Embed Size (px)

Citation preview

Does China Have an Impact on Foreign Direct Investment to Latin

America?

Alicia García-Herrero and Daniel Santabárbara

Banco de España

WORLD BANK ABCD CONFERENCE

Amsterdam 21-22 May, 2005

2INTERNATIONAL ECONOMICS AND INTERNATIONAL RELATIONS DEPARMENT

ROADMAP TO PRESENTATION

1.Motivation

2.Determinants of FDI

3.Variables and data issues

4.Empirical methodology

5.Results

6.Policy implications

3INTERNATIONAL ECONOMICS AND INTERNATIONAL RELATIONS DEPARMENT

1. MOTIVATION

Rapid emergence of China as global player has consequences for the rest of the world

Particularly true for FDI being China a major recipient

FDI is key for Latin America– Most important

source of finance since mid 1990s

– Contribution to modernizing the economic structure

OBJECTIVE:Analyse empirically whether the emergence of China as a large recipient of FDI has affected the amount of FDI received by Latin

American countries

Source: Customs Administration of China, WEO database of the IMF

0

40

80

120

160

200

1993 1995 1997 1999 2001 2003

CHINA

LATIN AMERICA

EMERGING MARKETS

FDI INFLOWS

Billions of USD

4INTERNATIONAL ECONOMICS AND INTERNATIONAL RELATIONS DEPARMENT

1. MOTIVATION (cont’)

Whether FDI is diverted from Latin America to China may depend on:

1.Degree of integration of capital markets2.Substitution between FDI and other capital flows3.Objective of FDI to Latin American countries

– exports or domestic demand4.How much Chinese inward FDI increases imports

– especially commodities

EMPIRICAL QUESTION

5INTERNATIONAL ECONOMICS AND INTERNATIONAL RELATIONS DEPARMENT

1. MOTIVATION (cont’)

Existing evidence very scarce:– IADB (2004): Descriptive account of degree of coincidence

in FDI home countries– Chantasasawat et al. (2004): Impact of Chinese inward FDI

on Asia and Latin America• No impact on the level of Latin American inward FDI...• But negative impact on the share of FDI. However

– No country analysis, only region– Aggregate FDI data, not bilateral– Treatment of very important problem for this kind of

studies - potential endogeneity - can be improved– Strong assumptions, such as inelastic supply of capital

flows

6INTERNATIONAL ECONOMICS AND INTERNATIONAL RELATIONS DEPARMENT

2. DETERMINANTS OF FDI

No clear consensus for most variables:– Generally, the higher size, the more macroeconomic/

political stability and human capital and the better the institutions, the more inward FDI

• However, Haussmann challenges this view: Good cholesterol

– Non consensus on the relation between trade and FDI:• Complements or subtitutes?

– Also doubts on the role of push factors:• Home and global

– What about the impact of other FDI recipients?:• Complementarity or substitution?

7INTERNATIONAL ECONOMICS AND INTERNATIONAL RELATIONS DEPARMENT

3. VARIABLES AND DATA

Dependent variable:

– Annual bilateral FDI flows to

• Six largest Latin American countries: Argentina, Brazil, Chile, Colombia, Mexico and Venezuela

• From: OECD Countries

• Sample:1980-2001

• Source: OECD International Direct Investment Statistics

8INTERNATIONAL ECONOMICS AND INTERNATIONAL RELATIONS DEPARMENT

Objective variable: – Annual bilateral FDI flows to China

• OECD data: – Hong Kong, Macao, Taiwan or Singapore excluded from

home investor– Probably irrelevant for potential substitutability with Latin

America

– Taking into account:• FDI to Hong Kong (due to reinvesting)

– Separately and jointly

– Also check for role of similar economic structure with China• Two-digit manufactured value added data from UNIDO

3. VARIABLES AND DATA (cont’)

9INTERNATIONAL ECONOMICS AND INTERNATIONAL RELATIONS DEPARMENT

3. VARIABLES AND DATA (cont’)

Control variables:– (i) capital flows:

• Lag of FDI to Latin America (persistence)• Developments in portfolio and cross-border flows • Influence of competitors: OECD FDI to Latam, to China

and to Hong Kong• Regional decisions: FDI to whole Latin America• Other private capital flows

– (ii) bilateral variables• Bilateral nominal exchange rate• Host home interest rate differential • Bilateral exports• Bilateral imports• Similarity in productive structure

10INTERNATIONAL ECONOMICS AND INTERNATIONAL RELATIONS DEPARMENT

3. VARIABLES AND DATA (cont’)

Control variables (cont’):– (iii) host country factors

• Macroeconomic conditions• Size and natural resources• Institutional characteristics• Occurrence of financial crises

– (iv) home country variables • economic growth• GDP per capita

– (v) global factors• oil prices

11INTERNATIONAL ECONOMICS AND INTERNATIONAL RELATIONS DEPARMENT

3. VARIABLES AND DATA (cont’)

Two time spans– 1984-2001:

