Embed Size (px)

Citation preview

July 2017 EEnergy Informer Page 1

19

In this issue

� Trump’s Decision To Pull Out Of Paris Accord Invigorates Opposition 1

� California Governor Gets Red Carpet In China, Energy Secretary Does Not 4

� BP Acknowledges What Is Widely Known; Total Goes A Step Further 5

� Finkel Report: Imagine A World Without Electricity 7

� German Electricity Paradox 10

� NYISO: Times They Are A Changin’ 12

� EPA Solicits Input And Gets A Surprising Mouthful 15

� UBS Predicts EV Price Parity By 2018 17

� China On Top 18

� Nuclear’s Prospects Not Encouraging 19

� Making America Inefficient Again 20

� California Senate Passes 100% Renewable Bill 21

� California Regulators Examine Rapidly Changing Retail Landscape 21

� Electricity Consumption Falls As LEDs Go Mainstream 23

� Japan Powering Down As Retail Competition Is Introduced 25

� Just published: Innovation and Disruption at the Grid’s Edge 26

`

Trump’s Decision To Pull Out Of Paris Accord Invigorates Opposition The Administration has done an admirable job of unifying its climate foes

y now, it is generally accepted that President Donald Trump does not appear to think, or for that matter care, much about what reaction his frequent tweets, announcements or decisions may generate. He is the president, he calls the shots, and if you don’t like it, that is your problem – as

far as he is concerned. Yet, it is equally clear that some of his decisions thus far have been unpopular among many in the US – and even more overseas – which does not seem to bother him either. According to a recent poll, Trump’s net approval rating – that is the % of approvals minus disapprovals – hovers around minus 24, the lowest since he took office. In other words, he is viewed negatively by the majority of Americans. His Executive Order in late March 2017 to get rid of many environmental regulations, for which the US Environmental Protection Agency (EPA) is responsible – extensively covered in the May 2017 issue of this newsletter – had the effect of unifying all environmentally-minded people and organizations in opposition to his decision. But his call to pull the US out of the Paris Accord on 1st June 2017 set a new low for anyone who even remotely cares about environmental stewardship, climate change or the US role, let alone leadership, in the world. The reaction from within and outside America was immediate and resoundingly negative – setting aside his small and shrinking base

B

EEnergy Informer The International Energy Newsletter

July 2017

EEnergy Informer July 2017

Vol. 27, No. 7

ISSN: 1084-0419 http://www.eenergyinformer.com

Subscription options/prices on last page

Copyright © 2017. The

content of this newsletter is

protected under US copyright

laws. No part of this

publication may be copied,

reproduced or disseminated

in any form without prior

permission of the publisher.

Accord de Paris: C’est fait, it is

done, no negotiations required

Paris’ iconic Eiffel Tower with sign

declaring that the global agreement is a

done deal, 4 Nov 2016

2July 2017 EEnergy Informer Page 2

of supporters. Below is a sample of some of the immediate reactions his decision generated:

• The Europeans announced – politely – their regret, but said they will carry on with increased vigor, rejecting any notion of “renegotiating” the Paris Accord;

• China – also politely – indicated that it was delighted for the opportunity to fill the vacuum created by the departure of the US;

• Former Mayor of New York, Michael Bloomberg – not politely but rather bluntly – said he was donating $15 million of his own money to make up for the loss of US funding to the UNFCCC;

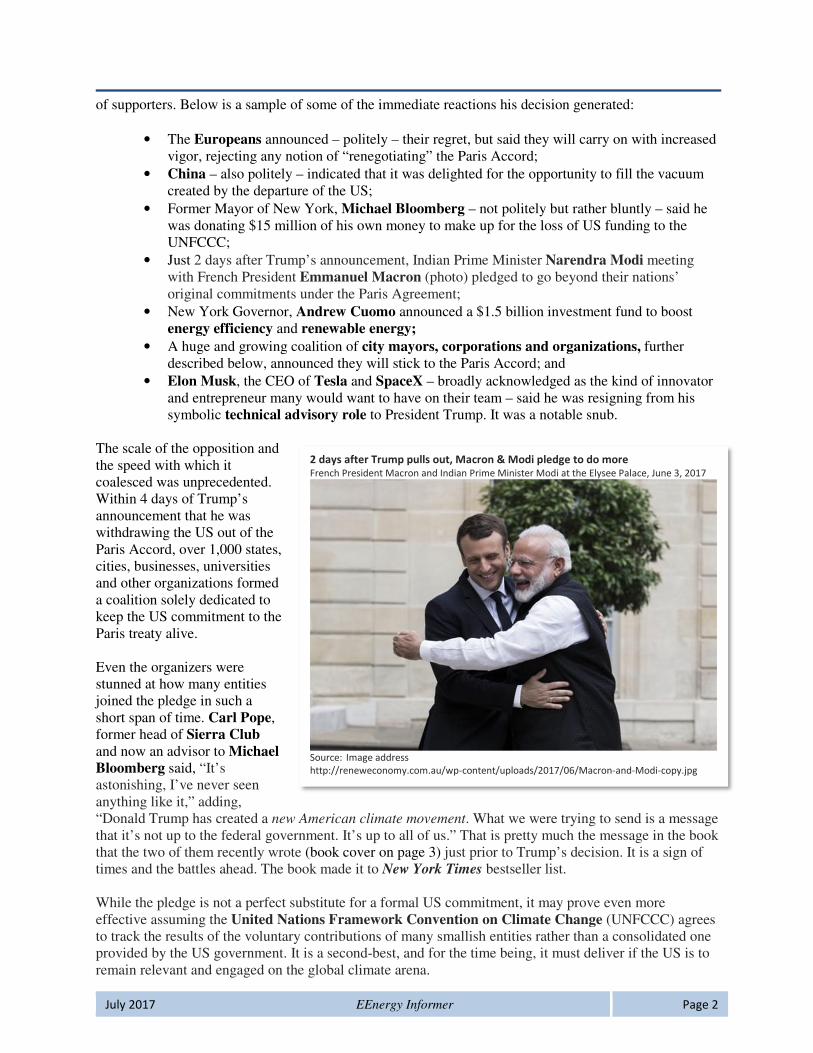

• Just 2 days after Trump’s announcement, Indian Prime Minister Narendra Modi meeting with French President Emmanuel Macron (photo) pledged to go beyond their nations’ original commitments under the Paris Agreement;

• New York Governor, Andrew Cuomo announced a $1.5 billion investment fund to boost energy efficiency and renewable energy;

• A huge and growing coalition of city mayors, corporations and organizations, further described below, announced they will stick to the Paris Accord; and

• Elon Musk, the CEO of Tesla and SpaceX – broadly acknowledged as the kind of innovator and entrepreneur many would want to have on their team – said he was resigning from his symbolic technical advisory role to President Trump. It was a notable snub.

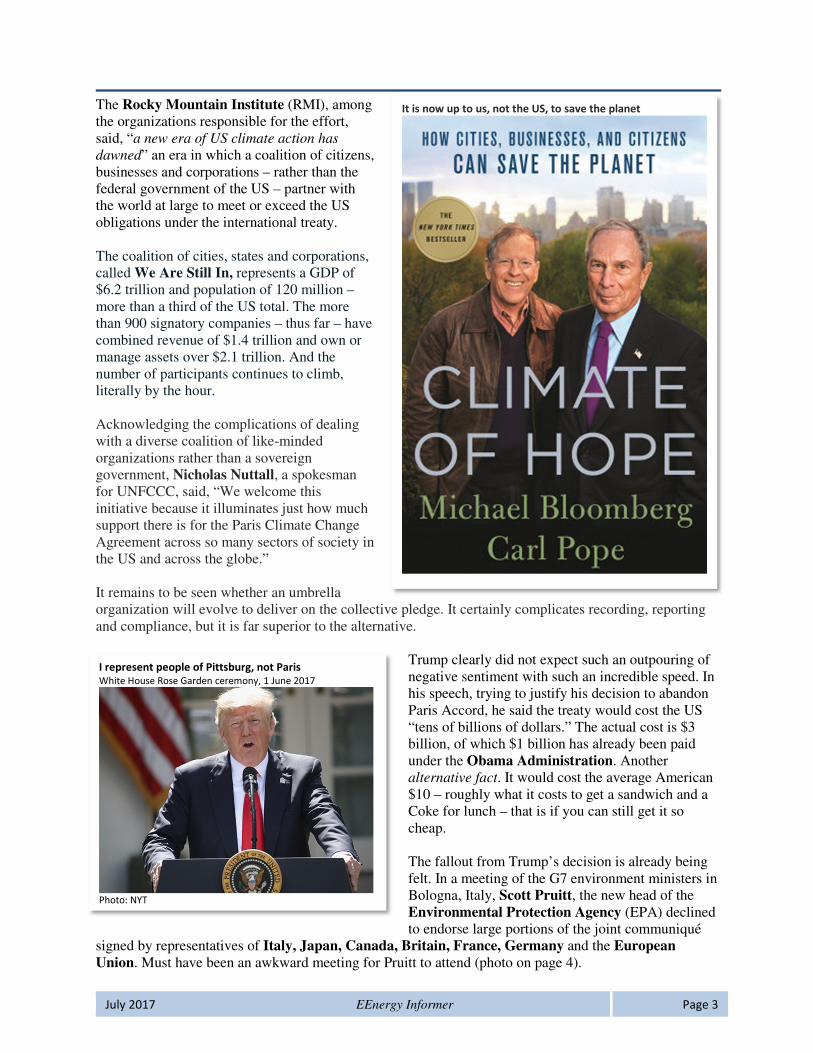

The scale of the opposition and the speed with which it coalesced was unprecedented. Within 4 days of Trump’s announcement that he was withdrawing the US out of the Paris Accord, over 1,000 states, cities, businesses, universities and other organizations formed a coalition solely dedicated to keep the US commitment to the Paris treaty alive. Even the organizers were stunned at how many entities joined the pledge in such a short span of time. Carl Pope, former head of Sierra Club and now an advisor to Michael Bloomberg said, “It’s astonishing, I’ve never seen anything like it,” adding, “Donald Trump has created a new American climate movement. What we were trying to send is a message that it’s not up to the federal government. It’s up to all of us.” That is pretty much the message in the book that the two of them recently wrote (book cover on page 3) just prior to Trump’s decision. It is a sign of times and the battles ahead. The book made it to New York Times bestseller list. While the pledge is not a perfect substitute for a formal US commitment, it may prove even more effective assuming the United Nations Framework Convention on Climate Change (UNFCCC) agrees to track the results of the voluntary contributions of many smallish entities rather than a consolidated one provided by the US government. It is a second-best, and for the time being, it must deliver if the US is to remain relevant and engaged on the global climate arena.

2 days after Trump pulls out, Macron & Modi pledge to do more French President Macron and Indian Prime Minister Modi at the Elysee Palace, June 3, 2017

Source: Image address

http://reneweconomy.com.au/wp-content/uploads/2017/06/Macron-and-Modi-copy.jpg

3July 2017 EEnergy Informer Page 3

The Rocky Mountain Institute (RMI), among the organizations responsible for the effort, said, “a new era of US climate action has

dawned” an era in which a coalition of citizens, businesses and corporations – rather than the federal government of the US – partner with the world at large to meet or exceed the US obligations under the international treaty. The coalition of cities, states and corporations, called We Are Still In, represents a GDP of $6.2 trillion and population of 120 million – more than a third of the US total. The more than 900 signatory companies – thus far – have combined revenue of $1.4 trillion and own or manage assets over $2.1 trillion. And the number of participants continues to climb, literally by the hour. Acknowledging the complications of dealing with a diverse coalition of like-minded organizations rather than a sovereign government, Nicholas Nuttall, a spokesman for UNFCCC, said, “We welcome this initiative because it illuminates just how much support there is for the Paris Climate Change Agreement across so many sectors of society in the US and across the globe.” It remains to be seen whether an umbrella organization will evolve to deliver on the collective pledge. It certainly complicates recording, reporting and compliance, but it is far superior to the alternative.

Trump clearly did not expect such an outpouring of negative sentiment with such an incredible speed. In his speech, trying to justify his decision to abandon Paris Accord, he said the treaty would cost the US “tens of billions of dollars.” The actual cost is $3 billion, of which $1 billion has already been paid under the Obama Administration. Another alternative fact. It would cost the average American $10 – roughly what it costs to get a sandwich and a Coke for lunch – that is if you can still get it so cheap. The fallout from Trump’s decision is already being felt. In a meeting of the G7 environment ministers in Bologna, Italy, Scott Pruitt, the new head of the Environmental Protection Agency (EPA) declined to endorse large portions of the joint communiqué

signed by representatives of Italy, Japan, Canada, Britain, France, Germany and the European Union. Must have been an awkward meeting for Pruitt to attend (photo on page 4).

