Embed Size (px)

Citation preview

Drägerwerk AG & Co. KGaACapital Markets Presentation

November, 2016

Interim financial reports as well as preliminaries are not audited.

Disclaimer

This presentation contains forward-looking statements regarding the future development of the Dräger Group. These forward-looking statements are based on the current expectations, presumptions, and forecasts of the Executive Board as well as the information available to it to date, and have been made to the best of its knowledge and belief. No guarantee or liability for the occurrence of the future developments and results specified can be assumed in respect of such forward-looking statements. Rather, the future developments and results are dependent on a number of factors; they entail risks and uncertainties beyond our control and are based on assumptions which could prove to be incorrect. Notwithstanding any legal requirements to adjust forecasts, we assume no obligation to update the forward-looking statements contained in this presentation.

This presentation does not constitute an offer of securities for sale or a solicitation of an offer to purchase any securities. No money, securities or other consideration is being solicited by this presentation.

2

Outlook

DrägerThe Company

Financials

3

DrägerThe Company

4

protectDräger products

supportsave

lives,

and

.

5

Net sales developmentStrong growth independent of the global economy

Source: International Monetary Fund, World Economic Outlook Database

Net sales developmentDräger net sales in EUR million

Global gross domestic product

2,500

2,000

1,500

1,000

500

0

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

Stock-market crash

Stock-market crash

Stock-market crash

GulfWarGulfWarGulfWar

Mexican pesocrisis

Mexican pesocrisis

Mexican pesocrisis

Russianfinancial

crisis

Russianfinancial

crisis

Russianfinancial

crisis

Stock-marketcrash

Stock-marketcrash

Stock-marketcrash

IraqWarIraqWarIraqWar

Financialcrisis

Financialcrisis

Financialcrisis

6

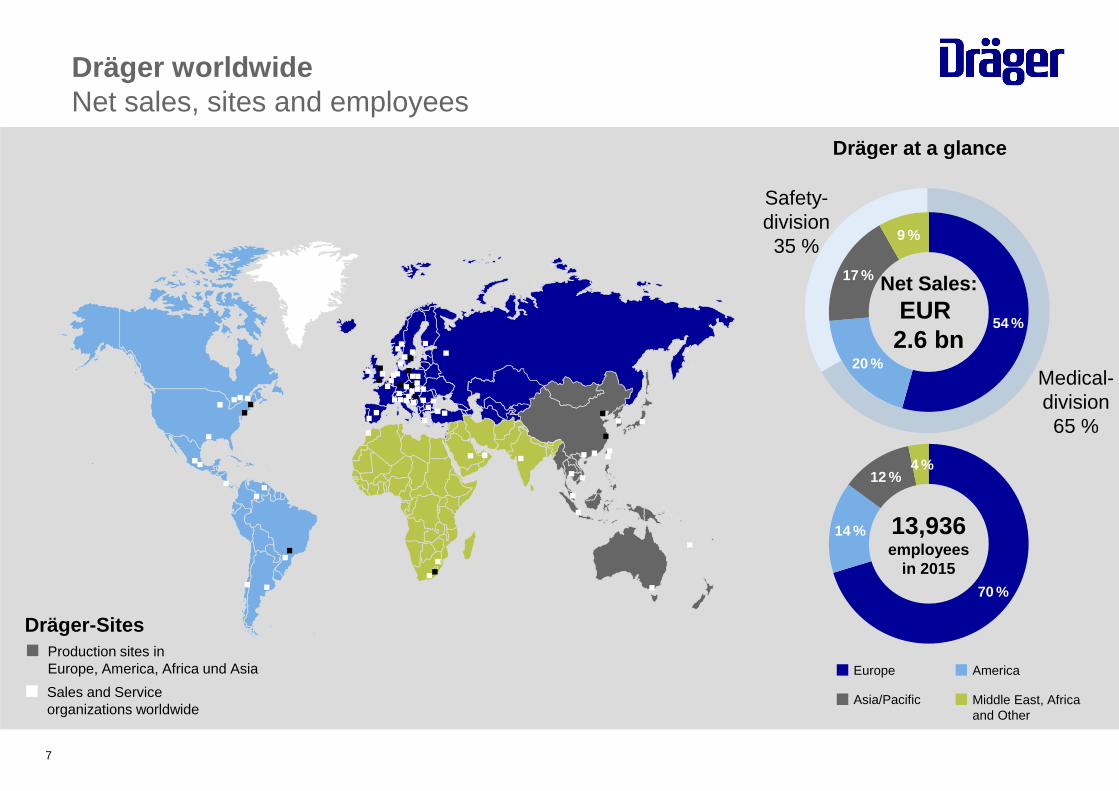

Dräger worldwideNet sales, sites and employees

54 %

20 %

17 %

9 %

70 %

14 %

12 %4 %

AmericaEurope

Middle East, Africaand Other

Asia/Pacific

Dräger at a glance

Net Sales:EUR 2.6 bn

13,936employees

in 2015

Production sites inEurope, America, Africa und Asia

Sales and Service organizations worldwide

Dräger-Sites

Safety-division35 %

Medical-division65 %

7

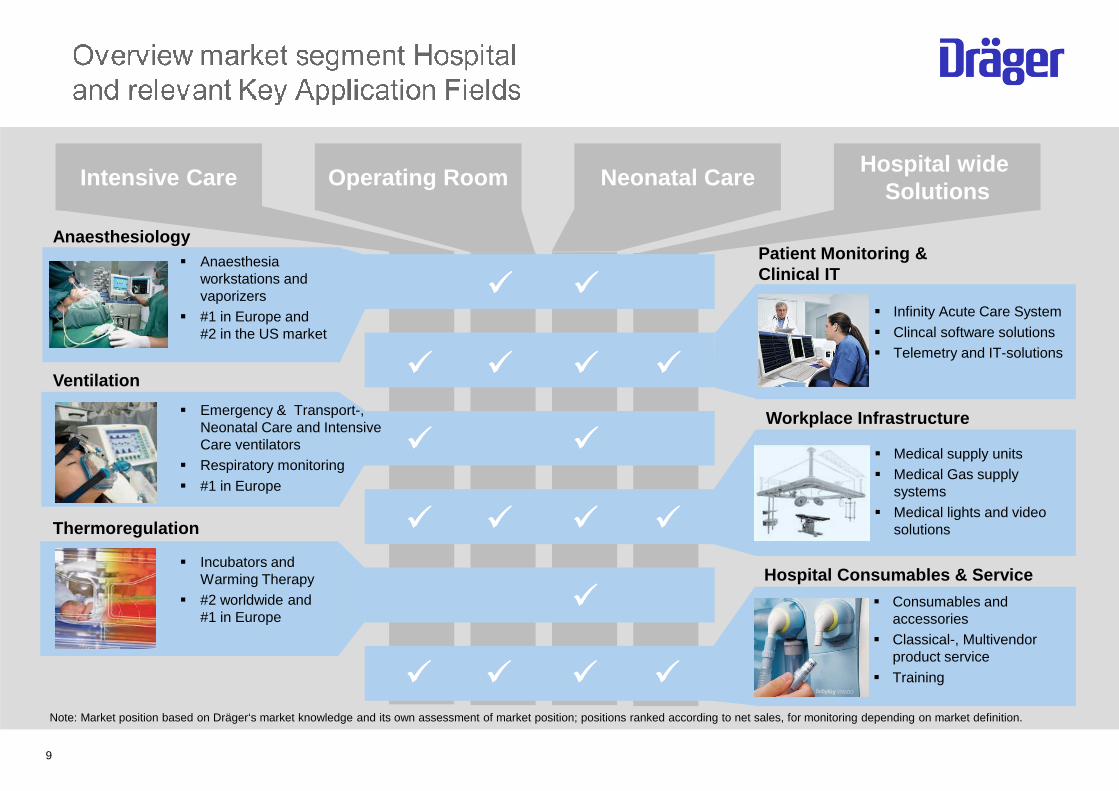

MarketsOur customers

Fire services Oil and gas industry

Mining Chemical industry

Hospital

8

Other markets

9

� Infinity Acute Care System � Clincal software solutions� Telemetry and IT-solutions

� Medical supply units� Medical Gas supply

systems � Medical lights and video

solutions

� Consumables and accessories

� Classical-, Multivendor product service

� Training

Anaesthesiology

Ventilation

Thermoregulation

Patient Monitoring & Clinical IT

Workplace Infrastructure

Hospital Consumables & Service

