Embed Size (px)

Citation preview

Does Country Regulation and Culture Explain International

Managers’ Metric Use in Marketing Mix Decisions?

Ofer Mintz

Imran S. Currim

July 2013

Ofer Mintz ([email protected]) is Assistant Professor of Marketing, E. J. Ourso College of

Business, Louisiana State University, Baton Rouge, LA 70803. Imran S. Currim

([email protected]) is Chancellor’s Professor at the Paul Merage School of Business, University

of California, Irvine, CA 92697. The authors would like to thank Mike Hanssens (UCLA),

Donna Hoffman (George Washington), John Hulland (Univ. of Georgia), and Ivan Jeliazkov,

Robin Keller, and Connie Pechmann (all of UCI) for their support and feedback throughout the

paper’s development and participants at the 2012 Theory + Practice in Marketing Conference at

the Harvard Business School and the 2013 Marketing Science Conference in Istanbul for their

comments. This research was supported by the Dean’s office of the Paul Merage School of

Business.

1

Does Country Regulation and Culture Explain International

Managers’ Metric Use in Marketing Mix Decisions?

Abstract

This paper extends Mintz and Currim’s (2013) conceptual framework on drivers of U.S.

managers’ metric use in marketing decisions by asking two unique questions. First, does country-level

regulation and culture, i.e., uncertainty avoidance, power distance, individualism, and long-term

orientation, explain differences in international managers’ metric use? Analysis of 1,704 marketing

decisions by 571 managers residing in 31 countries suggests managers in countries with increased

disclosure regulatory requirements, and greater uncertainty avoidant and long-term cultures, employ less

metrics. Second, are these country-level effects on metric use uniform across different managerial and

firm settings? Exploratory moderation analyses reveal marketing managers residing in less power distant

cultures employ less metrics in goods and market oriented firms lacking CMOs; while managers residing

in less individualistic cultures employ less metrics in B2C and goods oriented firms. Results allow

conditional expectation based assessments of managerial metric use for efficient targeting of metric

training and compensation programs.

Keywords: Metric Use; Marketing Decision Making; Culture; Survey; Multiple Regression

2

1. Introduction

There has been considerable concern about marketing’s decreasing influence in the firm (Rust et al.

2004), in the boardroom (Webster, Malter, and Ganesan 2005), and at the corporate strategy level

(McGovern et al. 2004). Marketing is increasingly viewed as a cost and not as an investment (Morgan and

Rego 2009). Strategically important aspects of marketing have moved to other functions in the

organization (Sheth and Sisodia 2005). Roles of financial managers have become more important than

marketing managers (Nath and Mahajan 2008), and the tenure of chief marketing officers only averages

22.9 months (Hyde, Landry, and Tipping 2004). One main reason identified for this decline in

marketing’s influence is its lack of accountability (Verhoef and Leeflang 2009). Further, global

competition, recession, and stock market pressures have only increased the demands for marketing

accountability (Lehmann and Reibstein 2006).

In response, marketing scholars have developed metrics for a variety of marketing mix decisions

(Ambler 2003, Farris et al. 2010, Lehmann and Reibstein 2006) and linked marketing mix efforts and

assets to financial metrics (see Srinivasan and Hanssens 2009 for a review). Despite valuable efforts,

there is no understanding of what drives managers residing in various countries to use metrics in their

marketing mix decisions. To the best of our knowledge, Mintz and Currim (2013) (henceforth MC) is the

only study to propose a conceptual model on drivers of managers’ metric use in marketing mix decisions1.

Their model focuses on U.S. managers and links managerial, firm, and environmental characteristics and

types of marketing mix decisions to metric use, but does not consider managers residing outside the U.S.

Consequently, no study, including MC (2013), has assessed (a) whether country level variables such as

regulation and culture drive international2 managers’ use of metrics and (b) whether the effects of

regulation and culture on managerial metric use are moderated by firm and managerial characteristics

(Figure 1).

1 The reader is referred to MC (2013) for a review of research on metrics for marketing mix decisions.

2 The words international and residing in various countries are used synonymously in this work.

3

Firms are increasingly expecting a larger proportion (on average a 20% increase) of their sales

from international markets (Moorman 2012), and there is a general expectation among top executives at

headquarters that all managers residing in different countries who make marketing decisions should

employ metrics regardless of the setting (country or firm) in which they operate, and the characteristics of

managers making marketing mix decisions (Farris et al. 2010). Hence, it is important for marketing

scholars and managers to ascertain whether country-level variables such as regulatory disclosure

requirements (La Porta, Lopez-de-Silanes, and Shleifer 2006) and culture (Hofstede, Hofstede, and

Minkov 2010) affect metric use and whether the effects of country-level variables on metric use are

moderated by firm and managerial characteristics. While there is evidence of the effects of regulatory

disclosure requirements and culture on general management decisions (Tung and van Witteloostuijn

2008), there is little if any evidence on whether regulatory and cultural variables explain international

managers’ metric use in marketing mix decisions.

Consequently, this study asks two unique questions, each offering theoretical contributions. First,

we ask whether five country-level variables, regulatory disclosure requirements, and cultural variables

such as uncertainty avoidance, power distance, individualism, and long-term orientation, explain

differences in metric use of managers residing in different countries. We propose a conceptual model and

hypotheses, based on (i) an interdisciplinary review of the marketing, finance, strategy, accounting,

organizational behavior, and international business literatures and (ii) interviews with 22 executives,

which incorporates the five aforementioned country-level variables and controls for the managerial, firm,

environmental, and type of marketing mix decision based variables advanced in MC (2013). We

empirically test the extended framework employing GLS-SUR estimation on 1,704 marketing mix

decisions as reported on by 571 managers in 31 countries. Results of the main effects proposed in our

conceptual model indicate that managers residing in countries with increased disclosure regulatory

requirements and greater uncertainty avoidant and long-term cultures, employ less metrics; while power

distance and individualism are not found to effect metric use. The model including the five country-level

regulatory disclosure and cultural variables outperforms its nested counterpart which excludes country-

4

level variables enabling a theoretical contribution to the understanding of metric use by managers

operating in different countries.

Second, we ask whether these country-level effects on metric use are uniform across managerial

and firm settings and conduct exploratory analyses to determine whether the effects of regulatory and

cultural variables on metric use are moderated by firm and managerial characteristics. We conduct

exploratory analyses rather than develop 25 additional hypotheses (5 country-level variables X 5

managerial and firm characteristics) since the literature on managerial metric use, although developing

recently, is currently sparse. Results of the exploratory moderation analyses reveal the importance of

power distance and individualism not found in the analysis of main effects. Specifically, we find

marketing managers residing in countries with lower power distant cultures employ less metrics in goods

and market oriented firms that lack chief marketing officers; while managers residing in countries with

lower individualistic cultures employ less metrics in B2C and goods oriented firms. Taken together these

new results clearly establish that metric use is not invariant to country-level variables such as regulation

and culture as has been assumed heretofore.

Our managerial contribution is that we are able to identify country based conditions such as

regulation and culture in which metric use by certain types of managers operating in particular types of

firms is likely to be lower (higher), which has not been accomplished heretofore. Such a conditional

assessment of managerial metric use provides basic understanding of why some managers residing in

certain countries and working in certain types of firms may employ fewer metrics than other managers in

different settings. Importantly, our model allows executives to compute the expected use of metrics by a

specific manager operating in a certain country and firm, when making a particular marketing mix

decision. If the actual metric use is lower (higher) than what is expected, such a difference enables a

diagnostic that the specific manager is found to be under (over) utilizing metrics, relative to the setting

(country, firm, type of manager, etc.) in which the manager operates. Such diagnostics can be (a) useful

for the efficient targeting of metric based training and compensation programs aimed at influencing

managerial metric use; and (b) important because the alternative option of expecting uniform metric use

5

by the firm’s managers operating in different countries myopically disregards differences due to

regulation, culture, and managerial characteristics shown to drive metric use.

Corporate initiatives created at headquarters and promoted worldwide run the risk of conflicting

with unreceptive national cultures. In particular, management practices that are favored in the U.S., such

as individual responsibility, merit-based rewards, and a short-term approach, are likely to be unwise in

some other countries that are culturally unlike the U.S., resulting in a mismatch between management

practices and national culture which is likely to reduce performance (Newman and Nollen 1996). In

contrast, the alignment between key characteristics of the external environment (national culture in this

case) and management practices (regarding metrics and rewards) can generate competitive advantage

(Burns and Stalker 1994, Powell 1992). Since metrics are about accountability, if metric use is found to

be culturally based, our theoretical and managerial contributions described above are important steps in

responding to the continuous calls from the Marketing Science Institute (e.g., see MSI Research Priorities

1998, 2000, 2002, 2004, 2006, 2008, 2012) and the Institute for the Study of Business Markets (e.g., see

ISBM B-To-B Marketing Trend Reports 2008, 2010, 2012) for research on metrics to improve

marketing’s accountability, particularly in a global context.

2. Conceptual Framework and Hypotheses

The unique and primary goal of this study is to focus on the relationship between country regulation and

cultural variables, and managerial metric use (Figure 1). Secondarily, we are interested in exploring

whether the effects of country regulation and culture variables on managerial metric use are moderated by

firm and managerial characteristics. Next, we develop hypotheses relating country-level regulation and

culture variables to metric use. Subsequently, we present our econometric model, describe a number of

controls in order to test the hypotheses developed, and conduct exploratory analyses to determine whether

the effects of regulation and culture on metric use are moderated by firm and managerial characteristics.

