Embed Size (px)

Citation preview

Eastcomtrans LLP

Annual report

for 2014 year

Content

1. Company overview • General information

• Vision, mission, and strategy

• Message from the CEO

• History of development

• Supervisory Board

• Key highlights 2014.

• Operational activity • Transport network of Kazakhstan

• Types of cars

• Railway freight industry and trends

• Structure of Kazakhstan rolling stock fleet

• Railway freight transportation demand in Kazakhstan

3. Financial activity • Financial and economic indicators

• Analysis of financial and economic activity

4. Risk factors

5. Social activity

6. Corporate Governance • Corporate governance

• Organizational structure

7. Financial statements

8. Additional information

2

General information

► Company was founded in 2002 as Limited Liability Partnership

► Structure of Ownership:

− Mr. Marat Sarsenov – 55,998%;

− Steinhardt Holding N.V. – 37,332%. (Netherlands)

− International Finance Corporation – 6,67% (USA)

► Company provides following types of services:

− Freight forwarding services;

− Leasing of private car fleet;

− Technical maintenance of the rolling stock;

− Tank wagon cleaning;

− Transshipment services at Aktau sea port;

− Multimodal forwarding;

− Leasing of wagons.

► As of 31, December 2014 own rail fleet made up to 12 035 wagons.

► Total capital investments for the 2002-2014 exceeded $720 ml.

► Total staff of 153 employees, including 50 administrative and managerial staff, and 103 – maintenance personnel.

► Head office is located in Almaty. Representative offices are located in Karaganda, Pavlodar, Atyrau, Shymkent, st. Zashita and Dostyk and branches in Astana and Aktau.

General information

3 3

Vision:

Eastcomtrans LLP is a leading private operator of railcars in Kazakhstan,

strong player on international cargo shipment market. Company provides full

range of high-quality transportation and logistics services due to its own

transport infrastructure, high professionalism of personnel and advanced

control management system. Final goal of management is to create largest,

regional, vertically integrated holding entity in Central Asia region.

Company overview

Mission:

Mission of Eastcomtrans LLP reflects its infrastructural purpose, which is to

provide clients with competitive, high-quality and modern transportation

services of industrial goods, thereby contributing to economic and

transportation development of the country.

Strategy:

To increase Company‟s added value by 2018 due to business diversification

and growth of economic efficiency.

Membership in associations:

Eastcomtrans LLP is a member of the Association of National Freight

Forwarders of Kazakhstan, Kazakhstan Association of Operators of carriers and

Railcars, and an individual member of the International Federation of Freight

Forwarders Associations (FIATA).

4

«Teamwork will empower us to achieve even more success!»

Message from CEO

5

We are pleased to welcome you on behalf of Eastcomtrans LLP, the biggest railcar operator on the transport market in the

Republic of Kazakhstan.

Our Company has been active in transport market for more than 12 years. Nowadays, Eastcomtrans is one of the most

acknowledged leaders on Kazakh transport market, providing full range of rail transportation services. The modern fleet

allows us to provide maximum effective services to our clients. Quality of our services has been recognized by large

Kazakh and global entities, since our Company‟s objective has been and always will be building solid reliable relationship

with our clients. Thanks to that, our Company regularly increases its shipment volumes and renews its car fleet.

We are certain that our teamwork will empower us to achieve even more success!

6

Message from CEO

History of development 2002- 2004

Establishment of the

Company

2005-2007

Growth of railcar fleet and

diversification of

operational activity

2009

Growth of railcar fleet Growth of railcar fleet.

Receipt of credit rating

2008

Diversification of financial

partners and business

processes‟ optimization

2011-2012

Switching to international

finance resources. Growth

of fleet. Improvement of

ratings.

• A group of private

investors founded

Eastcomtrans LLP.

• The Company signed a

loan agreement with

"BTA Bank“ for 10-

years credit facility.

• Signed the very first

contract on railcar lease

with Tengizchevroil.

• Signed first contract with

"Azovmash“ and

“Uralvagonzavod“.

Purchased first lot of

500 oil tanker cars.

• The period of an intense

operational portfolio

diversification. Signed

lease and forwarding

contracts with CNPC,

Turgay Petroleum,

Matin, Karakudukmunai,

KuatAmlon, etc.

• Within 3 years Company

increased its fleet size up

to 1700 cars.

• Financial statements

were transferred to IFRS.

• Financial audit was

provided by PWC.

• During the World

financial crisis period,

the Company makes

emphasis on the local

development institutes,

signing three lease

agreements with KDB-

Leasing.

• As of December 31,

2009 the Company's

railcar fleet amounted to

2822 units.

• For the very first time

signed a 3-year contract

with TCO.

• Total fleet size achieved

2 822 cars by the end of

2009.

• The Company becomes

an individual member of

FIATA (International

Federation of Freight

Forwarders

Associations).

• Signed a 7-year contract

with «Zhaykmunai" on

oil and gas tanker cars‟

lease in Chinarevskoe

oil field.

• Fitch Ratings assigned

the Company term

issuer default rating at

«B-» on international

scale. Outlook is

“Stable".

• 2010 was the year of the

largest car fleet growth

after 3,076 cars were

purchased. The total

fleet of cars reached

5901 units.

• In accordance with the

auditor rotation policy,

in 2010 the Company

switched to Deloitte in

audit of financial

indicators.

• The partnership with

Raiffeisen-Leasing

Kazakhstan was started.

• Successfully completed

ISO audit.

• Started an intense

diversification of the loan

portfolio.

• Signed a $25 ml. loan

agreement with «HSBC

Kazakhstan.“ to

refinance part of the debt

to BTA.

• Signed $100 ml.

Tranche-A syndicate

facility with BNP

Paribas. Loan was used

to fully refinance BTA

loan and to purchase

new cars.

• The company started to

diversify types of

transportation services,

focusing on the mining

sector.

• Fleet amount increased

to 9782 units.

• Fitch Ratings upgraded

the corporate rating from

«B-» to «B / Stable» - on

the international scale.

• Contracts with TCO

resigned for the new 4-

year term and transited

into U.S. dollars.

• Eastcomtrans had

become the largest

operator for TCO.

Увеличение парка

вагонов и улучшение

кредитного рейтинга

• IFC had become the new

shareholder for ECT

with 6.67% stake in

equity.

• The Company has

successfully completed a

debut 5-year $100ml.

Eurobonds emission on

the London Stock

Exchange at 7.75%

coupon yield.

• 1402 wagons were

purchased. The total

fleet size had achieved

11,184 units.

• The second rating from

Moody's Investor

Service at "B3“/Stable

was assigned.

• Signed the contract for

the financial statements

audit with KPMG.

Увеличение парка

вагонов и улучшение

кредитного рейтинга

• In 2014, Gazprombank

provided a 9-year loan

of $ 50 million, which

were used to purchase

853 cars.

• Moody's Investor

Services raised its

forecast for all of the

company's ratings from

"stable" to "positive."

Увеличение парка

вагонов и улучшение

кредитного рейтинга

Growth of fleet.

International projects

implementation. Status of

international corporate.

Growth of fleet and ratings

2010 2013 2014

7

Supervisory Board

8

Vadim Malakhov

Head of Supervisory Board

Head of Supervisory Board since June

2015. Mr. Malakhov graduated from

Kazakh Polytechnic Institute in 1982,

majoring in geochemistry.

From 1996 to 1998 he was a Head of the

company responsible for the quality –

“BEST” LLP. From 2002 till 2015 Mr.

Malakhov has been the General Director

of “Eastcomtrans“ LLP.

Ekaterina Benjamin

Independent Director

of Supervisory Board

was appointed as an Independent

member of the Supervisory Board in

December 2014. Mrs. E. Benjamin has

an extensive experience in financial

institutions such as Citibank

Kazakhstan, Bank Petrocommerce,

Kazinvestbank, HSBC Bank

Kazakhstan, Altyn Bank; From 2005 till

2011, Mrs. Benjamin has been an

Independent Director at Visor Capital,

"Kazakhmys“ Pension fund,

Altaypolimetal.

Yuri Lavrinenko

Independent Director

of Supervisory Board

was appointed as an Independent

member of the Supervisory Board in

2013. Mr. Lavrynenko holds a Ph.D. in

economics. Since 2010, Mr. Lavrynenko

served as Advisory to KTZ President.

Mr. Lavrinenko was the General

Director of

«KamkorRepairCorporation» from 2007

to 2008, Managing Director of the

branch of KTZ from 2006 to 2007, the

First Deputy Minister of Transport and

Communications of the Republic of

Kazakhstan from 2002 to 2006 and

Deputy Speaker of Majilis of

Kazakhstan from 1999 to 2002.

