Embed Size (px)

DESCRIPTION

Economics study book USQ

Citation preview

ECO1000

EconomicsFaculty of Business and Law

Study book

Published byUniversity of Southern QueenslandToowoomba Queensland 4350Australiahttp://www.usq.edu.au

© University of Southern Queensland, 2013.2.

Copyrighted materials reproduced herein are used under the provisions of the Copyright Act 1968 as amended, or as a result of application to the copyright owner.

No part of this publication may be reproduced, stored in a retrieval system or transmitted in any form or by any means electronic, mechanical, photocopying, recording or otherwise without prior permission.

Produced by Learning Resources Development using the ICE Publishing System.

Table of contentsPage

Module 1 – Introduction to economics 1Learning objectives 1Learning resources 1

Text 1Essential 1

1.1 Introduction 11.1.1 The economic way of thinking 21.1.2 The language of economics 3

1.2 Thinking like an economist 31.2.1 Economic models 4

1.3 Using graphs in economics 51.4 Production economics 6

1.4.1 Scarcity and opportunity cost 6Summary 9

Module 2 – How the market works 11Learning objectives 11Learning resources 11

Text 11Essential 11

2.1 Introduction 112.2 Tools of analysis: demand 12

2.2.1 The concept of demand 122.2.2 The demand curve 122.2.3 The downward-sloping demand curve 142.2.4 Movements along and shifts of the demand curve 142.2.5 Reasons for the demand curve to shift 15

2.3 Tools of analysis: supply 152.3.1 The concept of supply 152.3.2 A single firm’s supply 162.3.3 Market supply 172.3.4 Movements along and shifts of the supply curve 182.3.5 Reasons for the supply curve to shift 18

2.4 Tools of analysis: market equilibrium 182.5 Elasticity 20

2.5.1 Introduction 202.5.2 The concept of elasticity 212.5.3 Price elasticity of demand 212.5.4 Cross-price elasticity of demand 212.5.5 Income elasticity of demand 212.5.6 Price elasticity of supply 22

2.6 Economic efficiency and market failure 232.6.1 Consumer and producer surplus and economic efficiency 232.6.2 Price floors and price ceilings 242.6.3 The economic impact of taxes 24

Summary 25

Module 3 – Firms and market structure 27Learning objectives 27Learning resources 27

Text 27Essential 27

3.1 Introduction 273.2 The concept of cost revisited 283.3 The short run production function 293.4 Short run cost functions 303.5 Long run average cost 303.6 The model of perfect competition 32

3.6.1 Introduction 323.6.2 The perfectively competitive model: in the short run 323.6.3 The entry and exit of firms in the long run and efficiencies in perfect competition 32

3.7 Monopoly markets 353.7.1 Monopoly model 353.7.2 Economic efficiency and government regulation in monopoly market 36

Summary 37

Module 4 – Macroeconomic Foundations 39Learning objectives 39Learning resources 39

Text 39Essential 39

4.1 Introduction 404.2 GDP measures total production 40

4.2.1 Measuring the size of the total production 404.2.2 The circular flow model of an economy 414.2.3 Economic growth 42

4.3 Unemployment and inflation 434.3.1 Unemployment 434.3.2 Inflation 44

4.4 The business cycle 454.5 Aggregate demand and aggregate supply 45Summary 47

Module 5 – Monetary and Fiscal policy 49Learning objectives 49Learning resources 49

Text 49Essential 49

5.1 Introduction 505.2 Money, banks and the Reserve Bank of Australian 515.3 Monetary policy 525.4 Fiscal policy 54Summary 55Appendix 5.1 (optional reading, and not examinable) 59

Epilogue: brief review of selected schools of thought in economics 59

ECO1000 – Economics 1

Module 1 – Introduction to economics

Learning objectivesOn successful completion of this module, you should be able to:

● discuss the three important ideas: people are rational; people respond to incentives; optimal decisions are made at the margin

● understand the issues of scarcity, and trade-offs

● understand the concepts of opportunity cost, the difference between centrally planned economy and market economy, and the issues associated with efficiency and equity

● understand the role of models in economic analysis

● understand normative and positive analysis, and distinguish between microeconomics and macroeconomics

● apply graphical techniques in economic analysis and understand their interpretations

● apply the model of the ‘production possibilities frontier’ to illustrate the concepts of opportunity cost and economic growth

● understand comparative advantage and explain how it is the basis for trade

● explain the basic idea of how a market system works.

Learning resources

TextHubbard, Garnett, Lewis, and O'Brien, 2013, Economics, chapters 1 and 2 ; appendix to chapter 1.

EssentialStudy book: module 1.

1.1 IntroductionThis module introduces you to the study of the social science of economics. As a social science, economics provides an orderly approach to theory development, to the construction and testing of models, and to the analysis of economic policy. Practical economics seeks to focus the power of reason on the economic issues of our times.

© University of Southern Queensland

2 ECO1000 – Economics

When starting the study of economics, you have to learn the assumptions and language of this new way of thinking. One of the difficulties with learning economics is that it can take some time to get used to this approach to everyday life. Some people are fortunate, in that they grasp the principles quite quickly; however, for most, it takes some time. Therefore, the course team believes that it is best to start slowly with a few concepts and then add to them as you work through the course.

As with learning another language, you first learn very basic words, then you move to phrases, and then you ‘learn sentences’. Finally, you learn how to be ‘grammatically accurate’; but this can take many years. Due to time constraints, this course can only take you to the very early stage of ‘learning sentences’ or, in this case, applying concepts.

1.1.1 The economic way of thinkingEconomics provides a set of analytical tools, but it is also a way of thinking. In this course we are showing you some of those basic tools and trying to encourage you to understand the ‘economic way of thinking’. This way of thinking is characterised by a ‘language’ in which words have a meaning specific to economics. As with any language, you need to understand the terms and their definitions. However, economics is most importantly a particular way of looking at individual, group and national behaviour. In other words, economics provides another way of looking at our domestic lives, our working lives and national and international politics. Some economists have argued that even marriage, crime and human life can be analysed in terms of economic choices.

It may help you to understand the main concepts in this course if you keep posing the question ‘how would an economist interpret this?’ It may also help to relate the concepts to everyday situations; indeed, newspaper discussions on economics can provide some good material for consideration. However, remember that this is an introductory course, and we use a lot of assumptions to simplify the concepts for teaching purposes. Therefore, you cannot always get the ideas and examples to exactly conform to real-world situations. Try to think of the concepts presented at this level as being limited to the illustration of general tendencies.

An important part of the language of economics is maths. This course has been designed to de-emphasise the maths (believe it or not), but some knowledge of maths is useful. Apart from the use of simple algebraic formulae in economics, there are various ‘tools’ to show data and to illustrate or represent concepts. Economic data is presented in three main ways:

● descriptive prose (written work). Economics, as with any social science, relies heavily on descriptions of what has happened and what is happening

● tables of numbers that can be used to identify trends or points of note. Tables are used throughout the text and it is important that you learn to interpret information from them

● graphs of key indicators and measures, usually over time or in relation to each other. These are usually based on tables and are really a variation of the above.

Most of the course is based on written explanation, as you would expect when learning a social science. While there are other ways of representing economic ideas, this remains one of the most fundamental. Being able to explain an idea or concept is still a real test of understanding. That is why we use assessment, such as the written assignment and the extended response questions, in the exam.

© University of Southern Queensland

ECO1000 – Economics 3

There are also algebraic equations, where symbols are used to represent variables. These are occasionally used to calculate real numbers, for example calculating the size of an economy, but they are often symbolic. That is, the equation is just a shorthand way of explaining a relationship.

While the obvious focus of the course is on content, we also want you to develop skills in description and interpretation. Therefore, it is very important that you take the opportunity to develop the capacities to interpret data and to identify concepts as they are variously expressed.

1.1.2 The language of economicsYou will come across many terms used throughout this course and also in your career. Economics is the language used in politics, the media, and in business. It will be everywhere in your daily lives. The level of wages you receive, your job security and the interest you pay on a home loan are all indicators of economic activity and they will all be discussed in economic terms. If you want to interpret what is happening to you, you must be able to speak the language. You may find it useful to refer frequently to the glossary of terms at the back of the text.

1.2 Thinking like an economistEconomists get ‘bad press’. At best they are often portrayed as people who deal entirely with the abstract, having little or no experience of the ‘real world’. At worst, they are portrayed as hard-hearted, narrow people, seeking to reduce human activities to monetary values, and proposing policies that add to human misery. However, many economists are engaged with questions of poverty, development, fairness, distribution, the environment and so on and they do wish to make the world a better place, though often disagreeing with each other about how that might be achieved. At the heart of the activity of the economist lies the development of theories and models. In developing these theories and models, economists have sought to bring a particular way of thinking, which is really common sense plus careful reasoning and the use of data, to make the world a better place. It is a difficult task.

People must make choices as they try to attain their goals. These choices reflect trade-offs people make because we live in a world of scarcity; although our wants are unlimited, the resources available to satisfy our wants are limited. Economic models are simplified versions of some aspects of economic life. Economists construct models and use them to analyse economic issues. Economics focuses on the decisions buyers and sellers make through markets. Economists assume people (1) are rational, (2) respond to economic incentives, and (3) make optimal decisions at the margin.

