Embed Size (px)

Citation preview

Dominican Republic Growth Diagnostics Report

José María Fanelli

Rolando Guzman

Washington, DC,

September 19, 2007

Session II

The macroeconomic constraints

Debt sustainability, fiscal adjustment, and the exchange rate

José María Fanelli

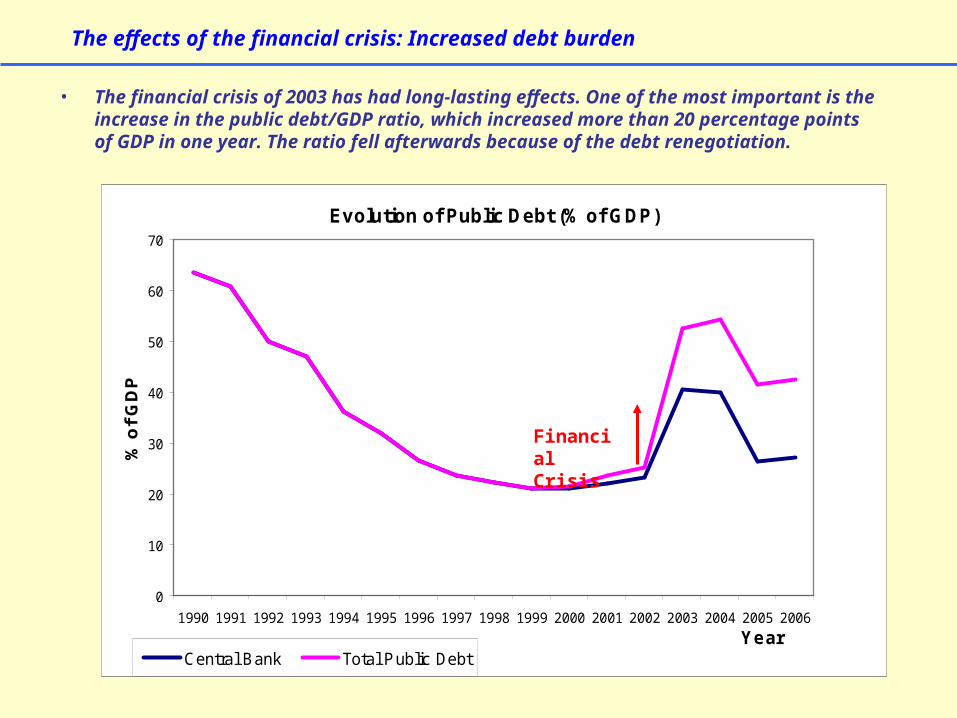

• The financial crisis of 2003 has had long-lasting effects. One of the most important is the increase in the public debt/GDP ratio, which increased more than 20 percentage points of GDP in one year. The ratio fell afterwards because of the debt renegotiation.

The effects of the financial crisis: Increased debt burden

Evolution of Public Debt (% of GDP)

