Embed Size (px)

DESCRIPTION

Edge is the journal of LeighFisher

Citation preview

The Journal of LeighFisher

Issu

e#4

win

ter_

11/1

2

stepping back to focus inThe challenging economic climate demands global perspective and analysis

winter 11/12_0302_ The Journal of LeighFisher

We are in a

time of change,

which brings

fresh challenges.

However, this

also presents new opportunities

to refresh our ideas and apply

innovative solutions to the varied

and complex issues we face.

While the LeighFisher aviation

business is over 60 years old,

as Edge went to press in winter

2011/12 we were celebrating the

first 12 months of operations of

our surface transport and local

government businesses. This

expansion has allowed us to

broaden the scope of the strategic

management and consultancy

services that we can offer clients –

just the start of planned expansion

across a range of sectors.

We also continue to expand our

geographical coverage, with growing

LeighFisher teams in Europe, Asia,

and the Americas and major new

projects in Brazil and Ghana.

The current climate shows just

how interconnected the global

economy is and how boundaries

between sectors, especially

in infrastructure, are blurring.

LeighFisher, is a broad based

consultancy, in terms of our global

reach and the sectors in which we

operate. We provide clients with

robust advice, mixing our global

perspective with the sharper focus

of a genuinely expert team.

Europe / UKChris WilsonVice President [email protected]

Americas / AsiaMark LunsfordVice [email protected]

issue#4 winter_11/12

cont

ents

Nick Davidson President

04

The Journal of LeighFisher

Published by:© 3Fox International Limited 2012. All material is strictly copyright and all rights are reserved. Reproduction in whole or in part without the written permission of 3Fox International Limited is strictly forbidden. The greatest care has been taken to ensure the accuracy of information in this magazine at time of going to press, but we accept no responsibility for omissions or errors. The views expressed in this magazine are not necessarily those of 3Fox International Limited or LeighFisher Inc.

Design: Smallfury Design

Images: ©Jens Nieth / Corbis, Felix Pharand-Deschenes Globaia / Science Photo Library, Pascal Le Segretain / Getty Images, American Airlines / Oneworld, asterix0597 / iStockphoto, Mlenny / iStockphoto, © Bruno Levy / Corbis, © Pawel Libera / Corbis, photosindia / Getty Images, © Ocean / Corbis, Clayton Perry, Jorg Greuel / Getty Images, © Tim Griffith / Arcaid / Corbis, © Topic Photo Agency / Corbis, © Anindito Mukherjee / epa / Corbis, Xavier Marchant / 123RF, Sciepro / Science Photo Library, Jason Hawkes, © Jason Hosking / Corbis, Hypostyle Architects, European Investment Bank, Aeroservice / Science Photo Library, Andy Rain / European Press Photo Agency

2208

04 Future tenseRohit Talwar, CEO of Fast Future Research, forecasts challenges for the next 20-30 years

06 Reverse forecastTop-down or bottom-up – experts discuss which forecasting model works best

Surface transport

08 Broken journeyEurope’s road network is fast and flowing but cannot yet provide an uninterrupted journey

11 Fleeting visionOne of the fastest growing global economies needs rapid rail travel – and it needs it soon

15 Public works, private funding?Trust funds in the US can no longer fund major projects – can P3s step in?

Aviation

18 Look eastThe growth of aviation markets in Asian economies contains lessons for others

22 Changing skiesWith US airports already at capacity, what are the opportunities for growth in the market?

Government and infrastructure

27 Nerve stimulusA second government plan outlines major UK projects – but will the market buy into it?

30 Weather eye Despite public sector budget restraints, hospitals and schools are being developed

33 Root and branchUK government’s review of procurement – can it cut costs and deliver efficiency?

www.facebook.com/LeighFisher.Global

www.linkedin.com/companies/leighfisher

www.leighfisher.com

While the articles in this edition

of Edge draw from this breadth

of expertise, we are also open

to fresh thinking from external

sources. We invited Rohit Talwar

of Fast Future Research as guest

author. He shares his views on

the implications of the current

economic crisis on the developed

economies and also considers

how developing economies might

respond to this situation.

Similarly, we consider the

pros and cons of top-down

and bottom-up approaches to

forecasting, before a number of

LeighFisher experts contribute

views to this conversation. Given

the range of skills and sectors

represented by these individuals, it

is not surprising that the responses

demonstrate differing views and

opinions on the subject.

In surface transport we examine

India’s requirement for High Speed

Rail and the challenges faced in

delivering to a timeframe that will

keep pace with the demands of

this vast and expanding economy.

We also look at the gaps in the

European road network and ask

whether the system is as complete

as is often portrayed.

Two of our experts also put

forward their analysis of the current

state of aviation, with a focus on

India and the USA.

We also consider evolving

transportation policy in the USA

across all modes, and in particular

the dominant issue – how will future

schemes be funded?

Finally, we look at the £30 billion

Second National Infrastructure Plan

published by the UK government,

and the implications for future

infrastructure across all sectors. We

look at two related issues affecting

infrastructure and government in

the UK. We initially consider recent

developments in the provision

of social infrastructure and what

lessons can be learnt for the future,

before looking at developments in

procurement of infrastructure, and

the search for “lean procurement”.

This fourth edition of Edge

provides a platform for debate and

analysis from our experts across

many sectors and from around

the globe: economists, planners,

financial analysts and experts in

other related fields. Edge enables

them to share their expertise and

thinking with a wider audience,

and we hope that you will find their

views stimulating. ■

General

winter 11/12_0504_ The Journal of LeighFisher

Guest author ■

The core of the western world

(the US and Europe) faces at

least a decade of unavoidable

turbulence, volatility and painful

correction. A combination of a broken

financial system, massive debt, income

inequality, under-investment, unemployment,

an ageing population and increasing social

security and healthcare costs is creating

challenges that would test even

the most talented of governments.

While all this is happening, citizens

are becoming more public and vociferous

and corporations are increasingly shifting

investment offshore.

This is compounded by slow government

decision-making and a reluctance to solve

problems in a fundamental way.

For most of the developed economies, a

period of low economic growth with regular

recessions seems much more likely than

a sustained depression, though at times

businesses and the public might not be able

to tell the difference.

The US and Europe still hold immense

comparative advantages in areas that will

form the bedrock of tomorrow’s economy –

education, biotechnology, nanotechnology,

personalised medicine and green energy.

Training, planning, and a vision for tomorrow

will be essential.

The emerging marketsIt has been estimated that $6 trillion needs

to be spent by emerging market countries

by 2014, simply to meet their basic

infrastructure needs, and around

$12-33 trillion is required over the period to

2030. However, infrastructure investors will

almost certainly have to reduce expectations

for investment performance because poorer

nations simply will not be able to offer the

historic returns financiers have grown used

to. A radical overhaul will also be required in

infrastructure planning, design, construction

and maintenance to shorten delivery

timescales and bring down costs.

A key challenge is to develop decision-

making capability and the long-range

thinking skills of policy makers.

No developing economy has a golden

ticket that will protect it whatever the

economic outlook. Many will repeat the

same mistakes as their counterparts in the

developed world, in terms of slow decision-

making, under-investment in infrastructure

and failure to control the finance system.

However some should fare better than

others. China has major debt challenges but

has a reasonable chance of avoiding a hard

landing that would be globally damaging.

India must reform planning systems,

accelerate decision-making, bring down

punitive interest rates and ensure delivery

of high-quality infrastructure solutions if it is

to stand a chance of fulfilling its potential.

Some Indian sources see population

primacy occurring by 2025. It is hard to

argue with demographic data: short of

war or a pandemic, India will eventually

overtake China in terms of population. This

could bring either a demographic dividend

or a nightmare depending on investment

in education, the rate of growth of its

economy and the state of its environment.

For example, it has been suggested India

will run out of fresh water by 2020, and even

by 2015, 60% of India will still only have an

average per head income of less than $2 per

day. Educational advancement, infrastructure

development and economic growth are

essential. If these are achieved, India holds

much potential in the coming decades.

For China the point of being passed is

more important. China has one of the world’s

worst demographic outlooks and is ageing

rapidly. People over the age of 60 now

account for 13.3% of the population,

up nearly 3% since 2000. The figure could

rise to 25-30% by 2030.

For China, the economic burdens of

ageing could be significant, which in part

explains the emphasis on economic growth

– no poor country has aged in peacetime

to the extent that China is doing. China

is in a rush to become rich, as the cost

of supporting such an ageing population

means it simply has no choice. ■

Training, planning, and a vision for tomorrow will be essential

What will be the impact of economic uncertainty and change on infrastructure development? LeighFisher invited a leading global futurist to share his thinking. By Rohit Talwar, CEO of Fast Future Research

Future tense

For more information go to:

www.fastfuture.com

Surface Transport

winter 11/12_0706_ The Journal of LeighFisher

Ask the expertsGraham Heald – Reading, UK

“Top-down gives an approximately right answer while bottom-up

gives a precisely wrong answer.” While not entirely agreeing, this offers

guidance as to the best approach. If an approximate answer is all the

end user requires, a top-down analysis is usually quick and cheap to produce. A

bottom-up analysis is more complex but, if properly developed with allowance for

uncertainty, provides multiple answers, permitting better understanding of the issues

and risks surrounding a forecast.

