Embed Size (px)

DESCRIPTION

As the largest search engine marketing firm, Efficient Frontier has access to tremendous amounts of search engine data. Join them for an overview of the most recent quarterly search engine performance report. Hear how the recession has affected consumer search trends and what we are likely to see in the future.

Citation preview

What’s around the corner? Trends in SEMTrends in SEM

Merinda Peppard

European Marketing Manager

Dr. Siddharth Shah

Director of Business Analytics

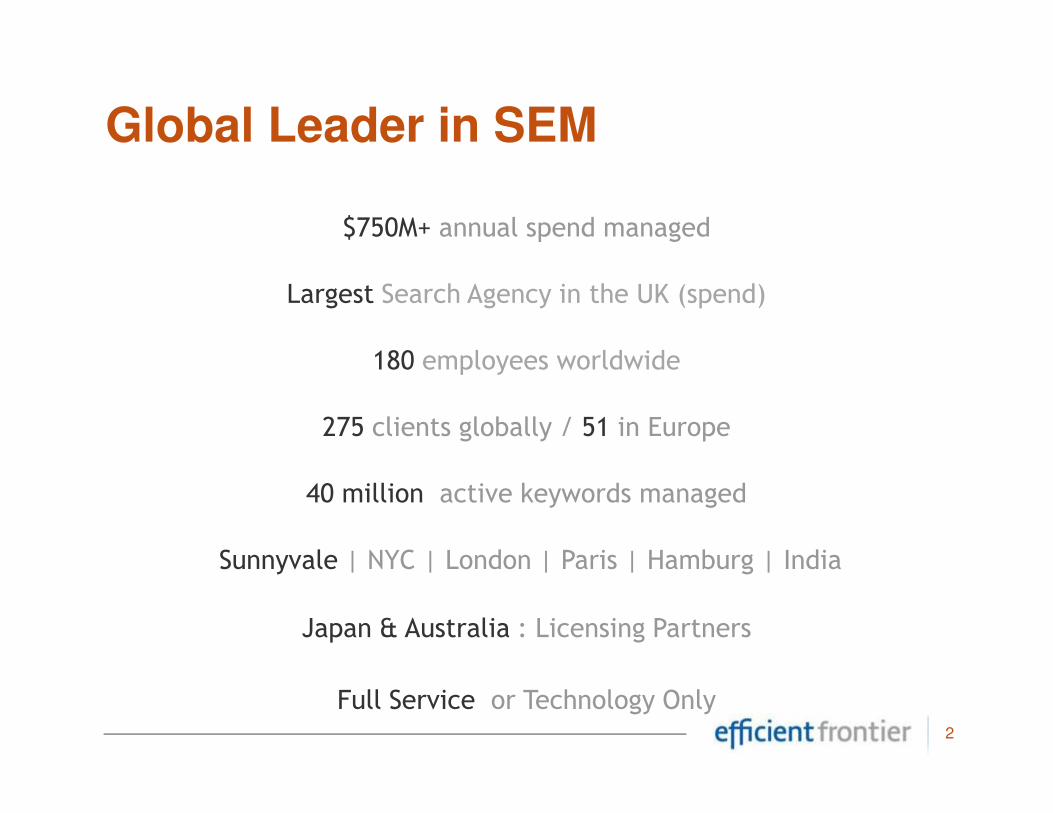

Global Leader in SEM

$750M+ annual spend managed

Largest Search Agency in the UK (spend)

180 employees worldwide

2

275 clients globally / 51 in Europe

40 million active keywords managed

Sunnyvale | NYC | London | Paris | Hamburg | India

Japan & Australia : Licensing Partners

Full Service or Technology Only

Today’s Agenda

• What’s new?

• How does online compare to other advertising?

• Taking a look at Search

• Efficient Frontier UK Search Report• Efficient Frontier UK Search Report

• Efficient Frontier U.S. Search Report

• What does it mean for the UK?

3

What’s New?

