Embed Size (px)

DESCRIPTION

laws on customs

Citation preview

THE EASTERN AFRICA CUSTOMS AND FREIGHT FORWARDING PRACTICING CERTIFICATE (EACFFPC)

CUSTOMS LAWS AND PROCEDURES

OCTOBER 2012

THE FEDERATION OF EAST AFRICAN FREIGHT FORWARDERS ASSOCIATIONS

In Collaboration with

EAST AFRICA REVENUE AUTHORITIES

With Support from

TRADEMARK EAST AFRICA (TMEA)

FOREWORD Clearing agents in the East African Community (EAC) region play a vital role in facilitation of trade particularly in regard to tax assessment and collection; this in turn facilitates cargo movement and clearance from all requisite ports.

It is important to note that clearing agents who also double up as customs agents in the region work very closely hand in hand with customs authorities to ensure that trade in the region is facilitated.

Whereas customs officers have continued to be trained and refreshed developing experts from their work force, the same has not been the case with their work counterparts; the customs agents.

The need to train and capacity build the customs agents has never been more necessary particularly after it has become imminent that the requisite knowledge gap continues to widen.

The customs agents who also double up as freight logisticians have a wider scope compared to customs officers creating need for more attention on their ability to deliver professionally.

Most development partners have been focusing more on training customs officers who apart from having better resources have better entry points. On the other hand the clearing agents do not have a defined academic entry point or defined resources for training.

This has resulted to a struggling clearing agent trying to catch up with the knowledgeable counter parts in the customs, yet both MUST work together.

Customs agents originate documents that facilitate movement and clearance of cargo culminating into errors that slow down the flow of business.

i

Movement of cargo depends on how fast and perfect the documentation is done by Customs agents that are verified by the respective customs authorities. A delay in customs clearance increases the cost of doing business.

The intervention by Trade Mark East Africa (TMEA) came at the right time to facilitate revision of EACFFPC training materials to enhance training and capacity build the private sector with emphasis on the practicing customs agents in the EAC region.

This support has not only focused on revision of the materials but also brought together the private sector and the regional revenue authorities’ experts who have worked together to come up with EACFFPC training materials acceptable to both parties.

With these revised materials, the road to enhancing training for clearing agents has earnestly begun.

ii

ACKNOWLEDGEMENT

The Curriculum Implementation Committee (CIC) is grateful to the National Revenue

Authorities and the National Freight Forwarders Associations for accepting to release their staff

and members to carry out the development of the training materials. CIC acknowledges the

FEAFFA secretariat for excellent co-ordination of the process of materials development and the

eventual compilation of the manuals.

Special thanks go to William Ojonyo who steered the team of experts that developed the

materials.

The tremendous support provided by our development partner, Trade Mark East Africa (TMEA),

cannot go unnoticed bearing in mind that they provided all financial support that culminated

into the development of the training materials.

A big THANK YOU to the following individual subject experts who took their valuable time and wide experience in developing this CUSTOMS MODULE- CUSTOMS LAWS AND CLEARANCE PROCEDURES UNIT that have gone down the history lane.

1. Ahmed Mohamed 2. Erizaphan Siringi 3. Felicite Nibigira 4. Joy Basabe 5. Lilian Baguma 6. Wambura Waryuba 7. Jean-Marie Vianney Bakanibona

……………………………………………………………………………..

Lillian Umuhire RugambwaChairpersonCurriculum Implementation Committee (CIC)

iii

TABLE OF CONTENTS

LIST OF ABBREVIATION................................................................................................................................................v

Unit I: CUSTOMS LAWS................................................................................................................................................1

Overview on Customs laws of the East African Community.........................................................................................1

Customs Laws under article 39 of the protocol establishing EAC Customs Union...................................................1

Other Laws and regulations impacting clearing and forwarding environment........................................................3

CUSTOMS LAW (EACCMA)...........................................................................................................................................3

Structure of the EACCMA........................................................................................................................................4

Compliance related provisions in clearance of goods from Customs (i.e. clearance at port, airports , border post and post office, transit, ICD and Warehouses).........................................................................................................9

Offences.................................................................................................................................................................12

Legal Proceedings and Appeals..............................................................................................................................13

Legal Proceedings..............................................................................................................................................13

Appeals..............................................................................................................................................................15

Exemption under 5th Schedule.........................................................................................................................15

Remission of duty..............................................................................................................................................16

Refunds and Drawbacks....................................................................................................................................17

Refunds of Duty.................................................................................................................................................17

Duty Drawbacks................................................................................................................................................19

Customs Agents.....................................................................................................................................................20

Sample Question...................................................................................................................................................22

Restrictions and Prohibitions.....................................................................................................................................24

iv

Conventions Governing Prohibitions and Restrictions...........................................................................................25

Prohibitions and Restrictions on Specific Imports/Exports Under EAC Customs Laws...........................................27

Restricted and Prohibited Imports and Exports Under the EAC Customs Management Act..................................28

Agencies That Enforce Prohibitions and Restrictions.............................................................................................33

OVERVIEW OF THE EAC CUSTOMS REGULATIONS (EACCMR)....................................................................................35

Structure of the EACCMR.......................................................................................................................................35

Customs Forms......................................................................................................................................................38

Fees and Penalties.................................................................................................................................................44

Other Regulations–................................................................................................................................................55

Duty Remissions,...............................................................................................................................................56

Enforcement and Compliance Regulation.........................................................................................................57

sample questions...................................................................................................................................................57

UNIT II: CUSTOMS CLEARANCE PROCEDURES............................................................................................................59

IMPORT PROCEDURES...............................................................................................................................................59

Reporting procedures for means of conveyance...................................................................................................59

Categories of imports............................................................................................................................................67

Import process.......................................................................................................................................................67

Importation documents.........................................................................................................................................68

Assessment of duties and taxes.............................................................................................................................69

Customs Declaration..............................................................................................................................................85

Meaning and Purpose of Customs declaration..................................................................................................85

Legal provisions for Customs declaration..........................................................................................................86

Obligation of Declarants....................................................................................................................................87

Identify various Customs regimes.....................................................................................................................87

Customs Procedure codes.................................................................................................................................88

Verification and release of imported goods......................................................................................................91

v

Case study:............................................................................................................................................................93

EXPORT PROCEDURES................................................................................................................................................96

Categories of exports.............................................................................................................................................96

Export process.......................................................................................................................................................97

Export documentation and declaration.................................................................................................................97

Conditions for exports...........................................................................................................................................98

Verification and release of goods for export.........................................................................................................99

Procedures for Outward Clearance of means of conveyance..............................................................................102

Export Promotion Schemes.................................................................................................................................103

Manufacturing Under Bond.............................................................................................................................103

Export Processing Zones..................................................................................................................................105

Duty Remission................................................................................................................................................107

Duty Draw Back...............................................................................................................................................107

Inward /Outward Processing...........................................................................................................................110

Outward processing........................................................................................................................................113

Customs bond securities..........................................................................................................................................114

Customs bond security........................................................................................................................................114

Bond Execution, cancellation and enforcement..................................................................................................115

Processes/transactions that require Customs security bonds.............................................................................118

Benefits of Security bonds...................................................................................................................................118

Challenges in the management of Customs security bonds................................................................................119

Warehousing procedure..........................................................................................................................................119

Types of Warehouses..........................................................................................................................................120

Conditions for licensing bonded warehouses......................................................................................................122

Declaration and documentation of warehoused goods.......................................................................................125

Transit and Transhipment procedures.....................................................................................................................132

vi

Transit..................................................................................................................................................................132

Transshipment.....................................................................................................................................................133

Declaration of Transit and Transshipment cargo.................................................................................................133

Customs Control of Transit and Transshipment...................................................................................................134

Challenges in the Control of Transit fraud...........................................................................................................135

References...............................................................................................................................................................137

vii

LIST OF ABBREVIATION

EACCMA East African Community Customs Management Act

ASYCUDA Automated Systems for Customs Data

AWB AirWay Bill

BIF Bond in Force

COMESA Common Market for Eastern and Southern Africa

CPC Customs Procedure Codes

EAC East African Community

EACCMR East African Community Customs Management Regulations

EACCMRR East African Community Customs Management (Duty Remission) Regulations

EPZ Export Processing Zones

GATT General Agreement on Tariffs and Trade

ICD Inland Container depot

ICT Information and communication Technology

MUB Manufacturing Under Bond

SAD Single Administrative Document

SADC South African Development corporation

TREO Tax Remission Office

VAT Value Added Tax

viii

UNIT I: CUSTOMS LAWS

This course is intended to enable the participants to correctly apply provisions of the customs law in the process of clearing and forwarding goods.

VIEW ON CUSTOMS LAWS OF THE EAST AFRICAN COMMUNITY

Sub-topic

CUSTOMS LAWS UNDER ARTICLE 39 OF THE PROTOCOL ESTABLISHING EAC

CUSTOMS UNION

Introduction

Over view of the East African Community Customs Union Protocol

The three Partner States of East Africa signed a treaty for the establishment of the East African

community. This treaty came into force on 7th July, 2000. These Partner States undertook to

establish among themselves a Customs Union as an integral part of the community.

A Customs union is an agreement between two or more countries to remove trade barriers

with each other and establish a common tariff and non-tariff policies with respect to imports

from countries outside of the agreement.

A Protocol for the establishment of the East African Community Customs Union was signed by

three East Africa Heads of State for Uganda, Kenya and Tanzania on 2nd March, 2004 in Arusha,

Tanzania. Later on, both Rwanda and Burundi joined the East African Community in the year

2007.

Customs Laws of the Community (provisions of Art. 39)

This unit will enable trainees to correctly apply provisions of the Customs law in the process of

clearing and forwarding goods.

1

According to article 39 of the protocol, the Customs law of the Community shall consist of:

(a) Relevant provisions of the Treaty;

(b) The Protocol for the establishment of EAC and its annexes;

(c) Regulations and directives made by the Council;

(d) Applicable decisions made by the Court;

(e) Acts of the Community enacted by the Legislative Assembly; and

(f) Relevant principles of international law.

The Customs law of the Community shall apply uniformly in the Customs Union except as

otherwise provided for in the Protocol. The Partner States shall conclude such annexes to this

Protocol as shall be deemed necessary.

OTHER LAWS AND REGULATIONS IMPACTING CLEARING AND FORWARDING

ENVIRONMENT

The clearing and forwarding environment is governed by various laws apart from the Customs

laws of the Community. That being the case, a Customs agent within the community is

supposed to be aware of the laws and regulations prior to engagement within the industry. The

regulations cater for the establishment of a company to practice within a clearing industry.

Whereas the EACCMA and its Regulations harmonizes the licensing and Customs Agents’

practices across the EAC, it is important to note that there are other National laws and

regulations impacting on establishment and registration of Companies such as :

a) Provision of Company’s Ordinance/Act with regards to establishing of a company. This

differs in each Partner States

b) Registration requirements from the registrar of companies.

2

c) Business Licensing requirements from the specific government organs.

d) Any other Laws or regulations necessary to be completed prior to starting a business.

A Customs agent is supposed to know all the stakeholders of the respective Partner States and

the relevant laws and Regulations as well as the respective Authorities granting them powers to

operate. It is the duty of the agent to know the various relevant laws and to fulfill regulatory

obligations.

CUSTOMS LAW (EACCMA)

Specific Objectives:

At the end of this topic, trainees should be able to:

i. Describe the structure of the EACCMA

ii. Comply with the provisions related to clearance of goods.

iii. Apply provisions related to valuations of goods and assessment of taxes

iv. Demonstrate understanding of Customs offences and offence procedures and

consequences of non-compliance.

v. Explain legal proceedings

vi. Exercise right to appeal

vii. Apply provisions related to exemption, remission, refunds and drawbacks.

viii. Comply with legal requirements for operationalization of Customs Agents.

STRUCTURE OF THE EACCMA

The EAC CMA is comprised of twenty one parts, two hundred and fifty three sections, and five

schedules as follows:

PART I:Preliminary provisions to include

Short title, application and commencement

3

Interpretation

PART II: Administration

The Directorate of Customs and its functions

Provisions relating to staff, Customs seal and flag

Officers to have powers of Police and hours of attendance

Offences by, or offences in relation to officers

Exchange of information and common border controls

PART III: Importation

Prohibited and restricted imports

Power to prohibit, etc, imports

Exemptions of goods in transit.