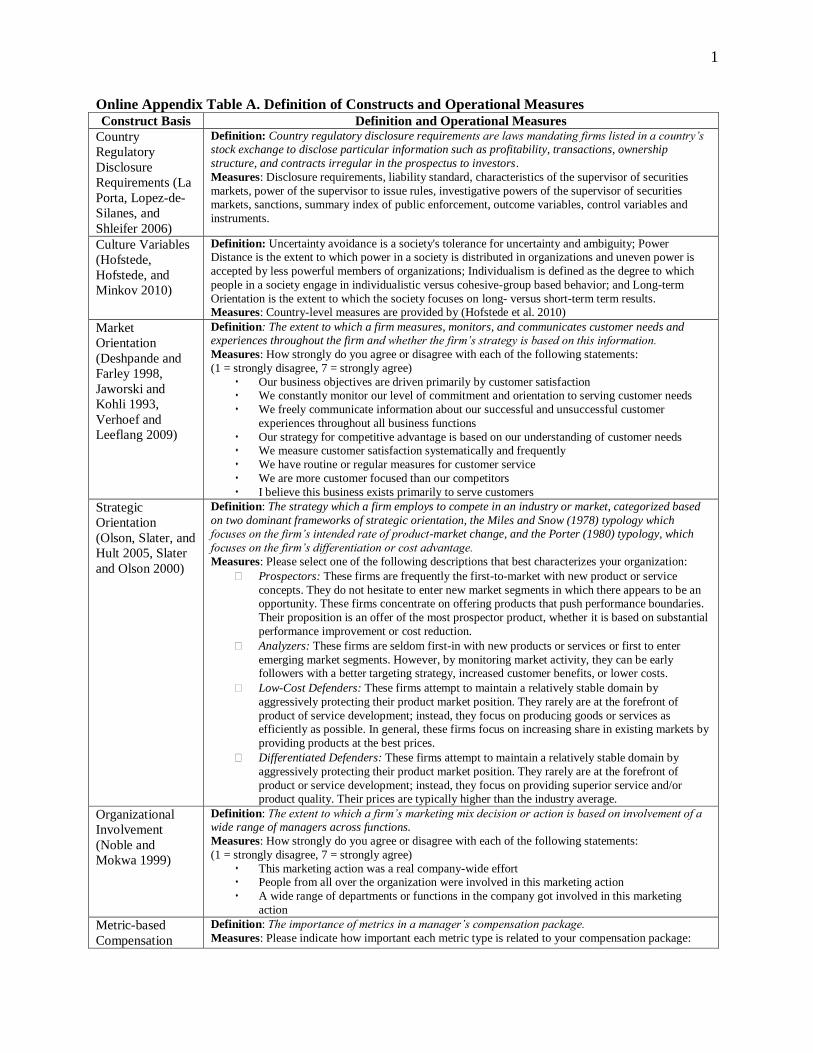

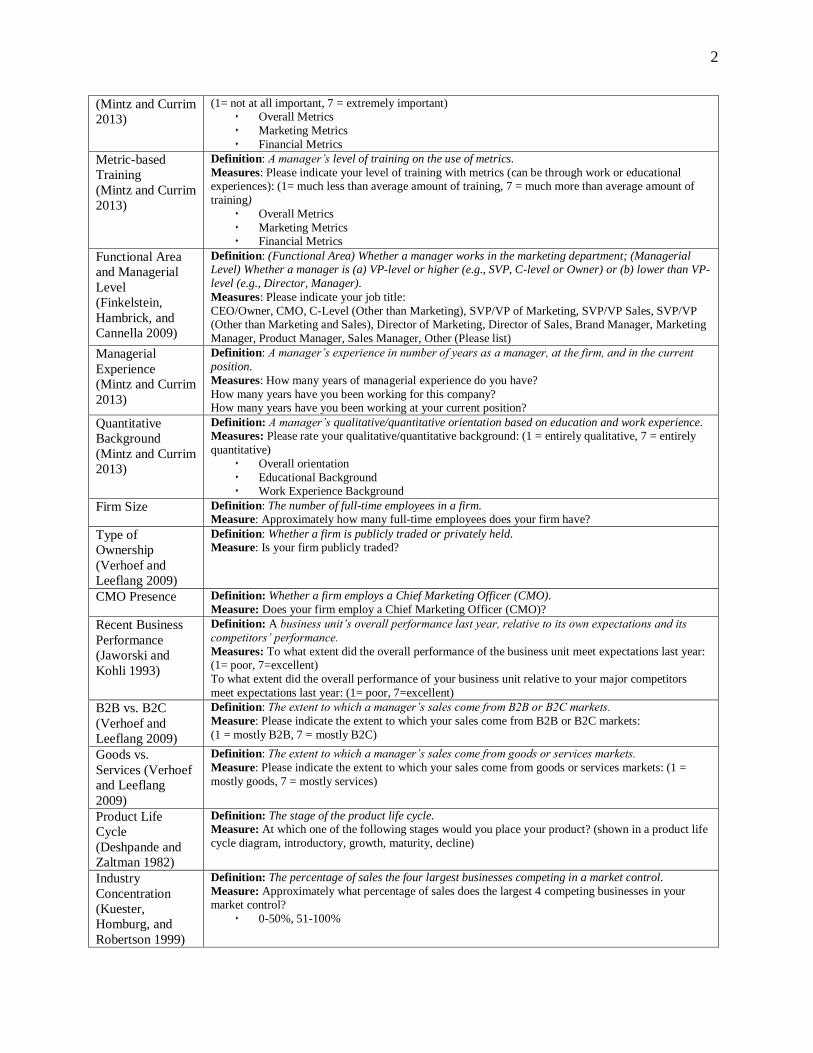

The definitions of all variables excluding the country level variables are from MC (2013) and provided in

Online Appendix Table A for the reader’s convenience.

6

2.1. Country Regulatory Disclosure Requirements

Country regulatory disclosure requirements are defined as laws mandating firms listed in a country’s

stock exchange to disclose particular information such as profitability, transactions, ownership structure,

and contracts irregular in the prospectus to investors (La Porta, Lopez-de-Silanes, and Shleifer 2006).

Regulatory disclosures are reflective of transparency, designed to keep owners (stockholders/ investors)

informed of the decisions and outcomes of managers to whom they delegate their duties, which can

impact managerial decision making.

Information asymmetry theory suggests that greater country regulatory disclosure requirements

leads firms to have more interactions with regulators and less interactions with investors and other agents,

with such reduced interactions leading to less transparency and less informed and involved investors and

agents (La Porta, Lopez-de-Silanes, and Shleifer 2006, Leuz, Nanda, and Wysocki 2003). Involved

investors, who often hold considerable long-term debt and equity in the firm, are able to obtain access to

undisclosed firm information and assert a role in firm decisions (Ball, Kothari, and Robin 2000).

Consequently, first, the value relevance, or the power of information required for regulatory security

disclosures, and the need for firms to publish financial statements to disclose firm information to involved

investors and agents is reduced (Ball, Kothari, and Robin 2000). Second, the need for managers to justify

their decisions to less involved investors and agents through use of additional metrics is decreased

because less involved investors believe that managers are complying with greater levels of regulatory

disclosure requirements (Ali and Hwang 2000). Hence, an increase in regulatory disclosure requirements

inhibits managers from focusing on, employing, and providing additional information and metrics to

investors and other agents of the firm, since managers are more likely focusing on employing, and

providing information and metrics to regulators. Consequently, we expect:

H1. Managers in countries with greater regulatory disclosure requirements will employ fewer

metrics in their marketing mix decisions.

7

2.2. Country Culture

Research on managerial decision making finds cultural variables such as uncertainty and ambiguity

norms, motivational techniques, and levels of group consensus and long-term orientation to impact

managerial decisions (e.g., Hewitt, Money, and Sharma 2006, Tan et al. 1998, Tse et al. 1988). Hence, we

expect country culture to also potentially impact managerial metric use in marketing decisions and

consider four of five cultural dimensions from Hofstede, Hofstede, and Minkov (2010); uncertainty

avoidance, power distance, individualism vs. collectivism, and short- vs. long-term orientation.3

2.2.1. Uncertainty Avoidance. Uncertainty avoidance is defined as a society's tolerance for

uncertainty and ambiguity. Managers residing in cultures that avoid uncertainty adopt strict codes of

behavior that are resistant to change from established patterns (Steenkamp, ter Hofstede, and Wedel

1999), and exhibit a greater herding mentality towards making decisions that align with the norm

(Deleersnyder et al. 2009). While managerial decision making in cultures that avoid uncertainty focuses

on risk avoidance and reduction (Roth 1995, Steenkamp, ter Hofstede, and Wedel 1999), we expect that

in cultures resistant to change, aligning with the norm in an organization is likely to be more powerful in

reducing uncertainty and risk than use of metrics. Since past managerial behavior in marketing is

characterized by less metric use (Lehmann and Reibstein 2006), resistance to change and aligning with

the norm implies continuing lower levels of metrics use. Further, managers operating in higher

uncertainty avoidant cultures and seeking to align with the norm may engage in less innovative marketing

mix approaches because of the risk assessed with such experimentation (Kanagaretnam, Lim, and Lobo

2011). Consequently, there may be less need for managers to employ metrics to demonstrate the value of

their innovative experiments. Therefore, we expect:

H2. Managers in countries with greater uncertainty avoidant cultures will employ fewer metrics

in their marketing mix decisions.

3 The fifth dimension, masculinity vs. femininity is excluded because of the absence of a clear rationale linking the

dimension to managerial metric use, hence we only include in our conceptual model the four cultural distance

dimensions that can be reasonably expected to affect metric use or ex post managerial behavior (Tung and Verbeke

2010).

8

2.2.2. Power Distance. Power distance is defined as the extent to which power in a society is

distributed in organizations and uneven power is accepted by less powerful members of organizations.

Greater power distance implies that final decisions are centralized and made by top executives; thus lower

level managers could face increasingly bureaucratic environments which require greater amounts of

approval from top executives necessitating greater justification of decisions (Hofstede, Hofstede, and

Minkov 2010). Metrics not only serve as decision aids, i.e., for considering, benchmarking, and

monitoring marketing mix decisions, but can also be employed to justify such decisions (Pauwels et al.

2009). Hence, we expect managers in greater power distance cultures to employ more metrics in order to

provide greater justification for marketing mix decisions. Consequently, we expect:

H3. Managers in countries with greater power distant cultures will employ more metrics in their

marketing mix decisions.

