Embed Size (px)

Citation preview

Economic overview and salient features from Kenya Budget 2016

© 2016 Five Elements Advisory, all rights reserved

2

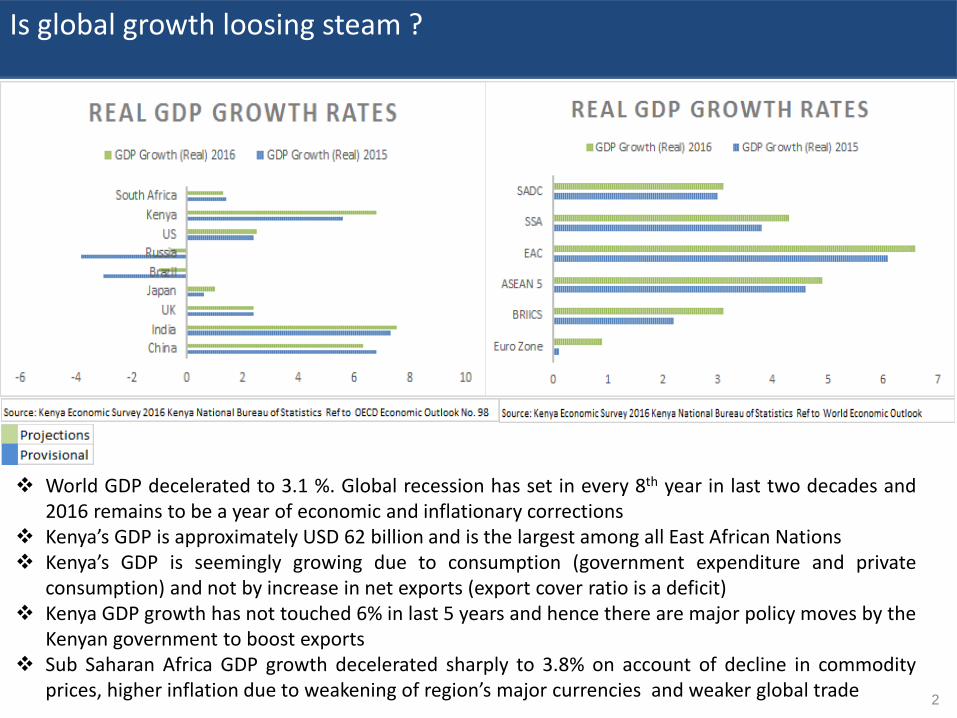

Is global growth loosing steam ?

World GDP decelerated to 3.1 %. Global recession has set in every 8th year in last two decades and2016 remains to be a year of economic and inflationary corrections

Kenya’s GDP is approximately USD 62 billion and is the largest among all East African Nations Kenya’s GDP is seemingly growing due to consumption (government expenditure and private

consumption) and not by increase in net exports (export cover ratio is a deficit) Kenya GDP growth has not touched 6% in last 5 years and hence there are major policy moves by the

Kenyan government to boost exports Sub Saharan Africa GDP growth decelerated sharply to 3.8% on account of decline in commodity

prices, higher inflation due to weakening of region’s major currencies and weaker global trade

3

Kenya not on top slot in FDI Destinations (last five years)

4

Macros

5

How the key Sector Performance tie to GDP growth

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

GDP Growth Rates YOY

Growth Rate YOY 2015 Growth Rate YOY 2014

Agriculture, Transport and Storage, Real Estate and Electricity Supply –sectors have expanded in last two years and are the key winners

Wholesale and retail trade & Information and Communication sector contribution to GDP has shown a decline over a period of last two years

6

Agriculture now accounts for 30% of GDP

-

100

200

300

400

500

2013 2014 2015

Marketed Production (in 000s Tonnes)

Tea Marketed Production Horticulture Marketed Production

Maize Marketed Production

7

Measure of growth in manufacturing sector

Shift of focus on higher value added goods in order to grow exports

Product focus on textile, apparel, leather, food processing, fish processing, agro-processing

Special Economic Zone to boost exports along with EPZs

New ISM Stamps to fight counterfeit products in the market

8

Trend indicators

23%

9

What is Kenya Exporting and which are the hot destinations

10

What is Kenya importing and which are the top importation partners

11

Horticulture (Cut Flowers)