0

10

20

30

40

50

60

70

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

Year

% o

f G

DP

Central Bank Total Public Debt

Financial Crisis

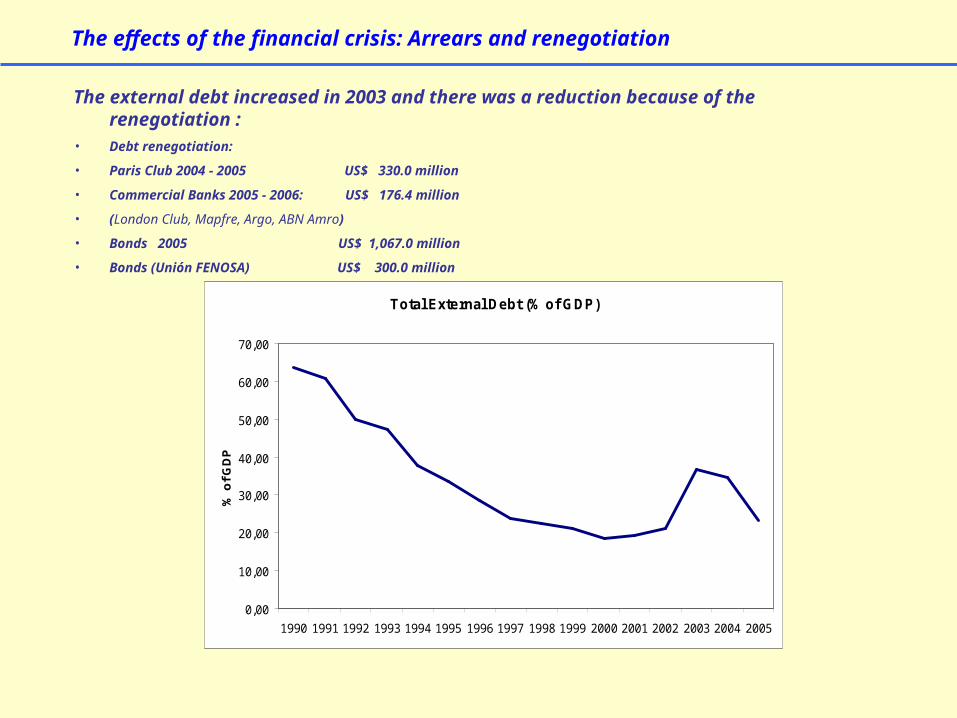

The external debt increased in 2003 and there was a reduction because of the renegotiation :

• Debt renegotiation:

• Paris Club 2004 - 2005 US$ 330.0 million

• Commercial Banks 2005 - 2006: US$ 176.4 million

• (London Club, Mapfre, Argo, ABN Amro)

• Bonds 2005 US$ 1,067.0 million

• Bonds (Unión FENOSA) US$ 300.0 million

The effects of the financial crisis: Arrears and renegotiation

Total External Debt (% of GDP)

0,00

10,00

20,00

30,00

40,00

50,00

60,00

70,00

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

% o

f G

DP

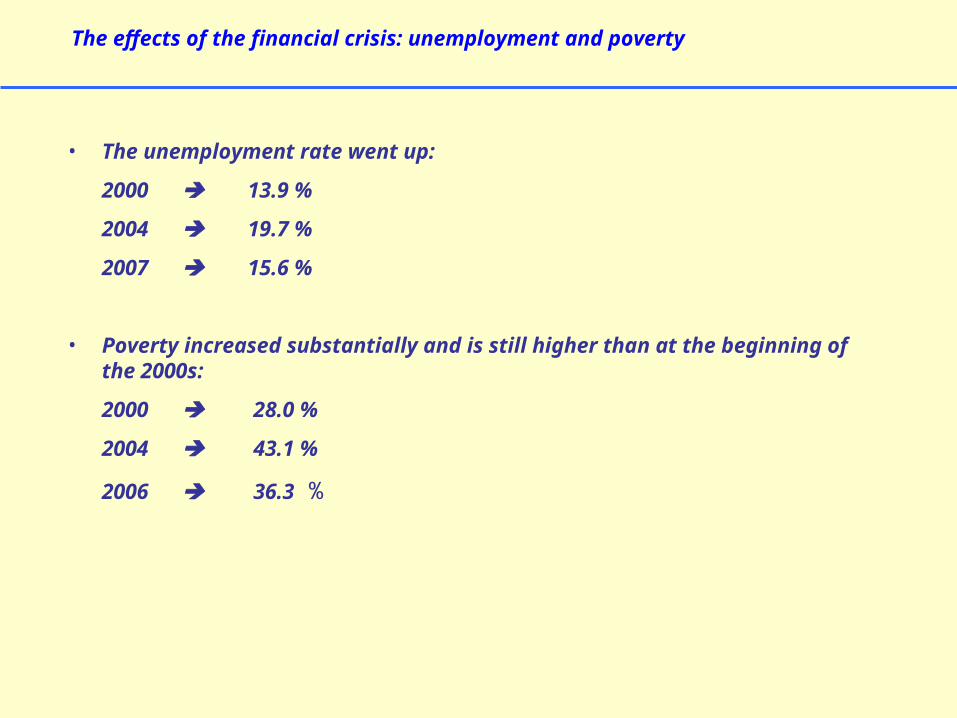

• The unemployment rate went up:

2000 13.9 %

2004 19.7 %

2007 15.6 %

• Poverty increased substantially and is still higher than at the beginning of the 2000s:

2000 28.0 %

2004 43.1 %

2006 36.3 %

The effects of the financial crisis: unemployment and poverty

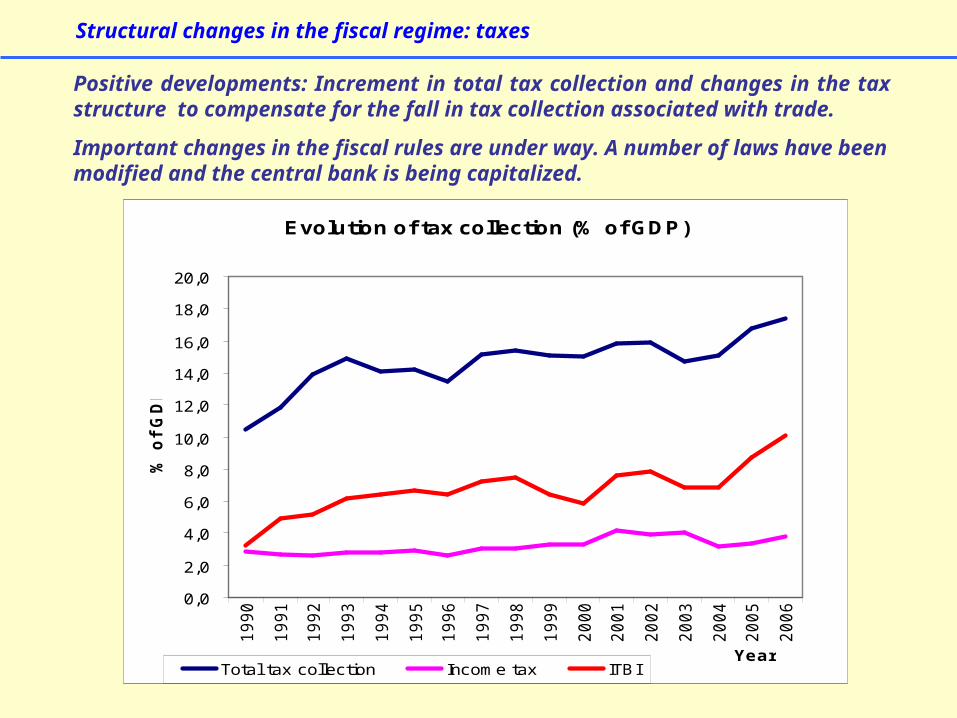

Positive developments: Increment in total tax collection and changes in the tax structure to compensate for the fall in tax collection associated with trade.

Important changes in the fiscal rules are under way. A number of laws have been modified and the central bank is being capitalized.

Structural changes in the fiscal regime: taxes

Evolution of tax collection (% of GDP)

0,0

2,0

4,0

6,0

8,0

10,0

12,0

14,0

16,0

18,0

20,0

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

Year

% o

f G

DP

Total tax collection Income tax ITBI

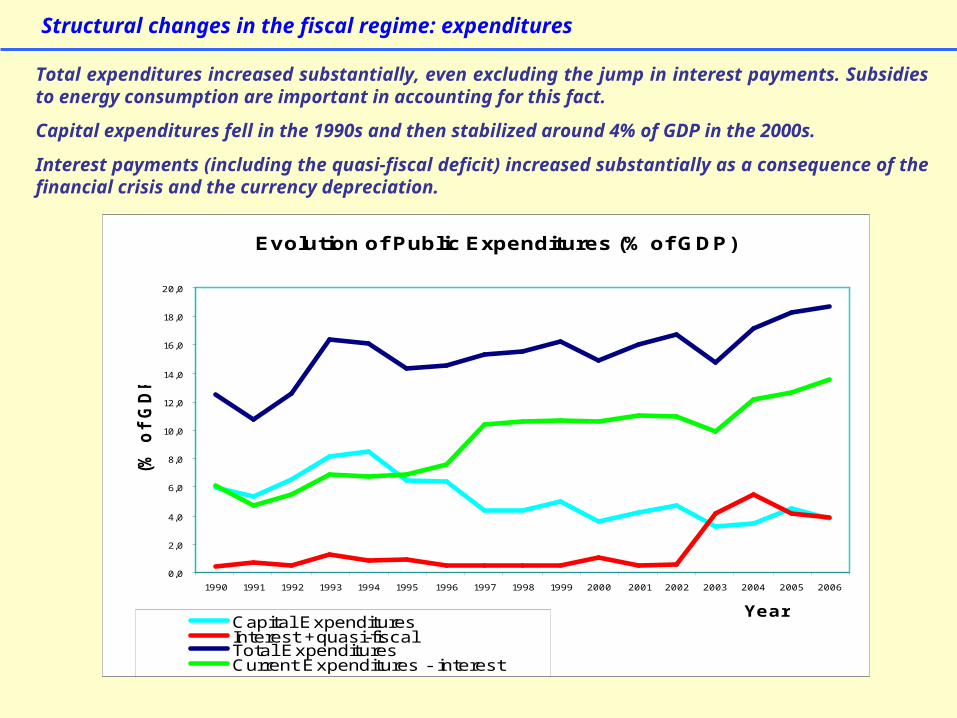

Structural changes in the fiscal regime: expenditures

Total expenditures increased substantially, even excluding the jump in interest payments. Subsidies to energy consumption are important in accounting for this fact.