Economists often focus on decision-making ‘at the margin’ on the grounds that when making choices, economic agents (be they consumers, firms or governments) focus on the benefits and costs associated with the extra, or marginal, activity. For example, when considering whether or not to buy another pizza, a consumer would calculate (however roughly) the marginal cost and the marginal consumption benefit; a business when considering whether or not to hire another saleswoman would calculate the marginal cost of employing the worker and the marginal revenue to be gained from her services; and a government when considering whether or not to build another hospital, would consider the extra costs and extra benefits

© University of Southern Queensland

4 ECO1000 – Economics

from constructing and running another hospital. For economists, economic agents will only make decisions to undertake the extra activity if the marginal benefit is equal to, or greater than, the marginal cost. Try a little introspection on this point; ask yourself if this what ‘goes through your mind’ when you make consumption choices (for example, to have another drink; to buy another loaf of bread; or to spend an extra week on holiday).

Each society faces the economic problem of having a limited amount of resources, and so can produce a limited amount of goods and services. Each society faces trade-offs, particularly when answering three questions: (1) What goods and services will be produced? (2) How will the goods and services be produced? (3) Who will receive the goods and services produced? Societies organise their economies in two main ways to answer these questions. A society can have a centrally planned economy characterised by extensive government decision making. Or a society can have a market economy in which the decisions of households and firms interacting in markets allocate resources. Most developed countries have predominately market economies with some central government regulation or control. Market economies tend to allocate resources more efficiently than do centrally planned economies, but efficient outcomes may not be perceived as fair. Determining what is a fair or equitable outcome calls for the application of normative economic analysis – what ought to be. Positive economic analysis is concerned with what is. While most or all economists can agree on the results of positive economic analysis, they may disagree widely on normative economic issues.

Microeconomics is the study of how individual choices are made by households, business firms, and government. Macroeconomics is the study of the economy as a whole.

1.2.1 Economic modelsIt is important to realise that economics is a social science, not a natural science. In other words, the ‘economy’ is not like a mechanical system, even though some economists and politicians speak as if it were. Economics is about the study of human activity in relation to the production, distribution and exchange of goods and services. The behaviour of humans is not always, or perhaps ever, scientifically predictable; however, economists have developed a range of techniques for trying to make sense of economic activity.

The ‘real’ world, that is, the world in which you live, is very complicated. Consequently, economists have to use ‘pretend economies’ to simplify it. These pretend economies, or models, are simplifications of the real world. From the models, you can derive general propositions about the relationships and the behaviour of groups of individuals. Such propositions are developed using economic theories. Remember, you are taking an introductory course and simplification is required; don’t try to make everything fit neatly into real world situations.

Theoretical reasoning, followed by data analysis, helps economists to explain the operation of the economy and to develop solutions to economic problems. An economic model cannot be so simple that it is completely unrealistic, but neither must it be so complex that important interrelationships are lost in the detail.

Finally, while the models and graphs might seem scientific and objective, it is important to note that they are very much based on certain assumptions about how people do, or will, behave in particular circumstances. When studying a model, always look for the assumptions, be they explicit or implicit, the logical reasoning used, and the conclusions reached.

© University of Southern Queensland

ECO1000 – Economics 5

Reading activity 1.1Study chapter 1 of the text (Hubbard et al.).

Make sure that you can:

● Discuss the three important economic ideas: people are rational; people respond to incentives; optimal decisions are made at the margin

● explain the social science of economics as the study of scarcity and choice

● understand the role of models in economic analysis

● distinguish between ‘positive’ and ‘normative’ economics

● distinguish between microeconomics and macroeconomics.

Learning activity 1.1NB: This is the essential set of exercises. If you have additional time, you should practise the quizzes and tests in MyEconlab (Check the StudyDesk on how to access MyEconlab).

1.1.1 Answer Review Questions 1-10 and Problems and Applications 2, 3, 4, 5, 11, 12, 14, 15, 16, 17, 20 at the end of chapter 1 (check your answers with those from the StudyDesk).

1.3 Using graphs in economicsIt is common practice in economics to use graphs to illustrate relationships among economic variables and to work out the effects of changes in economic circumstances. Accordingly, it is necessary that we pause to ensure that the essential aspects of graphical analysis are understood.

Reading activity 1.2Study Appendix to chapter 1 of the text (Hubbard et al.).

Make sure that you can:

● plot graphs of economic data to show the relationship between two variables

● use graphs to illustrate positive and negative relationships between economic variables

● calculate the slopes of a straight line and a curved line

© University of Southern Queensland

6 ECO1000 – Economics

Learning activity 1.2NB: This is the essential set of exercises. If you have additional time, you should practise the quizzes and tests in MyEconlab.

1.2.1 Answer all questions in 'Problems and Applications' for the appendix to chapter 1 (check your answers with those from the StudyDesk).

1.4 Production economics

1.4.1 Scarcity and opportunity costIn our previous study, we introduced economics as the science of scarcity and choice. The problem of scarcity is often developed in terms of the three fundamental economic questions: ‘what to produce’, ‘how to produce it’, and ‘for whom to produce it’? In this presentation of the problem of scarcity, two very important economic concepts emerge: ‘opportunity cost’ and ‘marginal analysis’.

Opportunity costOne of the most important concepts in economics is that of opportunity cost. This is a concept that has application in many aspects of our lives. Indeed, for every action we undertake, there is an opportunity cost (or something foregone). Every time you spend time or money, you make a choice and you forego all other opportunities. For example, if you go out in the evening to socialise, you forego the opportunity to watch television, or to study or to spend time with your family. You cannot claim you will catch up on those things later, because of the time factor. In economics, there is always scarcity. For humans, time is limited and the hours used cannot be recaptured. It is the same with spending. If you buy movie tickets, you cannot use that money for a meal, savings or for the purchase of DVD. You are making choices all the time and the cost is to be thought of in terms of what has been foregone. Accordingly, opportunity cost may be defined as:

The value of that which must be given up to acquire or achieve something.

Opportunity cost is therefore expressed in the terms of what is ‘given up’. Strictly speaking, opportunity cost is to be thought of in terms of the next best option that has been given up.

Here is an example:

● A visit to the movies. You go to the movies instead of studying. The financial cost is the entry fee (say $10) but an additional opportunity cost of going to the movies is the foregone 2 hours of study. Thus, the opportunity cost of going to the movies is $10 + the value of 2 hours of study.

© University of Southern Queensland

ECO1000 – Economics 7

Production possibilities frontier (PPF)Illustrating the concept of opportunity cost, the production possibility frontier is a valuable tool used to examine the consequences of production initiatives, changes in the resource mix and developments in technology. It is our first example of an economic model.

Production possibility frontiers may be used to graphically demonstrate the impact of inefficiency within the economy. In Australia, during the 1980s and the 1990s, an appreciation of this inefficiency led to the introduction of widespread industrial reform measures designed to deliver better work practices and, consequently, improvements to net community welfare. These changes, taken together, became known as microeconomic reform.

The PPF delineates what it is possible to produce from what it is not possible to produce. Individuals have PPFs in relation to particular goods that they can produce. That is, each of you has a limit to what you could produce, within a particular time frame, whether that is pages of typing, sales of goods or house painting. In similar fashion, we can think of the PPF for any economy. Given a number of assumptions, the PPF for an economy shows the combinations of goods that can be produced with full and efficient use of available resources.

The PPF is an example of an economic model that has been constructed to show the key relationships that underlie production in any economy. It is usually represented in terms of a graph with two goods shown on the axes, and is shown as a ‘bowed outwards’ curve. Essentially, it shows the production ‘boundary’ for an economy and the fact that, if the economy is producing efficiently, it can only produce more of one good by giving up increasing amounts of the other good (the ‘law of increasing opportunity costs’).

Note that, conceptually, we can apply the PPF to many resource-use questions (for example, the production of ‘defence’ or ‘peacetime’ goods; the production of a ‘clean environment’ or ‘ordinary’ industrial output; and the production of ‘health goods’ or ordinary consumer goods).

Note, also, that we may consider a change (such as an increase in the output of one good at the expense of the output of another) that is modelled by a movement along a given PPF, or a change that is modelled by a shift of the PPF (such as a change in technology that enables more of all goods to be produced from a given quantity of resources.

Specialisation and the gains from tradeThe logic that flows from the concept of opportunity cost is that if we, as individuals, business, people and citizens, want economic efficiency and to maximise the outcomes of our economic efforts, then both individuals and nations should ‘specialise’. Specialisation is the cornerstone of the modern economy. The principle is that it is theoretically more efficient to specialise in production and then exchange or trade, than to try and be fully self-sufficient.

The argument that nations gain by specialising in production and trading is based on the theory of comparative advantage. Essentially, this says that a country with a comparative advantage in the production of a good or service should specialise in the production of that good or service and exchange it for goods and services from other countries. A country is

© University of Southern Queensland

8 ECO1000 – Economics

said to have a comparative advantage when it has a lower opportunity cost of production than do its trading partners.

It is important to distinguish between ‘comparative advantage’ and ‘absolute advantage’. Whereas comparative advantage exists when a country has a lower opportunity cost of production, absolute advantage refers to the situation in which a country has a lower absolute cost of production in terms of resources used.

The market systemHubbard et al. (2013, pp. 40–45) have a good discussion of the following basic concepts. It is essential to understand them before we move on to modules 2 and 3.

A market is a group of buyers and sellers of a good or service and the institution or arrangement by which they come together to trade. Product markets are markets for goods – such as computers – and services – such as medical treatment. Factor markets are markets for the factors of production, such as labour, capital, natural resources, and entrepreneurial ability.

