Embed Size (px)

Citation preview

E d ition 26

Transactions Q uarterlyA perspective on the I ndian transactions market

J anuar y - M ar c h 2017

Tran

sact

ions

Qua

rter

ly –1

Q17

2

Edition 26 January - March 2017

In this edition

Foreword ................................................................3

Mergers and acquisition (M&A) ................................4

India M&A snapshot in 1Q17 ...................................5

Key sector highlights ...............................................7

Cross-border activity .............................................10

Global transaction activity .....................................11

Outlook ................................................................13

Methodology ........................................................15

Transactions Quarterly –1Q

17

3

Welcome to the 26th edition of Transactions Quarterly, our quarterly review of India’s M&A landscape.

The global economic recovery has started showing signs of improvement, shrugging off the challenges posed by a volatile geopolitical environment and increasing protectionism globally. Amidst this gradually stabilizing environment, corporate organizations internationally are now opening-up to large-scale acquisitions which drive their strategic long-term growth plans. The last

quarter saw the largest number of billion-dollar plus deals globally, recorded in the first quarter of any year since 2007. This is a clear sign of sound investor confidence in the global economy and high boardroom optimism, which is driving companies to pursue acquisitions as they look to push their expansion agenda.

The Indian M&A market also witnessed an increase in deal value, primarily on the back of US$11 billion-plus announced Vodafone-Idea merger. Notably, domestic players were seen more confident of India’s attractiveness and were engaged in a large number of consolidation and market share expansion deals. Big-ticket deal announcements are expected to make headlines in in the coming quarters as consolidation continues across several sectors, including telecom, e-commerce and retail. The results of EY’s latest Capital Confidence Barometer (CCB) April 2017 report reinstates this confidence as 57% of the Indian respondents expect their companies to actively pursue M&A in the next twelve months. Notably, this is the highest number ever reported in the history of CCB (for India results).

Cross-border activity witnessed a deceleration during the quarter, due to relatively lower inbound activity as compared to 1Q17. The inbound M&A activity, though not as intense when compared to previous quarters, continues to reflect global investors’ interest in India with a significant number of deals in technology and diversified industrial products sectors. From an outbound M&A perspective, deal activity remained stable as players from technology sector continued to evaluate opportunities for overseas acquisitions with a view to gain access to new markets and technologies.

Overall, the M&A environment remains conducive in India on the back of the country’s attractive investment profile and constant reforms push. In addition, the need to respond to challenges while navigating a complex and fast-changing business environment is making deal-making imperative for companies, creating a ground for healthy deal market.

Fore

wor

d

Amit Khandelwal Partner and National Director, Transaction Advisory Services, Ernst & Young LLP

Tran

sact

ions

Qua

rter

ly –1

Q17

4

M&A highlights

transnational deal of the quarter —€571 million outbound acquisition of a 93.75% stake in Finland-based PKC Group Oyj by Indian auto parts maker Motherson Sumi Systems Limited.

On the sectoral front, the diversified industrial products sector was the frontrunner in terms of volume with 31 deals worth US$533.4 million. The majority of these acquisitions were either domestic or inbound in nature with targets in the power and electrical equipment and packaging segments. These acquisitions were largely aimed at expanding market share and enhancing product lines. On the value front, the telecommunications sector was at the forefront.

Consolidation was also a key theme for sectors, like industrial products, technology and retail and consumer products, which drove the domestic deal activity of the country. With scale expansion becoming a critical element of Indian corporates’ strategy agenda, consolidation deals are likely to gain further prominence across sectors. Besides consolidation deals, we also saw large buy-backs by prominent PSUs, including HPC Limited and NLC India Limited.

The cross-border M&A activity was relatively silent due to the absence of mega deals this quarter. Amidst the muted activity, the automotive sector grabbed the headlines with the largest