2.2.3. Individualism versus Collectivism. Individualism vs. collectivism is defined as the degree

to which people in a society engage in individualistic vs. cohesive group-based behavior. In contrast to

collectivist cultures, in individualistic cultures decision making is largely the result of independent

decision making processes which involves less group-based consensus (Roth 1995, Steenkamp, ter

Hofstede, and Wedel 1999). Managers in such cultures are more likely to be empowered to make

decisions independently because they are individually held responsible for the results of their decisions,

with such responsibility requiring managers to demonstrate the results of their decisions (Newman and

Nollen 1996) through metric use. In addition, managers in cultures which are more individualistic (vs.

collectivist) could also face greater objections to their decisions from other managers who are not

involved in the decision making process but compete for firm resources (Tan et al. 1998). Consequently,

managers making decisions in individualistic cultures will face more pressure to provide support and

justification for their decisions through metric use. In contrast, in collectivist cultures, managers will face

less pressure to provide support and justification because decisions are made based on consensus between

group members. Therefore, we expect:

H4. Managers in countries with greater individualistic cultures will employ more metrics in their

marketing mix decisions.

9

2.2.4. Short- versus Long-Term Orientation. Long-term orientation is defined as the extent to

which the society focuses on long- vs. short-term term results. In short-term oriented cultures, firms and

managers are most interested in the “bottom-line” in the current period (Deleersnyder et al. 2009), which

leads managers in such cultures to be constantly judged by control systems and metrics designed by their

firms to evaluate such bottom-line results (Hofstede, Hofstede, and Minkov 2010). In addition, because

the focus of firms and managers making marketing mix decisions in long-term oriented cultures is on the

“long-term” (Hofstede, Hofstede, and Minkov 2010) and long-term outcomes are more removed from the

current decision-making period, managers in such cultures could be less reliant on metrics observable in

the current period. Managers residing in longer-term oriented cultures are also less likely to pursue “quick

fixes” (Newman and Nollen 1996), and hence less likely be required to use metrics to demonstrate the

value of quick fixes. Consequently, we expect:

H5. Managers in countries with greater short-term orientation cultures will employ more metrics

in their marketing mix decisions.

3. Model

Following the conceptual framework in Figure 1, we begin the model discussion by describing the

notation of two sub-models. In the first sub-model (equation 1), which is specified to test the hypotheses

developed above, our main dependent variable is the total number of metrics employed in a specific

marketing mix decision4 and the main independent variables are the five country-level variables

hypothesized to influence total metric use. In addition, we include managerial, firm, environmental, and

marketing mix effort based control variables advanced in MC (2013) in order to determine the effect of

the main country-level variables on total metric use. Subsequently, we conduct exploratory analyses with

this model to ascertain whether the main effects of regulation and culture on metric use are moderated by

firm and managerial characteristics. In the second sub-model (equation 2), the dependent variable is the

4 In addition to the total number of metrics employed, later, we consider the type of metrics employed (e.g.,

marketing vs. financial).

10

perceived performance of the marketing mix decision5 based on scale items proposed by Jaworski and

Kohli (1993), Moorman and Rust (1999), and Verhoef and Leeflang (2009), and the independent variable

is total metrics employed when making the marketing mix decision6.

3.1. Primary Analyses Model Specification

3.1.1. Sub-Model 1 Main Variables. The dependent variable is the total number of metrics

(TOTMET) employed by a manager for a certain marketing mix decision. MC (2013) considers two types

of metrics, (1) marketing and financial, and (2) general and specific to a marketing mix decision. These

metrics are defined in Online Appendix Table A and presented in Table 1 Panels A (general metrics) and

B (specific metrics). The five main independent variables employed to test the corresponding five

hypotheses are country-level variables, regulatory disclosure requirements (DSCREQ), and four cultural

variables, uncertainty avoidance (UAI), power distance (PDI), individualism vs. collectivism (IDV) and

long- vs. short-term orientation (LTO).

3.1.2. Control Variables. In addition to the country-level regulation and cultural variables, we

employ managerial, firm, environmental, and marketing mix decision based controls, shown by MC

(2013) to drive U.S. managers’ metric use. The definitions and operational measures of the control

variables are taken from MC (2013), based on published studies in various literatures, and presented in

Online Appendix Table A. First, we include six managerial characteristics (MGRCHR); metric-based

compensation, metric training level, functional area (marketing vs. non-marketing), managerial level

(TMT vs. non-TMT), experience, and quantitative background. Second, we include eleven firm

characteristics (FIRMCHR); market orientation, strategic orientation (whether the firm follows an

5 We focus on performance of the marketing mix decision (not firm performance, e.g., stock market returns) because

our unit of analysis is a manager, in a particular business unit of a firm, making a specific marketing mix decision.

In contrast, firm performance (e.g., based on stock market returns, or firm value) is based on several concurrent

marketing mix decisions, other contemporaneous non-marketing decisions (layoffs, R&D, etc.), and the combined

performance of marketing and non-marketing decisions across multiple business units. Consequently, it is difficult

to assess the impact of metric use on the performance of a specific marketing mix decision based on firm

performance. In addition, our choice of performance measures and the corresponding survey methodology,

described later, allows measurement of metric use for specific marketing mix decisions and several other important

moderating and control variables in our conceptual framework (Figure 1). 6 When types of metrics are considered (e.g., marketing vs. financial) we replace total metric use (1 IV) with

marketing and financial metric use (2 IVs).

11

analyzer, low-cost defender, or differentiated defender strategy, relative to a prospector strategy),

organizational involvement in the decision, and other firm characteristics such as firm size, type of

ownership (public vs. private), CMO presence, recent business performance, and B2C (vs. B2B) and

services (vs. goods) orientations. Since recent business performance is included as a firm characteristic,

endogeneity concerns between performance and metric use are controlled for. Third, we include four

environmental characteristics (ENVCHR); product life cycle (maturity/declining vs. introduction/growth),

industry concentration, and market growth and turbulence. Finally, we consider nine marketing mix

decisions (MKTMIX); traditional advertising, internet advertising, direct to consumer, social media, price

promotions, pricing, new product development, sales force, and distribution, all relative to public relations

(PR) / sponsorship decisions.

3.1.3. Sub-Model 2. We link the total number of metrics employed by a manager for a specific

marketing mix decision (TOTMET - the IV) to the perceived performance of that marketing mix decision

(PERFMKTMIX – the DV). Perceived performance of a marketing mix decision is defined based on a

firm’s stated marketing (customer satisfaction, loyalty, market share), financial (sales, profitability, ROI),

and overall outcomes, relative to the firm’s stated objectives and to similar prior activities or decisions

(Jaworski and Kohli 1993, Moorman and Rust 1999, Verhoef and Leeflang 2009).

3.1.4. Determining Whether a Manager is Underutilizing Metrics. An additional value of the

model is that an executive at company headquarters can compute the expected (or predicted) total metric

use (TOTMET) of a specific manager (MGRCHR) operating in a certain country (based on the country

scores for DSCREQ, UAI, PDI, IDV, and LTO), firm (based on FIRMCHR), and environment

(ENVCHR), when making a particular marketing mix decision (MKTMIX). The expected value can be

compared to the actual number of metrics employed by the specific manager in that country, firm,

environmental, and marketing mix decision setting to determine whether the manager is underutilizing

metrics, an important input into efficient managerial targeting and implementation of metric based

programs.

12

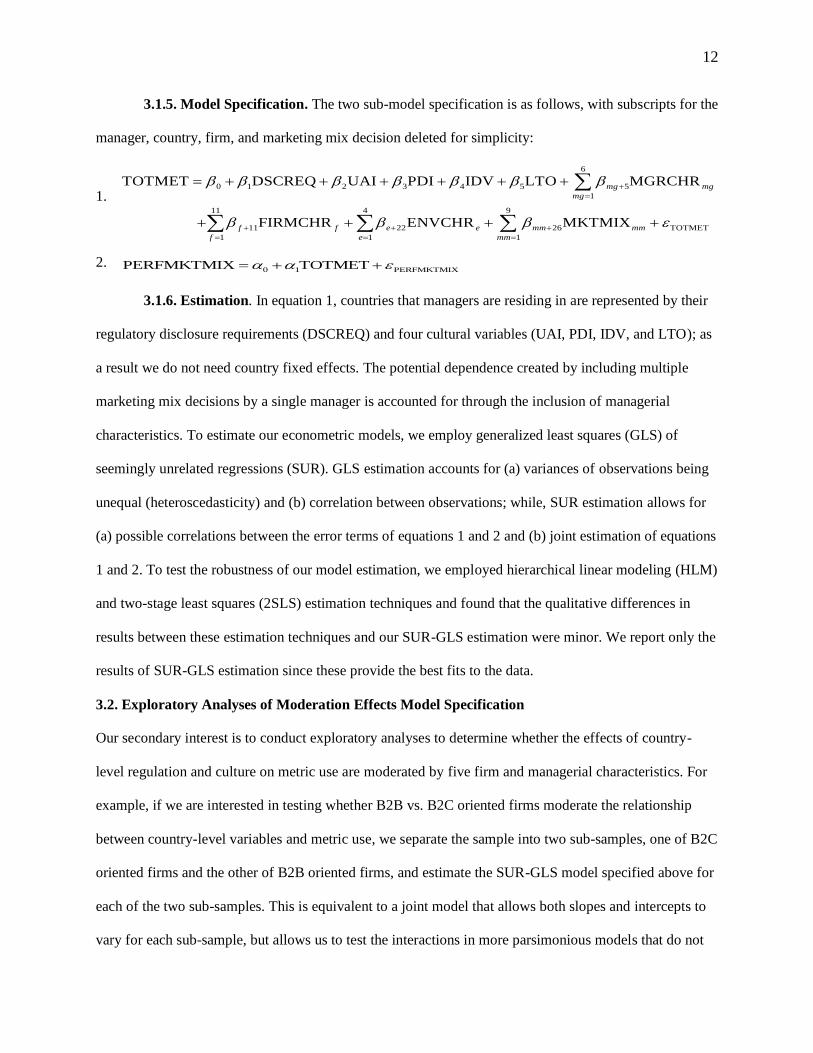

3.1.5. Model Specification. The two sub-model specification is as follows, with subscripts for the

manager, country, firm, and marketing mix decision deleted for simplicity:

1.