Mikhail Kuznetsov

Independent Director

of Supervisory Board

was appointed as an independent

member of the Supervisory Board in

May 2015. Mr. Kuznetsov (Ph.D.) and

holds a «Chartered Director" of the

British Institute of Directors cum

Executive MBA IE Business school

(Madrid). Mr. Kuznetsov held senior

positions in companies "Aviacor",

"LUKOIL-Volga", "Promsvyaz" and

"The International Finance Corporation»

(IFC). Currently, Mr. Kuznetsov is an

Independent director on the Board of

Directors of "Energosetproject“JSC, of

"Echo" (Roscosmos), "Credit Bank of

Moscow" JSC. He is also the CEO and

managing partner of Corporate

Development Center, and the executive

director of the Association of Corporate

Directors.

Key highlights in 2014

On February 11, 2014 the National Bank of Kazakhstan has devalued tenge by 18.9 percent. Tenge exchange rate increased from

155 to 185 per dollar.

Country Conditions:

Gross revenue in 2014 has grown to USD 174 923 ml.

EBITDA achieved USD 130 883 ml. in 2014

EBITDA margin comprised 75% in 2014

Financial highlights:

GazPromBank: Company disbursed a 9-year loan from GazPromBank JSC in the amount of $50 million with interest rate of

margin 6,5% + 1m LIBOR, tenor 7+2years.

Al Hilal provided 5-year loan in the amount of $34,5 million with interest rate 6,5 in USD and 8,25 in KZT. The received funds

were used to fully refinance of loan with HSBC Bank Kazakhstan.

EBRD: Company signed Term Sheet with EBRD in the amount of $140 million.

Borrowings:

Corporate rating: Fitch: June 03,2014 Fitch Ratings re-confirmed the corporate Eastcomtrans LLP long-term issuer rating at the level B on the

international scale. National scale rating was also increased from B + to BB, with a rating outlook "stable.“

Moody’s: July 10, 2014 Moody's Investors Service has changed to “Positive” from “Stable” the outlook on Eastcomtrans LLP's

B3 corporate family rating (CFR), B3-PD probability of default rating (PDR), B3.kz national scale rating (NSR) and the B3 senior

secured rating assigned to the company's $100 million five-year notes, with a loss given default (LGD) assessment of LGD3/49%.

Concurrently, Moody's has affirmed these ratings.

Acquisition of rolling stock : In 2014 the Company signed contracts for the purchase of 853 wagons, including:

200 Hoppers;

400 Covered wagons;

153 Open top;

100 Dump cars.

Supervisory Board 1. Mr. Vadim Malakhov – Head of Supervisory Board

2. Mrs. Ekaterina Benjamin – Independent Director of Supervisory Board

3. Mr Yuri Lavrinenko – Independent Director of Supervisory Board

4. Mr. Mikhail Kuznetsov – Independent Director of Supervisory Board

25.12.2014 Mrs. Ekaterina Benjamin was appointed as Independent member of the Supervisory Board, succeeding Mr. Adilzhan

Kozhabergenov.

19.05.2015 Mr. Mikhail Kuznetsov was appointed as Independent member of the Supervisory Board.

01.06.2015 Mr. Vadim Malakhov was appointed as Chairman of the Supervisory Board, succeeding Mr. Marat Sarsenov.

9

Operational activity

10

Transport network of Kazakhstan

Transport sector in Kazakhstan is of a significant importance. Vast territory of 2.7

million km², low density of population, long distances between industrial and

agricultural centers, as well as remoteness from world markets, makes developed

transportation system vital for Kazakhstan.

Railway is the main mode of long distance cargo shipment in Kazakhstan. Large

area, and high level of export, import and transit of goods makes railway transport

absolutely essential element of the whole Kazakh economics.

There are 16 boarder points (11 with Russia, 2 with Uzbekistan, 1 with Kyrgyzstan,

2 with China), which connect Kazakh railway network with neighboring countries.*

Management is carried out by Kazakhstan Temir Zholy National Company JSC

(KTZ). KTZ has railway network on its the balance sheet. Part of network is

managed by railway administration of Russian Federation and Kyrgyzstan.

Rail network of Kazakhstan

11

Kazakhstan has an extensive railway network with total length of approximately 15 thousand km, 6000 of which being double track, and about 5000 being electrified. Spread

out length of main ways comes up to 18.8 thousand km; station and specialized tracks - up to 6.7 thousand km. The value of rail transport in Kazakhstan is very large. More

than 68% of total turnover and more than 57% of the country's passenger traffic accounts for the railways. Railway industry employs more than 125,000 people, which comes

up to nearly 1% of whole population of Kazakhstan.

The share of transport in GDP amounts to 7.4%. The share of rail transport in total freight traffic of the country - 8.27%. At the same time, 48% of revenue of freight traffic

and 29% of passenger traffic accounts for railway enterprises from all the revenues of transport enterprises of the state.**

Source:Internet

* Source: https://ru.wikipedia.org

**Source: Agency of statistics of the RK

• Average lifetime – 40 years

• Average capacity – 40 tons

• Average tank volume – 76

m3

• Max speed – 120 kmp/h

• Used for transportation of

liquefied petroleum gases

(LPG) and light

hydrocarbons

Types of cars

• Average lifetime – 32 years

• Average capacity – 60 tons

• Average tanker volume –

73 m3

• Max speed – 120 kmp/h

• Used for transportation of

oil and refined products

(light refined products,

viscous refined products,

petrol)

Oil tanker car (RTW) Gas tanker car (RTW) Gondolas

• Average lifetime – 22

years

• Average capacity – 74

tons

• Max speed – 100 kmp/h

• Used for transportation of

bulk cargo (ore, coal, etc.)

Technical specifications: Technical specifications: Technical specifications:

Hoppers Platforms Dumpcars

• Average lifetime – 22

years

• Average capacity – 72,5

tons

• Max speed – 120 kmp/h

• Used for transportation of

cement

Technical specifications:

• Average lifetime – 32

years

• Average capacity – 72

tons

• Max speed – 120 kmp/h

• Used for transportation of

containers

Technical specifications:

• Average lifetime – 22

years

• Average capacity – 64

tons

• Max speed – 120 kmp/h

• Used for transportation of

bulk cargo (ore, coal, etc.)

Technical specifications:

12

Freight shipment market of Kazakhstan

13

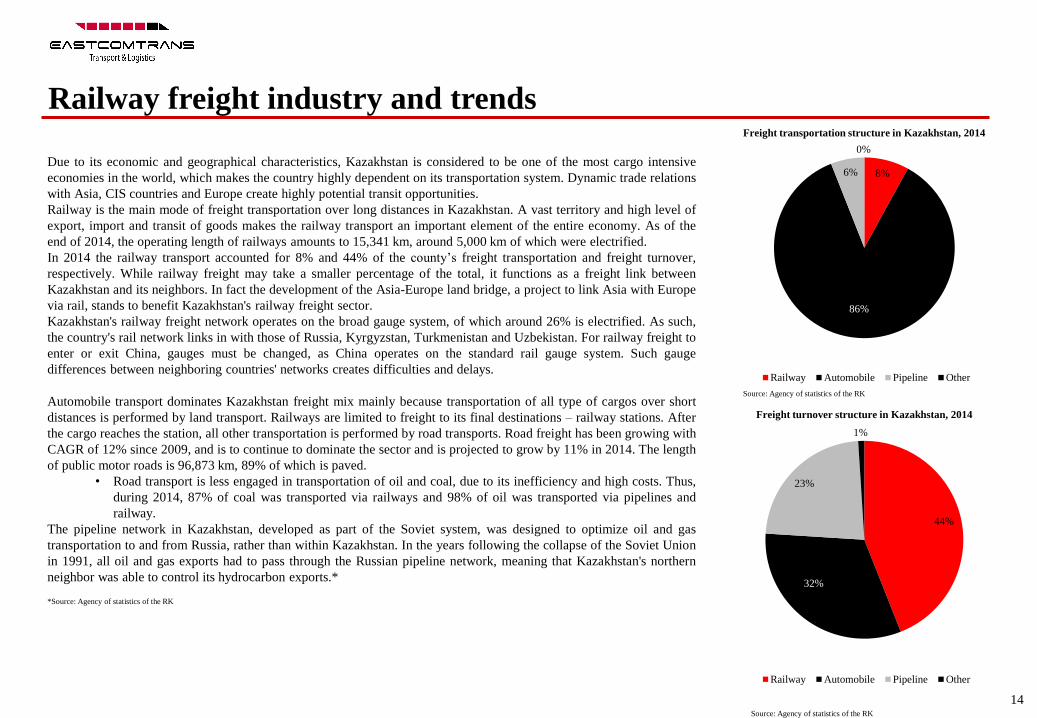

Railway freight industry and trends

Due to its economic and geographical characteristics, Kazakhstan is considered to be one of the most cargo intensive

economies in the world, which makes the country highly dependent on its transportation system. Dynamic trade relations

with Asia, CIS countries and Europe create highly potential transit opportunities.

Railway is the main mode of freight transportation over long distances in Kazakhstan. A vast territory and high level of

export, import and transit of goods makes the railway transport an important element of the entire economy. As of the

end of 2014, the operating length of railways amounts to 15,341 km, around 5,000 km of which were electrified.

