Embed Size (px)

DESCRIPTION

Doncaster's Local Housing Assessment

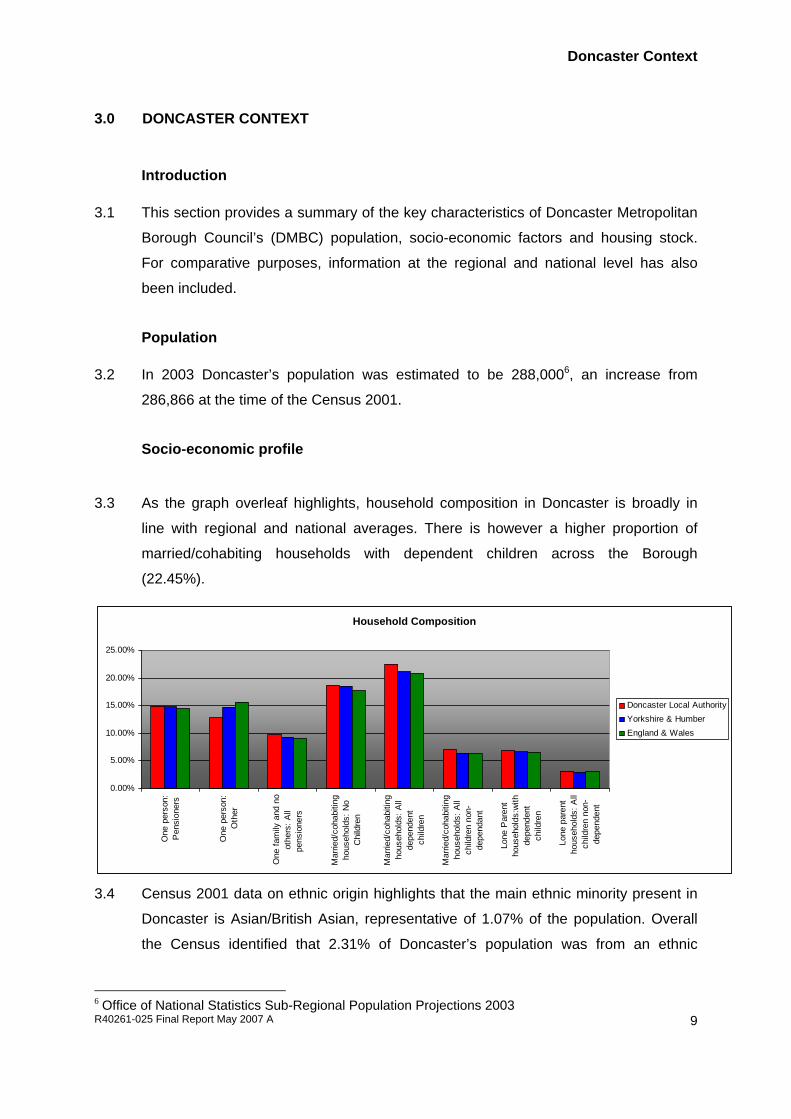

Citation preview

May 2007

Nathaniel Lichfield & Partners Ltd Generator Studios Trafalgar Street Newcastle upon Tyne NE1 2LA

T 0191 261 5685 F 0191 261 9180 [email protected] www.nlpplanning.com

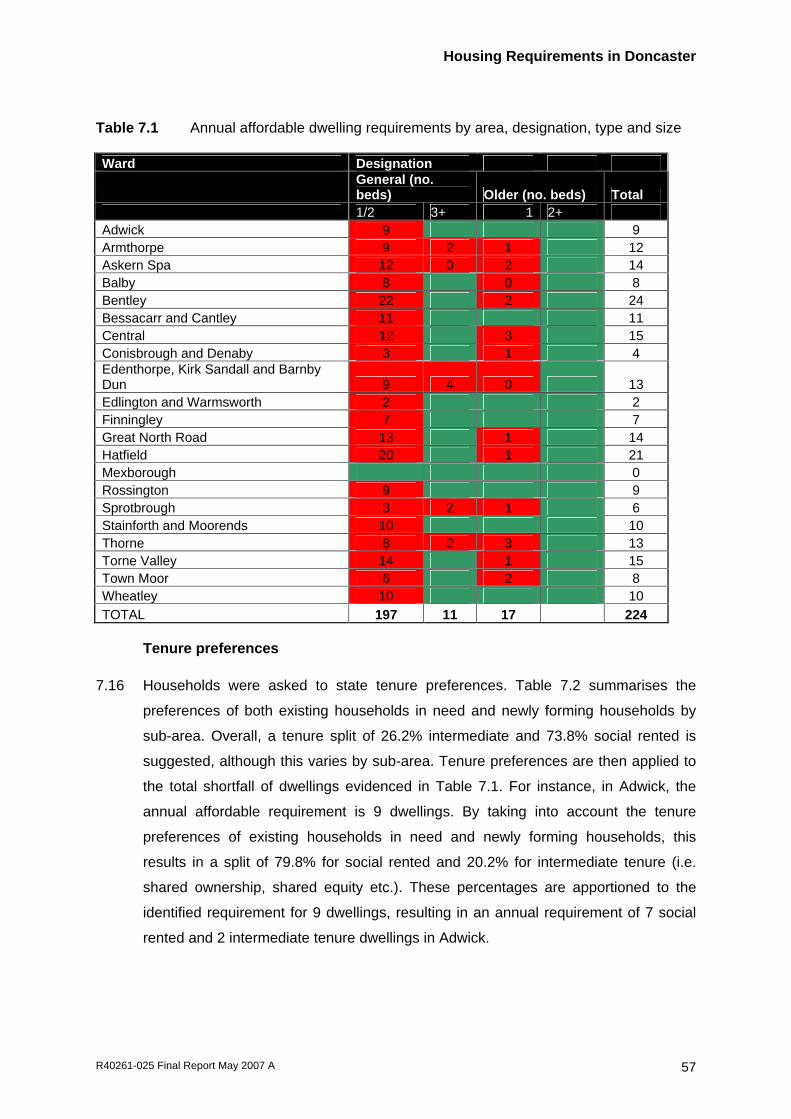

Doncaster Local Housing Assessment

Final Report

Offices also in: Cardiff London Manchester

R40261-025 Final Report May 2007 A 2

CONTENTS

1.0 INTRODUCTION.......................................................................................................... 2

2.0 POLICY AND STRATEGY CONTEXT ........................................................................ 2

Introduction .................................................................................................................. 2 Economy ...................................................................................................................... 2 Housing Mix ................................................................................................................. 3 Housing Numbers ........................................................................................................ 5 Total Net Provision over RSS Period ........................................................................... 6 Affordable Housing ...................................................................................................... 6 Sustainable Communities ............................................................................................ 7 Summary...................................................................................................................... 8

3.0 DONCASTER CONTEXT ............................................................................................ 9

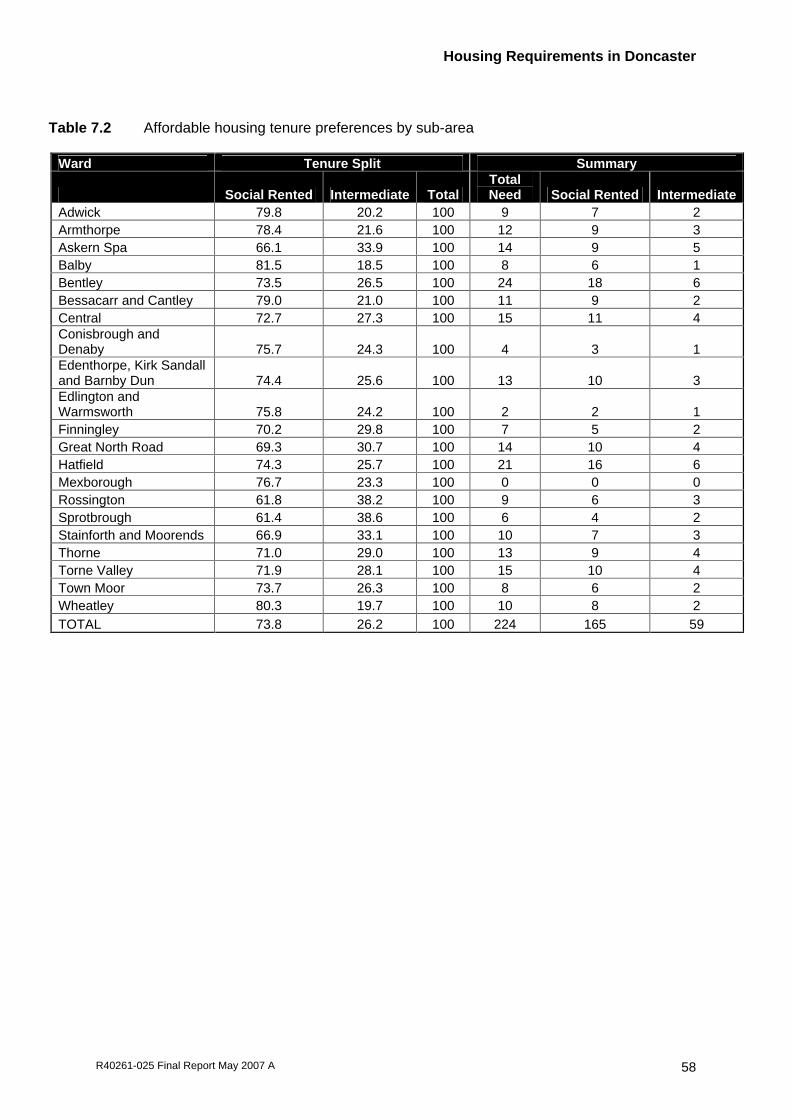

Introduction .................................................................................................................. 9 Population .................................................................................................................... 9 Socio-economic profile................................................................................................. 9 Housing Type and Tenure ......................................................................................... 12 Employment Structure ............................................................................................... 15 House Price Analysis ................................................................................................. 18 Summary.................................................................................................................... 21

