Embed Size (px)

Citation preview

19 June 2013 Business time in Middle-earth

Recent coverage by financial press (in particular the FT) in Europe of the New Zealand oil and gas sector has given a flavour of what could be looked back upon as an inflection point for the country and some of its players over the next 12-18 months. The New Zealand space is one that we know particularly well, underpinned by our 2012-13 New Zealand Petroleum Sector Yearbook.

While globally still very much a fringe play, momentum in New Zealand is in sharp ascent. Three offshore rigs have already been confirmed to arrive during H213: a shallow-water jack-up (Ensco-107), a mid-water semi-sub (Kan Tan IV) and a deepwater drill ship (Noble Bob Douglas). Onshore, there has been an equally sharp upswing in forward E&P work programmes.

Player attention continues to centre on the country’s only producing basin, Taranaki, which has already yielded 2 bln boe. Listed small and mid-cap players active in Taranaki include AWE (ASX:AWE), Beach Energy (ASX:BPT), Cue Energy (ASX:CUE), East West Petroleum (TSX-V:EW), Horizon Oil (ASX:HZN), Kea Petroleum (AIM:KEA), Loyz Energy (SGX:LOYZ), New Zealand Energy Corp (TSX-V:NZ), New Zealand Oil and Gas (NZX:NZO), Octanex (ASX:OXX), Pan Pacific Petroleum (ASX:PPP) and TAG Oil (TSX:TAO).

Increasingly players are also being drawn to the 17 other basins mapped within NZ’s 5.9m km2 (eight-times the size of the North Sea) of sovereign territory, more than 95% of which lies offshore. While a number are already known to house hydrocarbons, only Taranaki has graduated to commercial production. The frontier plays are largely the domain of deep-pocketed major and supermajor portfolio players, with the likes of Shell, OMV, PTTEP, Mitsui and Origin leading the way. An exception is the onshore East Coast Basin where TAG Oil and New Zealand Energy Corp hold significant acreage and are each advancing work programmes focused towards proving-up the commerciality of the region’s long-appreciated shale oil and gas potential.

Anadarko entered the New Zealand sector in early 2010 and has since advanced an aggressive work programme over a large offshore acreage position to the east of the South Island. Anadarko has said it sees Mozambique-like big-gas analogues in the region, causing others to tune in and listen. Further weight was added with the recent announcement of CNOOC partnering with Shell to lodge a prospecting permit application over 147,000km2 of virgin acreage across the New Caledonia Basin in the northwest corner of the New Zealand EEZ. The permit represents an area larger in size than England. A number of other majors are known also to be kicking the New Zealand tyres, with names already in the public domain including Chevron, Repsol, Woodside, Statoil and Santos. Numerous others are also known to be looking, and at least one other supermajor is also thought to be actively engaged.

Withi this frame, we highlight mid-caps AWE, Cue Energy and New Zealand Oil and Gas as ones to watch.

Catalytic converter New Zealand focus

For further details please contact: Oil & gas team

Ian McLelland +44 (0)20 3077 5756

Will Forbes +44 (0)20 3077 5749 John Kidd +64 (0)4 8948 555 Elaine Reynolds +44 (0)20 3077 5713 Peter Dupont +44 (0)20 3077 5741 Xavier Grunauer +44 (0) 20 3077 5700 [email protected]

Institutional sales

Gareth Jones +44 (0)20 3077 5704

Catalytic converter | 19 June 2013 2

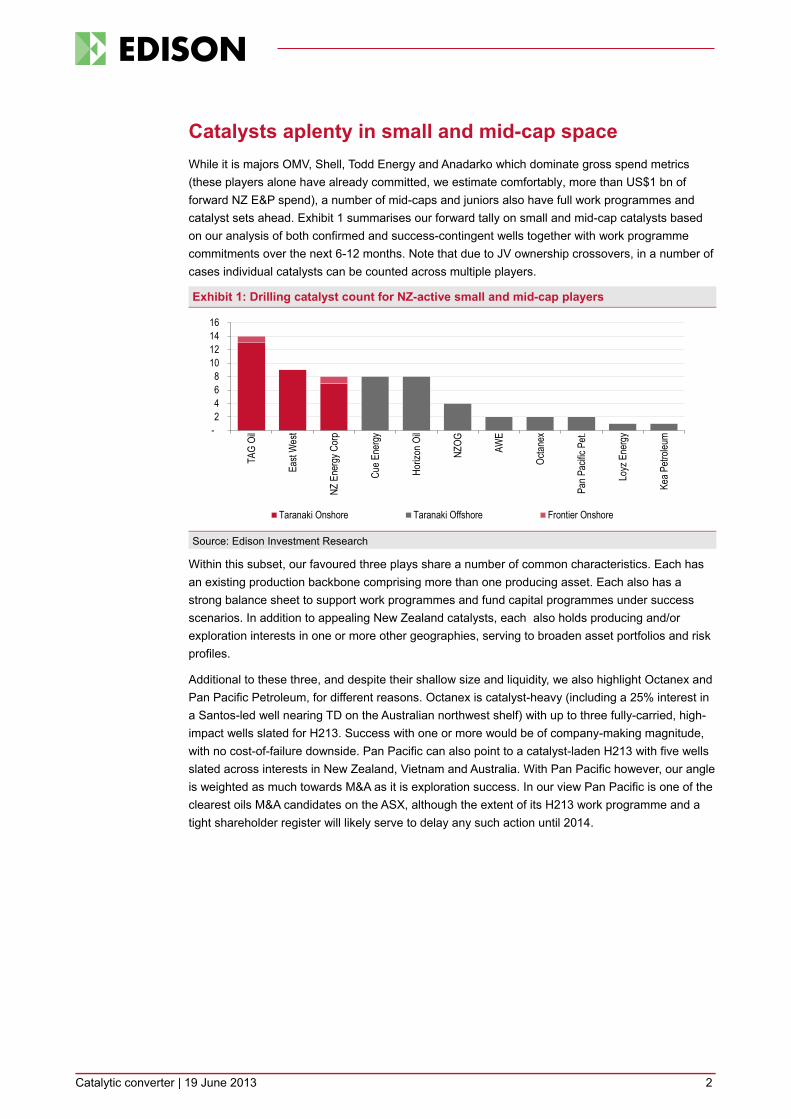

Catalysts aplenty in small and mid-cap space While it is majors OMV, Shell, Todd Energy and Anadarko which dominate gross spend metrics (these players alone have already committed, we estimate comfortably, more than US$1 bn of forward NZ E&P spend), a number of mid-caps and juniors also have full work programmes and catalyst sets ahead. Exhibit 1 summarises our forward tally on small and mid-cap catalysts based on our analysis of both confirmed and success-contingent wells together with work programme commitments over the next 6-12 months. Note that due to JV ownership crossovers, in a number of cases individual catalysts can be counted across multiple players.

Exhibit 1: Drilling catalyst count for NZ-active small and mid-cap players

Source: Edison Investment Research

Within this subset, our favoured three plays share a number of common characteristics. Each has an existing production backbone comprising more than one producing asset. Each also has a strong balance sheet to support work programmes and fund capital programmes under success scenarios. In addition to appealing New Zealand catalysts, each also holds producing and/or exploration interests in one or more other geographies, serving to broaden asset portfolios and risk profiles.

Additional to these three, and despite their shallow size and liquidity, we also highlight Octanex and Pan Pacific Petroleum, for different reasons. Octanex is catalyst-heavy (including a 25% interest in a Santos-led well nearing TD on the Australian northwest shelf) with up to three fully-carried, high-impact wells slated for H213. Success with one or more would be of company-making magnitude, with no cost-of-failure downside. Pan Pacific can also point to a catalyst-laden H213 with five wells slated across interests in New Zealand, Vietnam and Australia. With Pan Pacific however, our angle is weighted as much towards M&A as it is exploration success. In our view Pan Pacific is one of the clearest oils M&A candidates on the ASX, although the extent of its H213 work programme and a tight shareholder register will likely serve to delay any such action until 2014.

- 2 4 6 8

10 12 14 16

TAG

Oil

East

Wes

t

NZ E

nerg

y Cor

p

Cue E

nerg

y

Horiz

on O

il

NZOG AW

E

Octan

ex

Pan P

acific

Pet.

Loyz

Ene

rgy

Kea P

etrole

um

Taranaki Onshore Taranaki Offshore Frontier Onshore

Catalytic converter | 19 June 2013 3

Top NZ-active small/mid cap picks

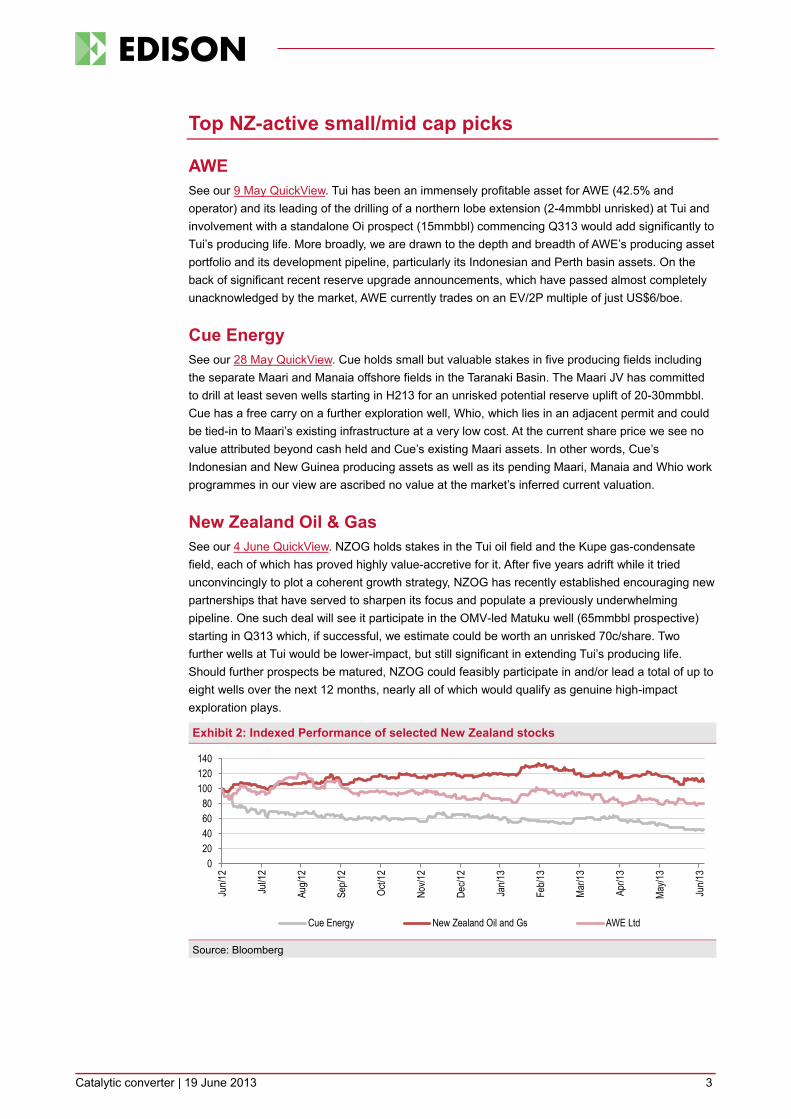

AWE See our 9 May QuickView. Tui has been an immensely profitable asset for AWE (42.5% and operator) and its leading of the drilling of a northern lobe extension (2-4mmbbl unrisked) at Tui and involvement with a standalone Oi prospect (15mmbbl) commencing Q313 would add significantly to Tui’s producing life. More broadly, we are drawn to the depth and breadth of AWE’s producing asset portfolio and its development pipeline, particularly its Indonesian and Perth basin assets. On the back of significant recent reserve upgrade announcements, which have passed almost completely unacknowledged by the market, AWE currently trades on an EV/2P multiple of just US$6/boe.

Cue Energy See our 28 May QuickView. Cue holds small but valuable stakes in five producing fields including the separate Maari and Manaia offshore fields in the Taranaki Basin. The Maari JV has committed to drill at least seven wells starting in H213 for an unrisked potential reserve uplift of 20-30mmbbl. Cue has a free carry on a further exploration well, Whio, which lies in an adjacent permit and could be tied-in to Maari’s existing infrastructure at a very low cost. At the current share price we see no value attributed beyond cash held and Cue’s existing Maari assets. In other words, Cue’s Indonesian and New Guinea producing assets as well as its pending Maari, Manaia and Whio work programmes in our view are ascribed no value at the market’s inferred current valuation.

New Zealand Oil & Gas See our 4 June QuickView. NZOG holds stakes in the Tui oil field and the Kupe gas-condensate field, each of which has proved highly value-accretive for it. After five years adrift while it tried unconvincingly to plot a coherent growth strategy, NZOG has recently established encouraging new partnerships that have served to sharpen its focus and populate a previously underwhelming pipeline. One such deal will see it participate in the OMV-led Matuku well (65mmbbl prospective) starting in Q313 which, if successful, we estimate could be worth an unrisked 70c/share. Two further wells at Tui would be lower-impact, but still significant in extending Tui’s producing life. Should further prospects be matured, NZOG could feasibly participate in and/or lead a total of up to eight wells over the next 12 months, nearly all of which would qualify as genuine high-impact exploration plays.

Exhibit 2: Indexed Performance of selected New Zealand stocks

Source: Bloomberg

020406080

100120140

Jun/1

2

Jul/1

2

Aug/1

2

Sep/1

2

Oct/1

2

Nov/1

2

Dec/1

2

Jan/1

3

Feb/1

3

Mar/1

3

Apr/1

3

May/1

3

Jun/1

3

Cue Energy New Zealand Oil and Gs AWE Ltd

Catalytic converter | 19 June 2013 4

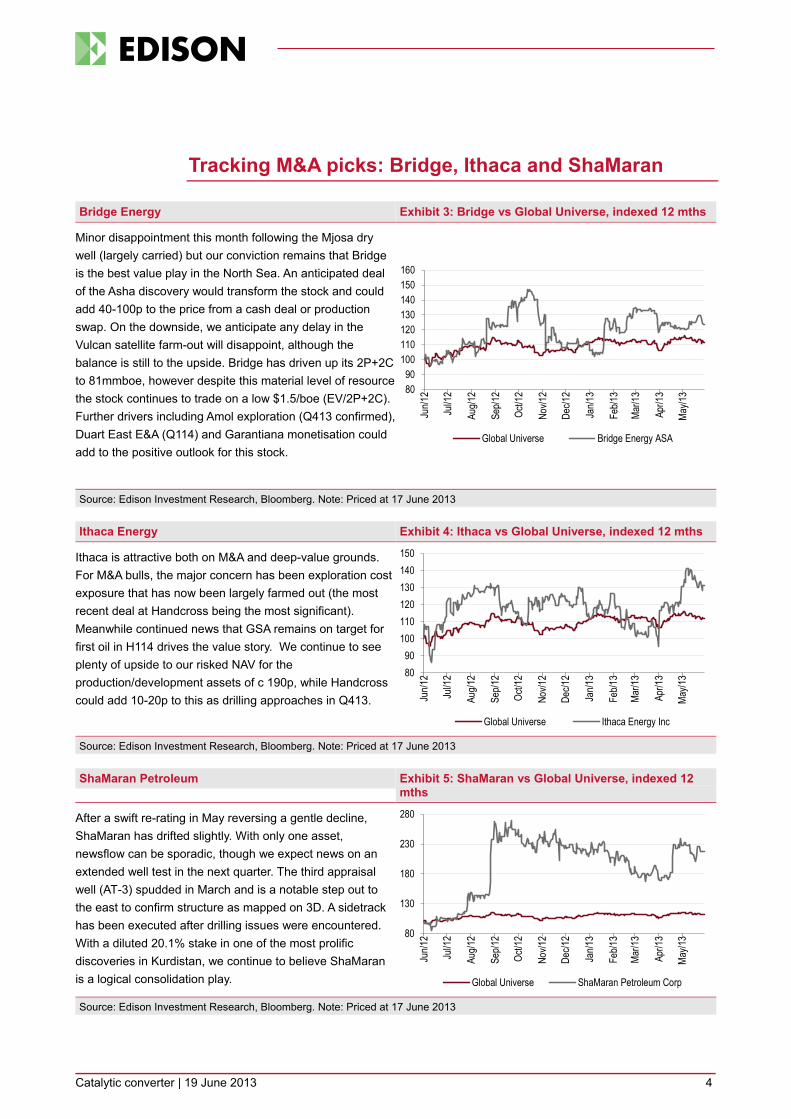

Tracking M&A picks: Bridge, Ithaca and ShaMaran

Bridge Energy Exhibit 3: Bridge vs Global Universe, indexed 12 mths

Minor disappointment this month following the Mjosa dry well (largely carried) but our conviction remains that Bridge is the best value play in the North Sea. An anticipated deal of the Asha discovery would transform the stock and could add 40-100p to the price from a cash deal or production swap. On the downside, we anticipate any delay in the Vulcan satellite farm-out will disappoint, although the balance is still to the upside. Bridge has driven up its 2P+2C to 81mmboe, however despite this material level of resource the stock continues to trade on a low $1.5/boe (EV/2P+2C). Further drivers including Amol exploration (Q413 confirmed), Duart East E&A (Q114) and Garantiana monetisation could add to the positive outlook for this stock.