A free market is a market with few government-imposed restrictions on how a good or service can be produced or sold, or on how a factor of production can be employed.

The market mechanism refers to the inherent forces in the market that will allocate resources in a way that maximises consumer satisfaction. The assumption is that individuals are rational and self-interested. Therefore producers will produce and sell what consumers want to buy, so that the producers can maximise their own profits. These inherent forces are what Adam Smith referred to as the ‘invisible hand’ of the market.

The price mechanism is the signalling device between consumers and producers; if consumers are willing to pay a higher price due to strong demand, this will signal producers to supply more; if demand for a product is low at the current price, the product won’t sell and producers will need to lower the price.

Entrepreneurs are an essential part of a market economy. An entrepreneur is someone who operates a business, bringing together the factors of production – labour, capital, and natural resources – in order to produce goods and services. Entrepreneurs often risk their own funds to start businesses and organise factors of production to produce those goods and services consumers want.

Reading activity 1.3Study chapter 2 of the text (Hubbard et al.).

Make sure that you can:

● define the term ‘opportunity cost’

● explain and apply the concept of the ‘production possibilities frontier’

● distinguish between the concepts of ‘absolute’ and ‘comparative’ advantage

● use the concept of the production possibilities frontier, and theory of comparative advantage, to explain the gains from trade.

● Explain the basic idea of how a market system works

© University of Southern Queensland

ECO1000 – Economics 9

Learning activity 1.3NB: This is the essential set of exercises. If you have additional time, you should practise the quizzes and tests in MyEconlab.

1.3.1 Answer Review Questions 1-10 and Problems and Applications 1, 2, 3, 4, 5, 6, 8, 9, 10, 11, 12, 14, 15, 16, 17, 19 at the end of chapter 2 (check your answers with those from the StudyDesk).

SummaryThis module introduced the study of economics and explored briefly some of the essential concepts and methods used by economists in their professional work. Economists seek to use the economic way of thinking to develop answers to a wide range of questions arising from the general problem of relative scarcity. Its methods are applicable to the analysis of the choices of households, businesses and governments. They are applicable, also, at the level of a region, a nation, or the world.

In this module, we explored the economic way of thinking, the use by economists of graphical analysis, a number of key concepts, and the model of the production possibilities frontier. We saw how this model enabled us to consider the decision problem faced by a country (or a person or business at the micro level) as it sought to use its resources efficiently. We saw also that the model can be used to explain the gains that a country may capture by engaging in specialisation and trade. We also acknowledged that Entrepreneurs, those who own and operate businesses, are critical to the working of a market system. They produce goods and services consumers want and decide how these goods and services should be produced to yield the most profit.

We will introduce a number of additional concepts and models in subsequent modules as we develop our understanding of the importance of economics for the welfare of people.

© University of Southern Queensland

10 ECO1000 – Economics

© University of Southern Queensland

ECO1000 – Economics 11

Module 2 – How the market works

Learning objectivesOn successful completion of this module, you should be able to:

● explain the concepts of demand, supply, and market equilibrium

● explain the concept of elasticity

● calculate and interpret price, income and cross-price elasticity of demand

● calculate and interpret price elasticity of supply.

● understand the concepts of consumer surplus and producer surplus

● use demand and supply graphs to analyse the economic impact of price ceiling and price floors

● use demand and supply graphs to analyse the economic impact of taxes

Learning resources

TextHubbard et al., 2013, Economics, chapters 3, 4 and 5.

EssentialStudy book: module 2.

2.1 IntroductionThis module introduces the well-known economic concepts (tools) of supply and demand, and their use in market analysis. The ‘supply-demand’ model of a market provides us with important insights into the use of resources in a market economy, largely a response to the signals conveyed to decision-makers by prices in an economy. Using this model, we are able to predict the general direction of changes in prices and quantities resulting from changes in the market-place (for example, those arising from the imposition of a sales tax on goods purchased by consumers, or from the payment of a subsidy to producers).

Before the ‘market’ model can be used, it is necessary to have a sound grasp of the concepts of supply and demand and of a measure of responsiveness to a given change in the market, known as elasticity.

© University of Southern Queensland

12 ECO1000 – Economics

Once the mechanics of the model have been mastered, you will find that you can use it to analyse contemporary economic issues, for example, the move to deregulate the Australian labour market. Our focus in this module is on the operation of particular markets (such as the market for unleaded petrol); this is the field of microeconomics as distinct from macroeconomics.

In the previous module, we introduced a number of concepts used by economists and also spent some time looking at what is means to ‘think like an economist’. In this module, we continue that pattern when we turn our attention to the economic analysis of markets.

We are aware, of course, that markets and trading in markets are as old as human history. Some markets are readily observable, such as those for fruit and vegetables, while others are quite obscure, such as those for futures and share options. Despite the legality, or otherwise, of markets, we should be able to apply our tools of market analysis to any market situation.

Our aim is to understand how markets work and to predict the direction of change in market prices and quantities traded that are likely to follow some change in the economy. For example, in Australia at the moment, many people are very concerned about the rising price of fuel for motor vehicles. As economists, we would like to use the tools of market analysis to predict the likely change in the price of fuel over the next month, or year. In this module, we will see how economists develop their predictions.

2.2 Tools of analysis: demand

2.2.1 The concept of demandEconomists define market demand as the set of possible prices per unit of the good and the quantities that would be demanded at each of those prices (other things remaining the same; the ‘ceteris paribus’ assumption). If we knew the set of prices and associated quantities, we could show this information in a table, or plot it to represent a market demand curve (more specifically, the price demand curve). This is usually drawn as a downward-sloping curve.

Individual demand is defined in the same way. It is the set of possible prices and the associated quantities demanded by a consumer (other things remaining equal: that is, ceteris paribus). As for market demand, we an represent individual demand in a table of data or by a plot of the price-quantity information contained in the table.

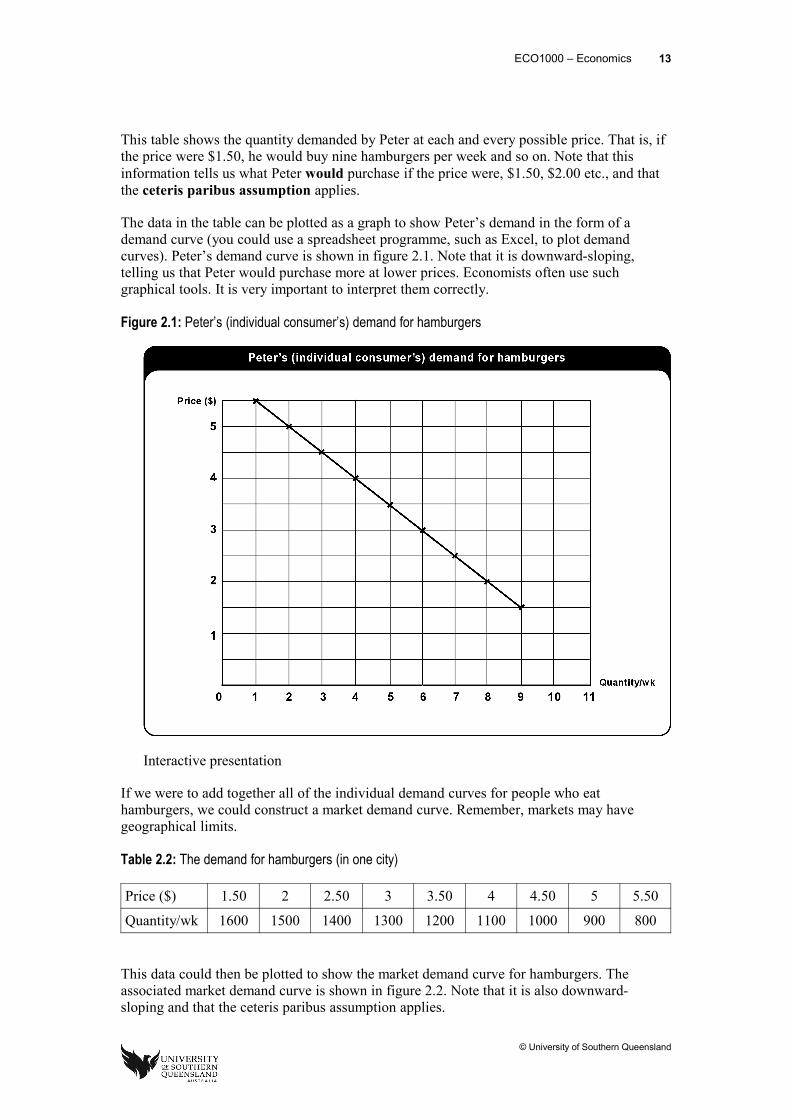

2.2.2 The demand curveSuppose we have the following price and quantity demanded information for a consumer. Table 2.1 is Peter’s demand for hamburgers (ceteris paribus).

Table 2.1: Peter’s demand for hamburgers

Price per hamburger ($) 1.50 2 2.50 3 3.50 4 4.50 5 5.50

Quantity demanded/wk 9 8 7 6 5 4 3 2 1

© University of Southern Queensland

ECO1000 – Economics 13

This table shows the quantity demanded by Peter at each and every possible price. That is, if the price were $1.50, he would buy nine hamburgers per week and so on. Note that this information tells us what Peter would purchase if the price were, $1.50, $2.00 etc., and that the ceteris paribus assumption applies.