• After China started its “open door” policy• Maximum number of years given data limitations

– 1995-2001: • Structural change in FDI • Acceleration in negotiations for WTO membership

12INTERNATIONAL ECONOMICS AND INTERNATIONAL RELATIONS DEPARMENT

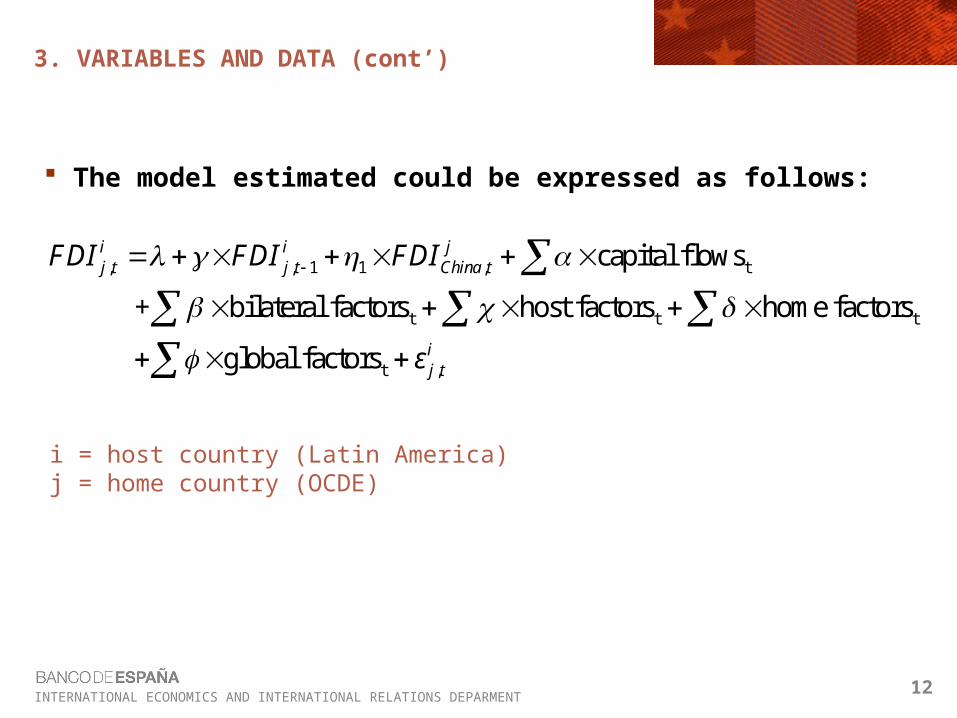

3. VARIABLES AND DATA (cont’)

The model estimated could be expressed as follows:

i = host country (Latin America)j = home country (OCDE)

, , 1 1 , t

t t t

t ,

capital flows

+ bilateral factors host factors home factors

global factors

i i jj t j t China t

ij t

FDI FDI FDI

ε

13INTERNATIONAL ECONOMICS AND INTERNATIONAL RELATIONS DEPARMENT

4. METHODOLOGY

Main challenges1. Endogeneity of

• Adjustment cost of capital – Lag of FDI GMM procedure

• other FDI flows• bilateral trade

2. Unobserved heterogeneity3. Choice of regressors

• Balance between degrees of freedom and problem of missing variables.