It is now up to us, not the US, to save the planet

I represent people of Pittsburg, not Paris White House Rose Garden ceremony, 1 June 2017

Photo: NYT

4July 2017 EEnergy Informer Page 4

Under Pruitt, the EPA has taken down substantial information previously on its website covering climate change and references to global warming. The next awkward meeting will take place in July in Germany where President trump will meet with the G20. There will be more opportunities for the US to be the sole country abstaining or going against the flow. Some observers point out that the US greenhouse gas emissions have been falling for some time, and are likely to continue falling – with or without the Paris Accord, so what is the big fuss? Others say symbolism matters, as does leadership, environmental stewardship, international cooperation and collaboration on such a critical global issue. Yet others point out – a view shared by this editor – that the Paris Accord would be substantially better off without a reluctant Trump Administration as a signatory. Who needs a player on the team – and a really big one – who is not even remotely interested in playing the game and is likely to try its best to sabotage the team from reaching its objectives from within? US, along with Syria and Nicaragua, are the only 3 countries pulling out of the global agreement. And that, as this editor sees it, speaks volumes. �

California Governor Gets Red Carpet In China,

Energy Secretary Does Not Sometimes symbolism matters more than substance

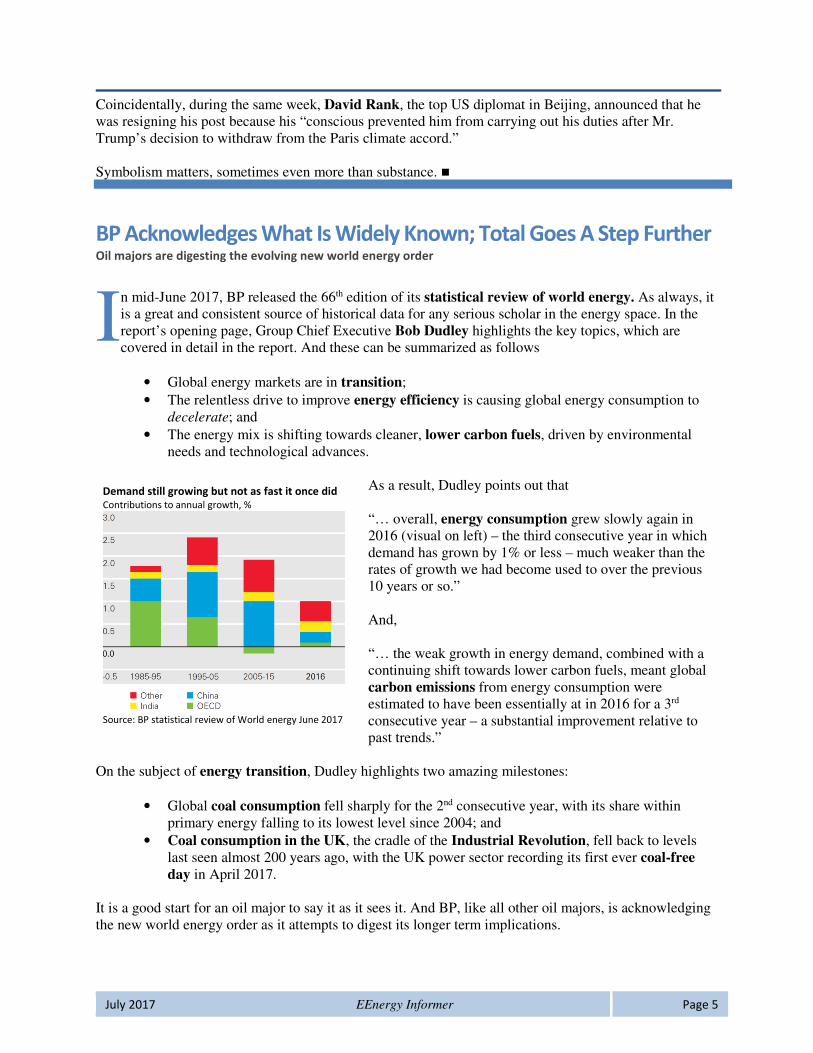

alifornia Governor Jerry Brown, a greener than green Democrat, did not mince any words in expressing his opposition to President Trump after the latter announced his decision to pull the US out of the Paris Accord. The next day, he flew to China’s capital and was treated as a dignitary – he is after all the elected official representing the world’s 6th largest economy –

including an audience in the Great Hall of the People in Beijing with President Xi Jinping, where they discussed mutual cooperation in clean and green energy technologies. Afterwards, Brown told reporters that President Xi “welcomed an increased role on the part of California to fight climate change.” Mostly fluff, you might say, but symbolism matters. As it happens, US Energy Secretary Rick Perry, was also visiting Beijing during the same week. He, however, did not get to meet with President Xi. It was not entirely clear what Mr. Perry was trying to achieve. Given that DOE is cutting funding for energy efficiency and renewable energy research, perhaps there was not much to talk about.

CTrump’s decision to pull out of Paris Accord: “Insane”

EPA’s Scott Pruitt: Listening but not endorsing

Photo: AP

5July 2017 EEnergy Informer Page 5

Coincidentally, during the same week, David Rank, the top US diplomat in Beijing, announced that he was resigning his post because his “conscious prevented him from carrying out his duties after Mr. Trump’s decision to withdraw from the Paris climate accord.” Symbolism matters, sometimes even more than substance. �

BP Acknowledges What Is Widely Known; Total Goes A Step Further Oil majors are digesting the evolving new world energy order

n mid-June 2017, BP released the 66th edition of its statistical review of world energy. As always, it is a great and consistent source of historical data for any serious scholar in the energy space. In the report’s opening page, Group Chief Executive Bob Dudley highlights the key topics, which are covered in detail in the report. And these can be summarized as follows

• Global energy markets are in transition;

• The relentless drive to improve energy efficiency is causing global energy consumption to decelerate; and

• The energy mix is shifting towards cleaner, lower carbon fuels, driven by environmental needs and technological advances.

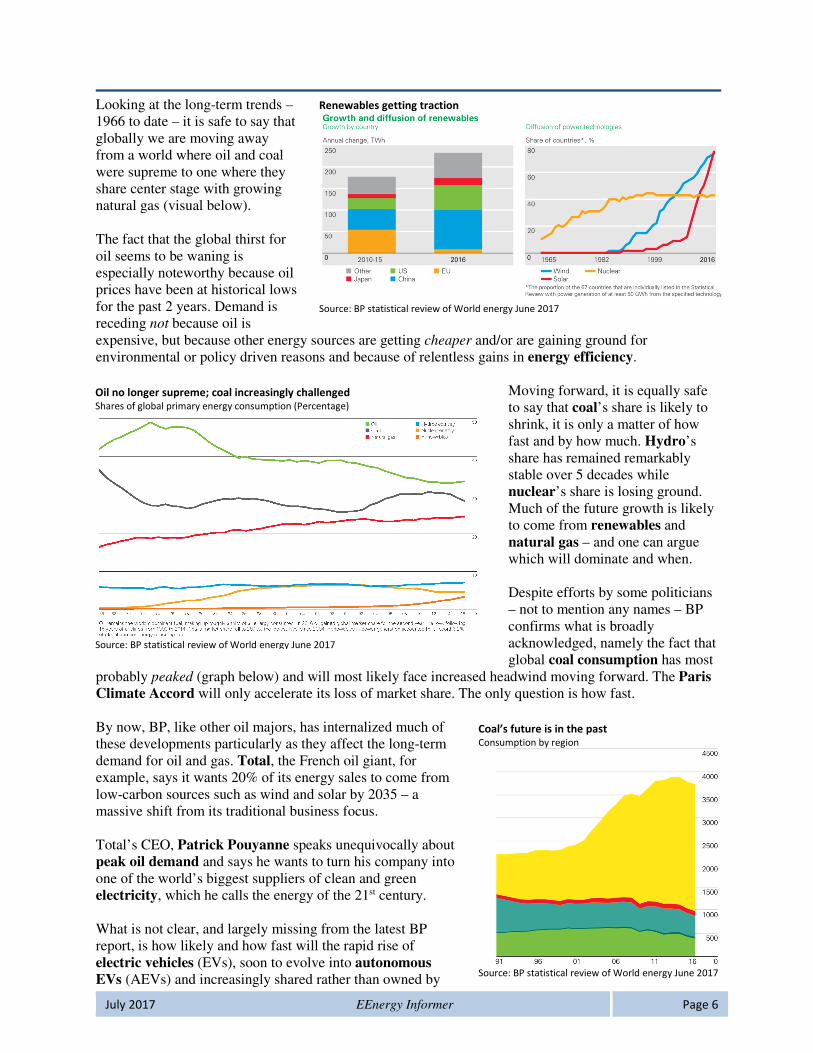

As a result, Dudley points out that “… overall, energy consumption grew slowly again in 2016 (visual on left) – the third consecutive year in which demand has grown by 1% or less – much weaker than the rates of growth we had become used to over the previous 10 years or so.” And, “… the weak growth in energy demand, combined with a continuing shift towards lower carbon fuels, meant global carbon emissions from energy consumption were estimated to have been essentially at in 2016 for a 3rd consecutive year – a substantial improvement relative to past trends.”

On the subject of energy transition, Dudley highlights two amazing milestones:

• Global coal consumption fell sharply for the 2nd consecutive year, with its share within primary energy falling to its lowest level since 2004; and

• Coal consumption in the UK, the cradle of the Industrial Revolution, fell back to levels last seen almost 200 years ago, with the UK power sector recording its first ever coal-free day in April 2017.

It is a good start for an oil major to say it as it sees it. And BP, like all other oil majors, is acknowledging the new world energy order as it attempts to digest its longer term implications.

I

Demand still growing but not as fast it once did Contributions to annual growth, %

Source: BP statistical review of World energy June 2017

6July 2017 EEnergy Informer Page 6

Looking at the long-term trends – 1966 to date – it is safe to say that globally we are moving away from a world where oil and coal were supreme to one where they share center stage with growing natural gas (visual below). The fact that the global thirst for oil seems to be waning is especially noteworthy because oil prices have been at historical lows for the past 2 years. Demand is receding not because oil is expensive, but because other energy sources are getting cheaper and/or are gaining ground for environmental or policy driven reasons and because of relentless gains in energy efficiency.

Moving forward, it is equally safe to say that coal’s share is likely to shrink, it is only a matter of how fast and by how much. Hydro’s share has remained remarkably stable over 5 decades while nuclear’s share is losing ground. Much of the future growth is likely to come from renewables and natural gas – and one can argue which will dominate and when. Despite efforts by some politicians – not to mention any names – BP confirms what is broadly acknowledged, namely the fact that global coal consumption has most

probably peaked (graph below) and will most likely face increased headwind moving forward. The Paris Climate Accord will only accelerate its loss of market share. The only question is how fast. By now, BP, like other oil majors, has internalized much of these developments particularly as they affect the long-term demand for oil and gas. Total, the French oil giant, for example, says it wants 20% of its energy sales to come from low-carbon sources such as wind and solar by 2035 – a massive shift from its traditional business focus. Total’s CEO, Patrick Pouyanne speaks unequivocally about peak oil demand and says he wants to turn his company into one of the world’s biggest suppliers of clean and green electricity, which he calls the energy of the 21st century. What is not clear, and largely missing from the latest BP report, is how likely and how fast will the rapid rise of electric vehicles (EVs), soon to evolve into autonomous EVs (AEVs) and increasingly shared rather than owned by

Oil no longer supreme; coal increasingly challenged Shares of global primary energy consumption (Percentage)

Source: BP statistical review of World energy June 2017

Coal’s future is in the past Consumption by region

Source: BP statistical review of World energy June 2017

Renewables getting traction

Source: BP statistical review of World energy June 2017

7July 2017 EEnergy Informer Page 7

individuals through ride hailing services such as Uber or its copycats, begin to eat into the massive road transportation demand for oil. As described in article on UBS on page 17 and prediction of peak oil by 2026 by Redburn reported in the April 2017 issue of this newsletter, some analysts believe that the peak demand for oil, like that of coal, may be upon us a lot faster than many had predicted. And once this happens, the subsequent fall in demand may very well be precipitous.

Total’s Pouyanne seems to have got the message much more clearly than his fellow CEOs at other oil majors. Total has invested big money on SunPower, a California-based solar PV manufacturer, in Saft Groupe SA, a French battery maker and more recently in Lampiris NV, a renewable energy retailer in Belgium. In case you are wondering, his game plan is to integrate distributed solar generation with storage and electricity retailing – skill sets that Total currently lacks totally, no pun intended.

If you think it sounds too similar to Tesla’s integrated energy and mobility business model involving the recent acquisition of SolarCity and its distributed battery business, Powerwall, you are spot on. If similar issues are a source for sleepless nights for BP’s CEO, Bob Dudley does not divulge. � BP Report

Finkel Report: Imagine A World Without Electricity Blueprint for Australia’s future electricity market pleases some but not all

magine a world without electricity,” those are the starting words of the so-called Finkel Report released in June 2017 amidst much anticipation in Canberra, the capital of Australia. The official name of the report is Independent review into the future security of the National Electricity Market (NEM): Blueprint for the future.

Following last year’s blackout in South Australia, Finkel, Australia’s Chief Scientist plus a panel of 4 other experts, were tasked to propose a blueprint for the future. The panel’s mission was to “recommend enhancements to the National Electricity Market (NEM) to optimize security and reliability, and to do so at lowest cost,” noting that it is being submitted during a public debate about international commitments under the Paris Agreement. Australia’s current government, not unlike the US under President Trump, does not appear wholeheartedly wedded to the global treaty – or equivocates on its commitments. In the report’s Preface, Finkel says, “If, as I hope, this blueprint is adopted by you, then our NEM should return to being the high-performance servant of our community that it once was.” As an official report to Australia’s Prime Minister Malcolm Turnbull, it says all the right things.