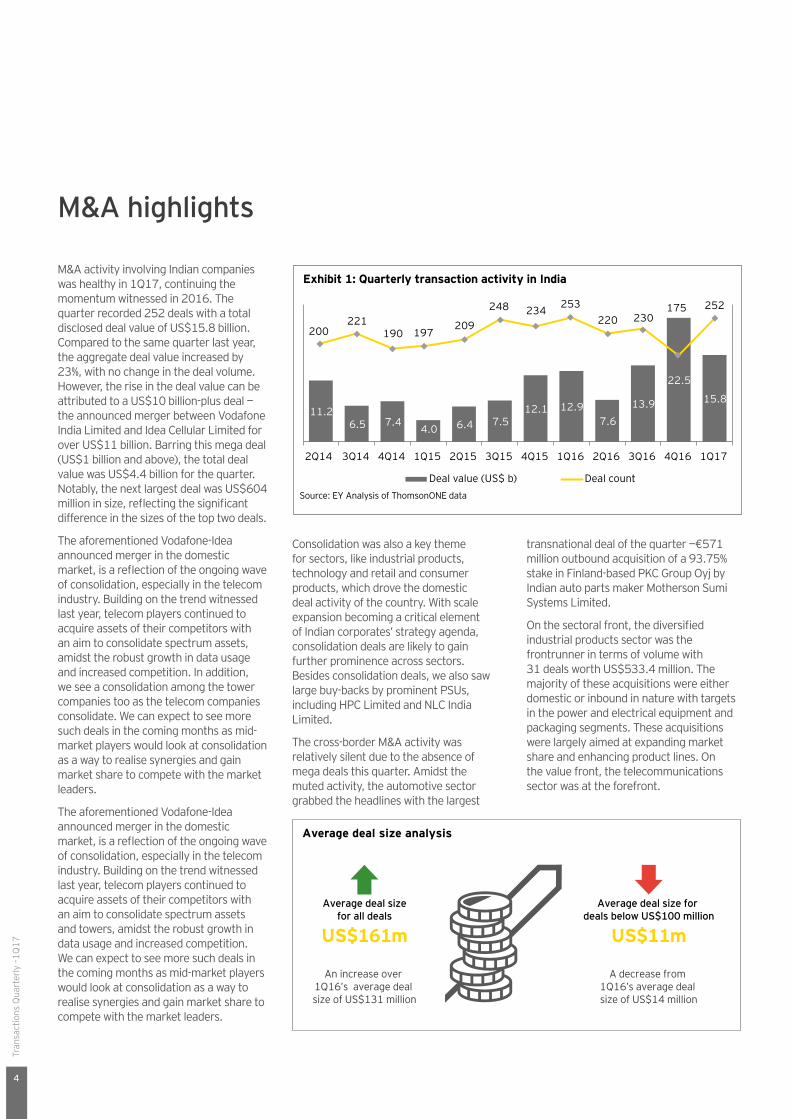

M&A activity involving Indian companies was healthy in 1Q17, continuing the momentum witnessed in 2016. The quarter recorded 252 deals with a total disclosed deal value of US$15.8 billion. Compared to the same quarter last year, the aggregate deal value increased by 23%, with no change in the deal volume. However, the rise in the deal value can be attributed to a US$10 billion-plus deal — the announced merger between Vodafone India Limited and Idea Cellular Limited for over US$11 billion. Barring this mega deal (US$1 billion and above), the total deal value was US$4.4 billion for the quarter. Notably, the next largest deal was US$604 million in size, reflecting the significant difference in the sizes of the top two deals.

The aforementioned Vodafone-Idea announced merger in the domestic market, is a reflection of the ongoing wave of consolidation, especially in the telecom industry. Building on the trend witnessed last year, telecom players continued to acquire assets of their competitors with an aim to consolidate spectrum assets, amidst the robust growth in data usage and increased competition. In addition, we see a consolidation among the tower companies too as the telecom companies consolidate. We can expect to see more such deals in the coming months as mid-market players would look at consolidation as a way to realise synergies and gain market share to compete with the market leaders.

The aforementioned Vodafone-Idea announced merger in the domestic market, is a reflection of the ongoing wave of consolidation, especially in the telecom industry. Building on the trend witnessed last year, telecom players continued to acquire assets of their competitors with an aim to consolidate spectrum assets and towers, amidst the robust growth in data usage and increased competition. We can expect to see more such deals in the coming months as mid-market players would look at consolidation as a way to realise synergies and gain market share to compete with the market leaders.

Exhibit 1: Quarterly transaction activity in India

Source: EY Analysis of ThomsonONE data

Deal value (US$ b) Deal count

11.2 6.5 7.4

4.0 6.4 7.5 12.1 12.9

7.6 13.9

22.5

15.8

200 221

190 197 209

248 234 253 220 230

175 252

2Q14 3Q14 4Q14 1Q15 2Q15 3Q15 4Q15 1Q16 2Q16 3Q16 4Q16 1Q17

Average deal size analysis

Average deal sizefor all deals

US$161m

Average deal size for deals below US$100 million

US$11m

An increase over 1Q16’s average deal size of US$131 million

A decrease from 1Q16’s average deal size of US$14 million

Transactions Quarterly –1Q

17

5

I n d i a M & A s n ap s h ot i n 1 Q 1 7

D eal type D eal d escription D ate T argetT arget nation

A cq uirerA cq uirer nation

Val ue ( U S $ mil l ion)

S ector

D om es tic M er g er 03- 20- 17I d ea Cellular L td . -M obile B us ines s

I nd iaVod af one G r oup P L C- Vod af one I nd ia A s s ets

UK 11,627. 3T elec om m uni - c ations

O utbound T end er - of f er 01- 19- 17 P K C G r oup O y j F inlandM oth er s on Sum i Sy s tem s L td .

