Embed Size (px)

Citation preview

E-Mobility – a promising field for the futureOpportunities and challenges for the German engineering industries

Dr. Thomas Schlick, Dr. Guido Hertel, Bernhard Hagemann, Dr. Eric Maiser, Michael Kramer Study

AmsterdamBahrainBarcelonaBeijingBerlinBrusselsBucharestBudapestCasablancaChicagoDetroitDüsseldorfFrankfurtGothenburgHamburgHong KongIstanbulKyivLisbonLondonMadridMilanMoscowMunichNew YorkParisPragueRigaRomeSão PauloShanghaiSingaporeStockholmStuttgartTokyoViennaWarsawZagrebZurich

© Roland Berger Strategy Consultants05/2011, all rights reserved www.rolandberger.com

Co-authors

Ralf KalmbachPartner, Roland Berger Strategy Consultants Member of the Management Board and Head of Global Automotive Competence Center, Munich [email protected]

Hartmut RauenMember of the VDMA General Board of Management Managing Director of VDMA Drive Technology and Fluid Technology Associations, the FVA Drive Technology Research Association and the Drive Technology Research Fund

E-Mobility – a promising field for the future

Dr. Thomas Schlick, Dr. Guido Hertel, Bernhard Hagemann, Dr. Eric Maiser, Michael Kramer Study

Opportunities and challenges for the German engineering industries

2 | Study

Table of contents

1. Executive summary 3

2. The role of German equipment suppliers worldwide 6

3. The effects of e-mobility on the German engineering industries 8

3.1. Fundamental changes in the automobile industry 8 3.1.1. E-mobility as a driver of change 8 3.1.2. Shift in competence/production capacity

for electric powertrain components 10 3.1.3. The need for changes in engineering industries 14 3.2. Case study: Battery production 15 3.2.1. Battery cells for e-mobility: Cell structure and main components 16 3.2.2. Production technologies for battery cells 18 3.2.3. Market overview for specific machines/technologies:

Main competitors 20 3.2.4. Assessment of the competitiveness of German manufacturers

and discussion of their major competitive advantages and disadvantages 22

3.2.5. General assessment of the importance of the technology for Germany as a location for plant equipment manufacturers 25

3.3. Case study: Electric motor production 26 3.3.1. Electric motors for e-mobility: Structure and main components 27 3.3.2. Production technologies for electric motors 29 3.3.3. Market overview for specific machines/technologies:

Main competitors 31 3.3.4. Assessment of the competitiveness of German manufacturers

and discussion of their major competitive advantages and disadvantages 31

3.3.5. General assessment of the importance of the technology for Germany as a location for plant equipment manufacturers

3.4. Summary 33 4. Approaches to exploiting the growth potential in the area of e-mobility 37

5. Recommendations for action 39

Authors and contacts 40

3 | E-Mobility – a promising field for the future

1. Executive summary

One of the most important trends in the automobile industry in the next few years as it moves towards sustainable mobility will be the introduction of electric drives. The main factors behind this development will be the shortage of resources and the targets for the reduction of CO2 in the various regions of the world which promote the use of alternative drive systems. The topic of e-mobility has already been examined in many of its facets in the past few years, but generally only from the perspective of automobile manufacturers, their component suppliers and the electricity supply industry – which vehicle and mobility concepts will prevail? Which components and competences will be needed in the future? How can costs be reduced the fastest? What will the business model of the future look like? The field of production technology will also see fundamental changes due to e-mobility. Through the use of new components, new technologies will be used in the future which have previously been used rarely or not at all in the automobile industry. This development will represent a major challenge for German machine constructors, which are today's world leaders in the production of "traditional" technologies for the automobile industry. In order to avoid losing their leading position to competitors in particular from Asia in the technological areas which will emerge as the result of the technological changeover to e-mobility, these companies will need to master additional competences. Not only this, but the German engineering industries could also make a significant contribution to helping battery and electric motor producers to achieve their cost and quality targets. The optimization of pro-duction technology for the mass-produced battery production, accounting for approximately 50% of the production costs of electric vehicles, will be a significant factor in ensuring the success of e-mobility. Against this background, the VDMA and Roland Berger Strategy Consultants have decided to conduct a joint study to investigate the future challenges and opportunities for the German engineering industries. In addition to extensive research, around 50 interviews were conducted with experts from machine constructors, automobile manufacturers and suppliers as well as in the field of science.

4 | Study

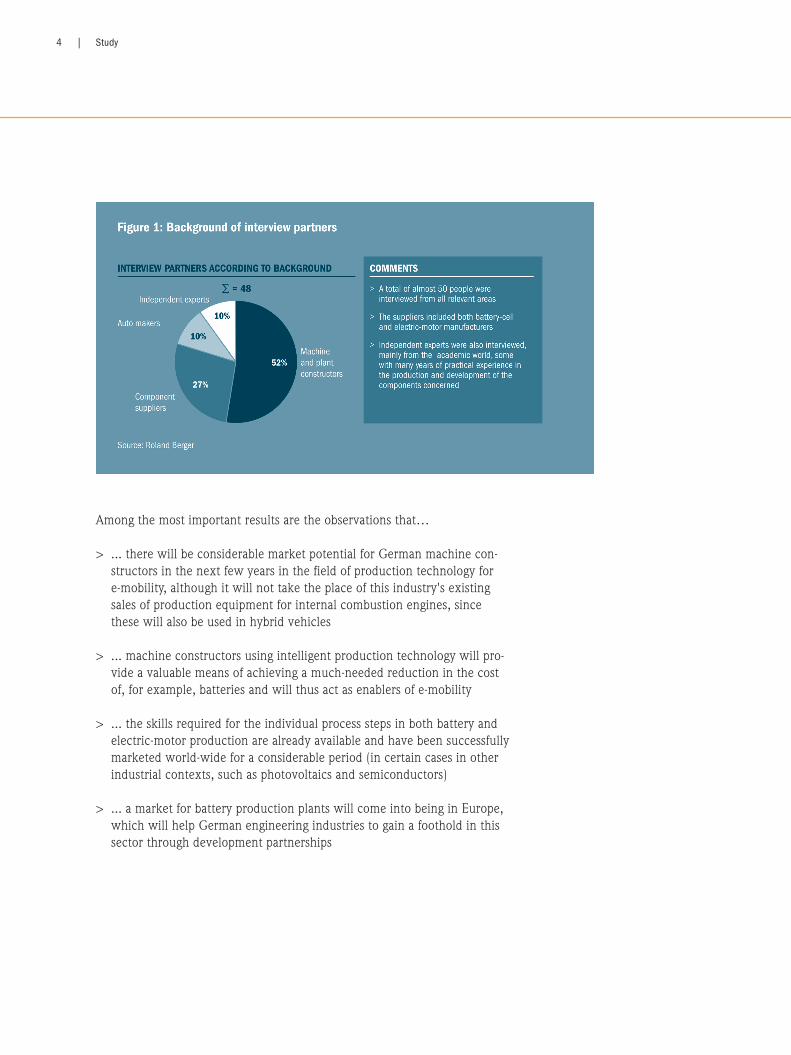

Among the most important results are the observations that…

> ... there will be considerable market potential for German machine con-structors in the next few years in the field of production technology for e-mobility, although it will not take the place of this industry's existing sales of production equipment for internal combustion engines, since these will also be used in hybrid vehicles

> ... machine constructors using intelligent production technology will pro-vide a valuable means of achieving a much-needed reduction in the cost of, for example, batteries and will thus act as enablers of e-mobility

> ... the skills required for the individual process steps in both battery and electric-motor production are already available and have been successfully marketed world-wide for a considerable period (in certain cases in other industrial contexts, such as photovoltaics and semiconductors)

> ... a market for battery production plants will come into being in Europe, which will help German engineering industries to gain a foothold in this sector through development partnerships

5 | E-Mobility – a promising field for the future

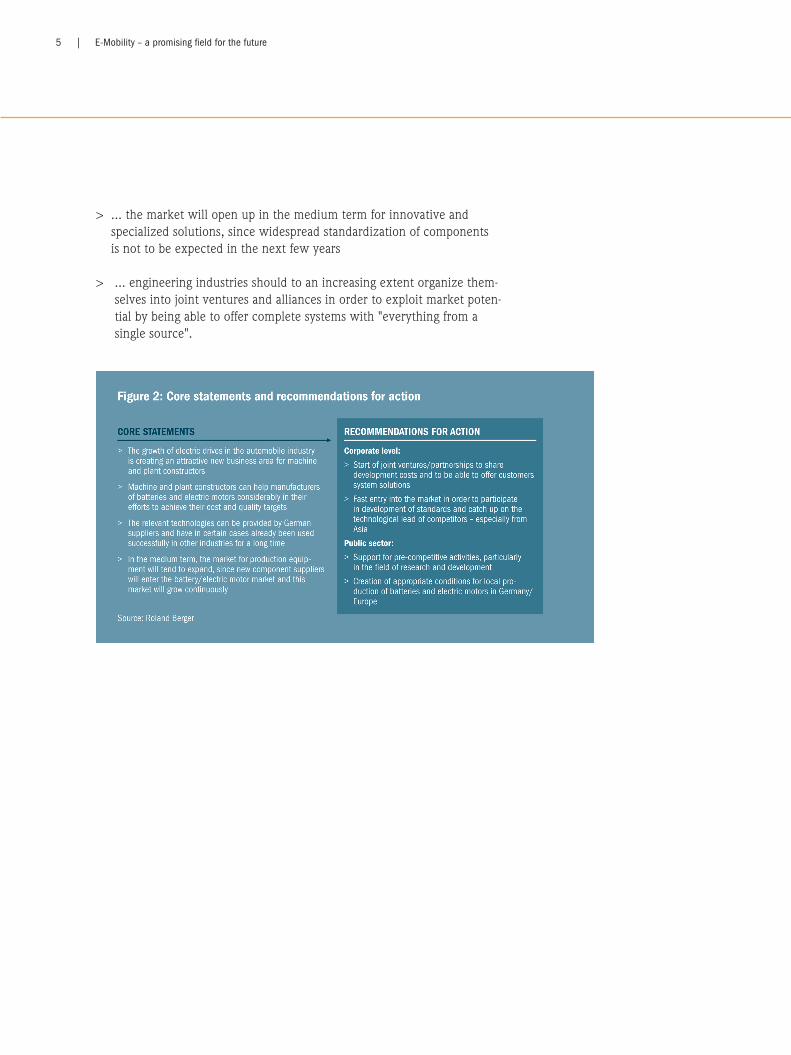

> ... the market will open up in the medium term for innovative and specialized solutions, since widespread standardization of components is not to be expected in the next few years

> ... engineering industries should to an increasing extent organize them - selves into joint ventures and alliances in order to exploit market poten-tial by being able to offer complete systems with "everything from a single source".

6 | Study

2. The role of German equipment suppliers worldwide

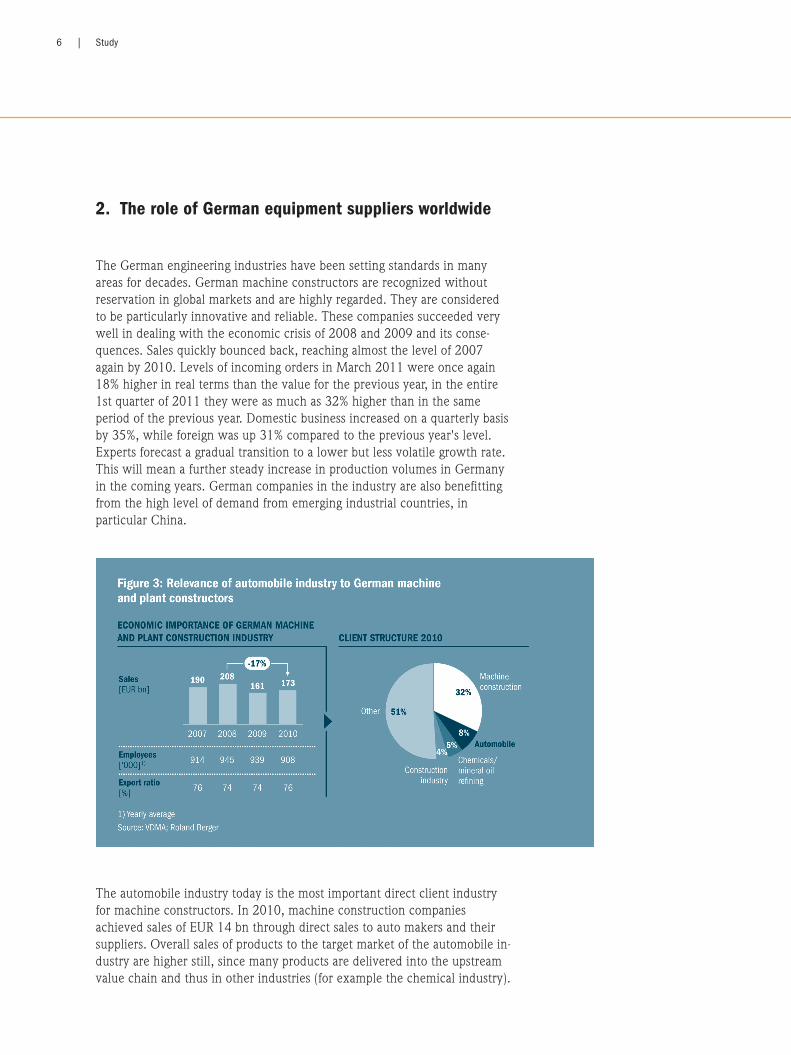

The German engineering industries have been setting standards in many areas for decades. German machine constructors are recognized without reservation in global markets and are highly regarded. They are considered to be particularly innovative and reliable. These companies succeeded very well in dealing with the economic crisis of 2008 and 2009 and its conse-quences. Sales quickly bounced back, reaching almost the level of 2007 again by 2010. Levels of incoming orders in March 2011 were once again 18% higher in real terms than the value for the previous year, in the entire 1st quarter of 2011 they were as much as 32% higher than in the same period of the previous year. Domestic business increased on a quarterly basis by 35%, while foreign was up 31% compared to the previous year's level. Experts forecast a gradual transition to a lower but less volatile growth rate. This will mean a further steady increase in production volumes in Germany in the coming years. German companies in the industry are also benefitting from the high level of demand from emerging industrial countries, in particular China.

