Embed Size (px)

Citation preview

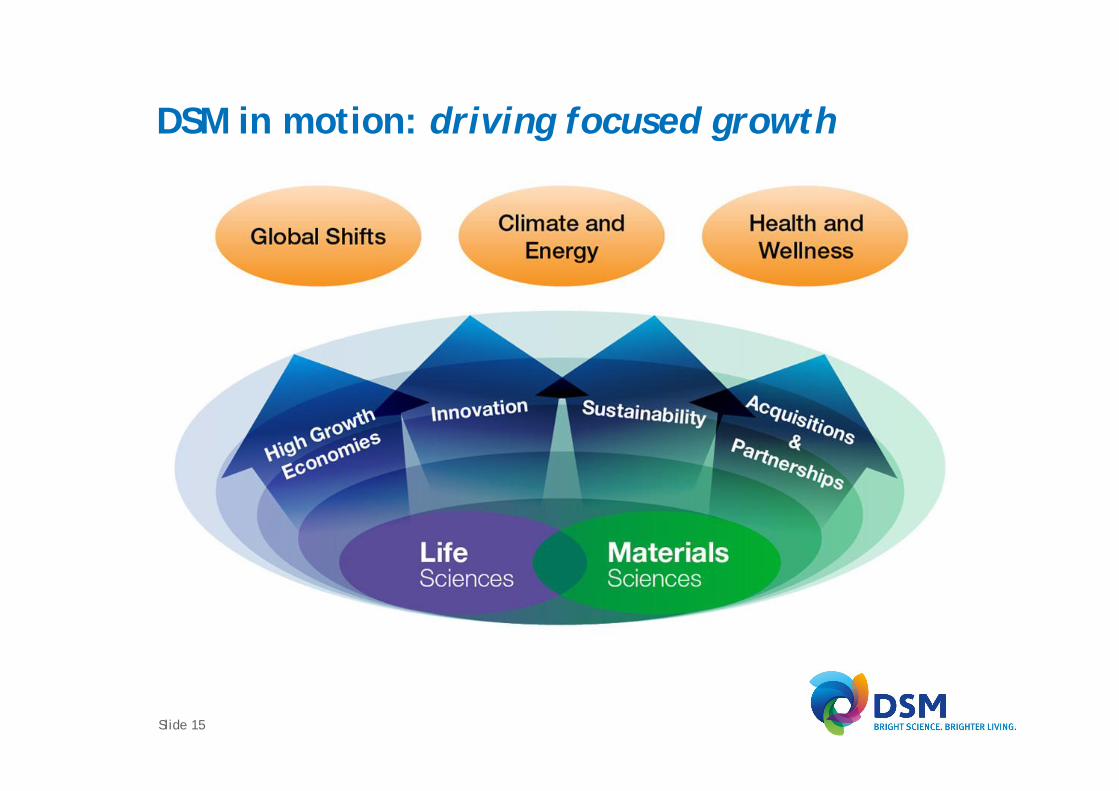

DSM in motion: driving focused growth

SRI roadshow presentation 2012

Safe Harbor Statement

Slide 1

This presentation may contain forward-looking statements with respect to DSM’s future(financial) performance and position. Such statements are based on current

expectations, estimates and projections of DSM and information currently available tothe company. DSM cautions readers that such statements involve certain risks and

uncertainties that are difficult to predict and therefore it should be understood thatmany factors can cause actual performance and position to differ materially from these

statements. DSM has no obligation to update the statements contained in thispresentation, unless required by law.

The English language version of this document is leading.

A more comprehensive discussion of the risk factors affecting DSM’s business can befound in the company’s latest Annual Report, which can be found on

the company's corporate website, www.dsm.com

Overview

• Global trends drive sustainability• Strategic progress• Sustainability achievements• Annexes

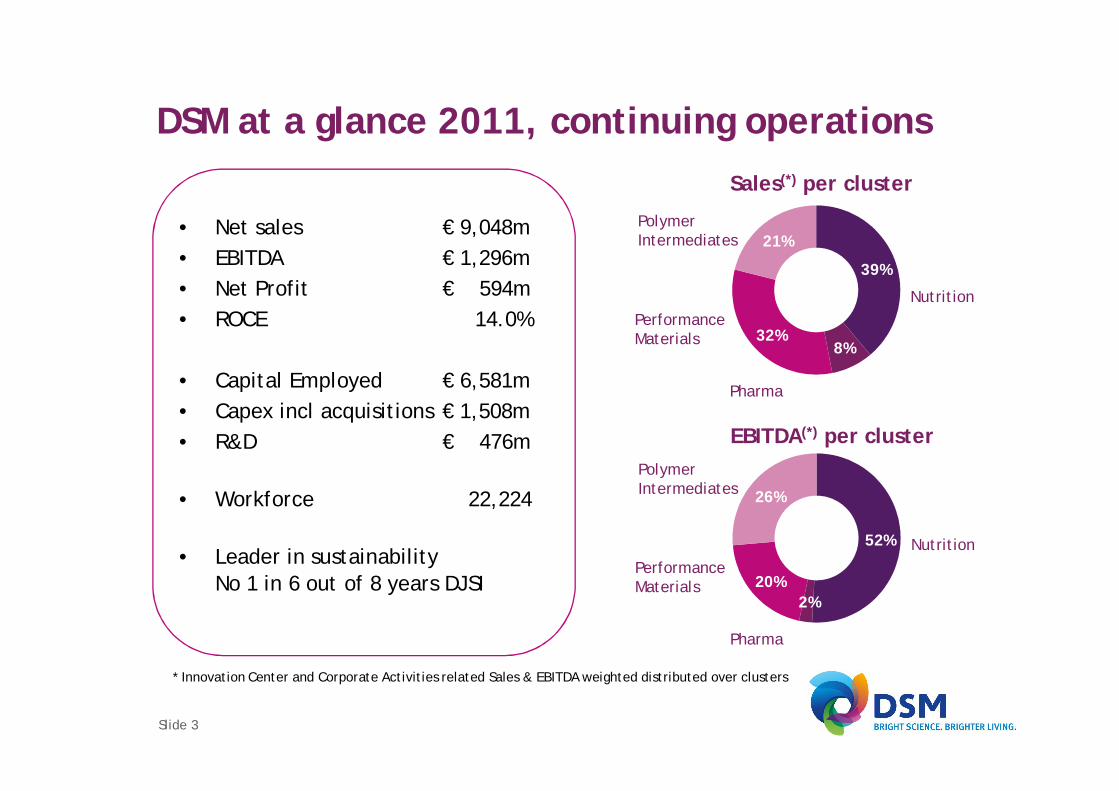

DSM at a glance 2011, continuing operations

• Net sales € 9,048m• EBITDA € 1,296m• Net Profit € 594m• ROCE 14.0%

• Capital Employed € 6,581m• Capex incl acquisitions € 1,508m• R&D € 476m

• Workforce 22,224

• Leader in sustainabilityNo 1 in 6 out of 8 years DJSI

39%

8%32%

21%

Nutrition

Pharma

PolymerIntermediates

PerformanceMaterials

Sales(*) per cluster

52%

2%20%

26%

Nutrition

Pharma

PolymerIntermediates

PerformanceMaterials

EBITDA(*) per cluster

* Innovation Center and Corporate Activities related Sales & EBITDA weighted distributed over clusters

Slide 3

MaterialsNutrition

Unique business positions of DSM

• Global leader in nutritional ingredients for feed, food and personal care

• Market leader in anti-infectives and key custom manufacturing player

• Market leader in sustainable high performance materials

• Merchant market leader in nylon precursor caprolactam

• Innovator active in advanced biofuels, biochemicals and biomedical materials

Health

Slide 4

5

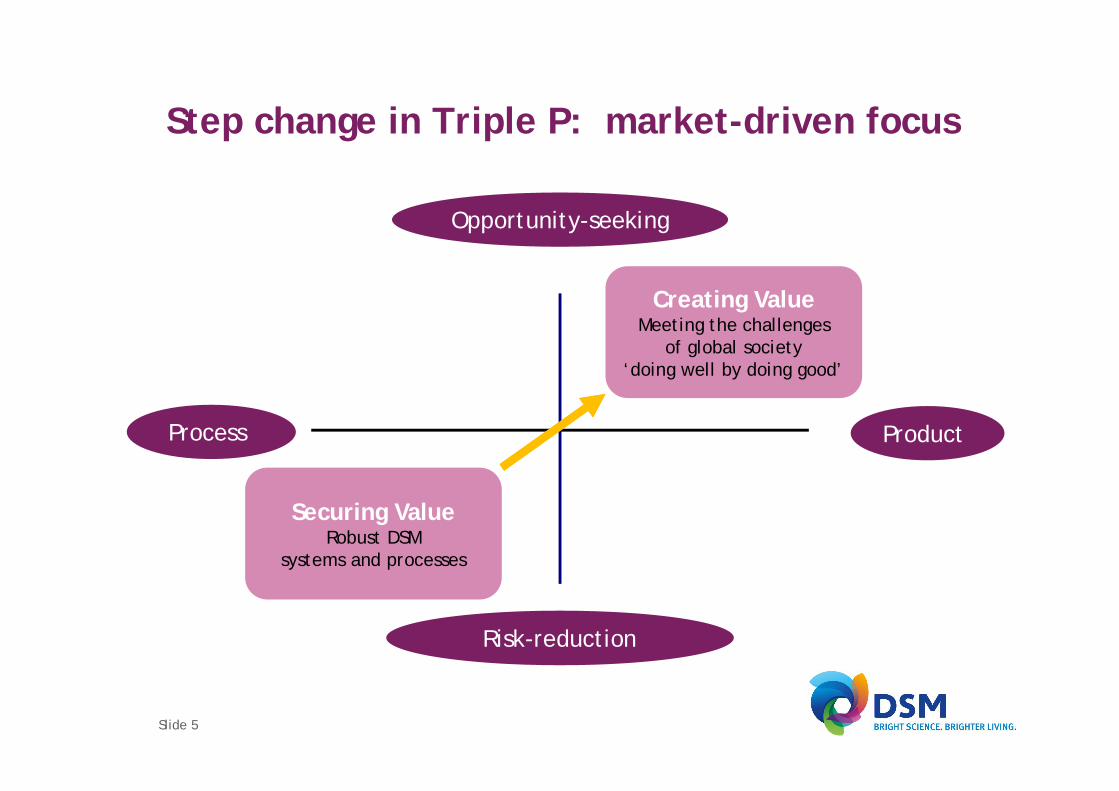

Step change in Triple P: market-driven focus

Opportunity-seeking

Risk-reduction

Process Product

Creating ValueMeeting the challenges

of global society‘doing well by doing good’