Intensive Care Operating Room Neonatal CareHospital wide

Solutions

�� ��

�� �� �� ��

�� ��

�� �� �� ��

��

�� �� �� ��

Note: Market position based on Dräger‘s market knowledge and its own assessment of market position; positions ranked according to net sales, for monitoring depending on market definition.

� Anaesthesia workstations and vaporizers

� #1 in Europe and #2 in the US market

� Emergency & Transport-, Neonatal Care and Intensive Care ventilators

� Respiratory monitoring� #1 in Europe

� Incubators and Warming Therapy

� #2 worldwide and #1 in Europe

10

Breathing Systems

Gas Detection Systems

Personal Protection Equipment

Impairment Check Equipment

Engineered Solutions

Service

� Fixed and mobile gas detection systems

� #1 worldwide and #1 in Europe

� Alcohol- and drugscreening devices

� Interlock devices� #1 worldwide and

#1 in Europe

� Protection equipment for hazardous working environments

� Body and Head protection, rescue and escape devices, Masks and Filters, etc.

� Self-containedBreathing Appartus forfire fighters

� #2 worldwide and #1 in Europe

� Customer specific solutions

� mobile and stationary firefighting training systems

� Rescue chambers

� Spareparts and consumables

� Classical-, Multivendor-Product Service

� Shutdown and Rental Service

Note: Market positions based on Dräger‘s market knowledge and its own assessment of market position; positions ranked according to net sales.

Fire Service

�� �� �� ��

Oil & Gas Chemical Mining Other Markets

��

�� �� �� �� ��

�� �� �� �� ��

�� �� �� �� ��

��

�� �� �� �� ��

11

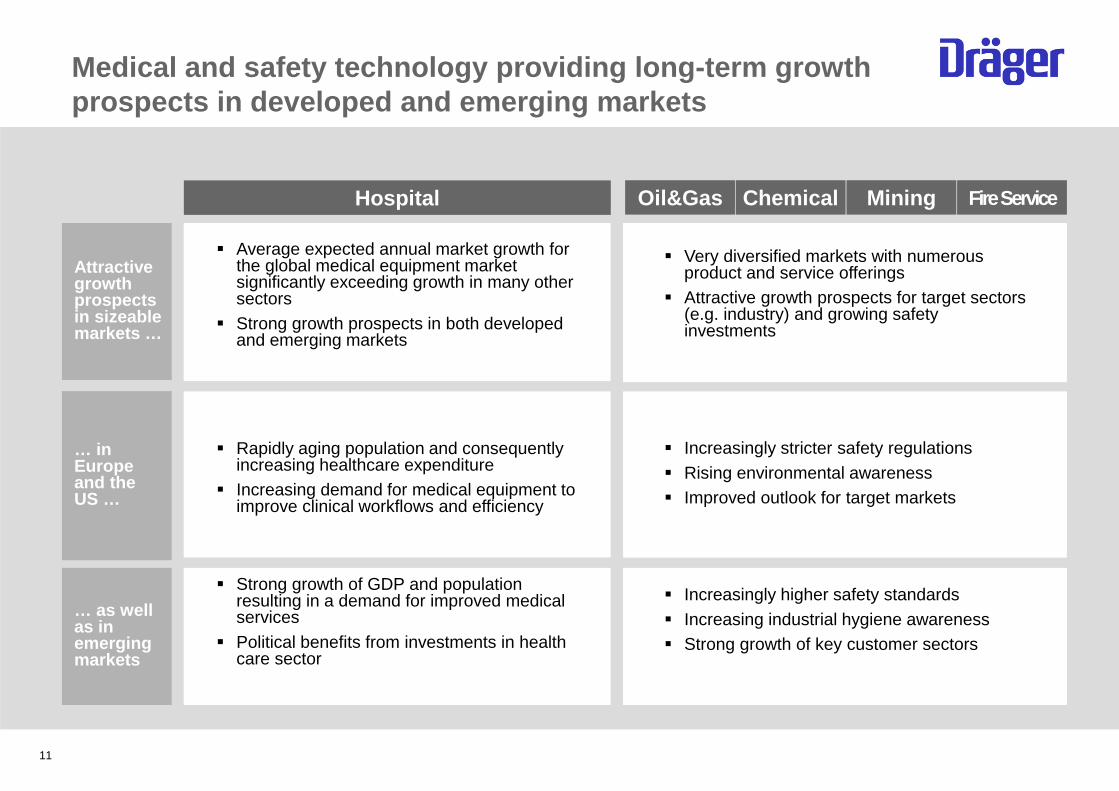

Medical and safety technology providing long-term g rowth prospects in developed and emerging markets

Hospital

Attractive growth prospects in sizeable markets …

… in Europe and the US …

… as well as in emerging markets

Oil&Gas Chemical Mining FireService

� Average expected annual market growth for the global medical equipment market significantly exceeding growth in many other sectors

� Strong growth prospects in both developed and emerging markets

� Very diversified markets with numerous product and service offerings

� Attractive growth prospects for target sectors (e.g. industry) and growing safety investments

� Rapidly aging population and consequently increasing healthcare expenditure

� Increasing demand for medical equipment to improve clinical workflows and efficiency

� Increasingly stricter safety regulations� Rising environmental awareness� Improved outlook for target markets

� Strong growth of GDP and population resulting in a demand for improved medical services

� Political benefits from investments in health care sector

� Increasingly higher safety standards� Increasing industrial hygiene awareness� Strong growth of key customer sectors

12

Management of innovation rate through continuous improvements in quality and R&D processes

Expansion of market positions in attractive markets . Special focus on profitable growth in developing co untries

