Embed Size (px)

Citation preview

Eagle Mine Site VisitNovember 3-4, 2014

Cautionary Statements

Caution Regarding Forward Looking Statements

This presentation contains forward-looking statements. These forward-looking statements arenot based on historical facts, but rather on current expectations and projections about futureevents. These forward-looking statements are subject to risks and uncertainties. These risksand uncertainties could cause actual results to differ materially from the future resultsexpressed or implied by the forward-looking statements.

Such risks may include, without limitation: risks and uncertainties relating to foreign currencyfluctuations; risks inherent in mining including environmental hazards, unusual or unexpectedgeological formations, ground control problems and flooding; risks associated with theestimation of mineral resources and reserves and the geology, grade and continuity of mineraldeposits; the possibility that future exploration, development or mining results will not beconsistent with the Company’s expectations; the potential for and effects of labor disputes orother unanticipated difficulties with or shortages of labor or interruptions in production; actualore mined varying from estimates of grade, tonnage, dilution and metallurgical and othercharacteristics; the inherent uncertainty of production and cost estimates and the potential forunexpected costs and expenses; and commodity price fluctuations.

For further details of other risks and uncertainties see Risk Factors Relating to the Company’sBusiness in the Company’s Annual Information Form and in each management discussion andanalysis.

Note: All dollar amounts are in US dollars unless otherwise denoted.

2

Table of Contents

• Introduction

•Safety, Environment & Social Responsibility

•Project Overview

•Exploration

•Corporate Update

3

INTRODUCTION(Mike Welch)

4

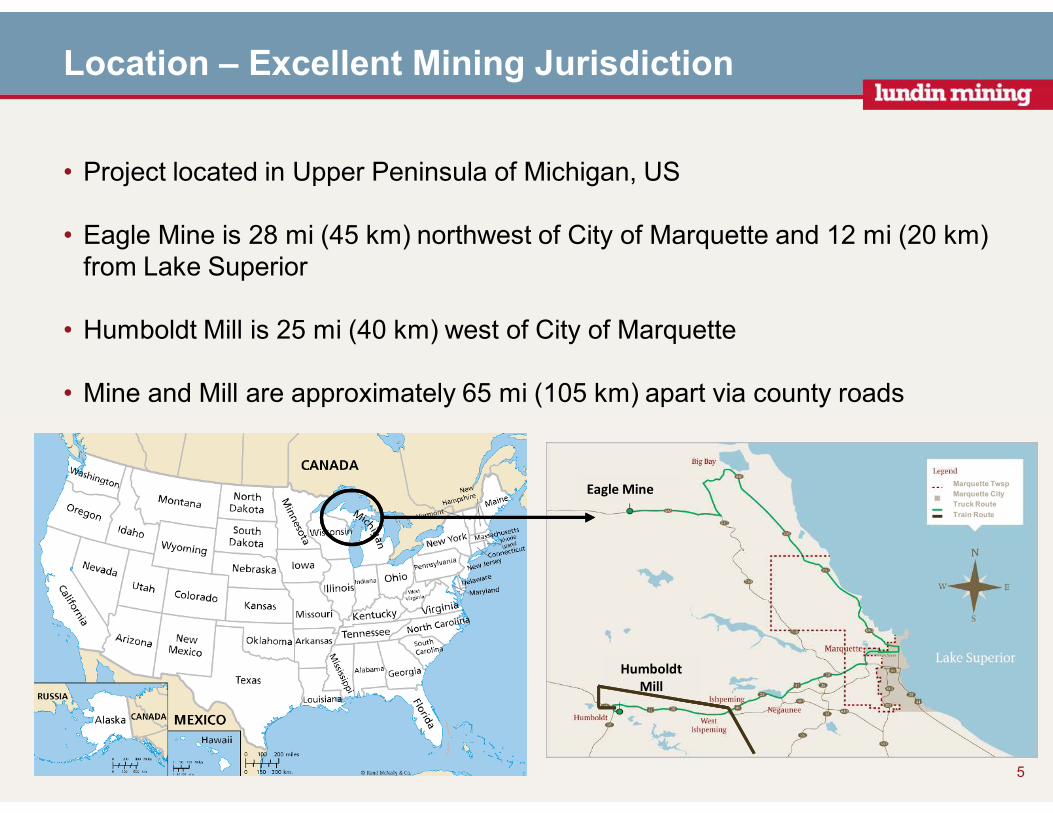

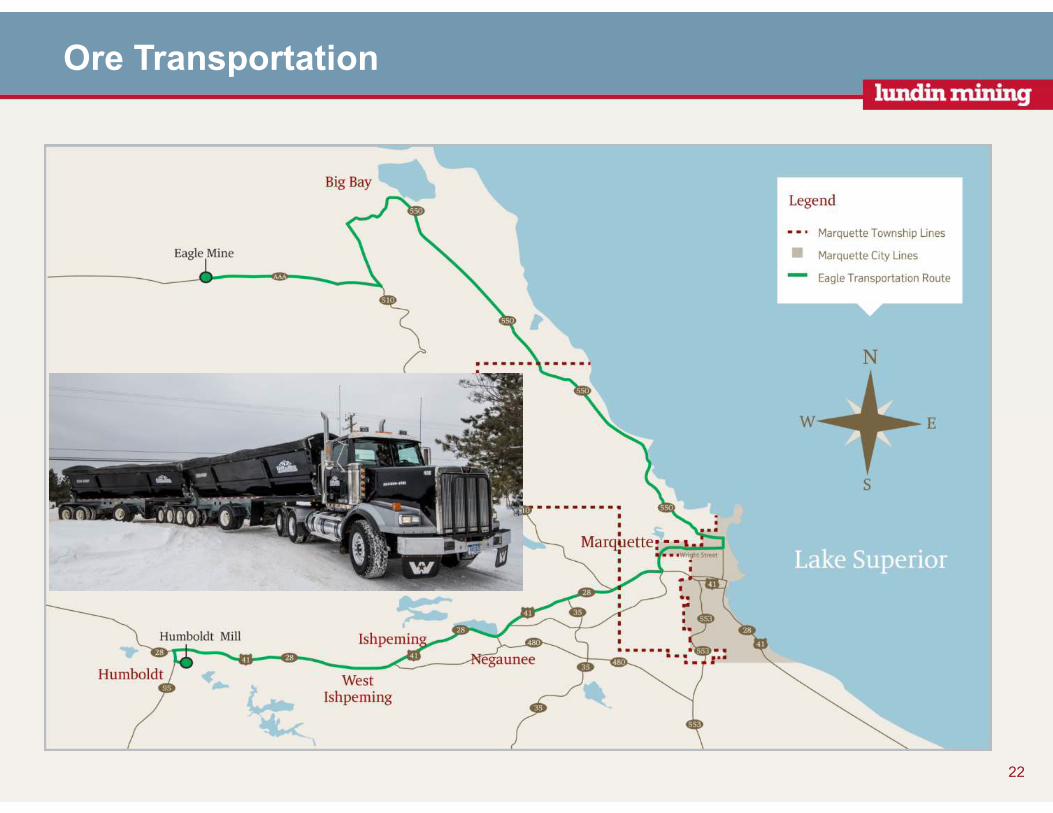

• Project located in Upper Peninsula of Michigan, US

• Eagle Mine is 28 mi (45 km) northwest of City of Marquette and 12 mi (20 km) from Lake Superior

• Humboldt Mill is 25 mi (40 km) west of City of Marquette

• Mine and Mill are approximately 65 mi (105 km) apart via county roads

Marquette Twsp

Marquette City

Truck Route

Train Route

Location – Excellent Mining Jurisdiction

5

Eagle Mine

Humboldt

Mill

Overview – High Grade Nickel and Copper Producer

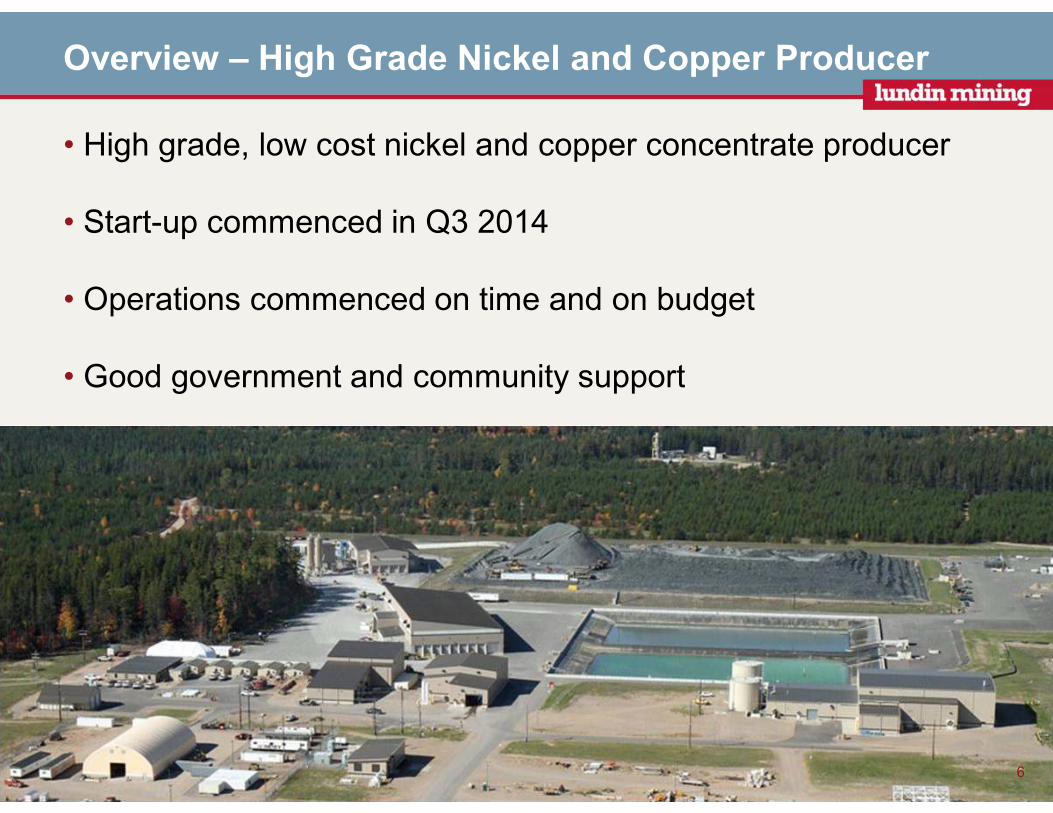

• High grade, low cost nickel and copper concentrate producer

• Start-up commenced in Q3 2014

• Operations commenced on time and on budget

• Good government and community support

6

Health & Safety

7

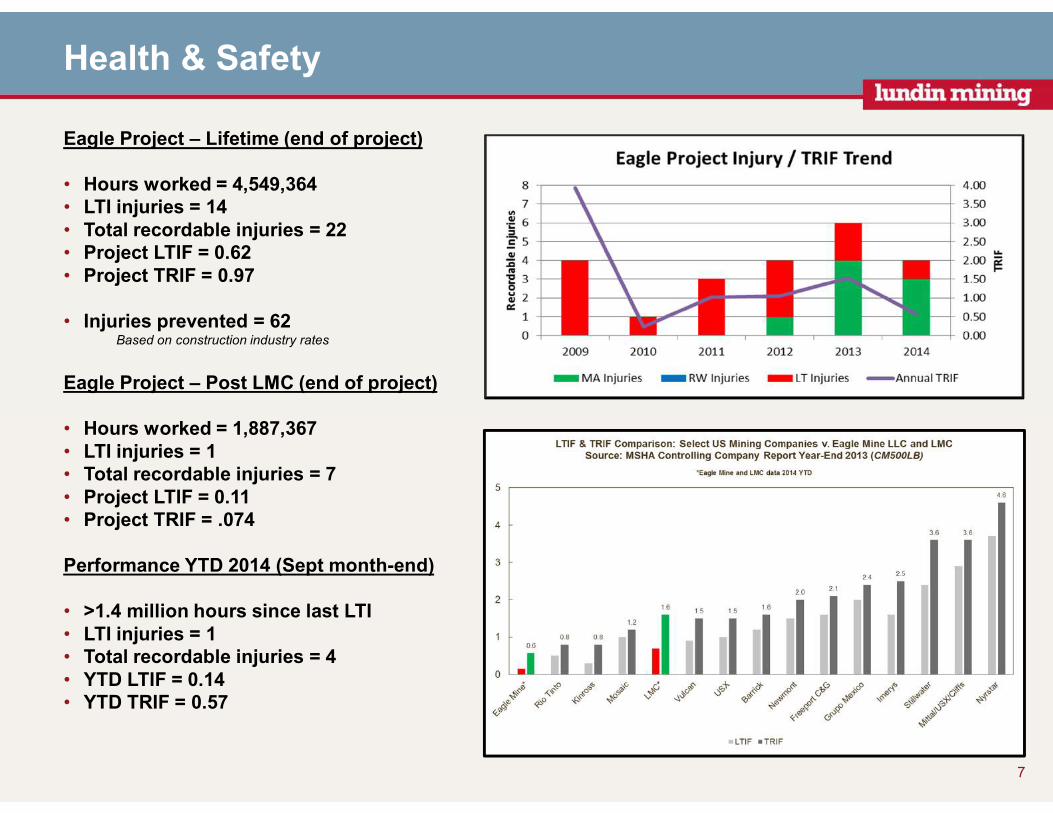

Eagle Project – Lifetime (end of project)

• Hours worked = 4,549,364• LTI injuries = 14• Total recordable injuries = 22• Project LTIF = 0.62• Project TRIF = 0.97

• Injuries prevented = 62Based on construction industry rates

Eagle Project – Post LMC (end of project)

• Hours worked = 1,887,367• LTI injuries = 1• Total recordable injuries = 7• Project LTIF = 0.11• Project TRIF = .074

Performance YTD 2014 (Sept month-end)

• >1.4 million hours since last LTI• LTI injuries = 1 • Total recordable injuries = 4• YTD LTIF = 0.14• YTD TRIF = 0.57