Source: Edison Investment Research, Bloomberg. Note: Priced at 17 June 2013

Ithaca Energy Exhibit 4: Ithaca vs Global Universe, indexed 12 mths

Ithaca is attractive both on M&A and deep-value grounds. For M&A bulls, the major concern has been exploration cost exposure that has now been largely farmed out (the most recent deal at Handcross being the most significant). Meanwhile continued news that GSA remains on target for first oil in H114 drives the value story. We continue to see plenty of upside to our risked NAV for the production/development assets of c 190p, while Handcross could add 10-20p to this as drilling approaches in Q413.

Source: Edison Investment Research, Bloomberg. Note: Priced at 17 June 2013

ShaMaran Petroleum Exhibit 5: ShaMaran vs Global Universe, indexed 12 mths

After a swift re-rating in May reversing a gentle decline, ShaMaran has drifted slightly. With only one asset, newsflow can be sporadic, though we expect news on an extended well test in the next quarter. The third appraisal well (AT-3) spudded in March and is a notable step out to the east to confirm structure as mapped on 3D. A sidetrack has been executed after drilling issues were encountered. With a diluted 20.1% stake in one of the most prolific discoveries in Kurdistan, we continue to believe ShaMaran is a logical consolidation play.

Source: Edison Investment Research, Bloomberg. Note: Priced at 17 June 2013

8090

100110120130140150160

Jun/1

2

Jul/1

2

Aug/1

2

Sep/1

2

Oct/1

2

Nov/1

2

Dec/1

2

Jan/1

3

Feb/1

3

Mar/1

3

Apr/1

3

May/1

3

Global Universe Bridge Energy ASA

8090

100110120130140150

Jun/1

2

Jul/1

2

Aug/1

2

Sep/1

2

Oct/1

2

Nov/1

2

Dec/1

2

Jan/1

3

Feb/1

3

Mar/1

3

Apr/1

3

May/1

3

Global Universe Ithaca Energy Inc

80

130

180

230

280

Jun/1

2

Jul/1

2

Aug/1

2

Sep/1

2

Oct/1

2

Nov/1

2

Dec/1

2

Jan/1

3

Feb/1

3

Mar/1

3

Apr/1

3

May/1

3

Global Universe ShaMaran Petroleum Corp

Catalytic converter | 19 June 2013 5

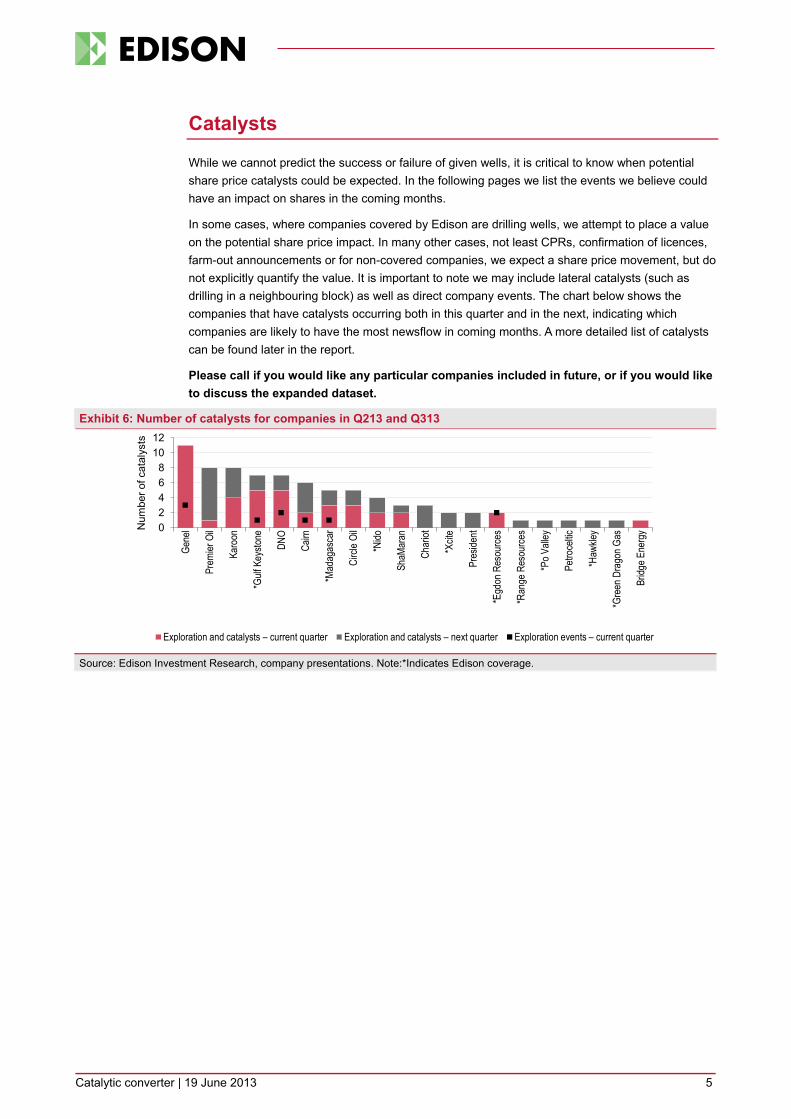

Catalysts

While we cannot predict the success or failure of given wells, it is critical to know when potential share price catalysts could be expected. In the following pages we list the events we believe could have an impact on shares in the coming months.

In some cases, where companies covered by Edison are drilling wells, we attempt to place a value on the potential share price impact. In many other cases, not least CPRs, confirmation of licences, farm-out announcements or for non-covered companies, we expect a share price movement, but do not explicitly quantify the value. It is important to note we may include lateral catalysts (such as drilling in a neighbouring block) as well as direct company events. The chart below shows the companies that have catalysts occurring both in this quarter and in the next, indicating which companies are likely to have the most newsflow in coming months. A more detailed list of catalysts can be found later in the report.

Please call if you would like any particular companies included in future, or if you would like to discuss the expanded dataset.

Exhibit 6: Number of catalysts for companies in Q213 and Q313

Source: Edison Investment Research, company presentations. Note:*Indicates Edison coverage.

02468

1012

Gene

l

Prem

ier O

il

Karo

on

*Gulf

Key

stone

DNO

Cairn

*Mad

agas

car

Circl

e Oil

*Nido

ShaM

aran

Char

iot

*Xcit

e

Pres

ident

*Egd

on R

esou

rces

*Ran

ge R

esou

rces

*Po V

alley

Petro

celtic

*Haw

kley

*Gre

en D

rago

n Gas

Bridg

e Ene

rgyN

umbe

r of c

atal

ysts

Exploration and catalysts – current quarter Exploration and catalysts – next quarter Exploration events – current quarter

Catalytic converter | 19 June 2013 6

Elephant hunters: Genel, DNO, Tullow and Africa

For investors looking for catalysts that could have a major impact, we highlight the following events (though we are not necessarily promoting these as buy ideas): Tawke Deep is a key well for Genel and DNO as it could add significant resources to the

producing fields from deeper horizons in the Jurassic and Triassic. On 11 June, DNO announced that it had flowed 1,500bopd from an Upper Jurassic reservoir underlying Tawke. DNO announced that this likely increases recoverable reserves at Tawke to over 1bn boe. We await the tests of the two reservoirs remaining.

Tullow Oil and Africa Oil are currently drilling the Etuko well in Kenya. Etuko is located on Block 10BB where the Ngamia-1 well was drilled, discovering a significant light oil resource. In addition to the discovery at Twiga South, Ngamia-1 materially de-risks the hydrocarbon system the Etuko well will test. Africa Oil estimates that the Etuko well will target 231mmbbl, with results expected in mid-July.

We also introduce Po Valley, which could have two significant well results by the end of the year. Gradizza should be spudded in Q313 and accounts for c 10% of the share price on a risked (13.5% CoS) basis. Success here could see a material value (if we move the CoS to 50%, it would imply a 40% move in the share price). The Canolo and Zini wells could see further upside later in the year.

Catalytic converter | 19 June 2013

7

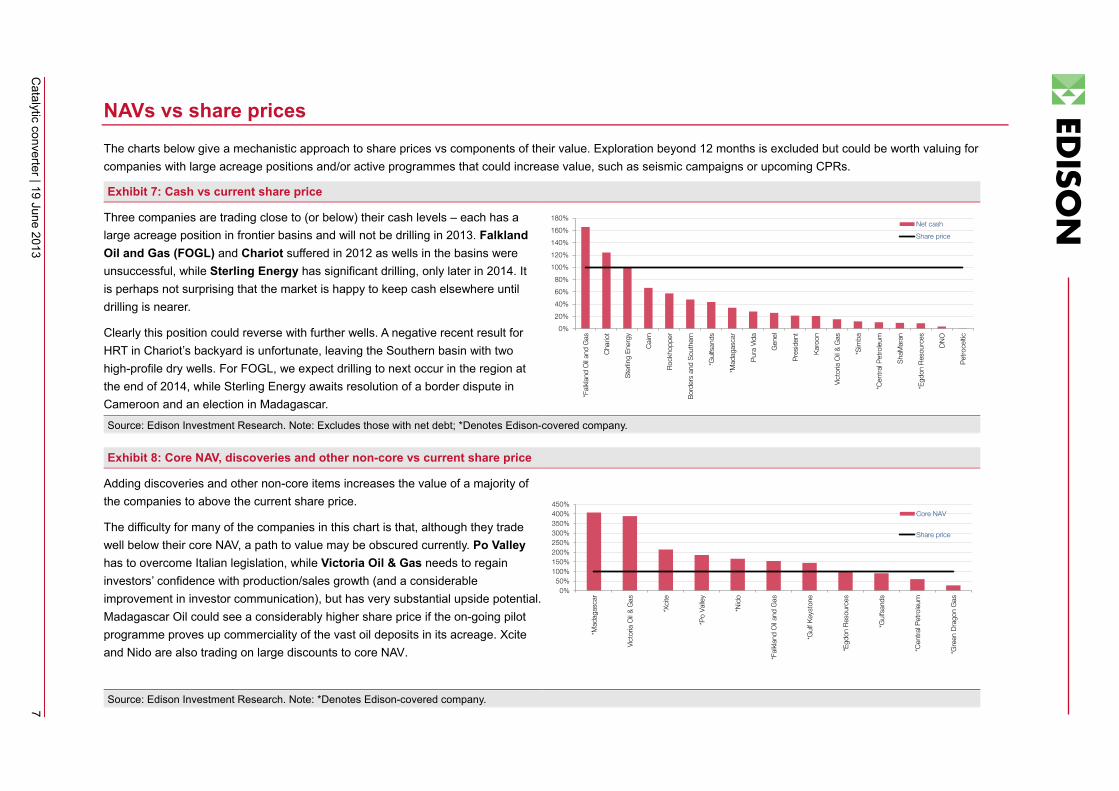

NAVs vs share prices

The charts below give a mechanistic approach to share prices vs components of their value. Exploration beyond 12 months is excluded but could be worth valuing for companies with large acreage positions and/or active programmes that could increase value, such as seismic campaigns or upcoming CPRs.

Exhibit 7: Cash vs current share price

Three companies are trading close to (or below) their cash levels – each has a large acreage position in frontier basins and will not be drilling in 2013. Falkland Oil and Gas (FOGL) and Chariot suffered in 2012 as wells in the basins were unsuccessful, while Sterling Energy has significant drilling, only later in 2014. It is perhaps not surprising that the market is happy to keep cash elsewhere until drilling is nearer.

Clearly this position could reverse with further wells. A negative recent result for HRT in Chariot’s backyard is unfortunate, leaving the Southern basin with two high-profile dry wells. For FOGL, we expect drilling to next occur in the region at the end of 2014, while Sterling Energy awaits resolution of a border dispute in Cameroon and an election in Madagascar. Source: Edison Investment Research. Note: Excludes those with net debt; *Denotes Edison-covered company.

Exhibit 8: Core NAV, discoveries and other non-core vs current share price

Adding discoveries and other non-core items increases the value of a majority of the companies to above the current share price.

The difficulty for many of the companies in this chart is that, although they trade well below their core NAV, a path to value may be obscured currently. Po Valley has to overcome Italian legislation, while Victoria Oil & Gas needs to regain investors’ confidence with production/sales growth (and a considerable improvement in investor communication), but has very substantial upside potential. Madagascar Oil could see a considerably higher share price if the on-going pilot programme proves up commerciality of the vast oil deposits in its acreage. Xcite and Nido are also trading on large discounts to core NAV.

Source: Edison Investment Research. Note: *Denotes Edison-covered company.

0%

20%

40%

60%

80%

100%

120%

140%

160%

180%

*Fal

klan

d O

il an

d G

as

Cha

riot

Ste

rling

Ene

rgy

Cai

rn

Roc

khop

per

Bor

ders

and

Sou

ther

n

*Gul

fsan

ds

*Mad

agas

car

Pur

a Vi

da

Gen

el

Pre

side

nt

Kar

oon

Vict

oria

Oil

& G

as

*Sim

ba

*Cen

tral

Pet

role

um

Sha

Mar

an

*Egd

on R

esou

rces

DN

O

Pet

roce

ltic

Net cash

Share price

0%50%

100%150%200%250%300%350%400%450%

*Mad

agas

car

Vict

oria

Oil

& G

as

*Xci

te

*Po

Val

ley

*Nid

o

*Fal

klan

d O

il an

d G

as

*Gul

f Key

ston

e

*Egd

on R

esou

rces

*Gul

fsan

ds

*Cen

tral

Pet

role

um

*Gre

en D

rago

n G

as

Core NAV

Share price

Catalytic converter | 19 June 2013

8

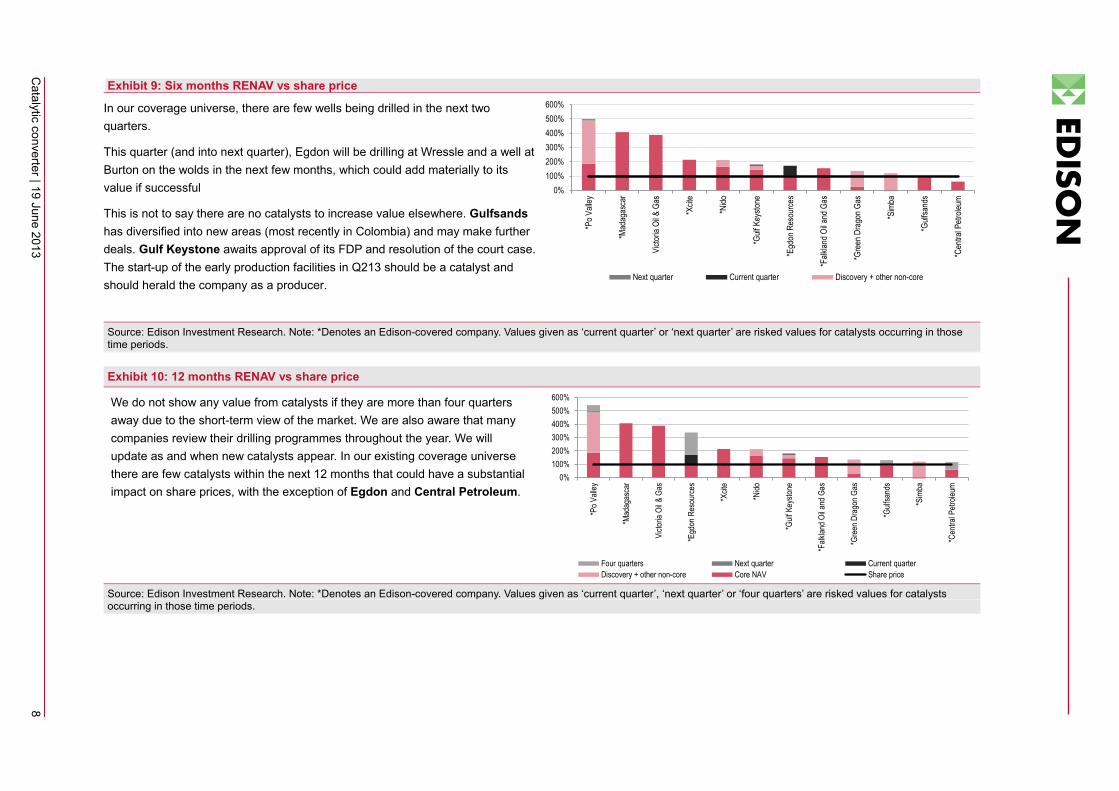

Exhibit 9: Six months RENAV vs share price

In our coverage universe, there are few wells being drilled in the next two quarters.

This quarter (and into next quarter), Egdon will be drilling at Wressle and a well at Burton on the wolds in the next few months, which could add materially to its value if successful

This is not to say there are no catalysts to increase value elsewhere. Gulfsands has diversified into new areas (most recently in Colombia) and may make further deals. Gulf Keystone awaits approval of its FDP and resolution of the court case. The start-up of the early production facilities in Q213 should be a catalyst and should herald the company as a producer.

Source: Edison Investment Research. Note: *Denotes an Edison-covered company. Values given as ‘current quarter’ or ‘next quarter’ are risked values for catalysts occurring in those time periods.

Exhibit 10: 12 months RENAV vs share price

We do not show any value from catalysts if they are more than four quarters away due to the short-term view of the market. We are also aware that many companies review their drilling programmes throughout the year. We will update as and when new catalysts appear. In our existing coverage universe there are few catalysts within the next 12 months that could have a substantial impact on share prices, with the exception of Egdon and Central Petroleum.

Source: Edison Investment Research. Note: *Denotes an Edison-covered company. Values given as ‘current quarter’, ‘next quarter’ or ‘four quarters’ are risked values for catalysts occurring in those time periods.

