemployer prior to filing a complaint.

THIRD LEVEL

STUDENTS WILL BE ABLE TO RELATE THEECONOMIC AND NONECONOMIC EFFECTS OFEMPLOYMENT LAWS AND REGULATIONS ONEMPLOYERS AND EMPLOYEES.

Summarize the potential consequences of re-scinding all employment legislation.Explain economic implications of protectivelegislation for employees and employers.

STUDENTS WILL BE ABLE TO JUDGE THE ADE-QUACY OF EMPLOYMENT LAWS AND REGULA-TIONS IN PROTECTING EMPLOYERS AND EM-PLOYEES.

Justify special protection employees receive ac-cording to age, sex or occupation.

Appraise the development of legislation protect-ing the employee in the United States.

Divide the class into research groups and have eachgroup choose one major federal law designed to pro-tect employees and study the background issueswhich led to the enactment of this law. Identify andclassify the major provisions of the law according to:benefits, including health and safety, economic se-curity, or employment security. Either support thelegislation as meeting employee needs today based onreview of provisions or rewrite the legislation so thatit meets current employee needs. As a follow-up, haveeach group develop a discussion paper on the poten-tial impact of rescinding all employment legislation.Include opinions as to what might happen withspecific occupations such as educators or mine work-ers, as well as an overview of the total effect onemployment in the United States.

Inv:te to class a panel of employees representinggroups who receive special protection through legisla-tion to discuss the reasons for such legislation. Havestudents ask questions about how the laws affectsuch "special" groups and other employees.

For students interested in self-employment occupa-tions, have them research the licensing and regula-tions required. Based on this study, ask students tochoose whether they wish to be self-employed anddefend their position by showing that they have in-vestigated the field.

Laws affecting workersMajor federal laws protecting workers/administering agencies

National Labor Relations Act (WagnerAct) U S Department of Labor

Fair Labor Standards Act of 1938(amended 1966. 1972 and 1974)Wage and Hour and PublicContracts DivisionsU SDepartment of Labor

Taft-Hartley Act U S Department ofLabor

Social Security Act U S Departmentof Health and Human Services

Williams-Steiger Occupational Safetyand Health Act of 1970 (OSHA)Department of Labor

Major state laws protecting workers/administering agencies

Oregon Safe Employment ActWorkers' Compensation Board,Accident Prevention Division

Workers' Compensation LawWorkers' Compensation Board

Employment Division LawOregonEmployment Division, OregonDepartment of Human Resources

Child Labor Standards ActWage andHouse Divisidh, Bureau of Laborand Industries

Major laws or regulations affectingemployment of minors*Covers such items asMinimum wages and hours of workWork permits and Social Security

numbersMinimum age limits

Jobs which 14- and 15-year-old

21 25

workers can doJobs which 16- and 17-year-old

workers can doInsurance requirementsSafety and health requirementsProhibited hazardous occupationsTraining agreements and plansLegal deductions from paychecks

*Both federal and state regulations maycover many of the same items; in suchcases, the more restrictive law orregulation will prevail.

moneymanagement.1.,..

2.1 Financial Security and Employment

2.2 Financial Planning2.3 Banking Services and Financial Records

2.4 Savings

2.5 Investments

2.6 Insurance

2.7 Legal Documents

2.8 Taxation

11/I

money management2.1 Financial Security and Employment

FIRST LEVEL

STUDENTS WILL KNOW THE TYPES OF FINAN-CIAL BENEFITS AND PROTECTION MADEAVAILABLE THROUGH EMPLOYMENT.

List various types of payroll deductions andemployment benefits.

Name types of income loss which can be protect-ed by employment benefits.

STUDENTS WILL COMPREHEND THE WAYSEMPLOYMENT CAN PROVIDE FINANCIALSECURITY.

Give examples of types of payroll deductionsand employment benefits.

Summarize the effects of employment on finan-cial security.

Review sample paycheck stubs for gross pay, take-home pay, involuntary deductions, voluntary deduc-tions (numerous options). Next, discuss the types ofprotection provided through employment to protectthe employee financially.

Use the Internal Revenue Service wage deductionchart to explain withholding taxes. (2.8) Invite asocial security representative to class to discuss: coststo the employee, benefits to minor dependents, ob-taining a social security number, how to check per-sonal accounts.

As a follow-up, have students talk to family andfriends about "fringe benefits" provided by em-ployers.

Have the class discuss financial problems and protec-tion available to the employee through employment

and individual responsibilities for financial security.