Expansion of service and consumables business

FIT FOR GROWTH efficiency program

1

2

3

4

Strategy for profitable growth

13

1

Strong R&D focus Innovation to enhance future growth (examples)

Clinical Apps

Software based decision support to improve medical

outcomes. E.g. Smart Pilot View,

Sepsis-Guard

� Approximately 1,400 employees in R&D around the globe

� EUR 231 million spent for R&D activities in 2015 (8.9 % of net sales)

� Tradition of innovation and quality leadership

� Very close collaboration with customers to develop new and improve existing products

� R&D focus on integration of products and services to provide solutions which support customer workflows

� R&D strives to leverage advantage of using same technology for different market segments and products (e.g. in gas sensors)

� Technological competency and high quality standards result in leading market positions and high barriers to entry

Technology and innovation leadership to drive profi table growth

Sensor Portfolio

Permanent expansion of the sensor portfolio:

broad spectrum of detectible gases,

low concentration, high reliability, long

life time

Integration Monitoring and

Anesthesia Device

Anesthesia device Perseus A500 with IACS Monitoring

integration for optimized workflow

in the OR

14

Investments in profitable

growth in developing countries

2

� Focus on the specific needs of customer in developing countries� Identify growth potential in strong growing markets like China, Brazil and India� Capitalize on the significant investments into the Sales & Service infrastructure and

specific market knowledge, especially in our Regions Asia / Pacific, Central- and South-America

� Enhance engagement with partners in developing countries to expand local presence with R&D, manufacturing, sales and after sales business

2

Net sales 2015

Developed Markets

76 %

Newly industrialized

countries24 %

Focused product range

Exploit growth potentials in developing countries

Fabius Plus XLVista 120Savina Color

15

Further expansion of service and

consumables business

3

Service- and consumables business a clear focus of o ur Sales activities

3

Dräger Service Dräger Consumables

� Functionalities with added value, e.g. optimizing workflow with RFID-based communication between consumables part and therapy machine

� Dräger quality to improve hygienic standards

� Dräger value add especially in development of consumables. Production usually via suppliers

� Partly proprietary consumable products, e.g. Dräger-Tubes

� Globally over 3,000 service technicians

� Fast and reliable service (repairs and spare parts) is a critical factor for customers

� Dräger Service technicians important for customer loyalty

� Efficient service solutions via remote service

� Multi Vendor Service

� Administration and Service-Documentation of customers equipment pool

� Capitalize on large installed base to expand after sales business� Continued expansion of service and spare parts offering� Focus on combined sale of equipment and after sales contracts

FIT FOR GROWTH Overview Initiatives

� Legal entity consolidation within sales organization� Streamlining, standardization and pooling of central, regional and local tasks and

processes� Effective expense management� Reduction of SGA ratio* to ~30% in 2017

Improve SG & A expense ratio and

working capital

SHAPE Optimize global Sales, Marketing & Administration set-up

Bring customer value faster to the market

and increase innovation share

Fit!

Improve workflow and delivery times

and reduce production cost

Global footprint

� E.g. Improve competency-, capability- and technology management, strengthen system and platform based development, increase global standardization, reengineer launch process to improve ramp-up speed, expand product portfolio targeted at Emerging Markets,…

� Improve “Time to market” by 50% until 2019 and increase innovation share

Optimize innovation set-up

� Investment into „Zukunftsfabrik“ in Lübeck, Germany

� Transfer of production with high labor content to Chomutov, Czech Republic

� Consolidation of US-facilities (closure of Pittsburgh site)

Optimize production set-up

4

16

* at comparable FX rates Jan. 2015 and before possible on-off expenses for restructuring or similar

Financials

17

Business developmentDräger Group

18

Note: 2015 EBIT includes approx. EUR 35 million restructuring charges

2011 2012 2013 9M 2015 9M 2016

million € million € million € million €

Order Intake 2,293.2 2,405.5 1,895.1 1,849.1 -2.4

Net Sales 2,255.8 2,373.5 1,783.6 1,704.3 -4.4 % growth 3.6% 5.2% 7.1% -4.4%% growth (FX adjusted) 4.4% 2.5% 2.3% -2.6%

Gross Profit 1,108.3 1,167.0 793.5 747.6 -5.8 Gross margin 49.1% 49.2% 44.5% 43.9% -0,6pp

Functional Expenses -894.5 -935.4 -787.5 -720.5 -8.5 % of Net Sales -39.7% -39.4% -44.2% -42.3%

EBIT 213.8 230.3 0.2 28.1 >100EBIT Margin 9.5% 9.7% 0.0% 1.6% +1.6pp

Interest Result -33.0 -32.8 -14.4 -12.3 14.6

Net Profit 125.1 135.7 -11.1 12.5 >100

DVA 134.6 150.0 -11.8 6.7 >100

million €

200.8 8.5%

119.9

-23.5

113.9

-942.2 -39.7%

2,384.6

2,374.2 0.0%3.1%

1,147.6 48.3%

104.7

178.6

-25.0

4.0%

1,138.0

81.6

-967.8

7.3%

46.7%

-39.7%

2014 Change

million € %

2,415.5

2,434.7 2.5%

2015

million €

2,532.2

2,608.9 7.2%2.9%

1,171.7 44.9%

-1,098.4 -42.1%

66.7 2.6%

-17.2

33.3

-46.3

Key figures

19

2011 2012 9M 2015 9M 2016

million € million € million € million €

Cashflow (from operating activities) 161.7 176.8 -7.2 90.9 >100

Investments 78.1 78.2 156.7 71.1 -54.6

Cash and cash equivalents1 412.3 332.4 128.7 173.9 35.1

Net financial debt1 39.8 56.8 165.5 121.0 -26.9 Net financial debt 1 /EBITDA 2 0.1 0.2 0.91 0.68

Capital employed 1 880.0 901.9 1,256.4 1,238.7 -1.4 ROCE (EBIT 2 /Capital employed 1 ) 24.3% 25.5% 7.8% 7.6%

Net Working Capital1 362.8 404.1 592.4 553.1 -6.6

Headcount1 11,924 12,516 14,014 13,292 -5.2 1 Values as of reporting date2 EBITDA and accordingly EBIT of the last twelve months