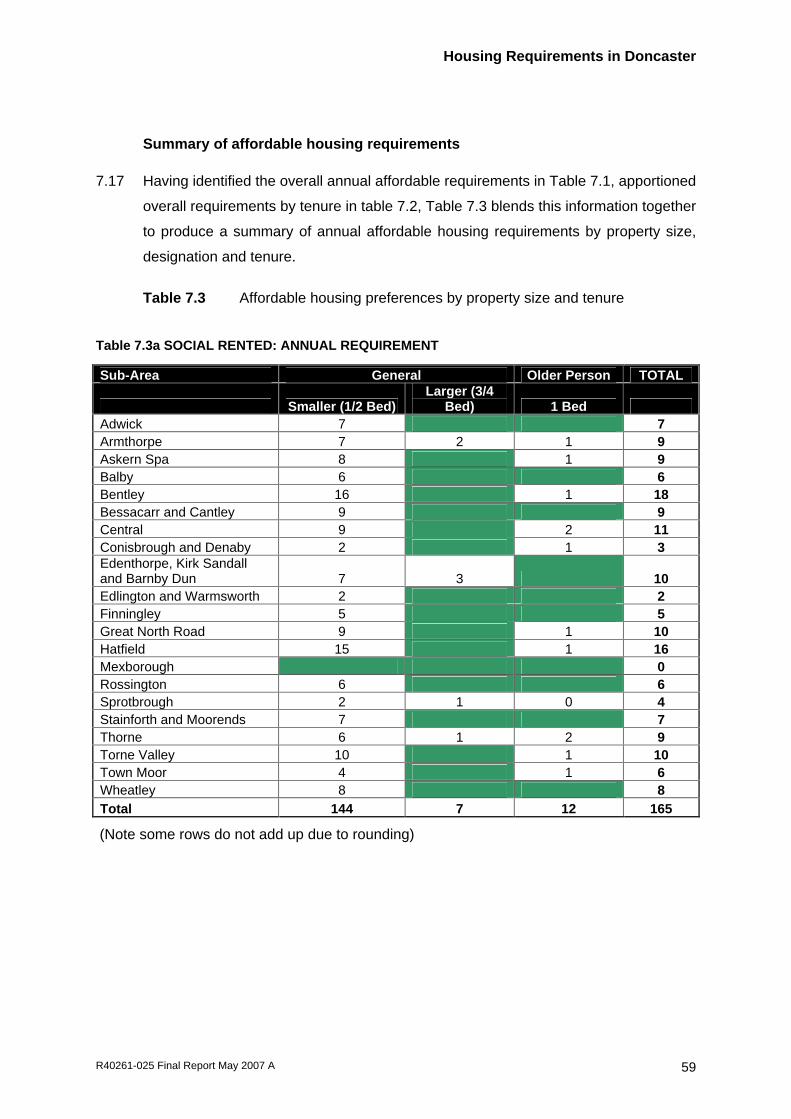

4.0 IDENTIFYING THE CURRENT HOUSING MARKET ............................................... 23

Travel to Work Data ................................................................................................... 23 Migration Patterns...................................................................................................... 25 Future Migration Patterns .......................................................................................... 27 Migration and Travel-to-Work Summary .................................................................... 28

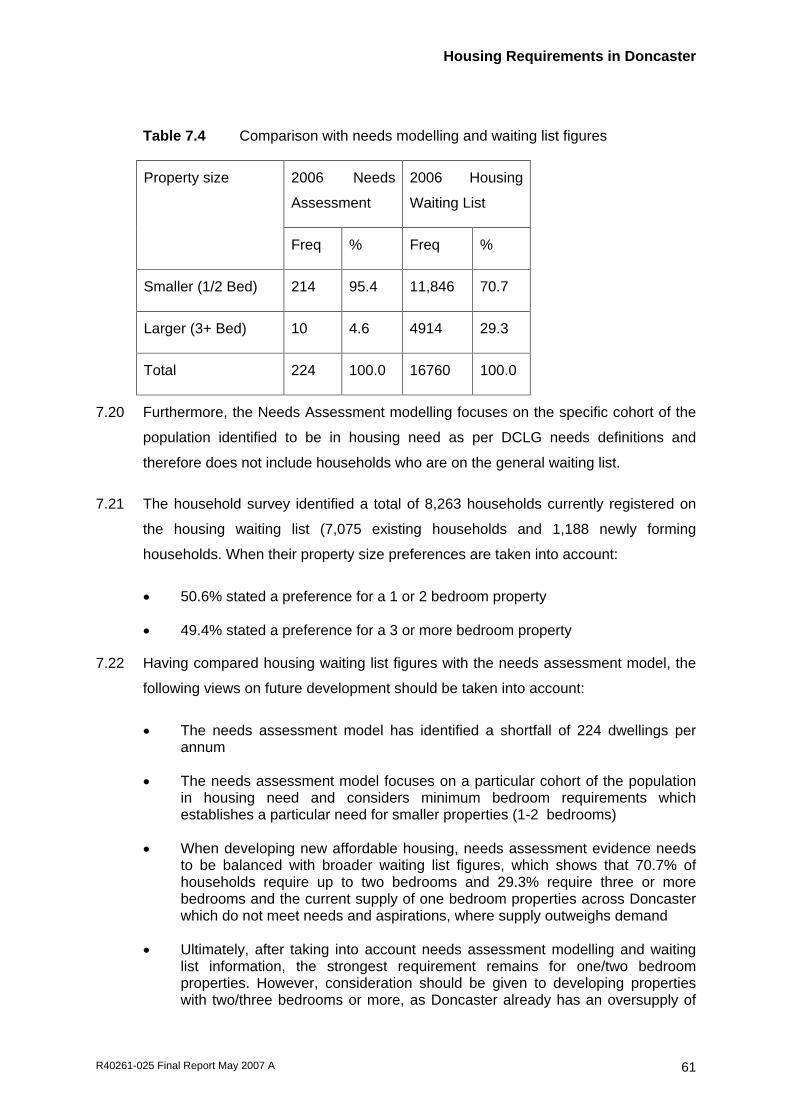

5.0 DEFINING LOCAL NEIGHBOURHOODS ................................................................ 29

Introduction ................................................................................................................ 29 Rural Hinterland ......................................................................................................... 32 Rural Centre............................................................................................................... 33 Peripheral Coalfield Community................................................................................. 33 Urban Core ................................................................................................................ 34 Social Suburb............................................................................................................. 35 Inner Suburb .............................................................................................................. 36 Prosperous Suburb .................................................................................................... 37 Affluent Suburb .......................................................................................................... 38 Summary.................................................................................................................... 38

6.0 UNDERSTANDING FUTURE SUPPLY AND DEMAND DYNAMIC ......................... 39

Understanding Housing Supply ................................................................................. 39 Stock Condition.......................................................................................................... 40 Drivers of Change ...................................................................................................... 44 Structural.................................................................................................................... 45 Locational................................................................................................................... 47 Policy Drivers ............................................................................................................. 49 Summary.................................................................................................................... 52

7.0 HOUSING REQUIREMENTS IN DONCASTER........................................................ 54

Introduction ................................................................................................................ 54 Affordability ................................................................................................................ 55 Role of the Private Rented Sector ............................................................................. 56

R40261-025 Final Report May 2007 A 3

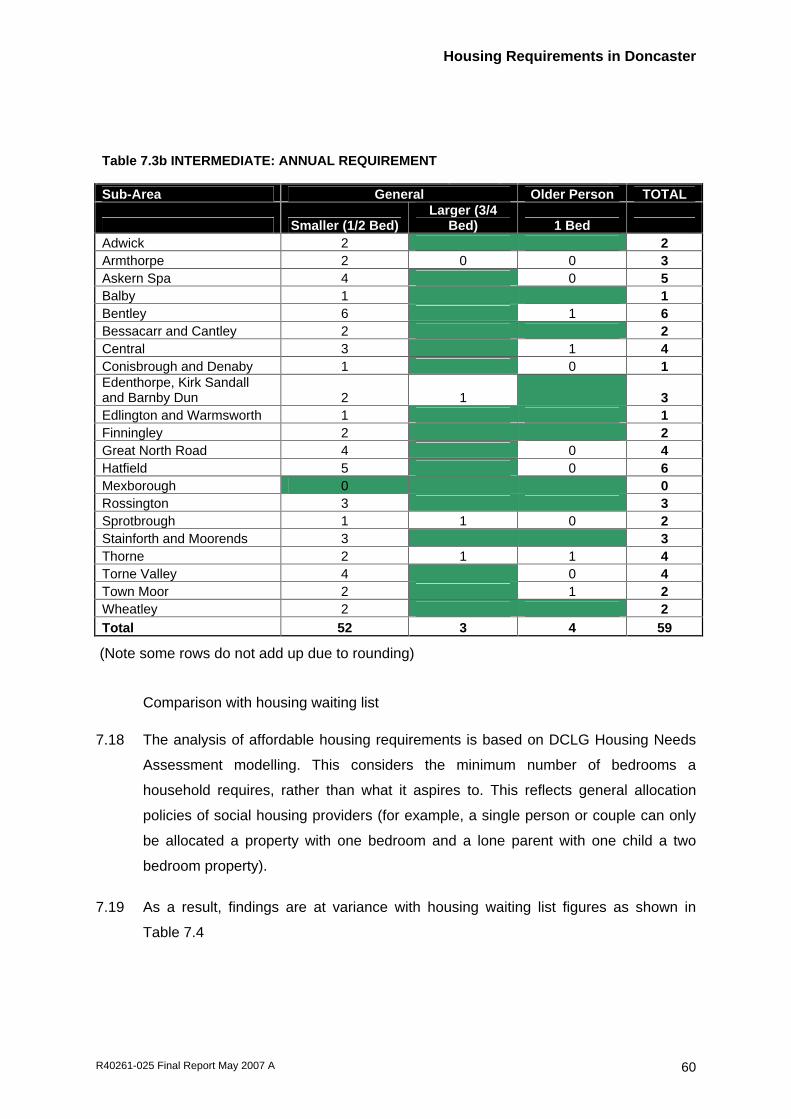

Affordable Housing Requirements ............................................................................. 56 Tenure preferences.................................................................................................... 57 Summary of affordable housing requirements ........................................................... 59 Intermediate Tenure Market, Prices and Options ...................................................... 62 Justifying the Need for Affordable Housing................................................................ 67 General market demand ............................................................................................ 68 Housing Requirements of Different Household Groups ............................................. 72 Summary.................................................................................................................... 72

8.0 CONCLUSIONS AND RECOMMENDATIONS ......................................................... 74

Influencing the mix of type and tenure of housing...................................................... 74 Affordability and Housing Need.................................................................................. 78 Approach to Housing and Neighbourhood Investment .............................................. 81 Plan, Monitor, Manage............................................................................................... 82 Typology Recommendations...................................................................................... 83

APPENDIX A......................................................................................................................... 85

Introduction

R40261-025 Final Report May 2007 A 2

1.0 INTRODUCTION

1.1 The Local Housing Assessment has been undertaken in accordance with the draft

practice guidance for Housing Market Assessments published by Communities and

Local Government (CLG), formerly the Office of the Deputy Prime Minister, in

December 2005. The guidance brings together the guidance on undertaking housing

needs assessments and the housing market assessment.