A core activity undertaken by

LeighFisher teams across the

globe is predicting the future for

our clients and, whether it is for

the short or the long term, related to costs

or revenues, operations or infrastructure,

they all start by asking one simple question

– top-down or bottom-up? Indeed, it is not

just the forecasters at LeighFisher who face

this issue; many in marketing, management

and finance are asking the same question.

So what is top-down and bottom-up?

Simplistically, top-down involves analyzing

the “big picture”, or to put it another way,

it is essentially the breaking down of a

system to gain insight into its compositional

sub-systems. In a top-down approach

an overview of the system is formulated,

specifying but not detailing any first-level

sub-systems. Those who don’t like top-down

claim it is a process locked in “Ivory Towers”.

In contrast, bottom-up forecasting

overlooks broad sector and economic

conditions and focuses on the individual

attributes of a system. It pieces together

systems to give rise to grander systems,

thus making the original systems

sub-systems of the emergent system. Those

who don’t like bottom-up argue that the

process results in analysts who “cannot see

the forest for the trees”.

Of course, the true benefit of top-down

and bottom-up forecasts is that they look at

the world from differing vantage points. Both

have strengths and weaknesses. In addition,

many argue top-down approaches are better

suited to existing stable systems, while

bottom-up is more appropriate for systems

that either don’t exist or are likely to have

undergone radical change.

For the forecasters at LeighFisher, there

are two other dimensions to consider:

how much data is available and how much

time do we have? Top-down is arguably

less data-hungry and quicker to develop,

while bottom-up is often reliant on the

development of complex data-hungry

models and consequently, it can take a lot

longer to develop.

We thought we would ask a number of

people at LeighFisher, who are faced with this

question every day, to share their views. ■

Reverse forecast In the analysis of data to predict the future, does top-down produce a better result than bottom-up forecastng? Or are they equally useful methods when deployed in complementary approaches? LeighFisher experts comment

David Ashmore – New Delhi, India

It’s about getting the two forecasts to meet. Top-down thinking gives

you an answer which, regardless of allegations of lack of rigour, will

always pass the sense test. Sometimes with bottom-up you can end

up with a ridiculous answer because of the propagation of errors through the chain. If

the bottom-up doesn’t roughly come out around the same answer as the top-down,

you’re probably on the wrong track.

Linda Perry – San Francisco, USA

With enough time and budget, the use of both bottom-up and

top-down approaches is preferable. If the drivers of cost or demand

are not sufficiently understood, underlying changes that could

materially affect future activity may be missed. Preparation of detailed plans or

schedules has become increasingly essential for planning studies which use them

for simulation and other computer modeling. The expectation is not that predicted

detail will occur with 100% certainty, but that the detail is consistent with the overall

top-down results, facilitating planning of future facilities.

Paul McKnight – Ontario, Canada

Both approaches are valid ways of ‘triangulating’ to a forecast.

The top-down approach carries more weight when forecasting

bigger-picture entities (eg for a continent, region or country),

particularly when the forecast horizon is relatively long. It provides a broad and

general overall direction of the future. The bottom-up approach, on the other hand,

provides a better forecast when forecasting smaller subsets (eg traffic for a specific

facility or route), particularly when the forecast horizon is relatively short. It takes into

account the local variables that may cause the forecast of the smaller subset to vary

from the bigger-picture entity.

Charles Williams – London, UK

Using both approaches enables sense checks on results at regular

intervals. Top-down can lead to incrementalism, where the underlying

assumption is no change in the status quo apart from one or two

economic assumptions. If looking forward 20 years, test by looking back 20 years –

how much change has there been in this time? – providing a bottom-up sense check

on the robustness of top-down assumptions.

Surface Transport

winter 11/12_0908_ The Journal of LeighFisher

Surface transport ■

Europe’s road network is widespread and substantial. But there are still plenty of gaps left to fill. By Riccardo Mattei and Philip Bates

Arguably one of the most influential

reports on transport in the UK in

recent years was the Eddington

Transport Study. Published in

2006, one of its most important findings was

as follows:

Historically, new connections have played

a pivotal role in periods of rapid economic

growth in many economies, but in mature

economies with well-developed transport

networks, it is transport constraints that

are most likely to impact upon a nation’s

productivity and competitiveness.

In other words, don’t stop building new

connections but also focus on solving

problems in the existing system.

Although the report was about the UK,

many of the symptoms that led to this

diagnosis (large but ageing infrastructure

coupled with large but ageing population)

apply equally to other western European

countries. As a consequence, Europe is

now seeing a programme of transport

infrastructure renewal and upgrade, such

as the A Modell in Germany, the new Forth

Crossing in Scotland, or more commonly,

high-speed rail projects such as Madrid to

Barcelona in Spain, or the HS2 in the UK.

While this leaves one with an image

of western Europe being a region with a

complete highway network, this is far from

the truth. So where are Europe’s road gaps

and what is being done to fill them?

In France, sections are still being added

to the strategic motorway network. The

most high profile of these is arguably the

A355 Strasbourg Bypass, a 25km-long

two-by-two-lane greenfield motorway with

an estimated cost of around €400 million.

However, there are plenty of others, including

the A150 Rouen to Le Havre in northern

France, the A45 Lyon to Saint Etienne, the

A63 Salles to Saint Geours de Maremne and

bypasses in Marseille, Tarbes and Vichy.

In Spain, we’re seeing major new

greenfield roads opening even at the very

Broken journey

winter 11/12_011010_ The Journal of LeighFisher

n xxxxxxxxxxxxx■ Surface transport

Fleeting visionThe apparition of a high speed train enters a Kerala station – no ghost train this, but India’s vision for the High Speed Rail network that its fast-growing economy demands. By David Ashmore

continued overleaf ➔

height of the recession, such as the new

Malaga ring road and Guadalmedina toll

road north of Malaga. Meanwhile in Portugal,

another country buffeted by the recession,

major new highway schemes are being built

to link the country with Spain (Transmontana

and Marão Tunnel).

In the UK, it could be argued that

strategic highway network construction

ended 20 years ago with the M40, an

alternative route between London and

Birmingham via Oxford. However, small gaps

are actually still very common – ask anyone

who drives on the A303 past Stonehenge.

But large gaps also appear if one looks

closely, including a Lower Dartford Crossing

and access to mid Wales. While road

construction activity in recent years has been

low, the Second National Infrastructure Plan,

published in the autumn of 2011, suggests

we may be facing a new dawn of investment

in the UK road network.

It is arguably Italy where we see the most

activity, with the jewel in the crown being

the chain of new, largely greenfield toll roads

north of Milan and Venice. The four schemes

– Pedemontana Piemontese, Pedemontana

Lombarda, Pedemontana Veneta and

Pedemontana Friulana, which represent

around 260km of new highway – are all at

very different stages of development.

These schemes aim to relieve the highly

congested strategic network, including the

A4 – one of the most congested in Italy – to

which they run parallel. As well as serving

the many cities in northern Italy (Turin, Milan,

Bergamo, Verona, Venice and Trieste), the

Pedemontana schemes will also provide

a strategic east-west link across Italy

(European Corridor V), a local link between

small- to medium-sized cities north of the

A4 (such as Verese, Como and Trento) that

have undergone dramatic growth over the

last decade. Finally, the new Pedemontana

system will provide an alternative motorway

arc closer to the Alps, improving access to

recreational facilities, both in the mountains

and on the lakes that fringe them.

While the Pedemontana schemes

are impressive, these are not the only

greenfield motorways under consideration.

Other schemes under evaluation include

two around Milan, Bre.Be.Mi and TEEM

– Tangenziale Est Esterna di Milano. The

delivery of both projects is being accelerated

so they will be available in time for Expo

2015, which will be held north-west of Milan.

Another scheme is the 400km-long

Nuova Romea toll road between Orte and

Mestre. This motorway will cross five regions

– Lazio, Umbria, Toscana, Emilia Romagna

and Veneto – and provide a brand new

north-south link to relieve traffic on the highly

congested A1 + A13 Rome-to-Padua toll

road. Tenders are expected in late 2012.

In addition, the proposed Cispadana and

Ferrara-Porto Garibaldi toll roads will create a

new east-west link parallel to the A1 toll road

in Emilia-Romagna, while the Nogara-Mare

and Cremona-Mantova highways would

provide an east-west link parallel to the

A4 toll road in the Veneto region.

If most of these projects are ultimately

built on the currently proposed timescales,

the upcoming decade could arguably see

the biggest expansion of the road network

in Italy since the Second World War.

So, while it is true that the highway

network of Europe is widespread and

substantial, it would be wrong to think we

have everything in place – we still have

many gaps left to fill. ■

Relieving congestion –

major highway developments

are under way in France, Portugal,

Spain, and in particular, Italy

winter 11/12_013012_ The Journal of LeighFisher

■ Surface transport

SRI LANKAPopulation Data according to Census of India 2011

Proposed stations for High Speed Rail

Other cities

Miles100 200 300

Km100 200 300 400

Political shenanigans, indignant

lobby groups, howls of protest

from those who see their rural

idylls potentially being decimated,

arguments, counter arguments, endless

debates. Welcome to the world of large

scale transport infrastructure projects.