13,334

110.0 0.4

1,052.9 19.1%

524.3

2013

million €

68.3

110.6

232.1

16.1%

0.04

1,107.2

million €

188.0

124.7

296.9

%

10.7

13,737

539.4

Change2014 2015

million €

39.9

196.8

172.8

145.3 0.96

1,269.3 5.3%

582.3

13,936

Outlook

20

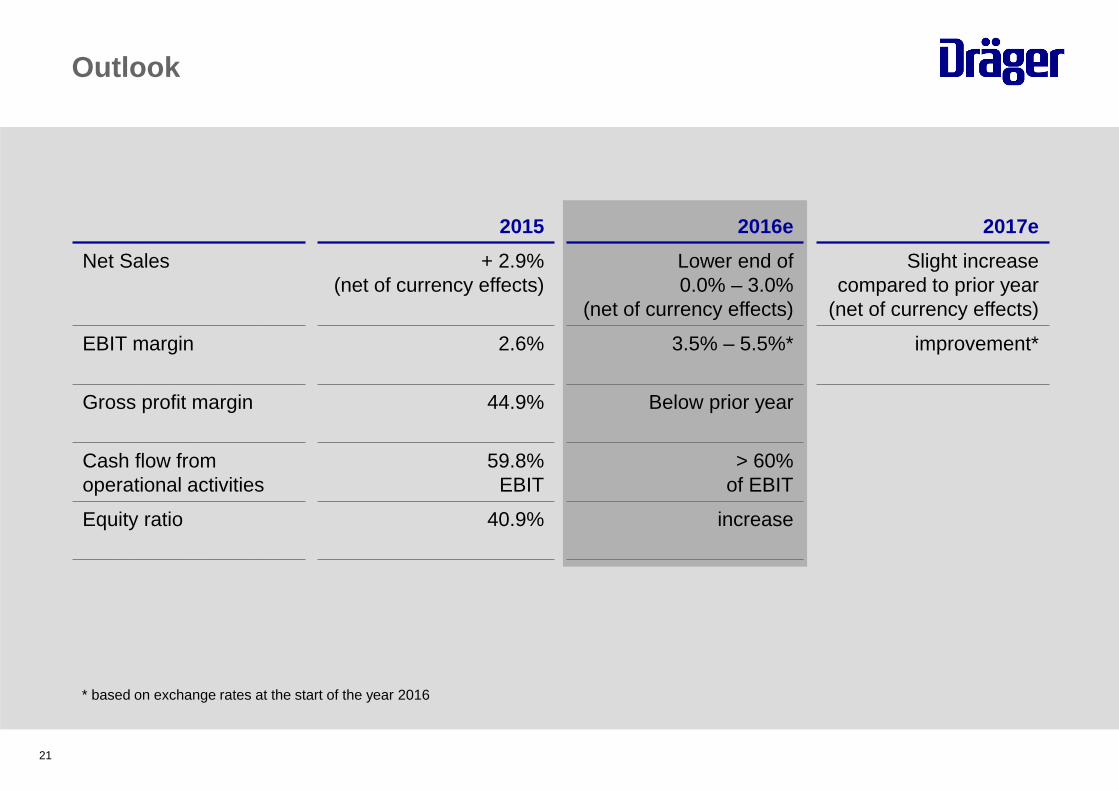

Outlook

2015 2016e 2017e

Net Sales + 2.9%(net of currency effects)

Lower end of0.0% – 3.0%

(net of currency effects)

Slight increasecompared to prior year

(net of currency effects)

EBIT margin 2.6% 3.5% – 5.5%* improvement*

Gross profit margin 44.9% Below prior year

Cash flow fromoperational activities

59.8% EBIT

> 60% of EBIT

Equity ratio 40.9% increase

* based on exchange rates at the start of the year 2016

21

Guiding philosophyWhat we stand for

22

23

Dräger management

Fifth generation of the Dräger family to lead the company

Chairman of the Executive Board (Chief Executive Officer)

At Dräger since 1992

Stefan Dräger

Vice Chairman of the Executive BoardExecutive Board member for Finance and IT

At Dräger since 2008

Gert-Hartwig Lescow

Executive Board member for Purchasing, Production and Logistics

At Dräger since 2015

Rainer Klug Dr. Reiner Piske

Chief Human Resources Officer

At Dräger since 2015

Executive Board member for Innovation and Quality

At Dräger since 2010

Anton Schrofner

Responsible for the Americas region

Responsible for the Europe region

Responsible for the Africa, Asia and Australia regions

24

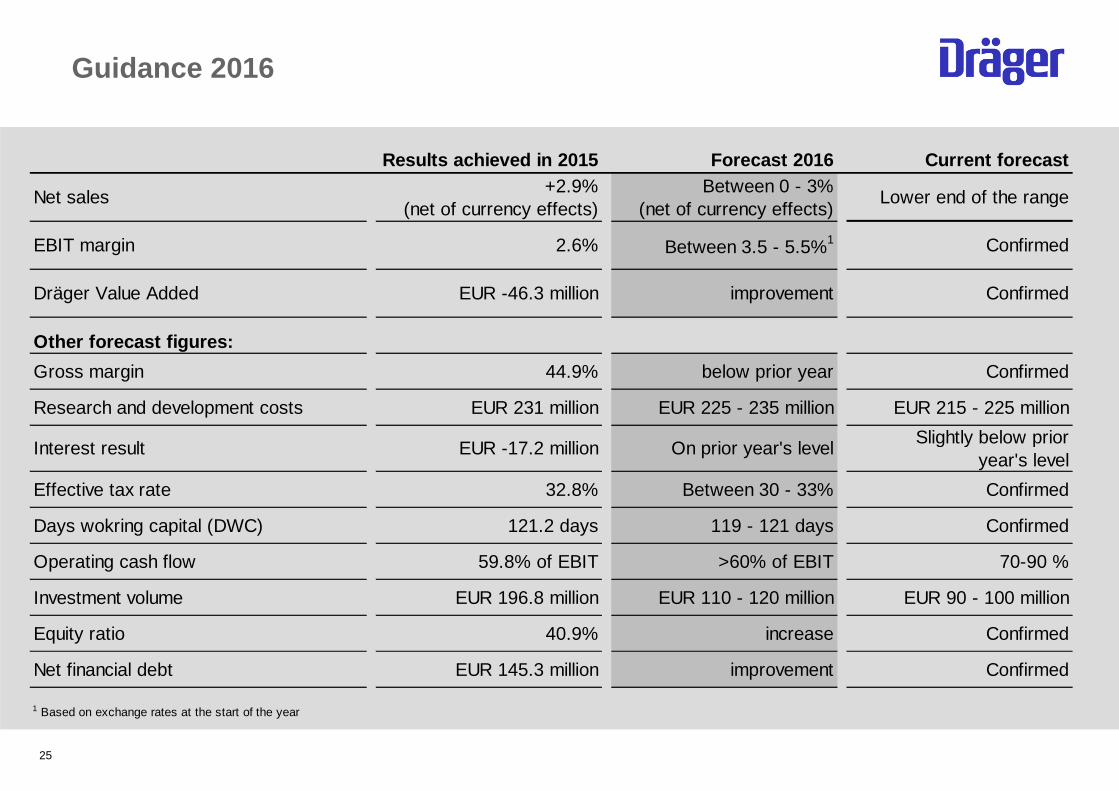

Guidance 2016

25

Results achieved in 2015 Forecast 2016 Current foreca st

Net sales+2.9%

(net of currency effects)Between 0 - 3%

(net of currency effects)Lower end of the range

EBIT margin 2.6% Between 3.5 - 5.5%1 Confirmed

Dräger Value Added EUR -46.3 million improvement Confirmed

Other forecast figures:

Gross margin 44.9% below prior year Confirmed

Research and development costs EUR 231 million EUR 225 - 235 million EUR 215 - 225 million