Securing ValueRobust DSM

systems and processes

Slide 5

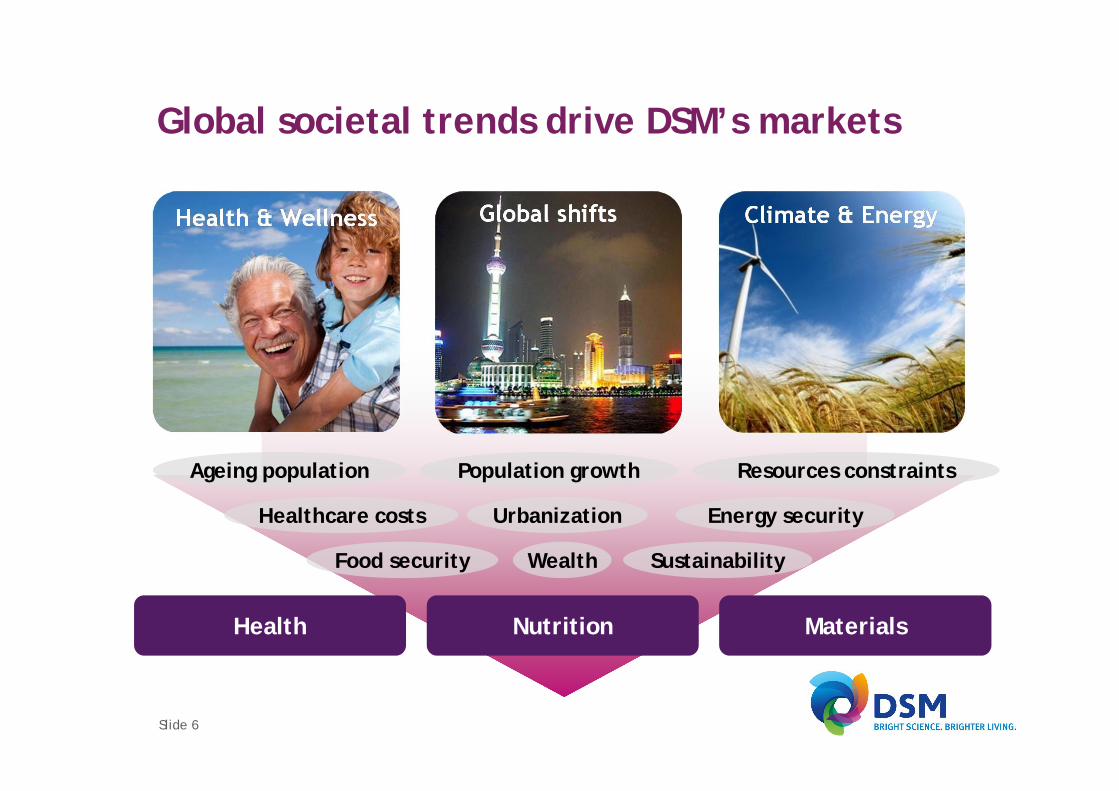

Global societal trends drive DSM’s markets

Population growth

Wealth

Resources constraints

Sustainability

UrbanizationHealthcare costs Energy security

Food security

Ageing population

MaterialsNutritionHealth

Slide 6

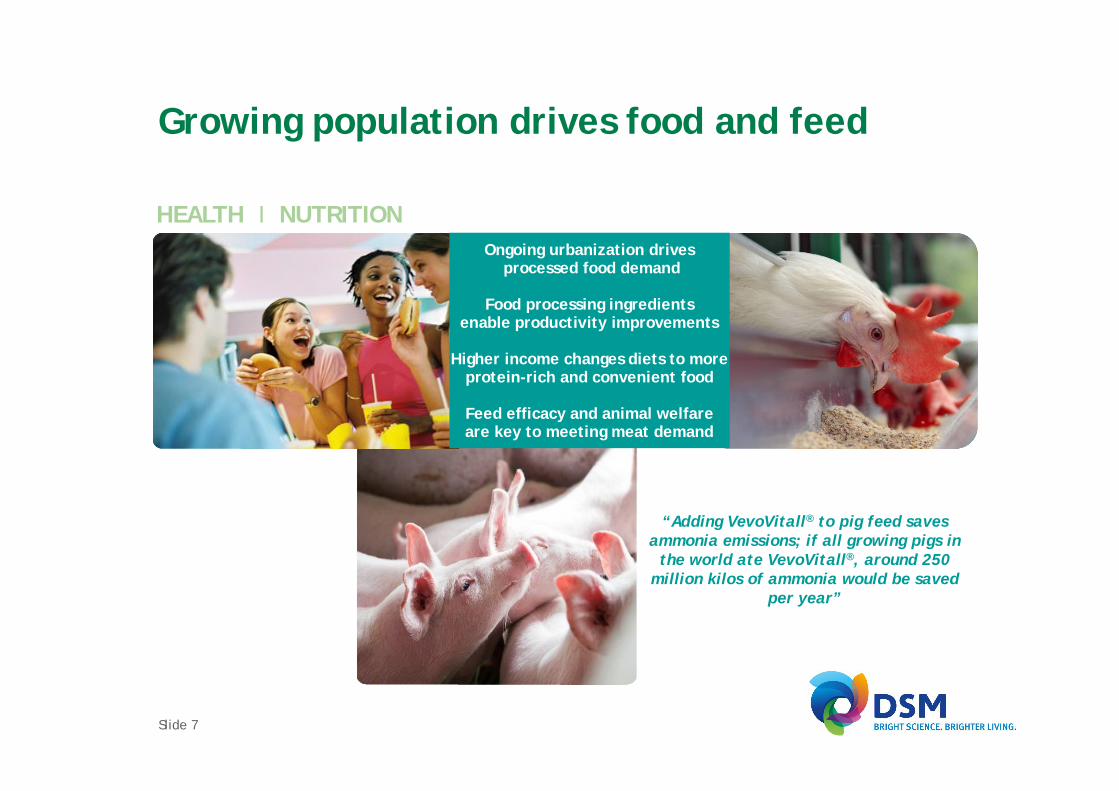

Ongoing urbanization drivesprocessed food demand

Food processing ingredientsenable productivity improvements

Higher income changes diets to moreprotein-rich and convenient food

Feed efficacy and animal welfareare key to meeting meat demand

Growing population drives food and feed

“Adding VevoVitall® to pig feed savesammonia emissions; if all growing pigs in

the world ate VevoVitall®, around 250million kilos of ammonia would be saved

per year”

HEALTH I NUTRITION

Slide 7

Increased awareness onnutrition for health

Health benefits throughsupplements & fortification

Nutritional ingredientsdifferentiate products

WFP partnership:Healthy nutrition for all

HEALTH I NUTRITION

Micronutrients are key drivers nutrition & health

“Every day, half a billion peopletake DSM vitamins;

but there are still 6.5 billionwho never take any.”

Slide 8

HEALTH I MATERIALS

Aging population wants to stayhealthy and active

“Every year DSMproduces antibiotics

to cure600 million people.”

“There are over 6 millionpeople who haveDyneema® Purity

in their body.”

Increased healthcare costdrives demand forlower cost generics

Focus on health throughfood and supplements

Active lifestyle requiresmaterials for replacement

of body parts

Slide 9

HEALTH I NUTRITION I MATERIALS

Protection and health for all

“20-50 percent of theworld’s harvest

currently goes to waste.”

“Food safety is key.Contamination with bacteria / viruses,

can result in illness ….and sometimes worse.”

Protection for peopleand food

Drive towardhealthier products

Legislation drives shift tosustainable coatings

Green image key for brandvalue in electronics

Slide 10

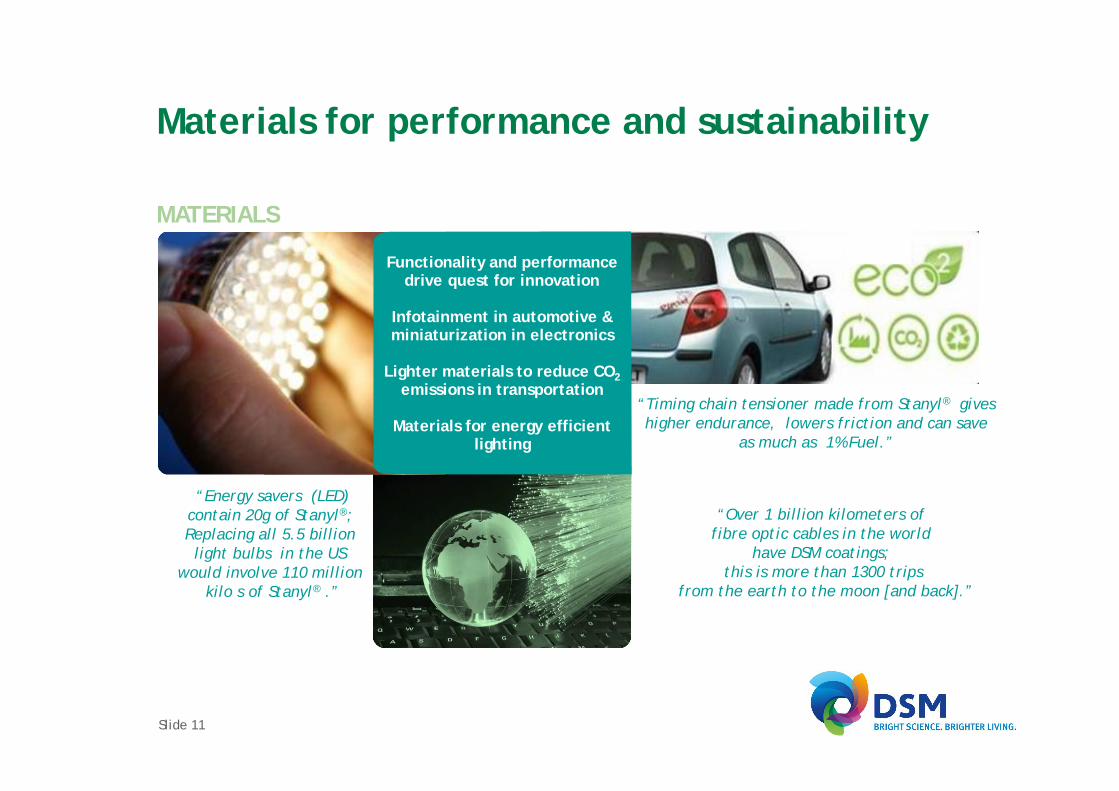

MATERIALS

Materials for performance and sustainability

“Energy savers (LED)contain 20g of Stanyl®;Replacing all 5.5 billionlight bulbs in the US

would involve 110 millionkilo s of Stanyl® .”

“Timing chain tensioner made from Stanyl® giveshigher endurance, lowers friction and can save

as much as 1% Fuel.”

“Over 1 billion kilometers offibre optic cables in the world

have DSM coatings;this is more than 1300 trips

from the earth to the moon [and back].”

Functionality and performancedrive quest for innovation

Infotainment in automotive &miniaturization in electronics

Lighter materials to reduce CO2emissions in transportation

Materials for energy efficientlighting

Slide 11

LIFE SCIENCES & MATERIALS SCIENCES

Renewables, enabling the bio-based economy

“Nature takes 10,000 years to turn plant material intofuels. DSM can do that in a week.”

Energy and resourcessecurity requiresrenewable energy

Renewable energy fromresidues & waste (biofuel,

biogas), sun and wind

Demand for ‘greener’products

Bio-based alternatives tooil-based products

“It can be calculated that by 2022 ~ 150-200 plantsto produce cellulosic bio-ethanol

from corn crop residue could be required in the US.”

Slide 12

Overview

• Global trends drive sustainability• Strategic progress• Sustainability achievements• Annexes