In 2014 the railway transport accounted for 8% and 44% of the county‟s freight transportation and freight turnover,

respectively. While railway freight may take a smaller percentage of the total, it functions as a freight link between

Kazakhstan and its neighbors. In fact the development of the Asia-Europe land bridge, a project to link Asia with Europe

via rail, stands to benefit Kazakhstan's railway freight sector.

Kazakhstan's railway freight network operates on the broad gauge system, of which around 26% is electrified. As such,

the country's rail network links in with those of Russia, Kyrgyzstan, Turkmenistan and Uzbekistan. For railway freight to

enter or exit China, gauges must be changed, as China operates on the standard rail gauge system. Such gauge

differences between neighboring countries' networks creates difficulties and delays.

Automobile transport dominates Kazakhstan freight mix mainly because transportation of all type of cargos over short

distances is performed by land transport. Railways are limited to freight to its final destinations – railway stations. After

the cargo reaches the station, all other transportation is performed by road transports. Road freight has been growing with

CAGR of 12% since 2009, and is to continue to dominate the sector and is projected to grow by 11% in 2014. The length

of public motor roads is 96,873 km, 89% of which is paved.

• Road transport is less engaged in transportation of oil and coal, due to its inefficiency and high costs. Thus,

during 2014, 87% of coal was transported via railways and 98% of oil was transported via pipelines and

railway.

The pipeline network in Kazakhstan, developed as part of the Soviet system, was designed to optimize oil and gas

transportation to and from Russia, rather than within Kazakhstan. In the years following the collapse of the Soviet Union

in 1991, all oil and gas exports had to pass through the Russian pipeline network, meaning that Kazakhstan's northern

neighbor was able to control its hydrocarbon exports.*

Freight transportation structure in Kazakhstan, 2014

Freight turnover structure in Kazakhstan, 2014

Source: Agency of statistics of the RK

*Source: Agency of statistics of the RK

8%

86%

6%

0%

Railway Automobile Pipeline Other

44%

32%

23%

1%

Railway Automobile Pipeline Other

14 Source: Agency of statistics of the RK

Railway freight industry and trends • With the trans-Caspian tanker and rail exports and the development of an oil pipe route to China,

Kazakhstan has slowly reduced its reliance on Russia. Nevertheless, the vast majority of exports

continue to transit via Russian territory. Gas is currently only exported to Russia, although exports to

China are being targeted for the future. Since 2009, pipeline transportation in Kazakhstan has been

growing with CAGR of 7%.

• Growing oil and gas production is driving new capacity expansion projects. Existing infrastructure is

either being rehabilitated or expanded, while new pipeline projects are underway to enable increased

exports and domestic distribution.

Sea freight is concentrated at the Caspian region and mainly associated with development of oil and gas

industry in Kazakhstan.

• The two main ports in Kazakhstan are Aktau on the Caspian Sea and Semey on the Irtish river in the

northeast of the country. As part of the Kazakhstan Caspian Transportation System (further “KCTS”)

project (discussed further in Railway freight transportation demand), Kazakhstan could expand its port

facilities, boosting capacity at Aktau and building a new port at Kuryk. Under the KCTS concept, these

two ports would also be linked by pipeline to key oil fields in western Kazakhstan. Smaller facilities at

Atyrau and Bautino are used to support offshore operations in the Caspian Sea.

Air freight transport comprises less than 1% of total freight turnover in Kazakhstan.

Transportation volumes in Kazakhstan

Freight turnover in Kazakhstan, bln ton-km

Source: Agency of statistics of the RK

Source: Agency of statistics of the RK

248 268

280 295 294 273

1688

1972

2476

2718

2983 3134

163 194 214 213 226 221

0

500

1000

1500

2000

2500

3000

3500

2009 2010 2011 2012 2013 2014

mln

to

nn

es

Railway Automobile Pipeline

198 213

224 236 231

214

66 80

121 132

145 158

72

89 101

107 116 116

0

50

100

150

200

250

2009 2010 2011 2012 2013 2014

mln

to

nn

es

Railway Automobile Pipeline

15

Structure of Kazakhstan rolling stock fleet Since the collapse of USSR, subsidiary of KTZ, Kaztemitrans JSC (further “Kaztemirtrans”), has dominated the rails freight market after inheriting more than 100,000

railcars. Due to poor economic situation in Kazakhstan in 1990‟s, under-investment into renewal of wagon fleet led to their aging and gradual write-off. The graph below

provides the comparison number of private and Kaztemirtans‟ freight cars.

Kaztemirtans‟ underinvestment is aggravated by regulation of tariffs by Antimonopoly Agency due to its dominating position in the market, and limits its ability to earn higher

profit margins compared to private sector.

After economic revival in the beginning of 2000‟s and reforms undertaken by the government in the rail sector, the number of railcars operated by private companies boosted

significantly.

The Restructuring Program of Railway Transport of the RK (the reform launched in early 2000s) was aimed to commercialize freight railways sector and allow private

companies to enter the market and bring additional investment into the industry.

Nevertheless, starting from 2005, Kaztemirtrans started renewing its wagon fleet backed up by borrowings from third parties and its parent company KTZ.

Boosting economy and deregulation of the railway sector created opportunities for the private operators due to deficit of the freight railcars. As a result major part of private

operators was established showing CAGR of 17.6% from 2002 to 2014. In 2014 the share of private operator reached almost 54% (71,351 out of 132,291 units) compared to

10% (11,300 out of 109,600 units) in 1995.*

Structure of Kazakhstan rolling stock fleet

98,3 98,3 93,1

89,9 88,1

78,5 77,6 77 70,4

60,8 56,8 56,9

61,5 59,8 60,6

53,1 55,9

66,5 65,8 60,9

11,3 11,3 12,2 10,1 12,6 11,3 8,5 10,7

18,4

26,7 30,1

33,6 34,7 35,2 39,6 43,3

51,9

62,2 63,5

71,3

0

20

40

60

80

100

120

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Kaztemirtrans (inventory) freight cars Private companies' freight cars

16

Source: Agency of statistics of the RK

*Source: Agency of statistics of the RK

Railway freight transportation demand in Kazakhstan

For the period 2009-2014 on average 59% of freight transported by railway is represented by coal, metals and metal ores,

and 12% was represented by construction cargo. Gondolas are the key means of transportation for coal, ores and construction

materials. The share of oil and oil products in railway transportation is around 12%.

Coal

Coal transportation comprises 43% of total volume of railway freight. The largest coal-basins are Karaganda and Ekibastuz

coal fields which account for more than 30% of coal production.

•From Karaganda coal basin, the coal is transported via railway to Russia and within Kazakhstan through the Astana-Almaty

and Zharyk-Dzhezkazgan railway routes;

•From Ekibastuz, the coal is transported via routes that connect stations of Ekibastuz coal fields (route Astana-Pavlodar) and

with internal consumers such as energy generating companies and power plants.

The main importer of Kazakhstani coal is Russia accounting for about 90% of total coal exported from Kazakhstan.

43%

28%

9%

3%

16%

Cargo turnover by railways in Kazakhstan, 2014

Gandolas Tanks Boxcars Platfoms Other

Source: Agency of statistics of the RK

Source: Agency of statistics of the RK

41%

18%

12%

10%

26%

The structure of railway freight transportation by main

cargoes in Kazakhstan, 2014

Coal Ore species Construction freight

Oil and oil products Other

98 104 107 108 102

44 44 46 47 43

33 26 26 45

23

17 28 29

36

35 26

27 25

34

24

0

50

100

150

200

250

300

350

2010 2011 2012 2013 2014

Freight transportation by type of products

Coal Ore species Other Construction cargo Oil and oil products Iron Wheat Chemicals and fertilizers

17

Source: Agency of statistics of the RK

Ferrous and non-ferrous metal ores

Transportation of ore and ferrous metals comprises about 19% and 3% respectively. Iron ore is mainly exported

to Russia and China. Main consumers of iron ore are metallurgical complexes. Non-ferrous metal ore is mainly

transported via domestic routes and consists of bauxite, copper ore, copper concentrate and polymetallic ore.

For metallurgic industry, railway provides the most effective mean of transportation compared to oil and gas

sector, where pipeline transportation is more practical. Therefore, the metallurgic sector is occupied by large

industrial groups having their own transportation facilities. As a result, the sector offers limited opportunities for

third party market players providing rolling stock leasing services.

Construction cargo

Construction materials transportation, which comprises around 16% of railway freight, is mainly linked to

construction projects carried out in Kazakhstan, and is subject to seasonality, with slowdown in December-

February period

Oil and gas

Oil, oil products, LPG and sulphur are the key products transported in Western Kazakhstan as the largest oil and

gas fields are located in this area. These fields include Tengiz, Karachaganak, Kisimbai, Zhetybai, Tenge and

other.

• Around 80% of all transportation is made via pipelines and a relatively small portion of produced oil

and oil products (15%) is transported by railway.