I nd ia 604. 3 A utom otiv e

D om es tic B us ines s p ur c h as e 03- 23- 17T ik ona D ig ital N etw or k s P v t. L td . -4G B us ines s

I nd ia B h ar ti A ir tel L td . I nd ia 244. 5T elec om m uni - c ations

D om es tic B us ines s p ur c h as e 02- 19- 17

L loy d E lec tr ic & E ng ineer ing L td . -Cons um er D ur able B us ines s

I nd ia H av ells I nd ia L td . I nd ia 238. 6Diversified ind us tr ial p r od uc ts

O utbound 100% acquisition 03- 06- 17CJ S Solutions G r oup L L C

United States

T ec h M ah ind r a L td .

UK 220. 0 T ec h nolog y

O utbound B us ines s p ur c h as e 01- 30- 17M allinc k r od t P L C-I ntr ath ec al T h er ap y B us ines s

United K ing d om

P ir am al E nter p r is es L td .

I nd ia 203. 0 P h ar m ac eutic als

I nbound

M inor ity s tak e ac q uis ition (ex c lud es inv es tm ent in s ubs id iar y )

02- 14- 17R eN ew P ow er Ventur es P v t. L td .

I nd ia J E R A Co I nc J ap an 200. 0 I nf r as tr uc tur e

D om es ticStak e inc r eas e/ac q uis ition in ex is ting J V

03- 28- 17SB I Car d s & P ay m ents Ser v ic es L td .

I nd iaState B ank of I nd ia

M alay s ia 178. 5 F inanc ial s er v ic es

O utbound 100% acquisition 01- 07- 17G ener is F ar m ac eutic a SA

P or tug alA ur obind o P h ar m a L td .

I nd ia 142. 2 P h ar m ac eutic als

I nboundA d d itional s tak e ac q uis ition in s ubs id iar y

01- 24- 17L um inous P ow er T ec h nolog ies P v t. L td .

I nd iaSc h neid er E lec tr ic SA

F r anc e 139. 6Diversified ind us tr ial p r od uc ts

T op 1 0 Ind ian d eal s of the q uarter*

*Internal restructuring deals including share buyback, merger have not been included

Tran

sact

ions

Qua

rter

ly –1

Q17

6

D omestic Inb ound O utb ound T otal

1Q16 149 51 53 253

2Q16 121 62 37 220

3Q16 151 48 31 230

4Q16 93 45 37 175

1Q17 169 42 41 252

D omestic Inb ound O utb ound T otal

1Q16 5. 2 1. 1 6. 6 12. 9

2Q16 5. 4 1. 3 0. 9 7. 6

3Q16 9. 9 3. 8 0. 2 13. 9

4Q16 5. 3 15. 2 2. 0 22. 5

1Q17 13. 8 0. 6 1. 4 15. 8

D eal type composition

D eal count D eal value ( U S$ billion)

Source: EY Analysis and ThomsonONE data

Und is c los ed 0- 20 20- 100 A bov e 100

D eal siz e composition

Sour c e: E Y A naly s is of T h om s onO N E d ata

61% 62% 61%51%

61%

26% 25% 25%23%

27%

7% 7% 6%13%

6%6% 6% 8% 13% 6%

1Q16 2Q16 3Q16 4Q16 1Q17

D eal s iz e r ang es (US$ m )

Transactions Quarterly –1Q

17

7

K ey s ec t or h i g h li g h t s

*Key sectors basis their positions in terms of value and volume

1 Q 1 7 V s 1 Q 1 6 change indicator I ncrease D ecrease

i ersifie in stria prod ucts

31 d eals

US$533mT el ecommunications

7 d eals

US$11. 96m

Infrastructure22 d eals

US$647mR eal estate

19 d eals

US$252m

O il and gas2 d eals

US$233mR etail and consumer prod ucts

20 d eals

US$64m

T echnol ogy30 d eals

US$268mP harmaceutical s

12 d eals

US$379m

F inancial serv ices31 d eals

US$240mA utomotiv es

8 d eals

US$631m

Tran

sact

ions

Qua

rter

ly –1

Q17

8

• Poland-based TenderHut SA fully acquired QBurst Poland Sp Zoo, a development division of the Indian company QBurst Technologies. The acquisition will expand TenderHut’s list of offered services based on the use of IoT, machine learning technology and virtual and augmented reality.

• Fairfax-controlled business services provider Quess Corporation Limited announced the acquisition of a 26% stake in Heptagon Technologies Private Limited, an Indian software development company, as it looks to cut costs and ramp up digitisation of business processes. The deal is also expected to enhance sales for the industrial IoT business of Quess.

deals in all spheres of logistics business, including air transportation, cold storage and shipping. Prominent deals were:

• Stellar Value Chain Solutions Private Limited acquired a 51% interest in Kelvin Cold Chain Logistics Private Limited, a domestic provider of refrigerated warehousing and storage services.