High Speed Rail (HSR – loosely defined

as a passenger rail system which operates

above 200 km/h) has never been more

topical, or contentious. Early successes

with the Shinkansen system in Japan,

followed by high profile European schemes

such as Eurostar and the TGV in France,

have made politicians sit up and take note

of this seemingly advantageous mode of

transport. This is unsurprising: HSR has

many characteristics which endear it to

politicians – it’s visible, grandiose and

futuristic – in other words highly sellable

from a political perspective. The snag is it is

extremely expensive and, like with all things,

if one politician goes out on a limb to support

it, his or her opponent will be equally dogged

in refuting it.

‘It’s wonderful’, cry the advocates. ‘It

rejuvenates local economies, redistributes

wealth and gets people out of cars and

planes. It’s good for the environment!’

‘Nonsense,’ the sceptics retort. ‘HSR

is expensive to build and run, and shifts

wealth from one epicentre to another. There

are simply better uses of our money. Like

upgrading what we have.’

Who is right? Well neither. And both.

As with all complex arguments relativity

is the key. It’s not about what you are

deploying as a solution, but how you are

deploying it, and where. But the electorate

understandably becomes bored with such

nuanced discussions, so the battle around

HSR in the developed world has largely fallen

back on to ideological and political fault lines,

not to mention survival battles from those

most strongly affected. And what a battle:

it’s brought governors head to head with

presidents, middle class residents of English

Shires side to side with environmental

HSR has many characteristics which endear it to politicians – it’s visible, grandiose and futuristic ...

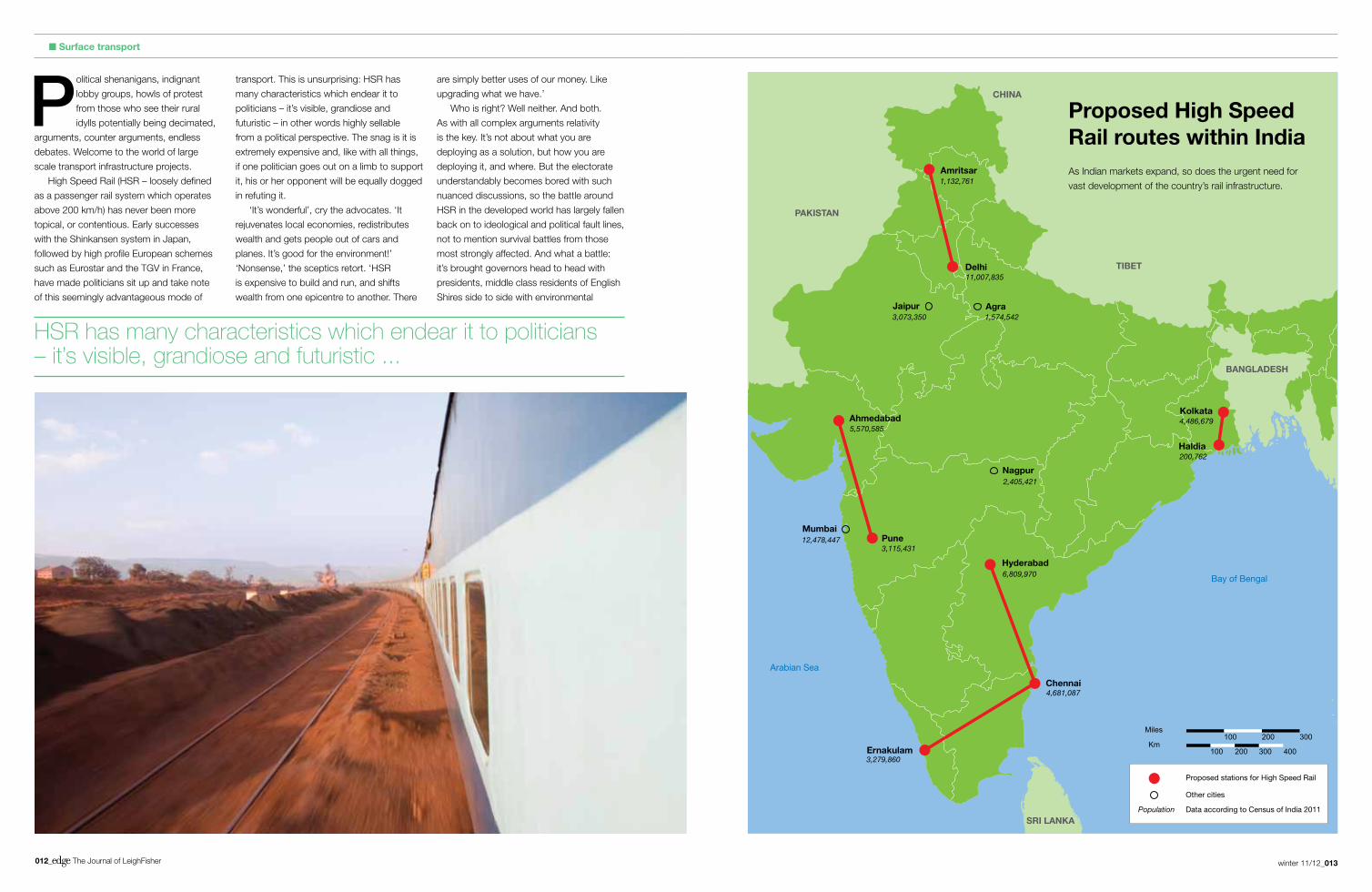

As Indian markets expand, so does the urgent need for

vast development of the country’s rail infrastructure.

Proposed High Speed Rail routes within India

winter 11/12_015014_ The Journal of LeighFisher

■ Surface transport Surface transport ■

activists, and had airlines and construction

companies fighting their corners with

politicians so as to influence what gets

built, if anything, and where – at least in the

developed world.

Build more and build it quicklyIn the developing world the attitude to

infrastructure is completely different. There

is no fast rail system to upgrade and if there

was one, upgrading it certainly would not

cope with the pace of growth being seen in

India and China, whose urban amenities and

economies have been catapulted into the

twenty first century in an unprecedented time

frame. No stagflation here – 8% growth per

annum is the current norm in India.

For decades such countries were

massively regulated by the government but

deregulation of key industries, combined

with innovations in technology, has allowed

highly skilled yet lower cost labour markets

to be utilised by western companies, leading

to boom times with which governments

simply cannot keep pace.

The attitude therefore is ‘build more and

build it quickly’, and given that governments

cannot move at the speed needed, the

void has been filled by the private sector,

which is being granted concessions to build

motorways, railways, airports and ports –

anything which will ensure the huge need

to travel and that freight movements can

be catered for.

The debates which characterize the

passage of HSR schemes in the developing

world are thus almost completely absent

here in India. HSR is seen as innovative,

modern, and a sign that India is moving

forward – everything that India’s colossal

existing rail system isn’t. Indian Railways may

existing Indian Railways’ track serves the city

centre markets, HSR stations will often be

located remotely from city centres, negating

any advantages over airline travel, especially

given India’s notorious traffic congestion.

The question of fare is also critical – to

pay back the capital costs of the systems,

fares may need to be set at market prices,

which again will offer little advantage

over airlines; setting fares at lower levels

will necessitate a subsidy, which may be

justifiable, but will need to be built into the

concession documents, depending upon

who bears revenue risk; and it’s unclear if

usage will cover operating costs.

Finally the spectre of Indian railways

looms in the background – their

role is as yet murky: if they are not

responsible for the operations, then

they could be custodians of the track, yet

separating the wheel and the rail may bring

problems at key operational interfaces.

But one of the incredible things about

India at the moment is the voracious desire

for infrastructure, combined with a ‘can do’

outlook. The Indian government is unlikely

to pontificate endlessly over cost benefit

considerations. It’s likely these schemes will

be built and people will have to wait and see

what happens.

Anathema to the western mind. But, after

all, this isn’t the west. ■

be the largest employer in the world, serving

all corners of the subcontinent, so, incredible

in their own way, but with poor reliability and

ailing infrastructure, modern they aren’t. If

you are travelling into an urban area for an

important meeting, there’s every chance you

will be several hours late. This is no longer

tolerated in the new economy.

The gap was first filled by low cost airlines

such as Kingfisher and Jet, whose services

are comprehensive, affordable and, more

importantly, punctual. Domestic air travel

in India, always sizeable, is now huge, with

many middle class families jumping on and

off budget airlines as a matter of course.

Queuing up for contractsSo this market is seemingly ripe for HSR. In

Europe it’s been shown that if stations are

located in the central business district, and

airports remote from city centres, provided

fares are competitive, for journeys under five

hours HSR can make significant inroads into

air travel’s market share. Getting to airports

can be painful and expensive and check-in

times can be long relative to flight times.

