Embed Size (px)

Citation preview

113

CHAPTER- 4

ECONOMIC IMPACT ASSESSMENT

ON SHG MEMBERS

4.1 Introduction

4.2 Impact Assessment (IA) Methodologies for Microfinance

4.3 Economic Impact on SHG Members

4.4 Summary of Findings

4.5. Conclusion

114

Chapter-4

Economic Impact Assessment on SHG Members

4.1. Introduction

Poverty reduction has been the main agenda of most developing countries.

As a measure of reducing poverty, most of the developing countries have

adopted the system of empowering the individual to be self-reliant. To help

the individuals become self-reliant, Non-Governmental Organizations

(NGOs) lent them some amount of capital to start some income generating

activities so that they can come out from poverty. On the contrary, it is

equally important to constantly monitor the potential negative impacts,

such as over-indebtedness of clients or risk of corruption and illegal use of

credit. At the same time, it is to be understood that microfinance is not the

solution to all problems in developing countries, but should be focused on

economically active poor, who can afford to borrow and repay money as

part of their normal budget and who are not living in an emergency

situation.

NGOs being non-profit organizations with an objective of social

development have been an important player as facilitator or intermediary in

microfinance movement in India. NGO-MFIs play significant roles in

115

supporting and nurturing SHGs by not only extending credit or other

financial services to SHGs but also in many other ways. This chapter

describes about research findings on economic impact on SHG members.

4.2. Impact Assessment (IA) Methodologies for Microfinance

Impact Assessment is the structured study, which measures the impact on

employment, income generation, nutrition, education, health, consumption,

business development (micro entrepreneurship) and gender equity on

MFI‟s clients.41

Impact assessment refers to the assessment of “how

financial products and services affected the lives of the poor. It is also the

measurement of income growth, assets growth and vulnerability reduction

of the poor by the microfinance programme. The indicators for such

assessment are not limited to economic development but extended to

development growth like health, education, empowerment, gender etc.

Impact assessment can be done through using qualitative as well as

quantitative data. The qualitative data are collected using the tools like

Participatory Rural Assessment (PRA), Rapid Rural Appraisal (RRA),

personal discussions, observations etc. Qualitative impact assessment

provides a broad idea, mostly open-ended, on the impact of microfinance

41

Debadutta K . Panda (2009), “ Understanding Microfinance”, Wiley India

116

programmes. The quantitative data collection tools are the schedule and

structured questionnaires for household survey. Data from secondary

sources complement the primary data. Quantitative impact assessment

requires various mathematical, statistical and econometric models for

analysis of data. In many microfinance programmes, both qualitative and

quantitative methods are jointly used for overall impact assessment.

Different levels and methodologies of impact assessment of microfinance

are briefly discussed here in this section.

4.2.1. AIMS’s Core Impact Assessment Method

According to Dunn (2002)42

, Impact Assessment (IA) for microfinance can

be carried out at three different level i.e. household level, enterprise level

and individual level.

Fig.4.1. Impact of microfinance in different levels43

42

Dunn, E. (2002). “Research Strategy for the AIMS Core Impact Assessment”, AIMS, ,

University of Manchester

Impact of

Micro-finance

Household Level

Individual Level Enterprise Level

117

Household Level: The impact assessment programmes should capture the

changes in the household level due to microfinance programme. The

household economic positions like income, expenditure, asset position and

livelihood portfolio may change over time due to the increase in access by

households to microfinance products and services. The socio-psycho

changes can be experienced at the household level due to reasons such as

increase in the level of household income, greater diversification in the

sources of household income, increase in household assets including

improvements in housing, increase in major household appliances and

transport vehicles, increase in microenterprise fixed assets, increase in

expenditures on children‟s education, increase in expenditures on food

especially among the very poor and increase in the household‟s

effectiveness in coping with shocks.

Individual Level: In general, effective microfinance programmes bring a

positive change in individual level. It develops managerial ability among

the beneficiaries and increases status and position not only in the society

but also in the house/family. The increase in capacity development due to

microfinance programmes leads to a change in individual income level,

43

Cohen, M. and Bourjorjee, D. (2003), “Impact of Microfinance”, Donor Brief No. 13, CGAP,

Washington, D.C.

118

expenditure pattern, living condition, literacy position, awareness,

accessibility, equity and equality to the household and community assets.

The programme results to increase in the client‟s control over resources

and income within the household economic portfolio, increase in self-

esteem and respect from others, increase in personal savings, gives better

position to deal with the future through more proactive behavior and

increase in confidence level.

Enterprise Level: Microfinance programmes influence microenterprise

operations i.e. change in profits, scale of operations, diversifications and

leads to increase in microenterprise revenue, increase in enterprise fixed

assets especially among repeat borrowers, increase in the paid and unpaid

employment generated by the enterprise and improvements in the

transactional relationships of the enterprise

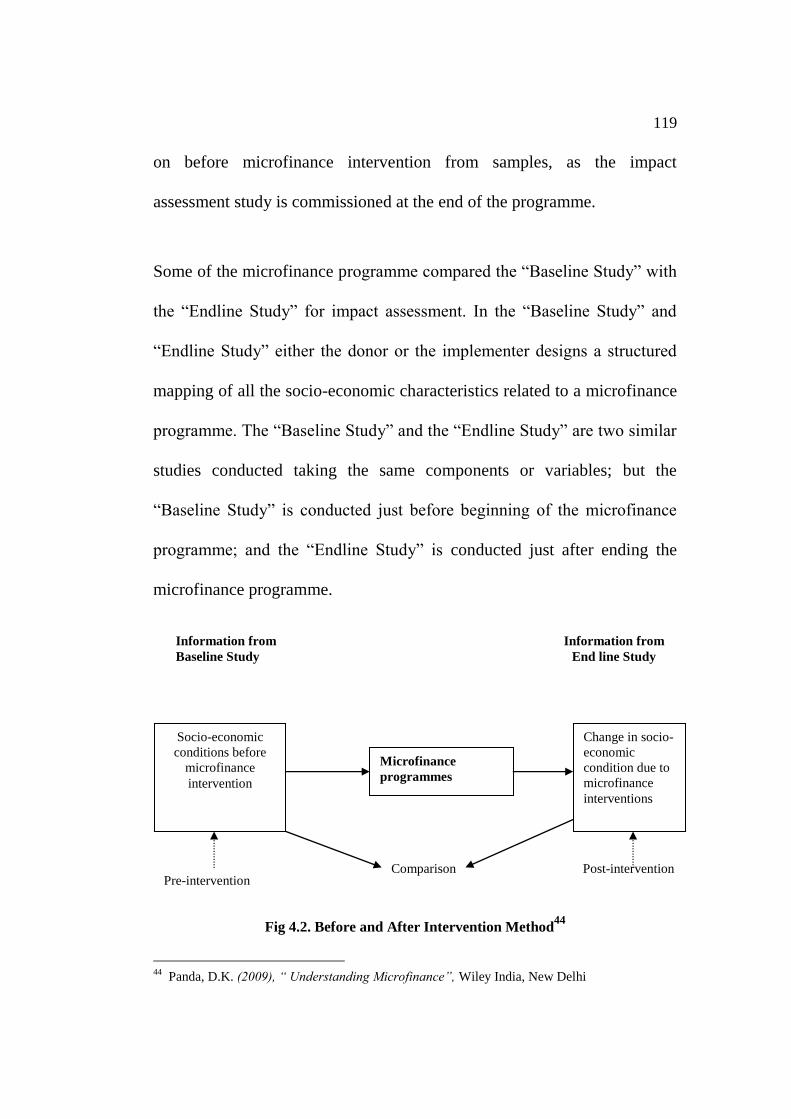

4.2.2. Impact Assessment Method: Before and After Intervention

Under this method, the status of the sample units (person/household/village

etc) before microfinance intervention is compared with that of the after

microfinance intervention; taking the various parameters or variables. This

method is good for assessment of the actual impact; but this method has a

limitation. It becomes difficult to get the data (related to various variables)

119

on before microfinance intervention from samples, as the impact

assessment study is commissioned at the end of the programme.

Some of the microfinance programme compared the “Baseline Study” with

the “Endline Study” for impact assessment. In the “Baseline Study” and

“Endline Study” either the donor or the implementer designs a structured

mapping of all the socio-economic characteristics related to a microfinance

programme. The “Baseline Study” and the “Endline Study” are two similar

studies conducted taking the same components or variables; but the

“Baseline Study” is conducted just before beginning of the microfinance

programme; and the “Endline Study” is conducted just after ending the

microfinance programme.

Fig 4.2. Before and After Intervention Method

44

44

Panda, D.K. (2009), “ Understanding Microfinance”, Wiley India, New Delhi

Socio-economic

conditions before

microfinance

intervention

Change in socio-

economic

condition due to

microfinance

interventions

Microfinance

programmes

Comparison Pre-intervention

Post-intervention

Information from

Baseline Study

Information from

End line Study

120

Barnes, Morris and Gaile (1998)45

have taken following broad four

parameters for their baseline study in Uganda i.e. 1) improvements in the

economic welfare of households; 2) enterprise growth or stability; 3)

increases in empowerment, especially among women; and 4) strengthened

social and rural networks.

Cohen and Chen (1997)46

explained their framework for core hypothesis

for measuring impact of microfinance at individual level. The framework

was based on following broad parameters: material change (income,

earning capacity, resources control, basic needs etc), cognitive change

(knowledge, skills, and awareness), perceptual change (self esteem, self

confidence, future vision, respect), relational change (decision making,

bargaining power, participation, self reliance, organizational strength)

4.3. Economic impact on SHG Members

Microfinance movement is comparatively new in the state of Manipur. But,

it is becoming popular in the rural areas of the State. Formation of SHGs

has become a movement in rural areas. It was found that microfinance

45

Barnes, C., Morris, G. and Gaile, G. (1998), “An assessment of impact of microfinance services

in Uganda, Basline findings”, AIMS, USAIDS, Washington, D.C.

46

Cohen, M. and Chen,M.A. (1997), “A Guide for assessing the microenterprise services at the

individual level”‟ AIMS, USAID, Washington, D.C.

121

activities of NGO-MFIs had direct impact on economic status of most of

the SHG members in terms of personal income, household income,

household assets, household expenditure, household saving, access to

credit and micro insurance products etc. The researcher used the recall

method for getting information related to economic activities before and

after joining the microfinance programme. To minimize the response bias,

cross questions were asked for verification and consistency of the answers

given by the respondents. Pair-t test was used to analyze the impact of

microfinance by comparing pre and post situations. Since most of the SHG

members did not avail any benefits from other programmes such as Govt‟s

schemes like SGSY, PMRY, etc, it was assumed that any change in

economic status was considered mainly due to microfinance programme.

The major findings of economic impact of SHG members are presented in

the following sections.

4.3.1. Impact on personal income of SHG members

In the context of research study, personal income of SHG members means

income of SHG members from their income generating activities for which

micro loans are given by the NGO-MFIs. Microfinance basically means

providing credit to SHG members for taking up income generating

122

activities or micro-enterprises. Therefore, it was considered relevant and

important to know whether there was any improvement in the personal

income of SHG members after joining microfinance programme. Recall

method was used to capture personal income of SHG members before and

after joining the microfinance programme. To minimize the respondent‟s

biasness, personal income was cross checked with the other members

having similar business activities as well as the same verified with the

records of SHG members maintained with NGO-MFIs. This is shown in

table 4.1 below.