Interest result EUR -17.2 million On prior year's levelSlightly below prior

year's level

Effective tax rate 32.8% Between 30 - 33% Confirmed

Days wokring capital (DWC) 121.2 days 119 - 121 days Confirmed

Operating cash flow 59.8% of EBIT >60% of EBIT 70-90 %

Investment volume EUR 196.8 million EUR 110 - 120 million EUR 90 - 100 million

Equity ratio 40.9% increase Confirmed

Net financial debt EUR 145.3 million improvement Confirmed

1 Based on exchange rates at the start of the year

26

Shareholder structure

ShareholdingCommon shares

67.2 %

28.8%

4.0%

Dr. Heinrich Dräger GmbH

Free float

Members of the Dräger family

10,160,000 common shares (28.8 % free float)7,600,000 preferred shares (100.0 % free float)

ShareholdingDr. Heinrich Dräger GmbH

Stefan Dräger GmbH

Dräger Foundation

Successors of Dr. Heinrich Dräger

58.7%

23.2%

18.1%

Business developmentSegments

27

Europa Amerika Afrika, Asien, Australien Dräger Konzern

Q3 2015 Q3 2016 Q3 2015 Q3 2016 Q3 2015 Q3 2016 Q3 2015 Q3 2016

million € million € million € million € million € million € million € million €

Order entry 345.1 336.7 129.0 134.7 171.6 156.6 645.7 628.0

Net Sales 339.3 325.0 115.8 119.7 149.0 148.2 604.0 592.9

EBITDA 14.7 25.8 -10.3 5.9 -5.1 11.5 -0.7 43.2

EBIT 3.0 15.5 -15.7 0.3 -9.9 6.8 -22.6 22.5

EBIT-margin 0.9 4.8 -13.5 0.2 -6.6 4.6 -3.7 3.8

Capital Employed1 597.3 572.5 270.5 298.5 388.7 367.7 1,256.4 1,238.7

ROCE1,2 15.2 10.7 -5.8 -1.5 5.7 10.3 7.8 7.6

DVA 39.5 20.8 -39.9 -24.9 -11.4 10.8 -11.8 6.7 1 Values at due date2 EBIT of the last twelve months

Business developmentSegments

28

Europa Amerika Afrika, Asien, Australien Dräger Konzern

9M 2015 9M 2016 9M 2015 9M 2016 9M 2015 9M 2016 9M 2015 9M 2016

million € million € million € million € million € million € million € million €

Order entry 1,024.2 1,009.9 368.2 371.2 502.7 468.0 1,895.1 1,849.1

Net Sales 985.6 949.2 348.5 335.9 449.4 419.3 1,783.6 1,704.3

EBITDA 55.3 56.2 -6.8 7.6 13.5 25.9 62.0 89.7

EBIT 23.8 25.7 -22.8 -8.7 -0.9 11.0 0.2 28.1

EBIT-margin 2.4 2.7 -6.5 -2.6 -0.2 2.6 0.0 1.6

Capital Employed1 597.3 572.5 270.5 298.5 388.7 367.7 1,256.4 1,238.7

ROCE1,2 15.2 10.7 -5.8 -1.5 5.7 10.3 7.8 7.6

DVA 39.5 20.8 -39.9 -24.9 -11.4 10.8 -11.8 6.7 1 Values at due date2 EBIT of the last twelve months

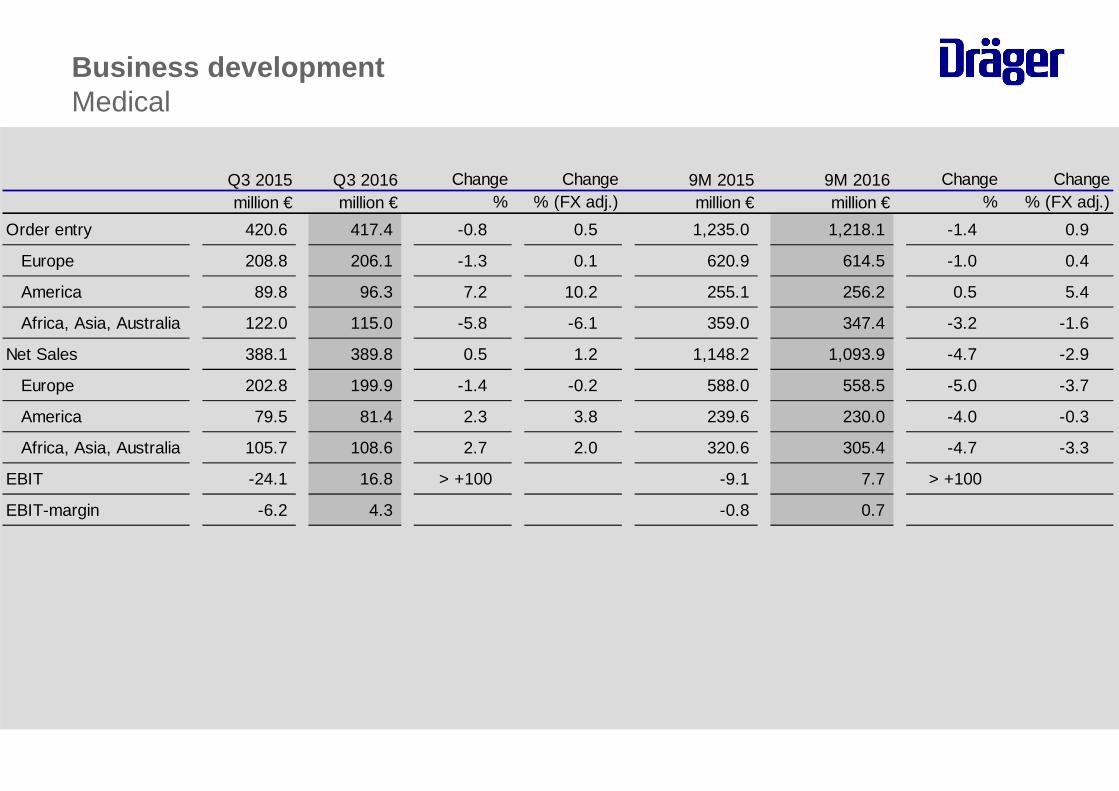

Business developmentMedical

Q3 2015 Q3 2016 9M 2015 9M 2016million € million € million € million €

Order entry 420.6 417.4 -0.8 0.5 1,235.0 1,218.1 -1.4 0.9

Europe 208.8 206.1 -1.3 0.1 620.9 614.5 -1.0 0.4

America 89.8 96.3 7.2 10.2 255.1 256.2 0.5 5.4

Africa, Asia, Australia 122.0 115.0 -5.8 -6.1 359.0 347.4 -3.2 -1.6

Net Sales 388.1 389.8 0.5 1.2 1,148.2 1,093.9 -4.7 -2.9

Europe 202.8 199.9 -1.4 -0.2 588.0 558.5 -5.0 -3.7

America 79.5 81.4 2.3 3.8 239.6 230.0 -4.0 -0.3

Africa, Asia, Australia 105.7 108.6 2.7 2.0 320.6 305.4 -4.7 -3.3

EBIT -24.1 16.8 > +100 -9.1 7.7 > +100

EBIT-margin -6.2 4.3 -0.8 0.7

Change% (FX adj.)