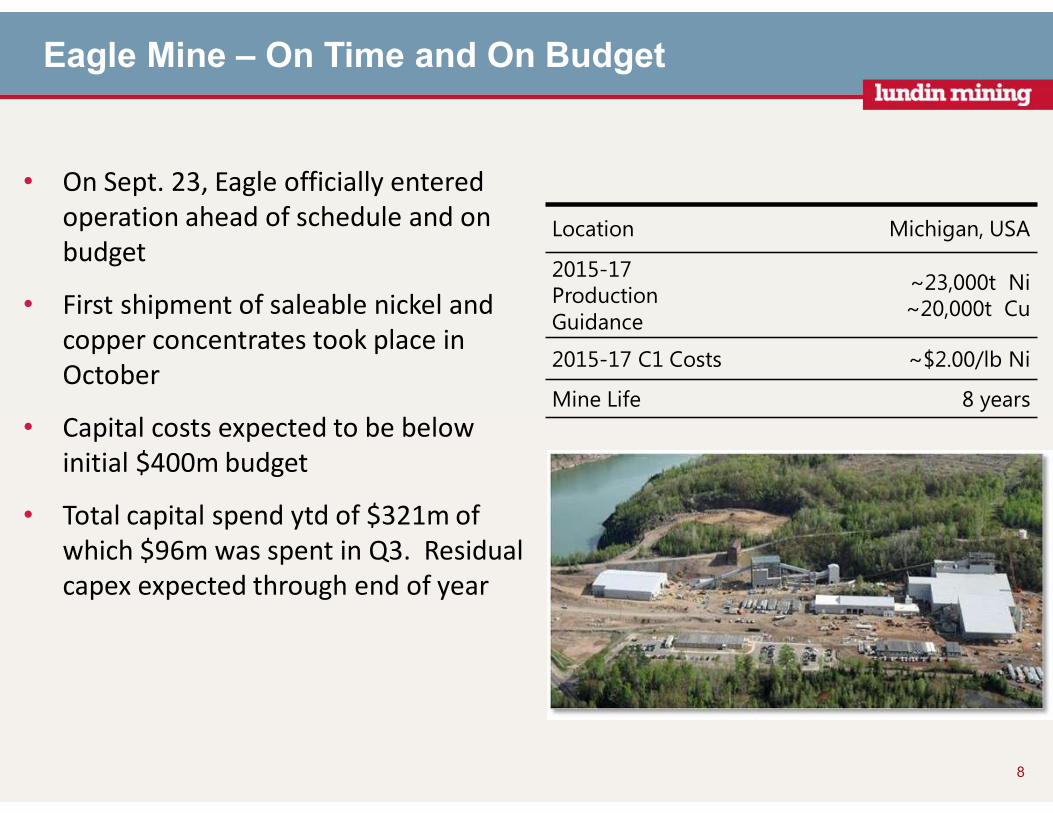

Location Michigan, USA

2015-17 Production Guidance

~23,000t Ni~20,000t Cu

2015-17 C1 Costs ~$2.00/lb Ni

Mine Life 8 years

8

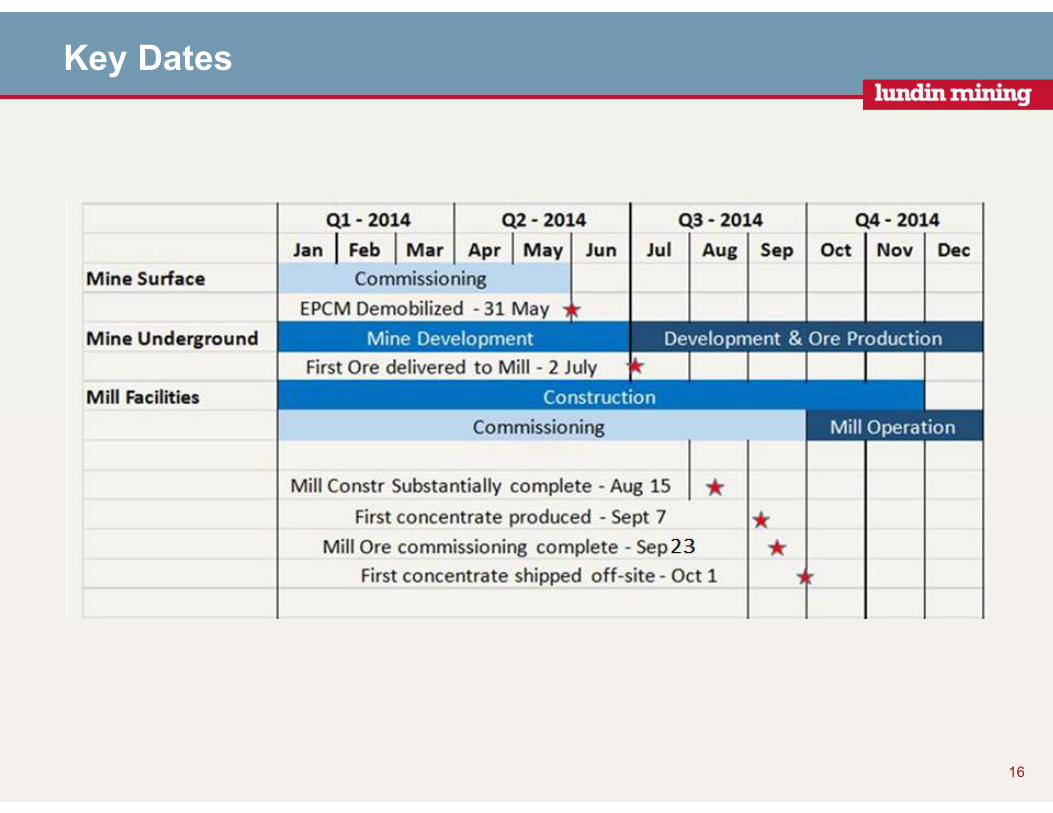

Eagle Mine – On Time and On Budget

• On Sept. 23, Eagle officially entered

operation ahead of schedule and on

budget

• First shipment of saleable nickel and

copper concentrates took place in

October

• Capital costs expected to be below

initial $400m budget

• Total capital spend ytd of $321m of

which $96m was spent in Q3. Residual

capex expected through end of year

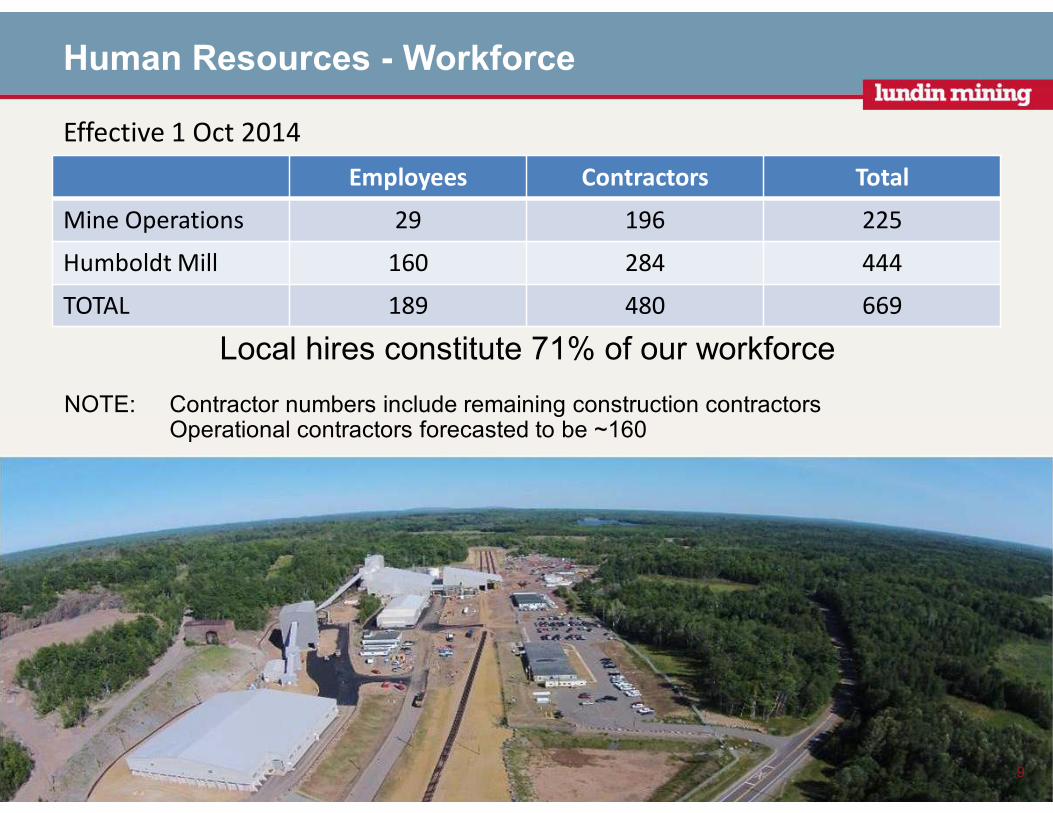

Human Resources - Workforce

Employees Contractors Total

Mine Operations 29 196 225

Humboldt Mill 160 284 444

TOTAL 189 480 669

9

Local hires constitute 71% of our workforce

NOTE: Contractor numbers include remaining construction contractorsOperational contractors forecasted to be ~160

Effective 1 Oct 2014

Environment and Social Responsibility(Kristen Mariuzza & Matt Johnson)

10

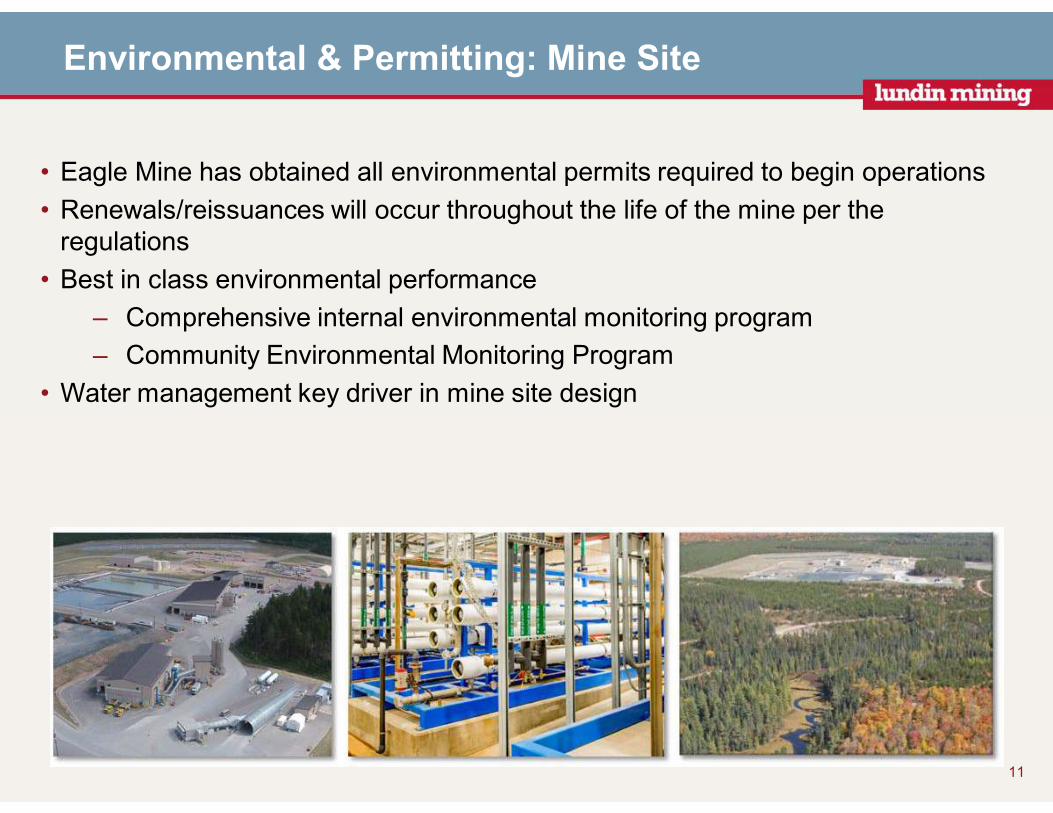

Environmental & Permitting: Mine Site

• Eagle Mine has obtained all environmental permits required to begin operations

• Renewals/reissuances will occur throughout the life of the mine per the regulations