Coal Ore and metals Oil and gas

Bogatyr Komir Kazzinc Tengizchevroil (TCO)

Kazakhmys Kazakhmys CNPC-AktobeMunaiGas

(Zhanazhol, Kenkiyak )

ENRC ENRC MangystauMunaiGas (Asar,

Zhetybai, Bekturly, other)

ArcelorMittal

Temirtau

ArcelorMittal

Temirtau

KazGerMunai (Akshabulak,

Nuraly and Aksai)

KSP Steel KazMunayGas Exploration and

Production (Uzen)

Frontier Mining Karachaganak Petroleum

Operating (Karachaganak)

Sunkar

Resources Zhaikmunai

Key goods transported by railway by companies

Railway freight transportation demand in Kazakhstan

Source: Agency of statistics of the RK

13 14 14 12 13

64 66 67

66 67

0 0 0

1 2

0

10

20

30

40

50

60

70

80

90

2010 2011 2012 2013

mlm

to

nn

es

Transportation of oil

Railway Pipelines Other

18

Gauge differences between Kazakhstan and Chinese rail network created difficulties and delays in transportation

of oil. This problem was tackled by the Dostyk JV (PetroKazakhstan), which constructed an oil terminal worth

USD 22.5 million with an annual capacity of 1.2 mln tons at Druzhba station (border with China). Test cargoes

began in mid-2000s and China began importing Kazakh crude from CNPC's AktobeMunaiGas fields and

PetroKazakhstan's Kumkol operations in 2003. The commissioning of the Kazakhstan-China oil pipeline in 2006

removed the need for rail exports to China.

Despite the inevitable restrictions of Kazakhstan's single gauge network, estimates suggest that the country has

the capacity to export 15-17 mln tons of oil by rail. However, actual volumes are believed to be much lower

(around 12-13 mln, please see adjacent graph). TCO, being the largest user of the rail network, has facilities to

load 11.3 mln tons of oil directly onto railcars at Tengiz for export via Russian and Ukrainian Black Sea ports.

Railway freight transportation demand in Kazakhstan

Kashagan 6

(Reserves –12,580 mln. barrels

in oil equivalent)

Karachaganak 4

(Reserves –6,252 mln. barrels

in oil equivalent)

Tengiz 2

(Reserves –8,060 mln. barrels

in oil equivalent)Uzen3

(Reserves –3,779 mln. barrels

in oil equivalent) Kalamkas and Zhetibay5

(Reserves –1,043 mln. barrels

in oil equivalent)

Chinarevskoye 7

(Reserves –459 mln. barrels

in oil equivalent)

Zhanazhol and Kenkiyak 8

(Reserves –1,534 mln. barrels

in oil equivalent)

Review of the key oil & gas fields in Kazakhstan by reserves 1

Notes to graphic

1.2P: Proven and probable reseves

2.Chevron, ExxonMobil, NC KMG, LUKOil

3.NC KMG

4.BG, Chevron, LUKOil, Eni, NC KMG

5.NC KMG, CNPC

6.Eni, ExxonMobil, NC KMG, Shell, Total, CNPC, INPEX

7.Zhaikmunai

8.CNPC AktobeMunaiGaz Source: Ministry of Oil and Gas of the RK, MEMR

48 49 47 46 44 42 40 38

34 35 33 36 38 41 43 43

12 12 11 11 10 9 8 9

7 13 15 15 15 15 16

0

20

40

60

80

100

120

2015F 2016F 2017F 2018F 2019F 2020F 2021F 2022F

mln

to

nn

es

Forecasted liquid production, 2015-2020

Other Tengiz Karachaganak Kashagan

19

Source: Internet

Financial Activity

20

Financial Statements: Balance Sheet (audited)

(KZT '000) 2008 2009 2010 2011 2012 2013 2014

Assets

Non-current assets

Property, plant and equipment 18 808 800 17 819 052 49 515 217 75 659 512 94 005 283 99 312 832 105 242 701

Long-term financial investments 3 722 581 4 206 585 19 281 22 464 314 109 115 163 23 997

Other non-current assets 678 469 642 088 1 636 995 4 096 312 51 527 48 263 44 798

Total non-current assets 23 209 850 22 667 725 51 171 493 79 778 288 94 370 919 99 476 258 105 311 496

Current assets

Inventories 10 082 8 012 40 866 62 278 68 478 79 185 93 774

Loans receivable 353 098 1 241 216 10 427 19 290 18 422 12 274 175 257

Trade and other receivables 2 442 109 1 388 964 2 031 584 2 166 373 3 722 031 5 138 954 6 900 135

Advance payments 137 158

- 505 347 689 647 680 621 2 989 141 1 837 775

Cash and cash equivalents 275 024 1 008 018 3 171 423 2 052 467 1 050 814 3 553 671 5 437 405

Total current assets 3 217 471 3 646 210 5 759 647 4 990 055 5 540 366 11 773 225 14 444 346

Total Assets 26 427 321 26 313 935 56 931 140 84 768 343 99 911 285 111 249 483 119 755 842

Equity and liabilities

Equity

Charter capital 840 000 840 000 840 000 840 000 840 000 3 845 400 3 845 400

Revaluation reserve on Property, plant and equipment 5 409 445 4 415 488 15 801 863 14 955 611 14 166 827 13 465 803 12 614 011

Retained earnings 3 677 771 5 018 040 8 761 111 13 584 322 19 451 800 26 809 948 28 370 829

Unpaid capital -207 460

- -

- - - -

Total Equity 9 719 756 10 273 528 25 402 974 29 379 933 34 458 627 44 121 151 44 830 240

Liabilities

Borrowings 14 191 741 13 739 679 24 365 305 47 127 311 55 459 394 56 132 752 63 576 739

Deferred income tax liabilty 1 761 886 1 747 578 5 972 022 6 751 301 7 830 051 9 445 321 9 766 550

Trade and other payables 753 938 553 150 1 190 839 1 509 798 2 163 213 1 550 259 1 582 313

Total Liabilities 16 707 565 16 040 407 31 528 166 55 388 410 65 452 658 67 128 332 74 925 602

TOTAL EQUITY AND LIABILITIES 26 427 321 26 313 935 56 931 140 84 768 343 99 911 285 111 249 483 119 755 842

21

Financial Statements: Income Statement (audited)

(KZT '000) 2008 2009 2010 2011 2012 2013 2014

Revenue 5 256 195 9 150 677 9 806 941 17 050 667 22 476 151 25 512 955 31 897 186

Cost of sales −3 017 971 −3 812 676 −2 037 302 −5 703 716 −8 766 962 −7 709 536 −10 930 694

Gross profit 2 238 224 5 338 001 7 769 639 11 346 951 13 709 189 17 803 419 20 966 492

Gross margin (%) 43% 58% 79% 67% 61% 70% 66%

General and administrative expenses −231 199 −459 984 −831 736 −979 913 −1 127 215 −1 685 002 −2 794 203

EBITDA 3 204 373 6 352 491 7 779 047 13 021 404 17 403 541 21 601 802 23 866 547

EBITDA margin (%) 61% 69% 79% 76% 77% 85% 75%

Depreciation accounting (total) −1 197 348 −1 474 474 −841 144 −2 654 366 −4 821 567 −5 483 385 −5 694 258

EBIT 2 007 025 4 878 017 6 937 903 10 367 038 12 581 974 16 118 417 18 172 289

EBIT Margin 38% 53% 71% 61% 56% 63% 57%

Finance income 504 374 474 302 879 583 101 468 611 116 57 077 35 278

Finance costs −1 518 437 −4 115 842 −2 003 072 −4 648 570 −5 380 377 −6 115 362 −14 571 996

Other Operating Expenses 681 585 70 010 −47 449 −13 674 −262 032 188 064 −91 662

Profit before income Tax 1 674 547 1 306 487 5 766 965 5 806 262 7 550 681 10 248 196 3 543 909

Income Tax 12 327 −388 978 −1 377 527 −1 178 736 −1 546 482 −2 090 022 −795 277

Net Income 1 686 874 917 509 4 389 438 4 627 526 6 004 199 8 158 174 2 748 632

Net Income margin (%) 32% 10% 45% 27% 27% 32% 9%

22

Financial Statements: Cash Flow Statement (audited)

(KZT '000) 2008 2009 2010 2011 2012 2013 2014

Cash generated from operations −687 033 5 717 844 9 182 676 13 513 891 11 625 837 14 074 136 15 534 705

Cash flows from investing activities −6 746 168 −205 847 −13 155 750 −31 058 765 −18 751 655 −14 678 684 −11 398 871

Cash flows from financing activities 6 777 660 −4 779 003 5 900 479 16 015 062 6 716 598 830 560 −3 504 753

Net change in cash and cash equivalents −655 541 732 994 1 927 405 −1 529 812 −409 220 226 012 631 082

Cash and cash equivalents at the beginning of the year 930 565 275 024 1 008 018 2 935 423 1 424 635 1 050 814 1 257 028

Cash and cash equivalents at the end of the year 275 024 1 008 018 2 935 423 1 424 635 1 050 814 1 257 028 2 155 105

23

24

Total revenue in 2014 reached 31 897 mln tenge ($174.9 mln at the exchange rate of the National Bank of Kazakhstan at the end of the year), which is higher than in 2013 by

25% in tenge and 6% in dollar terms.

