Embed Size (px)

Citation preview

IIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIINEWFOLDER

Z_

m_

Name: _-_(_x_ 5l _

//

mmmmmmm

ml

mmm

m

/

/

IIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIII------

ECON 3113Spring 2009

FINAL EXAM STUDY GUIDE

When and Where

ECON 3113-004: Friday, May 15 at 4:30 PM, Neilson 251

Format

25 Multiple Choice Questions

• These will cover concepts and definitions from the entire course.

• They may require some quick calculations and/or mathematical formulae.

3 or4 Long Questions _l--_[_ll0r_/[jo,_ _oo[c• Mathematical and/or graphical analysis similar to previous midterm questions.

• Potential topics for mathematically focused problems .,o Perfect Competition- 011I_ll_(Hrl

o Utility maximization or cost minimization -- Qh_l/l_'Im

o Oligopoly (Cournot) with comparison to monopoly, perfect competition

• Potential topics for questions based primarily on graphical analysis

o Consumer choice with a policy application- t_10t_l'l£[

o Monopolistic competition.

o Externalities, Public Goods, Game Theory

Office Hours

• Tuesday, May 12 from 3:00 to 5:00

• Thursday, May 14 from 3:00 to 5:00

• Or by appointment

\

81

ECON 3113 -_ Catherine Tyler Mooney

Study Tios

* Set aside a few hours during the next couple of days to go through your notes and homework

to see what you might want to come see me about during office hours.

• If you haven't been studying with other students, start a study group now. You can often

explain things to each other as well or better than I can.

• Outline and organize (maybe recopy) your notes. Refer to the book or to your classmates'

notes to fill in areas that are unclear.

• Make yourself a practice test. Go through your notes, problem sets, the midterms, and the

book and write problems on a separate sheet of paper. Save it for a day or so and go back and

take it later. See where your weaknesses are.

82

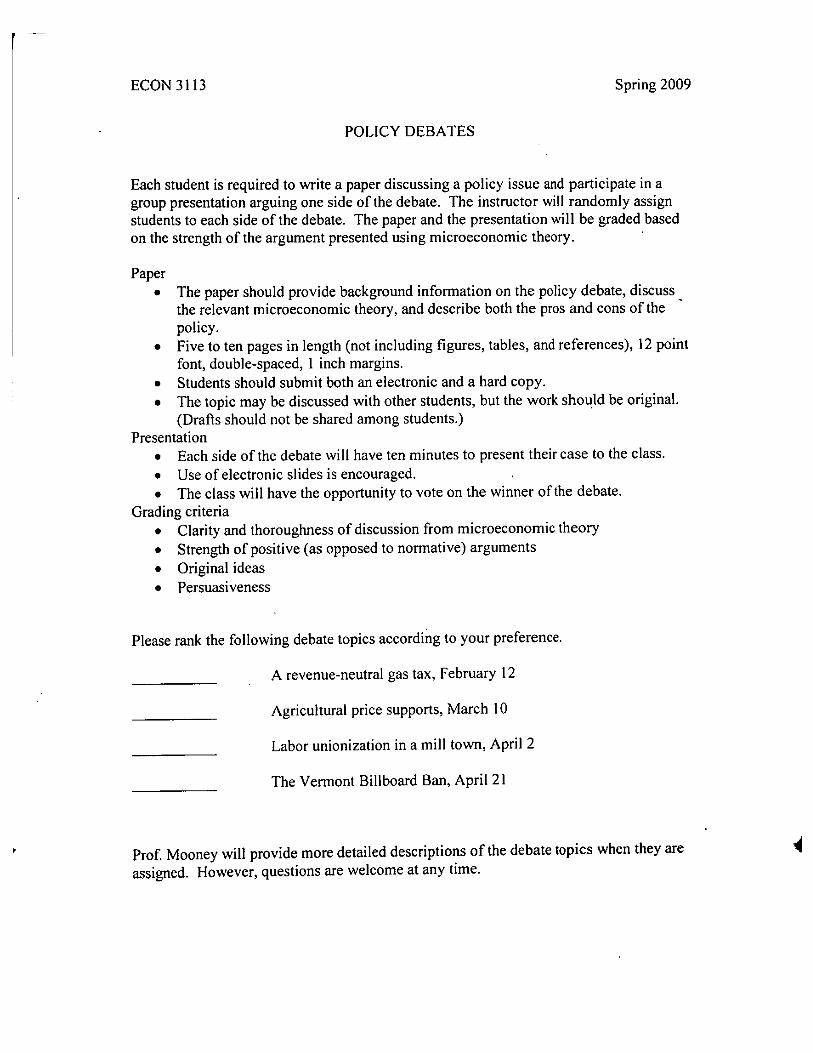

ECON 3113 Spring 2009

POLICY DEBATES

Each student is required to write a paper discussing a policy issue and participate in agroup presentation arguing one side of the debate. The instructor will randomly assignstudents to each side of the debate. The paper and the presentation will be graded basedon the strength of the argument presented using microeconomic theory.

Paper• The paper should provide background information on the policy debate, discuss

the relevant microeconomic theory, and describe both the pros and cons of thepolicy.

• Five to ten pages in length (not including figures, tables, and references), 12 pointfont, double-spaced, 1 inch margins.

• Students should submit both an electronic and a hard copy.• The topic may be discussed with other students, but the work should be original.

(Drafts should not be shared among students.)Presentation

• Each side of the debate will have ten minutes to present their case to the class.• Use of electronic slides is encouraged.• The class will have the opportunity to vote on the winner of the debate.

Grading criteria• Clarity and thoroughness of discussion from microeconomic theory• Strength of positive (as opposed to normative) arguments• Original ideas• Persuasiveness

Please rank the following debate topics according to your preference.

A revenue-neutral gas tax, February 12

Agricultural price supports, March 10

Labor unionization in a mill town, April 2

The Vermont Billboard Ban, April 21

Prof. Mooney will provide more detailed descriptions of the debate topics when they areassigned. However, questions are welcome at any time.

P Practice Problems for ECON 3113, Honors ClassDirections: Divide up into groups of three or four. Each group starts with adifferent problem. Once all groups have completed their assigned problem,representatives from the groups go to the board to explain and discuss their work.

1. A monopolist has total costs given by C(Q) = 300 + 20Q + 2Q2and faces a demandcurve given by P(Q) = 140 - 2Q.a. What price should it charge? What quantity will it sell? How much will total profits

be? Ib. What _imount of production is socially optimal? What is the deadweight loss

associated with producing at the monopolist's quantity rather than at the socialoptimum?

2. You are the manager of an amusement park. You face a constant MC = 0 as customersride your rides. There are two types of customers. Avid customers have demand QA=I0 - 2P, and general customers have demand Q = 5 - P. Assume there are 100customers of each type.

_x_-_ a. You only want avid customers to enter your park. How much should you chargethem each to enter and how much should you charge them for each ride in order to

_4 _ maximize profits? What will total profits be?0x b. You no longer care which type of customer enters your park, and you start to thinkit might be possible to increase your total profits with a different pricing scheme. Isthat possible? If so, what is your optimal pricing scheme? If not, why not?

c. Your theme park is a hit and 300 more avid customers enter the market.What is your optimal pricing scheme now? (Make sure to show that it isoptimal.)

3. Homecountry has a monopoly on groceries in the town of Norbert. Its customers fallinto two broad groups. The first sort of customer is a relatively small group of high-income folks with a high-powered, fast-paced lifestyle. Their demand for HC'sproducts is given by the function P = 100 -.5Qt (where Q is a generic good, "HCgroceries" bought per week, and P is its price in dollars.) A second group is composedof large, young families. They're in the midst of family formation, so they spend lesstime working in the labor market. Incomes are lower (but they need lots ofgroceries!). This group's demand curve is given by the function P = 50 -. 125Q2.Assume that HC can produce groceries at a marginal cost ofMC = 12 + .2Q.

Now a clever OU economics study group suggests the follow idea to Homecountry:"Why not publish ads in the local paper giving a discount on HC? But require thatthe ads be cut out and brought to the store. The fast-track folkswith lots of moneywon't bother - they don't have time, or the need, to cut out coupons. But the momswill. So using this approach, we can charge a different price to each group!"

Homecountry buys the approach, which involves maximizing profits by charging adifferent price to each group.

a) What is the price elasticity of demand in each submarket? Which group do youexpect to pay a higher price?

b) What price will be charged to each group? How much will each purchase aweek?

Who benefits from this pricing strategy - fast-track folks, big families, Homecountry?How do you know? b 0Aat.1

4. Bertrand and Cournot Oligopolies

0x_a. Two firms compete in an oligopolistic setting withMC = 0. Each firm's demand is_ n_3_ given by Q/= 60 - 6*Pi + 3"P2 and Q2 = 60 - 6*P2+ 3*Pt. What is the NashEquilibrium price and quantity for each firm? What will each firm's profits be?

b. Two firms compete in an oligopolistic setting. Market demand is given by P =

f,._,t,_k 60 - Q, where Q is the total quantity produced bythe two firms. Each firm'smarginal cost is given by: MC_ = $4, MC2 = $2. What is the Nash Equilibriumquantity for each firm? Also give the market price and each firm's profits.

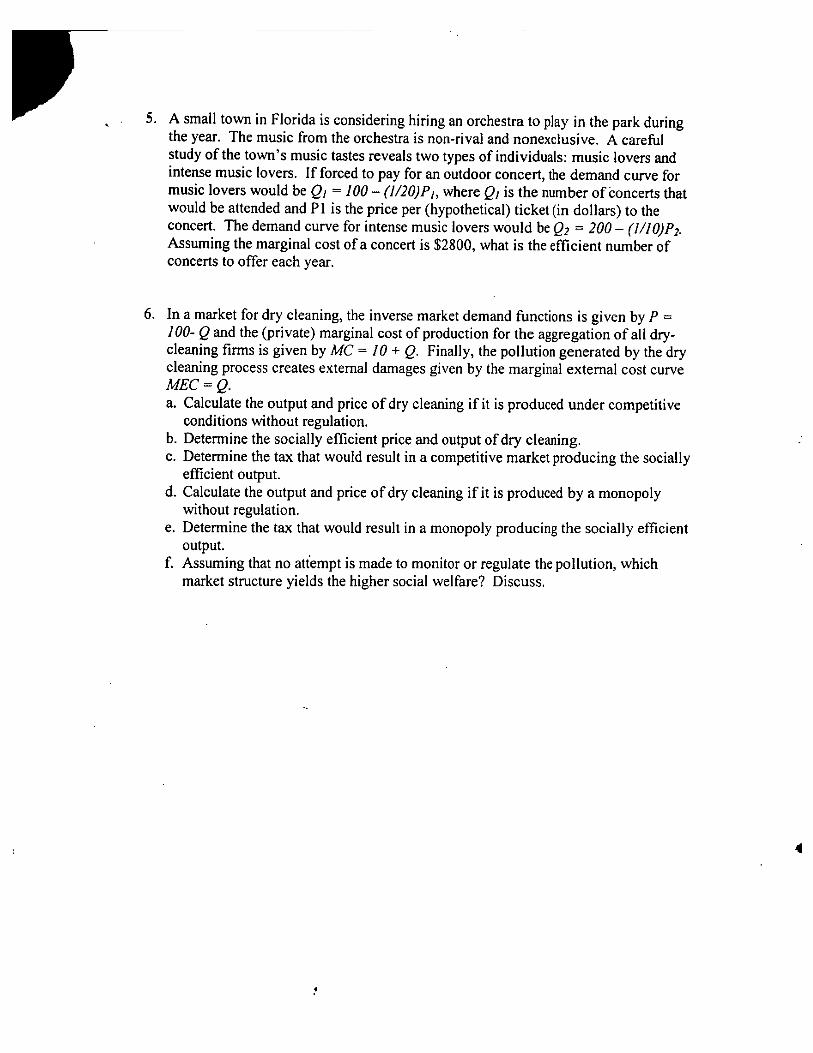

5. A small town in Florida is considering hiring an orchestra to play in the park duringthe year. The music from the orchestra is non-rival and nonexclusive. A carefulstudy of the town's music tastes reveals two types of individuals: music lovers andintense music lovers. If forced to pay for an outdoor concert, the demand curve formusic lovers would be QI = 100 - (1/20)P_, where Q/is the number of concerts thatwould be attended and P 1 is the price per (hypothetical) ticket (in dollars) to theconcert. The demand curve for intense music lovers would be Q2 = 200 - (1/10)P_.Assuming the marginal cost of a concert is $2800, what is the efficient number ofconcerts to offer each year.

6. In a market for dry cleaning, the inverse market demand functions is given by P =100- Q and the (private) marginal cost of production for the aggregation of all dry-cleaning firms is given by MC = 10 + Q. Finally, the pollution generated by the drycleaning process creates external damages given by the marginal external cost curveMEC = Q.a. Calculate the output and price of dry cleaning if it is produced under competitive

conditions without regulation.b. Determine the socially efficient price and output of dry cleaning.c. Determine the tax that would result in a competitive market producing the socially

efficient output.d. Calculate the output and price of dry cleaning if it is produced by a monopoly

without regulation.e. Determine the tax that would result in a monopoly producing the socially efficient

output.f. Assuming that no att'empt ismade to monitor or regulate the pollution, which

market structure yields the higher social welfare? Discuss.

