Embed Size (px)

Citation preview

First Empire Securities, Inc.(800) 645-5424 www.1empire.com

Effective Liquidity Management

Presented by: Frank Santucci

Managing Director ALM [email protected]

CUNA CFO Council Conference

New Orleans, LouisianaMay 2015

First Empire Securities, Inc.(800) 645-5424 www.1empire.com

Liquidity Risk Management Resources:

NCUA Rules and Regulations Part 741.12 - Liquidity and Contingency Funding Planshttp://www.ncua.gov/Legal/Documents/Regulations/FIR20131024LiquidityContingencyFunding.pdf

FFIEC Interagency Policy Statement on Funding and Liquidity Risk Managementhttp://www.ncua.gov/Resources/Documents/LCU2010-14Encl.pdf

NCUA AIRES Examination Questionnaire (Liquidity 1, 2, & 3 Worksheets)http://www.ncua.gov/DataApps/Documents/AIRES/question.zip

NCUA Examiner's Guide (Chapter 13, ALM: Section 3 - Liquidity Management) http://www.ncua.gov/Legal/GuidesEtc/ExaminerGuide/chapter13.pdf

NCUA Letter to Credit Unions 13-CU-10 - Guidance on How to Comply with Rule 741.12http://www.ncua.gov/Resources/Documents/LCU2013-10.pdf

NCUA Letter to Credit Unions 10-CU-14 - Strengthening Funding and Liquidity Risk Managementhttp://www.ncua.gov/Resources/Pages/LCU2010-14.aspx

NCUA Letter to Credit Unions 01-CU-19 - Managing Share Inflows in Uncertain Timeshttp://www.ncua.gov/Resources/Documents/LCU2001-19.pdf

NCUA Letter to Credit Unions 01-CU-08 - Highly Rate Sensitive and Volatile Funding Sources http://www.ncua.gov/Resources/Documents/LCU2001-08.pdf

NCUA Letter to Credit Unions 00-CU-13 - Liquidity and Balance Sheet Risk Managementhttp://www.ncua.gov/Resources/Documents/LCU2000-13.pdf

2

First Empire Securities, Inc.(800) 645-5424 www.1empire.com

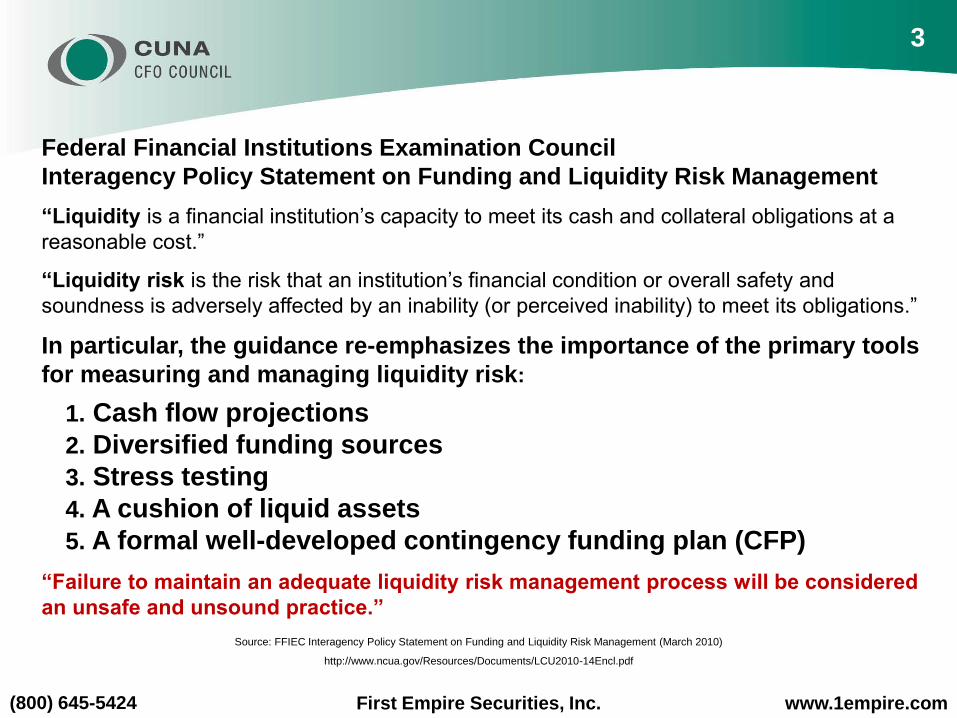

Federal Financial Institutions Examination Council

Interagency Policy Statement on Funding and Liquidity Risk Management

“Liquidity is a financial institution’s capacity to meet its cash and collateral obligations at a

reasonable cost.”

“Liquidity risk is the risk that an institution’s financial condition or overall safety and

soundness is adversely affected by an inability (or perceived inability) to meet its obligations.”

In particular, the guidance re-emphasizes the importance of the primary tools

for measuring and managing liquidity risk:

1. Cash flow projections

2. Diversified funding sources

3. Stress testing

4. A cushion of liquid assets

5. A formal well-developed contingency funding plan (CFP)

“Failure to maintain an adequate liquidity risk management process will be considered

an unsafe and unsound practice.”

Source: FFIEC Interagency Policy Statement on Funding and Liquidity Risk Management (March 2010)

http://www.ncua.gov/Resources/Documents/LCU2010-14Encl.pdf

3

First Empire Securities, Inc.(800) 645-5424 www.1empire.com

Liquidity Examination Ratios

NCUA AIRES Examination Questionnaire (Liquidity 1, 2, & 3 Worksheets)

http://www.ncua.gov/DataApps/Documents/AIRES/question.zip

NCUA Liquidity Examination Questionnaire Ratios Sep-13 Dec-13 Mar-14 Jun-14 Sep-14 Dec-14

Borrow ing+Non-member Deposits/ Shares and Liabilities 3.54% 3.61% 3.50% 4.03% 4.48% 4.51%

Cash & Short Term Assets-to-Total Assets 15.24% 14.93% 16.27% 14.53% 13.10% 13.67%

Regular Shares & Drafts / Total Shares and Borrow ings 25.05% 25.34% 26.58% 26.02% 25.75% 26.58%

Contingent Liabilities/Cash and Investments 44.96% 46.39% 44.52% 47.47% 50.03% 51.13%

Net Liquid Assets / Total Liabilities & Shares 33.24% 32.42% 34.17% 31.94% 29.65% 28.94%

Volatile Liabilities/ Cash+Investments <1yr 144.27% 225.14% 198.57% 224.53% 253.24% 241.20%

Year-over-Year Grow th in Volatile Liabilities/ Assets 0.48% 0.57% 0.55% 0.81% 0.88% 0.87%

Investment Loss Ratio -0.79% -1.06% -0.59% 0.00% -0.21% 0.00%

Estimated Loan Maturity 30 Mo 32 Mo 31 Mo 29 Mo 33 Mo 30 Mo

NCUA AIRES Examination Questionnaire – Liquidity

NCUA has published on their website a copy of the AIRES Examination

Questionnaire. The questionnaire is an Excel workbook containing over one hundred

worksheets/questionnaires the examiner may use in the course of their examination.

These questionnaires cover every aspect of the exam, including liquidity.

In the three liquidity questionnaires there are nine liquidity ratios the examiner will

calculate as well as 123 questions the examiner may ask as part of the examination.

In addition, most of these questions also have an “embedded comment” attached to

the cell. These comments provide additional guidance from NCUA to the examiner,

often describe “best practices,” and highlight various red flags or potential problems.

4

First Empire Securities, Inc.(800) 645-5424 www.1empire.com

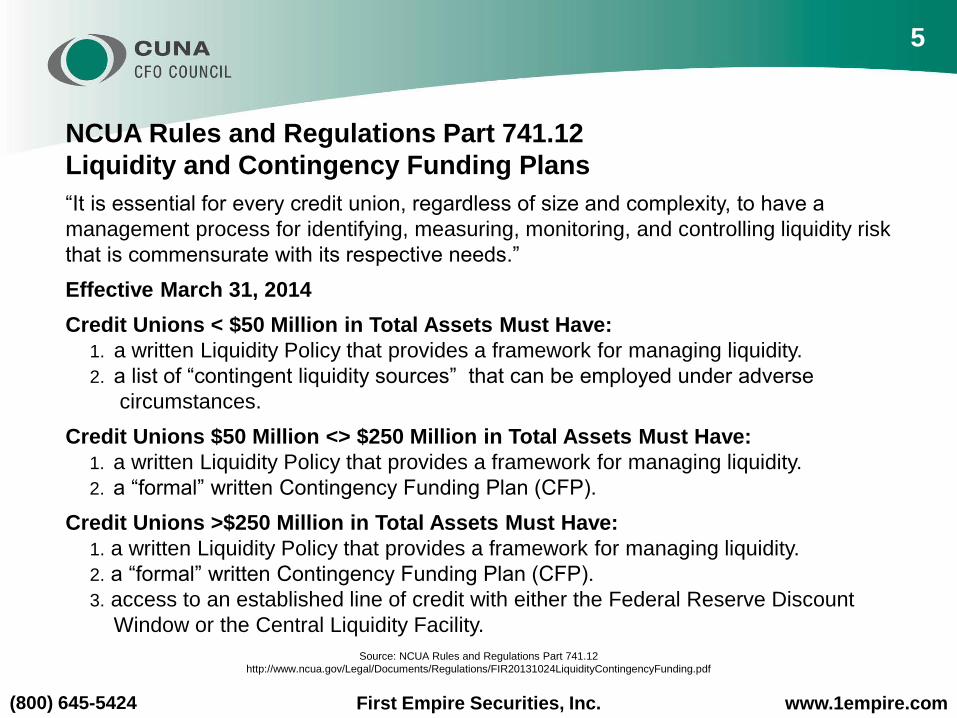

NCUA Rules and Regulations Part 741.12

Liquidity and Contingency Funding Plans

“It is essential for every credit union, regardless of size and complexity, to have a

management process for identifying, measuring, monitoring, and controlling liquidity risk

that is commensurate with its respective needs.”

Effective March 31, 2014

Credit Unions < $50 Million in Total Assets Must Have:

1. a written Liquidity Policy that provides a framework for managing liquidity.

2. a list of “contingent liquidity sources” that can be employed under adverse

circumstances.

Credit Unions $50 Million <> $250 Million in Total Assets Must Have:

1. a written Liquidity Policy that provides a framework for managing liquidity.

2. a “formal” written Contingency Funding Plan (CFP).

Credit Unions >$250 Million in Total Assets Must Have:

1. a written Liquidity Policy that provides a framework for managing liquidity.

2. a “formal” written Contingency Funding Plan (CFP).

3. access to an established line of credit with either the Federal Reserve Discount

Window or the Central Liquidity Facility.

Source: NCUA Rules and Regulations Part 741.12

http://www.ncua.gov/Legal/Documents/Regulations/FIR20131024LiquidityContingencyFunding.pdf

5

First Empire Securities, Inc.(800) 645-5424 www.1empire.com

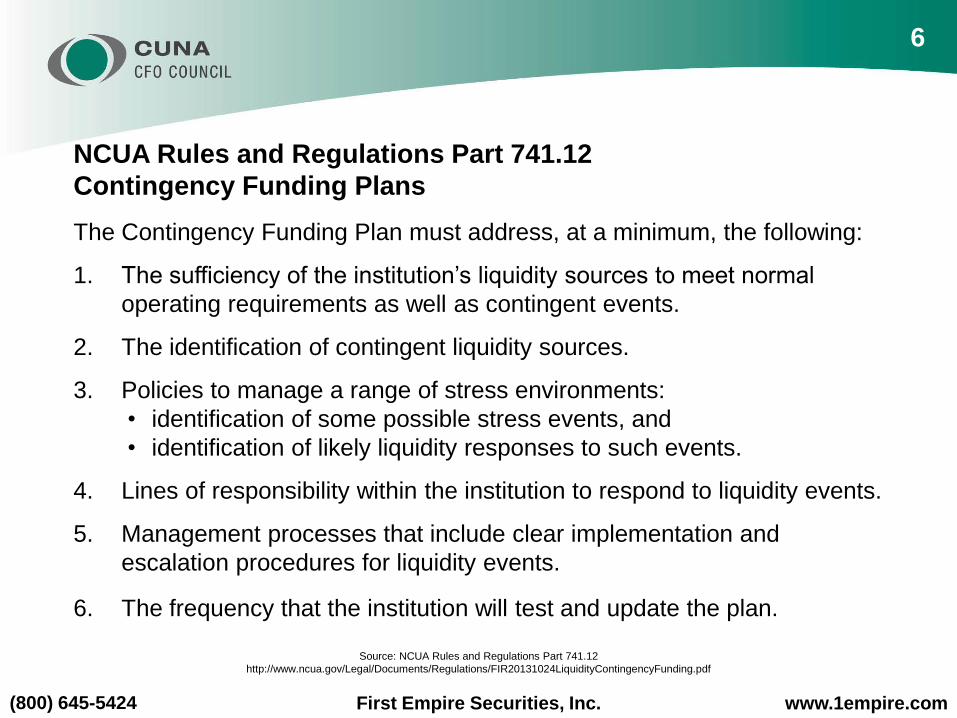

NCUA Rules and Regulations Part 741.12

Contingency Funding Plans

The Contingency Funding Plan must address, at a minimum, the following:

1. The sufficiency of the institution’s liquidity sources to meet normal

operating requirements as well as contingent events.