• Petronet LNG Limited acquired a 26% stake in India LNG Transport Company (No 4) Private Limited, a shipping consortium that provides deep sea freight transportation services, for an estimated amount of US$15 million. The consortium was jointly owned by Kawasaki Kisen Kaisha Limited and Mitsui OSK Lines Limited and Nippon Yusen Kabushiki Kaisha and Shipping Corporation of India Limited.

The technology sector clocked 30 deals with a disclosed deal value of US$267.9 million. The largest disclosed deal for the quarter was US$220 million acquisition of CJS Solutions Group, a US-based healthcare focused IT consulting company, by Tech Mahindra Limited.

IT consulting and services, and software segments remained hotbeds for deal activity during the quarter, contributing majority of the sector’s deal value and

Infrastructure sector clocked 22 deals with a total disclosed deal value of US$647.4 million. Majority of the deals were witnessed in the power (10 deals; US$589.5 million) and logistics and transportation (6 deals; US$38 million) segments.

Power segment contributed for majority of the deal value on the back of two mid-sized deals (US$100 million - US$500 million). The aforementioned buyback by NHPC Limited. for US$389.5 million and US$200 million acquisition of 10% stake in ReNew Power Ventures by Japan-based JERA Co. Inc. were the key transactions

Technology

Infrastructure

Albeit smaller in value terms, Internet of things (IoT) is gradually taking the centre stage in an increasingly connected and digital world

Power and logistics were in the spotlight for the deal activity in the sector

volume (24 deals; US$267.8 million). Deals were largely witnessed in areas including SMAC (Social, mobile, analytics and cloud) and the traditional IT consulting space, with IoT being the most popular one. Technology companies are building their capabilities in IoT with increasing adoption of IoT-based solutions/products across different industries, including utilities, manufacturing, automotive, transportation and logistics. The Indian government’s planned billion-dollar investment for 100 smart cities, over the next five years, is expected to be a key enabler for IoT adoption across these industries. Though still at infancy stage, India is seeing gradual traction in the space. some of the deals during the quarter include:

during the quarter. Within power segment, we also saw a few divestment deals with an aim to reduce debt. some of the deals included:

• Reliance Energy signed an agreement with the UK-based Energy Circle Plc which allows the latter to buy one or more distributed generation projects in the UK from Reliance Energy Limited.

• Inox Renewables Limited divested all its windfarms to JP Morgan-backed Leap Green Energy Private Limited. The sell-off would enable Inox Renewables to focus only on wind turbine manufacturing and also reduce debt of its parent company, Gujarat Fluorochemcials, the flagship company of Inox Group.

Logistics was also an active segment for the sector’s deal activity, as Indian players took the inorganic route to expand their respective businesses. We saw

Transactions Quarterly –1Q

17

9

Notably, Sona Group was the most active dealmaker in the sector with three transactions.

• In January 2017, Sona Group, via its subsidiary Sona Koyo Steering Systems Limited, acquired 37.5% stake in Mahindra Sona from its JV partner Mahindra & Mahindra for US$17 million.

• Subsequently, in February 2017, Sona made an exit from Sona Koyo Steering Group by selling its entire 25% stake to its JV partner JTKET Corporation.

• In March 2017, Sona Autocomp Holding Limited acquired the remaining 25% stake, which it did not already own, in SONA BLW Precision Forgings Limited, an auto-component manufacturer, from its JV partner Mitsubishi Materials Corporation.

These deals reflect Sona Group’s plans to focus solely on the forgings business.

The automotive sector made a comeback in M&A highlights in the quarter reported, as it was among the top three sectors in terms of disclosed deal value. Following the historic trend, majority of the deals were witnessed in the auto components segment (seven deals, US$757.9 million). The sector recorded a cumulative disclosed deal value of US$769.9 million from 10 deals. The largest deal of the sector was the €571 million acquisition of 93.75% stake in Finland-based PKC Group Oyj (PKC) by Indian auto parts maker Motherson Sumi Systems Limited (MSSL). This transaction was also the largest outbound deal during the quarter, making MSSL a market leader in the

AutomotiveAutomotive sector was in the limelight with the largest outbound deal of the quarter

wiring harness business for heavy duty commercial vehicles in the North American and European markets.

During the quarter, the sector also witnessed the sale of Hindustan Motors’ iconic brand, Ambassador, to French carmaker Peugeot SA for US$12 million. The deal was announced in the backdrop of a global agreement signed between the two companies to jointly manufacture and sell cars in India. As per the agreement, Peugeot will invest US$107 million to make cars with the Indian manufacturer.