The automobile industry today is the most important direct client industry for machine constructors. In 2010, machine construction companies achieved sales of EUR 14 bn through direct sales to auto makers and their suppliers. Overall sales of products to the target market of the automobile in-dustry are higher still, since many products are delivered into the upstream value chain and thus in other industries (for example the chemical industry).

7 | E-Mobility – a promising field for the future

Moreover, many automobile manufacturers and suppliers produce machin-ery and equipment in-house for their production processes which are not included in the statistics for machine construction. Only a few engineering companies in Germany are fully focused on the automobile industry, but for many companies this industry accounts for significant sales, well above their market share in the machine construction sector as a whole. The introduction of batteries and electric motors for automobile propulsion in certain cases requires new skills which German engineering industries have previously deployed only when supplying other industries not related to the automobile industry. This will result in attractive market opportuni-ties for companies who have not previously considered the automobile industry as a possible client. Many technologies that are essential for the production of batteries and electric motors (e.g. coating and automation technology) have been used successfully for years by the German engineer-ing industries. By adapting these technologies to the requirements of the automobile industry, it is possible for German engineering industries to exploit potential demand and open the way to interesting opportunities. At the same time, the suppliers who are in a dominant position today need to consider in strategic terms how they can develop their business model and their product and technology portfolio further to compensate for the fact that, for example, metal machining (turning, milling) will become less important in core product areas of the automobile industry in the future – especially in the powertrain area, where in future value will be created by battery or electric-motor production. There will also be other new forms of value creation as the result of innovations such as the increasing use of new materials to achieve lightweight construction. There will also be cross-technological benefits, for example in mobile machinery. In this way, for example, electrically-driven industrial vehicles such as forklift trucks will benefit from further developments in electric vehicles. The technological changes in the automobile industry are therefore of great importance for the German engineering industries, in particular the introduction of electrically-driven vehicles. Joint ventures between the German engineering industries and German automobile manufacturers will also be a driving force for innovation in machine construction, with a trickle-down benefit to other industries. Ger-man auto makers will in turn also significantly benefit from the wide range of highly specialized suppliers of innovative technology "on their doorstep". The expertise of these specialists will be valuable for the further develop-ment of both products and processes for auto makers. In many cases, a true symbiotic relationship has developed which generates competitive advan-tages for both sides. Significant productivity gains and cost reductions would not be possible without this special relationship.

8 | Study

3. The effects of e-mobility on the German plant equipment manufacturing industry

3.1. Fundamental changes in the automobile industry

3.1.1. E-mobility as a driver of change

The worldwide automobile market will grow strongly in the period up to 2020. It is expected that the number of vehicles sold will rise from 72 million units in 2010 to well over 100 million units. Demand will grow particularly strongly in the BRIC countries (Brazil, Russia, India and China). China has already become the most important single global market for the automobile industry – taking the place of the United States.

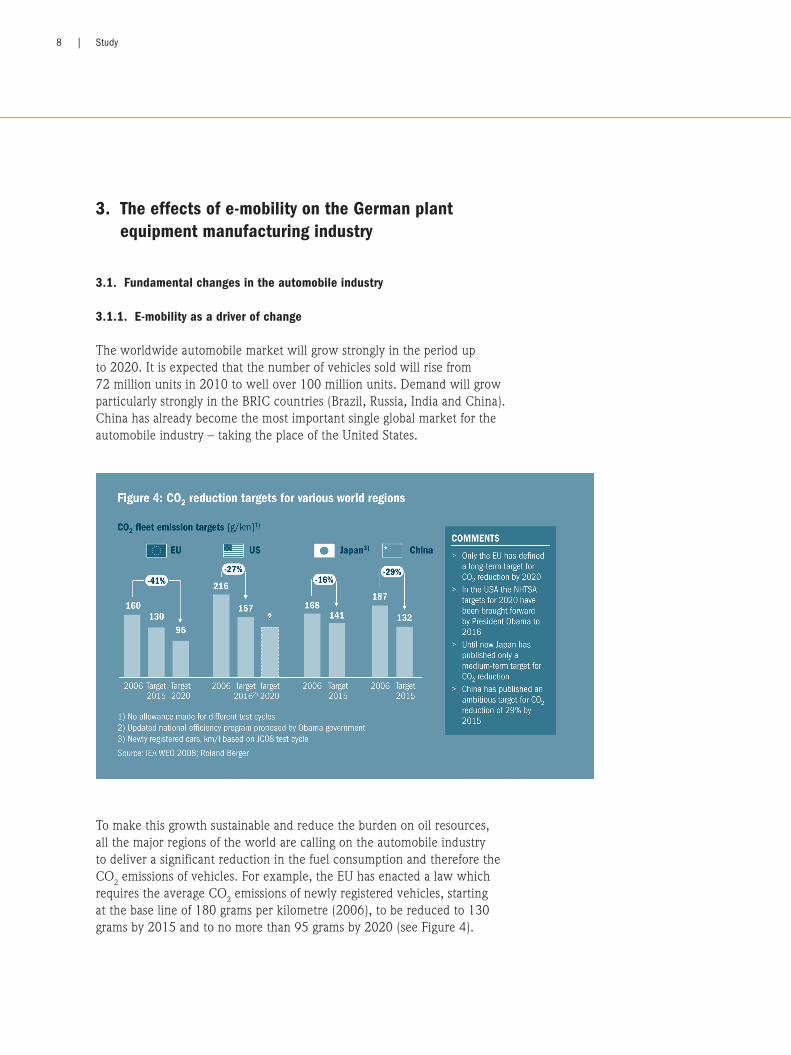

To make this growth sustainable and reduce the burden on oil resources, all the major regions of the world are calling on the automobile industry to deliver a significant reduction in the fuel consumption and therefore the CO2 emissions of vehicles. For example, the EU has enacted a law which requires the average CO2 emissions of newly registered vehicles, starting at the base line of 180 grams per kilometre (2006), to be reduced to 130 grams by 2015 and to no more than 95 grams by 2020 (see Figure 4).

9 | E-Mobility – a promising field for the future

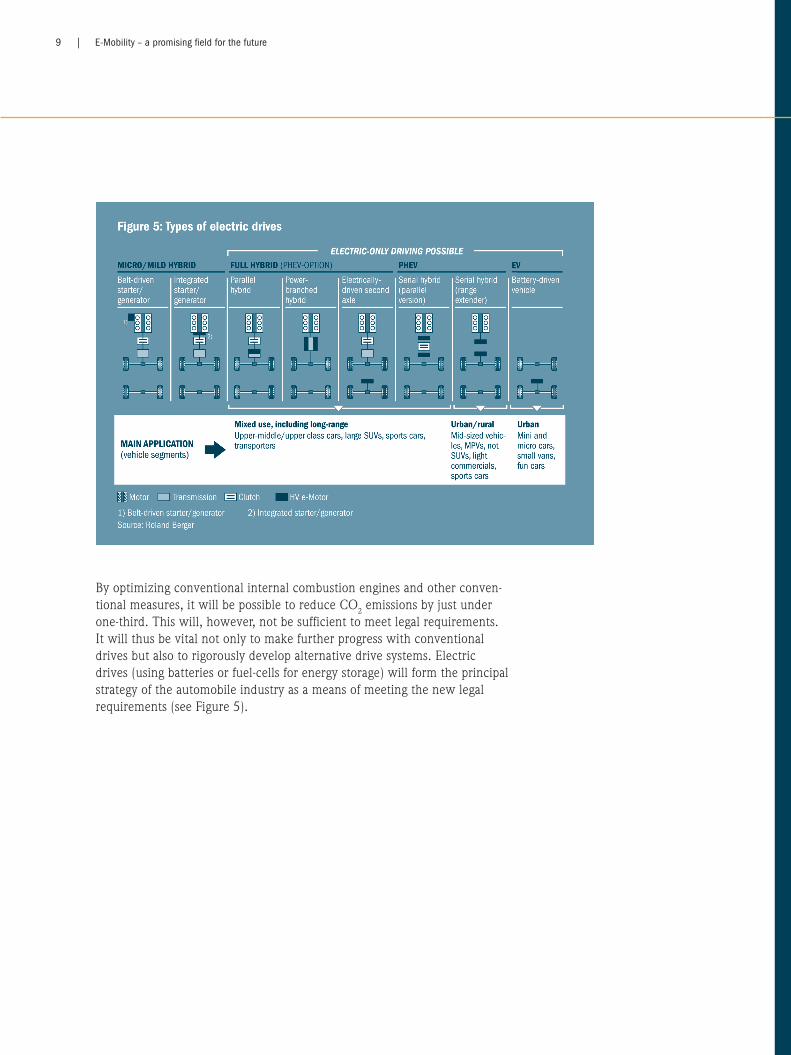

By optimizing conventional internal combustion engines and other conven-tional measures, it will be possible to reduce CO2 emissions by just under one-third. This will, however, not be sufficient to meet legal requirements. It will thus be vital not only to make further progress with conventional drives but also to rigorously develop alternative drive systems. Electric drives (using batteries or fuel-cells for energy storage) will form the principal strategy of the automobile industry as a means of meeting the new legal requirements (see Figure 5).

10 | Study

By the year 2025 the proportion of new vehicle registrations accounted for by wholly or partially electric vehicles will increase to 50%. The market will be dominated not by all-electric vehicles but by hybrid vehicles (in cluding range extenders). For the foreseeable future, all-electric vehicles will be successful for short-haul and fleet use (e.g. use in urban areas, delivery ser-vices), since the specific characteristics of these concepts do not allow their widespread use over long distances and in continuous operation as a repla-cement for vehicles with internal combustion engines. Increasing bat tery range and reducing battery costs are therefore the key factors for success in the rapid spread of electric drives and an increase in the level of customer acceptance. Machine constructors can make a significant contribution to achieving these objectives through intelligent, cost-reducing production technologies, since about 50% of the production costs of batteries are due to the manufacturing process.

3.1.2. The shift in competence/production capacity for electric powertrain components

With the increasing proliferation of electric drive components, new compe-tences are required with regard to production technologies and capacities for electric components. The position today is that the internal combustion engine is one of the primary competences of automobile manufacturers and an integral part of their brand identities.