Change% %

Change% (FX adj.)

Change

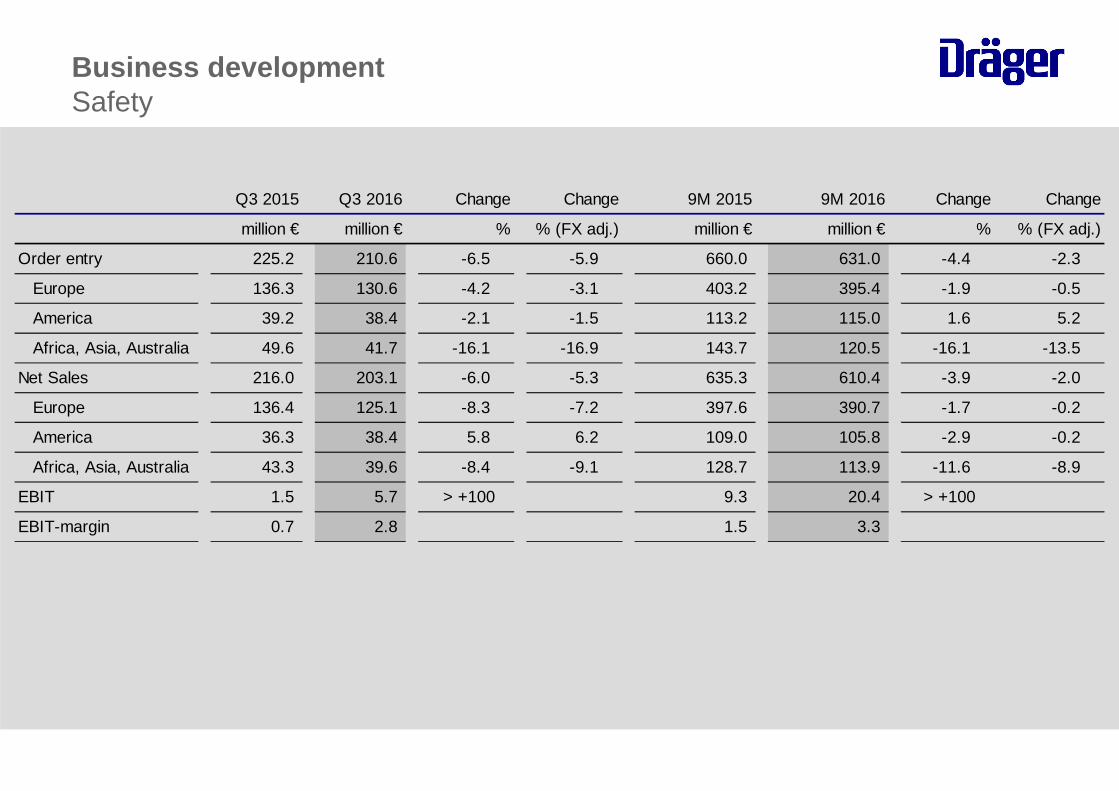

Business developmentSafety

Q3 2015 Q3 2016 9M 2015 9M 2016

million € million € million € million €

Order entry 225.2 210.6 -6.5 -5.9 660.0 631.0 -4.4 -2.3

Europe 136.3 130.6 -4.2 -3.1 403.2 395.4 -1.9 -0.5

America 39.2 38.4 -2.1 -1.5 113.2 115.0 1.6 5.2

Africa, Asia, Australia 49.6 41.7 -16.1 -16.9 143.7 120.5 -16.1 -13.5

Net Sales 216.0 203.1 -6.0 -5.3 635.3 610.4 -3.9 -2.0

Europe 136.4 125.1 -8.3 -7.2 397.6 390.7 -1.7 -0.2

America 36.3 38.4 5.8 6.2 109.0 105.8 -2.9 -0.2

Africa, Asia, Australia 43.3 39.6 -8.4 -9.1 128.7 113.9 -11.6 -8.9

EBIT 1.5 5.7 > +100 9.3 20.4 > +100

EBIT-margin 0.7 2.8 1.5 3.3

Change

% (FX adj.)

Change

%

Change Change

% % (FX adj.)

Functional Expenses

31

2011 2012 9M 2015 9M 2016

million € million € million € million €

R&D -160.5 -197.3 -174.9 -163.4 -6.6 % of Net Sales -7.1% -8.3% -9.8% -9.6%

SG&A -724.8 -735.4 -610.4 -554.5 -9.1 % of Net Sales -32.1% -31.0% -34.2% -32.5%

Functional Expenses total -894.5 -935.4 -787.5 -720.5 -8.5 % of Net Sales -39.7% -39.4% -44.2% -42.3%

