Embed Size (px)

Citation preview

Driving Innovation

in Retail Banking

Agenda

• Some background on CIMB

• Key challenges in Retail Banking

• Key trends impacting our plans for the future

• CIMB’s response

• Some questions and challenges

• A bit of fun with branding

Some background on CIMB

4

1Malaysia Origins

Bian Chiang Bank (1924)

CIMB, previously PBS (1974)

BHL (1935)

UAB (1972)

SBB (1965)

Bank Bumi (1965)

Transformed from Malaysian Investment Bank to Universal Bank…

5

2005 2006 2007

Acquired GK Goh CIMB-BCB merger

Acquired SBB Acquired Bank Niaga

… to ASEAN Universal Banking in 5 Years…

6

2009 2010

Acquired BankThai Singapore Retail Banking Launched

CIMB Bank Cambodia Launched

2008

Niaga-Lippo merger

RM 61.6 bil*

Over 38,000

RM 272.3 bil**

RM 32.2 bil AUM**

RM 23.5 bil**

4 core

9 non-core

…via RM18 bil Worth of Acquisitions…

RM 5.0 bil Market cap

1,000 Staff strength

RM 16.8 bil

RM 1.1 bil AUM Assets

RM 2.0 bil

Share-holders’ funds

Malaysia Markets

Jan 05

Date Deal Value

Jun 05

Jun 06

USD 146.1 mil

P/B 1.3x

USD 1.1 bil

P/B 1.0x

USD 1.8 bil

P/B 2.2x

Jun 08

Jan 09

USD 0.4 bil

P/B 2.0x

USD 0.4 bil

P/B 2.0x

Jan 07 USD 0.8 bil

P/B 2.1x

* Data as at 27 May 2011

** Data as at 31 Mac 2011 7

Integratio

n an

d tran

sform

ation

8

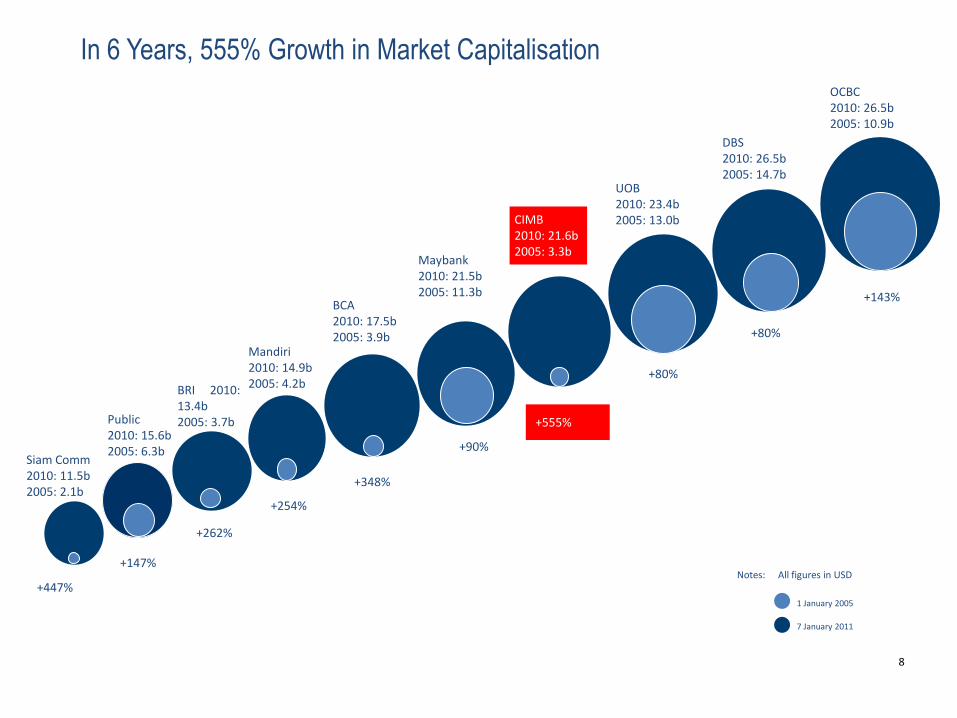

1 January 2005

7 January 2011

UOB 2010: 23.4b 2005: 13.0b

+80%

DBS 2010: 26.5b 2005: 14.7b

+143%

Siam Comm 2010: 11.5b 2005: 2.1b

+447%

Mandiri 2010: 14.9b 2005: 4.2b

+254%

Public 2010: 15.6b 2005: 6.3b

+147%

Maybank 2010: 21.5b 2005: 11.3b

+90%

OCBC 2010: 26.5b 2005: 10.9b

+80%

+348%

BCA 2010: 17.5b 2005: 3.9b

+555%

CIMB 2010: 21.6b 2005: 3.3b

+262%

BRI 2010: 13.4b 2005: 3.7b

Notes: All figures in USD

In 6 Years, 555% Growth in Market Capitalisation

Singapore

2 branches

6 ATMs

1,089 staff

205k customers

Malaysia

324 branches

2,061 ATMs

20,115 staff

6.1 mil customers

Indonesia

611 branches

1,276 ATMs

11,912 staff

3.6 mil customers

Thailand

147 branches

468 ATMs

3,787 staff

2.3 mil customers

CIBD Yes Yes Yes Yes

Treasury Yes Yes Yes Yes

Retail Banking Yes Yes Yes Yes

Credit Cards Yes Yes Yes WIP

Business

Banking

Yes Yes Yes Yes