11 | E-Mobility – a promising field for the future

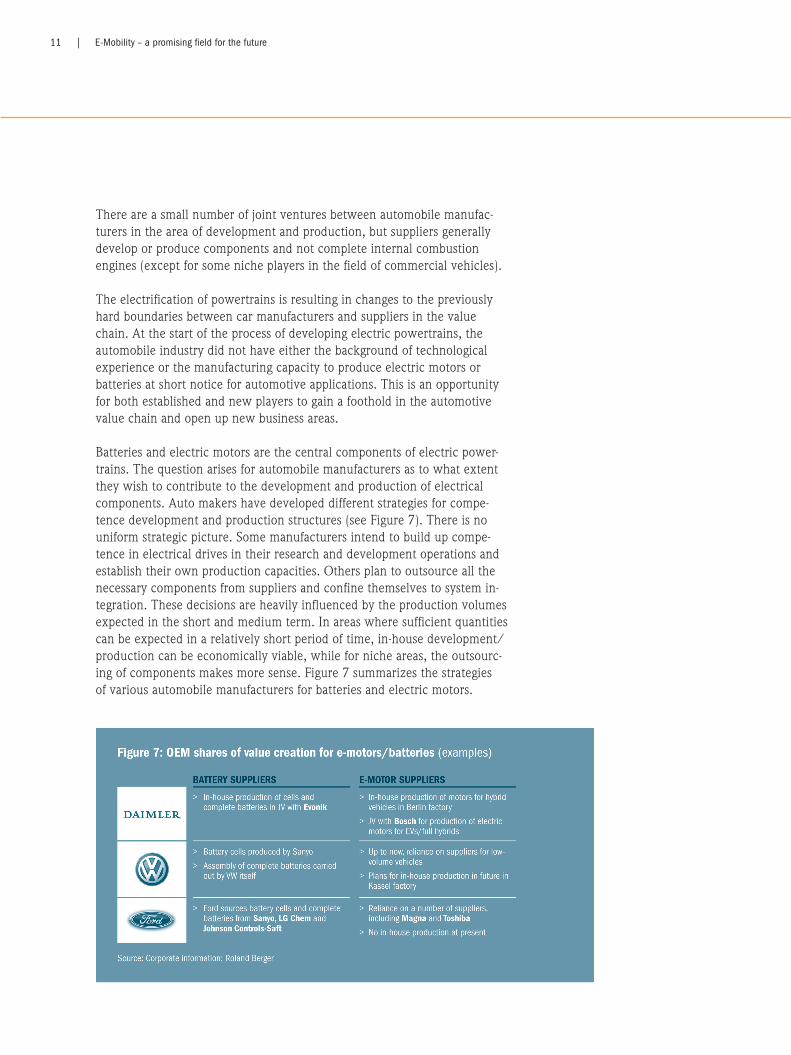

There are a small number of joint ventures between automobile manufac-turers in the area of development and production, but suppliers generally develop or produce components and not complete internal combustion engines (except for some niche players in the field of commercial vehicles). The electrification of powertrains is resulting in changes to the previously hard boundaries between car manufacturers and suppliers in the value chain. At the start of the process of developing electric powertrains, the automobile industry did not have either the background of technological experience or the manufacturing capacity to produce electric motors or batteries at short notice for automotive applications. This is an opportunity for both established and new players to gain a foothold in the automotive value chain and open up new business areas. Batteries and electric motors are the central components of electric power-trains. The question arises for automobile manufacturers as to what extent they wish to contribute to the development and production of electrical components. Auto makers have developed different strategies for compe-tence development and production structures (see Figure 7). There is no uniform strategic picture. Some manufacturers intend to build up compe-tence in electrical drives in their research and development operations and establish their own production capacities. Others plan to outsource all the necessary components from suppliers and confine themselves to system in-tegration. These decisions are heavily influenced by the production volumes expected in the short and medium term. In areas where sufficient quantities can be expected in a relatively short period of time, in-house development/production can be economically viable, while for niche areas, the outsourc-ing of components makes more sense. Figure 7 summarizes the strategies of various automobile manufacturers for batteries and electric motors.

12 | Study

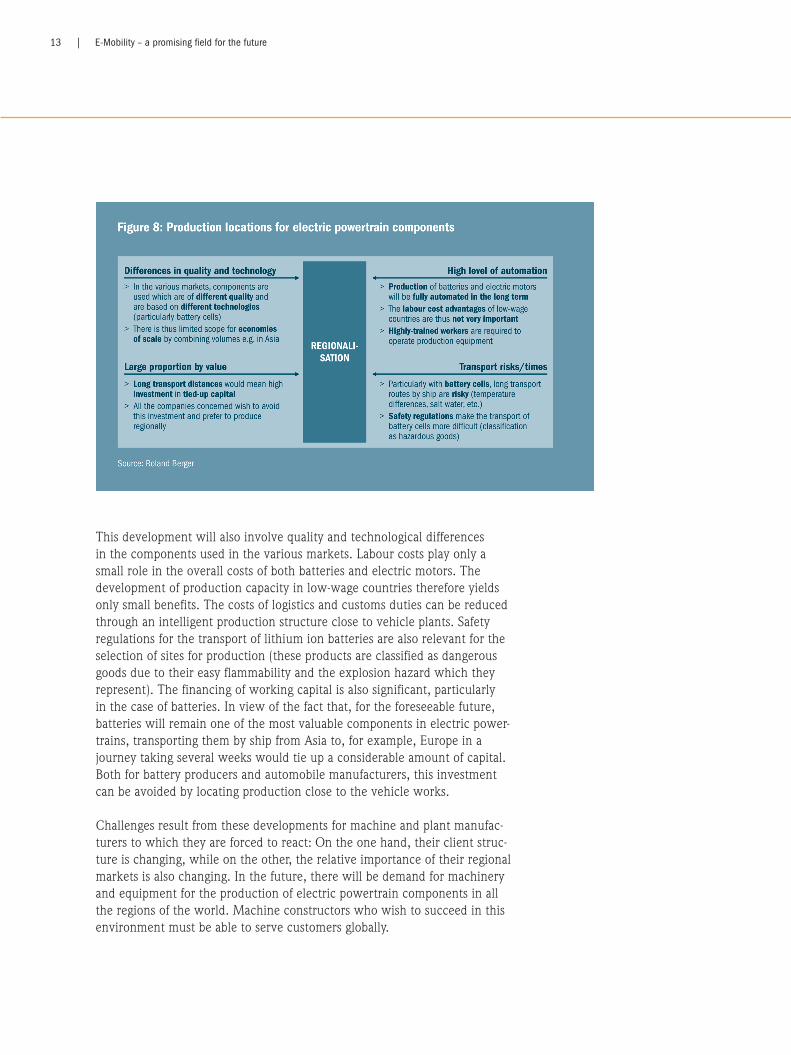

Daimler Benz, for example, produces batteries via a joint venture with Evonik, electric motors for hybrid vehicles in its own factory in Berlin (high expected volume) and the associated electric motors for all-electric vehicles through a joint venture with Bosch (low expected volume, sale to a third party currently under discussion). Volkswagen, on the other hand, plans to produce all the electric motors it needs at its plant in Kassel, while obtaining battery cells from suppliers. Ford plans to rely on suppliers for all groups. Benefiting from the subsidy policy of the US Government, General Motors is investing a total of approx. EUR 165 m in the construction of electric motor production facilities at three locations. This illustrates the various strategies of a number of automobile manufacturers which are aimed at helping these companies to retain their share of automobile value creation in the future. In the light of this change in the value chain, the question arises as to the future position of engineering companies: Who will be the client in the fu-ture, automobile manufacturers or suppliers? In the long term, auto makers will build up "in-house" expertise for the development of the most important components (in particular batteries and electric motors) of electric power-trains in order not to compromise their position in the product definition process and the value chain. The increased involvement of suppliers in the development and production of complete powertrain components will increase the diversity of its clients from the point of view of engineering industries. Engineering companies must accept that there will in future be established customers in powertrain development and production both among automobile manufacturers and also among automotive suppliers and new market players, e.g. suppliers of battery cells and electric motors. The regional distribution of the production of components for electric powertrains is also very important for machine and plant manufacturers. Despite the current heavy concentration of manufacturing capacity – in particular for battery cells – in Asia, production will in the long term spring up in the various vehicle market areas, in other words also in Europe and the United States. At the moment, components for electric drives are pro-duced mainly in Asia, since this is where demand has been concentrated so far. Several factors will lead to a situation in which the value chain takes on a new shape and production is spread around the world on a regional basis (see Figure 8).

13 | E-Mobility – a promising field for the future

This development will also involve quality and technological differences in the components used in the various markets. Labour costs play only a small role in the overall costs of both batteries and electric motors. The development of production capacity in low-wage countries therefore yields only small benefits. The costs of logistics and customs duties can be reduced through an intelligent production structure close to vehicle plants. Safety regulations for the transport of lithium ion batteries are also relevant for the selection of sites for production (these products are classified as dangerous goods due to their easy flammability and the explosion hazard which they represent). The financing of working capital is also significant, particularly in the case of batteries. In view of the fact that, for the foreseeable future, batteries will remain one of the most valuable components in electric power-trains, transporting them by ship from Asia to, for example, Europe in a journey taking several weeks would tie up a considerable amount of capital. Both for battery producers and automobile manufacturers, this investment can be avoided by locating production close to the vehicle works. Challenges result from these developments for machine and plant manufac-turers to which they are forced to react: On the one hand, their client struc-ture is changing, while on the other, the relative importance of their regional markets is also changing. In the future, there will be demand for machinery and equipment for the production of electric powertrain components in all the regions of the world. Machine constructors who wish to succeed in this environment must be able to serve customers globally.

14 | Study

The German engineering industries have in the past demonstrated impres-sively that it can meet these challenges. Exporting over 70% of their produc-tion, German machinery suppliers have been delivering international service and product support for many years. Individual companies which wish, for example, to supply machines for the battery production to all the global markets must be sure that they can also meet these demands.

3.1.3. Need for changes in engineering industries

New electric drive components require new production technologies which have previously been used very little if at all in the automobile industry, for example technology for coating battery electrodes. There will also be a shift in the weighting of the various production technologies. In the past in the automobile industry, particularly in powertrain production, metal processing has been of great importance (shaping and machining), but in the future other technologies will be used, especially in battery production (for examp-le for mixing and coating). Many suppliers will need to adjust their existing technology portfolio with regard to these changes in order to be successful players in the new markets. These changes will also mean that the plant equipment manufacturers who have previously played an important role in the automobile industry will in future not automatically benefit to an equal extent from developments and retain the same market share as before. Rather, the new technological requirements will result in new niches for new suppliers. Companies from other industries with technology which is now relevant to the automobile industry can take the opportunity to open up new areas of business. Ger-man engineer ing industries have in the past opened the way to many new clients and markets through innovative developments (e.g. the photovoltaic industry). This strength in responding to changes must also be deployed in the field of e-mobility. The following case studies highlight the technological and business challen-ges in production facilities for battery cells and electric motors, reflecting the fact that it is in these two areas that the most important technological chan-ges and future market potential are expected. The main focus is on identify-ing core process steps in production and the current competitive challenges affecting engineering industries.

15 | E-Mobility – a promising field for the future

3.2. Case study: Battery production

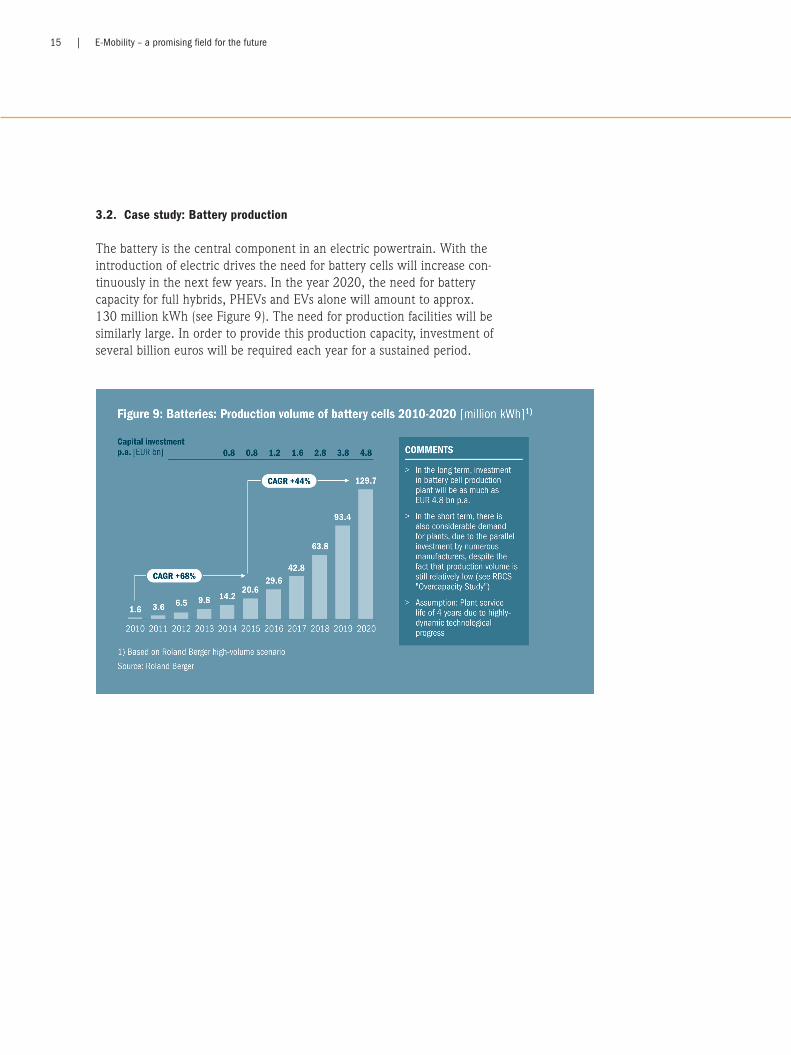

The battery is the central component in an electric powertrain. With the introduction of electric drives the need for battery cells will increase con-tinuously in the next few years. In the year 2020, the need for battery capacity for full hybrids, PHEVs and EVs alone will amount to approx. 130 million kWh (see Figure 9). The need for production facilities will be similarly large. In order to provide this production capacity, investment of several billion euros will be required each year for a sustained period.