Bright Science.BrighterLiving.TM creating value for

CUSTOMERS EMPLOYEES

SHAREHOLDERS

Meeting consumerdemands, becomingsupplier of choice

Engaged, motivatedand talented team

Delivering sustainablevalue creation

Innovations addressing:Global Shifts

Health & WellnessClimate & Energy

SOCIETY

Slide 14

DSM in motion: driving focused growth

Slide 15

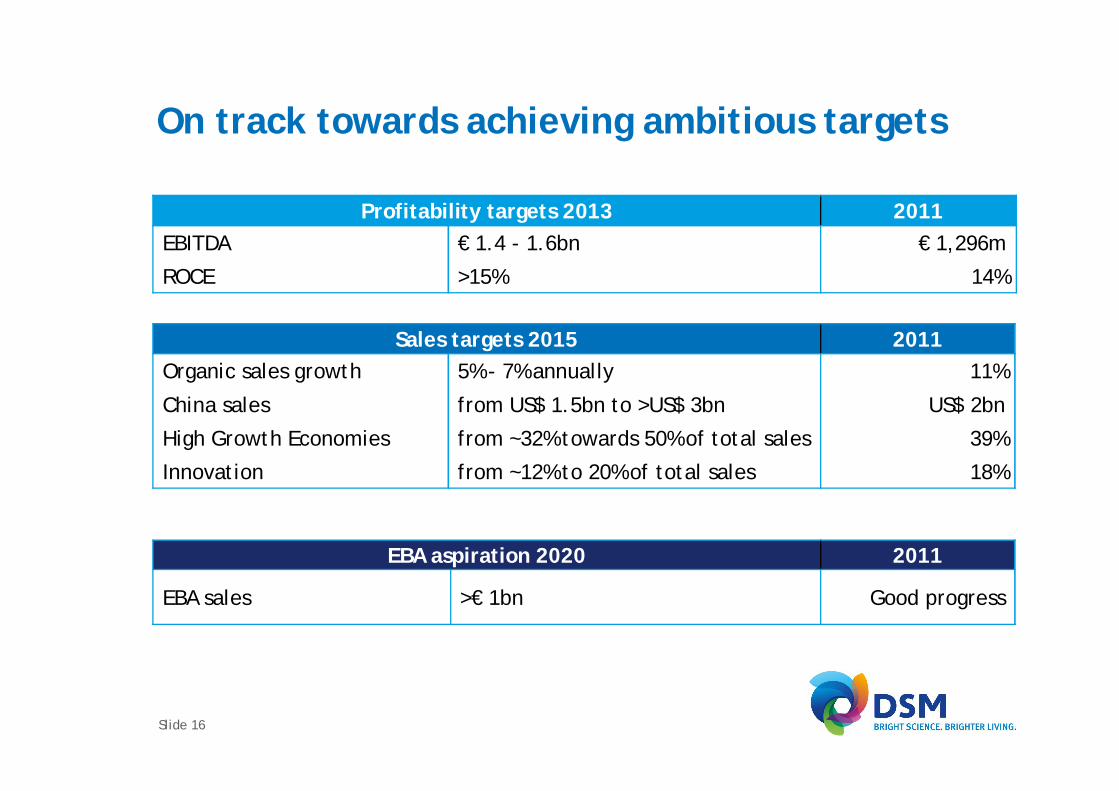

On track towards achieving ambitious targets

Profitability targets 2013 2011EBITDA € 1.4 - 1.6bn € 1,296m

ROCE >15% 14%

Sales targets 2015 2011Organic sales growth 5% - 7% annually 11%

China sales from US$ 1.5bn to >US$ 3bn US$ 2bn

High Growth Economies from ~32% towards 50% of total sales 39%

Innovation from ~12% to 20% of total sales 18%

EBA aspiration 2020 2011

EBA sales >€ 1bn Good progress

Slide 16

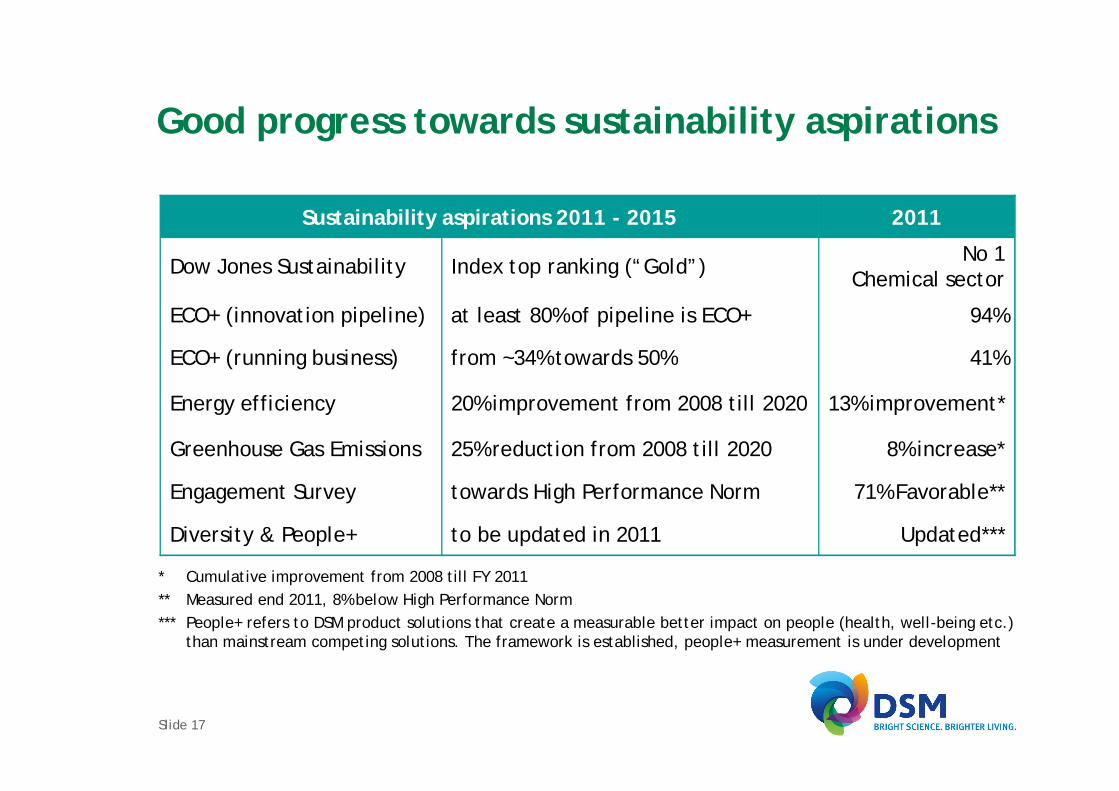

Good progress towards sustainability aspirations

Sustainability aspirations 2011 - 2015 2011

Dow Jones Sustainability Index top ranking (“Gold”) No 1Chemical sector

ECO+ (innovation pipeline) at least 80% of pipeline is ECO+ 94%

ECO+ (running business) from ~34% towards 50% 41%

Energy efficiency 20% improvement from 2008 till 2020 13% improvement*

Greenhouse Gas Emissions 25% reduction from 2008 till 2020 8% increase*

Engagement Survey towards High Performance Norm 71% Favorable**

Diversity & People+ to be updated in 2011 Updated***

* Cumulative improvement from 2008 till FY 2011** Measured end 2011, 8% below High Performance Norm*** People+ refers to DSM product solutions that create a measurable better impact on people (health, well-being etc.)

than mainstream competing solutions. The framework is established, people+ measurement is under development

Slide 17

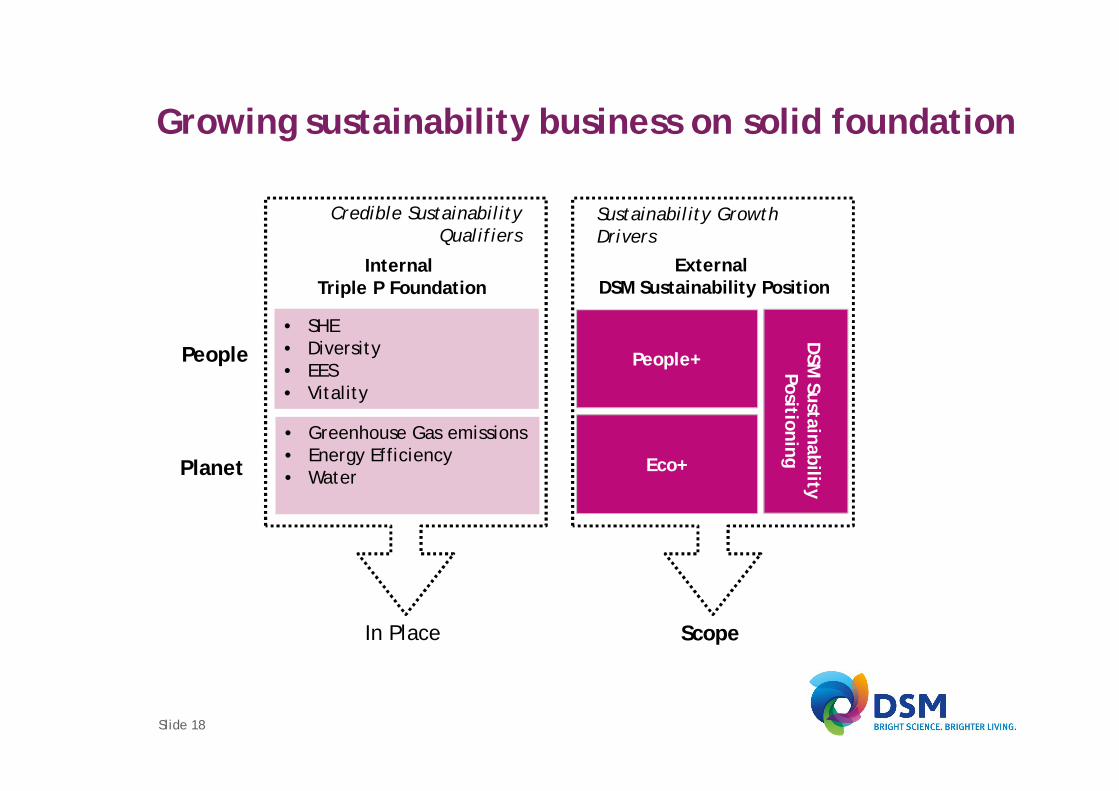

• Greenhouse Gas emissions• Energy Efficiency• Water

• SHE• Diversity• EES• Vitality

Planet

People

InternalTriple P Foundation

ExternalDSM Sustainability Position

Credible SustainabilityQualifiers

Sustainability GrowthDrivers

In Place Scope

DSM

SustainabilityPositioning

People+

Eco+

Growing sustainability business on solid foundation

Slide 18

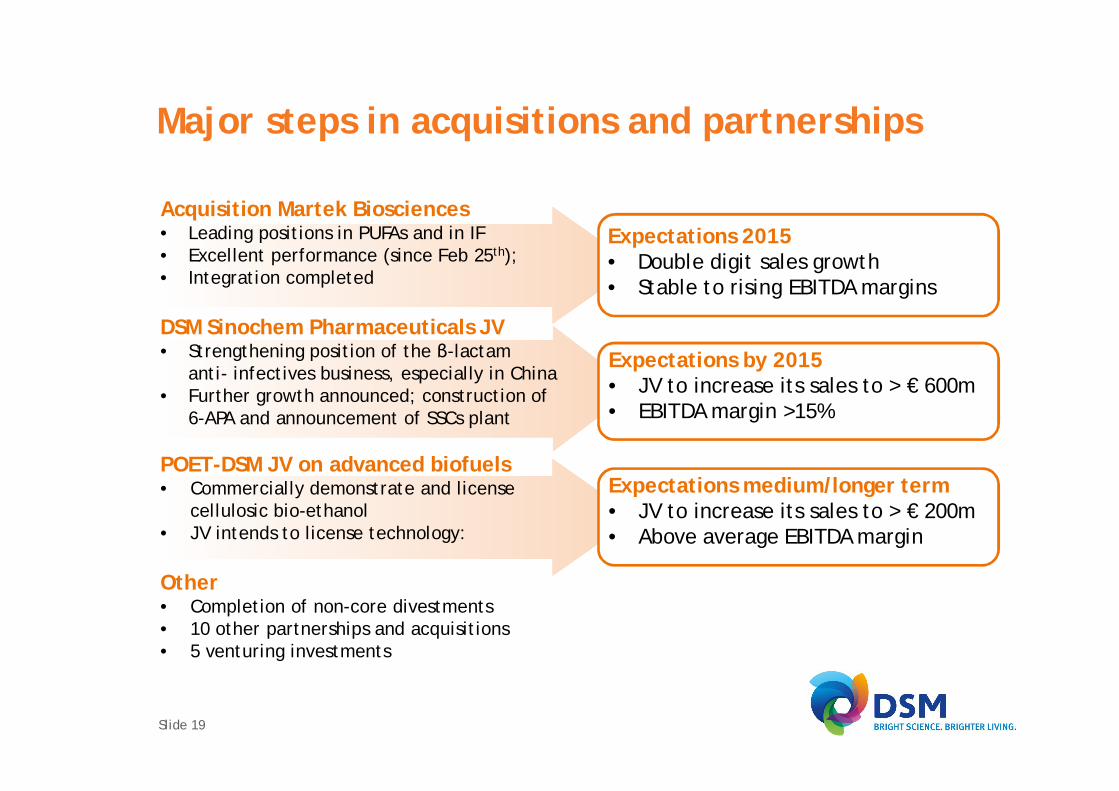

Major steps in acquisitions and partnerships

Slide 19

Acquisition Martek Biosciences• Leading positions in PUFAs and in IF• Excellent performance (since Feb 25th);• Integration completed

DSM Sinochem Pharmaceuticals JV• Strengthening position of the -lactam

anti- infectives business, especially in China• Further growth announced; construction of

6-APA and announcement of SSCs plant

POET-DSM JV on advanced biofuels• Commercially demonstrate and license

cellulosic bio-ethanol• JV intends to license technology:

Other• Completion of non-core divestments• 10 other partnerships and acquisitions• 5 venturing investments

Expectations by 2015• JV to increase its sales to > € 600m• EBITDA margin >15%

Expectations 2015• Double digit sales growth• Stable to rising EBITDA margins

Expectations medium/longer term• JV to increase its sales to > € 200m• Above average EBITDA margin