Islamic Banking Yes Yes Ltd No

Private banking Yes Yes No Yes

Insurance Yes Yes WIP WIP

Arguably the best UB platform in SEA

37,000 staff

serving 12 mil

customers via

1,084 branches

Comprehensive SEA UB Platform

Note: Data as at 30 September 2010

9

10

• CIMB is a major catalyst in driving ASEAN Integration •Our CEO and other prominent business people have created the ASEAN Business club •CIMB has its own ASEAN research institute CARI •CIMB is working closely with Central Banks in ASEAN to create a regional banking framework

11

Internet Banking base

CIMB Malaysia

Year 2009 (end July)

2010

2011* (Projection)

Total Base 146,821 205,457 498,731

Active Customers 30,567 - 189,517

Retail base Nil 1,980,201 2,512,949

Retail Base Penetration %

- 10% 19.85%

No. of Fin.Txns Nil 1,390,956 2,489,100

Revenue Nil RM1,767,210 RM3,162,402

CIMB Niaga

Year 2009 2010 2011* (Projection)

Total Base 465 5,334 3000 * migrated from 2010

users*

Active Customers 283 15,895 1,200 * migrated from 2010

users*

Retail base 542,111 471,312 450,804

Retail Base Penetration %

0.09% 1.13% 0.67%

No. of Fin.Txns 19,589 19,403 5,435

Revenue Nil Nil RM1589

CIMB Thai CIMB Singapore

Year 2009 2010 2011* (Projection)

Total Base 3,425 10,854 18,825

Active Customers Nil Nil 11,852

Retail base 5,714 13,144 33,152

Retail Base Penetration %

59.9% 82.6% 56.8%

No. of Fin.Txns 702 12,991 19,141

Revenue Nil Nil Nil

Year 2009 2010 2011

*(Projection)

Total Base 1,026,393 1,437,231 1,821,238

Active Customers 527,564 708,464 850,784

Retail base 5,893,223 6,308,527 6,664,923

Retail Base Penetration %

17% 23% 27%

No. of Fin.Txns 14,614,047 23,146,012 33,169,310

Revenue RM 4,940,136 RM8,181,843 RM 12,537,432

*2011 Projection is based on YTD Aug run rate

Key challenges in

Retail Financial Services

Key challenges in RFS

• Downright scary squeezing of margins – particularly in ASEAN

• Continually escalating costs, particularly manpower and IT

• Increasing domestic and global risk

• Increasingly sophisticated customers with decreasing brand loyalty

• Greater need for product and segment differentiation leading to greater cost and complexity

• Increasing cost of regulatory compliance

• Increasingly sophisticated criminals !