16 | Study

3.2.1. Battery cells for E-mobility - cell structure and major components

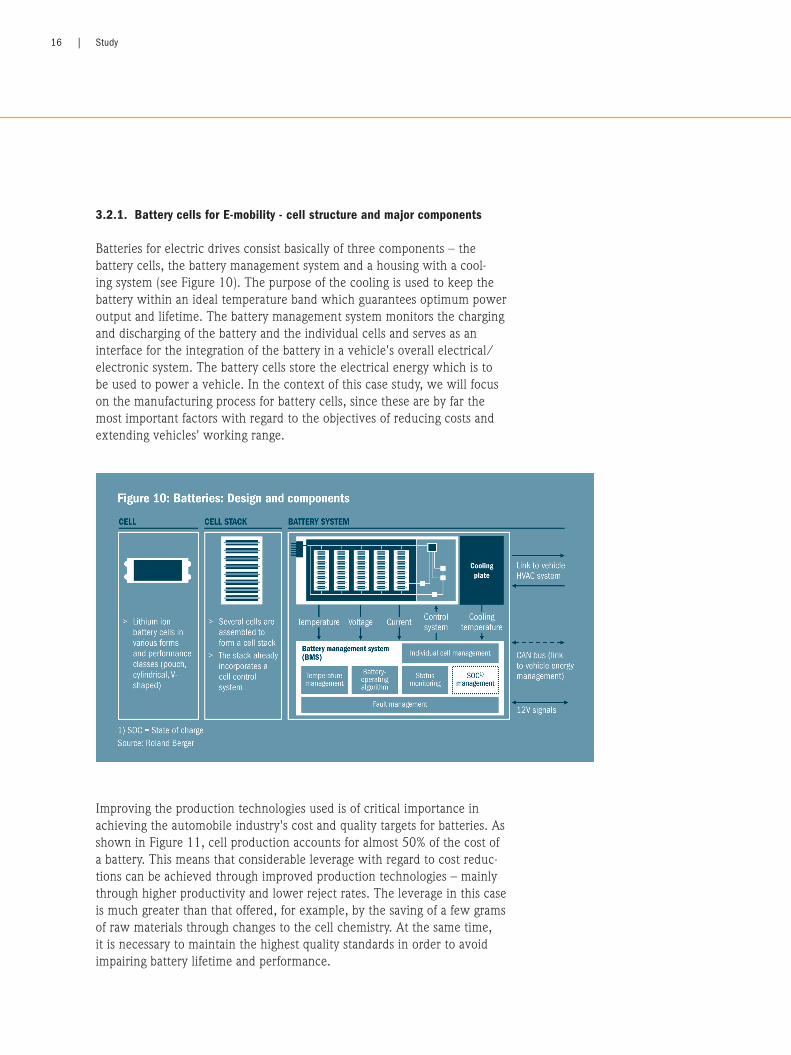

Batteries for electric drives consist basically of three components – the battery cells, the battery management system and a housing with a cool-ing system (see Figure 10). The purpose of the cooling is used to keep the battery within an ideal temperature band which guarantees optimum power output and lifetime. The battery management system monitors the charging and discharging of the battery and the individual cells and serves as an interface for the integration of the battery in a vehicle's overall electrical/electronic system. The battery cells store the electrical energy which is to be used to power a vehicle. In the context of this case study, we will focus on the manufacturing process for battery cells, since these are by far the most important factors with regard to the objectives of reducing costs and ex tending vehicles' working range.

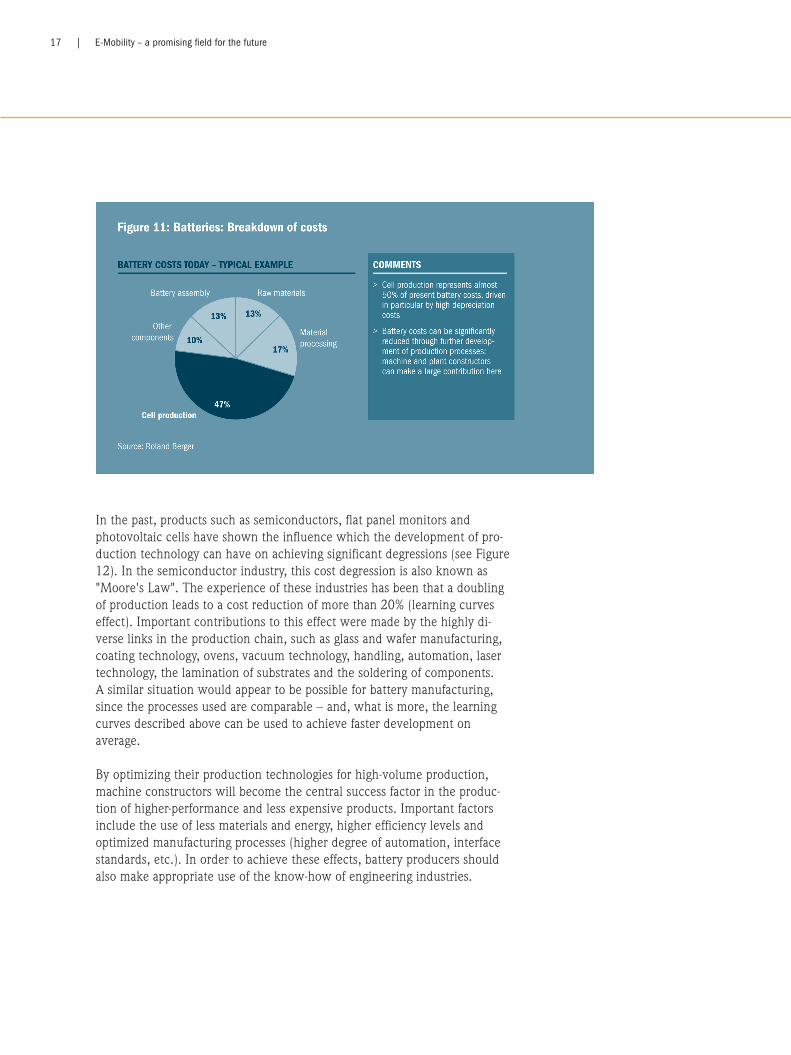

Improving the production technologies used is of critical importance in achieving the automobile industry's cost and quality targets for batteries. As shown in Figure 11, cell production accounts for almost 50% of the cost of a battery. This means that considerable leverage with regard to cost reduc-tions can be achieved through improved production technologies – mainly through higher productivity and lower reject rates. The leverage in this case is much greater than that offered, for example, by the saving of a few grams of raw materials through changes to the cell chemistry. At the same time, it is necessary to maintain the highest quality standards in order to avoid impairing battery lifetime and performance.

17 | E-Mobility – a promising field for the future

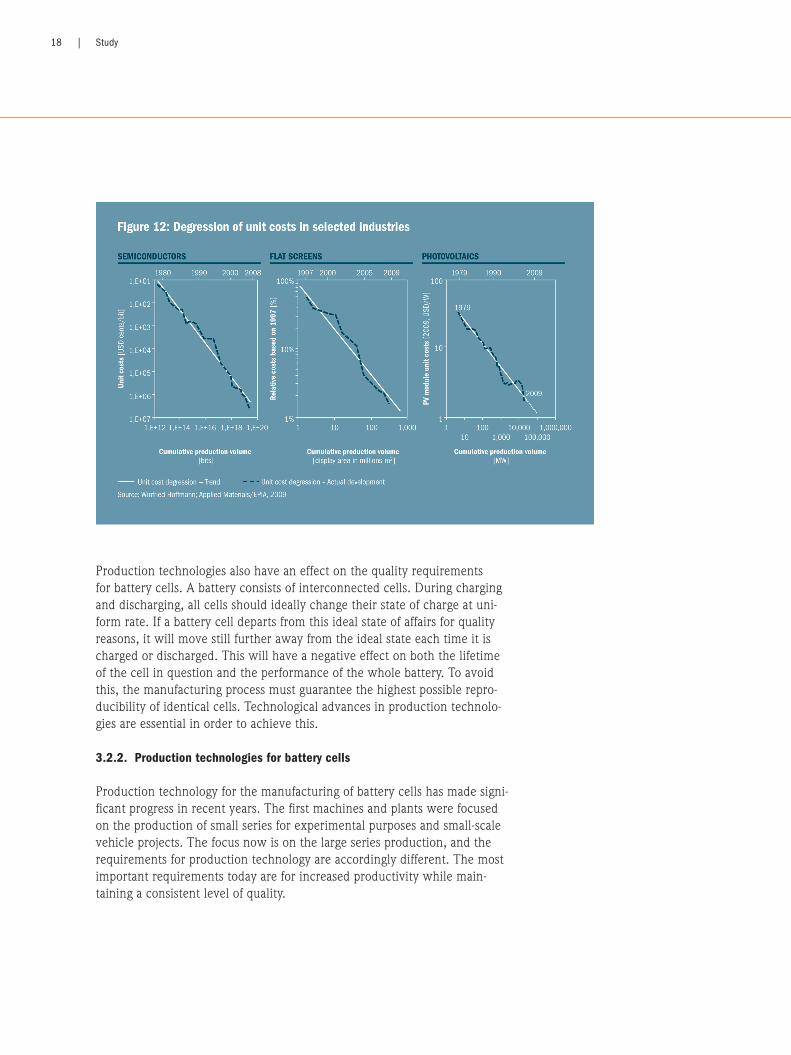

In the past, products such as semiconductors, flat panel monitors and photovoltaic cells have shown the influence which the development of pro-duction technology can have on achieving significant degressions (see Figure 12). In the semiconductor industry, this cost degression is also known as "Moore's Law". The experience of these industries has been that a doubling of production leads to a cost reduction of more than 20% (learning curves effect). Important contributions to this effect were made by the highly di-verse links in the production chain, such as glass and wafer manufacturing, coating technology, ovens, vacuum technology, handling, automation, laser technology, the lamination of substrates and the soldering of components. A similar situation would appear to be possible for battery manufacturing, since the processes used are comparable – and, what is more, the learning curves described above can be used to achieve faster development on average. By optimizing their production technologies for high-volume production, machine constructors will become the central success factor in the produc-tion of higher-performance and less expensive products. Important factors include the use of less materials and energy, higher efficiency levels and optimized manufacturing processes (higher degree of automation, interface standards, etc.). In order to achieve these effects, battery producers should also make appropriate use of the know-how of engineering industries.

18 | Study

Production technologies also have an effect on the quality requirements for battery cells. A battery consists of interconnected cells. During charging and discharging, all cells should ideally change their state of charge at uni-form rate. If a battery cell departs from this ideal state of affairs for quality reasons, it will move still further away from the ideal state each time it is charged or discharged. This will have a negative effect on both the lifetime of the cell in question and the performance of the whole battery. To avoid this, the manufacturing process must guarantee the highest possible repro-ducibility of identical cells. Technological advances in production technolo-gies are essential in order to achieve this.

3.2.2. Production technologies for battery cells

Production technology for the manufacturing of battery cells has made signi-ficant progress in recent years. The first machines and plants were focused on the production of small series for experimental purposes and small-scale vehicle projects. The focus now is on the large series production, and the requirements for production technology are accordingly different. The most important requirements today are for increased productivity while main-taining a consistent level of quality.

19 | E-Mobility – a promising field for the future

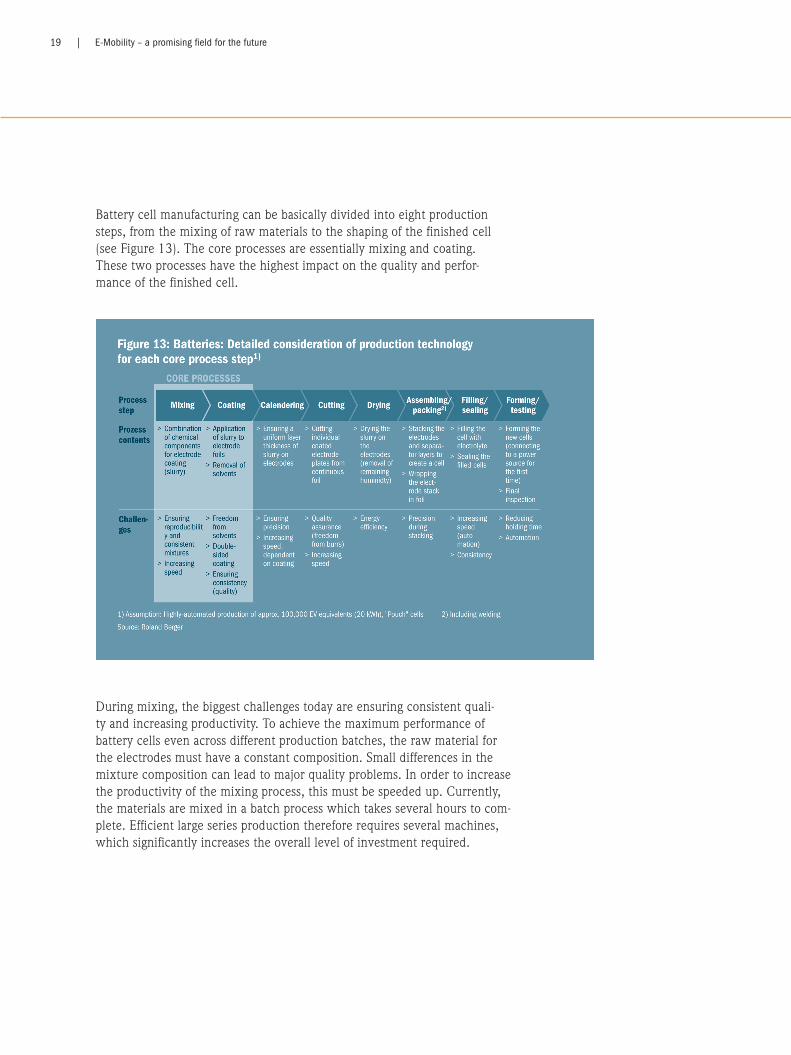

Battery cell manufacturing can be basically divided into eight production steps, from the mixing of raw materials to the shaping of the finished cell (see Figure 13). The core processes are essentially mixing and coating. These two processes have the highest impact on the quality and perfor-mance of the finished cell.