0.0

1.5

3.0

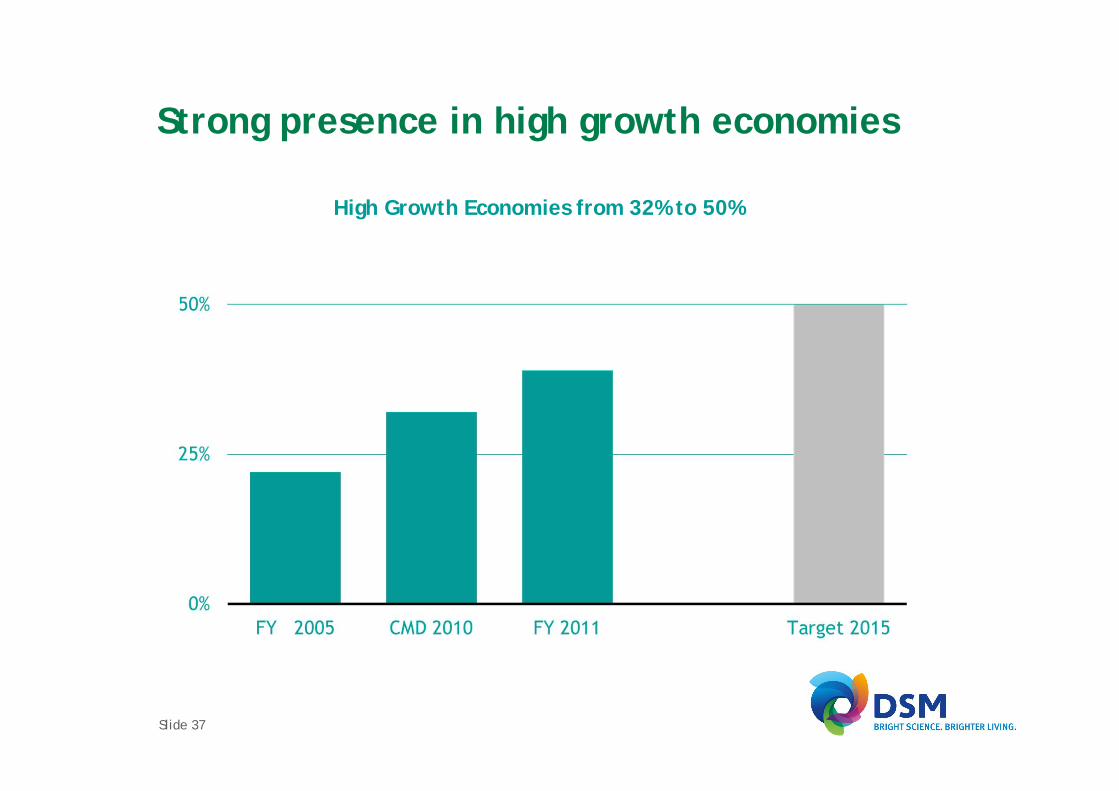

2005 CMD 2010 FY 2011 Target2015

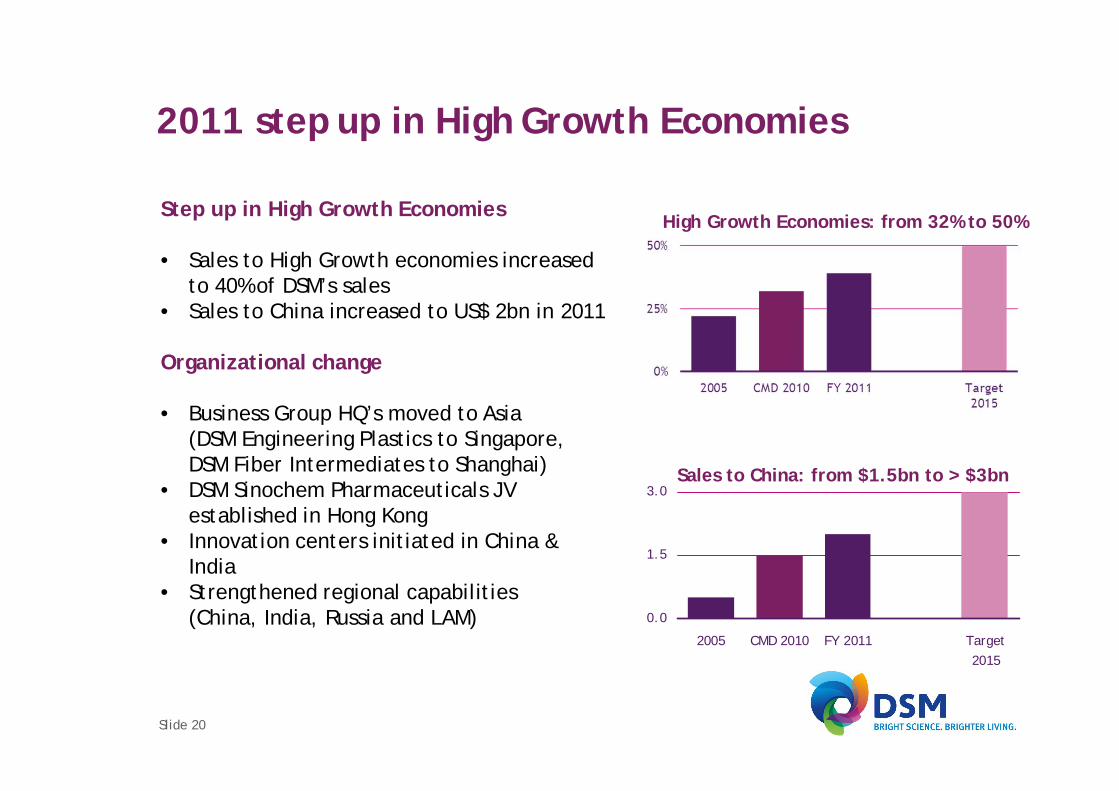

High Growth Economies: from 32% to 50%Step up in High Growth Economies

• Sales to High Growth economies increasedto 40% of DSM’s sales

• Sales to China increased to US$ 2bn in 2011

Organizational change

• Business Group HQ’s moved to Asia(DSM Engineering Plastics to Singapore,DSM Fiber Intermediates to Shanghai)

• DSM Sinochem Pharmaceuticals JVestablished in Hong Kong

• Innovation centers initiated in China &India

• Strengthened regional capabilities(China, India, Russia and LAM)

2011 step up in High Growth Economies

Sales to China: from $1.5bn to > $3bn

Slide 20

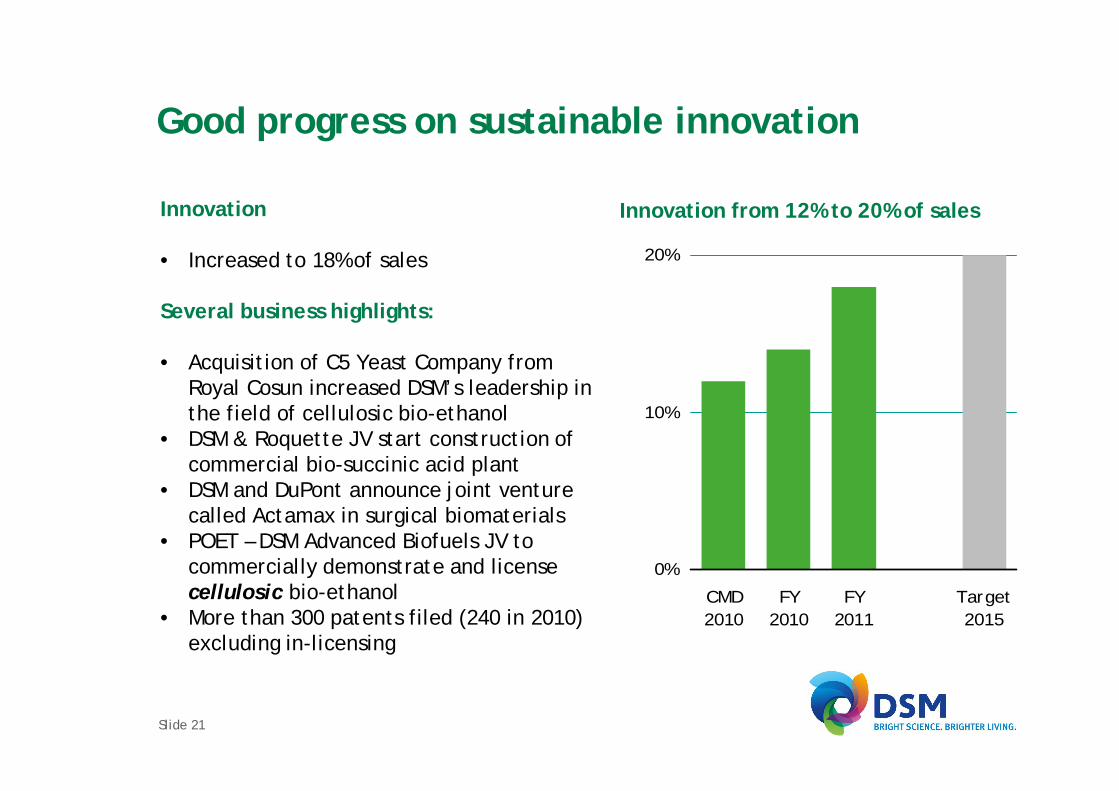

Innovation from 12% to 20% of sales

0%

10%

20%

CMD2010

FY2010

FY2011

Target2015

Innovation

• Increased to 18% of sales

Several business highlights:

• Acquisition of C5 Yeast Company fromRoyal Cosun increased DSM’s leadership inthe field of cellulosic bio-ethanol

• DSM & Roquette JV start construction ofcommercial bio-succinic acid plant

• DSM and DuPont announce joint venturecalled Actamax in surgical biomaterials

• POET – DSM Advanced Biofuels JV tocommercially demonstrate and licensecellulosic bio-ethanol

• More than 300 patents filed (240 in 2010)excluding in-licensing

Good progress on sustainable innovation

Slide 21

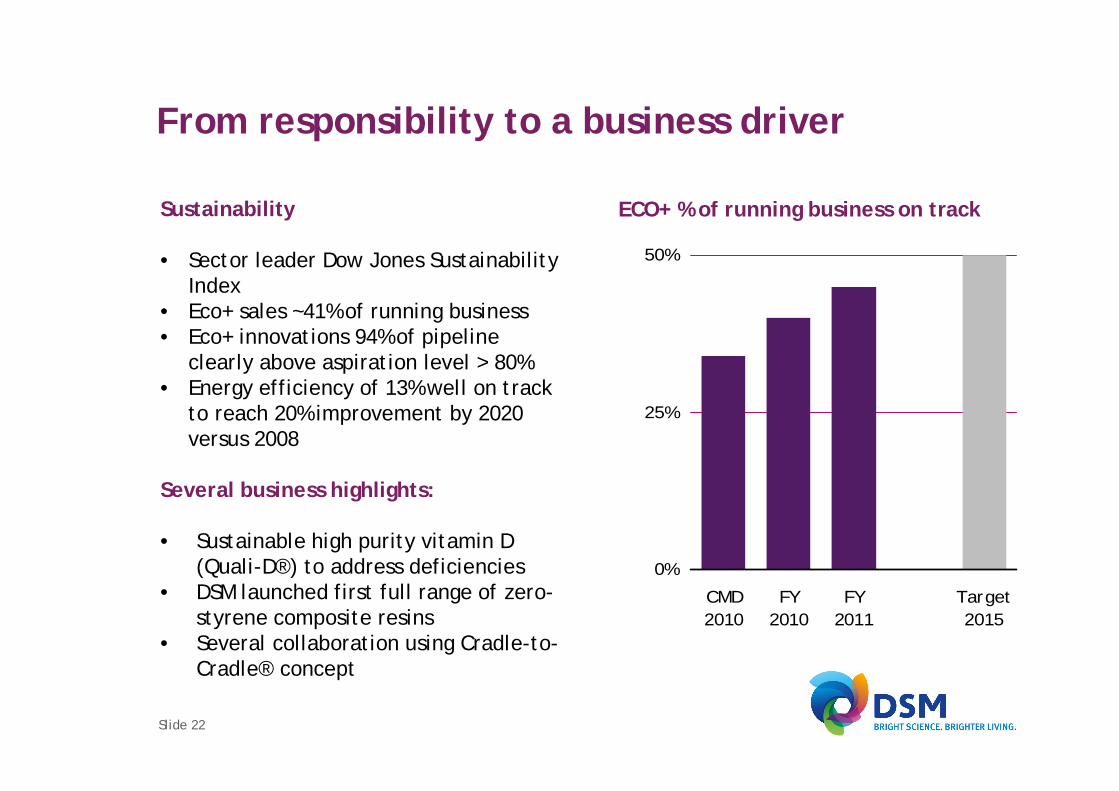

Sustainability

• Sector leader Dow Jones SustainabilityIndex

• Eco+ sales ~41% of running business• Eco+ innovations 94% of pipeline

clearly above aspiration level > 80%• Energy efficiency of 13% well on track

to reach 20% improvement by 2020versus 2008

Several business highlights:

• Sustainable high purity vitamin D(Quali-D®) to address deficiencies

• DSM launched first full range of zero-styrene composite resins

• Several collaboration using Cradle-to-Cradle® concept

0%

25%

50%

CMD2010

FY2010

FY2011

Target2015

ECO+ % of running business on track

From responsibility to a business driver

Slide 22

Overview

• Global trends drive sustainability• Strategic progress• Sustainability achievements• Annexes

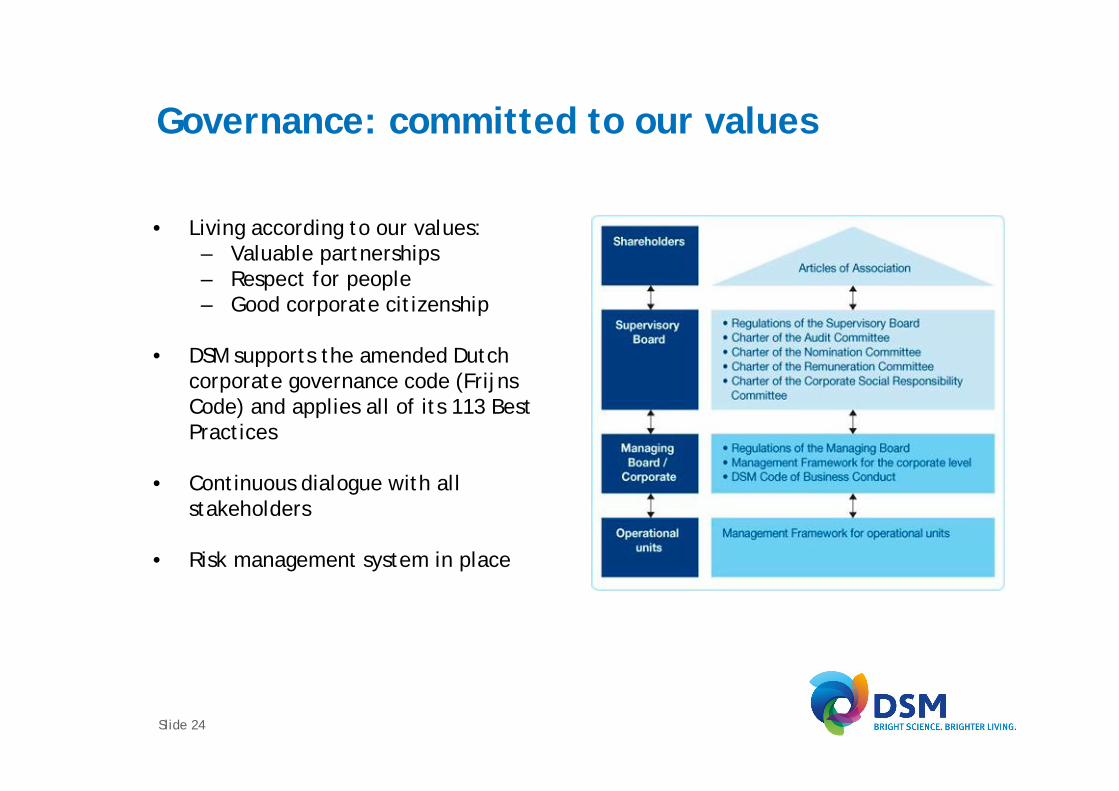

Governance: committed to our values

• Living according to our values:– Valuable partnerships– Respect for people– Good corporate citizenship