0%100%200%300%400%500%600%

*Po V

alley

*Mad

agas

car

Victo

ria O

il & G

as

*Xcit

e

*Nido

*Gulf

Key

stone

*Egd

on R

esou

rces

*Falk

land O

il and

Gas

*Gre

en D

rago

n Gas

*Sim

ba

*Gulf

sand

s

*Cen

tral P

etrole

um

Next quarter Current quarter Discovery + other non-core

0%100%200%300%400%500%600%

*Po V

alley

*Mad

agas

car

Victo

ria O

il & G

as

*Egd

on R

esou

rces

*Xcit

e

*Nido

*Gulf

Key

stone

*Falk

land O

il and

Gas

*Gre

en D

rago

n Gas

*Gulf

sand

s

*Sim

ba

*Cen

tral P

etrole

um

Four quarters Next quarter Current quarterDiscovery + other non-core Core NAV Share price

Catalytic converter | 19 June 2013 9

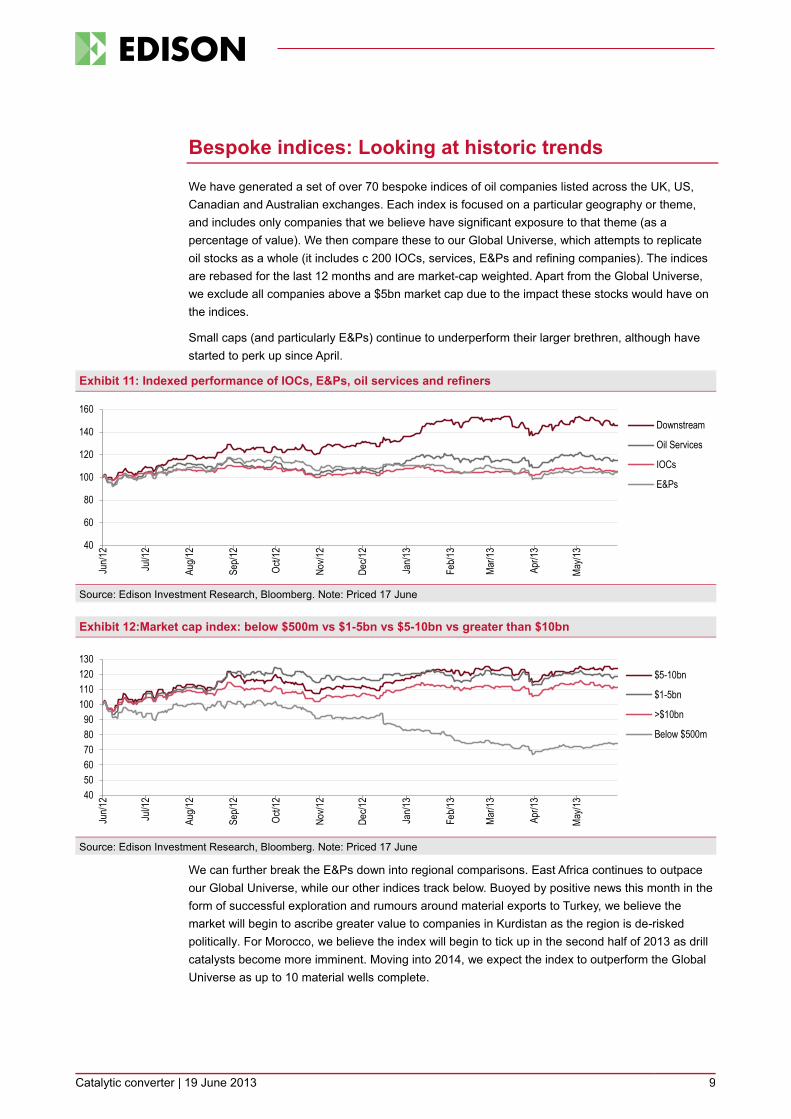

Bespoke indices: Looking at historic trends

We have generated a set of over 70 bespoke indices of oil companies listed across the UK, US, Canadian and Australian exchanges. Each index is focused on a particular geography or theme, and includes only companies that we believe have significant exposure to that theme (as a percentage of value). We then compare these to our Global Universe, which attempts to replicate oil stocks as a whole (it includes c 200 IOCs, services, E&Ps and refining companies). The indices are rebased for the last 12 months and are market-cap weighted. Apart from the Global Universe, we exclude all companies above a $5bn market cap due to the impact these stocks would have on the indices.

Small caps (and particularly E&Ps) continue to underperform their larger brethren, although have started to perk up since April.

Exhibit 11: Indexed performance of IOCs, E&Ps, oil services and refiners

Source: Edison Investment Research, Bloomberg. Note: Priced 17 June

Exhibit 12:Market cap index: below $500m vs $1-5bn vs $5-10bn vs greater than $10bn

Source: Edison Investment Research, Bloomberg. Note: Priced 17 June

We can further break the E&Ps down into regional comparisons. East Africa continues to outpace our Global Universe, while our other indices track below. Buoyed by positive news this month in the form of successful exploration and rumours around material exports to Turkey, we believe the market will begin to ascribe greater value to companies in Kurdistan as the region is de-risked politically. For Morocco, we believe the index will begin to tick up in the second half of 2013 as drill catalysts become more imminent. Moving into 2014, we expect the index to outperform the Global Universe as up to 10 material wells complete.

40

60

80

100

120

140

160

Jun/1

2

Jul/1

2

Aug/1

2

Sep/1

2

Oct/1

2

Nov/1

2

Dec/1

2

Jan/1

3

Feb/1

3

Mar/1

3

Apr/1

3

May/1

3

Downstream

Oil Services

IOCs

E&Ps

405060708090

100110120130

Jun/1

2

Jul/1

2

Aug/1

2

Sep/1

2

Oct/1

2

Nov/1

2

Dec/1

2

Jan/1

3

Feb/1

3

Mar/1

3

Apr/1

3

May/1

3

$5-10bn

$1-5bn

>$10bn

Below $500m

Catalytic converter | 19 June 2013 10

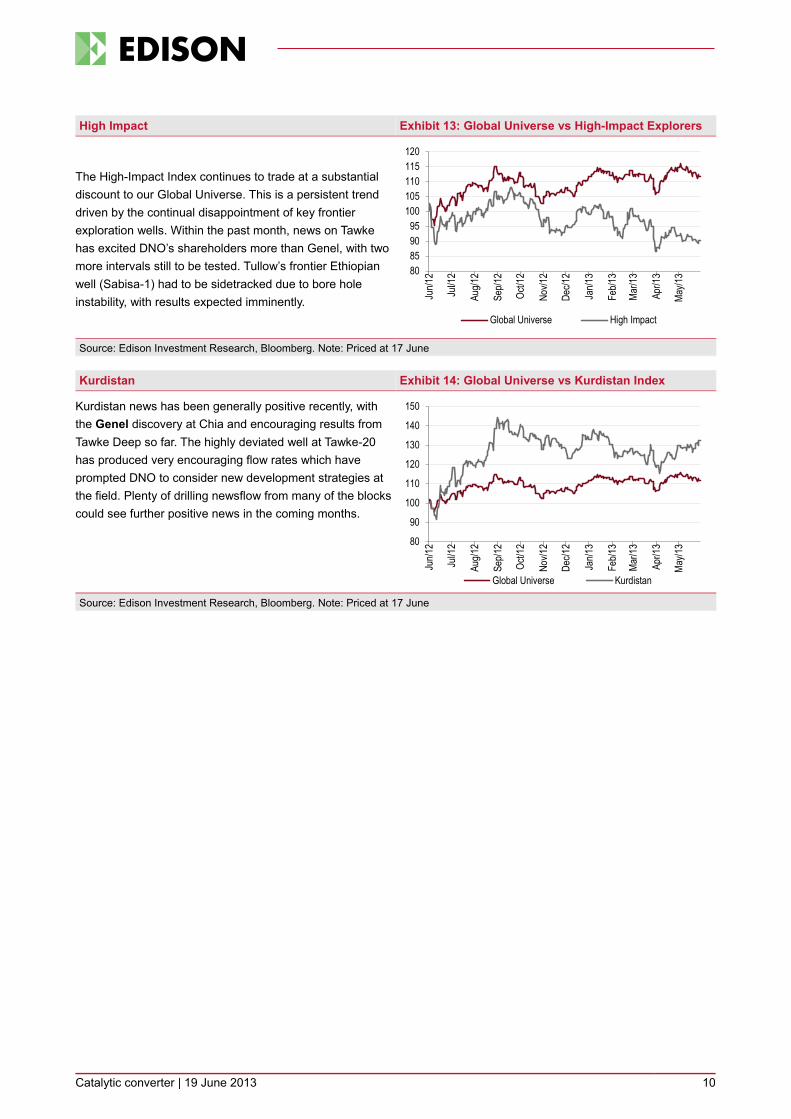

High Impact Exhibit 13: Global Universe vs High-Impact Explorers

The High-Impact Index continues to trade at a substantial discount to our Global Universe. This is a persistent trend driven by the continual disappointment of key frontier exploration wells. Within the past month, news on Tawke has excited DNO’s shareholders more than Genel, with two more intervals still to be tested. Tullow’s frontier Ethiopian well (Sabisa-1) had to be sidetracked due to bore hole instability, with results expected imminently.

Source: Edison Investment Research, Bloomberg. Note: Priced at 17 June

Kurdistan Exhibit 14: Global Universe vs Kurdistan Index

Kurdistan news has been generally positive recently, with the Genel discovery at Chia and encouraging results from Tawke Deep so far. The highly deviated well at Tawke-20 has produced very encouraging flow rates which have prompted DNO to consider new development strategies at the field. Plenty of drilling newsflow from many of the blocks could see further positive news in the coming months.

Source: Edison Investment Research, Bloomberg. Note: Priced at 17 June

80859095

100105110115120

Jun/1

2

Jul/1

2

Aug/1

2

Sep/1

2

Oct/1

2

Nov/1

2

Dec/1

2

Jan/1

3

Feb/1

3

Mar/1

3

Apr/1

3

May/1

3

Global Universe High Impact

80

90

100

110

120

130

140

150

Jun/1

2

Jul/1

2

Aug/1

2

Sep/1

2

Oct/1

2

Nov/1

2

Dec/1

2

Jan/1

3

Feb/1

3

Mar/1

3

Apr/1

3

May/1

3

Global Universe Kurdistan

Catalytic converter | 19 June 2013 11

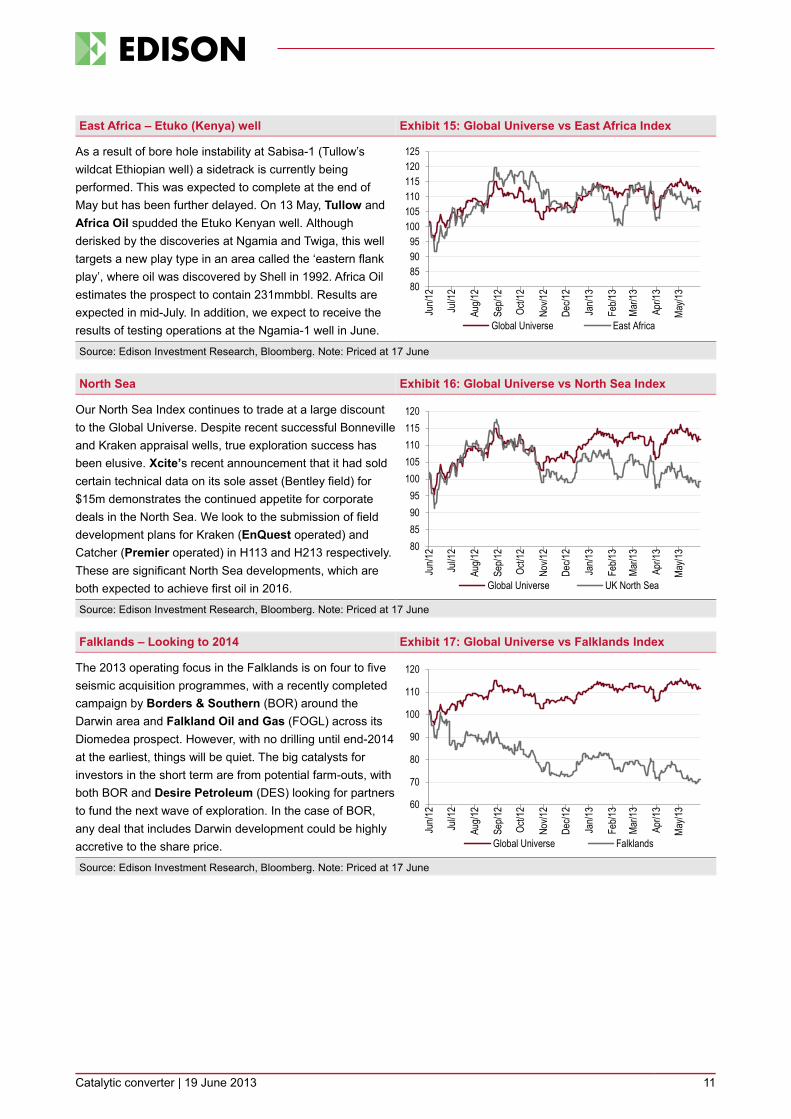

East Africa – Etuko (Kenya) well Exhibit 15: Global Universe vs East Africa Index

As a result of bore hole instability at Sabisa-1 (Tullow’s wildcat Ethiopian well) a sidetrack is currently being performed. This was expected to complete at the end of May but has been further delayed. On 13 May, Tullow and Africa Oil spudded the Etuko Kenyan well. Although derisked by the discoveries at Ngamia and Twiga, this well targets a new play type in an area called the ‘eastern flank play’, where oil was discovered by Shell in 1992. Africa Oil estimates the prospect to contain 231mmbbl. Results are expected in mid-July. In addition, we expect to receive the results of testing operations at the Ngamia-1 well in June. Source: Edison Investment Research, Bloomberg. Note: Priced at 17 June

North Sea Exhibit 16: Global Universe vs North Sea Index

Our North Sea Index continues to trade at a large discount to the Global Universe. Despite recent successful Bonneville and Kraken appraisal wells, true exploration success has been elusive. Xcite’s recent announcement that it had sold certain technical data on its sole asset (Bentley field) for $15m demonstrates the continued appetite for corporate deals in the North Sea. We look to the submission of field development plans for Kraken (EnQuest operated) and Catcher (Premier operated) in H113 and H213 respectively. These are significant North Sea developments, which are both expected to achieve first oil in 2016. Source: Edison Investment Research, Bloomberg. Note: Priced at 17 June

Falklands – Looking to 2014 Exhibit 17: Global Universe vs Falklands Index

The 2013 operating focus in the Falklands is on four to five seismic acquisition programmes, with a recently completed campaign by Borders & Southern (BOR) around the Darwin area and Falkland Oil and Gas (FOGL) across its Diomedea prospect. However, with no drilling until end-2014 at the earliest, things will be quiet. The big catalysts for investors in the short term are from potential farm-outs, with both BOR and Desire Petroleum (DES) looking for partners to fund the next wave of exploration. In the case of BOR, any deal that includes Darwin development could be highly accretive to the share price. Source: Edison Investment Research, Bloomberg. Note: Priced at 17 June

80859095

100105110115120125

Jun/1

2

Jul/1

2

Aug/1

2

Sep/1

2

Oct/1

2

Nov/1

2

Dec/1

2

Jan/1

3

Feb/1

3

Mar/1

3

Apr/1

3

May/1

3

Global Universe East Africa

80859095

100105110115120

Jun/1

2

Jul/1

2

Aug/1

2

Sep/1

2

Oct/1

2

Nov/1

2

Dec/1

2

Jan/1

3

Feb/1

3

Mar/1

3

Apr/1

3

May/1

3

Global Universe UK North Sea

60

70

80

90

100

110

120

Jun/1

2

Jul/1

2

Aug/1

2

Sep/1

2

Oct/1

2

Nov/1

2

Dec/1

2

Jan/1

3

Feb/1

3

Mar/1

3

Apr/1

3

May/1

3

Global Universe Falklands

Catalytic converter | 19 June 2013 12

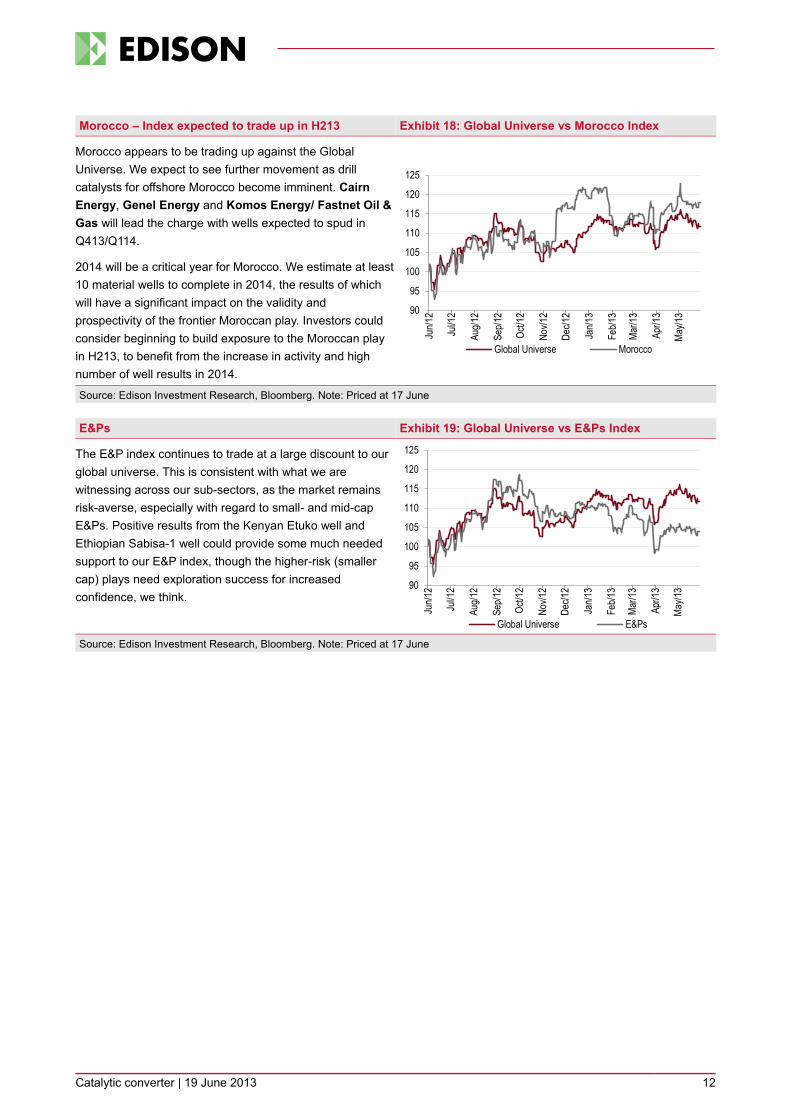

Morocco – Index expected to trade up in H213 Exhibit 18: Global Universe vs Morocco Index

Morocco appears to be trading up against the Global Universe. We expect to see further movement as drill catalysts for offshore Morocco become imminent. Cairn Energy, Genel Energy and Komos Energy/ Fastnet Oil & Gas will lead the charge with wells expected to spud in Q413/Q114.