During mixing, the biggest challenges today are ensuring consistent quali-ty and increasing productivity. To achieve the maximum performance of battery cells even across different production batches, the raw material for the electrodes must have a constant composition. Small differences in the mixture composition can lead to major quality problems. In order to increase the productivity of the mixing process, this must be speeded up. Currently, the materials are mixed in a batch process which takes several hours to com-plete. Efficient large series production therefore requires several machines, which significantly increases the overall level of investment required.

20 | Study

The requirements are similar for coating, Once again, the objective is to keep the reproducibility of the cells within close tolerances, while at the same time significantly increasing machine throughput. Attempts are already being made to carry out double-sided coating in order to coat large areas in a single pass. It is also planned to increase the throughput speed of coating machines, but this is subject to physical limitations. The flow rate of the slurry (the chemical compounds that are applied to the electrode films) is relatively low, which places an upward limit on the potential coating speed. New types of coating processes could allow significant improvements in productivity. The decoupling of the coating process from solvents is another challenge. Today, solvent is mixed with the slurry in order to guarantee the correct viscosity. This, however, results in high costs, in particular for solvent recovery, which could be reduced by solvent-free processes. In subsequent processes, too, the emphasis is usually on ensuring consistent quality, which is often in conflict with efforts to exploit direct potential for cost reduction. It is necessary, for example, to find a way of reducing wear with the cutter blades currently used. Blunt blades result in burrs on the outside of the electrodes that can affect the performance of the battery in the long term. New production techniques (e.g. laser cutting), could allow quantum leaps in quality to be achieved. With regard to forming, on the other hand, the focus is mainly on reducing holding times. Currently, the finished battery cells have to be formed for up to 24 hours. In view of the fact that daily production is thousands of cells, the costs (primarily the in-vestment in high-bay warehouses) are considerable. By reducing the holding time through better forming processes and equipment to about 10 hours, the investment required for battery production could be reduced significant-ly. Further development of production technology by engineering industries can make a decisive contribution to achieving the quality objectives of the automobile industry and creating productivity gains by reducing reject rates.

3.2.3. Market overview for specific machines/technologies: Main competitors

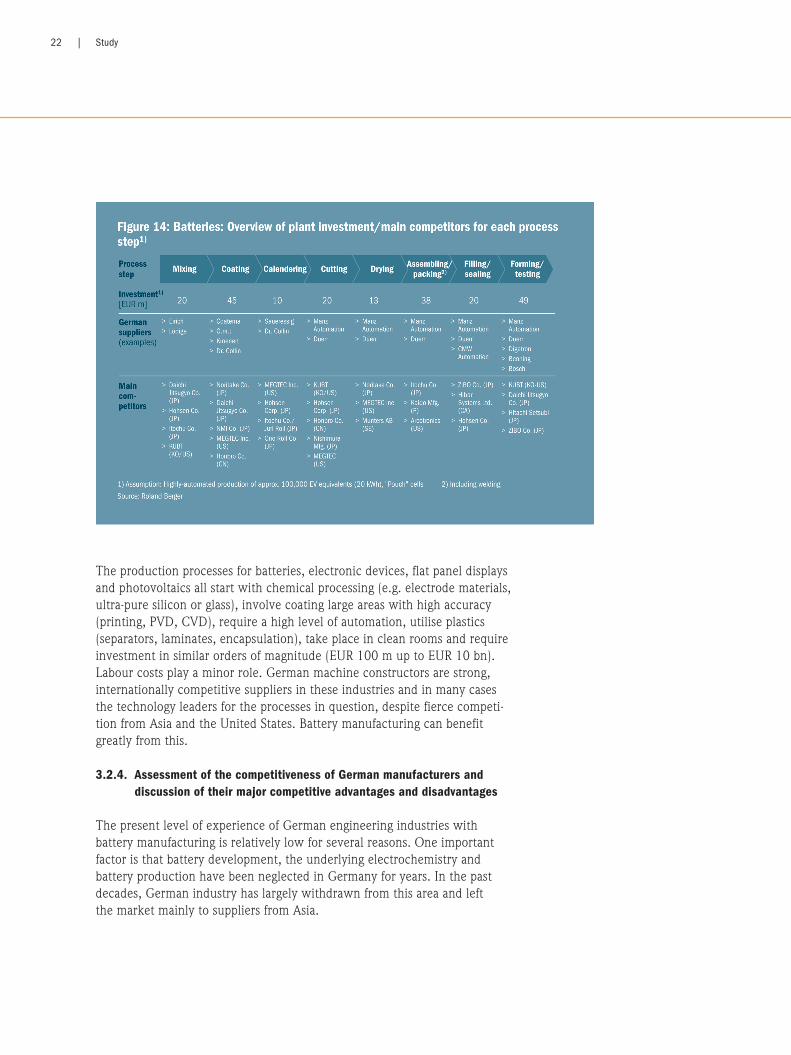

The plant shown in Figure 13, with a capacity of approx. 100,000 EV equivalents (20 kWh battery capacity) would require an investment today of approx. EUR 200 m. The processes requiring the most investment are coating and formation, at EUR 45 m each. Compared to the cost of production equipment for semiconductors and flat panel displays, which are several billion euros, production facilities for battery cells are thus relatively inexpensive.

21 | E-Mobility – a promising field for the future

However a number of production lines must be operated in parallel in order to produce large quantities parallel, which considerably increases the need for machines. The short innovation cycles in such a young manufacturing industry have increased the need for reliable high-performance manufactur-ing facilities. These will expand the market for battery production solutions over all and thus increase the potential for machine constructors in this sector. The market for machinery and equipment for the production of battery cells is today dominated by Asian manufacturers (see Figure 14). For all core processes, there are usually a number of suppliers from Japan, which is also are perceived by customers as being the most important supplier in the market. Moreover, companies from the United States, Korea, and now China have established themselves in this market in recent years. In the process chain as a whole, German companies are still relatively weakly represented. For the individual process steps (e.g. coating), however, Germany does have individual suppliers who are technologically competitive. Until now almost no company has offered a complete system for battery production which combines their own and third-party systems. The major Japanese suppliers, however, try to offer as large a part of the process chain as possible from a single source through their own developments or joint ventures with other suppliers. In Germany, this function is provided by system integrators, who combine machines from different suppliers to form production facilities as requested by their clients. From the customer's point of view, German suppliers are also regarded as not well established and enjoy only low levels of customer awareness. The reasons for this are not so much technological weaknesses as lack of recognition and the fact that many suppliers have entered the market only relatively recently. The position of German machine constructors in flat panel display manufac-turing was very similar in the 1990s. In photovoltaics, however, machine constructors were quick to realise that the ability to offer turnkey factories is a major competitive advantage, particularly in the development phase of an industry. Machine constructors grew in this industry along with their major customers. Machine constructors may also succeed in achieving this in bat-tery production. The expected demand for innovative production solutions alone will help German machine constructors expand their business in this field if the correct conditions are created and the experience is used which has been gained with other industries such as electronics, flat panel display and photovoltaics manufacturing.

22 | Study

The production processes for batteries, electronic devices, flat panel displays and photovoltaics all start with chemical processing (e.g. electrode materials, ultra-pure silicon or glass), involve coating large areas with high accuracy (printing, PVD, CVD), require a high level of automation, utilise plastics (separators, laminates, encapsulation), take place in clean rooms and require investment in similar orders of magnitude (EUR 100 m up to EUR 10 bn). Labour costs play a minor role. German machine constructors are strong, internationally competitive suppliers in these industries and in many cases the technology leaders for the processes in question, despite fierce competi-tion from Asia and the United States. Battery manufacturing can benefit greatly from this.

3.2.4. Assessment of the competitiveness of German manufacturers and discussion of their major competitive advantages and disadvantages

The present level of experience of German engineering industries with battery manufacturing is relatively low for several reasons. One important factor is that battery development, the underlying electrochemistry and battery production have been neglected in Germany for years. In the past decades, German industry has largely withdrawn from this area and left the market mainly to suppliers from Asia.

23 | E-Mobility – a promising field for the future

This has had an effect on machine construction. Without local product development and production, machine construction in this area could not evolve and the machine construction industry focused on other markets. This industry was therefore not able to fully follow the evolutionary leap to lithium ion batteries. Today, the production technology for lithium ion batteries is mainly domi-nated by suppliers from Asia. These benefit from many years of experience in the production of lithium ion batteries for consumer goods such as laptops and MP3 players. From this business segment, they are well acquainted with the basic requirements of battery production and have been able to transfer this knowledge to new installations for automotive battery production. Ex-perience from the production of consumer batteries is, however, of limited relevance to automotive batteries. These two fields differ both in terms of quality and lifetime (significant reduction in fault rate) and the production process itself (e.g. much larger electrodes). The pioneering role of the Asian automobile manufacturers (e.g. Toyota, BYD) has been considerable in building up battery production capacity, which gave Asian machine constructors an early opportunity to gather practical experience in the automobile industry and to develop their machines further. What is more, many machine constructors in Japan are financially linked to automobile manufacturers via "keiretsu", giving them significantly easier access to product development and the corresponding volume of orders. German engineering industries have in recent years rediscovered battery production as a relevant business area, driven among other things by the discussion concerning e-mobility. Certain companies from technologically related fields (e.g. coating, packaging, electronics) have begun to look for attractive niches in the field of battery production. In the meantime, Ger-man manufacturers are able to cover all the steps in production. However, for the majority of suppliers, battery production is a marginal business that generates only a small part of their turnover. The investment which they are able to make in the development of equipment and technologies is there-fore relatively low. This, combined with the fact that there is little or no existing local production of battery cells in Germany or the rest of Europe, means that machine constructors have difficulties to build up an appropriate volume of experience which would allow them to compete with suppliers from Asia.

24 | Study

The present situation in battery production is therefore difficult for the German machine construction industry: Strong competition from Japan, distance from the client industry in some cases, continuously evolving pro-ducts and high costs for research and development. However, German com-panies will be able to gain access to battery production, an important growth market, if they draw on and expand their strengths. Firstly, they can exploit their experience of the application of production technologies in other indus-tries, and secondly, further development steps can be expected in the next several years in lithium ion batteries which will open up new opportunities for innovative companies in the field of production technology.

