Embed Size (px)

Citation preview

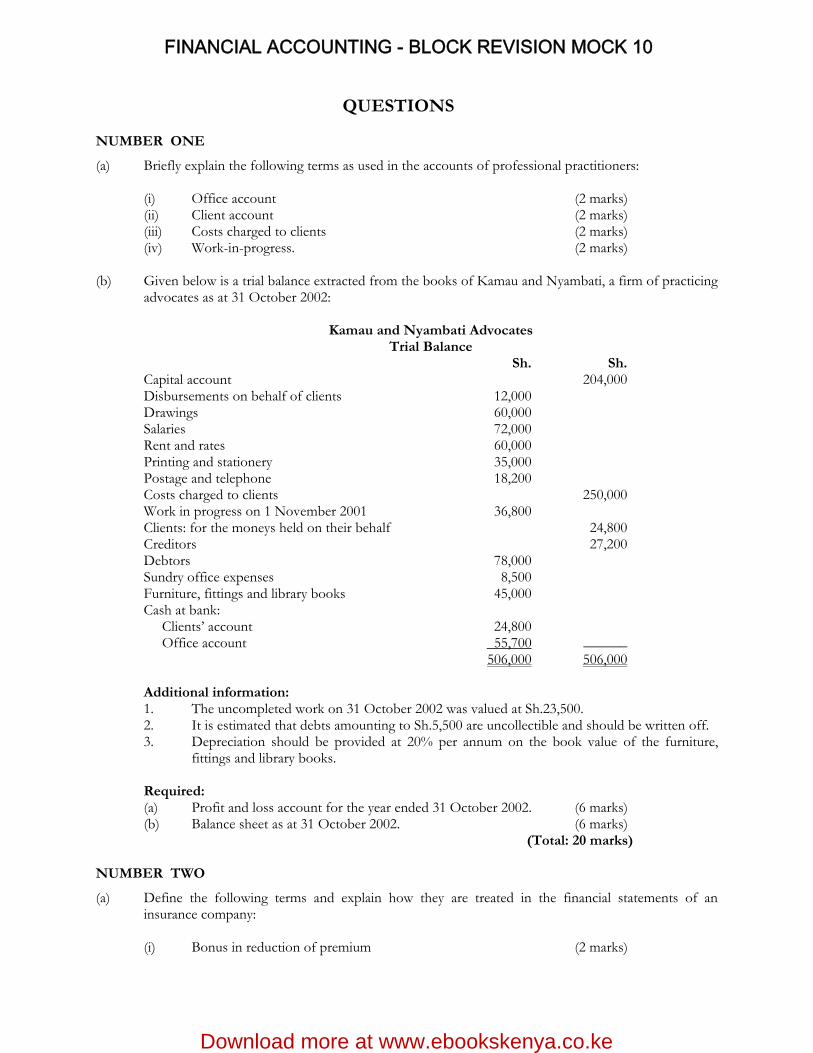

QUESTIONS NUMBER ONE

(a) Briefly explain the following terms as used in the accounts of professional practitioners:

(i) Office account (2 marks) (ii) Client account (2 marks) (iii) Costs charged to clients (2 marks) (iv) Work-in-progress. (2 marks)

(b) Given below is a trial balance extracted from the books of Kamau and Nyambati, a firm of practicing

advocates as at 31 October 2002:

Kamau and Nyambati Advocates Trial Balance

Sh. Sh. Capital account Disbursements on behalf of clients Drawings Salaries Rent and rates Printing and stationery Postage and telephone Costs charged to clients Work in progress on 1 November 2001 Clients: for the moneys held on their behalf Creditors Debtors Sundry office expenses Furniture, fittings and library books Cash at bank: Clients’ account Office account

12,000 60,000 72,000 60,000 35,000 18,200

36,800

78,000 8,500

45,000

24,800 55,700

204,000

250,000

24,800 27,200

______ 506,000 506,000

Additional information:

1. The uncompleted work on 31 October 2002 was valued at Sh.23,500. 2. It is estimated that debts amounting to Sh.5,500 are uncollectible and should be written off. 3. Depreciation should be provided at 20% per annum on the book value of the furniture,

fittings and library books.