Capital expenditures fell in the 1990s and then stabilized around 4% of GDP in the 2000s.

Interest payments (including the quasi-fiscal deficit) increased substantially as a consequence of the financial crisis and the currency depreciation.

Evolution of Public Expenditures (% of GDP)

0,0

2,0

4,0

6,0

8,0

10,0

12,0

14,0

16,0

18,0

20,0

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

Year

(% o

f G

DP

)

Capital ExpendituresInterest +quasi-fiscalTotal ExpendituresCurrent Expenditures - interest

1990-2002 2003-2006 Increment

Current expenditures - interest 8.4 12.1 3.7

Capital expenditures 5.7 3.7 -1.9

Interest payments + quasi-fiscal 0.7 4.4 3.7

Total expenditures 14.8 17.2 2.5

Total expenditures +quasi-fiscal 14.7 20.2 5.5

Total tax collection 14.2 16.0 1.8

Total revenues 15.2 17.1 1.9

Increment in fiscal deficit 3.7

Structural changes in the fiscal regime: crowding out?

•Current expenditures jumped after the crisis. The increment is sufficient to account for the increase in the fiscal deficit.

•It follows that the increase in interest payments was financed with the increase in revenues and the decrease in capital expenditures.

•Interest payments and current expenditures crowded out investment directly via public investment and indirectly via the increase in interest rates.

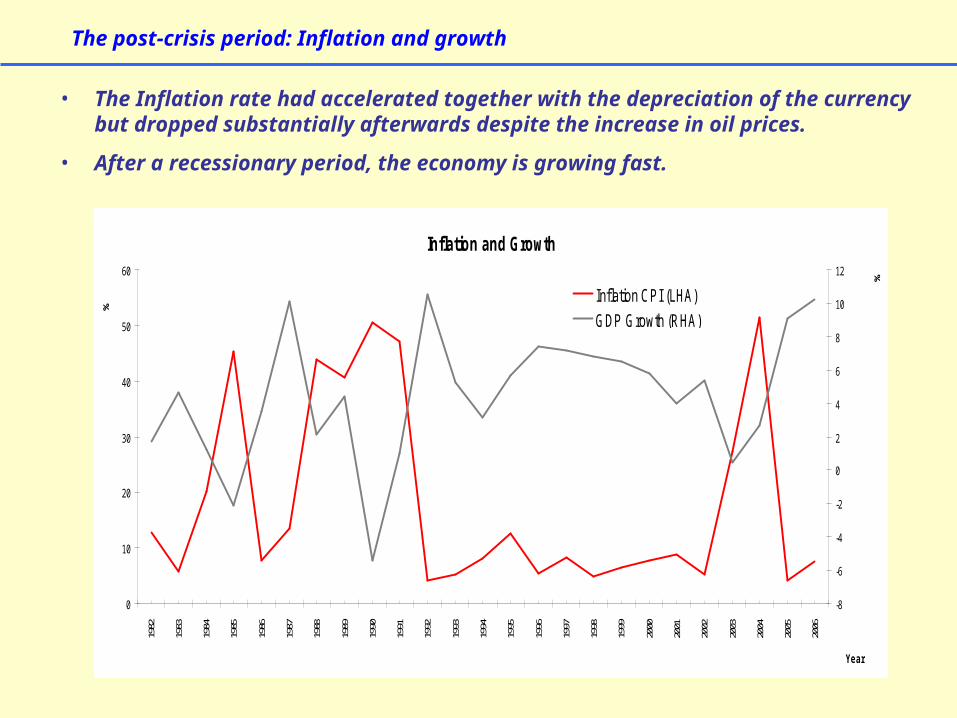

• The Inflation rate had accelerated together with the depreciation of the currency but dropped substantially afterwards despite the increase in oil prices.

• After a recessionary period, the economy is growing fast.