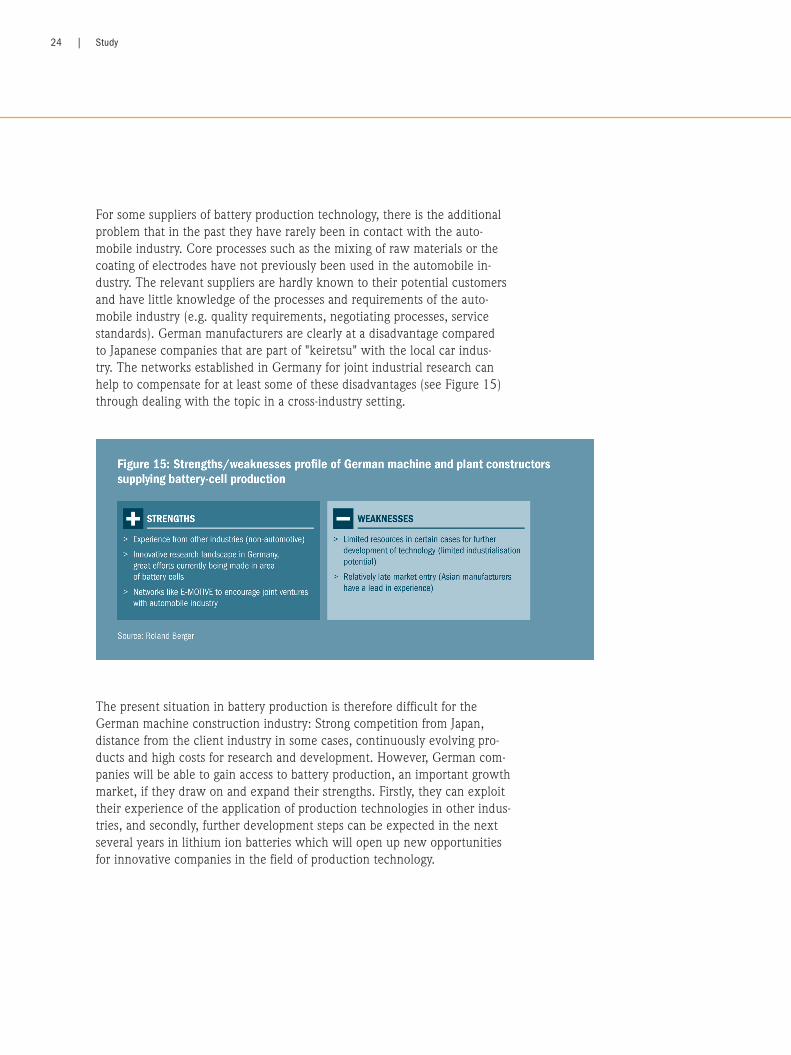

For some suppliers of battery production technology, there is the additional problem that in the past they have rarely been in contact with the auto-mobile industry. Core processes such as the mixing of raw materials or the coating of electrodes have not previously been used in the automobile in-dustry. The relevant suppliers are hardly known to their potential customers and have little knowledge of the processes and requirements of the auto-mobile industry (e.g. quality requirements, negotiating processes, service standards). German manufacturers are clearly at a disadvantage compared to Japanese companies that are part of "keiretsu" with the local car indus-try. The networks established in Germany for joint industrial research can help to compensate for at least some of these disadvantages (see Figure 15) through dealing with the topic in a cross-industry setting.

25 | E-Mobility – a promising field for the future

German engineering industries have demonstrated in the past (e.g. in the photovoltaics industry) that they can successfully establish themselves in a similarly challenging environment. The successful networks formed to promote co-operations at a pre-competitive stage with the automobile industry, such as E-MOTIVE in the VDMA, also allow the smaller companies in machine construction to discuss new technologies with the automobile industry and to conduct joint research at low risk.

3.2.5. General assessment of the importance of the technology for Germany as a location for plant equipment manufacturers

As described above, the German mechanical engineering has traditionally been strong in the automobile industry. Precisely for this reason, good positioning with regard to production technology for the manufacturing of battery cells is essential. In view of the fact that batteries will become one of the most important components for the future of automotive engineering, German plant equipment manufacturing industries should also position themselves strongly in this area in order to secure access to a business area which will be technologically significant in the long term. The German automobile industry will also have an interest in building up a local supplier base for machines and plants to prevent a loss of know-how. Ultimately, European automobile manufacturers or suppliers who developed a new battery technology would be reluctant to share this knowledge with Asian machine constructors who are linked via a "keiretsu" to major competitors. Close cooperation between the German automobile industry with the local engineering industry can help to avoid these conflicts. In the medium to long term, machines and plants for the production of batteries for electric drives will become a very interesting business area for the German suppliers. In view of the level of investment required (about EUR 200 m for a plant for the production of 100,000 EV batteries) and the predicted future growth in the market for batteries, it can be expected that the market for machinery of this kind will grow in the next few years to several billion euros. Moreover, the short innovation cycles both in produc-tion facilities and in the battery cells to be produced will generate consider-able demand for machines. As battery costs are currently one of the biggest obstacles to the introduction of electrically-driven vehicles, battery produc-ers are very interested in converting their machinery as soon as possible, as soon as new efficient production technologies with a potential for cost reduction are available.

26 | Study

An obstacle to the rapid replacement of machinery and the continuous evolution of production technology can be the long depreciation periods for production facilities. In view of the high investment costs involved, replacement of machinery before the end of the amortization period would not seem sensible from the operator's point of view. This could in turn slow down the development of battery technology and the process of optimizing production technologies. The introduction of declining-balance depreciation would therefore send an important message to potential investors which would have an immediate effect on investment decisions by entrepreneurs, since it would increase the return on investment and significantly relax the liquidity situation of the companies involved. Modular production concepts, which allow technology upgrades without replacing entire plants, could also make a valuable contribution. It is also important for the German engineering industries that "anchor investments" should be made in the production of battery cells. Even if the volume of investment was relatively limited in the short term, the expansion of capacity which can be expected in the longer term would mean that con-tinuous renewal of production facilities would create considerable market potential in the domestic market. At the same time, battery production in Germany would facilitate the further development of core competences, thanks to the close proximity to local producers and close cooperation with these, thus forming the basis for further global business.

3.3. Case study: Electric motor production

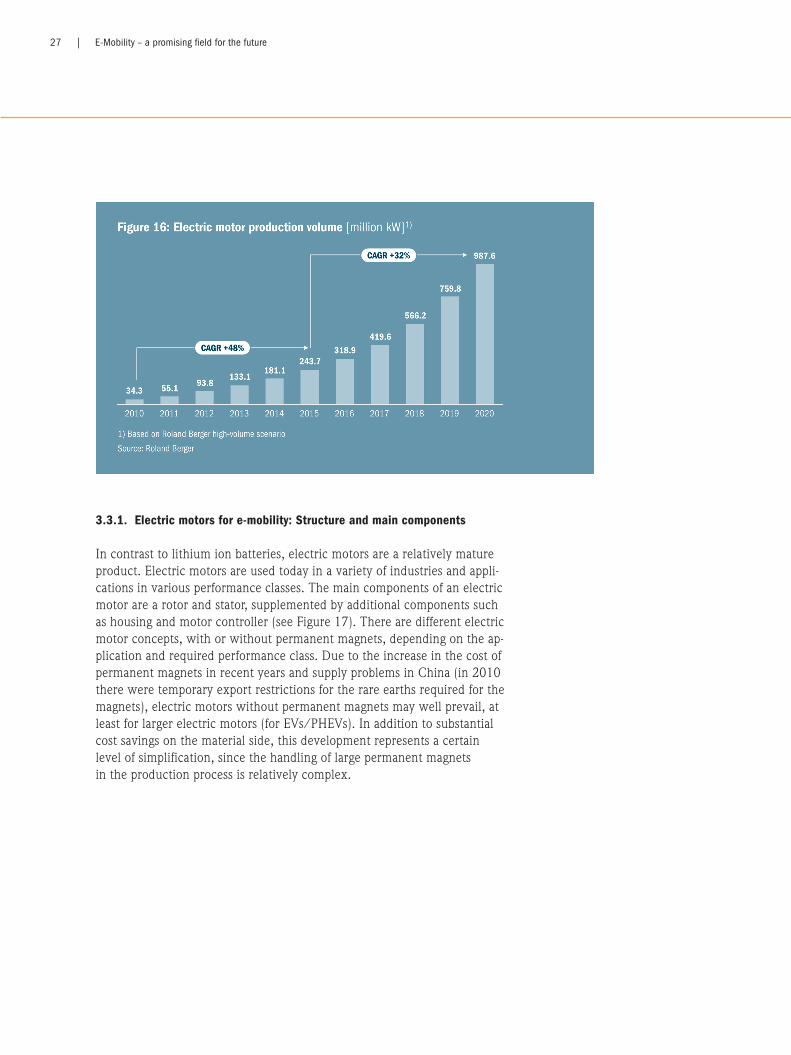

Electric motors can already be found today in many vehicles, for example as part of electric seat adjustment mechanisms. However, they have been used only as auxiliary units so far and have not been regarded by consumers as "characteristic" vehicle components. This situation will change radically with the introduction of electric powertrains. In recent years, the auto-mobile industry has focused strongly on electric motors as drive components in order to optimize these for automobile applications with regard to per-formance, cost, quality and operating conditions. In view of the expected volume of electric motor production in 2020, with approx. 990 million kW of combined performance (full hybrids, PHEVs and EVs), there is consider-able market potential for engineering industries to support these optimiza-tion efforts with innovative production technology (see Figure 16).

27 | E-Mobility – a promising field for the future

3.3.1. Electric motors for e-mobility: Structure and main components

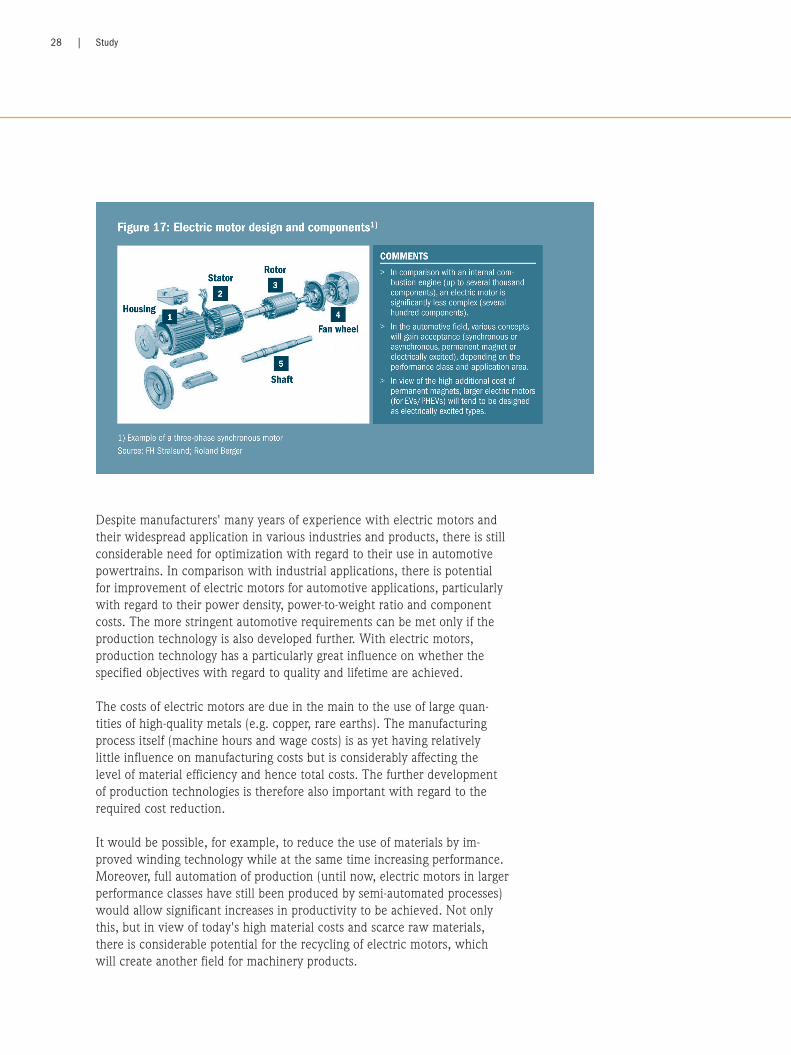

In contrast to lithium ion batteries, electric motors are a relatively mature product. Electric motors are used today in a variety of industries and appli-cations in various performance classes. The main components of an electric motor are a rotor and stator, supplemented by additional components such as housing and motor controller (see Figure 17). There are different electric motor concepts, with or without permanent magnets, depending on the ap-plication and required performance class. Due to the increase in the cost of permanent magnets in recent years and supply problems in China (in 2010 there were temporary export restrictions for the rare earths required for the magnets), electric motors without permanent magnets may well prevail, at least for larger electric motors (for EVs/PHEVs). In addition to substantial cost savings on the material side, this development represents a certain level of simplification, since the handling of large permanent magnets in the production process is relatively complex.

28 | Study

Despite manufacturers' many years of experience with electric motors and their widespread application in various industries and products, there is still considerable need for optimization with regard to their use in automotive powertrains. In comparison with industrial applications, there is potential for improvement of electric motors for automotive applications, particularly with regard to their power density, power-to-weight ratio and component costs. The more stringent automotive requirements can be met only if the production technology is also developed further. With electric motors, production technology has a particularly great influence on whether the specified objectives with regard to quality and lifetime are achieved. The costs of electric motors are due in the main to the use of large quan-tities of high-quality metals (e.g. copper, rare earths). The manufacturing process itself (machine hours and wage costs) is as yet having relatively little influence on manufacturing costs but is considerably affecting the level of material efficiency and hence total costs. The further development of production technologies is therefore also important with regard to the required cost reduction. It would be possible, for example, to reduce the use of materials by im-proved winding technology while at the same time increasing performance. Moreover, full automation of production (until now, electric motors in larger performance classes have still been produced by semi-automated processes) would allow significant increases in productivity to be achieved. Not only this, but in view of today's high material costs and scarce raw materials, there is considerable potential for the recycling of electric motors, which will create another field for machinery products.