SECOND LEVEL

*STUDENTS WILL BE ABLE TO PLAN FOR FI-NANCIAL SECURITY IN LIGHT OF BENEFITSPROVIDED THROUGH EMPLOYMENT.

Compute payroll deductions for specific situa-tions.

Modify a budget to allow for protection fromfinancial problems in specific situations.

Show how financial protection varies accordingto employment benefits.

STUDENTS WILL BE ABLE TO ANALYZE FINAN-CIAL SECURITY IN SPECIFIC EMPLOYMENTSITUATIONS.

Illustrate how various employment benefits pro-vide financial security.

Point out financial protection available to anemployee.

Using various case studies involving loss of incomedue to death, illness, disability or unemployment,have students investigate the types of protection pro-vided through employment. Discuss the potential fi-nancial effects when the individual or family does notprovide for additional protection.

Using various employment and income situations,have students plan individual and family budgetswhich provide for: loss of income for three months, achange in take-home pay, an inflation rate of 10percent with no salary increase.

Review changes in employee social security contribu-tions for the past two years and discuss the effect on

personal spendable income.

THIRD LEVEL

STUDENTS WILL BE ABLE TO PROPOSE WAYSTO PROVIDE FOR FINANCIAL SECURITYTHROUGH EMPLOYMENT BENEFITS AND PAY-ROLL DEDUCTIONS.

Design a program to provide protection againstloss of income in specific situations.

Reconstruct a budget to provide for an increasein savings through payroll deductions.

STUDENTS WILL BE ABLE TO JUDGE THE ADE-QUACY OF EMPLOYEE BENEFITS AND INCOMEPROTECTION.

Compare income protection to essential and de-sirable needs in specific situations.

Appraise the degree to which employee benefitsmeet personal financial goals.

Have students establish hypothetical family situa-tions with specific financial goals. After researchingtypes of employment and private income protectionavailable, ask each group to prepare a financial pro-tection plan that appears to best meet the situation,present findings to the class and defend the plan.

Have a panel of students debate the pros and cons ofthe social security system as a form of employeeprotection.