Analysis of financial-economic activity

9 151 9 807 17 051 22 476 25 513 31 897

61,7 66,5

114,9

149,1 165,6

174,9

2009 2010 2011 2012 2013 2014

Revenue, mln tenge Revenue, $ mln

The dynamics of total revenue for 2009-2014.

Comparative structure of total revenues, the 2013-2014.

79% 73%

16% 23%

5% 4%

2013 2014

Rent Operating Forwarding

Summary measure of total revenues in 2014 included proceeds in the following areas:

Revenue from rent of cars amounted to 23 227 million tenge (+ 16% year-to-g, 73% of total revenue).

Revenue from operating was 7 293 million tenge (an increase of 83% from the 2013, 23% of total revenue).

Revenue from freight forwarding and transshipment of cargo amounted to 1 295 million tenge (-1% year-to-g, 4% of total revenue).

Analysis of financial-economic activity

25

Revenue from other services in 2014 amounted to 83 million tenge ($ 0.5 million, -41% year-to-r) and its share in total revenues is negligible (-0.3% in 2014 against -0.5%

in 2013).

Cost of sales in 2014 were 10 931 million tenge ($ 59.9 million), higher than the previous year by 42% in tenge and 20% in dollar.

3 813 2 037 5 704 8 767 7 710 10 931

25,7

13,8

38,4

57,0

50,0

59,9

2009 2010 2011 2012 2013 2014

COGS, mln KZT COGS, $ mln

Dynamics of production costs (COGS), 2009–2014 гг. Comparative structure of production costs, 2013–2014

70% 52%

17%

24%

4% 8%

4% 4%

5%

2013 2014Depreciation Repair

Use of railway infrastructure Payroll expenses

Wagons lease Other

Cost items Revenue (mln KZT),

2014

Revenue (mln KZT),

2013 growth rate, y-to-y Share, 2014 Share, 2013

Difference,

y-to-y

Depreciation 5 631 5 415 4% 52% 70% −18 п.п.

Repair of wagons 2 671 1 299 2,1х 24% 17% +7 п.п.

Use of railway infrastructure 906 344 2,6х 8% 4% +4 п.п.

Wagons lease 514 13 39х 5% 0,2% +~5 п.п.

Payroll expenses 415 288 1,4х 4% 4% –

Insurance of wagons 109 109 – 1% 1% –

Other 685 242 2,8х 6% 4% +2 п.п.

Total 10 931 7 710 42% 100% 100%

In 2014, the total production cost structure has undergone several changes - decreased the proportion of depreciation, increased the cost of repair of rolling stock and the cost

of renting:

Analysis of financial-economic activity

26

Total financial expenses were 14 572 million tenge ($ 79.9 million), an increase of 2.4 times in tenge and 2 times in dollar

Cost items Revenue (mln KZT),

2014

Revenue (mln KZT),

2013 growth rate, y-to-y Share, 2014 Share, 2013 Difference

Expenses on compensation 5 820 5 112 14% 40% 84% −44 п.п.

Negative exchange rate. 8 752 1 003 8,7х 60% 16% +44 п.п.

Total 14 572 6 115 2,4х 100% 100%

Made payments to reimburse interest remuneration to financial institutions (BNP Paribas, HSBC Bank Kazakhstan "ATF Bank», IFC, Eurobonds, "Gazprombank», Al Hilal

Bank) and leasing companies ("Raiffeisen Leasing", "DBK-Leasing") for the received loans and credits.

Financial income in 2014 amounted to 35 million tenge against 57 million tenge a year earlier ($ 0.19 million and $ 0.37 million respectively), the rate of decline in tenge

made up 38%.

100; 29%

75; 21%

50; 14%

32; 9%

29; 8%

27; 8%

17; 5%

16; 5% 3; 1%

Eurobonds

BNP Paribas

Gazprombank

Al Hilal Bank

EBRD

IFC

KDB Leasing

ATF Bank

Raiffaisen Leasing

The structure of the loan portfolio, the end of 2014 ($ million and the share in the total portfolio)

Long-term and current financial debt of the Company at the end of

December 2014 amounted to $ 349 million (versus $ 364 million at the

beginning of the year, -4.3% year-to-r). The loan portfolio of the company

includes the following obligations to the financial institutions:

To the short-term portion of the debt accounted for about 15% of the total

loan portfolio, the long-term - 85%. The proportion of national currency

loans was 18%, the remaining 82% are denominated in US dollars. The

weighted average rate on the loan portfolio at the end of December 2014

amounted to 7.31% per annum.

General and administrative expenses in 2014 amounted to 2 794 million tenge ($ 15.3 million), + 66% y-to-y in tenge and 40% in US dollars

The main reasons for the growth of this group of expenditures in 2014 are large payments on insurance risks and unresolved offset VAT.

Cost items Revenue (mln KZT),

2014

Revenue (mln KZT),

2013 growth rate, y-to-y Share, 2014 Share, 2013 Difference

Payroll expenses 915 920 −1% 33% 55% −22 п.п.

Insurance of risks 946 0 − 34% − +~34 п.п.

Taxes other than CIT 325 47 7х 12% 3% +9 п.п.

Office rent 123 112 9% 4% 7% −3 п.п.

Other 485 606 −20% 17% 35% −18 п.п.

Total 2 794 1 685 66% 100% 100%

Analysis of financial-economic activity

27

Net profit at the end of 2014 was 2 749 million tenge (-66% year-to-r), which is explained almost ninefold increase in foreign exchange losses (8 752 million tenge in 2014

to 1 003 million tenge a year earlier) due to the 19% depreciation of the tenge against the US dollar in February 2014. In dollar terms, net income was $ 15.1 million (-72%

year-to-year).

The Company's EBITDA in 2014 increased by 10% in tenge and amounted to 23 867 million tenge, in US dollars, this indicator decreased by 7% to $ 140.2 million in 2013

to $ 130.9 million in 2014. The EBITDA margin was 75% (-10 pp. y to-y).

Formation of EBITDA, 2014. ($ Mln)

130,9

59,9

15,3 31,2

Total revenue COGS SGA DDA EBITDA

174,9

Cash at the end of 2014 amounted to 2 155 million tenge ($ 11.8 million, + 71% y-to-y), the amount of funds on deposit grew by 43% and reached 3 282 million tenge ($

18.0 million). Thus, the total amount of Company‟s Cash for the year amounted to ~ $ 29.8 million.

Capital expenses in 2014 were 10 184 million tenge ($ 57 million, -18%), which mainly focused on the purchase of new rolling stock (see. Section "Park of cars").

Key financial covenants:

Covenant Required Level Indicator in 2014 Compliance with

the requirements

Current Ratio Min 0,75 1,3

Net Debt / EBITDA Max 3,75 2,4

Debt Service Coverage

Ratio Min 1,2 2,3

Tangible Net Worth Min $90 mln

(16 412 mln KZT)

$176 mln

(32 086 mln KZT)

Risk factors

28

Demand

In Kazakhstan over 60% of goods transported by rail are raw materials in mining manufacturing (coal, ore, petroleum, nonferrous and ferrous metals). In this regard, the

demand for different types of cars is largely determined by trends in the development of relevant industries. Cargo owners prefer leasing cars, not wishing to have their

property in order to reduce the risk of downtime and protect themselves in the event of short-term contracts.

The need for tank wagons for the transportation of oil and LPG is directly dependent on the global demand for oil and gas production from oil and gas pipelines and power

available in the Republic of Kazakhstan.

Kazakhstan's oil reserves are estimated at about 30 billion barrels, 77% of which are located in three major fields - Kashagan, Tengiz and Karachaganak. (Other key fields

include: Uzen Zhetybai, Janajol, Kalamkas, Kenkiyak Karanzhanbas, Kumkol North Buzachi, Alibekmola Central and Eastern Prorva Kenbai, Royal).

It is expected that from 2015, oil exports from Kazakhstan will grow by more than 8% per year due to increased production volumes in key fields.

It is projected that by 2020 Kazakhstan's oil production will reach 145.7 million tons a year, while export is more than 80%. Domestically, oil will be transported to

refineries and petrochemical plants for the subsequent production of petroleum products.

Competitors

The company faces strong competition in the transportation of oil and petroleum products as a result of the development of a network of pipelines in Kazakhstan and the

countries bordering with Kazakhstan, as the transportation of crude oil by pipeline is more cost-effective and cost-effective than rail.

Kazakhstan and Russia use the same railway gauge. In Russia there is an excess of rolling stock, whereas in Kazakhstan - deficit. In addition, the last 5 years in Kazakhstan

rent rates were higher than in Russia. These factors pose a threat to the emergence of Russian operators in the rolling stock of Kazakhstan, which may lead to increased

competition and lower rental rates.

Risk factors

29

Social activity

30

Social activity

Dental care program "Give a smile“.

In 2014, we continued implementing «Give a smile» program.