1.2 The draft practice guidance sets out a number of stages which have been followed in

this research. These are:

The Current Housing Market – an analysis of the current market, key characteristics in terms of stock, socio-economic data and the active market which is evidenced by house price trends and interviews with estate agents

The Future Housing Market – this section aims to understand what the future demand will be in Doncaster, where there are current hot and cold spots, how affordability will change and issues which will influence the future of the housing market in Doncaster

Current and Future Housing Need – understanding gained through the Housing Needs Assessment, a comprehensive household survey in Doncaster

Housing Requirements of Different Household Groups – understanding the housing needs of specific groups, gathered through the housing needs assessment

1.3 The findings of all of these stages are then brought together and inform the

conclusions and recommendations which will influence further policy development.

1.4 One of the main aims of the research is to inform Doncaster’s Local Development

Framework development in particular the Housing Development Plan Document in

terms of the type, size and supply of future housing in Doncaster, where to target

future housing resources and inform future bidding documents for external funding.

1.5 This report is set out under a number of sections:

Policy and Strategy Context – this section reviews the current policy and strategy drivers which set the context for the Housing Market Renewal and Housing Needs Study

Doncaster Context - this section identifies Doncaster’s key characteristics in terms of population housing tenure, stock and socio-economic characteristics

Introduction

R40261-025 Final Report May 2007 A 3

Identifying the Current Housing Market – in this section the key findings from the analysis of migration and travel to work data are set out to help to identify the current housing market

Defining Local Neighbourhoods – this section sets out the characteristics of the housing market typologies which have been identified in Doncaster

Housing Supply – this section considers the past and current housing supply and issues around stock condition

Understanding Supply and Demand Dynamic – provides an understanding of the future supply and demand dynamic in Doncaster and identifies issues which will need further consideration when developing the Housing Development Plan Document and other important housing related strategies

Housing Market Requirements – provides evidence around the housing needs in Doncaster, affordability requirements and discussion around the general market demand in Doncaster

Issues for Consideration – this section sets out the key conclusions, recommendations and the issues which will need to be addressed through the development of appropriate policies

Policy and Strategy Context

R40261-025 Final Report May 2007 A 2

2.0 POLICY AND STRATEGY CONTEXT

Introduction

2.1 In order for Doncaster’s aspirations to be met it has been critical that sub-regional,

regional and local policies have been developed in alignment. The result is a clear

hierarchy of strategies and policies across Doncaster, from a sub-regional, regional

and local level, led by ‘Advancing Together’ which sets out the vision and strategic

framework for Yorkshire and Humber.

Economy

2.2 Doncaster is a key element of the Sheffield City Region. A number of City Region’s in

the north were identified through The Northern Way which was published in

September 2004. The document set out the desire and ambition for the North to

accelerate economic growth and narrow the gap between the north and south. The

vision set out in the Northern Way is:

‘Together we will establish the North of England as an area of exceptional opportunity, combining a world class economy with a superb quality of life’

2.3 Doncaster has strong local drivers of economic growth and it is also a key element of

the Sheffield City Region. The aim of the Sheffield City Region, which Doncaster is

within, is to become part of the ‘urban core’ of the Northern Way along with the Leeds

and Manchester City Regions.

2.4 Doncaster is highlighted as a key influence alongside Sheffield, Chesterfield,

Rotherham and Barnsley and particularly as an important logistics interchange which

has the capability of serving and supporting the north and east of England. Within the

CRDP, Doncaster is highlighted due to its road and rail network and the continuing

success and opportunities provided through the Robin Hood Airport.

2.5 The Regional Economic Strategy ‘Ten Year Strategy for Yorkshire and Humber 2003-

2012’ also sets the economic change agenda in Yorkshire and Humber. GDP1 in the

region is currently lower than the European average, although a slight improvement in

recent years has resulted in a slight narrowing of the gap in performance and showing

promising trends for the future.

Policy and Strategy Context

R40261-025 Final Report May 2007 A 3

2.6 Doncaster is identified as an important driver of economic growth due to its strategic

location and role as a transport hub, particularly identifying Robin Hood Airport and

key road/rail links.

2.7 The Northern Way and the Economic Strategy both highlight the need to attract

people to move to the area to meet the jobs created by the economic growth to drive

the economic change which is predicted. This will only be achieved through the

provision of the right housing, in neighbourhoods which have excellent access to

good quality education, community facilities and a choice of cultural and leisure

activities. The quality of the offer in Doncaster will be critical in its success in

achieving economic change and renaissance.

Housing Mix

2.8 Regional, sub-regional and local strategies identify that in order to achieve economic

success it is critical that the right housing is on offer to meet needs and aspirations.

2.9 The overall market signals in the region signify a buoyant housing market, but it is

identified that there is a growing imbalance between housing sub-markets. A number

of strategic initiatives have identified areas of particular housing markets. The

establishment of Transform South Yorkshire, one of the nine Government Housing

Market Renewal Pathfinders, confirmed the level of problems in this part of the

Region. As has the Green Corridor Initiative, a partnership between a number of

Local Authorities which has been established to address particular issues within

former coalfield communities.

2.10 Three themes for housing are established at the Regional Level:

Creating Better Places – responding to the diversity of markets and improving neighbourhood infrastructure and facilities

Delivering Better Homes, Choice and Opportunity – allowing people to meet their housing aspirations and improve housing condition and services

Ensuring Fair Access to Quality Housing – ensuring requirements and preferences of the community are met by sensitive and appropriate housing solutions and obstacles for specific groups to access housing choices are removed

1 Gross Domestic Product –a measure of economic success

Policy and Strategy Context

R40261-025 Final Report May 2007 A 4

2.11 The sub-regional and local strategies adopt these broad principles. Doncaster’s

Housing Strategy (2006-2009) also identifies another key local priority; ‘creating a

new impression for Doncaster’.

2.12 For Doncaster, a number of areas are identified which will be the focus for

intervention to deliver a balanced housing market. These include:

Transform South Yorkshire (the Housing Market Renewal Pathfinder) – Doncaster Dearne Valley

Green Corridor

Kingsway Estate

Six Streets – Hyde Park

Willow Estate – Thorne

Waterfront – Town Centre

Thompson and Dixon - Edlington

2.13 These areas set out above are aligned with the six areas identified within the Core

Strategy of the Local Development Framework (LDF), as principal settlements for

growth, outside of the urban core. These are:

Mexborough

Thorne

Adwick-le-Street/Woodlands

Armthorpe

Askern

Conisbrough

2.14 Housing renewal and change will help to create a more balanced housing market

providing a better mix, quality and choice of housing.

2.15 The Core Strategy for the draft LDF reflects the need to provide a mix of housing

types and tenures to meet the needs of local communities. This is one of its key roles

which PPS 3 identifies, particularly in relation to achieving a housing mix over the

plan period. Provision is also made so that new housing development of over sixty

units will need to demonstrate how they will support achieving mixed communities.

Policy and Strategy Context

R40261-025 Final Report May 2007 A 5

Housing Numbers

2.16 In order to support economic renaissance and housing market restructuring in

Yorkshire and Humber, the Regional Spatial Strategy (RSS) sets out the spatial

framework from 2005 to 2021. The approach for South Yorkshire is one of economic,

environmental and social transformation with emphasis placed on its main urban

centres.

2.17 In relation to housing, the RSS sets out a number of aims:

To take account of expected levels of economic growth, increased levels of migration, decreased household sizes and increased life expectancy

Provide sufficient homes to house the additional households expected to form with over 15,000 new houses provided a year up to 2011, rising to over 16,000 a year from 2011 and over 19,000 a year from 2016 to 2021

Ensure new housing is managed in a way that supports the restructuring of housing markets in areas where there is low demand and increasing the amount of affordable housing across the region, particularly in areas of high need

Create a better mix of housing across the region to reflect people’s different needs and make additional provision to meet the housing needs of gypsies and travellers

2.18 The RSS acknowledges Doncaster’s role as a rapidly developing logistics centre of

regional and national importance because of its strong national rail and motorway

network. Robin Hood Airport is a critical factor in the opportunity for economic

development and regeneration in Doncaster.