The data in the table can be plotted as a graph to show Peter’s demand in the form of a demand curve (you could use a spreadsheet programme, such as Excel, to plot demand curves). Peter’s demand curve is shown in figure 2.1. Note that it is downward-sloping, telling us that Peter would purchase more at lower prices. Economists often use such graphical tools. It is very important to interpret them correctly.

Figure 2.1: Peter’s (individual consumer’s) demand for hamburgers

Interactive presentation

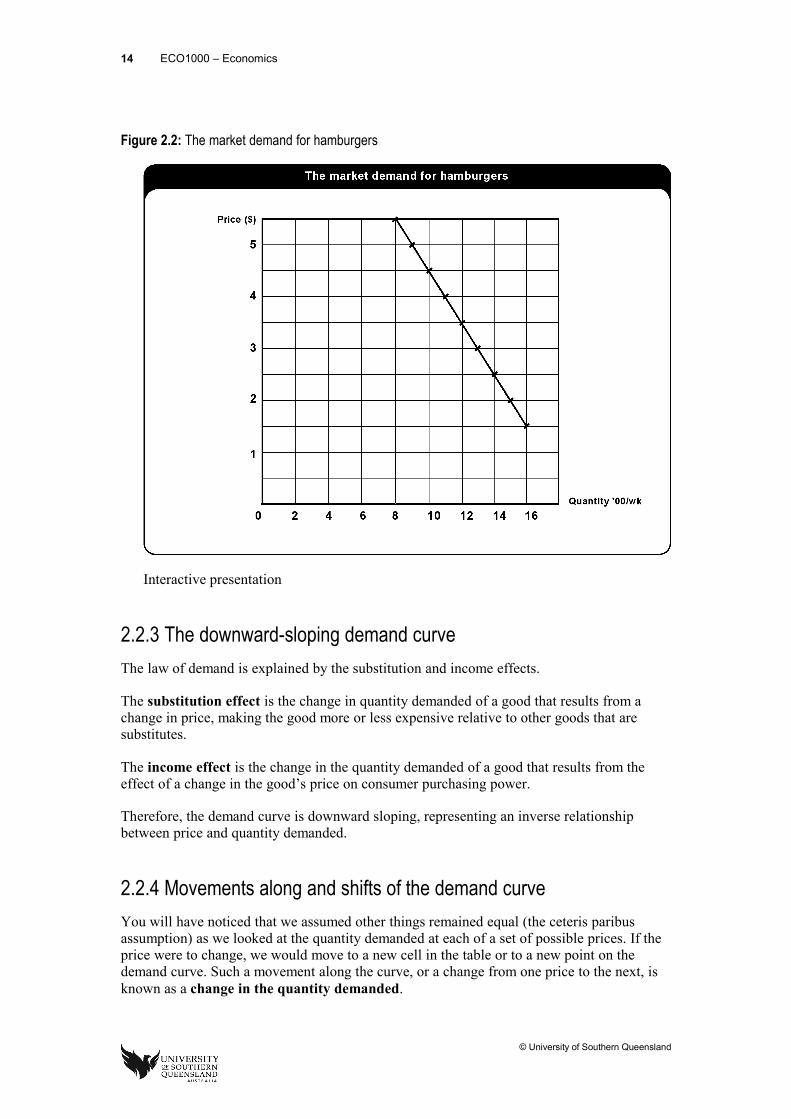

If we were to add together all of the individual demand curves for people who eat hamburgers, we could construct a market demand curve. Remember, markets may have geographical limits.

Table 2.2: The demand for hamburgers (in one city)

Price ($) 1.50 2 2.50 3 3.50 4 4.50 5 5.50

Quantity/wk 1600 1500 1400 1300 1200 1100 1000 900 800

This data could then be plotted to show the market demand curve for hamburgers. The associated market demand curve is shown in figure 2.2. Note that it is also downward-sloping and that the ceteris paribus assumption applies.

© University of Southern Queensland

14 ECO1000 – Economics

Figure 2.2: The market demand for hamburgers

Interactive presentation

2.2.3 The downward-sloping demand curveThe law of demand is explained by the substitution and income effects.

The substitution effect is the change in quantity demanded of a good that results from a change in price, making the good more or less expensive relative to other goods that are substitutes.

The income effect is the change in the quantity demanded of a good that results from the effect of a change in the good’s price on consumer purchasing power.

Therefore, the demand curve is downward sloping, representing an inverse relationship between price and quantity demanded.

2.2.4 Movements along and shifts of the demand curveYou will have noticed that we assumed other things remained equal (the ceteris paribus assumption) as we looked at the quantity demanded at each of a set of possible prices. If the price were to change, we would move to a new cell in the table or to a new point on the demand curve. Such a movement along the curve, or a change from one price to the next, is known as a change in the quantity demanded.

© University of Southern Queensland

ECO1000 – Economics 15

If, however, the price remained the same and some other economic variable that affects demand changed (for example, income), we would get a whole new set of price-quantity data. This would be shown by a shift of the demand curve, to the left or the right. A rightward shift represents an increase in demand (more is demanded at each and every price); a leftward shift represents a decrease in demand (less is demanded at each and every price).

2.2.5 Reasons for the demand curve to shiftWhen the demand curve is drawn, we assume that only the price of the good changes; all the other demand determining variables remain unchanged (this is what the ceteris paribus assumption means). If we subsequently let any of these other economic variables change, we show the effect by a shift of the demand curve. The economic variables ‘captured’ in the ceteris paribus pond are:

● the price of related goods

● the income

● the tastes

● population and demographics

● expected future prices

For example, consider the effect on the demand for fuel efficient dual-engine motor vehicles of an increase in consumer incomes. Assuming these are normal goods (more are purchased at higher income levels), more vehicles would be purchased at each and every price. Thus, we would show this by a rightward movement of the market demand curve.

You should make sure that you can reason through the effect of changes in the other variables on the demand for a good or service. When undertaking such analysis, however, it is best to begin by changing one variable at a time. Otherwise, things become rather complex.

2.3 Tools of analysis: supply

2.3.1 The concept of supplyEconomists define market supply as the quantity that would be supplied to the market at each and every price, other things remaining equal (the ceteris paribus assumption). As for demand, if we knew the set of prices and associated quantities, we could show this in a table or plot the data on a graph. Such a plot would give us what is known as the supply curve. It is usually drawn as upward-sloping, although there are some special cases.

© University of Southern Queensland

16 ECO1000 – Economics

Essentially, market supply is an aggregation of the supply of single firms in that market-place. We can think of single firm’s supply in the same way as we do market supply. It is the quantities the firm would be willing to supply at each of a possible set of prices, other things remaining equal (the ceteris paribus assumption). A single firm’s supply may be shown in a table or graph.

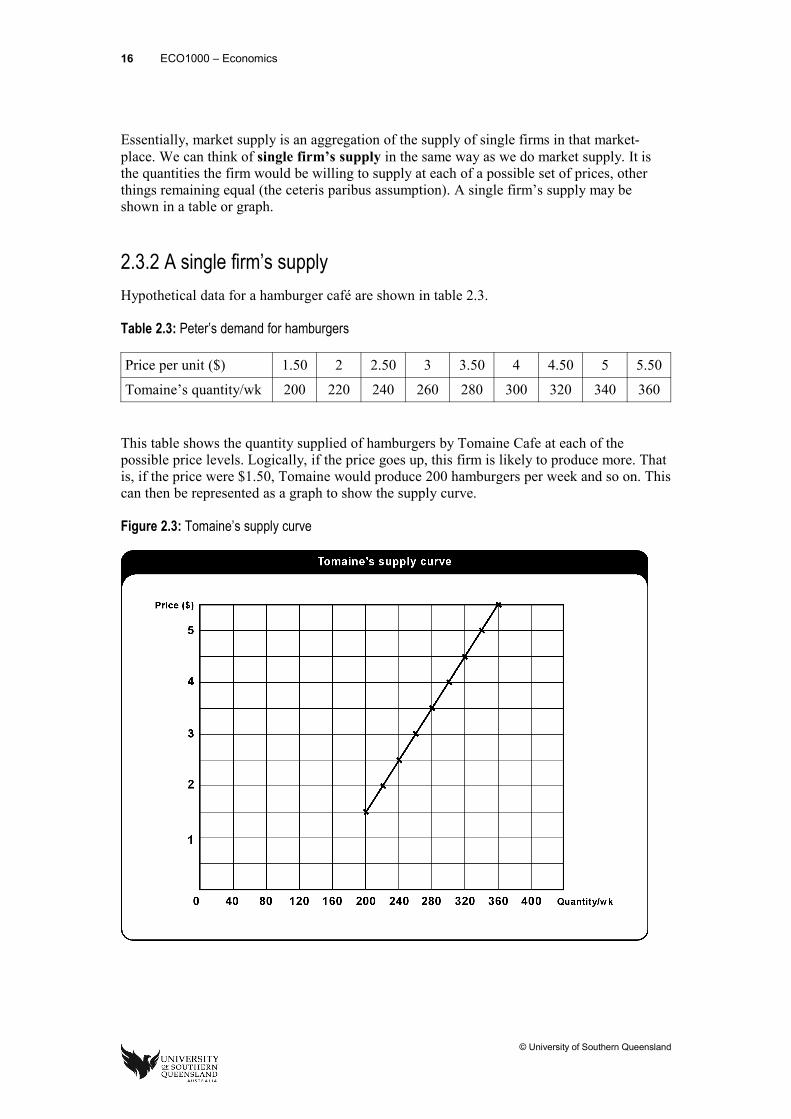

2.3.2 A single firm’s supplyHypothetical data for a hamburger café are shown in table 2.3.

Table 2.3: Peter’s demand for hamburgers

Price per unit ($) 1.50 2 2.50 3 3.50 4 4.50 5 5.50

Tomaine’s quantity/wk 200 220 240 260 280 300 320 340 360

This table shows the quantity supplied of hamburgers by Tomaine Cafe at each of the possible price levels. Logically, if the price goes up, this firm is likely to produce more. That is, if the price were $1.50, Tomaine would produce 200 hamburgers per week and so on. This can then be represented as a graph to show the supply curve.