The post-crisis period: Inflation and growth

Inflation and Growth

0

10

20

30

40

50

60

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

Year

%

-8

-6

-4

-2

0

2

4

6

8

10

12

%

Inflation CPI (LHA)

GDP Growth (RHA)

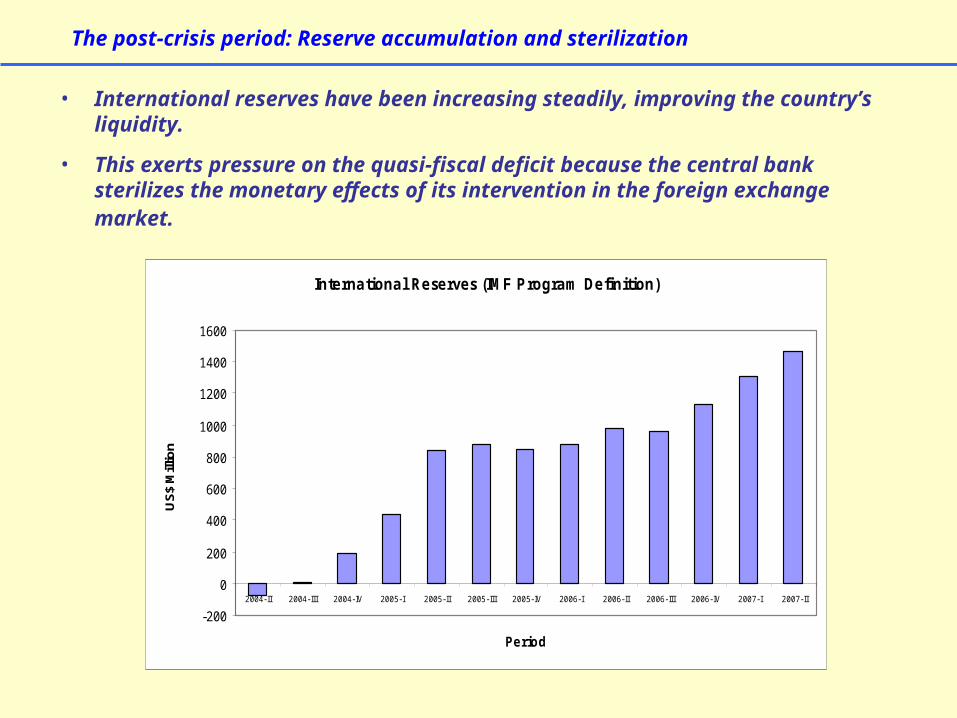

• International reserves have been increasing steadily, improving the country’s liquidity.

• This exerts pressure on the quasi-fiscal deficit because the central bank sterilizes the monetary effects of its intervention in the foreign exchange market.

The post-crisis period: Reserve accumulation and sterilization

International Reserves (IMF Program Definition)