6

0 1 2 3 4 5 5

1

11 4 9

11 22 26 TOTMET

1 1 1

TOTMET DSCREQ UAI PDI IDV LTO MGRCHR

FIRMCHR ENVCHR MKTMIX

mg mg

mg

f f e e mm mm

f e mm

2. 0 1 PERFMKTMIXPERFMKTMIX TOTMET

3.1.6. Estimation. In equation 1, countries that managers are residing in are represented by their

regulatory disclosure requirements (DSCREQ) and four cultural variables (UAI, PDI, IDV, and LTO); as

a result we do not need country fixed effects. The potential dependence created by including multiple

marketing mix decisions by a single manager is accounted for through the inclusion of managerial

characteristics. To estimate our econometric models, we employ generalized least squares (GLS) of

seemingly unrelated regressions (SUR). GLS estimation accounts for (a) variances of observations being

unequal (heteroscedasticity) and (b) correlation between observations; while, SUR estimation allows for

(a) possible correlations between the error terms of equations 1 and 2 and (b) joint estimation of equations

1 and 2. To test the robustness of our model estimation, we employed hierarchical linear modeling (HLM)

and two-stage least squares (2SLS) estimation techniques and found that the qualitative differences in

results between these estimation techniques and our SUR-GLS estimation were minor. We report only the

results of SUR-GLS estimation since these provide the best fits to the data.

3.2. Exploratory Analyses of Moderation Effects Model Specification

Our secondary interest is to conduct exploratory analyses to determine whether the effects of country-

level regulation and culture on metric use are moderated by five firm and managerial characteristics. For

example, if we are interested in testing whether B2B vs. B2C oriented firms moderate the relationship

between country-level variables and metric use, we separate the sample into two sub-samples, one of B2C

oriented firms and the other of B2B oriented firms, and estimate the SUR-GLS model specified above for

each of the two sub-samples. This is equivalent to a joint model that allows both slopes and intercepts to

vary for each sub-sample, but allows us to test the interactions in more parsimonious models that do not

13

include 25 interaction terms (5 country level x 5 managerial and firm variables). Further, this approach

allows us to conduct exploratory testing of whether the main effects of country-level variables identified

(not identified) in model 1 are found in each sub-sample.

4. Empirical Test

4.1. Sampling

Our sampling scheme needs to satisfy three criteria. First, in order to establish the main effect of each of

the five country-level variables on metric use, we need to maximize the variation on each of the five

country-level variables. Data on our first main independent country-level variable, regulatory disclosure

requirements (DSCREQ) are published by La Porta, Lopez-de-Silanes, and Shleifer (2006) in the Journal

of Finance. Data on our second through fifth main independent country-level or cultural variables,

uncertainty avoidance (UAI), power distance (PDI), individualism vs. collectivism (IDV) and long- vs.

short-term orientation (LTO) are published in Hofstede, Hofstede, and Minkov's (2010) book on Cultures

and Organizations. These data are found in the first 5 columns of Table 2. Second, in order to conduct

exploratory testing of the potential moderation effects of firm and managerial characteristics, we need

good variation on firm and managerial characteristics. Third, in order to ensure that we control for other

characteristics such as environmental and marketing mix decision shown by MC (2013) to drive

marketing metric use, we need good variation on environmental and marketing mix characteristics.

One sampling option is to focus on the countries which have the highest and lowest scores on

each of the five country-level variables, resulting in 10 countries. However, we were concerned that

limiting the data collection to 10 countries may not (a) give us a sufficient sample size to test model 1

since it has a large number of independent variables and controls; and (b) achieve the second and third

objectives outlined above (Cavusgil and Das 1997). Consequently, we did not place any restrictions on

the countries from which we collected our sample observations (Franke and Richey 2010). In addition,

the 3 top and 3 bottom countries, or 6 countries, on each of the 5 country-level variables listed in Table 2

are quite different. Hence, not placing restrictions on the 30 additional countries from which we sample

14

has the potential of achieving the first in addition to the second and third criteria. Following the three

criteria, we collected a new sample of 132 managers residing in 30 additional countries reporting on 471

marketing mix decisions. This new sample was merged with the MC (2013) sample of 439 U.S. managers

reporting on 1,287 marketing mix decisions, resulting in a total sample of 571 managers reporting on

1,704 marketing mix decisions7. Our sample of managerial decisions per country is small. This would be

a problem if the goal of the study were to compare metric use by managers residing in different countries,

which is not the goal. In contrast, the goal is to establish the main effects of country-level regulatory and

cultural variables and the moderation effects of firm and managerial characteristics; consequently, we

need to maximize the variation of the country level, firm, managerial, and other control variables (the

three sampling criteria outlined above). Of course, if our sampling scheme is inadequate, we will not be

able to establish the main and moderation effects we seek to establish. It is relatively easy for subsequent

studies that seek to compare managers from certain countries (e.g., U.S. and India) to restrict their

sampling to the countries of interest.

4.2. Questionnaire Design and Sampling Frames

In order to pool the new and previous data sets, we employed the same questionnaire, incentives,

sampling frames, and reminder communications as MC (2013). Briefly, the manager begins the

questionnaire by identifying 1-10 particular marketing mix decisions from a list of 10 different types of

marketing mix decisions. Next, for each type of marketing mix decision identified, the manager indicate

which marketing and financial metrics they employed prior to or while making the decision from a list of

12 general marketing and 12 general financial metrics common to all marketing mix decisions, and 3

specific marketing and 3 specific financial metrics related to the particular marketing mix decision (see

Table 1 Panels A [general metrics] and B [specific metrics]). Managers could view the definition of each

included metric, indicate any other metric employed, or select a no metric employed option. This was

followed by 8 measures of marketing mix activity performance observed after the decision was made;

consequently, simultaneity or endogeneity concerns are minimized. Subsequently, managers indicated the

7 We run hypotheses testing without the U.S. sample and find similar results as the full sample.

15

level of organizational involvement for each activity, and provided information on managerial, firm and

environmental characteristics. To obtain subjects, we collaborated with several marketing professional

organizations such as Marketing Executives Group, Marketing Executives Network Group, Society of

Marketing Professional Services, and VP’s of Sales/Marketing, who posted announcements to their

respective members on LinkedIn with a request to participate.

4.3. Descriptive Statistics

Table 1 Panels A and B report the full set of metrics considered in the study and the reported percentage

use of each metric in countries that were above versus below the mean on each of the five country-level

variables. On average, awareness, target volume, and return on investment are general metrics employed

most often; however there are differences in how often awareness and target volume are employed across

settings which are above or below the mean on some of the county-level variables. Similarly, click though

rate, strength of channel relationships, and hits/page views are specific metrics employed most often for

specific marketing mix decisions; however there are differences in how often click through rate, strength

of channel relationships, and hits/page views are employed across settings which are above or below the

mean on some of the county-level variables. Panels A and B of Table 1 will be useful for academicians

and practitioners who wish to assess the types of metrics expected to be employed in marketing mix

decisions in settings which are higher or lower than the mean of each one of the five country-level

variables.

In Table 3, we present sample descriptive statistics on our dependent variables, TOTMET and

PERFMKTMIX, and independent control variables, MGRCHR, FIRMCHR, ENVCHR, and MKTMIX.

The sample consists of a good mix of regulatory disclosure requirements (mean = 0.93, s.d. = 0.16),

uncertainty avoidance (mean = 49.5, s.d. = 11.8), power distance (mean = 42.8, s.d. = 10.8), collectivism

vs. individualism (mean = 84.9, s.d. = 14.2), and short vs. long-term orientation (mean = 30.7, s.d., =

11.8). Consequently, the first sampling goal outlined above is achieved.

The sample also consists of a good mix of TMT vs. non-TMT managers (54% vs. 46%),

managers in prospector (32%), analyzer (25%), differentiated defender (32%) and low-cost defender

16

(11%) organizations, companies in introductory/growth (47%) vs. maturity/decline (53%) stages of the

product life cycle, and in concentrated (44%) vs. fragmented (56%) industries. The average number of

employees in a manager’s firm is 9,425 and the median is 120 employees, and more managers work in

privately held vs. publicly traded companies (77% vs. 23%) and in firms without vs. with a CMO (68%

vs. 32%), which indicates a good mix of large and small firms. The mix of privately held vs. publicly

traded companies is 77% vs. 23%, close but higher than the 2007 US Census of 67% vs. 33% and firms

without vs. with a CMO is 68% vs. 32%, also close to Nath and Mahajan (2008) modalities of 75% vs.

25%. The sample also consists of good variance on metric-based compensation (mean = 5.0, s.d.= 1.5

where 1= not important and 7 = extremely important), metric training (mean = 4.5, s.d.= 1.7 where 1=

much less than average and 7 = much more than average), B2B and B2C oriented companies (mean = 2.9,

s.d. = 2.2 where 1= mostly B2B, 7 = mostly B2C), and goods and service oriented firms (mean = 4.6, s.d.

= 2.4 where 1= mostly goods, 7 = mostly services). Consequently, the second and third goals for

sampling goals outlined above are achieved.

4.4. Testing for Collinearity, and Non-Response, Self-Selection, and Common Method Biases

Almost all, 1356 of 1369 (99.1%), of the pairwise correlations calculated in Appendix A are below 0.4

(Leeflang et al. 2000). However, as expected from the international literature, some correlations between

country-level variables are greater than 0.4. For these variables and the other variables comprising the 3

additional pairwise correlations greater than 0.4, variance inflation factor scores are calculated, all of

which are well below 6, indicating no multicollinearity problems for estimation of the models (Hair et al.