13

Key trends affecting our

future plans

Key Underlying Trends – Looking across time

Trend 1 Usage trends of mobile technologies

Trend 2 Blurring of geographical boundaries

Trend 3 Growth of Internet Usage

Trend 4 Social media is changing customer

behavior

Trend 5 Fraud continues to gain sophistication

Key Trends

15

Proliferation of smart phones, tablets & PCs has brought technology closer

to a wider group of customers

• Leading to a shift in customer expectations –

anytime, everywhere, services at the tip of their fingertips

Usage Trends of Mobile Technologies Trend 1

Evolving Models of Retail Banking Distribution,

Deloitte Center for Banking Solutions, 2009 16

Technology has relaxed geographical boundaries, and it’s easier to replicate a

product from one market to another, especially when it’s an online proposition.

Blurring of Geographical Boundaries Trend 2

17

• Improvement in broadband infrastructure and lower cost of broadband fees

has brought technology closer to many Malaysians.

• Growth of internet usage in Asia over the last 10 years is 706.9%

•I joke with my wife that Singapore will soon be fully WIFI

World Regions Population

( 2011 Est.)

Internet Users

Dec. 31, 2000

Internet Users

Latest Data

Penetration

(% Population)

Growth

2000-2011

Users %

of Total

Africa 1,037,524,058 4,514,400 118,609,620 11.4 % 2,527.4 % 5.7 %

Asia 3,879,740,877 114,304,000 922,329,554 23.8 % 706.9 % 44.0 %

Europe 816,426,346 105,096,093 476,213,935 58.3 % 353.1 % 22.7 %

Middle East 216,258,843 3,284,800 68,553,666 31.7 % 1,987.0 % 3.3 %

North America 347,394,870 108,096,800 272,066,000 78.3 % 151.7 % 13.0 %

Latin America 597,283,165 18,068,919 215,939,400 36.2 % 1,037.4 % 10.3 %

Oceania / Australia 35,426,995 7,620,480 21,293,830 60.1 % 179.4 % 1.0 %

WORLD TOTAL 6,930,055,154 360,985,492 2,095,006,005 30.2 % 480.4 % 100.0 %

Growth of Internet Usage Trend 3

18

In Malaysia, Internet Banking continues to grow in popularity, but Mobile

Banking has yet to gain traction….

0

2

4

6

8

10

12

2005 2006 2007 2008 2009 2010

Internet Banking Subscribers

Total Subscribers (mil)

Peneration 9.8%

0

100

200

300

400

500

600

700

800

900

1000

2005 2006 2007 2008 2009 2010

Mobile Banking Subscribers

Total Subscribers (mil)

2.6 3.2

4.6

6.2

8.1

9.8

127.6

246.7

367.6

574.6

675

898.5

Peneration 12%

Peneration 16.9%

Peneration 22.5%

Peneration 29.1%

Peneration 34.8%

Peneration 0.7%

Peneration 1.3%

Peneration 1.6%

Peneration 2.1%

Peneration 2.2%

Peneration 2.7%

Penetration rate of Internet Banking &

Mobile Banking in Malaysia Trend 3

19

The meeting place for bankers to meet customers has changed

Social Media is Changing Customer

Behavior Trend 4

20

• Gen X & Y are increasingly spending more time at social networking sites.

• Banks must realise that customers have a life outside the bank.

• Work around the customers’ lifestyle needs, instead of churning out

products based only on high-level segment needs.

Life Outside the Bank Trend 4

21

• Many of us are natural skeptics, and in the virtual world, it becomes much easier to

listen, engage and believe in what others are saying.

• Begin to look at using social metric tools to analyse the influencers, customers

sentiments, how the bank’s brand is being perceived & obtain early warning signs of

dissatisfaction.

The Social Influencers Trend 4

22

• Along with the move to spend more effort in the social media space, fraud continues to be

prevalent.

• Fraudsters are continuously monitoring what the banks are introducing & use that very new

service to trick customers!

. The latest is SIM Hijack

• Creating the balance between moving into new channels rapidly, whilst ensuring security is

tightly controlled.