• Best in class environmental performance

– Comprehensive internal environmental monitoring program

– Community Environmental Monitoring Program

• Water management key driver in mine site design

11

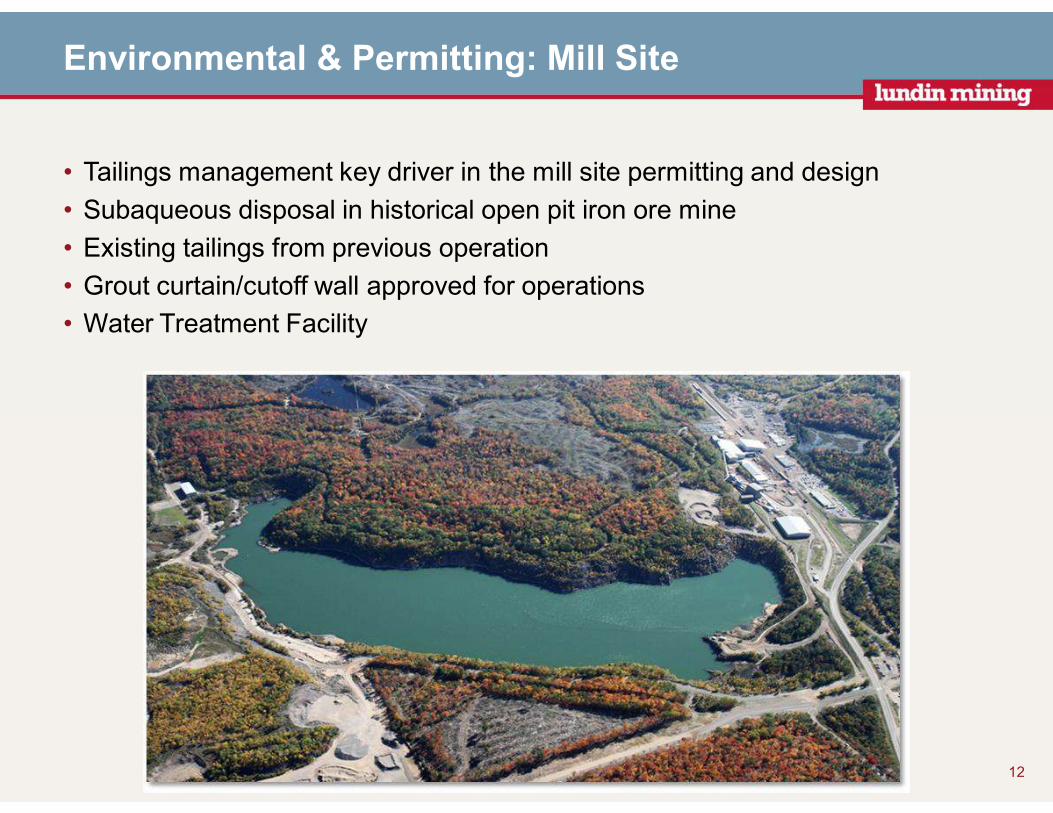

Environmental & Permitting: Mill Site

• Tailings management key driver in the mill site permitting and design

• Subaqueous disposal in historical open pit iron ore mine

• Existing tailings from previous operation

• Grout curtain/cutoff wall approved for operations

• Water Treatment Facility

12

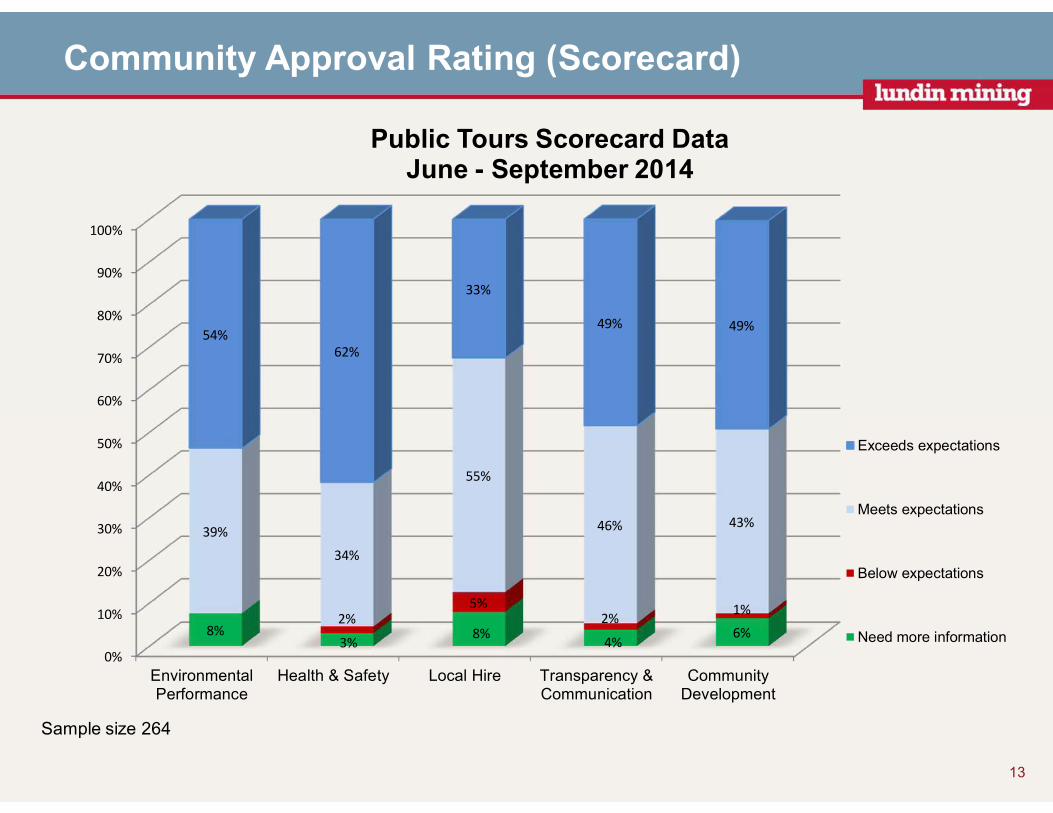

Community Approval Rating (Scorecard)

13

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

EnvironmentalPerformance

Health & Safety Local Hire Transparency &Communication

CommunityDevelopment

8%3%

8%4%

6%2%

5%2%

1%

39%

34%

55%

46% 43%

54%

62%

33%

49% 49%

Public Tours Scorecard Data June - September 2014

Exceeds expectations

Meets expectations

Below expectations

Need more information

Sample size 264

Community Approval Rating (Scorecard)

“Community engagement is Eagle’s social responsibility”

14

0%

20%

40%

60%

80%

100%

Fall 2012 Spring 2013 Fall 2013 Spring 2014 Summer 2014

Environment Safety Local Hire Transparency Community Development

Project Overview(Mike Welch)

15

Key Dates

16

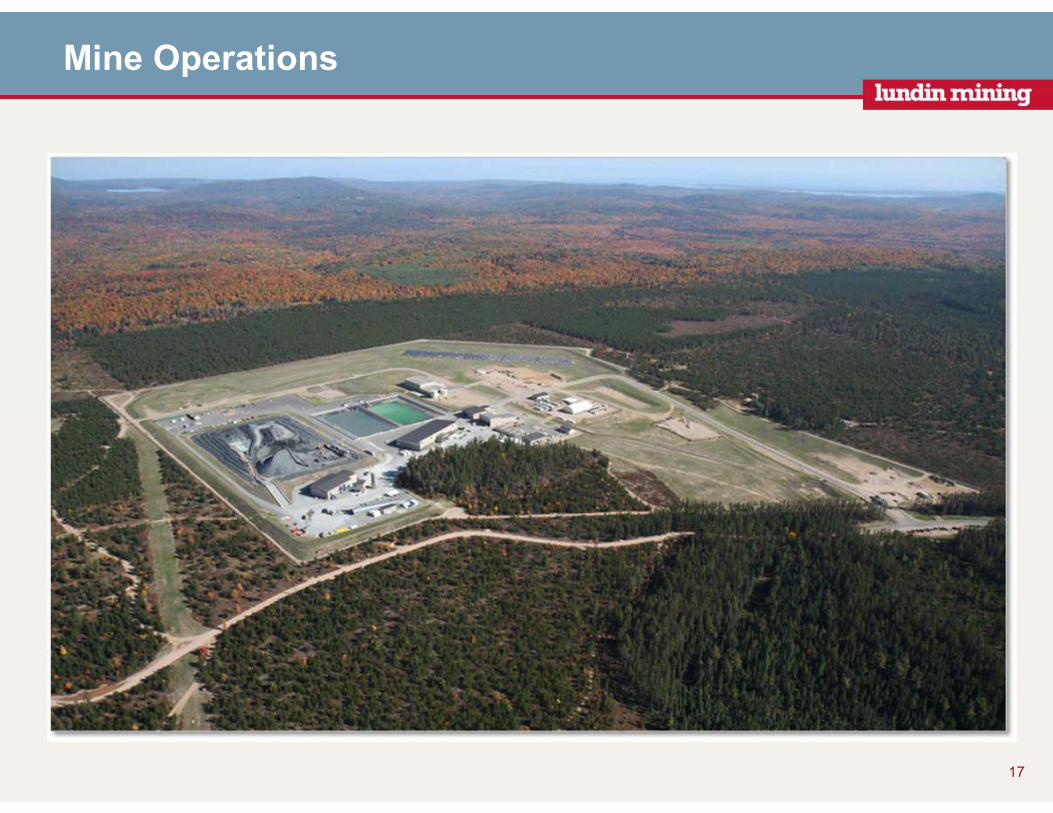

Mine Operations

Mine Operations

17

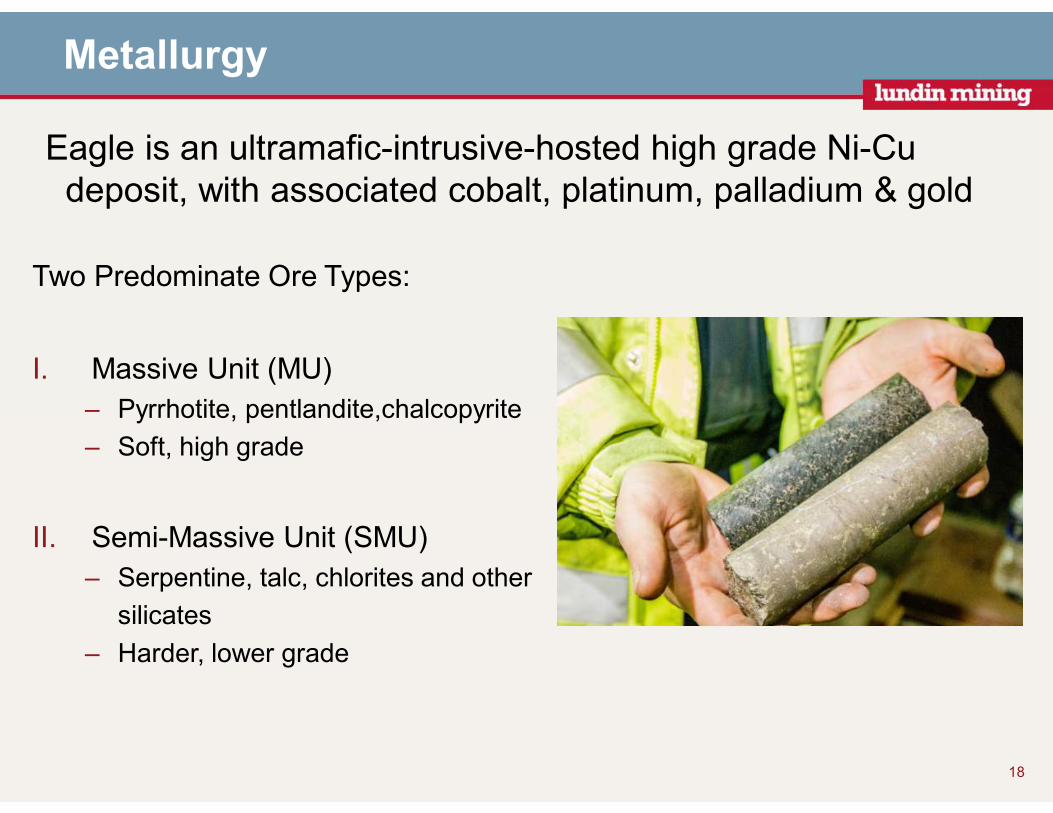

Metallurgy

Two Predominate Ore Types:

I. Massive Unit (MU)

– Pyrrhotite, pentlandite,chalcopyrite

– Soft, high grade

II. Semi-Massive Unit (SMU)

– Serpentine, talc, chlorites and other

silicates

– Harder, lower grade

18

Eagle is an ultramafic-intrusive-hosted high grade Ni-Cu deposit, with associated cobalt, platinum, palladium & gold