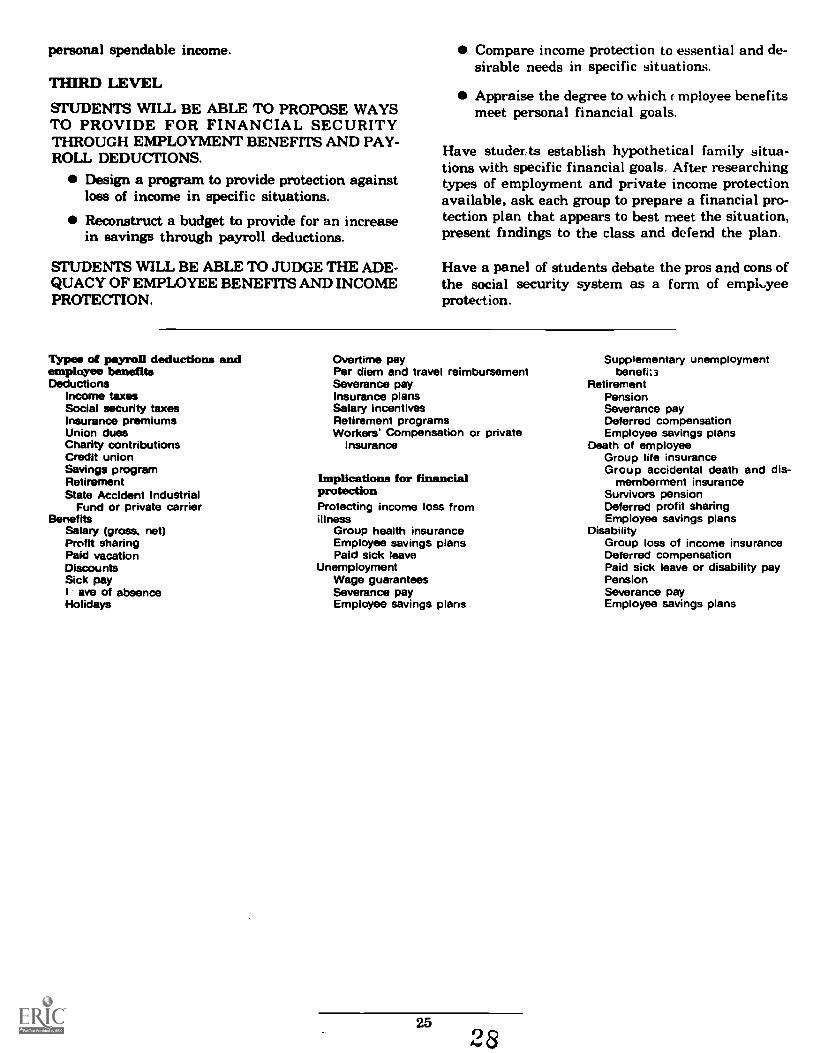

Types of payroll deductions andemployee benefitsDeductions

Income taxesSocial security taxesInsurance premiumsUnion duesCharity contributionsCredit unionSavings programRetirementState Accident Industrial

Fund or private carrierBenefits

Salary (gross, net)Profit sharingPaid vacationDiscountsSick payI ave of absenceHolidays

Overtime payPer diem and travel reimbursementSeverance payInsurance plansSalary incentivesRetirement programsWorkers' Compensation or private

insurance

Implications for financialprotectionProtecting income loss fromillness

Group health insuranceEmployee savings plansPaid sick leave

UnemploymentWage guaranteesSeverance payEmployee savings plans

2528

Supplementary unemploymentbenefit 3

RetirementPensionSeverance payDeferred compensationEmployee savings plans

Death of employeeGroup life insuranceGroup accidental death and dis-

memberment insuranceSurvivors pensionDeferred profit sharingEmployee savings plans

DisabilityGroup loss of income insuranceDeferred compensationPaid sick leave or disability payPensionSeverance payEmployee savings plans

2.2 Financial Planning

FIRST LEVEL

STUDENTS WILL KNOW BASIC PRINCIPLES OFFINANCIAL PLANNING.

Identify reasons for financial planning.

List steps in planning a budget.

Describe ways financial planning helps tobudget resources.

STUDENTS WILL COMPREHEND HOW FINAN-CIAL PLANNING CONTRIBUTES TO FINANCIALSECURITY.

Give examples of how financial planning helpsindividuals and families in specific situations.

Explain the steps involved in planning a budget.

Distinguish between fixed and flexible ex-penses.

Develop a list on the board of possible sources ofincome, including work, investments, insurance, andvarious retirement plans. Discuss financial planningand what it includes. As a follow-up, assign a commit-tee to study and report on different ways to organizeresources.

Invite a financial counselor from a bank, creditunion, social service agency, etc, to speak to the classabout the problems of individuals who fail to estab-lish plans for managing their money. Discuss familybudgeting problems, examples of inadequate moneymanagement (include several income levels) and pos-sible consequences of such major changes in the fam-ily as divorce. Have students tape interviews withpeople regarding their approaches to budgeting; in-clude a young married couple, middle-aged couplewith children, and a senior citizen. Outline the com-mon steps used in budget planning, noting fixed andflexible expenses.

Discuss how other economic units, such as local, stateand federal governments, plan budgets; compare withindividual and family budget planning.

SECOND LEVEL

*STUDENTS WILL BE ABLE TO APPLY BASICPRINCIPLES OF FINANCIAL PLANNING TOPERSONAL INCOME SITUATIONS.

Predict the effects of financial planning onspecific situations.

Prepare budgets for various income levels.

STUDENTS WILL BE ABLE TO ANALYZE HOWFINANCIAL PLANNING PROVIDES FORECONOMIC SECURITY.

Point out ways in which financial planninghelps individuals and families in various situa-tions.

Relate how financial planning provides foreconomic security generally.

After analyzing the steps involved in budgeting, havestudents determine the adjustments which might berequired in a family budget if the following situa-tions occurred: an offspring enters college; familyincome increases by one-third; the family buys asecond car; the family moves to the suburbs; an agedparent moves in with the family; utility or gasolinecosts double; father or mother is unemployed (2.1);father or mother dies or is disabled. Follow with adiscussion summarizing the benefits of plannedspending.

Have students develop and keep a budget for onemonth, based on their present incomes. As a fcllow-up, ask students to interview various financial plan-ning experts regarding the benefits of financial plan-ning to individuals and families, and how it providesfor financial stability. Compile the information into alist of the pros and cons of budgeting.

THIRD LEVEL

STUDENTS WILL BE ABLE TO FORMULATE AFINANCIAL PLAN TO MEET A VARIETY OFSITUATIONS.