Procedures on arrival

Reports

Arrival overland

Entry, examination and delivery of cargo

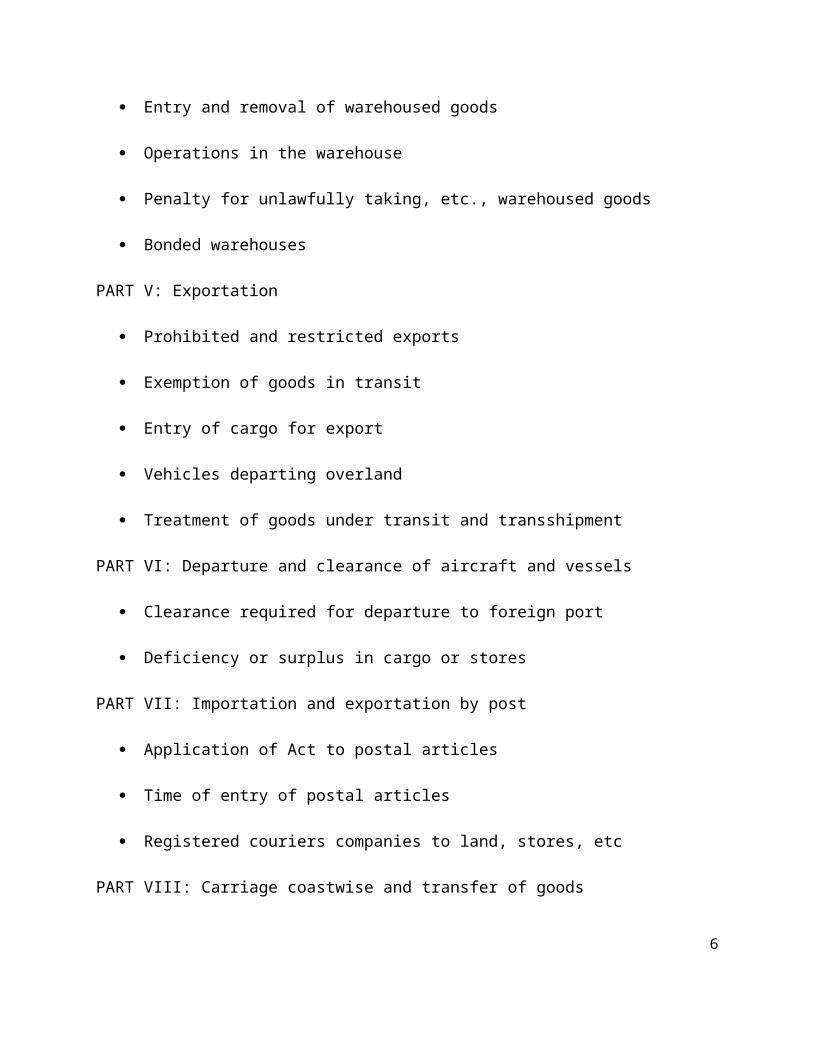

PART IV: Warehousing of goods

Dutiable goods may be warehoused

Entry and removal of warehoused goods

Operations in the warehouse

Penalty for unlawfully taking, etc., warehoused goods

4

Bonded warehouses

PART V: Exportation

Prohibited and restricted exports

Exemption of goods in transit

Entry of cargo for export

Vehicles departing overland

Treatment of goods under transit and transshipment

PART VI: Departure and clearance of aircraft and vessels

Clearance required for departure to foreign port

Deficiency or surplus in cargo or stores

PART VII: Importation and exportation by post

Application of Act to postal articles

Time of entry of postal articles

Registered couriers companies to land, stores, etc

PART VIII: Carriage coastwise and transfer of goods

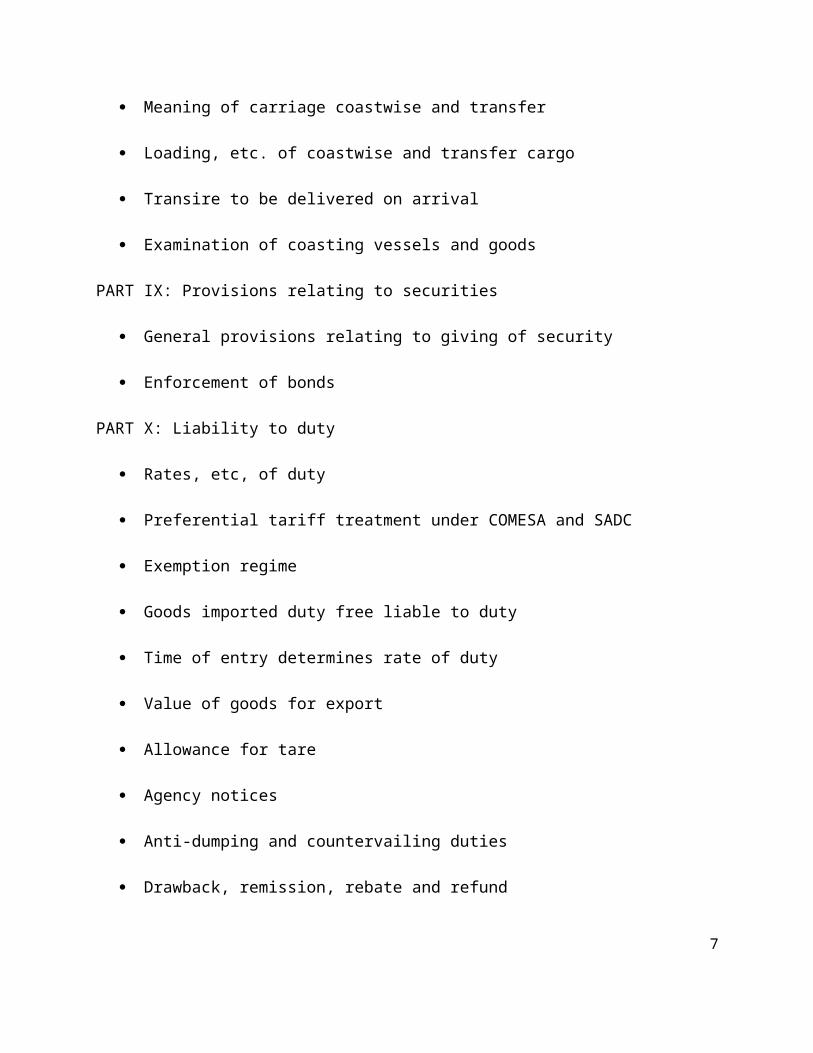

Meaning of carriage coastwise and transfer

Loading, etc. of coastwise and transfer cargo

Transire to be delivered on arrival

Examination of coasting vessels and goods

PART IX: Provisions relating to securities

5

General provisions relating to giving of security

Enforcement of bonds

PART X: Liability to duty

Rates, etc, of duty

Preferential tariff treatment under COMESA and SADC

Exemption regime

Goods imported duty free liable to duty

Time of entry determines rate of duty

Value of goods for export

Allowance for tare

Agency notices

Anti-dumping and countervailing duties

Drawback, remission, rebate and refund

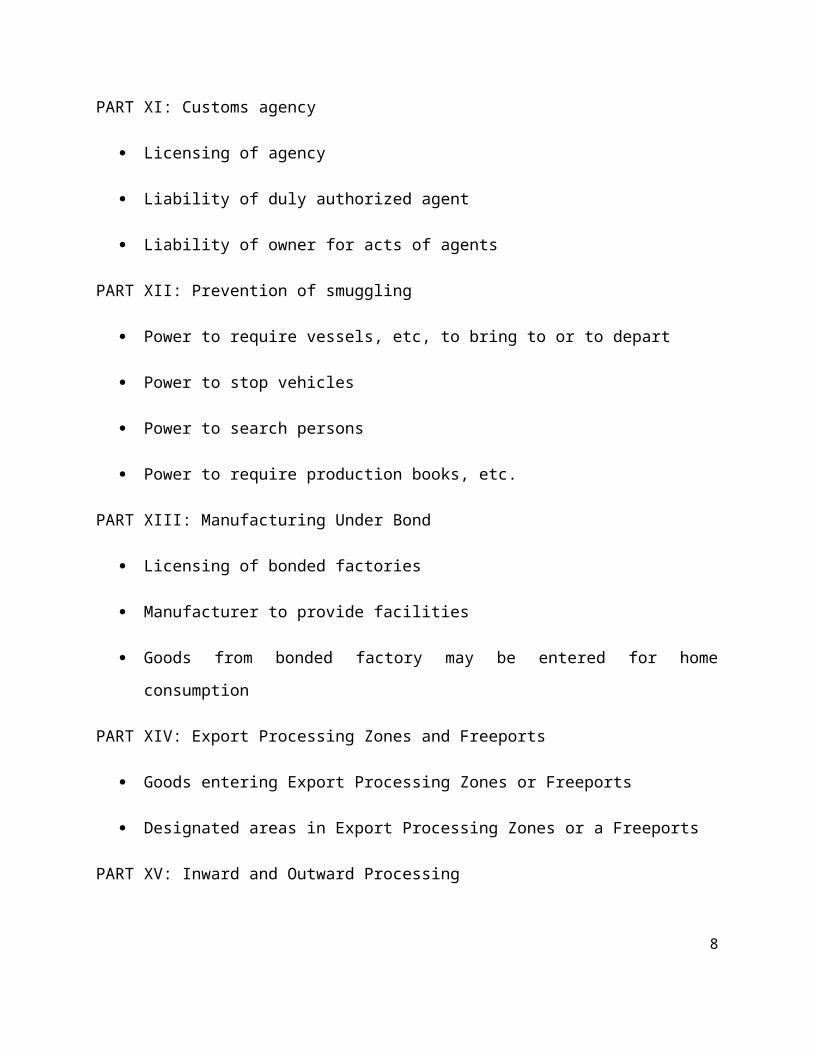

PART XI: Customs agency

Licensing of agency

Liability of duly authorized agent

Liability of owner for acts of agents

PART XII: Prevention of smuggling

Power to require vessels, etc, to bring to or to depart

Power to stop vehicles

6

Power to search persons

Power to require production books, etc.

PART XIII: Manufacturing Under Bond

Licensing of bonded factories

Manufacturer to provide facilities

Goods from bonded factory may be entered for home consumption

PART XIV: Export Processing Zones and Freeports

Goods entering Export Processing Zones or Freeports

Designated areas in Export Processing Zones or a Freeports

PART XV: Inward and Outward Processing

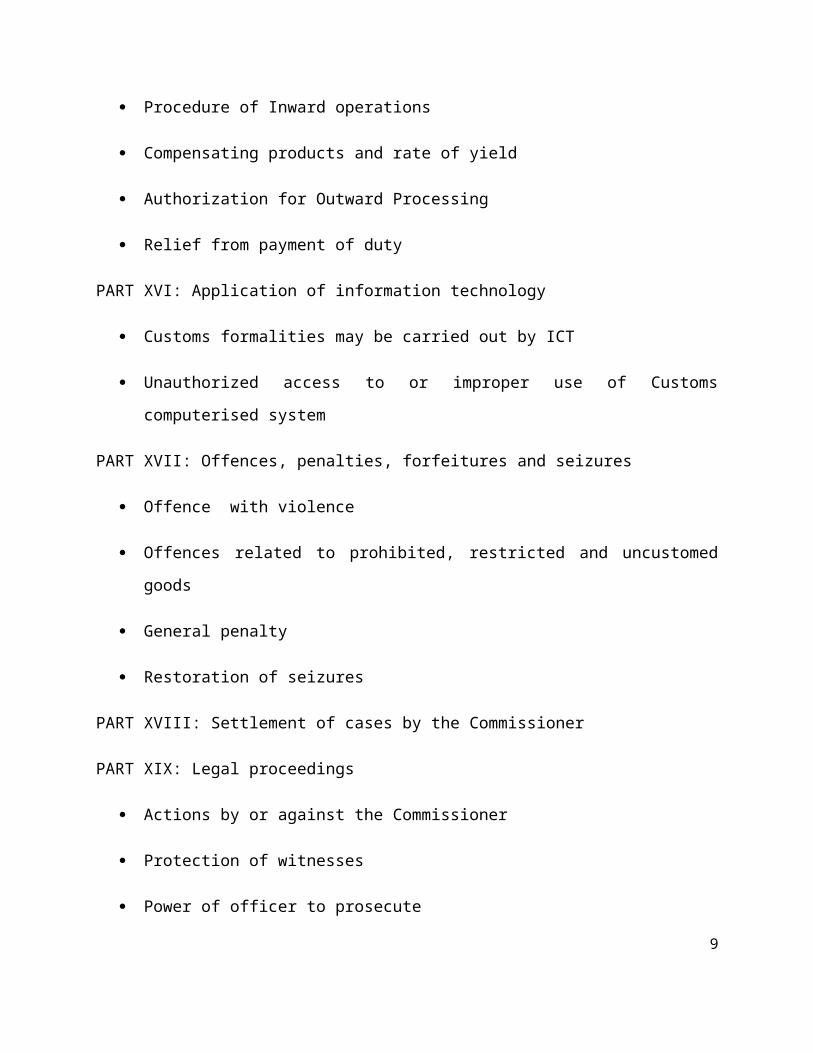

Procedure of Inward operations

Compensating products and rate of yield

Authorization for Outward Processing

Relief from payment of duty

PART XVI: Application of information technology

Customs formalities may be carried out by ICT

Unauthorized access to or improper use of Customs computerised system

PART XVII: Offences, penalties, forfeitures and seizures

Offence with violence

Offences related to prohibited, restricted and uncustomed goods

7

General penalty

Restoration of seizures

PART XVIII: Settlement of cases by the Commissioner

PART XIX: Legal proceedings

Actions by or against the Commissioner

Protection of witnesses

Power of officer to prosecute

PART XX: Appeals

PART XXI: Miscellaneous provisions

SCHEDULES:

First schedule: Declaration of Officer

Second schedule: Prohibited and Restricted Imports Generally

Third schedule: Prohibited and Restricted Exports Generally

Fourth schedule: Determination of Value of Imported Goods Liable to Ad Valorem

Import Duty

Fifth schedule: Exemption Regime

Sixth schedule: Warrant of Distress

COMPLIANCE RELATED PROVISIONS IN CLEARANCE OF GOODS FROM CUSTOMS (I.E.