• DSM supports the amended Dutchcorporate governance code (FrijnsCode) and applies all of its 113 BestPractices

• Continuous dialogue with allstakeholders

• Risk management system in place

Slide 24

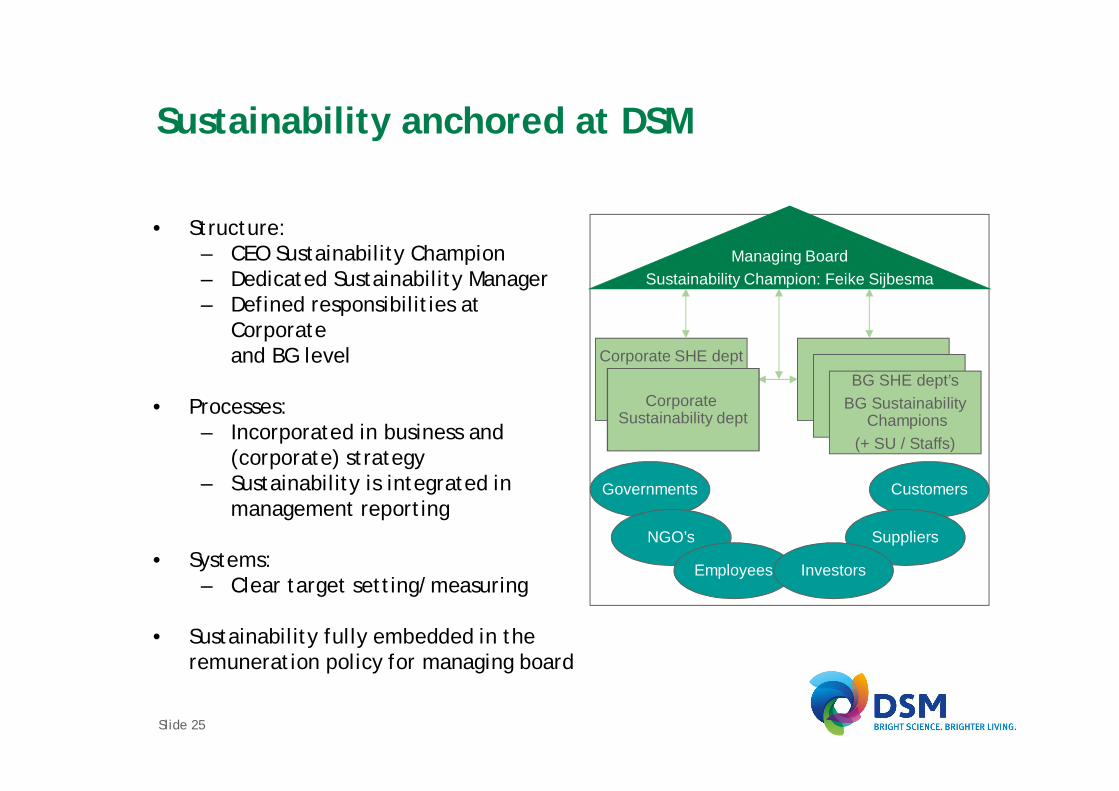

Corporate SHE dept

Managing BoardSustainability Champion: Feike Sijbesma

BG SHE dept’sBG Sustainability

Champions(+ SU / Staffs)

Governments

NGO’s

Employees

Customers

Suppliers

Investors

CorporateSustainability dept

Sustainability anchored at DSM

• Structure:– CEO Sustainability Champion– Dedicated Sustainability Manager– Defined responsibilities at

Corporateand BG level

• Processes:– Incorporated in business and

(corporate) strategy– Sustainability is integrated in

management reporting

• Systems:– Clear target setting/measuring

• Sustainability fully embedded in theremuneration policy for managing board

Slide 25

Slide 26

• Global high performance organization– Business Groups as building blocks– Strengthened by Regions– Optimized via Shared Services & Functional

Excellence

Collaborating in

‘One DSM’

• Change Themes:– External Orientation– Accountability for Performance– Inspirational Leadership

• Based on joint belief in:– Sustainability & Diversity

Supported byCulture Change program

Next step in organizational development

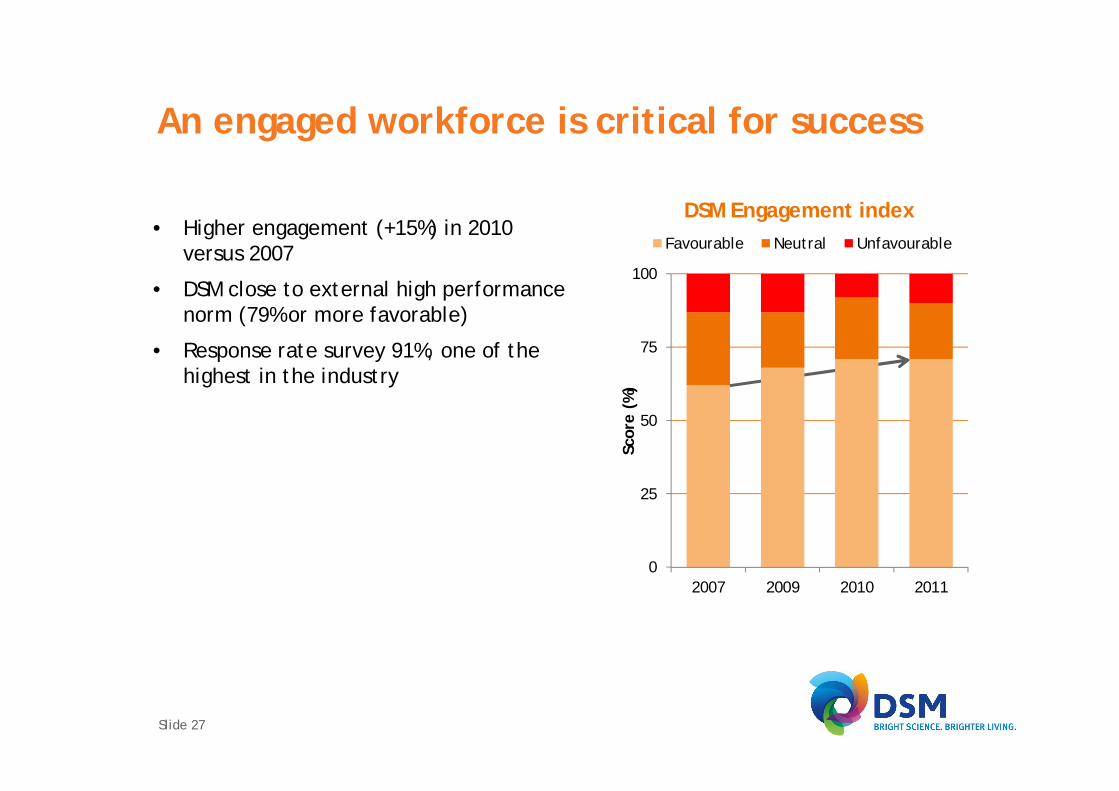

An engaged workforce is critical for success

• Higher engagement (+15%) in 2010versus 2007

• DSM close to external high performancenorm (79% or more favorable)

• Response rate survey 91%, one of thehighest in the industry

Slide 27

DSM Engagement index

0

25

50

75

100

2007 2009 2010 2011

Scor

e (%

)

Favourable Neutral Unfavourable

720 24

820 25

921 26

1021 27

0

25

50

75

100

Executives Management Others

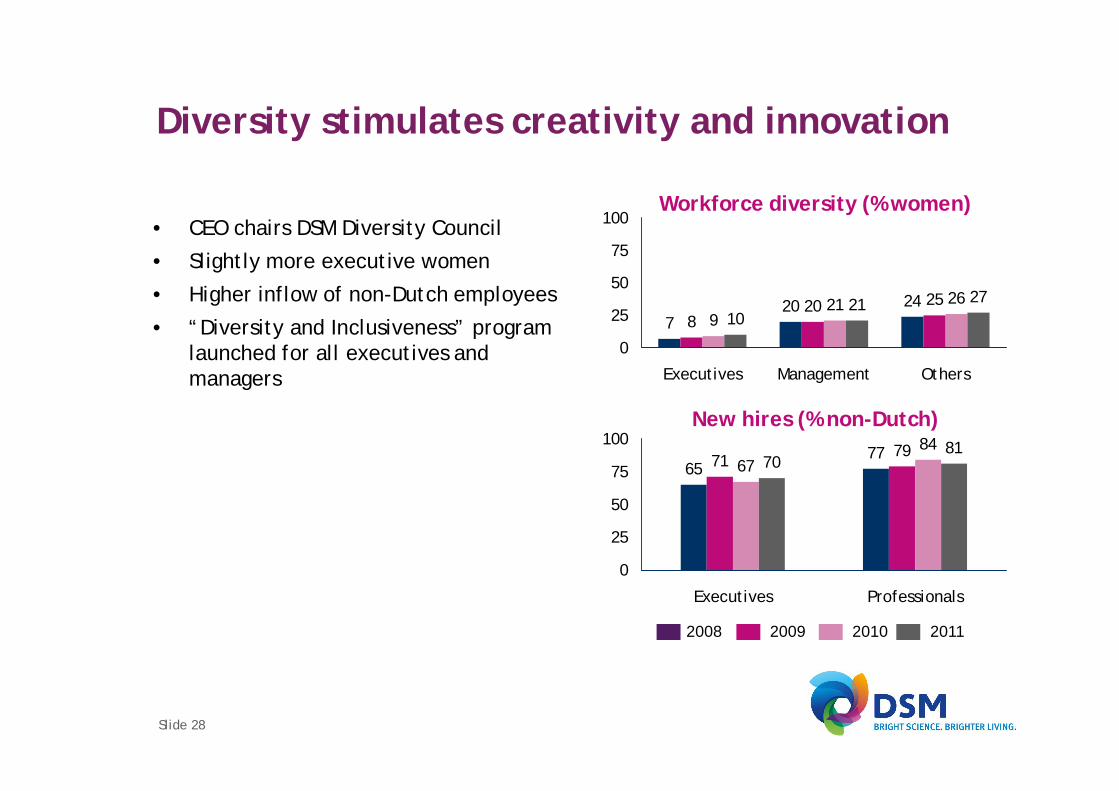

Diversity stimulates creativity and innovation

• CEO chairs DSM Diversity Council

• Slightly more executive women

• Higher inflow of non-Dutch employees

• “Diversity and Inclusiveness” programlaunched for all executives andmanagers

Slide 28

657771

7967

8470

81

0

25

50

75

100

Executives Professionals

Workforce diversity (% women)

New hires (% non-Dutch)