2. The identification of contingent liquidity sources.

3. Policies to manage a range of stress environments:

• identification of some possible stress events, and

• identification of likely liquidity responses to such events.

4. Lines of responsibility within the institution to respond to liquidity events.

5. Management processes that include clear implementation and

escalation procedures for liquidity events.

6. The frequency that the institution will test and update the plan.

Source: NCUA Rules and Regulations Part 741.12

http://www.ncua.gov/Legal/Documents/Regulations/FIR20131024LiquidityContingencyFunding.pdf

6

First Empire Securities, Inc.(800) 645-5424 www.1empire.com

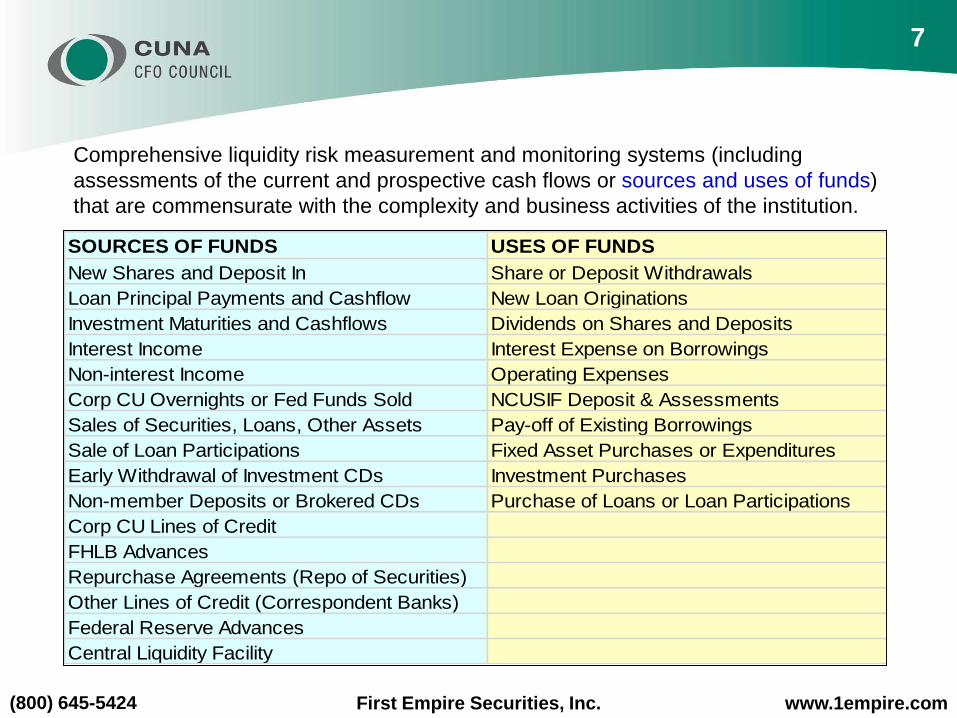

SOURCES OF FUNDS USES OF FUNDS

New Shares and Deposit In Share or Deposit Withdrawals

Loan Principal Payments and Cashflow New Loan Originations

Investment Maturities and Cashflows Dividends on Shares and Deposits

Interest Income Interest Expense on Borrowings

Non-interest Income Operating Expenses

Corp CU Overnights or Fed Funds Sold NCUSIF Deposit & Assessments

Sales of Securities, Loans, Other Assets Pay-off of Existing Borrowings

Sale of Loan Participations Fixed Asset Purchases or Expenditures

Early Withdrawal of Investment CDs Investment Purchases

Non-member Deposits or Brokered CDs Purchase of Loans or Loan Participations

Corp CU Lines of Credit

FHLB Advances

Repurchase Agreements (Repo of Securities)

Other Lines of Credit (Correspondent Banks)

Federal Reserve Advances

Central Liquidity Facility

Comprehensive liquidity risk measurement and monitoring systems (including

assessments of the current and prospective cash flows or sources and uses of funds)

that are commensurate with the complexity and business activities of the institution.

7

First Empire Securities, Inc.(800) 645-5424 www.1empire.com

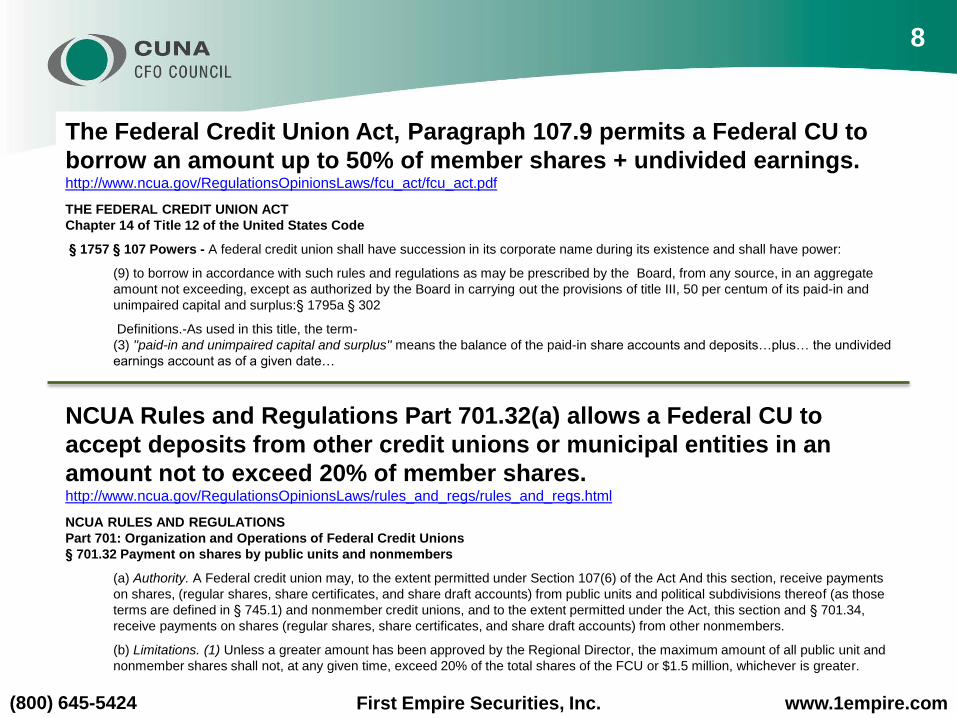

The Federal Credit Union Act, Paragraph 107.9 permits a Federal CU to

borrow an amount up to 50% of member shares + undivided earnings.http://www.ncua.gov/RegulationsOpinionsLaws/fcu_act/fcu_act.pdf

THE FEDERAL CREDIT UNION ACT

Chapter 14 of Title 12 of the United States Code

§ 1757 § 107 Powers - A federal credit union shall have succession in its corporate name during its existence and shall have power:

(9) to borrow in accordance with such rules and regulations as may be prescribed by the Board, from any source, in an aggregate

amount not exceeding, except as authorized by the Board in carrying out the provisions of title III, 50 per centum of its paid-in and

unimpaired capital and surplus:§ 1795a § 302

Definitions.-As used in this title, the term-

(3) ''paid-in and unimpaired capital and surplus'' means the balance of the paid-in share accounts and deposits…plus… the undivided

earnings account as of a given date…

NCUA Rules and Regulations Part 701.32(a) allows a Federal CU to

accept deposits from other credit unions or municipal entities in an

amount not to exceed 20% of member shares. http://www.ncua.gov/RegulationsOpinionsLaws/rules_and_regs/rules_and_regs.html

NCUA RULES AND REGULATIONS

Part 701: Organization and Operations of Federal Credit Unions

§ 701.32 Payment on shares by public units and nonmembers

(a) Authority. A Federal credit union may, to the extent permitted under Section 107(6) of the Act And this section, receive payments

on shares, (regular shares, share certificates, and share draft accounts) from public units and political subdivisions thereof (as those

terms are defined in § 745.1) and nonmember credit unions, and to the extent permitted under the Act, this section and § 701.34,

receive payments on shares (regular shares, share certificates, and share draft accounts) from other nonmembers.

(b) Limitations. (1) Unless a greater amount has been approved by the Regional Director, the maximum amount of all public unit and

nonmember shares shall not, at any given time, exceed 20% of the total shares of the FCU or $1.5 million, whichever is greater.

8

First Empire Securities, Inc.(800) 645-5424 www.1empire.com

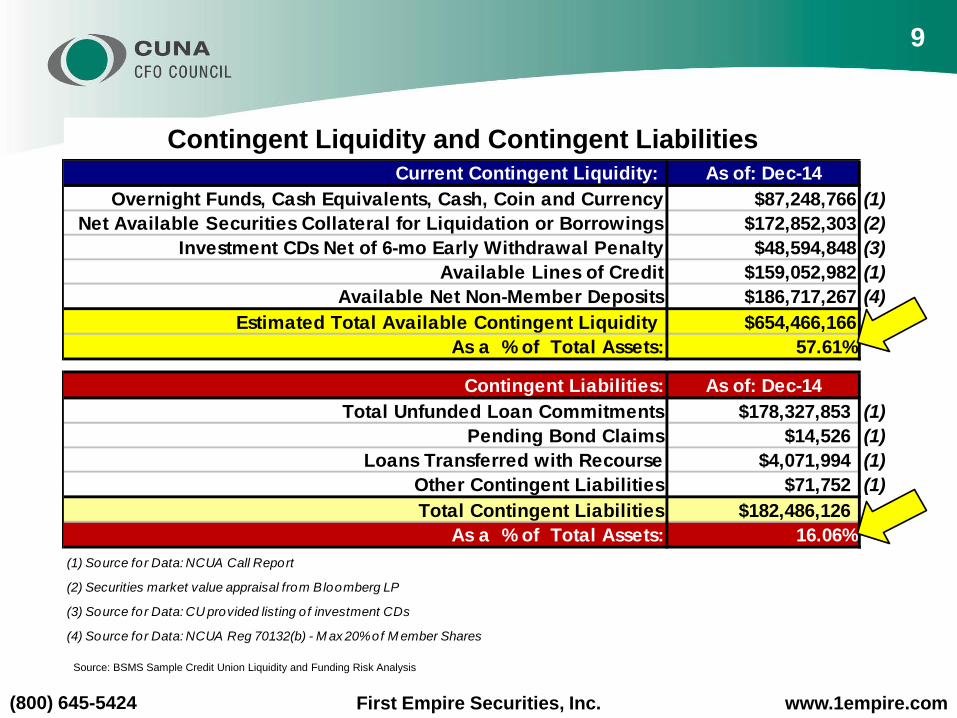

Contingent Liquidity and Contingent Liabilities

Source: BSMS Sample Credit Union Liquidity and Funding Risk Analysis

Current Contingent Liquidity: As of: Dec-14

Overnight Funds, Cash Equivalents, Cash, Coin and Currency $87,248,766 (1)

Net Available Securities Collateral for Liquidation or Borrowings $172,852,303 (2)

Investment CDs Net of 6-mo Early Withdrawal Penalty $48,594,848 (3)

Available Lines of Credit $159,052,982 (1)

Available Net Non-Member Deposits $186,717,267 (4)

Estimated Total Available Contingent Liquidity $654,466,166

As a % of Total Assets: 57.61%

Contingent Liabilities: As of: Dec-14

Total Unfunded Loan Commitments $178,327,853 (1)

Pending Bond Claims $14,526 (1)

Loans Transferred with Recourse $4,071,994 (1)

Other Contingent Liabilities $71,752 (1)

Total Contingent Liabilities $182,486,126 (1)

As a % of Total Assets: 16.06%

(1 ) Source for Data: NCUA Call Report

(2) Securities market value appraisal from Bloomberg LP

(3) Source for Data: CU provided listing of investment CDs

(4) Source for Data: NCUA Reg 701.32(b) - M ax 20% of M ember Shares

9

First Empire Securities, Inc.(800) 645-5424 www.1empire.com

• A critical element of a Contingency Funding Plan is

the quantitative projection and evaluation of expected

funding needs.

• Measuring liquidity risk should include robust

methods for comprehensively projecting cash flows

arising from assets, liabilities, and off-balance-sheet

items over an appropriate set of time horizons.

o Cash flow projections can range from simple spreadsheets to very

detailed reports depending upon the complexity and sophistication

of the institution and its liquidity risk profile.