12

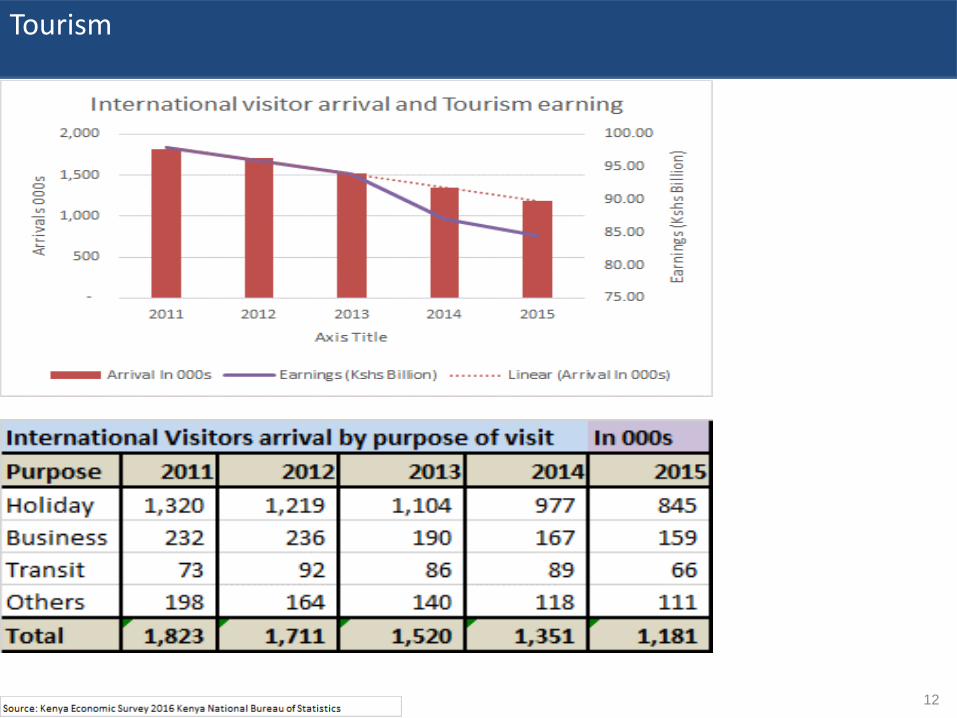

Tourism

13

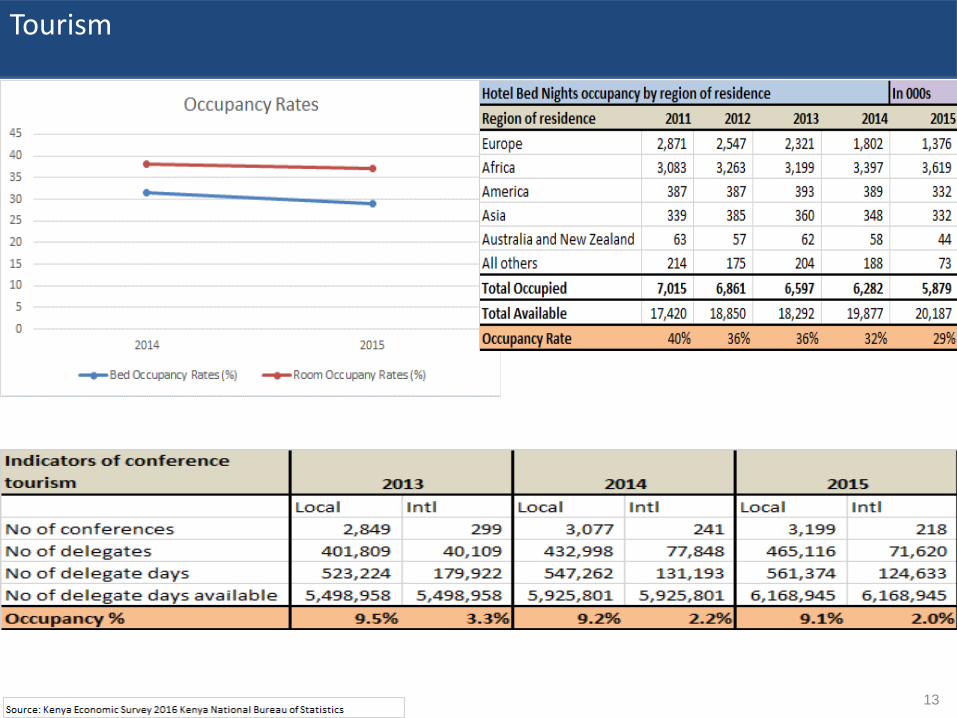

Tourism

14

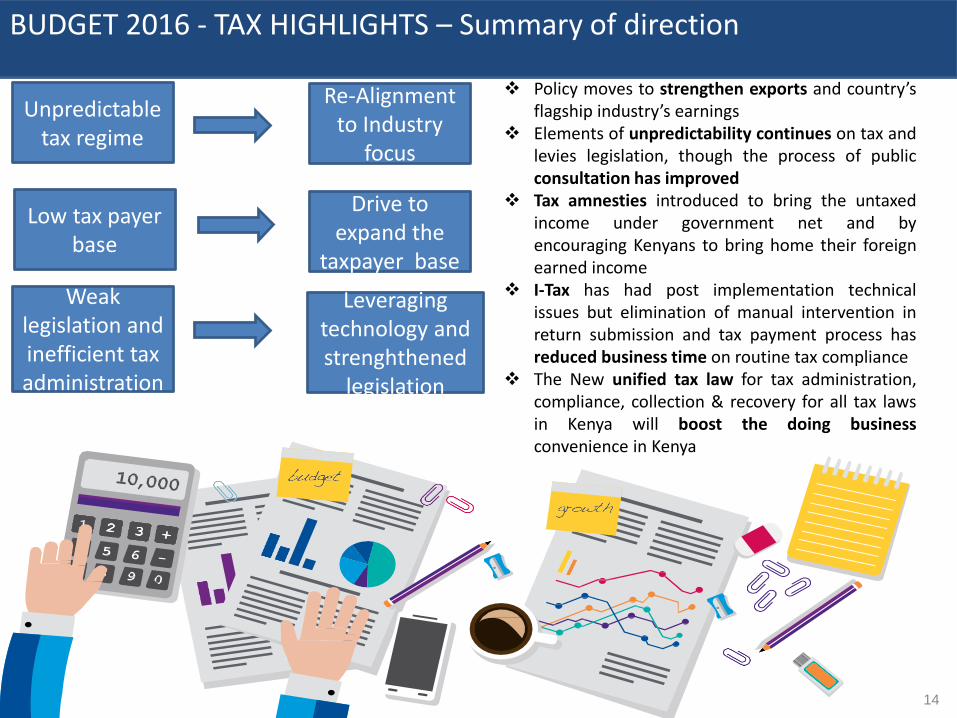

BUDGET 2016 - TAX HIGHLIGHTS – Summary of direction

Unpredictable tax regime

Re-Alignment to Industry

focus

Low tax payer base

Drive to expand the

taxpayer base

Policy moves to strengthen exports and country’sflagship industry’s earnings

Elements of unpredictability continues on tax andlevies legislation, though the process of publicconsultation has improved

Tax amnesties introduced to bring the untaxedincome under government net and byencouraging Kenyans to bring home their foreignearned income

I-Tax has had post implementation technicalissues but elimination of manual intervention inreturn submission and tax payment process hasreduced business time on routine tax compliance

The New unified tax law for tax administration,compliance, collection & recovery for all tax lawsin Kenya will boost the doing businessconvenience in Kenya

Weak legislation and inefficient tax administration

Leveraging technology and strenghthened

legislation

15

5E 2015 report card on Kenya

Where Kenya did well- Enactment of the New Companies Act to boost

Doing business convenience in Kenya

- Enactment of new SEZ (Special Economic Zone)

law to bring export driven focus of Kenya to

frontline

- Kenya joining the TFTA

- Signatory to AEOI with OECD countries to curb

Tax evasions

- Pre-shipment clearance of all imported goods for

time and cost efficiencies

- Issue of New ISM Mark to curb counterfeit

products in Kenya

- Mandatory move to I-TAX (electronic tax

compliance platform)

- CBK issuing an Average Lending rate comparison

for all commercial banks to boost transparency

- Concretization of plans for development of

industrial parks along the Standard Gauge

Railway line at Dongo Kundu in Mombasa, Voi,

Mtito Andei, Nairobi and Naivasha

Where Kenya performance lacked- Corporate earnings have be down in 2015 with many

listed companies issuing profit warning. This has

resulted in significant lower tax collections.