CLEARANCE AT PORT, AIRPORTS , BORDER POST AND POST OFFICE, TRANSIT, ICD

AND WAREHOUSES)

8

Introduction

The term compliance means adherence to the provisions or guidelines in relation to something.

For the case of Customs compliance to the laws is thus adherence to the provisions of Customs

laws in each and every aspect. The compliance provisions range from adherence to controls of

goods, movement of passengers as well as means of conveyance.

Compliance during Clearance of goods

According to the EACCMA, Customs operations are conducted within the specified places

identified as Customs areas. Those Customs areas are clearly mentioned in the Act (section 12).

Other than Customs areas, the Act also provides for appointment of ports, airports and places

of loading and unloading. The need to have all these is to ensure control of goods, means of

conveyance as well as passengers.

The role of agents is to comply with all procedures for the clearance of goods depending on

where goods are located. The necessary considerations by an agent before starting the

clearance process include the following:

i. Submission of Reports to the proper authority such as Port Authorities and Revenue

Authorities

ii. Legality of the places where the goods are to be loaded/unloaded

iii. Having in place the necessary documents

iv. Time limit for the entrance of goods and the implications of the time of entry

v. The implications of the regimes for which the goods will be entered

vi. The Customs controls in force for the goods.

Submission of reports

The major role of Customs agent is to clear goods from Customs area and deliver them to the

owner. Before a Customs agent starts the clearance process, he/she is supposed to know

whether goods have already been unloaded from the importing vessel and a report submitted

to the Proper Officer. Depending on the means of conveyance, the task to report is vested to

9

different persons but there should be a report before Customs authorize goods to be delivered.

Hence it is the role of a Customs agent to be aware on whether the report is already within the

Customs department.

Places of loading and unloading

These are places appointed for loading and unloading goods subject to Customs control.

The entry and exit to these Customs areas is restricted.

The discharge of goods in the proper place of loading is thus facilitated by a competent

Customs agent who should know all the places for discharge at a Customs area and how goods

must be so discharged. The master who fails to discharge the goods commits an offence and

will be held liable.

Time within which clearance must be effected

Imported goods must be cleared by the owner within 21 days from the date of discharge from

the means of transport on which they were imported. An Agent should inform the owner that

goods which remain un-entered after this period shall be removed to the Customs warehouse.

Accordingly, goods entered but not removed from the first place of entry within fourteen days

will attract Customs warehouse rent.

Customs controls of goods

A Customs agent has to understand his role in facilitating the clearance of goods under Customs

control as well as the purpose of Customs control of imported goods. Customs emphasis on

controls is to ensure that:-

the revenue due on imported goods is charged and collected;

prohibited goods are not imported;

allowed goods are imported in accordance with all the conditions governing their

importation; and

10

goods whose duty free importation is conditional upon the status of the importer

and/or their end use are imported and used in accordance with such conditions.

It is the role of a competent agent to inform the importer that goods under customs control are

subject to the following:

any officer may at any time examine such goods; and

no person may interfere in any way with such goods except in a manner authorized or

prescribed under the EACCM Act.

OFFENCES

Customs offences

This unit will enable trainees to understand how offences committed during the process of

clearing and forwarding of goods under Customs control are dealt with.

A Customs offence is any breach or attempted breach of the statutory or regulatory provisions

which are provided in the East African Community Customs Management Act (EACCMA) .

Customs offences may be dealt with by the Customs authorities, in accordance with procedures

laid down in the EACCMA, 2004.

Customs offences are committed when any person contravenes any of the provisions Act.

Offences are generally covered by part XVII of the EACCM Act. The sections under this part spell

out how a particular offence should be dealt with. Some of the offences covered in the Act

include the following:

i. Section 200- offences related to prohibited, restricted and unaccustomed goods

ii. Section 202-offences related to import or export of concealed goods

iii. Section 203-offences to make or use false documentation.

11

It is important to note that most of the offences are covered in sections 193-208 of the

Act.

Offences commonly committed

1. Misdeclarations in the following areas:

Tariff- example refrigerated container declared as cooling unit

Quantity- declare less weight or pieces

Wrong item e.g. mineral water yet its wine

Year of manufacture/registration especially on motor vehicles.

2. Smuggling /diversion

3. Concealment

4. Under-valuation

5. Abuse of temporary importation procedures

6. Counterfeit/prohibited goods

7. Abuse of transit/warehousing procedures.

LEGAL PROCEEDINGS AND APPEALS

Introduction

The East Africa Community Customs Management Act (EACCMA) 2004 provides various

measures for enforcing the compliance with the provisions of the Act and /or procedures

related thereto. The non-compliance with the provisions of the Customs laws is an offence for

which measure for enforcing compliance can be instituted. The measures include Tax recovery

measures and/or measures for non-compliance with any other provisions of the Customs laws.

12

The provisions of the Act empowers the Commissioner of Customs to apply measures, such as

compounding offence(s), recovery of tax by distress warrant, Agency notice etc; to recover

unpaid tax and/or enforce compliance with any provision(s) of the Act; whether for tax

recovery or mere compliance with the provision(s) of the Customs Law .On the other hand, the

compliance can also be enforced by instituting legal proceedings in the Court of law.

LEGAL PROCEEDINGS

Authority

Sections 220 and 221of the EACCMA 2004, legal proceedings can be instituted in the court of

law and suing done in the name of the Commissioner. However, some Acts establishing some

East African Revenue Authorities carry provision(s) stating that the suing should be done in the

name of the Commissioner General of the Revenue Authority.

Court proceedings may be instituted where the Commissioner is satisfied that an offence has

been committed.

Violations leading to Legal proceedings

Generally the violation of the requirement(s) of the provisions of Customs law(s) is an offence

for which legal proceedings can be instituted in the court of law. Penalties, fines and/or

imprisonment upon conviction are prescribed in various provisions of the EACCMA 2004.

Particularly sections 193 to section 208 of the Act state some of the offences and how they are

dealt with. Such offences include:

i. Conspiring to contravene the provisions of the EACCMA.

ii. Maliciously shooting at an aircraft, vessel, vehicle in the service of Customs.

iii. Being armed while committing offense under this Act.

iv. Rescuing person arrested for any offense under the Customs Law.

v. Removing or defacing a Customs seal

vi. Inducing another person to commit offence.

13

vii. Warning an offender with the intent to obstruct the proper officer in the

execution of his/her duty.

viii. Assuming character of a proper officer.

ix. Importing or carrying coastwise prohibited goods.

x. Importing or carrying coastwise restricted goods contrary to the conditions

governing their importation or carriage coastwise.

xi. Making or using false document(s)

xii. Refusing to produce document(s).

APPEALS

Various provisions of the EACCMA 2004, including sections 193 to 208 lists areas where offence

can be raised and legal proceedings be instituted, by the Commissioner of Customs, in a court

of law. On the other hand, the Commissioner is empowered by the EACCMA 2004 to make a

decision, assessment of tax or to determine the value of imports/exports within the framework

of the Customs laws. In the process, the assessment made can aggrieve a taxpayer, who may be

an importer or exporter. The aggrieved person may decide to apply for review or appeal against

the decision. An application for review or an appeal can be effected by an importer/exporter,

Customs Agent. Where an appellant is not satisfied with the Commissioner’s verdict, he/she

may appeal to the Tax Tribunal. In case one is not satisfied with the Tribunal’s decision may

appeal to a judicial Court. The appeals mechanisms are provided for under section 229 of the

Act.

EXEMPTION UNDER 5TH SCHEDULE

The 5th schedule to the Act provides for general and specific exemptions.

Specific exemptions cater for the following:-

a) The presidents,

b) Partner States Armed forces

c) Commonwealth and other governments

14

d) Diplomatic and first time arrivals

e) Donor Agencies with bilateral or multilateral agreement with Partner States

f) International and regional organizations.

g) The war graves commission

h) Disabled, blind and physically handicapped persons

i) Rally drivers

j) Goods and equipment for use in Aid funded projects

Likewise general exemptions provide narrative explanations for the importation of the

following:

a) Aircrafts operations

b) Container and Pellets

c) Deceased person’s effect

d) Fish, crustaceans and molluscs

e) Passengers Baggage and personal effects

f) Samples and Miscellaneous Articles

g) Ships and Other vessels

h) Preparation for cleaning diary apparatus

The complete list with the conditions for exemption is found in the fifth schedule and the agent

is urged to understand those conditions before clearance with Customs. It is also essential for

the agent to have all documents to justify qualification for specific exemptions.

REMISSION OF DUTY

Section 140 of the EACCMA 2004, empowers the EAC Council to grant remission of duty on goods imported for manufacture of goods for export or for home use in case of an urgent national need. The procedure for approval of goods, for which remission may be granted, is provided for in the East African Community Customs Management (Duty Remission) Regulations (EACCMRR) 2008.

EACCMRR 2008 regulation 6 provides that the remission of duty granted shall be valid for a

period of twelve months from the date of the publication of the grant in the Gazette.

15

Application for remission

An application for remission of duty shall be made to the Council through the Commissioner in

a specified form (Form R 1) in the Schedule to Remission Regulations.

Upon receipt of an application for remission, the Commissioner shall forward the application to

the Committee established to oversee to remission applications for its comments.

The Commissioner shall after receiving the comments forward the application together with his

or her comments to the Council.

The Council may for reasons to be communicated to the applicant reject or approve an

application for remission under the Regulations.

Maintenance of records

One of the mandatory task for a manufacturer is to maintain records for the goods produced.

When it comes to the issue of duty remission, a manufacturer is expected to maintain separate

books and records relating to the following;

(a) locally sourced goods;

(b) goods imported by the manufacturer;

(c) goods received by a manufacturer by way of transfer under regulation 11 of the Remission

Regulations.

All these records have to be availed for audit by the Commissioner as per section 236 of

EACCMA 2004. It is therefore the duty of the manufacturer to maintain those records for the

period specified under the Customs laws.

REFUNDS AND DRAWBACKS

16

REFUNDS OF DUTY

Refund of duty is the payment of import duty or part of it, previously paid on imported goods

which has been damaged or pillaged during the voyage or damaged or destroyed while subject

to Customs control. The refund also refers to the payment of import duty or export duty paid in

error.

Conditions for refund of duty

A refund claim may be effected where the commissioner is satisfied that:-

i. The description, quality, state and condition of the goods; for which a refund is claimed,

was not in accordance with the contract or that the goods were damaged before

delivery out of Customs control or the goods with consent of the seller are returned

unused or destroyed

ii. The goods for which a refund is claimed, were damaged or pillaged during the voyage or

damaged or destroyed while under Customs control. A refund in this case will be

proportional to what has been damaged, pillaged or destroyed

iii. Import or export duty was paid in error

iv. A claim for refund must be presented to the Commissioner within twelve months from

the date of payment of duty.

Circumstances under which refund may arise include:

i. Double lodgments where two entries are lodged and paid for to clear the same cargo

ii. Valuation dispute where a higher value led to over payment

iii. Tariff dispute where an issue under dispute led to overpayment

iv. Short landing whereby less quantities are received

17

v. Payment under protest

vi. Undelivered cargo

vii. Goods imported are not in accordance with the contract of sale and if returned to the

seller

viii. Goods are damaged or destroyed while under Customs control

ix. Goods are damaged or pillage during voyage

DUTY DRAWBACKS

Duty drawback is a refund of all or part of any import duty paid in respect of goods exported.

This is a facility adopted within revenue administration to facilitate trade and encourage

production of goods for export using imported inputs. During importation the manufacturer will

pay duties for the imported inputs and will claim a refund when the final goods are exported or

used in a manner or for a purpose prescribed as a condition for granting a duty drawback. The

goods under duty drawback are subject to Customs control as per section 16 of EACCMA.

Conditions for granting duty drawback

Sections 138 to 139 of the EACCMA 2004 provides for conditions under which duty drawback

can be allowed:

i. The goods should be entered in a prescribed form and manner; and produced for

examination by proper office prior to exportation.

ii. A person claiming drawback should Complete and subscribe a declaration on a

prescribed form.

iii. For goods exported or put on board any vessel/aircraft for use as stores the conditions

include that:

The goods have been exported or put on board as stores.

18

The owner, at the time of declaration of the goods for drawback was and

continues to be entitled to drawback

iv. The goods, after having been put on board any vessel/aircraft for exportation or use as

stores have been destroyed by accident and/or abandoned to Customs.

v. For goods imported for use in the manufacture of goods which are exported,

transferred to a free port or transferred to Export Processing Zone(EPZ) ,the drawback

is allowed if the goods exported, transferred to a free port or EPZ are a direct result of

the imported goods used in the manufacture of such goods.

vi. The claim for drawback is presented within twelve months from the date of exportation

of the goods or performance of the conditions for which a drawback is allowed.

CUSTOMS AGENTS

A Customs Agent is a person who is licensed by the Commissioner for transacting business

relating to the declaration or clearance of goods or baggage (other than accompanied un-

manifested baggage) subject to Customs control of a person travelling by air, land, or sea; on

behalf of the owner.