-861.2 -33.0%

-1,098.4 -42.1%

-231.1 -8.9%

2015

million €

Change

-30.8%

-967.8 -39.7%

million €

2014

-8.7%

-749.2

-212.0

%

2013

-39.7%

million €

-201.5 -8.5%

-738.4 -31.1%

-942.2

2,311.4

1,400.9

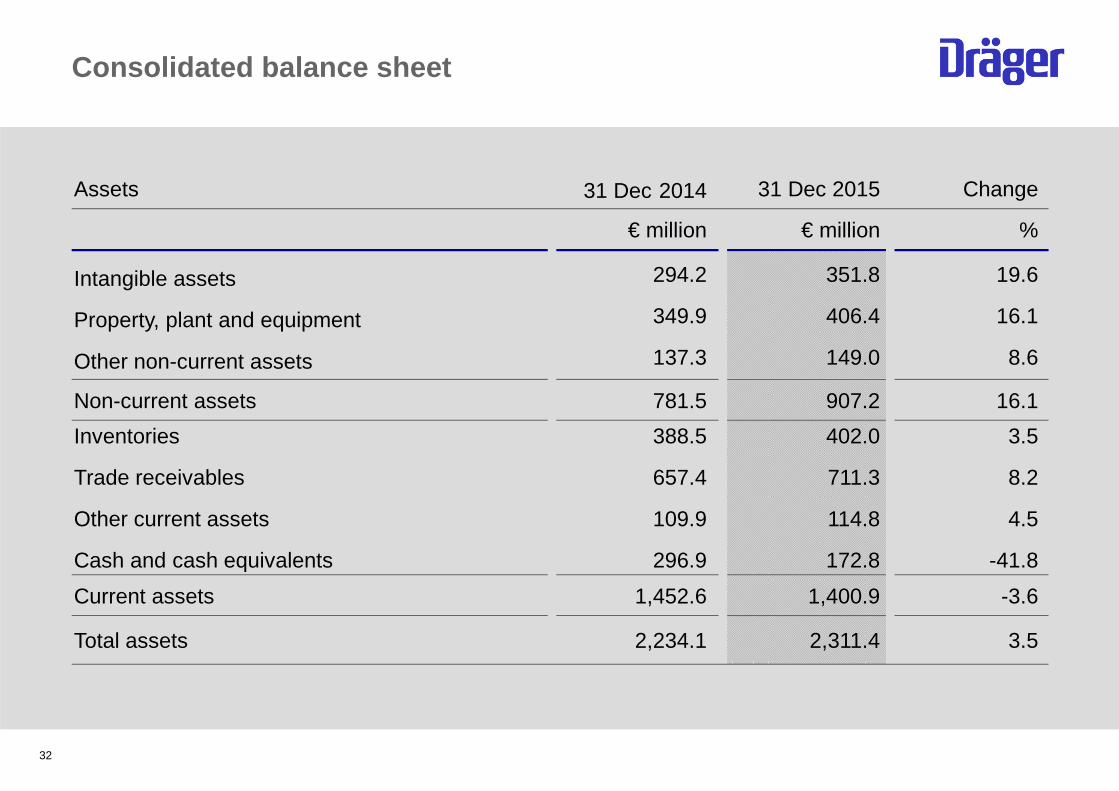

Consolidated balance sheet

€ million

Change31 Dec 201531 Dec 2014Assets

-3.61,452.6Current assets

3.5

8.2

4.5

-41.8

402.0

711.3

114.8

172.8

388.5

657.4

109.9

296.9

Inventories

Trade receivables

Other current assets

Cash and cash equivalents

16.1907.2781.5Non-current assets

19.6

16.1

8.6

351.8

406.4

149.0

294.2

349.9

137.3

Intangible assets

Property, plant and equipment

Other non-current assets

%€ million

3.52,234.1Total assets

32

2,311.4

21.8

288.1

138.1

97.8

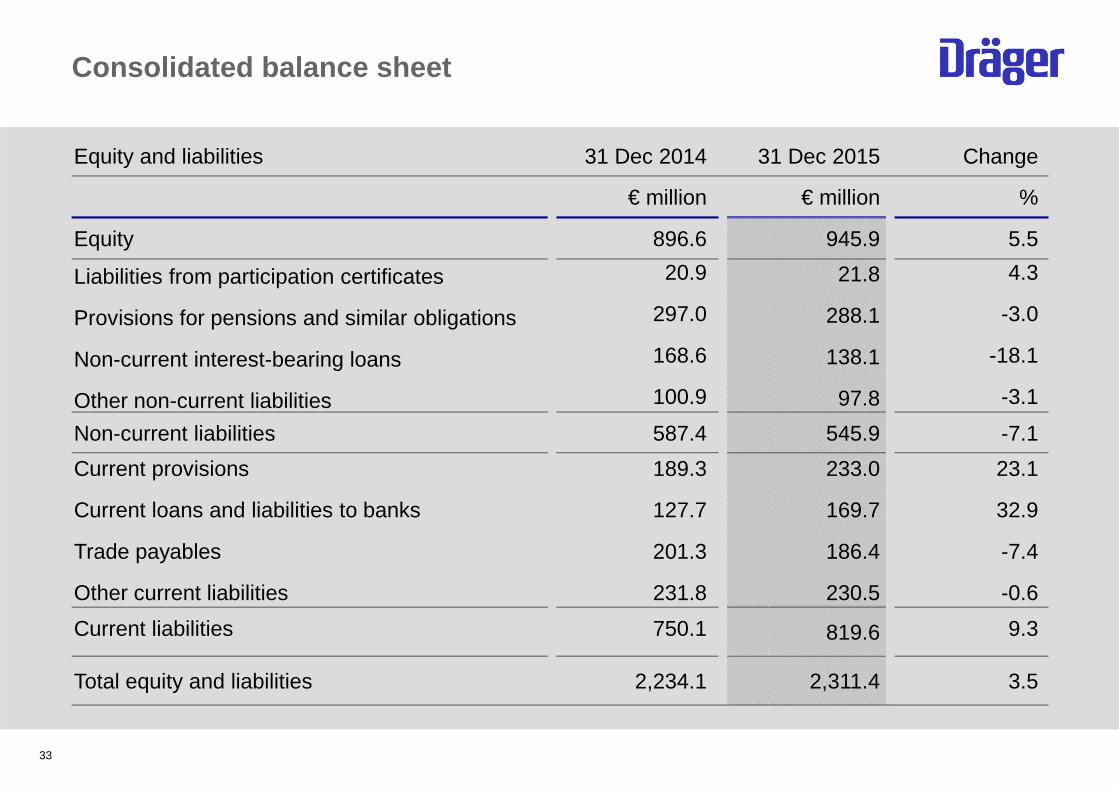

Consolidated balance sheet

€ million

Change31 Dec 201531 Dec 2014Equity and liabilities

9.3819.6750.1Current liabilities

23.1

32.9

-7.4

-0.6

233.0

169.7

186.4

230.5

189.3

127.7

201.3

231.8

-7.1545.9587.4Non-current liabilities

4.3

-3.0

-18.1

-3.1

20.9

297.0

168.6

100.9

Liabilities from participation certificates

Provisions for pensions and similar obligations

Non-current interest-bearing loans

Other non-current liabilities

5.5945.9896.6Equity

%€ million

3.52,234.1Total equity and liabilities

Current provisions

Current loans and liabilities to banks

Trade payables

Other current liabilities

33

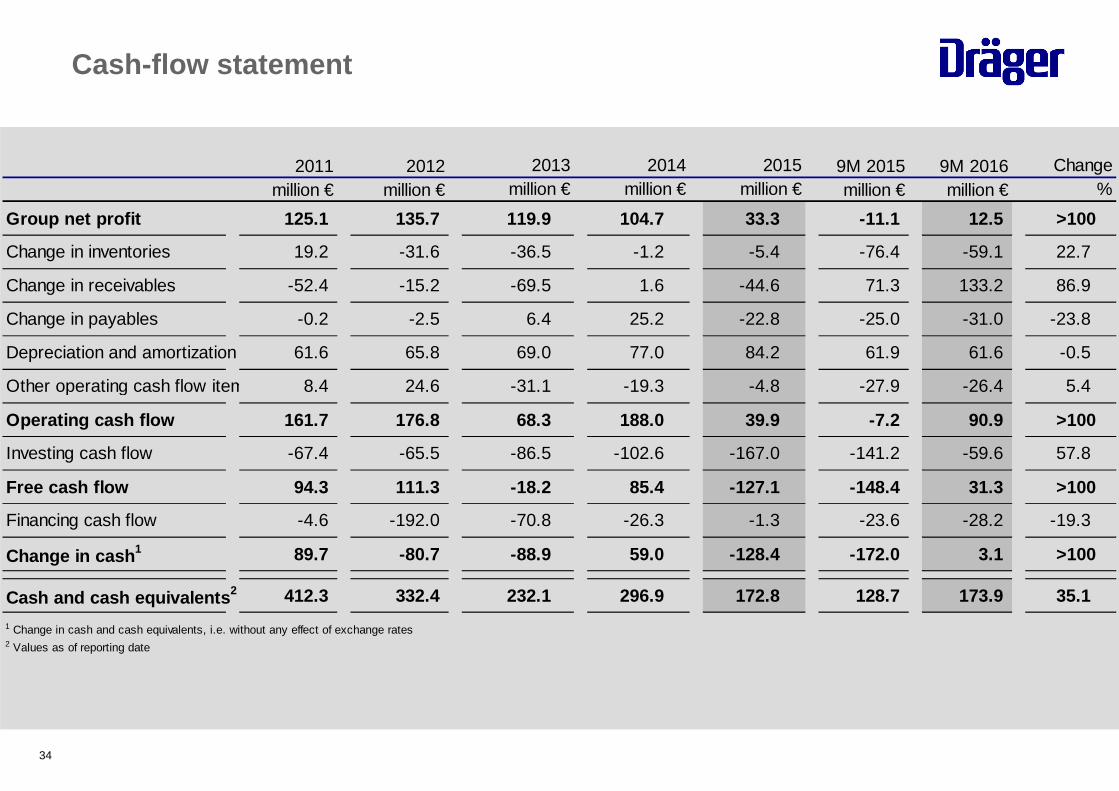

Cash-flow statement

34

2011 2012 9M 2015 9M 2016million € million € million € million €

Group net profit 125.1 135.7 119.9 104.7 33.3 -11.1 12.5 >100

Change in inventories 19.2 -31.6 -36.5 -1.2 -5.4 -76.4 -59.1 22.7

Change in receivables -52.4 -15.2 -69.5 1.6 -44.6 71.3 133.2 86.9

Change in payables -0.2 -2.5 6.4 25.2 -22.8 -25.0 -31.0 -23.8

Depreciation and amortization 61.6 65.8 69.0 77.0 84.2 61.9 61.6 -0.5

Other operating cash flow items 8.4 24.6 -31.1 -19.3 -4.8 -27.9 -26.4 5.4

Operating cash flow 161.7 176.8 68.3 188.0 39.9 -7.2 90.9 >100