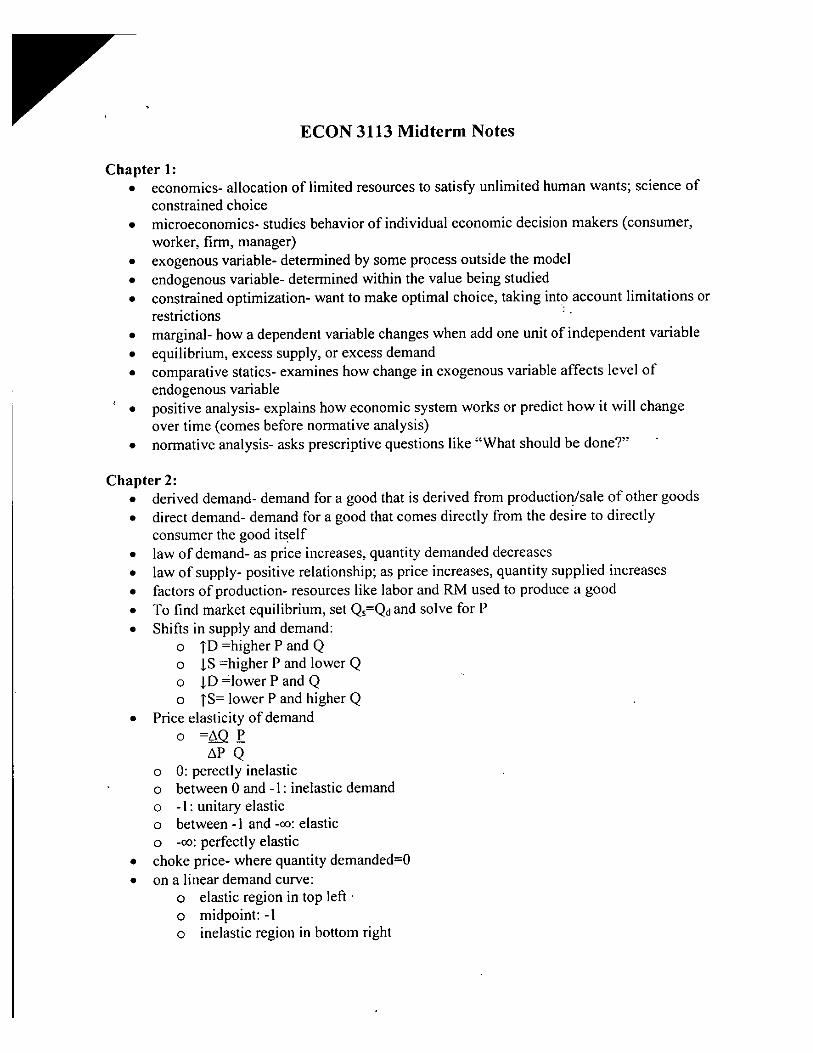

ECON 3113 Midterm Notes

Chapter 1:• economics- allocation of limited resources to satisfy unlimited human wants; science of

constrained choice• microeconomics- studies behavior of individual economic decision makers (consumer,

worker, firm, manager)• exogenous variable- determined by some process outside the model• endogenous variable- determined within the value being studied• constrained optimization- want to make optimal choice, taking into. account limitations or

restrictions• marginal- how a dependent variable changes when add one unit of independent variable• equilibrium, excess supply, or excess demand• comparative statics- examines how change in exogenous variable affects level of

endogenous variable' • positive analysis- explains how economic system works or predict how it will change

over time (comes before normative analysis)• normative analysis- asks prescriptive questions like "What should be done?"

Chapter 2:• derived demand- demand for a good that is derived from production/sale of other goods• direct demand- demand for a good that comes directly from the desire to directly

consumer the good itself• law of demand- as price increases, quantity demanded decreases• law of supply- positive relationship; as price increases, quantity supplied increases• factors of production- resources like labor and RaMused to produce a good• To find market equilibrium, set Qs=Qaand solve for P• Shifts in supply and demand:

o TD =higher P and Qo _.S=higher P and lower Qo ,LD--lower P and Qo TS= lower P and higher Q

• Price elasticity of demando =__._QP

AP Qo 0: perectly inelastico between 0 and -1: inelastic demando -1: unitary elastico between-1 and-oo: elastico -oo:perfectly elastic

• choke price- where quantity demanded=0• on a linear demand curve:

o elastic region in top left.o midpoint: -1o inelastic region in bottom right

,, elasticity with revenueo for inelastic: ifPT, Revenue1"o for elastic: if PI", Revenue_

• Determinants of Price Elasticityo more broad: more inelastic, b/c no substituteso brand level: more elastico when there are good substitutes: elastico when expenditure (% of income) is large: elastico when a necessity: inelastico luxuries: elastico long period of time: elastic

• Inqome Elasticity of Demando =AQ _I

AI Qo >1: income elastico between 0 and 1: income inelastico <0: inferior good (as income increases, demand for good decreases)

• Cross-Price Elasticity of Demando :0:P_j

APj Qio If>0: goods are substituteso If<0:goods are complements

• for most goods, long-run demand is more elastic than short-run, but...• durable goods, long-run demand is less elastic (more inelastic) than short-run• usually long-run supply is more elastic, but...recycled/resold goods: long-run supply is

less elastic• Deriving Demand

o Q*= a-bP*o b= -E(Q*/P*), where E is price elasticity of demando a= (1-E)Q*

• if increase supply:o price will barely reduce if elastico price will drop a lot if inelastic

Chapter 3:• Assumptions about consumer preferences:

o preferences are complete- able to rank any two basketso preferences are transitive- A>B, B>C, then A>Co more is better (quadrant thing)

• ordinal rankings-just give order of rankings• cardinal rankings- give information about intensity of preferences• marginal utility- change in utility per change in consumption

o slope of line that is tangent to utility function at that point• principle of diminishing marginal utility- after some point, as consumption of a good

increases, the marginal utility of that good will begin to fall• marginal utility can be negative

• when looking at MUx or MUy, hold the other good constant• indifference curves are the utility function reduced to 2-D• Indifference map properties:

o when both marginal utilities for x and y are positive, the ICs have a negative slopeo ICs can't intersecto each basket on only one ICo ICs are not "thick"

• marginal rate of substitution (MRS): consumer's willingfiess to substitute one good foranother

o when 2 goods have positive MUs, the trade-off is the slope of the ICo ex: if slope of IC at point A is -5, consumer would be willing to trade 5 units ofy

to gain 1 unit ofxo MRS is the negative slope of the IC

• -Ay/Ax = MU×/MUy=MRS• For many (but not all) goods, MRS diminishes as amount ofx increases-->IC must be

bowed in toward the origin (therefore, if MRS is increasing, will be concave to origin)• perfect substitutes- MRS of one good for the other is constant--)lCs are straight

o ex: always substitute 2 pancakes for 1 waffle: U= P+2W, so MUp=I and MUw=2• perfect complements- two goods tl_e consumer always wants to consume in fixed

proportions +o utility function will then be min(x,y)

• Cobb-Douglas utility function: U=Axay 13• Quasi-linear utility functions- linear in at least one of the good consumed

o U=v(x) + by, where v(x) is a function that increases in x

Chapter 4:• budget constraint- defines the set of baskets than a consumer can purchase with a limited

amount of incomeo permits consumer to purchase baskets both on and inside budget lineo Pxx+Pyy_<I

• budget line- indicates all combos ofx and y that consumer can purchase if spend allavailable income on the 2 goods

o Pxx+Pyy=Io slope is Ay/Ax, or -Px / Py

• tells us how many units of good on vertical axis a consumer must give upto gain an additional unit of good on x-axis

• increase in income shifts the budget line outward• change in price rotates the budget line along that good's axis

o price Trotates line inwardo price $ rotates line outward

• optimal choice- choice of a basket of goods that both maximizes utility, while allowingconsumer to live within budget constraint

o max U(x,y) subject to Pxx + Pyy < Io at optimal basket, budget line is just tangent to the ICo tangency condition: MUx/MUy = Px/Pyo or MUx/Px = MUy,/Py

• expenditure minimization problem- will minimize total spending while achieving a givenlevel of utility

o use budget constraint and tangency condition--)solve the tangency condition forone variable--)plug that into budget constraint--)solve for amounts of each good

• comer point- solution to optimal choice problem where some good s not being consumedat all, so the optimal choice lies on one axis

o consumer would like to continue substituting one good for the other, buteventually no further substitution is possible

o if get negative answer when solving optimal choice problem: comer solution• then spend all income on one good that comes back with positive answer

• composite good- good that represents the collective expenditures on every other goodexcept the commodity being considered

• revealed preference- can learn about consumers' ranking of baskets by observing howchoices change as prices and incomes vary

o some are strongly preferred, and some are just at least preferredo choices don't always maximize utility because consumers aren't consistent

• when get that A is strongly preferred to B and B is strongly preferred to AChapter 4 Applications:

• Coupons and Cash Subsidies:o cash would shift entire budget constraint outwardo coupons, such as food stamps, would just shift it outward for foodo depending on where consumers' ICs are, may or may not prefer one program over

the other• Joining a Club:

o reduce income if join a club, so less money can be spent on AOG, but price of theother good probably reduces, so have to see whether basket chosen before joiningthe club is still tangent to the IC after joining the club; if not: there is a differentoptimal choice

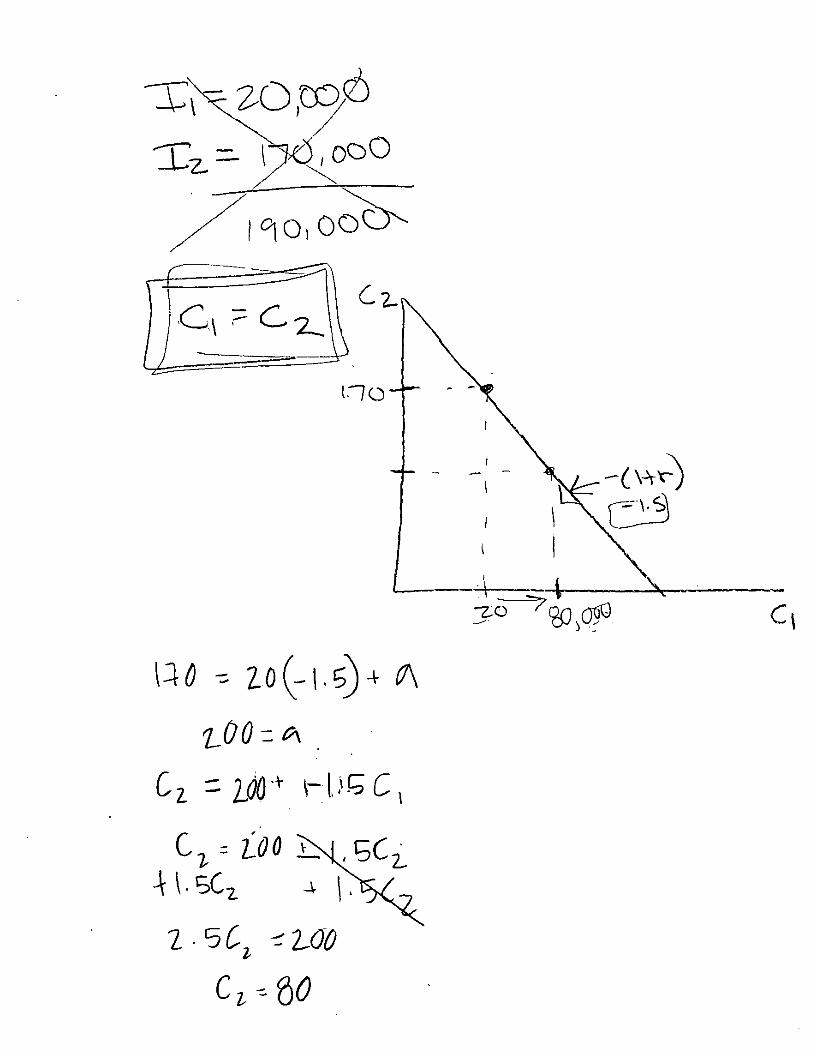

• Borrowing and Lending:o slope of the budget line is -(l+r) where r is the interest rateo every time you increase your consumption this year by $1 (moves to the right on

the budget line), needs to decrease consumption next year (move down the budgetline) by (l+r) dollars

o must find intercepts of budget line:• if spend nothing this year and puts I1 in the bank, next year he can spend