Section 145 of the EACCMA 2004 empowers the Commissioner of Customs to license or to

decline. The Commissioner may refuse to issue a license, suspend, revoke any license or decline

to renew such license if the agent has failed to meet certain conditions for licensing or

contravened the law.

A Customs Agent performs his/her duties under the authority of the owner of the goods. In

accordance with section 146 of the EACCMA 2004, the agent has to be authorized in writing by

the importer/exporter.

The importance of a Customs Agent

19

Declaration and /or clearance of goods through Customs, requires a professional knowledge

and competences without which the clearance of goods can be delayed or fail. A Customs

Agent with a professional knowledge and Competences in the clearance of goods through

Customs and subsequent forwarding them to the importer minimizes delays associated with

clearance and forwarding of goods to final destination(s). He uses his/her professional

knowledge for easy compliance with various laws and procedure related to clearing and

forwarding of goods; thus minimizing delays, costs and penalties associated with non-

compliance of the provisions of the laws governing clearance and forwarding of goods.

Importance of customs agents is reflected from the roles of customs agents which are;

i. Acts as an intermediary between an importer/exporter and other parties in clearance of

goods and border protection.

ii. Customs clearance of goods by capturing declarations and performing related activities

involving paper work in trade facilitation involving international shipping process

iii. Provide bond guarantees for goods under clearance where necessary

iv. Facilitate refund claims such as duty draw back claims

v. Prepare and facilitate goods for examination

vi. Facilitates and avails warehousing facilities

vii. Provides import/export consultancy services

viii. Acts as a freight forwarder on behalf of his clients

ix. Provide related transport/shipping and logistical services

x. Provides network with related government officials and agencies

Licensing procedures:

20

A person intending to be a Customs agent has to apply for a license in a prescribed form to

Commissioner. The application shall be accompanied with an application fee as may be

prescribed by the Commissioner.

Where the application is approved, the applicant shall pay the license fee and execute a

security bond of such amount as the Commissioner may require.

Conditions for licensing

The applicant must have the following:

He or She must have established office with office equipment including computers

capable of being connected to customs computer network

Employees with minimal acceptable qualifications according to customs regulations.

Documentary evidence regarding establishment of the customs agency.

Liability of a duly-authorized Agent:

The Customs agent shall be deemed to be the owner of the goods and hence:

•Be liable to pay all Customs duties and taxes.

•Be able to answer all questions asked by the proper officer in relation to a particular

transaction.

Role and Liability of owner

The owner of goods who authorizes an agent to perform any business transaction under

Customs control on his/her behalf, shall be liable to the declaration made by the agent and be

prosecuted for any offence committed by such agent, unless such offence is committed by the

agent due to his/her negligence.

21

For clearance purposes, the owner-the importer or exporter- will have to submit documents

related to the imported goods or goods under export to his/her Customs Agent.

SAMPLE QUESTION

Exercise I

The students from Masai Mara Girls School were on a study tour in Dar es Salaam being hosted

by Institute of Tax Administration (ITA) in collaboration with Tanzania Freight Forwarders

Association (TAFFA). The students had planned to visit Dar es Salaam Port and other customs

areas to gain expertise in various customs issues. On the part of TAFFA, you had been

appointed to head the delegates. Miss Kidunducy, one of the talkative students asked,

a) “You said most of the goods in customs area are there for the purpose of control. What

types of goods specifically should we expect to find in those customs areas?”

b) “What can we understand by the term goods being under Customs control?”

c) “What is the reporting procedure for a ship coming from Mombasa to the Port of Dar es

Salaam?”

TASK

Respond to her properly basing on the EACCMA 2004.

Exercise II

Mr. Nkosi arrives for the first time in Tanzania through Tunduma Border accompanied by his

wife, Nadhipa and Two Children using his Toyota Hiace with Zambia registration. The family

expects to pay a visit in various national parks before going back to Zambia.

TASK

What restrictions have been imposed to the use of the motor vehicle as far as temporary

importation is concerned?

22

RESTRICTIONS AND PROHIBITIONS

Specific Objectives

At the end of this topic, the trainee will be able to:

i. Differentiate between prohibitions from restrictions

ii. Identify specific provisions on prohibited and restricted imports/exports

iii. Identify prohibited and restricted imports and exports under the Customs law

iv. Identify various regulatory authorities administering restrictions

v. Identify legal requirements for complying with restrictions on specific imports/exports

INTRODUCTION

Movement across the border involves goods which are of different categories. These goods

may be acceptable either as they are or under certain specification in one region but banned in

the other. Prohibited goods are goods that are not allowed to be imported, exported or

transferred into or outside any of the Partner States. i.e These are goods that are banned to be

traded and cleared through Customs.

Restricted goods are goods whose importation or exportation is subject to meeting specific

conditions before they are allowed to be cleared through Customs. The importation or

exportation of such goods is controlled by specific government agencies depending on their

23

nature. According to the EACCMA 2004, restricted goods are any goods the importation,

exportation, transfer or carriage coastwise must abide with any set conditions regulated by or

under the Customs laws”.

It means therefore, that the importation of the identified goods will only be granted against

import permits, certificates or any other authority issued by a relevant agency before

importation or exportation.

CONVENTIONS GOVERNING PROHIBITIONS AND RESTRICTIONS

There are various international conventions regulating production, possession and movement

of certain goods. Countries signatories to these conventions must adhere to them and fulfill all

requirements. There are conventions relating to narcotic drugs, psychotropic substances,

intellectual property etc

International conventions on narcotic drugs

Shanghai Convention 1909

The control of narcotic drugs has been of global concern ever since the first international

conference on the subject, held in Shanghai in 1909.

The international control system has been built up step by step, continuing from 1920 under

the auspices of the League of Nations, and since 1946 by the United Nations

A series of treaties adopted under the auspices of the UN require that:

Governments exercise control over production and distribution of narcotic drugs and

psychotropic substances.

Governments combat drug abuse and illicit traffic.

24

Governments maintain the necessary administrative machinery and report to

international organs on their actions.

The Single Convention on Narcotic Drugs, 1961

This convention replaced the treaties concluded before the Second World War on opiates,

cannabis and cocaine.

At present, control is exercised over more than 116 narcotic drugs, including opium and its

derivatives as well as synthetic narcotics such as methadone and pethidine.

The Convention on Psychotropic Substances, 1971

This Convention controls drugs not covered by previous treaties. Substances under control

include; hallucinogens, amphetamines, barbiturates, non-barbiturate sedatives and

tranquilizers.

About 105 psychotropic substances are controlled, most of them in pharmaceutical products

acting on the central nervous system.

The Convention on psychotropic substances has judged some of these substances to be

particularly dangerous, such as LSD, and made calls to place them under even stricter control

than narcotic drugs. Furthermore, the convention calls for substances with very wide

legitimate medical use to be controlled in a less stringent way not to hamper their availability

for medical purposes but on the other hand to avoid their diversion and abuse.

The United Nations Convention against illicit Traffic in Narcotic Drugs and Psychotropic

Substances, 1988

This convention urges the member countries to;

i. Prevent the laundering of money obtained from illicit trafficking.

ii. Provide concrete instruments for international law enforcement cooperation.

25

iii. Provide legislation covering the tracing, freezing and confiscation of proceeds and

property derived from drug trafficking.

OTHER INTERNATIONAL CONVENTIONS/AGREEMENTS

i. CITES- Convention on International Trade for Endangered Species

ii. Basel (1992)-hazardous wastes /disposal

iii. Stockholm (2004)-Persistent Organic Pollutants (POPs)

iv. Rotterdam-prior informed consent on chemicals

v. Montreal (1987)-Ozone depleting substances

vi. Chemical weapons conventions-weapons

vii. Lusaka task force

PROHIBITIONS AND RESTRICTIONS ON SPECIFIC IMPORTS/EXPORTS UNDER EAC

CUSTOMS LAWS

Prohibition and restrictions of goods is governed by the provision of section 18, 19 and 20 of

EACCMA 2004 for imports and section 70, 71, 72 for exports.

Prohibited and Restricted Imports Legal Compliance

Goods specified in Part A of the Second Schedule are prohibited goods and the importation

thereof is prohibited (Sec 18 (1)). The list of prohibited items is however not exhaustive. Other

prohibited items are found in the national laws in a respective Partner States.

Goods specified in Part B of the Second Schedule are restricted goods and the importation

thereof, save in accordance with any conditions regulating their importation, is prohibited (Sec

18 (2))..This subsection provides a stepping stone for goods which are restricted within the

Partner States. The goods can be imported or exported upon complying with conditions

26

governing their importation/exportation. Apart from restrictions at EAC regional level, each

Partner State has laws governing restricted import/exports.

Prohibitions and restrictions are monitored by the council through publication in gazette. The

council is mandated to publish a list of goods which are prohibited or restricted either generally

or in relation to any Partner States. The order, in respect prohibited or restricted goods, made

by the Council will provide goods or class of goods, importation of which is prohibited or

restricted in the Partner State or any of its area. The Council may also limit, in respect of any

Partner State, the application of the provisions of the Second Schedule in respect of all or any of

the goods specified in the order.

Prohibitions and restrictions do not apply to goods imported in transit, or for transshipment, or

as stores of any aircraft or vessel, unless:

o The goods are within paragraph 2 of Part A of the Second Schedule of EACCMA, 2004

(that is: false money, counterfeit currency notes and coins and any money with no

established standard in weight or fineness) or

o The goods are expressly prohibited or restricted in any order made under the Act

prohibiting or restricting the importation of goods.

However, such goods shall be re-exported within such time and subject to such conditions as

the Commissioner may specify otherwise they will be deemed to be prohibited goods, or

restricted goods, as the case may be, and to have been imported on that date they were

required to be re-exported.

Prohibited and Restricted Exports

According to the EACCMA, goods specified in Part A of the Third Schedule are prohibited goods

and the exportation of the goods is prohibited and goods specified in Part B of the Third

Schedule are restricted goods and the exportation of the goods, save in accordance with any

conditions regulating their exportation, is prohibited (Sect 70 –Exports).

27

RESTRICTED AND PROHIBITED IMPORTS AND EXPORTS UNDER THE EAC CUSTOMS

MANAGEMENT ACT

Part A and Part B of the Second Schedule to the EAC Customs Management Act 2004 list

prohibited and restricted goods.

Part A - Prohibited Goods

i. All goods the importation of which is for the time being prohibited under this Act, or by

any written law for the time being in force in the Partner State.

ii. False money and counterfeit currency notes and coins and any money not being of the

established standard in weight or fineness.

iii. Pornographic materials in all kinds of media, indecent or obscene printed paintings,

books, cards, lithographs or other engravings, and any other indecent or obscene

articles.

iv. Matches in the manufacture of which white phosphorous has been employed.

v. Any article made without proper authority with the Armorial Ensigns or Court of Arms of

a partner state or having such Ensigns or Arms so closely resembling them as to be

calculated to deceive.

vi. Distilled beverages containing essential oils or chemical products, which are injurious to

health, including thijone, star arise, benzoic aldehyde, salicyclic esters, hyssop and

absinthe. Provided that nothing in this paragraph contained shall apply to "Anise and

Anisette" liquers containing not more than 0.1 per centum of oil of anise and distillates

from either pimpinella anisum or the star arise allicium verum.

vii. Narcotic drugs under international control.

viii. Hazardous wastes and their disposal as provided for under the base conventions.

28

ix. All soaps and cosmetic products containing mercury.

x. Used tyres for light Commercial vehicles and passenger cars.

xi. The following Agricultural and Industrial Chemicals:

(a) Agricultural Chemicals

1. 2.4 - T

2. Aldrin

3. Caplafol

4. Chlordirneform

5. Chlorobenxilate

DDT

6. Dieldrin

7. Dibroacethanel (EDB)

8. Flouroacelamide

9. HCH

10. Hiplanchlor

11. Hoscachlorobenzene

12. Lindone

13. Mercury compounds

14. Monocrolophs (certain formulations)

15. Methamidophos

29

16. Phospharrmion

17. Methyl - parathion

18. Parathion

(b) Industrial Chemicals

1. Crocidolite

2. Polychlorominatel biphenyls (PBB)

3. Polyuchorinted Biphenyls (PCB)

Polychlororinated Terphyenyls (PCT

4. Tris (2.3 dibromopropyl) phosphate

5. Methylbromide (to be phased out in accordance with the Montreal

6. Protocol by 2007).

(c) Counterfeit goods of all kinds

PART B- RESTRICTED GOODS

1. All goods the importation of which is for the time being regulated under this Act by any

written law for the time being in force in the Partner State.

2. Postal franking machines except and in accordance with the terms of a written permit

granted by a competent authority of the Partner State.

3. Traps capable of killing or capturing any game animal except and in accordance with the

terms of a written permit granted by the Partner State.

4. Unwrought precious metals and precious stones.

30

5. Arms and ammunition specified under Chapter 93 of the Customs Nomenclature.

6. Ossein and bones treated with acid.

7. Other bones and horn - cores, unworked defatted, simply prepared (but not cut to

shape) degelatinized, powder and waste of these products.