Within the domestic landscape, the sector also saw a deal in green mobility and e-mobility space, an emerging trend in the global automotive industry. Smartron India Private Limited acquired an undisclosed minority stake in Volta Motors Private Limited. With rising environmental concerns in India and tightening regulations for diesel cars, auto players are looking at environmentally friendly solutions.

In the wake of heightened competition and increasing consolidation in the sector by industry players, Bharti Airtel made two acquisitions to strengthen its position.

• Bharti Airtel announced the acquisition of the Indian unit of Norwegian operator Telenor ASA to strengthen its market position and bolster its holdings of airwaves. The acquisition is subject to regulatory approvals.

• Bharti Airtel also acquired Tikona Digital’s 4G airwaves for US$244.5 million, ramping up its high-speed broadband spectrum capacity to compete with Reliance Jio Infocomm and the Vodafone-Idea Cellular.

Telecommunications was the most active sector charts with the largest cumulative deal value of US$11.9 billion from a total of seven deals. The largest deal of the sector was the announced merger of Vodafone India and Idea valued at US$11.6 billion. Vodafone Plc agreed to combine its subsidiary Vodafone India (excluding its 42% stake in Indus Towers) with Idea. The implied enterprise value is INR828 billion (US$12.4 billion) for Vodafone India and INR722 billion

TelecomConsolidation wave drives deal activity in the telecommunications sector

(US$10.8 billion) for Idea excluding its stake in Indus Towers. Post completion of the transaction, Vodafone India will own 45.1% of the combined company after transferring a stake of 9% to the Aditya Birla Group for approximately INR39 billion (US$579 million) in cash. The Aditya Birla Group will then own 26.0% and has the right to acquire more shares from Vodafone India under an agreed mechanism with a view to equalising the shareholdings over time. The transaction is expected to close during calendar year 2018, subject to customary approvals. The merger is expected to bring in capex and operational synergies in the form of lower infrastructure costs, network consolidation and cost efficiencies in information technology.

Tran

sact

ions

Qua

rter

ly –1

Q17

10

Cross-border activity

• Cross-border activity involving Indian companies declined in 1Q17 as compared to 1Q16. While the deal volume declined to 83 from 104, the disclosed deal value was down by 74% to US$2 billion.

• The decline in value was on account of relatively subdued outbound activity. While 1Q17 registered 41 outbound deals with a disclosed deal value of US$1.4 billion, 1Q16 had clocked 53 deals totaling US$6.6 billion. The technology sector sustained its leadership position in terms of deal volume, recording 11 outbound deals. The automotive sector took the lead in terms of total deal value with a total disclosed deal value of US$604.3 million from two outbound deals.

• Deal value and volume declined on the inbound front as well. While deal value decreased by 51% to US$539.8 million in 1Q17, deal volume reduced to 42 deals from 51 deals. Notably, the diversified industrial products sector led both in terms of total inbound deal volume and value with 10 deals totaling US$224.3 million. The US continued to be the most active cross-border M&A partner for Indian companies during the quarter, with a total of 28 deals (12 inbound and 16 outbound) for a total disclosed value of US$449.9 million.