So the Government of India last year

announced an HSR programme. As

there are no indigenous manufacturers of

complete systems, much of the technology

will need to be imported and much of the

financing will come through international

development banks. So it’s been decided

that for all the benefits of technological

uniformity, it would be in India’s interest

to spread the trade opportunity around.

Understandably, the Japanese, the French,

the Germans – all the countries with ‘off the

peg solutions’ and development banking

institutions – are queuing up.

This is reflected in the award of contracts

following feasibility studies. Aside from

Hyderabad to Chennai, Chennai to Ernakulum,

and Delhi to Amritsar, all the projects are

progressing with different foreign sponsors.

Pune to Ahmedabad is being developed by

the French, Delhi to Patna by the British, and

Haldia to Kolkata by the Spanish.

Questions yet to be answeredIs the future bright for HSR in India? It

depends. The location of stations is key. As

HSR in India: on track

• Indian government is not

predicted to deliberate

over cost benefits

• Upgrading is not an

option, with no fast rail

system in place

• India has a positive,

‘can do’ attitude –

plus 8% growth per year

In the US, slow growth, high

unemployment and low interest rates

used to mean ideal conditions to invest

in infrastructure, with cheap labour,

materials and debt, and the economy

needing an injection of stimulus to kick-start

demand and growth. But the recession –

coupled with changes in driving habits and

airline travel – has reduced government

income and thus the resources available

for infrastructure investment. With new fuel

and excise taxes unlikely, now could be the

time for federal and state governments to

embrace public-private partnerships (PPPs).

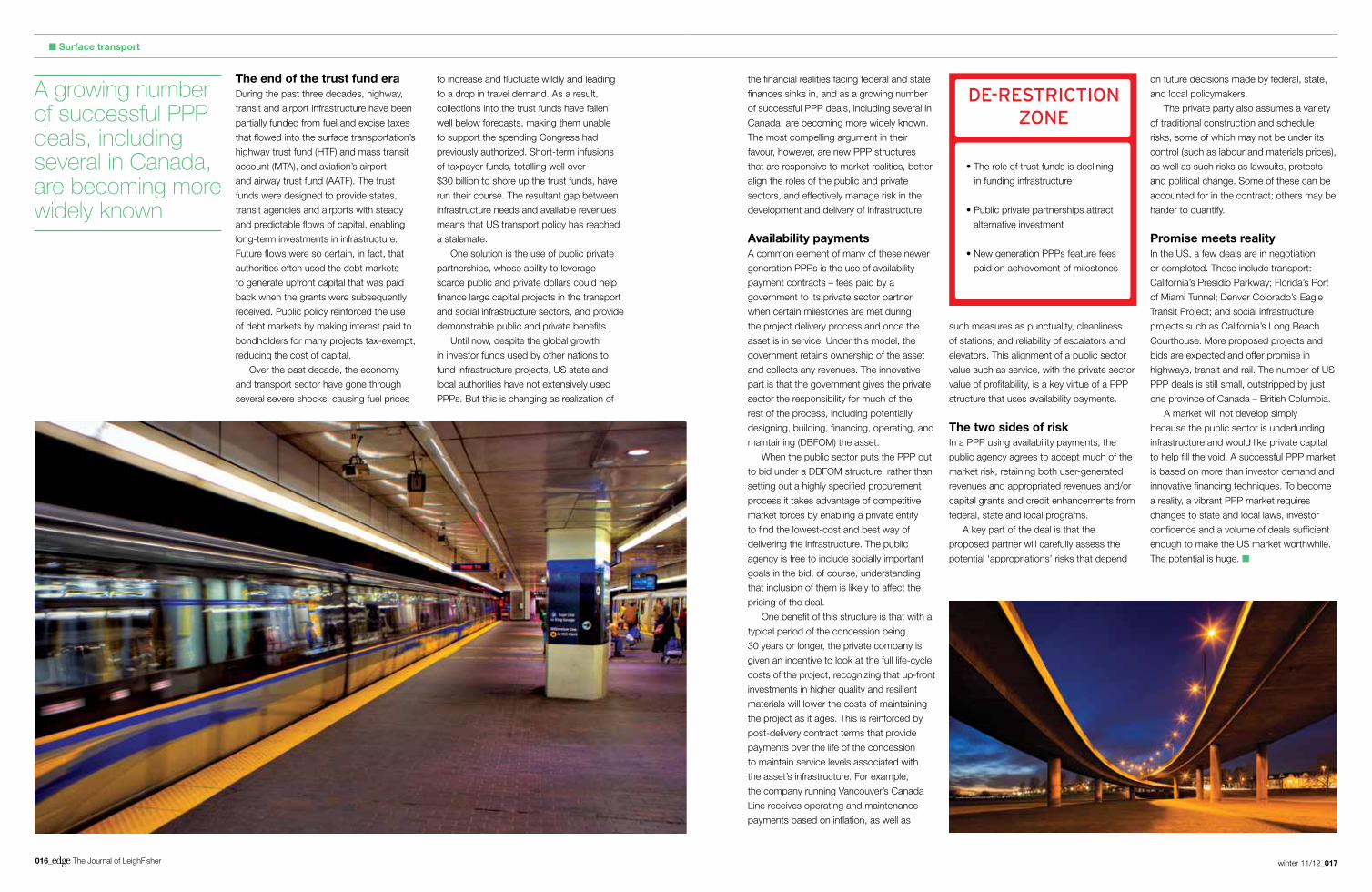

Public works, private funding?

With trust fund dollars declining for air and rail projects, public private partnerships offer a proven alternative. By Stephen Van Beek

One of the incredible things about India ... is the voracious desire for infrastructure

winter 11/12_017016_ The Journal of LeighFisher

■ Surface transport

The end of the trust fund eraDuring the past three decades, highway,

transit and airport infrastructure have been

partially funded from fuel and excise taxes

that flowed into the surface transportation’s

highway trust fund (HTF) and mass transit

account (MTA), and aviation’s airport

and airway trust fund (AATF). The trust

funds were designed to provide states,

transit agencies and airports with steady

and predictable flows of capital, enabling

long-term investments in infrastructure.

Future flows were so certain, in fact, that

authorities often used the debt markets

to generate upfront capital that was paid

back when the grants were subsequently

received. Public policy reinforced the use

of debt markets by making interest paid to

bondholders for many projects tax-exempt,

reducing the cost of capital.

Over the past decade, the economy

and transport sector have gone through

several severe shocks, causing fuel prices

the financial realities facing federal and state

finances sinks in, and as a growing number

of successful PPP deals, including several in

Canada, are becoming more widely known.

The most compelling argument in their

favour, however, are new PPP structures

that are responsive to market realities, better

align the roles of the public and private

sectors, and effectively manage risk in the

development and delivery of infrastructure.

Availability paymentsA common element of many of these newer

generation PPPs is the use of availability

payment contracts – fees paid by a

government to its private sector partner

when certain milestones are met during

the project delivery process and once the

asset is in service. Under this model, the

government retains ownership of the asset

and collects any revenues. The innovative

part is that the government gives the private

sector the responsibility for much of the

rest of the process, including potentially

designing, building, financing, operating, and

maintaining (DBFOM) the asset.

When the public sector puts the PPP out

to bid under a DBFOM structure, rather than

setting out a highly specified procurement

process it takes advantage of competitive

market forces by enabling a private entity

to find the lowest-cost and best way of

delivering the infrastructure. The public

agency is free to include socially important

goals in the bid, of course, understanding

that inclusion of them is likely to affect the

pricing of the deal.

One benefit of this structure is that with a

typical period of the concession being

30 years or longer, the private company is

given an incentive to look at the full life-cycle

costs of the project, recognizing that up-front

investments in higher quality and resilient

materials will lower the costs of maintaining

the project as it ages. This is reinforced by

post-delivery contract terms that provide

payments over the life of the concession

to maintain service levels associated with

the asset’s infrastructure. For example,

the company running Vancouver’s Canada

Line receives operating and maintenance

payments based on inflation, as well as

such measures as punctuality, cleanliness

of stations, and reliability of escalators and

elevators. This alignment of a public sector

value such as service, with the private sector

value of profitability, is a key virtue of a PPP

structure that uses availability payments.

The two sides of riskIn a PPP using availability payments, the

public agency agrees to accept much of the

market risk, retaining both user-generated

revenues and appropriated revenues and/or

capital grants and credit enhancements from

federal, state and local programs.

A key part of the deal is that the

proposed partner will carefully assess the

potential ‘appropriations’ risks that depend

on future decisions made by federal, state,

and local policymakers.

The private party also assumes a variety

of traditional construction and schedule

risks, some of which may not be under its

control (such as labour and materials prices),

as well as such risks as lawsuits, protests

and political change. Some of these can be

accounted for in the contract; others may be

harder to quantify.

Promise meets realityIn the US, a few deals are in negotiation

or completed. These include transport:

California’s Presidio Parkway; Florida’s Port

of Miami Tunnel; Denver Colorado’s Eagle

Transit Project; and social infrastructure

projects such as California’s Long Beach

Courthouse. More proposed projects and

bids are expected and offer promise in

highways, transit and rail. The number of US

PPP deals is still small, outstripped by just

one province of Canada – British Columbia.