8. Ivory, elephant unworked or simply prepared but not cut to shape.

9. Teeth, hippopotamus, unworked or simply prepared but not cut to shape.

10. Horn, rhinoceros, unworked or simply prepared but not cut to shape

11. Other ivory unworked or simply prepared but cut to shape.

12. Ivory powder and waste.

13. Tortoise shell, whalebone and whalebone hair, horns, antlers, hoovers, nail, Claws and

beaks, unworked or simply prepared but not cut to shape, powder and Waste of these

products.

14. Coral and similar materials, unworked or simply prepared but not otherwise Worked

shells of molasses, crustaceans or echinoderms and cattle-bone, Unworked or simply

prepared but not cut to shape powder and waste thereof.

15. Natural sponges of animal origin.

16. Spent (irradiated) fuel elements (cartridges) of nuclear reactors.

17. Worked ivory and articles of ivory.

18. Bone, tortoise shell, horn, antlers, coral, mother-of pearl and other animal carving

Material and articles of these materials (including articles obtained by moulding).

19. Ozone Depleting Substances under the Montreal Protocol (1987) and the Vienna

Convention (1985).

31

20. Genetically modified products.

21. Non-indigenous species of fish or egg of progeny.

22. Endangered Species of World Flora and Fauna and their products in accordance with

CITES March 1973 and amendments thereof.

23. Commercial casings (Second hand tyres).

24. All psychotropic drugs under international control.

25. Historical artefacts.

26. Goods specified under Chapter 36 of the Customs Nomenclature (for example,

percuassion caps, detonators, signalling flares).

27. Parts of guns and ammunition, of base metal (Section XV of the Harmonised Commodity

Description and Coding System), or similar goods of plastics under Chapter 39 of the

Customs Nomenclature.

28. Armoured fighting vehicles under heading No 8710 of the Customs Nomenclature.

29. Telescope sights or other optical devices suitable for use with arms, unless

30. Mounted on a firearm or presented with the firearm on which they are designed to be

mounted under Chapter 90 of the Customs Nomenclature.

31. Bows, arrows, fencing foils or toys under Chapter 95 of the Customs Nomenclature.

32. Collector's pieces or antiques of guns and ammunition under heading No 9705 or 9706

of the Customs Nomenclature.

AGENCIES THAT ENFORCE PROHIBITIONS AND RESTRICTIONS

Apart from the regional prohibitions and restrictions, Partner States have the power to

prohibit/ restricts some goods entering or leaving the country. However, this should be known

32

to others for the sake of harmony. Apart from Customs authority there are other government

organs administering the prohibitions and restrictions. The respective organs from each Partner

States are as hereunder (the list is not exhaustive):

i. Tanzania

a. Tanzania foods and Drugs Authority

b. Tanzania Bureau of standards

c. Fair Competition Commission

d. Ministry of Home Affairs- Police force

e. National Environmental Management Council ( NEMC)

ii. Kenya

a. Kenya Bureau of Standards

b. Public Health

c. National Environmental Management Authority (NEMA)

d. National Radiation Management Board.

iii. Rwanda

a. Rwanda Bureau of Standards

b. Rwanda Environmental Management Authority (REMA)

c. Ministry of Internal Affairs – Police Force department

iv. Burundi

a. Burundi Bureau of Standards

33

b. Ministry of security

c. Ministry of Health

v. Uganda

a. Uganda National Bureau of Standards (UNBS)

b. Wildlife Authority

c. National Drugs Authority

d. Ministry of Internal Affairs -Narcotics Squads division

e. National Environmental Management Authority (NEMA)

OVERVIEW OF THE EAC CUSTOMS REGULATIONS (EACCMR)

Specific Objectives

At the end of this topic, trainees should demonstrate the ability to;

i. Describe the structure of the EACCMR

ii. Identify and appropriately use prescribed forms under the EACCMR

iii. Identify fees and penalties applicable under specific provisions

iv. Comply with other regulations applicable in clearing and forwarding process

STRUCTURE OF THE EACCMR

The EAC Customs Management Regulations were made by the Council of Ministers under

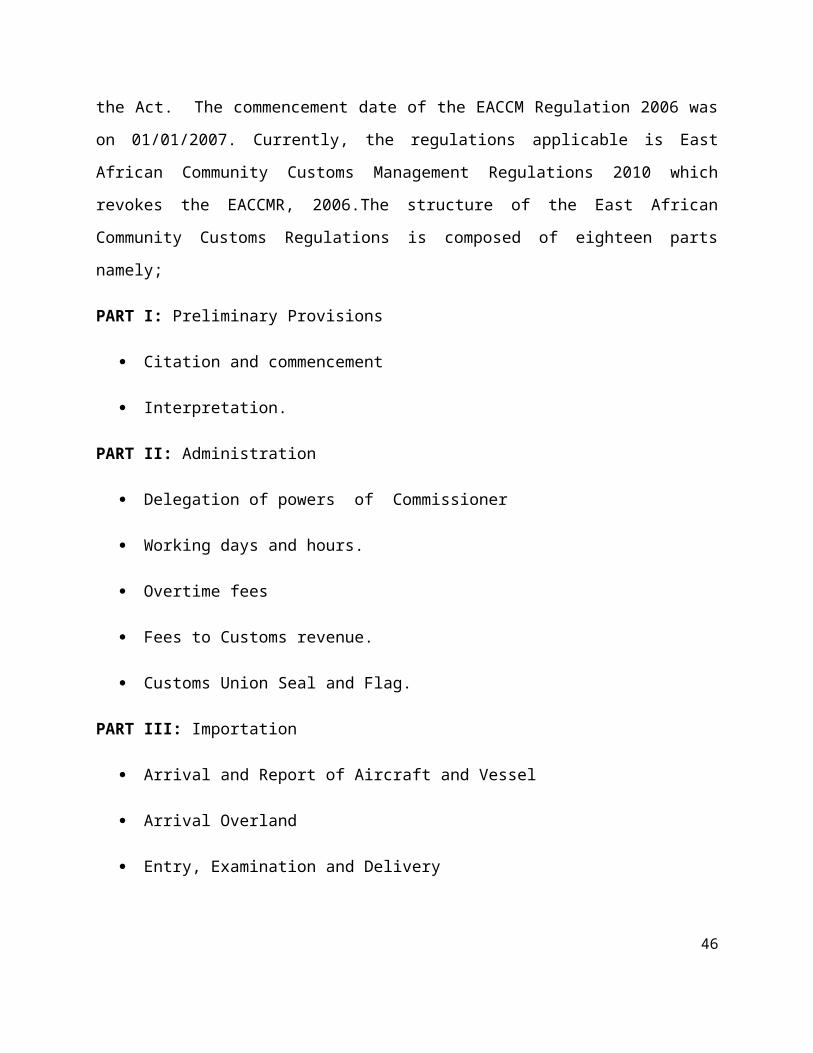

section 251 of the EAC CMA to give effect to the Act. The commencement date of the EACCM

Regulation 2006 was on 01/01/2007. Currently, the regulations applicable is East African

Community Customs Management Regulations 2010 which revokes the EACCMR, 2006.The

structure of the East African Community Customs Regulations is composed of eighteen parts

namely;

34

PART I: Preliminary Provisions

Citation and commencement

Interpretation.

PART II: Administration

Delegation of powers of Commissioner

Working days and hours.

Overtime fees

Fees to Customs revenue.

Customs Union Seal and Flag.

