Embed Size (px)

Citation preview

DOE Phase 1 SBIR Budget Justification Training"!Dave Donley // ReliAscent, LLC!DOE Phase 0 Program // December 17, 2014!"

INTRODUCTION/OUTCOMES Presenter Introduction Major Topics

• DOE Budget Justification Form • Introduction to indirect rates

Outcomes • Understand the data call requirements and approach for

each budget element • Highlight key factors in developing indirect rates

Pause for Questions

INTRODUCTION/OUTCOMES

You are here

Budget Justification Research and Related Budget Form

• Program budget form • Common Grants.gov budget form • Accompanies RR 424 form

Budget Justification Form • RR Budget Form, Section K • Word Document • Addresses 5 major cost types

Budget Justification

Labor Equipment Travel Other Direct Costs (ODC)

• Includes STTR partner Indirect Costs Note: Regulatory genesis – FAR Part 15, Table 15-2 Common to all negotiated acquisitions

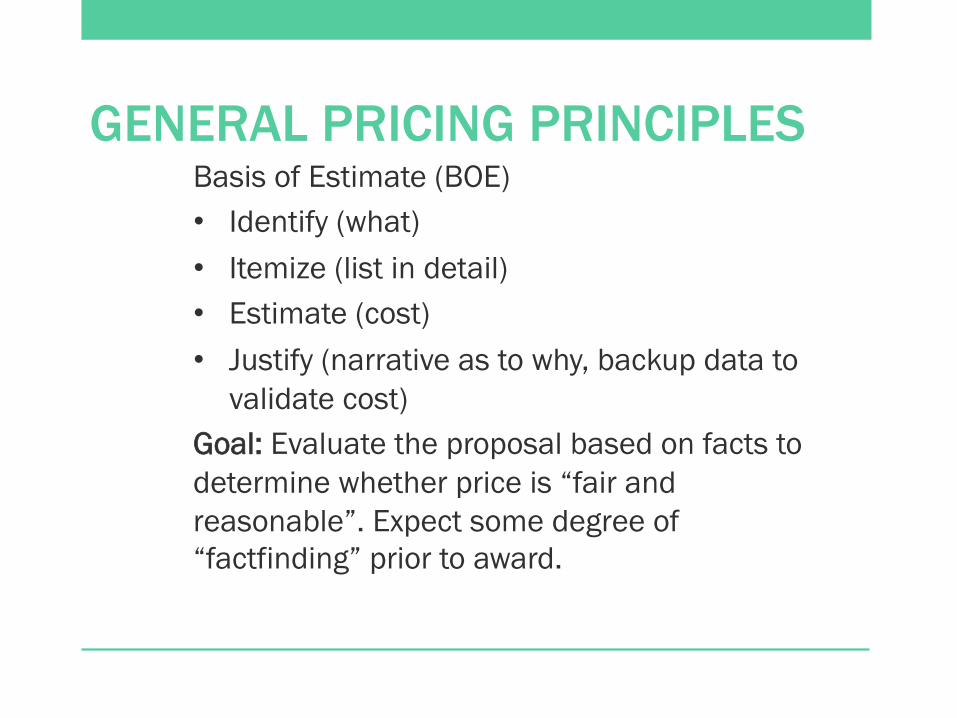

GENERAL PRICING PRINCIPLES

Basis of Estimate (BOE) • Identify (what) • Itemize (list in detail) • Estimate (cost) • Justify (narrative as to why, backup data to

validate cost) Goal: Evaluate the proposal based on facts to determine whether price is “fair and reasonable”. Expect some degree of “factfinding” prior to award.

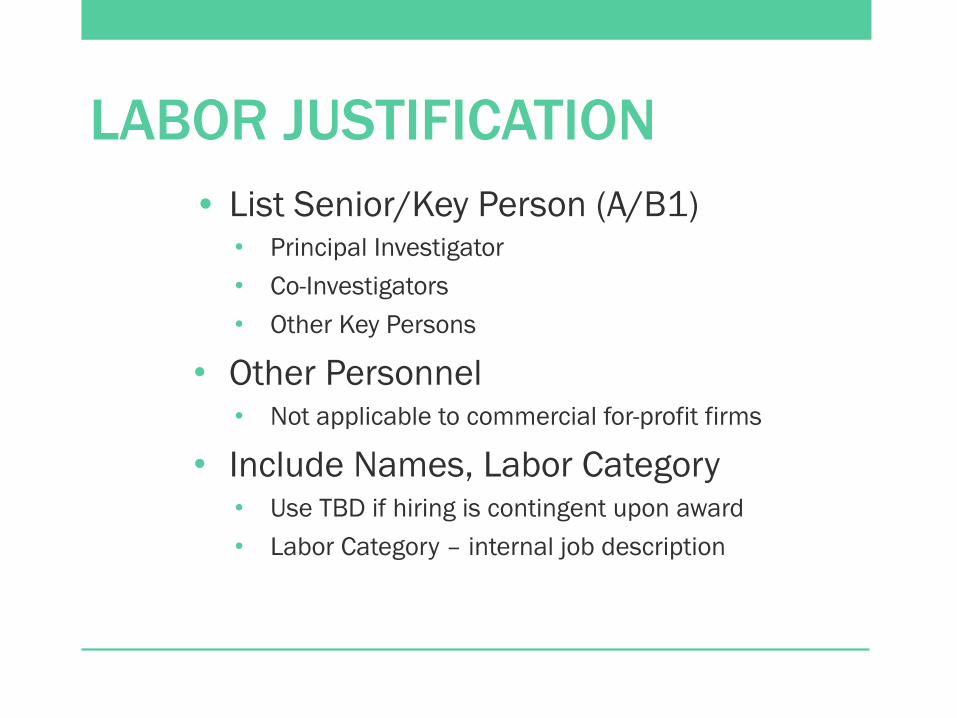

LABOR JUSTIFICATION • List Senior/Key Person (A/B1)

• Principal Investigator • Co-Investigators • Other Key Persons

• Other Personnel • Not applicable to commercial for-profit firms

• Include Names, Labor Category • Use TBD if hiring is contingent upon award • Labor Category – internal job description