10

Source: FFIEC Interagency Policy Statement on Funding and Liquidity Risk Management (March 2010)

http://www.ncua.gov/Resources/Documents/LCU2010-14Encl.pdf

First Empire Securities, Inc.(800) 645-5424 www.1empire.com

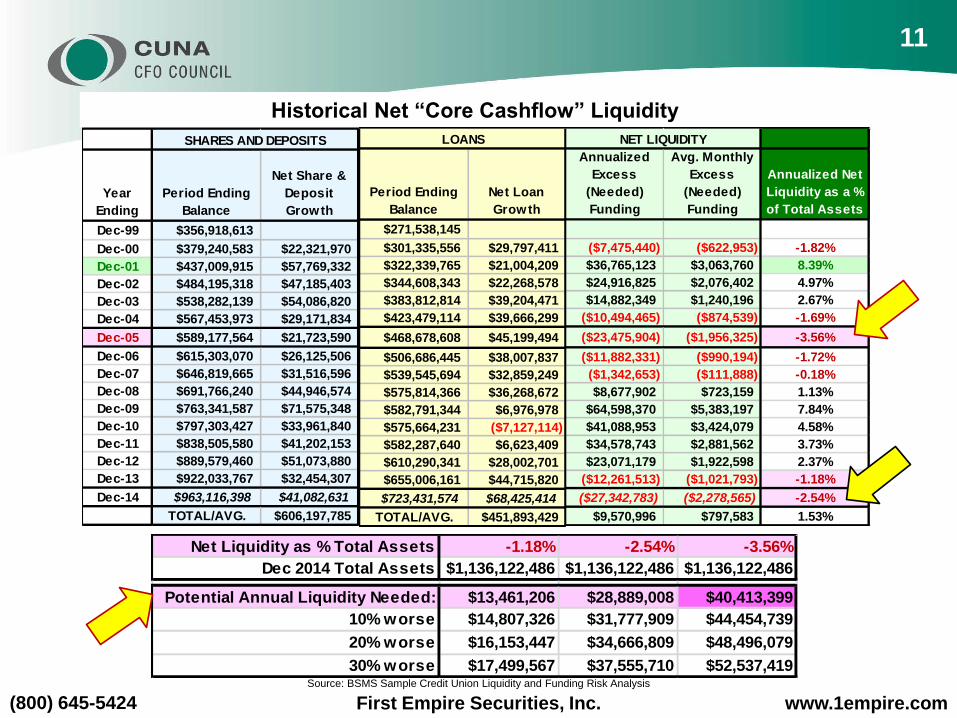

Year

Ending

Period Ending

Balance

Net Share &

Deposit

Growth

Dec-99 $356,918,613

Dec-00 $379,240,583 $22,321,970

Dec-01 $437,009,915 $57,769,332

Dec-02 $484,195,318 $47,185,403

Dec-03 $538,282,139 $54,086,820

Dec-04 $567,453,973 $29,171,834

Dec-05 $589,177,564 $21,723,590

Dec-06 $615,303,070 $26,125,506

Dec-07 $646,819,665 $31,516,596

Dec-08 $691,766,240 $44,946,574

Dec-09 $763,341,587 $71,575,348

Dec-10 $797,303,427 $33,961,840

Dec-11 $838,505,580 $41,202,153

Dec-12 $889,579,460 $51,073,880

Dec-13 $922,033,767 $32,454,307

Dec-14 $963,116,398 $41,082,631

TOTAL/AVG. $606,197,785

SHARES AND DEPOSITS

Year

Ending

Period Ending

Balance

Net Share &

Deposit

Growth

Period Ending

Balance

Net Loan

Growth

Annualized

Excess

(Needed)

Funding

Avg. Monthly

Excess

(Needed)

Funding

Annualized Net

Liquidity as a %

of Total Assets

Dec-99 $356,918,613 $271,538,145

Dec-00 $379,240,583 $22,321,970 $301,335,556 $29,797,411 ($7,475,440) ($622,953) -1.82%

Dec-01 $437,009,915 $57,769,332 $322,339,765 $21,004,209 $36,765,123 $3,063,760 8.39%

Dec-02 $484,195,318 $47,185,403 $344,608,343 $22,268,578 $24,916,825 $2,076,402 4.97%

Dec-03 $538,282,139 $54,086,820 $383,812,814 $39,204,471 $14,882,349 $1,240,196 2.67%

Dec-04 $567,453,973 $29,171,834 $423,479,114 $39,666,299 ($10,494,465) ($874,539) -1.69%

Dec-05 $589,177,564 $21,723,590 $468,678,608 $45,199,494 ($23,475,904) ($1,956,325) -3.56%

Dec-06 $615,303,070 $26,125,506 $506,686,445 $38,007,837 ($11,882,331) ($990,194) -1.72%

Dec-07 $646,819,665 $31,516,596 $539,545,694 $32,859,249 ($1,342,653) ($111,888) -0.18%

Dec-08 $691,766,240 $44,946,574 $575,814,366 $36,268,672 $8,677,902 $723,159 1.13%

Dec-09 $763,341,587 $71,575,348 $582,791,344 $6,976,978 $64,598,370 $5,383,197 7.84%

Dec-10 $797,303,427 $33,961,840 $575,664,231 ($7,127,114) $41,088,953 $3,424,079 4.58%

Dec-11 $838,505,580 $41,202,153 $582,287,640 $6,623,409 $34,578,743 $2,881,562 3.73%

Dec-12 $889,579,460 $51,073,880 $610,290,341 $28,002,701 $23,071,179 $1,922,598 2.37%

Dec-13 $922,033,767 $32,454,307 $655,006,161 $44,715,820 ($12,261,513) ($1,021,793) -1.18%

Dec-14 $963,116,398 $41,082,631 $723,431,574 $68,425,414 ($27,342,783) ($2,278,565) -2.54%

TOTAL/AVG. $606,197,785 TOTAL/AVG. $451,893,429 $9,570,996 $797,583 1.53%

LOANSSHARES AND DEPOSITS NET LIQUIDITY

Source: BSMS Sample Credit Union Liquidity and Funding Risk Analysis

Historical Net “Core Cashflow” Liquidity

Net Liquidity as % Total Assets -1.18% -2.54% -3.56%

Dec 2014 Total Assets $1,136,122,486 $1,136,122,486 $1,136,122,486

Potential Annual Liquidity Needed: $13,461,206 $28,889,008 $40,413,399

10% worse $14,807,326 $31,777,909 $44,454,739

20% worse $16,153,447 $34,666,809 $48,496,079

30% worse $17,499,567 $37,555,710 $52,537,419

11

Period Ending

Balance

Net Loan

Growth

$271,538,145

$301,335,556 $29,797,411

$322,339,765 $21,004,209

$344,608,343 $22,268,578

$383,812,814 $39,204,471

$423,479,114 $39,666,299

$468,678,608 $45,199,494

$506,686,445 $38,007,837

$539,545,694 $32,859,249

$575,814,366 $36,268,672

$582,791,344 $6,976,978

$575,664,231 ($7,127,114)

$582,287,640 $6,623,409

$610,290,341 $28,002,701

$655,006,161 $44,715,820

$723,431,574 $68,425,414

TOTAL/AVG. $451,893,429

LOANS

Annualized

Excess

(Needed)

Funding

Avg. Monthly

Excess

(Needed)

Funding

Annualized Net

Liquidity as a %

of Total Assets

($7,475,440) ($622,953) -1.82%

$36,765,123 $3,063,760 8.39%

$24,916,825 $2,076,402 4.97%

$14,882,349 $1,240,196 2.67%

($10,494,465) ($874,539) -1.69%

($23,475,904) ($1,956,325) -3.56%

($11,882,331) ($990,194) -1.72%

($1,342,653) ($111,888) -0.18%

$8,677,902 $723,159 1.13%

$64,598,370 $5,383,197 7.84%

$41,088,953 $3,424,079 4.58%

$34,578,743 $2,881,562 3.73%

$23,071,179 $1,922,598 2.37%

($12,261,513) ($1,021,793) -1.18%

($27,342,783) ($2,278,565) -2.54%

$9,570,996 $797,583 1.53%

NET LIQUIDITY

First Empire Securities, Inc.(800) 645-5424 www.1empire.com

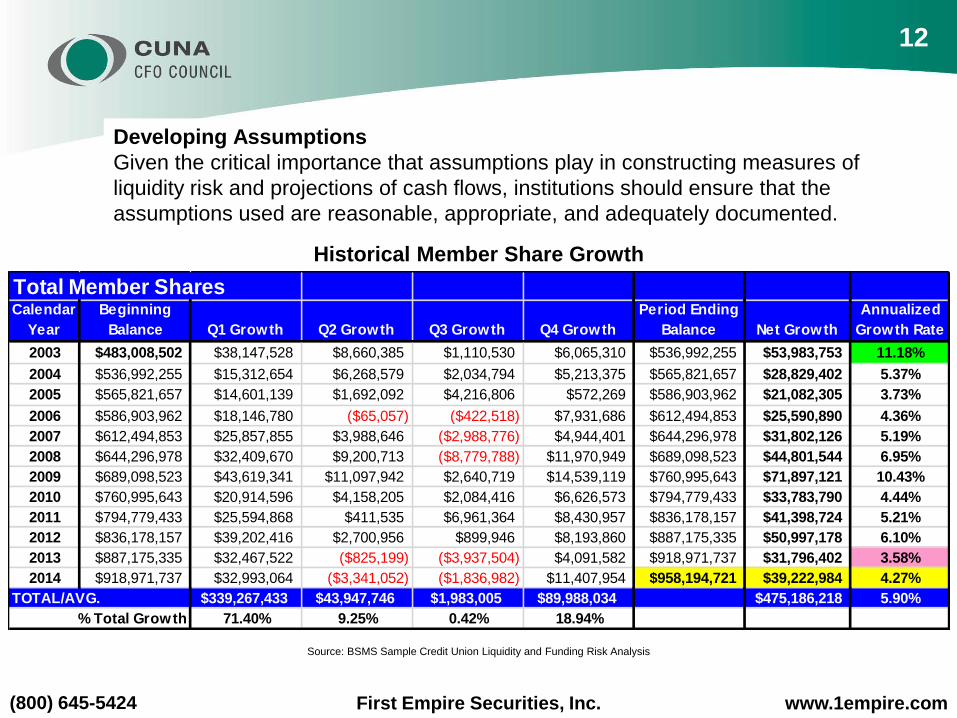

Total Member SharesCalendar

Year

Beginning

Balance Q1 Growth Q2 Growth Q3 Growth Q4 Growth

Period Ending

Balance Net Growth

Annualized

Growth Rate

2003 $483,008,502 $38,147,528 $8,660,385 $1,110,530 $6,065,310 $536,992,255 $53,983,753 11.18%

2004 $536,992,255 $15,312,654 $6,268,579 $2,034,794 $5,213,375 $565,821,657 $28,829,402 5.37%

2005 $565,821,657 $14,601,139 $1,692,092 $4,216,806 $572,269 $586,903,962 $21,082,305 3.73%

2006 $586,903,962 $18,146,780 ($65,057) ($422,518) $7,931,686 $612,494,853 $25,590,890 4.36%

2007 $612,494,853 $25,857,855 $3,988,646 ($2,988,776) $4,944,401 $644,296,978 $31,802,126 5.19%

2008 $644,296,978 $32,409,670 $9,200,713 ($8,779,788) $11,970,949 $689,098,523 $44,801,544 6.95%

2009 $689,098,523 $43,619,341 $11,097,942 $2,640,719 $14,539,119 $760,995,643 $71,897,121 10.43%

2010 $760,995,643 $20,914,596 $4,158,205 $2,084,416 $6,626,573 $794,779,433 $33,783,790 4.44%

2011 $794,779,433 $25,594,868 $411,535 $6,961,364 $8,430,957 $836,178,157 $41,398,724 5.21%

2012 $836,178,157 $39,202,416 $2,700,956 $899,946 $8,193,860 $887,175,335 $50,997,178 6.10%

2013 $887,175,335 $32,467,522 ($825,199) ($3,937,504) $4,091,582 $918,971,737 $31,796,402 3.58%

2014 $918,971,737 $32,993,064 ($3,341,052) ($1,836,982) $11,407,954 $958,194,721 $39,222,984 4.27%

TOTAL/AVG. $339,267,433 $43,947,746 $1,983,005 $89,988,034 $475,186,218 5.90%

% Total Growth 71.40% 9.25% 0.42% 18.94%

Developing Assumptions

Given the critical importance that assumptions play in constructing measures of

liquidity risk and projections of cash flows, institutions should ensure that the

assumptions used are reasonable, appropriate, and adequately documented.