Table 4.1: Average monthly personal income of SHG Member

Average Monthly

Income

Number of sample SHG Members

Before joining MFIs After joining MFIs

N % N %

Below Rs.1,000 99 82.5 38 31.67

Rs.1,000-Rs1,500 13 10.8 42 35.00

Rs.1,500-Rs.2,000 3 2.5 18 15.00

Rs.2,000-Rs.2,500 3 2.5 11 9.17

Rs.2,500-Rs.3,000 1 .8 8 6.67

Above Rs.3,000 1 .8 3 2.50

Total 120 100 120 100

Source: Primary data

It was found that majority of about 82.5 per cent of sample SHGs had

average monthly personal income below Rs.1000 before joining MFIs.

After joining MFIs, only 31.67 percent sample SHGs had average monthly

income below Rs.1000. It is observed that nos. of SHGs members

123

belonging to lower income groups had declined because of increase in

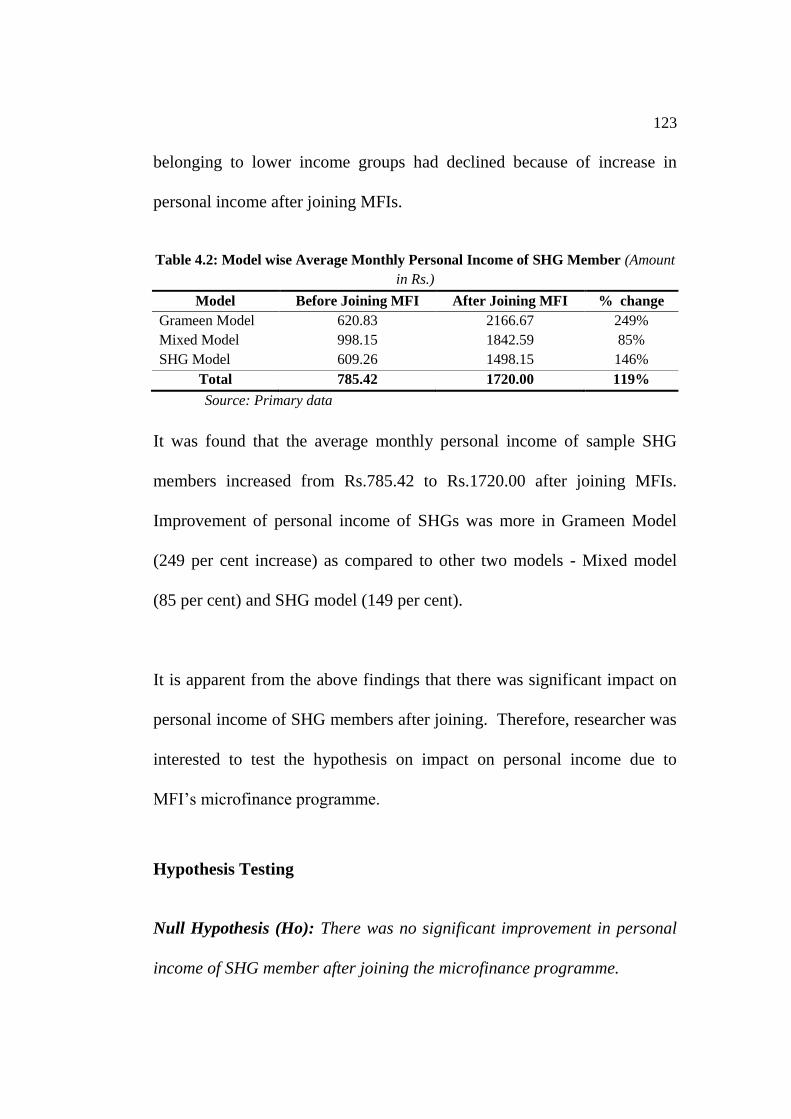

personal income after joining MFIs.

Table 4.2: Model wise Average Monthly Personal Income of SHG Member (Amount

in Rs.)

Model Before Joining MFI After Joining MFI % change

Grameen Model 620.83 2166.67 249%

Mixed Model 998.15 1842.59 85%

SHG Model 609.26 1498.15 146%

Total 785.42 1720.00 119%

Source: Primary data

It was found that the average monthly personal income of sample SHG

members increased from Rs.785.42 to Rs.1720.00 after joining MFIs.

Improvement of personal income of SHGs was more in Grameen Model

(249 per cent increase) as compared to other two models - Mixed model

(85 per cent) and SHG model (149 per cent).

It is apparent from the above findings that there was significant impact on

personal income of SHG members after joining. Therefore, researcher was

interested to test the hypothesis on impact on personal income due to

MFI‟s microfinance programme.

Hypothesis Testing

Null Hypothesis (Ho): There was no significant improvement in personal

income of SHG member after joining the microfinance programme.

124

Alternative Hypothesis (Ha): There was significant improvement in

personal income of SHG member after joining the microfinance

programme

For pre and post situation analysis of dependent samples, paired samples t-

test is generally used for testing hypothesis. The result of paired samples t-

test is given below:

Table 4.3: Paired Sample T-Test on Personal Income of SHG Member

Avg. Monthly

Personal

Income of

SHG Member

Paired Differences

t

df

Sig.

(2-

taile

d)

Mean

Std.

Deviat

ion

Std.

Error

Mean

95% Confidence

Interval of the

Difference

Lower Upper

After – Before

934.58 520.89 47.55 840.42 1028.73 19.65 119 .000

Statistical tool used: SPSS for Window (v.10.0.5)

Since t value is significant at = 0.05 level since p value (=0.00) <0.05,

Ho is rejected and Ha is accepted. It is seen that there was significant

improvement in personal income of MFI‟s SHG members after joining

MFI‟s microfinance programme. Therefore, it can be concluded that there

was positive impact on personal income of SHG members due to

microfinance programme.

125

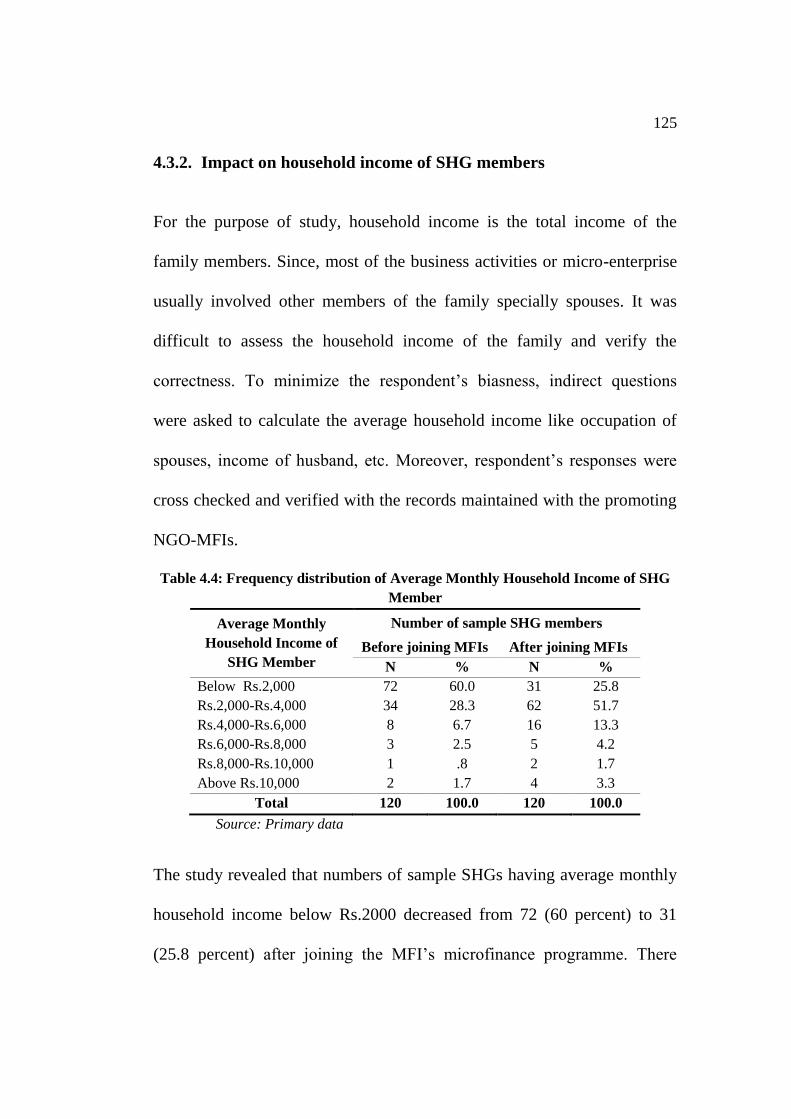

4.3.2. Impact on household income of SHG members

For the purpose of study, household income is the total income of the

family members. Since, most of the business activities or micro-enterprise

usually involved other members of the family specially spouses. It was

difficult to assess the household income of the family and verify the

correctness. To minimize the respondent‟s biasness, indirect questions

were asked to calculate the average household income like occupation of

spouses, income of husband, etc. Moreover, respondent‟s responses were

cross checked and verified with the records maintained with the promoting

NGO-MFIs.

Table 4.4: Frequency distribution of Average Monthly Household Income of SHG

Member

Average Monthly

Household Income of

SHG Member

Number of sample SHG members

Before joining MFIs After joining MFIs

N % N %

Below Rs.2,000 72 60.0 31 25.8

Rs.2,000-Rs.4,000 34 28.3 62 51.7

Rs.4,000-Rs.6,000 8 6.7 16 13.3

Rs.6,000-Rs.8,000 3 2.5 5 4.2

Rs.8,000-Rs.10,000 1 .8 2 1.7

Above Rs.10,000 2 1.7 4 3.3

Total 120 100.0 120 100.0

Source: Primary data

The study revealed that numbers of sample SHGs having average monthly

household income below Rs.2000 decreased from 72 (60 percent) to 31

(25.8 percent) after joining the MFI‟s microfinance programme. There

126

were also some instances where member‟s husband stopped drinking

alcohol, gambling, etc. and started contributing to the family income due to

motivation by SHG members.

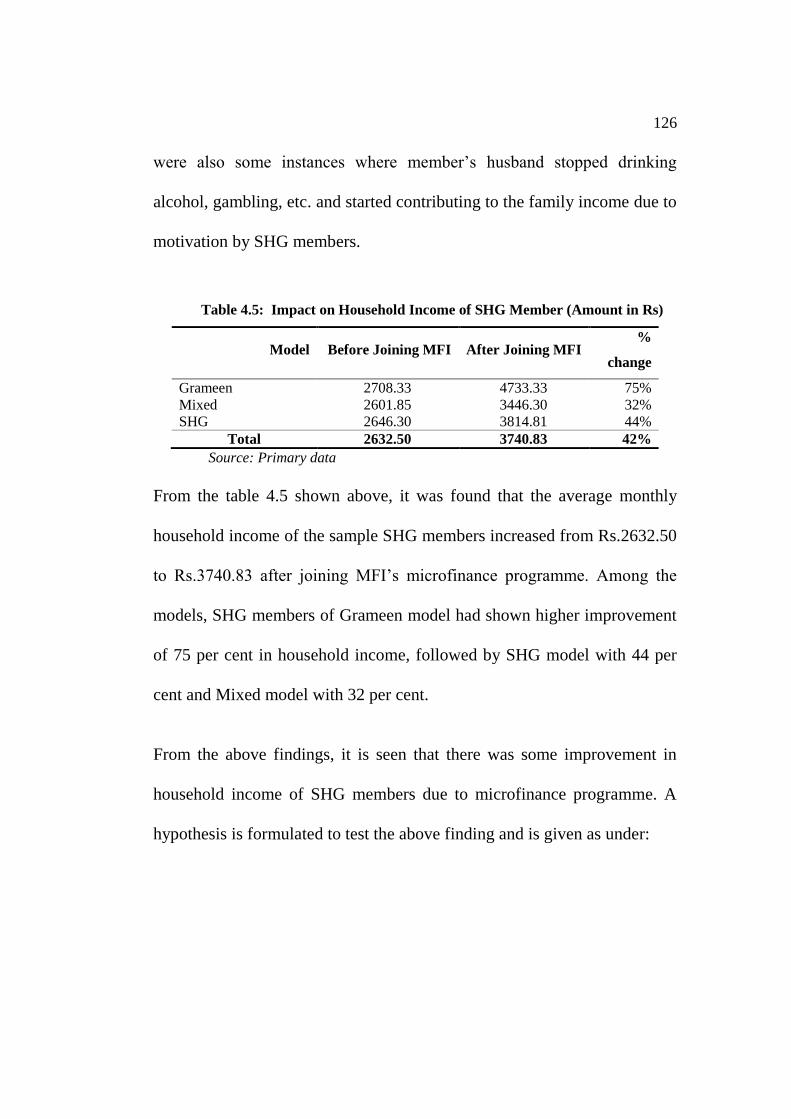

Table 4.5: Impact on Household Income of SHG Member (Amount in Rs)

Model Before Joining MFI After Joining MFI %

change

Grameen 2708.33 4733.33 75%

Mixed 2601.85 3446.30 32%

SHG 2646.30 3814.81 44%

Total 2632.50 3740.83 42%

Source: Primary data

From the table 4.5 shown above, it was found that the average monthly

household income of the sample SHG members increased from Rs.2632.50

to Rs.3740.83 after joining MFI‟s microfinance programme. Among the

models, SHG members of Grameen model had shown higher improvement

of 75 per cent in household income, followed by SHG model with 44 per

cent and Mixed model with 32 per cent.