2014 will be a critical year for Morocco. We estimate at least 10 material wells to complete in 2014, the results of which will have a significant impact on the validity and prospectivity of the frontier Moroccan play. Investors could consider beginning to build exposure to the Moroccan play in H213, to benefit from the increase in activity and high number of well results in 2014.

Source: Edison Investment Research, Bloomberg. Note: Priced at 17 June

E&Ps Exhibit 19: Global Universe vs E&Ps Index

The E&P index continues to trade at a large discount to our global universe. This is consistent with what we are witnessing across our sub-sectors, as the market remains risk-averse, especially with regard to small- and mid-cap E&Ps. Positive results from the Kenyan Etuko well and Ethiopian Sabisa-1 well could provide some much needed support to our E&P index, though the higher-risk (smaller cap) plays need exploration success for increased confidence, we think.

Source: Edison Investment Research, Bloomberg. Note: Priced at 17 June

90

95

100

105

110

115

120

125

Jun/1

2

Jul/1

2

Aug/1

2

Sep/1

2

Oct/1

2

Nov/1

2

Dec/1

2

Jan/1

3

Feb/1

3

Mar/1

3

Apr/1

3

May/1

3

Global Universe Morocco

90

95

100

105

110

115

120

125

Jun/1

2

Jul/1

2

Aug/1

2

Sep/1

2

Oct/1

2

Nov/1

2

Dec/1

2

Jan/1

3

Feb/1

3

Mar/1

3

Apr/1

3

May/1

3

Global Universe E&Ps

Catalytic converter | 19 June 2013

13

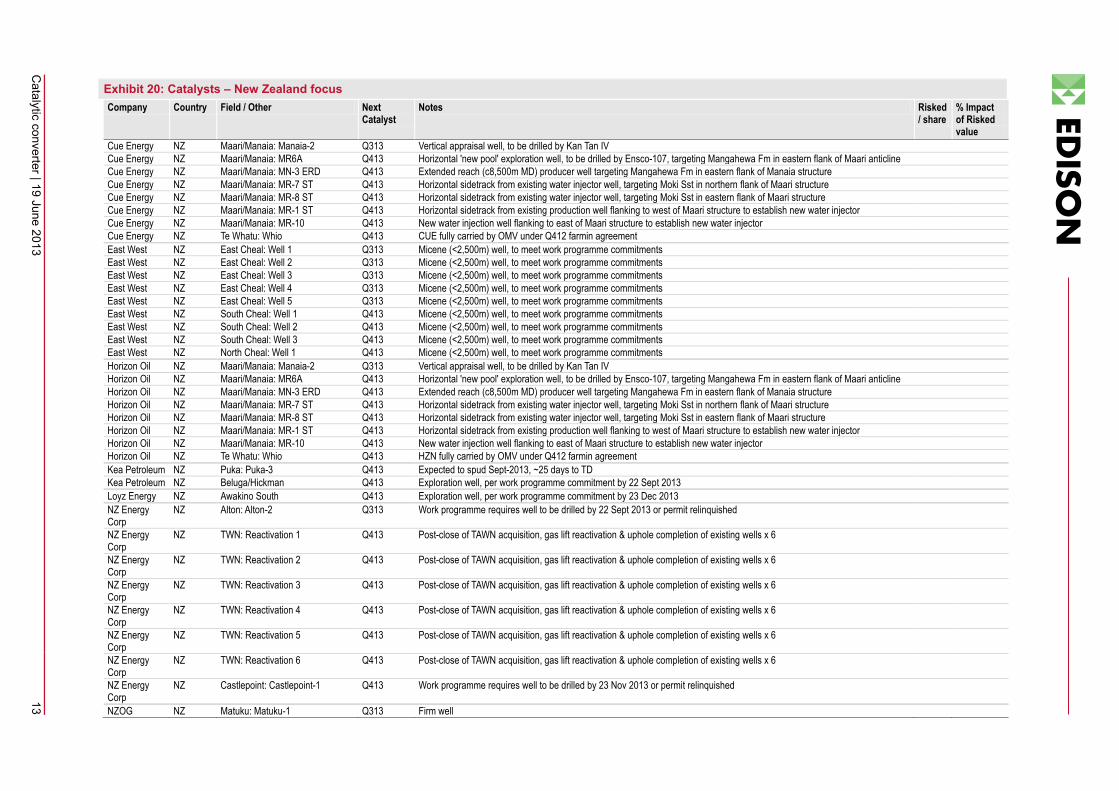

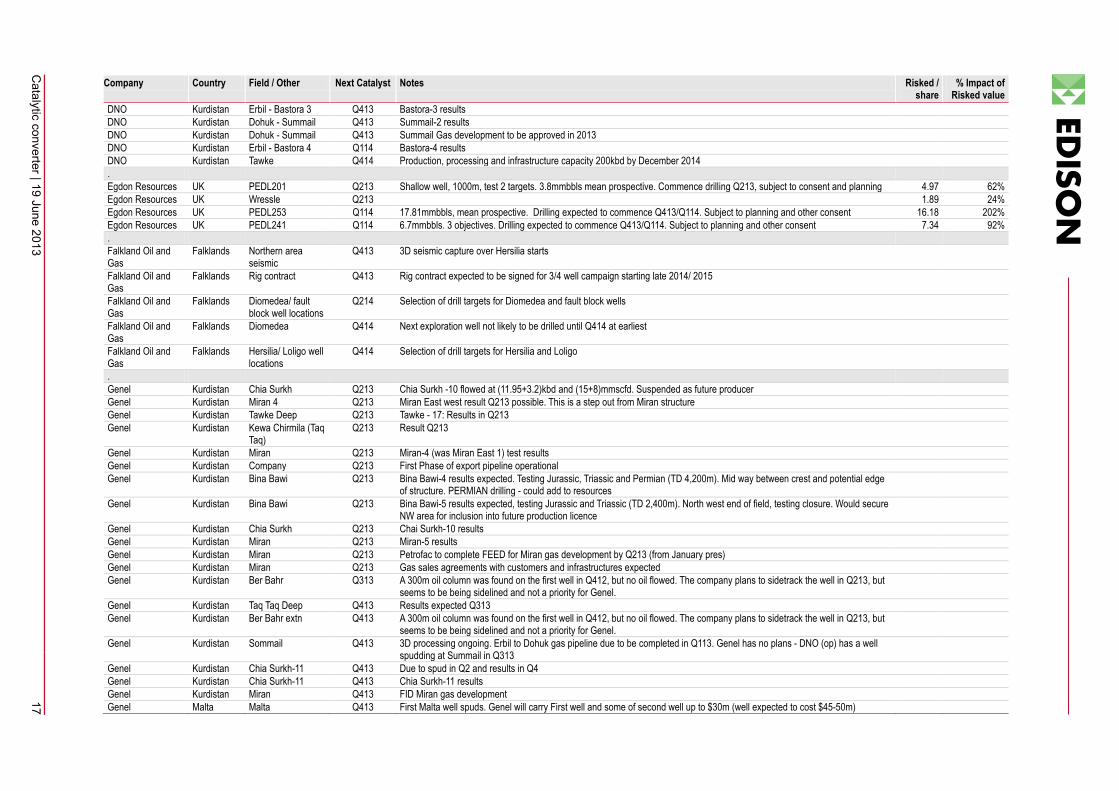

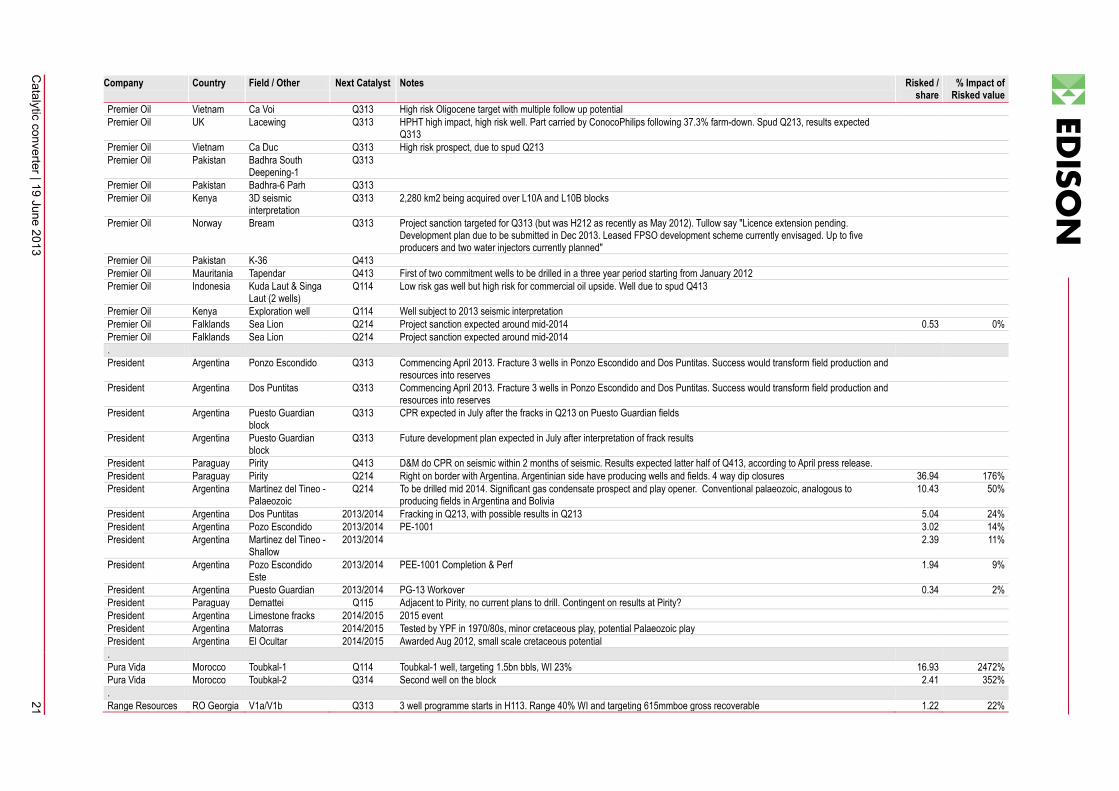

Exhibit 20: Catalysts – New Zealand focus Company Country Field / Other Next

Catalyst Notes Risked

/ share % Impact of Risked value

Cue Energy NZ Maari/Manaia: Manaia-2 Q313 Vertical appraisal well, to be drilled by Kan Tan IV Cue Energy NZ Maari/Manaia: MR6A Q413 Horizontal 'new pool' exploration well, to be drilled by Ensco-107, targeting Mangahewa Fm in eastern flank of Maari anticline Cue Energy NZ Maari/Manaia: MN-3 ERD Q413 Extended reach (c8,500m MD) producer well targeting Mangahewa Fm in eastern flank of Manaia structure Cue Energy NZ Maari/Manaia: MR-7 ST Q413 Horizontal sidetrack from existing water injector well, targeting Moki Sst in northern flank of Maari structure Cue Energy NZ Maari/Manaia: MR-8 ST Q413 Horizontal sidetrack from existing water injector well, targeting Moki Sst in eastern flank of Maari structure Cue Energy NZ Maari/Manaia: MR-1 ST Q413 Horizontal sidetrack from existing production well flanking to west of Maari structure to establish new water injector Cue Energy NZ Maari/Manaia: MR-10 Q413 New water injection well flanking to east of Maari structure to establish new water injector Cue Energy NZ Te Whatu: Whio Q413 CUE fully carried by OMV under Q412 farmin agreement East West NZ East Cheal: Well 1 Q313 Micene (<2,500m) well, to meet work programme commitments East West NZ East Cheal: Well 2 Q313 Micene (<2,500m) well, to meet work programme commitments East West NZ East Cheal: Well 3 Q313 Micene (<2,500m) well, to meet work programme commitments East West NZ East Cheal: Well 4 Q313 Micene (<2,500m) well, to meet work programme commitments East West NZ East Cheal: Well 5 Q313 Micene (<2,500m) well, to meet work programme commitments East West NZ South Cheal: Well 1 Q413 Micene (<2,500m) well, to meet work programme commitments East West NZ South Cheal: Well 2 Q413 Micene (<2,500m) well, to meet work programme commitments East West NZ South Cheal: Well 3 Q413 Micene (<2,500m) well, to meet work programme commitments East West NZ North Cheal: Well 1 Q413 Micene (<2,500m) well, to meet work programme commitments Horizon Oil NZ Maari/Manaia: Manaia-2 Q313 Vertical appraisal well, to be drilled by Kan Tan IV Horizon Oil NZ Maari/Manaia: MR6A Q413 Horizontal 'new pool' exploration well, to be drilled by Ensco-107, targeting Mangahewa Fm in eastern flank of Maari anticline Horizon Oil NZ Maari/Manaia: MN-3 ERD Q413 Extended reach (c8,500m MD) producer well targeting Mangahewa Fm in eastern flank of Manaia structure Horizon Oil NZ Maari/Manaia: MR-7 ST Q413 Horizontal sidetrack from existing water injector well, targeting Moki Sst in northern flank of Maari structure Horizon Oil NZ Maari/Manaia: MR-8 ST Q413 Horizontal sidetrack from existing water injector well, targeting Moki Sst in eastern flank of Maari structure Horizon Oil NZ Maari/Manaia: MR-1 ST Q413 Horizontal sidetrack from existing production well flanking to west of Maari structure to establish new water injector Horizon Oil NZ Maari/Manaia: MR-10 Q413 New water injection well flanking to east of Maari structure to establish new water injector Horizon Oil NZ Te Whatu: Whio Q413 HZN fully carried by OMV under Q412 farmin agreement Kea Petroleum NZ Puka: Puka-3 Q413 Expected to spud Sept-2013, ~25 days to TD Kea Petroleum NZ Beluga/Hickman Q413 Exploration well, per work programme commitment by 22 Sept 2013 Loyz Energy NZ Awakino South Q413 Exploration well, per work programme commitment by 23 Dec 2013 NZ Energy Corp

NZ Alton: Alton-2 Q313 Work programme requires well to be drilled by 22 Sept 2013 or permit relinquished

NZ Energy Corp

NZ TWN: Reactivation 1 Q413 Post-close of TAWN acquisition, gas lift reactivation & uphole completion of existing wells x 6

NZ Energy Corp

NZ TWN: Reactivation 2 Q413 Post-close of TAWN acquisition, gas lift reactivation & uphole completion of existing wells x 6

NZ Energy Corp

NZ TWN: Reactivation 3 Q413 Post-close of TAWN acquisition, gas lift reactivation & uphole completion of existing wells x 6

NZ Energy Corp

NZ TWN: Reactivation 4 Q413 Post-close of TAWN acquisition, gas lift reactivation & uphole completion of existing wells x 6

NZ Energy Corp

NZ TWN: Reactivation 5 Q413 Post-close of TAWN acquisition, gas lift reactivation & uphole completion of existing wells x 6

NZ Energy Corp

NZ TWN: Reactivation 6 Q413 Post-close of TAWN acquisition, gas lift reactivation & uphole completion of existing wells x 6

NZ Energy Corp

NZ Castlepoint: Castlepoint-1 Q413 Work programme requires well to be drilled by 23 Nov 2013 or permit relinquished