Create a financial plan that provides for in-creased expenditures in selected situations.

Reorganize budgeting steps and procedures toaccommodate specific situations.

STUDENTS WILL BE ABLE TO JUDGE THE IM-PACT OF FINANCIAL PLANNING ON MONEYMANAGEMENT AND ECONOMIC SECURITY.

Justify the need for financial planning in givensituations.

26 29

Compare the effects of using a budget as op-posed to not using a budget in given situations.

Ask each student to write a story about how theythink some figure in history, such as GeorgeWashington or Benjamin Franklin, might havemanaged finances. Have students support theirstories based on reading about the individual's habitsand lifestyle, and the economic needs and wants ofthe period.With various hypothetical family situations, have

students estimate the effect of financial planning orlack of planning, including the effects on individualfamily members and the community.

Using case studies depicting a variety of incomelevels and indebtedness situations, have studentsprepare several budgets which reflect financial goalsand budgeting techniques. As a class select one as themost logical ar d appropriate, and have students writea paper to defend the choice, describing the benefitsor disadvantages this budget plan might have.

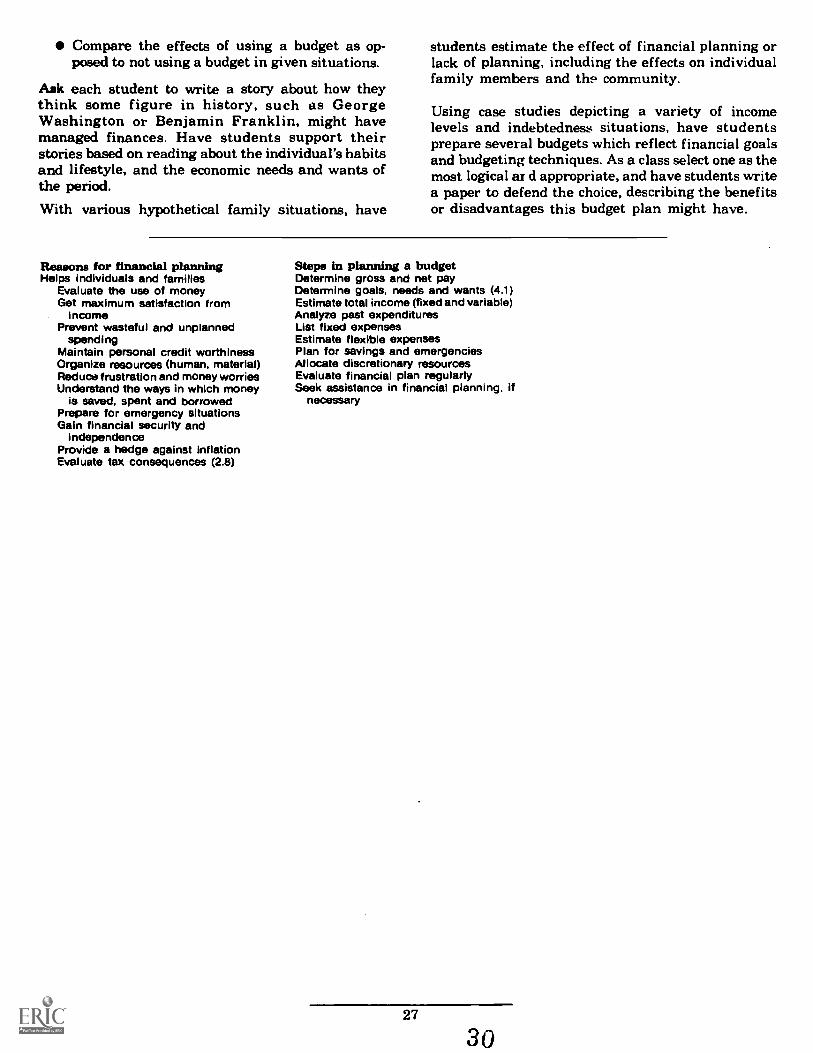

Reasons for financial planningHelps individuals and families

Evaluate the use of moneyGet maximum satisfaction from

incomePrevent wasteful and unplanned

spendingMaintain personal credit worthinessOrganize resources (human, material)Reduce frustration and money worriesUnderstand the ways in which money

is saved, spent and borrowedPrepare for emergency situationsGain financial security and

independenceProvide a hedge against inflationEvaluate tax consequences (2.8)

Steps in planning a budgetDetermine gross and net payDetermine goals, needs and wants (4.1)Estimate total income (fixed and variable)Analyze past expendituresList fixed expensesEstimate flexible expensesPlan for savings and emergenciesAllocate discretionary resourcesEvaluate financial plan regularlySeek assistance in financial planning, if

necessary

27

2.3 Banking Services and Financial Records

FIRST LEVEL

STUDENTS WILL KNOW TYPES OF BANKINGSERVICES AND RECORDKEEPING PLANSAVAILABLE WHICH FACILITATE FINANCIALPLANNING.