Source: BSMS Sample Credit Union Liquidity and Funding Risk Analysis

Historical Member Share Growth

12

First Empire Securities, Inc.(800) 645-5424 www.1empire.com

Source: BSMS Sample Credit Union Liquidity and Funding Risk Analysis

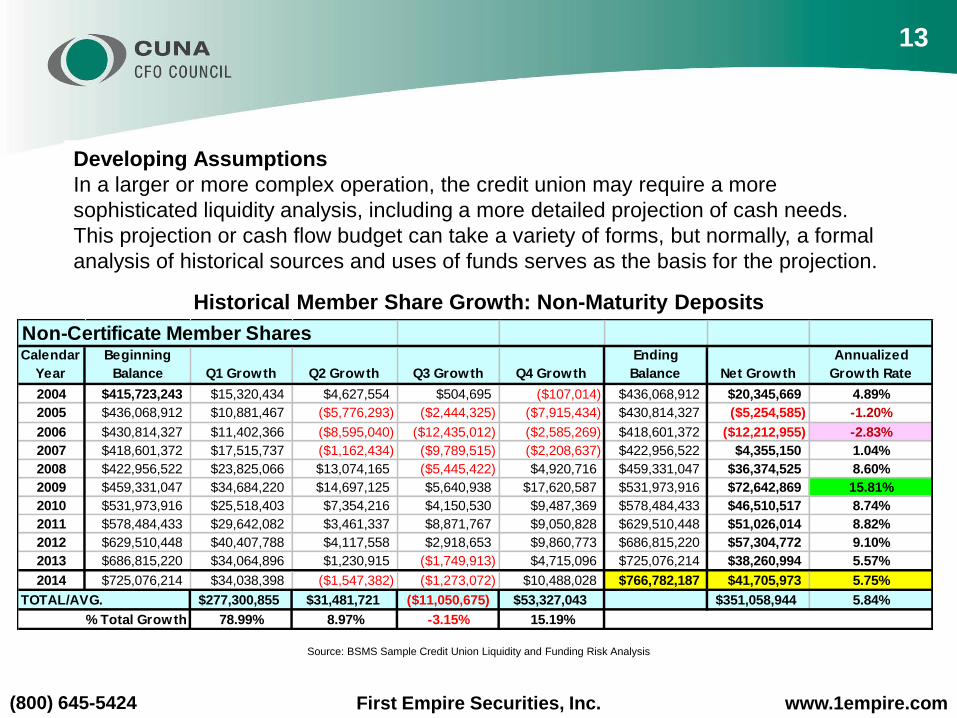

Historical Member Share Growth: Non-Maturity Deposits

Non-Certificate Member SharesCalendar

Year

Beginning

Balance Q1 Growth Q2 Growth Q3 Growth Q4 Growth

Ending

Balance Net Growth

Annualized

Growth Rate

2004 $415,723,243 $15,320,434 $4,627,554 $504,695 ($107,014) $436,068,912 $20,345,669 4.89%

2005 $436,068,912 $10,881,467 ($5,776,293) ($2,444,325) ($7,915,434) $430,814,327 ($5,254,585) -1.20%

2006 $430,814,327 $11,402,366 ($8,595,040) ($12,435,012) ($2,585,269) $418,601,372 ($12,212,955) -2.83%

2007 $418,601,372 $17,515,737 ($1,162,434) ($9,789,515) ($2,208,637) $422,956,522 $4,355,150 1.04%

2008 $422,956,522 $23,825,066 $13,074,165 ($5,445,422) $4,920,716 $459,331,047 $36,374,525 8.60%

2009 $459,331,047 $34,684,220 $14,697,125 $5,640,938 $17,620,587 $531,973,916 $72,642,869 15.81%

2010 $531,973,916 $25,518,403 $7,354,216 $4,150,530 $9,487,369 $578,484,433 $46,510,517 8.74%

2011 $578,484,433 $29,642,082 $3,461,337 $8,871,767 $9,050,828 $629,510,448 $51,026,014 8.82%

2012 $629,510,448 $40,407,788 $4,117,558 $2,918,653 $9,860,773 $686,815,220 $57,304,772 9.10%

2013 $686,815,220 $34,064,896 $1,230,915 ($1,749,913) $4,715,096 $725,076,214 $38,260,994 5.57%

2014 $725,076,214 $34,038,398 ($1,547,382) ($1,273,072) $10,488,028 $766,782,187 $41,705,973 5.75%

TOTAL/AVG. $277,300,855 $31,481,721 ($11,050,675) $53,327,043 $351,058,944 5.84%

% Total Growth 78.99% 8.97% -3.15% 15.19%

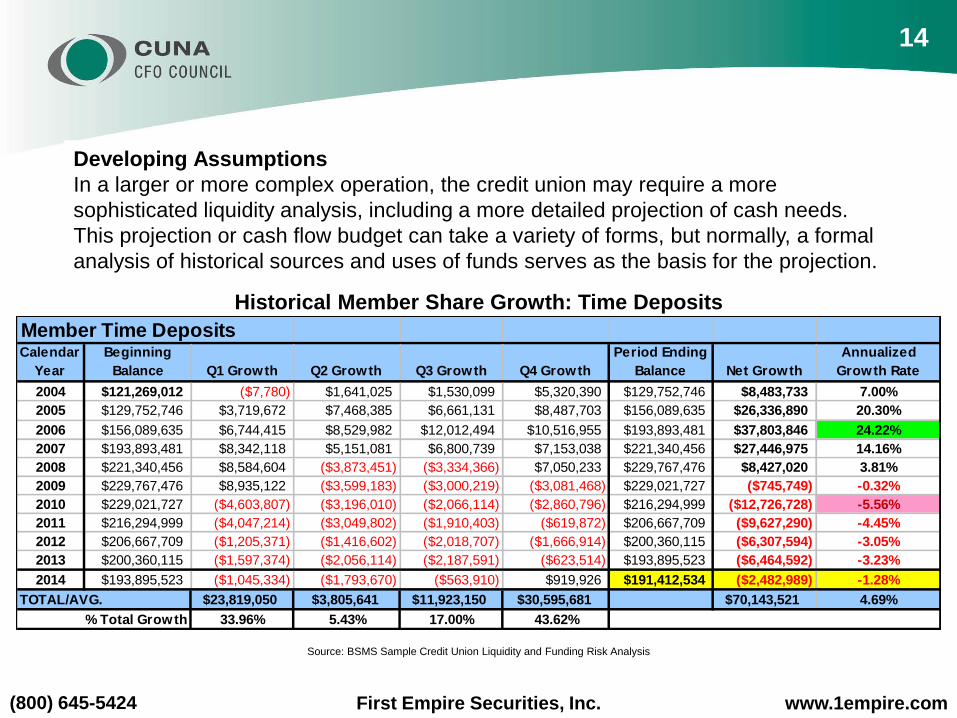

Developing Assumptions

In a larger or more complex operation, the credit union may require a more

sophisticated liquidity analysis, including a more detailed projection of cash needs.

This projection or cash flow budget can take a variety of forms, but normally, a formal

analysis of historical sources and uses of funds serves as the basis for the projection.

13

First Empire Securities, Inc.(800) 645-5424 www.1empire.com

Source: BSMS Sample Credit Union Liquidity and Funding Risk Analysis

Member Time DepositsCalendar

Year

Beginning

Balance Q1 Growth Q2 Growth Q3 Growth Q4 Growth

Period Ending

Balance Net Growth

Annualized

Growth Rate

2004 $121,269,012 ($7,780) $1,641,025 $1,530,099 $5,320,390 $129,752,746 $8,483,733 7.00%

2005 $129,752,746 $3,719,672 $7,468,385 $6,661,131 $8,487,703 $156,089,635 $26,336,890 20.30%

2006 $156,089,635 $6,744,415 $8,529,982 $12,012,494 $10,516,955 $193,893,481 $37,803,846 24.22%

2007 $193,893,481 $8,342,118 $5,151,081 $6,800,739 $7,153,038 $221,340,456 $27,446,975 14.16%

2008 $221,340,456 $8,584,604 ($3,873,451) ($3,334,366) $7,050,233 $229,767,476 $8,427,020 3.81%

2009 $229,767,476 $8,935,122 ($3,599,183) ($3,000,219) ($3,081,468) $229,021,727 ($745,749) -0.32%

2010 $229,021,727 ($4,603,807) ($3,196,010) ($2,066,114) ($2,860,796) $216,294,999 ($12,726,728) -5.56%

2011 $216,294,999 ($4,047,214) ($3,049,802) ($1,910,403) ($619,872) $206,667,709 ($9,627,290) -4.45%

2012 $206,667,709 ($1,205,371) ($1,416,602) ($2,018,707) ($1,666,914) $200,360,115 ($6,307,594) -3.05%

2013 $200,360,115 ($1,597,374) ($2,056,114) ($2,187,591) ($623,514) $193,895,523 ($6,464,592) -3.23%

2014 $193,895,523 ($1,045,334) ($1,793,670) ($563,910) $919,926 $191,412,534 ($2,482,989) -1.28%

TOTAL/AVG. $23,819,050 $3,805,641 $11,923,150 $30,595,681 $70,143,521 4.69%

% Total Growth 33.96% 5.43% 17.00% 43.62%

Historical Member Share Growth: Time Deposits

Developing Assumptions

In a larger or more complex operation, the credit union may require a more

sophisticated liquidity analysis, including a more detailed projection of cash needs.

This projection or cash flow budget can take a variety of forms, but normally, a formal

analysis of historical sources and uses of funds serves as the basis for the projection.

14

First Empire Securities, Inc.(800) 645-5424 www.1empire.com

All Non-maturity Deposits

Date

Period Ending

Balance $ Growth

Annualized

Growth Rate

Negative

Periods Only

Fed Fund

Rate Change

Jun-03 $406,821,588 1.00%

Sep-03 $414,494,703 $7,673,115 7.54% 1.00% 0.00%

Dec-03 $415,723,243 $1,228,540 1.19% 1.00% 0.00%

Mar-04 $431,043,677 $15,320,434 14.74% 1.00% 0.00%

Jun-04 $435,671,231 $4,627,554 4.29% 1.25% +0.25%

Sep-04 $436,175,926 $504,695 0.46% 1.75% +0.50%

Dec-04 $436,068,912 -$107,014 -0.10% -0.10% 2.25% +0.50%

Mar-05 $446,950,379 $10,881,467 9.98% 2.75% +0.50%

Jun-05 $441,174,086 -$5,776,293 -5.17% -5.17% 3.25% +0.50%

Sep-05 $438,729,761 -$2,444,325 -2.22% -2.22% 3.75% +0.50%

Dec-05 $430,814,327 -$7,915,434 -7.22% -7.22% 4.50% +0.75%

Mar-06 $442,216,693 $11,402,366 10.59% 4.75% +0.25%

Jun-06 $433,621,653 -$8,595,040 -7.77% -7.77% 5.25% +0.50%

Sep-06 $421,186,641 -$12,435,012 -11.47% -11.47% 5.25% 0.00%

Dec-06 $418,601,372 -$2,585,269 -2.46% -2.46% 5.25% 0.00%

Mar-07 $436,117,109 $17,515,737 16.74% 5.25% 0.00%

Jun-07 $434,954,674 -$1,162,434 -1.07% -1.07% 5.25% 0.00%

TOTAL/AVG. $28,133,087 +1.75% -4.69%

Historical Worst 12-month Period Sep-05 Sep-06 -4.00%

$438,729,761 $421,186,641 -$17,543,120

Avg of the 4 Worst Quarters -8.87%

Worst Quarter Q3 - 2006 Jun-2006 Sep-2006 -11.47%

Second Worst Q Q3 - 2007 Jun-2007 Sep-2007 -9.00%

Third Worst Q Q2 - 2006 Mar-2006 Jun-2006 -7.77%

Fourth Worst Q Q4 - 2005 Sep-2005 Dec-2005 -7.22%

Source: BSMS Sample Credit Union Liquidity and Funding Risk Analysis

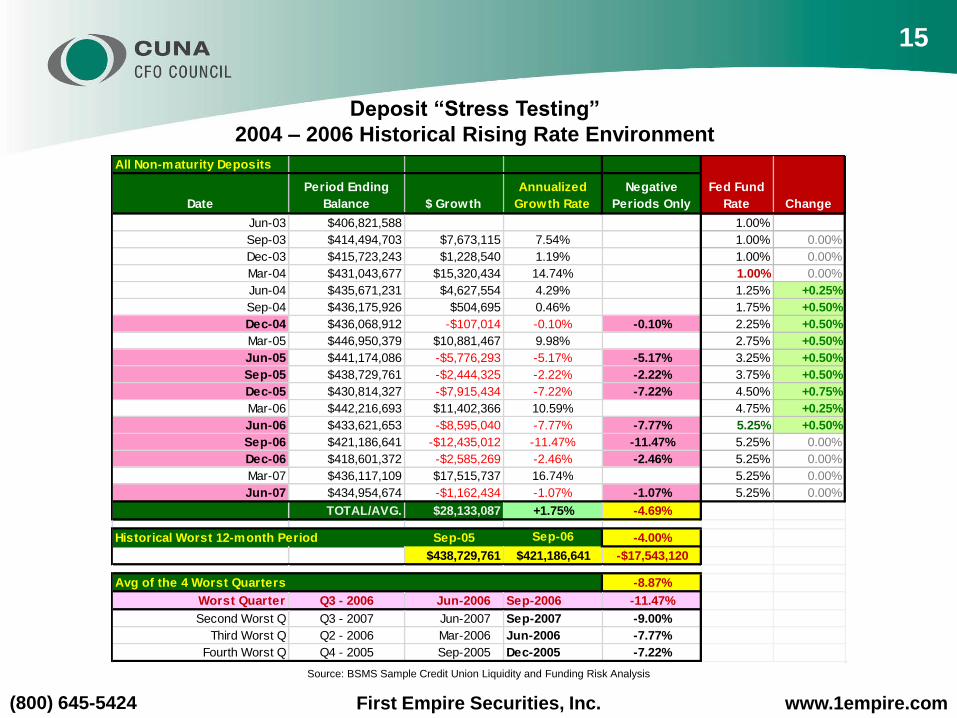

Deposit “Stress Testing”

2004 – 2006 Historical Rising Rate Environment

15

First Empire Securities, Inc.(800) 645-5424 www.1empire.com

Year

Beginning

Balance

Loan Payments

& Prepayments Loans Sold

Loan

Originations &

Purchases

Net Loan

Growth Ending Balance

2002 $322,339,765 $163,800,006 $25,063,922 $211,132,506 $22,268,578 $344,608,343

2003 $344,608,343 $184,513,397 $38,184,138 $261,902,006 $39,204,471 $383,812,814

2004 $383,812,814 $181,240,997 $22,387,858 $243,295,154 $39,666,299 $423,479,114

2005 $423,479,114 $194,217,474 $22,549,633 $261,966,601 $45,199,494 $468,678,608

2006 $468,678,608 $198,157,416 $18,232,553 $254,397,806 $38,007,837 $506,686,445

2007 $506,686,445 $208,365,931 $17,818,527 $259,043,707 $32,859,249 $539,545,694

2008 $539,545,694 $198,884,369 $21,880,103 $257,033,145 $36,268,672 $575,814,366

2009 $575,814,366 $213,534,880 $53,905,122 $274,416,980 $6,976,978 $582,791,344

2010 $582,791,344 $255,437,124 $46,461,550 $294,771,560 ($7,127,114) $575,664,231