A market will not develop simply

because the public sector is underfunding

infrastructure and would like private capital

to help fill the void. A successful PPP market

is based on more than investor demand and

innovative financing techniques. To become

a reality, a vibrant PPP market requires

changes to state and local laws, investor

confidence and a volume of deals sufficient

enough to make the US market worthwhile.

The potential is huge. ■

A growing number of successful PPP deals, including several in Canada, are becoming more widely known

to increase and fluctuate wildly and leading

to a drop in travel demand. As a result,

collections into the trust funds have fallen

well below forecasts, making them unable

to support the spending Congress had

previously authorized. Short-term infusions

of taxpayer funds, totalling well over

$30 billion to shore up the trust funds, have

run their course. The resultant gap between

infrastructure needs and available revenues

means that US transport policy has reached

a stalemate.

One solution is the use of public private

partnerships, whose ability to leverage

scarce public and private dollars could help

finance large capital projects in the transport

and social infrastructure sectors, and provide

demonstrable public and private benefits.

Until now, despite the global growth

in investor funds used by other nations to

fund infrastructure projects, US state and

local authorities have not extensively used

PPPs. But this is changing as realization of

• The role of trust funds is declining

in funding infrastructure

• Public private partnerships attract

alternative investment

• New generation PPPs feature fees

paid on achievement of milestones

winter 11/12_019018_ The Journal of LeighFisher

■ Aviation

Look eastWith the economic outlook – and aviation market – looking bleak for Western economies, the world should turn to the growing Asian market for answers. By Satyaki Raghunath

continued overleaf ➔

winter 11/12_021020_ The Journal of LeighFisher

■ Aviation

As major western economies

struggle, aviation is one of the

sectors most badly affected.

Major airlines are struggling

mightily, the market is consistently weak,

major network and legacy carriers are

disappearing or merging and there seems

to be little on the horizon to offer hope. As

a result, governments across the world are

seeking to involve private investors in the

development of airport infrastructure.

There are, however, pockets of optimism,

with some of the emerging markets across

Asia and Latin America bucking the trend.

China, India, Brazil and the Middle East are

all showing signs of growth and resilience

and it is in these markets that significant

capacity and growth are going to be seen.

In recent months, aviation news has

been all about Asia. Beijing is now the

second busiest airport in the world with

over 70 million passengers in 2010;

new terminals are in different stages of

planning and development at Incheon

and Hong Kong; airports in the Middle

East are being developed through public

private partnerships; and finally, in India

the long-awaited regulatory ruling on

aeronautical charges has been announced,

while IndiGo placed the largest aircraft order

in the history of commercial aviation.

Beijing’s growth as a major international

airport was never doubted – the only surprise

has been how quickly it reached the 70

million mark. As the Chinese economy

has grown rapidly, so has international

and domestic air traffic, increasing,

respectively, by over 30% and over 15%

on last year. This has been accompanied

by an unprecedented investment in the

development of new aviation infrastructure.

Beijing is well on its way to becoming the

busiest airport in the world over the next few

years, especially as growth at American and

European airports remains stagnant, thanks

to lowered demand or constrained capacity.

The Chinese government has already

announced plans for the development of a

third airport for the Beijing metropolitan area

to cater for long-term demand.

Elsewhere in Asia, Hong Kong and

Incheon international airports are developing

new terminals. The former is breaking ground

on a new midfield terminal concourse that

will add 20-odd gates, while the latter is in

the early stages of concept design for a new

terminal that will add approximately 30 million

people in annual capacity. If the existing

facilities are anything to go by, we can expect

to see new benchmarks set for the quality of

infrastructure and level of service at both of

these airports.

In the Middle East, airports are showing

signs of going down the public private

partnership route, a trend reflected in the

ongoing Madinah Airport build-operate-

transfer contract. Calling for investment in the

long-term development of the airport, the bid

process has been robust and well received

so far. It remains to be seen whether other

airports in the region will follow this route.

The Brazilian government plans to

privatize three major airports: São Paulo

Guarulhos, Brasilia and Campinas Viracopos.

Given impressive growth rates and upcoming

events such as the FIFA World Cup and

2016 Olympics, this is welcome news. There

have also been interesting developments in

India. Firstly, IndiGo – one of India’s fastest-

growing low-fare airlines – placed an order

for 180 Airbus A320-family aircraft valued

at approximately $16 billion in early 2011.

Along with another order of 30 turboprop

aircraft placed by Spicejet – another low-fare

carrier – it was a staggering affirmation

of faith in the long-term growth of Indian

aviation, especially in the low-fare segment,

which is where most of the recent growth

has been. Conversely, and surprisingly,

Kingfisher announced its exit from the

low-fare segment, thereby also bringing the

Air Deccan story to a sad end.

Secondly, the Airport Economic

Regulatory Authority (AERA), put forth its

final regulatory determination for airports

across India in 2011. The general ruling

was, as expected, to move towards a

single-till approach to aeronautical charges

with a view to maximizing welfare and

keeping tariffs for the general public as low

as possible. In addition, the Directorate

General of Civil Aviation (DGCA) has begun

to step in to regulate airfares in India, based

on complaints that some airlines were

overcharging passengers, including charging

them for seat selection. This decision seems

surprising and even counter-productive – in a

competitive market that is very fare-sensitive,

there is little need for a regulator to step in to

control fares.

Such measures might keep consumer

groups and the traveling public happy,

but it does not encourage private sector

participation in delivering urgently needed

aviation infrastructure. This will be crucial

in light of projected double-digit GDP

growth over the next decade. Without

reasonable rewards to private companies,

India runs a risk of developing sub-standard

infrastructure, a major stumbling block for a

nation that is likely to have the third largest

GDP in the world by 2030.

Despite structural and regulatory

challenges, China, India, the Middle East

and Brazil are likely to thrive, presenting

airport operators with huge opportunities for

innovation and improved performance.

Airport operators across the world

face similar challenges – access to capital,

regulatory uncertainty, investment in facilities

and implementation of capital programs,

pricing pressures.

In these uncertain times, airports around

the world could learn from these problems

and their solutions. ■

Aviation in the developing world

• Beijing – world’s second largest airport since 2010

• Incheon & Hong Kong – major expansion of airports

• Madinah – build-operate-transfer contract

• In Brazil, three major aiports are being privatized

IndiGo – one of India’s fastest-growing low-fare airlines – placed an order for 180 Airbus A320 family aircraft valued at approximately $16 billion in early 2011

Aviation

winter 11/12_023022_ The Journal of LeighFisher

Aviation ■

Aviation in the developed world, particularly in the US, is driven by cost and revenue initiatives rather than exponential traffic growth. By Linda Perry

A viation in the developed

world is characterized by

mature domestic and

international airline networks,

a population with above average incomes

and a high propensity to travel, and airport

facilities at or approaching capacity. As a

result, traffic growth is limited and airlines

and airport operators must identify

opportunities to improve financial and

operating performance.

Shifts in global aviationThe rapid growth of developing economies

such as Brazil, China, and India has resulted

in a shift in global aviation from Europe

and North America to the Asia-Pacific

region. Although advanced economies

accounted for the largest share of world

capacity (in terms of scheduled departing

seats) in 2011, total capacity has remained

relatively unchanged since 2000. The lack

of capacity growth in advanced economies

reflects, in part, airline efforts to reduce

costs by flying fewer aircraft and increasing

average load factors (the percent of seats

occupied) and to increase revenue by limiting

capacity, thereby improving their ability to

charge higher air fares. Airlines in advanced

economies have increasingly relied on the

development of international service to fuel

traffic and revenue growth. The liberalization

of international aviation-related treaties,

including the creation of more than 100

US Open Skies agreements, is expected

to facilitate future growth in international

service, although this growth will be

shared by airlines in developing economies

with the financial resources to build their

fleets. In 2010, airlines in the Asia-Pacific

region accounted for approximately 33%

of world orders for new aircraft through

2029, according to the global market

forecasts prepared by Airbus and the

Boeing Corporation. By 2029, airlines in the

Asia-Pacific region are expected to account

for 34% of the world aircraft fleet, compared

with a 22% share in 2010.