List various types of banking services and fi-nancial recordkeeping systems.

Identify guidelines for using banking servicesand financial records.

STUDENTS WILL COMPREHEND THE EFFECTSOF BANKING SERVICES AND RECORDKEEPINGON PERSONAL MONEY MANAGEMENT.

Explain how keeping financial records and us-ing banking services can aid in financial plan-ning.

Give examples of banking services and financialrecordkeeping systems.

As a class, construct a bulletin board display depict-ing various types of banking services. Ask students toread about electronic funds transfer systems andidentify the types available in the immediate area,including possible services such as bill checks, auto-matic payroll deductions, debit cards.*

Discuss business aspects of family living and list onthe board examples of valuable papers which familiesshould keep. Next to each example, list ideas aboutwhere each might be stored. Next, utilize transparen-cies to illustrate various types of household recordsystems; as a class, discuss the reasons for keepingsuch records.

SECOND LEVEL

*STUDENTS WILL BE ABLE TO APPLY BANK-ING SERVICES AND RECORDKEEPING TECH-NIQUES TO THEIR OWN FINANCIAL PLAN-NING.

Plan a personal recordkeeping system.Modify spendiag plans based on a review of

*A card which ultimately will be tied to retail outletsso that customer purchases can automatically be"debited" to the individual checking account.

financial records.

Write a check, balance a checkbook, and recon-cile a bank statement.

STUDENTS WILL BE ABLE TO ANALYZE THEEFFECTS OF BANKING SERVICES AND RE-CORDKEEPING ON FINANCIAL PLANNING.

Point out the importance of banking services topersonal money management.

Determine spending patterns based on a reviewof financial records.

Identify the types of banking services availableto meet various needs.

Have each student complete a project of personalchoice: net worth computation for a family in a givensituation, record of personal expenditures and incomefor two weeks as a basis for future planning, a class-room or home inventory, a home business center.

Ask students to utilize a current income tax bookletto determine allowable income tax deductions. As aclass, discuss deductions and develop a system forkeeping track of deductions during the year; discussalso what proof is necessary should tax returns beaudited.

Demonstrate for the class the correct way to write acheck. Use a transparency to illustrate how anamount on a check can be changed and what can bedone to prevent this. Then have students practicewriting checks, keeping records and reconciling ac-counts in simulated checkbooks. As a class, discussthe distinction between overdrawing a checking ac-count due to carelessness or error and overdrawingwith intent to defraud. Point out the effects of over-drafts on an individual's credit record.

THIRD LEVEL

STUDENTS WILL BE ABLE TO PREPAREGUIDELINES FOR THE USE OF BANKING SER-VICES AND FINANCIAL RECORDKEEPING.

Compile a list of banking services available

3128

currently and the advantages and disadvan-tages of each service in specific situations.

Design a plan for maintaining personal recordsfor specific situations and needs.

Revise personal budgcts based on a review offinancial records and expenditures.

STUDENTS WILL BE ABLE TO JUDGE THEADEQUACY OF BANKING SERVICES ANDRECORDKEEPING TECHNIQUES FOR SPECIFICSITUATIONS.

Compare the costs and convenience of bankingservices in specific situations.

Justify the use of one type of recordkeepingsystem over another in specific situations.

Invite a local banker to class to discuss current and

anticipated services available through electronictransfer systems in the community. Have each stu-dent write a paper describing the implications forfinancial planning and recordkeeping, as well as im-plications for personal privacy.

Have students investigate various types of bankingservices available in the local community, includingcosts, services and limitations of each. Using avariety of hypothetical situations, select the bankingservices which best meet individual needs and situa-tions and defend the selection.

Review several budgets and recordkeeping systemsand determine the potential strengths and weaknes-ses of each. Outline the possible financial goals for afamily that might use each budget method or record-keeping system. Determine whether som° situationsmight imply that families have not established finan-cial goals.