Cross-border M&A declined in 1Q17

Both inbound and outbound

Only inbound or outbound

Deal flow

Outbound

Inbound

USInbound: 12 deals, US$79mOutbound: 16 deals, US$371m

FranceInbound: 4 deals, US$141m-

UKInbound: 3 deals, undisclosed valueOutbound: 4 deals, US$218m

UAEInbound: 6 deals, US$52mOutbound: 1 deals, undisclosed value

SingaporeInbound: 2 deals, undisclosed valueOutbound: 4 deals, US$18m

JapanInbound: 7 deals, US$238m

Source: EY Analysis and ThomsonONE data

Transactions Quarterly –1Q

17

11

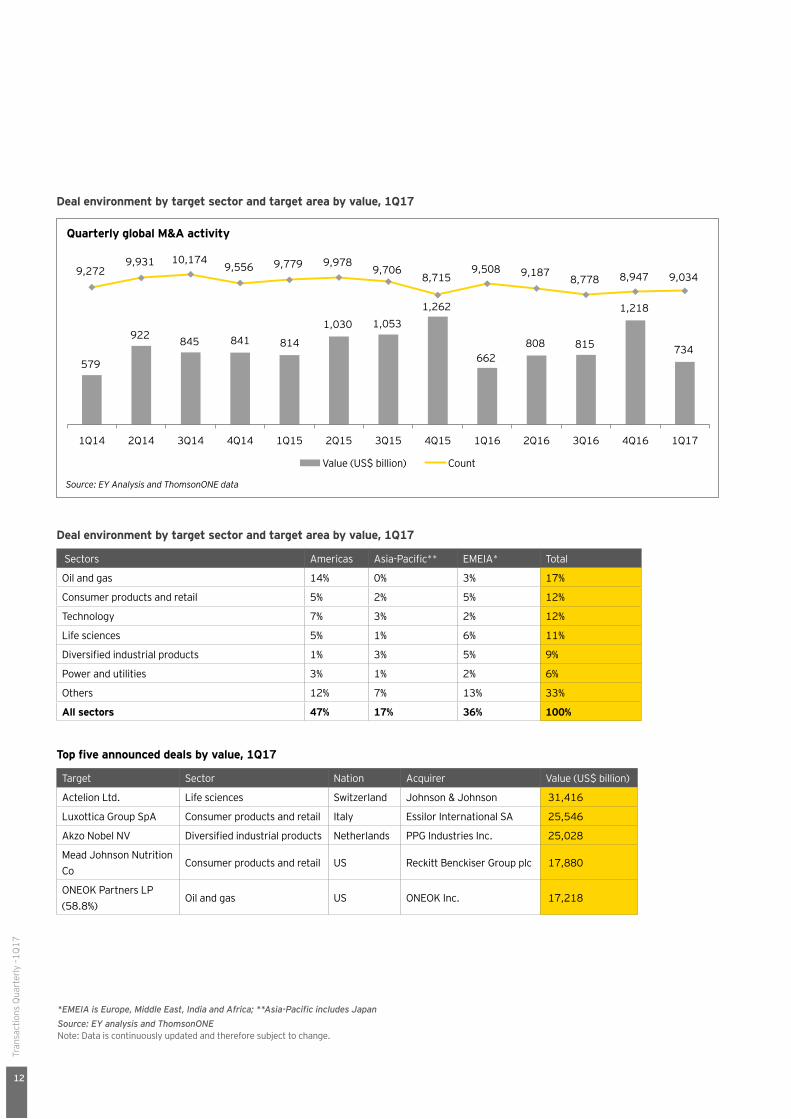

Global transaction activity

Global M&A activity remained healthy in 1Q17

• The first quarter of 2017 saw strong deal making — 9,034 deals worth a combined value of US$734 billion.

• Billion-dollar plus deals grabbed the headlines during the first quarter (136 deals valued at US$482 billion).

• The M&A outlook for 2017 remained healthy as companies looked to review their portfolios more frequently.

Current state

• Global market uncertainty did not impact M&A in the first quarter of 2017. The quarter saw deals worth US$734 billion, an 11% increase year on year (YOY). This was the third time over the past 10 years that deal value surpassed US$700 billion in the first quarter. The number of deals recorded in 1Q17 was 9,034 as against 8,757 in the first quarter of 2016 — an increase of 3% YOY.

• Interestingly, the quarter witnessed 136 deals valued at US$1 billion or more. This was the highest number of billion-dollar plus deals recorded in the first quarter of any year since 2007. This is a clear sign of investor confidence in the global economy and high boardroom optimism, which are driving companies to pursue acquisitions as they look to boost strategic growth prospects.

• The Americas was the most attractive target area by deal value in 1Q17, attracting US$344 billion of deals (47% of the global total), followed by EMEIA at US$263 billion (36%) and Asia-Pacific (including Japan) at US$126 billion (17%).

• Consequently, portfolio reorganization will be a key deal driver, making companies active both on the buy and the sell side. We expect to see an uptick in divestment deals, with companies reviewing their portfolios and looking to recycle capital in order to invest in growth opportunities.

By volume, EMEIA was the major contributor with 3,327 deals, followed by the Americas with 3,181 deals and Asia-Pacific (including Japan) with 2,526 deals.

• Oil and gas was the most active target sector (in terms of deal value) for M&A during the current quarter, with 268 deals totaling US$123 billion. Three out of top 10 deals of the quarter were from the oil and gas sector, worth a combined value of US$42 billion. The largest deal of the quarter saw an agreement by the US health care giant Johnson & Johnson (J&J) to buy Swiss biotech company Actelion for US$30 billion.

Outlook

• Global M&A is expected to stay robust in 2017. With an improving global economic outlook, the quest for growth is likely to be the main motivation for deals in the coming months. Supportive market factors, including low interest rates, availability of credit, surplus cash reserves and a relatively benign economic climate, look set to prevail through the year. M&A could provide the fastest route to innovation and digitalization, the key for survival in an increasingly disruptive environment.

• Cross-border deals are set to rise in 2017. Despite geopolitical headwinds, we should see heightened cross-border M&A to buy into pockets of growth and secure supply chains in an era of increasing geopolitical uncertainty. Transformative events such as the new administration in the US and Brexit have raised concerns over future policy actions and the direction of global politics, thus making dealmakers selective in their approach.