1998). Further, we do not detect non-response bias in our sample based on the Armstrong and Overton

(1977) test in which late and early respondents scores are compared on the included constructs (both new

and previous samples p>.05).

To help mitigate a priori common method and self-selection biases (i.e., where managers only

participate or will only report decisions in which they employ large amounts of metrics), we adapted the

Fredrickson and Mitchell (1984) instructions and stated in our cover letter posted online and in the

introduction to the questionnaire that we were interested in responses from managers who do and do not

17

employ metrics in their decisions and that their answers would remain anonymous (Chang, van

Witteloostuign and Eden 2010). Out of the 1,704 marketing mix decisions reported in the total sample,

115 (7%) decisions did not involve any metrics and 303 (18%) decisions involved 1-3 metrics, evidence

that managers were not reluctant to describe decisions in which no metrics or a very small number of

metrics were involved. Lastly, we do not find evidence of common-method bias based on Harman’s one-

factor test (Rubera, Ordanini and Griffith 2011) and Lindell and Whitney (2001) post hoc tests. We

employed White's (1980) test to check for heteroscedasticity and found that the null hypothesis on the

variance of residuals being homogenous cannot be rejected in any of our models, indicating no

heteroscedasticity.

5. Results

5.1. Primary Analyses

5.1.1. Hypothesis Testing. In Table 4, we present the SUR-GLS estimation results. We find

greater country regulatory disclosures requirements, uncertainty avoidance, and long-term orientation to

inhibit metric use, resulting in H1, H2, and H5 being supported (each p<.01); while power distance and

individualism do not drive metric use, resulting in H3 and H4 not being supported. A nested model-based

F test which compares the full model, i.e., country-level and control variables, to a model with only the

control variables is found to provide a statistically significant additional explanation of international

managers’ metric use (p<.05). We find similar results for both the hypotheses testing and the nested

model-based F test comparing the full model to the model with only the control variables when only

analyzing non-U.S. managers.

5.1.2. Controls. In Table 4, we also present the SUR-GLS estimation results for the control

variables. First, for managerial characteristics, we find managers to employ more metrics when they have

greater metric-based compensation and training (both p<.01). Second, for firm and environmental

characteristics, we find managers employ more metrics when their firms have greater market orientation,

follow an analyzer and low-cost defender strategic orientation (each relative to a prospector strategic

18

orientation), have greater recent business performance, are more B2C and goods oriented, and in more

(vs. less) concentrated industries (each p<.01). Third, for type of marketing mix activity, we find

managers employ more metrics when making internet advertising, direct to consumer, pricing, new

product development, and sales force decisions, each relative to making PR / sponsorship decisions (each

p<.01). Fourth, we find increased metric use to associate with improved marketing mix performance

(p<.01). Fifth, when a squared metric use term is added to sub-model 2, metric use is found to result in

decreasing returns to scale (p<.01), but still is positively associated with marketing mix performance in

the range of metric use reported by managers.

5.1.3. Determining Whether a Manager is Underutilizing Metrics. In Table 2, we provide an

example of how an executive at headquarters can employ our model to calculate an expectation of metric

use for a specific manager (e.g., belonging to the TMT, with an average metric-based compensation,

training, and quantitative background), operating in a certain country (as represented by the five country-

level regulatory and cultural variables), firm (e.g., public, prospector, with a CMO, average market

orientation, firm size, B2B [vs. B2C] and goods [vs. services] orientations, and organizational

involvement in marketing mix decisions), and environment (e.g., intro/growth PLC stage, and fragmented

industry), when making a particular marketing mix decision (e.g., PR/sponsorship). This expectation can

be compared to the actual use of metrics by the manager in that setting to determine whether s/he is under

(over) utilizing metrics. For example, suppose the headquarter-based executive is assessing metric use by

a manager in Finland, France, and the U.S. Table 2 indicates that the manager in Finland is expected to

employ the most metrics, while managers in France and the U.S. are expected to employ less metrics. If

the actual metric use by the managers in Finland and the U.S. are found to meet expectations but the

French manager is not found to meet the expectation, the headquarter-based executive could use such a

diagnostic to identify managers who are meeting or not meeting metric use expectations relative to other

managers operating in similar settings.

19

5.2. Exploratory Secondary Analyses

5.2.1. Type of Metrics. While the results of hypothesis testing above relate to the total metrics

employed, next, we investigate the effects of country-level regulatory and cultural variables on the types

of metrics employed, i.e., marketing and financial. We employ the following version of sub-models 1 and

2 wherein marketing and financial metrics take the place of total metrics.

3.

6

0 1 2 3 4 5 5

1

11 4 9

11 22 26 MKTMET

1 1 1

MKTMET DSCREQ UAI PDI IDV LTO MGRCHR

FIRMCHR ENVCHR MKTMIX

mg mg

mg

f f e e mm mm

f e mm

4.

6

0 1 2 3 4 5 5

1

11 4 9

11 22 26 FINMET

1 1 1

FINMET DSCREQ UAI PDI IDV LTO MGRCHR

FIRMCHR ENVCHR MKTMIX

mg mg

mg

f f e e mm mm

f e mm

5. 0 1 2 PERFMKTMIXPERFMKTMIX MKTMET FINMET '

The effect of (i) country regulatory disclosure requirements on metric use observed earlier for our

full sample (H1) is observed for marketing and financial metrics (each p<.05); (ii) uncertainty avoidance

observed earlier (H2) is observed for financial (p<.05) and marginally for marketing metrics (p<.1); and

(iii) long-term orientation observed earlier (H5) is observed for marketing and financial metric use (each

p<.05)8. We also find increased marketing and financial metric use to associate with improved marketing

mix performance (each p<.01).

5.2.2. Moderation Effects. Next, we explore whether the effects of country-level regulation and

culture on metric use are moderated by firm and managerial characteristics by splitting our original

sample into two sub-samples based on each of four firm and one managerial characteristics, resulting in

the following ten sub-samples; (1) B2B (n=1095) vs. B2C (n=609) oriented firms; (2) goods (n=606) vs.

8 In addition, we find firm characteristics to largely influence marketing (7 of 11) and financial (7 of 11) metric use,

type of marketing mix activity to largely influence financial (7 of 9) and only somewhat influence marketing (3 of 9)

metric use, and environmental (2 of 4 for marketing metrics; 1 of 4 for financial metrics) and managerial

characteristics (2 of 6 for marketing metrics; 3 of 6 for financial metrics) to somewhat influence marketing and

financial metric use. Unlike the full sample estimation, managers with greater quantitative backgrounds (p<.01), in

firms with CMO presence (p<.01), and making price promotions decisions in comparison to PR/sponsorship

decisions (p<.05) employ more financial metrics, while managers operating in introductory/growth life cycles also

employ more marketing metrics (p<.05).

20

services (n=1098) oriented firms; (3) above (n=852) vs. below (n=852) average market oriented firms; (4)

firms with (n=547) vs. without (n=1157) a CMO; and (5) marketing (n=922) vs. non-marketing (n=782)

managers.9 Our model and estimation technique is the same as originally specified in sub-models 1 and 2.

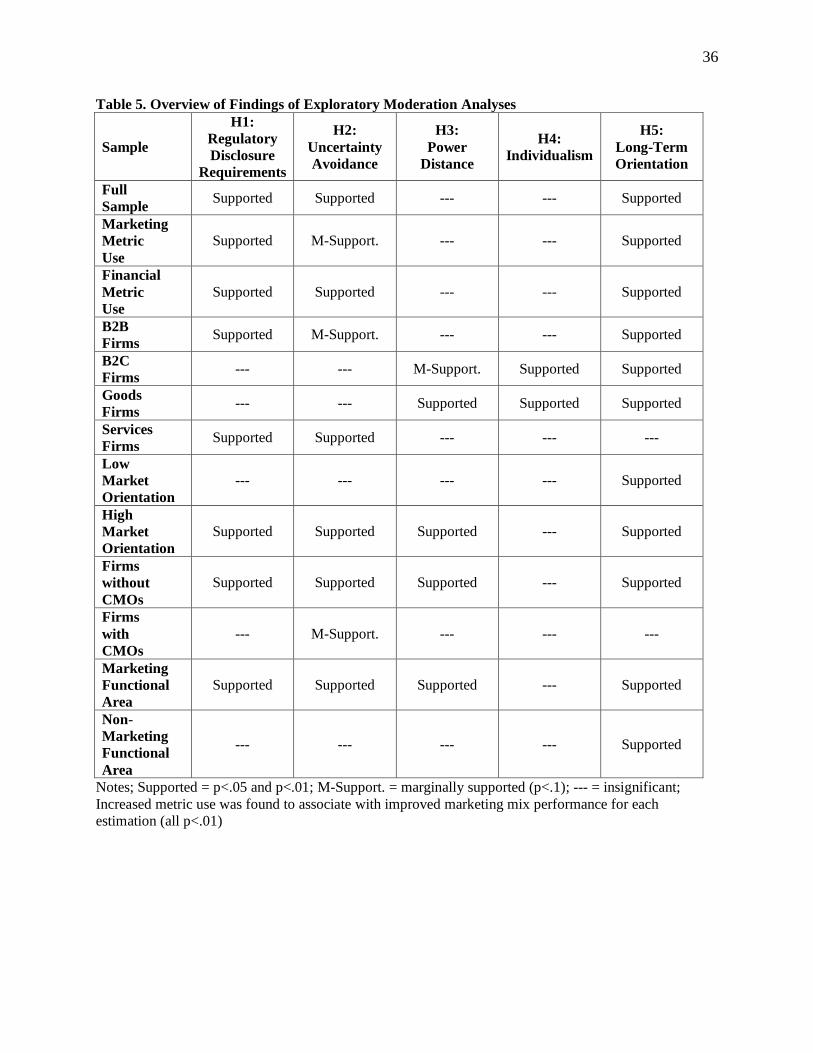

The results of the moderation analyses are summarized in Table 5. The effect of (i) country

regulatory disclosure requirements on metric use observed earlier for our full sample (H1) is similarly

observed in the samples of B2B (p<.05), services (p<.05), above average market oriented (p<.01) firms,

firms without a CMO (p<.01), and marketing managers (p<.01); (ii) uncertainty avoidance observed

earlier (H2) is similarly observed in the samples of services and above average market oriented firms,

firms without a CMO (each p<.01), and marketing managers; and (iii) long-term orientation observed

earlier (H5) is similarly observed in the samples of B2B (p<.01), B2C (p<.01), goods (p<.01), and above

(p<.01) and below (p<.05) average market oriented firms, firms without a CMO (p<.01), and marketing

(p<.01) and non-marketing (p<.05) managers. Interestingly, when we now conduct moderation analyses,

the analyses reveal that power distance significantly affects metric use (H3) for goods (p<.01) oriented

and above average market oriented (p<.05) firms, firms without a CMO (p<.01), and marketing managers

(p<.05); effects not observed for our full sample based analysis reported earlier. Consequently, H3 is now

supported for these relationships. And, the moderation analyses reveal that individualism significantly

affects metric use (H4) for B2C and goods oriented firms (both p<.01); effects not observed for our full

sample based analysis reported earlier. Consequently, H4 is now supported for B2C and goods oriented

firms.