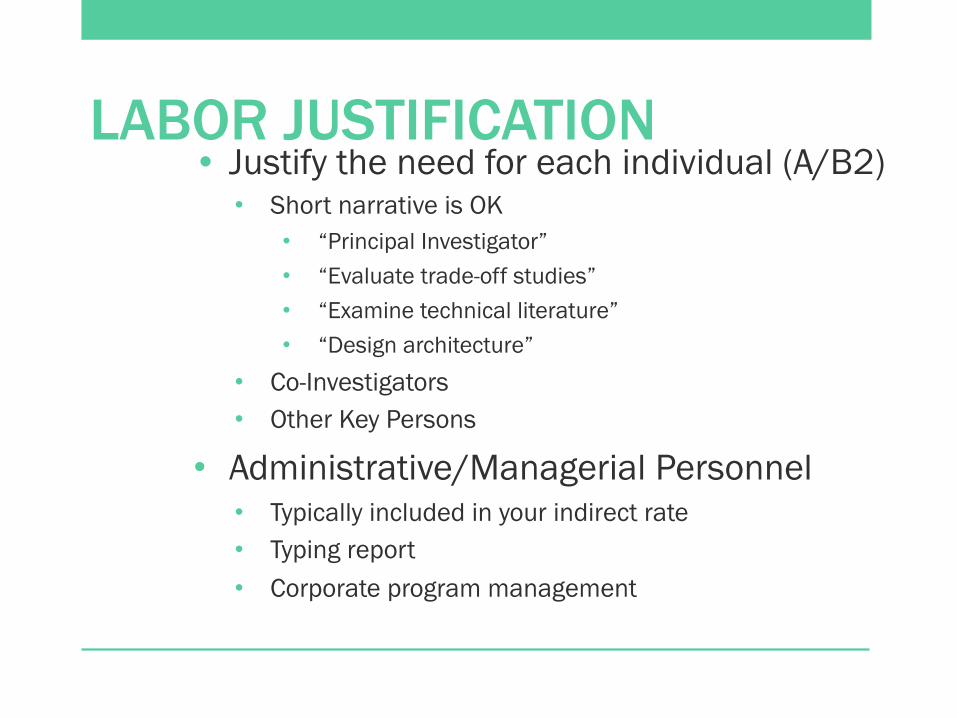

LABOR JUSTIFICATION • Justify the need for each individual (A/B2)

• Short narrative is OK • “Principal Investigator” • “Evaluate trade-off studies” • “Examine technical literature” • “Design architecture”

• Co-Investigators • Other Key Persons

• Administrative/Managerial Personnel • Typically included in your indirect rate • Typing report • Corporate program management

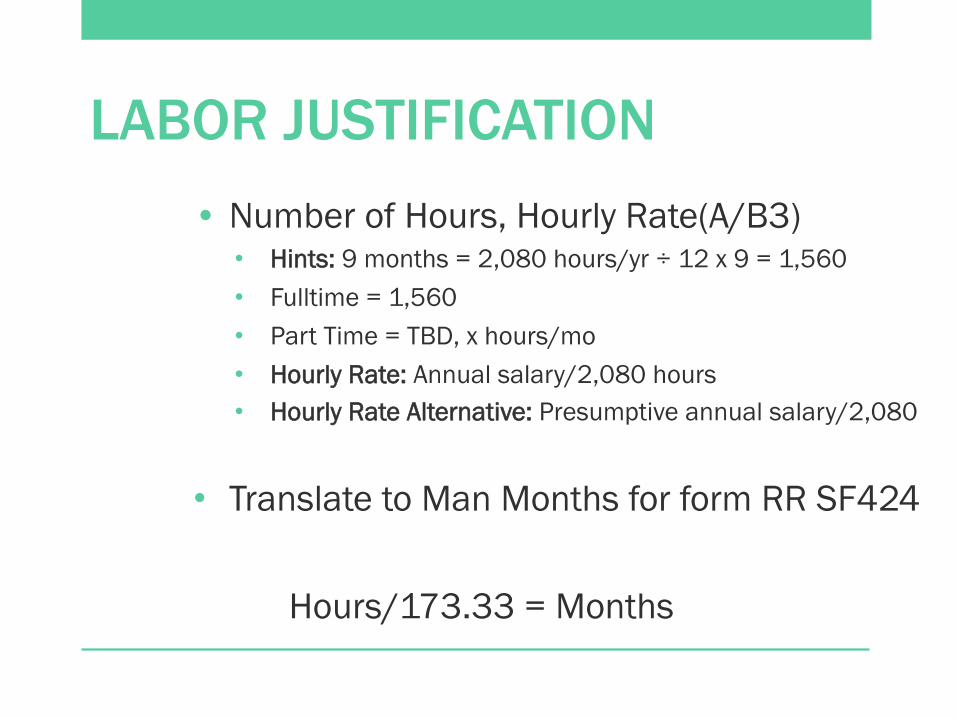

LABOR JUSTIFICATION • Number of Hours, Hourly Rate(A/B3)

• Hints: 9 months = 2,080 hours/yr ÷ 12 x 9 = 1,560 • Fulltime = 1,560 • Part Time = TBD, x hours/mo • Hourly Rate: Annual salary/2,080 hours • Hourly Rate Alternative: Presumptive annual salary/2,080

• Translate to Man Months for form RR SF424

Hours/173.33 = Months

LABOR JUSTIFICATION • Identify Basis of Labor Rate (A/B4)

• “Check stub helpful, but is not enough” • Defend reasonableness

• Salary Justification • Recent proposal reviews from others • Recent or current billings to other clients • Past employment labor rate • Competitors or suppliers • General statement: “Labor rates for each labor category

are within the range of labor rates given the particular education, skills, and experience of each individual, and based on our geographic location, business type and size.”

• Salary surveys

LABOR JUSTIFICATION • Salary Surveys

• Published surveys that are available for the general public to purchase regardless of participation in the survey.

• Private surveys based upon data from survey company clientele and which only participants may purchase.

• Bureau of Labor Statistics - http://www.bls.gov/ncs/ • Contractor self-conducted surveys. • Free on-line salary surveys are not considered

independent or objective. (DCAAM 5-808(c)(2)).

LABOR JUSTIFICATION

• Worst Case Scenario • You are responsible for justifying labor rates are fair

and reasonable. • Government does have similar evaluation tools. • You may be awarded with labor rates different than

proposed.

LABOR JUSTIFICATION

• Fringe (A/B5) • Address only if separately proposed as a direct cost.

(“See Indirect Rates.”) • Will address later in this and other webinars.

EQUIPMENT (C) Definition

• …an article of tangible, nonexpendable, personal property, including exempt property, charged directly to the award, having a useful life of more than one year and an acquisition cost of $5,000 per unit or more. Items of equipment to be leased or purchased must be described and justified in this section. Title to equipment purchased under this award lies with the government. It may be transferred to the grantee where such transfer would be more cost effective than recovery of the property by the government. (FOA pg 37).

EQUIPMENT (C) Concepts

• Preference is for contractors/grantees to buy this • C(1) – Itemize and justify the need

• Only useful on this project and perhaps a Phase 2 • No apparent future use after Phase 2 or on other

potential projects • Equipment is government property

• Complex ownership, control, and usage rules • Avoid if possible • C(2/3) – Estimate cost and include backup

• Quotes, catalog pricing, past purchases of exact or similar items

TRAVEL (C) Elements

• Airfare • “per diem” allowance • Maximum lodging allowance • Mileage • Rental cars • Other expenses • Travel time

See FAR 31.205-46 for details

TRAVEL (C) See FAR 31.205-46 for details

• “Costs for lodging, meals, and incidental expenses may be based on per diem, actual expenses, or a combination thereof, provided the method used results in a reasonable charge.”

• Maximum per diem (meals and incidentals) and lodging rates per Federal Travel Regulations (FTR) published by GSA. (DoD uses Joint Travel Regulations (JTR)).