From the above findings, it is seen that there was some improvement in

household income of SHG members due to microfinance programme. A

hypothesis is formulated to test the above finding and is given as under:

127

Hypothesis testing:

Null Hypothesis (Ho): There was no significant improvement in household

income of MFI’s SHG Members after joining the microfinance programme.

Alternative Hypothesis (Ha): There was significant improvement in

household income of MFI’s SHG Members after joining the microfinance

programme.

Paired sample t-test was used for testing the above hypothesis and the test

result is given as below:

Table 4.6: Paired Sample Test on Average Monthly Household Income of SHG

Member

Avg.

Monthly

Household

Income of

SHG

Member

Paired Differences

t

df

Sig.

(2-

tailed)

Mean

Std.

Deviat

ion

Std.

Error

Mean

95% Confidence

Interval of the

Difference

Lower Upper

After –

Before

1108.33 865.64 79.02 951.86 1264.80 14.02 119 .000*

Statistical tool used: SPSS * Significant at 0.01 level

It is observed from the above table that t value (14.02) is found significant

at = 0.05 level since p value (=0.00) <0.05. Therefore, Ho is rejected

and Ha is accepted. Thus, it can be concluded that there was significant

improvement in household income of MFI‟s SHG Members after joining

128

the microfinance programme. In other words, microfinance had significant

impact on household income of the SHG members.

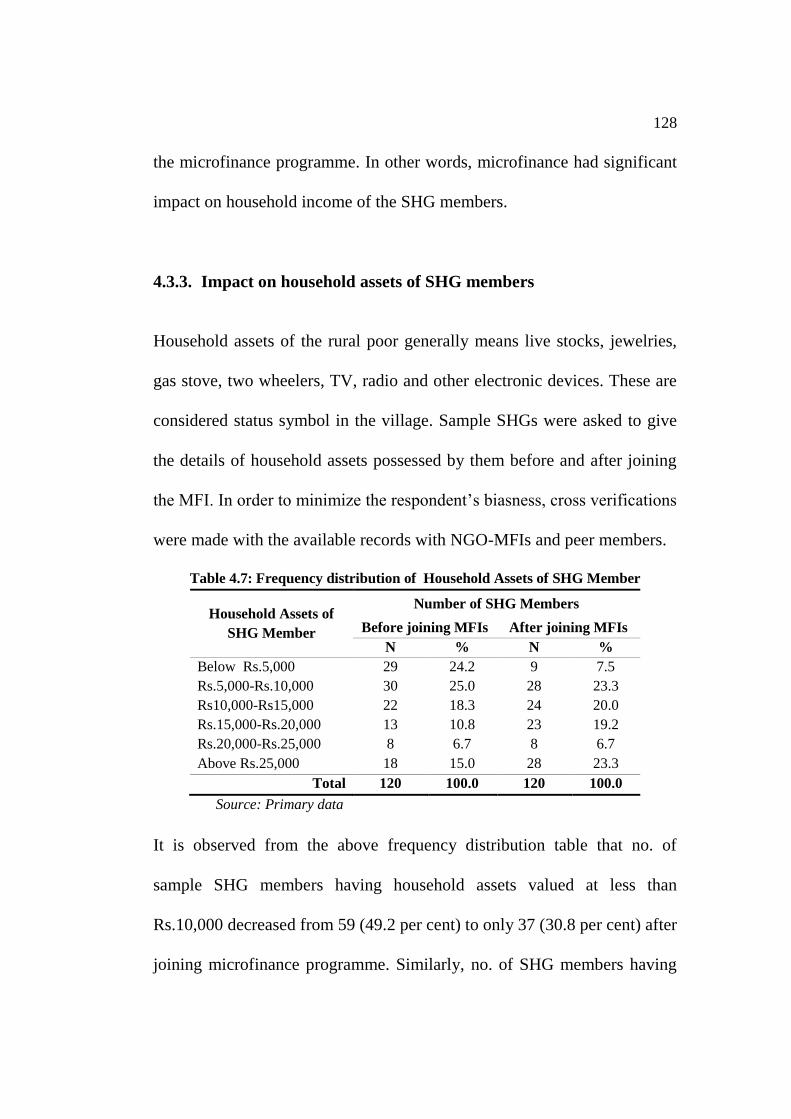

4.3.3. Impact on household assets of SHG members

Household assets of the rural poor generally means live stocks, jewelries,

gas stove, two wheelers, TV, radio and other electronic devices. These are

considered status symbol in the village. Sample SHGs were asked to give

the details of household assets possessed by them before and after joining

the MFI. In order to minimize the respondent‟s biasness, cross verifications

were made with the available records with NGO-MFIs and peer members.

Table 4.7: Frequency distribution of Household Assets of SHG Member

Household Assets of

SHG Member

Number of SHG Members

Before joining MFIs After joining MFIs

N % N %

Below Rs.5,000 29 24.2 9 7.5

Rs.5,000-Rs.10,000 30 25.0 28 23.3

Rs10,000-Rs15,000 22 18.3 24 20.0

Rs.15,000-Rs.20,000 13 10.8 23 19.2

Rs.20,000-Rs.25,000 8 6.7 8 6.7

Above Rs.25,000 18 15.0 28 23.3

Total 120 100.0 120 100.0

Source: Primary data

It is observed from the above frequency distribution table that no. of

sample SHG members having household assets valued at less than

Rs.10,000 decreased from 59 (49.2 per cent) to only 37 (30.8 per cent) after

joining microfinance programme. Similarly, no. of SHG members having

129

household assets valued at more than Rs.25,000 increased from 18 (15 per

cent) to 28 (23.33 per cent) after joining the microfinance. It is seen that

household assets of majority of the SHG members increased after joining

the microfinance.

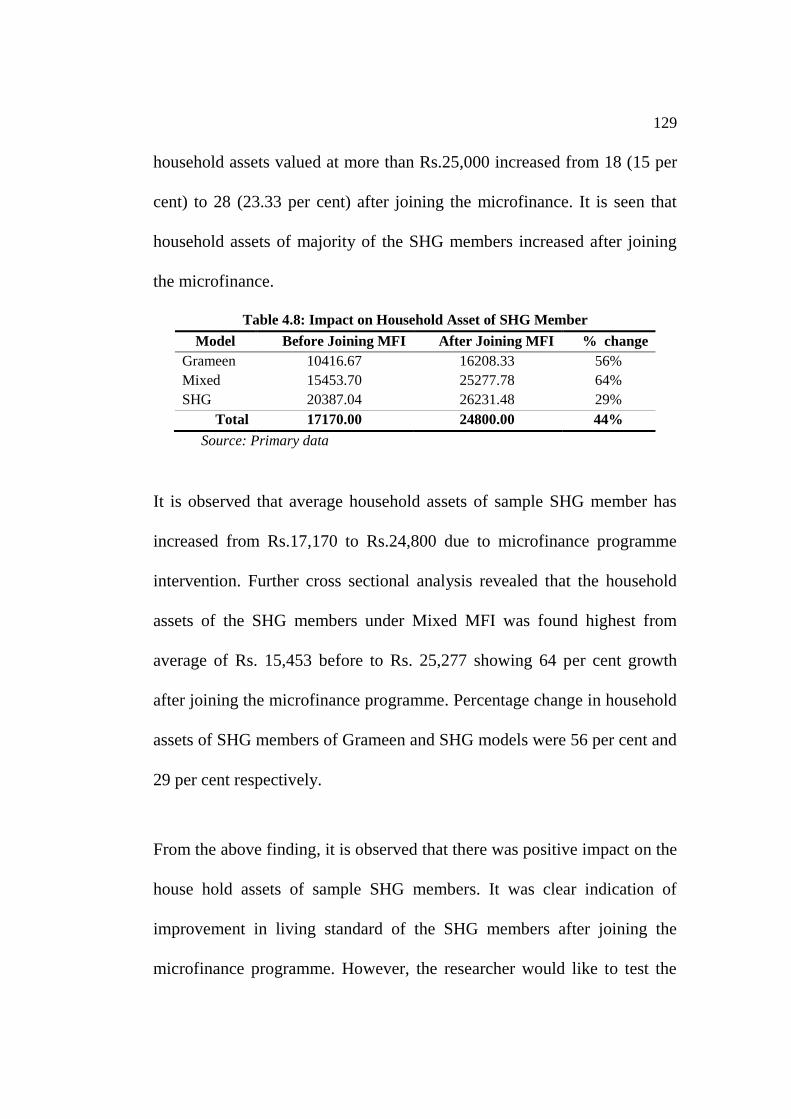

Table 4.8: Impact on Household Asset of SHG Member

Model Before Joining MFI After Joining MFI % change

Grameen 10416.67 16208.33 56%

Mixed 15453.70 25277.78 64%

SHG 20387.04 26231.48 29%

Total 17170.00 24800.00 44%

Source: Primary data

It is observed that average household assets of sample SHG member has

increased from Rs.17,170 to Rs.24,800 due to microfinance programme

intervention. Further cross sectional analysis revealed that the household

assets of the SHG members under Mixed MFI was found highest from

average of Rs. 15,453 before to Rs. 25,277 showing 64 per cent growth

after joining the microfinance programme. Percentage change in household

assets of SHG members of Grameen and SHG models were 56 per cent and

29 per cent respectively.

From the above finding, it is observed that there was positive impact on the

house hold assets of sample SHG members. It was clear indication of

improvement in living standard of the SHG members after joining the

microfinance programme. However, the researcher would like to test the

130

hypothesis before finally concluding the above finding. Therefore,

following hypothesis was formulated for testing impact on household

assets and the test result is shown below.