- In 2015, when domestic airlines in most countries

booked profits and stock prices went bullish, Kenya is

bailing out KQ

- Due to decline in commodity prices, global inflation

went to multi decade low at 3.3%. Ironically, Kenya’s

inflation was touching the CBK headroom rate of 8%

during 2015

- Kenya’s banking system needs a major fix. The Interest

rate spreads are unrealistic and SMEs are struggling to

access credit

- Three collapsed banks reflecting need to strengthen

regulator’s supervision system (CBK, CMA and ICPAK)

- Accounting scandals have hit some major Kenyan

organisations

- Value in the stock market has eroded by >25%. No IPOs

and only technical listings in last one year

- WHT VAT regime was introduced has resulted in cash

profit margin not being realized in retail/trading

business. Companies are either forced to borrow locally

at an exorbitant ROI in Kenya or curtail business or look

for off shore funding

16

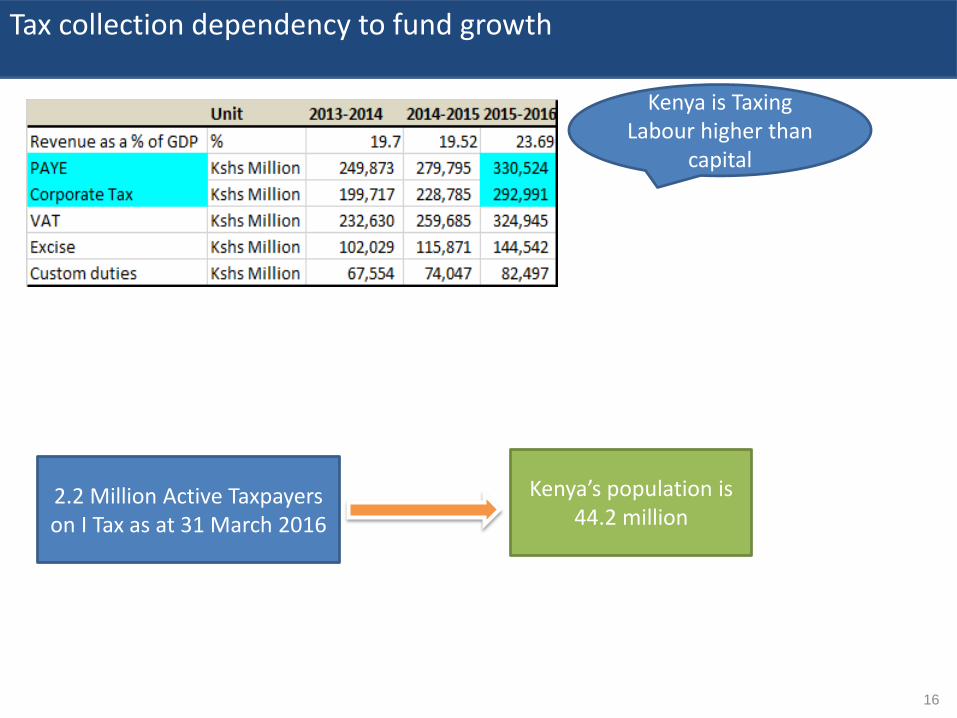

Tax collection dependency to fund growth

2.2 Million Active Taxpayers on I Tax as at 31 March 2016

Kenya’s population is 44.2 million

Kenya is Taxing Labour higher than

capital

17

Direct Taxes

Salient Corporate Tax Amendments

Tax incentive for graduate apprenticeship: Employers will now get an additional taxdeduction of 50% of the cost of the apprenticeship emoluments. This results in aadditional tax shelter to the employers of 15% of the cost of emoluments of theapprentices. In order to enjoy the incentive, employers must engage at least 10 graduates.Regulations to operationalize the incentive is expected to be gazetted soon.

