Embed Size (px)

Citation preview

EDEA- An Expert Knowledge-Based Tool for Performance Measurement

Kamel Bala

A thesis submitted to the Faculty of Graduate Studies in partial fulfillment of the requirernents

for the degree of

Doctor of Philosophy

Schulich School of Business York University

Toronto, ON, M6J 1P3

August 23,2001

National Library I*I ofCanada Bibliothèque nationde du Canada

Acquisitions and Acquisitions et Bibliographie Services services bibliographiques

395 Wellington Street 395. rue Wellington Ottawa ON K1A O N 4 OüawaON K I A W Canada Canada

The author has granted a non- exclusive licence allowing the NationaI Libmy of Canada to reproduce, loan, distribute or seU copies of this thesis in microfonn, paper or electronic formats.

The author retains ownership of the copyright in this thesis. Neither the thesis nor substantial extracts fiom it may be printed or othenvise reproduced without the author's permission.

L'auteur a accordé une licence non exclusive permettant à la Bibliothèque nationale du Canada de reproduire, prêter, disbcibuer ou vendre des copies de cette thèse sous la forme de microfiche/film, de reproduction sur papier ou sur format électronique.

L'auteur conserve la propriété du droit d'auteur qui protège cette thèse. Ni la thèse ni des extraits substantiels de celle-ci ne doivent être imprimés ou autrement reproduits sans son autorisation.

EDEA-AN EXPERT KNOWLEDGE-BASED PERFORMANCE MEASUREMENT TOOL

a dissertation submitted to the Faculty of Graduate Studies of York University in partial fulfillment of the requirements for the degree of

OOCTOR OF PHILOSOPHY

O Permission has been granted to the LIBRARY OF YORK UNIVERSITY to lend or sel1 copies of this dissertation. to the NATIONAL LIBRARY OF CANADA to microfilm this dissertation and to lend or seIl copies of the film, and to UNIVERSITY MlCROFlLMS to publish an abstract of this dissertation. The author reserves other publication rights, and neither the dissertation nor extensive extracts from it may be printed or otherwise reproduced without the author's writtefl permission.

ABSTRACT

This thesis presents an irnproved measurement tool for evaluating performance of

branches within a major Canadian bank. While there have been numerous previous

studies of performance at a branch levsl. within the banking industry. this study is

different in a signifîcant ariy: specifically two kinds of data are used to develop the

rnodel .

The first t>*pe of data is standard transaction data a\-ailable frorn an>- b a k . Such data have

formcd the basis of pre\ious studies. The second type of data. obtained from the site

studied. is what can be called classification information. based on branch

consultant/espert judgment as to good or poor performance of branches.

The purpose here is to develop an expert knowledge-based version of an esisting

benchrnarking model. Data Envelopment Analysis (DEA). and to show how this tool is

applied in the banking industr]i*. To reflect this extension of the basic DEA modeI. we

adopt the acronym EDEA.

Chapter 1 presents the contest of the research and briefly describes knowledge

acquisition techniques.

Chaptsr 2 introduces the DE.4 theor'.. ~vith its major modsls. and describes three diffèrent

discriminant techniques. namely:

Logistic regrsssion. nhich is based on the Maximum Likelihood concept:

Discriminant analysis. based on centroids and groups:

Goal programming. a powerful extension of linear prograrnming.

Chaptsr 3 builds classification concepts into the additive DEA model. It demonstrates

how DEA measures can be enhanced. by incorporating expert judgement into the

structure. This enhancement facilitates variable selection. as part of the modeling

esercise. This new mrthodology is tested using a set of data provided by a major

Canadian bank.

Chapter 4 estends the ideas of Chapter 3 to a nonlinear (input-orienred) DEA model

structure. As well. this chapter extends the expert system structure. by adding further

knowlsdge information in the form of a specification of the status (output or input). of a

subset o f the variables.

Chapter 5 investigates a number of extensions o f the models of the two previous chapters.

Specifically. an investigation is performed regarding the imposition of certain constraints

into the earlier models.

Conclusions are presented in Chapter 6.

ACKNOWLEDGEMENTS

1 would like to thank several people who have significantly contributed to this thesis.

In particular 1 am indebted to my supervisor. Professor Wade D. Cook (Mana, oement

Science). who proved to be an effective and unmatchable mentor.

1 u-ould also like to thank committee members Professor Gordon Roberts (Finance).

Professor Scott l'eomans (Management Science). and Professor Markus BiehI

(Management Science).

1 am also graieful to Dr. Mosz Hababou for his invaluable help and advice.

Finall!.. 1 would like to thanli m y family who helped and supported me. and who have

made this effort worthwhile.

TABLE OF CONTENTS

I I . OVERVIEW O F PERFORMANCE MEASUREMENT MODELS AND CLASSIFICATION TOOLS ......................................................................................................................................................... 1 1

I I . 1 DATA ESVELOPXIEST AS.-\LI'SIS MODEM .................................................................................... 1 1 1 . . I The concept ............................................................................................................................ / l 1 . 2 DE.?.\f~di.l~. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . I - f

.............................................................................................. 1 . 3 Mujor DE.4 . \ /UC/C/ Euerisiom -24 1 . 1.4 Srrengths und L~tnirurions ofDE.4 ......................................................................................... 23

1 . 2 DISCRlMIKAST MODELS ............................................................................................................. 27 7- 11.2. / Logisric Regwssiot~ ............................................................................................................... .-

............................................................................................. . I I 2.2 Multiple Disc*rin~ri~artr ? nui\-sis 32 1 . 2 3 Lirwar Gocd Pt-ugraniniit7g DiscritnNianr hfodels .................................................................. 37

III . EMBEDDING EXPERT KNOWLEDGE IN T H E ADDITIVE DEA MODEL ........................ 35

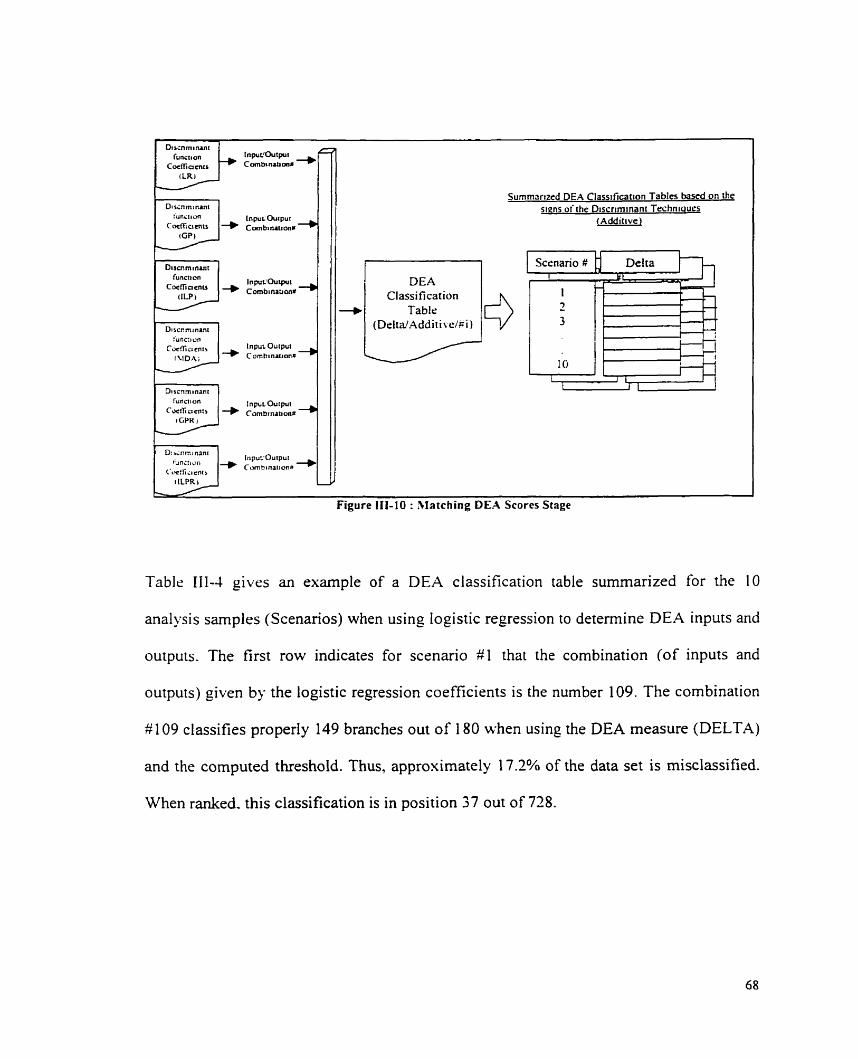

1 11 . 1 1 NTRODCCTIO'I ............................................................................................................................. .A4 /// . 1 / Linkirig disct-iturrtarir tecituiqms und the .-Iddiri i.e DE.4 Mo&/ ........................................... 50 /// . / 2 Daru Trat~fort t~~rt~oti ............................................................................................................ 33 I l 1 DE.4 .\le~r.swc.s .................................................................................................................... 55

111.2 METHODOLOGY .............................................................................................................................. 58 111.3 ESPERIMEST L!SIXG AS . ADDITIL'E DEA MODEL ............................................................................ 61

............................................................................................ / . . I Estinlaring rite Predictire . \focid 61 111.3 7 T e s h g tlw Pr~"it i tr i -~ . \ fo~/cl . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . -1

1 ' . EMBEDDING EXPERT KNOWLEDGE IN THE INPUT-ORIENTED DEA MODEL ......... 78

IV . I ISTRODUCTIOS ............................................................................................................................... 78 IV.? ESPERIMEST trS1sc; AS ISPCT-ORIENTED DEA MODEL ................................................................ 79

1 . 2 . / Estitmti17y rlir Pt-dicri)-e . t fodrl ..................................................................................... ' 9 ............................................................................. I 2 . 2 Tesfing rli t. Pt.èJicrrt.t, .\fodcl ............. .... 83

IV.3 COSCLUS [os ........................................................ .. ..................................................................... 85 / 3 1 C/ass1ficatioi7 uf'lio/~/ou/ surrrplrs ......................................................................................... 8- 11.. 3.2 Cases ~-itlr prt'tl@ed Iripzrr attd Ourpzrr variables ................................................................ 8 9

V . MODEL EXTENSIONS ..................................................................................................................... 99

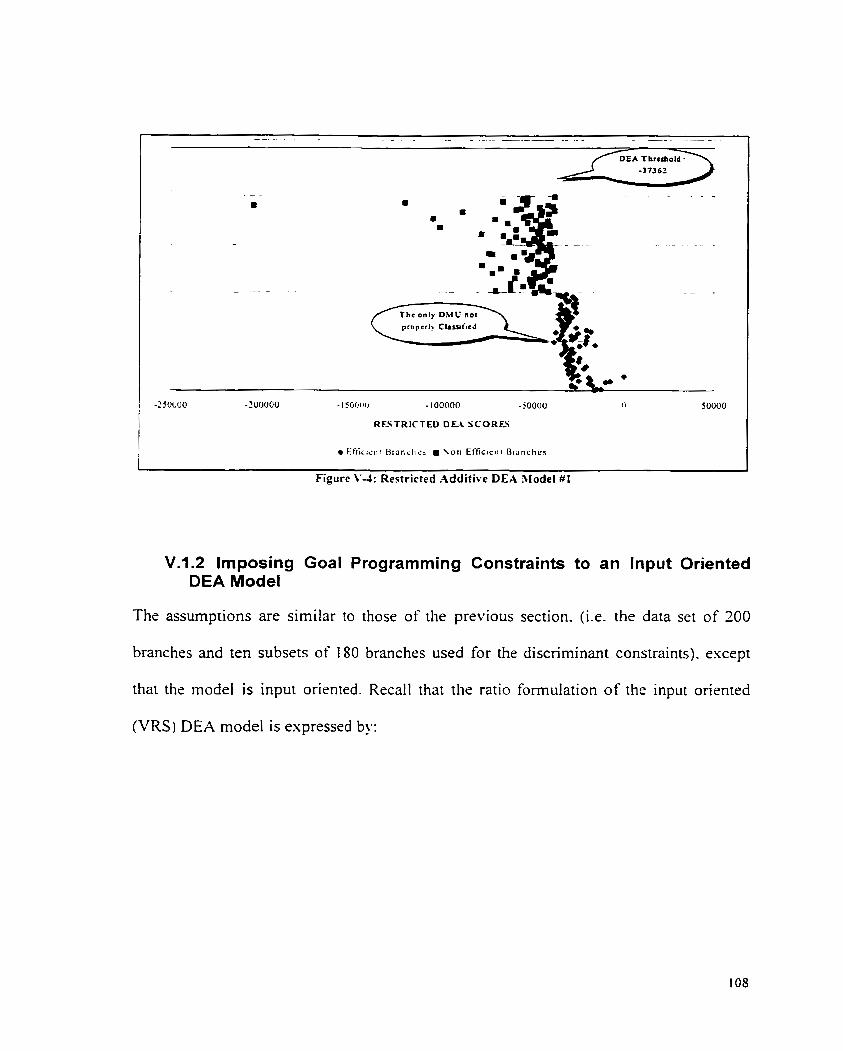

...................................................... V . 1 DEA MODEL EXlIASCE31EST- EXPERT OP~N~OS CONSTRAINTS 99 I .. 1.1 imposir~g Goal Progranrn~irig Consrraints wirhin an -4 dditivr DE.? Mode1 ........................... 99