Types and importance of bankingservices and financial recordsBanking services

Checking accountsBank statementsSavings accountsSafety deposit boxes/safe keepingForeign exchangeLoansFinancial advice to familiesEstate planning and trustsCredit cards/debit cardsPayment servicesInvestment services (2.5)Electronic funds transfer

Financial recordsAccounts of earning and spendingFinancial statement (net worth)Household inventoryinvestment recordsTax record (2.8) (eg. medical and drug

records, home purchase andimprovement records)

ImportancehelpsProvide proof of paymentEvaluate spending patternsProvide information for income tax

recordsAnalyze financial situationProvide a basis for determining future

purchasesProvide a basis for developing and

maintaining a budgetProvide proof of loss in case of fire or

theft

Guidelines for using banking servicesand financial recordsBanking services

Checking accountsWrite checks properlyKeep accurate record of checksMaintain up-to-date recordsConsider balance requirementsReconcile account monthlyCompare types of checking

accounts and costsSavings accounts

Compare types of accounts andinterest rates

Understand method of interestpayment

Know time period requirements. ifany

Safety deposit boxesIdentify valuables which need safe

storageKeep a separate record of contents

in personal safety deposit boxUnderstand safety deposit book

agreementFinancial records

Utilize check recordsDetermine those items necessary

for income tax recordsDevelop systems for filingKeep file up to dateCheck accuracy of records

29

32

2.4 Savings

FIRST LEVEL

STUDENTS WILL KNOW TYPES OF LAVINGSPLANS AVAILABLE AND FACTORS WHICH AF-FECT DECISIONS ABOUT SAVINGS.

List factors involved in making decisions aboutsavings.

List types of savings.

Identify methods of savings available.

STUDENTS WILL BE ABLE TO MAKE SAVINGSDECISIONS.

Distinguish between short-term and long-termsavings goals.

Defend the method and type of savings planselected in specific situations.

Give examples of types of indirect savings whichmeet personal needs in specific situations.

Develop a list of short- and long-term goals for teen-agers, young adults, newly married couples, growingfamilies, and retired people. Determine how muchwould have to be saved per week to achieve one ormore of these goals. Next, conduct a clasen.,om discus-sion around such questions as: How do attitudes in-fluence the habit of saving? What factors influencethe amount an individual or family may save? Is itpossible for a very low-income family to save?

Have students read about different types of savingsand discuss the advantages and disadvantages ofeach. Then, ask students to identify direct and indi-rect methods of saving, and construct a bulletin boarddisplay depicting examples of each.

SECOND LEVEL

*STUDENTS WILL BE ABLE TO APPLY DECI-SIONS ABOUT SAVINGS TO FINANCIAL PLAN-NING.

Predict the factors which influence savings deci-sions in specific situations.

Prepare savings plans for different situations.

STUDENTS WILL BE ABLE TO EVALUATE THEADEQUACY OF SAVINGS DECISIONS.

Point out the impact of various savings deci-sions on financial stability.

Select a method and type of savings that meetsneeds in specific situations.

Using hypothetical case studies, have groups of stu-dents research the amount of money a family couldsave in a given length of time by limiting or recyclingscarce resources. As a follow-up, have students com-pute the dollar amount of indirect savings from rid-ing the bus to school for one semester as opposed todriving a car.

Compare the earnings from a $50 savings bond and a$50 savings account for one year. Refigure for vari-ous lengths of time and discuss the differencesbetween both types of savings. Then, invite guestspeakers to class to talk about the types of savingsinstitutions and savings plans available. Discuss:Why is safety put first and earnings second? What ismeant by liquidity? In what circumstances mightliquidity be important? How does purpose affect thechoice of a savings plan? Based on personal goals andneeds, have students choose the most appropriatetype and method of savings.

THIRD LEVEL

STUDENTS WILL BE ABLE TO INTEGRATE SAV-INGS DECISIONS INTO FINANCIAL PLANNING.

Explain how savings decisions meet spendingplans.

Desiga a savings plan that meets both im-mediate and long-term needs.

Reconstruct a personal budget to reflect savingsdecisions.

STUDENTS WILL BE ABLE TO JUDGE THEVALUE OF SAVINGS TOWARD MEETINGPRESENT AND FUTURE FINANCIAL NEEDS.

Appraise the effects of utilizing savings plans inspecific situations.

Justify the selection of one type and method ofsaving in terms of a specific situation.

Interpret the effects of several factors on sav-ings decisions in selected situations.