2011 $575,664,231 $219,365,250 $41,340,025 $267,328,685 $6,623,409 $582,287,640

2012 $582,287,640 $238,893,977 $69,935,969 $336,832,647 $28,002,701 $610,290,341

2013 $610,290,341 $254,564,139 $59,567,403 $358,847,363 $44,715,820 $655,006,161

YTD 2014 $655,006,161 $264,544,355 $37,868,397 $370,838,165 $68,425,414 $723,431,574

Last 90 Days $706,298,348 $69,506,094 $11,435,075 $98,074,395 $17,133,227 $723,431,574

Last 12 Months $655,006,161 $264,544,355 $37,868,397 $370,838,165 $68,425,414 $723,431,574

Source: BSMS Sample Credit Union Liquidity and Funding Risk Analysis

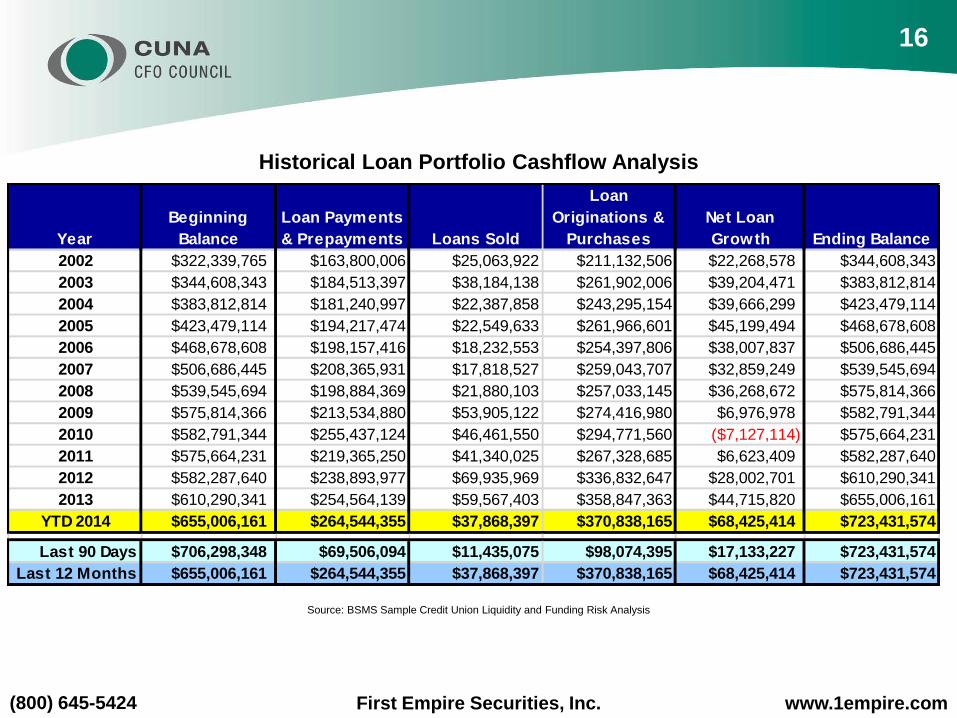

Historical Loan Portfolio Cashflow Analysis

16

First Empire Securities, Inc.(800) 645-5424 www.1empire.com

Year

Avg Monthly

Principal

Paydown

Payments +

Prepayments

as % Total

Loans

Loans Sold as

% Loan

Originations

Originations &

Purchases as a

% Total Loans

Annualized Net

Loan Growth

2002 $13,650,000 50.82% 11.87% 65.50% 6.91%

2003 $15,376,116 53.54% 14.58% 76.00% 11.38%

2004 $15,103,416 47.22% 9.20% 63.39% 10.33%

2005 $16,184,790 45.86% 8.61% 61.86% 10.67%

2006 $16,513,118 42.28% 7.17% 54.28% 8.11%

2007 $17,363,828 41.12% 6.88% 51.13% 6.49%

2008 $16,573,697 36.86% 8.51% 47.64% 6.72%

2009 $17,794,573 37.08% 19.64% 47.66% 1.21%

2010 $21,286,427 43.83% 15.76% 50.58% -1.22%

2011 $18,280,438 38.11% 15.46% 46.44% 1.15%

2012 $19,907,831 41.03% 20.76% 57.85% 4.81%

2013 $21,213,678 41.71% 16.60% 58.80% 7.33%

YTD 2014 $22,045,363 40.39% 10.21% 56.62% 10.45%

Average 43.07% 12.71% 56.75% 6.49%

Last 90 Days $23,168,698 39.36% 11.66% 55.54% 9.70%

Last 12 Months $22,045,363 40.39% 10.21% 56.62% 10.45%

Source: BSMS Sample Credit Union Liquidity and Funding Risk Analysis

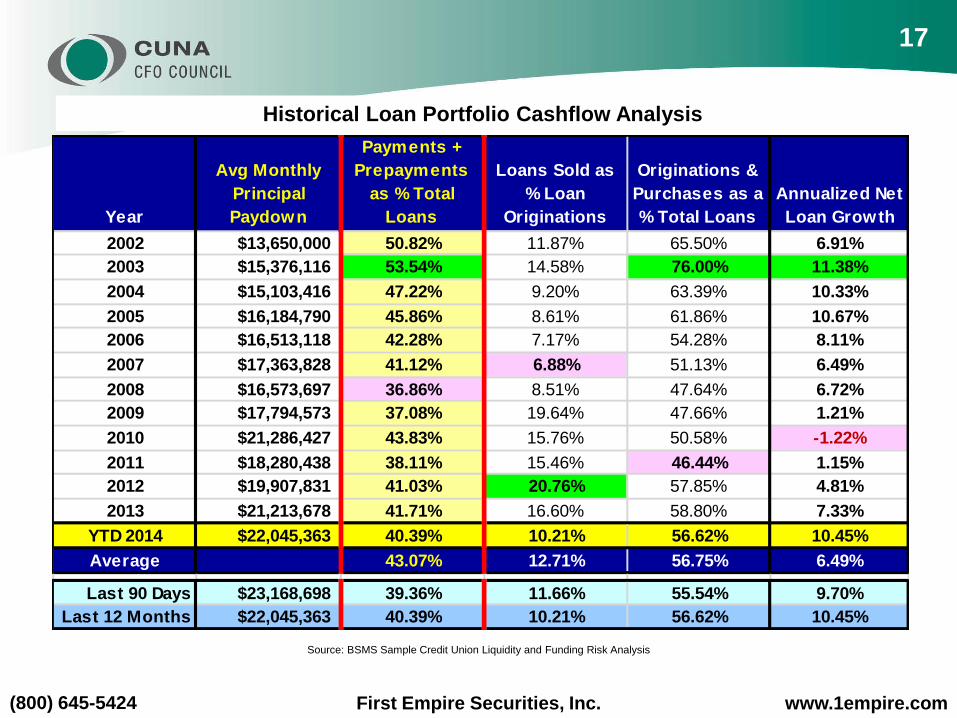

Historical Loan Portfolio Cashflow Analysis

17

First Empire Securities, Inc.(800) 645-5424 www.1empire.com

Scenario Yr 1 Yr 2 Yr 3 Yr 4 Yr 5 Yr 6 Yr 7 Yr 8 Yr 9 Yr 10

+300bps Shock $51,696 $55,821 $55,071 $42,781 $31,738 $22,526 $20,042 $22,905 $20,120 $20,620

Flat Rate $74,757 $59,521 $43,367 $33,951 $25,202 $17,896 $14,814 $12,542 $10,171 $8,283

-300bps Shock $116,769 $63,166 $41,541 $28,035 $16,884 $9,020 $6,575 $5,089 $3,801 $2,999

$0

$20,000

$40,000

$60,000

$80,000

$100,000

$120,000

$140,000

Yr 1 Yr 2 Yr 3 Yr 4 Yr 5 Yr 6 Yr 7 Yr 8 Yr 9 Yr 10

+300bps Shock Flat Rate -300bps Shock

Source: BSMS Sample Credit Union Liquidity and Funding Risk Analysis

Investment Cashflow Forecast and Rate-Shocks

18

First Empire Securities, Inc.(800) 645-5424 www.1empire.com

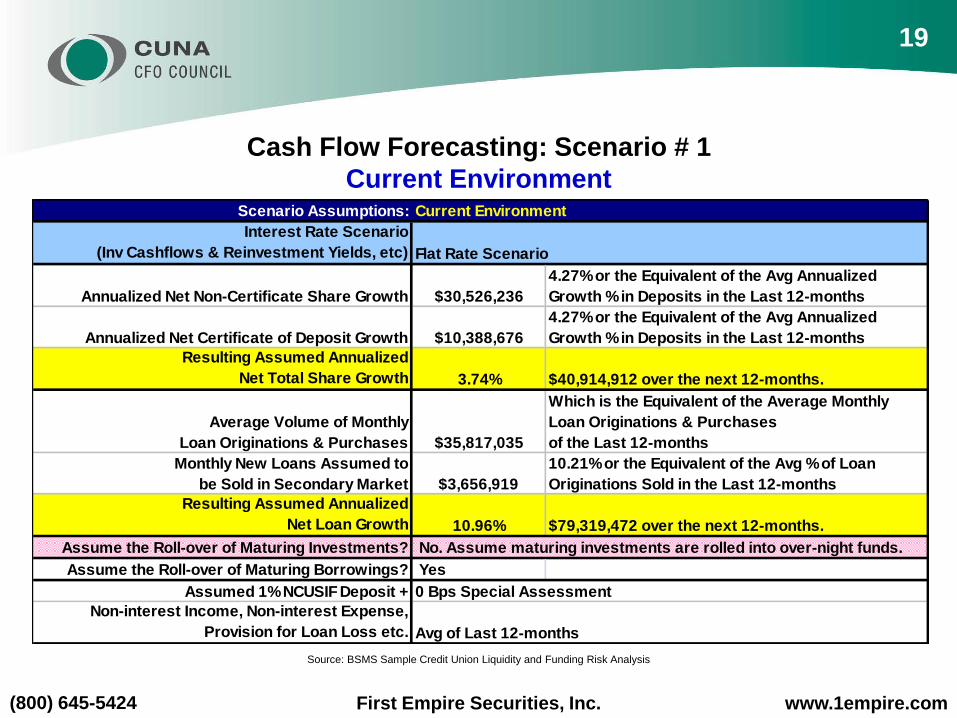

Cash Flow Forecasting: Scenario # 1

Current EnvironmentScenario Assumptions: Current Environment

Interest Rate Scenario

(Inv Cashflows & Reinvestment Yields, etc) Flat Rate Scenario

Annualized Net Non-Certificate Share Growth $30,526,236

4.27% or the Equivalent of the Avg Annualized

Growth % in Deposits in the Last 12-months

Annualized Net Certificate of Deposit Growth $10,388,676

4.27% or the Equivalent of the Avg Annualized

Growth % in Deposits in the Last 12-months

Resulting Assumed Annualized

Net Total Share Growth 3.74% $40,914,912 over the next 12-months.

Average Volume of Monthly

Loan Originations & Purchases $35,817,035

Which is the Equivalent of the Average Monthly

Loan Originations & Purchases

of the Last 12-months

Monthly New Loans Assumed to

be Sold in Secondary Market $3,656,919

10.21% or the Equivalent of the Avg % of Loan

Originations Sold in the Last 12-months

Resulting Assumed Annualized

Net Loan Growth 10.96% $79,319,472 over the next 12-months.

Assume the Roll-over of Maturing Investments? No. Assume maturing investments are rolled into over-night funds.