• “Airfare costs (reflecting) the lowest priced airfare available to the contractor during normal business hours …”

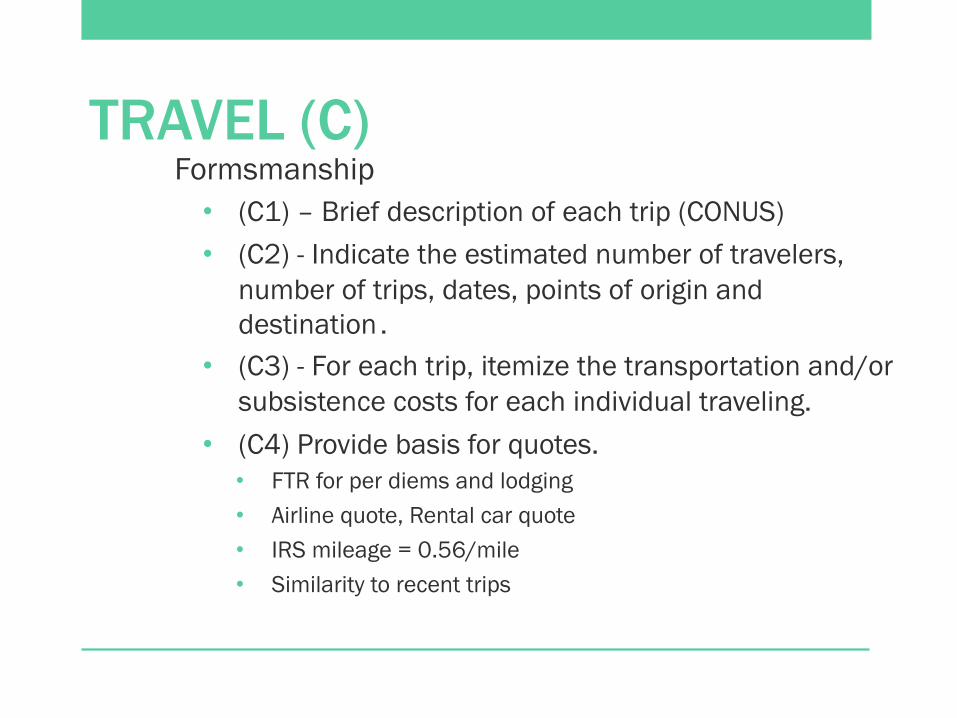

TRAVEL (C) Formsmanship

• (C1) – Brief description of each trip (CONUS) • (C2) - Indicate the estimated number of travelers,

number of trips, dates, points of origin and destination .

• (C3) - For each trip, itemize the transportation and/or subsistence costs for each individual traveling.

• (C4) Provide basis for quotes. • FTR for per diems and lodging • Airline quote, Rental car quote • IRS mileage = 0.56/mile • Similarity to recent trips

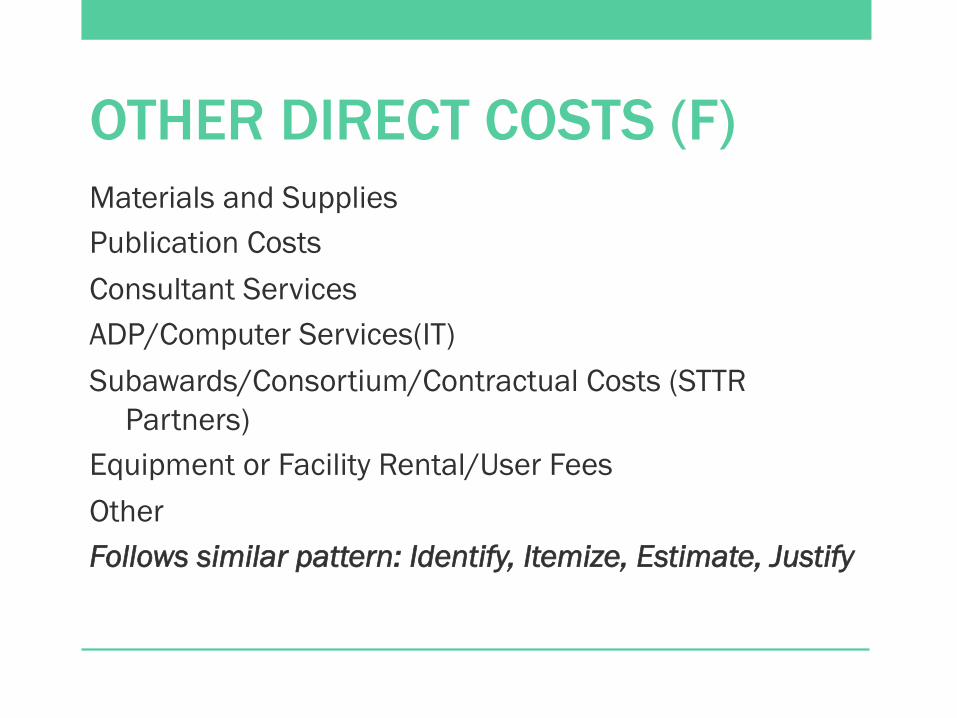

OTHER DIRECT COSTS (F) Materials and Supplies Publication Costs Consultant Services ADP/Computer Services(IT) Subawards/Consortium/Contractual Costs (STTR

Partners) Equipment or Facility Rental/User Fees Other Follows similar pattern: Identify, Itemize, Estimate, Justify

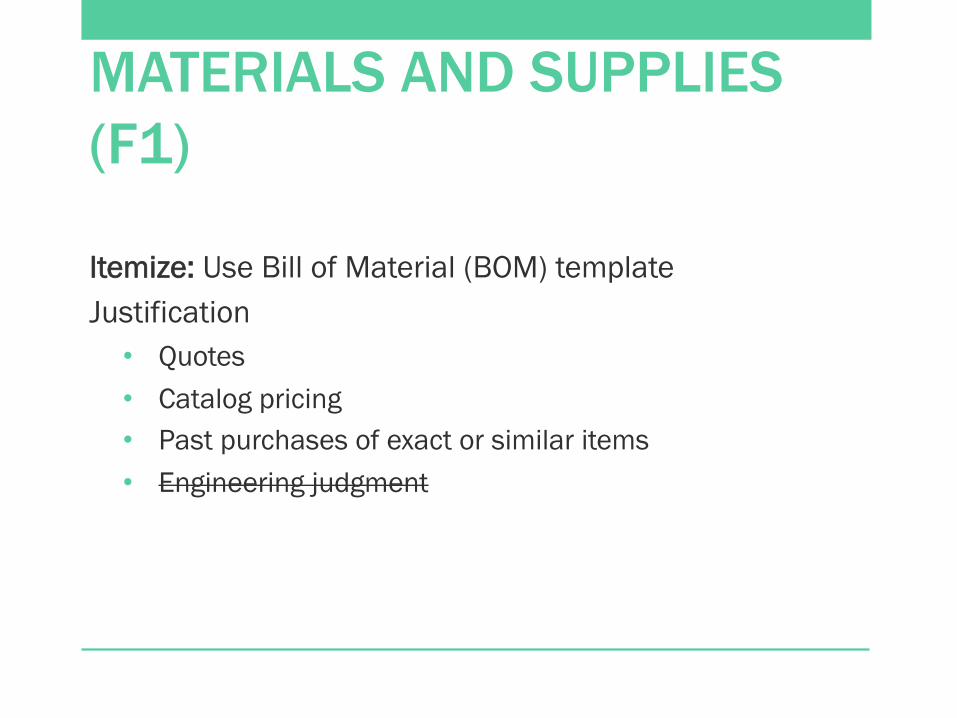

OTHER DIRECT COSTS MATERIALS AND SUPPLIES (F1)