I2 + Ii(1 +r)-)vertical intercept on consumption next year axis• if borrow maximum amount possible this year and save nothing, can

spend up to I_ + I2/(1+r)---)horizontal intercept on consumption this yearaxis

• Quantity Discounts:o budget line without discount is normalo budge line with discount is in 2 segments where first part is parallel but becomes

less steep after a certain quantity due to discount

Chapter 5:

• price consumption curve- connects all baskets that are optimal as the price of foodchanges (holding price of other good and income constant)

o take those points and plot them on demand curve with quantity on x-axis andprice on y-axis--)usually causes downward-sloping demand curve

o "willingness to pay" for an addition unit falls as buy more and more• income consumption curve- connects all baskets that are optimal as income changes

(keeping prices constant)o increase in income results in outward shift of demand curve

• Engel curve- graph relating the amount of good consumed to level of income (Q on x-axis and I on y-axis)

o normal good: positive slope on Engel curve; purchase more as income increases• income elasticity of demand is positive

o inferior good: negative slop on Engel curve; purchase less as income increases• can slope positive for certain segment of income where it is a normal

good, then negative slope where it is an inferior good• income elasticity is negative

• Deriving Demand Equation Algebraicallyo If Pxx + Pyy = I and MUx/MU = Px/Py, then solve tangency condition for

y-)substitute that into the budget constraint"-)solve for x-)demand curveo Ex: ifU(x,y)=xy, then x=I/(2Px)

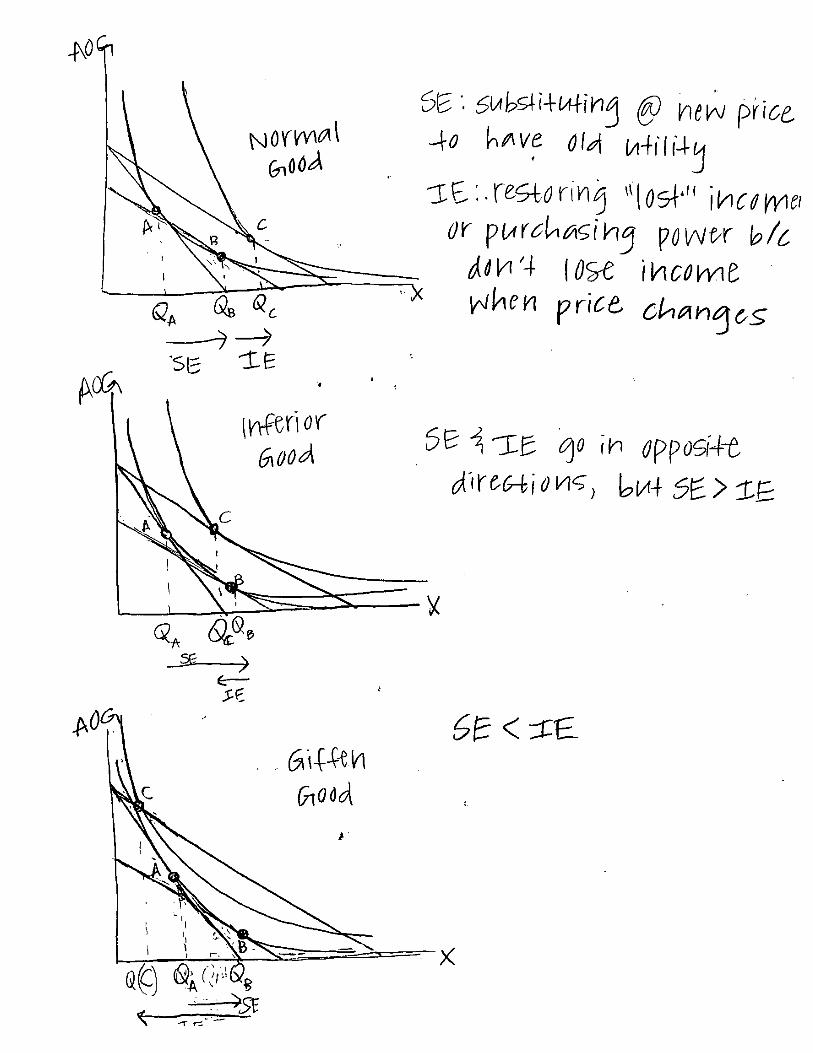

• As income increases, demand more'->normal good• substitution effect- change in the amount of a good that would be consumed as the price

of that good changes, holding constant all other prices and the level of utilityo quantity consumer would purchase after the price change to achieve same utilityo on graph: moving from A to B

• income effect- change in amount of a good that a consumer would buy as purchasingpower changes

o consumer realizes higher or lower level of utilityo on graph: moving from B to C (where C is final basket)o "restoring" the "lost" income because income doesn't fall when price falls, so

level of utility increases• Steps for Substitution Effect:

1. Find initial basket with initial prices (A)2. Find final basket with new prices and new budget line (C)3. Find decomposition basket (B): draw a budget line parallel to the new one, but

that is tangent to original utility curve• decomposition basket must (1) lie on original IC along with A, but must

be at point where decomposition budget line is tangent to IC"-)SE will be difference between A and B

• Steps for Income Effect:o IE is the difference between B and C

• For normal goods, SE and IE work in the same direction (ABC on graph when price1);(CBA when price]')

• For inferior goods, SE and IE work in opposite directions, but SE>IE (ACB on graphwhen price,t); (BCA when priceT)

• For Giffen goods, SE and IE work in opposite directions, but IE>SE (CAB on graphwhen price,t); (BAC when priceT)

o demand curve would be upward sloping because quantity demanded decreases asprices decrease

• IE with quasi-linear function is 0 wheli parallel along y-axis• consumer surplus- difference between maximum amount consumer is willing to pay for a

good and the amount he must actually pay for a good in the marketo area between demand curve and the horizontal line at market price

• compensating variation- measure of how much money a consumer would be willing togive up after a reduction in the price of a good to be just as well offas before the pricedecrease

o difference in income necessary to buy basket A at initial price and B as new price(B is at a point where a line parallel to the final budget line is tangent to initial IC)

o if price of good on y-axis is 1--)difference between those 2 budget line's verticalintercepts

• equivalent variation- measure of how much additional money a consumer would needbefore a price reduction to be as well off as after the price decrease

o difference in income necessary to buy basket A at initial price and basket E (E isat a point where a line parallel to the initial budget line is tangent to final IC)

o if price of good on y-axis is 1-)difference between that higher budget line parallelto the original and the original

• with quasi-linear functions: CV = EV, because there is no income effect; also = to changein consumer surplus

• change in area under the demand curve will not exactly measure either CV or EV whenIE is not 0

• market demand- horizontal sum of the demands of individual consumerso demand curves must be in normal form (Q=)o pay attention to reservation prices where some consumers may not demand

anything at a certain price• network externalities- amount of good demanded depends on number of other consumers

who purchase the goodo positive: consumers' demand increases when # of other consumers increaseso negative: consumers' demand increases when # of consumers decreases

J_c • bandwagon effect- positive network externality

o 2 demand curves (each with different number of consumers in market wheredemand with more consumers is farther out than initial)

I" __ o connect 2 points that lie on each demand curve• pure price effect is the difference in Q from A to B (an increase) where A[ : _$_. iI) _,a (_A"_ is quantity demanded on Is' demand curve and B lies on that curve as well,O, Q_ Q o but at the lower price equal to C

0_ /_ • bandwagon effect is the increase in Q from B to C where C is the point on- _" 6 the 2 nddemand curve after there are more consumers• snob effect- negative network externality

o 2 demand curves (each with different number of consumers in market, but

__q.o demand with more consumers is below initial demand)

connect 2 points that lie on each demand curve

QA%- : 5nob e£-cec4

• pure price effect is the large increase from A to B on same initial demandcurve by at lower price = to C's price on lower demand curve

• snob effect is the decrease in quantity demanded from B to C, where theycould be connected by a horizontal line

• leisure = 24 hours, labor=24 -L, where L is leisure hourso Income will be w(24-L)o For any wage rate, the slope of the budget line is -wo As wage rate rises, # of leisure hour falls, but eventually consumer begins to

increase his amount of leisure--)depicted by backward bending supply curve• Substitution effect on labor supply is positive--consumer substitutes more

of the composite good for leisure, leading to less leisure and more labor• Income effect on labor supply is negative--leads to more leisure and less

labor, because leisure is a normal good• On lower region of labor supply curve, SE>IE, so it is upward-sloping, but

on upper region IE>SE, so it is downward-sloping \ o_,p. C054 o4" 1¢.i5ut¢- _/

Chapter 6:• inputs/factors of production- resources, such as labor, capital equipment, and raw

materials that are combined to produce finished goods• output- amount of good or service produced by a firm• production function tells us maximum quantity of output the firm can produce given a

quantity of inputs• production set- points on or below the production function (feasible combinations)• technically inefficient- points below a production function; getting less output from its

labor than it could• technically efficient- on the production function; producing as much output as it possibly

ca, given amount of labor it employs• labor requirements function- indicates the minimum amount of labor required to produce

a given amount of output (ex: if Q=',/L, then L=Q 2)• total product functions- total production function with a single input• increasing marginal returns to labor- region along total product function where output

rises with additional labor at an increasing rateo due to gains from specialization of labor

• first increasing marginal retums--)decreasing marginal returns (output increasing atdecreasing rate)--)diminishing total returns (where total product function is downwardsloping)

• average product of labor- avg. amount of output per unit of labor (=Q/L)• marginal product of labor- rate at which total output changes as quantity of labor the firm

uses is changed (=AQ/AL)• Relationship between Marginal and Average Product

o when AP is increasing, MP>APo when AP is decreasing, MP<APo when AP neither increases nor decreases, AP is at its minimum, MP=APo i.e. if average height in class increases from 5'5" to 5'9", you know that the

person added, (the marginal product) is > than the average• total product hill- 3D graph that shows relationship between 2 inputs and output

• MPL= AQ/AL, holding K constant• MPK=AQ/AK, holding L constant• isoquant- "same quantity"; curve that shows all of the combinations of L and K that can

produce a given level of outputo downward sloping: shows the trade-off that a firm can substitute K for L and keep

its output unchanged• uneconomic region of production- region where isoquants are upward-sloping or

backward-bendingo there, at least one input has a negative marginal producto if want to minimize its production costs, a firm should never operate in this region

• economic region of production- region of downward-sloping isoquants• marginal rate of technical substitution of labor for capital (MRTS)- rate at which quantity

of capital can be reduced for every one unit of increase in the quantity of labor, holdingthe quantity of output constant

o tells both rate at which quantity K could be _ for every 1 unit 1'in quantity of Lo and rate at which quantity L could be/" for every 1 unit $ in quantity of Lo negative slope of isoquant drawn with L on horizontal axis and K on vertical

• diminishing marginal rate of technical substitution- MRTS decreases as quantity of laborincreases

• MRTS = MPL/MPK• Firm's Input Substitution Opportunities Graphically

o when production function offers limited input substitution opportunities, theMRTS changes substantially->isoquants are nearly L-shaped

o when production function offers abundant input substitution opportunities, theMRTS changes gradually-)isoquants are nearly straight lines

• elasticity of substitution- measure of how easy it is for a firm to substitute labor forcapital (=%A(K/L)/% zXMRTS)

o if it is close to 0, there is little opportunity to substitute between inputso if it is large, there is a substantial opportunity to substitute between inputso using 2 points and those points' K, L and MRTS

• Linear Production Function (perfect substitutes)o Q-- aL + bKo isoquants are straight lineso MRTS is constant--)any AMRTS=0, so the elasticity of substitution (a)=oo,

because they are perfect substitutes in production• Fixed-Proportions Production Function (perfect complements)

o Q= min(x, y)--take minimum of 2 #s in parentheseso isoquants are L-shapedo elasticity of substitutes =0o no flexibility in ability to substitute among inputs

• Cobb-Douglas Production Functiono Q=AL_K _o L and K can be used in variable proportionso elasticity of substitution on C-D is always 1

• Constant Elasticity of Substitution Production Functiono includes 3 previous special production functions

o elasticity of substitution (6) is between 0 and oo• returns to scale- tells us the % by which output will increase when all inputs are increased

by a given %o =(%Aquantity of outputs)/( %_quantity of all inputs)o increasing returns to scale- outputs increase by greater amounto constant returns to scale- outputs increase by same proportionate amount as inputso decreasing returns to scale- outputs increase by smaller proportionate amount than

inputs• returns to scale pertains to impact of increase in all input quantities, while marginal

returns pertains to impact of an increase in quantity of a single input, holding quantity ofother input constant

• technological progress- change in production process that enables a firm to achieve moreoutput from a given combination of inputs, or the same output from less inputs

o neutral: decreases amounts of L and K needed to produce a given output, withoutaffecting the MRTS

o labor-saving: MPK increases relative to MPL, so MRTS is less than before (slopeof the isoquant at that point is flatter)

o capital-saving: MPL increases relative to MPK, so MRTS is greater than before(slope of isoquant at that point is steeper)