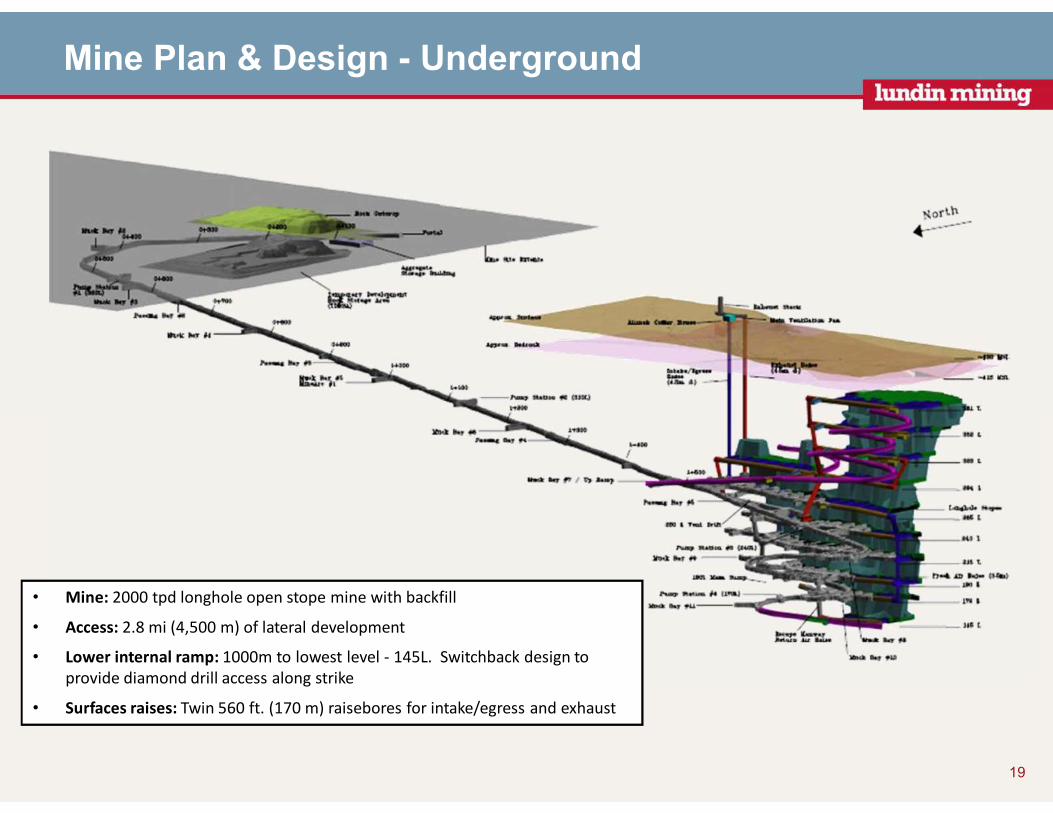

Mine Plan & Design - Underground

19

• Mine: 2000 tpd longhole open stope mine with backfill

• Access: 2.8 mi (4,500 m) of lateral development

• Lower internal ramp: 1000m to lowest level - 145L. Switchback design to

provide diamond drill access along strike

• Surfaces raises: Twin 560 ft. (170 m) raisebores for intake/egress and exhaust

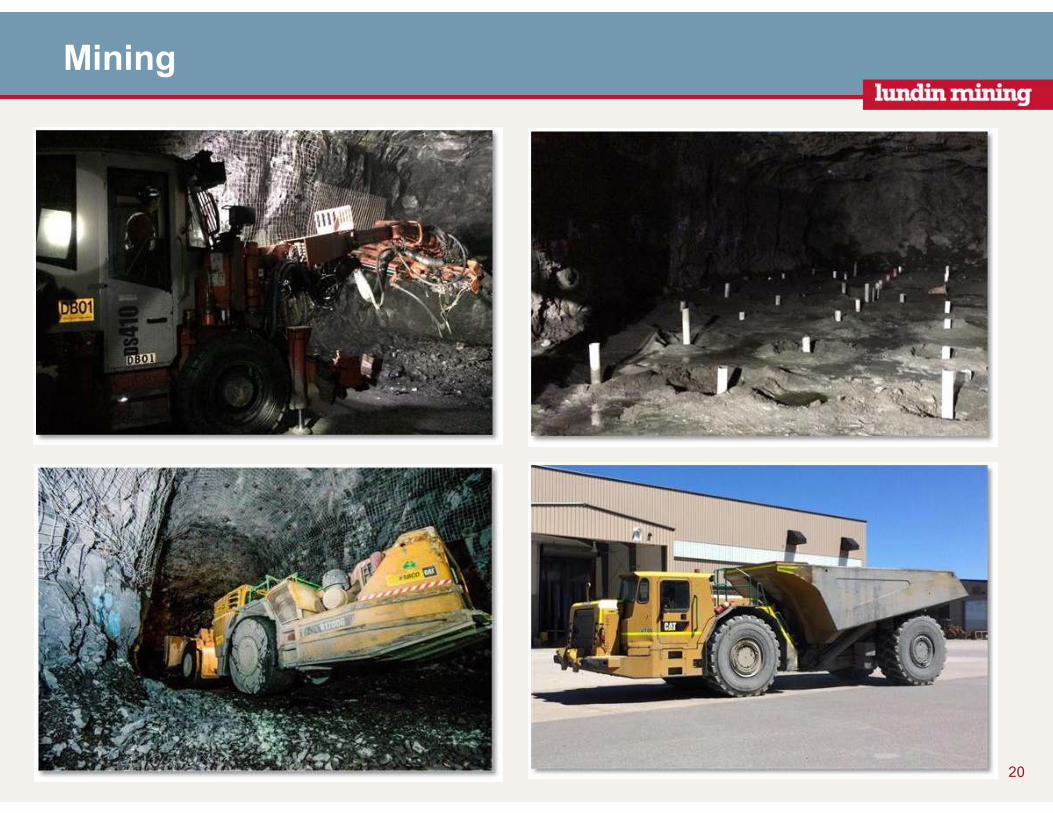

Mining

20

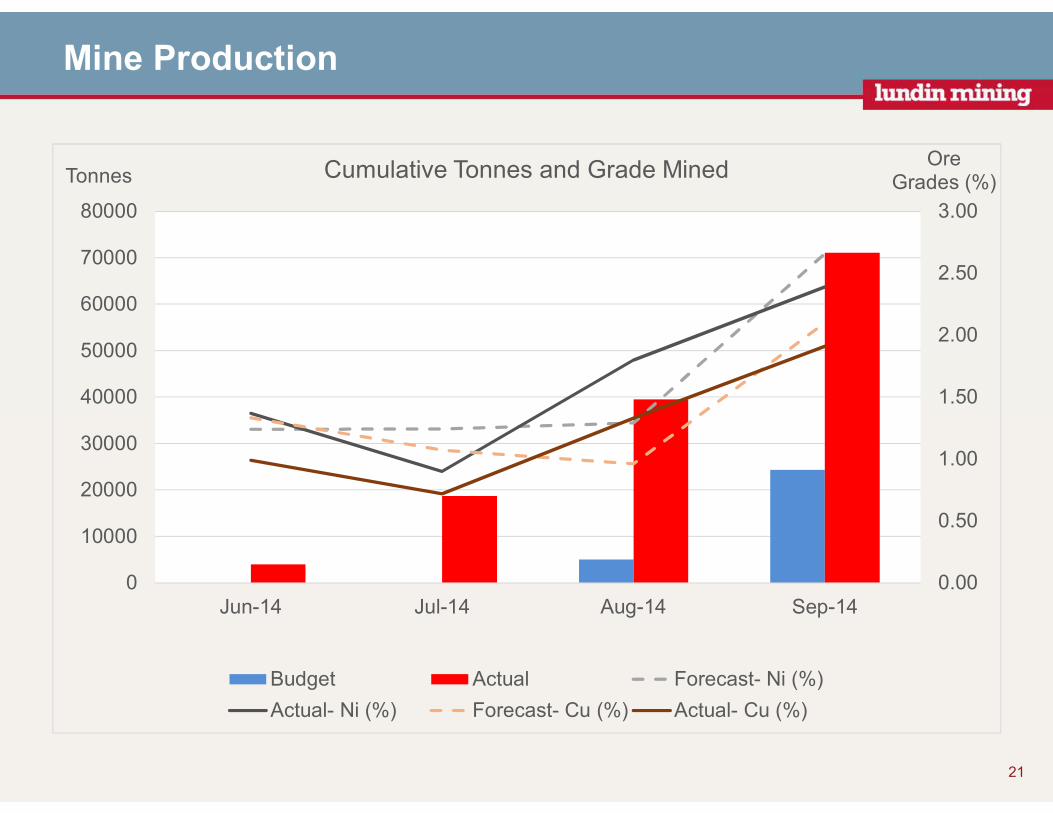

Mine Production

21

0.00

0.50

1.00

1.50

2.00

2.50

3.00

Jun-14 Jul-14 Aug-14 Sep-140

10000

20000

30000

40000

50000

60000

70000

80000

OreGrades (%)Tonnes Cumulative Tonnes and Grade Mined

Budget Actual Forecast- Ni (%)

Actual- Ni (%) Forecast- Cu (%) Actual- Cu (%)

Ore Transportation

22

Humboldt Mill

23

Mill Operations

Metallurgy

High Level Design Criteria

• 2,000 tpd operation at 95% availability

• 3-stage crushing plant (8 hr/day, 7-day/week operation)

• Concentrator (24 hr/day, 7-day/week operation)

• Concentrate Load-out (8 hr/day, 7 days/week depending on production)

Straight Forward Processing Circuit

• Conventional flotation to produce separate Ni and Cu concentrates

• Expected life of mine recovery is 82% nickel and 93% copper

• Flotation tailings thickened and deposited subaqueously in the existing Humboldt tailings disposal facility

24

Milling Process

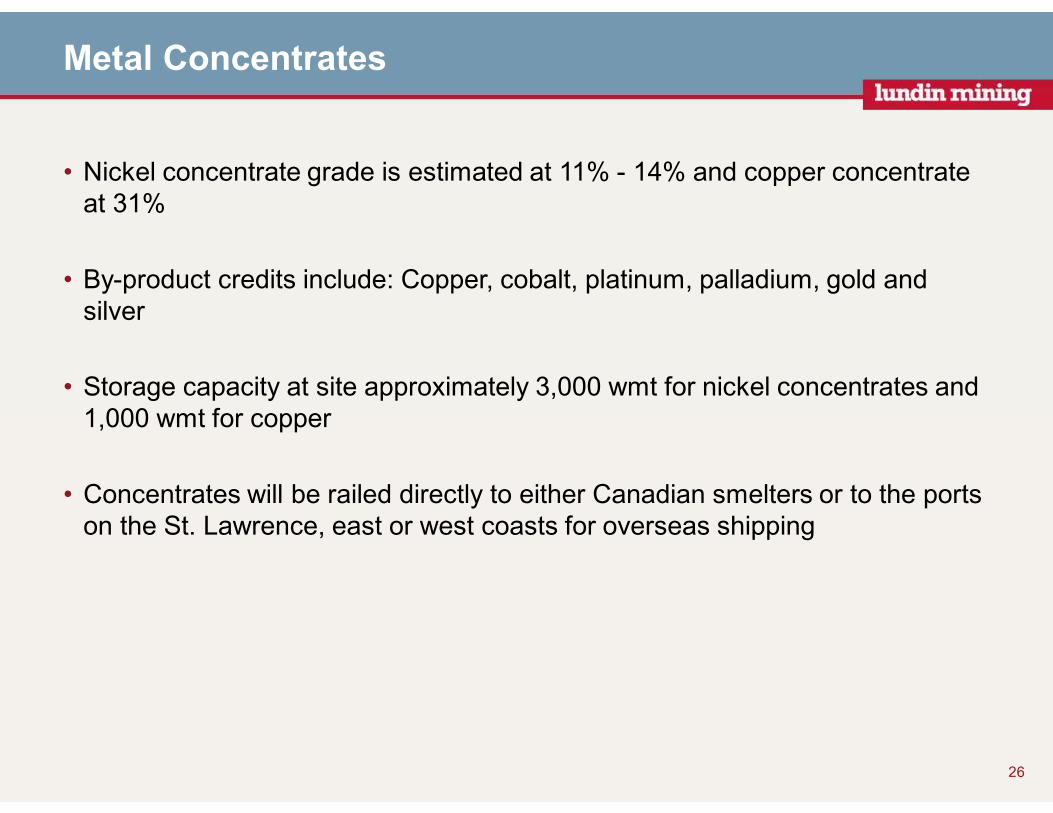

Metal Concentrates

• Nickel concentrate grade is estimated at 11% - 14% and copper concentrate at 31%

• By-product credits include: Copper, cobalt, platinum, palladium, gold and silver

• Storage capacity at site approximately 3,000 wmt for nickel concentrates and 1,000 wmt for copper

• Concentrates will be railed directly to either Canadian smelters or to the ports on the St. Lawrence, east or west coasts for overseas shipping

26

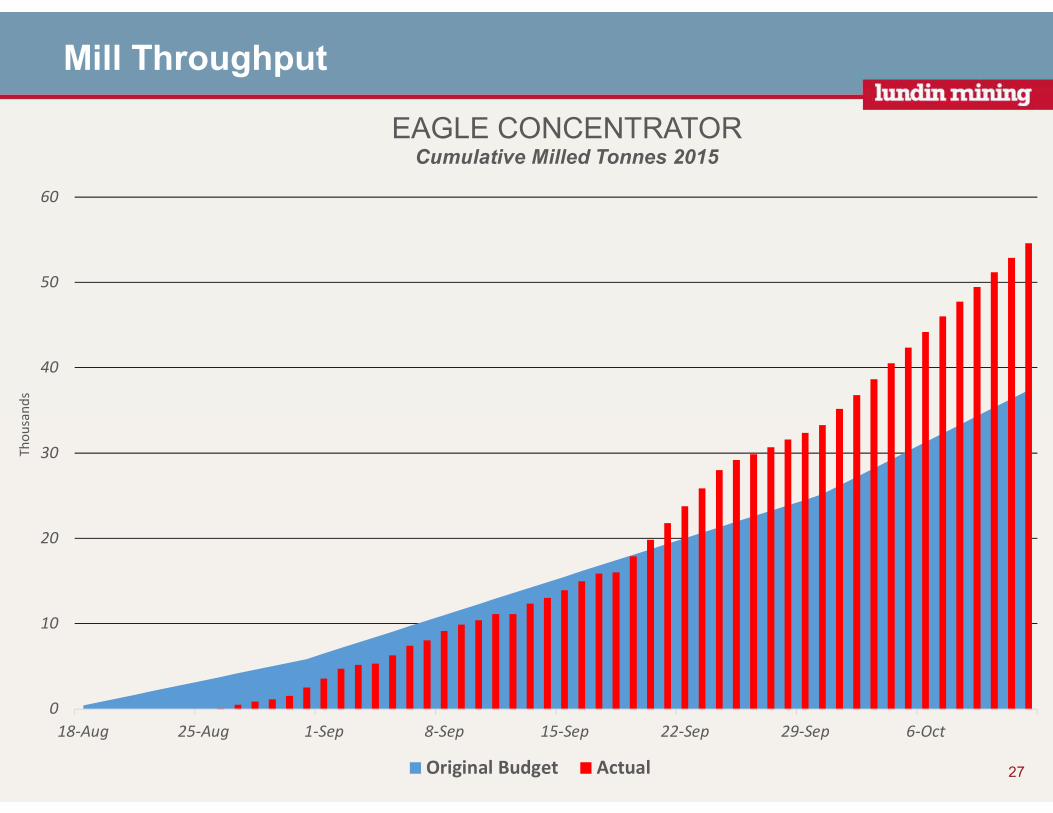

Mill Throughput

27

0

10

20

30

40

50

60

18-Aug 25-Aug 1-Sep 8-Sep 15-Sep 22-Sep 29-Sep 6-Oct

Th

ou

san

ds

EAGLE CONCENTRATORCumulative Milled Tonnes 2015

Original Budget Actual

28

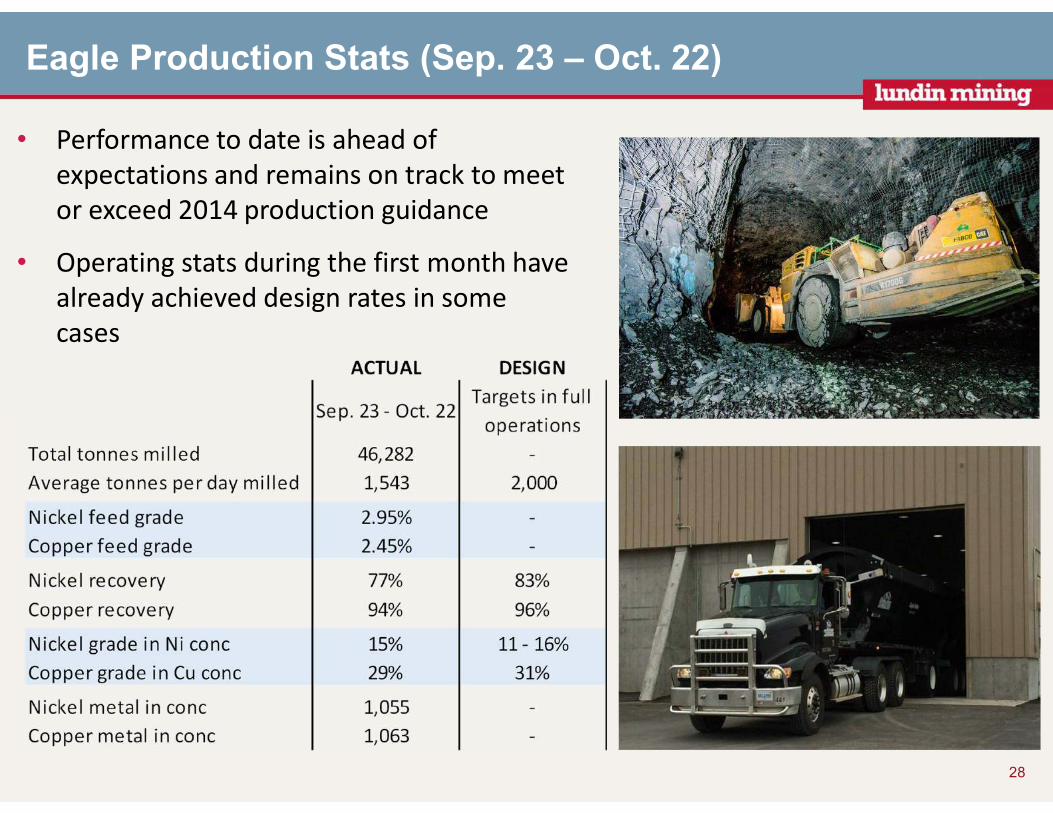

Eagle Production Stats (Sep. 23 – Oct. 22)

• Performance to date is ahead of

expectations and remains on track to meet

or exceed 2014 production guidance

• Operating stats during the first month have

already achieved design rates in some

cases

Transport and Marketing

29

• Rail spur was built connecting mill site to Canadian National Railroad network

• Concentrates will be loaded to covered rails cars for shipping to smelters or ports

• All concentrate off take agreements have been finalized:

• Nickel: Three off take agreements in place for 2+ years

• Copper: One off take agreement for copper to a smelter – five year agreement at annual market terms