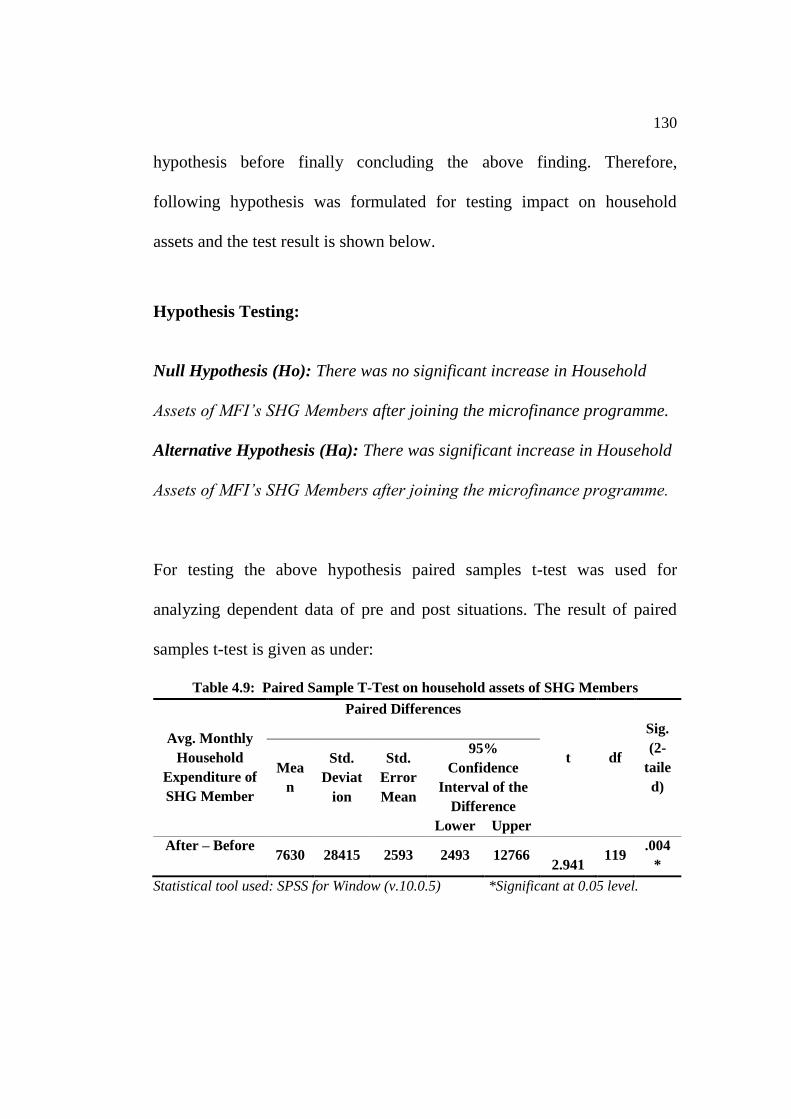

Hypothesis Testing:

Null Hypothesis (Ho): There was no significant increase in Household

Assets of MFI’s SHG Members after joining the microfinance programme.

Alternative Hypothesis (Ha): There was significant increase in Household

Assets of MFI’s SHG Members after joining the microfinance programme.

For testing the above hypothesis paired samples t-test was used for

analyzing dependent data of pre and post situations. The result of paired

samples t-test is given as under:

Table 4.9: Paired Sample T-Test on household assets of SHG Members

Avg. Monthly

Household

Expenditure of

SHG Member

Paired Differences

t

df

Sig.

(2-

taile

d)

Mea

n

Std.

Deviat

ion

Std.

Error

Mean

95%

Confidence

Interval of the

Difference

Lower Upper

After – Before

7630 28415 2593 2493 12766

2.941 119

.004

*

Statistical tool used: SPSS for Window (v.10.0.5) *Significant at 0.05 level.

131

Since t value of 2.941 is significant at = 0.05 level since p value (=0.00)

<0.05. Therefore, Ho is rejected and Ha is accepted. It can be concluded

that there was significant increase in household asset of MFI‟s SHG

Members after joining the microfinance programme. In other words, there

was significant impact of microfinance programme of NGO-MFIs on the

living standard of SHG members (indicated by household assets) of SHG

member.

4.3.4. Impact on household expenditure of SHG members

It is generally understood that household expenditure increases with the

increase in disposable income. Increase in household expenditure such as

food, clothing, children education, health care etc are also one of the

indicators of increase in household income. The analysis of basic

consumption and expenditure patterns of poor people is necessary for MFIs

while extending credit facilities. To minimize the respondents‟ biasness,

household expenditure of the SHG members were cross verified with nos.

of family members and household income as well as with similar peer

members.

132

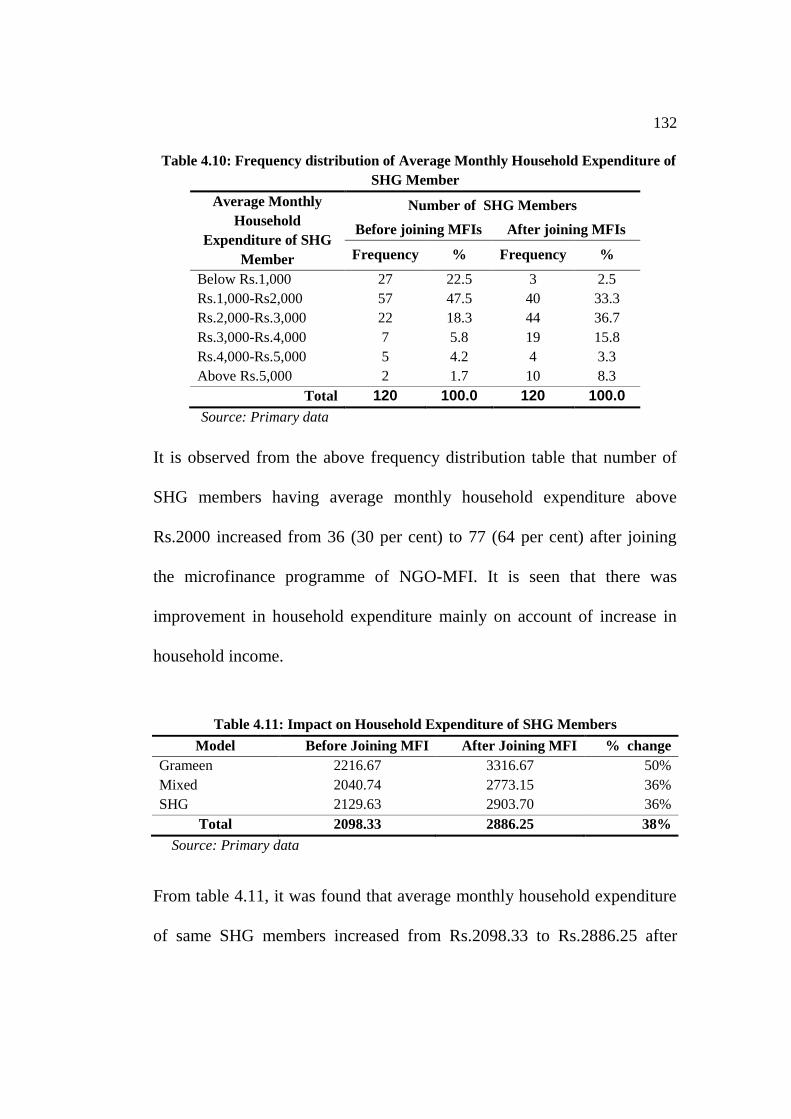

Table 4.10: Frequency distribution of Average Monthly Household Expenditure of

SHG Member

Average Monthly

Household

Expenditure of SHG

Member

Number of SHG Members

Before joining MFIs After joining MFIs

Frequency % Frequency %

Below Rs.1,000 27 22.5 3 2.5

Rs.1,000-Rs2,000 57 47.5 40 33.3

Rs.2,000-Rs.3,000 22 18.3 44 36.7

Rs.3,000-Rs.4,000 7 5.8 19 15.8

Rs.4,000-Rs.5,000 5 4.2 4 3.3

Above Rs.5,000 2 1.7 10 8.3

Total 120 100.0 120 100.0

Source: Primary data

It is observed from the above frequency distribution table that number of

SHG members having average monthly household expenditure above

Rs.2000 increased from 36 (30 per cent) to 77 (64 per cent) after joining

the microfinance programme of NGO-MFI. It is seen that there was

improvement in household expenditure mainly on account of increase in

household income.

Table 4.11: Impact on Household Expenditure of SHG Members

Model Before Joining MFI After Joining MFI % change

Grameen 2216.67 3316.67 50%

Mixed 2040.74 2773.15 36%

SHG 2129.63 2903.70 36%

Total 2098.33 2886.25 38%

Source: Primary data

From table 4.11, it was found that average monthly household expenditure

of same SHG members increased from Rs.2098.33 to Rs.2886.25 after

133

joining the microfinance programmes of MFI. Further, model wise analysis

reveals that change in the household expenditure was more in Grameen

model with 50 per cent, followed by Mixed and SHG model with 36 per

cent each.

From the above analysis, it appears that there was positive impact on the

household expenditure pattern of SHG members after joining microfinance

programme. However, to validate this finding, hypothesis testing was

carried out and the test result is described below.

Hypothesis Testing:

Null Hypothesis (Ho): There was no significant increase in household

expenditure of MFI’s SHG Members after joining the microfinance

programme.

Alternative Hypothesis (Ha): There was significant increase in household

expenditure of MFI’s SHG Members after joining the microfinance

programme.

For the pre and post situation analysis Paired samples t-test was used and

the result of the paired samples t-test is given below:

134

Table 4.12: Paired Sample T-Test on Avg. Monthly Household Expenditure of

SHG Member

Avg. Monthly

Household

Expenditure of

SHG Member

Paired Differences

t

df

Sig.

(2-

taile

d)

Mean

Std.

Deviat

ion

Std.

Error

Mean

95%

Confidence

Interval of the

Difference

Lower Upper

After – Before

787.91

625.54

57.10

674.84

900.98

13.79

119

.000

*

Statistical tool used: SPSS * Significant at 0.01 level.

Since t value of 13.79 is found significant at = 0.05 level since p value

(=0.00) < 0.05. Therefore, null hypothesis is rejected and alternative

hypothesis is accepted. Therefore, it can be concluded that there was

significant impact of microfinance on household expenditure of SHG

members.

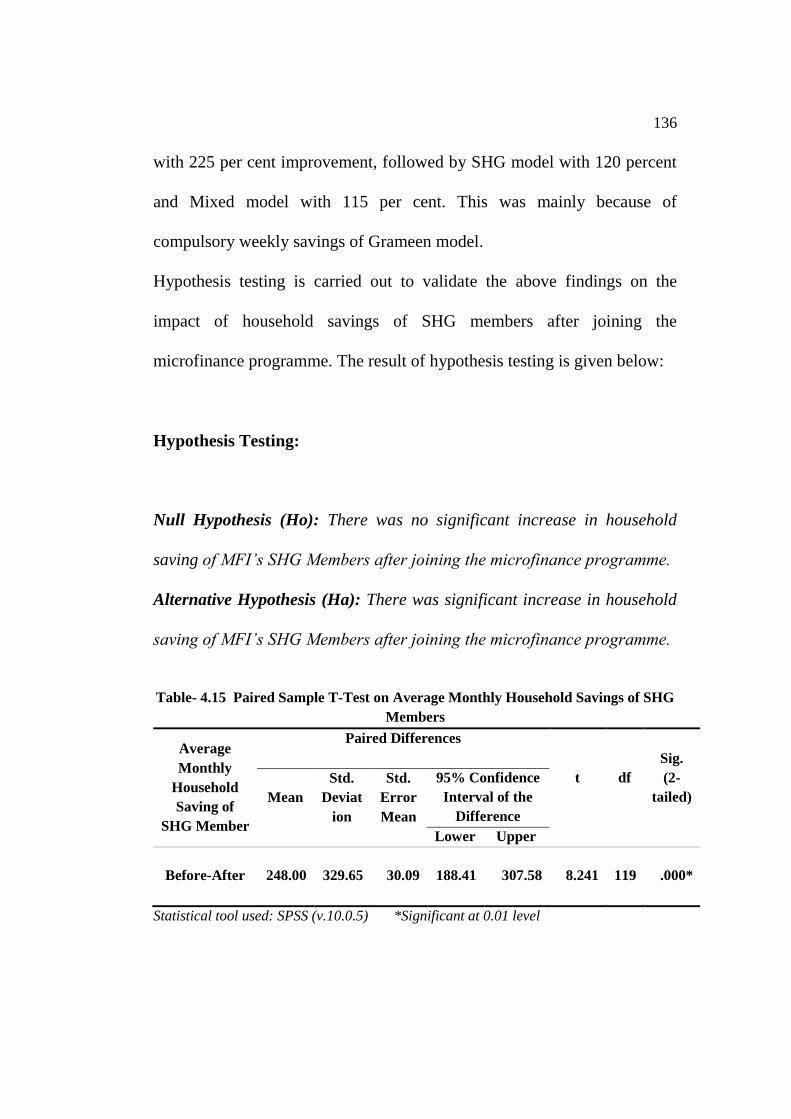

4.3.5. Impact on household saving of SHG members

For poor people, saving is very essential for meeting the emergency needs.