-200

0

200

400

600

800

1000

1200

1400

1600

2004-II 2004-III 2004-IV 2005-I 2005-II 2005-III 2005-IV 2006-I 2006-II 2006-III 2006-IV 2007-I 2007-II

Period

US

$ M

illio

n

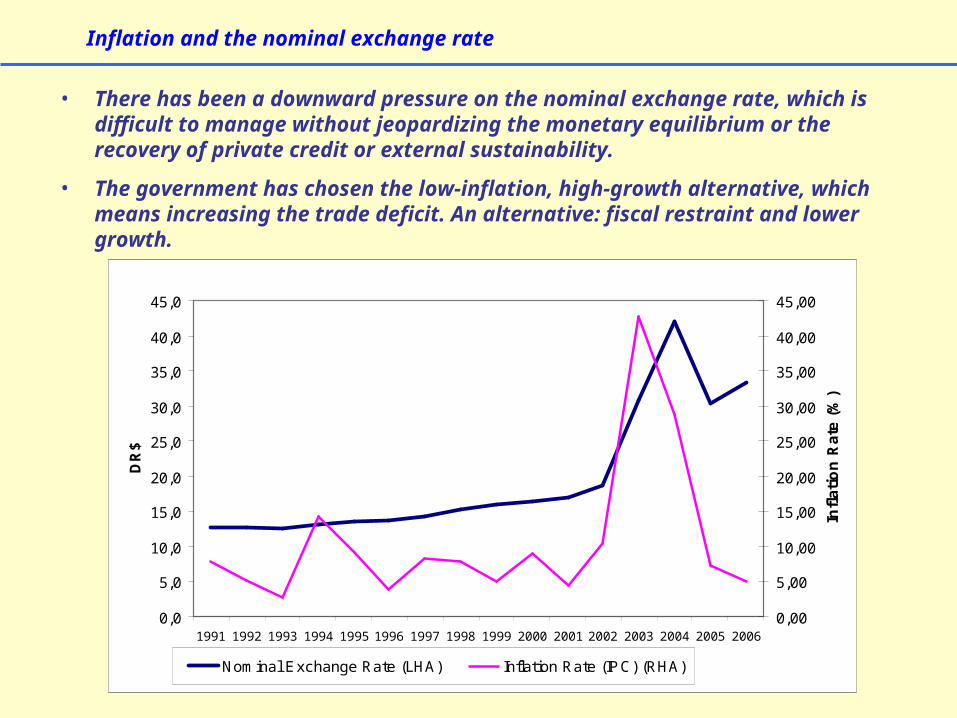

• There has been a downward pressure on the nominal exchange rate, which is difficult to manage without jeopardizing the monetary equilibrium or the recovery of private credit or external sustainability.

• The government has chosen the low-inflation, high-growth alternative, which means increasing the trade deficit. An alternative: fiscal restraint and lower growth.

Inflation and the nominal exchange rate

0,0

5,0

10,0

15,0

20,0

25,0

30,0

35,0

40,0

45,0

1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

Period

DR

$

0,00

5,00

10,00

15,00

20,00

25,00

30,00

35,00

40,00

45,00

Infl

ati

on

Ra

te (

%)

Nominal Exchange Rate (LHA) Inflation Rate (IPC) (RHA)

• The future evolution of relative prices may harm other policy goals

The real exchange rate

Real Exchange Rate (CPI)

0

20

40

60

80

100

120

140

160

Q1

19

91

Q3

19

91

Q1

19

92

Q3

19

92

Q1

19

93

Q3

19

93

Q1

19

94

Q3

19

94

Q1

19

95

Q3

19

95

Q1

19

96

Q3

19

96

Q1

19

97

Q3

19

97

Q1

19

98

Q3

19

98

Q1

19

99

Q3

19

99

Q1

20

00

Q3

20

00

Q1

20

01

Q3

20

01

Q1

20

02

Q3

20

02

Q1

20

03

Q3

20

03

Q1

20

04

Q3

20

04

Q1

20

05

Q3

20

05

Q1

20

06

Q3

20

06

Q1

20

07

Year

19

91

=1

00

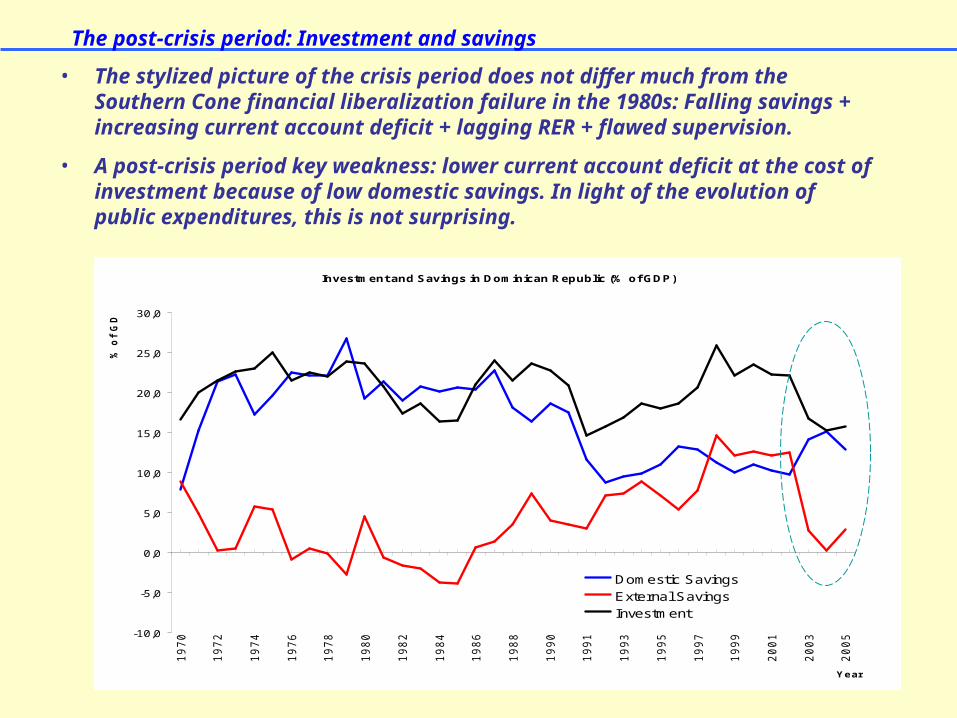

• The stylized picture of the crisis period does not differ much from the Southern Cone financial liberalization failure in the 1980s: Falling savings + increasing current account deficit + lagging RER + flawed supervision.