2008 2009 2010 2011

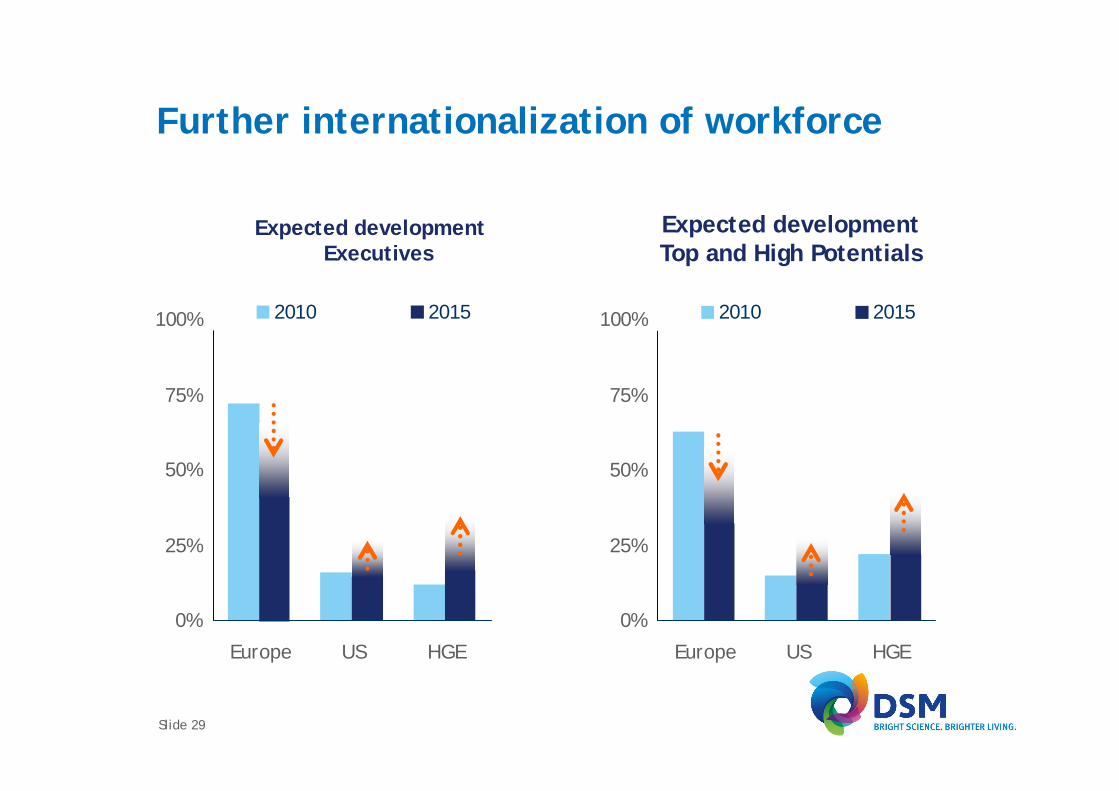

Further internationalization of workforce

Expected developmentExecutives

Expected developmentTop and High Potentials

0%

25%

50%

75%

100%

Europe US HGE

2010 2015

0%

25%

50%

75%

100%

Europe US HGE

2010 2015

Slide 29

Slide 30

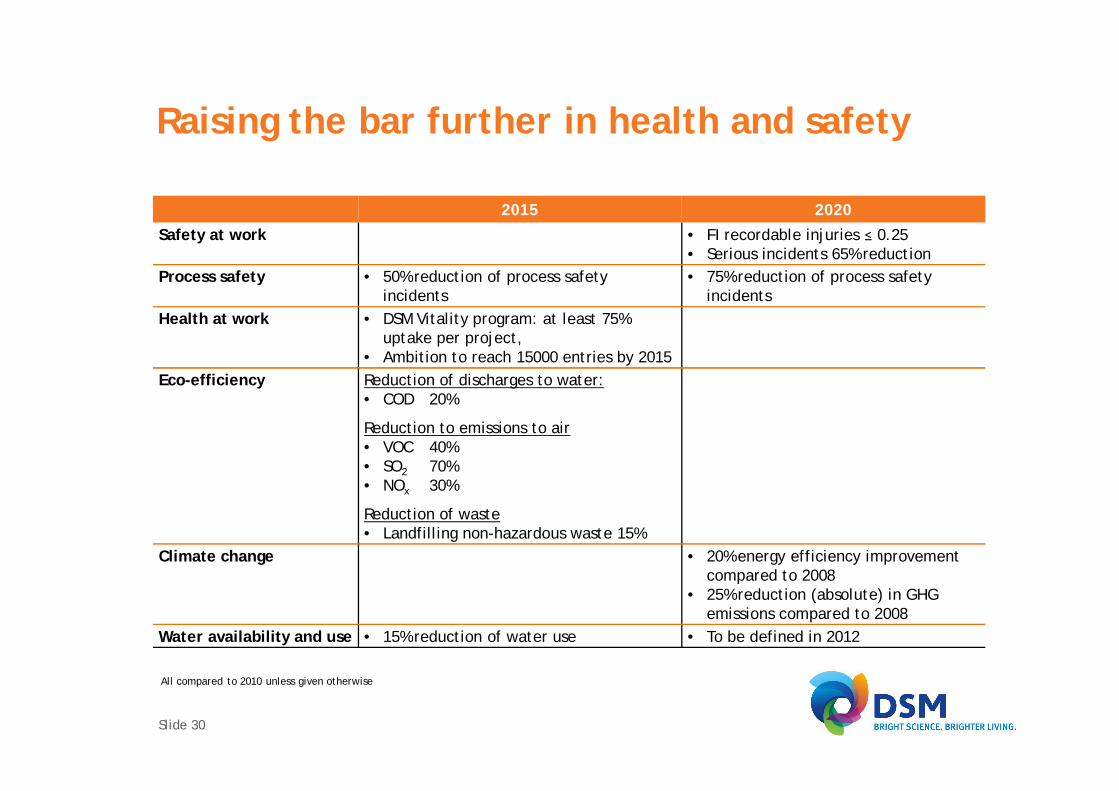

Raising the bar further in health and safety

2015 2020Safety at work • FI recordable injuries 0.25

• Serious incidents 65% reductionProcess safety • 50% reduction of process safety

incidents• 75% reduction of process safety

incidentsHealth at work • DSM Vitality program: at least 75%

uptake per project,• Ambition to reach 15000 entries by 2015

Eco-efficiency Reduction of discharges to water:• COD 20%

Reduction to emissions to air• VOC 40%• SO2 70%• NOx 30%

Reduction of waste• Landfilling non-hazardous waste 15%

Climate change • 20% energy efficiency improvementcompared to 2008

• 25% reduction (absolute) in GHGemissions compared to 2008

Water availability and use • 15% reduction of water use • To be defined in 2012

All compared to 2010 unless given otherwise

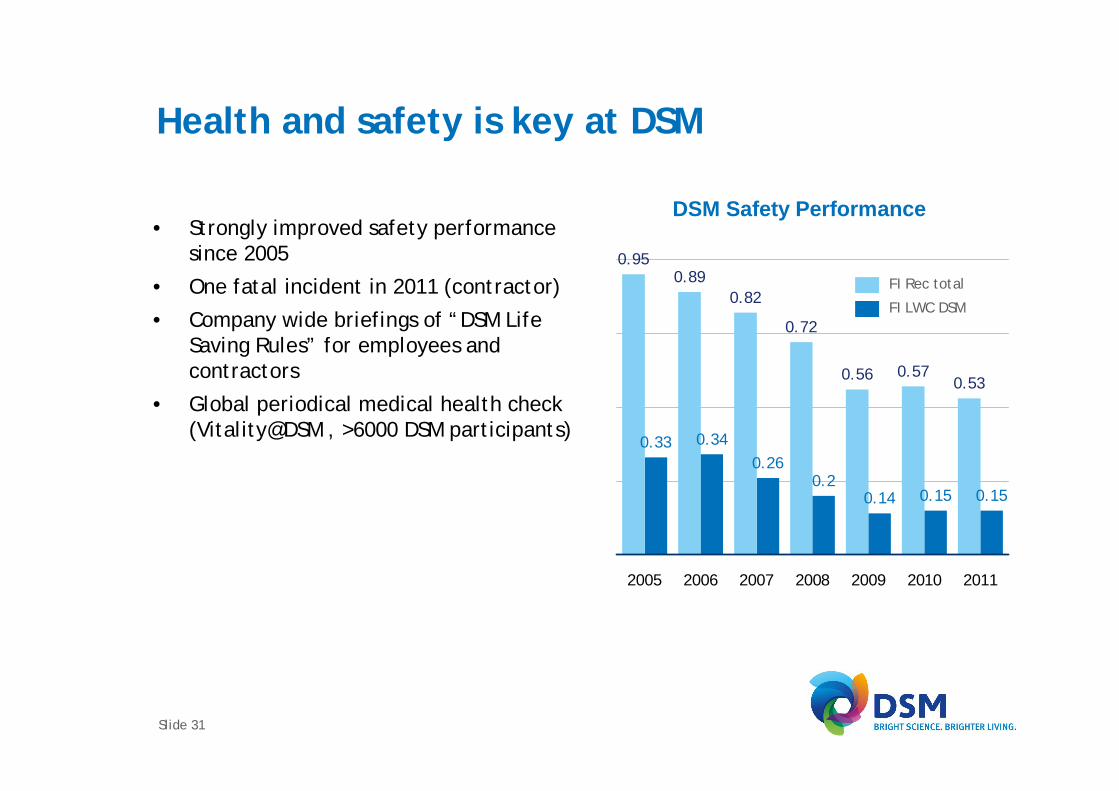

0.950.89

0.82

0.72

0.56 0.570.53

0.33 0.340.26

0.20.14 0.15 0.15

2005 2006 2007 2008 2009 2010 2011

Slide 31

Health and safety is key at DSM

• Strongly improved safety performancesince 2005

• One fatal incident in 2011 (contractor)

• Company wide briefings of “DSM LifeSaving Rules” for employees andcontractors

• Global periodical medical health check(Vitality@DSM , >6000 DSM participants)

DSM Safety Performance

FI Rec total

FI LWC DSM

-20% 0% 20% 40% 60% 80%

COD

VOC

SO2

NOx

Landfill NHW

Total water

GHG

Energy Efficiency

Target Actual

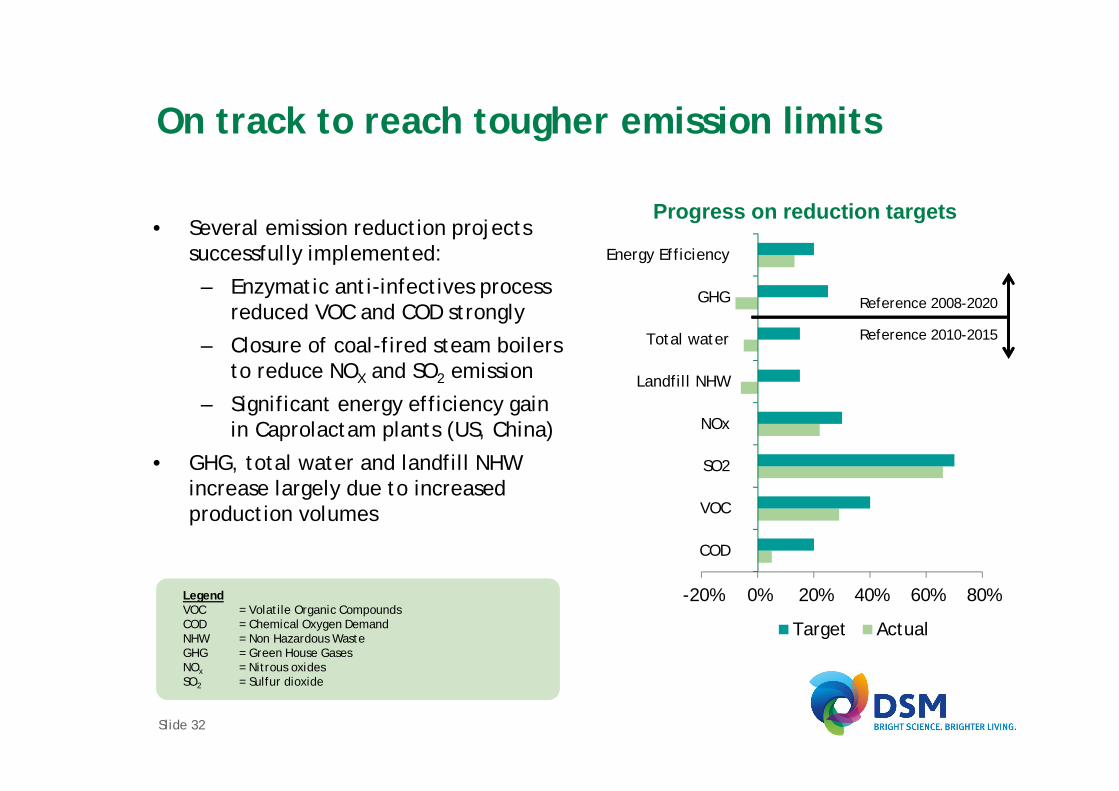

On track to reach tougher emission limits

• Several emission reduction projectssuccessfully implemented:

– Enzymatic anti-infectives processreduced VOC and COD strongly

– Closure of coal-fired steam boilersto reduce NOX and SO2 emission

– Significant energy efficiency gainin Caprolactam plants (US, China)

• GHG, total water and landfill NHWincrease largely due to increasedproduction volumes

Slide 32

Progress on reduction targets

Reference 2008-2020

Reference 2010-2015

LegendVOC = Volatile Organic CompoundsCOD = Chemical Oxygen DemandNHW = Non Hazardous WasteGHG = Green House GasesNOx = Nitrous oxidesSO2 = Sulfur dioxide

Slide 33

External recognition

• 2011: no. 1 in Dow Jones SustainabilityIndex (DSJI) for Chemicals; No. 1 in 6 outof last 8 years

• Listed in the FTSE4Good

• CEO received the United Nations Leadersof Change award in 2011

• CEO received the prestigious GeorgeWashington Carver award at BIO 2011

• CEO was awarded the United NationsHumanitarian of the year Award in 2010

Feike Sijbesma (right) receiving George Carver Award

Overview

• Global trends drive sustainability• Strategic progress• Sustainability achievements• Annexes