4

Positive news

5

Interesting Trends

£10 more per visit

25-34 year olds

6

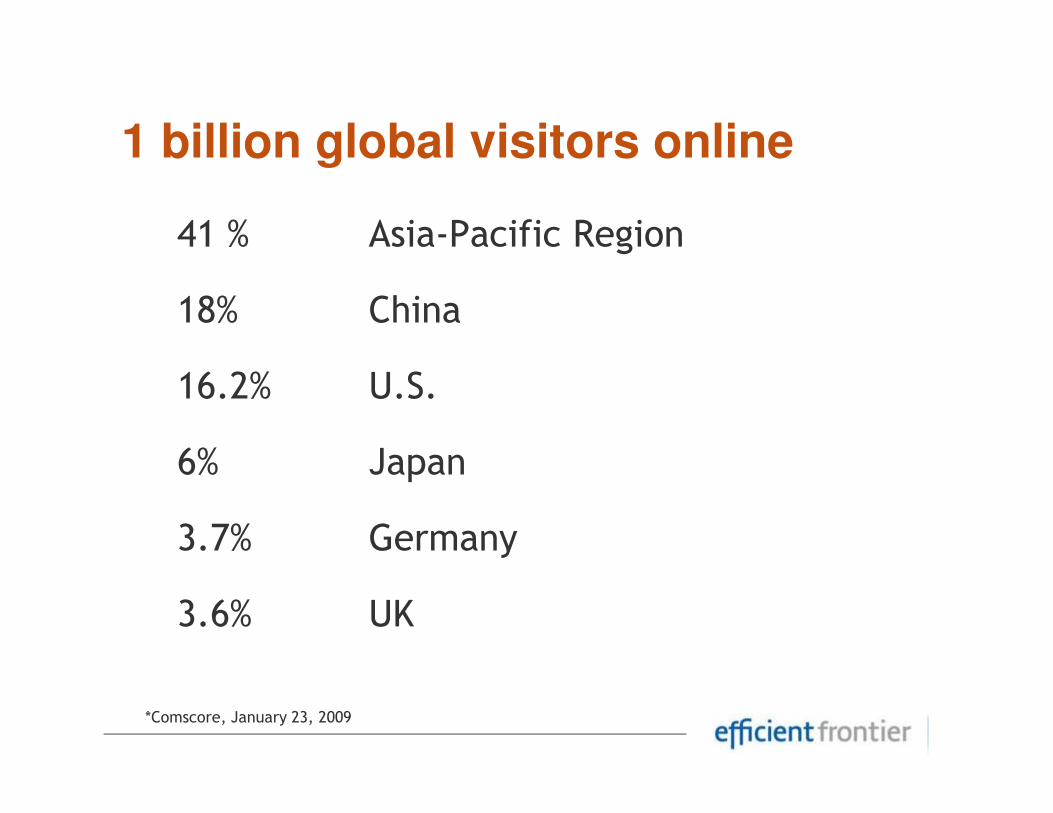

41 % Asia-Pacific Region

18% China

16.2% U.S.

1 billion global visitors online

16.2% U.S.