2.19 Three implementation phases for housing are set out within the RSS. This means:

2004-2011 – the focus is on making use of existing allocations and potential which have already been identified. This will also be the phase for improving low demand neighbourhoods and increasing the provision of the number of affordable homes

2011-2016 – this phase will be about using the opportunity to remodel and re-engineer existing urban areas and housing estates. It will also aim to change the roles of former industrial and commercial areas, realising the concept of ‘mixed use’

2016-2021 – will further exploit the potential of second phase urban remodelling and potential extension for new or expanded settlements. This will also be the phase which will deliver a better mix of housing types and a balanced housing stock to meet modern needs

Policy and Strategy Context

R40261-025 Final Report May 2007 A 6

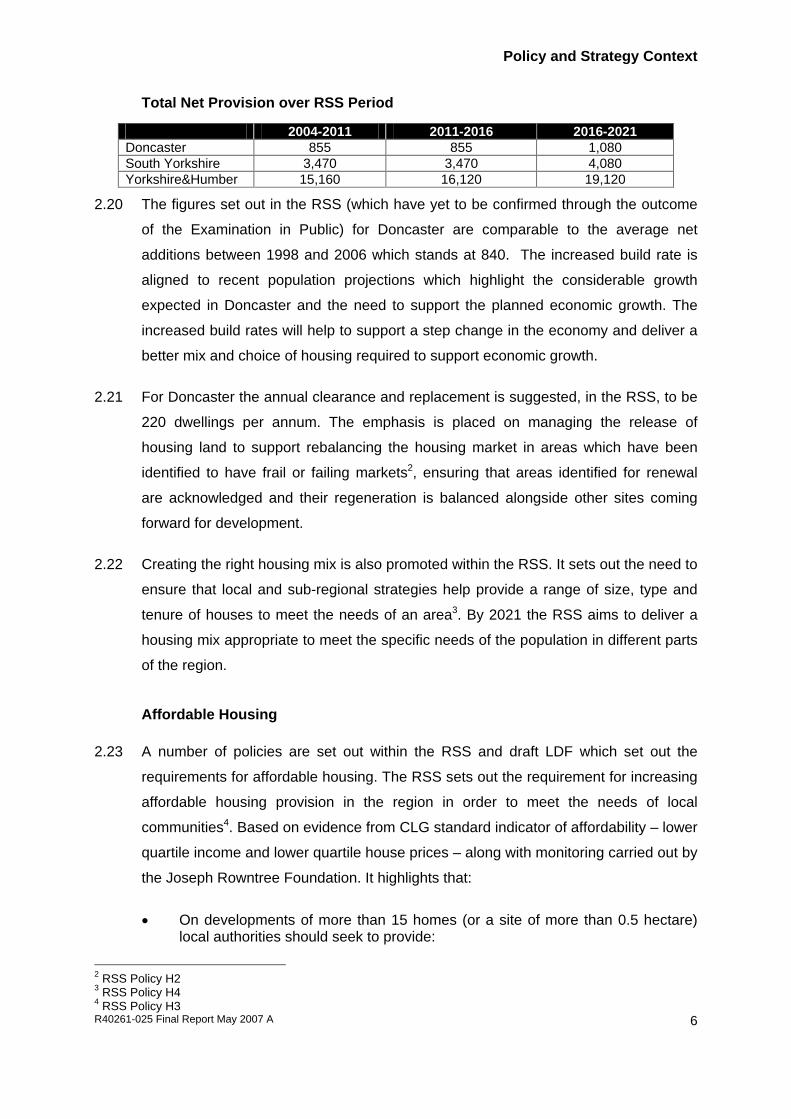

Total Net Provision over RSS Period

2004-2011 2011-2016 2016-2021

Doncaster 855 855 1,080 South Yorkshire 3,470 3,470 4,080 Yorkshire&Humber 15,160 16,120 19,120

2.20 The figures set out in the RSS (which have yet to be confirmed through the outcome

of the Examination in Public) for Doncaster are comparable to the average net

additions between 1998 and 2006 which stands at 840. The increased build rate is

aligned to recent population projections which highlight the considerable growth

expected in Doncaster and the need to support the planned economic growth. The

increased build rates will help to support a step change in the economy and deliver a

better mix and choice of housing required to support economic growth.

2.21 For Doncaster the annual clearance and replacement is suggested, in the RSS, to be

220 dwellings per annum. The emphasis is placed on managing the release of

housing land to support rebalancing the housing market in areas which have been

identified to have frail or failing markets2, ensuring that areas identified for renewal

are acknowledged and their regeneration is balanced alongside other sites coming

forward for development.

2.22 Creating the right housing mix is also promoted within the RSS. It sets out the need to

ensure that local and sub-regional strategies help provide a range of size, type and

tenure of houses to meet the needs of an area3. By 2021 the RSS aims to deliver a

housing mix appropriate to meet the specific needs of the population in different parts

of the region.

Affordable Housing

2.23 A number of policies are set out within the RSS and draft LDF which set out the

requirements for affordable housing. The RSS sets out the requirement for increasing

affordable housing provision in the region in order to meet the needs of local

communities4. Based on evidence from CLG standard indicator of affordability – lower

quartile income and lower quartile house prices – along with monitoring carried out by

the Joseph Rowntree Foundation. It highlights that:

On developments of more than 15 homes (or a site of more than 0.5 hectare) local authorities should seek to provide:

2 RSS Policy H2 3 RSS Policy H4 4 RSS Policy H3

Policy and Strategy Context

R40261-025 Final Report May 2007 A 7

Over 40% affordable housing in areas of high5 need

Between 30 and 39% in areas of medium need

Less than 29% in areas of low need

Where opportunities for the provision of new housing are generally limited to sites below the national threshold, in exceptional circumstances a lower threshold provision should be set for off site or off site contributions

In rural areas where opportunities are limited, Local Planning Authorities should identify exception sites in the DPD.

2.24 The RSS goes so far as setting the level of affordable housing provision at 33% as a

broad target across Yorkshire and Humber. This will be tested through the work

undertaken as part of the Housing Needs Study to assess whether this is appropriate

target for Doncaster or whether the findings from the study justify the need to develop

specific local policies.

2.25 At a local level the Draft LDF Core Strategy sets out that the net need for affordability

across the Borough is 369 units per annum (based on the 2003 Housing Needs

Study), a shortfall in all but one ward. In terms of affordable housing, the Core

Strategy sets out that any development over 15 units will be required to meet

affordable housing needs. This study will the findings of this Housing Needs Study will

inform whether the affordability requirements have changed and what level of

requirement is now needed in Doncaster to meet housing needs.

Sustainable Communities

2.26 Underlying the requirement for alignment of key strategies and policies is the need to

create long term sustainable communities, which have a good choice of housing

coupled with other factors which make neighbourhoods successful.

2.27 Improving the quality and choice of housing on offer is critical to attracting people into

Doncaster. However, it is not just the housing on offer which is important, but the

neighbourhoods and environment that they are within. The quality of services and

facilities in neighbourhoods, e.g. education, service provision and community

facilities, are key to contributing to the quality of place. Improving the quality of

services, opportunities and infrastructure all contribute to the choice people make in

moving to an area.

5 High, medium and low levels of affordable housing need are taken from the Regional Housing Strategy which identifies South Yorkshire as having a low level of need.

Policy and Strategy Context

R40261-025 Final Report May 2007 A 8

2.28 Meeting future housing needs and aspirations of a range of households will be critical

to creating long term mixed communities.

Summary

2.29 In summary, there is a clear hierarchy of strategies and policies driving change in

Yorkshire and Humber. There is significant economic restructuring required as a

result of the decline in traditional economies and as opportunities arise from the

growth of existing sectors. The economic renaissance required needs to be supported

by changes to the housing offer in particular areas to help improve the quality of life of

current residents and also to attract new people who will help drive the changing

economy.

2.30 The Draft RSS sets out the spatial framework which will underpin economic

renaissance and housing market renewal in Yorkshire and Humber. Doncaster’s

Local Development Framework is being developed which will set the spatial

framework for Doncaster. The Core Strategy which has been developed sets a

number of targets in relation to; affordable housing, developing a sustainable housing

mix and density. It also sets out the principles for future growth and urban

renaissance in Doncaster focussing on six principal urban areas, with a clearly

defined urban hierarchy where growth is expected and where potential growth will be

limited.

2.31 This study provides an understanding of housing markets and identifies issues which

should influence policy development to underpin the housing market changes

required to help support economic performance and deliver long term sustainable

communities.

Doncaster Context

R40261-025 Final Report May 2007 A 9

3.0 DONCASTER CONTEXT

Introduction

3.1 This section provides a summary of the key characteristics of Doncaster Metropolitan

Borough Council’s (DMBC) population, socio-economic factors and housing stock.

For comparative purposes, information at the regional and national level has also

been included.

Population

3.2 In 2003 Doncaster’s population was estimated to be 288,0006, an increase from

286,866 at the time of the Census 2001.

Socio-economic profile

3.3 As the graph overleaf highlights, household composition in Doncaster is broadly in

line with regional and national averages. There is however a higher proportion of

married/cohabiting households with dependent children across the Borough

(22.45%).

Household Composition

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

One

per

son:

Pen

sion

ers

One

per

son:

Oth

er

One

fam

ily a

nd n

oot

hers

: A

llpe

nsio

ners

Mar

ried/

coha

bitin

gho

useh

olds

: N

oC

hild

ren

Mar

ried/

coha

bitin

gho

useh

olds

: A

llde

pend

ent

child

ren

Mar

ried/

coha

bitin

gho

useh

olds

: A

llch

ildre

n no

n-de

pend

ant

Lone

Par

ent

hous

ehol

ds:w

ithde

pend

ent

child

ren

Lone

par

ent

hous

ehol

ds:

All

child

ren

non-

depe

nden

t

Doncaster Local Authority

Yorkshire & Humber

England & Wales

3.4 Census 2001 data on ethnic origin highlights that the main ethnic minority present in

Doncaster is Asian/British Asian, representative of 1.07% of the population. Overall

the Census identified that 2.31% of Doncaster’s population was from an ethnic

6 Office of National Statistics Sub-Regional Population Projections 2003

Doncaster Context

R40261-025 Final Report May 2007 A 10

minority background. The Housing Needs Study (HNS) suggests that this is rising and

3.8% of the population is now from an ethnic minority background.

3.5 An analysis of Doncaster’s socio-economic composition has been undertaken to help

develop a greater understanding of the social status of the area’s residents and the

types of employment they undertake.

3.6 The National Socio-Economic Classifications (NSEC) adopted by the 2001 Census

has been used to examine the socio-economic composition. One of the

characteristics of successful mixed communities is a balanced socio-economic profile.

3.7 For the purposes of this study they have been grouped together into higher,

intermediate and lower socio-economic bands as shown below.

Higher Intermediate Lower

Large employers and higher managerial occupations

Intermediate occupations

Small employers and own account workers

Higher professional occupations

Lower supervisory and technical occupations

Semi-routine occupations Lower managerial and professional occupations

Routine occupations

Socio Eocnomic Profile

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

Lower Intermediate Higher

Doncaster Local Authority

Yorkshire & Humber

England & Wales

3.8 The most noticeable element of Doncaster’s profile is the higher than average

proportion of residents who fall into the lower socio-economic category (35.72%).