In summary, the effects of country-level regulation (H1) and long-term oriented culture (H5) on

metric use are found to be moderated by all 5 firm and managerial variables considered; uncertainty

avoidant (H2) and power distant (H3) cultures on metric use are found to be moderated by all firm and

9 B2C vs. B2B and goods vs. services firms are split based on managers indicating the neutral, middle point on the

7-point scale asking them the extent to which their sales came from B2B or B2C and goods or services markets;

high vs. low market orientation is split at the median for our sample, and CMO presence and marketing managers

are discrete choices managers indicated in the questionnaire.

21

managerial characteristics assessed except B2B vs. B2C oriented firms; and individualism on metric use

(H4) is found to be moderated by B2B vs. B2C and goods vs. services oriented firms.

5.2.3. Additional Analyses. To conduct further exploratory analyses aimed at gaining insight into

the effects of country-level regulatory and cultural variables on metric use, we further decomposed our

dataset by two country economic and legal characteristics; (i) more vs. less economically developed

countries, since market research information and data to evaluate marketing actions are harder to obtain in

less developed countries (Cateora, Gilly, and Graham 2013), which may influence metric use; and (ii)

common vs. other types of legal systems, since legal traditions that influence corporate law and investor

protection (La Porta et al. 1997) may affect managerial metric use. For (i) we employed the International

Monetary Fund's (IMF) 2010 list of developed countries to classify the countries that managers reside.

We find the effects of country regulatory disclosure requirements (H1) and long-term orientation (H5) on

metric use observed earlier for our full sample are similarly observed for managers making marketing

decisions in developed countries. Interestingly, when we now only analyze managers residing in

developed countries, we also find individualism (H4) to significantly affect metric use (p<.01), which was

not observed in our full sample. Consequently, H4 is now supported when only considering managers that

reside in economically developed countries.

For (ii) we employed the Central Intelligence Agency's (CIA) 2012 World Factbook list of

countries to classify the countries that managers reside in as common or another type of legal system. The

English common law tradition, adopted by former and current English colonies including the US, is

shaped by the decisions of judges ruling on specific issues more than other legal traditions (Guler and

Guillén 2009). We find the effect of country regulatory disclosure requirements (H1) observed earlier for

our full sample is similarly observed for managers operating in common law countries. Interestingly,

when we now only analyze managers operating in common law countries, we also find power distance

(H3) (p<.01) and individualism (H4) (p<.05) to significantly affect metric use, which were not observed

in our full sample results reported earlier. Hence, H3 and H4 are now supported for managers residing in

common law countries.

22

6. Discussion

Prior research demonstrates that marketing enhances its stature within the firm when it increases the

accountability of its actions (O’Sullivan and Abela 2007, Verhoef and Leeflang 2009). Increased global

competition, regulations, and stock market pressures have only increased demands for greater marketing

accountability and metric use (Lehmann and Reibstein 2006). While progress has been made on

continuous calls from MSI and ISBM to encourage research on metrics and marketing decisions, no study

has investigated (i) whether metric use by managers residing in a variety of countries is driven by

country-level regulatory or cultural variables or (ii) whether the effects of country-level regulatory and

cultural variables on metric use are moderated by firm and managerial characteristics. The two questions

are important because the alternative expectation that managers residing in different countries should be

equally predisposed to employing metrics for marketing mix decisions may not be tenable. And if such an

expectation turns out, as demonstrated in this paper, corporate initiatives on metric use created at

headquarters and promoted uniformly worldwide run the risk of conflicting with unreceptive national

cultures (Newman and Nollen 1996). In contrast, the alignment between cultural aspects and management

practices regarding metrics and rewards can generate competitive advantage (Powell 1992).

Hence, this paper builds on related literature in three important ways, each offering theoretical,

empirical, and managerial contributions. First and foremost, the previous literature has focused on U.S.

managers’ metric use, while this paper focuses on metric use of managers residing in a variety of

countries. This difference in focus permits us to hypothesize and investigate whether five country-level

regulatory and cultural variables drive differences in metric use by managers operating in a variety of

countries. Analysis of a sample of 1,704 decisions made by 571 managers operating in 31 countries

reveals that increased country disclosure regulatory requirements (H1), uncertainty avoidance (H2), and

long-term orientation (H5) decrease total metric use, while power distance (H3) and individualism (H4)

are not associated with total metric use. Importantly, a model that incorporates these country-level

regulatory and cultural variables is found to be significantly better at explaining total metric use than a

23

restricted version of the model based on managerial, firm, environmental, and marketing mix decision

based controls from the related literature, enabling a theoretical contribution towards understanding

drivers of metric use by managers operating in various countries. Specifically, regulatory and cultural

theories are found to significantly explain managerial metric use in marketing mix decisions over and at

least equal to alternatives such as the decision maker perspective (managerial characteristics), resource

based theory of the firm (firm characteristics), contingency theory (environmental characteristics) and

value-chain theory (marketing mix characteristics). Similarly, we reach largely the same conclusions

when we investigate the types of metrics employed, i.e., marketing and financial metrics, with the full

sample of decisions (managers and countries).

Second, we explore whether the effects of country-level regulatory and cultural variables on total

metric use are moderated by firm and managerial characteristics, also not accomplished in the literature

heretofore. The results of the moderation analyses are important because (i) they reveal the effects of

power distance (H3) and individualism (H4) on metric use not revealed in the analysis of main effects

described in the earlier paragraph; (ii) they provide insight into the conditions under which power

distance and individualism affect total metric use; and (iii) they confirm the effects of country-level

regulation (H1) and cultural variables such as uncertainty avoidance (H2), and long-term orientation (H5)

revealed in the analysis of main effects, and more importantly, reveal the conditions under which the

effects of regulatory (H1), uncertainty avoidance (H2), and long term orientation (H5) on metric use are

more likely to hold.

For example, on (iii), we find that the effects of regulation, uncertainty avoidance, and long term

orientation are more prevalent for marketing (vs. non-marketing) managers, operating in firms with

higher (vs. lower) market orientation and without (vs. with) a CMO. One possibility is that when the firm

has a high market orientation, marketing decisions are ideologically-based (on a strong market

orientation), and as a result there may be less need for data-based metrics to determine the effectiveness

of marketing mix decisions. Another possibility is that when there is no CMO in the firm, there is less

pressure on managers to employ metrics to demonstrate the longer-term effects of marketing mix

24

decisions. And, for example, on (ii), we find that that the effects of power distance on metric use are more

likely for marketing managers in goods and market oriented firms without a CMO; while the effects of

individualism on metric use are more likely for managers operating in B2C and goods oriented firms. One

possibility is that the value of metrics is greater in goods oriented or B2C firms because customers are

further removed from the firm than in service or B2B oriented firms. The new support for power distance

(H3) and individualism (H4), in addition to the conditional results for all five hypotheses are important

empirical findings because they can lead to future theorizing about moderation effects that contributes to

a conditional theory of managerial metric use for marketing mix decisions.

Third, and finally, the proposed model permits an executive at headquarters to form expectations

of metric use by a specific manager (with certain managerial characteristics), operating in a certain

country (with certain regulatory and cultural characteristics), firm, and environment, while making a

particular marketing mix decision. If the manager’s actual use of metrics falls short of expectations, such

an individual-level diagnostic could prove useful in follow-up efforts regarding metric use which enable

managerial contributions. This permits the executive at headquarters to employ a cultural basis for

assessing metric use in contrast to assuming that metric use should be expected to be uniform across

managers operating in various countries.

This study has its limitations. For example, our main goal in this paper is to propose, test, and

establish the main effects of five country-level regulation and cultural variables on metric use, while our

analysis of the moderation of such effects is secondary and exploratory. Because the literature on metric

use is sparse and only recently developing, we do not propose hypotheses for each of the five moderator

variables explored for each of the five hypotheses developed and tested. However, we hope that future

research will employ our findings to develop such hypotheses followed by formal confirmatory testing of

interaction effects in sub-model 1. In addition, there are avenues for future research. For example, while

the primary focus of this work is to assess the effects of country-level variables on metric use and how

these effects may be moderated by firm and managerial characteristics, future research could focus

primarily on the relationship between metric use and performance of marketing mix decisions and how

25

that relationship may be moderated by firm and managerial characteristics. We hope that future research

will build on our efforts in some of these directions.

26

References

Ali, A., L.-S. Hwang. 2000. Country-specific factors related to financial reporting and the value relevance

of accounting data. J. Account. Res. 38(1) 1–21.

Ambler, T. 2003. Marketing and the bottom line: The marketing metrics to pump up cash flow 2nd ed.

London, FT Prentice Hall.

Armstrong, J. S., T. S. Overton. 1977. Estimating nonresponse bias in mail surveys. J. Mark. Res. 14(3)

396–402.