Itemize: Use Bill of Material (BOM) template Justification

• Quotes • Catalog pricing • Past purchases of exact or similar items • Engineering judgment

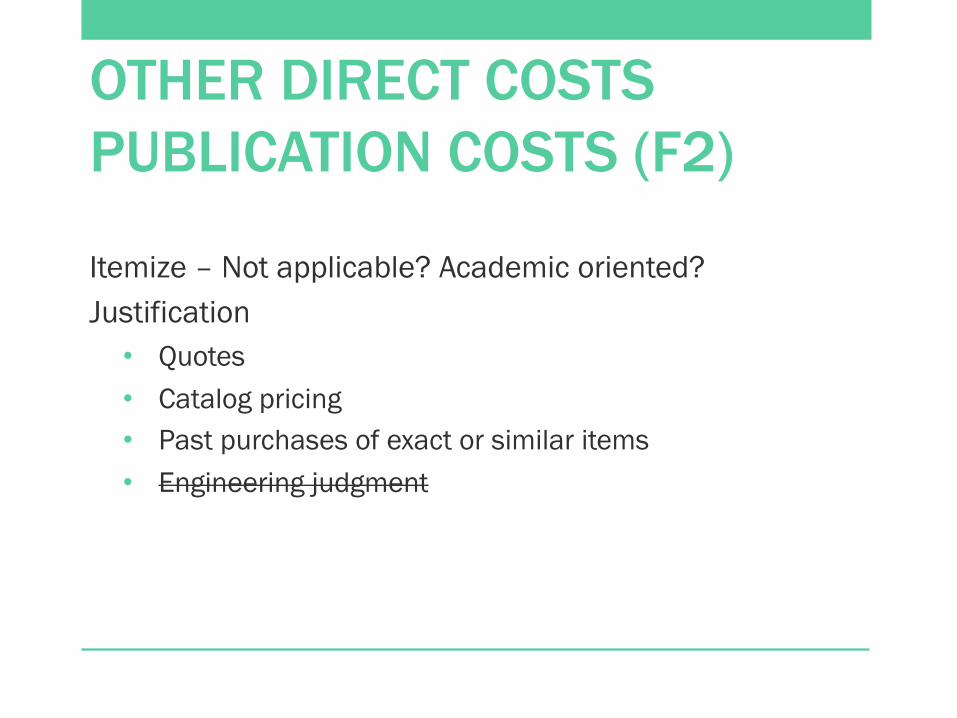

OTHER DIRECT COSTS PUBLICATION COSTS (F2)

Itemize – Not applicable? Academic oriented? Justification

• Quotes • Catalog pricing • Past purchases of exact or similar items • Engineering judgment

OTHER DIRECT COSTS CONSULTANTS (F3)

Special pricing data required: • As defined at FAR 31.205-22, consultant services (i.e.

professional services) as those services by persons who are members of a particular profession or possess a special skill that the contractor does not possess internally.

• Identify the firm/individual (a) • Estimated hours and hourly rate (b)

OTHER DIRECT COSTS CONSULTANTS (F3) Special pricing data required:

• (c)Documentation should include a signed letter from the consultant confirming agreement to perform the labor hours proposed, at the payment rate listed, and should provide verification that this rate is consistent with, or more favorable than, recent billings for similar work, e.g., copies of paid invoices.)

• If consultant is a new source, request consultant certify that the rate is consistent with, or more favorable than, recent billings for similar work.

• If a current consultant, produce an invoice.

OTHER DIRECT COSTS ADP/COMPUTER SERVICES/IT (F4)

What it is • Novel or state-of-the-art computing capability not

possessed by the contractor/grantee What it is not

• License or subscription-based software or services supporting all projects or administrative operations

OTHER DIRECT COSTS ADP/COMPUTER SERVICES/IT (F4)

Itemize (a) Justification (b)

• Quotes • Catalog pricing • Past purchases of exact or similar items • Engineering judgment

OTHER DIRECT COSTS SUBAWARDS (F5) STTR Partners Non-STTR Partners

• Other than an individual (consultant) • Substantial performance • Flowdown prime grant clauses to preserve government

rights Required to fill out the same DOE budget forms

OTHER DIRECT COSTS SUBAWARDS (F5)

• Describe the support and/or the services to be acquired. (a)

• Provide a brief justification for the use of the research institution or other subcontractor selected. (b)

• State the amounts of time to be devoted to the project, and the costs that will be charged to this award. (c)

OTHER DIRECT COSTS SUBAWARDS (F5)

• For professional services contracts, state the number of hours to be devoted to the project, and the costs that will be charged to this award. (d)

• Submit the research institution or other subcontractor documentation together with your written review comments confirming your determination of the reasonableness and acceptability of each element of the proposed budget. (e)

OTHER DIRECT COSTS SUBAWARDS (F5) • What does that mean?

• Cost analysis • Role reversal – you are now the buyer • Apply these same concepts in evaluating the subaward • May get into “proprietary financial data” issues

OTHER DIRECT COSTS SUBAWARDS (F5) Your review comments on the subaward should address

and substantiate the following: 1. Was the subaward competed or a market survey

performed? If so, what were the factors in selecting the subawardee?

2. Are the hours proposed adequate or reasonable for the effort described?

3. Are the labor rates within what you might pay for similar services? Are they approved by a gov’t agency?

4. Are other non-labor costs justified with a vendor quote or other objective evidence?

5. Are indirect rates approved by the government?

OTHER DIRECT COSTS SUBAWARDS (F5)

Special instructions for subawards to DOE National Labs • Paperwork lead time

OTHER DIRECT COSTS EQ/FAC RENTAL, OTHER (F6&7) As with IT, leading-edge services may be required from a

specialized source. Itemize Justification

• Quotes • Catalog pricing • Past purchases of exact or similar items • Engineering judgment

FREQUENTLY ASKED QUESTIONS

Where do I put sales tax or shipping for items received? Taxes and shipping can be considered a cost of an item. Also, direct purchases for resale to the government are usually exempt from sales tax.

Where do I charge the word processing and editing of the final report? This is typically considered an administrative indirect cost, although if consistently applied, it could be charged direct to the project.

Where do I estimate my travel time, especially if it’s beyond a typical 8 hour day? You are required to record all your time “on-the-job” which would include all travel. Travel time should be estimated as labor.