Low Corporate Tax Rate Regime introduced for Residential Estate Developers: The currentannual housing supply gap in Kenya is estimated at 150,000 units per year in the low costhousing market. The finance bill proposes to reduce the corporate tax rate from 30% to20% for housing developers who construct at least 1,000 units per year.

However, with the high interest cost and high inventory overhang period in Kenya, uptake ofthis incentive by developers could be a challenge. The effective date proposed for this new lawis 1st January 2017

Appointment of Tax Representative by Non-resident Person: Where a Non-resident personwith no fixed place of business in Kenya is required to register under a tax law, suchrepresentative shall appoint a tax representative in Kenya in writing. The effective dateproposed for this new law is 1st July 2016

New Income Tax Act – light at the end of tunnel – overhaul still in progress

18

Direct Taxes

Simplified taxation of Rental Income: Finance Bill 2016 builds on the new regime of rentaltaxation brought through by Finance Act 2015. The bill proposes that residential rentalincome which exceeds more than Kshs 144,000 (Kshs 12,000 p.m) but does not exceedKshs 10 million (Kshs 833,333 p.m) will be subject to witholding tax of 10% on gross rentalincome. This translates into the fact that residential rental income of less than Kshs 12,000p.m would not be governed by the Witholding Tax provisions. Finance Bill also provides forPower to Commissioner to appoint witholding tax agents for collection of tax on rentalincome and only such person appointed shall deduct the tax.The effective date proposed for this new law is 9 June 2016

Duty to submit third party returns: Finance Bill 2016 has inserted a new section in TaxProcedure Act 2015 which requires any person, as required by the Commissioner, to furnishinformation and returns in the manner and form prescribed by Commissioner.

This is a masterstroke from Kenya Revenue Authority which has been long waiting to requireBanks and Mobile Money Service Providers to furnish information about persons who haveundisclosed income and bring such income to tax net. Even though this provision has beenincluded in Finance Bill 2016, sharing of such information will require amendments tolegislations relating to customer privacy and protection of confidentiality and hence KRA isexpected to face stiff resistance from all counters against enactment of this provision. Theeffective date proposed for this new law is 1 July 2016

19

Direct Taxes

New tax Amnesty: In respect of the undisclosed income earned outside Kenya, Finance Bill2016 proposed to provide full amnesty from tax, penalty and interest for year of incomeupto 31 December 2016, if the returns and accounts for the year 2016 are submitted on orbefore 31 December 2017. The provisions also refrains the Commissioner from followingup on the source of income. This amnesty shall not be available if a person has alreadybeen assessed for taxes or any matters relating to it or is already undergoing audit orinvestigation for undisclosed income or any matters relating to it.The effective date proposed for this new law is 1 Jan 2017

Extension of time to pay tax: Finance Bill 2016 has amended Tax Procedure Act 2015 toprovide that where a taxpayer has applied for extension of time to pay a tax due under atax law, the Commissioner shall notify the tax payer of its decision regarding extension oftime within 30 days of receiving the application. This brings clarity and certainty inlegislation for response from Commissioner.The effective date proposed for this new law is 1 Jan 2017

Tax Refund application: Finance Bill 2016 has amended Tax Procedure Act 2015 to providethat refund application for overpaid taxes (except VAT which will follow rules under VAT Act2013) shall be made within 5 years from date of payment of tax. Commissioner shall notifythe tax payer of its decision regarding application within 90 days of receiving theapplication. The effective date proposed for this new law is 1 Jan 2017