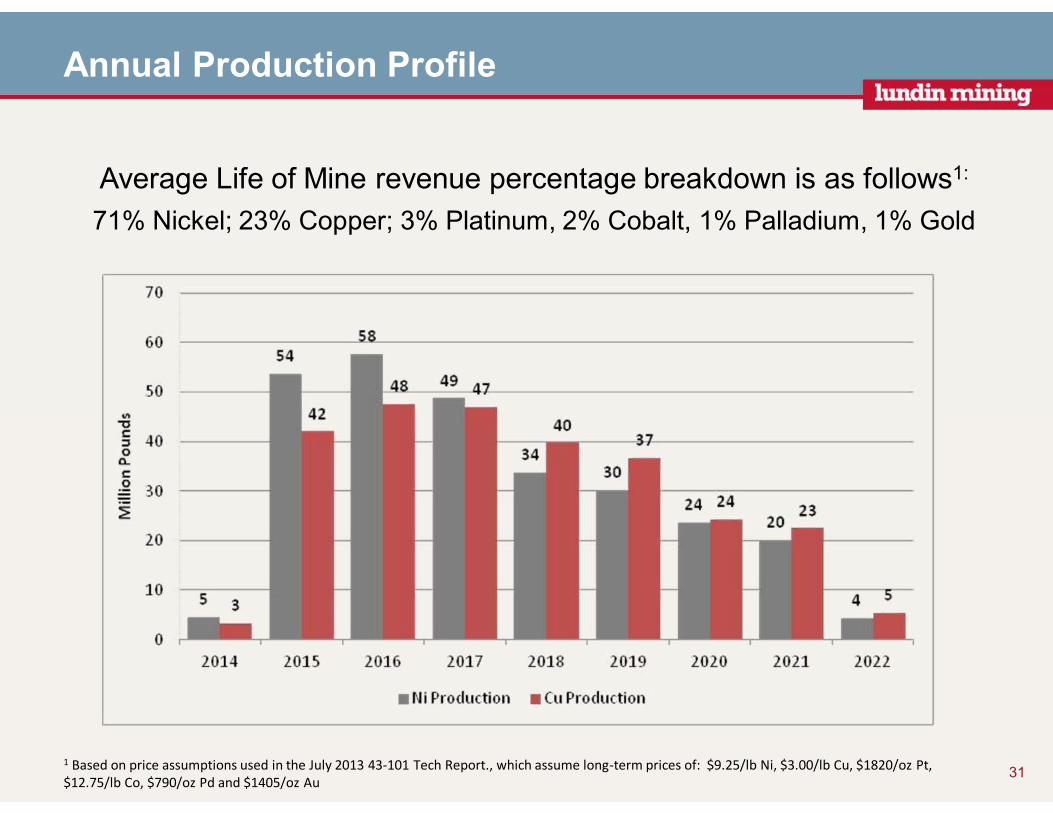

LOM Production & Cost Profile

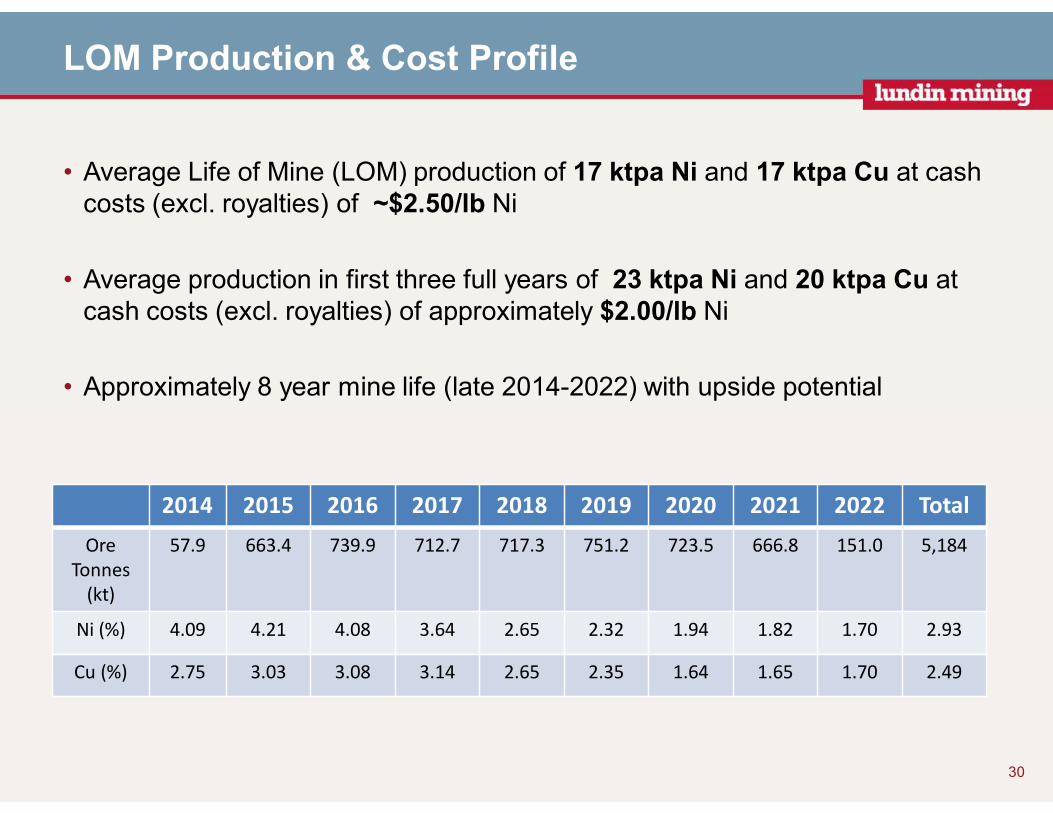

• Average Life of Mine (LOM) production of 17 ktpa Ni and 17 ktpa Cu at cash costs (excl. royalties) of ~$2.50/lb Ni

• Average production in first three full years of 23 ktpa Ni and 20 ktpa Cu at cash costs (excl. royalties) of approximately $2.00/lb Ni

• Approximately 8 year mine life (late 2014-2022) with upside potential

30

2014 2015 2016 2017 2018 2019 2020 2021 2022 Total

Ore

Tonnes

(kt)

57.9 663.4 739.9 712.7 717.3 751.2 723.5 666.8 151.0 5,184

Ni (%) 4.09 4.21 4.08 3.64 2.65 2.32 1.94 1.82 1.70 2.93

Cu (%) 2.75 3.03 3.08 3.14 2.65 2.35 1.64 1.65 1.70 2.49

Annual Production Profile

Average Life of Mine revenue percentage breakdown is as follows1:

71% Nickel; 23% Copper; 3% Platinum, 2% Cobalt, 1% Palladium, 1% Gold

1 Based on price assumptions used in the July 2013 43-101 Tech Report., which assume long-term prices of: $9.25/lb Ni, $3.00/lb Cu, $1820/oz Pt,

$12.75/lb Co, $790/oz Pd and $1405/oz Au 31

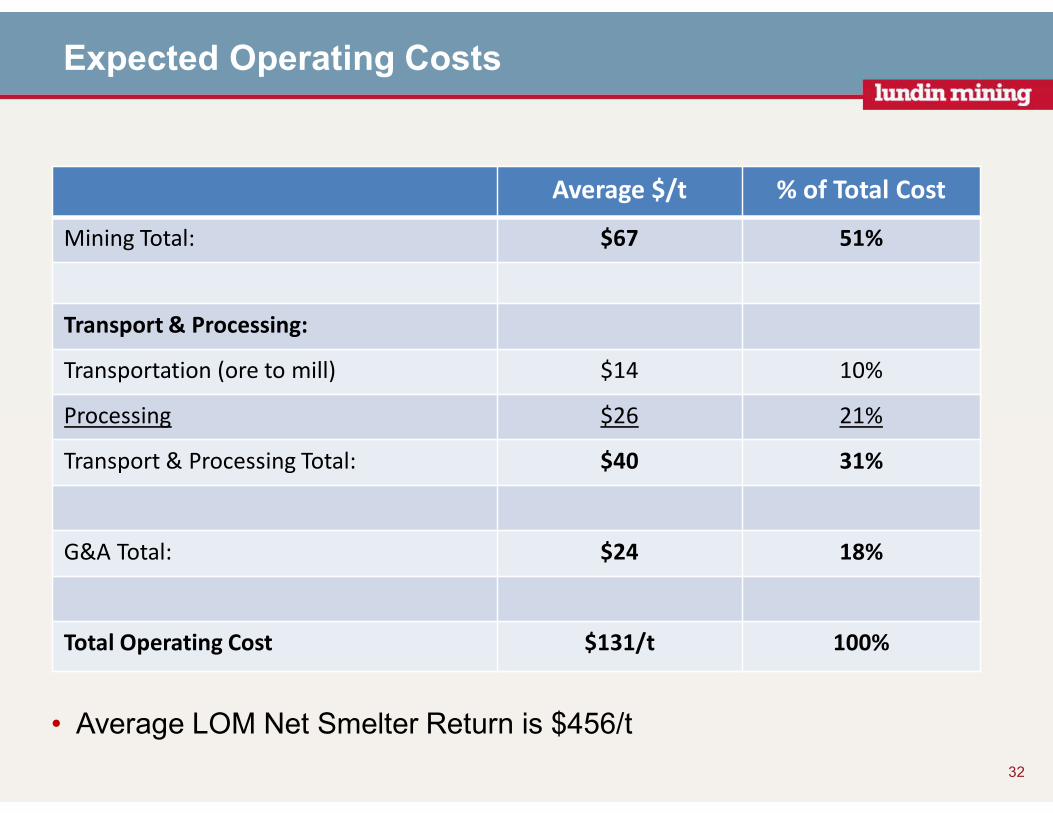

Expected Operating Costs

32

Average $/t % of Total Cost

Mining Total: $67 51%

Transport & Processing:

Transportation (ore to mill) $14 10%

Processing $26 21%

Transport & Processing Total: $40 31%

G&A Total: $24 18%

Total Operating Cost $131/t 100%

• Average LOM Net Smelter Return is $456/t

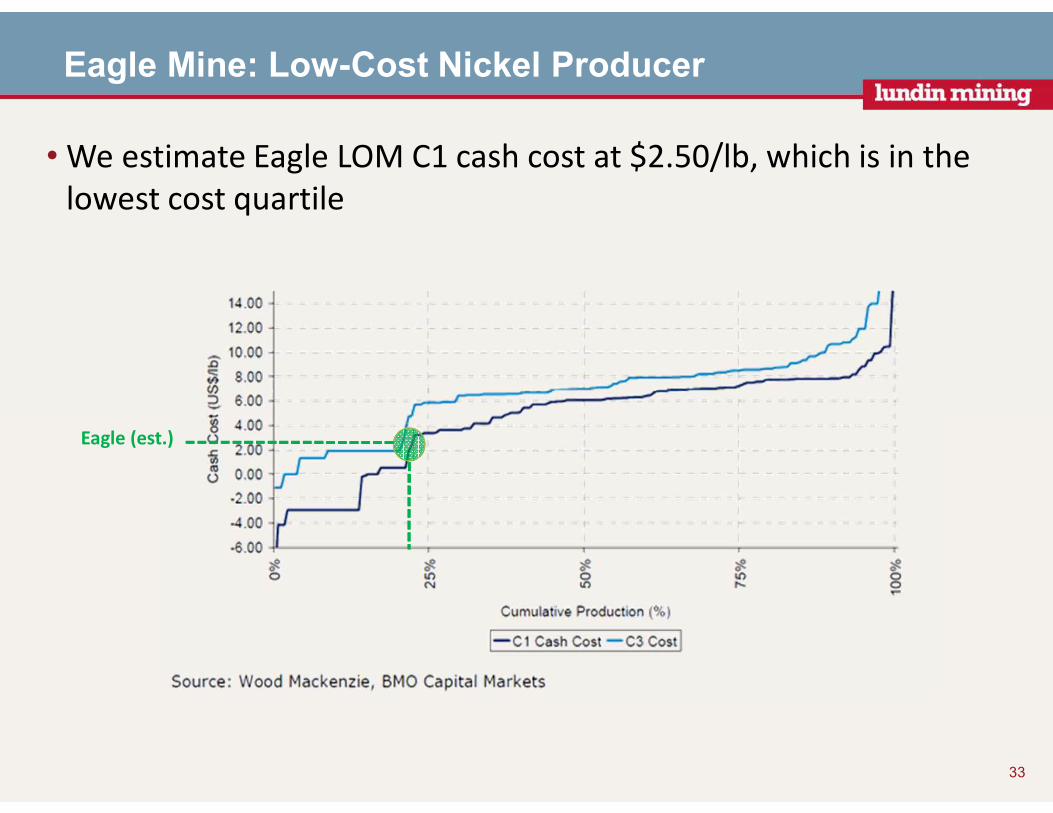

Eagle Mine: Low-Cost Nickel Producer

•We estimate Eagle LOM C1 cash cost at $2.50/lb, which is in the

lowest cost quartile

Eagle (est.)

33

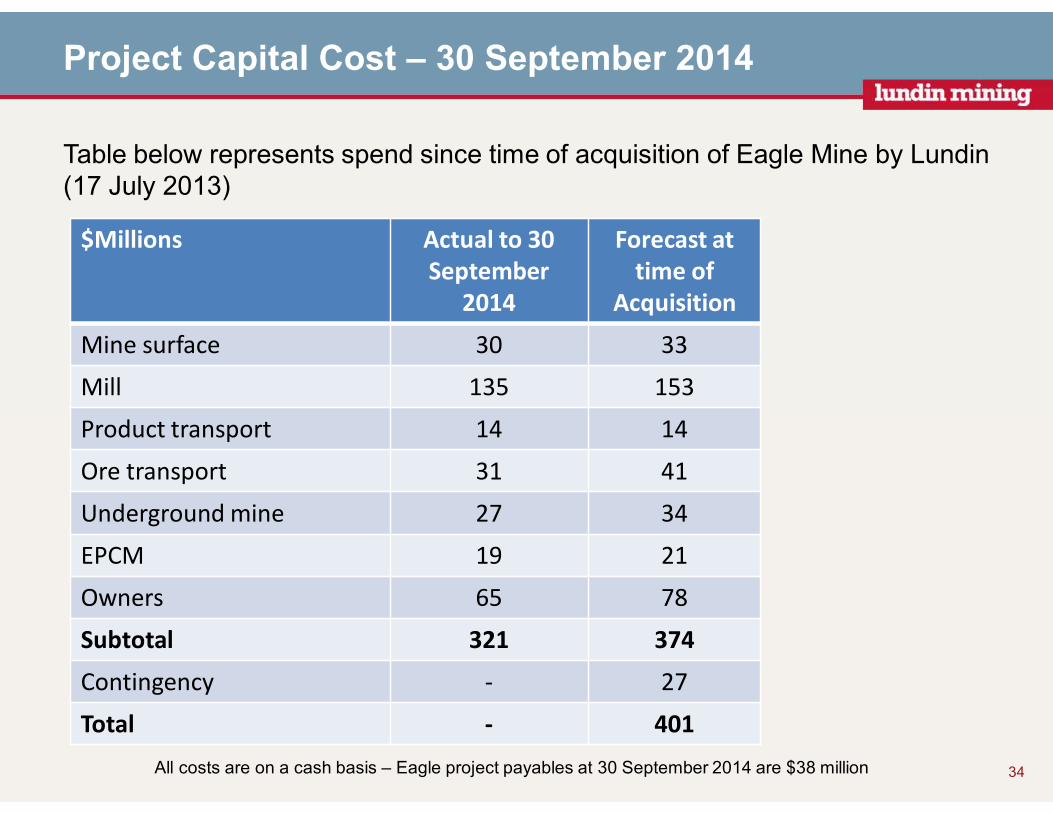

Project Capital Cost – 30 September 2014

Table below represents spend since time of acquisition of Eagle Mine by Lundin (17 July 2013)

34

$Millions Actual to 30

September

2014

Forecast at

time of

Acquisition

Mine surface 30 33

Mill 135 153

Product transport 14 14

Ore transport 31 41

Underground mine 27 34

EPCM 19 21

Owners 65 78

Subtotal 321 374

Contingency - 27

Total - 401

All costs are on a cash basis – Eagle project payables at 30 September 2014 are $38 million

Exploration(Mike Welch)