“I

Elon Musk & Patrick Pouyanne think alike: Integrated electricity services

Source: Tesla unveils residential solar roof and new Powerwall battery, Utility Dive, 28

Oct 2016

8July 2017 EEnergy Informer Page 8

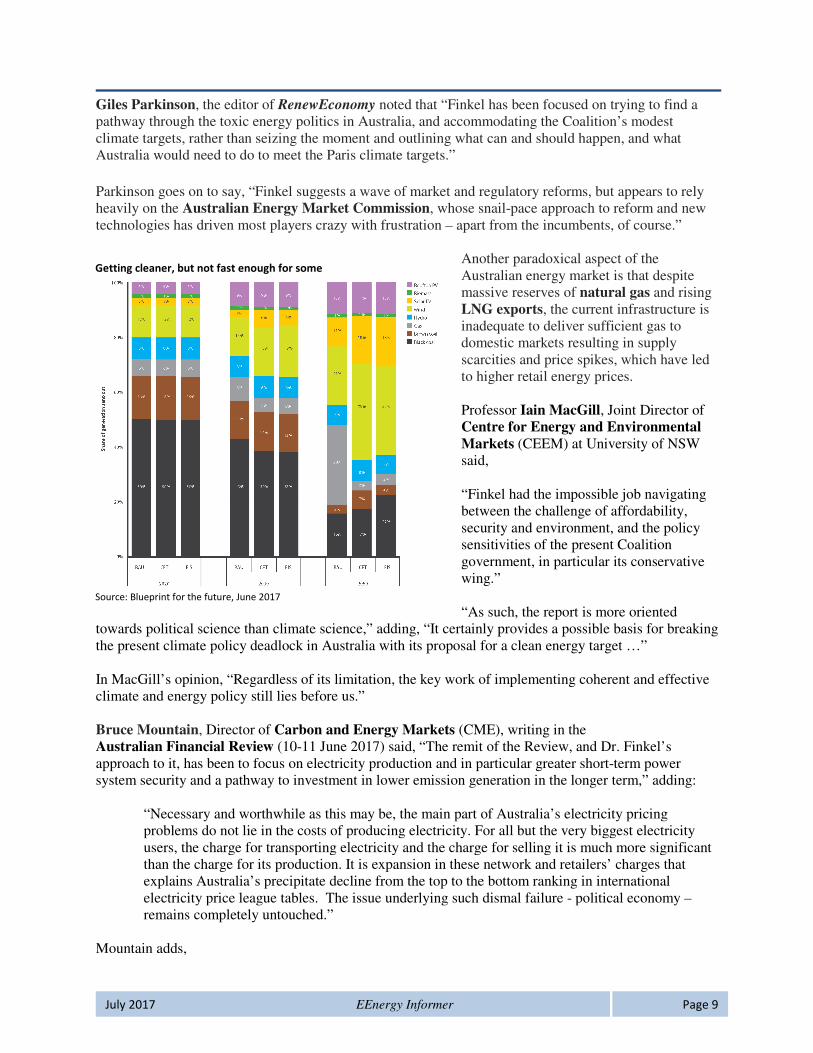

Finkel and his fellow panelists point out the obvious such as, “Australia’s electricity system is in transition” and that “the rate of transition is rapid.” That much we already know. The blueprint also makes other obvious points such as stating that the report is focused on 4 key outcomes:

• Increased security;

• Future reliability;

• Rewarding consumers; and

• Lower emissions Adding, “These outcomes will be underpinned by the 3 pillars of an orderly transition, better system planning and stronger governance. What is there not to like?

The report offers many recommendations, more than most can absorb – from mundane to profound. As everyone recognizes, it is a rather complicated topic. The bulk of the report is covered by spelling out and embellishing these recommendations. It says, “Australia has a once-in-

a-generation opportunity to reshape our electricity system for the future.” But is this that future? While it is hard to say how much of its recommendations will be accepted &/or implemented, it is fair to say that the report has already generated much publicity – not all in agreement with the report’s main recommendations. The Australian’s headline on 14 June 2017 read “Turnbull faces revolt on power.” The Australian Financial Review’s headline on the same date read: “Coalition in revolt over climate fix.” It said: “Finkel has provided a roadmap for energy policy that is determined to set off the freeway of carbon pricing in any form and seek instead the scenic backroads of encouraging renewables without discouraging the burning of coal.”

The fundamentals are here, for the most part

Source: Blueprint for the future, June 2017

Diversity of resources and ownership makes it complicated

Source: Blueprint for the future, June 2017

Australia’s NEM: Covering where most

Aussies live

Source: Independent review into the future

security of the National Electricity Market

(NEM): Blueprint for the future, June 2017

9July 2017 EEnergy Informer Page 9

Giles Parkinson, the editor of RenewEconomy noted that “Finkel has been focused on trying to find a pathway through the toxic energy politics in Australia, and accommodating the Coalition’s modest climate targets, rather than seizing the moment and outlining what can and should happen, and what Australia would need to do to meet the Paris climate targets.”

Parkinson goes on to say, “Finkel suggests a wave of market and regulatory reforms, but appears to rely heavily on the Australian Energy Market Commission, whose snail-pace approach to reform and new technologies has driven most players crazy with frustration – apart from the incumbents, of course.”

Another paradoxical aspect of the Australian energy market is that despite massive reserves of natural gas and rising LNG exports, the current infrastructure is inadequate to deliver sufficient gas to domestic markets resulting in supply scarcities and price spikes, which have led to higher retail energy prices. Professor Iain MacGill, Joint Director of Centre for Energy and Environmental Markets (CEEM) at University of NSW said, “Finkel had the impossible job navigating between the challenge of affordability, security and environment, and the policy sensitivities of the present Coalition government, in particular its conservative wing.” “As such, the report is more oriented

towards political science than climate science,” adding, “It certainly provides a possible basis for breaking the present climate policy deadlock in Australia with its proposal for a clean energy target …” In MacGill’s opinion, “Regardless of its limitation, the key work of implementing coherent and effective climate and energy policy still lies before us.” Bruce Mountain, Director of Carbon and Energy Markets (CME), writing in the Australian Financial Review (10-11 June 2017) said, “The remit of the Review, and Dr. Finkel’s approach to it, has been to focus on electricity production and in particular greater short-term power system security and a pathway to investment in lower emission generation in the longer term,” adding:

“Necessary and worthwhile as this may be, the main part of Australia’s electricity pricing problems do not lie in the costs of producing electricity. For all but the very biggest electricity users, the charge for transporting electricity and the charge for selling it is much more significant than the charge for its production. It is expansion in these network and retailers’ charges that explains Australia’s precipitate decline from the top to the bottom ranking in international electricity price league tables. The issue underlying such dismal failure - political economy – remains completely untouched.”

Mountain adds,

Getting cleaner, but not fast enough for some

Source: Blueprint for the future, June 2017

10July 2017 EEnergy Informer Page 10

“Almost 250 years ago Adam Smith exhorted: ‘Consumption is the sole end and purpose of all production and the interest of the producer ought to be attended to only so far as it may be necessary for promoting that of the consumer.’ It is a famous phrase, cited as often as it is ignored.” There is certainly a lot to read in the Finkel report, and depending on one’s perspective and vested interests, there is something for most, if not in the whole, then certainly in parts of the blueprint. It remains to be seen how the blueprint’s recommendations will be implemented and when. And as Parkinson, MacGill and Mountain point out many of Australia’s electricity market ills are political in nature – the most challenging to address. In the meantime, as Finkel warns, next summer’s heat waves, bushfires and storms are not far away. Politicians must act, sooner or later. � Blueprint for the future

German Electricity Paradox Cheap wholesale, expensive retail, not getting greener and hard to balance

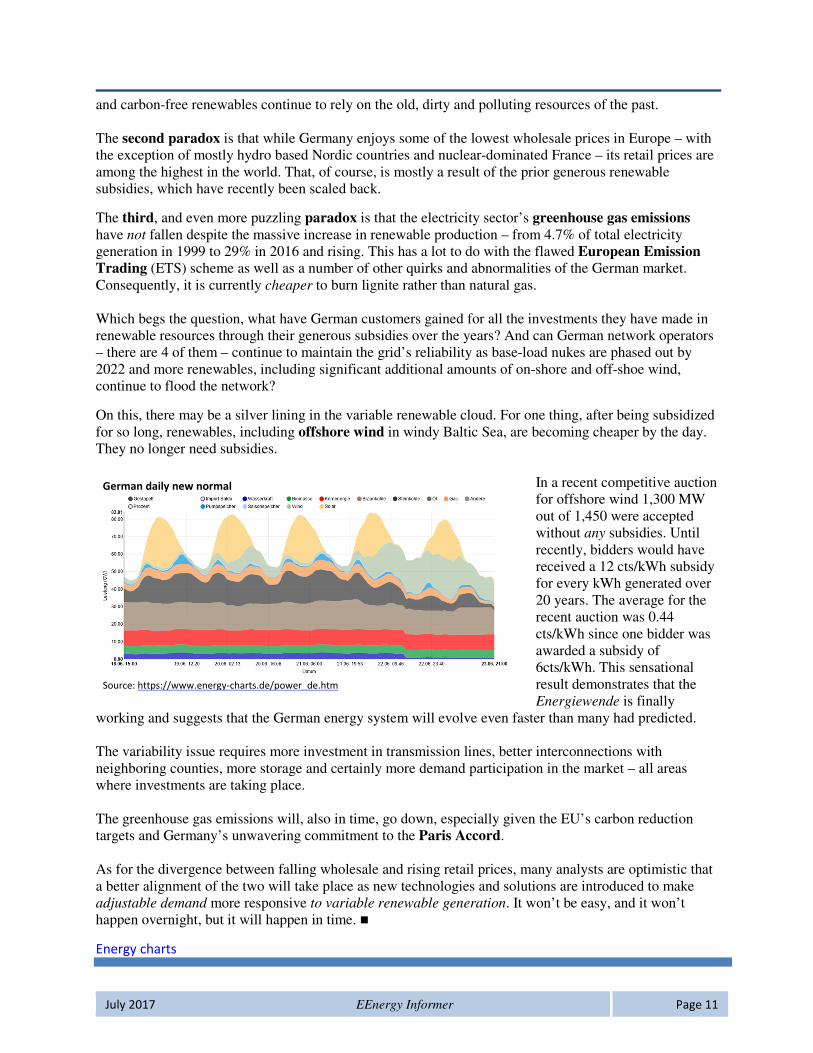

or some time, German consumers have been subsidizing renewables to the tune of €20 billion per annum through high retail tariffs, among the highest anywhere. Following Fukushima nuclear disaster in Japan in March 2011, the phase out of nuclear by 2022 was added to the Energiewende or German energy turnaround. While the public seems content with the progress of the scheme

and, to date, the lights have stayed on despite the increased penetration of variable renewable resources, Energiewende has failed to reduce the power sector’s greenhouse gas emissions. And here lies the German electricity paradox, actually a number of paradoxes. The first paradox is that Energiewende has doubled the country’s installed capacity – there is roughly as much variable renewable capacity as there is conventional thermal generation – while consumption has remained basically flat and peak load has not changed over the last 20 years. The network, however, needs the thermal units because renewables are variable. This is because of “Dunkelflaute,” which happens during cold, dark and windless winter months, where there is virtually no sun or wind and the entire system must rely on thermal plants. In this context, the new, clean

F

Australian electricity demand no more

Source: Blueprint for the future, June 2017

Lots of wind, lots of sun, but not all of the time

Source: https://www.energy-charts.de/power_de.htm

11July 2017 EEnergy Informer Page 11

and carbon-free renewables continue to rely on the old, dirty and polluting resources of the past. The second paradox is that while Germany enjoys some of the lowest wholesale prices in Europe – with the exception of mostly hydro based Nordic countries and nuclear-dominated France – its retail prices are among the highest in the world. That, of course, is mostly a result of the prior generous renewable subsidies, which have recently been scaled back.

The third, and even more puzzling paradox is that the electricity sector’s greenhouse gas emissions have not fallen despite the massive increase in renewable production – from 4.7% of total electricity generation in 1999 to 29% in 2016 and rising. This has a lot to do with the flawed European Emission Trading (ETS) scheme as well as a number of other quirks and abnormalities of the German market. Consequently, it is currently cheaper to burn lignite rather than natural gas. Which begs the question, what have German customers gained for all the investments they have made in renewable resources through their generous subsidies over the years? And can German network operators – there are 4 of them – continue to maintain the grid’s reliability as base-load nukes are phased out by 2022 and more renewables, including significant additional amounts of on-shore and off-shoe wind, continue to flood the network?

On this, there may be a silver lining in the variable renewable cloud. For one thing, after being subsidized for so long, renewables, including offshore wind in windy Baltic Sea, are becoming cheaper by the day. They no longer need subsidies.