I . 2 Iniposrrtg Goal Pt-ogratnntitlg Co)tstraints ro an lnpzrl Orienred DEA Mode/ ..................... / O 8 V.2 EXTENSION TO X1ORE THAN T\V0 CLASSES .................................................................................. 119 V.3 SENSITIVITY As.-\L\.sIs ................................................................................................................ 135

VI . CONCLUSION .............................................................................................................................. 127

VI1 . APPENDIX .................................................................................................................................... 131

vii

...................................................... .................. 1 7 . 1 . 2 Facror atzalr.sis rs Componen r ana!vsis .. 133 .................................................................................. 1 3 Facror .-lna -.sis Decision Diagrant 133

........................................................................................................ 1 . 1.4 The rorarion of Facrors 133 7 1.5 Crireria for rhe "Vzrmber of Facrors ro Be Extracred ......................................................... 137

................................................................. 1'11 . 1.6 Crireriafor rhe sigruficance of Facror Loadings 139 ........................................................................................................................... . ' 1 1. 7 L imiraliom 140

.............................................................. ' 1 1 1.8 Afarrir Formiilarion ofrhe Factor ..l n a b i s Mode1 141 ................................................................................................. . . 1 . 1 9 Facror .4nalj .sis Kej Termr 1 4 2

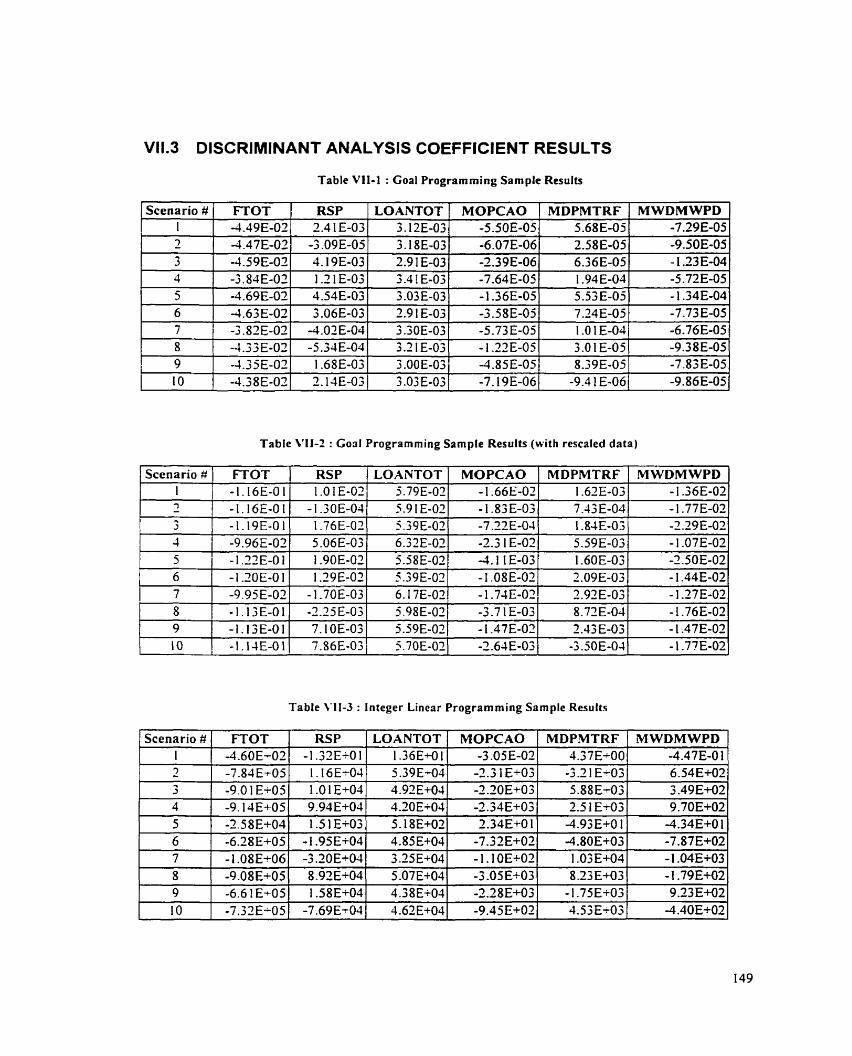

........................................................................................ V I 1.2 DATA SET PROViDED B'i' THE BANK 144 V I 1.3 D I S C R I ~ ~ I S :I NT ANALYSK COEFFICIENT RESULTS ..................................................................... 149

TABLE OF FIGURES FIGLiRE 1- 1 . REGRESSIOS LINE VS . FRONTIER LlNE ..................................... ... ................................................. 2 FIGURE 1-2: STANDARD DATA VS . HEURISTICS ............................... ... ......................................................... 7 FIGURE 1-3: KSOWLEDGE ACQUISITION TO I ~ ~ P R O V E DEA MODELS ............................................................ 10 FIGURE 11-1 : A BANK BRANCH CONSUMNG 2 INPUTS TO PRODUCE 2 OLTPL~TS .................................... .... 1 1 FIGURE 11-2 : COMP.ARISOX O F DEA ASD REGRESS!ON AXALYSIS ..................... .. ...................................... 13 FIGURE 11-3 ENVELOPXIENT SURFACE FOR THE ADDITIVE MODEL ......................... .... ............................. 14 FIGURE I I 4 : DEA RATIO AND NET PROFIT ORIENTED MODELS ..................... .. ....................................... 15 FIGURE 11-5 : DEA MODEL ORIENTATION ......................... .. ...................................................................... 16 FIGURE 11-6 : ESVELOP~IENT SURFACE FOR THE ADDITIVE MODEL ............................................................. 17 FIGURE 11-7 : ENVELOPMENT SURFACE FOR THE CCR-1 MODEL (CRS) ....................................................... 19 FIGURE 11-8 : ENVELOPXIEST SURFACE FOR THE CCR-O MODEL (CRS) ...................................................... 19 FIGGRE 11-9 : RATIO VS LISEAR DEA FOR.VCLATIOYS ................................................................................. 23 FIGURE 11-1 0: MODEL CL.ASSIFICATIOS BASED OS THE DISTRIBLITIOX OF T H E R-\SDOM COMPONENT ..... 2 8 FIGURE 11-1 1 : LOGIT RESPONSE FL~SCTION ................................................................................................... 30 - - FIGURE 11- 13 : DISCRIXIIN.ANT ANALYSIS CENTROIDS ................................................................................... 23 -. FIGURE Il-l3 : MDA RC'LE ............................................................................................................................ 23

FIGURE I I - I 4 : MD.4 OVERL.VPISG DIsTRIBUTIO.\;S ..................................................................................... 34 FIGURE 11- 1 5 : MDA OPTI~ILIS! TWRESHOLDS ................................ .. ................................................ ........35 FIGURE I I - 16 : GOAL PROGRX~!~IISG COSSTR.AIST ..................................................................................... ..38 FIGURE I I - I 7 : I[.LCSTR..\TION O F ISTEGER PROGR.A~\I.~~ISG DISCRI\IISANT MODEL ..................................... 41 FIGURE I I - 18 : GOAL P R O G R . . \ S I ~ M CLASSIFICATIOS WTH O\'ERLAPPISG GROCPS .................................. 4 3 FIGCRE I I 1- I : DISCRI%IIS.-\ST TECIISIQLTS VS . DEA ................................................................................. 4 8 FIGL~RE II I - ? PRIYCIPLE O F THE THEORY THAT IMPROVES DEA MODELS ................................................... 49 FIGURE 111-3 : DATA PROJECTIOS .................................................................................................................. 5 5 FIGURE I I I - l : TEK-FOLD CROSS VXL[D.ATIOS MET HO DO LOG'^' .................................................................... 6 0 FIGCRE I I 1-5 : GESER..\L STEPS FOR THE ADDITIVE DEA ESPERIMEST ........................................................ 61 FIGURE 111-6: R=~SDO~I S X X ~ P L I M ~ ST.-\GE ..................................................................................................... 6 2 FIGURE 111-7: DETER%lISISG JKPL'TS ASD 01'11>1:TS FOR SCES.-~RIO = I %'[TH LOGISTIC' REGRESSION (LR) .. 6 3 FIGVRE III-8 : DISCRI\(ISAST TECMSIQL'ES STAGL ....................................................................................... 64 FIGURE 111-9 : D E A CO~IBIN.ATORIAL STAGE (ADDITIVE ESPERI~IEST) ....................................................... 66 FIGURE 111- 10 : MATCHING DEA SCORES STAGE .......................................................................................... 6 8 FIGURE I I 1-1 1 : CLASSIFICATION SLWXIARY TABLE STAGE ........................................................................... 6 9 FIGURE I I I - 12 : DEA PREDICTIVE CLASSIFIC.L\TIOS STAGE ......................... ... ........................................... 72 FIGCRE I I I - 13 : COVPLETE VS PARTIAL DEA ANALYSES ............................................................................. 7 3 FIGURE 111- 14 : DEA PREDICTIVE STAGE ...................................................................................................... 74 FIGL'RE I I 1- 15 : MATCI~IXG DEA SCORES STAGE .......................................................................................... 7 5 FIGURE 111-1 6 : C L ~ ~ I F I C A T I O K SLNMARY TABLE STAGE .......................................................................... 76 FIGURE IV-1 : GENERAL STEPS FOR THE INPUT DE.4 EXPERIMENT ................... .. ...... .. ........................... 80 FIGURE IV-?: ILLUSTRATION OF ~ N K I N G DEA RESULTS (ADDITIVE MODEL/AN.ALYSIS STAGE) ............... 86

............ FIGCRE IV-3: ILLUSTRATION O F RANKING DEA RESULTS (ADDITIVE MODEL/PREDICTIVE STAGE) 8 7 FIGURE 1V-4: RESTRICTING WEIGHTS OF G 0 . 4 ~ P R O G ~ M N G MODEL ...................................................... 9 2 FIGURE V- 1 : IMPOSING GOAL P R O G R A M ~ ~ G CONSTRAINTS ON A DEA MODEL ...................................... 100 FIGURE V-2 - RESTRICTEO VS . UNRESTRICTED ADDITIVE DEA MODEL ..................................................... 105 FIGURE V-3: NON-RESTRICTED ADDITIVE DEA MODEL ............................................................................. 107 FIGURE V-4: RESTRICTED ADDITIVE DEA MODEL = 1 ................................................................................. 108 FIGURE V-5: NON-RESTRICTED INPUT DEA MODEL ................................................................................... 1 13 FIGURE V-6: RESTRICTED INPUT DEA MODEL f: l (NON LINEAR CONSTRAIKTS) ........................................ 1 14 FIGURE V-7: RESTRICTED INPUT DEA MODEL # 1 (LINEAR CONSTRAINTS) ................................................ 1 17 FIGURE V-8: IMPOSING GOAL P R O G R . ~ MMIKG CONSTRAINTS ON A DEA MODEL (3 GROL'PS) .................. 1 19 F I G U R E VI-I : DEA LEARNING MODEL .................................................................................................... 1 2 9