NZOG NZ Matuku: Matuku-1 Q313 Firm well

Catalytic converter | 19 June 2013

14

Company Country Field / Other Next Catalyst

Notes Risked / share

% Impact of Risked value

NZOG NZ Matuku: Matuku-2 Q413 Contingent well Octanex NZ Matuku: Matuku-1 Q313 Firm well, OXX fully carried Octanex NZ Matuku: Matuku-2 Q413 Contingent well, OXX would be fully carried if JV sanctions TAG Oil NZ Cheal: Cardiff H213 Eocene (<4,000m) deep gas prospect targeting Kapuni Fm TAG Oil NZ East Cheal: Well 1 Q313 Miocene (<2,500m) well, to meet work programme commitments TAG Oil NZ East Cheal: Well 2 Q313 Miocene (<2,500m) well, to meet work programme commitments TAG Oil NZ East Cheal: Well 3 Q313 Miocene (<2,500m) well, to meet work programme commitments TAG Oil NZ East Cheal: Well 4 Q313 Miocene (<2,500m) well, to meet work programme commitments TAG Oil NZ East Cheal: Well 5 Q313 Miocene (<2,500m) well, to meet work programme commitments TAG Oil NZ Sidewinder: SW-A8 Q313 Completion of Sidewinder-A8 production well following suspension due to noise level breach TAG Oil NZ South Cheal: Well 1 Q413 Miocene (<2,500m) well, to meet work programme commitments TAG Oil NZ South Cheal: Well 2 Q413 Miocene (<2,500m) well, to meet work programme commitments TAG Oil NZ South Cheal: Well 3 Q413 Miocene (<2,500m) well, to meet work programme commitments TAG Oil NZ North Cheal: Well 1 Q413 Miocene (<2,500m) well, to meet work programme commitments TAG Oil NZ Sidewinder: Hellfire-1 Q413 Eocene (<4,000m) deep gas prospect targeting Kapuni Fm TAG Oil NZ Heatseeker: Heatseeker-1 Q413 Eocene (<4,000m) deep gas prospect targeting Kapuni Fm TAG Oil NZ Waitangi Hill Q413 East Coast Basin targeting conventional and unconventional (shale) prospects in area near Gisborne TAG Oil NZ Canterbury Q413 Exploration well, per work programme commitment by 9 Nov 2013

Source: Edison Investment Research, Companies

Catalytic converter | 19 June 2013

15

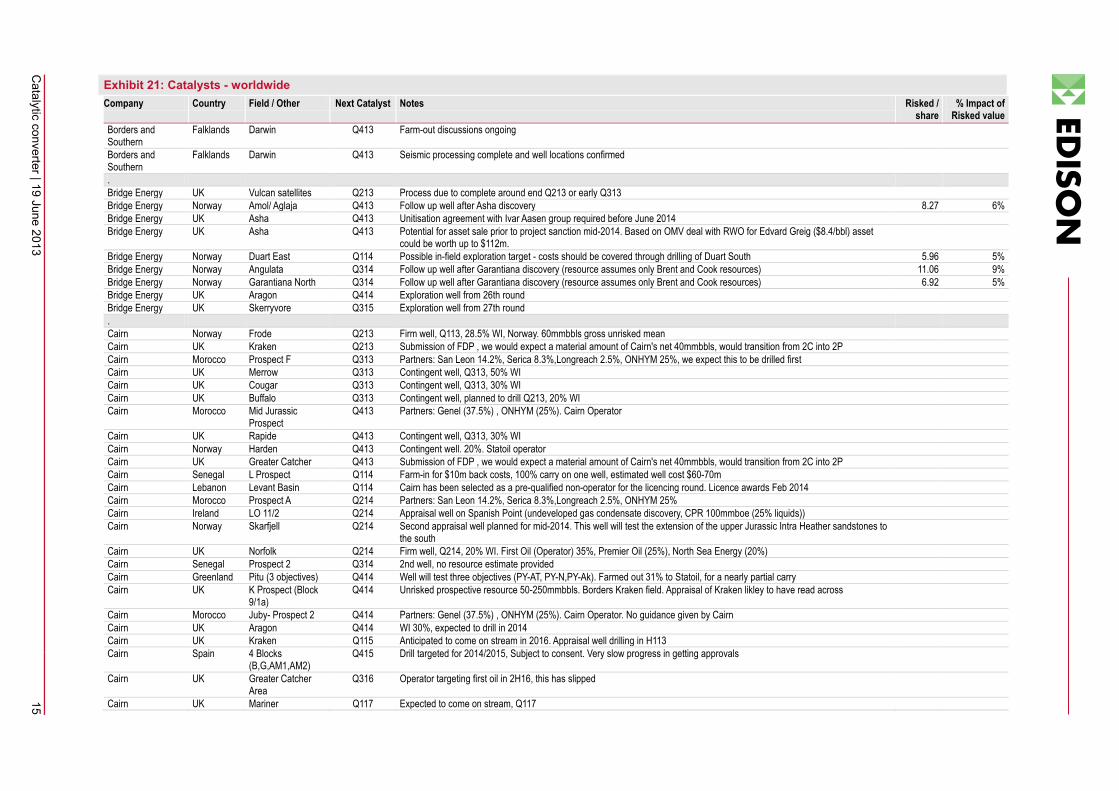

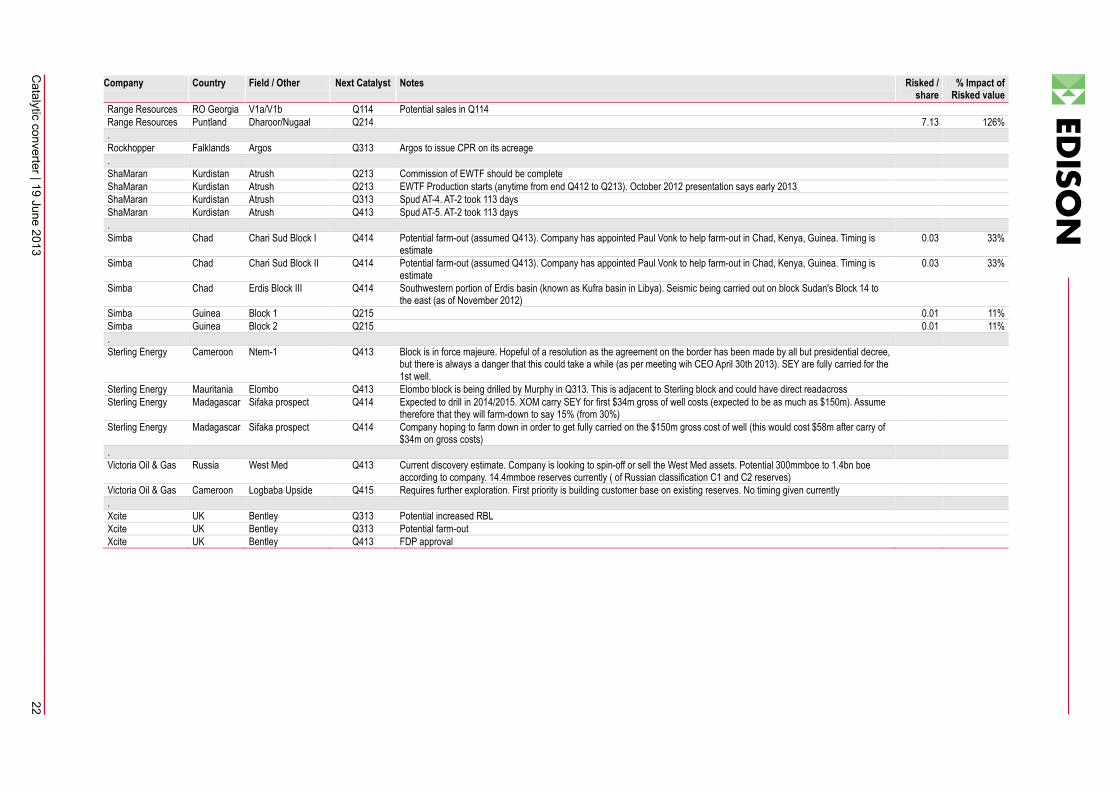

Exhibit 21: Catalysts - worldwide Company Country Field / Other Next Catalyst Notes Risked /

share % Impact of

Risked value Borders and Southern

Falklands Darwin Q413 Farm-out discussions ongoing

Borders and Southern

Falklands Darwin Q413 Seismic processing complete and well locations confirmed

. Bridge Energy UK Vulcan satellites Q213 Process due to complete around end Q213 or early Q313 Bridge Energy Norway Amol/ Aglaja Q413 Follow up well after Asha discovery 8.27 6% Bridge Energy UK Asha Q413 Unitisation agreement with Ivar Aasen group required before June 2014 Bridge Energy UK Asha Q413 Potential for asset sale prior to project sanction mid-2014. Based on OMV deal with RWO for Edvard Greig ($8.4/bbl) asset

could be worth up to $112m.

Bridge Energy Norway Duart East Q114 Possible in-field exploration target - costs should be covered through drilling of Duart South 5.96 5% Bridge Energy Norway Angulata Q314 Follow up well after Garantiana discovery (resource assumes only Brent and Cook resources) 11.06 9% Bridge Energy Norway Garantiana North Q314 Follow up well after Garantiana discovery (resource assumes only Brent and Cook resources) 6.92 5% Bridge Energy UK Aragon Q414 Exploration well from 26th round Bridge Energy UK Skerryvore Q315 Exploration well from 27th round . Cairn Norway Frode Q213 Firm well, Q113, 28.5% WI, Norway. 60mmbbls gross unrisked mean Cairn UK Kraken Q213 Submission of FDP , we would expect a material amount of Cairn's net 40mmbbls, would transition from 2C into 2P Cairn Morocco Prospect F Q313 Partners: San Leon 14.2%, Serica 8.3%,Longreach 2.5%, ONHYM 25%, we expect this to be drilled first Cairn UK Merrow Q313 Contingent well, Q313, 50% WI Cairn UK Cougar Q313 Contingent well, Q313, 30% WI Cairn UK Buffalo Q313 Contingent well, planned to drill Q213, 20% WI Cairn Morocco Mid Jurassic

Prospect Q413 Partners: Genel (37.5%) , ONHYM (25%). Cairn Operator

Cairn UK Rapide Q413 Contingent well, Q313, 30% WI Cairn Norway Harden Q413 Contingent well. 20%. Statoil operator Cairn UK Greater Catcher Q413 Submission of FDP , we would expect a material amount of Cairn's net 40mmbbls, would transition from 2C into 2P Cairn Senegal L Prospect Q114 Farm-in for $10m back costs, 100% carry on one well, estimated well cost $60-70m Cairn Lebanon Levant Basin Q114 Cairn has been selected as a pre-qualified non-operator for the licencing round. Licence awards Feb 2014 Cairn Morocco Prospect A Q214 Partners: San Leon 14.2%, Serica 8.3%,Longreach 2.5%, ONHYM 25% Cairn Ireland LO 11/2 Q214 Appraisal well on Spanish Point (undeveloped gas condensate discovery, CPR 100mmboe (25% liquids)) Cairn Norway Skarfjell Q214 Second appraisal well planned for mid-2014. This well will test the extension of the upper Jurassic Intra Heather sandstones to

the south

Cairn UK Norfolk Q214 Firm well, Q214, 20% WI. First Oil (Operator) 35%, Premier Oil (25%), North Sea Energy (20%) Cairn Senegal Prospect 2 Q314 2nd well, no resource estimate provided Cairn Greenland Pitu (3 objectives) Q414 Well will test three objectives (PY-AT, PY-N,PY-Ak). Farmed out 31% to Statoil, for a nearly partial carry Cairn UK K Prospect (Block

9/1a) Q414 Unrisked prospective resource 50-250mmbbls. Borders Kraken field. Appraisal of Kraken likley to have read across

Cairn Morocco Juby- Prospect 2 Q414 Partners: Genel (37.5%) , ONHYM (25%). Cairn Operator. No guidance given by Cairn Cairn UK Aragon Q414 WI 30%, expected to drill in 2014 Cairn UK Kraken Q115 Anticipated to come on stream in 2016. Appraisal well drilling in H113 Cairn Spain 4 Blocks

(B,G,AM1,AM2) Q415 Drill targeted for 2014/2015, Subject to consent. Very slow progress in getting approvals

Cairn UK Greater Catcher Area

Q316 Operator targeting first oil in 2H16, this has slipped

Cairn UK Mariner Q117 Expected to come on stream, Q117

Catalytic converter | 19 June 2013

16

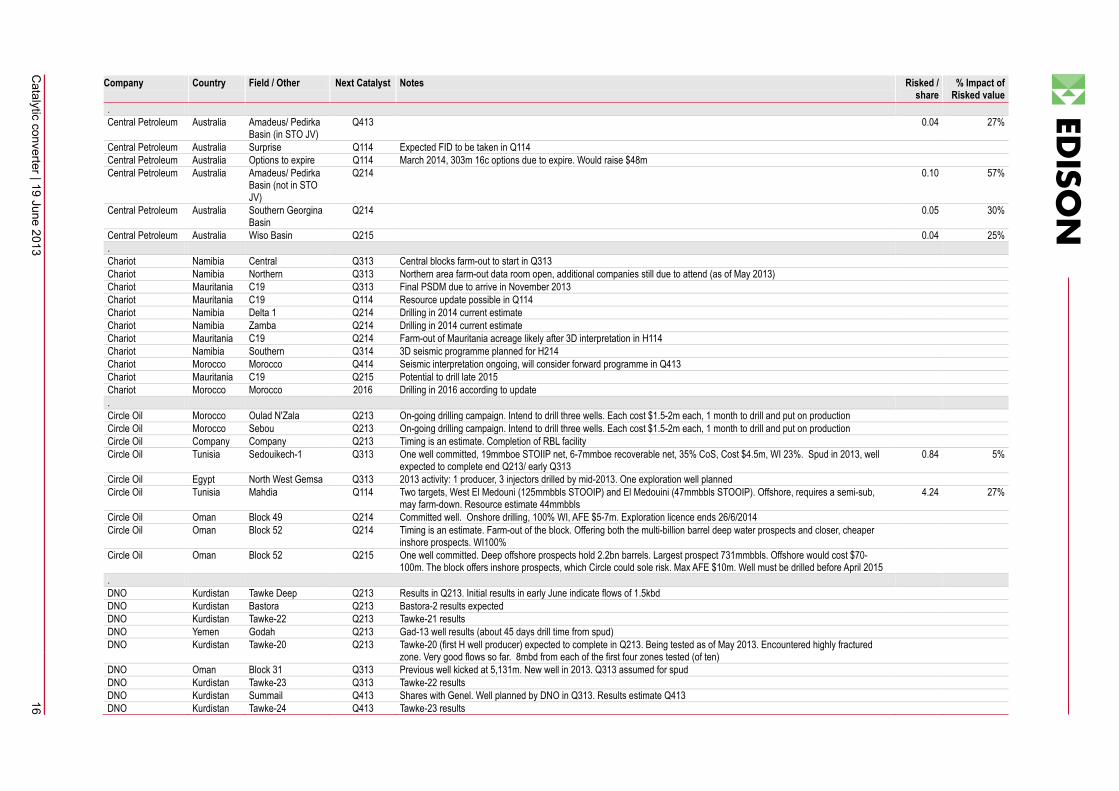

Company Country Field / Other Next Catalyst Notes Risked / share

% Impact of Risked value

. Central Petroleum Australia Amadeus/ Pedirka

Basin (in STO JV) Q413 0.04 27%

Central Petroleum Australia Surprise Q114 Expected FID to be taken in Q114 Central Petroleum Australia Options to expire Q114 March 2014, 303m 16c options due to expire. Would raise $48m Central Petroleum Australia Amadeus/ Pedirka

Basin (not in STO JV)

Q214 0.10 57%

Central Petroleum Australia Southern Georgina Basin

Q214 0.05 30%

Central Petroleum Australia Wiso Basin Q215 0.04 25% . Chariot Namibia Central Q313 Central blocks farm-out to start in Q313 Chariot Namibia Northern Q313 Northern area farm-out data room open, additional companies still due to attend (as of May 2013) Chariot Mauritania C19 Q313 Final PSDM due to arrive in November 2013 Chariot Mauritania C19 Q114 Resource update possible in Q114 Chariot Namibia Delta 1 Q214 Drilling in 2014 current estimate Chariot Namibia Zamba Q214 Drilling in 2014 current estimate Chariot Mauritania C19 Q214 Farm-out of Mauritania acreage likely after 3D interpretation in H114 Chariot Namibia Southern Q314 3D seismic programme planned for H214 Chariot Morocco Morocco Q414 Seismic interpretation ongoing, will consider forward programme in Q413 Chariot Mauritania C19 Q215 Potential to drill late 2015 Chariot Morocco Morocco 2016 Drilling in 2016 according to update . Circle Oil Morocco Oulad N'Zala Q213 On-going drilling campaign. Intend to drill three wells. Each cost $1.5-2m each, 1 month to drill and put on production Circle Oil Morocco Sebou Q213 On-going drilling campaign. Intend to drill three wells. Each cost $1.5-2m each, 1 month to drill and put on production Circle Oil Company Company Q213 Timing is an estimate. Completion of RBL facility Circle Oil Tunisia Sedouikech-1 Q313 One well committed, 19mmboe STOIIP net, 6-7mmboe recoverable net, 35% CoS, Cost $4.5m, WI 23%. Spud in 2013, well

expected to complete end Q213/ early Q313 0.84 5%

Circle Oil Egypt North West Gemsa Q313 2013 activity: 1 producer, 3 injectors drilled by mid-2013. One exploration well planned Circle Oil Tunisia Mahdia Q114 Two targets, West El Medouni (125mmbbls STOOIP) and El Medouini (47mmbbls STOOIP). Offshore, requires a semi-sub,

may farm-down. Resource estimate 44mmbbls 4.24 27%

Circle Oil Oman Block 49 Q214 Committed well. Onshore drilling, 100% WI, AFE $5-7m. Exploration licence ends 26/6/2014 Circle Oil Oman Block 52 Q214 Timing is an estimate. Farm-out of the block. Offering both the multi-billion barrel deep water prospects and closer, cheaper

inshore prospects. WI100%

Circle Oil Oman Block 52 Q215 One well committed. Deep offshore prospects hold 2.2bn barrels. Largest prospect 731mmbbls. Offshore would cost $70-100m. The block offers inshore prospects, which Circle could sole risk. Max AFE $10m. Well must be drilled before April 2015