In a recent competitive auction for offshore wind 1,300 MW out of 1,450 were accepted without any subsidies. Until recently, bidders would have received a 12 cts/kWh subsidy for every kWh generated over 20 years. The average for the recent auction was 0.44 cts/kWh since one bidder was awarded a subsidy of 6cts/kWh. This sensational result demonstrates that the Energiewende is finally

working and suggests that the German energy system will evolve even faster than many had predicted. The variability issue requires more investment in transmission lines, better interconnections with neighboring counties, more storage and certainly more demand participation in the market – all areas where investments are taking place. The greenhouse gas emissions will, also in time, go down, especially given the EU’s carbon reduction targets and Germany’s unwavering commitment to the Paris Accord. As for the divergence between falling wholesale and rising retail prices, many analysts are optimistic that a better alignment of the two will take place as new technologies and solutions are introduced to make adjustable demand more responsive to variable renewable generation. It won’t be easy, and it won’t happen overnight, but it will happen in time. �

Energy charts

German daily new normal

Source: https://www.energy-charts.de/power_de.htm

12July 2017 EEnergy Informer Page 12

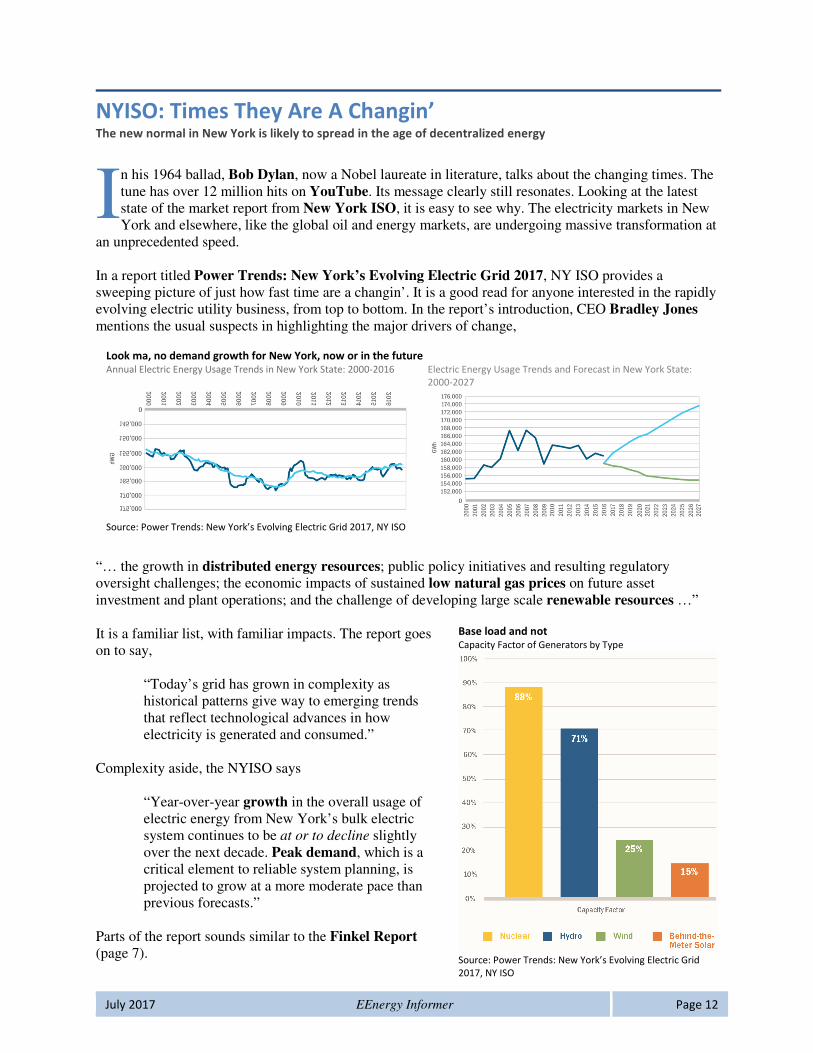

NYISO: Times They Are A Changin’ The new normal in New York is likely to spread in the age of decentralized energy

n his 1964 ballad, Bob Dylan, now a Nobel laureate in literature, talks about the changing times. The tune has over 12 million hits on YouTube. Its message clearly still resonates. Looking at the latest state of the market report from New York ISO, it is easy to see why. The electricity markets in New York and elsewhere, like the global oil and energy markets, are undergoing massive transformation at

an unprecedented speed. In a report titled Power Trends: New York’s Evolving Electric Grid 2017, NY ISO provides a sweeping picture of just how fast time are a changin’. It is a good read for anyone interested in the rapidly evolving electric utility business, from top to bottom. In the report’s introduction, CEO Bradley Jones mentions the usual suspects in highlighting the major drivers of change,

“… the growth in distributed energy resources; public policy initiatives and resulting regulatory oversight challenges; the economic impacts of sustained low natural gas prices on future asset investment and plant operations; and the challenge of developing large scale renewable resources …”

It is a familiar list, with familiar impacts. The report goes on to say,

“Today’s grid has grown in complexity as historical patterns give way to emerging trends that reflect technological advances in how electricity is generated and consumed.”

Complexity aside, the NYISO says

“Year-over-year growth in the overall usage of electric energy from New York’s bulk electric system continues to be at or to decline slightly over the next decade. Peak demand, which is a critical element to reliable system planning, is projected to grow at a more moderate pace than previous forecasts.”

Parts of the report sounds similar to the Finkel Report (page 7).

I

Look ma, no demand growth for New York, now or in the future Annual Electric Energy Usage Trends in New York State: 2000-2016 Electric Energy Usage Trends and Forecast in New York State:

2000-2027

Source: Power Trends: New York’s Evolving Electric Grid 2017, NY ISO

Base load and not Capacity Factor of Generators by Type

Source: Power Trends: New York’s Evolving Electric Grid

2017, NY ISO

13July 2017 EEnergy Informer Page 13

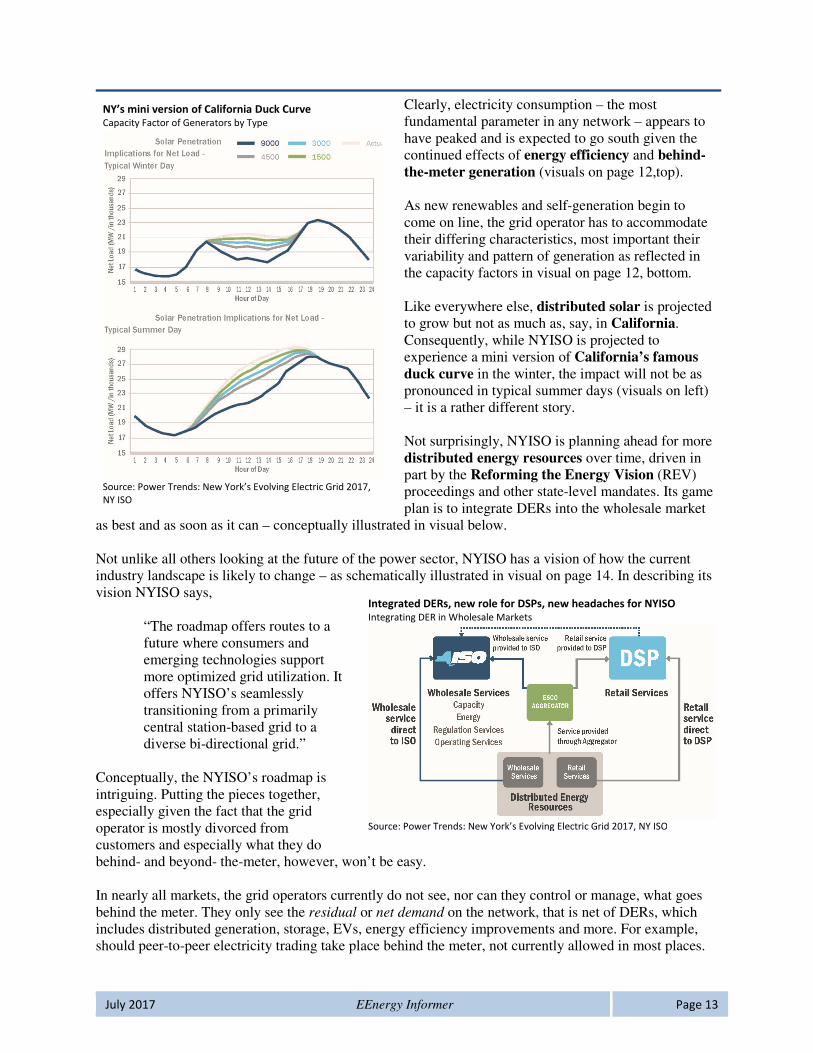

Clearly, electricity consumption – the most fundamental parameter in any network – appears to have peaked and is expected to go south given the continued effects of energy efficiency and behind-the-meter generation (visuals on page 12,top). As new renewables and self-generation begin to come on line, the grid operator has to accommodate their differing characteristics, most important their variability and pattern of generation as reflected in the capacity factors in visual on page 12, bottom. Like everywhere else, distributed solar is projected to grow but not as much as, say, in California. Consequently, while NYISO is projected to experience a mini version of California’s famous duck curve in the winter, the impact will not be as pronounced in typical summer days (visuals on left) – it is a rather different story. Not surprisingly, NYISO is planning ahead for more distributed energy resources over time, driven in part by the Reforming the Energy Vision (REV) proceedings and other state-level mandates. Its game plan is to integrate DERs into the wholesale market

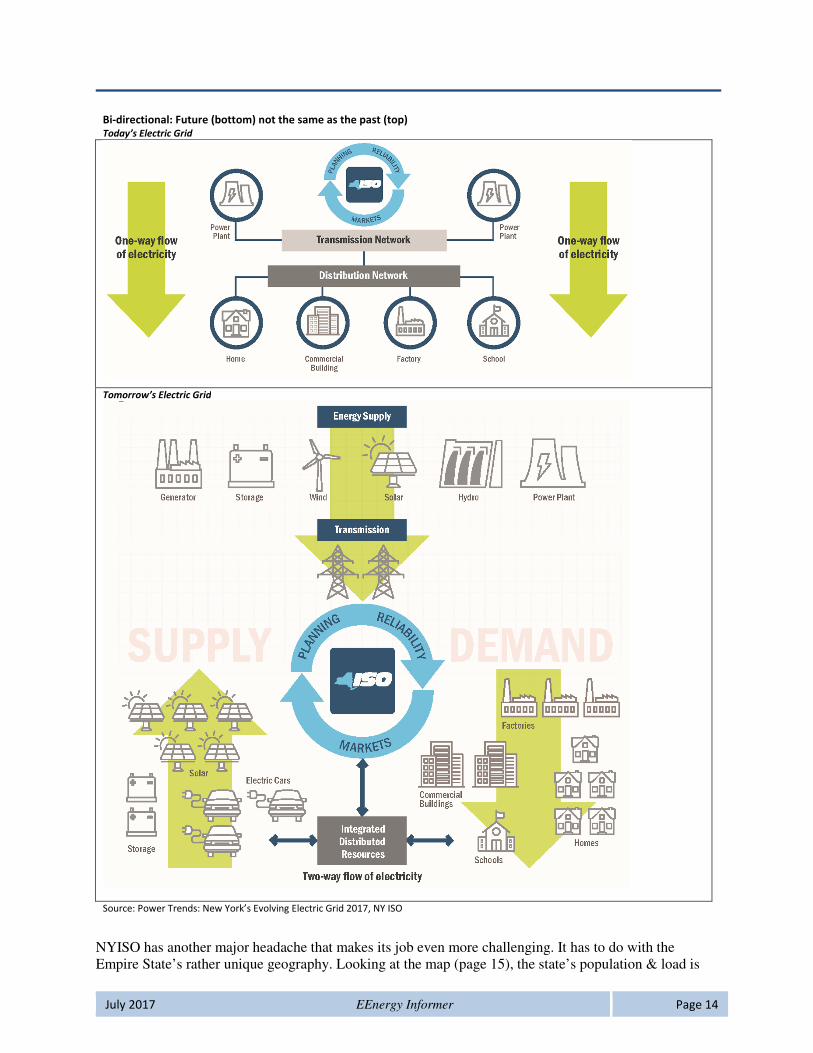

as best and as soon as it can – conceptually illustrated in visual below. Not unlike all others looking at the future of the power sector, NYISO has a vision of how the current industry landscape is likely to change – as schematically illustrated in visual on page 14. In describing its vision NYISO says,

“The roadmap offers routes to a future where consumers and emerging technologies support more optimized grid utilization. It offers NYISO’s seamlessly transitioning from a primarily central station-based grid to a diverse bi-directional grid.”

Conceptually, the NYISO’s roadmap is intriguing. Putting the pieces together, especially given the fact that the grid operator is mostly divorced from customers and especially what they do behind- and beyond- the-meter, however, won’t be easy. In nearly all markets, the grid operators currently do not see, nor can they control or manage, what goes behind the meter. They only see the residual or net demand on the network, that is net of DERs, which includes distributed generation, storage, EVs, energy efficiency improvements and more. For example, should peer-to-peer electricity trading take place behind the meter, not currently allowed in most places.