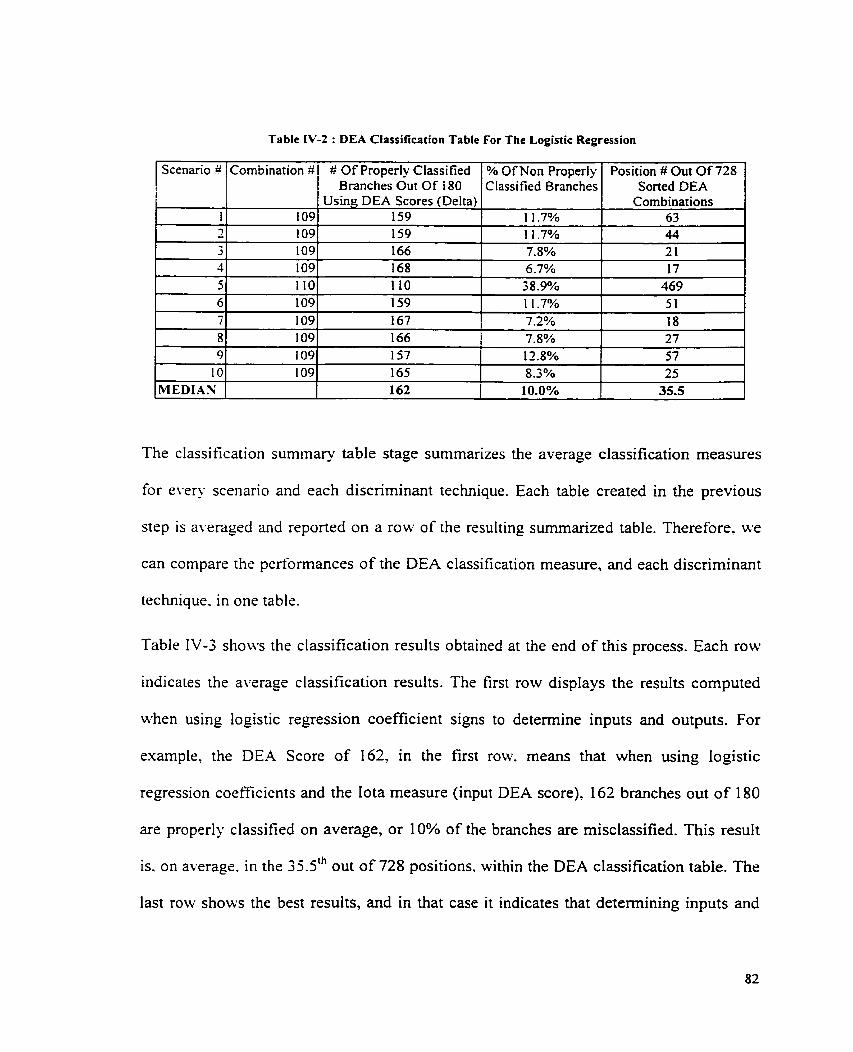

LIST OF TABLES TABLE 111- 1 : DEA VARIABLES ..................................................................................................................... 50 TABLE I I I - ? : LOGISTIC REGRESSION SAMPLE RESCLTS ....................... .,. ........ ... ................................... 64 T ~ L E 111-3 : DEA CLASSIFICATION TABLE FOR SCENARIO 2 I (OUT O F 1 O) .................. .... ..................... 67 TABLE I I 1 3 : DEA CLASSIFICATION TABLE FOR THE LOGISTIC REGRESSION ............................................... 69 TABLE I I 1-5 : SLMX~ARIZED DEA CLASSIFICATION T ~ L E (ADDITI'JE MODE~J'ANALYSIS STAGE) ............... 71 TABLE 111-6 : S U ~ ~ ~ ~ A R I Z E D DEA CLASSIFICATION TULE (ADDITIVE MODEL~PREDICTIVE STAGE) ............ 77 TABLE IV- 1 : DEA CLASSIFICATION TABLE FOR SCENARIO :: 1 (OUT O F IO) ................................................ 81 TABLE IV-? : DEA CLASSIFICATION TABLE FOR T H E LOGISTIC REGRESSION .............................................. 82

............ TMLE IV-:: SUMM.~RIZED DEA CLASSIFICATION T . ~ L E (INPUT DEA MODEL/AN.ALYSIS STAGE) 83 .......... TABLE IV-4: SCMXIARIZED DEA CLASSIFICATIOX T M L E (INPCT DEA MODEL'PREDICTIVE ST .GE) 84

TABLE IV-5: COMPARISON OF ANALYSIS STAGE RESULTS ......................................................................... 85 TABLE IV-6: COW.-\RISOS OF PREDICTIVE STAGE RESC~LTS ........................................................................ 86 TABLE IV-7 : CL ..\ SSIFICXTIOS OF HOLDOUT SAMPLES U s r w ADDITIVE DEA MODEM AXD G 0 . 4 ~

PROGR..\II\IISG COEFFICIENT SIGNS TO SELECT ISPCTS AKD OUTPCTS ................................................ 89 TABLE IV-S : CL.ASSIFIC~\TIOS OF HOLDOL'T SAMPLES USIXG ~ N P L ~ T DEA MODELS ASD GOAL

................................................ P R O G R W ~ I I X G COEFFICIENT SIGNS TO SELECT INPUTS AND OLITPCTS 89 TABLE IV-9: V . A R I . ~ L E PREDEF~NED ORIENTATIOSS .................................................................................... 90 TABLE IV- IO: ADDITIVE DEA CLASSIFICATIO~ TABLE FOR SCES.MIO 2 I ................................................... 9 4 TABLE IV- l 1 : ISPL'T DEA CLASSIFICATION T.ABLE FOR SCENXRIO I ...................................... T.AB~.E IV- 12: X\XK : \GED ADDITIVE DEA CL.4SS1FiCATIOS RESLILTS FOR THE I O SCES..\RIO~ ................... 97 T..\BLE IV- 15: AL'ERAGED INPCT DEA CLASSIFICATIOS RESLrLTS FOR THE 10 ScEN..\RlOS ......................... 9 8

................................... TABLE V- I : S C ~ I . . \ R I Z E D RESULTS FOR THE ADDITI\'E RESTRICTED ESPERIMENT 106 ......................................... T..\BLE V-2: S L ~ X I A R I Z E D RESULTS FOR THE ISPCT RESTRICTED ESPERIMEKT I 12

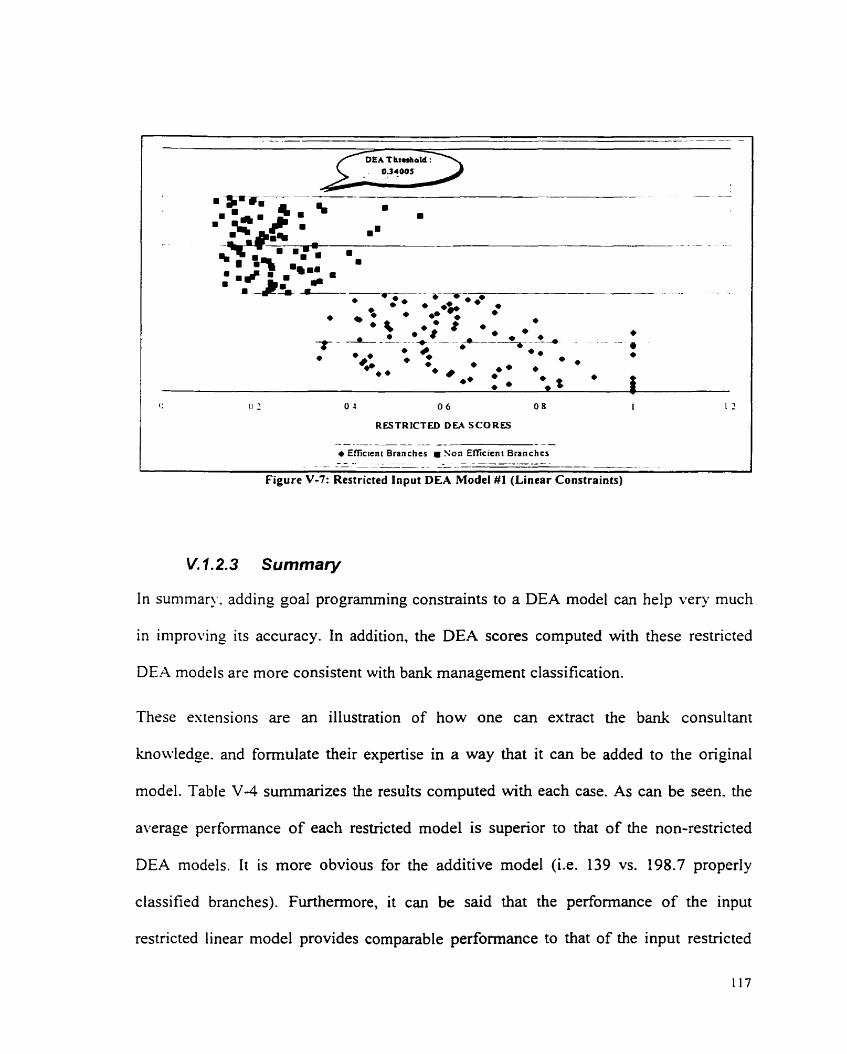

TABLE V-3: SLIIXIARIZED RESLLTS FOR THE ISPET RESTRICTED ESPERIMENT (LISEAR COSSTRAIXTS) .. I 16 T:\BLE V-4: SL!\I\I.ARY O F RESTRICTED DEA MODEL ............................................................................... 1 18

... TABLE V-5 : SEYSITIVITY ASALYSIS WlTH INPUT DEA MODELS USKG S.WPLES OF DIFFERENT SIZES 126 TABLE VII- 1 : GOXL PROGR.4iclMING SAMPLE RESCLTS .............................................................................. 149 .T..\si.tl V11-2 : GOXL PROGRAXI.VING SAXIPLE RESC'LTS (N.IT!{ RESC. - \ l .~~ D ..\TA ) ....................................... 1-49 TABLE VI 1-3 : I N T E G E R LISE.^ P R O G U ~ I ~ I I X G S.-\MPLE RESCL'TS ............................................................ 149

...................... TABLE L'Il-4 : ISTEGER LISEAR P R O G R A ~ M ~ ~ G SAS~PLE RESULTS (Ii'lTH RESC..\LED D.AT.4) I 50 ....................................................... TABLE VII-5 : MCLTIPLE DISCRIMINANT AMLI'SIS S.AMPLE RESCLTS 150

1. INTRODUCTION

1.1 PERFORMANCE MEASUREMENT

In todaj.'s business environment, particulariy in financial services, it is a constant

challenge to stay ahead of the cornpetition. To increase market share and operate more

effici entl y. pan-erful. flexible and advanced anal ytical methods are essential. Of

particular interest in the financial senrices setting. is the development and incorporation

of performance measurement methodologies. These permit management to investigate

the rslati\.e efficiency or productivit of various decision- making units, such as branches

of a bank. and to identify besr pt-ucfice.

In this thesis a performance measurement tool is developed for application in the

financial sen-ices setting. This tool builds upon esisting methodologies. spec i ficall).

rneroin~ C + n-ell- developed optimization models with expert knowledge, leading to a f o m

of expert s'rnstern for performance measurement.

As a simple illustration of the performance measurement problem, consider the esample

of eight branches of a bank. Suppose that these are to be evaluated in ternis of a single

output (sales). and a single input (total employees). Figure 1-1 is an illustration of how the

branches might be positioned. Notice that sales-per-ernployee is a measure of

"productivity" ofien used in management and investment analysis. Given these data. one

approach to measuring performance is to view the problem from the standpoint of output

prediction. and to construct a statistical regression line fitted to the two-dirnensional

profile of the branches. The dotted line in Figure 1-1 shows one exarnple of a regression

line passing through the origin which. under the least squares principle, is expressed by

y = bs.