Required: (a) Profit and loss account for the year ended 31 October 2002. (6 marks) (b) Balance sheet as at 31 October 2002. (6 marks) (Total: 20 marks)

NUMBER TWO

(a) Define the following terms and explain how they are treated in the financial statements of an insurance company:

(i) Bonus in reduction of premium (2 marks)

Download more at www.ebookskenya.co.ke

FINANCIAL ACCOUNTING - BLOCK REVISION MOCK 10

(ii) Surrender value (2 marks) (iii) Consideration for annuities granted (2 marks) (iv) Commission on reinsurance ceded. (2 marks)

(b) The Bahari Marine Insurance Company Ltd. accepts premiums from clients and settles claims as they

fall due. The company is obligated to pass over a portion of the business risk to a re-insurance company.

Direct business

Sh.’000’ Reinsurance

Sh.’000’ 1. Premiums : Received

: Receivable : Payable : Paid

- 1 December 2001 - 30 November 2002 - 1 December 2001 - 30 November 2002

4,600,000 248,000 336,000 - - -

720,000 27,000 34,000 37,500 62,000 460,000

2. Claims : Paid

: Payable : Received : Receivable

- 1 December 2001 - 30 November 2002 - 1 December 2001 - 30 November 2002

2,350,000 166,000 208,000 - - -

300,000 39,000 44,000

170,000 16,000 23,000

3. Commission : On insurance accepted : On reinsurance ceded

220,000 -

19,000 26,000

4. Other expenses and income in thousands of shillings:

Salaries – Sh.320,000; Rent and rates – Sh.29,000; Tax paid – Sh.440,000; Postage and stationery – Sh.43,000; Interest, dividends and rent receivable (net) – Sh.137,500; Withholding taxes – Sh.40,250; Legal expenses (inclusive of Sh.40,000 in connection with the settlement of claims) – Sh.72,000

5. The fund balance on 1 December 2001 was Sh.3,485,000,000.

6. The additional reserve on 1 December 2001 was Sh.445,000,000 and must be maintained at 5% of the net premium of the year. Required: Revenue account for the year ended 30 November 2002. (12 marks) NUMBER THREE