Chapter 7:• explicit costs- involve a direct monetary outlay• implicit costs- costs thatdon't involve outlays of cash• opportunity cost- value of next best alternative that is forgone when another alternative is

choseno diff. opportunity costs for different decisions under different circumstanceso from firm's perspective, opportunity cost of using the productive services of an

input is the current market price of the input• economic costs- include opportunity cost; both explicit and implicit• accounting costs- explicit costs that have been incurred in the past• sunk costs- costs that have already been incurred and cannot be recovered• nonsunk costs- costs that are incurred only ifa particular decision is made• cost-minimization problem• long-run: can vary all inputs• short-run: cannot adjust the quantities of some of its inputs or reverse the consequences

of past decisions that it has made regarding those inputs• w=wage; r= price per unit of capital• TC= wL + rK• isocost lines- represent a set of combinations of labors and capital that have the same

total cost (TC) for the firmo slope is-w/r Io K-axis intercept is TC/r, and L-axis intercept is TC/w

• cost-minimizing point where isocost line is tangent to production functiono -MRTS = -w/ro or MPL/MPK= w/r

• for comer point solutions: MPI]W > MPK/r• increase in price of labor (w), firm with substitute capital for labor-)cost-minimizing

input of labor will go down• when w/r decreases, the firm uses more labor and less capital, so the tangency point

moves farther down the isoquant• in a fixed proportions function, an increase in the price of an input will leave the cost-

minimizing input quantity unchanged• expansion path- a line that connects the cost-minimizing input combinations as the

quantity of output varies, holding input prices constant• normal inputs- cost-minimizing quantity increases as firm produces more

output--)expansion path is upward sloping• inferior inputs- cost-minimizing quantity decreases as the firm produces more

output--)expansion path is downward slopingo both inputs can't be inferior

• labor demand curve- curve that shows how the firm's cost-minimizing quantity of laborvaries with the price of labor (use points from isocosts/isoquants and their wage andquantity of labor to plot demand curve)

• capital demand curve- how firm's cost-minimizing quantity of labor varies with the priceof capital (same process as labor demand curve)

• price elasticity of demand for labor- % change in cost-minimizing quantity of labor withrespect to a 1% change in the price of labor

o =(AL/Aw). (w/L)o low elasticity of substitution implies inelastic demand for laboro high elasticity of substitution implies elastic demar/d for labor

• price elasticity of demand for capital- % change in cost-minimizing quantity of capitalwith respect to a 1% change in price of capital

o -(AK/Ar) .(r/K)• variable costs vs. fixed costs• short run costs can be:

o variable and non sucks (output sensitive)o fixed and nonsunk (output insensitive, but avoidable if produce 0 output)o fixed and sunk (output insensitive and unavoidable)

• short-run cost minimization: optimal choice doesn't depend on a tangency condition,because amount of one input is fixed

o in short-run, a firm will operate with higher total costs than it could if could adjustall inputs fi'eely

Chapter 8:• long-run total cost curve- shows how total cost varies with output, holding input pries

fixed and choosing all outputs to minimize costs• a given % increase in both input prices leaves the c0st-minimizing input combination

unchanged, while the total cost curve shifts up by exactly the same percentageo ex: a 10% increase in both input prices shifts TC curve up by 10%

• long-run average cost is firm's cost per unito AC = TC/Q

• long-run marginal cost is rate at which long-run TC changes with respect to change inoutput

o MC=_TC/AQ• Relationship between long-run AC and MC

o ifAC is decreasing, then AC>MCo ifAC is increasing, then AC<MCo ifAC is neither increasing nor decreasing (at its min.) then AC=MC

• economies of scale- situation where AC decreases as output increaseso can rise due to specialization of laboro can result from need to employ indivisible inputs (an input available only in a

certain minimum size--)its quantity can't be scaled down as output goes to 0)• these lead to decreasing average costs, because can "spread" that cost over

more units as output increases• diseconomies of scale- where AC increases as output increases

o thought to occur because of managerial diseconomies (arise when given %increase in output forces firm to increase its spending on the services of managersby more than this production)

• minimum efficient scale (MES)- smallest quantity at which long-run AC curve attains itsminimum point-)where it crosses the long-run MC curve

o the larger the MES is, in comparison to overall market ales, the greater themagnitude of economies of scale

• Relationship of Economies of Scale with Returns to Scaleo if we have economies of scale, we have increasing returns to scaleo if'o/e have diseconomies of scale, we have decreasing returns to scaleo if AC stays the same as output increases, we have constant returns to scale

• output elasticity of total cost- % change in total cost per 1% change in outputo =(ATC/TC) / (AQ/Q), which can be rearranged to be MC/AC

• equal to ratio of marginal to average cost• short-run total cost curve- shows minimized total cost of producing a given quantity of

output when at least one input is fixedo sum of 2 components:

• total variable cost curve and total fixed cost curve--)vertical distancebetween STC and TVC is TFC

• when comparing short-run costs to long-run costs, on the long-run you stay on your long-run expansion path (LREP), but for the short-run your capital is fixed, so to remain on acertain isoquant, you will not operate on the LREP

• short-run average cost (SAC)- firm's total cost per unit of output when it has one or morefixed inputs

o SAC= STC/Qo SAC = AFC + AVC, where AFC is avg. fixed costs and AVC is avg. variable

COSTS

• AVC = TVC/Q and AFC = TFC/Q• short-run marginal cost (SMC)- slope of short-run total cost curve

o SMC = &STC/AQ• long-run average cost curve forms an "envelope" around the set of SAC curves

corresponding to diff. levels of output and fixed input

• a short-run average cost curve (SAC) doesn't generally reach its minimum at the outputwhere short-run and long-run ACs are equal, but possible for SAC curve to reach its rain.at output where SAC and LAC are equal

• economies of scope- total cost of producing given quantities of 2 goods in the same firmis less than the total cost of producing those quantities in two single-product firms

o TC(Qu, Q2) < TC(Qa, 0) + TC(0, Q2)• zeros on right side indicate that single-product firms produce positive

amounts of one good but none of the other• stand-alone costs of producing goods 1 and 2

o tells us "variety" is more efficiento exist if it is less costly for a firm to add a product to its product line given that it

already produces another product (ex: Coca-Cola then producing cherry Coke)• economies of experience- cost advantages that result from accumulating experiences; aka

learning by doingo workers improve performance by performing them over and over againo firms become more adept at handling materialso engineers perfect product designso results in:

• greater labor productivity (more output per unit of labor)• fewer defects• higher material yields (more output per unit of RM input)

• experience curve- relationship between AVC and cumulative production volume (thetotal amount of output that has been producer up until that point in time)

o AVC(N)= AN B• B is experience elasticity (% change in AVC per 1% increase in

cumulative volume)• N is the cumulative production volume

o slope tell us how much AVC goes down as a % of initial level when cumulativeoutput doubles

• slope = AVC(2N) / AVC(N)• smaller the slope, the "steeper" the experience curve

• economies of scale are shown by downward sloping AC curve, but economies ofexperience are shown by downward shift of AC curve

Chapter 9:• Perfectly competitive markets have 4 characteristics:

o industry is fragmented--many buyers and sellers; neither individual buyers'demand nor individual suppliers' supply can impact market price

o firms produce undifferentiated products--consumers perceive each product asidentical no matter who produces them

o consumers have perfect information about prices all sellers in the market chargeo industry is characterized by equal access to resources; all firms (current and

prospective) have access to same technology and inputs• Those 4 characteristics have 3 implications:

o sellers and buyers are "price takers" (from 1)

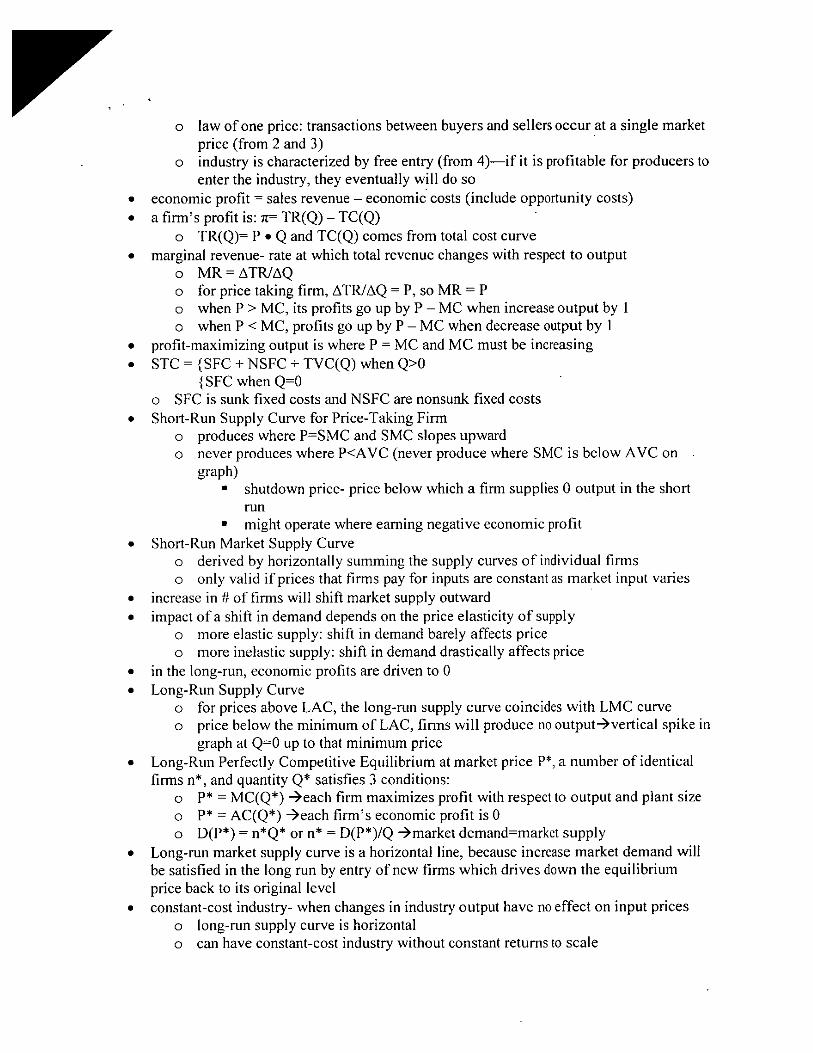

o law of one price: transactions between buyers and sellers occur at a single marketprice (from 2 and 3)

o industry is characterized by free entry (from 4)---if it is profitable for producers toenter the industry, they eventually will do so

• economic profit = sales revenue - economic costs (include opportunity costs)• a firm's profit is: rt= TR(Q)-TC(Q)

o TR(Q) = P • Q and TC(Q) comes from total cost curve• marginal revenue- rate at which total revenue changes with respect to output

o MR=ATR/AQo for price taking firm, ATR/AQ = P, so MR = Po when P > MC, its profits go up by P - MC when increase output by 1o when P < MC, profits go up by P - MC when decrease output by 1

• profit-maximizing output is where P = MC and MC must be increasing• STC = {SFC + NSFC + TVC(Q) when Q>0

{SFC when Q=0o SFC is sunk fixed costs and NSFC are nonsunk fixed costs

• Short-Run Supply Curve for Price-Taking Firmo produces where P=SMC and SMC slopes upwardo never produces where P<AVC (never produce where SMC is below AVC on

graph)• shutdown price- price below which a firm supplies 0 output in the short

run• might operate where earning negative economic profit

• Short-Run Market Supply Curveo derived by horizontally summing the supply curves of individual firmso only valid if prices that firms pay for inputs are constant as market input varies

• increase in # of firms will shift market supply outward• impact of a shift in demand depends on the price elasticity of supply

o more elastic supply: shift in demand barely affects priceo more inelastic supply: shift in demand drastically affects price

• in the long-run, economic profits are driven to 0• Long-Run Supply Curve

o for prices above LAC, the long-run supply curve coincides with LMC curveo price below the minimum of LAC, firms will produce no output->vertical spike in

graph at Q=0 up to that minimum price• Long-Run Perfectly Competitive Equilibrium at market price P*, a number of identical

firms n*, and quantity Q* satisfies 3 conditions:o P* = MC(Q*) --)each firm maximizes profit with respect to output and plant sizeo P* = AC(Q*) -->each firm's economic profit is 0o D(P*) = n'Q* or n* = D(P*)/Q --)market demand=market supply

• Long-run market supply curve is a horizontal line, because increase market demand willbe satisfied in the long run by entry of new firms which drives down the equilibriumprice back to its original level

• constant-cost industry- when changes in industry output have no effect on input priceso long-run supply curve is horizontalo can have constant-cost industry without constant returns to scale

• increasing-cost industry- when expansion of industry output increases the price of ninput; likely if use industry-specific inputs

o " long-run supply curve is upward sloping• decreasing-cost industry-increase in industry output can lead to a decrease in the price of

an inputo long-run supply curve is downward sloping

• free entry drives economic profit to 0: when profit opportunities are freely available to allfirms, economic profits will not last

• economic rent- economic return that is attributable to extraordinarily productive inputswhose supply is scarce

o ER = A-B, where• A -- maximum amount firm will pay for services of input• B = reservation value

• reservation value- return that the owner of an input could get by deploying the input in itsbest alternative use outside the industry

• producer surplus- difference between amount that a firm actually receives from selling agood in the marketplace and the minimum amount the firm must receive in order to bewilling to supply the good

o = to the area between the supply curve and the price, where the supply curve stopsat the minimum of the AC curve

o - total revenue- nonsunk costs• equal to economic profit when all costs are nonsunk, because economic

profit = total revenue - total costs• In the ldrlg run in perfectly competitive market...zero economic profit, so producer

surplus:- 0 also• Ifha'Je upward sloping LS curve (increasing-cost industry), economic rents are fully

captured by owners of the input; therefore, what would normally be producer surplus oreconomic profit is actually economic rent

Honors Intermediate Microeconomics _-S Spring 2009

Midterm Exam \0_-_ _:_0

Name:

Instructions: Please respond to the questions in the space provided. If you need extraspace, come to the front of the class for extra paper. This is a closed note, closed booktest. You have 75 minutes to complete the test, which has 58 total points. Allocate yourtime accordingly. Please make it clear which questions you do not choose. For fullcredit, you should show all of your work. Good luck.t

SHORTER QUESTIONS (Choose four of five, 7 points each.)