Ball, R., S. P. Kothari, A. Robin. 2000. The effect of international institutional factors on properties of

accounting earnings. J. Account. Econ. 29(1) 1–51.

Burns, T., G. M. Stalker. 1994. The management of innovation Revised edition. Oxford University Press,

USA.

Cateora, P. R., M. C. Gilly, J. L. Graham. 2013. International marketing 16th ed. Chicago, Illinois,

McGraw-Hill/Irwin.

Cavusgil, S. T., A. Das. 1997. Methodological issues in empirical cross-cultural research: A survey of the

management literature and a framework. Manag. Int. Rev. 37(1) 71–96.

Central Intelligence Agency. 2012. Central Intelligence Agency world factbook. Available at:

https://www.cia.gov/library/publications/the-world-factbook/ [Accessed April 2, 2012].

Chang, S.-J., A. van Witteloostuijn, L. Eden. 2010. From the editors: Common method variance in

international business research. J. Int. Bus. Stud. 41(2) 178–184.

Deleersnyder, B., M. G. Dekimpe, J.-B. E. M. Steenkamp, P. S. H. Leeflang. 2009. The role of national

culture in advertising’s sensitivity to business cycles: An investigation across continents. J. Mark.

Res. 46(5) 623–636.

Farris, P. W., N. T. Bendle, P. E. Pfeifer, D. J. Reibstein. 2010. Marketing metrics: The definitive guide to

measuring marketing performance 2nd ed. Upper Saddle River, New Jersey, Wharton School

Publishing.

Franke, G. R., R. G. Richey. 2010. Improving generalizations from multi-country comparisons in

international business research. J. Int. Bus. Stud. 41(8) 1275–1293.

Fredrickson, J., T. Mitchell. 1984. Strategic decision processes: Comprehensiveness and performance in

an industry with an unstable environment. Acad. Manage. J. 27(2) 399–423.

Guler, I., M. F. Guillén. 2009. Institutions and the internationalization of US venture capital firms. J. Int.

Bus. Stud. 41(2) 185–205.

Hair, J. F., R. E. Anderson, R. L. Tatham, W. C. Black. 1998. Multivariate data analysis. Upper Saddle

River, New Jersey, Prentice Hall.

Hewitt, K., R. B. Money, S. Sharma. 2006. National culture and industrial buyer-seller relationships in

the United States and Latin America. J. Acad. Mark. Sci. 34(3) 386–402.

27

Hofstede, G., G. J. Hofstede, M. Minkov. 2010. Cultures and organizations: Software of the mind 3rd ed.

New York, McGraw-Hill.

Hyde, P., E. Landry, A. Tipping. 2004. Making the perfect marketer: A study from the Association of

National Advertisers and Booz Allen Hamilton suggests five ways to make marketing more

relevant than ever. Strat. Bus. 37(Winter) 36–43.

International Monetary Fund. 2010. International Monetary Fund world economic outlook database.

World Econ. Outlook Database. Available at:

http://www.imf.org/external/pubs/ft/weo/2010/01/weodata/index.aspx [Accessed April 2, 2012].

Jaworski, B. J., A. K. Kohli. 1993. Market orientation: Antecedents and consequences. J. Mark. 57(3) 53–

70.

Kanagaretnam, K., C. Y. Lim, G. J. Lobo. 2011. Effects of national culture on earnings quality of banks.

J. Int. Bus. Stud. 42(6) 853–874.

La Porta, R., F. Lopez-De-Silanes, A. Shleifer. 2006. What works in securities laws? J. Finance 61(1) 1–

32.

La Porta, R., F. Lopez-De-Silanes, A. Shleifer, R. W. Vishny. 1997. Legal determinants of external

finance. J. Finance 52(3) 1131–1150.

Leeflang, P. S. H., D. R. Wittink, M. Wedel, P. A. Naert. 2000. Building models for marketing decisions.

Dordrecht, Kluwer Academic Publishers.

Lehmann, D. R., D. J. Reibstein. 2006. Marketing metrics and financial performance. Cambridge,

Massachusetts, Marketing Science Institute.

Leuz, C., D. Nanda, P. D. Wysocki. 2003. Earnings management and investor protection: An international

comparison. J. Financ. Econ. 69(3) 505–527.

Lindell, M. K., D. J. Whitney. 2001. Accounting for common method variance in cross-selectional

research designs. J. Appl. Psychol. 86(1) 114–121.

Marketing Science Institute. 1998, 2000, 2002, 2004, 2006, 2008, 2012. Research priorities: A guide to

MSI research programs and procedures. Cambridge, Massachusetts.

McGovern, G. J., D. Court, J. A. Quelch, B. Crawford. 2004. Bringing customers into the boardroom.

Harv. Bus. Rev. 82(11) 70–80.

Mintz, O., I. S. Currim. 2013. What drives managerial use of marketing and financial metrics and does

metric use affect performance of marketing-mix activities? J. Mark. 77(2) 17–40.

Moorman, C. 2012. The CMO Survey: Highlights and insights February 2012. Fuqua School of Business,

Duke University. Available at:

http://cmosurvey.org/files/2012/03/The_CMO_Survey_Highlights_and_Insights_Feb-

2012_Final.pdf.

Moorman, C., R. T. Rust. 1999. The role of marketing. J. Mark. 63(4) 180–197.

Morgan, N. A., L. L. Rego. 2009. Brand portfolio strategy and firm performance. J. Mark. 73(1) 59–74.

28

Nath, P., V. Mahajan. 2008. Chief marketing officers: A study of their presence in firms’ top management

teams. J. Mark. 72(1) 65–81.

Newman, K. L., S. D. Nollen. 1996. Culture and congruence: The fit between management practices and

national culture. J. Int. Bus. Stud. 27(4) 753–779.

O’Sullivan, D., A. V. Abela. 2007. Marketing performance measurement ability and firm performance. J.

Mark. 71(2) 79–93.

Pauwels, K., T. Ambler, B. H. Clark, P. LaPointe, D. J. Reibstein, B. Skiera, B. Wierenga, and T. Wiesel.

2009. Dashboards as a service: Why, what, how, and what research is needed? J. Serv. Res. 12(2)

175–189.

Powell, T. C. 1992. Organizational alignment as competitive advantage. Strat. Manag. J. 13(2) 119–134.

Roth, M. S. 1995. The effects of culture and socioeconomics on the performance of global brand image

strategies. J. Mark. Res. 32(2) 163–175.

Rubera, G., A. Ordanini, D. A. Griffith. 2011. Incorporating cultural values for understanding the

influence of perceived product creativity on intention to buy: An examination in Italy and the US.

J. Int. Bus. Stud. 42(4) 459–476.

Rust, R. T., T. Ambler, G. S. Carpenter, V. Kumar, R. K. Srivastava. 2004. Measuring marketing

productivity: Current knowledge and future directions. J. Mark. 68(4) 76–89.

Sheth, J. N., R. S. Sisodia. 2005. A dangerous divergence: Marketing and society. J. Public Policy Mark.

24(1) 160–162.

Srinivasan, S., D. M. Hanssens. 2009. Marketing and firm value: Metrics, methods, findings, and future

directions. J. Mark. Res. 46(3) 293–312.

Steenkamp, J.-B. E. M., F. ter Hofstede, M. Wedel. 1999. A cross-national investigation into the

individual and national cultural antecedents of consumer innovativeness. J. Mark. 63(2) 55–69.

Tan, B. C. Y., K. Wei, R. T. Watson, D. L. Clapper, E. R. Mclean. 1998. Computer-Mediated

communication and majority influence: Assessing the impact in an individualistic and a

collectivistic culture. Manag. Sci. 44(9) 1263–1278.

The Institute for the Study of Business Markets. 2008, 2010, 2012. B-to-B marketing trends. University

Park, Pennsylvania.

Tse, D. K., K. Lee, Ii. Vertinsky, D. A. Wehrung. 1988. Does culture matter? A cross-cultural study of

executives’ choice, decisiveness, and risk adjustment in international marketing. J. Mark. 52(4)

81–95.

Tung, R. L., A. Verbeke. 2010. Beyond Hofstede and GLOBE: Improving the quality of cross-cultural

research. J. Int. Bus. Stud. 41(8) 1259–1274.

Tung, R. L., A. van Witteloostuijn. 2008. From the editors: what makes a study sufficiently international?

J. Int. Bus. Stud. 39(2) 180–183.

29

Verhoef, P. C., P. S. H. Leeflang. 2009. Understanding the marketing department’s influence within the

firm. J. Mark. 73(2) 14–37.

Webster Jr., F. E., A. J. Malter, S. Ganesan. 2005. The decline and dispersion of marketing competence.

MIT Sloan Manag. Rev. 46(4) 35–43.

White, H. 1980. A heteroskedasticity-consistent covariance matrix estimator and a direct test for

heteroskedasticity. Econometrica 48(4) 817–838.