PART III: Importation

Arrival and Report of Aircraft and Vessel

Arrival Overland

Entry, Examination and Delivery

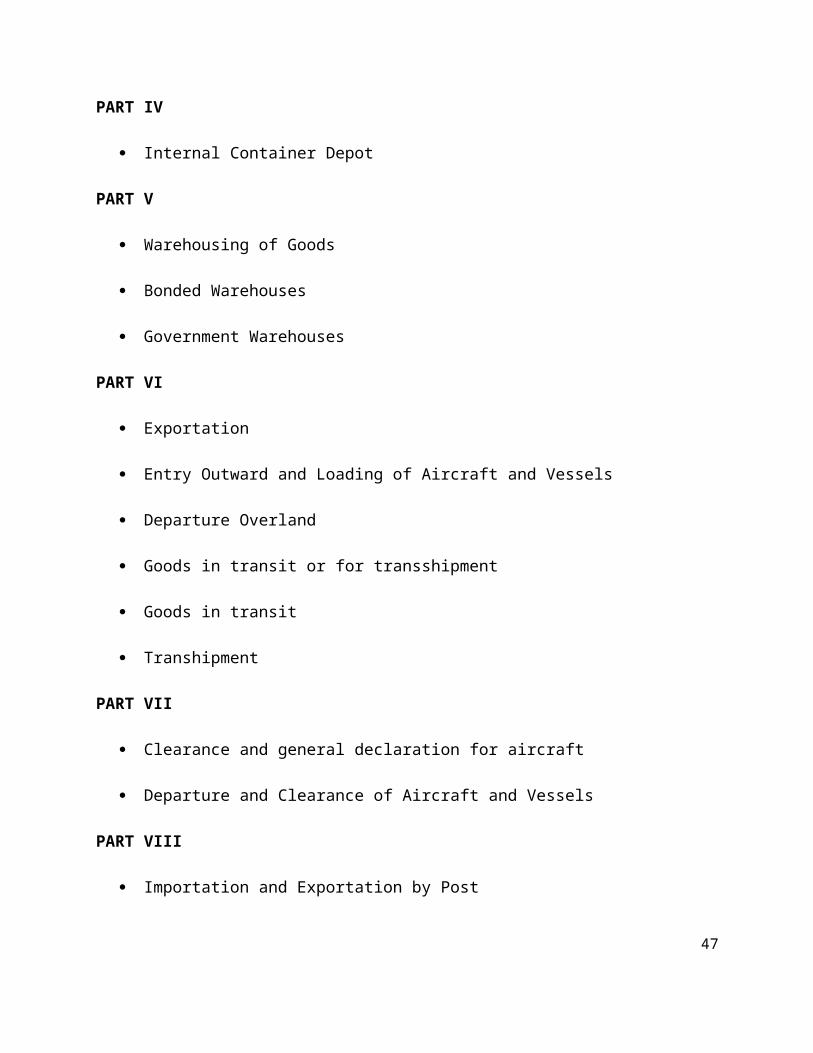

PART IV

Internal Container Depot

PART V

Warehousing of Goods

Bonded Warehouses

Government Warehouses

PART VI

35

Exportation

Entry Outward and Loading of Aircraft and Vessels

Departure Overland

Goods in transit or for transshipment

Goods in transit

Transhipment

PART VII

Clearance and general declaration for aircraft

Departure and Clearance of Aircraft and Vessels

PART VIII

Importation and Exportation by Post

PART IX

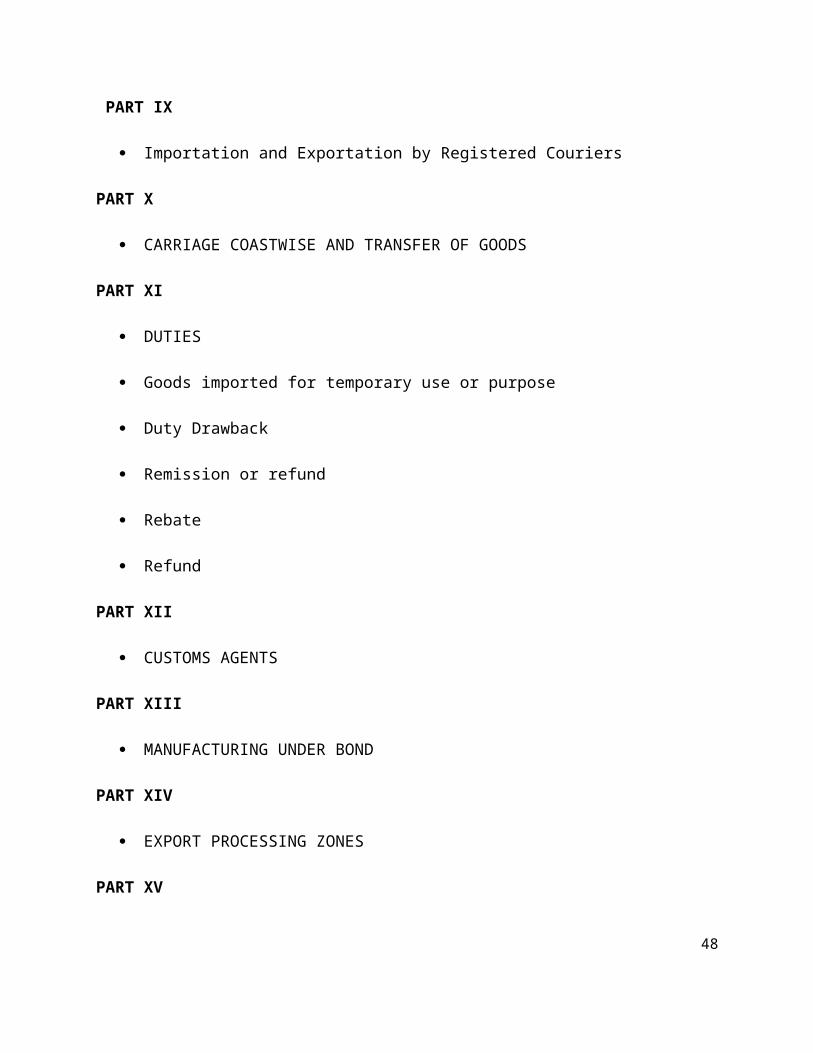

Importation and Exportation by Registered Couriers

PART X

CARRIAGE COASTWISE AND TRANSFER OF GOODS

PART XI

DUTIES

Goods imported for temporary use or purpose

Duty Drawback

Remission or refund

36

Rebate

Refund

PART XII

CUSTOMS AGENTS

PART XIII

MANUFACTURING UNDER BOND

PART XIV

EXPORT PROCESSING ZONES

PART XV

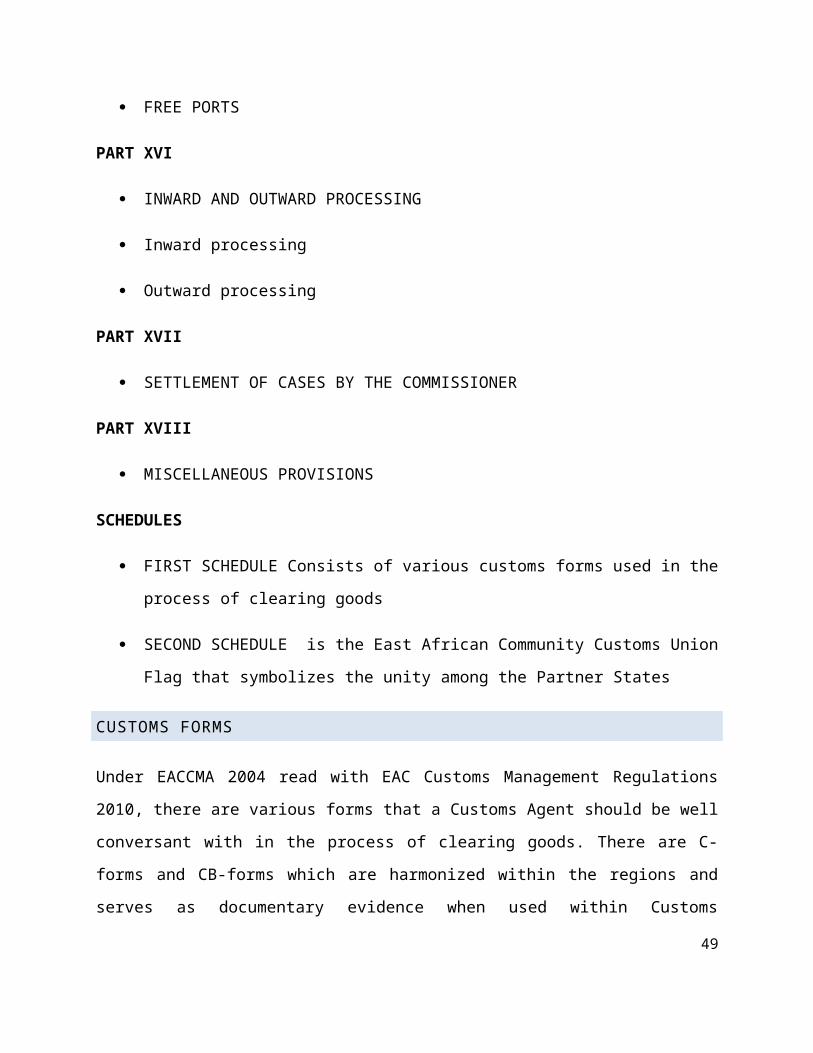

FREE PORTS

PART XVI

INWARD AND OUTWARD PROCESSING

Inward processing

Outward processing

PART XVII

SETTLEMENT OF CASES BY THE COMMISSIONER

PART XVIII

MISCELLANEOUS PROVISIONS

SCHEDULES

FIRST SCHEDULE Consists of various customs forms used in the process of clearing goods

37

SECOND SCHEDULE is the East African Community Customs Union Flag that symbolizes

the unity among the Partner States

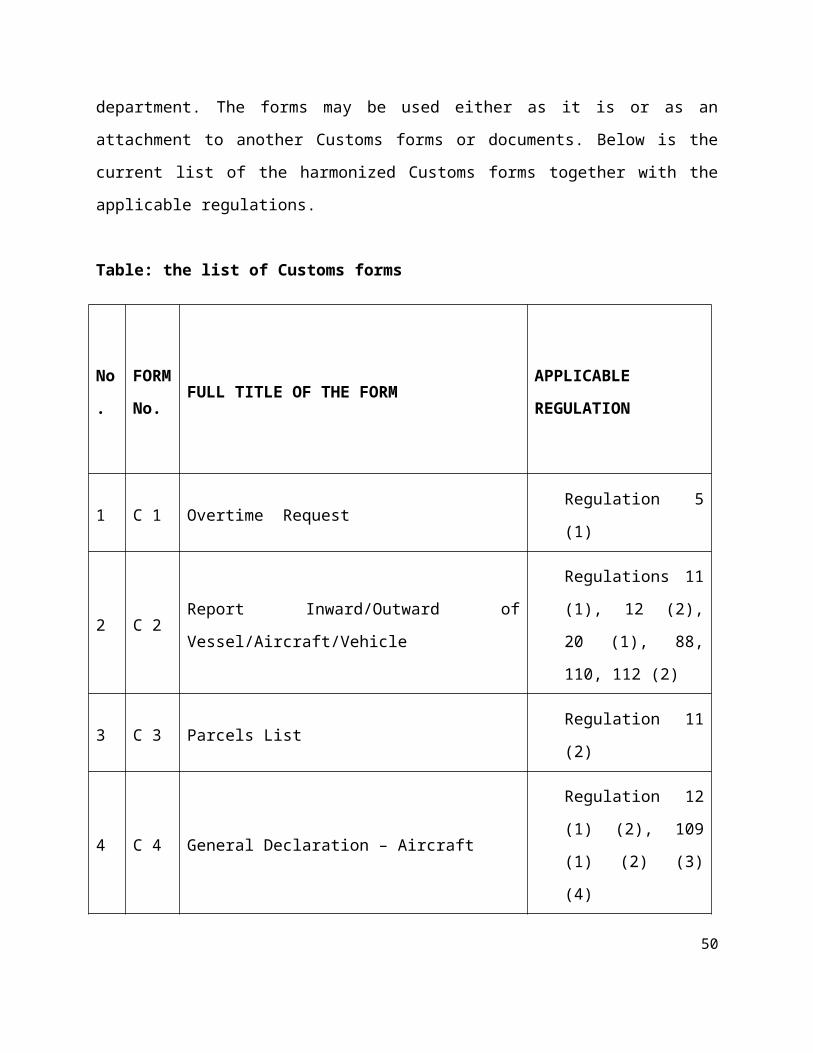

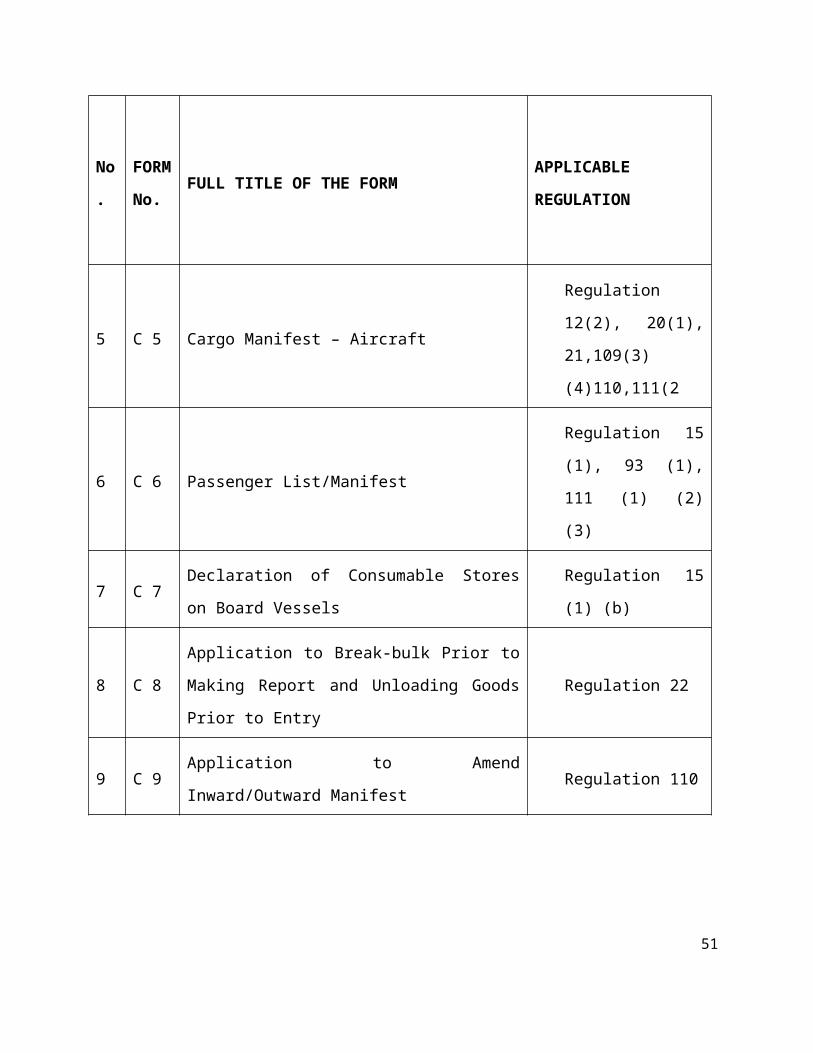

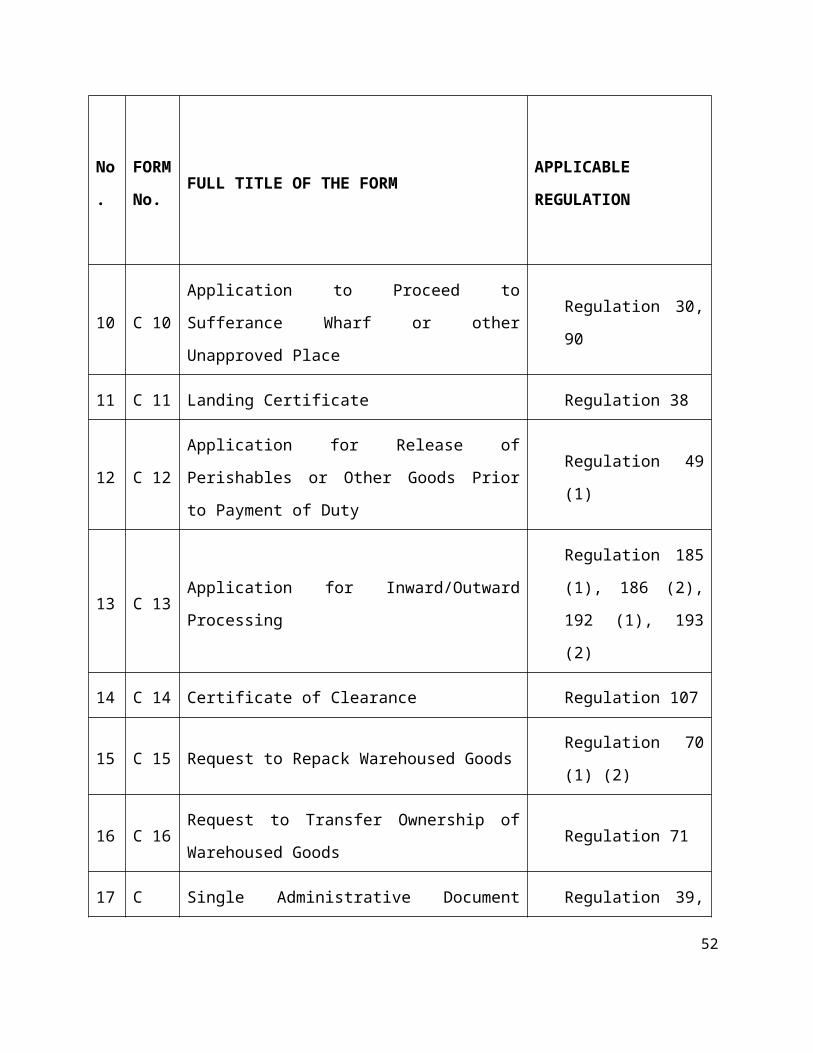

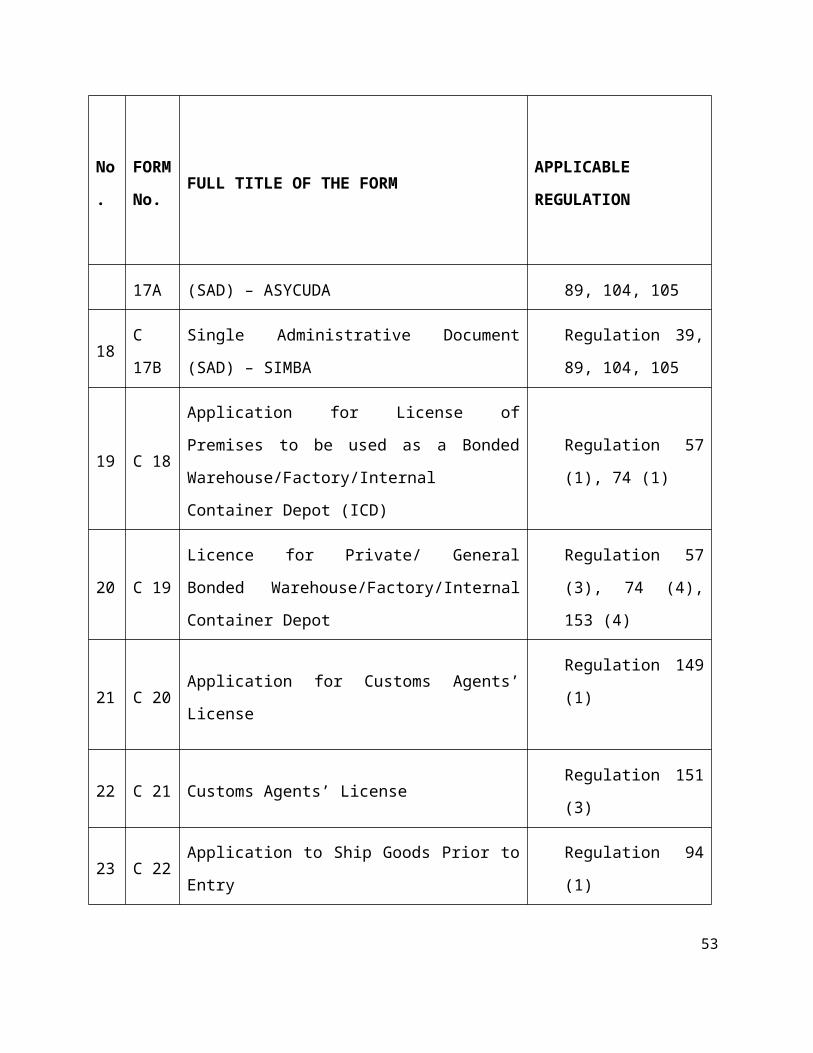

CUSTOMS FORMS

Under EACCMA 2004 read with EAC Customs Management Regulations 2010, there are various

forms that a Customs Agent should be well conversant with in the process of clearing goods.