Conversely the proportion of residents that fall into the high category (18.76%) is

below the average for the region (22.98%). These two factors highlight that Doncaster

Doncaster Context

R40261-025 Final Report May 2007 A 11

has an imbalanced socio-economic profile, with a considerable imbalance towards

lower socio-economic groups. This is likely to be as a result of past economic

influences towards manual labour. However, if Doncaster is going to achieve the

economic growth required the challenge will be to rebalance the economic profile and

skills of the Borough.

3.9 The table below provides a summary of the social grade composition of the

population of Doncaster according to the household representative7 .

Social Grade Doncaster Local Authority

Yorkshire and Humber England and Wales

AB8 16.9% 20.36% 23.31%

C1 & C29 51.35% 52.03% 52.25% DE10 31.71% 27.6% 24.44%

3.10 The most notable element of Doncaster’s profile is the under representation of

residents in the highest category AB (16.90%) and the over representation of

residents who fall into the lowest DE category (31.7%). The proportion of Doncaster

residents in the low social grade exceeds the national average by 7.3%.

3.11 Job Seekers Allowance Claimants (September 2006)11 shows that 3.3% of

Doncaster’s working age population are in receipt of JSA, higher than the Yorkshire

and Humber average of 2.8%. The proportion of people claiming for over twelve

months is also higher than the Yorkshire and Humber average, 17.0% compared to

14.9%. Also worthy of note is the high proportion of Doncaster residents who are

unable to work as a result of sickness or disability; this was 22% at the time of the

2001 Census. This is nearly 6% higher than the national average, suggesting there is

a high proportion of inactivity from Doncaster’s economically active population.

3.12 It will be important for Doncaster to increase the skills of existing residents to take up

new employment growth which is generated by economic growth.

7 Using the NSEC profiles taken from Census 2001 data 8 AB contains those employed within higher and intermediate managerial and professional occupations 9 C1 & C2 contain those employed within supervisory, clerical and junior managerial administration and professional occupations as well as skilled manual workers 10 DE contains those employed in semi skilled and unskilled occupations as well as the unemployed and those on state benefit. 11 NOMIS statistics

Doncaster Context

R40261-025 Final Report May 2007 A 12

Housing Type and Tenure

3.13 As the following graph highlights, the proportion of detached properties and flats in

Doncaster is broadly in line with regional and national averages. There is a distinctly

higher proportion of semi-detached properties (45%) than the national average (32%)

and a relatively small proportion of flats at just 6.41% compared to regional and

national averages.

Housing Type

0.00%5.00%

10.00%15.00%20.00%25.00%30.00%35.00%40.00%45.00%50.00%

Detached Semi-detached

Terraced Flat

Doncaster Local Authority

Yorkshire & Humber

England & Wales

3.14 The 2006 Housing Needs Study (HNS) data has enabled data to be updated for

Doncaster to show current house type profile. The graph below shows that

Doncaster’s house type profile has not changed considerably since the Census 2001.

House Type Profile 2006

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

45.0%

Detach

ed

Semi D

etac

hed

Terra

ced

Town H

ouse

Flat/M

aison

ette

Bunga

low

Carava

n

3.15 The table below compares the house type breakdown in Doncaster with adjacent

Local Authority areas. It highlights that Doncaster has a smaller proportion of

Doncaster Context

R40261-025 Final Report May 2007 A 13

detached properties compared to other areas, combined with a higher proportion of

terraced properties.

3.16 The higher proportion of detached properties in adjacent areas also has an impact on

average house prices which are considerably higher in areas such as North

Lincolnshire, Selby and East Riding.

House Type Comparison

0.00

10.00

20.00

30.00

40.00

50.00

60.00

Donca

ster

Sheffie

ld

Barns

ley

Basse

tLaw

East R

iding

North

Lincs

Rothe

rham

Selby

Englan

d & W

ales

%

Detached

SemiDetached

Terraced

Flat

3.17 As with housing type, tenure in Doncaster is similar to regional and national averages,

shown in the graph below. However there are lower levels of privately rented

properties (6.57%)12 compared to the regional average (9.10%)13. The dominant

tenure in Doncaster is owner occupation (69.58%)14.

Housing Tenure

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

70.00%

80.00%

OwnerOccupied

Households

Social RentedHouseholds

Private RentedHouseholds

Living RentFree

Doncaster Local Authority

Yorkshire & Humber

England & Wales

12 Census 2001 13 Census 2001 14 Census 2001

Doncaster Context

R40261-025 Final Report May 2007 A 14

3.18 The 2006 HNS has provided up to date information on Doncaster’s housing tenure,

shown in the table below. The table shows that the tenure balance has not

significantly changed since the Census, owner occupation remains the dominant

tenure and has increased since the Census.

2006 HNS (%) Census (%)

Owned 73.7

69.5

RSL 20.7

20.9

Private Rented 5.1

6.5

Other 0.5

3.1

3.19 The tenure profile for Doncaster is not significantly different to the adjacent local

authority areas of Wakefield and Rotherham. However its neighbours of North

Lincolnshire and North Nottingham and Selby all have a lower proportion of socially

rented properties and a higher proportion of owner occupation.

3.20 In relation to house size in Doncaster, the 2006 HNS has highlighted the dominance

of 3 bedroom properties, over half of the total stock is this size, 22% are two

bedrooms and 13.6% four bedrooms.

3.21 Council tax data helps to illustrate the range of housing across an area, where there

are concentrations of lower value, smaller properties (Band A) and where the

dominance is of high value (Band E,F,G,H).

3.22 The graph below shows there is a proportionately higher percentage of band A

properties (61.81%) in Doncaster compared to regional and national averages. This is

36%15 higher than the national average.

3.23 Conversely, there are substantially less properties in the higher tax bands E, F, G and

H at only 4.6% compared to the national average of 18.6%.

15 Census 2001 Data

Doncaster Context

R40261-025 Final Report May 2007 A 15

Council Tax

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

Band A Band B Band C Band D Band E Band F Band G Band H

Doncaster Local Authority

Yorkshire & Humber

England & Wales

3.24 With regards to the age of the properties within Doncaster, the housing stock is

dominated by post 1944 dwellings (82.8%), with only 17.2% of Doncaster’s housing

stock built prior to 194416 compared to 38.3% nationally17.

Employment Structure

3.25 Annual Business Inquiry (ABI) data has been used to analyse the current employment

structure of Doncaster. Employment is broken down into sectors as classified by the

Standard Industrial Classification structure.

3.26 The table below shows that the major growth sectors (percentage of employment

change) within Doncaster during the period 2000-2004 were construction, which grew

by 28.25%, and banking/finance/insurance, with a growth rate of 8.05%. The

construction industry in Doncaster demonstrated a rate of growth which exceeded

that displayed at the regional level, which grew by only 17.11%.

3.27 The major growth sector at the Regional level was Public

administration/Education/Health at a growth rate of 20.54%. This is nearly three times

more than for the same sector in Doncaster, which grew by only 7.11%.

16 From Housing Needs Study 2006 17 2005/2006 Survey of English Housing

Doncaster Context

R40261-025 Final Report May 2007 A 16

3.28 The manufacturing industry declined in the period 2000-2004. Doncaster was not

affected to the same extent as the Region as a whole, with a decline of 3.83% in

comparison to the Regional average which saw a rate of decline of 14.41%.

Doncaster Context

R40261-025 Final Report May 2007 A 17

Manufacturing

Banking/ Finance/

Insurance Distribution/

Hotels

Public administration/

Education/ Health Construction

Doncaster 2000 15,733 11,065 25,155 28,686 6,394

Doncaster 2004 15,131 11,956 25,675 30,726 8,200

Net Change -3.83% +8.05% +2.07% +7.11% +28.25% Yorkshire and the Humber

2000 383,832 320,676 502,233 520,709 98,706 Yorkshire and the Humber

2004 328,541 359,977 551,882 627,640 115,590

Net Change -14.41% +12.26% +9.98% +20.54% +17.11%

3.29 Employment in Doncaster is not heavily reliant upon any one sector. As the graph

below shows:

Employment Change

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

2000 2001 2002 2003 2004

Year

%

Agriculture and fishing

Energy and water

Manufacturing

Construction

Dis tribution, hotels and res taurants

Transport and com m unications

Banking, finance and insurance, etc

Public adm inis tration,education &health Other services

3.30 The data shows dominant sectors within Doncaster are public administration,

education and health, construction and transport sectors. Data also shows a lower

proportion of jobs in banking/finance and insurance, which collectively account for

11.3% of jobs within Doncaster; this is below the regional average of 16.0%.

Doncaster Context

R40261-025 Final Report May 2007 A 18

House Price Analysis

3.31 An analysis of house prices in Doncaster has been carried out using data gathered

from HM Land Registry which lists all house sales. For comparative purposes

information has also been included at the regional level. It should be noted that the

Land Registry collect data per quarter. As such, data for 2006 represents the two

quarters up to June 2006.

Average House Price Comparison

3.32 The graph below shows average house prices in Doncaster and Yorkshire & Humber

between 2000 and up to June 2006.

Average House Price Comparison

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

2000 2001 2002 2003 2004 2005 Until June2006

Year

Pri

ce Doncaster

Yorkshire & Humber

3.33 It highlights that:

Average house prices in Doncaster are below the regional average. In 2005, average prices in Doncaster were £20,659 less than in Yorkshire & Humber

House prices have increased steadily in Doncaster since 2000.

3.34 Furthermore, calculations show that Doncaster has experienced a larger percentage

increase in house prices for the period 2000 up to June 2006 (126.02%) in

comparison to Yorkshire & Humber (62.89%).