Will DOE pay for patent applications? No, not during the Phase 1, but they will during Phase 2.

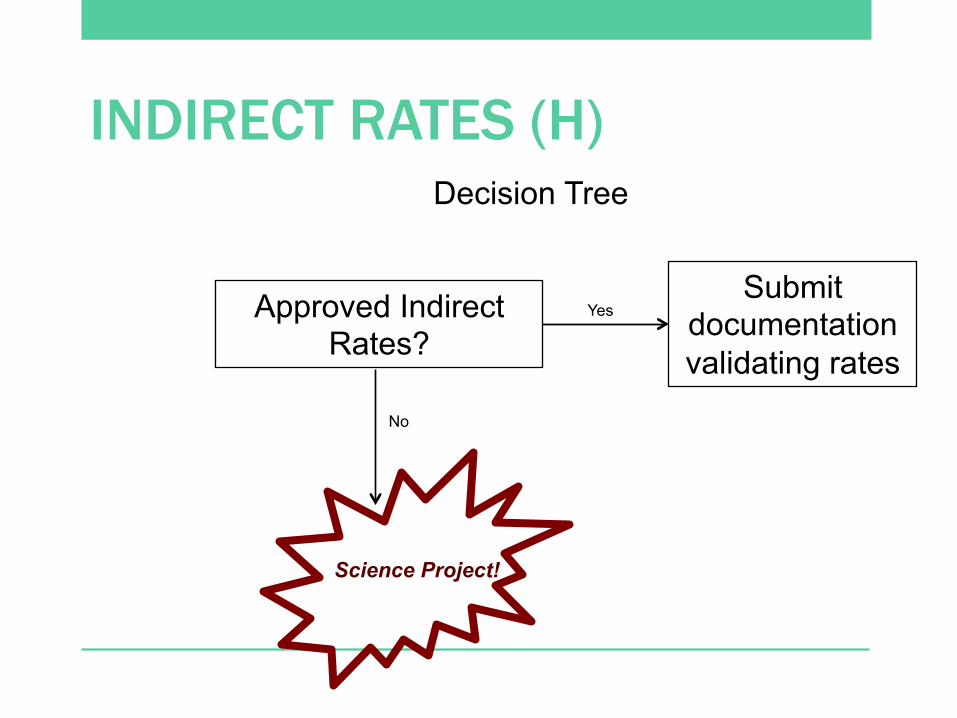

INDIRECT RATES (H)

Decision Tree

Approved Indirect Rates?

Submit documentation validating rates

Yes

No

Science Project!

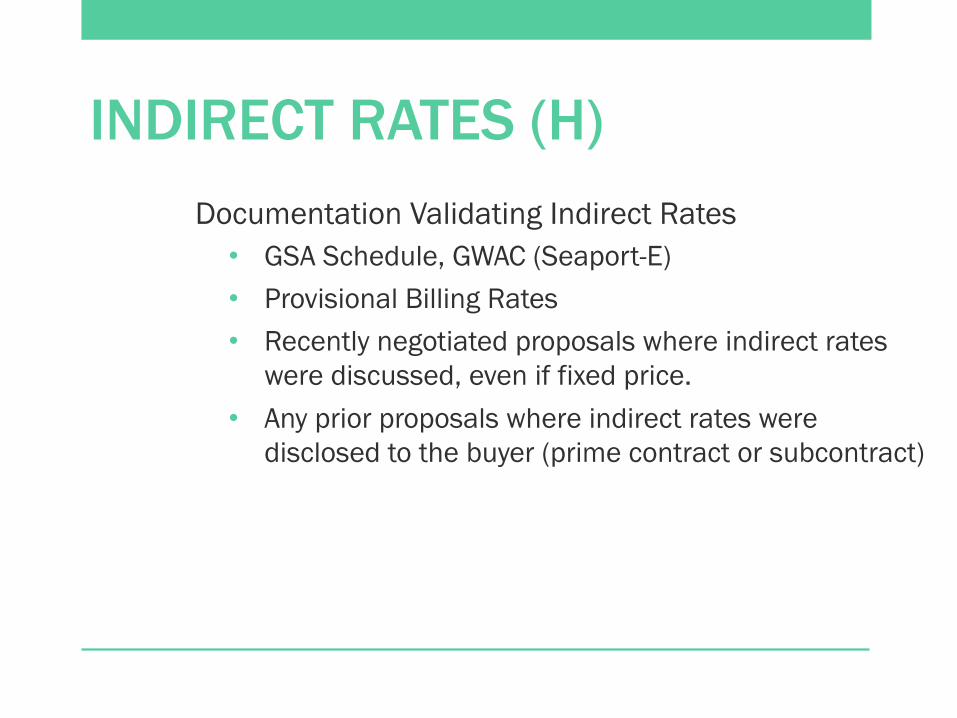

INDIRECT RATES (H) Documentation Validating Indirect Rates

• GSA Schedule, GWAC (Seaport-E) • Provisional Billing Rates • Recently negotiated proposals where indirect rates

were discussed, even if fixed price. • Any prior proposals where indirect rates were

disclosed to the buyer (prime contract or subcontract)

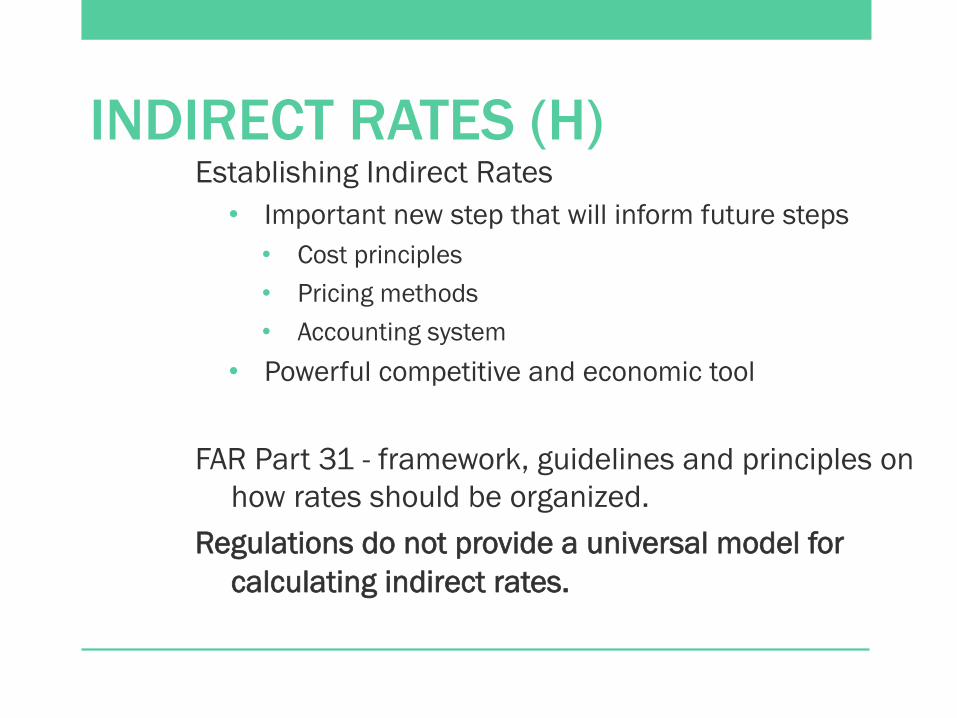

INDIRECT RATES (H) Establishing Indirect Rates

• Important new step that will inform future steps • Cost principles • Pricing methods • Accounting system

• Powerful competitive and economic tool

FAR Part 31 - framework, guidelines and principles on how rates should be organized.