30 33

As a class, compile a fact sheet for the purpose ofcomparing or ranking different types of savings planson the basis of interest paid, services offered, anddegree of risk involved. Ask students to defend theselection of one savings plan over another based onpersonal goals and needs. Next, support the attrac-tiveness of various savings plans based on economicconditions and tax implications.

Using hyv)thetical case studies involving variousincome levels and financial goals, have studentsselect the most appropriate type and method of sav-ings for each. Describe how a specific savings ap-proach would affect each situation, and make budgetchanges to include such an approach.

Factors affecting savings decisionsNeeds and wantsGoals (short- and long-term)Amount of discretionary incomeAttitudes toward savingCompatibility with spending plansSafety of principalPurpose of savingsConvenience of method of savingNeed for liquidity or long-term investmentPotential for growth, as determined by:

Rate of interestMethod of compoundingMethod of determining balance on

which interest is paidLength of time investedType of savings

Economic conditionsTax implications (2.8)

Types and methods of savingsTypes

Passbook accountsCertificate of deposit (CD)Government bonds

MethodsDirect (through institutions)Mutual savings banksCommercial banksSavings and loan associationsCredit unionsU S Government (bonds, treasury

bonds)Indirect (through limiting use of

resources)RecyclingFinding alternatives, such as car

pooling

31

2.5 Investments

FIRST LEVEL

*STUDENTS WILL KNOW HOW VARIOUS FAC-TORS INFLUENCE INVESTMENT DECISIONS.

List several types of investments.

Identify factors involved in making investmentdecisions.

STUDENTS WILL COMPREHEND THE FACTORSINVOLVED IN MAKING INVESTMENT DECI-SIONS.

Give examples of fixed and variable incomeinvestments.

Give examples of factors affecting investmentdecisions.

Summarize the advantages and disadvantagesof various types of investments.

As a class, investigate and report on the differenttypes of investment plans and their features, includ-ing get-rich-quick schemes. (5.3) Next, have studentsidentify investments of which they are aware and listthese on the board. Following a reading assignment,add to the list, and then classify each listing as fixed,variable, or a combination of both.

Discuss reasons for investing, including nonmone-tary gain such as travel. Then assign students ingroups to research specific types of investments andreport the advantages and disadvantages of suchinvestments to the class. Follow up with a classdiscussion on various personal and economic consid-erations when making investment decisions.

SECOND LEVEL

STUDENTS WILL BE ABLE TO APPLY INVEST-MENT DECISIONS TO PRESENT AND FUTUREFINANCIAL PLANNING.

Compute the anticipated rate of return onspecific investments.

Prepare investIne lific situations.

Modify .5pendinf5decisions.

.,.ude investment

STUDENTS WILL BE ABLE TO ANALYZE THEEFFECTS OF INVESTMENT DECISIONS ON FU-

TURE FINANCIAL SECURITY.

Illustrate how investment plans affect financialstability.

Select an investment plan to meet specific situa-tions.

Point out potential problems of various invest-ment plans.

Using various types of investments, have studentsfigure how the amount and regularity of payment orpurchase affect the rate of return.

Invite a panel of investment consultants to explainthe products and services they represent. Discuss:potential risk and anticipated return from varioustype:; of investments, reasons for investing, limita-tions or restrictions on various types of investments.Based on personal goals, needs and economic condi-tions, have students choose the most appropriate typeof investment for their present and future situations.Review financial plans to verify that choices areappropriate.

THIRD LEVEL

STUDENTS WILL BE ABLE TO FORMULATE IN-VESTMENT PLANS WHICH MEET PRESENTAND FUTURE FINANCIAL NEEDS.

Devise an investment plan that utilizes bothfixed and variable income investments.

Modify an investment decision based on in-fluencing factors in specific situations.

STUDENTS WILL BE ABLE TO jr THE ADE-QUACY OF INVESTMENT DECISIONS FORPRESENT AND FUTURE FINANCIAL PLAN-NING.

Interpret the consequences of a number of in-vestment plans.

Compare a number of investment plans in termsof specific criteria.Justify the selection of either fixed or variableinvestments for given situations.

Have students review inflationary trends for the pastthree years and project the anticipated inflationaryrate for the next ten years. Based on projected fig-

32

ures, ask students to explore various types of invest-ments, including collectibles and commodities, andplan investment portfolios to meet this projection.

Review various investment returns in terms of tax

implications and varying income levels. Ask studentsto select the type of investment that ',..-7ovides thegreatest after-tax return for each situation and de-fine the selection in terms of the potential disadvan-tages of other types of investments.