Tran

sact

ions

Qua

rter

ly –1

Q17

1 2

Sec tor s A m er ic as Asia-Pacific** EMEIA* T otal

O il and g as 14% 0% 3% 17%

Cons um er p r od uc ts and r etail 5% 2% 5% 12%

T ec h nolog y 7% 3% 2% 12%

L if e s c ienc es 5% 1% 6% 11%

Diversified industrial products 1% 3% 5% 9%

P ow er and utilities 3% 1% 2% 6%

O th er s 12% 7% 13% 33%

A l l sectors 4 7 % 1 7 % 3 6 % 1 0 0 %

T ar g et Sec tor N ation A c q uir er Value (US$ billion)

A c telion L td . L if e s c ienc es Sw itz er land J oh ns on & J oh ns on 31,416

L ux ottic a G r oup Sp A Cons um er p r od uc ts and r etail I taly E s s ilor I nter national SA 25,546

A k z o N obel N V Diversified industrial products N eth er land s P P G I nd us tr ies I nc . 25,028

M ead J oh ns on N utr ition Co

Cons um er p r od uc ts and r etail US R ec k itt B enc k is er G r oup p lc 17,880

O N E O K P ar tner s L P (58.8%)

O il and g as US O N E O K I nc . 17,218

D eal env ironment b y target sector and target area b y v al ue, 1 Q1 7

D eal env ironment b y target sector and target area b y v al ue, 1 Q1 7

o fi e anno n e ea s a e

Source: EY analysis and ThomsonONE N ote: D ata is c ontinuous ly up d ated and th er ef or e s ubj ec t to c h ang e.

*EMEIA is Europe, Middle East, India and Africa; **Asia-Pacific includes Japan

Quarterl y gl ob al M & A activ ity

Source: EY Analysis and ThomsonONE data

Value (US$ billion) Count

579

922 845 841 814

1,030 1,053 1,262

662 808 815

1,218

734

9,272 9,931 10,174

9,556 9,779 9,978 9,706

8,715 9,508 9,187

8,778 8,947 9,034

1Q14 2Q14 3Q14 4Q14 1Q15 2Q15 3Q15 4Q15 1Q16 2Q16 3Q16 4Q16 1Q17

Transactions Quarterly –1Q

17

13

Near-term prospects of Indian M&A activity remain positive, with a strong exhibit of that in the recent quarter. The deal environment looks conducive on the back of a strong economic outlook, accommodative monetary policy and healthy capital markets. At the same time, the Indian government’s increasing focus on improving infrastructure and expanding digital reach across the country are expected to keep the investments flowing in the economy.

Domestically, M&A activity is expected to remain buoyant during 2017. We are likely to see restructuring and asset sales by highly leveraged companies in the domestic arena. Consolidation deals, especially in sectors such as telecommunications, e-commerce, retail, financial services and pharmaceuticals, in the light of burgeoning competition should also support domestic deal activity.

Inbound deal activity is likely to stay robust as foreign players reap the advantages of relaxed FDI rules across sectors. Simultaneously, the Government of India’s increasing focus on improving ease of doing business and GST implementation will help improve India’s attractiveness as one of key investment destinations. Additionally, as the US becomes more inward looking and protectionist, and Europe tackles political concerns and Brexit discussions, Asia-Pacific, especially India, is likely to have an increasing share in global trade and investments.

With respect to outbound investments, cash-rich Indian players will continue looking for opportunistic buys, largely in the US, Europe and Africa, with an aim to seek new technology and access to new markets. Pharmaceuticals and technology are expected to be active sectors for outbound investments. Furthermore, India’s quest to secure supplies of natural resources is expected to continue, with the government taking steps to encourage Indian players to acquire oil, gas and coal assets overseas.

Outlook

Deal activity to stay strong in 2017

Tran

sact

ions

Qua

rter

ly –1

Q17

1 4

Is post-merger integration a first thought or an afterthought?An effective post-merger integration strategy helps ensure success beyond sealing the deal. Find out how EY’s Operational Transaction Services can help you grow from challenger to leader and achieve lasting success.

The better the question. The better the answer. The better the world works.

Visit ey.com/in/ots #BetterQuestions

Transactions Quarterly –1Q

17

1 5

Is post-merger integration a first thought or an afterthought?An effective post-merger integration strategy helps ensure success beyond sealing the deal. Find out how EY’s Operational Transaction Services can help you grow from challenger to leader and achieve lasting success.

The better the question. The better the answer. The better the world works.

Visit ey.com/in/ots #BetterQuestions

M et h od olog y

Transactions quarterly i s b as ed on E Y ’ s an aly s i s of T h om s on O N E ’ s M & A d at a.

• D ata us ed in th is ed ition is f or th e p er iod 1 J anuar y 2017 to 31 M ar c h 2017.