Figure 2.3: Tomaine’s supply curve

© University of Southern Queensland

ECO1000 – Economics 17

Interactive presentation

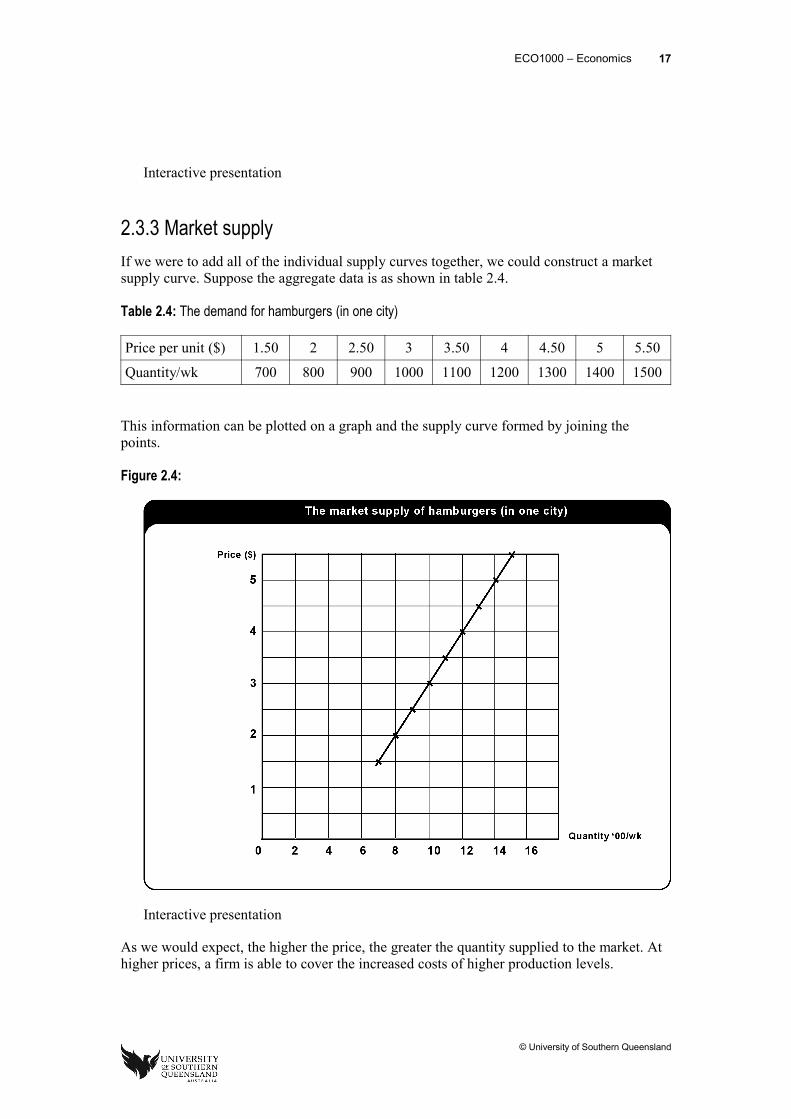

2.3.3 Market supplyIf we were to add all of the individual supply curves together, we could construct a market supply curve. Suppose the aggregate data is as shown in table 2.4.

Table 2.4: The demand for hamburgers (in one city)

Price per unit ($) 1.50 2 2.50 3 3.50 4 4.50 5 5.50

Quantity/wk 700 800 900 1000 1100 1200 1300 1400 1500

This information can be plotted on a graph and the supply curve formed by joining the points.

Figure 2.4:

Interactive presentation

As we would expect, the higher the price, the greater the quantity supplied to the market. At higher prices, a firm is able to cover the increased costs of higher production levels.

© University of Southern Queensland

18 ECO1000 – Economics

2.3.4 Movements along and shifts of the supply curveAs for the treatment of demand curves, we need to distinguish between a movement along a given supply curve and a shift of that curve. If we allow price of the good to vary, and keep all other determining economic variables constant (the ceteris paribus assumption), as price changes we move along the supply curve. This is known as a change in quantity supplied.

If we hold price constant and let any of the other determining economic variables change (such as input prices), we have a new set of price-quantity data. This change is known as a change in supply. If there is an increase in supply (more would be supplied at each and every price) the supply curve shifts to the right. If there is a decrease in supply (less would be supplied at each and every price) the supply curve shifts to the left.

2.3.5 Reasons for the supply curve to shiftAs for the treatment of demand, there are a number of ‘non-price’ determining variables of supply. When we construct the supply curve, these are held constant (the ceteris paribus assumption). If we relax that assumption and allow one of them to change, we have a change in supply (show by a shift of the curve). It is important that we can explain the effect of a change in these variables on supply. The variables include:

● prices of inputs

● technology

● prices of substitutes in production

● number of firms in the market

2.4 Tools of analysis: market equilibriumIn a competitive, or freely operating market, the market equilibrium price is the price at which the quantity demanded equals the quantity supplied (ceteris paribus). That is, buyers and sellers, by a process of trial and error are ‘agreeing’ on a price and quantity that ‘clears’ the market (the equilibrium price and quantity). Producers are prepared to sell that amount at the particular price and buyers are prepared to buy that same amount. At a price higher than the equilibrium price, there will be an excess supply in the market. At a price less than the equilibrium price, there will be excess demand in the market. Such prices are not sustainable and eventually the price will adjust to the equilibrium price.

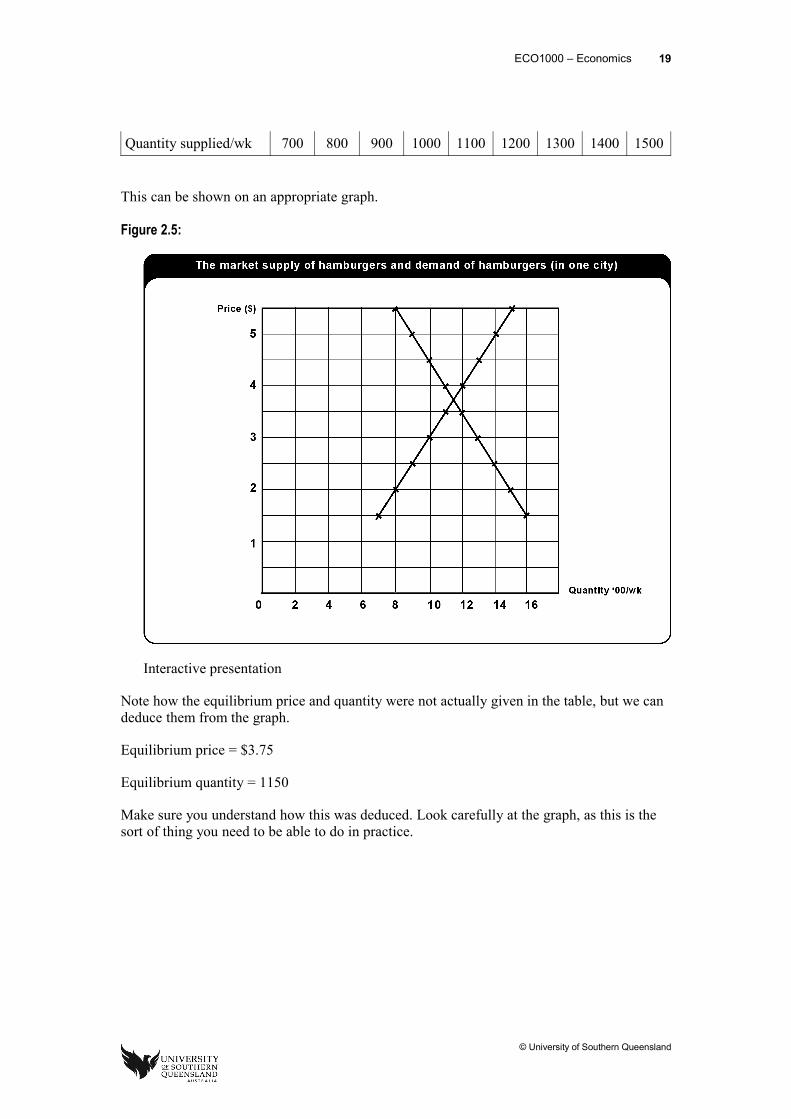

To illustrate the point, let us return to the market for hamburgers and put market supply and demand together. Table 2.5 shows the relevant market data.

Table 2.5: The market supply and demand of hamburgers (in one city)

Price per unit($) 1.50 2 2.50 3 3.50 4 4.50 5 5.50

Quantity demanded/wk 1600 1500 1400 1300 1200 1100 1000 900 800

© University of Southern Queensland

ECO1000 – Economics 19

Quantity supplied/wk 700 800 900 1000 1100 1200 1300 1400 1500

This can be shown on an appropriate graph.