1. Microeconomics is the study of the allocation of resources in a world with unlimitedwants. What three outcomes of the perfectly competitive market model providecriteria for evaluating a market's allocation of resources?

/[ _ jr© ,_fo_4iv_ _,_ie_v_, _r_ P= ,L,,c,• .,_. L:,,,,,

._'_o ,,_(-_PrimO, re.¢-r.Cl_ie.m_vj,t,'qhd¢ -4.o4_ l 6¢l_l,4mer_

Adam Smith describesan "invisible hand" leading economic agentsto thiscompetitive market equilibrium, To what economic decisions is hereferring?

_)-.,rv_¢rk¢+:, l,_a-rt. S_pph.e.rg I,,'vtll e.._4er 4.he_.,.O_rO4_ncr_) ,:J -, _, _- . .. .m:x(mi_e__ ifl4t_r/udd l/Vl,,l_lfl _dOtqOU_lC _O_l-l'g _1"_ _o_f41ble.

rr°a_cer_ gro drire del,,v'l_ -.l-he, &_tlAil ;D,rit._., ,.,,,+,.r,.,," {,¢t& --Fro-+'_s-_ _n411 N re,_/_e£ -4 k_iwiv'v'_m d-.f4J,,ve.

(_on_i LAC CNrv-e-1,4/_&(¢ ll_gr'O _cdr_Ol4niC

s_+-,_g+,+_erofi4+:are t_o_ _ _girLieS WII $4dp/__.t:_ , c°°'?¢_'pdq¢..k_-k-_rieq_) _kt_ v_r ,.--,_,..4A,_rt,.,.x_/"Auil,lortl,,,,,,,,_11

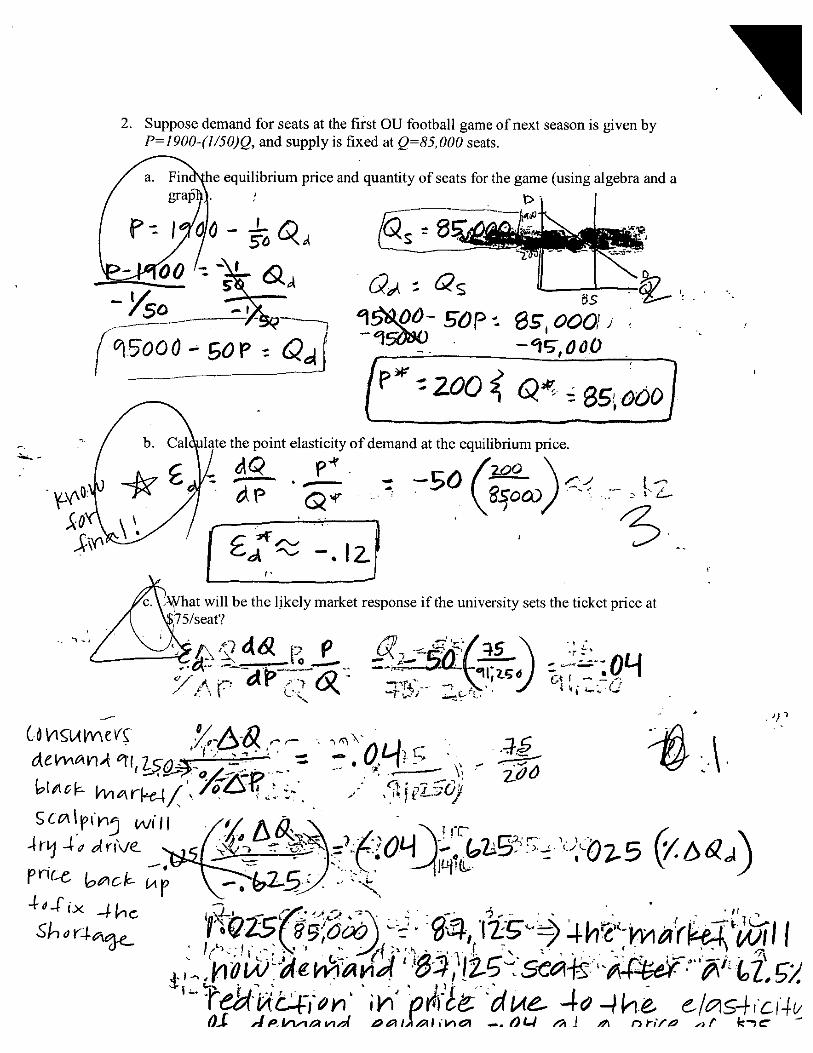

2. Suppose demand for seats at the first ou football game of next season is given byP=1900-(1/50)Q, and supply is fixed at Q=85, 000 seats.

:he equilibrium price and quantity of seats for the game (using algebra and a

" _ flate the point elasticity of demand at the equilibrium price.

"y--v_' :_ . " _ e co,_ _ ' I,_sooo) -"_ .-:Sz..

at Iwillbe thee" I IA_h " e likely market response if the university sets the ticket price at, /_ k_75/seat?

l -- .... I _ " , 0"- _" ; Za 0 _ ]

/'. \

% ./

,;: .'_o_ _=a_ "_,:!z_.:sc_: "_ -:''_'__Z'.g_._c-F-lam. ,1_p_g t_e_4a -4he. e..I,_s4,cl4_

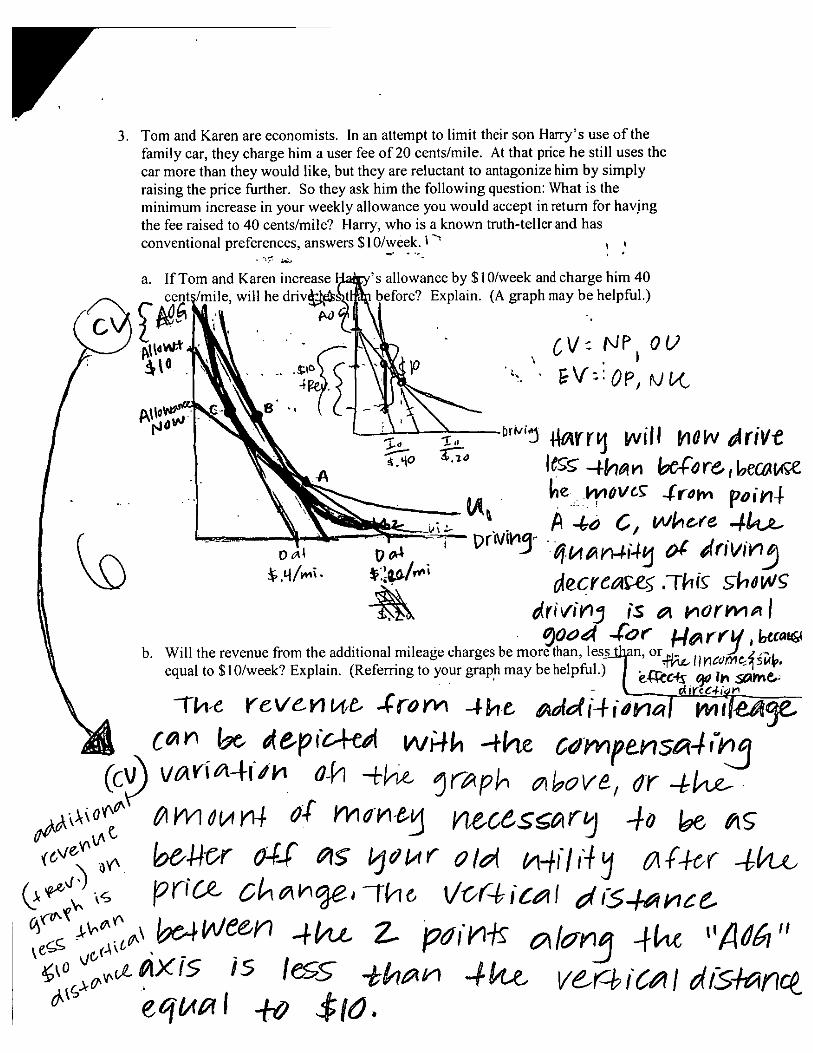

3. Tom and Karen are economists. In an attempt to limit their son Harry's use of thefamily car, they charge him a user fee of 20 cents/mile. At that price he still uses thecar more than they would like, but they are reluctant to antagonize him by simplyraising the price further. So they ask him the following question: What is theminimum increase in your weekly allowance you would accept in return for havingthe fee raised to 40 cents/mile? Harry, who is a known troth-teller and hasconventional preferences, answers $10/week. t ">

o

a. If Tom and Karen increase _ _'s allowance by $10/week and charge him 40_ cent :mile, will he driv_tt _II_before? Explain. (A graph may be helpful.)

",_._. d__\ _., b,_,,t__rrvj will [noI,v alriW4[,Ia_ _cnre,,_ec0_z

-"--_-- "_:'_ " --. -='T-"Dr_/iY_... , r '

char esbemoret_haOn,l_essft_For _'/_KleY ' [_'a_

b. Will the revenue from the additional mileage g , s.Ib.a , ., ........... L..

equal to $10/week? Explain (Referring to your graph may be helpful.).I / _.-,a _,_,..,_.-,,.,..__'tr_r'_v_e"'/_"r'_227'i. - _ dir_o_,'_, ,

-1-1,,.ereve_.vi_e.4row,a 4M,c _atdi4i_v_al _le./4_..

!c_ vaKi,a4f,_v, o-h-+_ _r'-:_ph_l,,ove, or 41,1:--.

:, ,e4wen 4t,t+ z. 41, "Ae4"_e_ C/At , _ . . r "-I

0 q - ...,i .

_;_.j,_._lxts _s lecs_ -klnatn 4h.e.. v_.r"4fC_ldfN4_n_

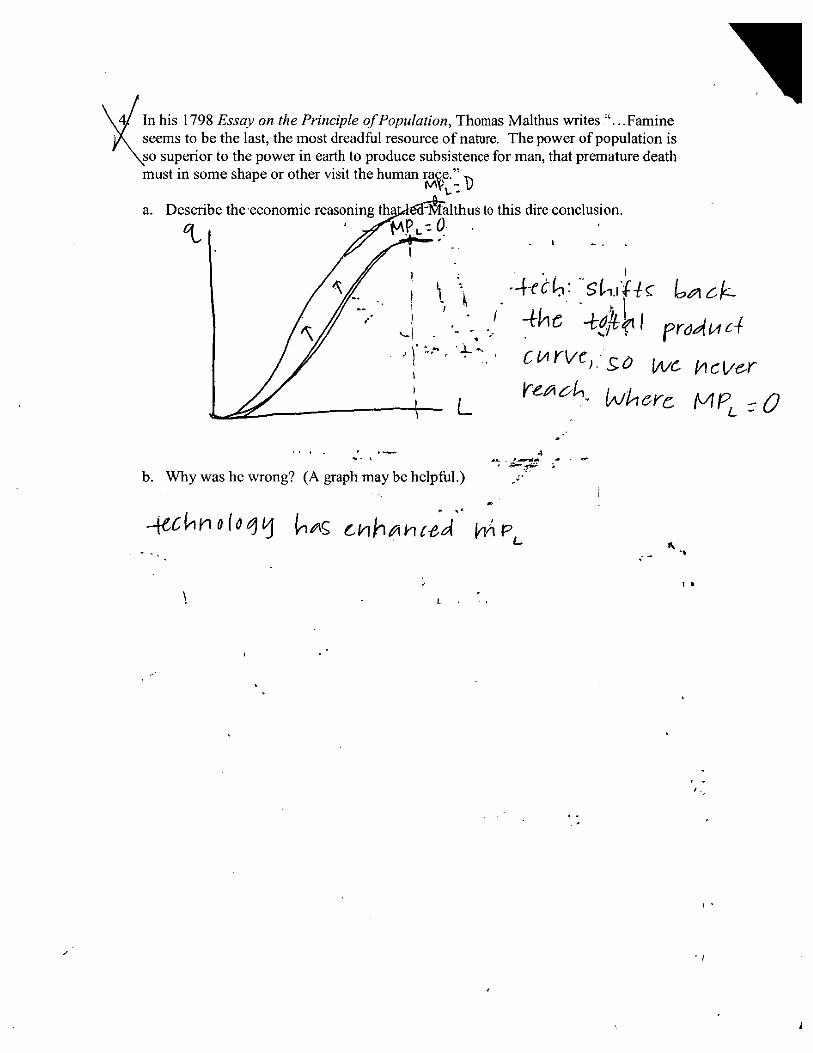

ln his 1798 Essay on the Principle of Population, Thomas Malthus writes "...Famineseems to be the last, the most dreadful resource of nature. The power of population iso superior to the power in earth to produce subsistence for man, that premature death

ra e."must in some shape or other visit the human .._-:a. Describe the'economic reasoning thj_ilz'_'althus to this dire conclusion•

/_ // I o ",

L//> i '. , 4ac 4f_1 roa.c_

'l L r-_/?.. L-h.rc f_PL - 0

_--",_.Z "b. Why was he wrong? (A graph may be helpful.) ;"

• I I

t

#.