The program aims to provide social assistance to children from disadvantaged

groups in the form of assistance in their health care (dental services unwarranted

public services (orthodontics).

Target Audience: orphanages, boarding schools for children from poor families of

Almaty and Almaty region. Beneficiaries are LEU «SOS Children's Village

Almaty" Boarding School № 10 for low-income children, children's home number

2, number 1 Orphanage, NC "family-type children's home" Perzent "Regional and

orphanage.

Timeline for program implementation: 2013-2015.

Project is carried out with the participation of volunteer students from faculty of

Dentistry of Kazakh state University named after Asfendiyarov through practical

workshops on dental hygiene.

31

The "Professional orientation of children”

On 31 March, 2014 was a start date of “Professional world“ project. As part

of that, Viktor Tskhay, Head of repair department of "Eastcomtrans“ met up

with the youngsters to tell them all about working in railway field from A to Z.

Adilzhan Kozhabergenov, CFO of Eastcomtrans spoke about “Financial

management”, having young students deeply interested and involved in an

active dialogue and discussion of an example of equity investments and its

growth.

Introduction to the legal profession was carried out by Maxim Martynovsky,

Chief of legal department of Eastcomtrans in an orphanage №2, Almaty.

Children were very keen on learning more about types, statuses of the

profession, its positive and negative sides. They happily came to conclusion

that to love what you do is essential since people contribute great deal of their

time to work.

Corporate governance

32

Corporate governance

33

General Meeting of Participants

Supervisory Board

Director General

Entry of international strategic investor (IFC) into the Company, its leading positions on the market, emission of Eurobonds at KASE and LSE, geographical expansion of business,

projects for IPO - all these factors contribute to Company's transition to a new level of development. It also applies to importance of more complex and serious issues of corporate

governance, which not only involves adopting a formal approach, but more importantly - implementing principles of corporate governance into practice, including corporate

governance. The Company adheres to the principles of a national code of corporate governance, following the recommendations of international best practices in corporate governance.

The supreme body consisting of Participants or their representatives

The Supervisory Board

is a body of strategic

management and

control of the

Company.

The number of members

of the Supervisory Board

is determined by the

general meeting of

members, but cannot

excess five.

In 2014, the Supervisory Board of the Company consisted of 3 and from 19/05/2015 – of 4 members:

Structure of the Supervisory Board of the Company:

1.Marat Sarsenov - Chairman of the Supervisory Board. Born on June 6, 1967. Has been the Chairman of the Supervisory Board for the

last three years (scope of business – railway transport), until 01/06/2015; the shareholder of the Partnership with 55.998% stake in charter

capital of the Company;

By the decision of the General Meeting of participants dated on 01.06.2015, Mr. Vadim Malakhov, who previously held the position of

General Director of the Company, was elected as the Chairman of the Supervisory Board.

2.Ekaterina Benjamin - Independent Member of the Supervisory Board. Born on January 9, 1974. Mrs. Benjamin has extensive

experience working in financial institutions, such as Citibank Kazakhstan, Bank Petrocommerce, Kazinvestbank, HSBC Bank Kazakhstan,

Altyn Bank. Mrs Benjaminis is not a member of the Company and/or its subsidiaries and affiliates, was elected as Independent member of

the Supervisory board by the decision of the General Meeting of participants from 25.12.2014 instead of Mr. Kozhabergenov Adilzhan

Akhmetzhanovich;

3.Yuri Lavrinenko - Independent Member of the Supervisory Board. Born November 24, 1945. Advisor to the President of “Kazahstan

Temir Zholy" (KTZ) since November 2010; not a member of Company and/or its subsidiaries and affiliates.

By the decision of the General Meeting of participants dated 19.05.2015 the Supervisory board was extended to 4 members and Mr.

Mikhail Kuznetsov was elected as Independent Member of the Supervisory Board. Mr. Kuznetsov held senior positions in such

companies as "Aviacor", "LUKOIL-Volga", "Promsvyaz" and "The International Finance Corporation» (IFC). Currently, Mr. Kuznetsov

is an Independent director on the Board of Directors of "Energosetproject“JSC, of "Echo" (Roscosmos), "Credit Bank of Moscow" JSC.

He is also the CEO and managing partner of Corporate Development Center, and the executive director of the Association of Corporate

Directors.

Mr. Vadim Malakhov had been working as Director General in 2014. Mr. Malakhov was born on August 28, 1960, he held the position of

Director General of the Company from 2002 till 01.06.2015; He is not a member of the Company and/or its subsidiaries and affiliates. By

the decision of the General Meeting of participants dated on 01.06.2015, Mr. Yevgeniy Plakhotin, who previously held the post of the

First Deputy General Director of the Company, was appointed as the Director General of the Company;

The sole executive body

The company continues to introduce some elements of evaluation and monitoring of the internal control and risk management, in particular:

• The Company developed and approved the Rules of internal control on management and use of insider information.

• The Company takes steps to implement the system of IT-incident management control to formalize processing applications received by Information Technology Division

• The Company adopted the Regulations on the insurance policy for creation of insurance to protect property interests of the Company.

• In 2014 the Company adopted and implemented a plan for the development of the corporate governance system, provides for an adjustment of internal documents and

policies, the introduction of the Corporate Secretary, improving the quality of internal control and risk management, information disclosure, the quality of planning and

reporting practices of the remuneration of management and key personnel .

Organizational structure

Director General

Deputy to Director

General for commercial &

manufacturing

Commercial

Department

Representative office in

Astana

Aktau Branch

Finance Department

Administrative

Department

Technical Department

Legal Department

HR Department

IT Department

Logistic Department

34

Financial Statement

35

To the Management of Eastcomtrans LLP

We have audited the accompanying financial statements of Eastcomtrans LLP

(the “Company”), which comprise the statement of financial position as at 31

December 2014, and the statements of profit or loss and other comprehensive income,

changes in equity and cash flows for the year then ended, and notes, comprising a

summary of significant accounting policies and other explanatory information.

Management’s Responsibility for the Financial Statements

Management is responsible for the preparation and fair presentation of these financial

statements in accordance with International Financial Reporting Standards, and for

such internal control as management determines is necessary to enable the

preparation of financial statements that are free from material misstatement, whether

due to fraud or error.

Auditors’ Responsibility

Our responsibility is to express an opinion on these financial statements based on our

audit. We conducted our audit in accordance with International Standards on

Auditing. Those standards require that we comply with ethical requirements and plan

and perform the audit to obtain reasonable assurance about whether the financial

statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts

and disclosures in the financial statements. The procedures selected depend on the

auditor‟s judgment, including the assessment of the risks of material misstatement of

the financial statements, whether due to fraud or error. In making those risk

assessments, the auditor considers internal control relevant to the entity‟s preparation

and fair presentation of the financial statements in order to design audit procedures

that are appropriate in the circumstances, but not for the purpose of expressing an

opinion on the effectiveness of the entity‟s internal control. An audit also includes

evaluating the appropriateness of accounting policies used and the reasonableness of

accounting estimates made by management, as well as evaluating the overall

presentation of the financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to

provide a basis for our audit opinion.

Independent Auditors’ Report

Opinion

In our opinion, the financial statements present fairly, in all material respects, the

financial position of the Company as at 31 December 2014, and its financial

performance and its cash flows for the year, then ended in accordance with

International Financial Reporting Standards.

Kim Y.V.

Certified Auditor

of the Republic of Kazakhstan,

Auditor‟s Qualification Certificate

No.МФ-0000042 of 8 August 2011

Alla Nigay

General Director of KPMG Audit LLC

acting on the basis of the Charter

36

Statement of financial position

37

In thousands of tenge Note

As at 31

December 2014

As at 31

December 2013

ASSETS

Non-current assets

Property, plant and equipment 6 105.242.701 99.312.832

Intangible assets 44.798 48.263

Loans due from employees 23.997 10.603

Non-current due from DAMU 13 - 104.560

Total non-current assets 105.311.496 99.476.258

Current assets

Inventories 93.774 79.185

Trade and other receivables 7 6.776.374 4.921.892

Other current assets 8 1.827.519 2.981.338

Current due from DAMU 13 123.761 217.062

Current income tax prepayment 10.256 7.803

Loans due from employees 175.257 12.274

Short-term bank deposits 9 3.282.300 2.296.643

Cash and cash equivalents 10 2.155.105 1.257.028

Total current assets 14.444.346 11.773.225

TOTAL ASSETS 119.755.842 111.249.483

EQUITY AND LIABILITIES

Equity 11

Charter capital 3.845.400 3.845.400

Revaluation fund 12.614.011 13.465.803

Retained earnings 28.370.829 26.809.948

TOTAL EQUITY 44.830.240 44.121.151

Non-current liabilities

Loans and borrowings 13 33.786.241 27.848.936

Bonds 14 17.862.890 14.990.000

Financial lease liabilities 15 2.427.289 3.614.491

Deferred tax liability 23 9.766.550 9.445.321

Total non-current liabilities 63.842.970 55.898.748

Current liabilities

Loans and borrowings 13 8.039.541 8.273.028

Bonds 14 266.940 225.526

Financial lease liabilities 15 1.193.838 1.180.771

Trade payables 16 731.923 790.800

Advances received 252.750 106.409

Other current liabilities 17 597.640 653.050

Total current liabilities 11.082.632 11.229.584

TOTAL LIABILITIES 74.925.602 67.128.332

TOTAL EQUITY AND LIABILITIES 119.755.842 111.249.483

Statement of profit or loss

38

In thousands of tenge Note 2014 2013

Revenue 18 31.897.186 25.512.955

Cost of sales 19 (10.930.694) (7.709.536)