There are C-forms and CB-forms which are harmonized within the regions and serves as

documentary evidence when used within Customs department. The forms may be used either

as it is or as an attachment to another Customs forms or documents. Below is the current list of

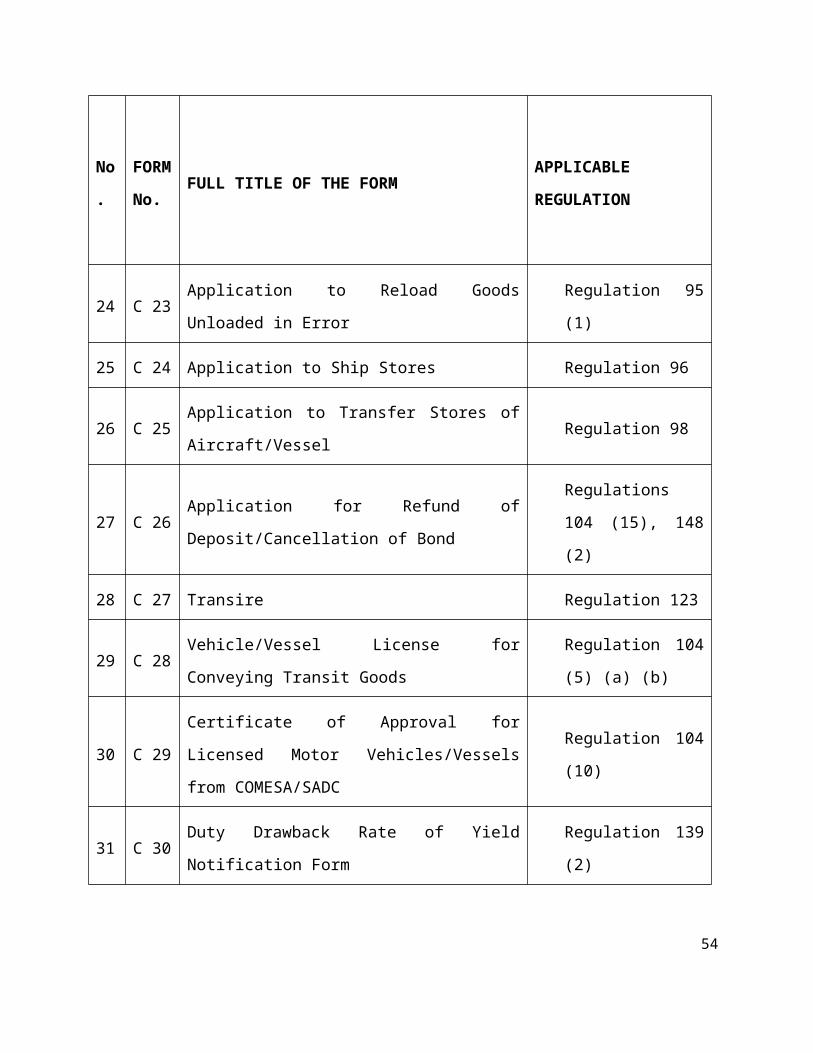

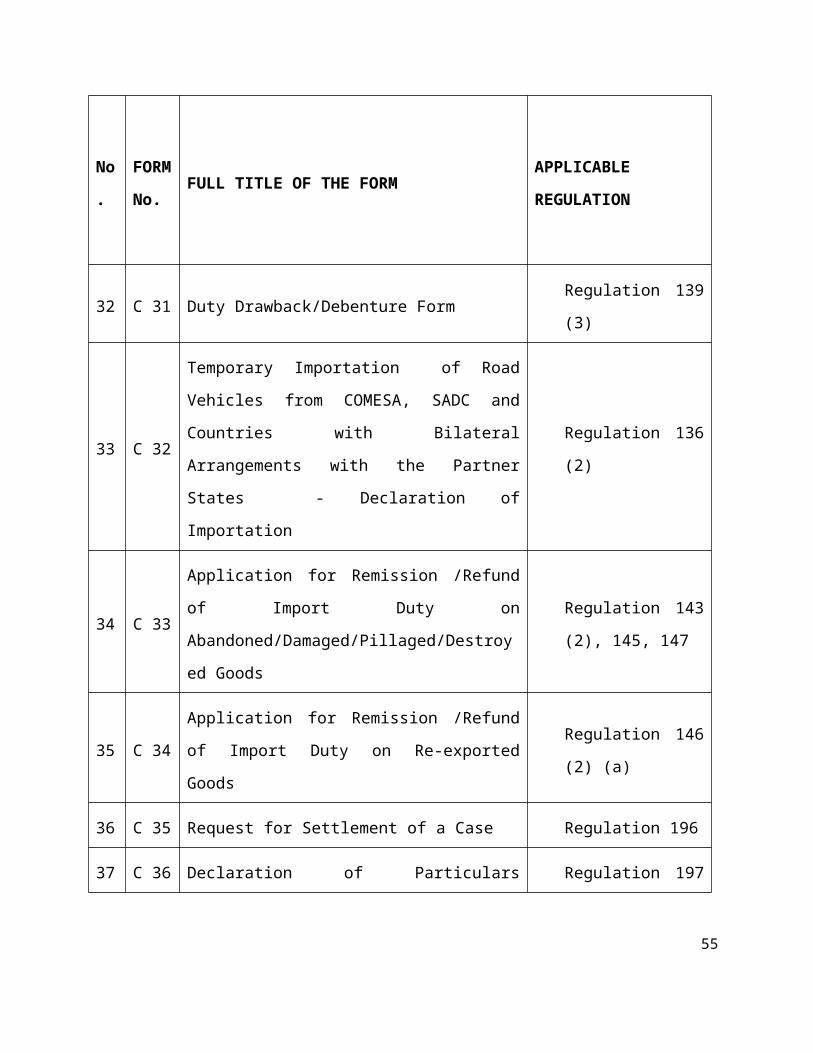

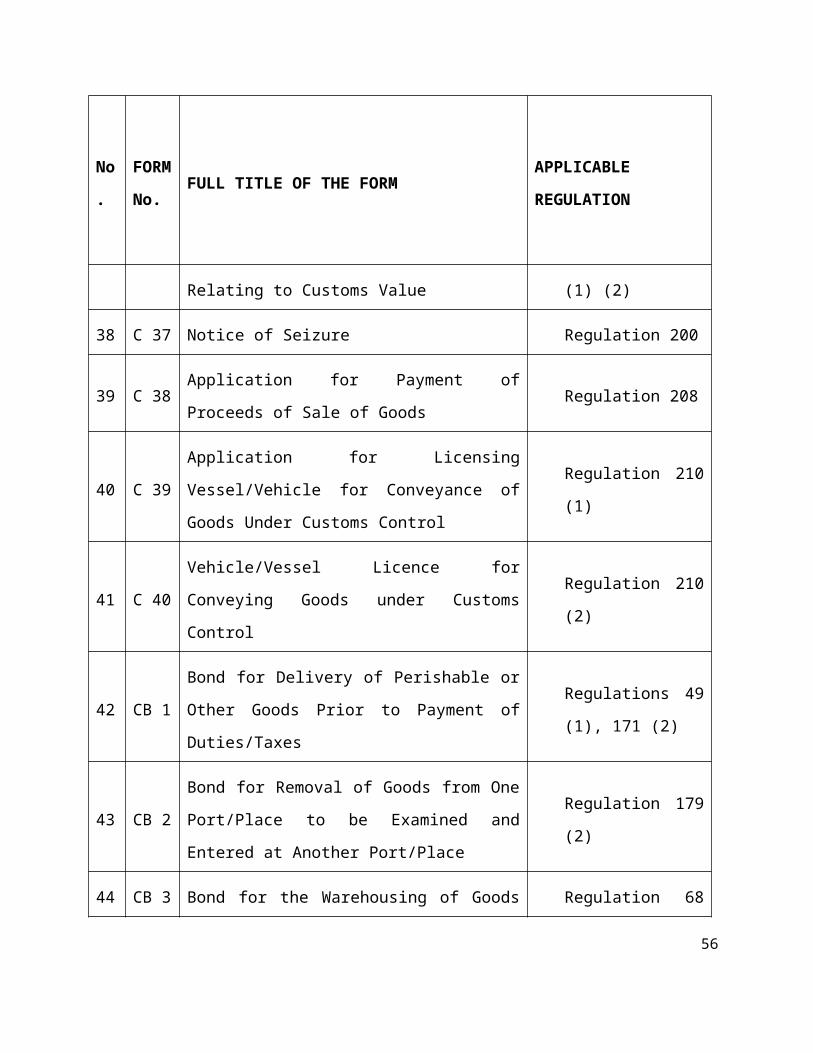

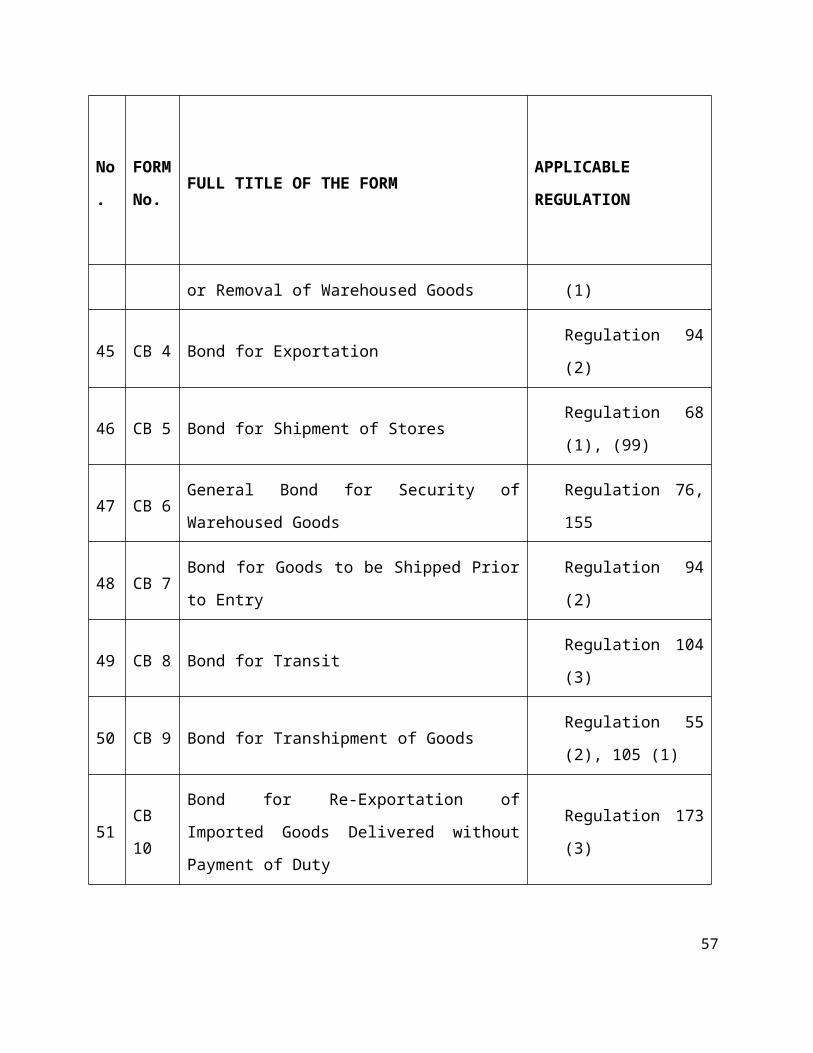

the harmonized Customs forms together with the applicable regulations.