20

Direct Taxes

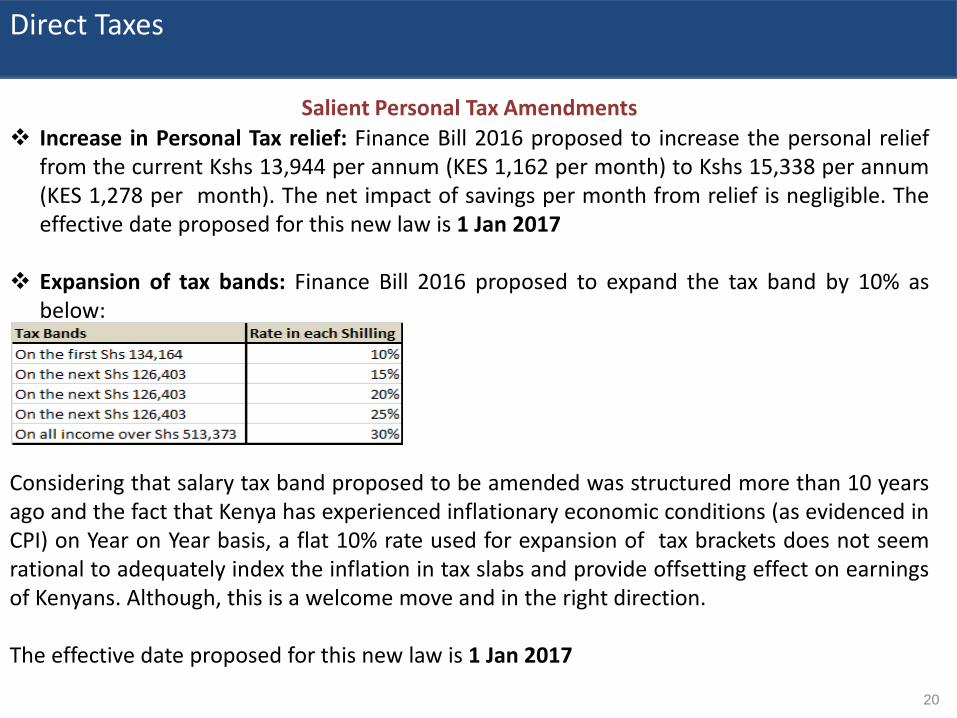

Salient Personal Tax Amendments

Increase in Personal Tax relief: Finance Bill 2016 proposed to increase the personal relieffrom the current Kshs 13,944 per annum (KES 1,162 per month) to Kshs 15,338 per annum(KES 1,278 per month). The net impact of savings per month from relief is negligible. Theeffective date proposed for this new law is 1 Jan 2017

Expansion of tax bands: Finance Bill 2016 proposed to expand the tax band by 10% asbelow:

Considering that salary tax band proposed to be amended was structured more than 10 yearsago and the fact that Kenya has experienced inflationary economic conditions (as evidenced inCPI) on Year on Year basis, a flat 10% rate used for expansion of tax brackets does not seemrational to adequately index the inflation in tax slabs and provide offsetting effect on earningsof Kenyans. Although, this is a welcome move and in the right direction.

The effective date proposed for this new law is 1 Jan 2017

21

Direct Taxes

Exemption of tax on bonus, overtime allowance and retirement benefits for low incomeemployees: Finance Bill 2016 proposes a welcome move to help low income earners tofight high cost of living in Kenya. This benefit will be available to employees whose taxableemployment income before bonus and overtime allowance does not exceed the lowest taxband.The effective date proposed for this new law is 1 July 2016

Transfers not considered for Capital Gains: Finance Bill 2016 proposes amendments toexempts transfers between following from being considered as a “Transfer of asset” forCapital Gains tax. Transfer of assets- Between Spouses- Between former spouses as part of divorce settlement or a Bona fide separation

agreement- to immediate family- to immediate family as part of a divorce or Bona fide separation agreement- to a company where spouse or a spouse and immediate family hold 100% shareholding

22

Indirect Taxes

Salient Excise Duty Amendments

Excise duty imposed on illuminating Kerosene at Kshs 7,205 per 1,000 litre.The effective date proposed for this new law is 9 June 2016

Excise duty imposed on cosmetic and beauty products at 10%The effective date proposed for this new law is 9 June 2016

Excise duty on motor vehicles amended to 20%. The provisions relating to fixed rate ofduty based on age of vehicles has been removedThe effective date proposed for this new law is 9 June 2016

Excise duty on plastic sacks and bags of following tariff number except vacuum bags forfood juices, tea and coffee (the words “Plastic shopping bags” has been deleted from TheExcise Duty Act 2015 – First Schedule – Part I)