Average Prices by House Type

3.35 The table below sets out average house prices broken down by house type. It

highlights that:

Doncaster Context

R40261-025 Final Report May 2007 A 19

Average prices for all house types in Doncaster are below regional averages. The biggest difference is for Detached house prices which in 2005 was £36,866 less than the regional average,

Average prices for all house types in Doncaster have seen a larger percentage increase than the increase seen in Yorkshire and Humber

Terraced house prices have experienced the largest percentage increase at 201.22%

Year

Type 2000 2001 2002 2003 2004 2005

Until June 2006

% Change 2000-2006

Detached 87,457 93,894

117,738 152,620 183,820 200,238 203,416 132.59 Semi-Detached 43,900 46,597

56,287 75,325 100,103 110,715 115,334 162.72 Terraced 28,464 28,695

34,550 50,295 69,942 82,106 85,738 201.22 Doncaster

Flats 47,860 37,720

48,057 76,896 112,826 116,598 109,354 128.49 Detached 138,298 90,801

149,747 185,067 216,111 237,104 242,820 75.58 Semi-Detached 79,463 65,269

77,839 98,397 120,439 133,231 137,689 73.27 Terraced 62,688 47,983

56,151 69,796 87,732 100,512 106,656 70.14 Yorkshire & Humber

Flats 86,735 72,219

86,802 104,655 121,729 127,192 131,818 51.98

3.36 The table below compares Doncaster’s average house price for 2005 with other

adjacent Local Authority areas.

Detached

Semi-Detached Terraced Flat/Maisonette

Overall Doncaster 200,238

110,715

82,106

116,598

118,352

Barnsley 185,490

105,592

82,955

99,528

113,528

Bassetlaw 205,220

110,015

92,504

90,126

140,012

East Riding of Yorkshire 228,394

136,695

110,799

98,027

154,806

North Lincolnshire 180,644

103,236

84,638

66,607

124,189

Rotherham 193,698

110,866

80,006

105,828

118,848

Selby 233,624

141,724

130,710

102,898

173,068

3.37 The table highlights that Doncaster has some of the lowest house prices across all

types compared to adjacent areas. Its prices are on a par with those in Barnsley and

Rotherham. It also highlights the significant gap between prices in South Yorkshire

and neighbouring areas, particularly East Riding of Yorkshire and Selby. This may be

as a result of the quality of the environment and influence on house type resulting in

the area being more attractive to house buyers.

Detached and Semi-Detached

3.38 As the following graph overleaf shows:

Detached and semi-detached house prices in Doncaster are below the regional average

Doncaster Context

R40261-025 Final Report May 2007 A 20

Doncaster has experienced a steady increase in average detached and semi-detached house prices since 2000. Yorkshire & Humber saw a decrease in 2001, but a steady increase in the following years

There has been a larger increase in detached house prices in Doncaster than semi-detached house prices

In Doncaster, average semi-detached house prices are closer to the regional average than detached house prices

Average House Price Comparison - Detached and Semi-Detached

0

50,000

100,000

150,000

200,000

250,000

300,000

2000 2001 2002 2003 2004 2005 UntilJune2006

Year

Pri

ce

Doncaster Detached

Yorkshire & HumberDetached

Doncaster Semi-Detached

Yorkshire & Humber Semi-Detached

Doncaster Context

R40261-025 Final Report May 2007 A 21

Terraced and Flats

Average House Price Comparison - Terraced & Flats

0

20000

40000

60000

80000

100000

120000

140000

1 2 3 4 5 6

Year

Pri

ce

Type

Doncaster Terraced

Yorkshire & Humber Terraced

Doncaster Flats

Yorkshire & Humber Flats

3.39 The graph above highlights that:

In 2005, the average terraced property in Doncaster cost £82,106 and on average a flat was priced at £116,598

Average terraced house prices in Doncaster are below the regional average, but have seen a steady increase in price since 2000

Whilst there was a large difference between Doncaster and regional flat prices in 2000, a sharp increase between 2001 and 2004 saw the gap between Doncaster and regional average prices narrow.

Summary

3.40 Analysis of the key characteristics of DMBC’s population and socio-economic factors

illustrates that Doncaster has:

A younger demographic profile, that is broadly similar to regional and national averages

A high proportion of married/cohabiting households with dependent children

A higher than average proportion of residents in the lower socio-economic category, which impacts upon household composition, population and income

A high proportion of inactivity within the economically active population

Doncaster Context

R40261-025 Final Report May 2007 A 22

Dominance of public sector jobs and a lower proportion of more highly skilled employment

3.41 The analysis of the housing stock highlights that within DMBC:

The area is dominated by owner occupied semi-detached housing

There is a low proportion of privately rented properties

There is a proportionately higher percentage of council tax band A properties than regional and national averages, suggestive of a lower value housing stock

The majority of properties are post 1944 dwellings.

The peripheral areas of Doncaster have housing market characteristics similar to North Lincolnshire and North Nottinghamshire

3.42 Analysis of house prices in Doncaster has shown that:

Average house prices in Doncaster are below the regional average

Average house prices in Doncaster have increased steadily since 2000 and have increased at a higher rate than for the region as a whole

There has been a larger increase in detached house prices than semi-detached.

Semi-detached house prices are closer to the regional average than detached house prices

Since 2005 there has been a decline in average flat prices.

3.43 The challenge for Doncaster is to move towards a more highly skilled workforce is to

ensure that capacity within the existing population is maximised to ensure that they

are able to take up employment opportunities the right type of housing is provided to

attract new more highly skilled workers in Doncaster and vary the current household

composition of Doncaster.

Identifying the Current Housing Market

R40261-025 Final Report May 2007 A 23

4.0 IDENTIFYING THE CURRENT HOUSING MARKET

4.1 This section summarises the analysis undertaken to understand the current

Doncaster housing market. The analysis has been based on Census 2001 data,

migration and travel to work (TTW) data. The analysis of this data has helped to

define the spatial extent of Doncaster’s housing market in relation to its wider context.

4.2 Analysis has been carried at a number of levels; Doncaster wide and then further

analysis at a smaller geographical level (usually Census Output Areas), which cover

around 125 households, to help define housing market typologies and sub-markets

which exist within the main housing market.

Travel to Work Data

4.3 The travel-to-work data analysis for Doncaster highlights that the majority of flows

take place within the Local Authority Area. 24.7% of the working population who live

in Doncaster, travel out of the Doncaster area to work. This is quite a low proportion

compared to Wakefield, Rotherham and Barnsley where more than 30% (38.9% in

Rotherham) travel out of their Local Authority areas to work18.

4.4 There are some specific areas which can be identified which have relationships with

the adjacent Local Authorities of Sheffield, Barnsley and Rotherham. These areas

include:

Bessacarr

Mexborough

Rossington

4.5 The majority of Bessacarr’s population travels out of the Local Authority to work and a

large number travel to adjacent Local Authorities. The reasons behind these trends

will be explored further in this paper, but it is envisaged that the location, housing

stock, neighbourhood characteristics and transport links have influenced the trends

identified in these particular neighbourhoods.

18 Census 2001 Data

Identifying the Current Housing Market

R40261-025 Final Report May 2007 A 24

19

19 The plan illustrates 2001 Census Data annotated with 2006 ward boundaries

Identifying the Current Housing Market

R40261-025 Final Report May 2007 A 25

4.6 The main urban core is the focus of a large proportion of travel to work in-flows, from

both short and long distances. This is likely to be as a result of its role as the main

employment centre.

4.7 The plan also highlights that there a number of smaller, but nonetheless important,

employment destinations which include:

Doncaster Carr – key retail employment cluster

Prisons located within Doncaster Local Authority

Warehousing around Thorne

Larger centres of Mexborough and Conisbrough

Migration Patterns

4.8 Migration patterns are based on Census 2001 data and show the movement of

households in Doncaster a year before the Census. The migration patterns highlight a

relatively contained housing market, with some limited connections to adjacent

authorities, similar to the connections highlighted by the travel to work patterns.

Overall, the dominant pattern (highlighted by the plan below) is out-migration from

central areas to the urban periphery and more rural areas.

Identifying the Current Housing Market

R40261-025 Final Report May 2007 A 26

20

20 The plan illustrates 2001 Census Data annotated with 2006 ward boundaries

Identifying the Current Housing Market

R40261-025 Final Report May 2007 A 27

4.9 The migration analysis highlights: Mexborough, Conisbrough, the town centre area

and the north eastern areas of Stainforth and Thorne (A18 corridor) as areas where

there is a higher turnover of population and a lower containment rate21 compared to

the rest of Doncaster. These characteristics suggest that these areas are distinct

housing sub-markets within the Doncaster housing market.

4.10 The analysis has also highlighted that on the whole the distances people who have

moved house are relatively small, suggesting a local self-contained market with

smaller markets operating within the wider Doncaster market.

4.11 This is confirmed by the HNS which identified that the majority of people who have

moved in the last 5 years have moved within Doncaster. Some of the more rural

housing areas have seen a higher proportion of people moving in, these include

Torne Valley, Sprotbrough and Askern Spa. This is likely to be linked to the quality of

life factors of these areas which make them attractive which include; more rural

environment, mix of house types and less dense structure.

Future Migration Patterns

4.12 Information on future house movement patterns gathered through the HNS highlight

that the majority of people (84%) looking to move in the next 5 years want to move

within Doncaster, with only 15% looking to move out. This is suggests that the self

contained nature of Doncaster’s housing market is likely to continue in the future.

4.13 Particular areas were highlighted through the survey where a higher proportion of

people were looking to move, suggesting issues with the housing and the

neighbourhood. These are; Balby (Woodfield Plantation), Bentley and Wheatley. The

survey identified a mix of households looking to leave these areas, but the main

reasons identified for moving was moving to a bigger property/better in some way or

moving to a better neighbourhood/more pleasant area

4.14 Of those people thinking about moving, 50% of those are owner occupiers and 31.9%

rent from St Leger.

4.15 In terms of the preferred location of where people want to move to, a number of areas

were identified as preferred locations. These are:

21 The containment rate is the number of people who have moved house but remained within the local area.

Identifying the Current Housing Market

R40261-025 Final Report May 2007 A 28

Armthorpe

Edenthorpe

Balby (Woodfield Plantation)

Bawtry

Tickhill

Bessacarr/Cantley

Sprotbrough

4.16 This suggests that the characteristics of these areas are influencing their popularity

for households in Doncaster.