Most of the microfinance programme encourages SHG members for

savings and saving is made compulsory. Saving also forms a part of capital

required for starting a micro enterprise or any other income generating

activities. Therefore, member‟s saving is one of the pillars of the

microfinance programme. House saving in the context of the study covers

all kinds of savings made by SHG members as well as spouses.

135

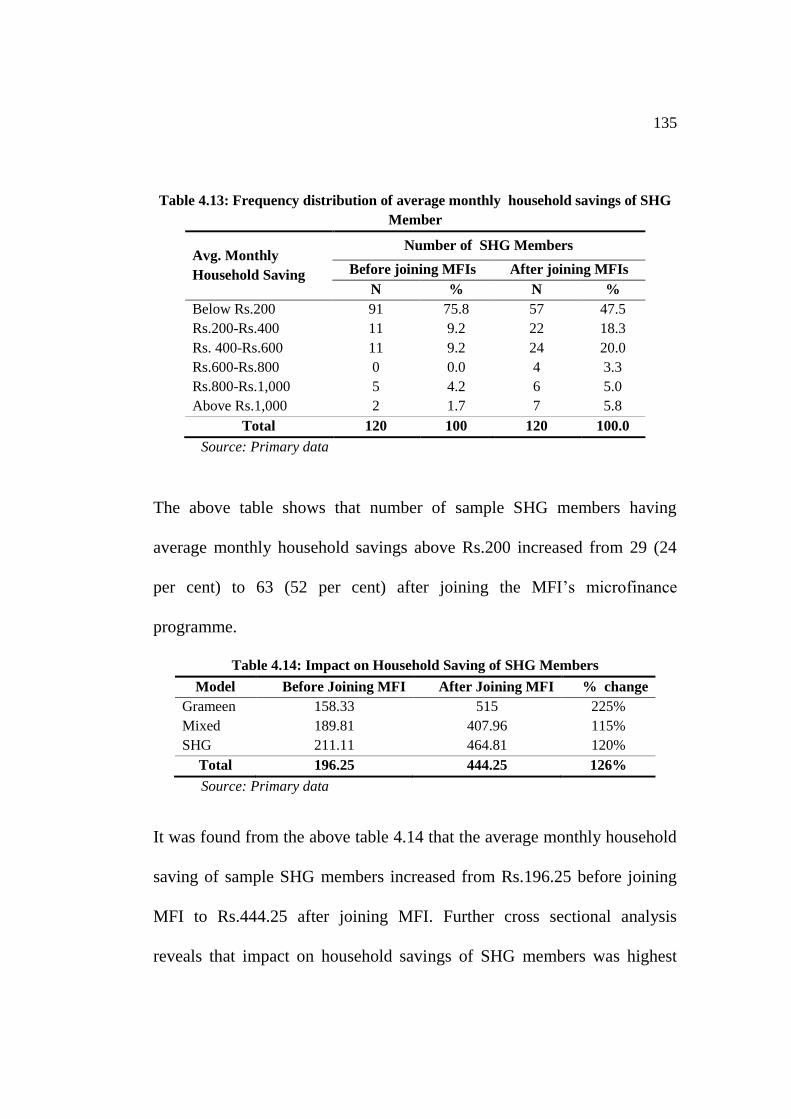

Table 4.13: Frequency distribution of average monthly household savings of SHG

Member

Avg. Monthly

Household Saving

Number of SHG Members

Before joining MFIs After joining MFIs

N % N %

Below Rs.200 91 75.8 57 47.5

Rs.200-Rs.400 11 9.2 22 18.3

Rs. 400-Rs.600 11 9.2 24 20.0

Rs.600-Rs.800 0 0.0 4 3.3

Rs.800-Rs.1,000 5 4.2 6 5.0

Above Rs.1,000 2 1.7 7 5.8

Total 120 100 120 100.0

Source: Primary data

The above table shows that number of sample SHG members having

average monthly household savings above Rs.200 increased from 29 (24

per cent) to 63 (52 per cent) after joining the MFI‟s microfinance

programme.

Table 4.14: Impact on Household Saving of SHG Members

Model Before Joining MFI After Joining MFI % change

Grameen 158.33 515 225%

Mixed 189.81 407.96 115%

SHG 211.11 464.81 120%

Total 196.25 444.25 126%

Source: Primary data

It was found from the above table 4.14 that the average monthly household

saving of sample SHG members increased from Rs.196.25 before joining

MFI to Rs.444.25 after joining MFI. Further cross sectional analysis

reveals that impact on household savings of SHG members was highest

136

with 225 per cent improvement, followed by SHG model with 120 percent

and Mixed model with 115 per cent. This was mainly because of

compulsory weekly savings of Grameen model.

Hypothesis testing is carried out to validate the above findings on the

impact of household savings of SHG members after joining the

microfinance programme. The result of hypothesis testing is given below:

Hypothesis Testing:

Null Hypothesis (Ho): There was no significant increase in household

saving of MFI’s SHG Members after joining the microfinance programme.

Alternative Hypothesis (Ha): There was significant increase in household

saving of MFI’s SHG Members after joining the microfinance programme.

Table- 4.15 Paired Sample T-Test on Average Monthly Household Savings of SHG

Members

Average

Monthly

Household

Saving of

SHG Member

Paired Differences

t

df

Sig.

(2-

tailed)

Mean

Std.

Deviat

ion

Std.

Error

Mean

95% Confidence

Interval of the

Difference

Lower Upper

Before-After

248.00

329.65

30.09

188.41

307.58

8.241

119

.000*

Statistical tool used: SPSS (v.10.0.5) *Significant at 0.01 level

137

Paired samples t-test result shows that t value of 8.241 is significant at =

0.05 level since p value (=0.00) < 0.05. Therefore, it can be concluded that

there was significant increase in household saving of sample SHG

members after joining the microfinance programme. In other words, there

was significant impact of microfinance programme on average monthly

household saving of SHG members.

4.3.6. Relationship between household income and household

expenditure of SHG members

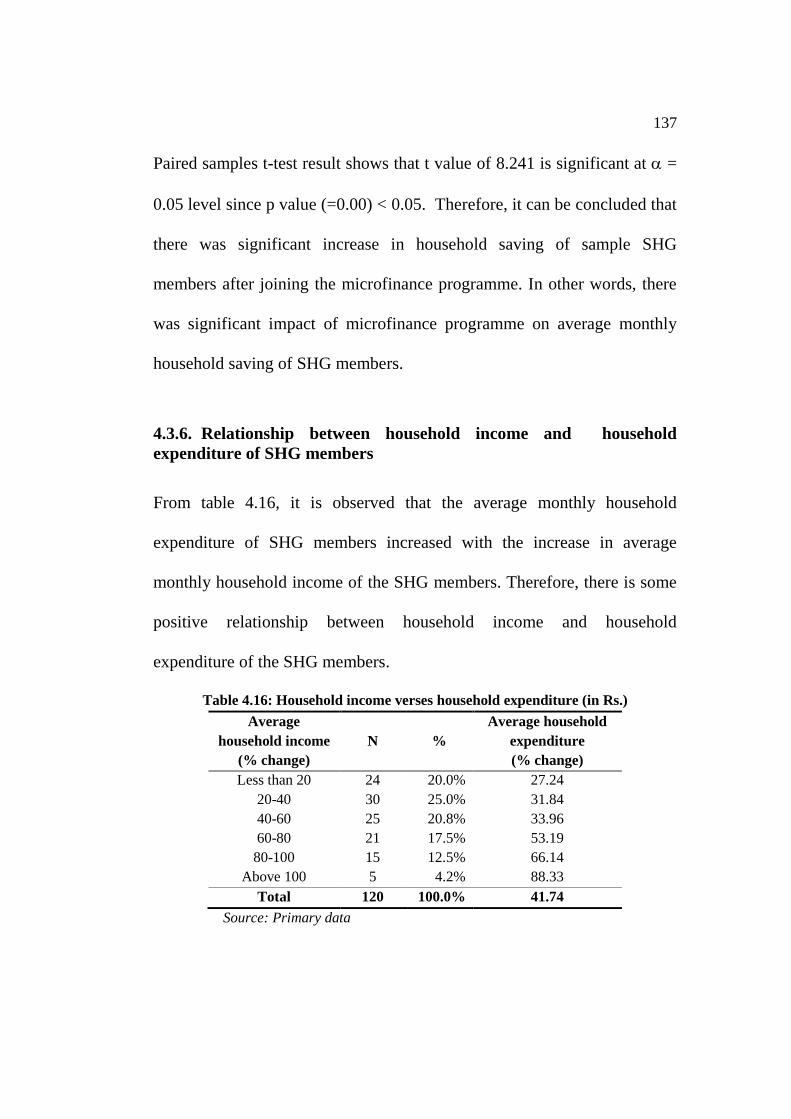

From table 4.16, it is observed that the average monthly household

expenditure of SHG members increased with the increase in average

monthly household income of the SHG members. Therefore, there is some

positive relationship between household income and household

expenditure of the SHG members.

Table 4.16: Household income verses household expenditure (in Rs.)

Average

household income

(% change)

N %

Average household

expenditure

(% change)

Less than 20 24 20.0% 27.24

20-40 30 25.0% 31.84

40-60 25 20.8% 33.96

60-80 21 17.5% 53.19

80-100 15 12.5% 66.14

Above 100 5 4.2% 88.33

Total 120 100.0% 41.74

Source: Primary data

138

33.9648

53.1933

66.1433

88.334

31.84327.2475

0

10

20

30

40

50

60

70

80

90

100

Less

than 20

20-40 40-60 60-80 80-100 Above

100

% increase in household income

% in

cre

se in

ho

useh

old

exp

en

dit

ure

Fig. 4.3. Household income verses household expenditure

However, in order to validate the above finding, a hypothesis testing was

carried out the result of which is given below.

Hypothesis testing:

Null Hypothesis (Ho): There was no significant relationship between

household income and household expenditure of SHG Members.

Alternative Hypothesis (Ha): There was significant relationship between

household income and household expenditure of SHG Members.

Karl Pearson Coefficient of correlation was used to examine the degree of

association between the household income and household expenditure of

SHG members. The result of the correlation analysis using SPSS software

is given under:

139

Pearson Co-efficient of

correlation

0.728

Significance (2-tailed) 0.01

The Pearson co-efficient of correlation (r) is 0.728 and is found significant

at = 0.05 level since p value (=0.01) <0.05. Therefore, Ho is rejected and

Ha is accepted. It can be concluded that that there was significant positive

co-relationship between household income and household expenditure of

SHG member. In other words increase in household income will result in

increase in household expenditure.

4.3.7. Relationship between household income and household saving

of SHG members

Usually, savings are made out of surplus income. It is difficult to increase

the savings without substantial increase in income. An attempt was made in

this study to examine the correlation between household income and

household savings of SHG members.