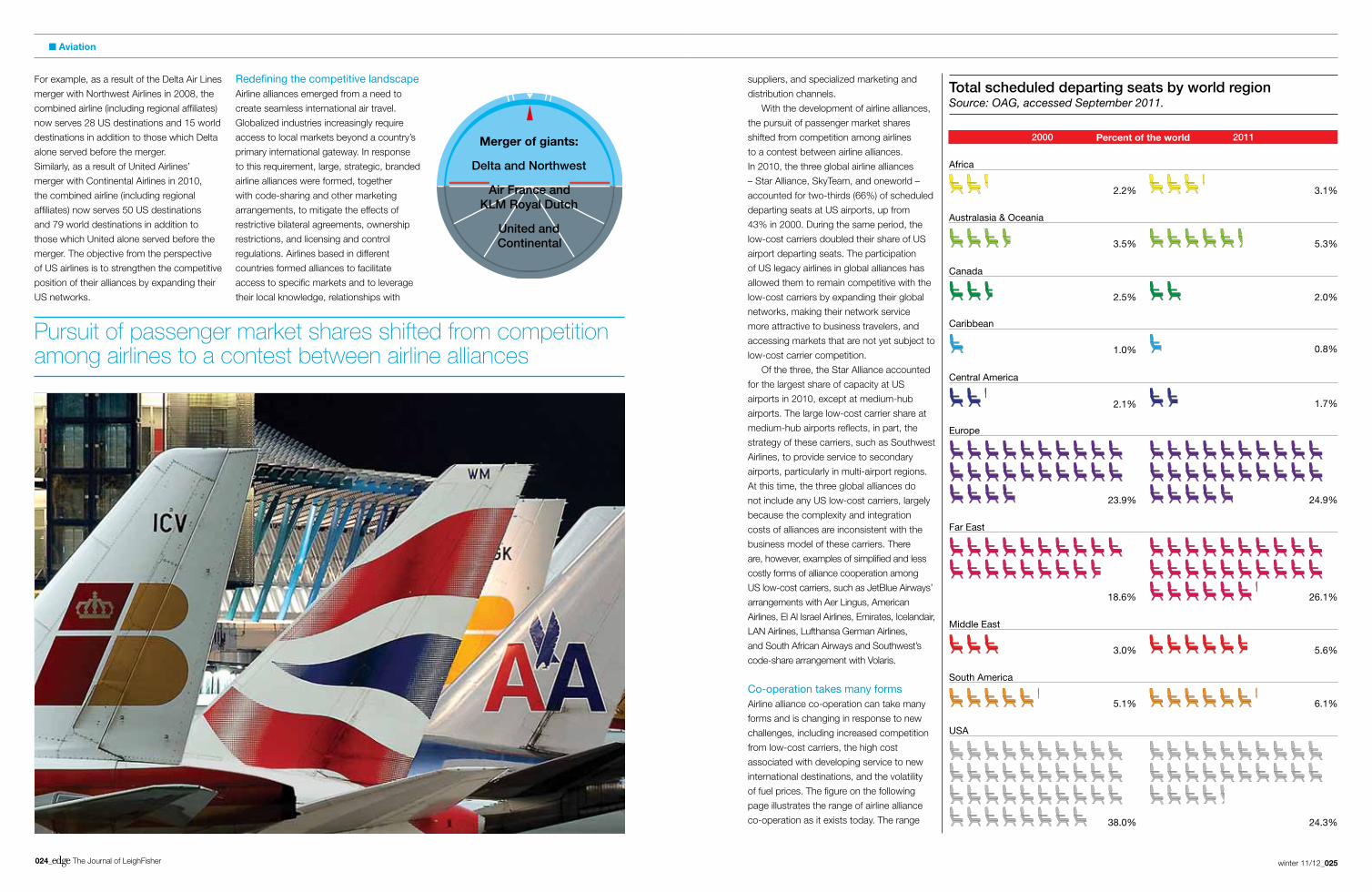

Role of airline mergersSince the merger of Air France and KLM

Royal Dutch Airlines in 2004, most of the

recent mergers have been between US

airlines. In contrast to the Air France/KLM

merger, in which each airline continues to

operate separately, mergers of US airlines

have resulted in single-branded entities with

consolidated operations and facilities. The

result is a combined airline that serves a

greater number of destinations within the

United States and throughout the world than

the individual airlines before the merger.

Changing skies

winter 11/12_025024_ The Journal of LeighFisher

■ Aviation

For example, as a result of the Delta Air Lines

merger with Northwest Airlines in 2008, the

combined airline (including regional affiliates)

now serves 28 US destinations and 15 world

destinations in addition to those which Delta

alone served before the merger.

Similarly, as a result of United Airlines’

merger with Continental Airlines in 2010,

the combined airline (including regional

affiliates) now serves 50 US destinations

and 79 world destinations in addition to

those which United alone served before the

merger. The objective from the perspective

of US airlines is to strengthen the competitive

position of their alliances by expanding their

US networks.

Redefining the competitive landscapeAirline alliances emerged from a need to

create seamless international air travel.

Globalized industries increasingly require

access to local markets beyond a country’s

primary international gateway. In response

to this requirement, large, strategic, branded

airline alliances were formed, together

with code-sharing and other marketing

arrangements, to mitigate the effects of

restrictive bilateral agreements, ownership

restrictions, and licensing and control

regulations. Airlines based in different

countries formed alliances to facilitate

access to specific markets and to leverage

their local knowledge, relationships with

suppliers, and specialized marketing and

distribution channels.

With the development of airline alliances,

the pursuit of passenger market shares

shifted from competition among airlines

to a contest between airline alliances.

In 2010, the three global airline alliances

– Star Alliance, SkyTeam, and oneworld –

accounted for two-thirds (66%) of scheduled

departing seats at US airports, up from

43% in 2000. During the same period, the

low-cost carriers doubled their share of US

airport departing seats. The participation

of US legacy airlines in global alliances has

allowed them to remain competitive with the

low-cost carriers by expanding their global

networks, making their network service

more attractive to business travelers, and

accessing markets that are not yet subject to

low-cost carrier competition.

Of the three, the Star Alliance accounted

for the largest share of capacity at US

airports in 2010, except at medium-hub

airports. The large low-cost carrier share at

medium-hub airports reflects, in part, the

strategy of these carriers, such as Southwest

Airlines, to provide service to secondary

airports, particularly in multi-airport regions.

At this time, the three global alliances do

not include any US low-cost carriers, largely

because the complexity and integration

costs of alliances are inconsistent with the

business model of these carriers. There

are, however, examples of simplified and less

costly forms of alliance cooperation among

US low-cost carriers, such as JetBlue Airways’

arrangements with Aer Lingus, American

Airlines, El Al Israel Airlines, Emirates, Icelandair,

LAN Airlines, Lufthansa German Airlines,

and South African Airways and Southwest’s

code-share arrangement with Volaris.

Co-operation takes many formsAirline alliance co-operation can take many

forms and is changing in response to new

challenges, including increased competition

from low-cost carriers, the high cost

associated with developing service to new

international destinations, and the volatility

of fuel prices. The figure on the following

page illustrates the range of airline alliance

co-operation as it exists today. The range

Total scheduled departing seats by world region Source: OAG, accessed September 2011.

Percent of the world2000 2011

USA

Pursuit of passenger market shares shifted from competition among airlines to a contest between airline alliances

Africa

2.2%

3.5%

2.5%

1.0% 0.8%

2.1% 1.7%

23.9% 24.9%

18.6% 26.1%

3.0% 5.6%

3.1%

5.3%

2.0%

Australasia & Oceania

Canada

Caribbean

Central America

Europe

Far East

Middle East

South America

Merger of giants:

Delta and Northwest

Air France and KLM Royal Dutch

United and Continental

5.1% 6.1%

38.0% 24.3%

winter 11/12_027

n xxxxxxxxxxxxx

026_ The Journal of LeighFisher

■ Aviation

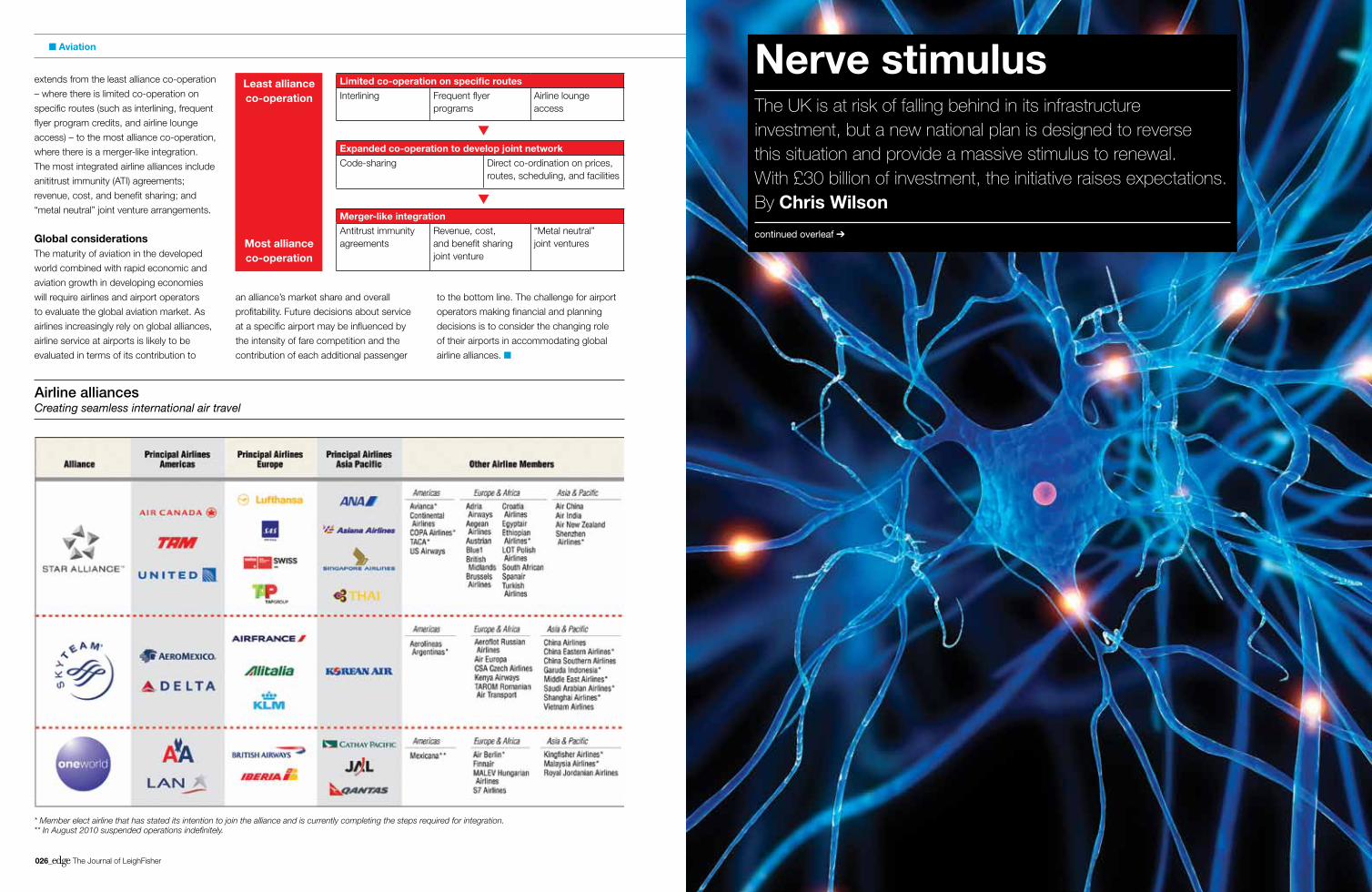

Least alliance co-operation

Limited co-operation on specific routes

Interlining Frequent flyer programs

Airline lounge access

extends from the least alliance co-operation

– where there is limited co-operation on

specific routes (such as interlining, frequent

flyer program credits, and airline lounge

access) – to the most alliance co-operation,

where there is a merger-like integration.

The most integrated airline alliances include

anititrust immunity (ATI) agreements;

revenue, cost, and benefit sharing; and

“metal neutral” joint venture arrangements.

Global considerationsThe maturity of aviation in the developed

world combined with rapid economic and

aviation growth in developing economies

will require airlines and airport operators

to evaluate the global aviation market. As

airlines increasingly rely on global alliances,

airline service at airports is likely to be

evaluated in terms of its contribution to

Most alliance co-operation

* Member elect airline that has stated its intention to join the alliance and is currently completing the steps required for integration. ** In August 2010 suspended operations indefinitely.

Airline alliances Creating seamless international air travel

Nerve stimulusThe UK is at risk of falling behind in its infrastructure investment, but a new national plan is designed to reverse this situation and provide a massive stimulus to renewal. With £30 billion of investment, the initiative raises expectations. By Chris Wilson

continued overleaf ➔

Merger-like integration

Antitrust immunity agreements

Revenue, cost, and benefit sharing joint venture

“Metal neutral” joint ventures

Expanded co-operation to develop joint network

Code-sharing Direct co-ordination on prices, routes, scheduling, and facilities

an alliance’s market share and overall

profitability. Future decisions about service

at a specific airport may be influenced by

the intensity of fare competition and the

contribution of each additional passenger

to the bottom line. The challenge for airport

operators making financial and planning

decisions is to consider the changing role

of their airports in accommodating global

airline alliances. ■

winter 11/12_029028_ The Journal of LeighFisher

■ Government and infrastructure

The coalition government published

the UK’s second National

Infrastructure Plan in November

2011 and many professional

bodies, including the Institution of Civil

Engineers, believe it is an opportunity not to

be missed. The plan is intended to stimulate

£200 billion worth of investment over the

next five years. This could prove vitally

important to the task of renewing the UK’s

economic infrastructure. High expectations,

however, are balanced by concerns that the

plan’s specific commitments need to be both

credible and fundable.

What needs to be doneInfrastructure is a rapidly changing game

within a highly competitive global market.

Funders, sponsors, contractors and

consultants inevitably seek out the best

opportunities in global infrastructure markets

and countries such as Brazil, Australia,

India, China and Canada are leading the

way in innovation and opportunities. The

UK must reassert its leadership position on

innovation and deal-flow. The government

has estimated national demand for economic

infrastructure investment at £40-50 billion

every year to 2030 and to meet this, the UK

needs to be seen as a leader in the global

market. Funders and sponsors have to be

attracted to provide a stream of projects

and assets, funding opportunities, workforce

and skills capacity, intellectual capital,

research and development, cost-effective

procurement procedures and opportunities

for innovation.

Present and previous governments have

stated their commitment to infrastructure

but the UK lags well behind its major

competitors in the World Economic Forum’s

most recent Infrastructure Index. Similarly,

while the first National Infrastructure Plan in

2010 was met with real excitement, many

believed it was long overdue. There has also

been disappointment about the pace and

leadership needed to tackle deep-seated

issues of policy and capacity as well as

attitudes and behaviours.

We need to deliver on the promise of

a more consistent, joined-up approach to

infrastructure planning for long-term gains.

Infrastructure development needs to become

apolitical. Stop/start planning policy creates

uncertainty for funders, sponsors and

contractors. The planning approvals process

is a major obstacle to progress and is at the

heart of an overly complex and centralized

bureaucracy that needs simplifying and

rationalizing. Legislation on planning must

be fast-tracked and clear decisions rapidly

reached on major projects like HS2 and a

new London airport to drive and support

economic growth. The focus must also be

national, not just in the south-east, in order

to give real stimulus to regional industries.

Some delay has been inevitable with

the government in review and policy

development mode, but there have been

valuable outputs from the review of private

finance initiative (PFI) contracts (although

the current PFI review has less support),

the Penfold Review of non-planning

consents and also policy developments

around the new Planning Framework. It is

time to signal leadership and delivery across

the whole infrastructure landscape. There

is progress with transformational projects

such as super-fast broadband, Crossrail and

(prospectively) HS2. But many believe that,

with growth of around 0.2% and a prevailing

sovereign debt crisis, there is urgent need for

action to stimulate infrastructure expansion

as a pull-through for economic growth.

Pulling the strands togetherRecently, the government set out strands of

its high-level infrastructure policy: a focus on

smart management, particularly in energy

and transport (eg managed motorways);

the targeting of network pinch-points

and stress points for investment in flood

defence, railways and road transport; the

development of large-scale projects; and

the low-carbon agenda.

There is increasing recognition that

infrastructure networks, up to now

managed separately, are more and more

interdependent. Recognition of this can

form the start of a major integrated

program to provide huge growth and

efficiency opportunities across both public

and private sectors.

The proposed National Policy Statements

on areas such as ports, waste, and aviation

are a step forward. Equally the publication of

lists of public and private sector projects will

certainly increase transparency on deal-flow.

The Green Bank is another major step

forward, even if its funding is inadequate to

the task. While a more proactive approach

to funding is clearly needed, it may be that

the government will not support the idea of a

National Infrastructure Bank.

Against this background, a significant

development was the government’s

acknowledgement that PFI has a better track

record on time and budget than other public

sector infrastructure procurement methods,

and also, that it successfully transfers

appropriate risks to the private sector.

On the back of the Romford pilot to test

the deliverability of savings on PFI projects,

the government’s target of £1.5 billion

looks realistic.

Aviation policy is one of the biggest

challenges. Whilst the South East Airports

Taskforce is seeking short term alleviation

and improvement measures to sweat the

current asset base, the policy delays risk

causing a further slowing of economic

growth and a loss of traffic to other major

European airport hubs.

The priority is economicThe previous government preferred

investment in social infrastructure such as

schools and hospitals, but the shift now is

to economic infrastructure (energy, road and

rail transport). Investors now need to see

a credible flow of new projects and assets

coming to market, rather than a focus on

secondary assets via sales and

The government has estimated national demand for economic infrastructure investment at £40-50bn to 2030

The previous government preferred investment in schools and hospitals but the shift is now to energy, road and rail

the consolidation and rationalisation of

existing portfolios.

Recognising the interdependence of

infrastructure sectors, we believe that

government needs to establish a centre

of excellence for program management

and cross-departmental implementation.

This would cut through red tape and

tackle the issues of project implementation

across government and the private sector.

In summary, the second National

Infrastructure Plan marks a significant

further step forward in showing: firstly,

that the government will take the lead;

secondly, that private sector investors

will be attracted back to the UK market;

thirdly, that there will be a real focus

for infrastructure and capacity growth

alongside the flagship projects; and

fourthly, that the planning system will

be reformed.