• D eals h av e been tak en f r om T h om s onO N E . c om th r oug h th e “ A d v anc ed M & A ” s ear c h , w h er e an I nd ian c om p any w as eith er a tar g et, ac q uir er , tar g et’ s ultim ate p ar ent or ac q uir er ’ s ultim ate p ar ent. T h e ter m inated d eals h av e been ex c lud ed .

• D eals h av e been tak en w h er e “ d eal s tatus ” as p er T h om s onO N E . c om w as eith er p end ing , p ar tially c om p lete, c om p leted , p end ing r eg ulator y or unc ond itional.

• P r iv ate eq uity d eals or d eals w ith a f inanc ial s p ons or h av e been ex c lud ed .

• D eal v alues h av e been tak en as s tated in T h om s onO N E . c om (ac c es s ed 4 A p r il 2017) or as p er th e c om p any p r es s r eleas e in c er tain c as es . A ll am ounts ar e in US$ unles s oth er w is e s tated . T h e c onv er s ion r ate of non-US$ d eals ar e in ac c or d anc e w ith T h om s onO N E . c om g uid elines — th e f or eig n ex c h ang e r ate as on th e d eal announc em ent d ate.

• F or our analy s is , d eals h av e been c las s if ied into:

• Sec tor s : bas ed on tar g et’ s bus ines s

• I nbound , outbound and d om es tic : bas ed on tar g et/ ac q uir er / tar g et’ s ultim ate p ar ent and ac q uir er ’ s ultim ate p ar ent c ountr ies

• D eal s iz e: bas ed on announc ed d eal v alues

• A v er ag e d eal s iz e h as been c alc ulated as total d eal v alue d iv id ed by num ber of d eals w ith d is c los ed v alue.

• T h e num ber s h av e been r ound ed of f unles s oth er w is e ind ic ated .

• F or any f ur th er d etails on th e d eal inc lus ion c r iter ia us ed by T h om s onO N E . c om , c ontac t us at ey tas ind ia@ in. ey . c om .

A bout E YE Y is a g lobal lead er in as s ur anc e, tax , tr ans ac tion and ad v is or y s er v ic es . T h e ins ig h ts and q uality s er v ic es w e d eliv er h elp build tr us t and c onf id enc e in th e c ap ital m ar k ets and in ec onom ies th e w or ld ov er . W e d ev elop outs tand ing lead er s w h o team to d eliv er on our p r om is es to all of our s tak eh old er s . I n s o d oing , w e p lay a c r itic al r ole in build ing a better w or k ing w or ld f or our p eop le, f or our c lients and f or our c om m unities .

E Y r ef er s to th e g lobal or g aniz ation, and m ay r ef er to one or m or e, of th e m em ber f ir m s of E r ns t & Y oung G lobal L im ited , eac h of w h ic h is a s ep ar ate leg al entity . E r ns t & Y oung G lobal L im ited , a UK c om p any lim ited by g uar antee, d oes not p r ov id e s er v ic es to c lients . F or m or e inf or m ation about our or g aniz ation, p leas e v is it ey . c om .

E r ns t & Y oung L L P is one of th e I nd ian c lient s er v ing m em ber f ir m s of E Y G M L im ited . F or m or e inf or m ation about our or g aniz ation, p leas e v is it w w w . ey . c om / in.

E r ns t & Y oung L L P is a L im ited L iability P ar tner s h ip , r eg is ter ed und er th e L im ited L iability P ar tner s h ip A c t, 2008 in I nd ia, h av ing its r eg is ter ed of f ic e at 22 Cam ac Str eet, 3r d F loor , B loc k C, K olk ata - 700016

© 2017 E r ns t & Y oung L L P . P ublis h ed in I nd ia. A ll R ig h ts R es er v ed .

E Y I N 1706- 067 E D N one

T h is p ublic ation c ontains inf or m ation in s um m ar y f or m and is th er ef or e intend ed f or g ener al g uid anc e only . I t is not intend ed to be a s ubs titute f or d etailed r es ear c h or th e ex er c is e of p r of es s ional j ud g m ent. N eith er E r ns t & Y oung L L P nor any oth er m em ber of th e g lobal E r ns t & Y oung or g aniz ation c an ac c ep t any r es p ons ibility f or los s oc c as ioned to any p er s on ac ting or r ef r aining f r om ac tion as a r es ult of any m ater ial in th is p ublic ation. O n any s p ec if ic m atter , r ef er enc e s h ould be m ad e to th e ap p r op r iate ad v is or .

VN

E r ns t & Y oung L L PEY | Assurance | Tax | Transactions | Advisory

ey.com/ in

@ E Y _ I nd ia E Y | L ink ed I n E Y I nd ia E Y I nd ia c ar eer s

E Y r ef er s to th e g lobal or g aniz ation, and / or one or m or e of th e ind ep end ent m em ber f ir m s of E r ns t & Y oung G lobal L im ited