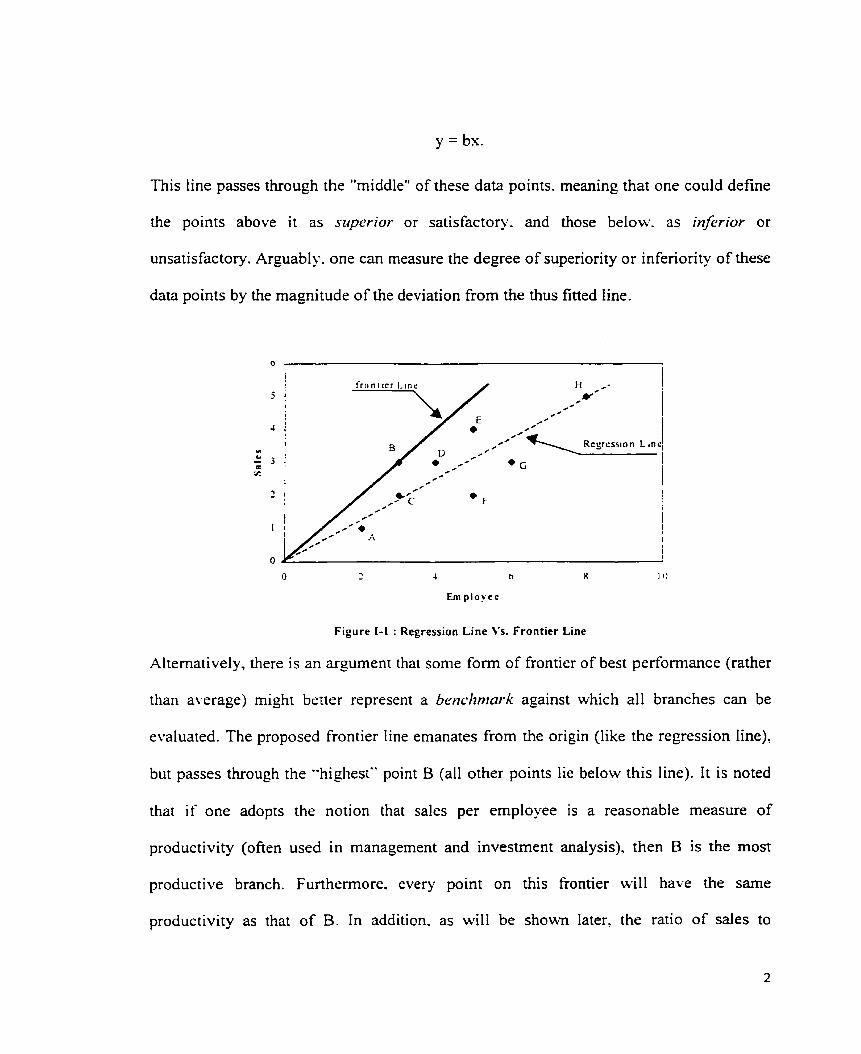

This line passes through the "rniddle" of these data points. meaning that one could define

the points above it as sriperior or satisfactory. and those belobv. as inferior or

unsatisfactory. Arguably. one can measure the degree of superiority or inferiority of these

data points by the magnitude of the deviation from the thus fitted Iine.

O i - 4 b 8 1 O

Em p l o y c e

- -

Figure 1-1 : Regression Line Vs. Frontier Line

Alternatively, there is an argument that sorne form of frontier of best performance (rather

than average) might better represent a b e d m a r k against which al1 branches can be

evaluated. The proposed frontier Iine emanates from the origin (like the regression line),

but passes through the "highest" point B (al1 other points lie below this line). It is noted

thar if one adopts the notion that sales per employee is a reasonable measure of

productivity (often used in management and investment analysis). then B is the rnost

productive branch. Furthermore. every point on this frontier will have the same

productivity as that of B. In addition. as will be shown later, the ratio of sales to

employees. for any branch below the line. is expressible as a measure of the distance of

that point from this line. Thus. the arguably reasonable way of defining performance as a

ratio. can actually be uncovered as a distance from the constructed frontier.

Hence. there esists a fundamental difference between statistical approaches via

regression analysis. and frontier or benchmark approaches. The former reflect "average"

or "central tendenqq" behavior of the observations. while the latter deal with the best

performance. and evaluate the performances of al1 branches as deviations frorn the

frontier line. Thcse two points of view can result in major differences when used as

methods of evaluation. They can also result in different approaches to improvement.

A rrlatively ne\\- efficient?. analysis method. Data Envelopment Analysis (DEA). was

designed to preciselj. construct frontier lines like that displayed in Figure 1-1. Moreover.

it is a tool that is able to do so in a multi output-multi input environment. rendering ir

ideally suited to the problem setting under study. This tool. first developed by Chames.

Cooper. and Rhodes [78CA]. is in widespread use today in a number of areas including

the banking industry. Sherman and Gold [85SG] first used DEA to evaluate 14 branches

of a US salting bank. DEA is a powerful tool that was developed specifically for

determining relative efficiencies within a group of similar Decision Making Units

(DMUs). where a set of outputs. e . g . core deposits. earnings assets, etc.. is created

utilizing severai inputs such as salary expense. numbers of customers. and so on. DEA

calculates a maximal performance measure for each DMU relative to al1 other DMUs in

the observed population. with the sole requirement that each DMU lie on or below the

extrema1 frontier. 1t is a relative benchrnarking tool. meaning that the set of best

practices is based on the particular set of DMUs under study. Typically. this approach is

applied to situations where some factors (both inputs and outputs) are qualitative in

nature. and where conventional engineering approaches to measuring efficiency are of

limired utility. Such is the case in many non-profit institutions. and in the public sector.

With reference again to the simple illustration. DEA would identie a point such as B for

future esamination or to sewe as a "benchmark" to use in seeking improvements. The

statistical approach. on the other hand. averages B along with the other observations.

including F. as a basis for suggesting where improi-ements might be sought.

Although many studies and applications have demonstrated the effectiveness of DEA, it

remains tliat for large-scals problems. with many different factors or variables available,

at least nc.o impedinlsnts to effective implementation still esist.

Fiisr. it is recognized that a DEA analysis entails esplicitly specifying a set of factors to

be used in the modeI. As well. a set of inputs and a set of outputs must be specified for

the analysis to be performed. In many settings. bon-ever. it c m be problematic to define

the most appropriate of those factors to be integrated into the analysis. As with

conventional statistical analysis. many choices c m exist. Equally pertinent. it can be a

challenge to specify which of the chosen factors should serve as inputs. and which as

outputs. Indeed. dependincg on the way the factors are organized. Le.. inputs vs. outputs, a

DEA analysis may result in a particular DMU being classified as inefficient. when, with a

different choice of factors. it may be declared efficient.

A secor~d major element involves implementation. and has to do with management's own

perceptions as to what constitutes good versus poor performance. If a methodology fails

to uncover what management feels is best or worst practice, that methodology is unlikely

to succeed as the measurement tool of choice.

This thesis presents an improved rneasurement tool for evaluating performance of

branches within a major Canadian bank. M i l e there have been nurnerous previous

srudies of performance at the branch level. within the banking industry. this study is

different in a very significant way: specifically two kinds of data are used to develop the

model.

The first type of data is standard transaction data available from any bank. Such data have

formed the b a i s of previous studies. The second type of data. obtained from the site

studied. is n-hat can be called ciass~~cution information. based on branch

consultant'espert judgment as to good or poor performance of branches.

Evaluation of brandi performance by intemal consultants is a common practice in most

major banks. Typically. micro-level work-studies are conducted within a sarnpie of

branches to establish some forrn of standards. While the evaluation of branch

performance attempts to view al1 operational activities as important components of both

the sales and service profiles of the organization, the prevailing emphasis appears to be

on the sales of financial services products (RSPs, mutual funds, etc.). There is usually no

transparent definition of the mechanisms whereby the performance status of the branch is

derived. This is generally due to the attempt of the consultants to merge any computed

quantitative evaluation with factors that capture the environment or context within which

the branch is compelled to conduct its business. This contest c m include the

demographic makeup of the custorner base. such as the financial profile of the average

customer. age. ethnic makeup. and so on.

In most banks. there is seldorn a single and definitive quantitative measure available as to

the performance status of branches. Rather. the practice appears to be to "classify"

branches into two or more groups on the basis of perceived levels of productivity. The

simplest of these classification schemes is a high/low. or good/poor grouping. This is the

case in the present context. and forms the basis of the development in this thesis.

Specificall-. branch consultants have been asked to classify a sample of branches into

two major groups (good performers and poor performers). Arguably. incorporation of

such information into a performance measurement model c m senfe to provide a more

accurate rspresentation of branch et'ticiency. -4s well. any model that builds on such

information is more likely to succeed in being accepted internally.

This thesis demonstrates ho^ this second type of information c m be used in selecting

variables for a DEA analysis in an appropriate way. and can. as well. be used to sharpen

the accuracy of the multipliers applied to these variables in a DEA model.

A major contribution of this work is. therefore. the linkage that it forges between

performance measurement tools (various forms of the DEA model), and the coliection of

tools for classification. e-g. goal programminp. logistic regression and multiple

discriminant analysis. This work is seen as an important and timely step in transforming

the esisting static DEA methodology to a more dynamic performance measurement tool,

along the lines of an expert system. In summary. the thesis develops a DEA methodology

termed EDEA (Expert Data Envelopment Analysis). that combines conventional

6

performance measurement constructs with expert knowledge tools. Such a dynamic

structure will facilitate model updates. and enhance performance measurement accuracy

over tirne.

To provide a backdrop for the model development in the chapters to follow. we briefly

discuss knowledge acquisition. and the basic ideas surrounding expert systems and

artificial intelligence. This provides suppon for. and hopefully validates the contention

that classification information of the type used here is now a valid data source for

performance measurement that deserves attention.

1.2 KNOWLEDGE ACQUISITION

Many areas of research have been developing techniques or approaches to tackle

information that cannot be handled directl!.. because of its "non-sra~zdcr)-d' nature. This is

the case of problems with qualitative data or more sophisticated infom~ation such as

expertise [86B SI.

Figure 1-2: Standard Data Vs. Heuristics

Knowledge acquisition has developed into a mature field. as evidenced by the creation of

artificial intelligence. and more specifically. expert systems. Essentially. the idea of such

systems is to capture the expert's knowledge. and to train the tool to replicate the results

in F~ture.

The expert has a knowledge that the novice does not possess. He also has a recorded and

weli-hown past. proving that he is able to use this knowledge. We rely on experts for

information. their ability to solve problems, and the explmations they give. The

following features characterize them :

Their linowledge is real : the espert can use his knowledge to solve problems with an

acceptable percentage of success.

Their knowled~e is efficient : It is not sufficient to only be able to solve the problems.

an espert can solve them quickll- and efficiently.

Experts know their linlits : An expert is aware of the Iimits to his knowledge. He

knows what hs has to dral with. and when he must rely on others.

Kno~vledgs acquisition techniques use methods in order to gather and organize experts'

knowledge in a form that can be adapted to hardware and to analytic models. These

methods are based on a range of ideas sternming fiom several areas.

The classification techniques involve presenting to the expert the objects to be classified.

Thus. Lve obtain a hierarch which can either be simple (rwo groups). or complex.

according to the cases involved (several groups or hierarchical networks). Thus, one can

see that such techniques can be used to better formalize complex information. Their

ad~~antages are to gi1.e more data. and improve objectivity. thus leading to better models

or systems.