6% Japan

3.7% Germany

3.6% UK

Source: PricewaterhouseCoopers / Internet Advertising Bureau / WARC

*Comscore, January 23, 2009

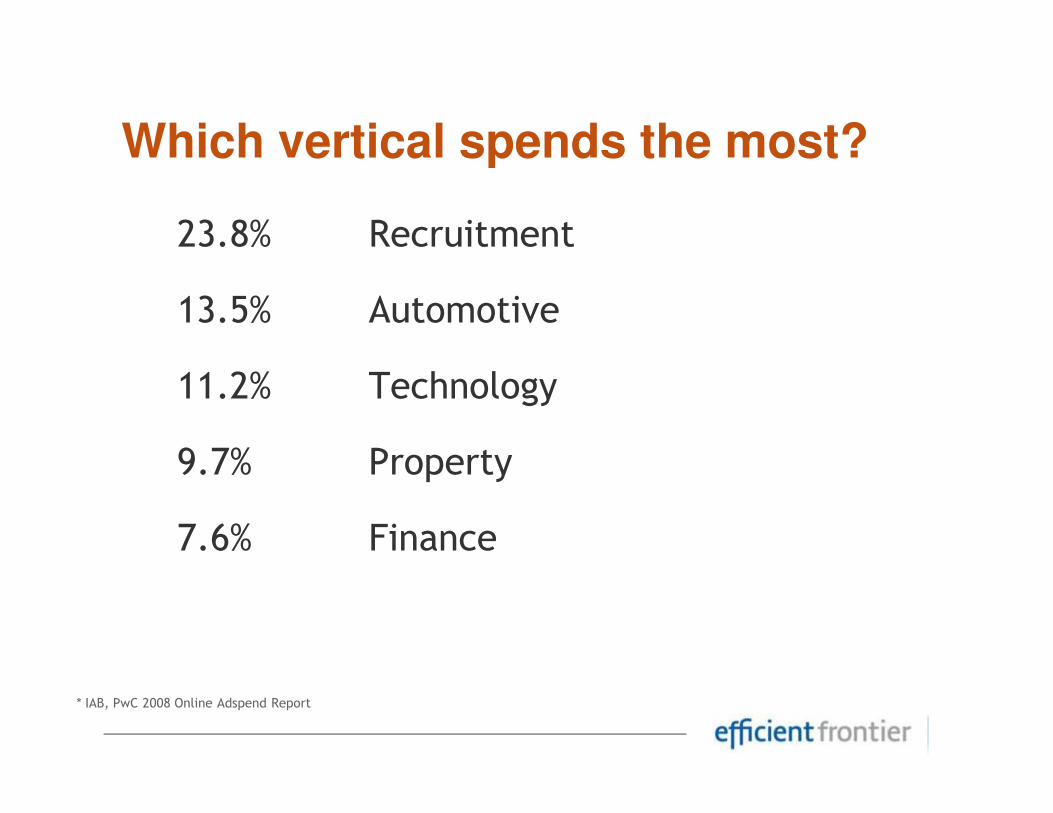

23.8% Recruitment

13.5% Automotive

11.2% Technology

Which vertical spends the most?

11.2% Technology

9.7% Property

7.6% Finance

Source: PricewaterhouseCoopers / Internet Advertising Bureau / WARC

* IAB, PwC 2008 Online Adspend Report

How does online compare to other

advertising?