30

Figure 1. Conceptual Model

Marketing Mix

Performance

Managerial

Metric Use

Country-Level Variables Regulatory Disclosure

Requirements (-)

Culture

o Uncertainty Avoidance (-)

o Power Distance (+)

o Individualism (+)

o Long-Term Orientation (-)

Exploratory Analyses

Moderator Variables Managerial

Characteristics

Firm Characteristics

Control Variables Managerial Characteristics

Firm Characteristics

Environmental Characteristics

Type of Marketing Mix Decision

Mintz and Currim (2013)

This paper

31

Table 1. Panel A. Reported Percentage Use of General Metrics

Over

all

Low

DS

CR

EQ

Hig

h

DS

CR

EQ

Low

UA

I

Hig

h

UA

I

Low

PD

I

Hig

h

PD

I

Low

IDV

Hig

h

IDV

Low

LT

O

Hig

h

LT

O

Average Number of

Metrics Used 6.95 7.41 6.81 6.85 7.58 6.92 7.18 7.17 6.89 6.99 6.81

Average Number of

Mkt. Metrics Used 3.72 3.99 3.64 3.66 4.12 3.68 3.98 3.83 3.69 3.75 3.60

Average Number of

Fin. Metrics Used 3.23 3.42 3.17 3.19 3.46 3.23 3.20 3.34 3.20 3.23 3.21

Percent Using

No Metrics 7% 4% 8% 7% 3% 7% 5% 5% 7% 7% 5%

Marketing Metrics

Awareness

(Product or Brand) 41% 37% 43% 42% 37% 42% 36% 35% 43% 43% 34%

Consideration Set 4% 5% 4% 4% 4% 4% 5% 5% 4% 4% 5%

Likeability

(Product or Brand) 15% 14% 15% 15% 16% 15% 15% 13% 16% 16% 10%

Loyalty

(Product or Brand) 21% 22% 20% 21% 20% 21% 20% 22% 20% 21% 21%

Market Share

(Units or Dollars) 28% 33% 26% 26% 38% 27% 31% 31% 27% 27% 31%

Perceived Product

Quality 21% 21% 21% 20% 26% 21% 24% 20% 22% 22% 17%

Preference

(Product or Brand) 19% 23% 17% 17% 28% 18% 23% 21% 18% 19% 17%

Satisfaction

(Product or Brand) 21% 23% 20% 20% 25% 21% 22% 20% 21% 22% 18%

Share of Voice 10% 14% 9% 10% 12% 9% 14% 14% 9% 9% 12%

Share of Customer

Wallet 13% 15% 12% 12% 14% 12% 15% 14% 12% 12% 13%

Total Customers 36% 38% 35% 35% 40% 35% 41% 39% 35% 35% 38%

Willingness to

Recommend

(Product or Brand)

22% 22% 22% 22% 21% 23% 19% 18% 23% 24% 17%

Other Mkt. Metric 5% 4% 5% 5% 3% 5% 6% 4% 5% 5% 5%

Financial Metrics

CLV 12% 12% 11% 12% 10% 12% 11% 13% 11% 11% 12%

Customer Segment

Profitability 17% 17% 17% 17% 16% 18% 13% 15% 18% 17% 16%

EVA 4% 5% 4% 4% 5% 4% 4% 4% 4% 4% 4%

Marketing

Expenditures (%

specifically on Brand

Building Activities)

21% 18% 22% 21% 21% 22% 17% 16% 22% 23% 16%

NPV 8% 8% 8% 7% 11% 8% 8% 9% 8% 8% 6%

Net Profit 24% 23% 24% 23% 30% 24% 23% 23% 24% 26% 19%

ROI 38% 39% 38% 38% 39% 38% 39% 37% 39% 39% 36%

ROMI 21% 25% 20% 21% 24% 21% 27% 24% 21% 21% 23%

ROS 18% 22% 17% 16% 27% 17% 25% 23% 17% 17% 20%

Stock Prices /

Stock Returns 1% 2% 1% 1% 2% 1% 2% 2% 1% 1% 2%

Target Volume

(Units or Sales) 39% 44% 38% 39% 43% 39% 40% 44% 38% 39% 41%

Tobin’s q 0% 0% 0% 0% 0% 0% 0% 0% 0% 0% 0%

Other Fin. Metric 3% 3% 3% 3% 3% 3% 2% 3% 3% 3% 3%

32

Table 1. Panel B. Reported Percentage Use of Specific Metrics

Over

all

Low

DS

CR

EQ

Hig

h

DS

CR

EQ

Low

UA

I

Hig

h

UA

I

Low

PD

I

Hig

h

PD

I

Low

IDV

Hig

h

IDV

Low

LT

O

Hig

h

LT

O

Marketing Metrics

Channel Margins 9 60% 56% 61% 64% 33% 61% 50% 58% 60% 59% 62%

Conversion Rate 2,3 52% 59% 49% 50% 61% 52% 51% 57% 50% 49% 60%

Cost per Click 2 63% 57% 64% 63% 63% 64% 54% 58% 64% 63% 60%

Cost per Customer

Acquired 3 37% 39% 37% 39% 29% 38% 35% 39% 37% 35% 45%

CPM 1 32% 33% 31% 32% 27% 33% 25% 34% 31% 31% 32%

Cost per Exposure 4,10 37% 49% 33% 36% 48% 36% 48% 49% 34% 35% 45%

Expected Margin % 7 50% 38% 54% 53% 34% 53% 32% 40% 53% 53% 39%

IRR 1,2,5,7 8% 7% 10% 10% 8% 9% 12% 9% 10% 10% 7%

Lead Generation1,3,4,10 36% 47% 43% 45% 40% 45% 35% 44% 44% 43% 49%

Level of

Cannibalization 7 28% 27% 28% 28% 28% 29% 23% 28% 28% 29% 24%

Optimal Price 6 36% 48% 32% 34% 48% 33% 56% 45% 33% 35% 39%

Price Elasticity 6 40% 36% 42% 42% 29% 41% 31% 29% 44% 44% 25%

Promotional Sales /

Incremental Lift 5 58% 63% 56% 59% 50% 58% 56% 64% 55% 57% 60%

Redemption Rates 5 24% 22% 25% 24% 25% 23% 28% 20% 26% 26% 20%

Sales Force

Productivity 8 56% 63% 54% 56% 58% 55% 65% 64% 54% 54% 64%

Sales Funnel 8 58% 63% 56% 57% 63% 58% 61% 62% 57% 56% 64%

Sales per Store /

SKUS 9 26% 31% 24% 25% 33% 24% 38% 42% 22% 24% 31%

Sales Potential

Forecast 8 54% 59% 53% 56% 46% 55% 48% 54% 55% 54% 56%

Total Costs 4,10 27% 29% 26% 27% 24% 27% 22% 28% 26% 27% 26%

Total Inventory /

Total Distributors 9 40% 44% 39% 42% 33% 41% 38% 50% 38% 39% 46%

Unit Margin 6 49% 55% 47% 48% 52% 49% 50% 55% 47% 47% 57%

Financial Metrics

Attitude toward

Product / Brand 7 38% 44% 36% 37% 41% 37% 45% 45% 36% 36% 45%

Belief in New

Product Concept 7 44% 44% 44% 45% 38% 46% 27% 43% 44% 45% 42%

Click-through Rate 2 75% 72% 75% 76% 67% 78% 57% 68% 77% 75% 73%

Expected Annual

Growth Rate 7 34% 19% 39% 37% 17% 36% 18% 18% 38% 37% 18%

Hits/Page Views 2,4 65% 61% 66% 65% 60% 66% 57% 60% 66% 65% 61%

Impressions 1,2,5 39% 35% 40% 39% 38% 40% 33% 37% 39% 39% 37%

New Customer

Retention Rate 3,8 31% 46% 27% 29% 46% 30% 40% 44% 28% 27% 47%

# of Followers4 60% 58% 60% 61% 54% 60% 57% 58% 60% 61% 55%

# of Responses by

Campaign 3,8 51% 57% 49% 51% 54% 51% 50% 55% 50% 50% 56%

Out of Stock Percent9 23% 19% 24% 23% 22% 22% 25% 25% 22% 24% 15%

Price Premium 6 42% 58% 37% 37% 67% 39% 63% 58% 37% 39% 54%

PCV 9 19% 19% 20% 17% 33% 19% 25% 25% 18% 20% 15%

Reach 1,3,5,7,10 33% 35% 32% 33% 32% 32% 40% 37% 32% 33% 31%

Recall 1,10 17% 27% 14% 15% 35% 15% 33% 25% 15% 16% 20%

Relative Price 6 42% 45% 41% 40% 52% 39% 63% 45% 41% 42% 39%

Reservation Price 6 10% 9% 10% 9% 14% 9% 19% 10% 10% 10% 11%

Strength of Channel

Relationships 9 66% 75% 63% 64% 78% 65% 75% 67% 66% 65% 69%

Trial / Repeat

Volume (or Ratio) 5 26% 37% 22% 25% 30% 23% 39% 40% 22% 23% 36%

Volume of

Coverage4,10 30% 43% 26% 28% 42% 27% 46% 39% 27% 27% 39%

Specific metrics corresponds to the following marketing mix decisions: 1=Traditional Advertising, 2=Internet Advertising, 3=Direct to

Consumer, 4=Social Media, 5=Price Promotions, 6=Pricing, 7=New Product Development, 8=Sales Force, 9=Distribution, 10=PR/Sponsorship

33

Table 2. Country-level Data and Predictions of Managerial Metric Use*

Country DSCREQ UAI PDI IDV LTO Predicted

Metric

Use**

Argentina 0.50 86 49 46 20 6.17

Australia 0.75 51 36 90 21 6.37

Austria 0.25 70 11 55 60 5.34

Belgium 0.42 94 65 75 82 3.71

Brazil 0.25 76 69 38 44 6.99

Canada 0.92 48 39 80 36 4.61

Chile 0.58 86 63 23 31 5.08

Denmark 0.58 23 18 74 35 7.03

Finland 0.50 59 33 63 38 6.12

France 0.75 86 68 71 63 3.17

Germany 0.42 65 35 67 83 4.00

Greece 0.33 112 60 35 45 4.87

India 0.92 40 77 48 51 4.45

Ireland 0.67 35 28 70 24 6.81

Israel 0.67 81 13 54 38 3.75

Italy 0.67 75 50 76 61 3.84

Japan 0.75 92 54 46 88 0.91

Mexico 0.58 82 81 30 24 6.10

Netherlands 0.50 53 38 80 67 5.12

Pakistan 0.58 70 55 14 50 4.34

Philippines 0.83 44 94 32 27 6.25

Portugal 0.42 104 63 27 28 5.53

Slovenia 1.00 51 104 52 49 4.32

South Africa 0.83 49 49 65 34 5.20

Spain 0.50 86 57 51 48 4.89

Sweden 0.58 29 31 71 53 6.05

Switzerland 0.67 58 34 68 74 3.31

Thailand 0.92 64 64 20 32 3.88

Turkey 0.50 85 66 37 46 5.02