Increased Sophistication in Fraud Trend 5

23

Our response

Online Continue the expansion of

CIMB Clicks

Going Social Interact with customers in their ‘space’

Mobile + Introduce more lifestyle

services

Fraud Tighten the bolts

Our Response

25

Our Response

Growing the Internet Banking space

• Expanding the services offered

• Creating differentiated experience based on

customer segment

• Starting on convergence of Internet banking and

social networking

• Providing value added services, such as

payment alerts, online consolidated statements

• Multi channel integration that enables

customers to change ATM limits, activate their

ATM cards for overseas usage, link accounts to

the ATM card and the capability to integrate online

bill payments with ATM and cash deposit machine

payments.

26

Our Response Engaging customers online

27

Our response - CIMB on Facebook

28

Our current fan count across our M.I.S.T pages is over 460,000. We have grown by 288,000 since June 2011. Malaysia (Fan growth 13.06.11 – 10.10.11) 117,300 • Urbanscapes ticket giveaway – As a lead in to our CIMB YOUth community application launch, we ran a music festival ticket giveaway. • CIMB YOUth – To drive awareness for our new segment proposition, we launched a youth community portal • Facebook Deals – We were presented with a unique opportunity to tie up directly with Facebook to rollout a first of its kind deal in Malaysia.

Singapore (Fan growth 13.06.11 – 10.10.11) 4,947 Established its presence in the 1st week of August. The kickoff campaign for the page is the regional campaign with our first in-country campaign in the pipeline to support SG’s end of year Credit Card campaign

Our response - CIMB on Facebook

29

Thailand (Fan growth 13.06.11 – 10.10.11) 79,910 Thailand’s strong growth can be attributed to the Get with Gang kickoff campaign and growth is persisting with launch of the regional campaign. Indonesia (Fan growth 13.06.11 – 10.10.11) 84,000 Since the launch of the page, Indonesia has been rolling out engagement activities. The first campaign, Wujudkan MimpiMu, brought in the necessary fanbase that allowed subsequent campaigns to reap viral potential. Since then, the Ucapkan CIMB video contest, regional campaign and the 2nd phase of Wujudkan MimpiMu has taken flight. Regional Campaign • ASEAN For You – To provide extended reach and reinforcement for our new tagline, we designed an application that embodies our ASEAN ambition.

Our response - CIMB on Facebook

30

Gaining traction as a bank to watch on social media . CIMB was listed by Retail Banker International as the #6 most socially active bank in the world! This was behind the likes of Chase and Amex (which technically have huge fan bases because they are not specifically focusing on banking – Chase runs a community giving site and Amex is a credit card site which gives out benefits via Facebook)

Our response - CIMB on Facebook

31

Our Jammin’ and YOUth application was noticed by Visible Banking, a UK based site that monitors social media activities conducted by banks globally.

The reviews written about the applications were positive applauding the viral effect these applications have taken.

Turned the content we have been getting on social media into positive PR – reinforcing brand positioning.

Our response - CIMB on Facebook

32

32

• CIMB is the first brand in Malaysia to tie-up with Facebook to rollout Facebook Deals

• Check in to San Fran through FB on your smartphone and enjoy a free drink and chocolate bar with every drink purchase with your CIMB Bank Credit Card.

• The campaign, which clocked 1692 check-ins at 15 San Francisco outlets nationwide, ended on 5 October 2011

ASEAN For You on Facebook

33

• We launched our very first regional application on 24 Sept.

• The objective of this campaign is to amplify awareness of ASEAN For You as our tagline and at the same time grow our fanbase across the region.

• Users that visit the app will be given a chance to turnover pixels that contain prizes hidden randomly beneath them. Throughout the user journey, they will be served factoids on ASEAN.

• This application is currently running simultaneously across all 4 in-country FB pages (M.I.S.T)

• To date, this has helped us grow our regional FB presence by 95,000 fans

Development of YOUth community on Facebook

34

• This application was designed to provide another layer of engagement that complements the current initiatives on the CIMB YOUth microsite.