Table: the list of Customs forms

No

.

FOR

M

No.

FULL TITLE OF THE FORMAPPLICABLE

REGULATION

1 C 1 Overtime Request Regulation 5 (1)

2 C 2 Report Inward/Outward of Vessel/Aircraft/Vehicle

Regulations 11 (1),

12 (2), 20 (1), 88,

110, 112 (2)

3 C 3 Parcels List Regulation 11 (2)

4 C 4 General Declaration – AircraftRegulation 12 (1) (2),

109 (1) (2) (3) (4)

5 C 5 Cargo Manifest – Aircraft Regulation 12(2),

38

No

.

FOR

M

No.

FULL TITLE OF THE FORMAPPLICABLE

REGULATION

20(1), 21,109(3)

(4)110,111(2

6 C 6 Passenger List/ManifestRegulation 15 (1), 93

(1), 111 (1) (2) (3)

7 C 7Declaration of Consumable Stores on Board

VesselsRegulation 15 (1) (b)

8 C 8Application to Break-bulk Prior to Making Report

and Unloading Goods Prior to EntryRegulation 22

9 C 9 Application to Amend Inward/Outward Manifest Regulation 110

10 C 10Application to Proceed to Sufferance Wharf or

other Unapproved PlaceRegulation 30, 90

11 C 11 Landing Certificate Regulation 38

12 C 12Application for Release of Perishables or Other

Goods Prior to Payment of DutyRegulation 49 (1)

13 C 13 Application for Inward/Outward Processing

Regulation 185 (1),

186 (2), 192 (1), 193

(2)

14 C 14 Certificate of Clearance Regulation 107

39

No

.

FOR

M

No.

FULL TITLE OF THE FORMAPPLICABLE

REGULATION

15 C 15 Request to Repack Warehoused Goods Regulation 70 (1) (2)

16 C 16Request to Transfer Ownership of Warehoused

GoodsRegulation 71

17 C 17A Single Administrative Document (SAD) – ASYCUDARegulation 39, 89,

104, 105

18 C 17B Single Administrative Document (SAD) – SIMBARegulation 39, 89,

104, 105

19 C 18

Application for License of Premises to be used as a

Bonded Warehouse/Factory/Internal Container

Depot (ICD)

Regulation 57 (1), 74

(1)

20 C 19Licence for Private/ General Bonded

Warehouse/Factory/Internal Container Depot

Regulation 57 (3), 74

(4), 153 (4)

21 C 20 Application for Customs Agents’ LicenseRegulation 149 (1)

22 C 21 Customs Agents’ License Regulation 151 (3)

23 C 22 Application to Ship Goods Prior to Entry Regulation 94 (1)

24 C 23 Application to Reload Goods Unloaded in Error Regulation 95 (1)

25 C 24 Application to Ship Stores Regulation 96

40

No

.

FOR

M

No.

FULL TITLE OF THE FORMAPPLICABLE

REGULATION

26 C 25 Application to Transfer Stores of Aircraft/Vessel Regulation 98

27 C 26Application for Refund of Deposit/Cancellation of

Bond

Regulations 104 (15),

148 (2)

28 C 27 Transire Regulation 123

29 C 28 Vehicle/Vessel License for Conveying Transit GoodsRegulation 104 (5)

(a) (b)

30 C 29Certificate of Approval for Licensed Motor

Vehicles/Vessels from COMESA/SADCRegulation 104 (10)

31 C 30 Duty Drawback Rate of Yield Notification Form Regulation 139 (2)

32 C 31 Duty Drawback/Debenture Form Regulation 139 (3)

33 C 32

Temporary Importation of Road Vehicles from

COMESA, SADC and Countries with Bilateral

Arrangements with the Partner States -

Declaration of Importation

Regulation 136 (2)

34 C 33

Application for Remission /Refund of Import Duty

on Abandoned/Damaged/Pillaged/Destroyed

Goods

Regulation 143 (2),

145, 147

35 C 34 Application for Remission /Refund of Import Duty Regulation 146 (2)

41

No

.

FOR

M

No.

FULL TITLE OF THE FORMAPPLICABLE

REGULATION

on Re-exported Goods (a)

36 C 35 Request for Settlement of a Case Regulation 196

37 C 36Declaration of Particulars Relating to Customs

Value

Regulation 197 (1)

(2)

38 C 37 Notice of Seizure Regulation 200

39 C 38Application for Payment of Proceeds of Sale of

GoodsRegulation 208

40 C 39Application for Licensing Vessel/Vehicle for

Conveyance of Goods Under Customs ControlRegulation 210 (1)

41 C 40Vehicle/Vessel Licence for Conveying Goods under

Customs ControlRegulation 210 (2)

42 CB 1Bond for Delivery of Perishable or Other Goods

Prior to Payment of Duties/Taxes

Regulations 49 (1),

171 (2)

43 CB 2Bond for Removal of Goods from One Port/Place to

be Examined and Entered at Another Port/PlaceRegulation 179 (2)

44 CB 3Bond for the Warehousing of Goods or Removal of

Warehoused GoodsRegulation 68 (1)

45 CB 4 Bond for Exportation Regulation 94 (2)

42

No

.

FOR

M

No.

FULL TITLE OF THE FORMAPPLICABLE

REGULATION

46 CB 5 Bond for Shipment of StoresRegulation 68 (1),

(99)

47 CB 6 General Bond for Security of Warehoused Goods Regulation 76, 155

48 CB 7 Bond for Goods to be Shipped Prior to Entry Regulation 94 (2)

49 CB 8 Bond for Transit Regulation 104 (3)

50 CB 9 Bond for Transhipment of GoodsRegulation 55 (2),

105 (1)

51 CB 10Bond for Re-Exportation of Imported Goods

Delivered without Payment of DutyRegulation 173 (3)

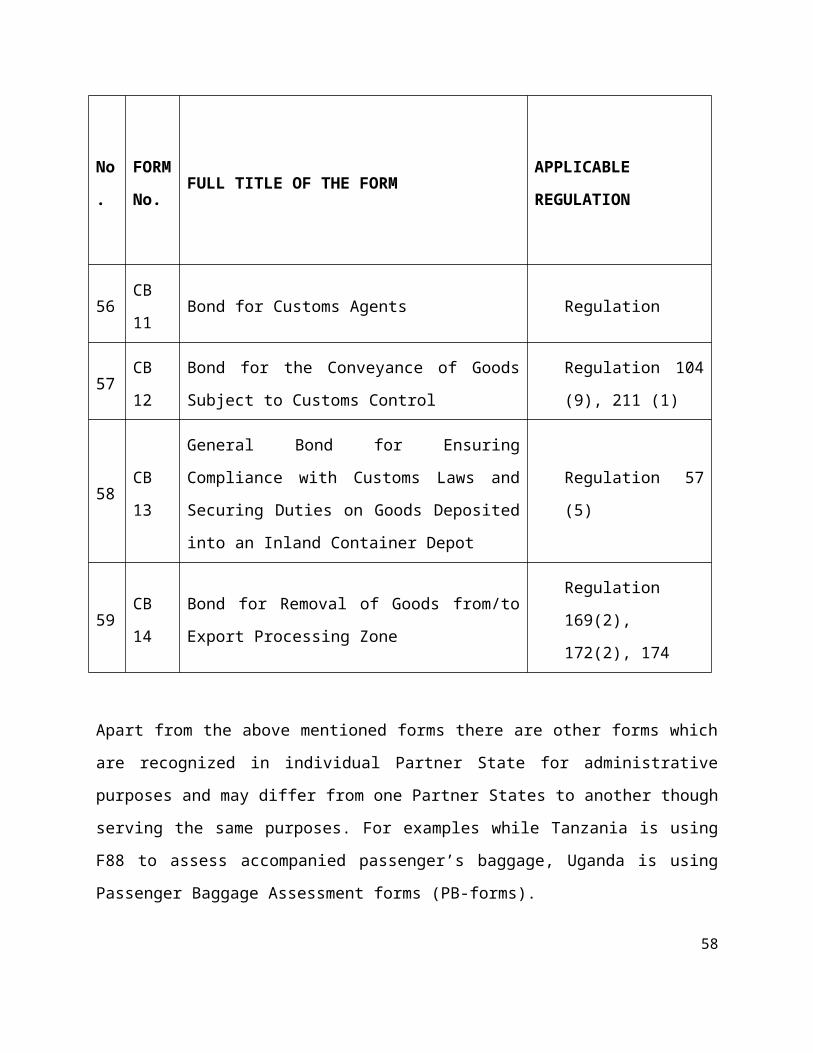

56 CB 11 Bond for Customs Agents Regulation

57 CB 12Bond for the Conveyance of Goods Subject to

Customs Control

Regulation 104 (9),

211 (1)

58 CB 13

General Bond for Ensuring Compliance with

Customs Laws and Securing Duties on Goods

Deposited into an Inland Container Depot

Regulation 57 (5)

59 CB 14Bond for Removal of Goods from/to Export

Processing Zone

Regulation 169(2),

172(2), 174

43

Apart from the above mentioned forms there are other forms which are recognized in

individual Partner State for administrative purposes and may differ from one Partner States to

another though serving the same purposes. For examples while Tanzania is using F88 to assess

accompanied passenger’s baggage, Uganda is using Passenger Baggage Assessment forms (PB-

forms).

FEES AND PENALTIES

To ensure compliance to the Customs laws and regulations, the Act provide for penalties in case

of non- compliance. These are charges imposed for either doing what is not supposed to be

done or abstain from doing the rightful act within the premises of the laws and regulations.

There are penalties applied in respect to Customs offences for example;

Offence on arrival (Sec 21)

i. Landing a vessel, aircraft or vehicle at place other than authorized port or are

within the Partner States

ii. Departing from the authorized place of unloading without clearence from the

proper officer

iii. The return of a vessel, aircraft or motor vehicle into Partner State after depature

to foreign without authority of the Proper Officer while on any voyage to a

foreign port, bring the vessel or aircraft into within the Partner States except in

accordance with the Act.

iv. A person should consult a Proper Officer before boarding a vessel. If he/she does

it commits an offence and shall be liable to a fine not exceeding $25O (Sec 23).

It is an offence to remove goods from a Customs area without payment of duty. Once removed,

these goods shall be liable to forfeiture (Sec 39).

44

It is an offence for people to disembark from an aircraft or vessel. A place shall be appointed in

accordance with section 11 of the Act (Sec 44).

Warehoused goods can be delivered as stores provided they shall not be used as stores for a

vessel of less than 250 tons. Contravention of this provision is an offence (Sec 55).

Taking warehoused goods unlawfully is an offence, once committed, there is a penalty of an

emprisonment term not exceeding two years or a fine equal to 25% of the dutiable value of

goods (Sec 61).

Failure to enter cargo for exportation in the prescribed manner and lack of documentary

evidence of the goods referred to in the entry is an offence (Sec 73).

Deficiency in cargo is when the goods are reported on arrival as remaining on board and yet

upon inspection, the goods are actually not on board.This is also an offence (Sec 91).

Surplus in cargo is when goods which are not contained in the manifest are found on an aircraft

or vessel. Any goods in respect of which such offence has been committed shall be lable to

forteiture.

The transire should be delivered to the proper officer immediately, but in the case of a vessel of

250 tons register, such transire may be delivered within 24 hrs of arrival. ( Sec 101)

Goods on transit should be conveyed on routes approved by the Commissioner. A person who

does not follow the specified route commits an offence. (Sec104)

The owner of goods shall be prosecuted for any offence committed by his authorized agent as

if the owner has himself committed the offence. (Sec 160)

It is an offence for any person to use his premises for manufacture under bond without a

license and on conviction will be liable to a fine not exceeding $5000 or imprisonment for a

term not exceeding three years or both. (Sec 160)

45

It is possible for a licensee to alter the premises of a bonded factory as long as he/she has prior

permission from the commissioner. (Sec 161)

It is an offence to remove goods from an export processing zone or freeport for home

consumption without prior authority from the Commissioner. The offender shall be liable to a

fine of $5000 or 50% of the value of the goods, whichever is higher. ( Sec 168)

Any individual person who accesses Customs computerized system without prior authorization

commits an offence and is liable to an imprisonmet for a term not exceeding two years or a fine

not exceeding five US thousand dollars.

In the case of a corporate body , a fine not exceeding twenty five thousand US dollars.

Any person who conspires with others to act contrary to the CMA commits an offence

punishable by 5 years imprisonment if convicted.

Aperson who for no reason shoots at any aircraft , vessel or vehicle belonging to Customs,

wounds an officer on duty in the process or commits any form of violent acts commits an

offence punishable by improsonment for a period not exceeding 20 years.

A person who commits an offence with any firearm or other weapons and is found with goods

that should be detained commits an offence punishable by imprisonment for a period not

exceeding 10 years

Aperson who commits a crime in disguise and poses illegal goods whilw doing so commits an

offence punishable by imprisonment for a period not exceeding 3 years

A person who breaks, destroys or throws seized goods off an air craft, vessel or vehicle, rescues

any person arrested for any offence or obstructs any officer commits an offence.

46