The knowledge acquisition principles can be applied in fields such as DEA. Indeed, we

often have quantitative data available conceming agencies' activities. but seldom use

qualitative information. such as environmental data or the expertise of branch

consultants. The objective herein is to design a construct to capture as much information

as possible. by taking into account this espertise. and thereby produce improved DEA

models. Knowledge acquisition is an iterative and continuous process. This process can

be divided into four major steps:

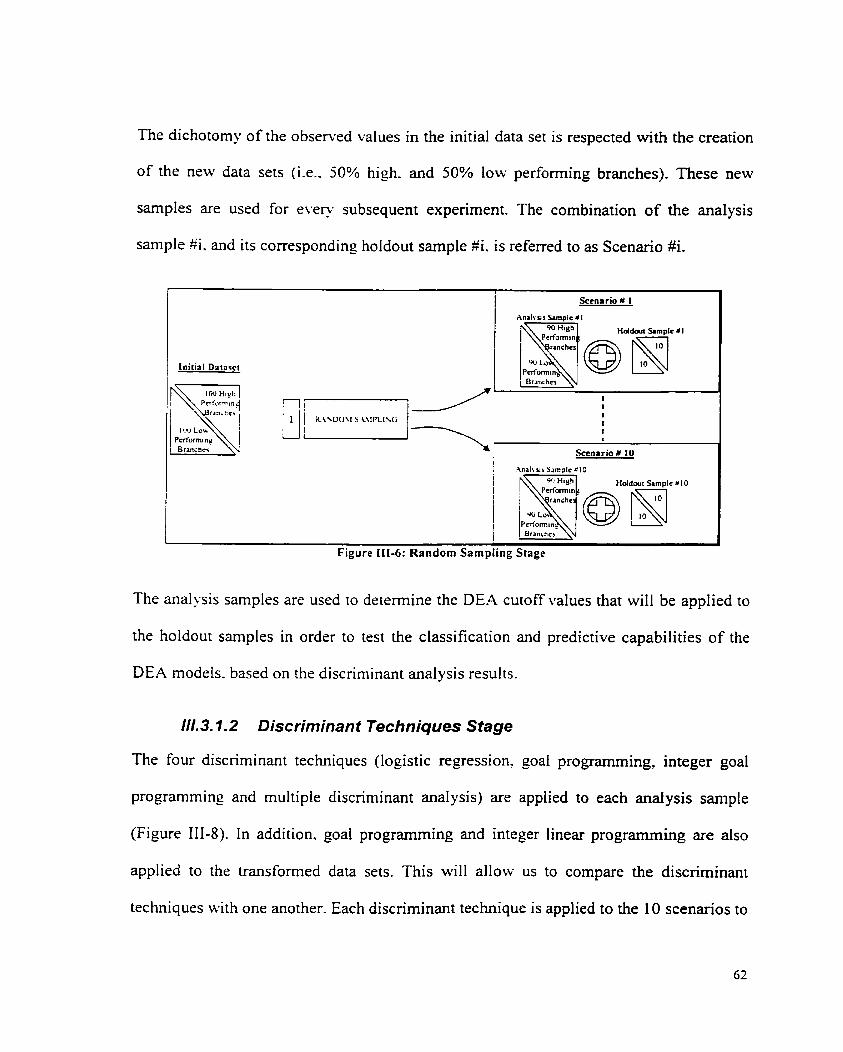

Acquisition: The bank branch consuItants have provided standard data such as the

number of employees and the nurnber of RRSP sold per branch (Table 111-1). In

addition. as pan of their expertise. they have dassified a set of branches into two

groups: specifically. lotv and high perforrning branches:

Formulation: We use the standard data to build the DEA models. and then utilize

discriminant techniques and operational research 1001s to formulate and integrate the

branch consultant expertise into these models:

Transfer: The entire set of information provided by branch consultants (standard data

and espertise) is integrated into the selected DEA models. to compare their

performance rvith "classical" DEA models. and thus demonstrate the possible

improvements that can resuh:

Test & Validation: The models thus obtained are tested and used to provide

benchrnarking resulrs that can aid branch consultants in managing the branch

network.

Figure 1-3: Knowledge Acquisit ion T o Irnprove DEA hlodels

In the chapter to follow. we review some of the basic DEA and classification models.

This \vil1 pro~pide the necessary fiarnework for the development in Chapters 3-5.

Conclusions are presented in Chapter 6.

II. OVERVIEW OF PERFORMANCE MEASUREMENT MODELS AND CLASSIFICATION TOOLS

11.1 DATA ENVELOPMENT ANALYSIS MODELS

11.1 .l The concept

Data Envelopment Analysis (DEA). a frontier analysis tool, is a special application of

linear programming based on Farrell's frontier methodology [57FM] as advanced by

Chames. Cooper and Rhodes [78CA]. and Banker. Chames, and Cooper [WBR].

DEA compares the inputs and outputs of Decision-Making Units (DMUs) and assesses

their relati\.e efticiency. .A DMU is a basic entity (e.g.. a bank branch) utilizing several

inputs to produce a set of outputs (Figure 11-1 ). that the decision-maker wishes to analyze

and rank nithin a comparable set of entiries (DMUs). DEA calculates a masimal

performance measure for sach DMU r-elariiv ro al1 other DMUs in the observed

population. with the sole requirsment that each DMU lie on or below the estremal

frontier. It is a relative bencharking tool. which means that the set of best practices is

based on the set of DMUs being considered at the time. Each time a new DMU is

included in the samplr. the set of best practices and the efficient frontier have to be

recomputed.

gure II-! : ri Bank Branch

The DMUs found to be inefficient are stnctly inefficient in a Pareto sense in that at least

one other DMU can produce at least the sarne outputs using less inputs. A significant

feature of DEA is that it allows for the inclusion of multiple input and output variables

that are calcuiated simultaneously. This ability sets DEA apart from the other single

dimension analytical techniques generally used in comparative analysis (e. g.. ratio

analysis and regression analysis). It is. thersfore. a performance measurement technique.

\vhich can be used for evaluating the relative efficisncy of DMUs in organizations.

Conventional ratio analyses give different pictures depending on the particular analpzed

ratio. In addition. it is difficult to combine an entire set of ratios into a single judgement.

This n.ould be especiall). true i f one wcre to increase the number of Dh,ILs.

In contrast to pararnetric approaches ~vhose objecti\.e is to optimize a single regression

plane through the data. DEA optimizes on each indi\.idual observation with an objective

of calculating a discrete piecet\-ise frontier. the efficient frontier. dettirminsd b). the set of

Pareto-efficient DMUs (Figure 11-2).

Pîrarnetric approaches require a specific functional forni (e.g.. a regression equation. a

production function. etc.). relating the independent \.ariables to the dependent variable(s).

The functional form selected also requires specific assumptions about the distribution of

the error t e m s (e-g., independently and identically normally distributed). and many other

restrictions. In contrast. DEA does not require any assumption about the functional form.

O O 5 10 15 20

INPUT -- - - --

Figure 11-2 : Cornparison Of DEA And Regression Analysis

The purpose of DEA is to find the best strategy to bring inefficient DMUs (belou. the

efficient frontier) ont0 the efficient frontier. either by reducing their inputs (the use of

their resources such as the number of cashiers), or by increasing their outputs (irnproving

somr parameters such as the numbers of operations per hour). This is illustrated by

Figure II-;.

By projectin each unit ont0 the frontier, it is possible to determine its Ievel of

inefficiency bjr comparison to a single reference unit or to a combination of reference

unirs. The projection refers to a vinual efficient DMU, which is a combination of one or

more efficient DM&. Thus. the projected point may itself not be an actual DMU.

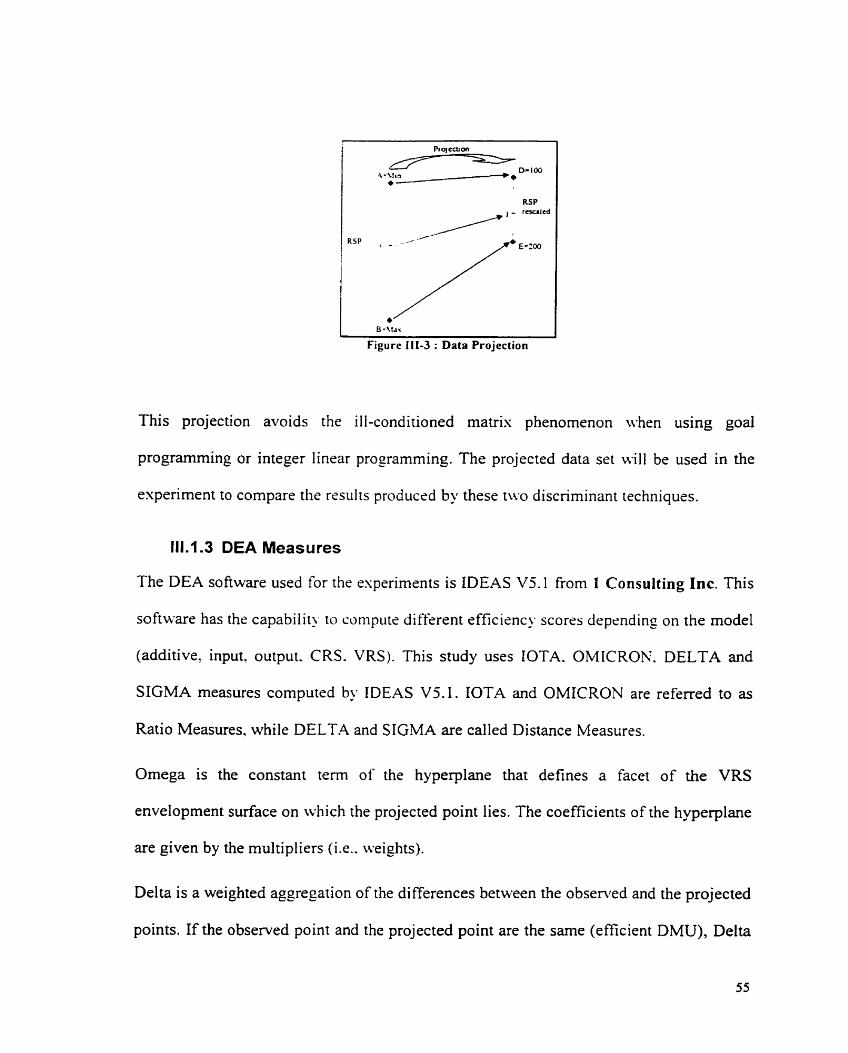

I For the additive rnodel we can cornpute the corresponding efficient DMU of every DMUj by using the following projection: .y, . )-, 1 + ( .\' , . f , ) = (.y, - s-', 1; + ) . The slacks for an efficient DMU are both

nul!. Thus. this formula wiil give the DMU itself if it is an efficient one (identity mapping for efficient DMUs). See the surnrnac. tables for the projections of each rnodel.

INPUT

. .

Figure 11-3 : Enveloprnent Surface For The Additive hlodel

In summary. the DEA approach offers three main features:

1. Characterization of each DMU b!. a single summary relative-sfficiency score;

2. DMU-specific projections for irnpr~\~ements bascd on best-practice DMUs; and

3. Obviation of the alternative and indirect approach of specieing abstract statistical

models. and making inferences based on residual and parameter coefficient analysis.

11.1.2 DEA Models

DEA. in e\-aluating an!. number of DMUs. with any number of inputs and outputs:

Requires the inputs and outputs for each DMU to be specified:

Defines efficiency for each DMU by an objective function. The objective function in

DEA can be ratio oriented (outputs!inputs). or net protit oriented (outputs - inputs);

In calculating the efficiency of a particular DMU. weights are chosen to maximize its

efficiency. thereby presenting the DMU in the best possible light.

L 1 I 1 Figure I I 4 : DEA Ratio And Net Proiit Oriented Models

Man', DEA models and extensions can be found in literature. The main ones are the

additive model and the extended additive mode1 [87CA]. the multiplicative models

[83C.A]. the CCR (Charnes. Cooper and Rhodes) mode1 [78CA]. the BCC (Banker.

Charnes. and Cooper) mode1 [84BR]. and their ratio counterparts. Each model can have

different options. We discuss only the CCR. BCC. and additive models herein.