Highlights Q4 / FY 2011

DSM reports another strong year and increases dividend

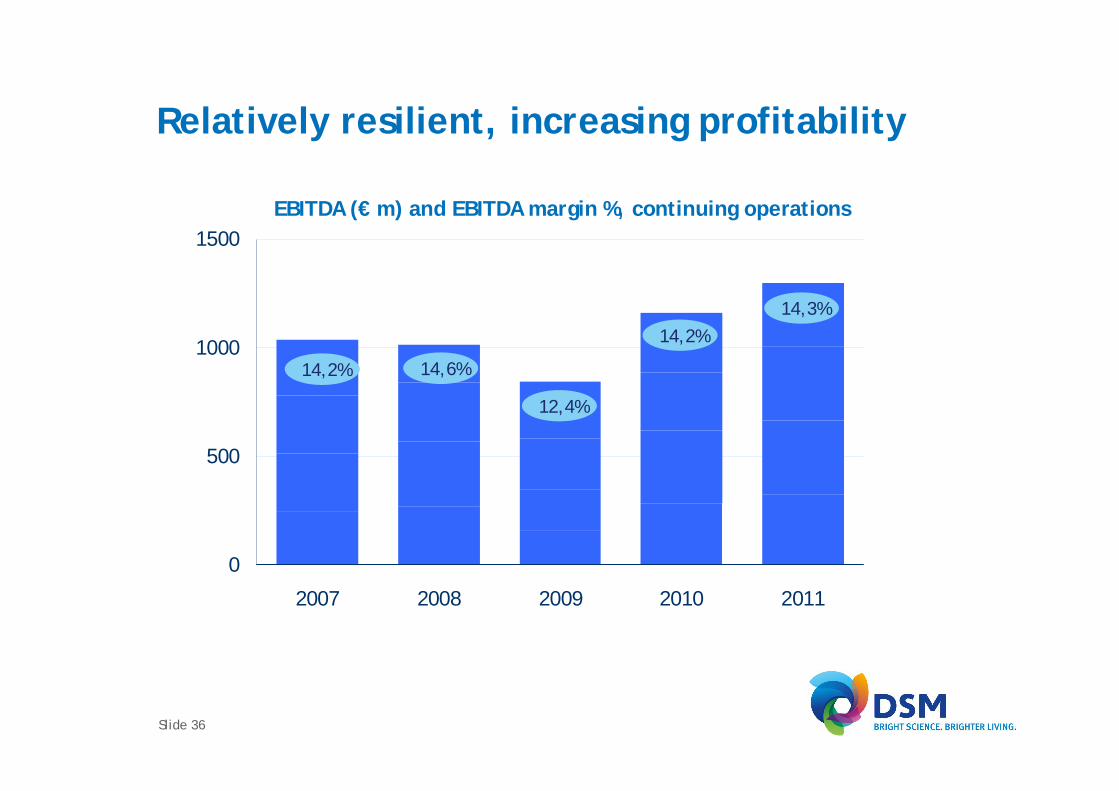

• Q4 EBITDA from continuing operations up 6% to €293 million

• Full year EBITDA from continuing operations increased 12% to €1,296 million

• Life Sciences delivered further EBITDA growth through Nutrition

• Materials Sciences posted a strong year with record Polymer Intermediates results

• Good strategic progress with Martek acquisition and joint venture with Sinochem

• EPS (before exceptional items, continuing operations) up 22% to €3.53

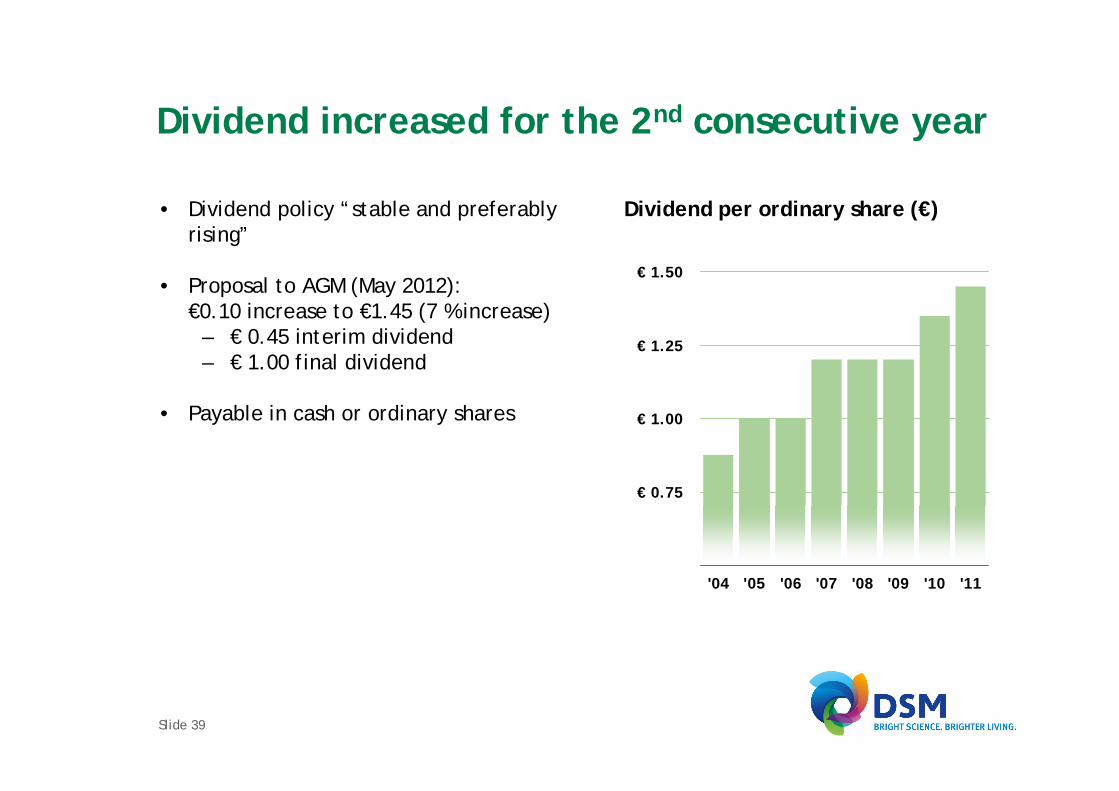

• Dividend increase by €0.10 to €1.45 per ordinary share proposed for 2011

• Cautiously optimistic outlook; on the way to achieve 2013 targets

Slide 35

Relatively resilient, increasing profitability

0

500

1000

1500

2007 2008 2009 2010 2011

EBITDA (€ m) and EBITDA margin %, continuing operations

14,2% 14,6%

12,4%

14,2%14,3%

Slide 36

Strong presence in high growth economies

High Growth Economies from 32% to 50%

Slide 37

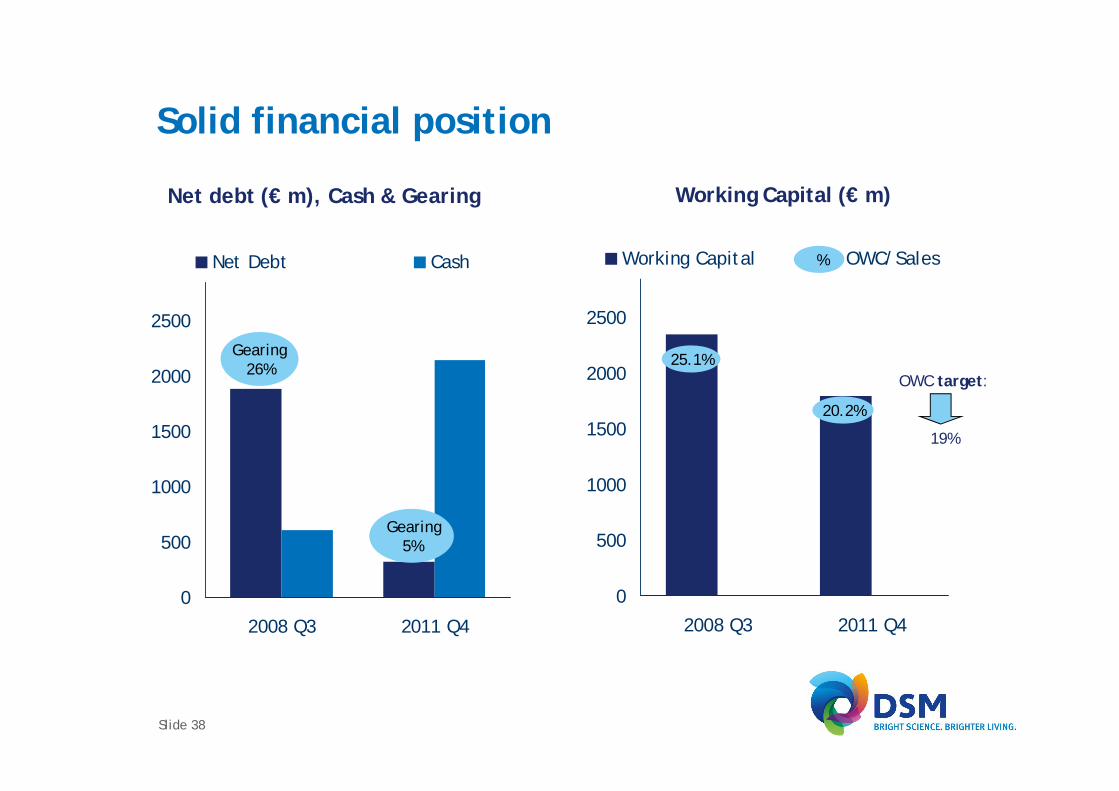

Solid financial position

0

500

1000

1500

2000

2500

3000

2008 Q3 2011 Q4

Net Debt Cash

Net debt (€ m), Cash & Gearing Working Capital (€ m)

Gearing26%

Gearing5%

0

500

1000

1500

2000

2500

3000

2008 Q3 2011 Q4

Working Capital OWC/Sales

20.2%

%

25.1%OWC target:

19%

Slide 38

Dividend increased for the 2nd consecutive year

€ 0.50

€ 0.75

€ 1.00

€ 1.25

€ 1.50

'04 '05 '06 '07 '08 '09 '10 '11

Dividend per ordinary share (€)• Dividend policy “stable and preferablyrising”

• Proposal to AGM (May 2012):€0.10 increase to €1.45 (7 % increase)

– € 0.45 interim dividend– € 1.00 final dividend

• Payable in cash or ordinary shares

Slide 39

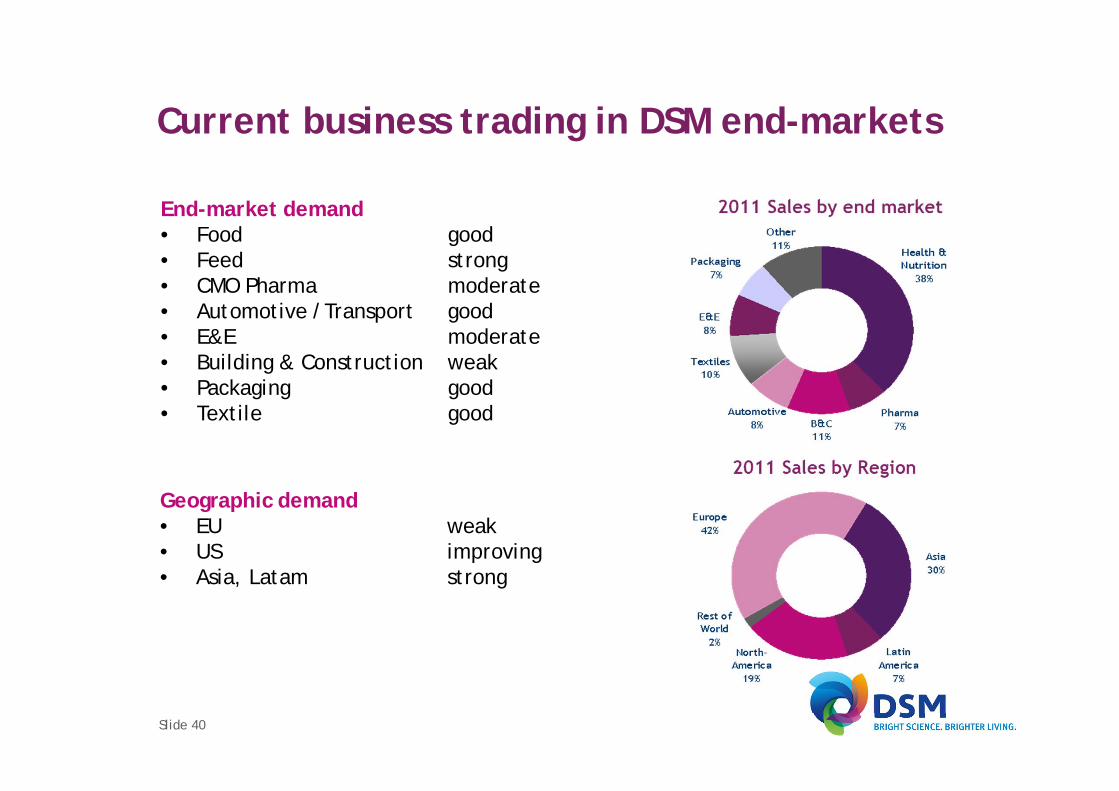

Current business trading in DSM end-markets

End-market demand• Food good• Feed strong• CMO Pharma moderate• Automotive /Transport good• E&E moderate• Building & Construction weak• Packaging good• Textile good

Geographic demand• EU weak• US improving• Asia, Latam strong

Slide 40

Outlook

• Cautiously optimistic outlook.