Regulations do not provide a universal model for calculating indirect rates.

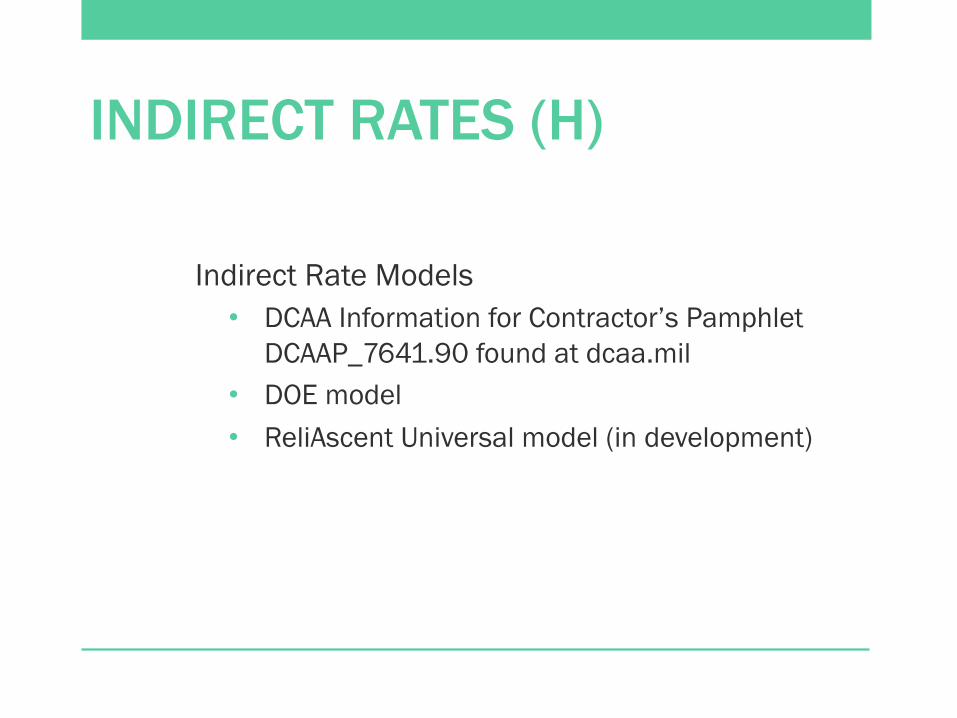

INDIRECT RATES (H)

Indirect Rate Models • DCAA Information for Contractor’s Pamphlet

DCAAP_7641.90 found at dcaa.mil • DOE model • ReliAscent Universal model (in development)

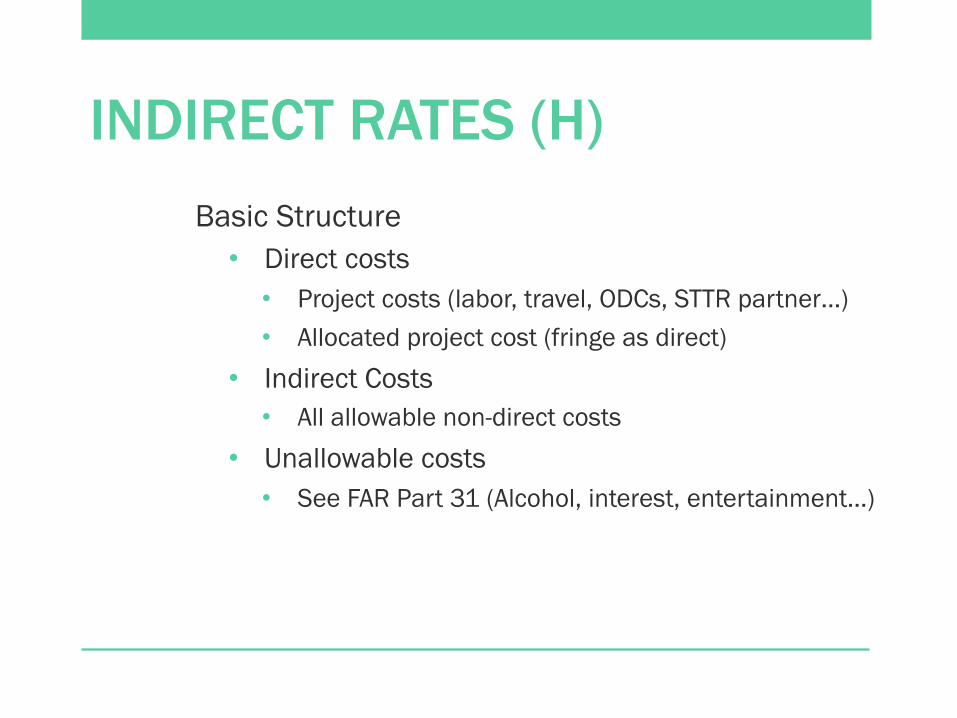

INDIRECT RATES (H) Basic Structure

• Direct costs • Project costs (labor, travel, ODCs, STTR partner…) • Allocated project cost (fringe as direct)

• Indirect Costs • All allowable non-direct costs

• Unallowable costs • See FAR Part 31 (Alcohol, interest, entertainment…)