Ratio oriented models

11.7.2.1 DEA Mode1 Options

DEA offers three different orientations; input-oriented models, output-oriented models

and additive oriented rnodels (also called base-oriented models). Each of these

orientations can ha\.e constant returns to scale or variable returns to scale.

Net profit oriented models

In the input-oriented models, the inefficient DMUs are projected ont0 the efficient

frontier bl. decreasing their consumption of inputs. Input minimization allows us to

determine the estent to which a DMU can reduce inputs while maintaininç the curent

le\.el of outputs. This might occur in a situation where competition limits the market for

finished goods.

In the output-oriented models, the inefficient DMUs are projected ont0 the efficient

frontier by increasing their production of outputs. Output rnaximization might be used

when the inputs are constrained, such as by a fixed allocated budget, and the emphasis is

on increasing the outputs.

In the base. or additive models. inefficient DMUs are projected ont0 the efficient frontier

by simultaneously reducing their inputs and increasing their outputs to reach an optimum

level.

Figure 11-5 is an illustration of these possible orientations. The efficient DMU P5-1 is the

input projection of the inefficient DMU P5. Similarly. the efficient DMU P5-0 is its

output projection. and P2 is its base projection. However. there are cases where an input

reduction or an output increase u-il1 not be sufficient to make a DMU efficient because of

the fronrier boundaries. In such cases. additionai movement toward the envelopment

surface ma!. be necessar!. via an input reduction (DMU P7) or an output augmentation

(DMU P6).

O 2 4 6 8 10 12

l NPUT

Figure 11-5 : DEA hlodel Orientation

The constant retums to scale (CRS) model assumes that one unit of input results in a

constant nurnber of units of output (Figure 11-6). The variable returns to scale (VRS)

model assumes that one unit of input can result in a number of units of output. where this

number can be different at any point on the input scale. In the VRS model. DEA

determines the relationship (positive or negative) as well as the size of the retums to

scale. This provides flexibility to test different scenarios of performance based on

different assumptions. Additionally. under the VRS rnodel, one can explore the impact of

input minimization or output maximization.

O 2 4 6 8 1 O 12

INPUT

Figure 11-6 : Envelopment Surface For The Additive Mode1

The computing process is the sarne for any model. Given a set of n DMUs. the model

deiermines for each DMUo the optimal set of input weights and output weights that

optirnize its efficiency score under the set of constraints represented by DMUs in the

cornparison set. The objective funîtion gives the efficiency score o f the DMUo. This

process is repeated n times- once for each DMU, that has to be rated.

11.1.2.2 Efficiency measures in DEA

As can be seen in Figure 11-6, an efficient score can be computed for every DMU. This

efficient score is based on the efficient frontier and the projection o f the DMUs to this

frontier. Thus, the efficiency depends on the model itself. For a given DMU,. the input-

D, oriented efficiency score. for example, is given by the fol lo~ing formula: E, = - .

D,

where Dj is the distance of the DMUj from its projected point on the output axes and 8,

the distance of its projecred position on the fiontier fiom its own projection on the output

axes. For instance. the efficiency for the DMU, in the case of the VRS model is

AP. E- =- while the efficiency for the DMUl is E, = - AP3 = 1 = 100% . A P- A 4

This figure also illustrates the impact of a CRS model on the efficient fiontier and the

efficiency scores. Indeed. this model relaxes the convexity constraints. which reduces the

number of efficient DMCis (P I . P; and P7 are nu longer efficient). and ofien lowers the

efficiency scores of the inefficient DMUs. With this model. the same DMU7 has a score

clearly smaller than with the VRS model:

The following sections present the principal DEA models with their characteristics and

properties. We highlight specifically the basic radial projection models. and the additive

or base model. We do not discuss. herein, models such as the multiplicative DEA

structure. These models are the application of the additive models to the logarithrns of the

original data values. Therefore. the interpretations of the additive models apply, but in the

transformed logarithmic space. They yield log-linear envelopment surfaces.

1 . 2 3 The CCR Model

The CCR [78CA] model determines the set of weights that maximizes any DMU

efficiency relative to other DMUs of the sample. provided that no other DMU or convex

combination of DMUs could achieve the same output vector with a srnalier input vector.

In the input-oriented model (Figure 11-7): the objective is to produce the observed outputs

using a minimum level of resources.

Figure 11-7 : Envelopment Surface For The CCR-1 Mode1 (CRS)

In the output-oriented mode1 (Figure 11-8). the objective is to produce the maximum ievel

of outputs gi\*en an observed level of inputs.

O 2 4 6 8 10 7 2

INPUT

Figure 11-8 : Envelopment Surface For The CCR-O Model (CRS)

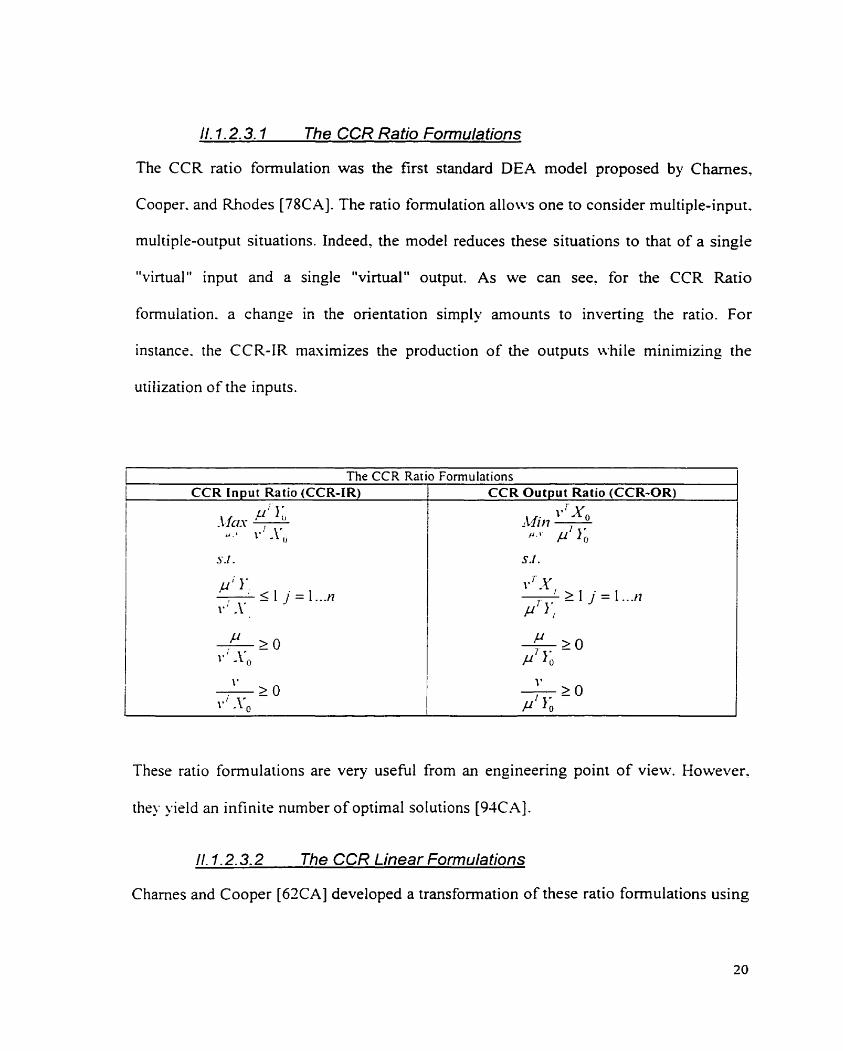

11.1.2.3.1 The CCR Ratio Formulafions

The CCR ratio formulation was the first standard DEA mode1 proposed by Charnes,

Cooper. and Rhodes [78CA]. The ratio formulation allows one to consider multiple-input.

multiple-output situations. Indeed, the mode1 reduces these situations to that of a single

"virtual" input and a single "virtual" output. As we c m see. for the CCR Ratio

formulation. a change in the orientation simply amounts to inverting the ratio. For

instance. the CCR-IR masimizes the production of the outputs while minimizing the

utilization of the inputs.

The CCR Ratio Formulations CCR Input Ratio (CCR-IR) CCR Output Ratio (CCR-OR)

These ratio formulations are very useful from an engineering point of view. However.

the). >.ield an infinits number of optimal solutions [93CA].

/1.1.2.3.2 The CCR Linear Formulations

Chames and Cooper [62CA] developed a transformation of these ratio formulations using

linear fractional programming and a representative solution (vTxo=l). Consequently. by

replacing the expression vTxo with 1. each of these formulations can be solved using their

corresponding net profit oriented mode1 formulations. Figure 11-9 sumrnarizes the mode1

equivalencies. The follo\ving figure presents the prima1 and dual input formulations of

the CCR linear model. There are CCR output oriented linear rnodels as weI1, but we will

not present these here. A DMU is efficient in a CCR input oriented model if and only if it

is efficient in the corresponding CCR output oriented model.

A small non-archimedian infinitesimai E has been introduced to prevent the zero weight solution [83CA].

The projectrd coordinates for an' DMU are: + ex, - S- ; y. + Y, + St

The CCR Linear Formuiations

The absence of the convesity constraint reduces the number of efficient DMUs and

results in a constant returns to scale envelopment surface (Figure 11-6).

Input-Oriented CCR Prima1 (CCRp-1) - - Adin z,, = B -E. 1s- - E . 15-

d ;..\- . \

S.[ .

1-2 - s- = 1;

&Y,, --Y2 - 5 - = O

%.s* .s - 2 O

We might have some cases where the proportional input reduction by itself may not be

sufficient to achieve efficiency; specifically, we might have to reduce some inputs and

augment some outputs (positive input and output slacks are frequently necessary to reach

the envelopment surface). This is common with multiple inputs and outputs problems.

Input-Oriented CCR Dual (CCRD-1)

Max wo = ,ury0 p.r

SJ*

vrx, = 1

~ ' Y - V ~ X 5 O -

pT 2&.1 -

v r 2 E. 1

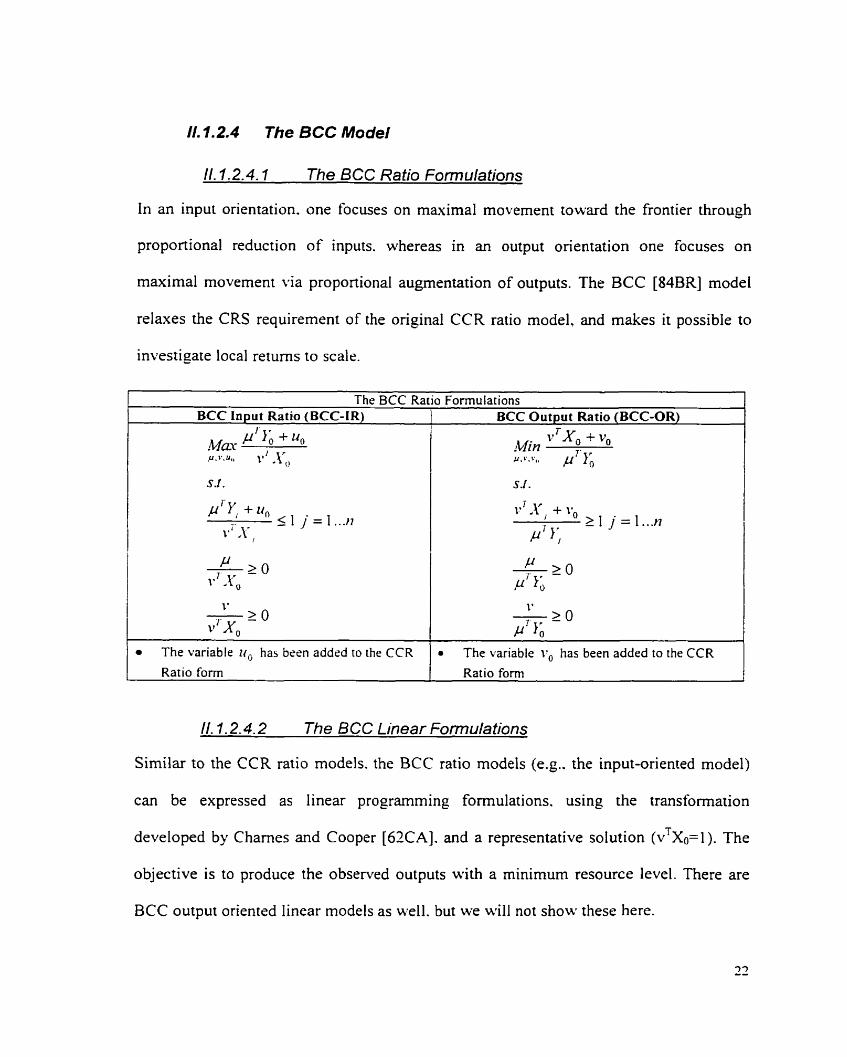

11.7.2.4 The BCC Mode1

11.1.2.4.7 The BCC Ratio Fomulations

In an input orientation. one focuses on maximal movement toward the frontier through

proportional reduction of inputs. whereas in an output orientation one focuses on

maximal movement via proportional augmentation of outputs. The BCC [84BR] mode1

relaxes the CRS requirement of the original CCR ratio model. and makes it possible to

investigate local retums to scale.