• From general to simple• More efficient unbiased estimators

14INTERNATIONAL ECONOMICS AND INTERNATIONAL RELATIONS DEPARMENT

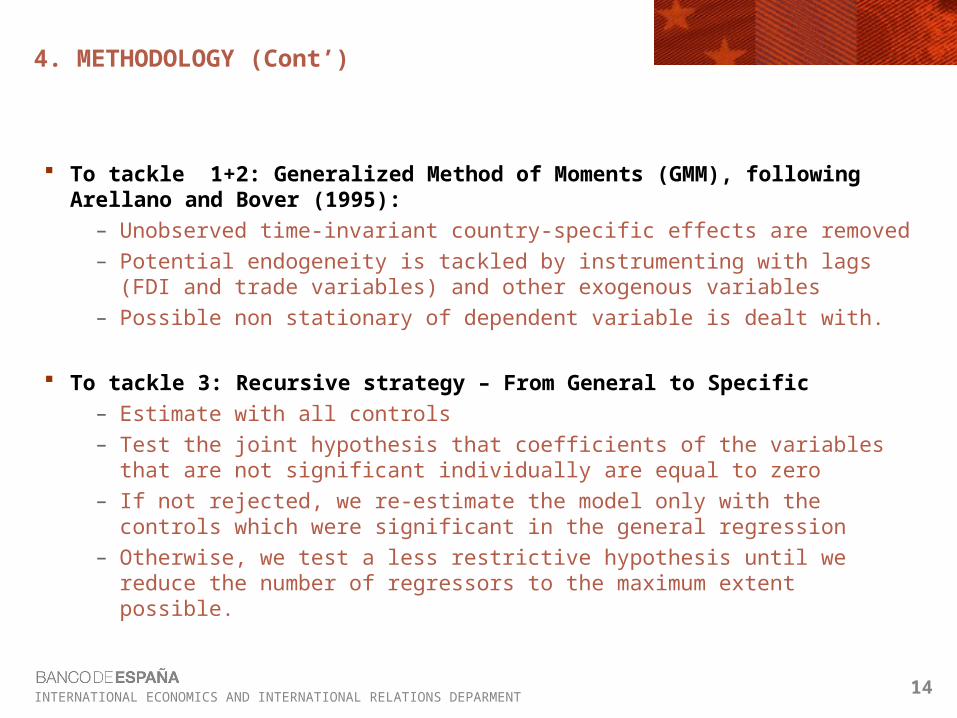

4. METHODOLOGY (Cont’)

To tackle 1+2: Generalized Method of Moments (GMM), following Arellano and Bover (1995):– Unobserved time-invariant country-specific effects are removed– Potential endogeneity is tackled by instrumenting with lags (FDI

and trade variables) and other exogenous variables– Possible non stationary of dependent variable is dealt with.

To tackle 3: Recursive strategy – From General to Specific– Estimate with all controls – Test the joint hypothesis that coefficients of the variables that

are not significant individually are equal to zero – If not rejected, we re-estimate the model only with the controls

which were significant in the general regression – Otherwise, we test a less restrictive hypothesis until we reduce

the number of regressors to the maximum extent possible.

15INTERNATIONAL ECONOMICS AND INTERNATIONAL RELATIONS DEPARMENT

5. RESULTS

Longer time span (1984-2001):– No substitution from Latin American inward FDI to

China • With all controls (column 1) and only with jointly

significant regressors (column 2)

– Argentina and Colombia negatively affected but small parameters and eventually not significant

• We cannot reject the hypothesis that the coefficients of each Latin American country are the same and equal to zero

In sum, no “Chinese effect” on Latin America in this time span

16INTERNATIONAL ECONOMICS AND INTERNATIONAL RELATIONS DEPARMENT

5. RESULTS (cont’)

Some other results:– Strong substitution effect between FDI and other

private capital flows– Regional effect in Latin American FDI– Complementarities between FDI and bilateral trade– Occurrence of banking crises appears to foster FDI

• Due to opening up to foreign investors after crisis?

– Other results are weaker: significant in general model but not in restricted one

• bilateral exchange rate• the debt service • Home GDP growth• Host GDP growth

17INTERNATIONAL ECONOMICS AND INTERNATIONAL RELATIONS DEPARMENT

5. RESULTS (cont’)

More recent time span (1995-2001)– Negative effect of Chinese inward FDI on that of Latin

America • With all controls and only with jointly significant ones

– Mexico and Colombia are the two countries for which Chinese inward FDI reduces FDI inflows in a significant way (at 99% confidence level for Mexico)

• When Chinese inward FDI increases Colombian and Mexican FDI is reduced about half.

• Given that Mexico’s FDI started to fall only in 2002 it should be read as the amount it could have grown more and did not!

– No negative effect on region when Mexico & Colombia excludedIn sum, negative “Chinese effect” in a more recent

time frame

18INTERNATIONAL ECONOMICS AND INTERNATIONAL RELATIONS DEPARMENT

5. RESULTS (cont’)

Results on control variables in more recent panel

– Previous results maintained but also:

– Bilateral exchange depreciation clearly significant in increasing FDI to Latin American countries

• Lower investment costs seems to weigh more than a reduction in the repatriated benefits

– Larger bilateral imports imply a lower level of Latin American FDI

• Supports the hypothesis of substitution between imports & FDI

• FDI is oriented towards domestic demand

19INTERNATIONAL ECONOMICS AND INTERNATIONAL RELATIONS DEPARMENT

6. POLICY IMPLICATIONS

Evidence of substitution from Latin American inward FDI to China’s coinciding with acceleration of WTO negotiations

– Results driven by Mexico and Colombia

– No impact on the rest

• We do not explore channels for this result but…

• Qquick look at sectoral FDI shows similarities with China, particularly for Mexico

China will probably continue to be a magnet for FDI

– Liberalization

– Privatization

– High return on capital from growth and productivity (given low labor costs)

20INTERNATIONAL ECONOMICS AND INTERNATIONAL RELATIONS DEPARMENT

6. POLICY IMPLICATIONS (cont’)

This may seem worrisome for Latin American countries

– Particularly those with a more similar productive/export(/FDI structure with China

But also tremendous opportunities in the medium term.

–Latin America in a worse position than Asia to reap some of these benefits, such as assembling and re-exporting of manufactured products.

–But will clearly benefit from China’s demand for raw materials: opportunities for FDI from OECD countries but also China!