_o

LONGER QUESTIONS (Choose two of three, 15 points each.)

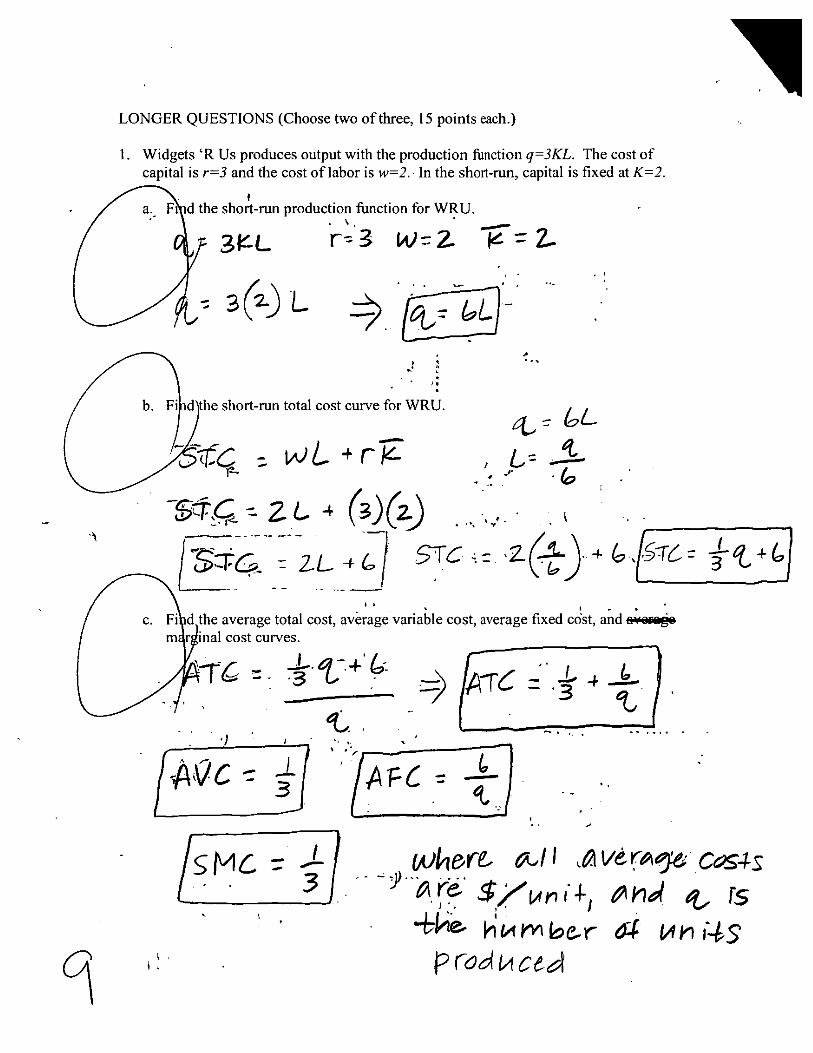

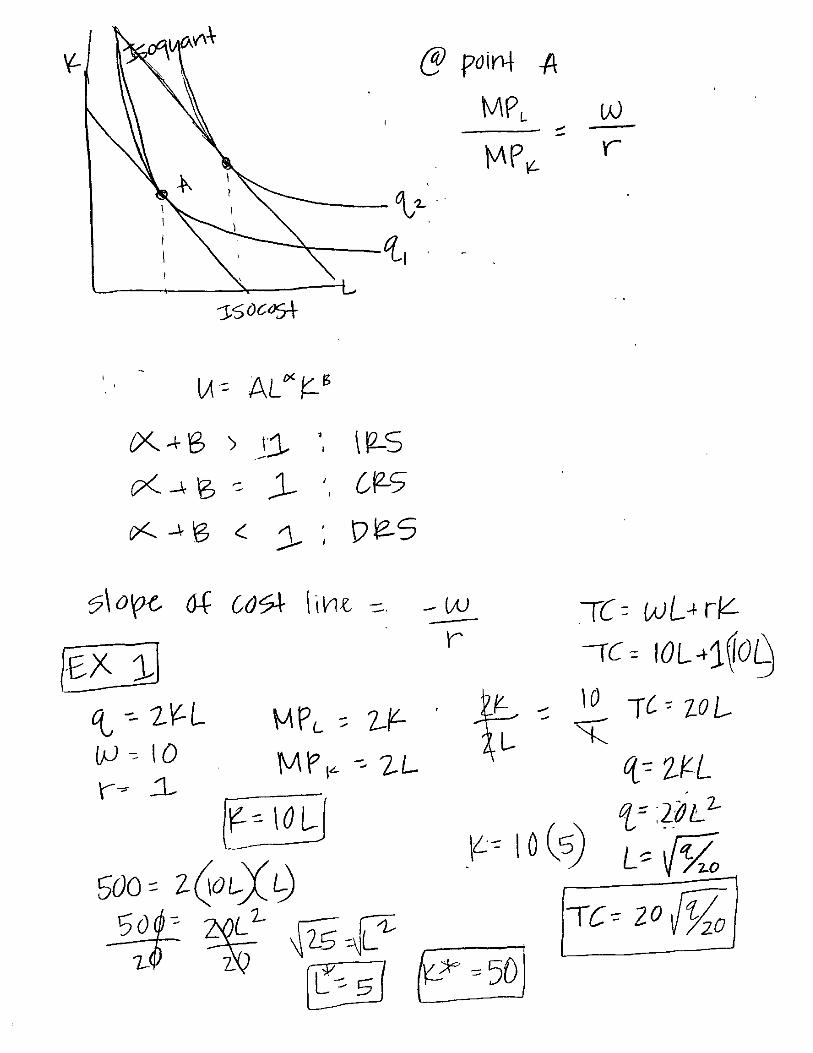

1. Widgets 'R Us produces output with the production function q=3KL. The cost ofcapital is r=3 and the cost of labor is w=2. . In the short-run, capital is fixed at K=2.

• d the short-run production function for WRU.

i_L r-3 W--Z _- -.,

he short-run total cost curve for WRU.

wL "-_ +rZ- , L: ._..¢

-s_.c,.--z c _(_)M • ,_"J1

/ -[ m_ r_inal cost curves. . .

:: I,J '7 ' ' -1 ": "' -- "1 "......

,: pro_ceA

m f-./ d. Inth_ long-run, WRU can also vary its capital. What is the firm's cost-/ -.. '_ ' " " 9minirr 1zing ratio of capital to labor. In other words, what is the long-run

r ;ion path? Nla_:- _3L. t..

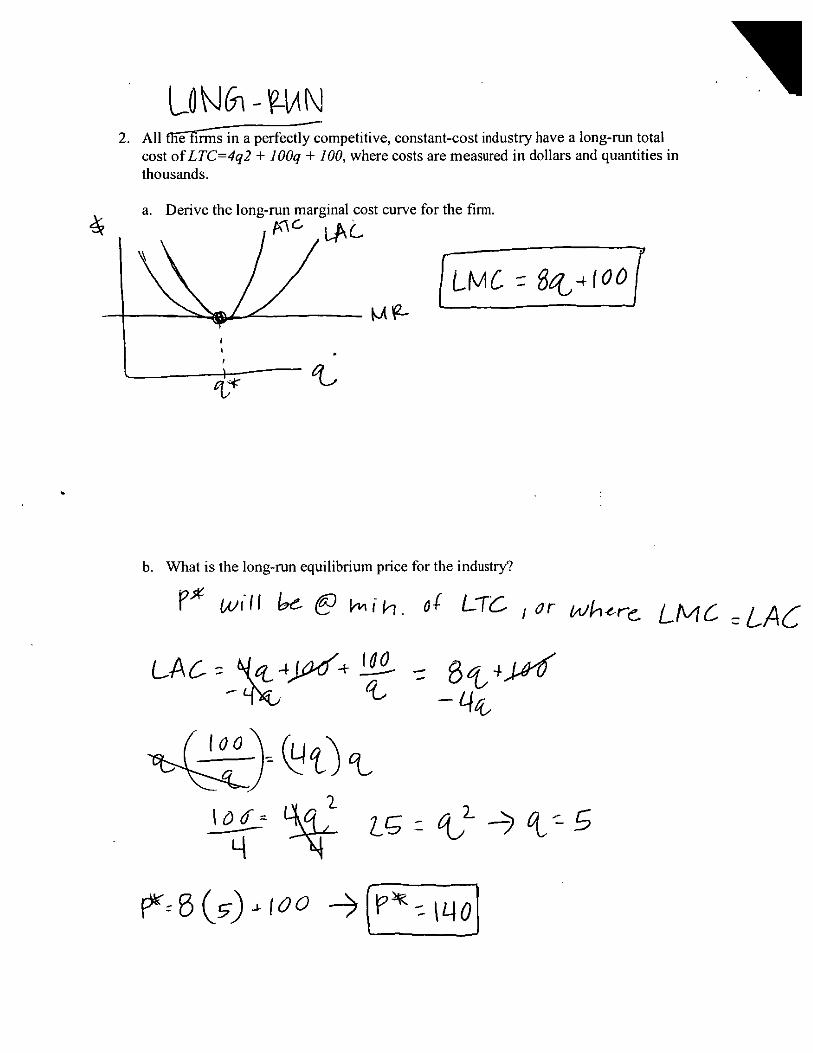

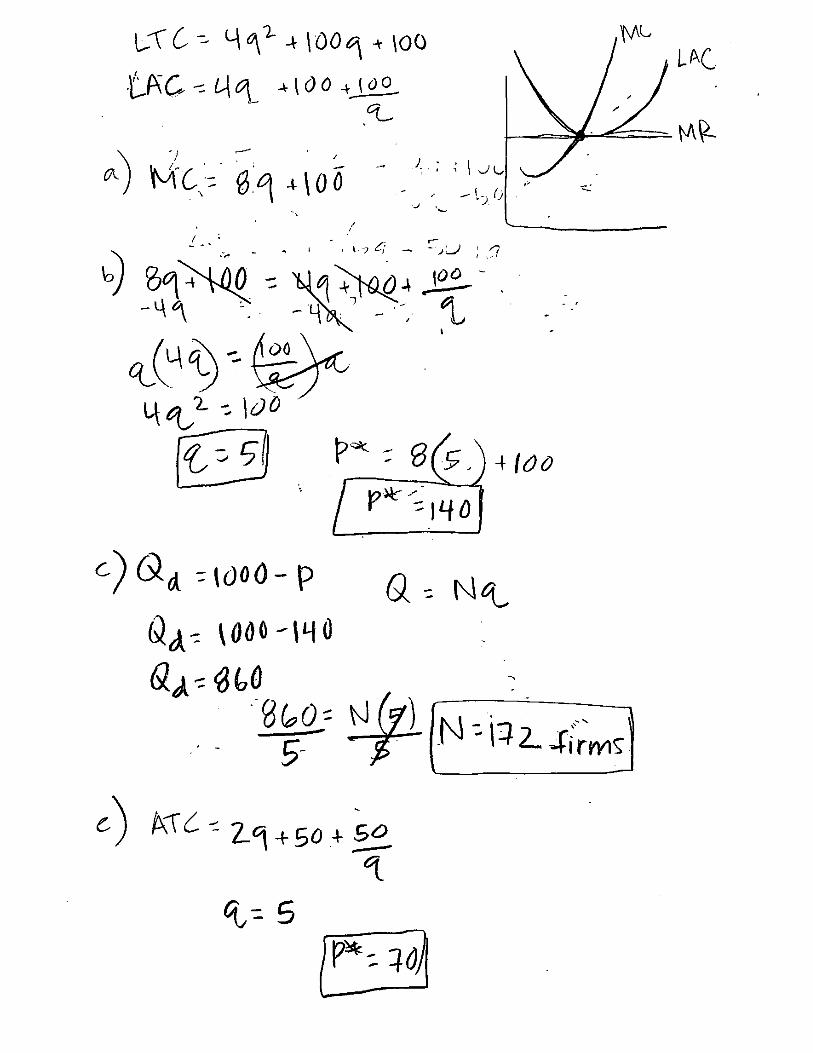

2. All _n a perfectly competitive, constant-cost industry have a long-run totalcost ofLTC=4q2 + lOOq + 100, where costs are measured in dollars and quantities inthousands.

a. Derive the long-run marginal cost curve for the firm.