35

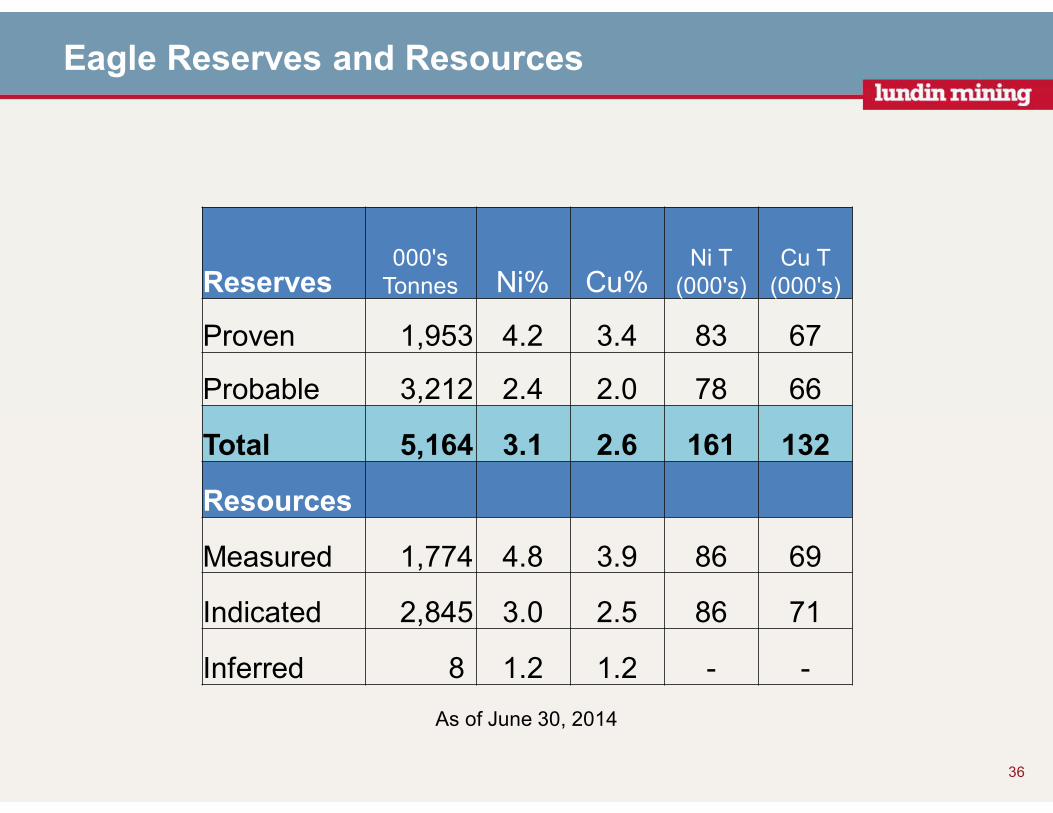

Eagle Reserves and Resources

36

Reserves000's Tonnes Ni% Cu%

Ni T (000's)

Cu T (000's)

Proven 1,953 4.2 3.4 83 67

Probable 3,212 2.4 2.0 78 66

Total 5,164 3.1 2.6 161 132

Resources

Measured 1,774 4.8 3.9 86 69

Indicated 2,845 3.0 2.5 86 71

Inferred 8 1.2 1.2 - -

As of June 30, 2014

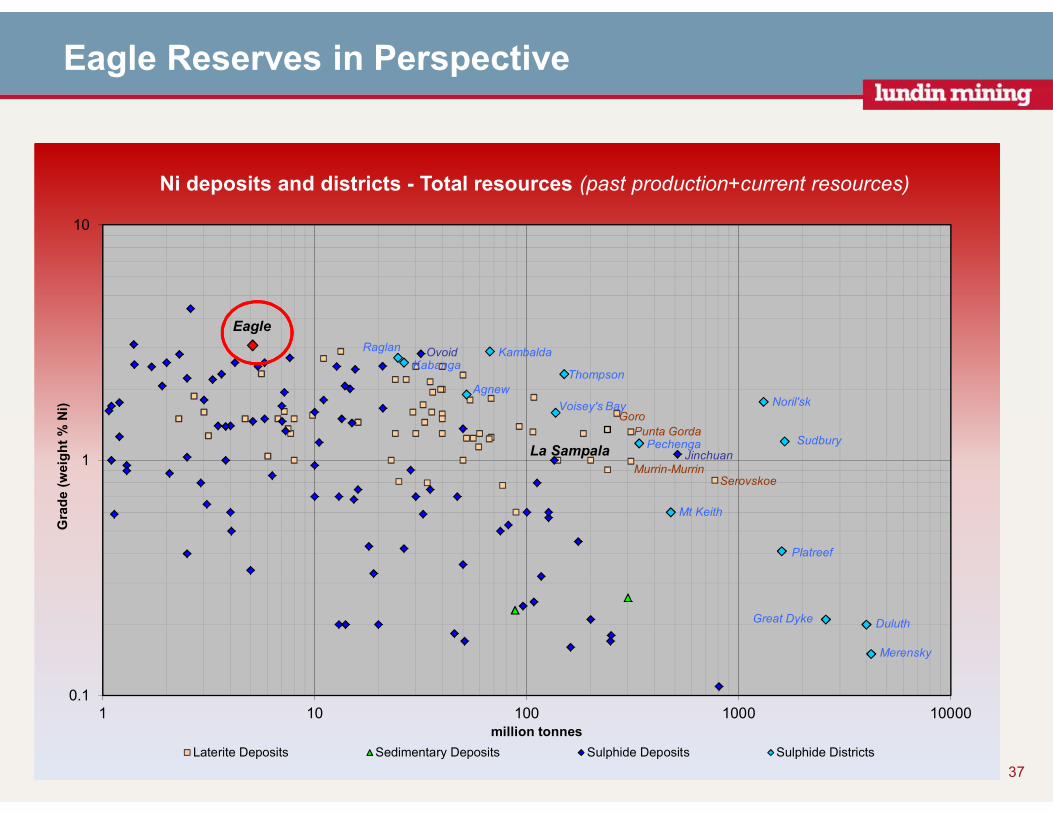

Eagle Reserves in Perspective

37

0.1

1

10

1 10 100 1000 10000

Gra

de (

weig

ht

% N

i)

million tonnes

Ni deposits and districts - Total resources (past production+current resources)

Laterite Deposits Sedimentary Deposits Sulphide Deposits Sulphide Districts

Sudbury

Noril'sk

Duluth

Platreef

Merensky

Great Dyke

Mt Keith

Pechenga

Thompson

Voisey's Bay

Kambalda

Agnew

Raglan

Kabanga

Jinchuan

Ovoid

Eagle

Serovskoe

Punta Gorda

Murrin-Murrin

Goro

La Sampala

`

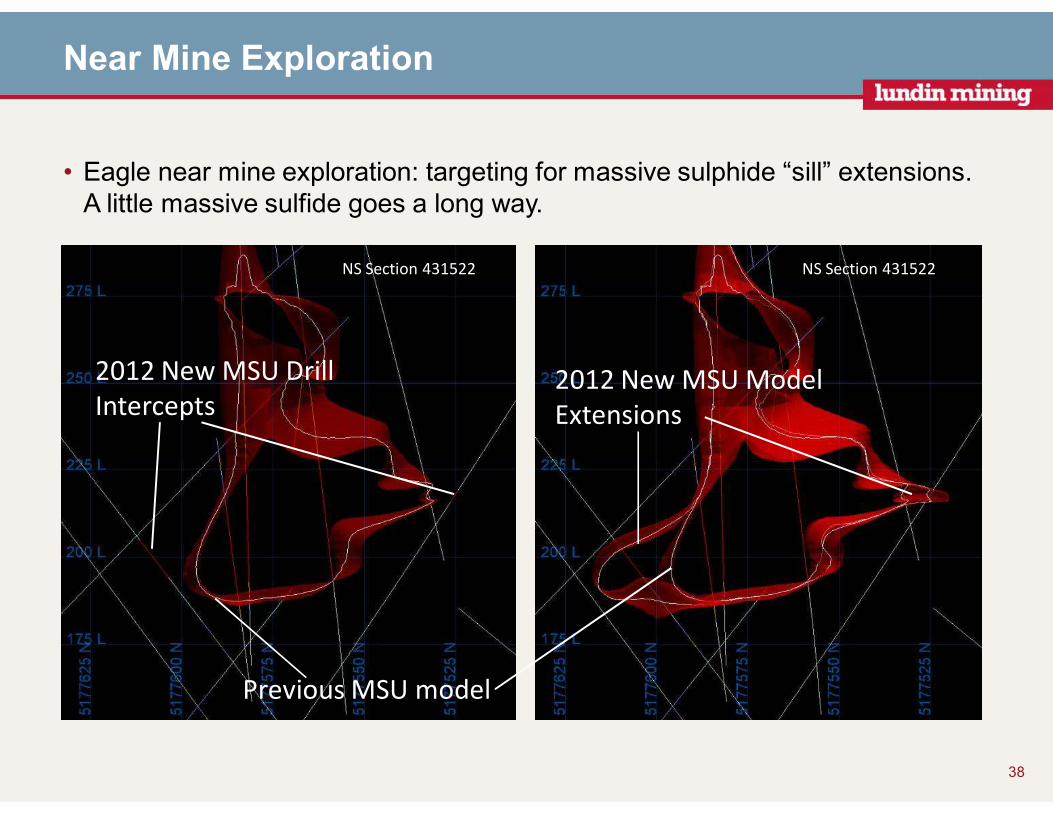

Near Mine Exploration

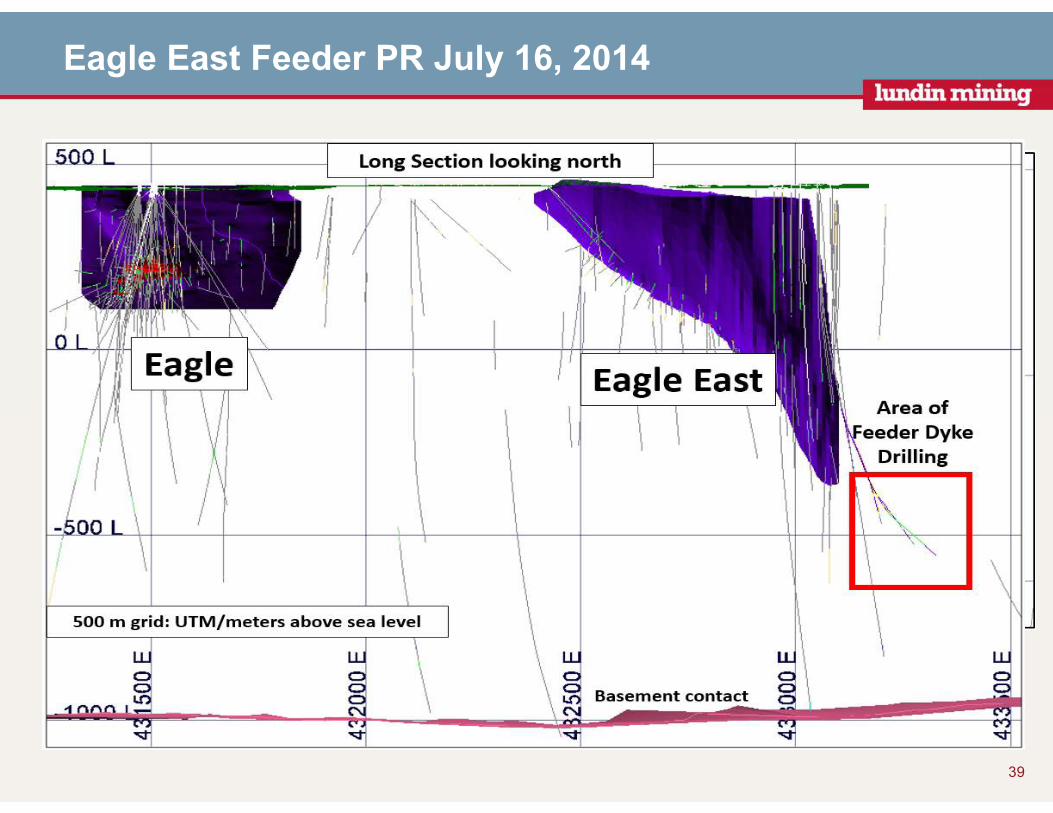

• Eagle near mine exploration: targeting for massive sulphide “sill” extensions. A little massive sulfide goes a long way.

38

NS Section 431522 NS Section 431522

2012 New MSU Drill

Intercepts2012 New MSU Model

Extensions

Previous MSU model

Eagle East Feeder PR July 16, 2014

39

40

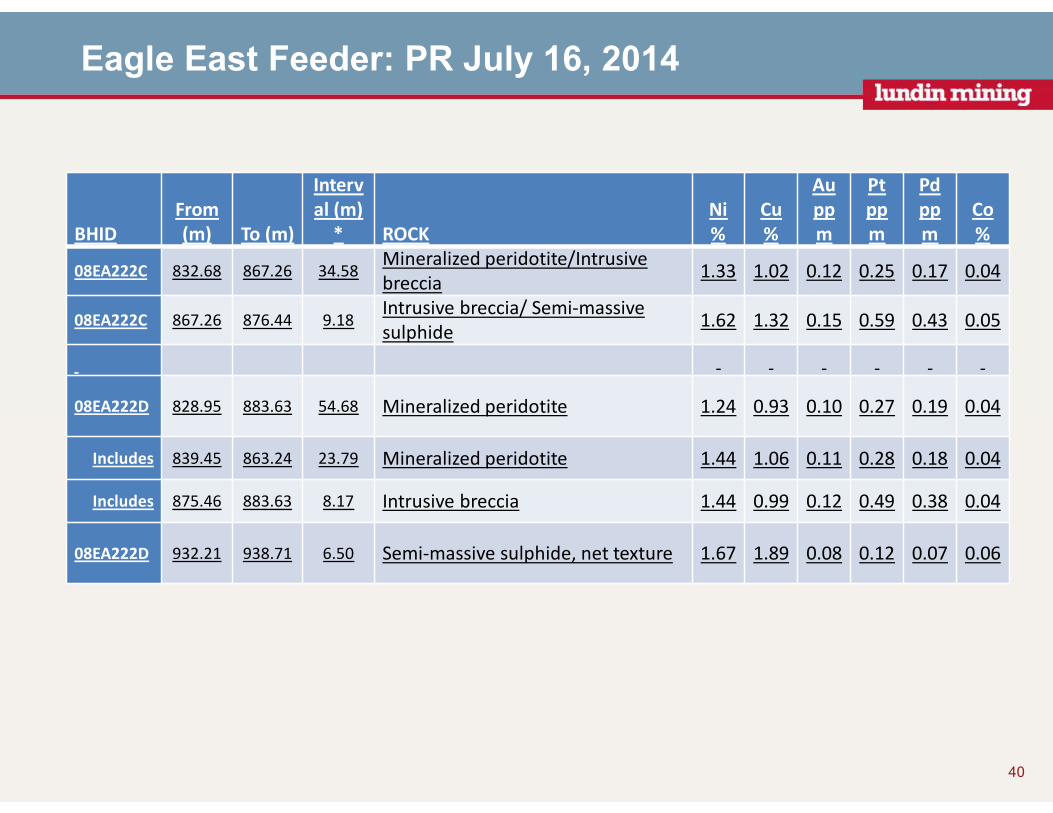

BHID

From

(m) To (m)

