Embed Size (px)

DESCRIPTION

E-commerce : Payment Systems. Traditional Payment Methods. US Census Bureau 2003. Cash. Why are so many transactions still done by cash? What ramifications exist for a company that does its business exclusively online?. Cash. Why are so many transactions still done by cash? - PowerPoint PPT Presentation

Citation preview

E-commerce : Payment Systems

Traditional Payment Methods

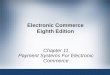

Number of Transactions

Personal Checks, 25%

Cash, 44%Credit Cards, 18%

Debit Cards, 10%

Electronic, 2%

US Census Bureau 2003

Cash

• Why are so many transactions still done by cash?

• What ramifications exist for a company that does its business exclusively online?

Cash

• Why are so many transactions still done by cash?– Customers with poor credit, no credit, no bank

accounts, etc. Anonymity issues.– Cash is easier, quicker for smaller transactions

• What ramifications exist for a company that does its business exclusively online?– Can’t reach or sell to many customers– Transactions require more cognitive energy;– Minimum 5 items must be entered.

Traditional Payment MethodsTotal Transaction Amount

Debit Cards, 8%

Electronic, 5%

Cash, 19%

Personal Checks, 41%

Credit Cards, 24%

US Census Bureau 2003

Number of Transactions

Personal Checks, 25%

Cash, 44%Credit Cards, 18%

Debit Cards, 10%

Electronic, 2%

Personal Checks

• Why are large value transactions done by check?

• What ramifications (if any) does this pose for online retailers?

Personal Checks

• Why are big (large value) transactions done by check?– Customers are nervous about carrying large sums of cash– “transaction reversal;”

check can be canceled if transaction goes awry

• What ramifications (if any) does this pose for online retailers?– Some customers are nervous about large online transactions;

security, fraud, etc.– Funds transfer immediately; debit incurred in real time; no built-

in transaction reversal

Cash requires No Intermediation

• Unlike all the other payment methods, cash does not require intermediation.

Payment Method Intermediate

Personal Check Bank

Credit Card Visa, Master Card

Debit (Stored Credit) Bank

Accumulating Balance American Express

Intermediation

• Adds cost to each transaction.– customer can directly absorb this cost.

• Some small businesses still charge more if you use a credit card.

– costs are always indirectly absorbed by the customer

• considered a cost of doing business.• this cost ultimately leads to higher prices

Credit Cards 101

• Pretend you are a merchant that wants to accept credit cards– Visa and Master Card have different plans

• depends on your bank (called “acquirer”) and your business type.

1. Monthly fee (unlimited transactions) - $1000/month

2. Set fee for each transaction - $0.30/transaction

3. Percent fee on transaction amount - 2.5%

• Which one would be best if you’re a very small retailer and sell very inexpensive items?

Credit Cards 101

• Credit Card transactions are not as simply as you might think.

• How it works…

Credit Cards 101

• Intermediaries (Banks/Credit Card Companies) developed their IT over long period of time.

• Banks can afford millions $$$ in IT investment– economy of scale; they can wait a long time for

payback

• Retailers/Merchants collectively paid for IT development over long period of time.

• How does this benefit new Retailers/Merchants?

Credit Cards 101

• Q: How does this benefit new Retailers/Merchants?

• A: They don’t have to pay for IT development and overhead costs associated with supporting credit card transactions.– Card readers are cheap; free with some plans.– No setup fees with some plans

• Visa, MC, and the Banks want 0.5%-3.0% of your business and will give you the technology for nothing.

Credit Cards 101

• Analogy 1:– Gillette will sell you a deluxe razor with two

replacement blades for $5.– But, replacement blades cost about $2.50

each, so the razor handle is free, right?

• Analogy 2:– Original Sony Playstation sold for $200, even

though it cost Sony $250 to manufacture and distribute. Why?

Intermediation Re-visited

• During the E-commerce exuberance of the late 1990’s.– Banks and Credit Card companies were slow

movers…– They failed to integrate their services with the WWW– Online retailers had to build their own web-based

information systems to support online transactions• The costs were enormous and were not considered when

projecting profits.

Big Company = Slow mover

• Surprisingly, Visa and MasterCard were…– not initially interested in supporting Web-

based transactions; – concerns that there would be no payback

• Online retailers/merchants were forced to build their own systems– PayPal emerged– VeriSign emerged

• Early systems were not good.

Visanet:

Early Systems

MerchantsBanks/Credit Card

Companies

Manual Entry

Online payment

systems were very costly to

develop

Typically, 1% to 3% cost

of business increase

WWW

CustomSoftware Systems

Web Server

Customers

Dot.com Bust

More Factors leading to the dot.com bust…1. failure to recognize how many people …

• still use cash only• won’t fill out 5 lines on the web• unwilling to make large “non-reversible”

transactions.

2. Finally, (The Big One) failure to recognize the intense costs of developing reliable, secure, online payment systems.

Visanet:

Early Systems

MerchantsBanks/Credit Card

Companies

Manual Entry

Many merchantsare independently developing nearly identical systems

Must be integrated with

existing proprietary

VISA/MC systems

WWW

CustomSoftware Systems

Web Server

Customers

WWW vs. Visa/MC networks

WWW• very open / flexible• limitless options• fully customizable• unbounded costs• Individual

merchants pay for IT development costs

Visa/MC networks• very specific

technology• few options• limited customizations• set costing• shared development

costs: VISA, MC, Banks pay for IT development

PayPal: B2C E-commerce Savior

• Basic Idea: develop a general web-based system for interfacing with leading intermediaries.

• Unlike VISA/MC networks, PayPal makes it as easy as possible to integrate your website with PayPal’s system.

• Small companies can now accept credit cards online with minimal development costs.

PayPal: Middle-man

• PayPal is yet another middle-man– contradicts the assumption that the web could

enable friction-free commerce.

• dot.com exuberance was based on the principle that the web would cut out the middle man

Customer PayPal Visa Merchant$10

1% + $0.30$9.60

3%$9.30

$0.40 $0.30 $9.30

PayPal: Digital Cash Intermediary

• Icing on the cake: PayPal is also a Digital Cash (e-Cash) intermediary.

• Using Credit Cards or Direct Bank Transfers, customers can transfer money to an individual PayPal account.– The individual can “cash out” their account to their

own credit card or bank account.

• This allows individuals to receive payments electronically without the need for merchant VISA/MC account or business banking.

PayPal’s impact

• Visa, MC, Discover Card, etc. saw that they had missed a huge opportunity.

• One on hand…– PayPal was giving them more business…

• On the other hand…– they could have seized all the

opportunities if they were quick to move.• PayPal helped create a new opportunity:

P2P E-commerce.

Security and Irrefutability

• Traditional credit card transactions have two built in security measures.

1. You have to present the card– Without it, no transaction can take place, or

can it?

2. You have to sign the receipt– Even if someone steals your card, there is

still a back up?– This protects the consumer, right?

Security and Irrefutability

• Long before the WWW, merchants wanted to accept credit cards over the phone.

• Thus, the card does not have to be presented; only the number is needed.

• Stealing the number could be easier than stealing the card.

• How do you sign the receipt?

Classic Fraud Example

• Make a phone purchase with a credit card.

• Have the item shipped to another location.

• Intercept the item.

• Claim that you never made the purchase.

• Summary: You falsely refute the purchase.