III

q;. %

b. What is the long-run equilibrium price for the industry?

px uJ,ll _ C _i_. o; LzC _or w_'c LML -LA_

-_ c_ v_t4c _

q

V •

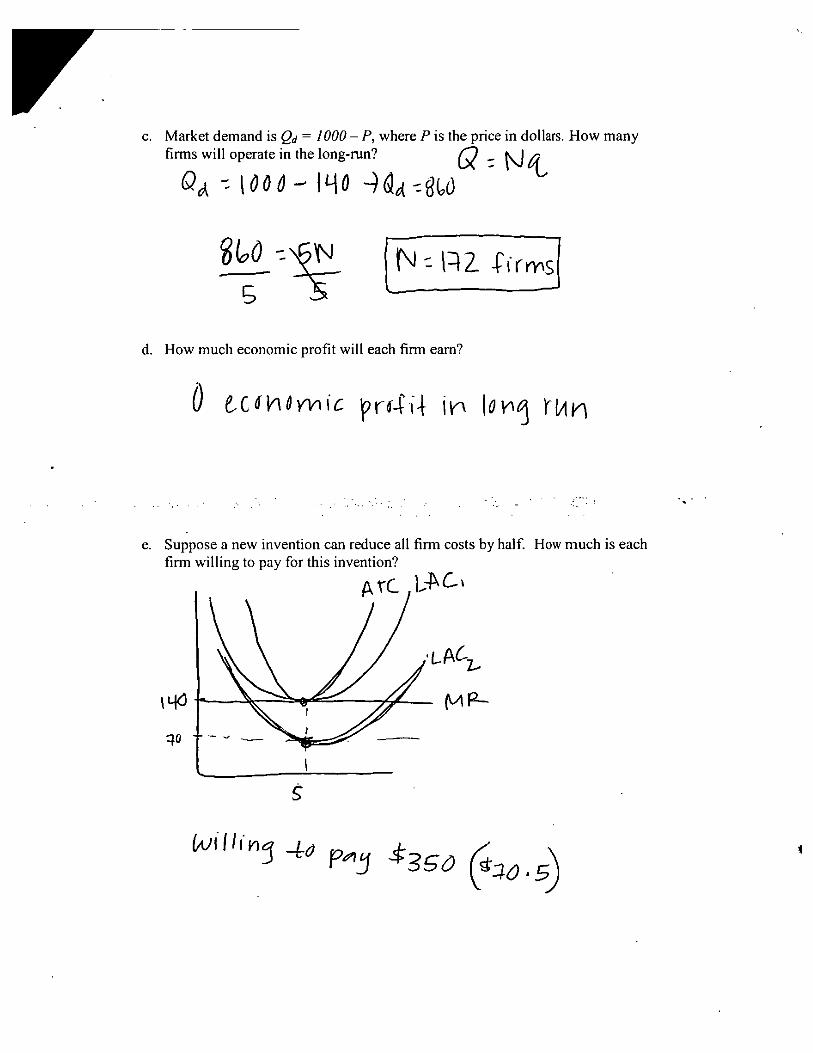

c. Market demand is Qd = 1000- P, where P is the price in dollars. How many

firms will operate in the long-run? _ z _Oa -IO00- Iq0 --)_ --_,O

d. How much economic profit will each firm earn?

0 e.c_o_ic pr_4i4i_ 10_j ruv_

. • .. • . ,'... :. • .....

3. Linda consumes two goods, X and Y. Her utility function is U(X,,Y)=IOXY. Initially,Px=$18 and Pr=$2. Linda's income is $288• Then the price of Xfalls to $8.

alculate the optimal amount ofXand Y that Linda would consume with Pk=$18._t is her total utility at the optimal point? (Show how you reach yore:

late the bptlmal amoun_ ofX ano_Y'Wdt Li.th wqu!d _bugu_%with Px=a_Y. --js her total utility at the optimal point? (Show how you reach your

n.) ,

_M_AZI : lax, I_- z ,' -;x - -7 ,u - -

8.'<-,2-j5 _.Ze,_o

•

..

Lo

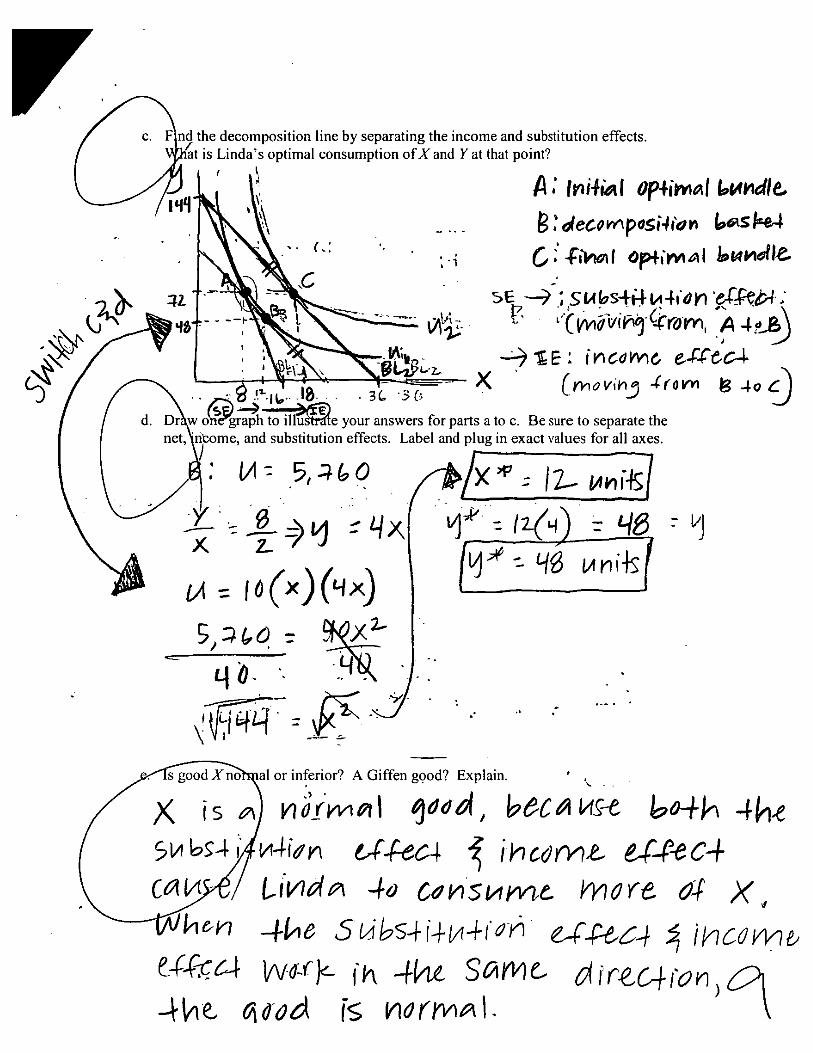

Vc. the ition line by separating the income and substitution effects.

optimal consumption of X and Y at that point?

( . l '. , Cs 2,G

_z' _E ----)';Stabs4_4,alo "eff_T_._.:

I

..._..... 3c st, .K [r.ovi_ 4ro_ le,40d. your answers for parts a to c. Be sureto separatethe

andsubstitution effects. Label andplug in exact valuesfor all axes.

5j _ t,O__- .Xyj "

q0-

_al or inferior? A Giffen good? Explain. ' ,. .

_X_<_4I/v_.r:k_ fU d-kz _mc. o_ic6c,.ffon ,,_

_o-,_- Q_,_,q a-_ ar.R,-_

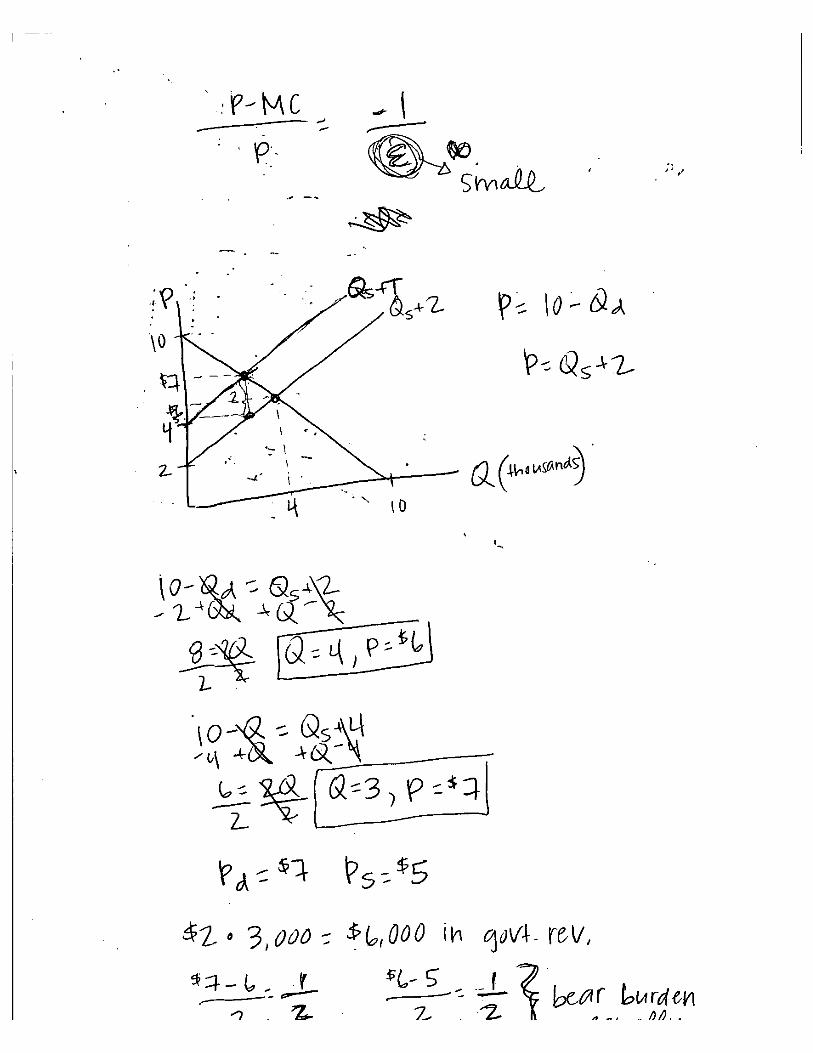

$2- ° 3,000 -- ast, O00 iV_ c,joV_t. r_V,

-_ _ 7_. -'2. . ..

.....................i_,_ CI

r...... , ..... I:I.-_ '

......q_c -_wL _-rIC............L_-_ .......

. ......i.7_ _ _ i..].._ - .

............ _ _ _ _

't________.__

©

' _ AL_- _

Z-.-__ _ JS ' tP-S

•. 0

\-

Spring 2009

FINAL EXAM STUDY GUIDE

When and Where

ECON 3113-002: Wednesday, May 13 at 8:00 AM, Hester 213B

Format

25 Multiple Choice Questions

• These will cover concepts and definitions from the entire course.

• They may require some quick calculations and/or mathematical formulae.

3 or 4 Long Questions ---) tq ; _baOd_5_.

• Mathematical and/or graphical analysis similar to previous midterm questions.

• Potential topics for mathematically focused problems

o Perfect Competition -

o Utility maximization or cost minimization

o Oligopoly (Coumot) with comparison to monopoly, perfect competition

• Potential topics for questions based primarily on graphical analysis

o Consumer choice with a policy application _ Jl'Jr-e 01,'1_. 0/o I,wid--hsrev_

o Monopolistic competition

o Externalities, Public Goods, Game Theory _ 4" "l-t"_l_Je,_t_ 0-if"-4-k_ (-zT/o'l_rlalq_

Office Hours

• Tuesday, May 12 from 3:00 to 5:00

• Thursday, May 14 from 3:00 to 5:00

• Or by appointment

81

Study_.!jp_s

• Set aside a few hours during the next couple of days to go through your notes and homework

to see what you might want to come see me about during office hours.

• If you haven't been studying with other students, start a study group now. You can often

explain things to each other as well or better than I can.

• Outline and organize (maybe recopy) your notes. Refer to the book or to your classmates'notes to fill in areas that are unclear.

• Make yourself a practice test. Go through your notes, problem sets, the midterms, and the

book and write problems on a separate sheet of paper. Save it for a day or so and go back and

take it later. See where your weaknesses are.