Gross profit 20.966.492 17.803.419

Administrative expenses 20 (2.794.203) (1.685.002)

Other income 151.306 411.209

Other expenses (141.732) (149.873)

Net loss from disposal of property, plant and equipment (101.236) (73.272)

Operating profit 18.080.627 16.306.481

Finance income 22 35.278 57.077

Finance costs 22 (5.820.223) (5.112.401)

Foreign exchange loss, net (8.751.773) (1.002.961)

Profit before income tax 3.543.909 10.248.196

Income tax expense 23 (795.277) (2.090.022)

Profit and other comprehensive income for the year 2.748.632 8.158.174

Statement of cash flows

39

In thousands of tenge 2014 2013

Cash flows from operating activities

Profit before income tax 3.543.909 10.248.196

Adjustments:

Amortisation 5.694.258 5.483.385

Finance income (35.278) (57.077)

Finance costs 5.820.223 5.112.401

Net loss from disposal of property, plant and equipment 101.236 73.272

Provision for doubtful debts 4.074 912

Unrealized foreign exchange losses 8.156.114 967.504

Working capital adjustments

Increase of operating assets:

Inventories (14.589) (10.707)

Trade and other receivables (1.481.607) (1.339.975)

Other current assets (398.875) (763.880)

Increase of operating liabilities

Trade payables (58.877) (171.232)

Advances received 146.341 (251.875)

Other current liabilities (55.410) (18.787)

Cash flows from operating activities 21.421.519 19.272.137

Income tax paid (476.501) (467.276)

Interest paid on finance lease liability (433.904) (602.149)

Interest paid on loans and borrowings and bonds (4.976.408) (4.128.576)

Net cash flows from operating activity 15.534.706 14.074.136

Cash flows from investing activities

Purchase of property, plant and equipment (10.184.017) (12.470.272)

Purchase of intangible assets - (2.268)

Proceeds from sale of property, plant and equipment 14.814 58.925

Interest received from deposits 17.320 12.918

Deposits placed (14.875.026) (34.209.308)

Proceeds from repayment of deposits 13.804.369 31.912.666

Repayment of loans due from employees 19.439 20.255

Loans provided to employees (195.770) (1.600)

Net cash flows used in investing activities (11.398.871) (14.678.684)

Statement of cash flows

40

In thousands of tenge Note 2014 2013

Cash flows from financing activities

Proceeds from borrowings 21.448.198 4.839.543

Proceeds from bonds issuance - 14.782.727

Proceeds from contribution to the share capital - 3.005.400

Repayment of borrowings, including loan origination fees (21.745.067) (17.987.021)

Repayment of finance lease liabilities (1.168.341) (2.137.959)

Dividends paid (2.039.543) (1.672.130)

Net cash flows from financing activity (3.504.753) 830.560

Net increase in cash and cash equivalents 631.082 226.012

Effect of exchange rate fluctuations on cash and cash equivalents 266.995 (19.798)

Cash and cash equivalents as at 1 January 10 1.257.028 1.050.814

Cash and cash equivalents as at 31 December 10 2.155.105 1.257.028

Statement of changes in Equity

41

In thousands of tenge

Charter

capital

Revaluation

fund

Retained

earnings Total

Balance at 1 January 2013 840.000 14.166.827 19.451.800 34.458.627

Profit for the year – – 8.158.174 8.158.174

Other comprehensive income for the year

Amortization of revaluation reserve – (701.024) 701.024 –

Total comprehensive income for the year – (701.024) 8.859.198 8.158.174

Transactions with owners of the Company

Contribution to charter capital (Note 11) 3.005.400 – – 3.005.400

Dividends (Note 11) – – (1.501.050) (1.501.050)

Total transactions with owners of the Company 3.005.400 – (1.501.050) 1.504.350

Balance at 31 December 2013 3.845.400 13.465.803 26.809.948 44.121.151

Profit for the year - - 2.748.633 2.748.633

Other comprehensive income for the year

Amortization of revaluation reserve - (851.792) 851.792 -

Total comprehensive income for the year - (851.792) 3.600.424 2.748.632

Transactions with owners of the Company

Dividends (Note 11) - - (2.039.543) (2.039.543)

Total transactions with owners of the Company - - (2.039.543) (2.039.543)

Balance at 31 December 2014 3.845.400 12.614.011 28.370.829 44.830.240

Notes to the financial statement

1 REPORTING ENTITY

(a) Organization and operations

Eastcomtrans LLP (the “Company”) is a limited liability partnership established

under the laws of the Republic of Kazakhstan on 4 October 2002.

The principal activity of the Company is rendering of the services in the sphere of oil

and gas freight operations by railway over the territory of the Republic of

Kazakhstan.

The registered office of the Company is located at: office 11a, 77/7 Al-Farabi

Avenue, Almaty, 050040, Republic of Kazakhstan.

The Company is owned by Mr. M. Zh. Sarsenov (55,998%), a citizen of Republic of

Kazakhstan, and Steinhardt Holding N.V (37,332%), a company established under

the laws of the Netherlands, and International Finance Corporation (6.67%). The

ultimate controlling party is Mr. M.Zh. Sarsenov.

On 10 July 2014, Moody's Rating Agency confirmed B3 corporate credit rating under

the international and national scales to Eastcomtrans LLP. A credit rating outlook is

“Positive”.

On 3 June 2014, Fitch Ratings confirmed the Company‟s long-term credit ratings at B

level according to the international scale, and at BB(kaz) according to the local scale.

The credit rating outlook is “Stable”.

(b) Kazakhstan business environment

The Company‟s operations are primarily located in Kazakhstan. Consequently, the

Company is exposed to the economic and financial markets of the Republic of

Kazakhstan which display characteristics of an emerging market. The legal, tax and

regulatory frameworks continue its development, but are subject to varying

interpretations and frequent changes which together with other legal and fiscal

impediments contribute to the challenges faced by entities operating in the Republic

of Kazakhstan. The financial statements reflect management‟s assessment of the

impact of the Republic of Kazakhstan business environment on the operations and the

financial position of the Company. Actual business environment may differ from the

management‟s assessment.

2 BASIS OF ACCOUNTING

(a) Statement of compliance

These financial statements have been prepared in accordance with International

Financial Reporting Standards (“IFRSs”).

(b) Basis of measurement

These financial statements are prepared based on historic (primary) cost, except for

machinery and equipment and embedded financial instruments, accounted at the

revalued amount.

3 FUNCTIONAL AND REPRESENTATION CURRENCY

The national currency of the Republic of Kazakhstan is the Kazakh tenge (“KZT”),

which is the Company‟s functional currency and the currency in which these

financial statements are presented. All financial information presented in KZT,

unless otherwise specified, has been rounded to the nearest thousand.

4 USE OF ESTIMATES AND JUDGMENTS

The preparation of financial statements in conformity with IFRSs requires

management to make judgments, estimates and assumptions that affect the

application of accounting policies and the reported amounts of assets, liabilities,

income and expenses. Actual results may differ from those estimates.

Estimates and underlying assumptions are reviewed on an ongoing basis. Revisions

to accounting estimates are recognised in the period in which the estimates are

revised and in any future periods affected.

Information about critical judgments in applying accounting policies that have the

most significant effect on the amounts recognised in the financial statements is

included in the Note 6 - Property, plant and equipment.

Information about assumptions and estimation uncertainties that have a significant

risk of resulting in a material adjustment within the next financial year is included

in the following notes:

Note 6 - Property, plant and equipment;

Note 14 – Bonds.

Measurement of fair values

A number of the Company‟s accounting policies and disclosures require the

determination of fair value, for both financial and non-financial assets and

liabilities.

42

A number of the Company‟s accounting policies and disclosures require the

determination of fair value, for both financial and non-financial assets and liabilities.

The Company has an established control framework with respect to the measurement

of fair values. As a part of the control framework the Company‟s Financial Director

has overall responsibility for overseeing all significant fair value measurements,

including Level 3 fair values, and reports directly to the management of the

Company.

The Finance Department specialists regularly review significant unobservable inputs

and valuation adjustments. If third party information, such as broker quotes or pricing

services, is used to measure fair values, then the Finance Department specialist

assesses the evidence obtained from the third parties to support the conclusion that

such valuations meet the requirements of IFRS, including the level in the fair value

hierarchy in which such valuations should be classified.