• A post-crisis period key weakness: lower current account deficit at the cost of investment because of low domestic savings. In light of the evolution of public expenditures, this is not surprising.

The post-crisis period: Investment and savings

Investment and Savings in Dominican Republic (% of GDP)

-10,0

-5,0

0,0

5,0

10,0

15,0

20,0

25,0

30,0

19

70

19

72

19

74

19

76

19

78

19

80

19

82

19

84

19

86

19

88

19

90

19

91

19

93

19

95

19

97

19

99

20

01

20

03

20

05

Year

% o

f G

DP

Domestic Savings

External Savings

Investment

Fiscal Sustainability

• Fiscal sustainability can give rise to difficulties in the future.

-6,00

-4,00

-2,00

0,00

2,00

4,00

6,00

1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

% o

f G

DP

Primary Surplus + Quasi-fiscal Result

Required Primary Fiscal Surplus (long run)

Required Primary Fiscal Surplus (8% interest rate)

Required Primary Fiscal Surplus (with extra effort)

Real interest rate = 6%

Growth rate = 5 %

External Sustainability

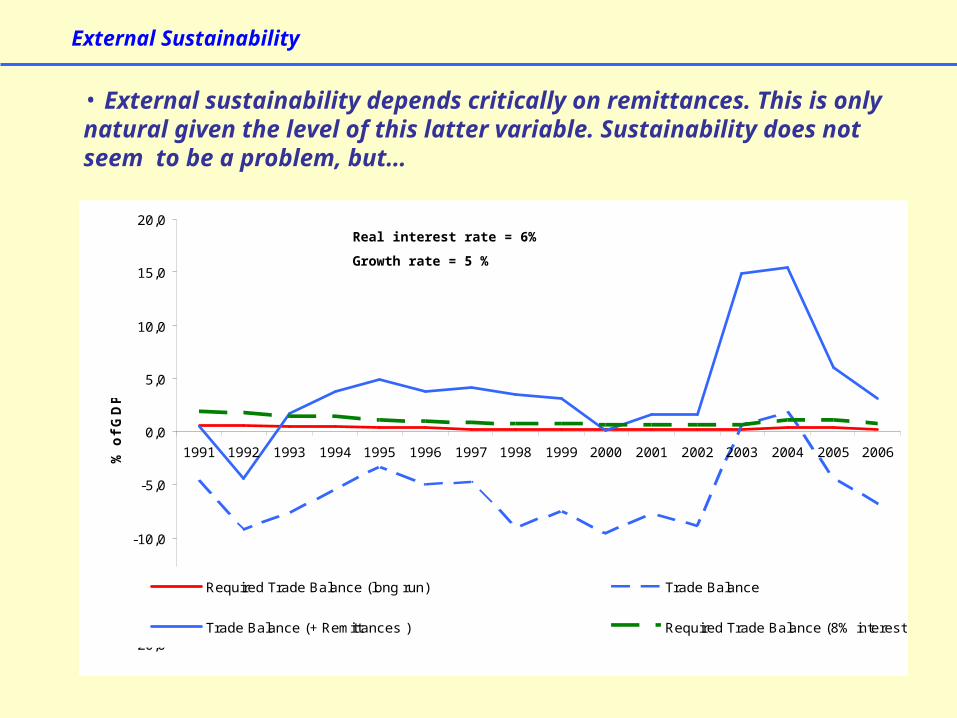

• External sustainability depends critically on remittances. This is only natural given the level of this latter variable. Sustainability does not seem to be a problem, but…

-20,0

-15,0

-10,0

-5,0

0,0

5,0

10,0

15,0

20,0

1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

% o

f G

DP

Required Trade Balance (long run) Trade Balance

Trade Balance (+ Remittances ) Required Trade Balance (8% interest rate)