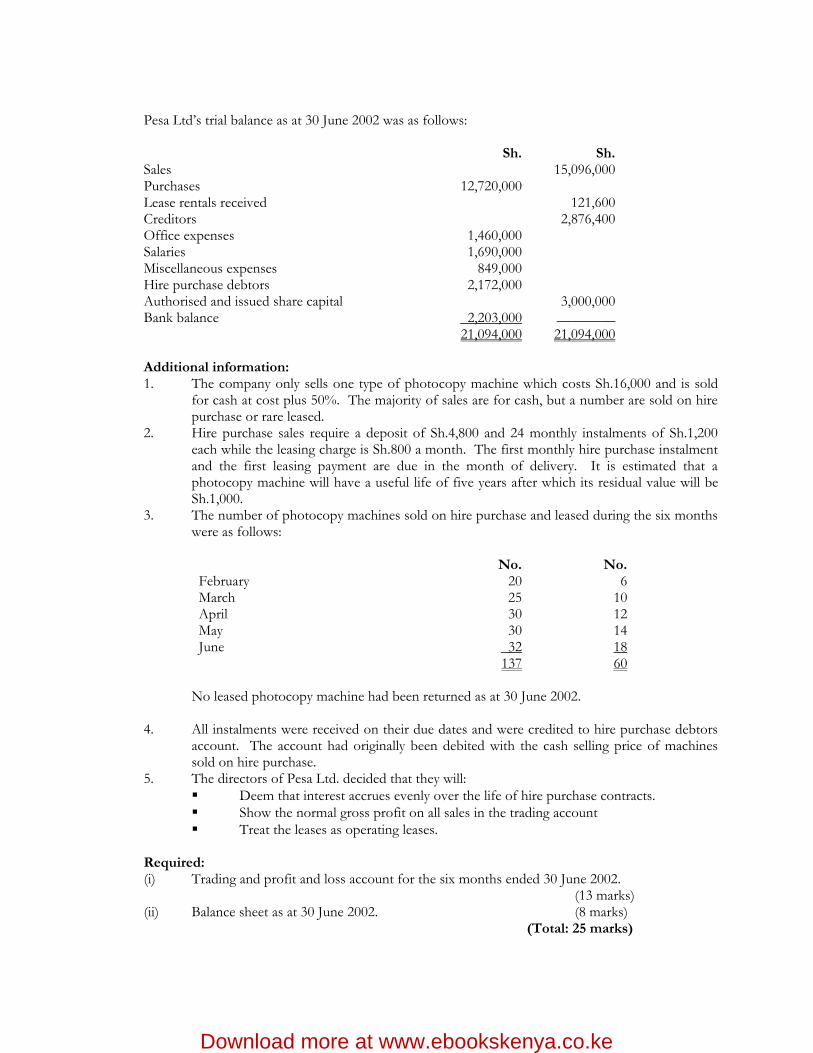

(a) Distinguish between hire purchase and lease. (4 marks) (b) Pesa Limited commenced trading on 1 January 2002, selling photocopy machines.

Download more at www.ebookskenya.co.ke

Pesa Ltd’s trial balance as at 30 June 2002 was as follows:

Sh. Sh. Sales Purchases Lease rentals received Creditors Office expenses Salaries Miscellaneous expenses Hire purchase debtors Authorised and issued share capital Bank balance

12,720,000

1,460,000 1,690,000

849,000 2,172,000

2,203,000

15,096,000

121,600 2,876,400

3,000,000 ________

21,094,000 21,094,000 Additional information:

1. The company only sells one type of photocopy machine which costs Sh.16,000 and is sold for cash at cost plus 50%. The majority of sales are for cash, but a number are sold on hire purchase or rare leased.

2. Hire purchase sales require a deposit of Sh.4,800 and 24 monthly instalments of Sh.1,200 each while the leasing charge is Sh.800 a month. The first monthly hire purchase instalment and the first leasing payment are due in the month of delivery. It is estimated that a photocopy machine will have a useful life of five years after which its residual value will be Sh.1,000.

3. The number of photocopy machines sold on hire purchase and leased during the six months were as follows:

No. No. February March April May June

20 25 30 30 32

6 10 12 14 18

137 60 No leased photocopy machine had been returned as at 30 June 2002.

4. All instalments were received on their due dates and were credited to hire purchase debtors account. The account had originally been debited with the cash selling price of machines sold on hire purchase.

5. The directors of Pesa Ltd. decided that they will:

Deem that interest accrues evenly over the life of hire purchase contracts.

Show the normal gross profit on all sales in the trading account

Treat the leases as operating leases.

Required: (i) Trading and profit and loss account for the six months ended 30 June 2002. (13 marks) (ii) Balance sheet as at 30 June 2002. (8 marks) (Total: 25 marks)

Download more at www.ebookskenya.co.ke

NUMBER FOUR

Mwalu Traders Ltd. sells most of its goods through consignees. One of the consignees is Bali Enterprises Ltd. who operates in Mombasa. Bali Enterprises Ltd. is entitled to a commission of 5% on sales. Given below are the transactions carried out between Mwalu Traders Ltd. and Bali Enterprises Ltd. for the three months ended 31 October 2002. August - A consignment of 500 bicycles each costing Sh.4,000 was sent to Bali Enterprises Ltd.

Mwalu Traders Ltd. paid packing costs Sh.80,000, freight Sh.100,000 and insurance Sh.40,000. Bali Enterprises Ltd. paid carriage-in costs of Sh.18,000 from the railway station to the trading premises. Bali Enterprises Ltd. also paid Sh.12,000 with respect to offloading the bicycles.

September - Bali Enteprises Ltd. sold 300 bicycles at Sh.6,000 each and paid carriage out-costs of Sh.30,000 In order to sell the remaining 200 bicycles, they were fitted with head lamps at a total cost of Sh.50,000, the amount being paid by Bali Enterprises Ltd. Bali Enterprises Ltd. paid storage costs of Sh.18,000 and advertisment costs of Sh.20,000.

October - Bali Enterprises Ltd. sold 160 bicycles at Sh.6,500 each. Bali Enterprises Ltd. sent account sales to Mwalu Traders Ltd. accompanied by a cheque for Sh.2,150,000 after deducting its commission and payments on behalf of the consignor, the balance remaining as a debt due to Mwalu Traders Ltd. Mwalu Traders Ltd. prepares separate trading and profit and loss accounts for consignment sales made through each consignee.