29 | E-Mobility – a promising field for the future

The biggest upheaval will result from the changing requirement profiles in the automobile industry: The quality requirements for drive technology and thus electric motors are fundamentally different from the requirements for industrial applications. In industry, electric motors are to a large extent used in stationary applications (e.g. machine tools), are subject to virtually no environmental influences (e.g. temperatures in production halls are almost constant), and are regularly maintained. Operating conditions in a car are fundamentally different: Mobile use under a wide range of climatic and weather conditions (e.g. temperature fluctuations between summer and winter, salting of road surfaces in the winter) and irregular maintenance intervals and facilities. In order to meet the high quality requirements of the automobile industry, the manufacturing processes must also be designed differently. For example, the reproducibility of high product quality can be increased significantly for motors of higher power ratings taking the step to full automation of production. Machine construction itself will also benefit from optimizing and reducing the costs of electric motors. All stationary machines use electric drives and hence electric motors. If the focus of the automobile industry on electric motors leads to significant cost reductions, this will also help machine constructors to further improve the competitiveness of their machines.

3.3.2. Production technologies for electric motors

The production technologies used for electric motors have been known for a long time. Even for the production of electric motors for use in automotive powertrains, the individual production steps will most likely not change fun-damentally. There will, however, have to be changes to and further develop-ments of the production technologies used within the individual production steps in order to obtain the required cost reductions. The most important core process in electric motor production is the wind-ing of the wire coils. This process step is technologically highly demanding and of crucial importance for the optimized production of electric motors. Through more efficient winding, it will be possible in the future to signi-ficantly reduce the material costs of motors, since less wire will then be needed for the same performance. At the same time, there must be further development of winding technology in order to meet the requirements of the automobile industry with regard to quality and the reproducibility of identical components.

30 | Study

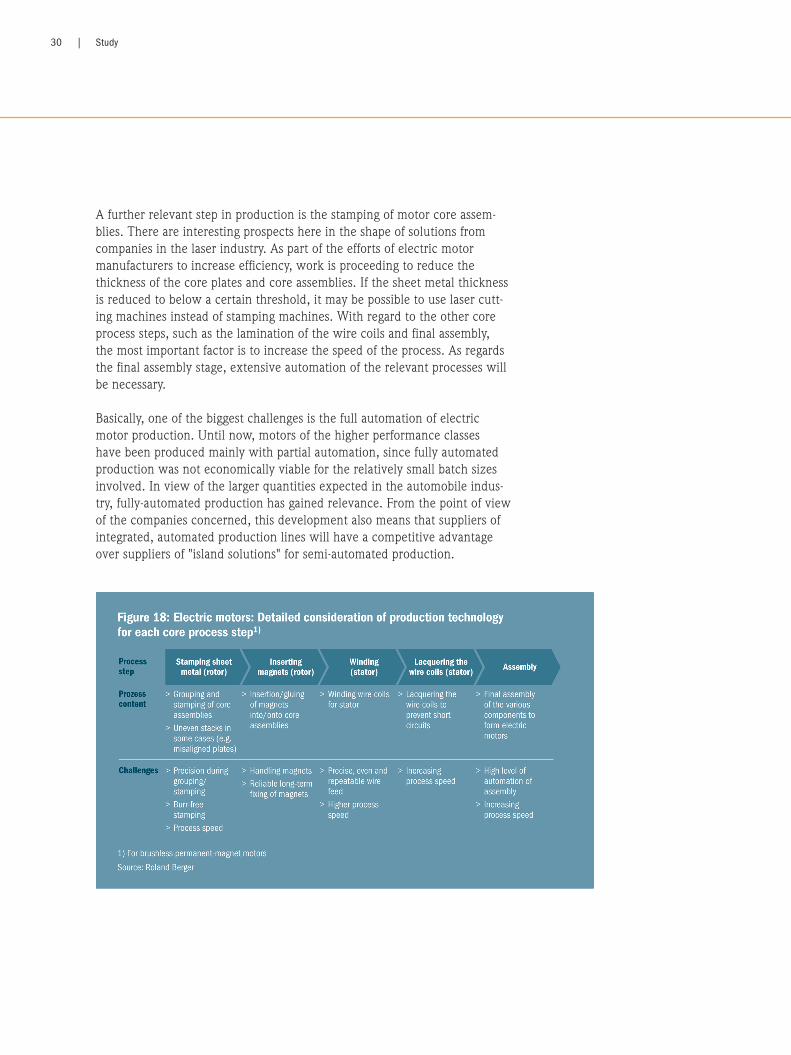

A further relevant step in production is the stamping of motor core assem-blies. There are interesting prospects here in the shape of solutions from com panies in the laser industry. As part of the efforts of electric motor manufacturers to increase efficiency, work is proceeding to reduce the thickness of the core plates and core assemblies. If the sheet metal thickness is reduced to below a certain threshold, it may be possible to use laser cutt-ing machines instead of stamping machines. With regard to the other core process steps, such as the lamination of the wire coils and final assembly, the most important factor is to increase the speed of the process. As regards the final assembly stage, extensive automation of the relevant processes will be necessary. Basically, one of the biggest challenges is the full automation of electric motor production. Until now, motors of the higher performance classes have been produced mainly with partial automation, since fully automated production was not economically viable for the relatively small batch sizes involved. In view of the larger quantities expected in the automobile indus-try, fully-automated production has gained relevance. From the point of view of the companies concerned, this development also means that suppliers of integrated, automated production lines will have a competitive advantage over suppliers of "island solutions" for semi-automated production.

31 | E-Mobility – a promising field for the future

3.3.3. Market overview for specific machines/technologies: Main competitors

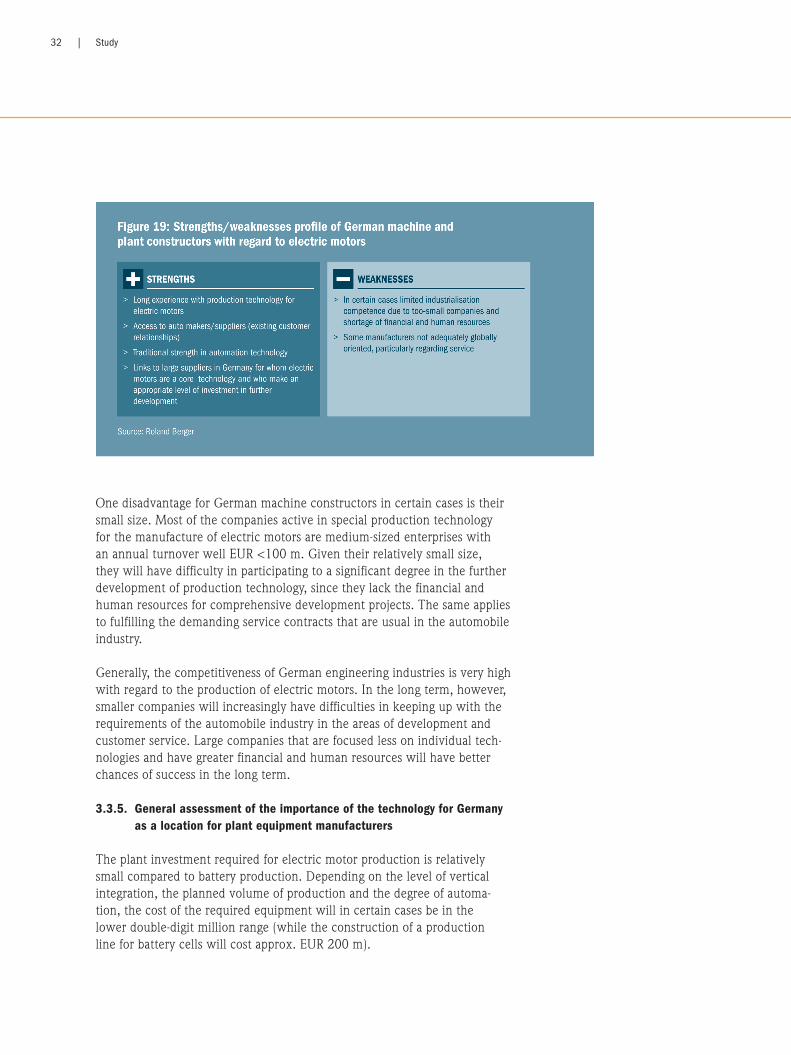

German engineering industries are very well positioned in the market for equipment for the production of electric motors. They cover both the "traditional" metalworking process technologies as well as the technologies (e.g. laser cutting) which may be relevant in the future. German manufac-turers have already supplied machines for electric motor production for a long time. German machine constructors can draw in particular on their strengths in process integration and automation and can thus offer skills which differentiate them from their competitors. In contrast to the case of battery production, the most important competi-tors in the field of electric motors come not from Asia but for example from Italy and Switzerland. Since electric motor production is also carried out in Germany and Europe and is not focused in Asia as in the case of batteries, German suppliers have an opportunity to help shape the continuous further development of production technology. There is therefore no experience advantage among competitors in the production technology for electric motors as there is in the case of battery production. 3.3.4. Assessment of the competitiveness of German manufacturers and

discussion of their major competitive advantages and disadvantages

German suppliers benefit from their years of experience with the various production technologies. In contrast to the case of batteries, production technology for electric motors does not break any technologically new ground and has for many years been part of the core business of many machine constructors. German companies are admittedly not represented in large numbers in the core processes (e.g. winding) but are at least able to contribute their competences to the production process. This includes in particular expertise in automation. Another plus for German manufacturers is the presence of electric motor production virtually "on the doorstep". Large German suppliers such as Bosch, Continental, Brose (in a JV with SEW Eurodrive) and Siemens are active in this sector, and machine con-structors benefit from cooperation with these companies. At the same time, these suppliers have discovered the production of electric motors for use in automotive powertrains as a business area for themselves and are interested in technological innovations by the established German machine construc-tors. Both sides benefit equally from the research activities in this area.

32 | Study

One disadvantage for German machine constructors in certain cases is their small size. Most of the companies active in special production technology for the manufacture of electric motors are medium-sized enterprises with an annual turnover well EUR <100 m. Given their relatively small size, they will have difficulty in participating to a significant degree in the further development of production technology, since they lack the financial and human resources for comprehensive development projects. The same applies to fulfilling the demanding service contracts that are usual in the automobile industry. Generally, the competitiveness of German engineering industries is very high with regard to the production of electric motors. In the long term, however, smaller companies will increasingly have difficulties in keeping up with the requirements of the automobile industry in the areas of development and customer service. Large companies that are focused less on individual tech-nologies and have greater financial and human resources will have better chances of success in the long term.

3.3.5. General assessment of the importance of the technology for Germany as a location for plant equipment manufacturers

The plant investment required for electric motor production is relatively small compared to battery production. Depending on the level of vertical integration, the planned volume of production and the degree of automa-tion, the cost of the required equipment will in certain cases be in the lower double-digit million range (while the construction of a production line for battery cells will cost approx. EUR 200 m).

33 | E-Mobility – a promising field for the future

Companies such as General Motors are, however investing up to EUR 160 m in production capacity for electric motors. Depending on the long-term development of the market for PHEVs and EVS, a very interesting segment could develop here, not least in terms of the potential volume of sales. In the next few years, this trend will continue at the same rate as electric drives establish themselves in the automobile industry. Currently, there are already numerous examples of how automobile manufacturers and their suppliers are making significant investments in electric motor production (GM, VW, Daimler, Bosch, Continental, etc.). This will result in the near future in some interesting growth opportunities for engineering industries. The importance of technology for the production of electric motors will increase. As the result of the introduction of electric drives, development of electric motors in the higher performance classes has gained a new dynamic, and this will mean significant potential business for engineering industries. Due to the future importance of electric motors for the automobile industry, interest in innovative production technology has significantly increased, creating very good opportunities for German engineering industries in the long term. On the one hand, the industry will be able to benefit from its existing strengths, which can be incorporated into the automation pro-cess, while on the other hand its traditional capabilities in innovation and research will provide the industry with a leading competitive position in the long term. Some companies have already recognized this trend and set up initial joint ventures, for example, SEW Eurodrive and Brose.

3.4. Summary

An analysis of the technology for battery cell and electric motor production shows that the current position of German engineering industries is not ideal in every respect. While the necessary technological competences can be covered by German manufacturers, in certain cases these companies have limited resources which prevent the commercial exploitation of the available opportunities. Furthermore, there are established competitors in all the rele-vant fields of technology who also, in the case of battery technology, have the advantage of local production in Asia. However, German engineering industries have every opportunity to gain a footing in the areas mentioned. The parameters for new business areas for these companies will develop very positively in the next several years.