82

Intermediate Microeconomics .-. Fall 2008

Midterm Exam 1

Name: __ Class time: _Z70 _

Instructions: Please respond to the questions in the space provided. If you need extraspace, come to the front of the class for extra paper. This is a closed note, closed booktest. You have 75 minutes to complete the test, which has 60 total points. Allocate yourtime accordingly. Please make it clear which questions you do not choose, and showhow you reach your solutions. Good luck!

Part i. Shorter Questions (Choose 4 of 5)

_. Complete the following sentence. "Microeconomics is the study of .... "

C["iOl'_ c,,,,:{_k_ _ .,4-e.v,,w_-:d_i5,<:,/I u,..9 .Z,.o,_,4

I / =..b at_f'atiTti'ltC [zo.J_Ola't. off. t_-t_VCiuc,g _eea'vz,t',_t_C(¢_ei'5_t'4_ nac_.t_.,t_' -'3c_bl_a5

O .Boris budgets $9 per week for his morning coffee with milk. He likes it only if itis prepared with exactly 4 parts coffee, 1 part milk. Coffee costs $1/oz, milk$0.50/oz. How much coffee and how much milk will Boris buy per week?

.2.'_ _q :," _ll_,. :/::"q k c-_l C i,: _"

I_ ,<_4__ "3 :,_// z, z = 4 .-"")_///

Q .I

= ,,I

"x

--.,.

(b$ $666.67 D

- (, _ I"..a' .D $400 ........... . //

1

15,000 100,000 I'_1!_ 250,000i

g-

Q _.¢_The graph above depicts the supply and demand of hotel rooms in New York

City.f_----_ ....a.//What are the equi_brium price and quantity in this market?

( _p: I"s_O J/t e_a-_icoocQ,"{

b. Is-there-another price that would increase total welfare in this market. Why orwhy-not? J - ',1 _, _r &e__o_.6_._L_.__.a.c:S_r e c,-,_<..I<_ t_c., <_c,._.( _ag p,,.c,:_

ps ,<.<._, _, ,..... _.<_?.,,_ ,s (,-<.-.<<_.44.,_aT.,,,.,_,..<._+_(-t

c. Depict on the graph the change in the market that would occur if DonaldTrump built a new hotel with 1000 rooms.

'""us,,d-

\x 1

f"N

/r

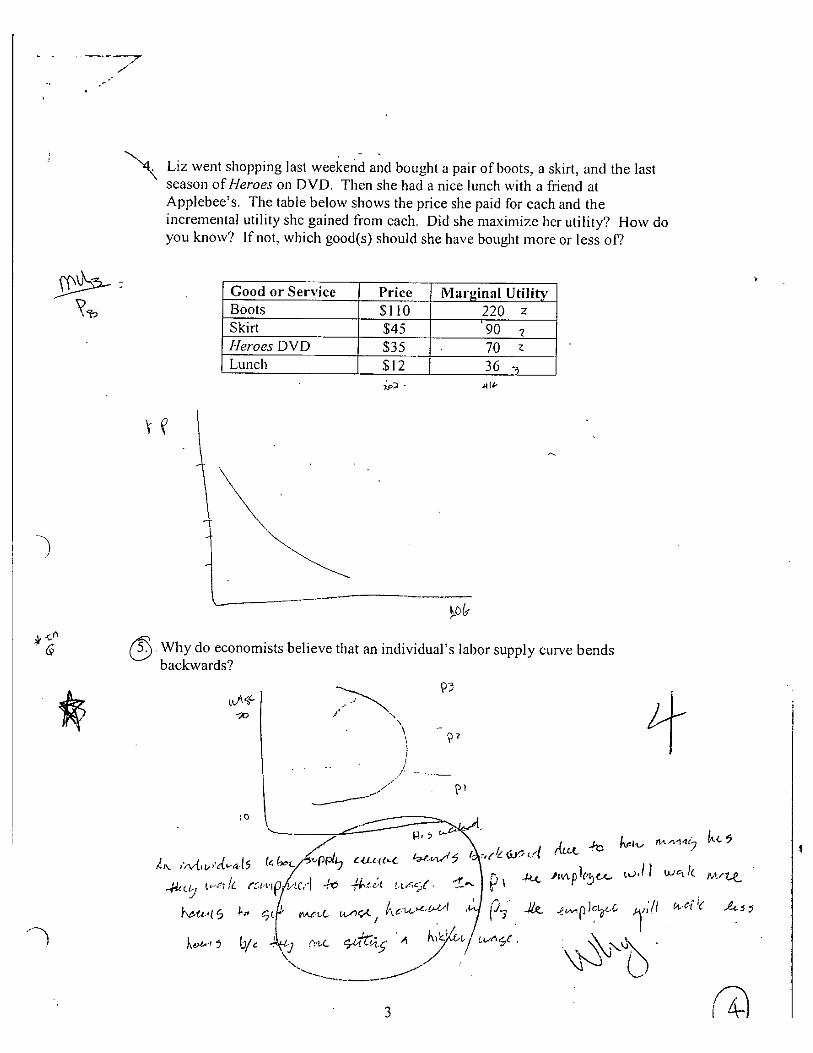

"_. Liz went shopping last bought a pair of boots, a skirt, and the lastweekend andseason of Heroes on DVD. Then she had a nice lunch with a friend atApplebee's. The table below shows the price she paid for each and theincremental utility she gained from each. Did she maximize her utility? How doyou know? If not, which good(s) should she have bought more or less off

: Good or Service Price Marginal Utility_'b Boots $1t0 220 z

Skirt $45 '90 7Heroes DVD $35 70 z

Lunch $12 36 ._

,l'.ca (_ Why do economists believe that an individual's labor supply curve bendsbackwards?

\i - ,_z., ]

J"" _51

, Av.. ",% k y t

_", _1<_ _"__<5 " "y7 "_< : _ """---._.... .... //

"-- 7,I

Part II. Longer Questions (Choose 2 o1".3).

1. Suppose the market for backpacks has two types of consumers, students and hikers.Student demand is P = 30 -3Qa and hiker demand is P = 30 - 2Q1,_"

a. Find the market demand curve for backpacks.

b. If the supply curve is given by P=O.8Qs, find the equilibrium price and quantityfor the market.

--)

c. Calculate the price elasticity of market demand at the equilibrium point.

A_

d. Is market demand more or less elastic than student demand? Explain.

h

) (_)Antonio spends all his $200 weekly.income on two goods, Xand Y. His utilityfunction is given by U(X,, Y)=O.5XY. His marginal utilities are MUx=O.5Y andMUr = O.5Aq

¢

a. What is Antonio's marginal rate ofsubstitution.dfXfor Y?_

t_.I@ :'o,_:_- r:- t 2)t , o.s i /t

b. If P,.=4 and Py=l 0,. hoW'm__ch of each good should he

G,s't_c1 _zaP °'_'_;N,_ ,:/ buy?

t/ ; i_:) , "

/c. Draw a graph to depict Antonio's optimal choice in part b.

Z\Io

N gqO

d. Suppose the price of X falls to P,=2, and Anton_Q;dhooses the bundle X=50, Y=10.

Show this on your graph above. /__

e. Is X a normal or inferior good? How d6 you know? (Hint: think about substitution. .-r_,:t._.e- Z_O

andincomeeffects.) _._*,,'_/ _s _¢-- p_.'_e Tr_ _ -{_ _, ..,_ _,_ _ .g 7._oI¢ ,O,_t ,_ , ,z ; ZF

i, -;,_fO

"-._ ..... ..... . _,e.,..eD_r-d""_'@ \-,.

"7\i \.

i -,. 7

- 77 q: % -s_!; :"0R I

(_ .l_z;;:.'co t;,crO

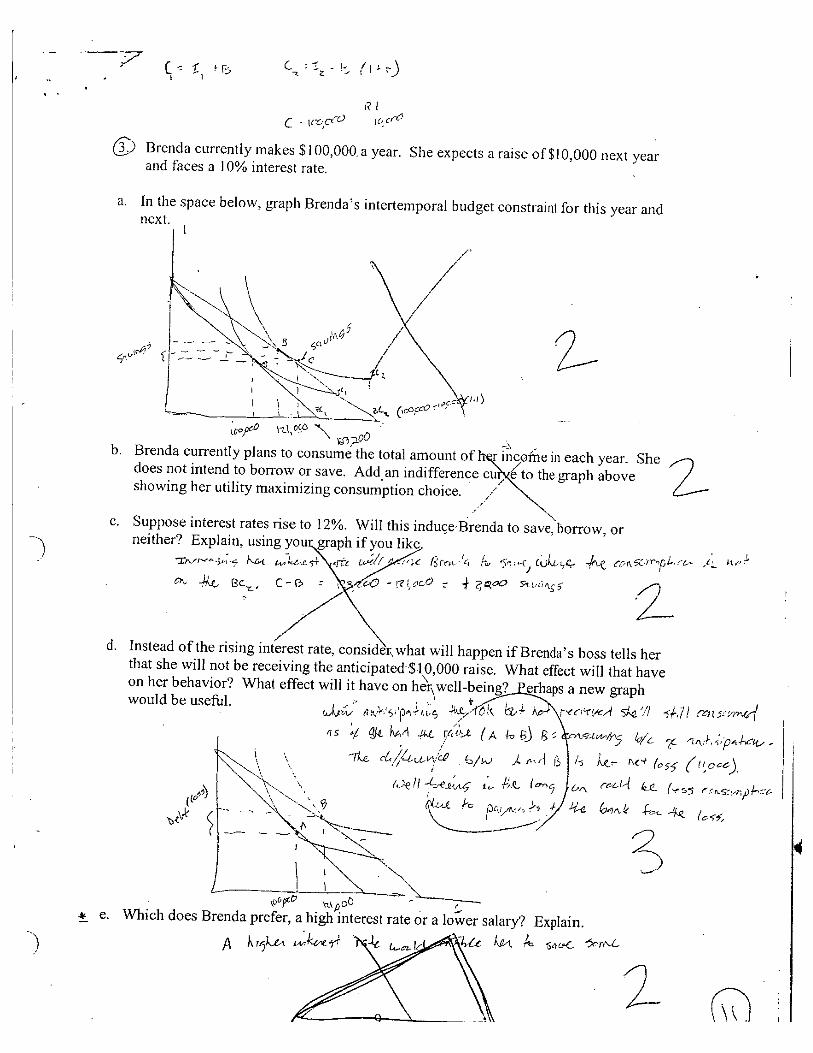

3C.) Brenda currently makes $100,000. a year. She expects a raise of $10,000 next yearand faces a 10% interest rate.

a. In the space below, graph Brenda's intertemporal budget constraint for this year andnext.

[ '_ //>

, ,, _ qtu '?'_'_j

b. Brenda currently plans to consume the total amount oft_r income in each year. Shedoes not intend to borrow or save. Add an indifference cu_/to the m-anh above "_

.... .showing her utlhty maximizing consumption choice. /

c. Suppose interest rates rise to 12%. Will this induce-Brenda to save(borrow, orneither? Explain, using your graph if you like. "

d. Inste£dof therisi:-inte_5_ '.'I:_, ,wnat will happen ifBrenda's boss tells herthat she will not be receiving the anticipated.$10,O00 raise. What effect will that haveon her behavior? What effect will it have on heXr£well-being? P_erhaos a new m'anhwould be useful. . ... , ) _-,_" _ " , .

i ,, . _/ Z' ; ' '

e. Which does Brenda prefer, a high interest rate or a lower salary? Explain.

-') A kr,_k_ " ' " _ _ _-_--c

ECON 3113

POLICY DEBATES

Each student is required to write a paper discussing a policy issue and participate in agroup presentation arguing one side of the debate. The instructor will randomly assignstudents to each side of the debate. The paper and the presentation will be graded basedon the strength of the argument presented using microeconomic theory.

Paper• The paper should provide background information on the policy debate, discuss

the relevant microeconomic theory, and describe both the pros and cons of thepolicy.

• Five to ten pages in length (not including figures, tables, and references), 12 pointfont, double-spaced, 1 inch margins.

• Students should submit both an electronic and a hard copy.• The topic may be discussed with other students, but the work should be original.

(Drafts should not be shared among students.)Presentation

• Each side of the debate will have ten minutes to present their case to the class.• Use of electronic slides is encouraged.• The class will have the opportunity to vote on the winner of the debate.

Grading criteria• Clarity and thoroughness of discussion from microeconomic theory• Strength of positive (as opposed to normative) arguments• Original ideas• Persuasiveness

Please rank the following debate topics according to your preference.

A revenue-neutral gas tax, February 12 _._

"_ _ _A_gricultural price support---_,March 10 "(_O"30-_._ _"7-- Labor unionization in a mill town, April 2

__ The Vermont Billboard Ban, April21- _9_'0_e:_k_(_ _e_i_i3cg[_

Prof. Moooey will provide more detailed descriptions of the debate topics when th_y are ;_assigned. However, questions are welcome at any time.