Integrated DERs, new role for DSPs, new headaches for NYISO Integrating DER in Wholesale Markets

Source: Power Trends: New York’s Evolving Electric Grid 2017, NY ISO

NY’s mini version of California Duck Curve Capacity Factor of Generators by Type

Source: Power Trends: New York’s Evolving Electric Grid 2017,

NY ISO

14July 2017 EEnergy Informer Page 14

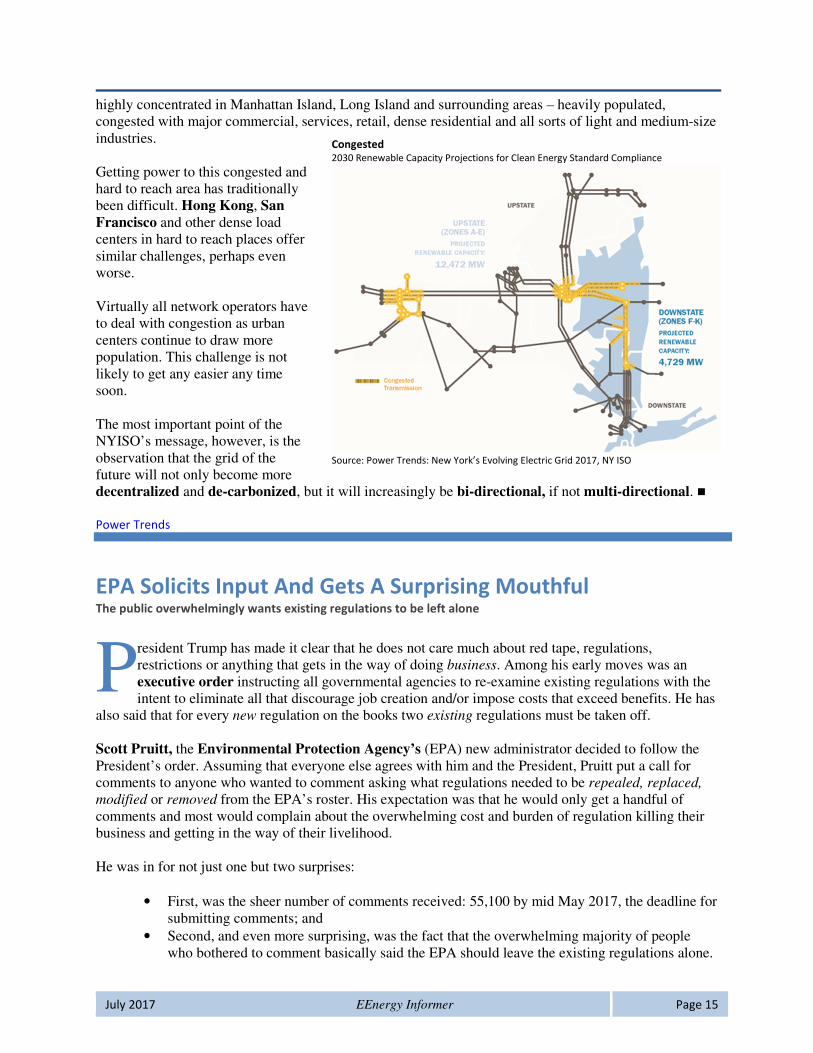

NYISO has another major headache that makes its job even more challenging. It has to do with the Empire State’s rather unique geography. Looking at the map (page 15), the state’s population & load is

Bi-directional: Future (bottom) not the same as the past (top) Today’s Electric Grid

Tomorrow’s Electric Grid

Source: Power Trends: New York’s Evolving Electric Grid 2017, NY ISO

15July 2017 EEnergy Informer Page 15

highly concentrated in Manhattan Island, Long Island and surrounding areas – heavily populated, congested with major commercial, services, retail, dense residential and all sorts of light and medium-size industries. Getting power to this congested and hard to reach area has traditionally been difficult. Hong Kong, San Francisco and other dense load centers in hard to reach places offer similar challenges, perhaps even worse. Virtually all network operators have to deal with congestion as urban centers continue to draw more population. This challenge is not likely to get any easier any time soon. The most important point of the NYISO’s message, however, is the observation that the grid of the future will not only become more decentralized and de-carbonized, but it will increasingly be bi-directional, if not multi-directional. � Power Trends

EPA Solicits Input And Gets A Surprising Mouthful The public overwhelmingly wants existing regulations to be left alone

resident Trump has made it clear that he does not care much about red tape, regulations, restrictions or anything that gets in the way of doing business. Among his early moves was an executive order instructing all governmental agencies to re-examine existing regulations with the intent to eliminate all that discourage job creation and/or impose costs that exceed benefits. He has

also said that for every new regulation on the books two existing regulations must be taken off. Scott Pruitt, the Environmental Protection Agency’s (EPA) new administrator decided to follow the President’s order. Assuming that everyone else agrees with him and the President, Pruitt put a call for comments to anyone who wanted to comment asking what regulations needed to be repealed, replaced,

modified or removed from the EPA’s roster. His expectation was that he would only get a handful of comments and most would complain about the overwhelming cost and burden of regulation killing their business and getting in the way of their livelihood. He was in for not just one but two surprises:

• First, was the sheer number of comments received: 55,100 by mid May 2017, the deadline for submitting comments; and

• Second, and even more surprising, was the fact that the overwhelming majority of people who bothered to comment basically said the EPA should leave the existing regulations alone.

P

Congested 2030 Renewable Capacity Projections for Clean Energy Standard Compliance

Source: Power Trends: New York’s Evolving Electric Grid 2017, NY ISO

16July 2017 EEnergy Informer Page 16

Surely not what Pruitt had expected or wanted to hear. And this editor suspects not the kind of feedback he would want to share with the President, or anyone else, for that matter. As reported in a 16 May article in The Washington Post, a large number of Americans recalled their experiences of growing up with dirty air and water. They pleaded to EPA not to undue the safeguards that could return the country to its polluted past. Few noteworthy excerpts from the comments received as reported by The Washington Post:

• “Environmental regulations came about for a reason;”

• “If anything, regulations need to be more stringent;”

• “Regulations are PROTECTIONS. Please enforce all existing clean air and water protections and consider creating more;”

• “So here are my thoughts on doing away with existing EPA regulations, or doing away with the EPA itself: ARE YOU BLOODY CRAZY?????”

• One commenter simply wrote the word “No” over and over, 1,665 times;

• “I implore you, as defenders of our nation’s health and security, to avoid shortsighted steps that might create prosperity for a few in the short term, at the expense of the many in the long term.”

To be fair, few smallish businesses complained about excessive and unnecessary regulations stifling their livelihood. That is to be expected. If you ask any business owner how much regulation they want or need, the answer is inevitably as little as possible, preferably none. Take away regulations, however, and many businesses will dump their waste in the air, water or soil – if they can get away with it. Labor safety and security will get lip service, if that, if there are no inspectors and no fines. If there are no speed limits and no cops enforcing them, drivers will speed, and fewer would wear safety belts. This explains why so few people want to go back to the dawn of the Industrial Revolution when regulation did not exist. Not surprisingly, the dominant message to the EPA, according to The Washington Post was do not “jettison protections for clean water and clean air in the name of reducing burdens on corporations.” Dumbfounded by the comments received, EPA said a task force will examine the comments and submit a progress report to Pruitt. Don’t hold your breath. In March 2017, EPA said it was withdrawing a requirement that operators of existing oil and gas wells to report any leakage of methane from their oil or gas wells since it was “burdensome and costly.” And Pruitt recently refused to ban a commonly used pesticide that the Obama Administration had sought to outlaw based on mounting concerns about its risks to human health.

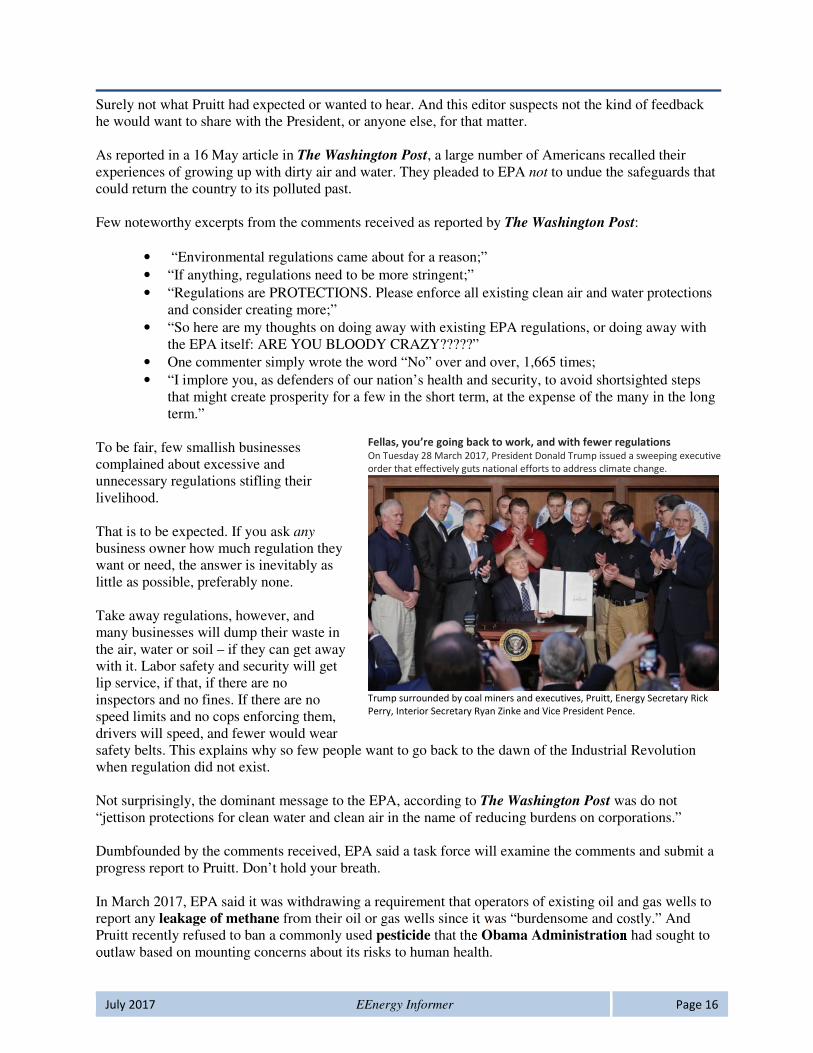

Fellas, you’re going back to work, and with fewer regulations On Tuesday 28 March 2017, President Donald Trump issued a sweeping executive

order that effectively guts national efforts to address climate change.

Trump surrounded by coal miners and executives, Pruitt, Energy Secretary Rick

Perry, Interior Secretary Ryan Zinke and Vice President Pence.

17July 2017 EEnergy Informer Page 17

Regulation may be costly, burdensome and seem unnecessary. Lack of regulation, however, could be even worse – and that is not a message that Pruitt is likely to draw from the feedback received. �

EPA asked the public which regulations to gut — and got an earful about leaving them alone

16 May, Brady Dennis, Washington Post

UBS Predicts EV Price Parity By 2018 If not 2018, soon after

n May 2017 UBS reported that electric vehicles (EVs) could reach price parity with internal combustion engines (ICEs) as early as 2018 – that is next year. This, of course, is not to say that the purchase price of an EV would match that of an ICE, but the total ownership cost, including fuel, operating and maintenance costs of the two

would be equal over the life of the cars. EVs may cost more to buy, but they have few moving parts, requiring far less replacement and maintenance. And depending on assumptions about cost of petrol vs. electricity, EVs tend to have much lower operating costs since they are far more efficient in delivering the energy to the wheels. Not only fewer moving parts, but no radiator, no pumps, no belts, no mufflers, no exhaust pipe, etc. etc. The UBS study said, “This will create an inflection point for demand. We raise our 2025 forecast for EV sales by 50% to 14.2 million — 14% of global car sales.” There are, of course, as many predictions on how fast EV sales will penetrate the car market, as there are studies, but the numbers are generally creeping up as more automakers enter the fray, offering an ever-increasing array of all electric and hybrid vehicles, no longer targeted at the up-scale end of the market but for the common folks.

What is noteworthy about UBS’ 14% by 2025 prediction is that it is nearly identical to the state of California’s target of 15% by the same date. But UBS is talking about global demand. If such predictions prove real, it spells trouble for traditional automakers who must switch form ICEs to EVs. Even more troubling are the fortunes of thousands of ICE component and parts manufacturers whose livelihood depends on the continued sales of such vehicles.