. DNO Kurdistan Tawke Deep Q213 Results in Q213. Initial results in early June indicate flows of 1.5kbd DNO Kurdistan Bastora Q213 Bastora-2 results expected DNO Kurdistan Tawke-22 Q213 Tawke-21 results DNO Yemen Godah Q213 Gad-13 well results (about 45 days drill time from spud) DNO Kurdistan Tawke-20 Q213 Tawke-20 (first H well producer) expected to complete in Q213. Being tested as of May 2013. Encountered highly fractured

zone. Very good flows so far. 8mbd from each of the first four zones tested (of ten)

DNO Oman Block 31 Q313 Previous well kicked at 5,131m. New well in 2013. Q313 assumed for spud DNO Kurdistan Tawke-23 Q313 Tawke-22 results DNO Kurdistan Summail Q413 Shares with Genel. Well planned by DNO in Q313. Results estimate Q413 DNO Kurdistan Tawke-24 Q413 Tawke-23 results

Catalytic converter | 19 June 2013

17

Company Country Field / Other Next Catalyst Notes Risked / share

% Impact of Risked value

DNO Kurdistan Erbil - Bastora 3 Q413 Bastora-3 results DNO Kurdistan Dohuk - Summail Q413 Summail-2 results DNO Kurdistan Dohuk - Summail Q413 Summail Gas development to be approved in 2013 DNO Kurdistan Erbil - Bastora 4 Q114 Bastora-4 results DNO Kurdistan Tawke Q414 Production, processing and infrastructure capacity 200kbd by December 2014 . Egdon Resources UK PEDL201 Q213 Shallow well, 1000m, test 2 targets. 3.8mmbbls mean prospective. Commence drilling Q213, subject to consent and planning 4.97 62% Egdon Resources UK Wressle Q213 1.89 24% Egdon Resources UK PEDL253 Q114 17.81mmbbls, mean prospective. Drilling expected to commence Q413/Q114. Subject to planning and other consent 16.18 202% Egdon Resources UK PEDL241 Q114 6.7mmbbls. 3 objectives. Drilling expected to commence Q413/Q114. Subject to planning and other consent 7.34 92% . Falkland Oil and Gas

Falklands Northern area seismic

Q413 3D seismic capture over Hersilia starts

Falkland Oil and Gas

Falklands Rig contract Q413 Rig contract expected to be signed for 3/4 well campaign starting late 2014/ 2015

Falkland Oil and Gas

Falklands Diomedea/ fault block well locations

Q214 Selection of drill targets for Diomedea and fault block wells

Falkland Oil and Gas

Falklands Diomedea Q414 Next exploration well not likely to be drilled until Q414 at earliest

Falkland Oil and Gas

Falklands Hersilia/ Loligo well locations

Q414 Selection of drill targets for Hersilia and Loligo

. Genel Kurdistan Chia Surkh Q213 Chia Surkh -10 flowed at (11.95+3.2)kbd and (15+8)mmscfd. Suspended as future producer Genel Kurdistan Miran 4 Q213 Miran East west result Q213 possible. This is a step out from Miran structure Genel Kurdistan Tawke Deep Q213 Tawke - 17: Results in Q213 Genel Kurdistan Kewa Chirmila (Taq

Taq) Q213 Result Q213

Genel Kurdistan Miran Q213 Miran-4 (was Miran East 1) test results Genel Kurdistan Company Q213 First Phase of export pipeline operational Genel Kurdistan Bina Bawi Q213 Bina Bawi-4 results expected. Testing Jurassic, Triassic and Permian (TD 4,200m). Mid way between crest and potential edge

of structure. PERMIAN drilling - could add to resources

Genel Kurdistan Bina Bawi Q213 Bina Bawi-5 results expected, testing Jurassic and Triassic (TD 2,400m). North west end of field, testing closure. Would secure NW area for inclusion into future production licence

Genel Kurdistan Chia Surkh Q213 Chai Surkh-10 results Genel Kurdistan Miran Q213 Miran-5 results Genel Kurdistan Miran Q213 Petrofac to complete FEED for Miran gas development by Q213 (from January pres) Genel Kurdistan Miran Q213 Gas sales agreements with customers and infrastructures expected Genel Kurdistan Ber Bahr Q313 A 300m oil column was found on the first well in Q412, but no oil flowed. The company plans to sidetrack the well in Q213, but

seems to be being sidelined and not a priority for Genel.

Genel Kurdistan Taq Taq Deep Q413 Results expected Q313 Genel Kurdistan Ber Bahr extn Q413 A 300m oil column was found on the first well in Q412, but no oil flowed. The company plans to sidetrack the well in Q213, but

seems to be being sidelined and not a priority for Genel.

Genel Kurdistan Sommail Q413 3D processing ongoing. Erbil to Dohuk gas pipeline due to be completed in Q113. Genel has no plans - DNO (op) has a well spudding at Summail in Q313

Genel Kurdistan Chia Surkh-11 Q413 Due to spud in Q2 and results in Q4 Genel Kurdistan Chia Surkh-11 Q413 Chia Surkh-11 results Genel Kurdistan Miran Q413 FID Miran gas development Genel Malta Malta Q413 First Malta well spuds. Genel will carry First well and some of second well up to $30m (well expected to cost $45-50m)

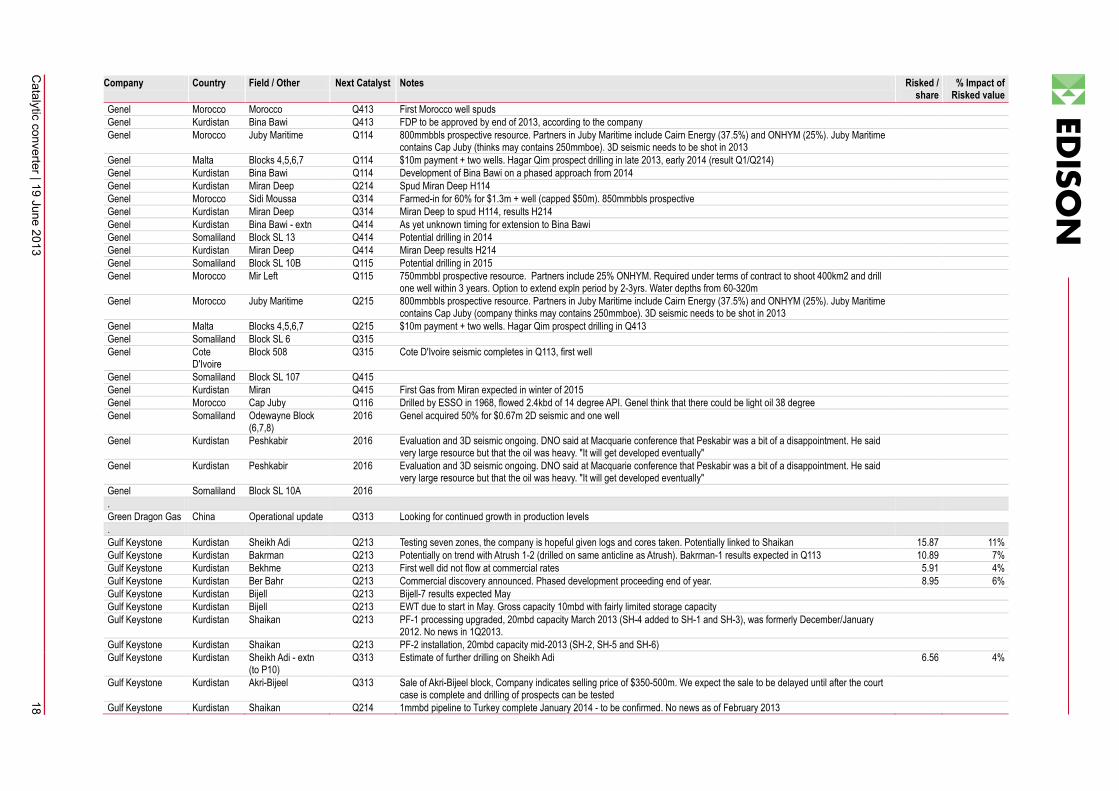

Catalytic converter | 19 June 2013

18

Company Country Field / Other Next Catalyst Notes Risked / share

% Impact of Risked value

Genel Morocco Morocco Q413 First Morocco well spuds Genel Kurdistan Bina Bawi Q413 FDP to be approved by end of 2013, according to the company Genel Morocco Juby Maritime Q114 800mmbbls prospective resource. Partners in Juby Maritime include Cairn Energy (37.5%) and ONHYM (25%). Juby Maritime

contains Cap Juby (thinks may contains 250mmboe). 3D seismic needs to be shot in 2013

Genel Malta Blocks 4,5,6,7 Q114 $10m payment + two wells. Hagar Qim prospect drilling in late 2013, early 2014 (result Q1/Q214) Genel Kurdistan Bina Bawi Q114 Development of Bina Bawi on a phased approach from 2014 Genel Kurdistan Miran Deep Q214 Spud Miran Deep H114 Genel Morocco Sidi Moussa Q314 Farmed-in for 60% for $1.3m + well (capped $50m). 850mmbbls prospective Genel Kurdistan Miran Deep Q314 Miran Deep to spud H114, results H214 Genel Kurdistan Bina Bawi - extn Q414 As yet unknown timing for extension to Bina Bawi Genel Somaliland Block SL 13 Q414 Potential drilling in 2014 Genel Kurdistan Miran Deep Q414 Miran Deep results H214 Genel Somaliland Block SL 10B Q115 Potential drilling in 2015 Genel Morocco Mir Left Q115 750mmbbl prospective resource. Partners include 25% ONHYM. Required under terms of contract to shoot 400km2 and drill

one well within 3 years. Option to extend expln period by 2-3yrs. Water depths from 60-320m

Genel Morocco Juby Maritime Q215 800mmbbls prospective resource. Partners in Juby Maritime include Cairn Energy (37.5%) and ONHYM (25%). Juby Maritime contains Cap Juby (company thinks may contains 250mmboe). 3D seismic needs to be shot in 2013

Genel Malta Blocks 4,5,6,7 Q215 $10m payment + two wells. Hagar Qim prospect drilling in Q413 Genel Somaliland Block SL 6 Q315 Genel Cote

D'Ivoire Block 508 Q315 Cote D'Ivoire seismic completes in Q113, first well

Genel Somaliland Block SL 107 Q415 Genel Kurdistan Miran Q415 First Gas from Miran expected in winter of 2015 Genel Morocco Cap Juby Q116 Drilled by ESSO in 1968, flowed 2.4kbd of 14 degree API. Genel think that there could be light oil 38 degree Genel Somaliland Odewayne Block

(6,7,8) 2016 Genel acquired 50% for $0.67m 2D seismic and one well

Genel Kurdistan Peshkabir 2016 Evaluation and 3D seismic ongoing. DNO said at Macquarie conference that Peskabir was a bit of a disappointment. He said very large resource but that the oil was heavy. "It will get developed eventually"

Genel Kurdistan Peshkabir 2016 Evaluation and 3D seismic ongoing. DNO said at Macquarie conference that Peskabir was a bit of a disappointment. He said very large resource but that the oil was heavy. "It will get developed eventually"

Genel Somaliland Block SL 10A 2016 . Green Dragon Gas China Operational update Q313 Looking for continued growth in production levels . Gulf Keystone Kurdistan Sheikh Adi Q213 Testing seven zones, the company is hopeful given logs and cores taken. Potentially linked to Shaikan 15.87 11% Gulf Keystone Kurdistan Bakrman Q213 Potentially on trend with Atrush 1-2 (drilled on same anticline as Atrush). Bakrman-1 results expected in Q113 10.89 7% Gulf Keystone Kurdistan Bekhme Q213 First well did not flow at commercial rates 5.91 4% Gulf Keystone Kurdistan Ber Bahr Q213 Commercial discovery announced. Phased development proceeding end of year. 8.95 6% Gulf Keystone Kurdistan Bijell Q213 Bijell-7 results expected May Gulf Keystone Kurdistan Bijell Q213 EWT due to start in May. Gross capacity 10mbd with fairly limited storage capacity Gulf Keystone Kurdistan Shaikan Q213 PF-1 processing upgraded, 20mbd capacity March 2013 (SH-4 added to SH-1 and SH-3), was formerly December/January

2012. No news in 1Q2013.

Gulf Keystone Kurdistan Shaikan Q213 PF-2 installation, 20mbd capacity mid-2013 (SH-2, SH-5 and SH-6) Gulf Keystone Kurdistan Sheikh Adi - extn

(to P10) Q313 Estimate of further drilling on Sheikh Adi 6.56 4%

Gulf Keystone Kurdistan Akri-Bijeel Q313 Sale of Akri-Bijeel block, Company indicates selling price of $350-500m. We expect the sale to be delayed until after the court case is complete and drilling of prospects can be tested

Gulf Keystone Kurdistan Shaikan Q214 1mmbd pipeline to Turkey complete January 2014 - to be confirmed. No news as of February 2013

Catalytic converter | 19 June 2013

19

Company Country Field / Other Next Catalyst Notes Risked / share

% Impact of Risked value

Gulf Keystone Kurdistan Shaikan Q214 440mbd pipeline from Shaikan due for completion - to be confirmed. No news on plans as of February 2013, therefore expected 2014. Crucial for production

Gulf Keystone Kurdistan Company 2014 Plan to list on FTSE main list. Given the Excalibur court case, we expect this to be in 2014 at earliest . Gulfsands Morocco Rharb Q413 Gas production to start Q3/Q413 20.25 18% Gulfsands Tunisia Dougga West Q114 Exploration well spud (Committed well, farm-out required). Likely to be Dougga West 11.55 10% Gulfsands Morocco Fes Well 1 Q314 Exploration well spud. Deep wells, expected to cost $7m gross. WI 50% 29.79 26% Gulfsands Tunisia Chorbane Q414 Exploration well spud 2.60 2% Gulfsands Colombia Llanos-50 Q115 Exploration well spud (contingent on seismic result) Gulfsands Morocco Fes Well 2 Q215 Exploration well spud. Deep wells, expected to cost $7m gross. WI 50% Gulfsands Colombia Putumayo-14 Q215 Exploration well spud (contingent on seismic result) Gulfsands Morocco Fes Well 3 Q315 Exploration well spud. Deep wells, expected to cost $7m gross. WI 50% . Hawkley Ukraine Lower B18 work

over Q313 Rig due mid-June to prepare well bore for flow testing of lower B18 at #202 well

. Karoon Australia Proteus-1 Q213 14km SE of Poseidon Karoon Australia 3D Seismic

interpretation 2013 Throughout 2013

Karoon Australia 3D Seismic interpretation

2013 Start Q213 end Q214

Karoon Peru 3D Interpretation 2013 Throughout year Karoon Peru Prospects Q313 Sixteen prospects and leads identified (net unrisked mean 1.92bn boe). Implies average mean prospect is 120mboe.