Migration and Travel-to-Work Summary

4.17 The analysis of travel to work and migration trends suggest that overall Doncaster’s

housing market has a number of key characteristics which include:

A relatively self contained housing market; with little impact from surrounding Local Authority areas, which is likely to continue into the future

Strongest relationship to adjacent areas is in the southern part of Doncaster and its links with Rotherham

Relatively low turnover of population

Short migration distances, suggesting that small/local housing market areas are in operation

Urban to rural drift, where a number of households are moving from urban areas into more rural areas

Dominance of urban core for employment activity

Influence of key transport routes/hubs where secondary employment destinations concentrated

Areas where people particularly want to move from are Balby (Woodfield Plantation), Wheatley and Bentley

Defining Local Neighbourhoods

R40261-025 Final Report May 2007 A 29

5.0 DEFINING LOCAL NEIGHBOURHOODS

Introduction

5.1 Housing markets are inherently linked to economic activity and demographics. In

order to understand the dynamics of Doncaster’s housing market and the emerging

sub-markets/housing market typologies, further analysis has been carried out to

identify key characteristics and issues within the Doncaster market.

5.2 The analysis has included the following variables with data taken from the Census

2001 and the findings of the Housing Needs Study:

Council Tax bands

Tenure

Type

Household Composition

Age Composition

Socio-economic classification

House Prices

5.3 A detailed analysis for each typology is set out under the following headings. A

number of typologies have been identified for Doncaster, these are:

Rural Hinterland – rural communities which are located furthest from the urban core and have borders with adjacent Local Authorities.

Rural Centre – semi-rural communities which have characteristics which mean they function more of a centre to peripheral areas

Peripheral Coalfield Community – former Coalfield communities which can be defined by certain characteristics

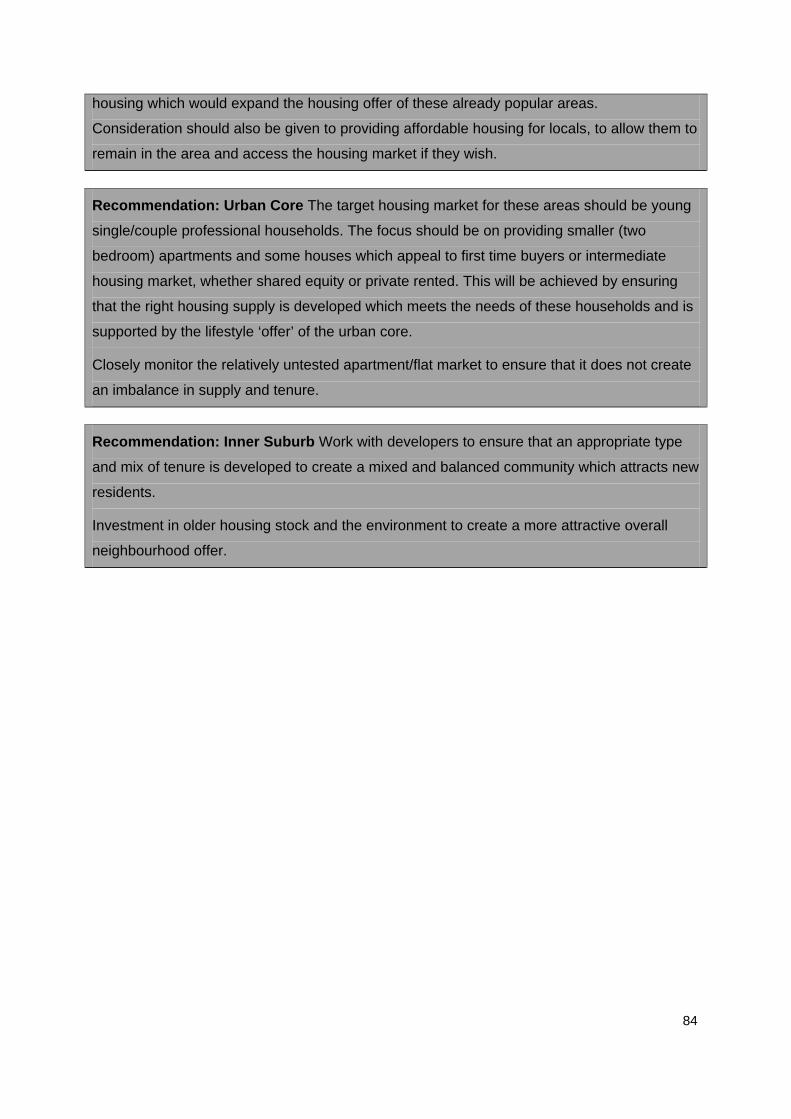

Urban Core – central Doncaster area

Social Suburb – areas characterised by the dominance of social housing

Inner Suburb – areas close to the urban core but with certain characteristics setting it apart from the central urban area

Prosperous Suburb – areas which have recently grown in popularity and show characteristics of housing market demand

Defining Local Neighbourhoods

R40261-025 Final Report May 2007 A 30

Affluent Suburb – area with long standing popularity and housing market demand

Defining Local Neighbourhoods

R40261-025 Final Report May 2007 A 31

Defining Local Neighbourhoods

R40261-025 Final Report May 2007 A 32

Rural Hinterland

5.4 This category refers to the areas including Hatfield, Clayton, Norton,

Wadworth, Finningley and Bawtry located close to the DMBC outer Local

Authority border. This typology is characterised by a higher than average

proportion of detached properties (47.69%22) of which a significant proportion

fall into the higher council tax bands signifying a high quality of housing stock

of higher value. This area is also characterised by a high proportion of larger

properties, particularly 4 bedroom properties.

5.5 The Rural Hinterland typology has larger proportions of higher (24.80%) and

intermediate (17.45%) socio-economic category residents in comparison to

the Doncaster average. The age profile highlights a higher proportion of 45–

64 year olds (28.01%), which is 3.61% higher than the Doncaster average

(24.40%).

5.6 This typology has the highest proportion of married/cohabiting households

with no children (24.08%) within Doncaster. Suggesting a more stable

housing market area, where families are older and children are no longer

dependants and linked to the large proportion of residents who have lived in

this area for a long period of time23.

Wadworth’s household composition profile highlights a higher than average proportion of married/cohabiting households with children (26.5%) in comparison to the average for Doncaster (35.72%).

Within Bawtry a substantial proportion of properties fall into tax band D (17.58%) which is nearly 12% higher than the average for Doncaster (6.17%). This, along with the large proportion of detached housing in this settlement (40.43%) is suggestive of a higher quality of housing stock. There is also an older demographic profile within Bawtry with higher proportions of 45-64 year olds (27.13%) and 65+ year olds (19.27%).

5.7 House prices in this area reflect stability and areas of demand. Prices are

higher than the Doncaster average and some of the highest within the

Doncaster Local Authority area. The rural hinterland creates a band of high

house prices around the periphery of Doncaster with average detached house

price in 2005 upwards of £180,000.

22 Percentages in this section are taken from Census 2001 figures based on Census Output Areas 23 Data gathered from the Housing Needs Survey 2006

Defining Local Neighbourhoods

R40261-025 Final Report May 2007 A 33

Rural Centre

5.8 This category describes the rural neighbourhoods of Doncaster which function

as a centre to more rural areas. It includes; Thorne, Fishlake and Moorends.

These areas have a similar house type profile to Doncaster.

5.9 Its household composition profile is broadly in line with Doncaster averages

with a slightly higher proportion of lone parent households with dependent

children (7.94%) and a lower proportion of one person: other households

(10.91%)

Thorne is similar to the averages for the Borough as a whole. A large proportion of the neighbourhood’s population fall into the lower socio-economic category (40.40%). The area is dominated by owner occupied terraced properties that fall within the lower tax bands A and B

5.10 The characteristics of this typology suggest a relatively successful mixed

housing market area with high levels of owner occupation. However, there is

an opportunity to diversify the mix of housing to provide a better range of

housing. The lifestyle within these areas is predominantly dominated by the

private car due to the more remote nature of the area and the good links to

major road networks.

Peripheral Coalfield Community

5.11 This typology covers the north east peripheral areas of Askern, Carcroft,

Adwick-le -Street and Skellow.

5.12 There is a large proportion of lower socio-economic residents (39.41%) and a

high proportion of council tax band A properties (65.45%). Household

composition is similar to averages for the Borough as a whole with a higher

proportion of lone parent households.

Askern has a more balanced house type profile with a higher proportion of detached compared to other areas and Doncaster as a whole. This is balanced with a mix of house sizes. Askern also has a more balanced household composition,

Adwick-le-Street and Carcroft display similar characteristics within this typology. There is a higher than average proportions of tax band A properties (73.9%) which is 12.11% higher than the Doncaster average. In comparison to other areas there is also a large proportion of lone parent households with dependent children (8.4%). This is nearly 2% higher than the regional average (6.4%)

Defining Local Neighbourhoods

R40261-025 Final Report May 2007 A 34

5.13 Socio-economic circumstances in these neighbourhoods are mixed, with

some areas experiencing higher levels of deprivation and disadvantage and

others like Askern Spa being more affluent. The area overall is ranked within

the most deprived neighbourhoods in the UK, in the Index of Multiple

Deprivation (IMD) which ranks neighbourhoods against a number of key

indicators to assess the level of deprivation.

5.14 Employment and housing are two of the key indicators which are particularly

highlighted as issues through the various indicators used in the IMD. The area

is also included in the Green Corridor initiative. This is a partnership between

adjacent Local Authorities acknowledging the range of issues in this area.

There is a need to consider how these areas can benefit from economic

change and projected growth expected to take place in Doncaster.

5.15 House prices vary considerably across this area, with pockets of house prices

lower than the Doncaster average and areas where prices are higher.

Urban Core

5.16 This typology is characterised by a high proportion of flats (13.46%), more

than double the Doncaster average (6.41%) and older terraces, combined

with a high proportion of tax band A properties. The area has the highest

proportion of privately rented households (12.57%) which is 6% higher than

the average for the Borough. In terms of house type, this typology is

dominated by small properties, compared to other areas.

5.17 In relation to household composition, this typology has the highest proportion

of one person: pensioner (16.90%) and one person: other (19.52%)

households in the Borough. It also has a slightly higher than average

proportion of lone parent households and a lower proportion of other families.

Some of the key characteristics of the urban core are:

In comparison to other neighbourhoods, Town Centre North has a significant proportion of properties in tax band B (20%) and a high proportion of terraced (53.9%) and privately rented properties (10.38%). The socio-economic profile of this area is broadly similar to the averages for the borough as a whole. Compared to most other neighbourhoods, there is also a larger proportion of people aged 65+ years (17.95%) in Town Centre North.