Interv

al (m)

* ROCK

Ni

%

Cu

%

Au

pp

m

Pt

pp

m

Pd

pp

m

Co

%

08EA222C 832.68 867.26 34.58Mineralized peridotite/Intrusive

breccia1.33 1.02 0.12 0.25 0.17 0.04

08EA222C 867.26 876.44 9.18Intrusive breccia/ Semi-massive

sulphide1.62 1.32 0.15 0.59 0.43 0.05

08EA222D 828.95 883.63 54.68 Mineralized peridotite 1.24 0.93 0.10 0.27 0.19 0.04

Includes 839.45 863.24 23.79 Mineralized peridotite 1.44 1.06 0.11 0.28 0.18 0.04

Includes 875.46 883.63 8.17 Intrusive breccia 1.44 0.99 0.12 0.49 0.38 0.04

08EA222D 932.21 938.71 6.50 Semi-massive sulphide, net texture 1.67 1.89 0.08 0.12 0.07 0.06

Eagle East Feeder: PR July 16, 2014

Eagle 2014 3D Seismic Survey

41

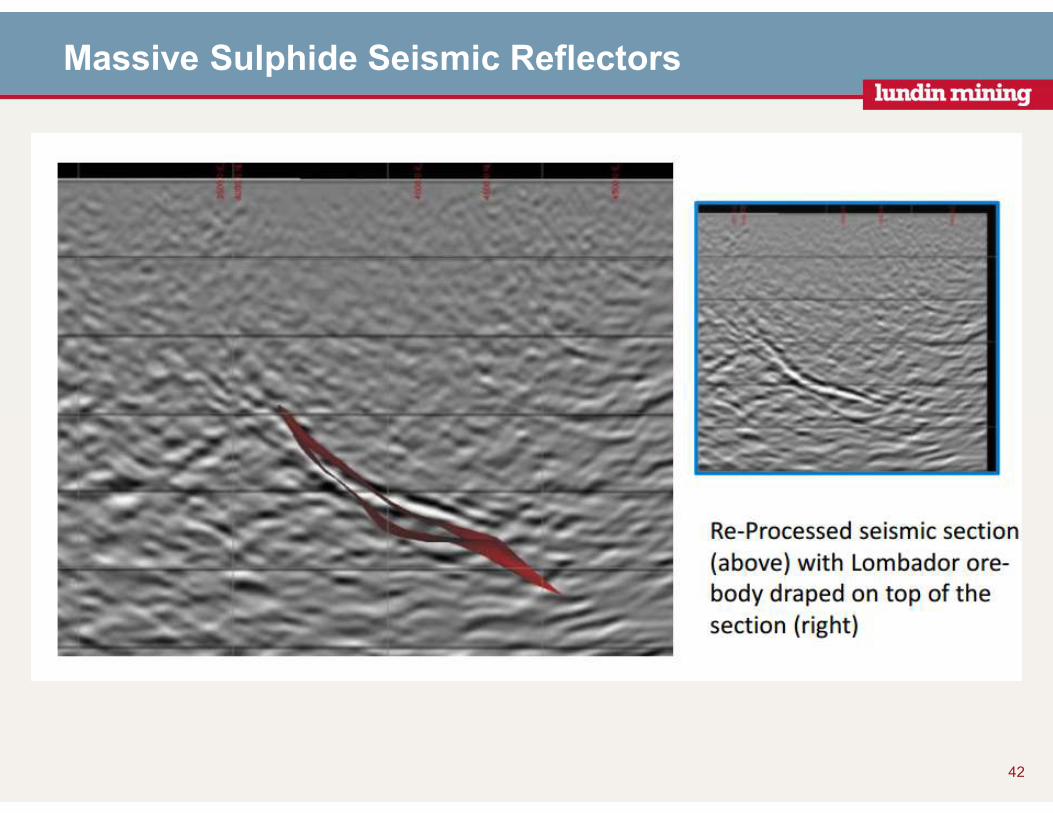

Massive Sulphide Seismic Reflectors

42

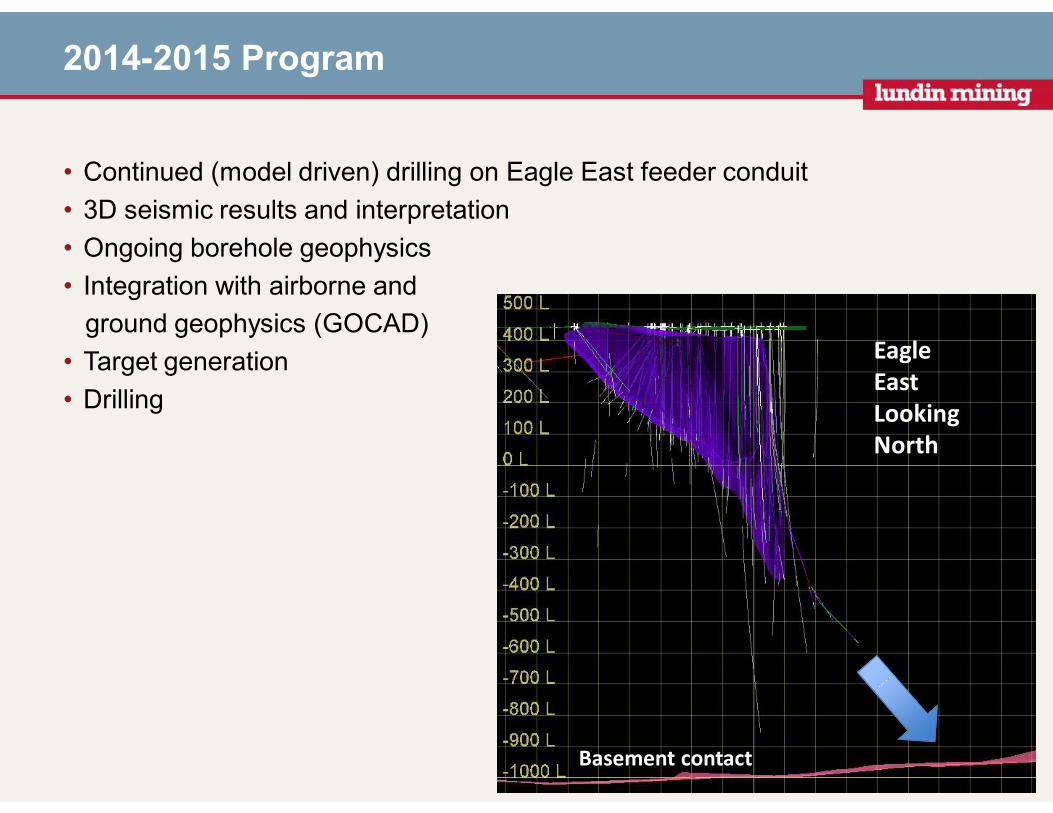

2014-2015 Program

• Continued (model driven) drilling on Eagle East feeder conduit

• 3D seismic results and interpretation

• Ongoing borehole geophysics

• Integration with airborne and

ground geophysics (GOCAD)

• Target generation

• Drilling

43

Eagle

East

Looking

North

Basement contact

Corporate Update(Paul Conibear)

44

45

Tenke Fungurume (24%)(DRC)

Tenke Fungurume (24%)(DRC)

Eagle (100%) (USA)

Eagle (100%) (USA)

Zinkgruvan (100%)(Sweden)

Zinkgruvan (100%)(Sweden)

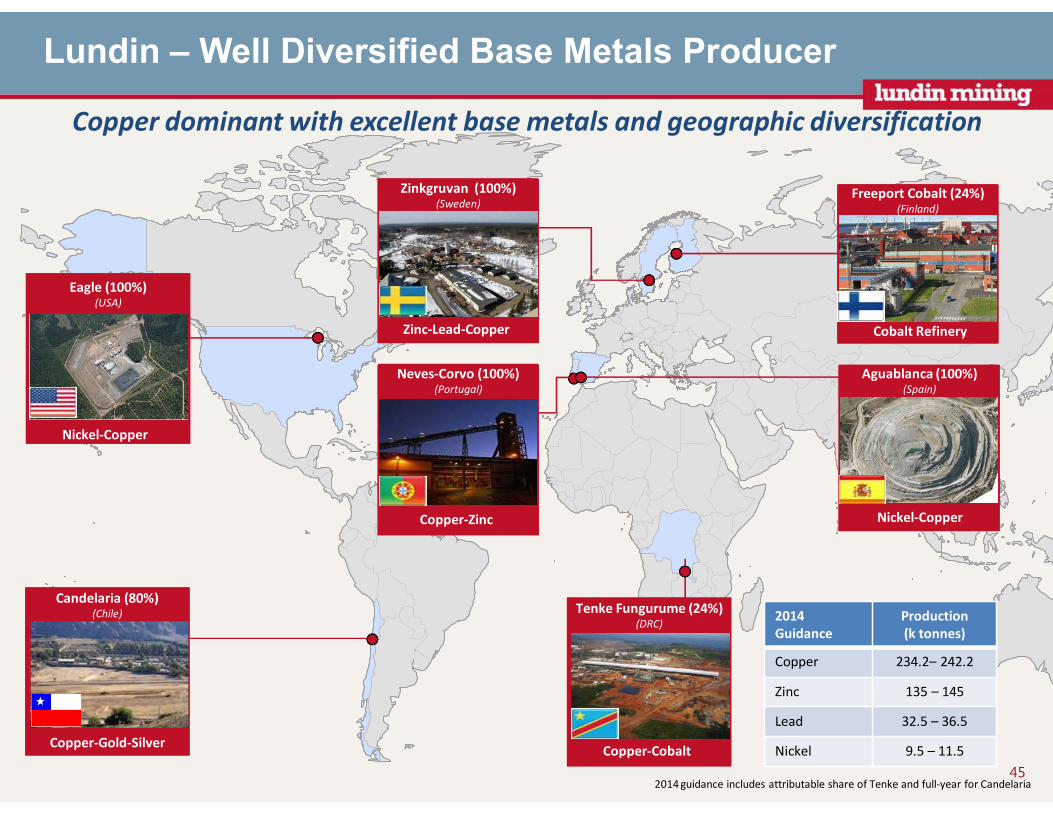

Lundin – Well Diversified Base Metals Producer

Aguablanca (100%) (Spain)

Aguablanca (100%) (Spain)

Copper dominant with excellent base metals and geographic diversification

Candelaria (80%) (Chile)

Candelaria (80%) (Chile)

Neves-Corvo (100%)(Portugal)

Neves-Corvo (100%)(Portugal)

Freeport Cobalt (24%)(Finland)

Freeport Cobalt (24%)(Finland)

Nickel-Copper

Zinc-Lead-Copper

Copper-Zinc

Copper-Gold-SilverCopper-Cobalt

Nickel-Copper

Cobalt Refinery

2014

Guidance

Production

(k tonnes)

Copper 234.2– 242.2

Zinc 135 – 145

Lead 32.5 – 36.5

Nickel 9.5 – 11.5

2014 guidance includes attributable share of Tenke and full-year for Candelaria

46

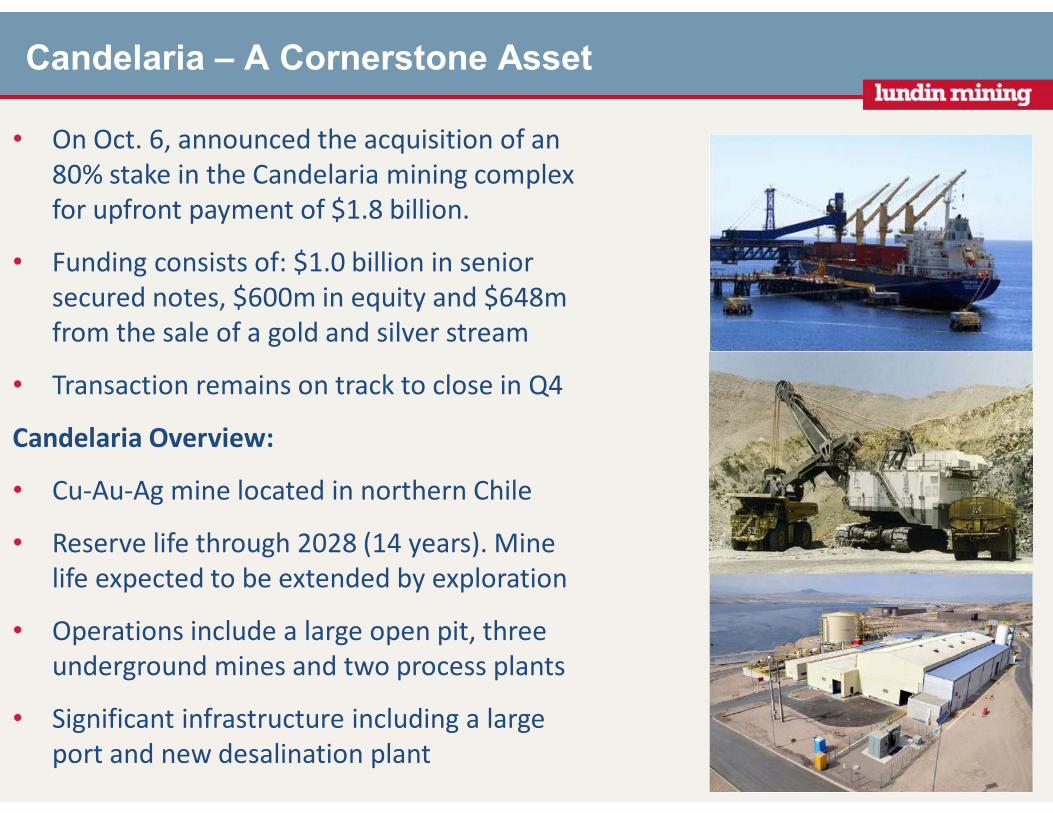

Candelaria – A Cornerstone Asset

• On Oct. 6, announced the acquisition of an

80% stake in the Candelaria mining complex

for upfront payment of $1.8 billion.