I If Pope goes electric, so will everyone else Opel CEO Karl-Thomas Neumann presented Pope Francis with an Opel

Ampera-e, a rebranded Chevy Bolt EV, at the recent Laudato Si

sustainability conference

Source: Cleantechnica

Tesla ties GM – Market valuation in $B, on 10 April 2017

18July 2017 EEnergy Informer Page 18

The UBS study warns manufacturers of components and replacement parts of the impending doom. EV drivetrains are far simpler, have far fewer parts and do not wear out as often as those in ICEs. UBS figures a typical gasoline engine may have as many as 1,000 moving parts compared to a handful in an EV. Car repair shops, mechanics, muffler stores, those fixing radiators and many others are also in jeopardy since many such services would not be needed in a future increasingly dominated by EVs. The biggest impact, of course, will be on big oil if EVs begin to replace ICEs in large numbers as some analysts are predicting. It is not entirely clear if major oil companies are taking this threat seriously. Automakers, on the other hand, appear to have concluded that the future of mobility will increasingly be electric. �

China On Top As US recedes inward, China is poised to fill the void, on multiple dimensions

rnst & Young, now simply called EY, publishes an annual renewable energy country attractiveness index (RECAI), ranking countries based on their overall attractiveness to renewable energy investments. It is a somewhat subjective index, yet it gets noticed. This year’s report, released in May 2017 ranks China on top, followed by India, US, Germany and –

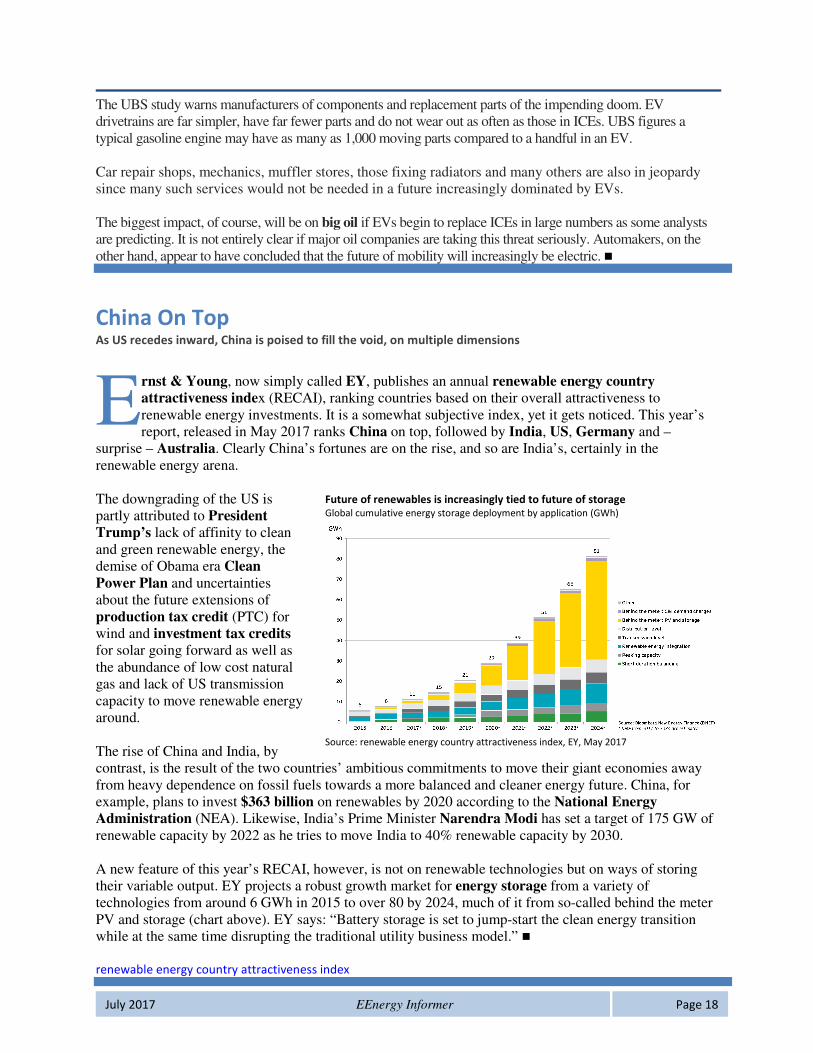

surprise – Australia. Clearly China’s fortunes are on the rise, and so are India’s, certainly in the renewable energy arena. The downgrading of the US is partly attributed to President Trump’s lack of affinity to clean and green renewable energy, the demise of Obama era Clean Power Plan and uncertainties about the future extensions of production tax credit (PTC) for wind and investment tax credits for solar going forward as well as the abundance of low cost natural gas and lack of US transmission capacity to move renewable energy around. The rise of China and India, by contrast, is the result of the two countries’ ambitious commitments to move their giant economies away from heavy dependence on fossil fuels towards a more balanced and cleaner energy future. China, for example, plans to invest $363 billion on renewables by 2020 according to the National Energy Administration (NEA). Likewise, India’s Prime Minister Narendra Modi has set a target of 175 GW of renewable capacity by 2022 as he tries to move India to 40% renewable capacity by 2030. A new feature of this year’s RECAI, however, is not on renewable technologies but on ways of storing their variable output. EY projects a robust growth market for energy storage from a variety of technologies from around 6 GWh in 2015 to over 80 by 2024, much of it from so-called behind the meter PV and storage (chart above). EY says: “Battery storage is set to jump-start the clean energy transition while at the same time disrupting the traditional utility business model.” � renewable energy country attractiveness index

EFuture of renewables is increasingly tied to future of storage Global cumulative energy storage deployment by application (GWh)

Source: renewable energy country attractiveness index, EY, May 2017

19July 2017 EEnergy Informer Page 19

Nuclear’s Prospects Not Encouraging Only a handful of countries are still committed to the atom

ith a few exceptions, the prospects for future of nuclear power do not seem encouraging. And aside from a miracle, such a universal and hefty carbon tax or similar scheme heavily favorable to carbon-free nuclear generation, it is hard to imagine a major turnaround any time soon. Consider the following recent developments as examples of the strong headwind facing

nuclear power:

� Switzerland – In a referendum in late May 2017, over 58% of Swiss voters endorsed Energy Strategy 2050, which includes a gradual phase out of the country’s 5 existing reactors and no new ones once they are retired. The strategy relies on more renewables, in addition to existing hydro, and an ambitious plan to reduce per capita energy consumption: 16% by 2020 and 43% by 2035 from 2000 levels.

� France – Newly elected President Emmanuel Macron has announced an equally ambitious

renewable energy agenda with – shall we say – less emphasis on nuclear over time, understandable for a country that currently gets nearly 75% of its electricity from the atom.

� South Korea – Also with newly elected president Moon Jae-in, the country is shifting its

energy strategy away from heavy reliance on coal and nuclear to a more balanced portfolio which includes increased use of natural gas and renewables. As currently planned, gas-fired generation’s share is expected to rise from around 18% of the power mix to 27% by 2030, while the share of renewables including hydropower would rise from 5% to 20%. This will result in a shrinking share of coal from 40% to 22% and that of nuclear from 30% to 22%.

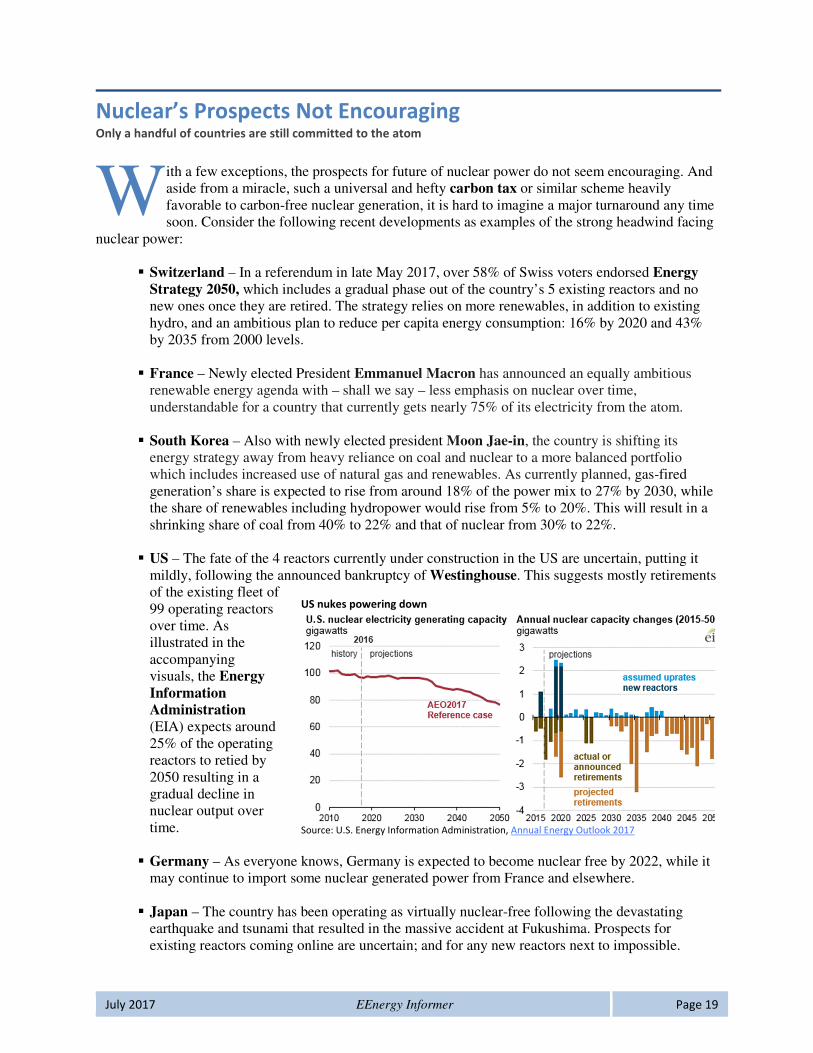

� US – The fate of the 4 reactors currently under construction in the US are uncertain, putting it

mildly, following the announced bankruptcy of Westinghouse. This suggests mostly retirements of the existing fleet of 99 operating reactors over time. As illustrated in the accompanying visuals, the Energy Information Administration (EIA) expects around 25% of the operating reactors to retied by 2050 resulting in a gradual decline in nuclear output over time.

� Germany – As everyone knows, Germany is expected to become nuclear free by 2022, while it

may continue to import some nuclear generated power from France and elsewhere. � Japan – The country has been operating as virtually nuclear-free following the devastating

earthquake and tsunami that resulted in the massive accident at Fukushima. Prospects for existing reactors coming online are uncertain; and for any new reactors next to impossible.

W

US nukes powering down

Source: U.S. Energy Information Administration, Annual Energy Outlook 2017

20July 2017 EEnergy Informer Page 20

� UK – The country is officially on track for building Hinkley Point C, its first new reactor in 20 years. But with Brexit and a host of related issues, don’t hold your breath for seeing its completion any time soon.

That leaves China, Russia, India and a handful of others as the main growth markets for nuclear power. It is a club with shrinking membership. �

Making America Inefficient Again Trump Administration’s budget proposal guts energy efficiency

andidate Trump, and now President Trump’s favorite saying is to “Make America great again.” He likes the slogan so much that he has a patent on it. While how he plans to deliver on that promise remains to be seen, there are indications that he is making excellent progress on making America inefficient again. At least that is what the American Council for an Energy Efficient

Economy (ACEEE), a non-profit energy efficiency advocacy organization, believes. Commenting on President Trump’s budget proposal in late May 2017, Lowell Ungar, ACEEE’s Sr. Policy Advisor said, “We appreciate the budgetary goals of creating jobs, generating wealth, and putting the taxpayer first. But cutting energy efficiency programs does the opposite.” Highlights of Trump’s proposed budget cuts as identified by ACEEE are shown below. The percentages refer to proposed cuts, with 100% indicating total elimination of budget. DOE’s Energy Efficiency and Renewable Energy Office

� Building Technologies Office 66% � Advanced Manufacturing Office 68% � Vehicle Technologies Office 73% � Weatherization Assistance Program 100% � State Energy Program 100% � Federal Energy Management Program 63%

Environmental Protection Agency

� ENERGY STAR 100% � Vehicle Standards and Certification 25%

Energy efficiency, according to ACEEE, employs some 2.2 million Americans, while saving billions in fuel and energy costs and in lowering greenhouse gas emissions. While supporting fossil fuels and attempting to revive a dying coal industry, the Trump Administration appears totally uninterested in renewables (following article) and even more so in energy efficiency or R&D. The path for making American great again rests on more fossil fuels, more greenhouse gas emissions, less efficient cars and apparently less efficient everything else. � Making America inefficient: the budget’s gory details, 24 May 2017, Lowell Ungar

C

21July 2017 EEnergy Informer Page 21

California Senate Passes 100% Renewable Bill If passed by the lower assembly, Governor most likely to sign into law

t the end of May 2017, with a vote of 25-13, California’s State Senate passed Senator Kevin de Leon’s bill, SB 100. If approved by the State Assembly, it will most likely be signed into law by Governor Jerry Brown. He is a big proponent of renewables as energy sources of the future as well as creators of jobs and economic prosperity. The pending bill requires moving the

current 50% target for renewable portfolio standard (RPS) from 2030 to 2026 while requiring a 100% renewable electricity mix by 2045. Among the states, only Hawaii currently has such an ambitious target for 2045.

In announcing the landmark vote, Senate Pro Tem, De Leon, said, “Today, we passed the most ambitious target in the world to expand clean energy and put Californians to work.” The vote was supported by the environmentalists across the country. It stands in stark contrast with what has been coming out of Washington, DC lately.