34 | Study

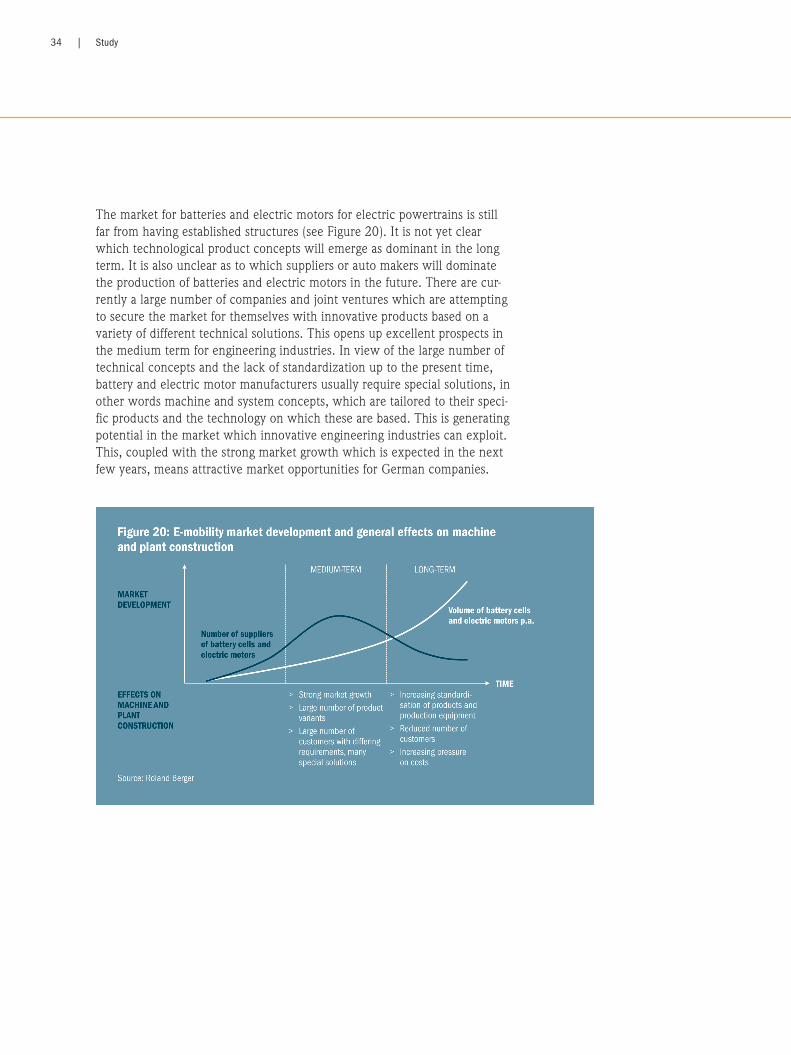

The market for batteries and electric motors for electric powertrains is still far from having established structures (see Figure 20). It is not yet clear which technological product concepts will emerge as dominant in the long term. It is also unclear as to which suppliers or auto makers will dominate the production of batteries and electric motors in the future. There are cur-rently a large number of companies and joint ventures which are attempting to secure the market for themselves with innovative products based on a variety of different technical solutions. This opens up excellent prospects in the medium term for engineering industries. In view of the large number of technical concepts and the lack of standardization up to the present time, battery and electric motor manufacturers usually require special solutions, in other words machine and system concepts, which are tailored to their speci-fic products and the technology on which these are based. This is generating potential in the market which innovative engineering industries can exploit. This, coupled with the strong market growth which is expected in the next few years, means attractive market opportunities for German companies.

35 | E-Mobility – a promising field for the future

In the long term, a consolidation phase generally occurs in established indus-tries. This will also happen in e-mobility. With the growth in the electrical drive market, increasingly stable structures will emerge, both in terms of the number of producers and the product technologies used (for example, in the long run, only a few of today's electric motor concepts will prevail). This will also reduce the variety of production facilities required, and the attrac-tive niches in the market will accordingly disappear. Increasing standardiza-tion and cost pressures will also reduce the attractiveness of the market. However, it is not clear when this consolidation will occur. It has been expected for some years in the market for photovoltaics production systems but has not yet occurred despite the increasing maturity of the market over-all. German engineering industries should therefore not be discouraged by the long-term consolidation scenario from addressing more energetically the highly-dynamic medium-term market for production systems for batteries and electric motors in the next few years. What are the factors for success in this market? On the basis of discussions undertaken in the course of the study, it has been possible to identify three key factors. Not all of these are fulfilled by the engineering industries con-cerned at the present time. The first factor is that the basic requirement for successful exploitation of market developments is mastery of the relevant technologies for the produc-tion steps involved. As described in the case studies, German suppliers can cover all the process steps. In some sub-areas (e.g. battery production), the required technologies have until now mainly been used in other industries. And with great success - in the fields of photovoltaics, electronics and flat screen production, German production technology is in demand worldwide. The production technologies used here are related to battery production. German engineering industries have proved in the past that the transfer and development of existing technologies is one of their strengths and has the potential also to be successful in the field of e-mobility. Secondly, engineering industries need a high level of financial resources in view of the need for continuous technological development. As illustrated in the study, production technology must make a significant contribution to reducing the costs and improving the quality of batteries and electric motors for electric powertrains. In order to successfully negotiate the step-up from bespoke manufacture to high volume production, continuous investment will be necessary in research and development.

36 | Study

Many of the companies which are developing the relevant production technology are financially strong and will be able to manage the necessary up-front investment, but some of the smaller medium-sized companies may have difficulties – if forced to rely on their own resources – in "holding their breath" long enough until a strong market position has been established and a high-yield volume of business has been achieved. This situation requires strong partners. The third factor for success is an understanding of the clients involved, in terms of both technological requirements and the rules for partnerships. From the technological point of view, German engineering industries have the disadvantage that little battery production is currently taking place in Germany and the rest of Europe. This makes the further development of machines more difficult and also threatens the industry's ability to with-stand competition from Asia. The export strength of German engineering industries must be exploited quickly in order to gain a footing in the specific markets in which batteries and electric motors for electric powertrains are already being produced on a large scale. This would enable the companies concerned to control technological development at "first hand" and also participate fully in the boom taking place in the industry world-wide.

Understanding the industry is another important aspect in which German engineering industries are not fully up to the required level. Many com-panies that provide production technology for batteries and electric motors have been established for years or even decades and know both the custom-ers and the processes involved. Certain medium-sized manufacturers of pro-duction technologies, which are only now becoming relevant to the automo-bile industry (such as mixing, coating and winding), have some catching-up to do here. They have previously had little contact with automotive manu-facturers or the large automotive suppliers and are also little-known in the industry. Here, too, the companies need support. The successful business networks such as for example E-MOTIVE in the VDMA, which promote an exchange of engineers with the automobile industry all along the value chain, can help at this here.

37 | E-Mobility – a promising field for the future

4. Approaches to exploiting the growth potential in the area of e-mobility

The great challenge facing German engineering industries in the field of e-mobility is at the intersection between technological expertise and the exploitation of commercial potential. Production technology for electric powertrain components could become a major business area for German engineering industries, given the long-term market potential, provided that the industry is able to translate its existing technological capabilities into concepts for its customers which are suitable for large-series production. Many German suppliers are technologically competitive but do not in cer-tain cases have direct contacts in the automobile industry and the necessary financial resources to pursue research and development to the necessary extent and to open up access globally to new customers and markets.

Moreover, if these companies are to prevail against established competitors, particularly from Asia, there are additional challenges which they need to address in order to achieve a strong market position. At the same time, the large suppliers which have so far dominated the automobile industry market do have the necessary financial resources and very good contacts in this industry. They do not, however, have all the relevant technologies available in-house which are necessary for the production of batteries and electric motors. This dilemma can be resolved successfully through the strategic steps described briefly below. Given the necessity for financial resources, the machine constructors con-cerned should develop strategies which will help them to reach the critical size required in order to succeed in making future investment in research & development, sales & service, etc. Here, it is advantageous to consider for example the development of machine construction for the photovol-taics industry. Much as in the case of battery production, customers in the first phase of strong market growth were asking for complete production lines. Instead of presenting themselves exclusively as suppliers of individual special machines and solutions, German engineering industries seized the opportunity to meet the demand for complete systems by forming joint ventures. This contributed significantly to the rapid development of German engineering in this area. Joint ventures of this kind would also be a logical approach in the case of battery production, and one which would result in competitive advantages.

38 | Study

Above and beyond this, joint research projects could also be an important step in helping smaller companies in particular to absorb high development costs. Tools such as collaborative research and research by industry associa-tions can offer tailor-made platforms that make full use of the innovation potential of the machine construction industry. It is precisely this collabora-tive industrial research which can allow small and medium-sized companies to join with large automobile industry in conducting research projects at low cost and low risk and to develop innovations together with these. Tax incentives would ensure a high level of take-up of these opportunities. In this way, research which might otherwise be risky would become less expensive and easier to plan for all the companies concerned. Further alliances between German engineering industries could prove to be a useful means of winning new markets. Special machine manufacturers have the knowledge of the key technologies of production today, whilst the established suppliers have the necessary financial strength and a deep under-standing of the processes in the automobile industry. A combination of these competences will significantly drive forward the development of German engineering with regard the production technology for e-mobility. Individual suppliers (e.g. Dürr) are already following this path and establishing them- selves (as a first step) as a supplier of battery assembly lines, with the inten-tion in the long term of being able to offer a complete battery cell produc-tion line as an integrated system. There is also a need for a stronger commitment by automobile manufactur-ers and their suppliers to cooperation with engineering industries in the field of e-mobility. Strong engineering industries supplying the field of e-mobility will also help the automobile industry significantly in making possible the necessary cost reductions in battery production and achieving a leading position in the field of electrical drives. Efforts should be made to achieve successful partnerships in the e-mobility market of the future in just the same way as in "traditional" manufacturing processes.

39 | E-Mobility – a promising field for the future

5. Recommendations for action

The gradual introduction of e-mobility represents significant additional business potential for German engineering industries. At the same time, this increases the pressure to carry out further development of production technology and represents a considerable challenge for many companies – particularly smaller medium-sized companies. If the German engineering industries are to have a strong market position in the medium and long term, this will depend heavily on the financial strength of these companies and their capacity for innovation. This present study shows that partnerships are essential to pave the way for innovative but often medium-sized companies to commercialize their technologies in the new e-mobility market. Strategic alliances are needed in order to open up new markets and to create a competitive advantage, for example as a process-chain or system supplier. With regard to the public sector, priority should be given to financial support for pre-competitive joint research as part of the state's overall joint industrial research program. The commitment of engineering industries from technologically related fields in the field of e-mobility will be an important factor in opening up new markets. This also applies to companies from other sectors, for ex- ample photovoltaics production, which can provide useful ideas. This sec- tor is technologically closely related to battery production, and the finan- cial strength of the engineering industries in the photovoltaics industry would be an important lever in creating greater stability and growth. The German engineering industries have a good position relative to its global competitors as a basis from which to develop an attractive global business in the long term with production technology for electric power-train components. In order to gain a footing in this sector, however, it is very important for development departments to be geographically close to producers. It is thus crucial that, at a time when European manufacturing sites for the new components are being nominated, that anchor investment is attracted to Germany. The introduction of front-loaded depreciation allo-wances for this would be an important step, not only for engineering indus-tries but also in order to safeguard the capacity of the automobile industry for innovation and the competitiveness of e-mobility in Germany.

40 | Study

Authors and contact persons

Dr. Thomas SchlickPartner, Roland Berger Strategy ConsultantsAutomotive Competence Center, Frankfurt

Dr. Guido HertelPartner, Roland Berger Strategy ConsultantsEngineered Products and High-Tech Competence Center, Munich [email protected]

Bernhard HagemannDirector of VDMA E-mobility Forum E-MOTIVE Deputy Chairman of FVA Drive Technology Research Association

Dr. Eric MaiserDeputy Managing Director of VDMA Productronic Association Managing Director of VDMA AG Photovoltaics Production Equipment

Michael KramerConsultant, Roland Berger Strategy ConsultantsAutomotive Competence Center, Munich

Co-authors

Ralf KalmbachPartner, Roland Berger Strategy Consultants Member of the Management Board and Head of Global Automotive Competence Center, Munich [email protected]

Hartmut RauenMember of the VDMA General Board of Management Managing Director of VDMA Drive Technology and Fluid Technology Associations, the FVA Drive Technology Research Association and the Drive Technology Research Fund

E-Mobility – a promising field for the futureOpportunities and challenges for the German engineering industries

Dr. Thomas Schlick, Dr. Guido Hertel, Bernhard Hagemann, Dr. Eric Maiser, Michael Kramer Study

AmsterdamBahrainBarcelonaBeijingBerlinBrusselsBucharestBudapestCasablancaChicagoDetroitDüsseldorfFrankfurtGothenburgHamburgHong KongIstanbulKyivLisbonLondonMadridMilanMoscowMunichNew YorkParisPragueRigaRomeSão PauloShanghaiSingaporeStockholmStuttgartTokyoViennaWarsawZagrebZurich

© Roland Berger Strategy Consultants05/2011, all rights reserved www.rolandberger.com

![Channel scaling and field-effect mobility extraction in ... · Amorphous oxide semiconductors (AOSs) based on In 2O 3 are technologically promising due to high carrier mobility [1–3]](https://img.pdfslide.net/doc/110x75/5fc6c25986726d5f6f6cbaeb/channel-scaling-and-field-effect-mobility-extraction-in-amorphous-oxide-semiconductors.jpg)