Required:

(a) In the books of Mwalu Traders Ltd: (i) Consignment out account. (5 marks) (ii) Trading and profit and loss account for the three months ended 31 October

2002. (5 marks) (b) Mwalu Traders Ltd.’s account in the books of Bali Enterprises Ltd. (5 marks) (Total: 15 marks) NUMBER FIVE

(a) Explain briefly the meaning of the terms listed below in relation to Government accounting:

(i) The Exchequer account (3 marks) (ii) The General account of Vote (3 marks) (iii) The Paymaster General (3 marks) (iv) Appropriations in Aid. (3 marks)

Download more at www.ebookskenya.co.ke

(b) The approved estimates and actual expenditure details for the Ministry of Planning and Development for the year 2001/2002 were as follows:

Sh. Sh. Personal emoluments House allowances Passage and leave Traveling and accommodation Transport and mainenance Postage and telephone expenses Miscellaneous charges Training expenses Purchase of equipment Appropriations in Aid

14,793,600 2,346,000 4,024,800

160,080 1,932,000

552,000 2,097,600

717,600 2,520,000

120,000

11,702,400 1,711,200

80,040 198,720

1,631,160 397,440

2,025,840 568,560

4,776,000 667,200

The ministry made four equal withdrawals from the exchequer in July 2001, October 2001, January

2002 and May 2002. In total, the ministry had withdrawn Sh.24,000,000 by the year end. Required:

(i) The General Account of Vote. ( 2 marks) (ii) The Exchequer Account ( 1 mark) (iii) The Paymaster General Account. ( 2 marks) (iv) Statement of assets and liabilities as at 30 June 2002. ( 3 marks)

(Total: 20 marks)

Download more at www.ebookskenya.co.ke

ANSWERS NUMBER ONE

A) (I) OFFICE ACCOUNT This is an account opened by a professional practitioner separate form those of the client to serve as bank account which would deal with operation of the office only e.g. Fee received or charged and expenses paid for the office. ii) CLIENT ACCOUNT It is separate account through which all transactions concerning the clients are recorded. No office dealings are charged in this account except where disbursement of the professionals being charged or fees being charged to client. It may contain amount of money held on the client behalf. iii) COST CHARGED TO CLIENTS These are amounts, which are owed to the professionals by their clients charged to their accounts. They are disbursements fees charged or other expenses incurred on client behalf and charged to them. They reduce the amounts of money that the professional is holding on behalf of clients. iv) WORK-IN-PROGRESS This means work that remain uncompleted at the year end e.g. a lawyer may be handling some cases at the end of the year where the judgment has not been heard. It must be accounted for in the profit and loss account. Kamau and Nyambati Advocates Profit and loss A/C

For the year ended 31.10.2002

Debts Disbursement on behalf of clients Salaries Rent and rates Printing and stationery Postage and telephone Sundry expenses Depreciation 20% x 45,000 Profit c/d Opening work in progress Profit c/d for the year

5,500 12,000 72,000 60,000 35,000 18,200 8,500

9,000

298,000 250,000 36,800 16,500 53,300

Cost charged to clients (fees) Profit b/d Closing work in progress

250,000

250,000 29,800 23,500 53,300

Download more at www.ebookskenya.co.ke

Kamau and Nyamati Advocates

Balance sheet as at 31.10.2002 Capital Profit Less drawings Current liabilities creditor

204,000 16,500

27,200 24,800

220,500 60,000

160,000

52,000

_____ 212,500

Fixed assets Furniture fittings Current assets Debtor less B. debts Cash at bank: client A/C :office work in progress

Cost 45,000

Dep. 9,000

72,500 24,800 55,700 23,500

NBV 36,000

176,500 _____

212,500

Note: all adjustments concerning the office account and client account have already been affected. NUMBER TWO

a)

i) BONUS IN REDUCTION OF PREMIUMS It is a bonus given by life insurance company in which has an effect of reducing the future premiums payable. It is not given in cash form. ii) SURRENDER VALUE Money paid back to the insured party if he decides to cancel the insurance agreement before the specified period.

iii) CONSIDERATION FOR ANNUTIES GRANTED. It is an income to the insurance company for insurance compensation paid to the insured party in form of annuities and not lump sums. iv) COMMISSION REINSURANCE CEDED

It is a commission received from another insurance company for acting as agent and generating business

on behalf of it. It is an income.