If passed by the lower house and signed into law, it will – in time – make all kWhs sold in California to be clean and green, obviating the need to pay a premium for the green electrons, sign PPAs with a renewable supplier, buy renewable energy certificates or any of the above. It will also have implications for anyone selling greener electricity as further described in the following article. �

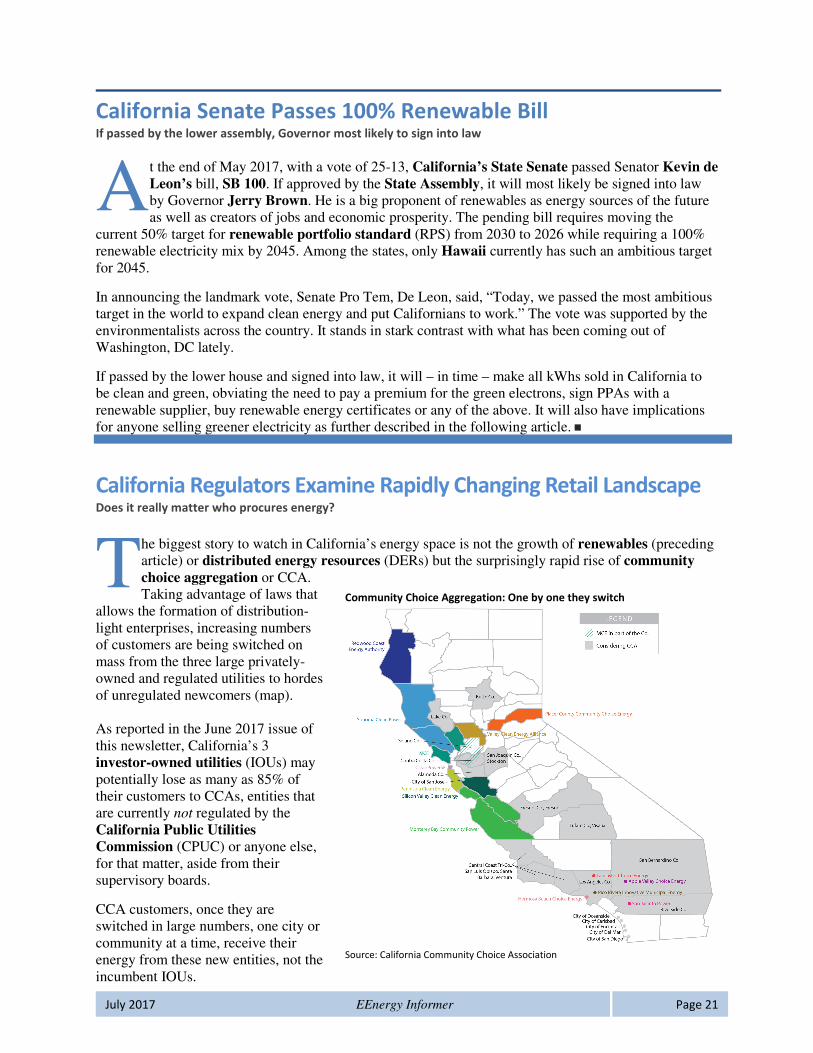

California Regulators Examine Rapidly Changing Retail Landscape

Does it really matter who procures energy?

he biggest story to watch in California’s energy space is not the growth of renewables (preceding article) or distributed energy resources (DERs) but the surprisingly rapid rise of community choice aggregation or CCA. Taking advantage of laws that

allows the formation of distribution-light enterprises, increasing numbers of customers are being switched on mass from the three large privately-owned and regulated utilities to hordes of unregulated newcomers (map). As reported in the June 2017 issue of this newsletter, California’s 3 investor-owned utilities (IOUs) may potentially lose as many as 85% of their customers to CCAs, entities that are currently not regulated by the California Public Utilities Commission (CPUC) or anyone else, for that matter, aside from their supervisory boards.

CCA customers, once they are switched in large numbers, one city or community at a time, receive their energy from these new entities, not the incumbent IOUs.

A

TCommunity Choice Aggregation: One by one they switch

Source: California Community Choice Association

22July 2017 EEnergy Informer Page 22

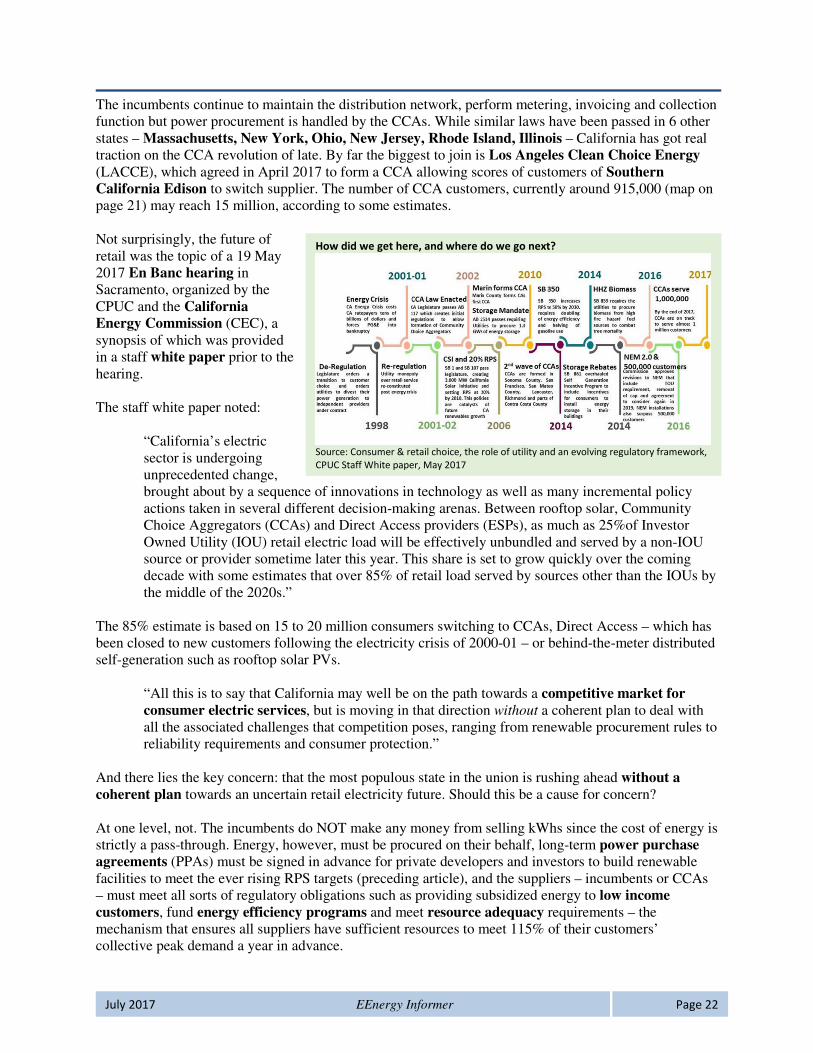

The incumbents continue to maintain the distribution network, perform metering, invoicing and collection function but power procurement is handled by the CCAs. While similar laws have been passed in 6 other states – Massachusetts, New York, Ohio, New Jersey, Rhode Island, Illinois – California has got real traction on the CCA revolution of late. By far the biggest to join is Los Angeles Clean Choice Energy (LACCE), which agreed in April 2017 to form a CCA allowing scores of customers of Southern California Edison to switch supplier. The number of CCA customers, currently around 915,000 (map on page 21) may reach 15 million, according to some estimates. Not surprisingly, the future of retail was the topic of a 19 May 2017 En Banc hearing in Sacramento, organized by the CPUC and the California Energy Commission (CEC), a synopsis of which was provided in a staff white paper prior to the hearing. The staff white paper noted:

“California’s electric sector is undergoing unprecedented change, brought about by a sequence of innovations in technology as well as many incremental policy actions taken in several different decision-making arenas. Between rooftop solar, Community Choice Aggregators (CCAs) and Direct Access providers (ESPs), as much as 25%of Investor Owned Utility (IOU) retail electric load will be effectively unbundled and served by a non-IOU source or provider sometime later this year. This share is set to grow quickly over the coming decade with some estimates that over 85% of retail load served by sources other than the IOUs by the middle of the 2020s.”

The 85% estimate is based on 15 to 20 million consumers switching to CCAs, Direct Access – which has been closed to new customers following the electricity crisis of 2000-01 – or behind-the-meter distributed self-generation such as rooftop solar PVs.

“All this is to say that California may well be on the path towards a competitive market for consumer electric services, but is moving in that direction without a coherent plan to deal with all the associated challenges that competition poses, ranging from renewable procurement rules to reliability requirements and consumer protection.”

And there lies the key concern: that the most populous state in the union is rushing ahead without a coherent plan towards an uncertain retail electricity future. Should this be a cause for concern? At one level, not. The incumbents do NOT make any money from selling kWhs since the cost of energy is strictly a pass-through. Energy, however, must be procured on their behalf, long-term power purchase agreements (PPAs) must be signed in advance for private developers and investors to build renewable facilities to meet the ever rising RPS targets (preceding article), and the suppliers – incumbents or CCAs – must meet all sorts of regulatory obligations such as providing subsidized energy to low income customers, fund energy efficiency programs and meet resource adequacy requirements – the mechanism that ensures all suppliers have sufficient resources to meet 115% of their customers’ collective peak demand a year in advance.

How did we get here, and where do we go next?

Source: Consumer & retail choice, the role of utility and an evolving regulatory framework,

CPUC Staff White paper, May 2017

23July 2017 EEnergy Informer Page 23

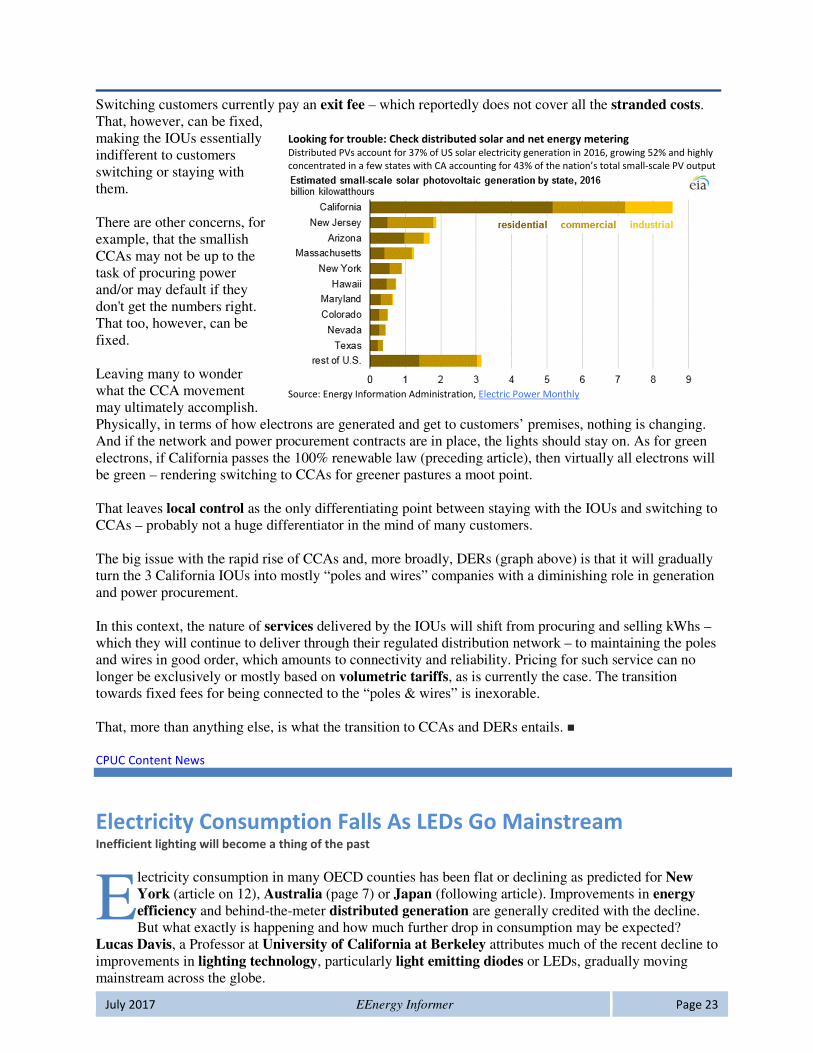

Looking for trouble: Check distributed solar and net energy metering Distributed PVs account for 37% of US solar electricity generation in 2016, growing 52% and highly

concentrated in a few states with CA accounting for 43% of the nation’s total small-scale PV output

Source: Energy Information Administration, Electric Power Monthly

Switching customers currently pay an exit fee – which reportedly does not cover all the stranded costs. That, however, can be fixed, making the IOUs essentially indifferent to customers switching or staying with them. There are other concerns, for example, that the smallish CCAs may not be up to the task of procuring power and/or may default if they don't get the numbers right. That too, however, can be fixed. Leaving many to wonder what the CCA movement may ultimately accomplish. Physically, in terms of how electrons are generated and get to customers’ premises, nothing is changing. And if the network and power procurement contracts are in place, the lights should stay on. As for green electrons, if California passes the 100% renewable law (preceding article), then virtually all electrons will be green – rendering switching to CCAs for greener pastures a moot point. That leaves local control as the only differentiating point between staying with the IOUs and switching to CCAs – probably not a huge differentiator in the mind of many customers. The big issue with the rapid rise of CCAs and, more broadly, DERs (graph above) is that it will gradually turn the 3 California IOUs into mostly “poles and wires” companies with a diminishing role in generation and power procurement. In this context, the nature of services delivered by the IOUs will shift from procuring and selling kWhs – which they will continue to deliver through their regulated distribution network – to maintaining the poles and wires in good order, which amounts to connectivity and reliability. Pricing for such service can no longer be exclusively or mostly based on volumetric tariffs, as is currently the case. The transition towards fixed fees for being connected to the “poles & wires” is inexorable. That, more than anything else, is what the transition to CCAs and DERs entails. � CPUC Content News

Electricity Consumption Falls As LEDs Go Mainstream Inefficient lighting will become a thing of the past

lectricity consumption in many OECD counties has been flat or declining as predicted for New York (article on 12), Australia (page 7) or Japan (following article). Improvements in energy efficiency and behind-the-meter distributed generation are generally credited with the decline. But what exactly is happening and how much further drop in consumption may be expected?