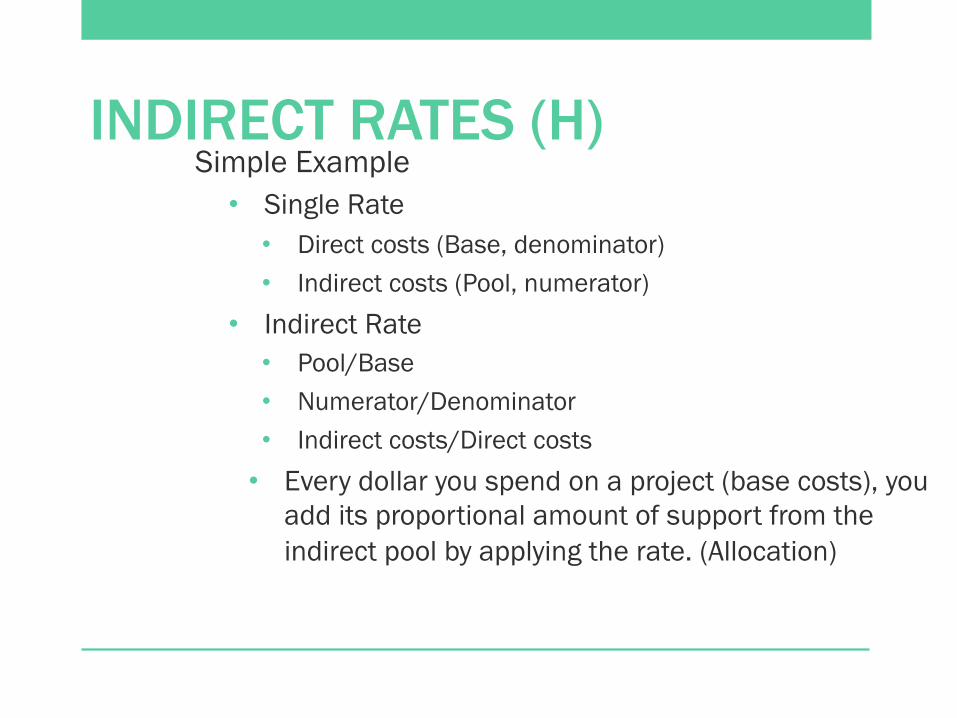

INDIRECT RATES (H) Simple Example

• Single Rate • Direct costs (Base, denominator) • Indirect costs (Pool, numerator)

• Indirect Rate • Pool/Base • Numerator/Denominator • Indirect costs/Direct costs

• Every dollar you spend on a project (base costs), you add its proportional amount of support from the indirect pool by applying the rate. (Allocation)

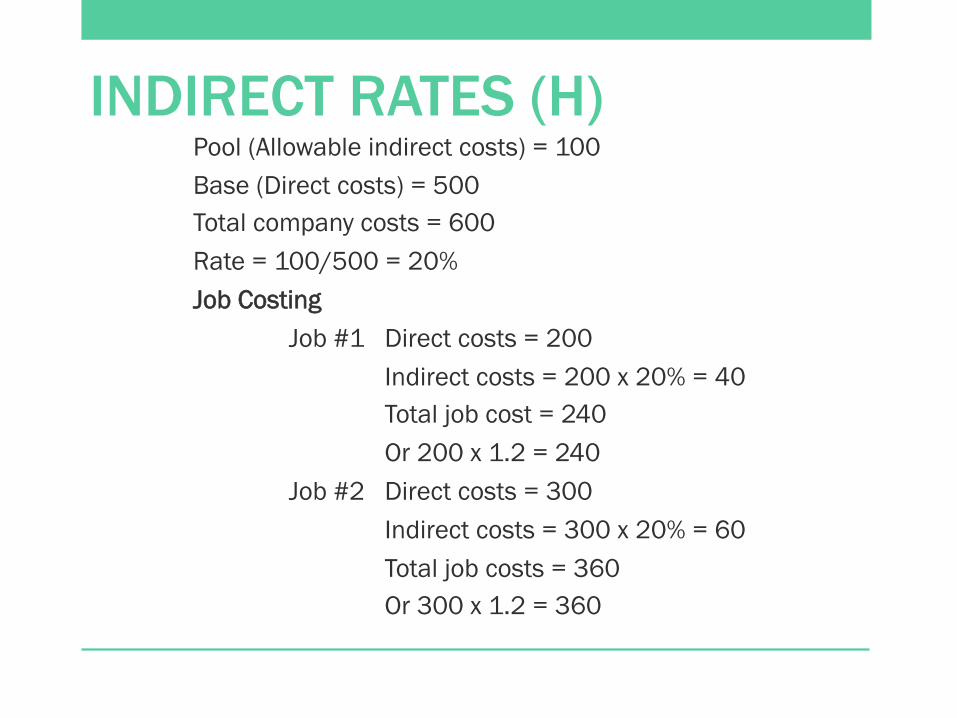

INDIRECT RATES (H) Pool (Allowable indirect costs) = 100 Base (Direct costs) = 500 Total company costs = 600 Rate = 100/500 = 20% Job Costing

Job #1 Direct costs = 200 Indirect costs = 200 x 20% = 40 Total job cost = 240 Or 200 x 1.2 = 240 Job #2 Direct costs = 300 Indirect costs = 300 x 20% = 60 Total job costs = 360 Or 300 x 1.2 = 360

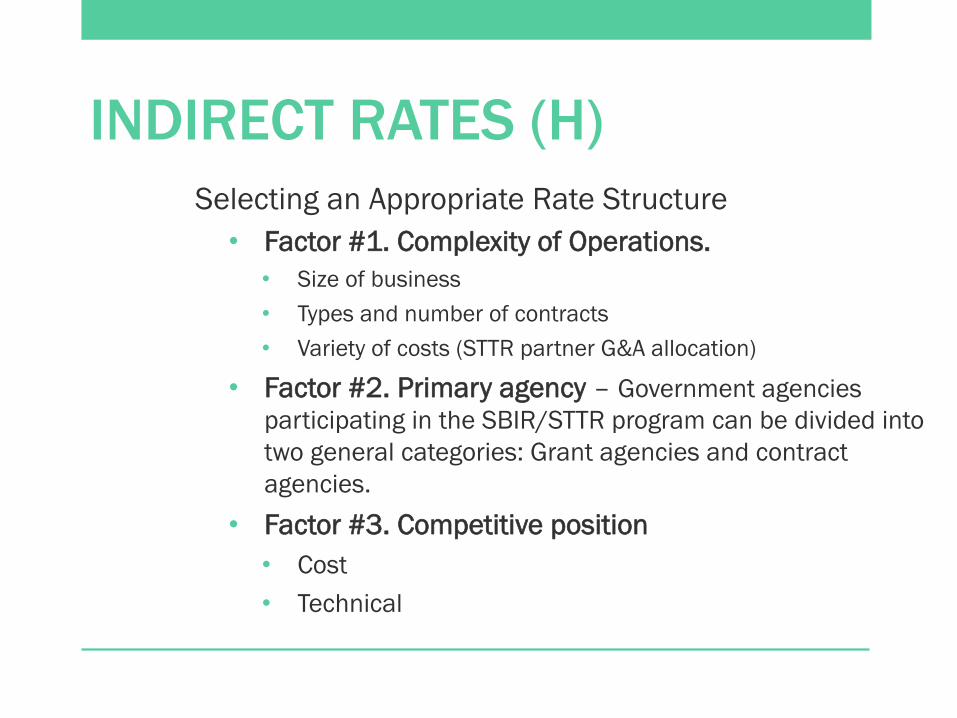

INDIRECT RATES (H) Selecting an Appropriate Rate Structure

• Factor #1. Complexity of Operations. • Size of business • Types and number of contracts • Variety of costs (STTR partner G&A allocation)

• Factor #2. Primary agency – Government agencies participating in the SBIR/STTR program can be divided into two general categories: Grant agencies and contract agencies.

• Factor #3. Competitive position • Cost • Technical

INDIRECT RATES (H)

So What’s a Good Rate? A good rate is one that allows the contractor to

meet its contractual obligations in its competitive environment while running and perpetuating its business. It also assures the government receives value for the goods and services it purchases.