Town Centre South has a large proportion of terraced housing (45.6%). This is 20.7% higher than the borough average. There is also

Defining Local Neighbourhoods

R40261-025 Final Report May 2007 A 35

a large proportion of flats in the neighbourhood in comparison to other neighbourhoods, and at 12.77% is similar to the regional average. The housing stock, as across most of the Borough, is dominated by Council Tax Band A properties (82%). Of which a large proportion are socially rented.

5.18 Average house prices in the urban area are some of the lowest in Doncaster.

In 2005 average house prices were around £80,000. The urban core has

experienced significant house price increases between 2000 and 2005; this is

not an unusual trend and has occurred in other areas where the bottom of the

market experiences the most significant price increases. The majority of

house prices in this area remain below the Doncaster average of £116,000.

5.19 This typology has been identified where there are a number of

neighbourhoods where sustainability is considered to be fragile. Higher

proportion of older properties and private rented properties correlate with a

higher turnover of population and a less stable housing market in this area.

Neighbourhoods within the urban core are ranked among the most deprived

of Doncaster, within the top 5% most deprived in the UK.

Social Suburb

5.20 This typology is generally representative of large areas of socially rented

housing, dominated by council tax band A terraced and semi-detached

properties, on the periphery of the urban core. The age profile is on the whole

younger than other neighbourhoods with the highest proportion of 0-15 year

olds in the Borough (22.64%). Its household composition highlights a high

proportion of lone parent households: all dependent children (8.78%) in

comparison to other neighbourhoods.

Stainforth is dominated by St Leger Homes properties. The area has the highest proportion of people aged 0-15 years (25%) within Doncaster. It also has the highest proportion of lone parent households with dependent children (20%),13% higher than the Borough average. This is backed up by housing type and tenure data which highlights a higher than average proportion of socially rented semi-detached and terraced properties. This neighbourhood has the highest proportion of residents in the lower socio-economic category at 42.7%. This is 11% higher than the average for the Yorkshire and Humber region.

Rossington, has a higher proportion of 0-15 years (22.74%) than the Doncaster average (20.91%). Compared to other neighbourhoods Rossington has the largest proportion of married/cohabiting households: all dependent children at 25%. It also has a slightly higher than average proportion of lone parent households with dependent children in

Defining Local Neighbourhoods

R40261-025 Final Report May 2007 A 36

comparison to the average for the borough as a whole. The neighbourhood also exhibits a broadly similar housing tenure and type profile as the Doncaster averages, but Rossington does have a higher proportion of terraced housing at 29%. Rossington’s characteristics are a result of the dynamic housing mix in the area – poor social stock adjacent to a large amount of new house building results in contrasting housing markets within a very confined geographic area.

Mexborough, Conisbrough, Edlington & Denaby Main display similar characteristics. The majority of residents fall into the lower socio-economic category. There are also large proportions of socially rented households, with marginally more in Conisbrough & Denaby Main. The majority of properties in these neighbourhoods fall into council tax band A. Identified in the top 5% most deprived areas in the UK24.

5.21 This typology is also categorised by a high proportion of residents who have

lived in their current homes for a short time, signifying a less stable local

housing market.

5.22 The area is identified as a Housing Market Renewal Pathfinder area due to

the fall in demand for properties and housing market dysfunction. The mono-

tenure of these areas combined with poor environment and socio-economic

characteristics has contributed to market fragility and housing market

dysfunction.

Inner Suburb

5.23 This typology covers the areas including Bentley and Toll Bar. It is

characterised by owner occupation, with a large proportion of semi detached

properties in comparison to the Borough average and a large proportion of

terraced properties. The household composition is similar to that of Doncaster

as a whole.

Bentley’s household composition is broadly similar to the averages for the borough, although there is a slightly higher proportion of married/cohabiting households: all children dependent. Predominately properties in the area fall into the lower tax bands A and B, and the housing tenure and type profile highlights a large proportion of owner occupied terraced housing.

5.24 Overall the HNS identified that these areas have a high proportion of people

who have no qualifications and links to a high proportion of unemployed

people in Bentley.

24 Index of Multiple Deprivation 2004

Defining Local Neighbourhoods

R40261-025 Final Report May 2007 A 37

5.25 House prices within this typology are as low as £60,000, with the majority

lower than the Doncaster average. The lower average prices around Bentley

have shown a considerable percentage change between 2000 and 2005,

likely to be as a result of the volume of new building and the increase

popularity of housing in this area.

5.26 Past new house building has also increased demand in these

neighbourhoods, as a result of improving the choice and quality of housing

available.

Prosperous Suburb

5.27 These are predominantly in East Doncaster, with the exception of Balby to the

West and are characterised by higher tax band properties and owner

occupied detached properties and higher proportions of new housing built in

the last six years. Large proportions of higher socio-economic category

residents live in this area (23.23%) in comparison to the rest of Doncaster.

They also have a larger older population (26.54%) compared to the regional

average (23.93%).

Hatfield’s socio-economic profile shows that it has one of the highest proportions of higher socio-economic category residents (23%) within Doncaster. A large proportion of properties fall into the higher tax bands, and the housing stock is dominated by owner occupied semi-detached housing suggesting the neighbourhood has high value, larger properties and is an affluent part of Doncaster. There is also a large proportion of people aged 45-64 years (29.05%), and the proportion of married/cohabiting households with no children in Hatfield (23.7%) exceeds the regional average by nearly 6%. In comparison to the rest of Doncaster, Hatfield has one of the lowest proportions of one person: pensioner households (12.13%).

Edenthorpe and Armthorpe also have a high proportion of larger, detached properties and a high proportion of owner occupied properties.

5.28 One of the other characteristics of this typology is the number of new houses

built in the area, this is likely to have influenced the increased

popularity/housing demand in these areas.

5.29 All of the suburbs within this typology have a more balanced stock and tenure

profile and exhibit signs of housing market stability and demand. Confirmed

through average house prices, which in 2005 were up to £220,000 in some

Defining Local Neighbourhoods

R40261-025 Final Report May 2007 A 38

parts of the prosperous suburban areas, significantly higher than the

Doncaster average.

5.30 However, some of these statistics may mask the more deprived parts of this

area which are within the New Deal for Communities government initiative

which was identified for areas of significant disadvantage.

Affluent Suburb

5.31 This typology applies only to two areas to the East and West of the urban

core namely; Bessacarr and Sprotbrough. These areas are characterised by a

high proportion of larger, owner occupied detached housing, with a

substantial proportion of the properties in this area falling into the higher tax

bands.

Bessacarr and Sprotbrough have a balanced mix of type and size of housing, with the dominant tenure being owner occupation. Bessacarr has a smaller proportion of low tax band properties than other parts of Doncaster, and a distinctly higher percentage of properties in the higher council tax bands C, D and E. 11.2% of properties in Bessacarr fall into band E. The socio-economic profile for these neighbourhoods is weighted towards higher economic groups, with a significant proportion who have further educational qualifications.

5.32 Demand for housing in this area is buoyant and characterised by high house

prices. Neighbourhood factors and reputation are important and contribute to

the characteristics of this typology. The lifestyle associated with these areas is

dominated by the car and a large proportion of the population travel longer

distances to work than other areas of Doncaster.

5.33 Data gathered through the Housing Needs Study, indicate that a large

proportion of residents within these two areas have lived there for a

considerable period of time; around 30% of residents have live there for more

than twenty years. This correlates to the stable nature of population in this

area.

Summary

5.34 It will be important that policies/initiatives address issues identified within the

typologies. This will help to address housing market dysfunction, reinforce

stable housing market areas and created mixed and balanced communities.

Understanding Future Supply and Demand Dynamic

R40261-025 Final Report May 2007 A 39

6.0 UNDERSTANDING FUTURE SUPPLY AND DEMAND DYNAMIC

Understanding Housing Supply

Introduction

6.1 This Section looks at past trends in relation to Doncaster’s housing supply, what is

projected to come forward in the future and the implications on the demand and

supply of housing arising from different economic growth scenarios.

6.2 Housing supply data has been obtained from Metropolitan Doncaster Borough

Council (DMBC) to provide an insight into the current and future supply of housing

within Doncaster. Data has also been taken from the Doncaster Unitary

Development Plan (UDP) (Adopted July 1998), the Regional Spatial Strategy

Submission Draft 2006 (RSS), DMBC’s Residential Land Availability (2006), as well

as information on past demolitions supplied by DMBC’s Planning Department.

Doncaster Housing Allocation and Past Supply

6.3 Doncaster’s long term housing supply has averaged at approximately 850 units per

annum for the last 20 years. This has reduced slightly to approximately 800 units in

the last 2 to 5 years, predominately due to a low number of completions in

2001/2002. The historic number of completions is lower than the allocation in

Doncaster’s Unitary Development Plan of 1,113 units per annum. The Regional

Planning Guidance Figure since 1998 has been 735 units per annum, which has

been slightly exceeded by the number of completions.

6.4 There is little information on the house types that have been built during this period,

however it is anticipated that the majority will have been semi detached and detached

properties, with more flatted accommodation being built or in the pipeline in the last

couple of years.

6.5 In 2002 following changes in planning policy at a national level (PPG3), a greenfield

moratorium was introduced in Doncaster, to encourage development to take place on

brownfield sites in sustainable locations. The moratorium sets out a presumption

against the granting of planning permissions for housing development on greenfield

sites, including those sites that are allocated within the UDP. The theoretical

Understanding Future Supply and Demand Dynamic

R40261-025 Final Report May 2007 A 40

capacity of these greenfield allocations is approximately 5,000 units. A review of

sites that are currently allocated in the UDP will be undertaken as part of the

preparation of the Local Development Framework. The review will be mindful of the

need to achieve brownfield land targets as set out in the draft RSS (65% of

development to be on previously developed land), regeneration priorities and ensure

that housing is brought forward in sustainable locations (i.e close to employment,

transport nodes, services etc)

Stock Condition

Doncaster Private Sector Stock Condition Survey 2003 (David Adamson and

Partners)

6.6 The most recent stock condition survey for Doncaster was carried out in 2003 by