Types of investmentsFixed income investments

Credit union sharesNotes and debenturesCertificates of deposit (CD)Corporate and municipal bonds.

Includes state bonds (tax free,taxable)

Endowment insuranceU S Savings Bonds (Series EE and H)Certain types of tax sheltered annu-

ities (TSA), Keogh plans, indivi-dual retirement annuities (IRA)

Variable income investmentsCommon stocksBusiness (single proprietorship,

partnership, corporation or''co-op**)

Real estate (rentals or mortgages)Commodities (eg, gold, silver, dia-

monds)

CollectiblesCertain types of tax sheltered annu-

ities (TSA), Keogh plans, individ-ual retirement annuities (IRA)

Money market instruments

Factors affecting investment decisionsNeeds and wantsGoals (short- and long-term)Amount of discretionary incomeAttitude toward investmentCompatibility with previously established

savings and insurance plansCriteria for choosing an investment

SafetyPriceAnticipated rate of return (growth,

income)Liquidity

Economic conditionsTax implications (2.8)

33

3 6

2.6 Insurance

FIRST LEVEL

STUDENTS WILL KNOW THE WAYS THAT IN-SURANCE PROVIDES FOR ECONOMIC PROTEC-TION.

Identify types of insurance protection needed.

List the steps in planning for insurance needs.

List types of insurance available.

Identify points to consider when planning insur-ance programs.

STUDENTS WILL COMPREHEND THE COMPO-NENTS INVOLVED IN A BALANCED INSUR-ANCE PROGRAM.

Distinguish which types of auto insurance arerequired by law and which are not.

Paraphrase the benefits available throughspecific types of health, accident and incomereplacement insurance plans.

Give examples of permanent and temporary lifeinsurance plans.

Explain the protection provided by a specifictype of home and auto insurance.

Have students compose a humorous skit illustratingall the different risks a person might run into in oneday. Which risks might one be insured against? Havethe class discuss the concept of insurance and decidethe type of insurance which might be best suited foreach risk. Discuss considerations in planning for in-surance needs and prepare a checklist on the board.

Have a student committee invite an insurance repre-sentative to class to discuss different types of lifeinsurance plans, as well as individual and familyneeds for life insurance. Discuss important points toremember when planning insurance programs.

As a class, discuss the current cost of hospitalizationafter examining a representative hospital statementfor a broken leg, birth of a child, etc. Identify thetypes of medical insurance provided by various groupplans and private carriers.

Discuss various types of auto insurance plans and thecoverage provided by each. Determine which are re-quil by Oregon statute and which are at the option

of the insured party. Invite an auto insurance agentto class to discuss auto insurance for teenagers. In-clude the importance of a good driving record andother factors which influence insurance rates.

Discuss various types of home and personal propertyinsurance and identify those which non-homeownersmight need.

SECOND LEVEL

STUDENTS WILL BE ABLE TO PLAN FOR IN-SURANCE NEEDS FOR SPECIFIC SITUATIONS.

Compute the costs and benefits of specific insur-ance plans.

Predict how personal factors affect insuranceneeds and costs.

*STUDENTS WILL BE ABLE TO ANALYZE HOWSPECIFIC TYPES OF INSURANCE MEET PER-SONAL INSURANCE NEEDS.

Select home and personal property insuranceaccording to specific circumstances.

Select life insurance according to specific cir-cumstances.

Select auto insurance according to legal require-ments and specific circumstances.

Outline the costs and benefits offered by severalhealth insurance programs made availablethrough employment.

Prepare a chart showing the major features of vari-ous forms of life, health, home and auto insuranceand discuss factors which influence rates. Then,utilizing hypothetical case studies depicting a varietyof individual and family situations, and economicconditions, plan for the least expensive coverage tomeet minimum needs for home, life, auto and healthinsurance.

Compute the cost of first dollar coverage, deductibleand major medical plans and determine which plan ismost appropriate and economical, considering protec-tion provided through employment. As a follow-up,have students debate the effects of various personalfactors on insurance costs, including health habits,lifestyle, driving record, etc.

34

THIRD LEVEL

STUDENTS WILL BE ABLE TO FORMULATE IN-SURANCE PLANS BASED ON PRESENT AND FU-TURE NEEDS.

Design insurance plans for individuals andfamilies in different situations.

Create several insurance plans to meet similarsituations.