Lucas Davis, a Professor at University of California at Berkeley attributes much of the recent decline to improvements in lighting technology, particularly light emitting diodes or LEDs, gradually moving mainstream across the globe.

E

24July 2017 EEnergy Informer Page 24

Latest data from the Energy Information Administration (IEA) agrees, attributing the falling costs of LEDs and their superior performance among the main reasons. In a blog posted on 8 May 2017, Prof. Davis points out that:

“Americans tend to use more and more of everything. As incomes have risen, we buy more food, live in larger homes, travel more, spend more on health care, and, yes, use more energy.”

Not surprisingly,

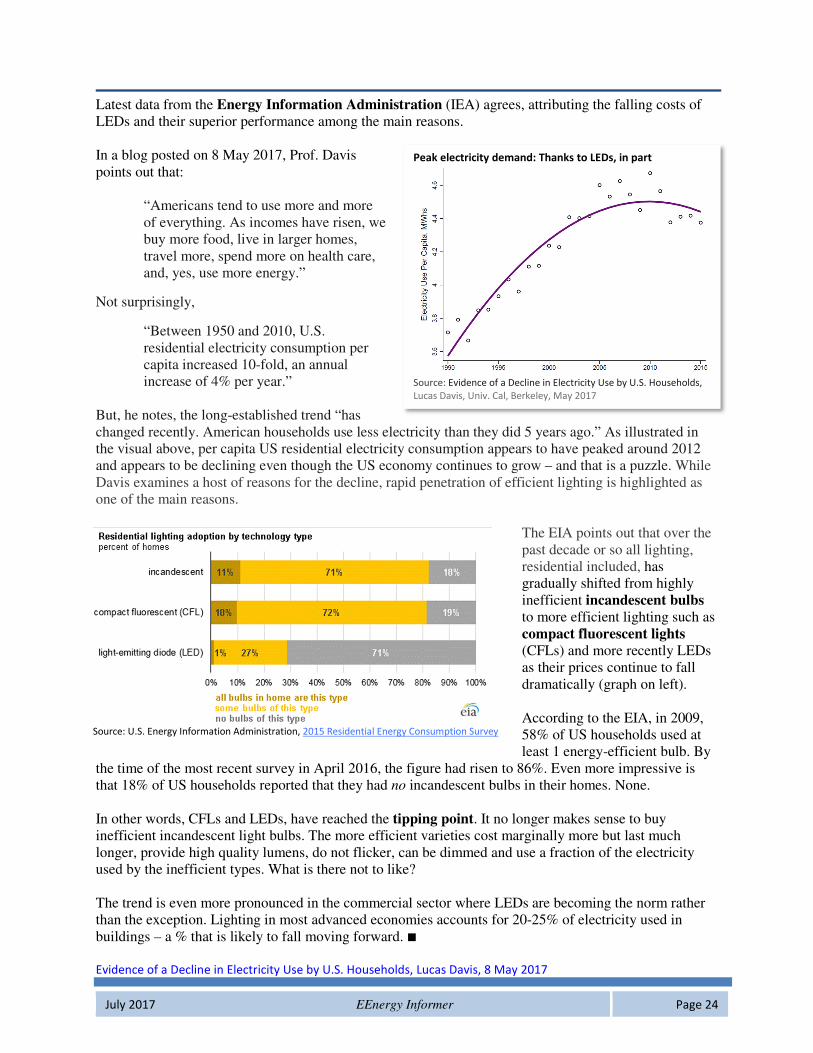

“Between 1950 and 2010, U.S. residential electricity consumption per capita increased 10-fold, an annual increase of 4% per year.”

But, he notes, the long-established trend “has changed recently. American households use less electricity than they did 5 years ago.” As illustrated in the visual above, per capita US residential electricity consumption appears to have peaked around 2012 and appears to be declining even though the US economy continues to grow – and that is a puzzle. While Davis examines a host of reasons for the decline, rapid penetration of efficient lighting is highlighted as one of the main reasons.

The EIA points out that over the past decade or so all lighting, residential included, has gradually shifted from highly inefficient incandescent bulbs to more efficient lighting such as compact fluorescent lights (CFLs) and more recently LEDs as their prices continue to fall dramatically (graph on left). According to the EIA, in 2009, 58% of US households used at least 1 energy-efficient bulb. By

the time of the most recent survey in April 2016, the figure had risen to 86%. Even more impressive is that 18% of US households reported that they had no incandescent bulbs in their homes. None. In other words, CFLs and LEDs, have reached the tipping point. It no longer makes sense to buy inefficient incandescent light bulbs. The more efficient varieties cost marginally more but last much longer, provide high quality lumens, do not flicker, can be dimmed and use a fraction of the electricity used by the inefficient types. What is there not to like? The trend is even more pronounced in the commercial sector where LEDs are becoming the norm rather than the exception. Lighting in most advanced economies accounts for 20-25% of electricity used in buildings – a % that is likely to fall moving forward. � Evidence of a Decline in Electricity Use by U.S. Households, Lucas Davis, 8 May 2017

Source: U.S. Energy Information Administration, 2015 Residential Energy Consumption Survey

Peak electricity demand: Thanks to LEDs, in part

Source: Evidence of a Decline in Electricity Use by U.S. Households,

Lucas Davis, Univ. Cal, Berkeley, May 2017

25July 2017 EEnergy Informer Page 25

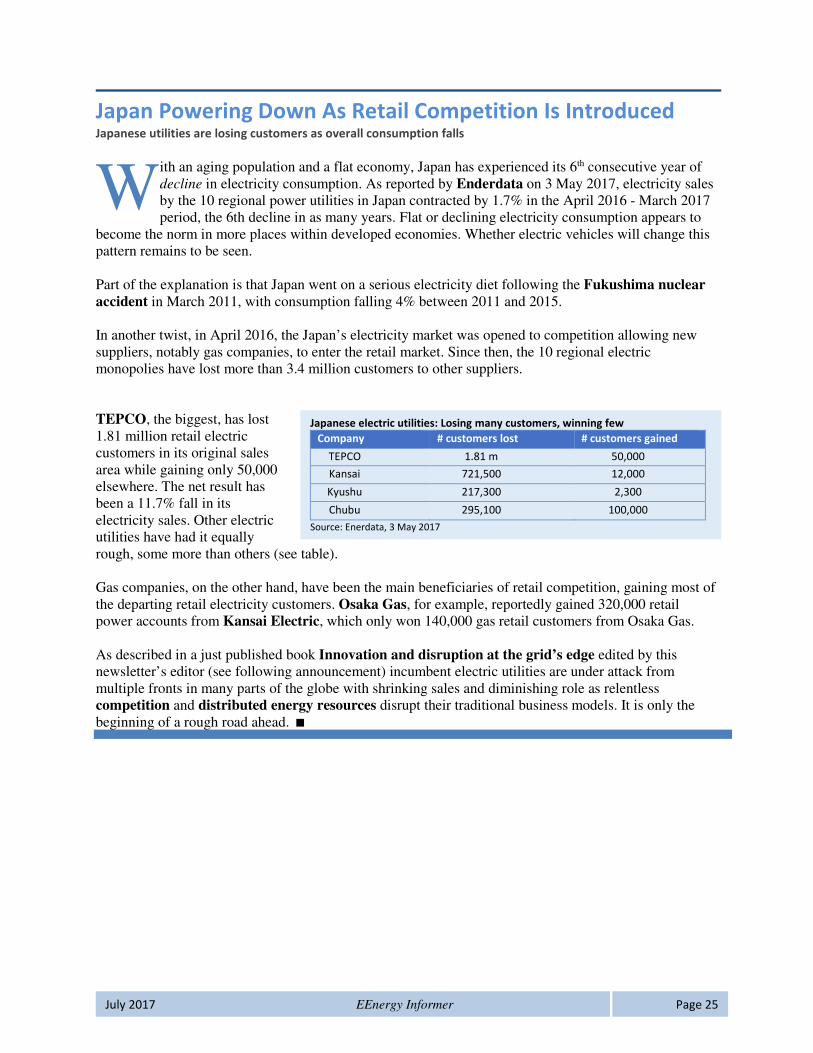

Japan Powering Down As Retail Competition Is Introduced Japanese utilities are losing customers as overall consumption falls

ith an aging population and a flat economy, Japan has experienced its 6th consecutive year of decline in electricity consumption. As reported by Enderdata on 3 May 2017, electricity sales by the 10 regional power utilities in Japan contracted by 1.7% in the April 2016 - March 2017 period, the 6th decline in as many years. Flat or declining electricity consumption appears to

become the norm in more places within developed economies. Whether electric vehicles will change this pattern remains to be seen. Part of the explanation is that Japan went on a serious electricity diet following the Fukushima nuclear accident in March 2011, with consumption falling 4% between 2011 and 2015. In another twist, in April 2016, the Japan’s electricity market was opened to competition allowing new suppliers, notably gas companies, to enter the retail market. Since then, the 10 regional electric monopolies have lost more than 3.4 million customers to other suppliers. TEPCO, the biggest, has lost 1.81 million retail electric customers in its original sales area while gaining only 50,000 elsewhere. The net result has been a 11.7% fall in its electricity sales. Other electric utilities have had it equally rough, some more than others (see table). Gas companies, on the other hand, have been the main beneficiaries of retail competition, gaining most of the departing retail electricity customers. Osaka Gas, for example, reportedly gained 320,000 retail power accounts from Kansai Electric, which only won 140,000 gas retail customers from Osaka Gas. As described in a just published book Innovation and disruption at the grid’s edge edited by this newsletter’s editor (see following announcement) incumbent electric utilities are under attack from multiple fronts in many parts of the globe with shrinking sales and diminishing role as relentless competition and distributed energy resources disrupt their traditional business models. It is only the beginning of a rough road ahead. �

W

Japanese electric utilities: Losing many customers, winning few

Company # customers lost # customers gained

TEPCO 1.81 m 50,000

Kansai 721,500 12,000

Kyushu 217,300 2,300

Chubu 295,100 100,000

Source: Enerdata, 3 May 2017

26July 2017 EEnergy Informer Page 26

Just published:

Innovation and Disruption at the Grid’s Edge

Special 30% discount offer for EEnergy Informer subscribers

EEnergy Informer subscribers are entitled to a 30% discount when ordering copies of the just published book,

Innovation and Disruption at the Grid’s Edge, with further details provided at the end of this month’s newsletter.

The link below will take you directly to the publisher's website and a 30% discount code ENER317, which you can

apply at checkout, free shipping included. Please share with others who may be interested in ordering a copy.

https://www.elsevier.com/books/innovation-and-disruption-at-the-grid-s-edge/sioshansi/978-0-12-811758-

3?start_rank=1&producttype=books&sortby=sortByRelevance&q=sioshansi

EEnergy Informer subscription prices

EEnergy Informer is available by subscription only at the following options/prices:

Subscription type Annual price

• Regular subscription $450

Single reader, no distribution

• Discounted subscription $300

Small business, single reader, no distribution

• Limited site license $900

Distribution limited to 4 readers in same organization, single location

• Unlimited site license $1,800

Unlimited distribution within same organization including multiple locations

• Student subscription $150

Limited to students & qualified solo professionals (Please inquire if you qualify for this special discounted price)

How to subscribe to EEnergy Informer

To extend existing or start new subscription to EEnergy Informer visit

website www.eenergyinformer.com under toolbar SUBSCRIBE TO

EENERGY INFORMER and select the appropriate price. You will be

prompted to provide credit card details, which are securely handled

through PayPal. You will get an instant electronic transaction receipt

and we will get notification of payment. You do NOT need a PayPal

account and need NOT be a current PayPal user.

If you require a customized invoice &/or prefer to wire funds directly

to our bank, please contact us at [email protected]. If you are

paying with a check, it must be in US$, payable to EEnergy Informer

and mailed to 1925 Nero CT, Walnut Creek, CA 94598, USA. Any

questions or if you experience problems with the PayPal payment

system, kindly notify us at [email protected] or the editor at

EEnergy Informer

Copyright © 2017

July 2017, Vol. 27, No. 7

ISSN: 1084-0419

http://www.eenergyinformer.com

EEnergy Informer is an independent

newsletter providing news, analysis,

and commentary on the global

electric power sector.

For all inquiries contact

Fereidoon P. Sioshansi, PhD

Editor and Publisher

1925 Nero Court

Walnut Creek, CA 94598, USA

Tel: +1-925-256-1484

Mobile: +1-650-207-4902

e-mail: [email protected]

Published monthly in electronic format.

Annual subscription rates in USD:

Regular $450

Discounted $300

Limited site license $900

Unlimited site license $1,800

Student/special rate $150

27July 2017 EEnergy Informer Page 27

28July 2017 EEnergy Informer Page 28