Assume the Roll-over of Maturing Borrowings? Yes

Assumed 1% NCUSIF Deposit + 0 Bps Special Assessment

Non-interest Income, Non-interest Expense,

Provision for Loan Loss etc. Avg of Last 12-months

Source: BSMS Sample Credit Union Liquidity and Funding Risk Analysis

19

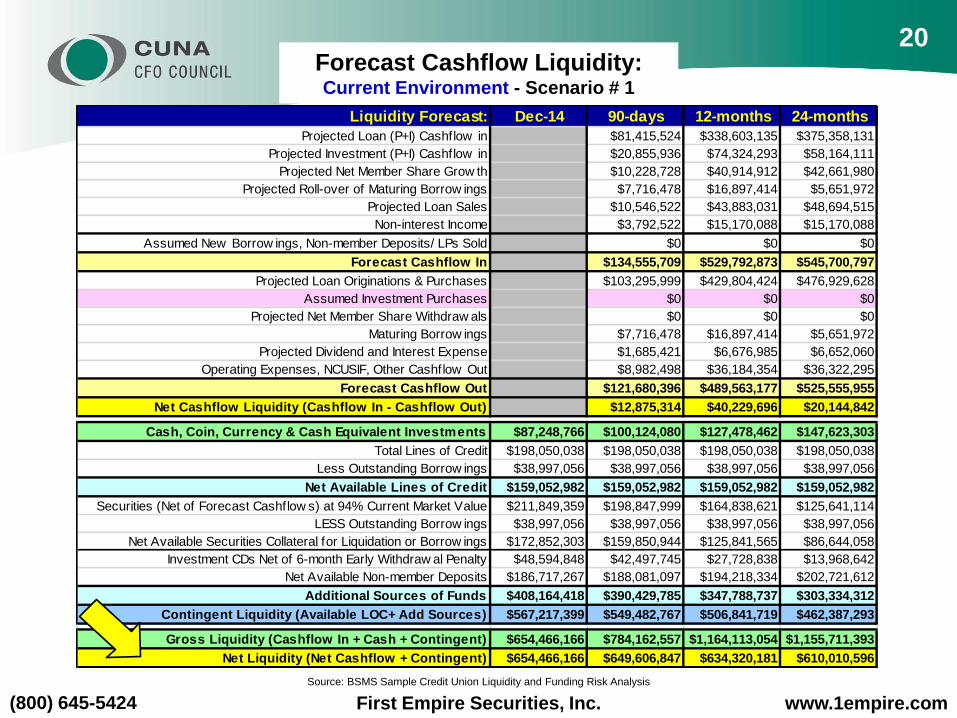

First Empire Securities, Inc.(800) 645-5424 www.1empire.com

Liquidity Forecast: Dec-14 90-days 12-months 24-months

Projected Loan (P+I) Cashflow in $81,415,524 $338,603,135 $375,358,131

Projected Investment (P+I) Cashflow in $20,855,936 $74,324,293 $58,164,111

Projected Net Member Share Grow th $10,228,728 $40,914,912 $42,661,980

Projected Roll-over of Maturing Borrow ings $7,716,478 $16,897,414 $5,651,972

Projected Loan Sales $10,546,522 $43,883,031 $48,694,515

Non-interest Income $3,792,522 $15,170,088 $15,170,088

Assumed New Borrow ings, Non-member Deposits/ LPs Sold $0 $0 $0

Forecast Cashflow In $134,555,709 $529,792,873 $545,700,797

Projected Loan Originations & Purchases $103,295,999 $429,804,424 $476,929,628

Assumed Investment Purchases $0 $0 $0

Projected Net Member Share Withdraw als $0 $0 $0

Maturing Borrow ings $7,716,478 $16,897,414 $5,651,972

Projected Dividend and Interest Expense $1,685,421 $6,676,985 $6,652,060

Operating Expenses, NCUSIF, Other Cashflow Out $8,982,498 $36,184,354 $36,322,295

Forecast Cashflow Out $121,680,396 $489,563,177 $525,555,955

Net Cashflow Liquidity (Cashflow In - Cashflow Out) $12,875,314 $40,229,696 $20,144,842

Cash, Coin, Currency & Cash Equivalent Investments $87,248,766 $100,124,080 $127,478,462 $147,623,303

Total Lines of Credit $198,050,038 $198,050,038 $198,050,038 $198,050,038

Less Outstanding Borrow ings $38,997,056 $38,997,056 $38,997,056 $38,997,056

Net Available Lines of Credit $159,052,982 $159,052,982 $159,052,982 $159,052,982

Securities (Net of Forecast Cashflow s) at 94% Current Market Value $211,849,359 $198,847,999 $164,838,621 $125,641,114

LESS Outstanding Borrow ings $38,997,056 $38,997,056 $38,997,056 $38,997,056

Net Available Securities Collateral for Liquidation or Borrow ings $172,852,303 $159,850,944 $125,841,565 $86,644,058

Investment CDs Net of 6-month Early Withdraw al Penalty $48,594,848 $42,497,745 $27,728,838 $13,968,642

Net Available Non-member Deposits $186,717,267 $188,081,097 $194,218,334 $202,721,612

Additional Sources of Funds $408,164,418 $390,429,785 $347,788,737 $303,334,312

Contingent Liquidity (Available LOC+ Add Sources) $567,217,399 $549,482,767 $506,841,719 $462,387,293

Gross Liquidity (Cashflow In + Cash + Contingent) $654,466,166 $784,162,557 $1,164,113,054 $1,155,711,393

Net Liquidity (Net Cashflow + Contingent) $654,466,166 $649,606,847 $634,320,181 $610,010,596

Forecast Cashflow Liquidity: Current Environment - Scenario # 1

Source: BSMS Sample Credit Union Liquidity and Funding Risk Analysis

20

First Empire Securities, Inc.(800) 645-5424 www.1empire.com

Liquidity Ratios: Dec-14 90-days 12-months 24-months

Forecast Cashflow In as % Total Assets 11.72% 44.69% 44.04%

Forecast Cashflows Out as % Total Assets 10.60% 41.29% 42.42%

Net Cashflow Liquidity % Total Assets 1.12% 3.39% 1.63%

Cash & Cash Equivalents as % of Total Assets 7.68% 8.72% 10.75% 11.91%

Available Lines of Credit as % Total Assets 14.00% 13.85% 13.42% 12.84%

Additional Sources of Funds as % Total Assets 35.93% 34.00% 29.34% 24.48%

Total Contingent Liquidity as % of Total Assets 49.93% 47.85% 42.75% 37.32%

Gross Liquidity as % of Total Assets 57.61% 68.29% 98.19% 93.28%

Net Liquidity as % of Total Assets 57.61% 56.57% 53.51% 49.23%

Source: BSMS Sample Credit Union Liquidity and Funding Risk Analysis

Forecast Cashflow – Scenario # 1

Current Environment: Liquidity Ratios

21

First Empire Securities, Inc.(800) 645-5424 www.1empire.com

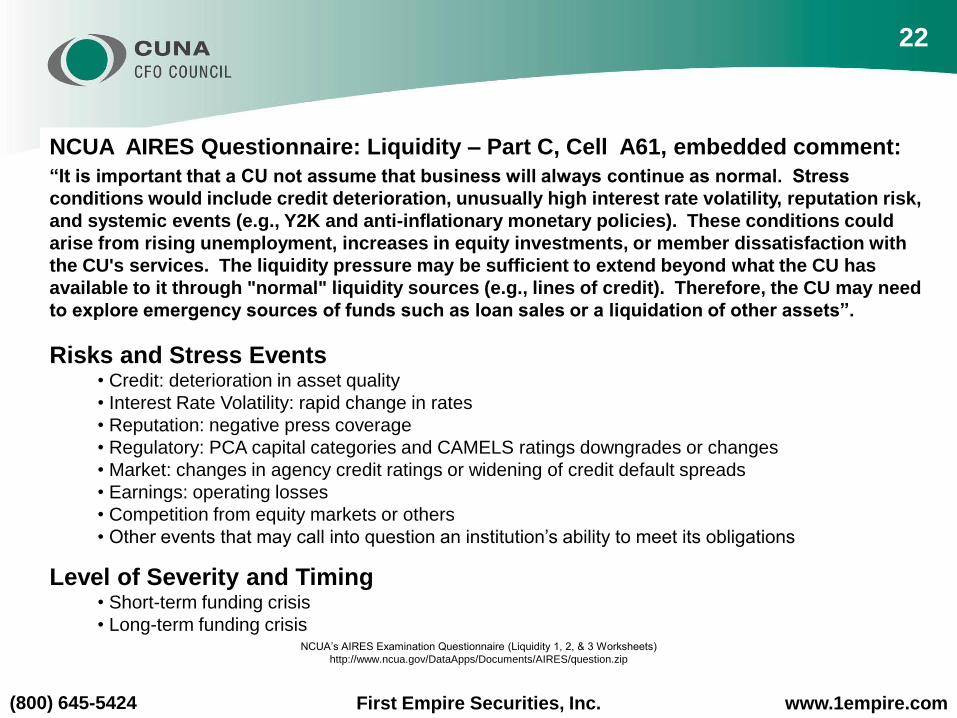

NCUA AIRES Questionnaire: Liquidity – Part C, Cell A61, embedded comment:

“It is important that a CU not assume that business will always continue as normal. Stress

conditions would include credit deterioration, unusually high interest rate volatility, reputation risk,

and systemic events (e.g., Y2K and anti-inflationary monetary policies). These conditions could

arise from rising unemployment, increases in equity investments, or member dissatisfaction with

the CU's services. The liquidity pressure may be sufficient to extend beyond what the CU has

available to it through "normal" liquidity sources (e.g., lines of credit). Therefore, the CU may need

to explore emergency sources of funds such as loan sales or a liquidation of other assets”.

Risks and Stress Events• Credit: deterioration in asset quality

• Interest Rate Volatility: rapid change in rates

• Reputation: negative press coverage

• Regulatory: PCA capital categories and CAMELS ratings downgrades or changes

• Market: changes in agency credit ratings or widening of credit default spreads

• Earnings: operating losses

• Competition from equity markets or others

• Other events that may call into question an institution’s ability to meet its obligations

Level of Severity and Timing• Short-term funding crisis

• Long-term funding crisisNCUA’s AIRES Examination Questionnaire (Liquidity 1, 2, & 3 Worksheets)

http://www.ncua.gov/DataApps/Documents/AIRES/question.zip

22

“It is important that a CU not assume that business will always continue as normal. Stress

conditions would include credit deterioration, unusually high interest rate volatility, reputation risk,

and systemic events (e.g., Y2K and anti-inflationary monetary policies). These conditions could

arise from rising unemployment, increases in equity investments, or member dissatisfaction with

the CU's services. The liquidity pressure may be sufficient to extend beyond what the CU has

available to it through "normal" liquidity sources (e.g., lines of credit). Therefore, the CU may need

to explore emergency sources of funds such as loan sales or a liquidation of other assets”.

Risks and Stress Events• Credit: deterioration in asset quality

• Interest Rate Volatility: rapid change in rates

• Reputation: negative press coverage

• Regulatory: PCA capital categories and CAMELS ratings downgrades or changes

• Market: changes in agency credit ratings or widening of credit default spreads

• Earnings: operating losses

• Competition from equity markets or others

• Other events that may call into question an institution’s ability to meet its obligations

Level of Severity and Timing• Short-term funding crisis

• Long-term funding crisis

First Empire Securities, Inc.(800) 645-5424 www.1empire.com

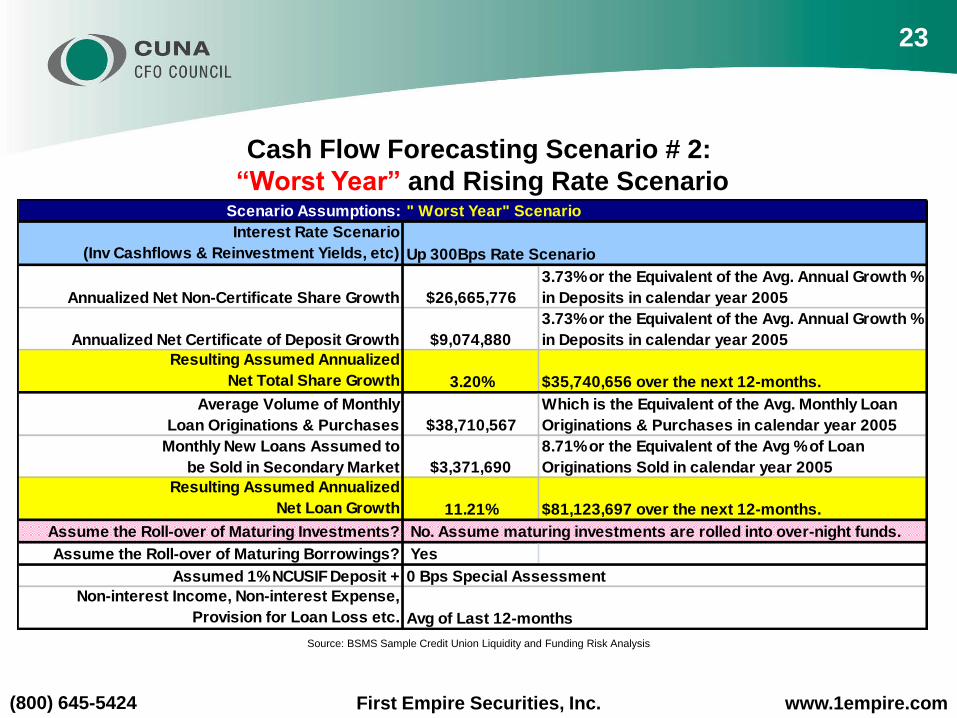

Cash Flow Forecasting Scenario # 2:

“Worst Year” and Rising Rate ScenarioScenario Assumptions: " Worst Year" Scenario

Interest Rate Scenario

(Inv Cashflows & Reinvestment Yields, etc) Up 300Bps Rate Scenario

Annualized Net Non-Certificate Share Growth $26,665,776

3.73% or the Equivalent of the Avg. Annual Growth %

in Deposits in calendar year 2005

Annualized Net Certificate of Deposit Growth $9,074,880

3.73% or the Equivalent of the Avg. Annual Growth %

in Deposits in calendar year 2005

Resulting Assumed Annualized

Net Total Share Growth 3.20% $35,740,656 over the next 12-months.

Average Volume of Monthly

Loan Originations & Purchases $38,710,567

Which is the Equivalent of the Avg. Monthly Loan

Originations & Purchases in calendar year 2005

Monthly New Loans Assumed to

be Sold in Secondary Market $3,371,690

8.71% or the Equivalent of the Avg % of Loan

Originations Sold in calendar year 2005

Resulting Assumed Annualized

Net Loan Growth 11.21% $81,123,697 over the next 12-months.