When measuring the fair value of an asset or a liability, the Company uses market

observable data as far as possible. Fair values are categorised into different levels in a

fair value hierarchy based on the inputs used in the valuation techniques as follows.

Level 1: quoted prices (unadjusted) in active markets for identical assets or liabilities.

Level 2: inputs other than quoted prices included in Level 1 that are observable for

the asset or liability, either directly (i.e. as prices) or indirectly (i.e. derived from

prices).

Level 3: inputs for the asset or liability that are not based on observable market data

(unobservable inputs).

If the inputs used to measure the fair value of an asset or a liability might be

categorised in different levels of the fair value hierarchy, then the fair value

measurement is categorised in its entirety in the same level of the fair value hierarchy

as the lowest level input that is significant to the entire measurement.

The Company recognises transfers between levels of the fair value hierarchy at the

end of the reporting period during which the change has occurred.

Further information about the assumptions made in measuring fair values is included

in the following notes:

Note 6 - Property, plant and equipment;

Note 14 - Bonds;

Note 24 – Fair value and risks management.

5 OPERATING SEGMENTS

The management of the Company considers the Company as one segment, which

uses out the wagons and renders the services of routine maintenance and freight

forwarding. The Company‟s assets are registered in Kazakhstan. All revenues of

the Company are generated in Kazakhstan. The Company‟s management analyses

the segment performance based on statement of profit or loss and other

comprehensive income prepared in accordance with IFRS.

The major client of the Company in 2014 and 2013 is Tengizchevroil LLP.

Information on sales is disclosed in Note 18.

6 PROPERTY, PLANT AND EQUIPMENT

43

Depreciation expense of KZT 5.631.469 thousand (2013: KZT 5.414.745 thousand)

has been charged to cost of sales and KZT 59.323 thousand to administrative

expenses (2013: KZT 63,088 thousand).

Notes to the financial statement

In thousands of tenge

Machinery and

equipment Other Total

Cost:

At 1 January 2013 110.433.517 343.974 110.777.491

Additions 10.914.000 3.579 10.917.579

Disposal (121.497) (64.045) (185.542)

At 31 December 2013 121.226.020 283.508 121.509.528

Additions 11.696.254 40.457 11.736.711

Disposal (131.725) (32.262) (163.987)

At 31 December 2014 132.790.549 291.703 133.082.252

Accumulated depreciation and impairment:

At 1 January 2013 (16.714.214) (57.994) (16.772.208)

Depreciation charge (5.414.119) (63.714) (5.477.833)

Disposal 30.978 22.367 53.345

At 31 December 2013 (22.097.355) (99.341) (22.196.696)

Depreciation charge (5.630.977) (59.815) (5.690.792)

Disposal 34.696 13.241 47.937

At 31 December 2014 (27.693.636) (145.915) (27.839.551)

Net carrying amounts

At 1 January 2013 93.719.303 285.980 94.005.283

At 31 December 2013 99.128.665 184.167 99.312.832

At 31 December 2014 105.096.913 145.788 105.242.701

(a) Revaluation of machinery and equipment

Machinery and equipment are mainly represented by the railway wagons and gondola

wagons. The latest revaluation of the Company‟s machinery and equipment was

performed as at 31 December 2010 by an independent appraiser, American Appraiser

LLP. The fair value was determined based on the analysis of the CIS secondary

market, which was classified as an active secondary market by the appraiser.

As at 31 December 2014 the Company analysed the market value of the machinery

and equipment (or property, plant and equipment represented mostly by the different

types of wagons). As there was no active secondary market for relatively large lots of

wagons which was due to high uncertainty in the Russian market at the end of 2014,

the Company decided to abandon the comparative approach to value the wagons and

used the cost method. The Company requested prices on the wagons similar to those

used by the Company from two major suppliers, Scientific and Production

Corporation UralVagonZavod OJSC and Altaiwagon OJSC, and adjusted these prices

for physical depreciation to present the current condition of the wagon rolling stock.

Based on results of the analysis the Company made decision not to revalue the wagon

rolling stock, as its carrying amount did not materially differ from fair value as at the

valuation

As at 31 December 2014 the carrying amount of machinery and equipment would

have been KZT 92,482,901 thousand (2013: KZT 82,774,988 thousand), if machinery

and equipment had been recognized at cost less the accumulated depreciation and

impairment.

(b) Security

As at 31 December 2014 the machinery and equipment with net carrying amount of

KZT 63.411.094 thousand (2013: KZT 54,999,950 thousand) are subject to a

registered debenture to secure bank loans and borrowings (see Note 13); machinery

and equipment with net carrying amount of KZT 18.959.645 thousand (2013: KZT

20,116,951 thousand) are subject to a registered debenture to secure the Company‟s

bonds (see Note 14). Moreover, as at 31 December 2014 the machinery and

equipment with net carrying amount of KZT 6.467.714 thousand (2013: KZT

6,868,722 thousand) are subject to a registered debenture to secure the loans and

borrowings received by Center of Wagon Service – Yeskene LLP, an enterprise

under common control of the ultimate controlling party of the Company.

Leased property, plant and equipment

Machinery and equipment are mainly represented by the railway wagons and

gondola wagons. Machinery and equipment include wagon acquired under the

finance lease contracts signed with banks, with net carrying amount of KZT

9.551.123 thousand (2013: KZT 10,033,943 thousand). The wagons are pledged as

security of the respective finance lease contracts (see Note 15).

7 TRADE AND OTHER RECEIVABLES

44

As at 31 December 2014 the trade receivables of the Company‟s major customer -

Tengizchevroil LLP – accounted for 32% of the total trade receivables (2013:

36%).

The movement in the provision for doubtful debt during the years ended 31

December was as follows:

As at 31 December 2014 the trade receivables not overdue and not impaired

amounted to KZT 6.776.374 thousand (2013: KZT 4,921,892 thousand).

As at 31 December the Company‟s trade receivables were denominated in the

following currencies:

Notes to the financial statement

In thousands of tenge 2014 2013

Trade receivables 6.518.694 4.664.032

Other receivables from a related party (Note 26) 262.000 262.024

Less provision for doubtful debts (4.320) (4.164)

6.776.374 4.921.892

In thousands of tenge 2014 2013

Provision for doubtful debt at the beginning of the year (4.164) (37.042)

Provision for the year (4.074) (335)

Writes-off 3.918 33.213

Provision for doubtful debt at the end of the year (4.320) (4.164)

In thousands of tenge 2014 2013

USD 2.600.371 2.047.230

KZT 4.102.407 2.686.276

RUR 73.596 188.386

6.776.374 4.921.892

The Company‟s exposure to credit risk related to trade receivables is disclosed in

Note 24.

As at 31 December 2013 other current assets included advances paid to TD

Azovobschemash CJSC and WagontradePlus LLC for procurement of wagons, which

were provided to the Company in 2014. As at 31 December 2014 there were no

advances paid for wagons.

As at 31 December the advances paid were as follows:

On 30 and 31 December 2014 the Company opened a deposit in USD in SB

Sberbank JSC in the total amount of KZT 3.282.300 thousand with the interest rate

6% per annum. The term of deposit matures on 1 April 2015.

During 2013 the Company opened deposits in USD and in KZT in ATF Bank JSC

for the total amount of KZT 1,292,942 thousand with the interest rates from 0.2-

3.66% per annum. The terms of the deposits vary from 3 to 12 months.

On 28 November 2013 the Company opened a deposit in USD in SB HSBC Bank

Kazakhstan JSC for the amount of KZT 1,003,701 thousand at the interest rate of

0.15%. The deposit matured on 20 February 2014. A bank deposit in SB HSBC

Bank Kazakhstan JSC as at 31 December 2013 is subject to a registered debenture to

secure the bonds obligations if the rolling stock appears to be insufficient as security

(see Note 14). However, the bank deposit is not restricted.

The Company's exposure to credit risk and interest rate risks and sensitivity analysis

for financial assets and liabilities are disclosed in Note 24.

10 CASH AND CASH EQUIVALENTS

45

The movements in the impairment allowance for the years ended 31 December were

as follows: Altyn Bank JSC has a right to set a limitations with respect to cash placed in the

banks, if the Company fails to observe the payments schedule of the principal or

interest on the loans of the International Finance Corporation. As at 31 December

2014 the total of such cash placed in Altyn Bank JSC (SB Halyk Bank of

Kazakhstan JSC) was KZT 260.211 thousand (2013: on accounts of BNP

PARIBAS (SUISSE) SA and ATF Bank JSC: 578.572 thousand) (see Note 13).

Bank accounts in SB Sberbank JSC in the amount KZT 65.563 thousand as at 31

December 2014 are subject to secure completion of obligations on a loan from

BNP PARIBAS (SUISSE) SA. However, cash on these accounts is not restricted.

In December 2014 the Company opened a deposit in KZT in Altyn Bank JSC for

the total amount of KZT 85.000 thousand with the interest rate 10% per annum.

The term of the deposit matured on 15 January 2015.

The Company‟s exposure to credit risk and interest rate risk and a sensitivity