Table 4.17: Household income verses Household savings

(Amount in Rs)

Increase in

household income N %

Increase in household

saving

Less than 500 41 34.2% 119.51

500-1000 45 37.5% 191.77

1000-1500 17 14.2% 319.41

1500-2000 12 10.0% 633.33

2000-2500 1 .8% 300.00

140

Above 2500 4 3.3% 725.00

Total 120 100.0% 248.00

Source: Primary data

300

725

633.33

119.51

191.77

319.41

0

100

200

300

400

500

600

700

800

Less than

500

500-1000 1000-1500 1500-2000 2000-2500 Above

2500

Increase in monthly household income

Incre

ase i

n m

on

thly

ho

useh

old

savin

g

Fig 4.4. Household income verses household savings

From the analysis of the above table and graph, it is observed that with the

increase in household income of sample SHG members, their respective

household saving also increased. Thus, there was positive relationship

between household income and household savings of SHG members.

In order to supplement the above findings, hypothesis testing was carried

out the result of which is presented below.

Hypothesis testing:

Null Hypothesis (Ho): There was no significant relationship between

household income and household saving of SHG members.

141

Alternative Hypothesis (Ha): There was significant relationship between

household income and household saving of SHG members.

Pearson Co-efficient of

correlation (r)

0.485

Significance (2-tailed) 0.01

The Pearson co-efficient of correlation (r) between household income and

household saving is 0.485 and is found significant at = 0.05 level since p

value (=0.01) <0.05. Therefore, it can be concluded that there was

significant positive co-relation between household income and household

saving of SHG members. In other words, household saving of SHG

members increased with the increase in their household income.

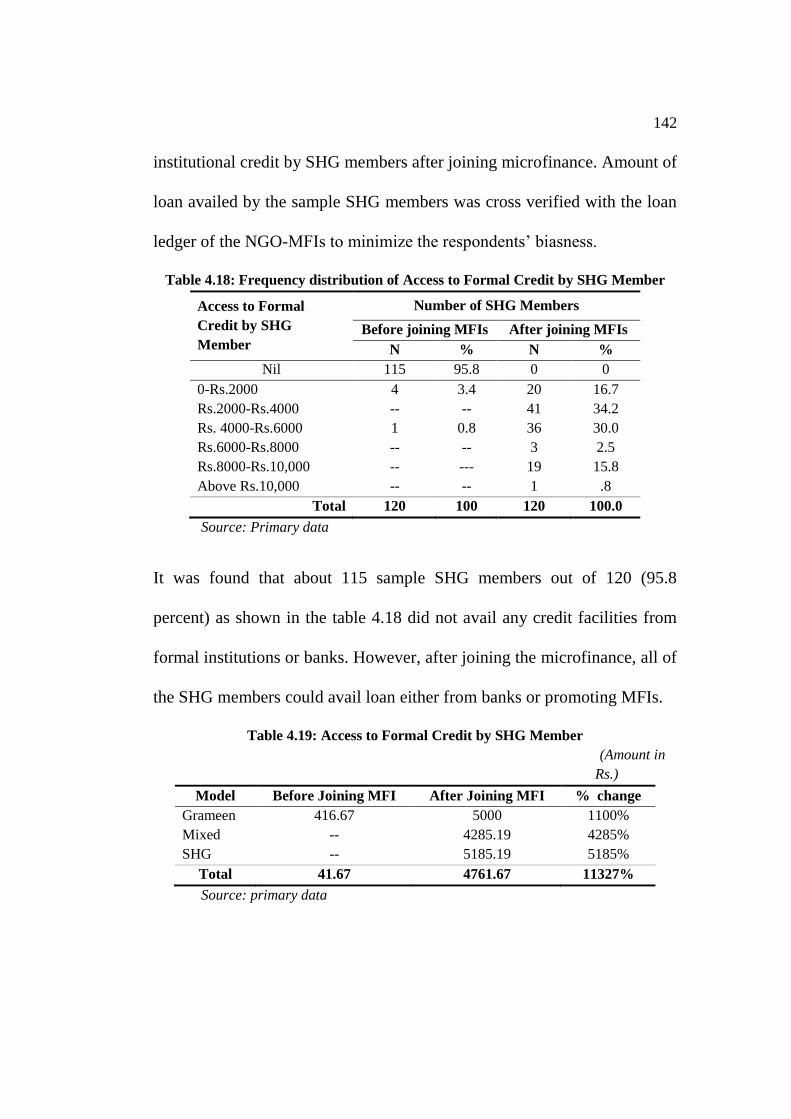

4.3.8. Access to formal credit by SHG members

Providing micro credit to the poor people for taking up income generating

activities is the basic principle of microfinance as poor people find it

difficult to access credit from formal banking system. Poor people

generally depend on local money lenders who charge high interest rates.

With the SHG-bank linkage programme or directly financing by MFIs,

most of the SHG members could avail formal or institutional credit

facilities after joining the microfinance programme. Therefore, it was

considered relevant to find out the impact on ability to access the formal or

142

institutional credit by SHG members after joining microfinance. Amount of

loan availed by the sample SHG members was cross verified with the loan

ledger of the NGO-MFIs to minimize the respondents‟ biasness.

Table 4.18: Frequency distribution of Access to Formal Credit by SHG Member

Access to Formal

Credit by SHG

Member

Number of SHG Members

Before joining MFIs After joining MFIs

N % N %

Nil 115 95.8 0 0

0-Rs.2000 4 3.4 20 16.7

Rs.2000-Rs.4000 -- -- 41 34.2

Rs. 4000-Rs.6000 1 0.8 36 30.0

Rs.6000-Rs.8000 -- -- 3 2.5

Rs.8000-Rs.10,000 -- --- 19 15.8

Above Rs.10,000 -- -- 1 .8

Total 120 100 120 100.0

Source: Primary data

It was found that about 115 sample SHG members out of 120 (95.8

percent) as shown in the table 4.18 did not avail any credit facilities from

formal institutions or banks. However, after joining the microfinance, all of

the SHG members could avail loan either from banks or promoting MFIs.

Table 4.19: Access to Formal Credit by SHG Member

(Amount in

Rs.)

Model Before Joining MFI After Joining MFI % change

Grameen 416.67 5000 1100%

Mixed -- 4285.19 4285%

SHG -- 5185.19 5185%

Total 41.67 4761.67 11327%

Source: primary data

143

From table 4.19 it was observed that the average size of loan availed from

the formal institutions or banks increased from Rs.41.67 to Rs.4761.67

after joining microfinance programme of NGO-MFIs. Among the models,

increase in access to formal credit was found highest in Grameen model as

compared to Grameen and Mixed model due to active support of Banks

under SHG-bank linkage programme. It was evident from the above

finding that access to formal or institutional credit increased after joining

after microfinance programme. However, for concluding the finding, a

hypothesis testing was carried out to test the significant improvement in

access to formal credit by SHG members the result of which is given as:

Hypothesis testing:

Null Hypothesis (Ho): There was no significant increase in access to

formal credit by MFI’s SHG Members after joining the microfinance

programme.

Alternative Hypothesis (Ha): There was significant increase in access to

formal credit by MFI’s SHG Members after joining the microfinance

programme.

Since it was the comparison of pre and post situation of the sample, paired

t-test was used.

144

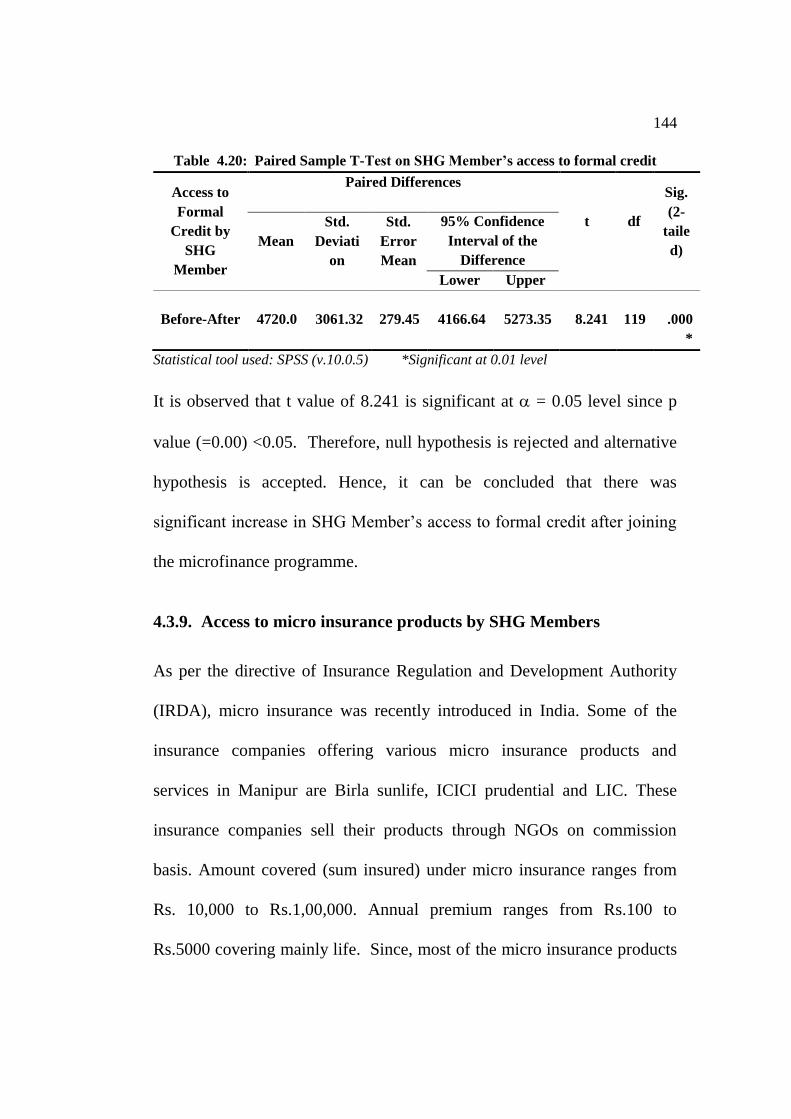

Table 4.20: Paired Sample T-Test on SHG Member’s access to formal credit

Access to

Formal

Credit by

SHG

Member

Paired Differences

t

df

Sig.

(2-

taile

d)

Mean

Std.

Deviati

on

Std.

Error

Mean

95% Confidence

Interval of the

Difference

Lower Upper

Before-After

4720.0

3061.32

279.45

4166.64

5273.35

8.241

119

.000

*

Statistical tool used: SPSS (v.10.0.5) *Significant at 0.01 level

It is observed that t value of 8.241 is significant at = 0.05 level since p

value (=0.00) <0.05. Therefore, null hypothesis is rejected and alternative

hypothesis is accepted. Hence, it can be concluded that there was

significant increase in SHG Member‟s access to formal credit after joining

the microfinance programme.

4.3.9. Access to micro insurance products by SHG Members

As per the directive of Insurance Regulation and Development Authority

(IRDA), micro insurance was recently introduced in India. Some of the

insurance companies offering various micro insurance products and

services in Manipur are Birla sunlife, ICICI prudential and LIC. These

insurance companies sell their products through NGOs on commission

basis. Amount covered (sum insured) under micro insurance ranges from

Rs. 10,000 to Rs.1,00,000. Annual premium ranges from Rs.100 to

Rs.5000 covering mainly life. Since, most of the micro insurance products

145

were routed through NGO-MFIs and was closely associated with micro

loans and saving, it was considered important to know whether there was

any significant increase in access to micro insurance product by SHG

members after joining the microfinance programme.