Assume the Roll-over of Maturing Investments? No. Assume maturing investments are rolled into over-night funds.

Assume the Roll-over of Maturing Borrowings? Yes

Assumed 1% NCUSIF Deposit + 0 Bps Special Assessment

Non-interest Income, Non-interest Expense,

Provision for Loan Loss etc. Avg of Last 12-months

Source: BSMS Sample Credit Union Liquidity and Funding Risk Analysis

23

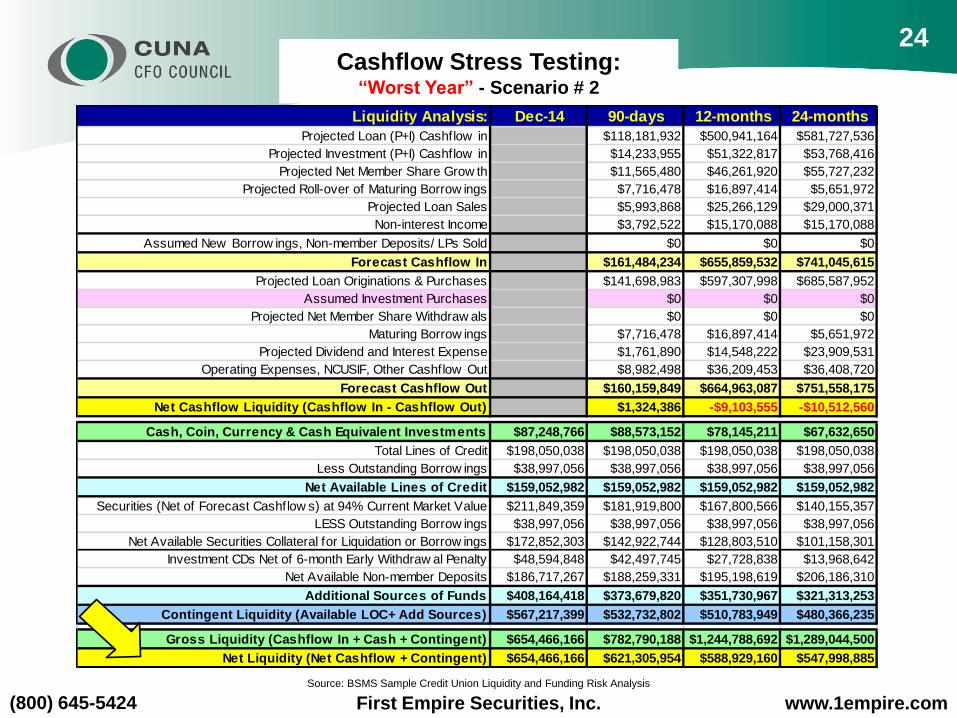

First Empire Securities, Inc.(800) 645-5424 www.1empire.com

Source: BSMS Sample Credit Union Liquidity and Funding Risk Analysis

Cashflow Stress Testing:“Worst Year” - Scenario # 2

Liquidity Analysis: Dec-14 90-days 12-months 24-months

Projected Loan (P+I) Cashflow in $118,181,932 $500,941,164 $581,727,536

Projected Investment (P+I) Cashflow in $14,233,955 $51,322,817 $53,768,416

Projected Net Member Share Grow th $11,565,480 $46,261,920 $55,727,232

Projected Roll-over of Maturing Borrow ings $7,716,478 $16,897,414 $5,651,972

Projected Loan Sales $5,993,868 $25,266,129 $29,000,371

Non-interest Income $3,792,522 $15,170,088 $15,170,088

Assumed New Borrow ings, Non-member Deposits/ LPs Sold $0 $0 $0

Forecast Cashflow In $161,484,234 $655,859,532 $741,045,615

Projected Loan Originations & Purchases $141,698,983 $597,307,998 $685,587,952

Assumed Investment Purchases $0 $0 $0

Projected Net Member Share Withdraw als $0 $0 $0

Maturing Borrow ings $7,716,478 $16,897,414 $5,651,972

Projected Dividend and Interest Expense $1,761,890 $14,548,222 $23,909,531

Operating Expenses, NCUSIF, Other Cashflow Out $8,982,498 $36,209,453 $36,408,720

Forecast Cashflow Out $160,159,849 $664,963,087 $751,558,175

Net Cashflow Liquidity (Cashflow In - Cashflow Out) $1,324,386 -$9,103,555 -$10,512,560

Cash, Coin, Currency & Cash Equivalent Investments $87,248,766 $88,573,152 $78,145,211 $67,632,650

Total Lines of Credit $198,050,038 $198,050,038 $198,050,038 $198,050,038

Less Outstanding Borrow ings $38,997,056 $38,997,056 $38,997,056 $38,997,056

Net Available Lines of Credit $159,052,982 $159,052,982 $159,052,982 $159,052,982

Securities (Net of Forecast Cashflow s) at 94% Current Market Value $211,849,359 $181,919,800 $167,800,566 $140,155,357

LESS Outstanding Borrow ings $38,997,056 $38,997,056 $38,997,056 $38,997,056

Net Available Securities Collateral for Liquidation or Borrow ings $172,852,303 $142,922,744 $128,803,510 $101,158,301

Investment CDs Net of 6-month Early Withdraw al Penalty $48,594,848 $42,497,745 $27,728,838 $13,968,642

Net Available Non-member Deposits $186,717,267 $188,259,331 $195,198,619 $206,186,310

Additional Sources of Funds $408,164,418 $373,679,820 $351,730,967 $321,313,253

Contingent Liquidity (Available LOC+ Add Sources) $567,217,399 $532,732,802 $510,783,949 $480,366,235

Gross Liquidity (Cashflow In + Cash + Contingent) $654,466,166 $782,790,188 $1,244,788,692 $1,289,044,500

Net Liquidity (Net Cashflow + Contingent) $654,466,166 $621,305,954 $588,929,160 $547,998,885

24

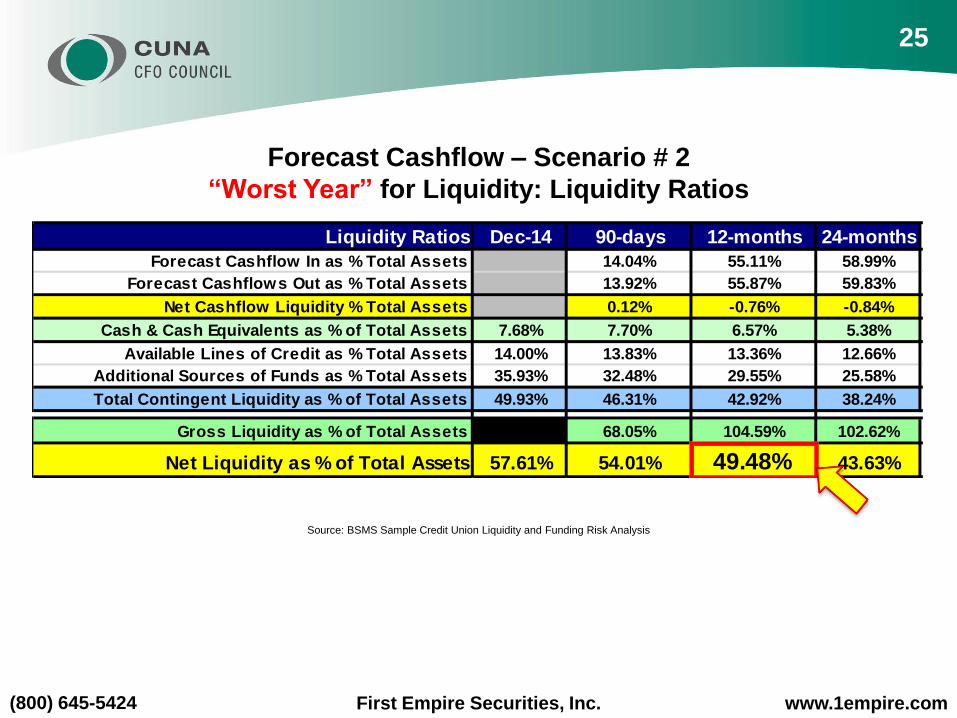

First Empire Securities, Inc.(800) 645-5424 www.1empire.com

Liquidity Ratios Dec-14 90-days 12-months 24-months

Forecast Cashflow In as % Total Assets 14.04% 55.11% 58.99%

Forecast Cashflows Out as % Total Assets 13.92% 55.87% 59.83%

Net Cashflow Liquidity % Total Assets 0.12% -0.76% -0.84%

Cash & Cash Equivalents as % of Total Assets 7.68% 7.70% 6.57% 5.38%

Available Lines of Credit as % Total Assets 14.00% 13.83% 13.36% 12.66%

Additional Sources of Funds as % Total Assets 35.93% 32.48% 29.55% 25.58%

Total Contingent Liquidity as % of Total Assets 49.93% 46.31% 42.92% 38.24%

Gross Liquidity as % of Total Assets 57.61% 68.05% 104.59% 102.62%

Net Liquidity as % of Total Assets 57.61% 54.01% 49.48% 43.63%

Source: BSMS Sample Credit Union Liquidity and Funding Risk Analysis

Forecast Cashflow – Scenario # 2

“Worst Year” for Liquidity: Liquidity Ratios

25

First Empire Securities, Inc.(800) 645-5424 www.1empire.com

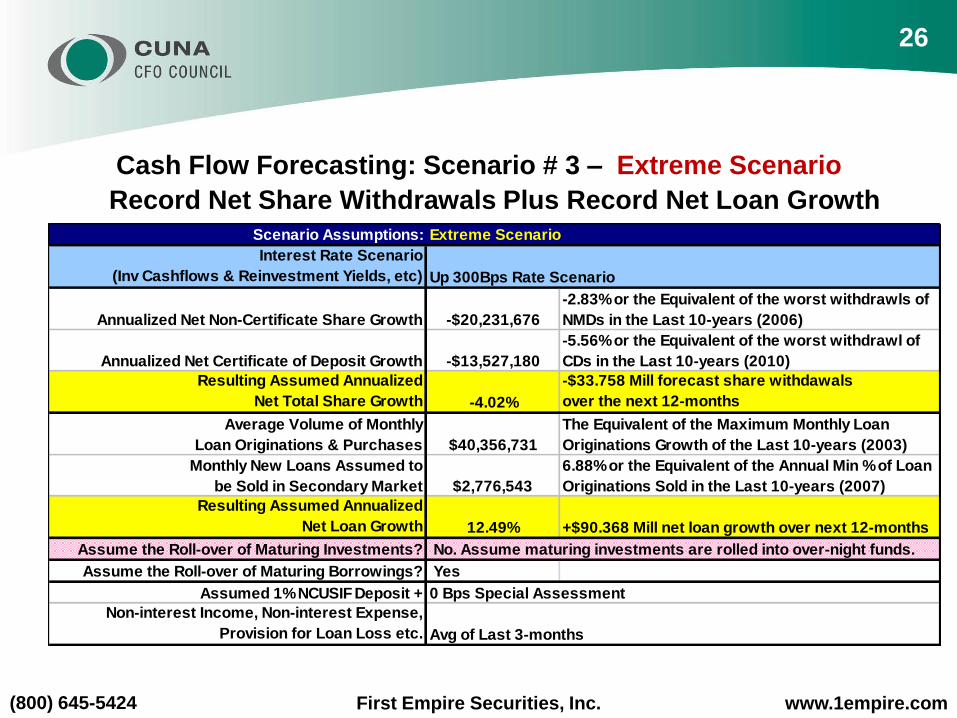

Cash Flow Forecasting: Scenario # 3 – Extreme Scenario

Scenario Assumptions: Extreme Scenario

Interest Rate Scenario

(Inv Cashflows & Reinvestment Yields, etc) Up 300Bps Rate Scenario

Annualized Net Non-Certificate Share Growth -$20,231,676

-2.83% or the Equivalent of the worst withdrawls of

NMDs in the Last 10-years (2006)

Annualized Net Certificate of Deposit Growth -$13,527,180

-5.56% or the Equivalent of the worst withdrawl of

CDs in the Last 10-years (2010)

Resulting Assumed Annualized

Net Total Share Growth -4.02%

-$33.758 Mill forecast share withdawals

over the next 12-months

Average Volume of Monthly

Loan Originations & Purchases $40,356,731

The Equivalent of the Maximum Monthly Loan

Originations Growth of the Last 10-years (2003)

Monthly New Loans Assumed to

be Sold in Secondary Market $2,776,543

6.88% or the Equivalent of the Annual Min % of Loan

Originations Sold in the Last 10-years (2007)

Resulting Assumed Annualized

Net Loan Growth 12.49% +$90.368 Mill net loan growth over next 12-months

Assume the Roll-over of Maturing Investments? No. Assume maturing investments are rolled into over-night funds.