9

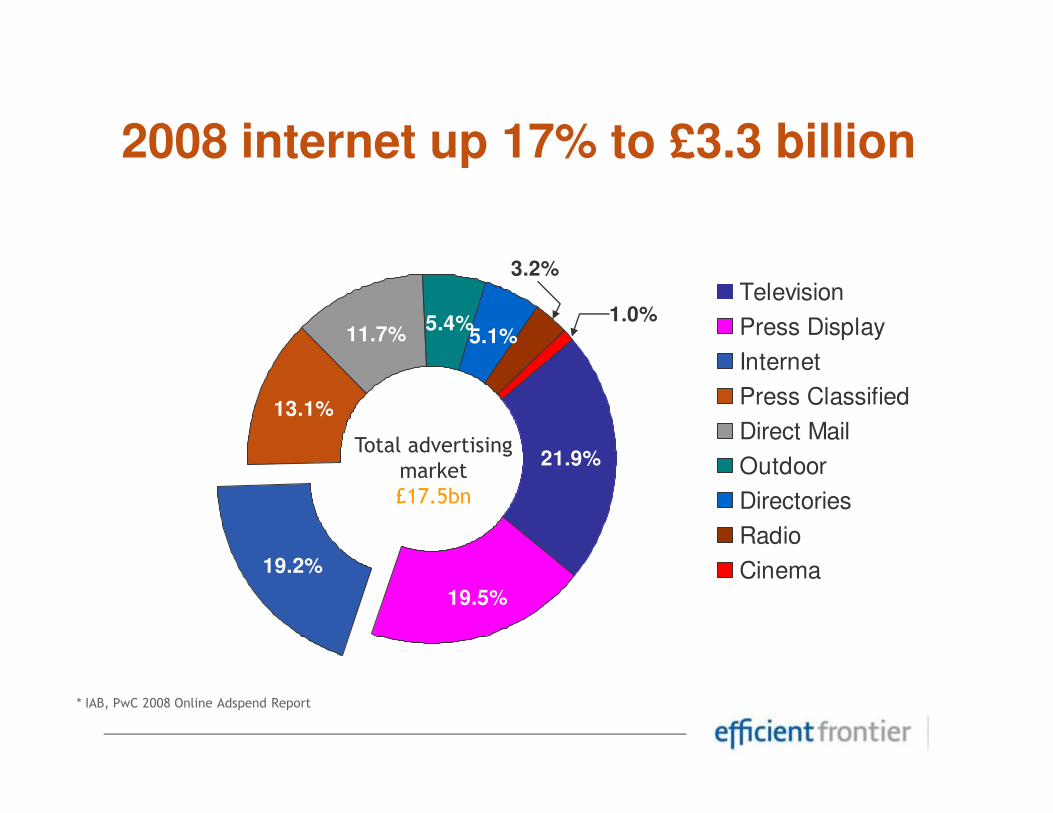

2008 internet up 17% to £3.3 billion

11.7% 5.1%

3.2%

1.0%5.4%

13.1%

Television

Press Display

Internet

Press Classified

Source: PricewaterhouseCoopers / Internet Advertising Bureau / WARC

* IAB, PwC 2008 Online Adspend Report

Total advertisingmarket£17.5bn

21.9%

19.2%

13.1%

19.5%

Press Classified

Direct Mail

Outdoor

Directories

Radio

Cinema

Taking a look at Search

11

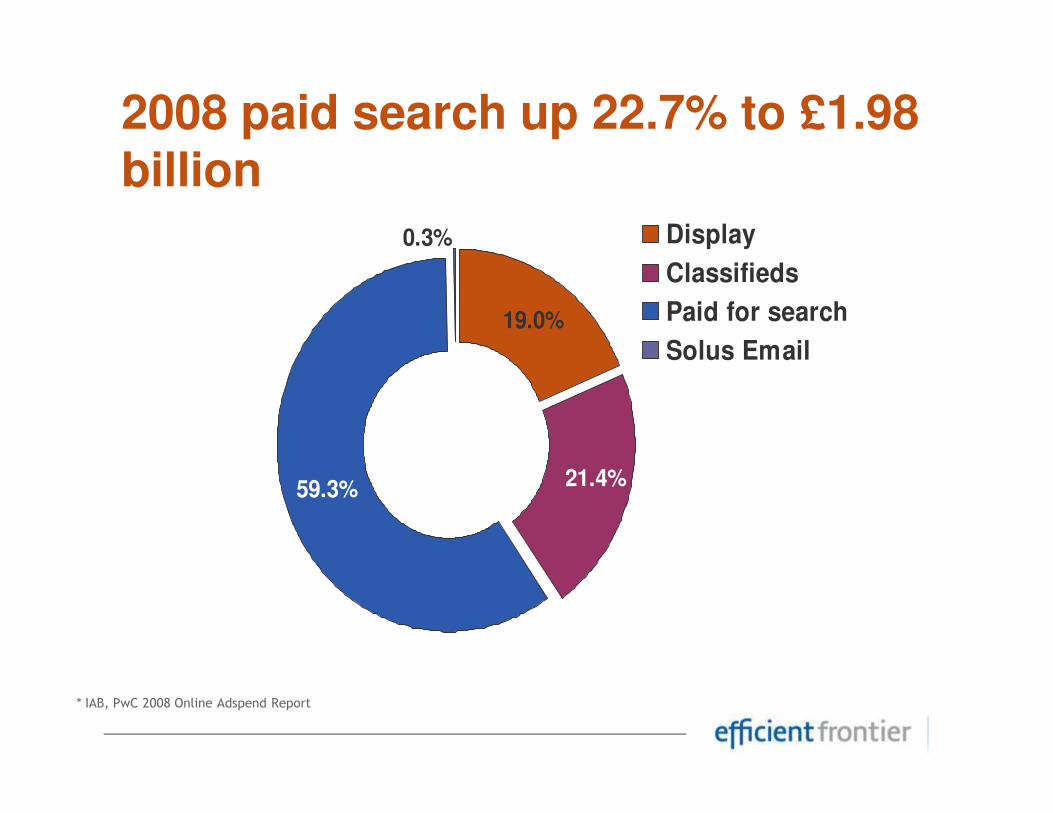

19.0%

0.3% Display

Classifieds

Paid for search

Solus Email

2008 paid search up 22.7% to £1.98 billion

59.3% 21.4%