Table 4.21: Frequency distribution of Access to Micro Insurance Products

Access to Micro

Insurance Products by

SHG Member

Number of SHG Members

Before joining MFIs After joining MFIs

N % N %

No insurance coverage 102 85.0 51 42.5

Below Rs.25,00 -- -- 31 25.8

Rs. 25,000-Rs.50,000 6 5.0 16 13.3

Rs.50,000-Rs.75,000 -- -- -- --

Rs.75,000-Rs.1,00,000 7 5.8 14 11.7

Above Rs.1,00,000 5 4.2 8 6.7

Total 120 100 120 100.0

Source: primary data

From the above frequency distribution table, it is observed that number of

sample who did not have any insurance coverage reduced from 102 (85 per

cent) to 51 (42.5 per cent). Moreover, sum insured varied from Rs.25,000

to Rs.1,00,000. It was also found that majority (42.5 per cent) of sample

SHG members did not have insurance coverage. Therefore, there is lot of

scope for insurance products in the near future.

Table 4.22: SHG Member’s Access to Micro insurance products

Model Before Joining MFI After Joining MFI %

change

Grameen 20833.33 42727.27 105%

Mixed 18518.52 38555.56 108%

SHG 19444.44 46388.89 139%

Total 19166.67 42495.8 122%

Source: Primary data

146

Further cross sectional analysis revealed that access to insurance products

was more in SHG model with 139 per cent improvement in insurance

coverage, followed by Mixed and SHG model with 108 per cent and 105

per cent respectively.

The study also revealed that the average amount of insurance coverage of

the members of the SHG members increased from Rs.19166.66 to

Rs.42495.79 after joining the microfinance. Therefore, it was imperative to

test the hypothesis to confirm this change. Accordingly, the hypothesis

testing was carried out and the test result is summarized below.

Hypothesis testing:

Null Hypothesis (Ho): There was no significant increase in access to

micro insurance products by MFI’s SHG Members after joining the

microfinance programme.

Alternative Hypothesis (Ha): There was significant increase in access to

micro insurance products by MFI’s SHG Members after joining the

microfinance programme.

147

Paired samples t-test was used to test the above hypothesis as it was the

testing pre-post situation comparison of the same samples. The result of

hypothesis testing is presented in the table 4.23.

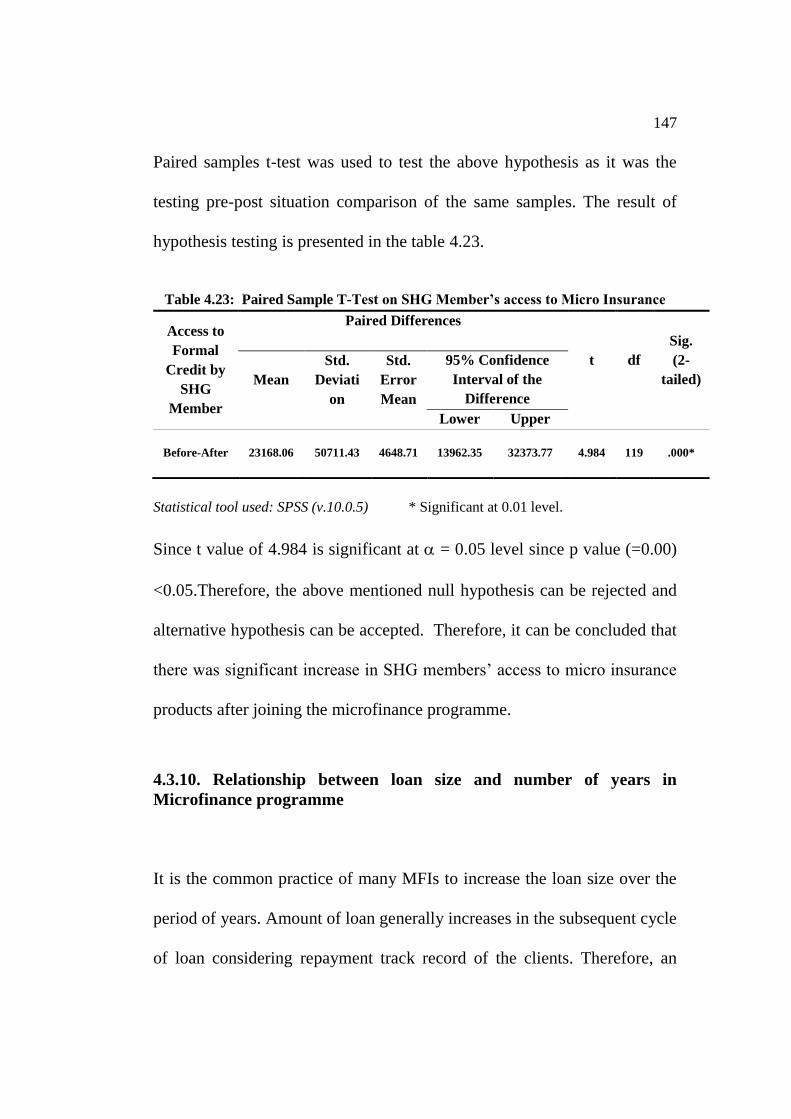

Table 4.23: Paired Sample T-Test on SHG Member’s access to Micro Insurance

Access to

Formal

Credit by

SHG

Member

Paired Differences

t

df

Sig.

(2-

tailed)

Mean

Std.

Deviati

on

Std.

Error

Mean

95% Confidence

Interval of the

Difference

Lower Upper

Before-After

23168.06

50711.43

4648.71

13962.35

32373.77

4.984

119

.000*

Statistical tool used: SPSS (v.10.0.5) * Significant at 0.01 level.

Since t value of 4.984 is significant at = 0.05 level since p value (=0.00)

<0.05.Therefore, the above mentioned null hypothesis can be rejected and

alternative hypothesis can be accepted. Therefore, it can be concluded that

there was significant increase in SHG members‟ access to micro insurance

products after joining the microfinance programme.

4.3.10. Relationship between loan size and number of years in

Microfinance programme

It is the common practice of many MFIs to increase the loan size over the

period of years. Amount of loan generally increases in the subsequent cycle

of loan considering repayment track record of the clients. Therefore, an

148

attempt was made to understand the relationship between loan size and

number of years of the SHG members in MFI‟s microfinance programme.

Average loan size of different groups according to number of years in the

group is tabulated as given under.

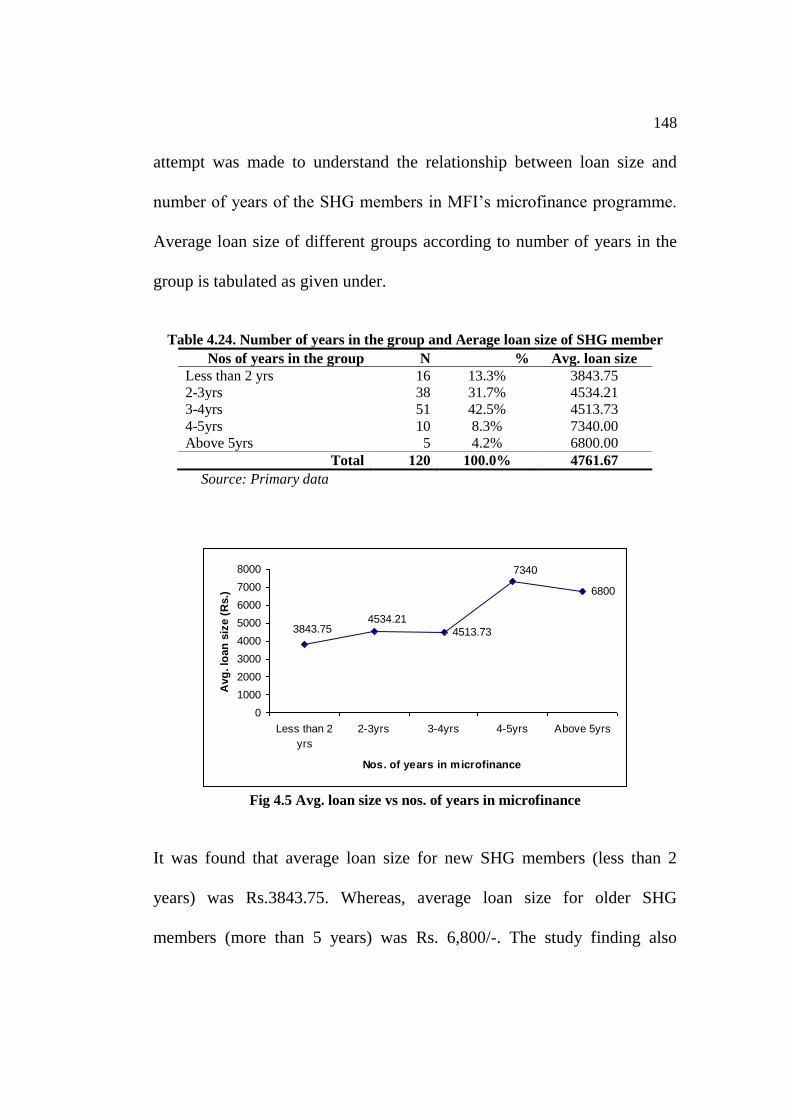

Table 4.24. Number of years in the group and Aerage loan size of SHG member

Nos of years in the group N % Avg. loan size

Less than 2 yrs 16 13.3% 3843.75

2-3yrs 38 31.7% 4534.21

3-4yrs 51 42.5% 4513.73

4-5yrs 10 8.3% 7340.00

Above 5yrs 5 4.2% 6800.00

Total 120 100.0% 4761.67

Source: Primary data

4513.73

6800

7340

3843.754534.21

0

1000

2000

3000

4000

5000

6000

7000

8000

Less than 2

yrs

2-3yrs 3-4yrs 4-5yrs Above 5yrs

Nos. of years in microfinance

Avg

. lo

an

siz

e (

Rs.)

Fig 4.5 Avg. loan size vs nos. of years in microfinance

It was found that average loan size for new SHG members (less than 2

years) was Rs.3843.75. Whereas, average loan size for older SHG

members (more than 5 years) was Rs. 6,800/-. The study finding also

149

supplemented the general assumption of positive relationship between loan

size and age of SHG members in the group. However, to confirm the

relationship between loan and age of SHG members, a hypothesis was

formulated to test the validity of this relationship. The inference drawn

from the hypothesis testing is narrated below.

Hypothesis testing:

Null Hypothesis (Ho): There was no significant relationship between loan

amount availed by SHG members and nos. of years in microfinance

programme of NGO- MFI.

Alternative Hypothesis (Ha): There was significant relationship between

loan amount availed by SHG members and nos. of years in microfinance

programme of NGO- MFI.