Investing cash flow -67.4 -65.5 -86.5 -102.6 -167.0 -141.2 -59.6 57.8

Free cash flow 94.3 111.3 -18.2 85.4 -127.1 -148.4 3 1.3 >100

Financing cash flow -4.6 -192.0 -70.8 -26.3 -1.3 -23.6 -28.2 -19.3

Change in cash 1 89.7 -80.7 -88.9 59.0 -128.4 -172.0 3.1 >100

Cash and cash equivalents 2 412.3 332.4 232.1 296.9 172.8 128.7 173.9 35.1

1 Change in cash and cash equivalents, i.e. without any effect of exchange rates2 Values as of reporting date

2015million €

2014 Changemillion € %

2013million €

35

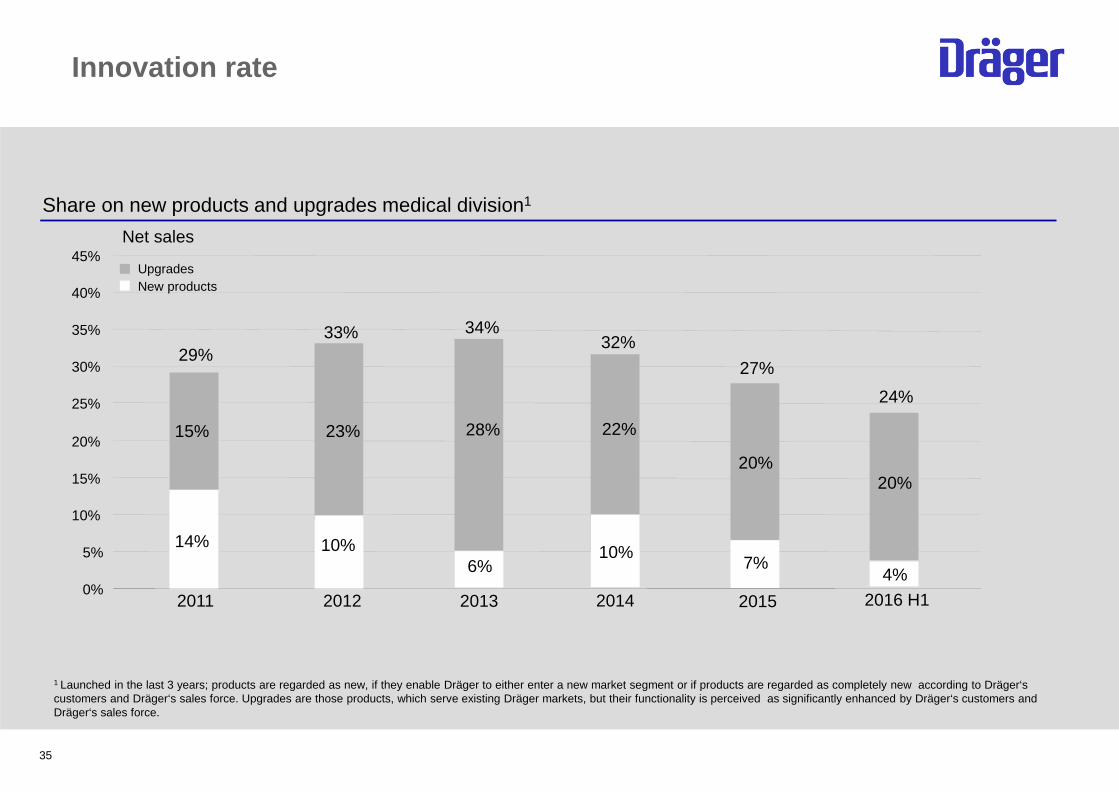

Innovation rate

Share on new products and upgrades medical division1

1 Launched in the last 3 years; products are regarded as new, if they enable Dräger to either enter a new market segment or if products are regarded as completely new according to Dräger‘s customers and Dräger‘s sales force. Upgrades are those products, which serve existing Dräger markets, but their functionality is perceived as significantly enhanced by Dräger‘s customers and Dräger‘s sales force.

New productsUpgrades

Net sales

20%

15% 23%

14%7%

20152011 20120%

5%

10%

15%

20%

25%

30%

35%

40%

45%

10%

27%

33%29%

28%

2013

6%

34%

22%

2014

10%

32%

20%

4%

2016 H1

24%

March 8, 2017 - Accounts press conference, Lübeck- Analysts meeting

May 4, 2017 - Report for the first three months 2017 Conference call, Lübeck

May 10, 2017 - Annual shareholders' meeting, Lübeck

July 27, 2017 - Report for the first six months 2017 Conference call, Lübeck

November 2, 2017 - Report for the first nine months 2017 Conference call, Lübeck

Financial calendar 2017

36

37

Melanie Kamann Thomas FischlerCorporate Communications Investor Relations

Drägerwerk AG & Co. KGaA Drägerwerk AG & Co. KGaAMoislinger Allee 53−55 Moislinger Allee 53−5523558 Lübeck, Germany 23558 Lübeck, Germany

Tel +49 451 882-3998 Tel +49 451 882-2685 Fax +49 451 882-3944 Fax +49 451 882-3296

Mobile +49 170 8558152 Mobile +49 151 12245295

[email protected] [email protected] www.draeger.com

Contact