If the plan delivers on these, it will go a

long way to providing the step-change that

the UK needs to boost its infrastructure and

economic growth. ■

UK National Infrastructure Plan 2011

• £20 billion investment from pension funds

• Local government able to borrow to support major projects and raise funds eg from toll roads

• £1 billion investment to tackle road congestion

• £1.4 billion investment in railway infrastructure

• £100 million investment in superfast broadband

• Cabinet committee to push 40 priority projects

Government and Infrastructure

winter 11/12_031030_ The Journal of LeighFisher

Government and infrastructure ■

Over the past two years, there has

been a surprisingly high level of

global investment in schools,

hospitals, social housing and

other social infrastructure, with about 400

greenfield public private partnership (PPP)

projects started around the world, of which

135 had reached financial close, as Edge

went to press. This includes 25 schools, six

hospitals and two social housing projects

in the UK alone. In Canada, there is the

US$1001 million Humber River Regional

Hospital in North West Ontario; and in

Germany, the Braunschweig Schools PPP

in Lower Saxony cost €280 million. And it is

not just PPP; conventionally funded projects

have also got off the ground, notably

South Glasgow Hospitals in the UK, with

investment of £842 million.

But funding social infrastructure has not

been achieved without difficulty, particularly

in the European market. Many governments

have been forced to cut public spending

and refocus investment programs. In 2010

the UK coalition government canceled 12

major projects and suspended 12 others

in various sectors. The North Tees and

Hartlepool hospital project, with a lifetime

cost of £450 million, and the Leeds Holt

Park wellbeing centre, with a lifetime cost

of £50 million, were among those canceled.

The government also cut back the Building

Schools for the Future (BSF) program,

canceling 719 school projects that were

under procurement and reviewing 14 other

projects to find savings. A further 123

academy schemes, another policy of the

previous government, were also reviewed.

The story is similar elsewhere.

Funding is difficult. Budgetary cutbacks

have left many public sector bodies tight

for cash and this has been exacerbated

by a fall in capital receipts and developer

contributions from a sluggish property

market. Finance is also difficult. Bank debt

is hard to obtain. Terms are shorter than

they previously were and margins are higher,

reflecting a more cautious appetite for risk.

Equity is looking for safer investments in

the secondary market. Bonds offer most

promise, but wrapped products are difficult

to obtain since the downgrading of many of

France is investing 3.4 billion, Germany 200 million, and Italy, Ireland, Spain

and Portugal some 5.5 billion

the monolines (insurers of credit risk). The

sovereign debt crisis and difficulties with the

euro have made Europe less attractive than

emerging economies such as Brazil or India.

Why then is there an apparent high level

of project activity? Social infrastructure

projects are ideal for infrastructure investment

plans, as they usually take less time to plan

and deliver than transport infrastructure. The

benefits are therefore realized sooner; a point

not lost on politicians looking for quick wins

to kick-start growth. From an investor’s point

of view, a well-defined program of potential

investment is always attractive.

As regards investment in Europe, the main

attractions are familiarity with the regulatory

regime and the local market, a local presence

and local partners (although some might say

that the nature of the asset is more important

than its location).

Some of the current activity is down to

legacy projects from previous programmes

that have survived the cuts – the majority

of the PPP schools projects in the UK

completed since 2010 were BSF projects –

but much of it is new. In the UK, Scotland

has its £1.25 billion Schools for the Future

program, its hub program, which is valued at

more than £1 billion over the next 10 years,

and the previously mentioned Southern

General Hospital. The UK government has

announced a budget of between £1 billion

and £3 billion for its new Priority School

Building Programme and is seeking a

private sector partner, as well as continuing

investment through other initiatives.

Elsewhere in Europe, France is investing

some €3.4 billion, Germany €200 million,

and Italy, Ireland, Spain and Portugal, some

€5.5 billion collectively in social infrastructure

through PPP alone.

Innovative approaches are being

developed to address the problems in

obtaining finance. A number of project bonds

using sub-debt loans or guarantees are

being prepared, such as the European 2020

project bond. If it receives final approval it

will see the European Investment Bank (EIB)

providing sub-debt loans or guarantees

worth up to 20% of a project bond’s total

debt, which the EIB hopes will enhance the

credit of senior tranches of issued bonds to

at least A-rating. Current thinking on senior

debt is that shorter terms of typically six

Weather eyeThis is a turbulent economic climate, particularly in Europe. So how has investment in social infrastructure: schools, hospitals and social housing, survived relatively unscathed? Along with a well-defined program of potential investment, a synopsis of the market points to flexibility and innovation of funding and finance. By Andrew Clearie

winter 11/12_033032_ The Journal of LeighFisher

n xxxxxxxxxxxxx■ Government and infrastructure

to seven years could be addressed by a

regulated refinancing within the contract.

The public sector is adopting a mixed

economy for funding, using capital where

available or private finance where it isn’t. It

makes use of grants or funding sources such

as JESSICA, and looks at partnering with

other authorities, with private sector partners

or the third sector.

JESSICA allows EU member states to

use the European Regional Development

Fund for loans and equity investment and

guarantees, alongside complementary

resources from the EIB and other funders,

support for projects forming part of an

integrated plan for sustainable urban

development. The investments generate a

financial return, which is recycled to keep the

fund going. Funds are delivered to projects

via urban development funds (UDFs), which

can be established at national, regional or

local level. They can be a separate legal

entity or a separate block of finance within

an existing financial institution. So far, the EIB

has undertaken the procurement of UK UDF

investment partners, typically a consortium of

companies, investors and the public sector.

Scotland’s hub program features

partnering, setting up five joint venture

companies to deliver primary and social care

premises and schools (three are already

established). It aims to improve effectiveness

of the existing community planning process

through streamlined facilities procurement,

based around collaboration between

different public bodies. The initiative aims

to reduce procurement and design costs,

streamline construction, operation and

maintenance of the facilities and realize

savings through joint working. The Scottish

government addresses its non-profit

distributing policy through the structure and

funding of the joint venture company (hubco)

rather than directly through the project

contracts. Projects are funded either through

capital or revenue (private finance).

Despite difficult times, a well defined

program of potential investment is

always attractive. Flexibility and innovation

in the approach to funding and finance

are key to continued investment in

social infrastructure. ■

The public sector is adopting a mixed economy for funding, using capital where available or private finance where it isn’t

Root and branchWith cuts in expenditure being applied across UK public services, the government is conducting an extensive review of procurement – rooting out wasteful practices and cumbersome processes to streamline the system. But will the Lean Review process succeed in cutting costs? By Tracey Lee

continued overleaf ➔

Funding mechanisms and sources:

Public private partnership Joint venture company

JESSICA European Investment Bank via urban development funds

winter 11/12_035034_ The Journal of LeighFisher

■ Government and infrastructure

At the end of 2010, the minister for

the UK’s cabinet office, Francis

Maude, announced a Lean

Review designed to uncover

any wasteful practices and unnecessary

complexity in central government

procurement processes – and to suggest

actions to rectify them. The objective was

to examine how the procurement process

can be accelerated within UK central

government, to make doing business with

government faster and cheaper, both for

buyer and supplier.

The study investigated procurements

using competitive dialogue in central

departments. It found that there were

significant savings to be made in time and

cost by working in a more efficient and

effective way. It was concluded that there

was potential to reduce turnaround time by

70% on competitive dialogue procurements,

reduce supplier bid costs by £3.5 million

per competitive dialogue, and reduce

government resource and processing costs

by £400,000 per competitive dialogue.

Five key themes emerged from the study.

There was misuse and poor selection of

procurement route. Excessive waste was

built into the existing procurement process

from inception through to award. There

was a lack of sufficient capable senior

procurement resources and commercial

in-house legal advice. There was insufficient

preparation and planning for tenders via

the Official Journal of the European Union

(OJEU) process. Endemic bureaucracy was

leading to excessive levels of approvals

and governance.

The key output of the lean review

is a proposed new way of managing

competitive dialogue procurements, based

on lean principles, within the existing legal

This is not simply “standarization” but instead, a change in the way government thinks about procurement

framework, which eliminates waste and

unnecessary sequential activity. From

this starting point, the Cabinet Office has

developed a “standard solution” – a suite of

tools aimed at procurement practitioners for

the sourcing stages of competitive dialogue,

restricted and open procurement routes.

This standard solution is yet to be made

available to the public. At its centre, is the

understanding that there will be a future map

of materials and information required. This

value stream map will cover the stages of

procurement, from policy through business

need identification and baselining, market

analysis and sourcing strategy, supplier

identification, finalising contract and handing

off to contract management.

Whilst the standard solution has not been

made available to the public, we can expect

the overview to include suggestions such as

publication of a prior information notice (PIN).

This is designed to warm up the market and

advertize the industry engagement event, the

elimination of lengthy proposal documents,

the use of an outline solution template for

bidders to complete, and a draft contract to

be used as the vehicle for the dialogue so

the detailed solution emerges in the form of

contract schedules.

We have already seen standardized

contracts being used effectively across the

public private partnerships (PPP) initiative

in the UK to understand common risks, to

allow consistency of approach and pricing

across similar projects, and to reduce time

and costs of negotiation.