Three wells to be drilled in 2013

Karoon Australia Processing 3D Seismic data

Q313 Start Q213 end Q313

Karoon Peru Drilling - planning & approvals

Q313 End Q313

Karoon Peru New 2D Seismic acquisition

Q313 Throughout the quarter

Karoon Brazil SM 1101 (Kangaroo)

Q413 Second well expected Q413 / Q115

Karoon Peru Drilling Q413 One well result expected Q413 Karoon Peru Interpretation Q413 Throughout the quarter Karoon Brazil SM 1166 (Bilby-1) Q114 Second well expected Q413 / Q115 Karoon Peru Drilling - planning &

approvals 2014 Throughout year

Karoon Brazil SM 1101 (Wallaby) Q414 A prospect of similar Eocene type to Kangaroo discovery (but to the west), of a similar size. Therefore adding to the prospect list, even though not in company presentation. Unsure of drilling timetable, so assumed 4Q414

Karoon Australia Well option Q414 Potential well option in late 2014. Seismic required first (2013) Karoon Peru Drilling 2015 No drilling planned in 2014, assumed 2015 . Madagascar Madagascar Tsimiroro

delineation Q213

Madagascar Madagascar Bemolanga conventional

Q213

Madagascar Madagascar Tsimiroro Q213 Continuous steam injection to start Madagascar Madagascar Tsimiroro Q313 Resource report on Tsimoro expect early 2013, after delinieation drilling in 2012 and 2011

Catalytic converter | 19 June 2013

20

Company Country Field / Other Next Catalyst Notes Risked / share

% Impact of Risked value

Madagascar Madagascar Tsimiroro Q313 Fugro report for conventional targets following AGG expected 4Q2012 Madagascar Madagascar Tsimiroro

Prospective 2014 25.05 167%

Madagascar Madagascar Manambolo 2014 Madagascar Madagascar Morondava 2014 Madagascar Madagascar Manandaza 2014 . Nido Philippines Galoc Exploration

Area Q213 Galoc North drilling decision to be made

Nido Philippines West Linapacan A 2013 Drilling phase 2013 Nido Philippines Galoc Phase II Q313 First Oil expected Nido Philippines Nido 1x1 Q313 Indicative first drilling H213 subject to agreement with SC14A partners Nido Philippines Exploration

prospect Q413 Exploration well commitment by November 2013, 676 mmbbl OIP Baragatan prospect approved as target

Nido Philippines Exploration prospect

Q114 Exploration well commitment by Jan 2014, JV election to drill decision now extended to Jan 2014

Nido Philippines West Linapacan A 2014 First Oil expected 2014 . Petroceltic Romania Est Cobalcesu-

South-1 Q313 Two months to drill

Petroceltic Kurdistan Shakrok-1 Q413 Seismic ongoing in late 2012, hope to drill 1 well in block in Q313. Results Q114 Petroceltic Italy Carpignano Seisa-1

(contingent) Q413 Eni lodged further extension application until 30 June 2013 to allow revised well location

Petroceltic Italy B.R272.EL Q413 Awarded in April 2013. Six year initial period 3D seismic Petroceltic Romania Muridava-A Q413 Petroceltic Italy Carpignano Sesia

(Rovasenda) Q413 Farm-out of Carpignano Sesia potential

Petroceltic Kurdistan Pelewan Q413 Petroceltic Kurdistan Shireen-1 Q114 Seismic ongoing in late 2012, hope to drill 1 well in block in Q313. Results Q114 Petroceltic Kurdistan Chinara Q114 Petroceltic Italy Elsa-2 (contingent) Q214 Petroceltic Romania Muridava-B Q214 Petroceltic Romania Est Cobalcescu-C Q314 Petroceltic Romania Muridava-C Q314 Petroceltic Romania Est Cobalcescu-B Q414 Petroceltic Kurdistan Bradost Q115 . Po Valley Italy Gradizza Q313 Spud late June/ early July 2013 with partial carry on well costs. 20 day drill 0.01 9% Po Valley Italy Canolo & Zini Q413 First well expected Q413 subject to necessary authorisations. 0.05 42% Po Valley Italy Bezzecca Q413 Final approval expected following EIA Po Valley Italy Carola Irma Q413 Final approval expected following EIA Po Valley Italy La Risorta Q414 Preliminarily granted, TD 2100m 0.15 127% Po Valley Italy Fantuzza Q414 0.03 24% . Premier Oil Falklands Sea Lion Q213 Concept select stage gate expected during Q213 Premier Oil Norway Bream Q313 Project sanction targeted for Q313 (but was H212 as recently as May 2012). Tullow say "Licence extension pending.

Development plan due to be submitted in December 2013. Leased FPSO development scheme currently envisaged. Up to five producers and two water injectors currently planned"

0.01 0%

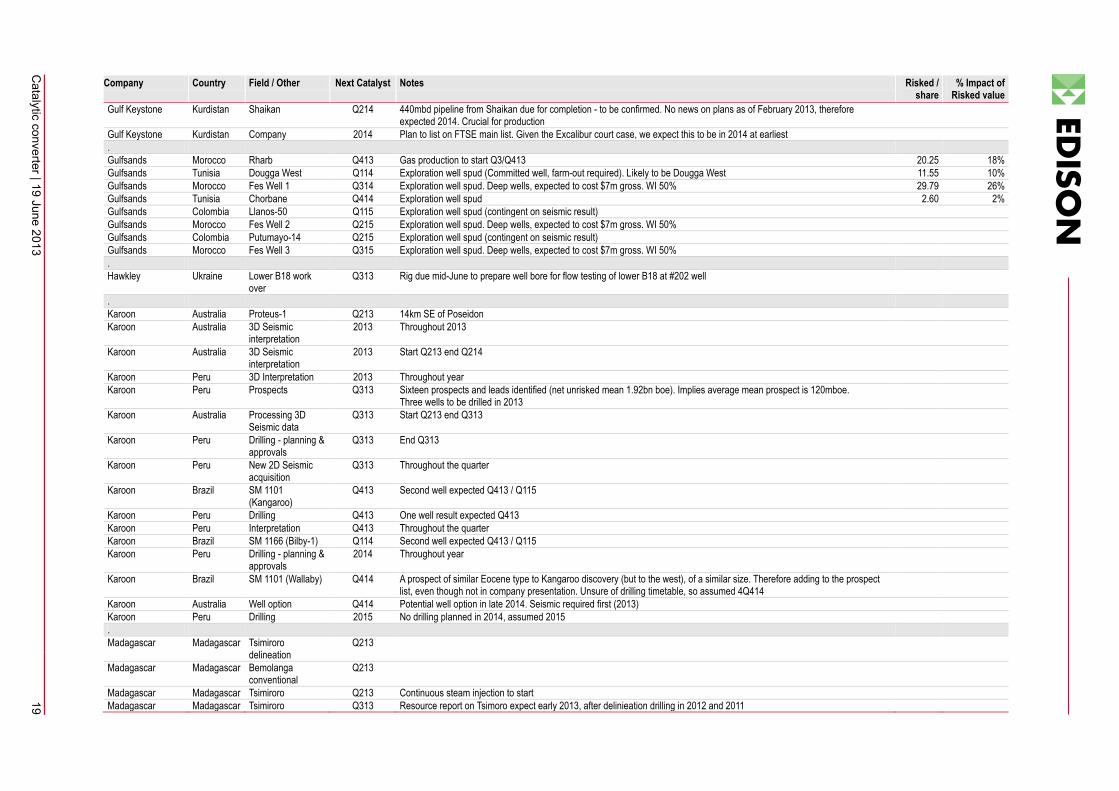

Catalytic converter | 19 June 2013

21

Company Country Field / Other Next Catalyst Notes Risked / share

% Impact of Risked value

Premier Oil Vietnam Ca Voi Q313 High risk Oligocene target with multiple follow up potential Premier Oil UK Lacewing Q313 HPHT high impact, high risk well. Part carried by ConocoPhilips following 37.3% farm-down. Spud Q213, results expected

Q313

Premier Oil Vietnam Ca Duc Q313 High risk prospect, due to spud Q213 Premier Oil Pakistan Badhra South

Deepening-1 Q313

Premier Oil Pakistan Badhra-6 Parh Q313 Premier Oil Kenya 3D seismic

interpretation Q313 2,280 km2 being acquired over L10A and L10B blocks

Premier Oil Norway Bream Q313 Project sanction targeted for Q313 (but was H212 as recently as May 2012). Tullow say "Licence extension pending. Development plan due to be submitted in Dec 2013. Leased FPSO development scheme currently envisaged. Up to five producers and two water injectors currently planned"

Premier Oil Pakistan K-36 Q413 Premier Oil Mauritania Tapendar Q413 First of two commitment wells to be drilled in a three year period starting from January 2012 Premier Oil Indonesia Kuda Laut & Singa

Laut (2 wells) Q114 Low risk gas well but high risk for commercial oil upside. Well due to spud Q413

Premier Oil Kenya Exploration well Q114 Well subject to 2013 seismic interpretation Premier Oil Falklands Sea Lion Q214 Project sanction expected around mid-2014 0.53 0% Premier Oil Falklands Sea Lion Q214 Project sanction expected around mid-2014 . President Argentina Ponzo Escondido Q313 Commencing April 2013. Fracture 3 wells in Ponzo Escondido and Dos Puntitas. Success would transform field production and

resources into reserves

President Argentina Dos Puntitas Q313 Commencing April 2013. Fracture 3 wells in Ponzo Escondido and Dos Puntitas. Success would transform field production and resources into reserves

President Argentina Puesto Guardian block

Q313 CPR expected in July after the fracks in Q213 on Puesto Guardian fields

President Argentina Puesto Guardian block

Q313 Future development plan expected in July after interpretation of frack results

President Paraguay Pirity Q413 D&M do CPR on seismic within 2 months of seismic. Results expected latter half of Q413, according to April press release. President Paraguay Pirity Q214 Right on border with Argentina. Argentinian side have producing wells and fields. 4 way dip closures 36.94 176% President Argentina Martinez del Tineo -

Palaeozoic Q214 To be drilled mid 2014. Significant gas condensate prospect and play opener. Conventional palaeozoic, analogous to

producing fields in Argentina and Bolivia 10.43 50%

President Argentina Dos Puntitas 2013/2014 Fracking in Q213, with possible results in Q213 5.04 24% President Argentina Pozo Escondido 2013/2014 PE-1001 3.02 14% President Argentina Martinez del Tineo -

Shallow 2013/2014 2.39 11%

President Argentina Pozo Escondido Este

2013/2014 PEE-1001 Completion & Perf 1.94 9%

President Argentina Puesto Guardian 2013/2014 PG-13 Workover 0.34 2% President Paraguay Demattei Q115 Adjacent to Pirity, no current plans to drill. Contingent on results at Pirity? President Argentina Limestone fracks 2014/2015 2015 event President Argentina Matorras 2014/2015 Tested by YPF in 1970/80s, minor cretaceous play, potential Palaeozoic play President Argentina El Ocultar 2014/2015 Awarded Aug 2012, small scale cretaceous potential . Pura Vida Morocco Toubkal-1 Q114 Toubkal-1 well, targeting 1.5bn bbls, WI 23% 16.93 2472% Pura Vida Morocco Toubkal-2 Q314 Second well on the block 2.41 352% . Range Resources RO Georgia V1a/V1b Q313 3 well programme starts in H113. Range 40% WI and targeting 615mmboe gross recoverable 1.22 22%

Catalytic converter | 19 June 2013

22

Company Country Field / Other Next Catalyst Notes Risked / share

% Impact of Risked value

Range Resources RO Georgia V1a/V1b Q114 Potential sales in Q114 Range Resources Puntland Dharoor/Nugaal Q214 7.13 126% . Rockhopper Falklands Argos Q313 Argos to issue CPR on its acreage . ShaMaran Kurdistan Atrush Q213 Commission of EWTF should be complete ShaMaran Kurdistan Atrush Q213 EWTF Production starts (anytime from end Q412 to Q213). October 2012 presentation says early 2013 ShaMaran Kurdistan Atrush Q313 Spud AT-4. AT-2 took 113 days ShaMaran Kurdistan Atrush Q413 Spud AT-5. AT-2 took 113 days . Simba Chad Chari Sud Block I Q414 Potential farm-out (assumed Q413). Company has appointed Paul Vonk to help farm-out in Chad, Kenya, Guinea. Timing is

estimate 0.03 33%

Simba Chad Chari Sud Block II Q414 Potential farm-out (assumed Q413). Company has appointed Paul Vonk to help farm-out in Chad, Kenya, Guinea. Timing is estimate

0.03 33%

Simba Chad Erdis Block III Q414 Southwestern portion of Erdis basin (known as Kufra basin in Libya). Seismic being carried out on block Sudan's Block 14 to the east (as of November 2012)

Simba Guinea Block 1 Q215 0.01 11% Simba Guinea Block 2 Q215 0.01 11% . Sterling Energy Cameroon Ntem-1 Q413 Block is in force majeure. Hopeful of a resolution as the agreement on the border has been made by all but presidential decree,

but there is always a danger that this could take a while (as per meeting wih CEO April 30th 2013). SEY are fully carried for the 1st well.

Sterling Energy Mauritania Elombo Q413 Elombo block is being drilled by Murphy in Q313. This is adjacent to Sterling block and could have direct readacross Sterling Energy Madagascar Sifaka prospect Q414 Expected to drill in 2014/2015. XOM carry SEY for first $34m gross of well costs (expected to be as much as $150m). Assume

therefore that they will farm-down to say 15% (from 30%)

Sterling Energy Madagascar Sifaka prospect Q414 Company hoping to farm down in order to get fully carried on the $150m gross cost of well (this would cost $58m after carry of $34m on gross costs)

. Victoria Oil & Gas Russia West Med Q413 Current discovery estimate. Company is looking to spin-off or sell the West Med assets. Potential 300mmboe to 1.4bn boe

according to company. 14.4mmboe reserves currently ( of Russian classification C1 and C2 reserves)

Victoria Oil & Gas Cameroon Logbaba Upside Q415 Requires further exploration. First priority is building customer base on existing reserves. No timing given currently . Xcite UK Bentley Q313 Potential increased RBL Xcite UK Bentley Q313 Potential farm-out Xcite UK Bentley Q413 FDP approval

Catalytic converter | 19 June 2013

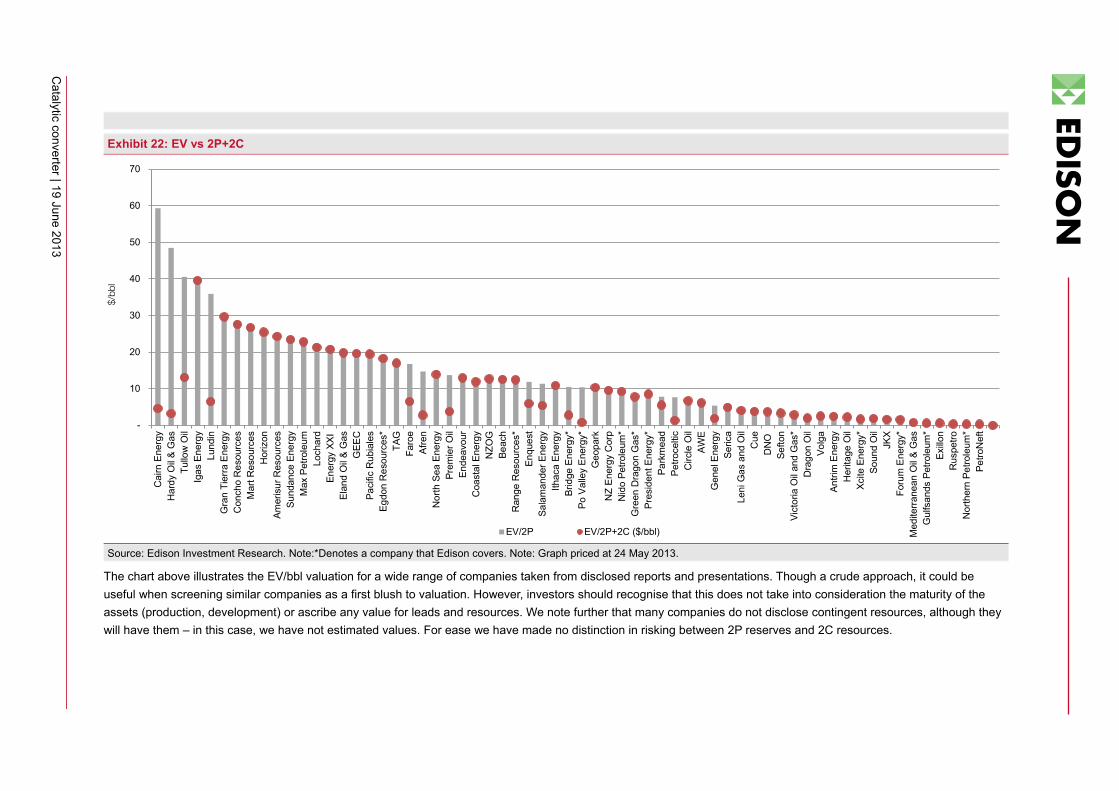

Exhibit 22: EV vs 2P+2C

Source: Edison Investment Research. Note:*Denotes a company that Edison covers. Note: Graph priced at 24 May 2013.

The chart above illustrates the EV/bbl valuation for a wide range of companies taken from disclosed reports and presentations. Though a crude approach, it could be useful when screening similar companies as a first blush to valuation. However, investors should recognise that this does not take into consideration the maturity of the assets (production, development) or ascribe any value for leads and resources. We note further that many companies do not disclose contingent resources, although they will have them – in this case, we have not estimated values. For ease we have made no distinction in risking between 2P reserves and 2C resources.