• Participants earn FUNds by sharing.These FUNds can then be used to bid for prizes such as XBoX 360 consoles, Galaxy Tabs, Cameras and much more.

• Participants that have YOUth accounts are given exclusivity in bidding for premium items and other privileges. This creates desirability towards the YOUth savers account.

• The application has helped draw in 31,229 fans for the CIMB Malaysia page to date and was labeled as the “Most Viral Facebook Application for the Under 25s”

Our Response

Going mobile

• Offering multiple access modes

• Additional services utilizing the

phones native capabilities

35

Our Response

Implementing tighter fraud prevention

methods

• Transaction Protection which provides real-time

analysis of customers behavior and scores

every transaction that comes via CIMB Clicks

• Additional Authentication for higher risk scores

• Awareness

• Multiple TAC Methods

36

Some questions and

challenges

Our Challenges The experience on the mobile is different for each of us.

38

Our Challenges

• Do we continue to build and enhance apps, or do we optimize the website

for mobile browsing?

• Wait and leverage off the NFC-enabled handsets, or innovate now using

SD cards, SIM overlays or NFC Sleeves?

NFC Enabled

Handset

SIM Overlay

(with RFID Antenna)

MicroSD External Hardware NFC Sticker

(Active/Passive)

39

Our Challenges

Keeping the lights on!

• Ensuring the IT infrastructure is able to

support these new channels.

• Ability to scale up quickly, if any new

channel introduced becomes popular.

• Removing common bottlenecks such as

network bandwidth, data storage when

there is a seasonal surge in usage

• The cost of all this is significant… are

alternate channels really cheaper ?

40

Final Challenge • Invest, pilot & experiment…

• Grow new markets…

• Stop avoiding risks … just managing them

• Be comfortable with being uncomfortable of

new ideas…

• Understand that banking is not the only

priority in customers’ lives.

41

Some fun with

branding

43

The Journey of CIMB Clicks’ Octo Octo has evolved into one of the most recognizable and talk-about mascots in the global banking industry!!!

Octo is making big waves in the blog space…

“ Octo is seriously cute!”

… both in Malaysia as well as aboard!

“Comel…. Seronok!”

“Postman was also smiling”

“Enzy my new friend is so so cute and so so cuddly!”

And is also a hot item on Ebay…

The Octo is now getting its tentacles across CIMB Group…

But in Singapore… the “sotong” is “kosong”!

The last frontier…

Coming soon

The next frontier

49

Thank You!

![NO. SEBUTHARGA: 2/2021 NO. FAIL: … · 2021. 2. 9. · pemotongan rumput kekerapan : bil tempat/kawasan [ zon 1 ] keluasan kawasan ( m² ) kadar (rm) / m ² kadar bulanan (rm) 1](https://img.pdfslide.net/doc/110x75/610f99370ca437030342db77/no-sebutharga-22021-no-fail-2021-2-9-pemotongan-rumput-kekerapan-bil.jpg)

![JADUAL 3 FI RAWATAN - jknmelaka.moh.gov.my Rawatan3.pdf · Bil. Prosedur (BM) Procedure (BI) TAHUN 2015 (RM) TAHUN 2016 (RM) TAHUN 2017 (RM) TAHUN 2018 [Kos perkhidmatan (RM)] 1 RAWATAN](https://img.pdfslide.net/doc/110x75/5d5ca96e88c99390578be07e/jadual-3-fi-rawatan-rawatan3pdf-bil-prosedur-bm-procedure-bi-tahun-2015.jpg)

![TAHUN 2018 TAHUN [Kos 2015 2016 2017 Perkhidmatan (RM) … Ujian Makmal.pdf · Bil. Prosedur TAHUN 2015 (RM) TAHUN 2016 (RM) TAHUN 2017 (RM) TAHUN 2018 [Kos Perkhidmatan (RM)] JADUAL](https://img.pdfslide.net/doc/110x75/5d211bdc88c993045a8b9ab7/tahun-2018-tahun-kos-2015-2016-2017-perkhidmatan-rm-ujian-makmalpdf-bil.jpg)