- Tariff Number 3923.21.00 - Articles for the conveyance or packing of goods, of plastics;stoppers, lids, caps and other closures, of plastics of polymers of ethylene

- Tariff Number 3923.29.00 - Articles for the conveyance or packing of goods, of plastics;stoppers, lids, caps and other closures, of others plastics

The effective date proposed for this new law is 9 June 2016

23

Indirect Taxes

Salient VAT Amendments

Definition of “Hotel” included in VAT Act: Definition of Hotel will include service flats,service apartments, beach cottages, holiday cottages, games lodges, safari camps, bandas,holiday villas. The inclusion of definition clarifies the legal stand point on application of VATfor all premises which will be considered within the definition of “Hotel”.The effective date proposed for this new law is 1 July 2016

Provisions of Witholding VAT has been codified by insertion of proposal of new Section inthe Tax Procedure Act 2015. The person appointed as Witholding VAT agent would berequired to withhold 6% of taxable value on purchasing taxable supplies at the time ofpayment of supplies and remit the same to CommissionerThe effective date proposed for this new law is 19 Jan 2016

Service charges paid in lieu of tips shall not be considered as “supply” of accommodationor restaurant services- if the same is distributed directly to employees of the hotel or restaurant in accordance

with a written agreement between employer and employee and- service charges does not exceed 10% of price of service, excluding such service chargeThe effective date proposed for this new law is 1 Jan 2017

24

Indirect Taxes

VAT exempt on LPG

VAT exempt on entry fees in National Parks

VAT exempt on commission of Tour operators

VAT exempt on direction finding compasses, instruments and appliances for aircraft

VAT exempt on supply of garments and leather footwear manufactured in an EPZ. This is asignificant move to boost business and employment in Export Processing Zones. This willalso allow Kenyans to buy new clothes and shoes at affordable prices. However, the impactof this provision on the un-organized and popular “Mitumba” market needs to be assessed.

The effective date proposed for above exemptions is 9 June 2016

Supply of goods or taxable services to Special Economic Zone have been Zero-rated

The effective date proposed for above exemptions is 9 June 2016

25

Indirect Taxes

Salient Import Duty Amendments

Protecting the local iron and steel industry: Introduce a specific import duty rate of USD200/MT on a wide range of iron and steel products. This is in a bid to cushion localmanufacturers from unfair competition and create more jobs in the iron and steel sector.

Local production of aluminum cans: To encourage and protect the local production of aluminium cans, the Government has proposed to:- Remit, under the EAC duty remission scheme, import duty on aluminium plates and

sheets used in the manufacture of aluminium cans, and- Increase import duty on importation of aluminium cans from 10% to 25% making the

import of these products into Kenya more expensive. Exempt HVAC Air Conditioners from payment of duty in order to make them affordable to

the manufacturers of pharmaceutical products Purchases from EPZ: To encouraging growth of industries in the Export Processing Zones

(EPZ) and enhance employment creation, the Government has proposed to stay applicationof import duty (at the rate of 0%) on the purchases of made up garments and leatherfootwear from the zones

Energy efficient stoves: Reduction in import duty of stoves that use cleaner sources ofenergy (electricity, gas and other fuels) from 25% to 10%

26

Miscellaneous Taxes

Removal of ad valorem levy on tea: Since 2012, tea farmers in the Kenya have beenrequired to pay a 1% percent ad valorem levy on the sale price of each kilo of tea sold atauction. In the long run, the move may result in the improved competitiveness of Kenyantea in the international markets if the savings are reinvested towards improving yields andquality

Removal of Sugar Development Levy: 4 percent sugar development levy paid on the netprice of sugar has been abolished. This is a welcome move and we need to await and see ifthe benefit of this will be passed on to farmers and end customers

All fees of National Environmental Management Authority and the National ConstructionAuthority has been abolished: This move will be a big boost for Kenya on Doing BusinessConvenience Index as it takes away the administrative hurdles and cost. Implementationneeds to be watched out for.