-

10

20

30

40

50

60

70C

airn

Ene

rgy

Har

dy O

il &

Gas

Tullo

w O

ilIg

as E

nerg

yLu

ndin

Gra

n Ti

erra

Ene

rgy

Con

cho

Res

ourc

esM

art R

esou

rces

Hor

izon

Amer

isur

Res

ourc

esSu

ndan

ce E

nerg

yM

ax P

etro

leum

Loch

ard

Ener

gy X

XI

Elan

d O

il &

Gas

GEE

CPa

cific

Rub

iale

sEg

don

Res

ourc

es*

TAG

Faro

eAf

ren

Nor

th S

ea E

nerg

yPr

emie

r Oil

Ende

avou

rC

oast

al E

nerg

yN

ZOG

Beac

hR

ange

Res

ourc

es*

Enqu

est

Sala

man

der E

nerg

yIth

aca

Ene

rgy

Brid

ge E

nerg

y*Po

Val

ley

Ene

rgy*

Geo

park

NZ

Ene

rgy

Cor

pN

ido

Petro

leum

*G

reen

Dra

gon

Gas

*Pr

esid

ent E

nerg

y*Pa

rkm

ead

Petro

celti

cC

ircle

Oil

AWE

Gen

el E

nerg

ySe

rica

Leni

Gas

and

Oil

Cue

DN

OSe

fton

Vict

oria

Oil

and

Gas

*D

rago

n O

ilVo

lga

Antri

m E

nerg

yH

erita

ge O

ilXc

ite E

nerg

y*So

und

Oil

JKX

Foru

m E

nerg

y*M

edite

rran

ean

Oil

& G

asG

ulfs

ands

Pet

role

um*

Exillo

nR

uspe

troN

orth

ern

Petro

leum

*Pe

troN

eft

$/bb

l

EV/2P EV/2P+2C ($/bbl)

Catalytic converter | 19 June 2013 24

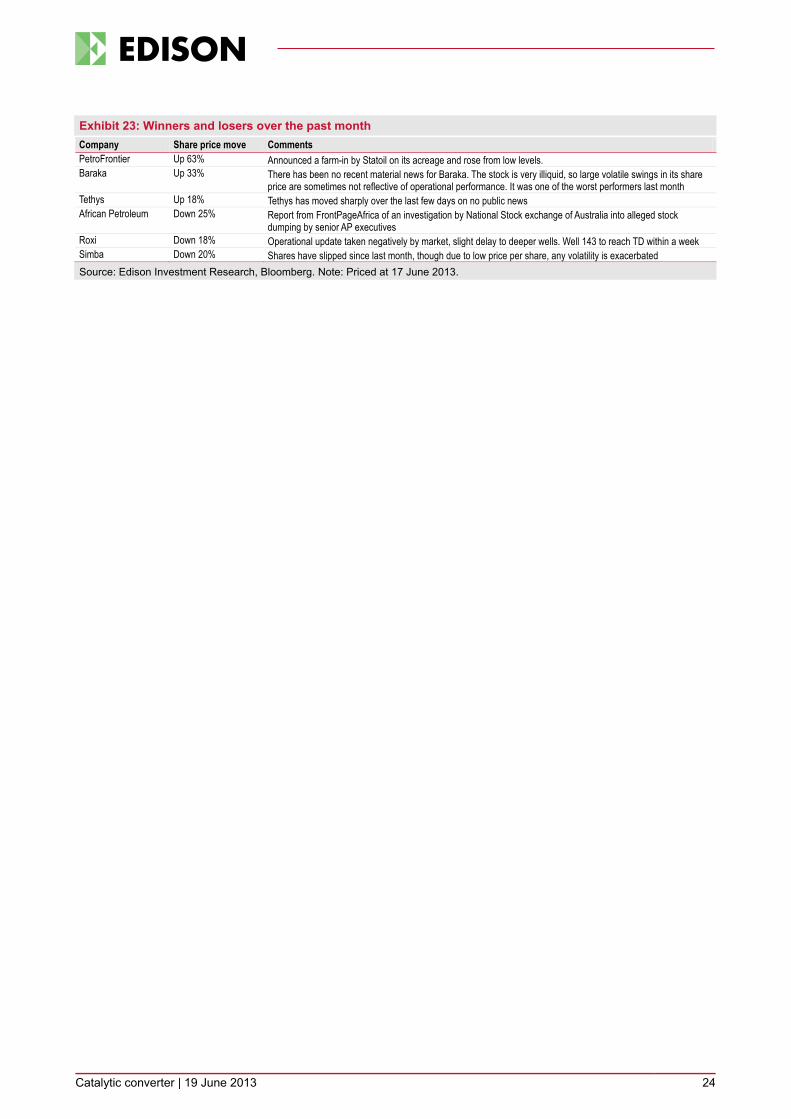

Exhibit 23: Winners and losers over the past month Company Share price move Comments PetroFrontier Up 63% Announced a farm-in by Statoil on its acreage and rose from low levels. Baraka Up 33% There has been no recent material news for Baraka. The stock is very illiquid, so large volatile swings in its share

price are sometimes not reflective of operational performance. It was one of the worst performers last month Tethys Up 18% Tethys has moved sharply over the last few days on no public news African Petroleum Down 25% Report from FrontPageAfrica of an investigation by National Stock exchange of Australia into alleged stock

dumping by senior AP executives Roxi Down 18% Operational update taken negatively by market, slight delay to deeper wells. Well 143 to reach TD within a week Simba Down 20% Shares have slipped since last month, though due to low price per share, any volatility is exacerbated Source: Edison Investment Research, Bloomberg. Note: Priced at 17 June 2013.

Catalytic converter | 19 June 2013 25

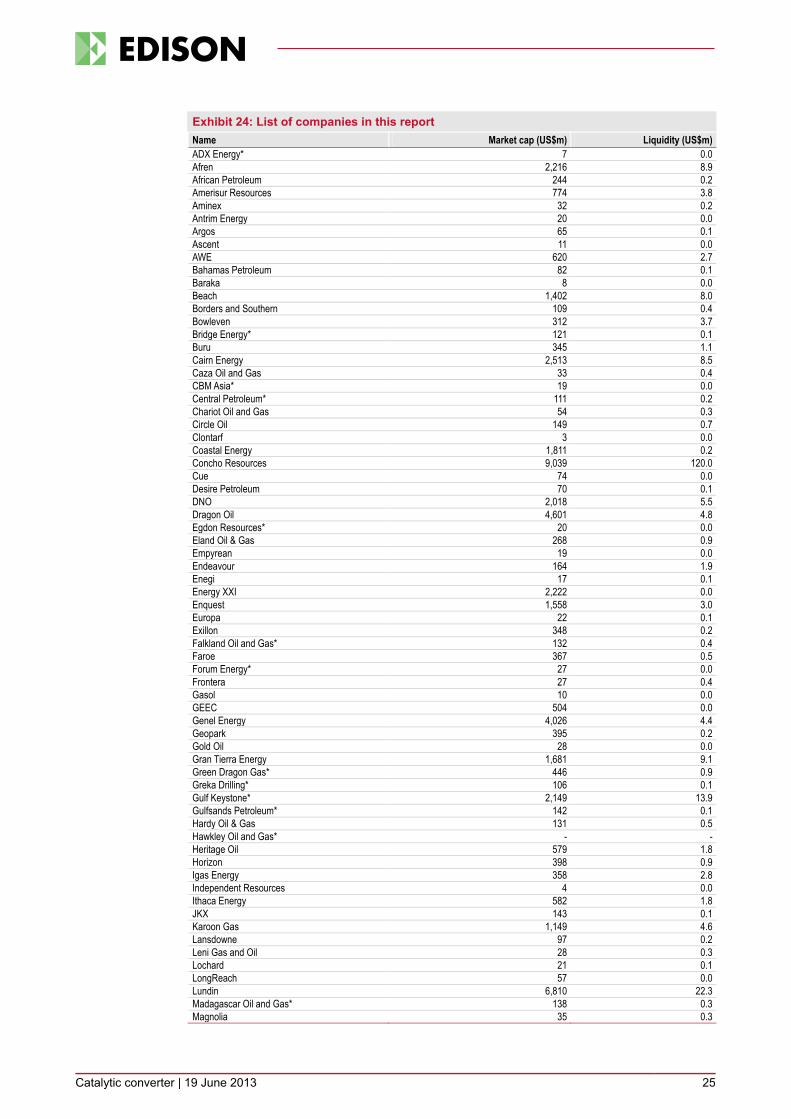

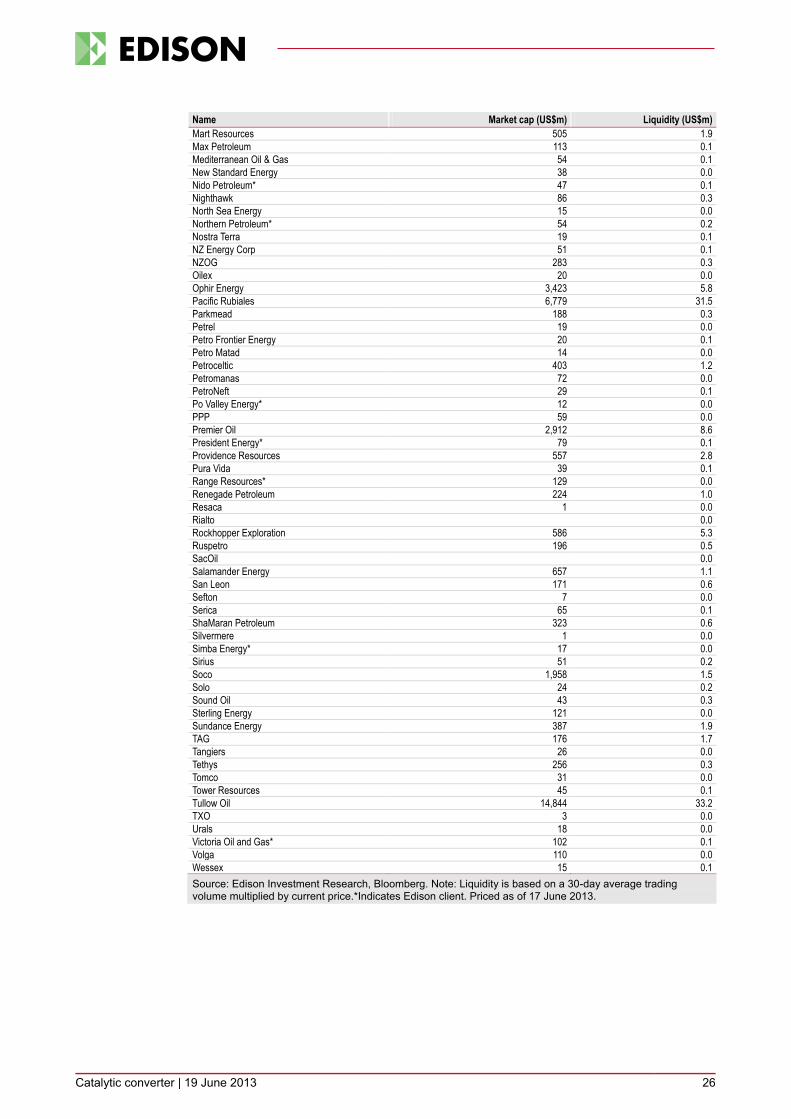

Exhibit 24: List of companies in this report Name Market cap (US$m) Liquidity (US$m) ADX Energy* 7 0.0 Afren 2,216 8.9 African Petroleum 244 0.2 Amerisur Resources 774 3.8 Aminex 32 0.2 Antrim Energy 20 0.0 Argos 65 0.1 Ascent 11 0.0 AWE 620 2.7 Bahamas Petroleum 82 0.1 Baraka 8 0.0 Beach 1,402 8.0 Borders and Southern 109 0.4 Bowleven 312 3.7 Bridge Energy* 121 0.1 Buru 345 1.1 Cairn Energy 2,513 8.5 Caza Oil and Gas 33 0.4 CBM Asia* 19 0.0 Central Petroleum* 111 0.2 Chariot Oil and Gas 54 0.3 Circle Oil 149 0.7 Clontarf 3 0.0 Coastal Energy 1,811 0.2 Concho Resources 9,039 120.0 Cue 74 0.0 Desire Petroleum 70 0.1 DNO 2,018 5.5 Dragon Oil 4,601 4.8 Egdon Resources* 20 0.0 Eland Oil & Gas 268 0.9 Empyrean 19 0.0 Endeavour 164 1.9 Enegi 17 0.1 Energy XXI 2,222 0.0 Enquest 1,558 3.0 Europa 22 0.1 Exillon 348 0.2 Falkland Oil and Gas* 132 0.4 Faroe 367 0.5 Forum Energy* 27 0.0 Frontera 27 0.4 Gasol 10 0.0 GEEC 504 0.0 Genel Energy 4,026 4.4 Geopark 395 0.2 Gold Oil 28 0.0 Gran Tierra Energy 1,681 9.1 Green Dragon Gas* 446 0.9 Greka Drilling* 106 0.1 Gulf Keystone* 2,149 13.9 Gulfsands Petroleum* 142 0.1 Hardy Oil & Gas 131 0.5 Hawkley Oil and Gas* - - Heritage Oil 579 1.8 Horizon 398 0.9 Igas Energy 358 2.8 Independent Resources 4 0.0 Ithaca Energy 582 1.8 JKX 143 0.1 Karoon Gas 1,149 4.6 Lansdowne 97 0.2 Leni Gas and Oil 28 0.3 Lochard 21 0.1 LongReach 57 0.0 Lundin 6,810 22.3 Madagascar Oil and Gas* 138 0.3 Magnolia 35 0.3

Catalytic converter | 19 June 2013 26

Name Market cap (US$m) Liquidity (US$m) Mart Resources 505 1.9 Max Petroleum 113 0.1 Mediterranean Oil & Gas 54 0.1 New Standard Energy 38 0.0 Nido Petroleum* 47 0.1 Nighthawk 86 0.3 North Sea Energy 15 0.0 Northern Petroleum* 54 0.2 Nostra Terra 19 0.1 NZ Energy Corp 51 0.1 NZOG 283 0.3 Oilex 20 0.0 Ophir Energy 3,423 5.8 Pacific Rubiales 6,779 31.5 Parkmead 188 0.3 Petrel 19 0.0 Petro Frontier Energy 20 0.1 Petro Matad 14 0.0 Petroceltic 403 1.2 Petromanas 72 0.0 PetroNeft 29 0.1 Po Valley Energy* 12 0.0 PPP 59 0.0 Premier Oil 2,912 8.6 President Energy* 79 0.1 Providence Resources 557 2.8 Pura Vida 39 0.1 Range Resources* 129 0.0 Renegade Petroleum 224 1.0 Resaca 1 0.0 Rialto 0.0 Rockhopper Exploration 586 5.3 Ruspetro 196 0.5 SacOil 0.0 Salamander Energy 657 1.1 San Leon 171 0.6 Sefton 7 0.0 Serica 65 0.1 ShaMaran Petroleum 323 0.6 Silvermere 1 0.0 Simba Energy* 17 0.0 Sirius 51 0.2 Soco 1,958 1.5 Solo 24 0.2 Sound Oil 43 0.3 Sterling Energy 121 0.0 Sundance Energy 387 1.9 TAG 176 1.7 Tangiers 26 0.0 Tethys 256 0.3 Tomco 31 0.0 Tower Resources 45 0.1 Tullow Oil 14,844 33.2 TXO 3 0.0 Urals 18 0.0 Victoria Oil and Gas* 102 0.1 Volga 110 0.0 Wessex 15 0.1 Source: Edison Investment Research, Bloomberg. Note: Liquidity is based on a 30-day average trading volume multiplied by current price.*Indicates Edison client. Priced as of 17 June 2013.

Catalytic converter | 19 June 2013 27

Exhibit 25: Bespoke indices categories Continents Regions Countries Themes Africa East Africa Argentina <$500m Americas Eastern Europe Australia $500m-$1bn Arctic FSU Barents Sea $1-5bn Asia Middle East Brazil $5-10bn Australasia North Africa Canada >$10bn Europe North America Caspian Cash heavy

North-West Europe Falklands CBM

South America Gabon Deep water

South-East Asia Guianas Downstream

Sub-Saharan India Financially stressed

West Africa Indonesia Fully funded

Iraq High impact

Kazakhstan High political

Kenya IOCs

Kurdistan Low political

Mauritania Major independents

Morocco Midstream

Mozambique Oil services

Namibia Oil shale

New Zealand Pre-salt

Nigeria Pre-salt Middle East

Norwegian North Sea Pre-salt South America

Russia Pre-salt West Africa

Somaliland Producer

Tanzania Shale Gas

UK North Sea Shale oil

US Skin in the game

Unconventionals Source: Edison Investment Research

Catalytic converter | 19 June 2013 28

Exhibit 26: Winners and losers

Source: Edison Investment Research, Bloomberg. Note: *Denotes a company that Edison covers. Priced at 17 June 2013.

No. B es t performers % change No. Wors t performers % change

1 Petro Frontier Energy 62.5% 1 African Petroleum -25.0%

2 Baraka 33.3% 2 Roxi -17.6%

3 Tethys 18 .2% 3 Simba Energy -20.0%

4 Xtract 15.1% 4 Ascent -14.3%

5 Sefton 13.6% 5 CBM Asia* -11.5%

No. B es t performers % change No. Wors t performers % change

1 Xtract 117.9% 1 Aminex -35.5%

2 Igas Energy 55.0% 2 Resaca -35.0%

3 Petro Frontier Energy 44.4% 3 San Leon -28 .8 %

4 Caza Oil and Gas 41.4% 4 African Petroleum -25.0%

5 Sefton 38 .9% 5 Greka Drilling* -23.6%

No. B es t performers % change No. Wors t performers % change

1 Xtract 8 4.8 % 1 Antrim Energy -77.6%

2 Ruspetro 70.5% 2 Silvermere -68 .1%

3 North Sea Energy 51.4% 3 Wessex -65.4%

4 Nighthawk 50.6% 4 Clontarf -63.6%

5 Frontera 42.6% 5 Rialto -57.9%

No. B es t performers % change No. Wors t performers % change

1 Tethys 107.3% 1 African Petroleum -8 4.2%

2 Petro Frontier Energy 100.0% 2 Silvermere -79.5%

3 Frontera 92.9% 3 Antrim Energy -78 .8 %

4 Greka Drilling* 8 8 .9% 4 Resaca -75.9%

5 Xtract 74.3% 5 Wessex -72.4%

No. B es t performers % change No. Wors t performers % change

1 Petrel 235.1% 1 Resaca -91.8 %

2 ShaMaran Petroleum 113.2% 2 African Petroleum -8 8 .0%

3 Igas Energy 96.8 % 3 Rialto -8 6.1%

4 Amerisur Resources 8 1.0% 4 Silvermere -8 4.7%

5 Nighthawk 78 .5% 5 Antrim Energy -8 2.8 %

1 week

1 month

3 months

6 months

1 year

Catalytic converter | 19 June 2013 29