NUMBER THREE

(B)

REVENUE A/C

Download more at www.ebookskenya.co.ke

Claims wk 1 Commission: direct : reinsurance tax paid salaries rent & rates postage & stationery legal expenses fund balance c/d additional reserve c/d

uuu

2,520,000

220,000 19,000

446,000 220,000 29,000 43,000 72,000

5,721,000 246,525 9,280,000

Premium wk ii Fund balance b/f Comm on insurance ceded Interest, dividend + rent Additional fund 1.12.2001

4,930,500 3,845,000

26,000 137,500 445,000

_______ 9,280,000

WK I

Claims A/C

WK

II

Premiums A/c Receivable: direct business B/f: reinsurance Revenue A/c Bank: reinsurance Payable b/d

248,000 27,000

4,930,500 460,000 62,000

_______ 5,727,500

Payable b/f Received (bank a/c): direct Reinsurance Receivable c/d: direct bus :reinsurance

37,500

4,600,000 720,000

336,000

______ 5,720,500

Additional = 5% 4930500 Funds (30.Nov.2002) = 246,525 NUMBER FOUR

a) Under hire purchase system, the buyer agrees to pay for commodity in instalments on signing the agreement, the buyer can take possession of the commodity and use it. But the ownership of the assets rests with the seller until the final payment instalment is made. In lease agreement, the supplier of good retains the title himself, the customers merely paying a hire charge or rental for as long as he posses goods leases can be i) Operating ii) Finance

Bank: direct bus 2,350,000 Reinsurance 300,000 Receivable 16,000

Payables: c/d :direct bus 208,000 Reinsurance 44,000 ______

2,918,000

Payables b/f direct business 166,000 Reinsurance 39,000 Received: reinsurance 170,000 Revenue A/c 2,520,000 Receivable 23,000 _______

2,918,000

Download more at www.ebookskenya.co.ke

Pesa LTD Trading profit and loss Account for the year ended 30.6.2002

Opening stock Purchases Provision for Profit (wk 1) Gross profit Mis expenses Salaries Office expenses depreciation

- 12,720,000

1,137,714.2 3,798,285.8 17,656,000

849,000 1,690,000 1,460,000

38,000 4,037,000

Sales Closing stock wk ii Gross profit Lease rentals wk iv Net loss

15,096,000

2,560,000 17,656,000

3,798,285.8 121,600

124,862 4,037,000

Balance sheet

Authorized issued Share capital Net loss Current liabilities creditors

3,000,000

(117,114.2)

2,876,400

________ 5,759,285.8

Leased photocopy Machines 60 x 16,000 less depreciation week III current assets bank hire purchase debtors less provision wk I closing stock

960,000 38,000

2,203,000

2,172,000 1,137,714.2

2,560,000

922,000

4,829,538 ________

5,759,285.8 Workings 1 Hire purchase: price = 4800 + (24 x 1200) = 4800 + 28800 = 33,600 Cash price 16000 x 150 = 24,000 100 hire purchase interest = 33,600 – 24,000 = 9600 deposit instalment totals total amount rec : feb: 20 x4800=9600 1200x5=6000x20 120,000 25 x 4800=120000 1200x4=4800x25 120,000 30x4800=144000 1200x3=3600x30 108,000 30x4800=144000 1200x2=2400x30 72,000 32x4800=153600 1200x1=1200x32 38,400 657,600 458,400 provision for unrealized profits: outstanding installments x gross profit (selling price – cost of goods sold) H.P selling price Instalments: 20x1200x19=456000 25x1200x20=600000 30x1200x21=756000