Figure 2.5:

Interactive presentation

Note how the equilibrium price and quantity were not actually given in the table, but we can deduce them from the graph.

Equilibrium price = $3.75

Equilibrium quantity = 1150

Make sure you understand how this was deduced. Look carefully at the graph, as this is the sort of thing you need to be able to do in practice.

© University of Southern Queensland

20 ECO1000 – Economics

Reading activity 2.1Study chapter 3 of the text (Hubbard et al.).

Make sure that you can:

● explain the ‘law of demand’

● explain why the demand curve is downward-sloping

● distinguish between a movement along and a shift of a demand curve

● explain and illustrate the effect on demand of changes in non-price determinants of demand

● illustrate the concept of demand using either a table or a demand curve.

● explain the ‘law of supply’

● distinguish between a movement along and a shift of a supply curve

● explain and illustrate the effect on supply of changes in non-price determinants of supply

● illustrate the concept of supply using either a table or a supply curve.

● explain the concepts of equilibrium price and quantity

● explain the concepts of market ‘surplus’ and market ‘shortage’

● explain and illustrate the effect of a market shortage on market price

● explain and illustrate the effect of a market surplus on market price.

Learning activity 2.1NB: This is the essential set of exercises. If you have additional time, you should practise the quizzes and tests in MyEconlab.

2.3.1 Answer Review Questions 1-10 at the end of chapter 3 (check your answers with those from the StudyDesk).

2.3.2 Answer Problems and Applications 1, 2, 3, 4, 6, 9, 10, 11, 12, 13, 14, 15, 16, 17, 18, 19, 20 at the end of chapter 3 (check your answers with those from the StudyDesk).

2.5 Elasticity

2.5.1 IntroductionIn our development of the tools of analysis above, we have used a downward-sloping demand curve and an upward-sloping supply curve. When changes in price or other economic variables occurred, we focussed on the direction of the resulting effect on prices and

© University of Southern Queensland

ECO1000 – Economics 21

quantities, rather than on the responsiveness of the dependent economic variable. If we had a measure of responsiveness of one economic variable to a change in another (for example, the responsiveness of quantity demanded to a price change), we could take out analysis to the next level and reach more useful conclusions.

Elasticity is a measure of responsiveness. In this section of the module, we introduce the concept of elasticity, study the calculation and interpretation of various elasticity measures, and see how knowledge of elasticity can be used in market analysis.

2.5.2 The concept of elasticityElasticity is a measure of responsiveness. It is a measure of the responsiveness in one economic variable (the dependent variable) to a change in another economic variable (the independent variable). For example, consider the ‘own-price’ elasticity of demand; this is a measure of the responsiveness in the quantity demanded of a good to a change in its price. Or, consider the price elasticity of supply; this is a measure of the responsiveness in quantity supplied of a good to a change in the price of the good. Clearly, the responsiveness in either case could be high or low. The measure that we calculate for the elasticity indicates to us the relative size of the responsiveness. There are many measures of elasticity that we could calculate using appropriate economic variable. Here we focus on some of the most common ones.

2.5.3 Price elasticity of demandPrice elasticity of demand is a measure of the responsiveness in quantity demanded of a good to a change in the price of that good. The calculation is straightforward, but the resultant elasticity does require correct interpretation.

2.5.4 Cross-price elasticity of demandCross-price elasticity of demand is defined as the responsiveness in the quantity demanded of a good to a change in the price of another good. The value calculated for the cross-price elasticity of demand may be positive or negative, and high or low. If the value calculated is positive, the goods are substitutes; if the value is negative, the goods are complements. Knowledge of cross-price elasticities may help in defining industries and seeing the strength of the cross-price link between goods. For example, the cross-price elasticity of demand between Toyota four-wheel drives and Mitsubishi four wheel drives would be of interest to firms producing those vehicles as they determine their pricing policy.

2.5.5 Income elasticity of demandIncome elasticity of demand is defined as the responsiveness in quantity demanded of a good to a change in money income. The value calculated for income elasticity of demand may be positive or negative, and high or low. The sign for the calculated value tells whether the good is a normal one (positive value) or an inferior one (negative value). Knowledge of

© University of Southern Queensland

22 ECO1000 – Economics

this elasticity would be of use to business and governments seeking to cater for populations with rising incomes.

2.5.6 Price elasticity of supplyThe price elasticity of supply (often just the elasticity of supply) is defined as the responsiveness in quantity supplied of a good to a change in the price of that good. This elasticity may be of high or low value, and various cases are distinguished in terms of that value. It is of interest to market analysts as they consider supply responses; for example, the change in the quantity of oil supplied to the world market as the price of oil rises.

Reading activity 2.2Study chapter 4 of the text (Hubbard et al.).

Make sure that you can:

● define and calculate ‘price elasticity of demand’

● explain the midpoint formula for the calculation of price elasticity of demand

● distinguish among elastic demand, inelastic demand and unit elastic demand

● outline the determinants of price elasticity of demand

● interpret calculated price elasticities of demand

● explain why price elasticity of demand varies along a straight line demand curve and the relationship between price elasticity and total revenue

● define ‘cross-price elasticity of demand’

● define the terms ‘complements’ and ‘substitutes’ in terms of the cross-price elasticity of demand

● interpret calculated cross-price elasticities.

● define ‘income elasticity of demand’

● define the terms ‘normal’ and ‘inferior’ goods in terms of income elasticity of demand

● interpret calculated income elasticities of demand.

● define price elasticity of supply

● understand the determinants of the price elasticity of supply

● distinguish and illustrate the various cases of elastic and inelastic supply

● interpret calculated supply elasticities.

© University of Southern Queensland

ECO1000 – Economics 23

Learning activity 2.2NB: This is the essential set of exercises. If you have additional time, you should practise the quizzes and tests in MyEconlab.

2.7.1 Answer Review Questions 1-12 for chapter 4 (check your answers with those from the StudyDesk).

2.7.2 Answer Problems and Applications 1, 2, 3, 4, 5, 6, 7, 8, 9, 10, 12, 13, 15, 17, 18, 19 for chapter 4 (check your answers with those from the StudyDesk).

2.6 Economic efficiency and market failure Now that we have developed a number of the tools used by economists, let us turn our attention to the use of those tools. In this section of the module, we explore the effects of government policy to control prices in a market, the economic impact of taxes and the interesting question of why markets may fail to provide desirable outcomes in an economy. Before we go into all these applications, we introduce the concepts of consumer and producer surplus first.

2.6.1 Consumer and producer surplus and economic efficiencyConsumer surplus is the difference between the highest price a consumer is willing and able to pay and the price the consumer actually pays.

Producer surplus is the difference between the lowest price a firm would have been willing and able to accept and the price it actually receives.

When equilibrium is reached in a competitive market, the marginal benefit from the last unit sold will equal the marginal cost of producing that last unit. This is an economically efficient outcome.

If less than the equilibrium output were produced, the marginal benefit of the last unit bought would exceed its marginal cost.

If more than equilibrium quantity were produced, the marginal benefit of this last unit would be less than its marginal (opportunity) cost.

Economic surplus is the sum of consumer and producer surplus. Economic surplus, or the net benefit to society from the production of a good or service, is maximised at equilibrium in a competitive market (when there are no externalities).

A deadweight loss is the reduction in economic surplus resulting from a market not being in competitive equilibrium.

© University of Southern Queensland

24 ECO1000 – Economics

Economic efficiency is a market outcome in which the marginal benefit to consumers of the last unit produced is equal to its marginal cost of production, and where the sum of consumer and producer surplus is at a maximum.

2.6.2 Price floors and price ceilingsThough the total benefit to society is maximised at a competitive market equilibrium, individual consumers would be better off if they could pay a lower than equilibrium price, and individual producers would be better off if they could sell at a higher than equilibrium price.Consumers and producers sometimes lobby government to legally require a market price different from the equilibrium price. These lobbying efforts are sometimes successful.

A price floor is a legally determined minimum price that sellers may receive.

Price floors were established in agricultural markets in the USA, European Union (EU) and in many other countries in response to pleas from farmers who could sell their product only at low prices.

A price ceiling is a legally determined maximum price that sellers may charge.

It is reported that Venezuelan President Hugo Chavez's policy of keeping a tight control on food retail prices have caused severe food shortage in recent years.

2.6.3 The economic impact of taxesWe are now in a position to return to market analysis and to see how knowledge of elasticity enables us to draw useful conclusions about market changes. Here we focus on the effects of a tax (such as a sales tax) imposed on the sale or the production of goods and services.

A tax on the sale of a good or service also results in a reduction of economic efficiency. For example, if the federal government were to impose an additional tax on cigarettes of $1.00 per pack, this would decrease the supply (shift the supply curve of cigarettes to the left, or shift it up by $1.00). The tax would result in a loss of consumer and producer surplus. Some of the reduction of consumer and producer surplus becomes government revenue and the rest is a deadweight loss, which is referred to as the excess burden of the tax.

The incidence of a tax is the actual division of the excess burden between producers and consumers in the market. The tax incidence varies depending on how responsive producers and consumers are to the price change caused by the tax (ie, elasticities of demand and supply).

© University of Southern Queensland

ECO1000 – Economics 25

Reading activity 2.3Study chapter 5 of the text (Hubbard et al.).