Increase in Road Maintenance Levy from Kshs 12 to Kshs 18 which is now bound toincrease the cost of petroleum products and an overall impact on the inflationary effectson the economy

Special Tourism Promotion Fund to be financed by Air Passenger Service Charges:Increase by 25% for International Travel and 20% for Domestic travel

27

Insurance and Bank

Goods Imported into Kenya to be insured by Kenyan Insurance Companies: Section 20 ofthe Insurance Act expressly prohibits placement of “Kenyan Business” with non-Kenyan orforeign insurance markets except under certain circumstances. The exceptions are primarilyin respect of placement of reinsurance business outside Kenya with the laid out conditions.Despite the existence of the law, imports into Kenya continue to be on a Cost, Insuranceand Freight (CIF) basis instead of Cost and Freight basis. This business practice has deniedinsurance companies registered in Kenya significant business that could substantiallybenefit the industry and the economy. Cabinet Secretary for National Treasury has directedKenya Revenue Authority to work with the relevant stakeholders to ensure that this part ofthe law is implemented. It is expected that this move will also be beneficial to Kenyanimporters who will be able to exercise greater control and participation before the importsarrive into Kenya.

Minimum core capital for Banks: The Banking Act (CAP 488) has been amended to providefor banks and mortgage finance companies to increase their core capital to minimum Kshs5 billion by 31 December 2019. The amendment provides for a phased increase over thefinal deadline of 31 December 2019 as below:31 December 2017 – Kshs 2 Billion31 December 2018 – Kshs 3.5 Billion31 December 2019 – Kshs 5 BillionSignificant Merger & Acquisition activity along with capital raising expected in run to

deadlines

28

Our client's business challenges are our thinking and execution lab. At FE Advisory, it’s not about us. It’s about our client’s business potential. Our workplace DNA enables our clients to bridge the gaps between their business potential and excellence in business execution

We are designed to work with large and mid sizedcompanies who are looking for new levels of growth &sustainability. At the same time our advisory in customizedfor companies that are start-ups, SME’s who are passionateto turn a business idea into revenue.

Our team dynamics and a controlled client base perpartner, allows us to bring creativity in advisory solutions,poise our relationships with flexibility and bring muchneeded intimacy in execution of our projects.

Our service delivery is focused in following areas :- Strategy and business process improvement- International tax- Business intelligence and data Analytics- Risk and transaction advisory- Business advisory services

Five Elements Advisory – Brief Profile

29

FE Advisory has operating units and service delivery centers in following countries: - Kenya- Tanzania- Mauritius- Canada Our teams are organized to deliver onsite work in East Africa, South Africa, West Africa, Mauritius and CanadaFE Advisory is socially responsible and supports themission of Sadguru Sadafal Deo Vihangam YogSansthan which is under special consultative statuswith United Nations Economic and Social Council

Five Elements Advisory – Brief Profile

FE Advisory is a culturally diverse specialist team withpast experience on delivering assignments in diversegeographies.

Team comprises of- Risk auditors- Forensic experts- International tax law experts- IT experts- Data Analytic experts

30

SELECTIVE INDUSTRY EXPERIENCE

31

SELECTIVE INDUSTRY EXPERIENCE

32

Disclaimer

Information provided here is of general nature and is not intended to address the circumstancesof any particular individual or entity. The Information compiled in this document has been drawnand interpreted from the Budget Statement by Cabinet Secretary for National Treasury on 8 June2016, Finance Bill 2016, Economic Survey 2016 issued by Kenya National Bureau of Statistics,Central Bank of Kenya website, UCTAD Knowledge resource website, East Africa CommunityCustoms Resources. A misstatement or omission of any fact or a change or amendment in any ofthe facts and assumptions we have relied upon may require a modification of all or a part of thisdocument. Although we endeavor to provide accurate and timely information, there can be noguarantee that such information is accurate as of the date of it is received or that it willcontinue to be accurate in future. No one should action such information without appropriateprofessional advice and after a thorough examination of the particular situation

33

Contacts:

Jitendra SwalyPartnerFive Elements AdvisoryM: +254 7373 50969

Simant PrakashManaging PartnerFive Elements AdvisoryM: +(254) 789 399 685

Imran JumaPrincipalFive Elements AdvisoryM: +(254) 724 156 222

Kenya | Tanzania | Mauritius | Canada

© 2016 Five Elements Advisory, all rights reserved

THANK YOU