Download more at www.ebookskenya.co.ke

30x1200x22=792000 32x1200x23=883200 3,487,700 HP Selling price = 137x33600= 4,603,200 Cost of goods sold = 137 x 1600 = 2,192,000 Gross profit: (H.P) 2,411,200 2,172,000 X 2,411,200 = 1,137,714.2 4,603,200 Purchases in units sale: 12,720,000 795-137=658 units 16,000 795units

closing stock: Sales 15,096,000 units = 10,492,800 Less HP 4,603,200 24,000 = 437.2 units Cash 10,492,800 =438 Unsold: 795-(137+438) = 220 - (less 60) = 160 160 units x 16,000 = 2,560,000 (WKII) depreciation = cost – salvage = 16000 – 1000 life(yrs) 5 =3000 p.a. on profits: 3,000 12 units =250 all leases items – dep. 250x6x5= 7,500 250x10x4=10,000 250x12x3= 9,000 250x14x2= 7,000 250x18x1= 4,500 wk III 38,000 Lease rental receivable 6x800x5= 24,000 10x800x4=32,000 12x800x3=28,000 14x800x2=22,400 18x800x1=14,400 wk IV =121,600 NUMBER FOUR

A (I)

Consignment

Download more at www.ebookskenya.co.ke

Goods sent on consignment Bank A/c packaging costs Freight Insurance Consignee A/C carriage in Off loading expenses Carriage out costs Head lamps costs Storage costs Advertisement costs Commission P&L(profit)

2,000,000 80,000

100,000 40,000 18,000 12,000 30,000 50,000 18,000 20,000

142,000 520,000

3,030,000

Consignee A/C – sales Consignee A/c-sales Bal. c/d wk I

1,800,000 1,040,000

190,000

3,030,000 A (ii) Trading A/c for 3 months ended 31.10.2002

Goods sent Consignment Gross profit c/d Expenses Packing Freight Insurance Carriage in Off-loading Carriage out Head lamps Storage costs Advertisement Commission Net profit

2,000,000

1,030,000 3,030,000

80,000

100,000 40,000 18,000 12,000 30,000 50,000 18,000 20,000

142,000

520,000 1,030,000

Sales Closing stock wk I Gross profit b/f

2,840,000

190,000 3,030,000

1,030,000

1,030,000 Working: 1 Closing stock = 500-300-160=40 Total costs Packing cost 80,000 total costs = (500x4000) + 250,000 = 2,250,000 Freight 100,000 I unit = 2,250,000 = 4,500 Insurance 40,000 500 Carriage in 18,000 40 x (4,500+(50,000) Off loading 12,000 200 250,000 40 x 4750 = 190,000 (b) Mwalu Traders Ltd A/c

Bank A/c Carriage in Off loading expenses

18,000 12,000

Bank A/c- sales sales

1,800,000 1,040,000

Download more at www.ebookskenya.co.ke

Carriage out Head lamps Storage costs Advertisement cost Commission Advance payment Bal c/d

30,000 50,000 18,000 20,000

142,000 2,150,000

400,000 2,840,000

2,840,000 NUMBER FIVE

A (i) EXCHEQUER ACCOUNT It records the amount authorized from the consolidated funds regarding a specific vote and amounts withdrawn from this account by the paymaster general. It is contra to the general account of vote. It is an asset A/c (ii) GENERAL ACCOUNT OF VOTE It records the amounts allocated by the treasury to the particular ministry, department or a government unit. It is similar to the capital account of a private sector. (iii) PAYMASTER GENERAL It records the withdrawals and expenditure incurred by the government unit. It also records other incomes received e.g. A.I.A (iv) APPROPRIATIONS IN AID Are particular revenues collected by a ministry or a government unit which the treasury authorizes an accounting office to use in addition to the amount appropriated from the consolidated funds. It is scheduled in the annual appropriation Act. b) G.A.V a/c

Expenditure A/c Excess A.I.A Bal. c/d

23,091,360 547,200 6,952,320 30,590,880

Exchequer A/C A.I.A

29,923,680 667,200 30,590,880

Exchequer a/c G.A.V A/C 29,932,6890

29,923,680

P.M.G Bal. c/d

2,400,000 5,923,680 29,923,680

iii) P.M.G a/c

Exchequer A/C A.I.A

24,000,000

__667,000

Expenditure A/C Bal. c/d

23,071,360

_1,575,840

Download more at www.ebookskenya.co.ke

24,667,000

24,667,200

iv) statements of assets and liabilities as at 30.6.2002

Liabilities General A/c of vote Excess A.I.A A/C

6,952,320 _547,200 7,499,520

Assets Exchequer A/C Paymaster general A/C

5,923,680 1,575,840 7,499,520

Download more at www.ebookskenya.co.ke

Download more at www.ebookskenya.co.ke