Make sure that you can:

● explain the concepts of consumer surplus and producer surplus

● explain the concepts of marginal benefit and marginal cost

● explain and illustrate the concept of economic efficiency

● explain and illustrate the effect of the policy of setting a price floor in a market

● explain and illustrate the effect of the policy of setting a price ceiling in a market.

● illustrate the effect of taxes on economic efficiency

● define the term ‘tax incidence’

● use a supply and demand diagram to illustrate the tax incidence of a unit tax (tax placed on each unit of a good) in terms of prices paid and received, and in terms of tax paid by buyers and sellers

● discuss the importance of demand and supply elasticity for the determination of the tax paid by buyers and sellers when a unit tax is imposed.

Learning activity 2.3NB: This is the essential set of exercises. If you have additional time, you should practise the quizzes and tests in MyEconlab.

2.8.1 Answer Review Question 1-12 at the end of chapter 5 (check your answers with those from the StudyDesk).

2.8.2 Answer Problems and Applications 1, 2, 3, 4, 5, 7, 8, 9, 10, 11, 14, 17, 19, 20 at the end of chapter 5 (check your answers with those from the StudyDesk).

SummaryIn this module, we introduced a number of important tools for use in economic analysis. These were the concepts of demand, supply, market equilibrium, consumer surplus, producer surplus and elasticity. Use of these concepts, often in terms of graphical analysis, enables us to work out the effects of changes in a competitive market in terms of changes in prices, quantities, and revenues. We are now able to use the economic way of thinking to analyse a wide range of market situations.

© University of Southern Queensland

26 ECO1000 – Economics

© University of Southern Queensland

ECO1000 – Economics 27

Module 3 – Firms and market structure

Learning objectivesOn successful completion of this module, you should be able to:

● explain the concepts of ‘explicit’ and implicit’ costs

● use the law of diminishing returns to explain and illustrate the short-run production function

● explain the relationship between short run costs and output in terms of total, average, and marginal cost curves

● explain the relationship between marginal and average cost and between marginal product and marginal cost

● explain the construction and shape of the firm’s long run average cost curve

● explain the model of perfect competition.

● explain the model of monopoly

● discuss the efficiency issues in both perfectly competitive market and monopoly market.

Learning resources

TextHubbard et al. 2013, Economics, chapters 6, 7 and 8.

EssentialStudy book: module 3.

3.1 IntroductionIn modules 1 and 2, we used the concepts of the production possibilities frontier, the supply curve, and market equilibrium without going into much detail about the underlying economics. In this module, we will explore the economics of production, costs and the market structures of perfect competition and monopoly.

Our earlier analysis of market equilibrium assumed a market structure of perfect competition: one in which there are many buyers and sellers and in which no individual buyer or seller has any market power over price.

© University of Southern Queensland

28 ECO1000 – Economics

In this module, we add to our study of economic models by examining the model of perfect competition. This is the well-known model of the ‘free market’; a model which lies at the heart of much of the argument about the need to make actual markets more competitive.

To understand the operation of this model, we need to consider carefully the relationships between production and cost in both the short run time period and the long-run time period. Once we know a typical firm’s short run and long run cost functions (the relationships between cost and output), we can combine this information with information about the revenue function (the relationship between output and revenue) to work out how much output a firm will be willing to supply. From this, we can deduce the shape of the market supply curve which is used in market analysis.

A monopoly is a firm that is the only seller of a good or service that does not have a close substitute. For a monopoly to exist barriers to entering the market must be so high that no other firms can enter. A monopolist will produce less and charge a higher price than would a perfectly competitive industry producing the same good. The monopolist’s profit-maximising price exceeds marginal cost. The monopoly equilibrium is neither productively efficient nor allocatively efficient.

There are a number of production, cost and revenue concepts to be understood in this module. We begin with production and costs in the two time periods and then turn to the analysis of the perfectly competitive firm and market.

3.2 The concept of cost revisitedIn module one, we introduced the concept of opportunity cost. Opportunity cost is an important consideration when business decisions are made. Most people would be familiar with the basic idea of business costs, which would include wages for workers, materials, other production costs, and capital costs for buildings and equipment. Think of these as accounting costs, or the payments for actual things; that is think of them as explicit costs. Business profit is calculated as:

Revenue (or income) – accounting costs = profit.

Audio: explicit costs explicit costs

This seems quite simple, but economists believe that such a simple calculation misleads the business person. The economic question is: what has the business owner foregone in order to be in a particular business?

Suppose that Sally earns $100 000 a year as a corporate economist, but like many people she wants to ‘be her own boss’. She buys a small business for $300 000, using funds she inherited. However, she realises the new business can only afford to pay her a managing director’s salary of $80 000. Sally is ‘paying’ an implicit cost for her decision to be an owner operator. This implicit cost is the $20 000 a year in her personal income ($100 000 – $80 000) that she foregoes.

© University of Southern Queensland

ECO1000 – Economics 29

She also foregoes interest income by investing her funds in the business, rather than in financial assets. Suppose that the current interest rate is 10%. This is taken to be the return on the best alternative use of her funds. Sally could be earning $30 000 a year from a financial investment of $300 000 at 10% per year.

In total, the annual implicit cost she incurs by investing in the business is:

$20 000 + $30 000 = $50 000 per year

This cost should be added to the explicit accounting cost to give the economic cost of choosing the business option. That is:

Economic cost = accounting cost (explicit costs) + implicit cost (implicit costs).

Audio: economic costs economic costs

Audio: implicit costs implicit costs

This does not mean that business people should slavishly follow such a principle and always pursue the alternative yielding the highest return. People go into business for all sorts of reasons, including job satisfaction, the desire for independence and to create family assets. In addition, in some years, profits will be down compared to other investments, so the opportunity cost will be higher, but you would not necessarily sell out to pursue always the short term best option. There are costs in transferring assets and skills. There may also be taxation benefits in having a business which yields a better return than salaries, although this can be overestimated. The important point to note is that as a business person, you should know what the options are and how much your choices really ‘cost’. Harsh as it may seem, if you stay in an enterprise that has a persistent negative economic profit, you might have difficulty. Over time, the temptation to pursue better options will increase.

In summary, in economics we measure costs as opportunity costs including explicit costs and implicit costs. Explicit costs are the payments to non-owners of a firm for their resources, e.g., wages, lease payments, cost of materials, etc. Implicit costs are the opportunity costs that do not require an outlay of money by the firm, e.g., the use of the owner's time, money and car for production.

© University of Southern Queensland

30 ECO1000 – Economics

3.3 The short run production functionEconomists usually consider the economics of a firm’s production in two time periods. The short run is that time period in which at least one of the firm’s inputs is fixed in quantity. The long run time period is that time period in which all of a firm’s inputs can be considered to be variable in quantity. This leads to the classification of inputs as variable or fixed, depending on the time period in question.

Given this time period distinction, we can speak of the firm’s short and long run production functions, where a production function refers to the relationship between the inputs used by a firm and the output it produces. These production functions become the basis for the firm’s cost functions in the long and short run time periods.

If we assume that labour and machine capital are the only two inputs for a firm and the number of machines is fixed. The marginal product of labour is the additional output the firm produces as a result of hiring one more worker. The law of diminishing returns states that at some point, adding more of a variable input, such as labour, to the same amount of a fixed input, such as capital, will cause the marginal product of the variable input to decline.

The average product of labour is the total output produced by a firm divided by the quantity of workers. When the average product is rising, the marginal product is above the average product; when the average product is falling, the marginal product is below the average product. Therefore, the marginal product curve cuts the average product curve at the point where the average product is at its maximum.

3.4 Short run cost functionsWith our knowledge of the short run production function, we can turn to a consideration of a firm’s short run cost function. This is the relationship between a firm’s output and costs. The cost function can be displayed in terms of its output and total costs (total fixed cost, total variable cost and total cost), or in terms of its output and its average costs (average fixed cost, average variable coast, and marginal cost). We need to understand the shape of the typical cost curves (functions) and to appreciate that there are geometrical relationships between the various cost curves that need to be observed when we draw and interpret the cost relationships.

Marginal cost is the change in a firm’s total cost from producing one more unit of a good or service. The law of diminishing returns explains why the marginal cost curve is U-shaped. The relationship between marginal cost and average total cost can be explained as: when MC is below ATC, ATC will fall; when MC is above ATC, ATC will rise; MC curve cuts ATC curve when ATC is at its lowest point; the ATC curve is U-shaped because MC is U-shaped. The same reasoning applies to the relationship between MC and AVC.

© University of Southern Queensland

ECO1000 – Economics 31

3.5 Long run average costIn the long run period, all inputs are variable. Consequently, all costs are variable as well. For this time period, economists use the concept of long run average cost to represent the long run cost function. This cost function is typically U-shaped and is formed by the lowest portions of the set of short run cost functions that enable production at least cost as output is increased. As we explore the long run cost function, we need to note that the long run is essentially a firm’s planning period. Once a decision has been made to build a certain size of plant, the firm is operating in the short run.

Reading activity 3.1Study chapter 6 of the text (Hubbard et al.).

Make sure that you can:

● understand the concepts of 'short run' and 'long run'

● define total cost, variable cost and fixed cost

● define the terms ‘explicit’ and ‘explicit cost’

● explain the concept of a ‘production function’

● calculate average cost

● explain the concepts of ‘marginal product’ and 'average product'

● state the law of diminishing returns

● explain the relationship between marginal and average product.