• Funding consists of: $1.0 billion in senior

secured notes, $600m in equity and $648m

from the sale of a gold and silver stream

• Transaction remains on track to close in Q4

Candelaria Overview:

• Cu-Au-Ag mine located in northern Chile

• Reserve life through 2028 (14 years). Mine

life expected to be extended by exploration

• Operations include a large open pit, three

underground mines and two process plants

• Significant infrastructure including a large

port and new desalination plant

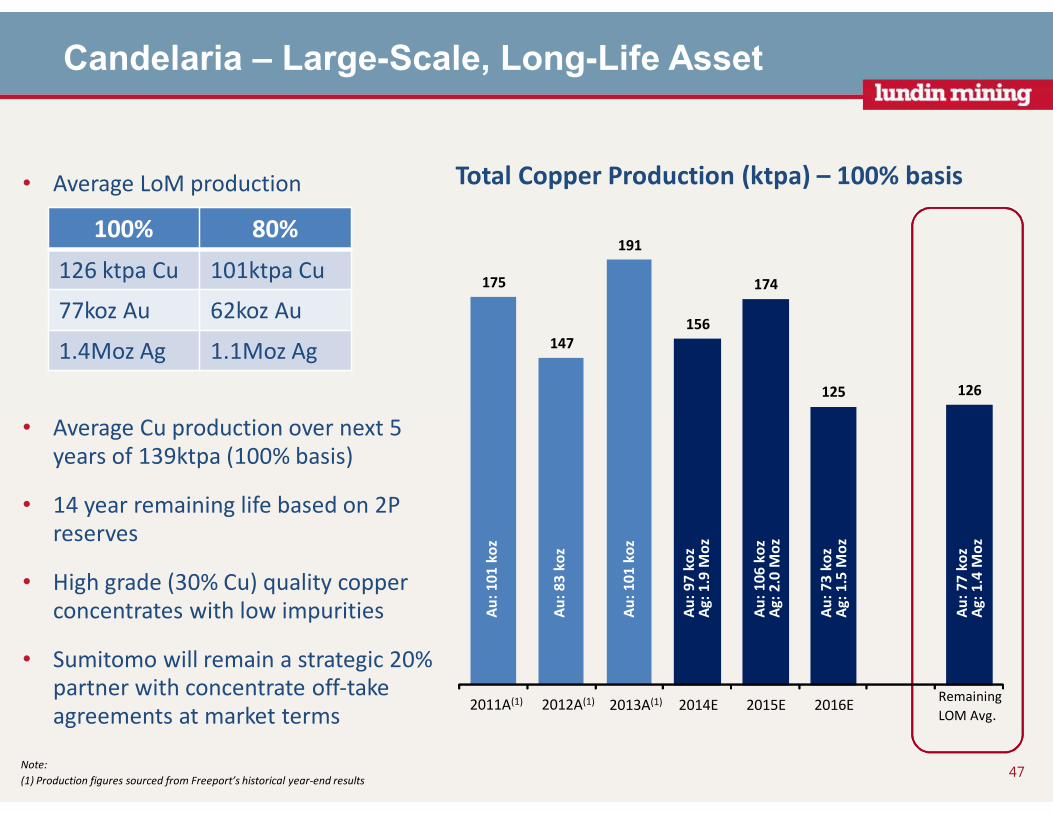

Candelaria – Large-Scale, Long-Life Asset

47

• Average LoM production

• Average Cu production over next 5 years of 139ktpa (100% basis)

• 14 year remaining life based on 2P reserves

• High grade (30% Cu) quality copper concentrates with low impurities

• Sumitomo will remain a strategic 20% partner with concentrate off-take agreements at market terms

Total Copper Production (ktpa) – 100% basis

175

147

191

156

174

125 126

2011A(1) 2012A(1) 2013A(1) 2014E 2015E 2016ERemaining

LOM Avg.

Au

: 77

ko

zA

g: 1

.4 M

oz

Au

: 73

ko

zA

g: 1

.5 M

oz

Au

: 101

ko

z

Au

: 83

ko

z

Au

: 101

ko

z

Au

: 97

ko

zA

g: 1

.9 M

oz

Au

: 106

ko

zA

g: 2

.0 M

oz

Note:

(1) Production figures sourced from Freeport’s historical year-end results

100% 80%

126 ktpa Cu 101ktpa Cu

77koz Au 62koz Au

1.4Moz Ag 1.1Moz Ag

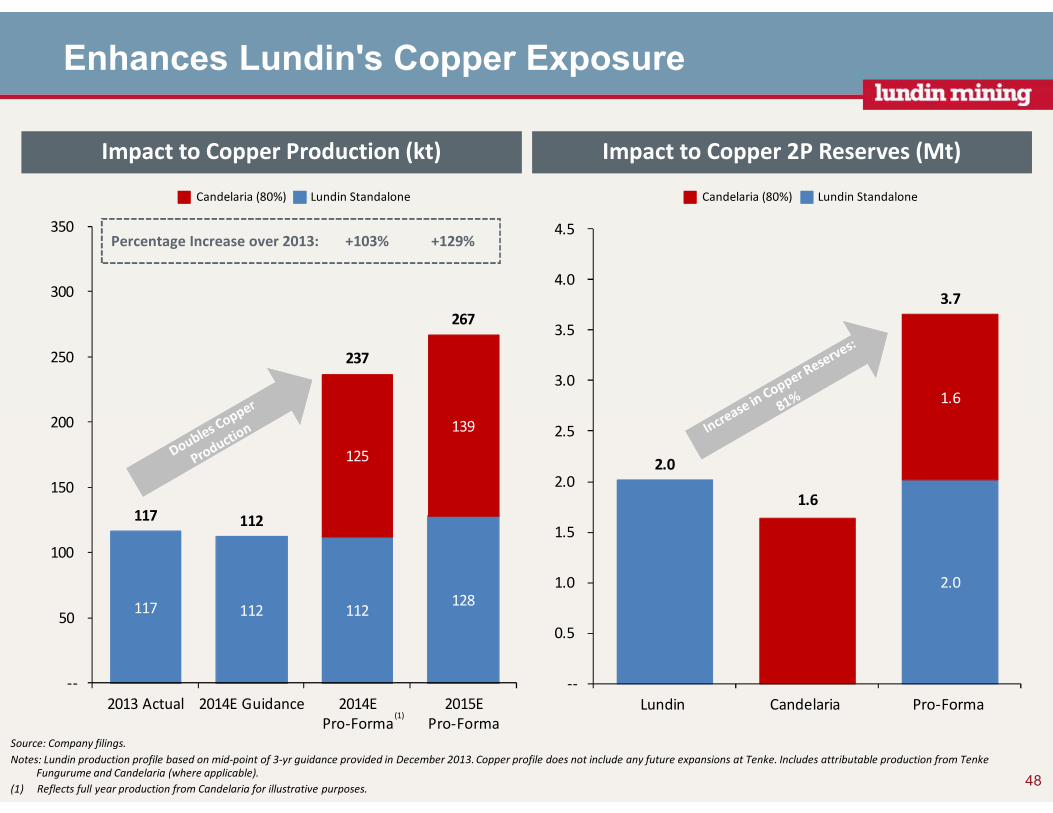

117 112 112 128

125

139

117 112

237

267

--

50

100

150

200

250

300

350

2013 Actual 2014E Guidance 2014E

Pro-Forma

2015E

Pro-Forma

1.6

2.0

1.6

2.0

3.7

--

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

Lundin Candelaria Pro-Forma

Source: Company filings.

Notes: Lundin production profile based on mid-point of 3-yr guidance provided in December 2013. Copper profile does not include any future expansions at Tenke. Includes attributable production from TenkeFungurume and Candelaria (where applicable).

(1) Reflects full year production from Candelaria for illustrative purposes.

Impact to Copper Production (kt) Impact to Copper 2P Reserves (Mt)

48

Enhances Lundin's Copper Exposure

(1)

Percentage Increase over 2013: +103% +129%

Candelaria (80%) Lundin StandaloneCandelaria (80%) Lundin Standalone

49

(1) Based on midpoint of 2015E production guidance provided by Lundin. Only includes commodities for which Lundin provides public guidance. Excludes gold and silver. Based on 80% interest in Candelaria.

(2) Equivalency calculated according to the following prices: $3.00/lb Cu, $1.00/lb Zn, $8.00/lb Ni, $12.00/lb Co and $1.05/lb Pb.

(3) Cobalt guidance for 2015E assumed equal to 2014E guidance.

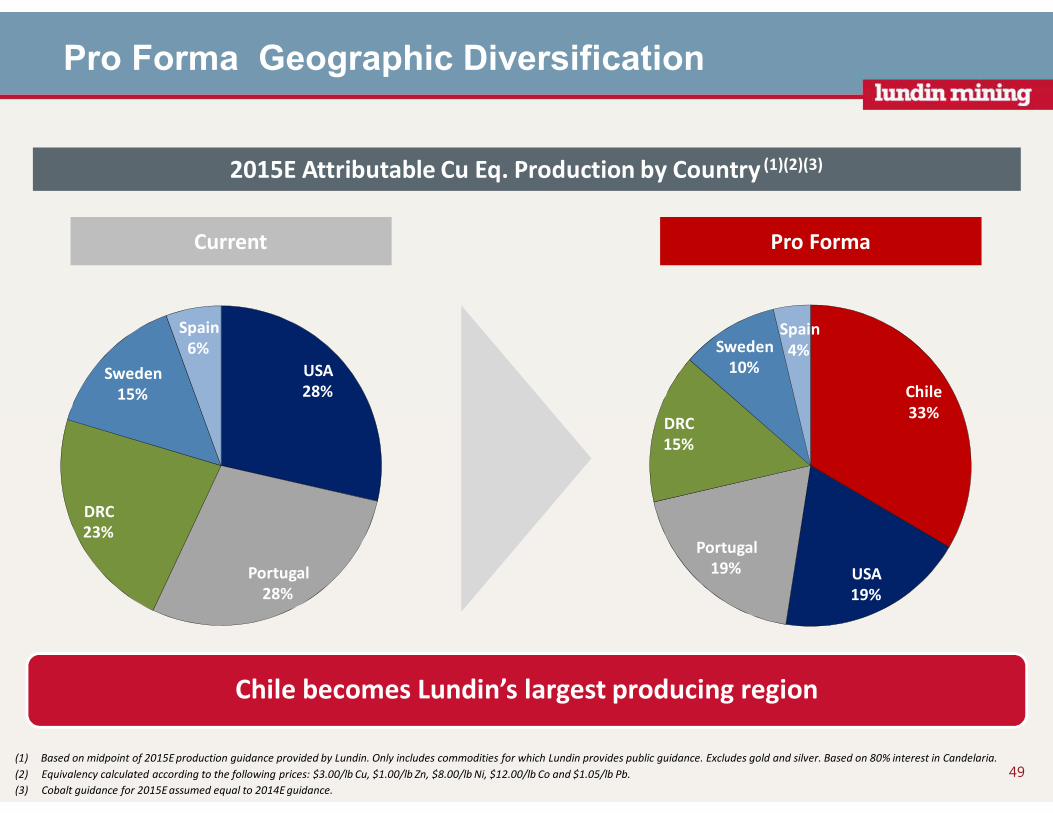

Pro Forma Geographic Diversification

2015E Attributable Cu Eq. Production by Country (1)(2)(3)

Current Pro Forma

USA

28%

Portugal

28%

DRC

23%

Sweden

15%

Spain

6%

Chile

33%

USA

19%

Portugal

19%

DRC

15%

Sweden

10%

Spain

4%

Chile becomes Lundin’s largest producing region

50

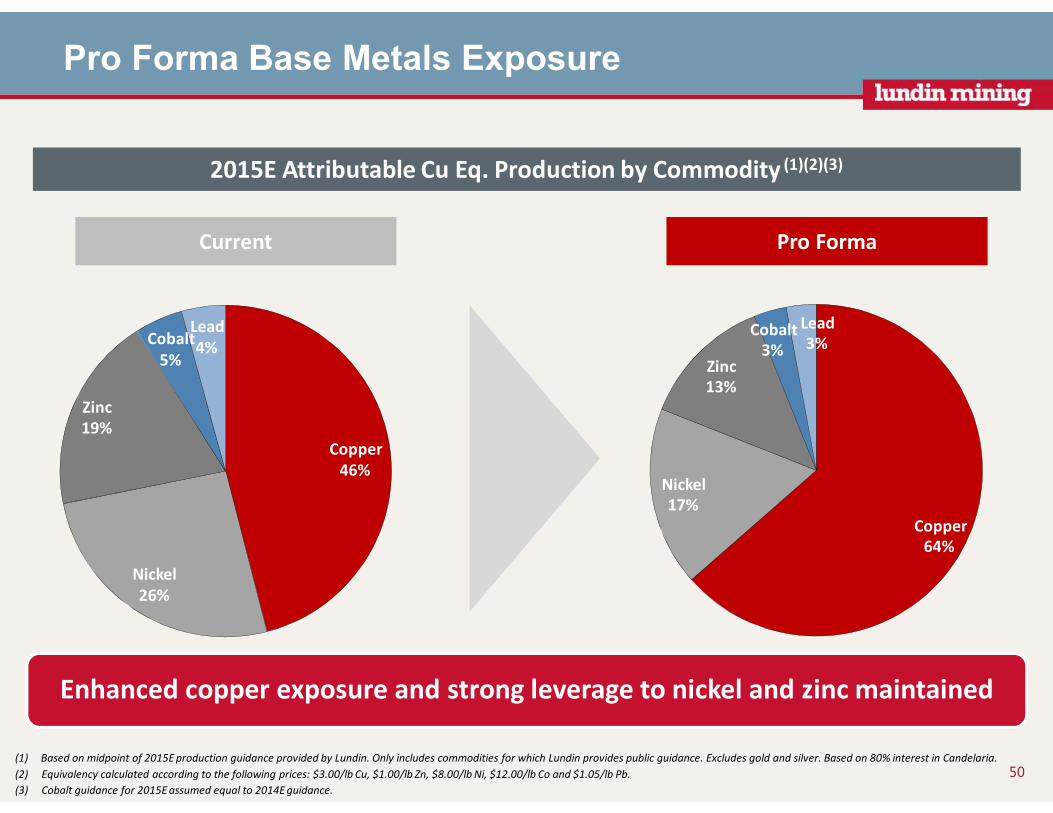

2015E Attributable Cu Eq. Production by Commodity (1)(2)(3)

Pro Forma Base Metals Exposure

Pro FormaCurrent

(1) Based on midpoint of 2015E production guidance provided by Lundin. Only includes commodities for which Lundin provides public guidance. Excludes gold and silver. Based on 80% interest in Candelaria.

(2) Equivalency calculated according to the following prices: $3.00/lb Cu, $1.00/lb Zn, $8.00/lb Ni, $12.00/lb Co and $1.05/lb Pb.

(3) Cobalt guidance for 2015E assumed equal to 2014E guidance.

Copper

46%

Nickel

26%

Zinc

19%

Cobalt

5%

Lead

4%

Copper

64%

Nickel

17%

Zinc

13%

Cobalt

3%

Lead

3%

Enhanced copper exposure and strong leverage to nickel and zinc maintained

Enhanced earnings and cash flow per share with the addition of an

established, large scale, high quality operation

Diverse geographic and base metals portfolio - copper, zinc and nickelDiverse geographic and base metals portfolio - copper, zinc and nickel

Maintains a conservative balance sheet going forwardMaintains a conservative balance sheet going forward

Further strengthens asset base of long-life mines with strong growth potentialFurther strengthens asset base of long-life mines with strong growth potential

Lundin Mining – with Candelaria

Secures Lundin’s position as a leading intermediate base metals

producer with competitive costs

Secures Lundin’s position as a leading intermediate base metals

producer with competitive costs

51

Questions and Answers