S.I. I

The BCC Ratio Formulations

- - - --

The variable I r , has been added ro the CCR-IT The variable iTo has been added to the CCR

BCC Input Ratio (BCC-IR)

+ u, M a . P.'..., ,*l'.\r()

BCC Output Ratio (BCC-OR)

v T x , + v, min P.'.',, p7'&

II. 1.2.4.2 The BCC Linear Formulations

Ratio forrn

Similar to the CCR ratio models. the BCC ratio models (e.g.. the input-oriented model)

can be expressed as linear programming formulations. using the transformation

developed by Chames and Cooper [62CA]. and a representative solution (vTxo=l). The

objective is to produce the observed outputs with a minimum resource level. There are

BCC output oriented linear models as well. but we will not show these here.

Ratio forrn

I f a DMU is efficient in a CCR model it will also be efficient with the BCC modeI. but

the converse does not nocessarily hold [88BR].

The BCC Linea Input-Oriented BCC Primal (BCCp-1) - -

Mit? Z, = 8 - E. Is' - E. Is- t I . i . \ * . b

r Formulations Input-Oriented BCC Dual (BCCD-1)

7 M a y rr, = p Y. + tc, p.)'

Sf.

i " ~ , = I

1 The scalar variable 0 is the proportional reduction applied to al1 inputs of DMU,. A DkIU is efficient if and on[>. if û* = 1 and al1 slacks are zero.

Or. a DMU is efficient if and only if Z; = il{ = 1 . An!. non zero slacks and the value 0* <= I identiQ the sources and amount of inefficiencies that may be present. The projected coordinates for an' DMC on the efficient frontier are:

,Y, -P &Y, -s- : 1; + 1; -t s-

Figure 11-9 is an illustration of the relations between ratio and linear DE4 formulations.

For esample a CCR input ratio model can be transforrned into a CCR input linear model

by using the solution \?io = 1.

vTX,= I CCR-IR < CCRp-1

CCR-OR CCRD-O

I.~S, ,= I CCR-OR < > CCRp-O

Figure 11-9 : Ratio Vs L

vT.L ,= 1 BCC-IR BCCD-I

vTX ,= 1 BCC-IR BCCP-1

BCC-OR BK,-O

vTX, = 1 BCC-OR Bcc~-O

near DEA Formulations

i . 2 5 The Additive Model

As illustrated in Figure 11-5. the additive (or base) model projects along both output and

input dimensions. The additive model selects the point on the envelopment surface that

maximizes the L I distance in the "nonhwesterly" direction (reduces the inputs and

increases the outputs). This model has variable retums to scale and the efficient frontier is

invariant with respect to an affine translation of the data (consequences o f the convexity

constraint in the prima1 problrm or the unconstrained variable uo in the dual).

The Additive Model Additive Prima1 (ADDp) l- Also calfed the Envelopment Form - - M i 1 7 = - 1 s * . - - - 1 s -

K . % . \

- - 2.5 .s 2 0 n : number o f DMUs Y : marris o f output measures X : matris o f input measures

Additive Dual (ADDD) Also called the Multiplier Form

7 Alm Il-(, =,Y Y. - leJ -Yo + uo , U . 1 ' . l i , ,

s* and s- : siack variables on inputs and outputs

DMUo is efficient if and onl? if Z: = i1.I = O

DMUo is inefficient if and only if s*' # O or s-' # O The projected coordinates for an' DMU on the efficient fronrier are:

11.1.3 Major DEA Model Extensions

In realistic situations. one might need to incorporate some variations into the DEA

2 4

models such as non-discretionary variables. categorical inputs and outputs. and

qualitative data factors. We might also want to incorporate judgment or a priori

knowledge in the form of restrictions on variable rnultipliers. Because non-discretionary

variables are beyond control of the DMU's management. they will be excluded from the

objective function of the model but not from the constraints. With categoncal inputs and

outputs. one could run different DEA models for each category by following a

hierarchical process based on the hierarchy of the categories. Judgment or a priori

knowledge allows the analyst to tune hislher model in accordance with hisher knowledpe

of the situation. One will be able to restrict the range of the multipliers. for example.

11.1.4 Strengths and Limitations of DEA

DEA provides a new approach to organizing and analyzing data ("discussing ncu- truth").

It demonstrates that by the use of another methodology. unanticipated insights ma' be

obtained and ma'. therefore. redirect managerial action. The DE.4 framework creates a

new approach for learning from outliers and for applying new theories of best practice. It

provides a mors comprehensive picture of organizational performance. In fact. DEA

seems to be a very suitable tool that offers the possibility of handling multiple inputs and

outputs stated in different measurement units. It focuses on a best practice frontier instead

of the population central-tendencies: the inefficient DMUs are compared to their

projected efficient DMUs in order to analyze their inefficiencies. The multiple DEA

variations allow one to address many managerial problems by taking into account their

own properties (limited inputs and/or outputs, for instance).

DEA. as with other concepts has some limitations not yet resolved and some unexplored

dimensions. Noise in the data. even symmetncal noise with zero rneans. such as

measurement error. can cause significant problems. Statistical hypothesis tests are

difficult and are the focus of ongoing research. Finally. the standard formulation of DEAS

which creates a separate linear program for each DMU. c m be computationally intensive

for large problems.

In this section the basic DEA models have been exarnined. In the section to follow. some

of the standard models for handling classification data are discussed. It is emphasized

again. that the mode1 structures devsioped in later chapters are designed to evaluate those

situations where standard numerical data in a DEA setting is augmented with

classification data. Hence. there is a need to examine which classification methodologies

best suit this linkage essrcise.

11.2 DISCRIMINANT MODELS

In this section we review some of the standard classification rnodels. Specifically. we

examine logistic regression. multiple discriminant analysis. and goal prograrnrning.

11.2.1 Logistic Regression

/1.2..1 Introduction

The logistic regression technique [94DK] analyzes the relationship between dependent

(or response) variables and independent (or explanatory) variables. The dependent

variables are always categorical. while the independent variables can be categorical

(factors) or continuous.

When we study a random ~eariable Y using a linear model. we specify its espectation as a

h'

linear combination of K unknown parameters and covariates.: E ( Y ) = ,u = P, x, . k

We introduce a more generalized forrn called the link function: >I = g ( p ) .

The link function defines the mode1 used. which c m be determined by the distribution of

the randorn component. The distribution of the random component in Y (the part that

cannot be systernatically esplained by s variables) determines the type of generalized

linear rnodel (Figure 11-1 O). The distribution of the randorn component cornes from an

exponential family. to which the normal. binomial. and Poisson distributions beIong.

Ordinary Least Squares (OLS) assumes the normality of this distribution. while the Logit

and Probit models are both based on the binomial distribution.

Logistic regression has the advantage of being less affected than multiple discriminant

analysis (MDA) when the basic assumptions, particularly normality of the variables, are

not met. It also can accommodate non-metric variables through dummy-variable coding,

jus1 as regression c m . It is limited, however, to prediction of only a two-group dependent

measure. Thus. in cases where three or more groups form the dependent measure. MDA

is best suited.

Distribution of the Lin k Function

Binomial Logit

--

Binomial Probit = ' P h is

the inverse of the standard normal cumulative distribution function

Poisson Logarithm 7 = log(^)

Multinomial Multinomial Logit P q = l o g ( L ) j = 1, ..., J

PJ Figure 11-10: hlodet Classification Based On The Distribution OfThe Random Cornponent

Logit models have only two categories in the response variable - event A or non-A. The

response variable y is a realization of a binomial process.

We may express logit models in probability form:

The probability of non-event is then:

By simplifying. we O btain:

Therefore. we can state that:

The fraction - is called the odds ratio. Norv. take the natural log of the odds ratio: 0 - p, )

J11111 lim Prob(1' = 1) = l und lim Prob(I' = l ) = O ,$;-++x p. r - -cc

L ' is called the logit. and hence the name logit model' (Figure 11-1 1) .

I L, the log of the odds ratio, is not only linear in X. but also (fiom the estimation viewpoint) linear in the parameters. However. Although L is linear in X. the probabilities themselves are not. This property is in contrast uith the LPM model where the probabiiities increase linearly with X. ' The interpretation of the iogit model is as follows: the P, measure the change in L for a unit change in x,. The intercept P, is the value of the log-odds when X =O. Like most interpretations of intercepts, this interpretation may not have any physical meariing. Given a certain x,, if we actually want to estirnate not the odds in favor of being solvent but the probability of being solvent itself, this can be done directly fiom

I once the estimates of p l and p, are available. J + exp(-(P, + P, -Y, 1)

-- - O

Figure 11-1 I : Logit Üesponse ~ u n c t i o n

2 1.3 The Maximum Likelihood Estimation

Estimation of binary choice rnodels is usually based on the method of Maximum

Likelihood. Each observation is treated as a single draw frorn a Bernoulli distribution

(binomial with one draw - Figure 11-1 0). The mode1 with success probability F(P's)' and

independent observations leads to the joint probabili ty. or Iikelihood function:

By stating that P, = F(Ptx) , this formula can be rew~itten more conveniently as

Since it is easier to work with sums than with products we start by taking logarithms.

h(L) = x[i; L ~ P , + ( 1 - Y, )Ln(l - P, )] I

Maximizing the likelihood L is equivalent to mavimizing the Log Likelihood Ln(L).

Therefore. the first derivatives are computed with respect to each of the K coefficients PL,

and set to zero. The solutions of these K equations. called the likelihood equations. will

give the Maximum Likelihood &timation2 (MLE) estimators. The logit iikelihood

equation c m be written as:

Where the term in brackets is the deviation between the observation Y i and its expected

\-alue. X , are the weights.

1 The general Framework of probability models is: Prob(Y = 1 ) = F(P'x) and Pmb(Y = 0) = 1 - F(P'x). ' The minimum chi-square estimation for replicated. dichotomous data is an alternative to maximum likelihood estimation.

11.2.2 Multiple Discriminant Analysis

11.2.2.1 Introduction

The basic purpose of multiple discriminant analysis (MDA) is to estimate the relationship

between a single nonmetric (categorical) dependent variable (groups) and a set of metric

independent variables (predictors). The MDA can classify more than two groups'. When

two classifications are involved. the technique is referred to as two-group discriminant

analysis (DA) in contrast kvith MDA.

The MDA identifies the areas m-here the greatest difference exists between the groups.

derives a discriminant weighting coefficient for each variable to reflect these differences.

and then assigns each indi\.idual to a group using the weights and each individual's

ratings on the characteristics. The ultimate goal in MDA is to predict to which group a

new observation belongs.

11.2.2.2 Discriminant Analysis Model

MDA is based on centroids2 and groups (Figure 11-12). The centroids indicate where the

groups are centered or located. In general. the more centroids for the groups differ. the

easier it is to distinguish between the groups. However, most of time the difficulty is to

distinguish the groups when there is an overlapping area.