● define and calculate average marginal cost, fixed cost, average variable cost, and average total cost

● explain and illustrate the relationship between marginal cost and average cost

● interpret graphs showing either total cost curves, or average cost curves

● explain and illustrate a firm’s long run average cost curve in terms of a series of short average run cost curves

● explain the typical shape of the long run average cost curve in terms of ‘economies’ of scale; ‘diseconomies’ of scale and ‘constant returns’ to scale.

© University of Southern Queensland

32 ECO1000 – Economics

Learning activity 3.1NB: This is the essential set of exercises. If you have additional time, you should practise the quizzes and tests in MyEconlab.

3.4.1 Answer Review Questions 1-10 for chapter 6 (check your answers with those from the StudyDesk).

3.4.2 Answer the study questions and problems 1, 3, 4, 5, 6, 7, 8, 10, 11, 12, 13, 14, 15, 18, 20 for chapter 6 (check your answers with those from the StudyDesk).

3.6 The model of perfect competition

3.6.1 IntroductionThis is one of the most well-known models of the standard microeconomics literature. It deals with a market structure in which there are many buyers and sellers, and in which no buyer or seller has any power over the price in the market. Like all models, there are a number of assumptions made about this market structure. Given these assumptions, a number of important conclusions about firm and industry pricing and production follow. We will find that, although it might be somewhat unrealistic in terms of typical market structures in existence today, it still provides a very useful beginning to our study of the way in such competitive forces work.

In our study of this model, we will look at the firm and the market (industry) in both the short and the long run periods. We will use our knowledge of cost functions for these periods to see how firm’s decide on their choice of output, and how these choices flow into industry supply. This will complete our understanding of the economics ‘beneath’ the market supply curve that we have met already in the previous module.

3.6.2 The perfectively competitive model: in the short runIn a perfectly competitive market, each individual firm is a price taker and its demand curve is horizontal, which is different from the downward-sloping market demand curve. The individual firm cannot decide the market price, but it can decide its optimal output level based on its marginal cost information to maximise the profit.

The profit is maximised at the output where the difference between total revenue (TR) and total cost (TC) is the largest. It is equivalent to say that the profit is maximised at the level of output where the firm's marginal cost equals the market price.

The firm will make an economic profit if P > ATC. The firm will break even if P = ATC. The firm will experience a loss if P < ATC.

In the short run, the firm will stay in the business if P>AVC. The firm will shut down if P<AVC. There is no difference for the firm to shut down or to continue to operate if

© University of Southern Queensland

ECO1000 – Economics 33

P=AVC. So the firm's marginal cost curve is its supply curve only for prices at or above average variable cost. The market supply curve is the horizontal sum of the individual firms' supply curves.

3.6.3 The entry and exit of firms in the long run and efficiencies in perfect competition While entry into, and exit from, the industry is not possible in the short run (firms adjust by changing their output), in the long run firms may exit the industry and new firms may enter. If a firm cannot make a normal profit (a term that means zero economic profit or break even), it will leave the industry. If firms outside the industry observe that more than normal profits are made within it, they will seek to enter the industry. Consequently, in the long run there are both industry and firm adjustments to consider. This makes the analysis slightly more complicated.

A long-run supply curve represents the relationship between market price and the quantity supplied. Its position is determined by the minimum point of the ATC curve. In the long run, the ATC could increase, decrease or remain constant. Therefore, the long-run supply curve could be upward sloping, downward sloping or horizontal.

Perfect competition can be used as a benchmark to compare with other market structures such as monopoly. In the absence of external cost or benefits a perfectly competitive market can achieve allocative efficiency in both short run and long run as the price is equal to the marginal cost(P=MC), meaning that the scarce resources are allocated in accordance with the wishes of consumers. Productive efficiency also occurs when price equals the minimum of average total cost (P=minATC). This may not be achieved in the short run, but productive efficiency is attained in the long run in perfect competition.

Productive efficiency is the situation in which a given quantity of a good or service is produced using the least amount of inputs (P=min ATC).

Allocative efficiency is a state of the economy in which production reflects consumer preferences; in particular, every good or service is produced up to the point where the last unit produced provides a marginal benefit to consumers equal to the marginal cost of producing it (P=MC).

Dynamic efficiency is the ability for firms over time to develop and utilise technological innovation, and to adapt their product to changes in consumer preferences and tastes. However, it is debatable whether a firm in a competitive environment is more innovative or a monopoly firm tends to be more innovative.

© University of Southern Queensland

34 ECO1000 – Economics

Reading activity 3.2Study chapter 7 of the text (Hubbard et al.).

Make sure that you can:

● describe the characteristics of the market structure of perfect competition

● explain why a perfectly competitive firm is a ‘price-taker’ and that its demand curve is perfectively elastic

● explain and illustrate why a perfectly competitive firm maximises profit (or minimises losses) when marginal revenue is equal to marginal cost, or total revenue minus total cost is a maximum

● explain why a perfectly competitive firm will ‘shut down’ if the price falls below average variable cost

● explain and illustrate the construction of perfectly competitive firm’s short run supply curve

● explain and illustrate the construction of the perfectly competitive industry’s supply curve.

● explain why a perfectly competitive firm in long run equilibrium makes zero economic profit (normal profit)

● explain why a perfectly competitive industry is in long run equilibrium when each firm is producing an output for which price is equal to short run marginal cost, short run average total cost and long run average cost

● explain productive, allocative and dynamic efficiencies.

Learning activity 3.2NB: This is the essential set of exercises. If you have additional time, you should practise the quizzes and tests in MyEconlab.

3.6.1 Answer Review Questions 1-12 for chapter 7 (check your answers with those from the StudyDesk).

3.6.2 Answer Problems and Applications 1, 2, 3, 5, 6, 7, 8, 9, 10, 11, 12, 13, 14, 16, 17, 18, 19 for chapter 7 (check your answers with those from the StudyDesk).

3.7 Monopoly markets

3.7.1 Monopoly modelA monopoly is a firm that is the only seller of a good or service that does not have close substitutes. Although few firms are monopolies, the economic model of monopoly can still

© University of Southern Queensland

ECO1000 – Economics 35

be very useful. As with the perfect competition model, which provides a benchmark for how a firm acts in an industry where many firms supply identical product, monopoly provides a benchmark for the other extreme, where a firm is the only supplier and faces no competition from other firms.

There are higher barriers in the monopoly market which prevent other firms from entering. The barrier could be created by the government, for example, blocking the entry of more than one firm into a market, or because the firm controls over a material necessary to produce a product. The barriers could also result from important network externalities and economies of scale.

The monopoly firm is a price maker. But it is constrained by the downward-sloping demand curve. A monopoly firm’s demand curve is the market demand curve. A monopoly firm maximises profit by producing the level of output where marginal revenue equals marginal cost.

Please note that profit is not guaranteed in a monopoly market. If the demand is very low while the firm's ATC is very high, the firm could make a loss. However, if the monopolist’s price exceeds its average total cost at the output where marginal revenue equals marginal cost, it will earn an economic profit. Because of high entry barriers new firms will not be able to enter the market, so if other things remain the same, the firm will be able to continue to earn economic profits, even in the long run.

A monopolist will produce less and charge a higher price than would a perfectly competitive industry producing the same good. The monopolist’s profit-maximising price exceeds marginal cost (P>MC) and the firm does not produce at the minimum point of ATC (P>min ATC). Thus the monopoly equilibrium is neither productively efficient nor allocatively efficient.

3.7.2 Economic efficiency and government regulation in monopoly market Compared to equilibrium in a perfectly competitive market, which results in the maximum amount of economic surplus, a monopoly will produce less and charge a higher price, resulting in reduction in consumer surplus and allocative efficiency. This is actually another form of market failure. Therefore, government plays an important role in such markets to promote competition, thereby improving efficiency.

The Australian Competition and Consumer Commission (ACCC) monitors competitive behaviour in Australia, and enforces the Competition and Consumer Act 2010 (CCA), which contains laws against anti-competitive actions by firms.

The ACCC cracks down price-fixing activities (collusion) and regulates business mergers.

Federal, state or territory government regulatory commissions usually set prices for natural monopolies.

However, given the important role played by the application of new production methods and equipment in the productive growth of industrial countries, some economists argue that

© University of Southern Queensland

36 ECO1000 – Economics

dynamic efficiency should be given the highest priority, followed by productive efficiency. As a result, allocative efficiency is said to be of less policy importance (a normative statement!). Having done this module, students should be able to formulate their own argument on this issue.

Reading activity 3.3Study chapter 8 of the text (Hubbard et al.).

Make sure that you can:

● explain entry barriers created by government action, control of key resources, network externalities and natural monopoly

● explain and illustrate how a monopoly firm determines its output and price

● explain and illustrate consumer surplus, producer surplus and deadweight loss in a monopoly market

● Understand the concept of 'market power'

● explain why there is a need to regulate collusive behaviour and merger activities

● Understand the practices in regulating natural monopolies

Learning activity 3.3NB: This is the essential set of exercises. If you have additional time, you should practise the quizzes and tests in MyEconlab.

3.6.1 Answer Review Questions 1-12 for chapter 8 (check your answers with those from the StudyDesk).

3.6.2 Answer Problems and Applications 1, 2, 3, 4, 7, 8, 9, 10, 11, 12, 13, 14, 15, 16, 17, 19, 20 for chapter 8 (check your answers with those from the StudyDesk).