• In Nutrition EBITDA is expected to be above 2011.

• EBITDA in Pharma is expected to improve slightly compared to 2011, despitethe impact of the 50% deconsolidation of the anti-infectives business.

• Based on current insights EBITDA of the Performance Materials cluster isexpected to be somewhat higher than in 2011.

• For Polymer Intermediates another strong year is expected, at a level abovethe historical average, but the EBITDA will be clearly lower than theexceptional result in 2011.

• DSM expects the second half of 2012 to be stronger than the first half of 2012.

• DSM on its way to achieve 2013 targets.

Slide 41

Wrap up

• 2011 another strong year for DSM

• Good strategic progress• Martek acquisition (poly-unsaturated fatty acids)• JV with DSM Sinochem Pharmaceuticals (anti-infectives)• JV with POET to make advanced biofuels a reality

• DSM is well placed in current macro-economic environment• Relatively resilient portfolio,• Strong presence in High Growth Economies• Strong balance sheet

• Cautiously optimistic outlook, DSM on its way to achieve 2013 targets

Slide 42

Overview

• Global trends drive sustainability• DSM in motion: driving focused growth• People, planet and profit achievements• Annex:

• Highlights Results FY 2011• POET-DSM JV on advanced biofuels

Slide 44

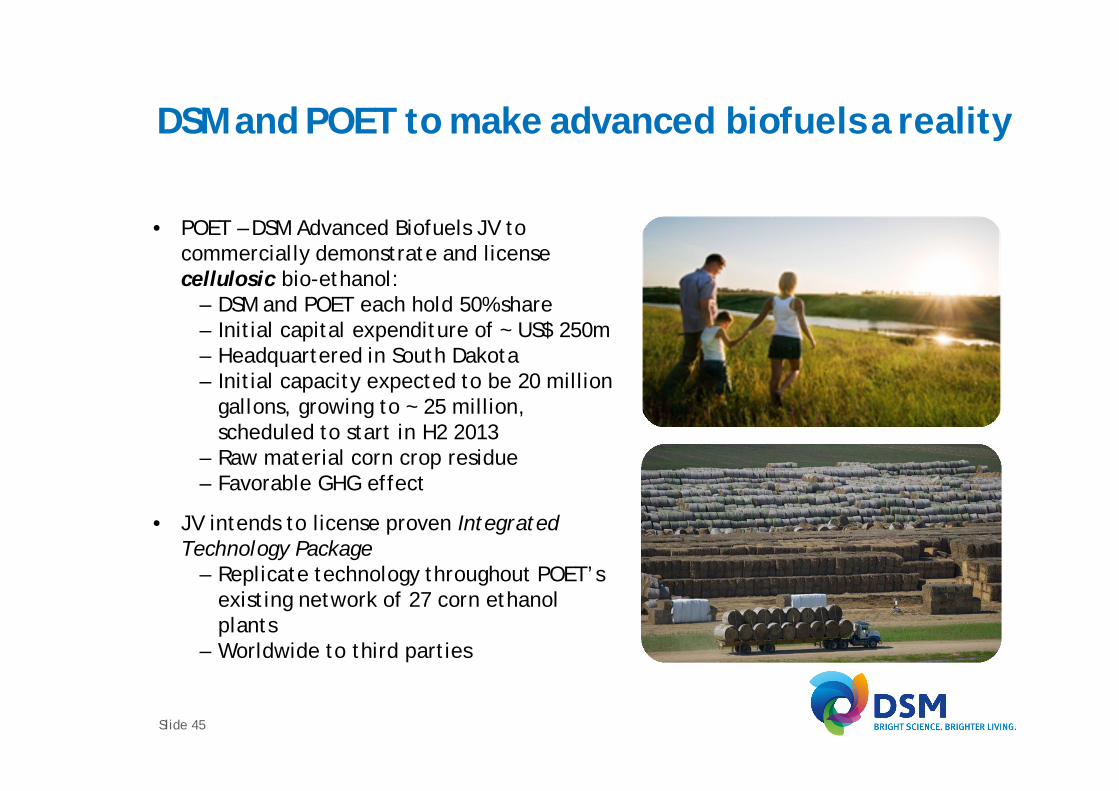

DSM and POET to make advanced biofuels a reality

• POET – DSM Advanced Biofuels JV tocommercially demonstrate and licensecellulosic bio-ethanol:

– DSM and POET each hold 50% share– Initial capital expenditure of ~ US$ 250m– Headquartered in South Dakota– Initial capacity expected to be 20 million

gallons, growing to ~ 25 million,scheduled to start in H2 2013

– Raw material corn crop residue– Favorable GHG effect

• JV intends to license proven IntegratedTechnology Package

– Replicate technology throughout POET’sexisting network of 27 corn ethanolplants

– Worldwide to third parties

Slide 45

Highly attractive market opportunity

• Global cellulosic ethanol market expected togrow to 18bn gallons in 2022, ~ US$ 50bn

• Resulting in market value for enzymes &yeasts of ~ US$ 3-5 bn in 2022

• US is leading, forecast ~ 7.5bn gallons ofcellulosic bio-ethanol by 2022

• It can be calculated that by 2022 ~ 150-200plants to produce cellulosic bio-ethanol fromcorn crop residue could be required in the US.

0

5

10

15

20

2011 2015 2020 2022

US

China

Brazil

EU

Market expectations(*)

cellulosic ethanol(global demand in billion gallons)

*: derived from Hart’s Global Energy Study

Slide 46

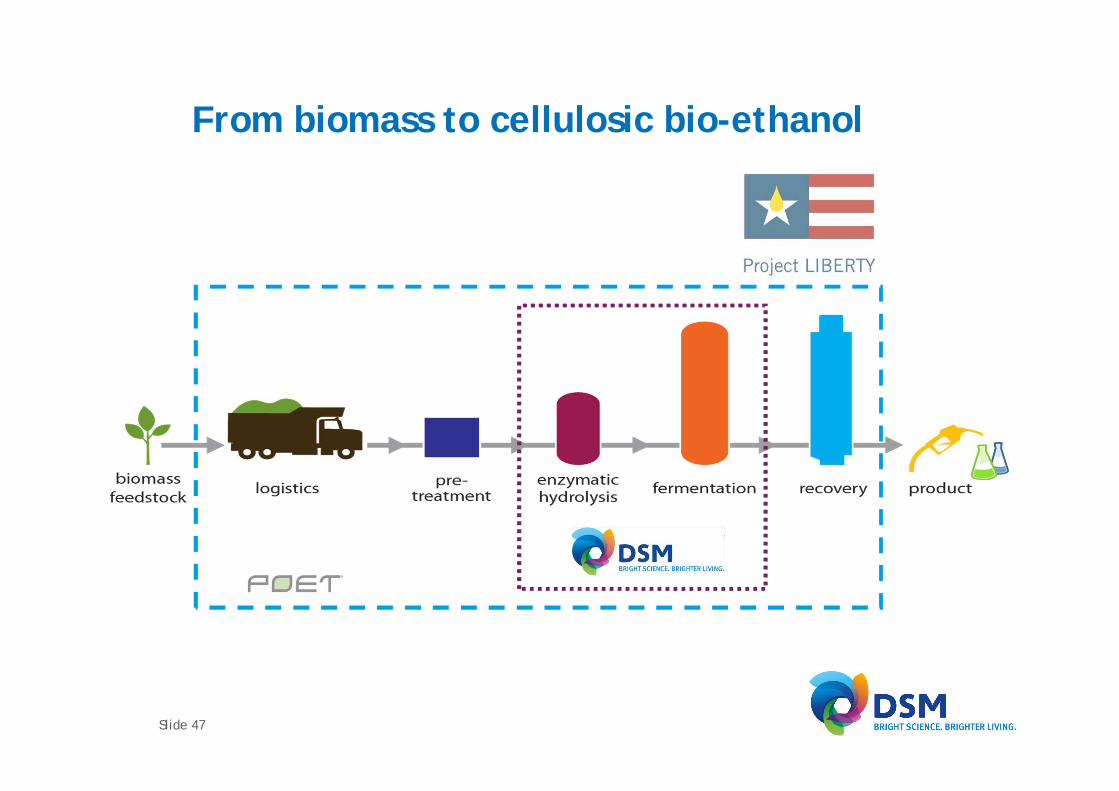

From biomass to cellulosic bio-ethanol

Slide 47

Two innovative leaders, one shared vision

• Has more than 140 years ofexperience in biotechnology

• Has a proven track record in scalingup industrial operations

• Leadership position in conversiontechnologies (yeast and enzymes) forcellulosic biomass to ethanol

• DSM is the only company that cansimultaneously co-ferment all C6 andC5 sugars (xylose & arabinose) incellulosic biomass

• US market leader in bio-ethanol witha network of 27 corn ethanol plantsand revenues ~ US$ 6 bln in 2011.

• Has significant experience in scalingup technology within its network ofcorn ethanol plants

• Has a leadership position in cellulosicethanol process technology and hasbeen operating a pilot scale cellulosicethanol plant since 2008

• Has spent five years developing asystem to harvest, transport and storecellulosic biomass and has built aninfrastructure for corn crop residuearound the Emmetsburg, Iowa facility

Slide 48

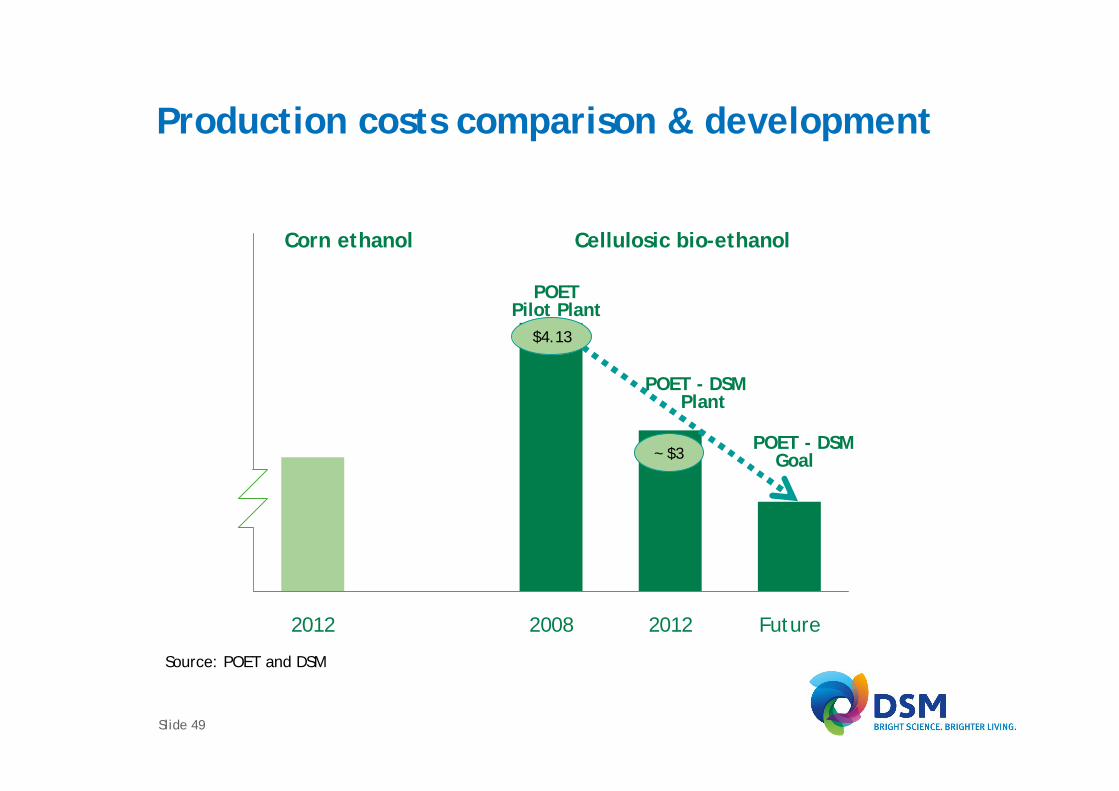

Production costs comparison & development

Source: Poet and DSM

2012 2008 2012 Future

$4.13

~ $3

POETPilot Plant

POET - DSMPlant

Cellulosic bio-ethanolCorn ethanol

POET - DSMGoal

Source: POET and DSM

Slide 49

Value creation in biofuels: now & tomorrow

• Goal is to establish a solid leadership position in theglobal cellulosic bio-ethanol market

• First revenues expected in 2013. JV is expected to beprofitable in first full year of production (2014)

• Projected sales (cellulosic bio-ethanol, biogas and lateron licensing) from JV to grow to > US$ 200m* with aboveaverage EBITDA contribution in the medium/longerterm. Future license income could add up to severaltens of millions of US$.

• JV expected to contribute significantly towards DSMstrategic aspirations for the EBAs by 2020

* Due to IFRS rules as of 2013 DSM will consolidate the JV using the equity method

Slide 50

Contact:

DSM Investor RelationsP.O. Box 6500, 6401 JH Heerlen, The Netherlands

(+31) 45 578 2864e-mail: [email protected]

internet: www.dsm.com

visiting address: Het Overloon 1, Heerlen, The Netherlands