[ Problems involving only two groups could be handled with lest squares regession. ' A centroid is the mean value for the discriminant Z scores for a particular category or group. A two-group discriminant analysis has two centroids. one for each of the groups.

.\ Figure 11-12 : Discriminant Analysis Centroids

MDA involves deriving the linear combination of the two (or more) independent

variables that \vil1 discriminate best between the a priori defined group. This is achieved

by the statistical decision rule of maximizing the between-group variance relative to the

within-group variance. This relationship is expressed as the ratio of between-group to

within-group variance (Figure 11-13). It is similar to maximizing the between-group

variance and minimizing the within-group variance. If the variance between groups is

large relative to the variance within the groups, we say that the discriminant function

separates the groups tnell (Figure 11-1 4).

MDA Ruie

MAX ( Between - grorrp var iance) Benveet~ - group variance Ifirhir~ - group var lance ] 0 ami

MIN(WÏrhitr - groirp var tance)

Figure 11-13 : M D A Ruie

The linear combinations for a discriminant analysis are derived from an equation that

takes the following fom:

1

2, = Discriminant score

= Discriminant weight for the jIh observation and the i l h variable

X, = id' Independent variable for the jth observation I

The centroids for the two groups. Cl and C2. are the average discriminant scores of al1

the observations within each group. They indicate the most typical location of an

observation from a particular group' and a cornparison of the group centroids shows how

far apart the groups are along the dimension being tested.

The test for the staristical significance of the discriminant function is a generalized

measure of the distance betkveen the group centroids. This is done by comparing the

distribution of the discriminant scores for the two groups. If the overlap in

distribution is small. the discriminant function separates the groups well.

the

-- Figure 11-14 : M D A Overlapping Distributions

11.2.2.3 Determining the Cutoff Value

There are different ways to determine an appropriate cutoff value. One way would be to

select the cutoff value that minimizes the number of misclassifications in the analysis

sample. Another way would be to select the cutoff value as the midpoint between the

centroids of the groups:

Here Ni and N2 are. respectiveIl.. the numbers of observations in groups 1 and 2. Figure

11-15 is an illustration of the cutoff \ralue ~vhen the two group sizes are equal and

differenr. The right-hand side shows tw-O cutoff values: the unweighted cutting score does

not take into account the Sroup sizes. and thus leads to a poor classification.

Optirnrl iut:ins 5 id rc iiith cqual urriplc ,ire\

Figure 11-15 : %IDA Optimum Thresholds

Generally. MDA attempts to minimize the oïerlapping area b e t w r n groups. Depending

on how data are distributed. these cutoff value approaches can lead to poor classification

results. Therefore. we use a more refined cutoff value. which considers the cost of

misclassifying an obsenration into the wonp group. The optimum cutting score will be

the one that minimizes the cost of misciassification. It is represented by:

LN(.): natural logarithrn

, (q - l)$, + (17: - l)s;, SE, =

n, + nI - 2

C( 1 12): the cost of classifiing an observation into group 1 when it belongs to group 2.

C(2ll): the cost of classi-ing an observation into group 2 when it belongs to group 1.

P l : the prior probability that a new observation belongs to group 1 .

P:: the prior probability that a new observation belongs to group 2.

.4 more re fined formula is sometimes used. the Mahalanobis distance measure. which

takes into account the differences in the covariances between the independent variables

[97GR'].

11.2.3 Linear Goal Programrning Discriminant Models

II. 2.3.1 Introduction

Linear goal programming (GP) is a polverful extension of linear programming (LP). The

goal prograrnming approach is probablj. most popular for handling multi-objective

problems. It has the added conveniences that different objective fùnctions can be

measured in different units. and that it is not necessary to have al1 the objective functions

in the same forrn (masimization or minimization).

The first step in fomulating a GP mode1 is to create a constraint for each goal in the

problem (Figure 11-16). This allows us to determine hou- close a given solution cornes to

achieving the goal. Thus. a goal can be viewed as a constraint with a flesible Right-Hand

Side (RHS) value.

The RHS value of each constraint is the target value for the goal because it represents the

level of achievement that the decision-maker wants to obtain. The ~rariables d,+ and d,- are

called deviational variables. in that the' represent the amounts by uhich each goal

deviates from its target \value. The d,* represents the amount b!. ivhich each goal's target

value is underachieved. and d,- the amount by which each goal's target value is

overachieved ' .

1 1) In goal programming it does not make any sense for both deviational variables to take non-zero values simultaneously. In fact. due to the nature of the solution process. we do not have to model this condition. 2 ) In a GP problem. not al1 constraints have to be goal constraints. .4 GP rnodel can also include one or more hard constraints typically found in LP problems.

l I

Goal constraint formulation

1 1 Dscision variables 1 1 RHS = Target Value 1

1 Deviaiional variables I 1

Figure 11-16 : Goal Programming Constraint

The objective in a GP problem is to detemiine a solution that achieves a11 goals as closely

as possible. The ideal solution to any GP problem is one in which each goal is achieved

esactly at the level specified by its target value (d,- = d,- = O). One possible objective

(many variations are possible and depend on the probIem itself) would be to minimize the

sum of the deviations:

Min x ( d , + tri:)

Based on these principles. mode1 formulations depend on the problems treated and the

decision-maker's objectives. Indeed, some goal constraints will be more important than

some othrrs. or the objective function ma? emphasize one specific goal being reached

before some others would (preernptive goal programming). We can find many variations

in the literature [90GF]. One of them is the use of goal programming as a dis cri min an^

11.2.3.2 Goal Programming Discriminant Models

Applications of linear goal prograrnming-based approaches in discriminating between

two groups of observations. have appeared in numerous publications [95GF]. The main

idea here is that with GP models. we seek a hyperplane to separate two groups of points

"in the best possible way". regardless of whether or not they can be completely separated

[90GF].

A goal programming discriminant problem will have three parts:

1 . The objective function. which determines the way the model will solve the problem.

If the objective is to minirnize the number of misclassifications, we will use models

such as integer programming ($ 11.2.3.2.1). If the objective is to minimize the total

amount of esternal deviations and masirnize the total amount of intemal deviations

from the separating hyperplane. Ive will use models such as Giover's formulations

(9 11.2.3 .X) .

2. The constraints. representing the observations of each group. will be espressed

according to the model and the objective function.

3. The extemal constraints. not rea1Iy based on the model but necessary to reach an

optimum solution and avoid some problems such as the zero solution.

Many difficulties arise m-hen we try to discriminate between overlapping groups. Some

formulations have been proposed to handle these cases [86GF]. They al1 depend on the

problem itself and the objectives sought. The. could be of simple linear form,

incorporating variables such as interna1 and estemal deviations, or of a more complex

form. using quadratic. power or logarithrnic models.

11.2.3.2.1 lnteaer Goal Programmina Mode1

The integer programming formulation. where the objective is to minimize the nurnber of

misclassified points, c m be stated as follows:

subject to :

A , x - M y , <b i E G,

-4, x + iLI7, > b i E G?

7. E ~0.1) I. b wu-estricted in sign

A,. i E GI. represent the points of group 1 and A,. i E G?. represent the points of

group 2 (A, is an n-vector in Euclidran space):

x is the associated n-vector of variables that weight the points A,:

b is the scalar variable (The Threshold):

M is a large positive nurnber and is related to the esternal deviations. which a i s e for

points on the wrong side of the hyperplane (improperl?. classified):

-J, are binary integer variables (O or 1). which are used to count the number of

violations;

The discriminating ability of this mode1 can be improved by adding an infinitesimal

parameter. Say E: which avoids having some observations lying on the hyperplane

(neither in the group 1 nor in the group 2).

subjeci to : A , x - My: < 6 - E ~ E G ,

.-l,s+My, > b t & k G 2

7, E (0.1) .Y. 6 rrnrestricted in sign

In Figure 11-17. we can see how the mode1 discriminates between groups. A circle

represents the observations from group 1 and a star, those from group 2 . As we can see

that observations 2 and 5 are misclassified. Therefore, their corresponding y variables

\si11 take on the value of 1. and the others will be zero. The value of the objective

function will be 2. meaning two misclassified observations are present.

Group Differentiation with Integer Programming

Croup 2

Figure 11-17 : Illustration Of Integer Programming Discriminant Model

11.2.3.2.2 Glover's Fornula fion

Glover. in [90GF] introduces two models based on the same assumptions. but differing in

the way they handle the points lying on the hyperplane. The full model introduces two

variables a0 and Po, whereas the reduced mode1 uses an infinitesimal variable. B. In fact,

the full model can be formulated with or without E, but it is not recomrnended pnmarily

because it induces a redundancy. and makes the interpretation more difficult.

Full mode1 (with or without E) Reduced Model

s, b unrestricted in sign

Minirnize ~ l l n , - ~ k , f l

subject to :

( I ) . . i ,x -a , +P, = h - r ~ E G ,

(2).4,s+ori -Pr = b + r i~ G,

(;)a, 2 O

(3)P. 2 0

( 5 ) n , X ( P 1 -a.)+q Z(P, -a.) = 2n,n2 f * 1;, .cc;.

x. b unrestricted in sign

Where : A,. i E G I - represent the points of group 1 and Al. i E Gz. represent the points of group 2 (A, is an n-vector in Euclidean space); s is the associated n-vector of variables that weight the points .A1: b is the scalar variable; a, represent the external deviations. which arise for points on the \+Tong side of the hyperplane (improperly classified): pi represent the interna! deviations, which &se for points on the correct side of the hyperplane (properly classified); h, and ki are the coefficients that weight the external and internal deviations in the objective function; a,-, represents the maximum externa! deviation; Po represents the minimum internal deviation: ho and ko are the coefficients that weight a0 and Po; nl and nz are, respectively. the numbers of points in groupl and group 2: E is a non negative parameter utilized to induce a strict separation between the groups.

32

The goal is to minimize the weighted surn of extemal deviations and maximize the

weighted surn of intemal deviations (Figure 11-18). In problems where it is especially

imponant to correctly classify certain observations. those observations can be weighted

by increasing the appropriate h, and k, values in the objective function. Applying equal hi

and k, weights to both groups of data implies that the cost of a Type 1 error is equal to the

cost of a Type II error.

An example M-here Type 1 and Type II errors deserve different emphasis c m be the

following. N'hile tqing to identify banks that will succumb to bankruptcy. it ma' be

more important to be assured that a bank classified as financiallu strong will in fact

escape bankruptcy than to bs assured that a bank classified as financiall>- weak will

become insolvent. In addition. with the capacity to give higher weights to banks that are

dramatically successful or unsuccessful, the LP formulation will tend to position the "sure

bets" more deeply inside thsir associated half spaces. It is also a way of isolating these

cases that are difficult to discriminate. or even those that ~rould be considered as outliers

[90GF].

Group Differentiation with Overlapping Groups

I I I --

Figure 11-18 : Goal Programming Classification W'ith Overlapping Groups

The normalization constraint (constraint 5 in full and reduced models) is equivalent to

requiring a meaningful separation, and eliminates the nul1 weighting x=O as a feasible

solution. Glover in [89GF] has shown that the LP formulation employing the

normalization is a direct relaxation of a corresponding integer programrning problem for

minimizing the number of misclassified points.

Note that it is possible to obtain an LP discriminant analysis formulation that does not

require a normalization by relying on an objective function that is either derived from

regression analysis or that represents a norrnalization itseIf.

Even if some formulations tend to discriminate "well enough". it remains that for man-

problems. difficuities in efficient]! segregating groups will occur. due to degeneracy. as

has been pointed out in [86GF] : ". . . I A ~ S L ' CUSES represenr norhing pa[hologicul. Szrch un

ozrrconte nlerel~. signals [hm rhe grozdps cannor be separated, and thar rhe forin of group

oi*erlap co~fozrrids an). rensonuble 'purrial separarion' with the ppe of- n~odcl

enrplo-ved. . . ".

III. EMBEDDING EXPERT KNOWLEDGE IN THE ADDITIVE DEA MODEL

111.1 INTRODUCTION