Assume the Roll-over of Maturing Borrowings? Yes

Assumed 1% NCUSIF Deposit + 0 Bps Special Assessment

Non-interest Income, Non-interest Expense,

Provision for Loan Loss etc. Avg of Last 3-months

26

Record Net Share Withdrawals Plus Record Net Loan Growth

First Empire Securities, Inc.(800) 645-5424 www.1empire.com

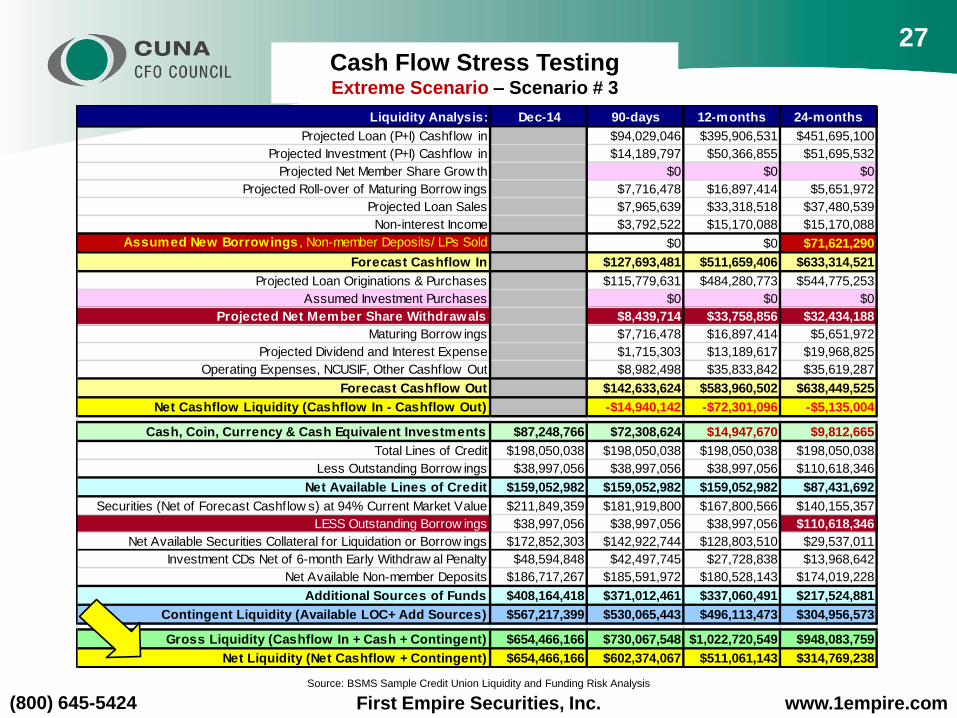

Cash Flow Stress Testing Extreme Scenario – Scenario # 3

Source: BSMS Sample Credit Union Liquidity and Funding Risk Analysis

Liquidity Analysis: Dec-14 90-days 12-months 24-months

Projected Loan (P+I) Cashflow in $94,029,046 $395,906,531 $451,695,100

Projected Investment (P+I) Cashflow in $14,189,797 $50,366,855 $51,695,532

Projected Net Member Share Grow th $0 $0 $0

Projected Roll-over of Maturing Borrow ings $7,716,478 $16,897,414 $5,651,972

Projected Loan Sales $7,965,639 $33,318,518 $37,480,539

Non-interest Income $3,792,522 $15,170,088 $15,170,088

Assumed New Borrowings , Non-member Deposits/ LPs Sold $0 $0 $71,621,290

Forecast Cashflow In $127,693,481 $511,659,406 $633,314,521

Projected Loan Originations & Purchases $115,779,631 $484,280,773 $544,775,253

Assumed Investment Purchases $0 $0 $0

Projected Net Member Share Withdrawals $8,439,714 $33,758,856 $32,434,188

Maturing Borrow ings $7,716,478 $16,897,414 $5,651,972

Projected Dividend and Interest Expense $1,715,303 $13,189,617 $19,968,825

Operating Expenses, NCUSIF, Other Cashflow Out $8,982,498 $35,833,842 $35,619,287

Forecast Cashflow Out $142,633,624 $583,960,502 $638,449,525

Net Cashflow Liquidity (Cashflow In - Cashflow Out) -$14,940,142 -$72,301,096 -$5,135,004

Cash, Coin, Currency & Cash Equivalent Investments $87,248,766 $72,308,624 $14,947,670 $9,812,665

Total Lines of Credit $198,050,038 $198,050,038 $198,050,038 $198,050,038

Less Outstanding Borrow ings $38,997,056 $38,997,056 $38,997,056 $110,618,346

Net Available Lines of Credit $159,052,982 $159,052,982 $159,052,982 $87,431,692

Securities (Net of Forecast Cashflow s) at 94% Current Market Value $211,849,359 $181,919,800 $167,800,566 $140,155,357

LESS Outstanding Borrow ings $38,997,056 $38,997,056 $38,997,056 $110,618,346

Net Available Securities Collateral for Liquidation or Borrow ings $172,852,303 $142,922,744 $128,803,510 $29,537,011

Investment CDs Net of 6-month Early Withdraw al Penalty $48,594,848 $42,497,745 $27,728,838 $13,968,642

Net Available Non-member Deposits $186,717,267 $185,591,972 $180,528,143 $174,019,228

Additional Sources of Funds $408,164,418 $371,012,461 $337,060,491 $217,524,881

Contingent Liquidity (Available LOC+ Add Sources) $567,217,399 $530,065,443 $496,113,473 $304,956,573

Gross Liquidity (Cashflow In + Cash + Contingent) $654,466,166 $730,067,548 $1,022,720,549 $948,083,759

Net Liquidity (Net Cashflow + Contingent) $654,466,166 $602,374,067 $511,061,143 $314,769,238

27

First Empire Securities, Inc.(800) 645-5424 www.1empire.com

Cash Flow Forecasting: Scenario # 3 – Extreme Scenario

Record Net Share Withdrawals Plus Record Net Loan Growth

Liquidity Ratios Dec-14 90-days 12-months 24-months

Forecast Cashflow In as % Total Assets 11.30% 46.09% 54.62%

Forecast Cashflows Out as % Total Assets 12.62% 52.61% 55.06%

Net Cashflow Liquidity % Total Assets -1.32% -6.51% -0.44%

Cash & Cash Equivalents as % of Total Assets 7.68% 6.40% 1.35% 0.85%

Available Lines of Credit as % Total Assets 14.00% 14.07% 14.33% 7.54%

Additional Sources of Funds as % Total Assets 35.93% 32.82% 30.36% 18.76%

Total Contingent Liquidity as % of Total Assets 49.93% 46.90% 44.69% 26.30%

Gross Liquidity as % of Total Assets 57.61% 64.59% 92.13% 81.76%

Net Liquidity as % of Total Assets 57.61% 53.29% 46.04% 27.15%

Source: BSMS Sample Credit Union Liquidity and Funding Risk Analysis

28

First Empire Securities, Inc.(800) 645-5424 www.1empire.com

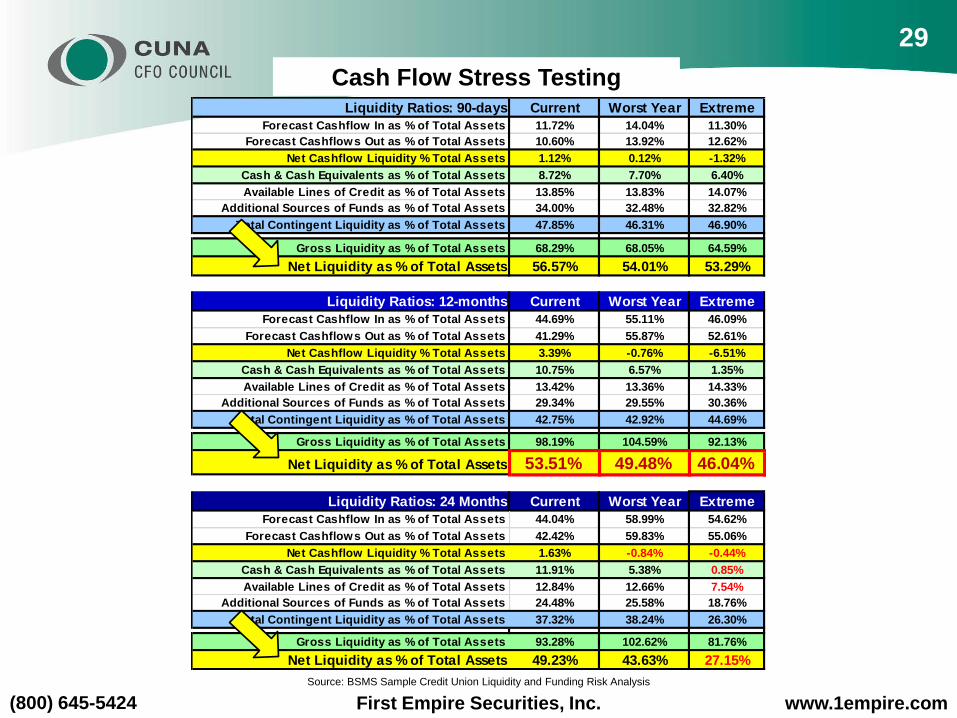

Liquidity Ratios: 90-days Current Worst Year Extreme

Forecast Cashflow In as % of Total Assets 11.72% 14.04% 11.30%

Forecast Cashflows Out as % of Total Assets 10.60% 13.92% 12.62%

Net Cashflow Liquidity % Total Assets 1.12% 0.12% -1.32%

Cash & Cash Equivalents as % of Total Assets 8.72% 7.70% 6.40%

Available Lines of Credit as % of Total Assets 13.85% 13.83% 14.07%

Additional Sources of Funds as % of Total Assets 34.00% 32.48% 32.82%

Total Contingent Liquidity as % of Total Assets 47.85% 46.31% 46.90%

Gross Liquidity as % of Total Assets 68.29% 68.05% 64.59%

Net Liquidity as % of Total Assets 56.57% 54.01% 53.29%

Liquidity Ratios: 12-months Current Worst Year Extreme

Forecast Cashflow In as % of Total Assets 44.69% 55.11% 46.09%

Forecast Cashflows Out as % of Total Assets 41.29% 55.87% 52.61%

Net Cashflow Liquidity % Total Assets 3.39% -0.76% -6.51%

Cash & Cash Equivalents as % of Total Assets 10.75% 6.57% 1.35%

Available Lines of Credit as % of Total Assets 13.42% 13.36% 14.33%

Additional Sources of Funds as % of Total Assets 29.34% 29.55% 30.36%

Total Contingent Liquidity as % of Total Assets 42.75% 42.92% 44.69%

Gross Liquidity as % of Total Assets 98.19% 104.59% 92.13%

Net Liquidity as % of Total Assets 53.51% 49.48% 46.04%

Liquidity Ratios: 24 Months Current Worst Year Extreme

Forecast Cashflow In as % of Total Assets 44.04% 58.99% 54.62%

Forecast Cashflows Out as % of Total Assets 42.42% 59.83% 55.06%

Net Cashflow Liquidity % Total Assets 1.63% -0.84% -0.44%

Cash & Cash Equivalents as % of Total Assets 11.91% 5.38% 0.85%

Available Lines of Credit as % of Total Assets 12.84% 12.66% 7.54%

Additional Sources of Funds as % of Total Assets 24.48% 25.58% 18.76%

Total Contingent Liquidity as % of Total Assets 37.32% 38.24% 26.30%

Gross Liquidity as % of Total Assets 93.28% 102.62% 81.76%

Net Liquidity as % of Total Assets 49.23% 43.63% 27.15%

Source: BSMS Sample Credit Union Liquidity and Funding Risk Analysis

Cash Flow Stress Testing

29

First Empire Securities, Inc.(800) 645-5424 www.1empire.com

Summary:

Effective March 2014, NCUA requires every credit union to have a Liquidity Policy and

to measure, monitor, and manage its liquidity and liquidity risk.

Credit unions over $50 million in assets must have a formal written Contingency

Funding Plan. Credit unions over $250 million in assets must also have an

established line of credit with the Federal Reserve or the Central Liquidity Facility.

The examiners expect each credit union to have liquidity management processes and

procedures in place commensurate with the size and complexity of its balance sheet.

In particular, the examiners expect credit unions to measure and manage liquidity risk:

1. Using cashflow projections

2. Having diversified funding sources

3. Stress testing cashflow forecasts

4. Maintaining a cushion of liquid assets

5. Adopting a formal well-developed Contingency Funding Plan (CFP)

Historical analysis of member behavior will provide the credit union unique, institution-

specific metrics for developing reasonable and supportable assumptions.

30

First Empire Securities, Inc.(800) 645-5424 www.1empire.com

Thank You!

The information in this document has been obtained from sources we believe to be reliable, however, we do not guarantee it is accurate or

complete. From time to time officers, employees of the firm, or the firm itself holds a position in the securities referred herein, or acts as principal

in transactions referred to herein. Parts of this document are based on assumptions, which we believe to be reasonable and supportable,

however, future events may influence actual performance. The projections contained herein are hypothetical in nature, and do not reflect actual

balance sheet or investment results and are not guarantees of future results. This document is not and should not be construed as an offer or

solicitation of an offer to buy or sell any security or securities. Securities have inherent risk, including credit, prepayment, extension and market

risk. This information is subject to change without notice. Clients of First Empire Securities, Inc. may also be clients of FESI’s affiliated

companies. Affiliated companies may receive compensation or fees from clients and, as a result, the affiliated companies may have conflicted

interests, loyalties and responsibilities. Balance Sheet Management Services, LPC Services and First Empire CD Management are affiliates of

First Empire Securities, Inc. The affiliates are not a member of FINRA/SIPC. First Empire Securities, Inc., is solely a member of FINRA/SIPC.

31

![NCUA SIF Presentation Mar 2014 [Read-Only]](https://img.pdfslide.net/doc/110x75/6251de20917ba076b31e8dc3/ncua-sif-presentation-mar-2014-read-only.jpg)