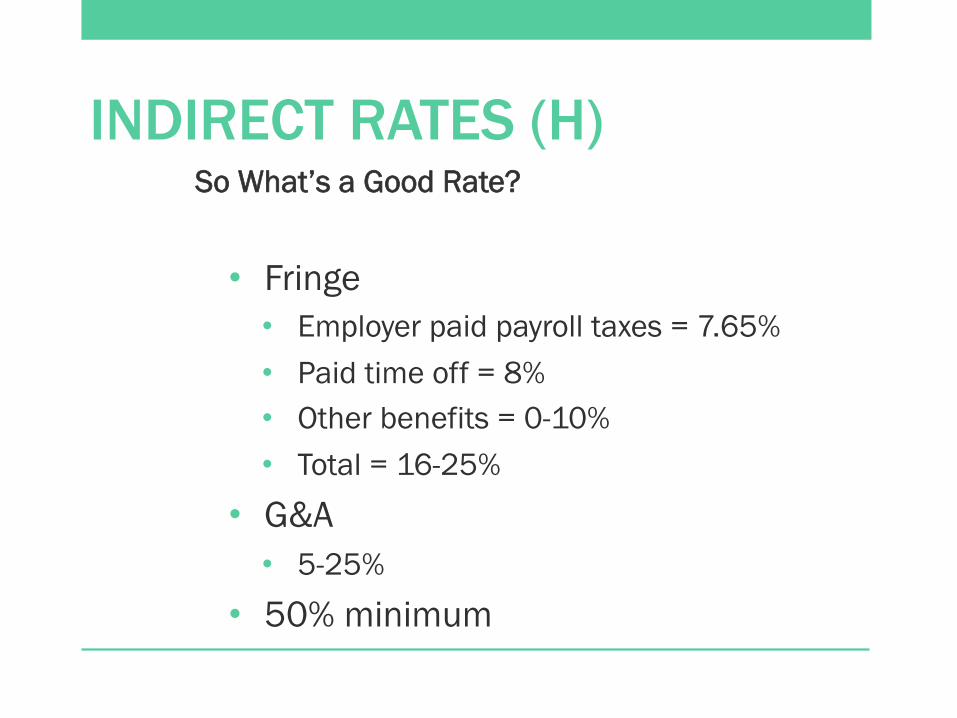

INDIRECT RATES (H) So What’s a Good Rate?

• Fringe • Employer paid payroll taxes = 7.65% • Paid time off = 8% • Other benefits = 0-10% • Total = 16-25%

• G&A • 5-25%

• 50% minimum

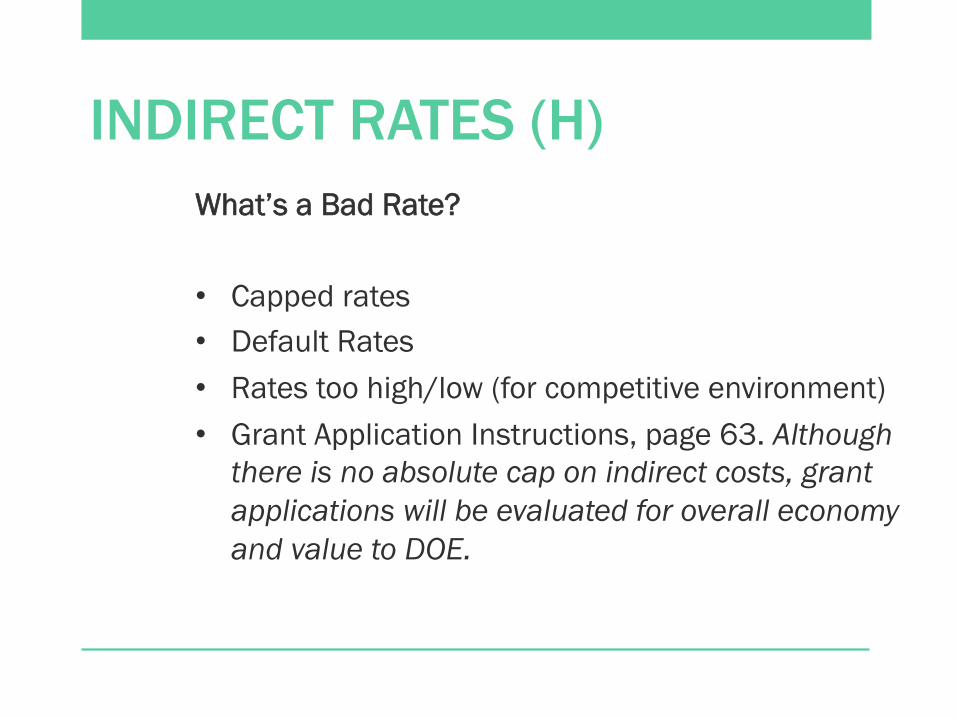

INDIRECT RATES (H) What’s a Bad Rate?

• Capped rates • Default Rates • Rates too high/low (for competitive environment) • Grant Application Instructions, page 63. Although

there is no absolute cap on indirect costs, grant applications will be evaluated for overall economy and value to DOE.

QUESTIONS? Questions later, Please feel free to contact us:

• Dave Donley • 303-999-3805 • 307-272-4841 • [email protected]

• Mike Anderson • 303-999-3802 • 303-475-4761 (cell) • [email protected]

www.ReliAscent.com

Today’s Presenters Dave Donley, Account Executive ReliAscent LLC Dave has a BS in Aeronautical Engineering and a Certificate in Government Contract Management from the National Contract Management Association (NCMA). He currently manages the needs of a number of DoD and non-DoD clients. Dave was a contract and subcontract manager for a small optics firm specializing in SBIR contracting. He also managed

a large contract issued by a prime government contractor for a major weapon system. He performed a number of financials management duties, including submitting budget proposals, managing billings, and supporting DCAA audits. Prior to that, Dave spent his early career as a Program Manager and Contract Administrator for large and small government contractors.

Mike Anderson, Vice President ReliAscent LLC Mike has a BS in Aerospace Engineering with an MBA in Finance. He has more than 30 years of experience with manufacturing companies with over 15 years of experience in government contracting. He has a broad base of experience from engineering to manufacturing to quality assurance to sales, marketing and business development. Mike has managed both prime government contracts as well as subcontracts and has experience in both the SBIR contract market as well as government contracts for direct products and services. Mike also has extensive experience in handling multi-million dollar high paced, high volume commercial product contracts.

PRESENTING COMPANY ReliAscent LLC was formed by the

merger of two of the naBon’s leading consulBng firms for helping small federal contractors with DCAA and other Federal regulatory compliance issues, mainly related to accounBng and contract administraBon. ReliAscent expands on that base by not only providing consulBng in those areas but by offering complete outsourced back office services to allow small businesses to completely focus on their core competencies and allow them to maximize their growth.

Services include, but are not limited to: • Outsourced full funcBon

accounBng (including CFO services)

• Outsourced contract administraBon

• Outsourced payroll funcBons

• Other back office services • Business consulBng

services