Real interest rate = 6%

Growth rate = 5 %

External Sustainability

Investment Income

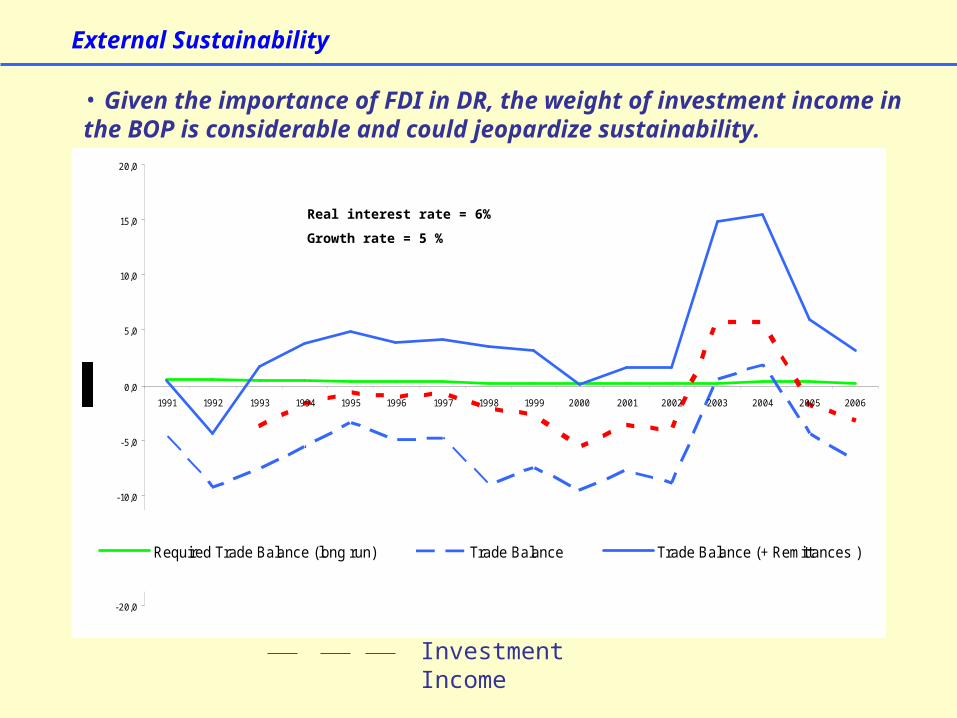

• Given the importance of FDI in DR, the weight of investment income in the BOP is considerable and could jeopardize sustainability.

-20,0

-15,0

-10,0

-5,0

0,0

5,0

10,0

15,0

20,0

1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

Required Trade Balance (long run) Trade Balance Trade Balance (+ Remittances ) FDI income

Real interest rate = 6%

Growth rate = 5 %

• The authorities established targets for the inflation rate, although the IMF monitors the domestic money supply.

• Under the current circumstances, the instability of the demand for money may translate into price instability and relative-price distortions.

• The country is running a current account deficit and still accumulates reserves; this means that the instability of capital inflows also matters to price and aggregate demand stability.

• It will be necessary to discuss what the best regime for the Dominican Republic is; this will have to be discussed in the near future, if the IMF ceases to monitor the country.

• It seems that a “risk management approach” could help to the extent that there are many sources of macro risk that should be taken simultaneously into account (financial, fiscal, and external shocks).

• A risk management approach calls for a tighter coordination between monetary and fiscal policies. The current tax-expenditures mix may be crowding out private investment and, hence, growth.

The policy stance: monetary and fiscal regimes

• In line with DR tradition, the authorities have shown an ability to deal with macro disequilibria. However, potential sources of macro risk remain. Macro risks will increase and can jeopardize growth if DR does not solve a number of imbalances.

• The weakening-of-competitiveness problem that affects FTZs and has to do with weak self-discovery could menace external sustainability or restrain growth if imports cannot grow dynamically or there is a fall in FDI flows.

• The negative features of the fiscal regime associated with interest payments, subsidies, and the crowding out of private investment may negatively influence the investment in infrastructure, human capital, and the national innovation system.

• The definition of a financial development-friendly monetary regime is central to the extent that financial intermediation plays a role in reducing duality and fostering self-discovery.

Why does all this macro matter to growth diagnostics?

• Policies should be oriented to defining a development-friendly macroeconomic regime, which takes into account the following.

• The real exchange rate matters to the development of both the tradable and the non-tradable sectors: The real exchange rate may have a role as a “first mover” concerning the tradable sector and can make the accumulation of human capital cheaper. An appreciated currency would not help.

• It is necessary to design coordinated fiscal and financial policies oriented to promote the allocation of remittances to human capital accumulation.

• Haitian cheap labor is probably exerting a relevant downward pressure on wages. This can help price-competitiveness in a context in which the competitive pressures are increasing. It is an advantage that other competitors in Central America may not have.

• Cheap labor, however, cannot do much to improve other non-price components of competitiveness, which are closely associated with self-discovery, finance, and the national system of innovation.

Why does all this macro matter to growth diagnostics?