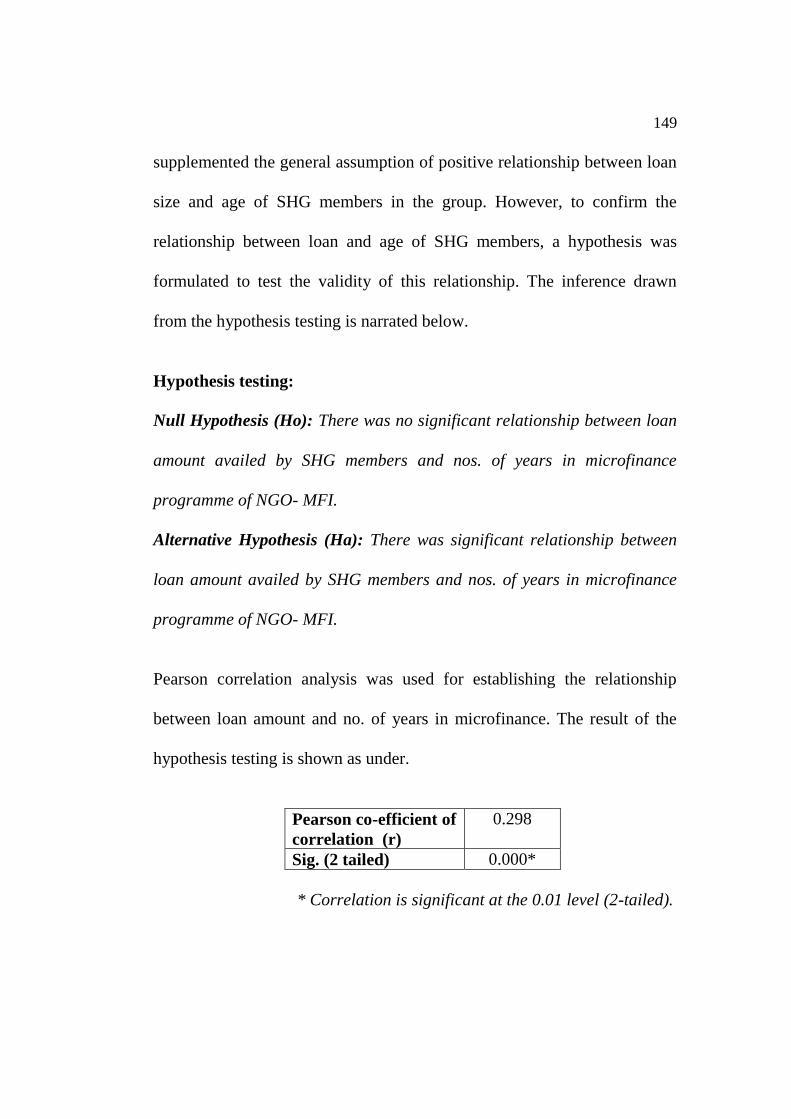

Pearson correlation analysis was used for establishing the relationship

between loan amount and no. of years in microfinance. The result of the

hypothesis testing is shown as under.

Pearson co-efficient of

correlation (r)

0.298

Sig. (2 tailed) 0.000*

* Correlation is significant at the 0.01 level (2-tailed).

150

It is observed from the above that Pearson‟s co-efficient of correlation(r) is

0.298 (positive) and is significant at = 0.05 level since p value (=0.00)

<0.05. Therefore, null hypothesis is rejected and alternative hypothesis is

accepted. It can be concluded that there was significant positive

relationship between no. of years in MFIs and loan amount availed by

MFI‟s SHG Members.

4.3.11. Days of Employment

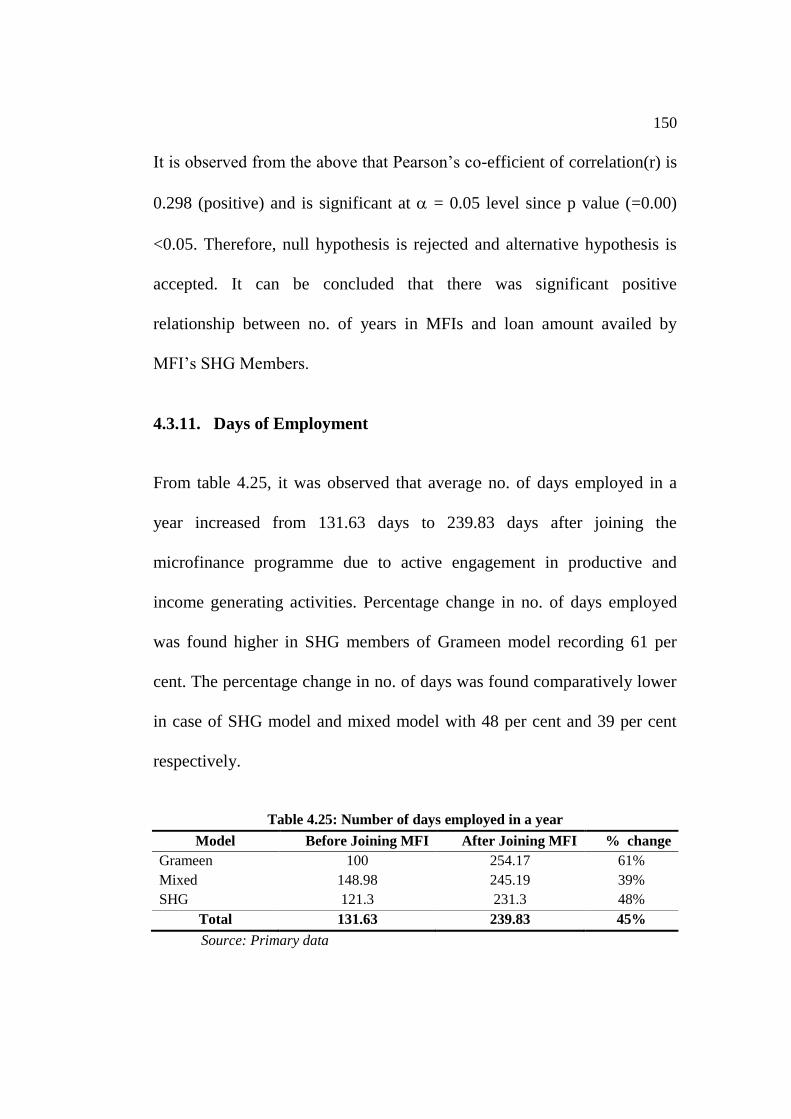

From table 4.25, it was observed that average no. of days employed in a

year increased from 131.63 days to 239.83 days after joining the

microfinance programme due to active engagement in productive and

income generating activities. Percentage change in no. of days employed

was found higher in SHG members of Grameen model recording 61 per

cent. The percentage change in no. of days was found comparatively lower

in case of SHG model and mixed model with 48 per cent and 39 per cent

respectively.

Table 4.25: Number of days employed in a year

Model Before Joining MFI After Joining MFI % change

Grameen 100 254.17 61%

Mixed 148.98 245.19 39%

SHG 121.3 231.3 48%

Total 131.63 239.83 45%

Source: Primary data

151

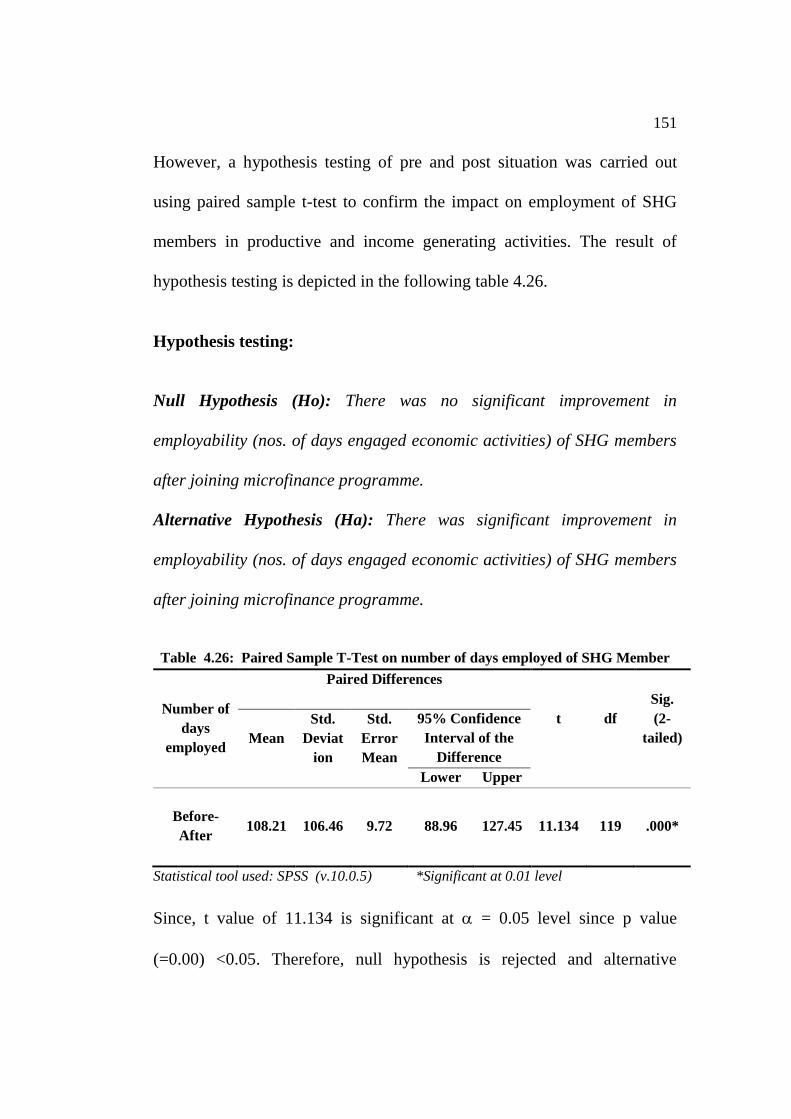

However, a hypothesis testing of pre and post situation was carried out

using paired sample t-test to confirm the impact on employment of SHG

members in productive and income generating activities. The result of

hypothesis testing is depicted in the following table 4.26.

Hypothesis testing:

Null Hypothesis (Ho): There was no significant improvement in

employability (nos. of days engaged economic activities) of SHG members

after joining microfinance programme.

Alternative Hypothesis (Ha): There was significant improvement in

employability (nos. of days engaged economic activities) of SHG members

after joining microfinance programme.

Table 4.26: Paired Sample T-Test on number of days employed of SHG Member

Number of

days

employed

Paired Differences

t

df

Sig.

(2-

tailed)

Mean

Std.

Deviat

ion

Std.

Error

Mean

95% Confidence

Interval of the

Difference

Lower Upper

Before-

After

108.21 106.46 9.72 88.96 127.45 11.134 119 .000*

Statistical tool used: SPSS (v.10.0.5) *Significant at 0.01 level

Since, t value of 11.134 is significant at = 0.05 level since p value

(=0.00) <0.05. Therefore, null hypothesis is rejected and alternative

152

hypothesis is accepted. Therefore, it can be concluded that there was

significant improvement in employability (number of days engaged in

economic activities) of SHG members after joining the microfinance

programme.

4.4. Summary of Findings

4.4.1. Economic Impact on SHG members

Personal income: There was significant improvement in personal

monthly income of the SHG members after joining the microfinance

programme. The average monthly personal income increased from

Rs.785.41 to Rs.1720.00.

Household income: There was significant improvement in

household income of the SHG members after joining the

microfinance programme. The average monthly household income

increased from Rs.2632 to Rs.3740.

Household assets: There was significant improvement in household

assets of the SHG members after joining the microfinance. The

average value of household assets increased from Rs.17,170 to

Rs.24,800.

Household expenditure: There was significant increase in household

expenditure of the SHG members after joining the microfinance.

153

The monthly household expenditure increased from Rs.2098.33

toRs.2886.25.

Household saving: There was significant improvement in household

saving of the SHG members after joining the microfinance

programme. The monthly household saving increased from

Rs.196.25 to Rs.444.25.

Access to Credit: There was significant increase in access to formal

credit by members of SHGs after joining the microfinance

programme. The maximum limit of the credit increased from

Rs.5000 to Rs.15000. And the average amount of the credit

increased from Rs.41.66 to Rs.4761.66.

Access to Micro insurance: There was significant increase in access

to micro insurance products by members of SHGs after joining the

microfinance programme. The average amount of insurance

coverage of the members of the SHGs increased from Rs.19166.66

to Rs.42495.79.

4.5. Conclusions

From the above analysis most of the NGO-MFIs were found to have

changed their roles from social intermediary to financial intermediary by

154

providing various financial services to SHGs such as loan, savings, micro-

insurance etc. It was found that there was significant economic impact on

SHG members due to NGO-MFIs‟ intervention programme. It has been

witnessed that there has been significant improvement of personal income

and household income, household savings, access to insurance products

after joining the micro finance programmes of the NGO-MFIs.