Source: PricewaterhouseCoopers / Internet Advertising Bureau / WARC

* IAB, PwC 2008 Online Adspend Report

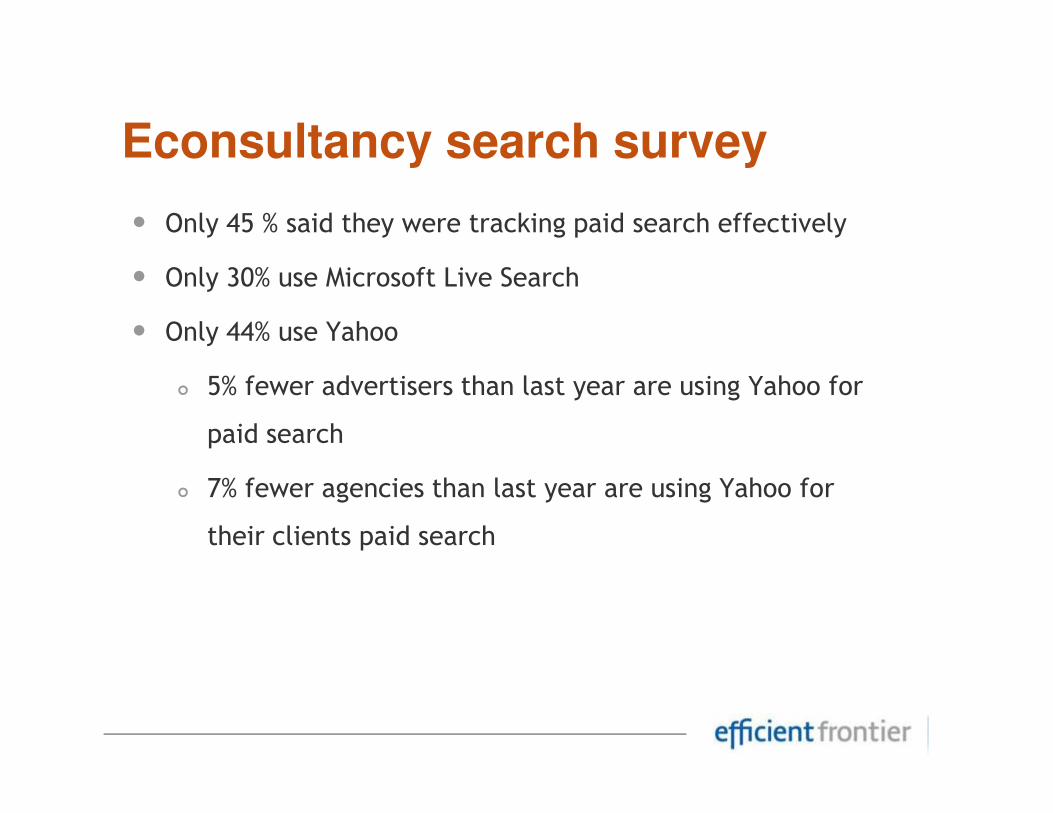

• Only 45 % said they were tracking paid search effectively

• Only 30% use Microsoft Live Search

• Only 44% use Yahoo

� 5% fewer advertisers than last year are using Yahoo for

Econsultancy search survey

paid search

� 7% fewer agencies than last year are using Yahoo for

their clients paid search

Efficient Frontier

UK Search Report

14

• SE spend reports issued each quarter

• Consistent basket of UK clients

• Travel, retail, finance and other verticals

Quarterly Reports

15

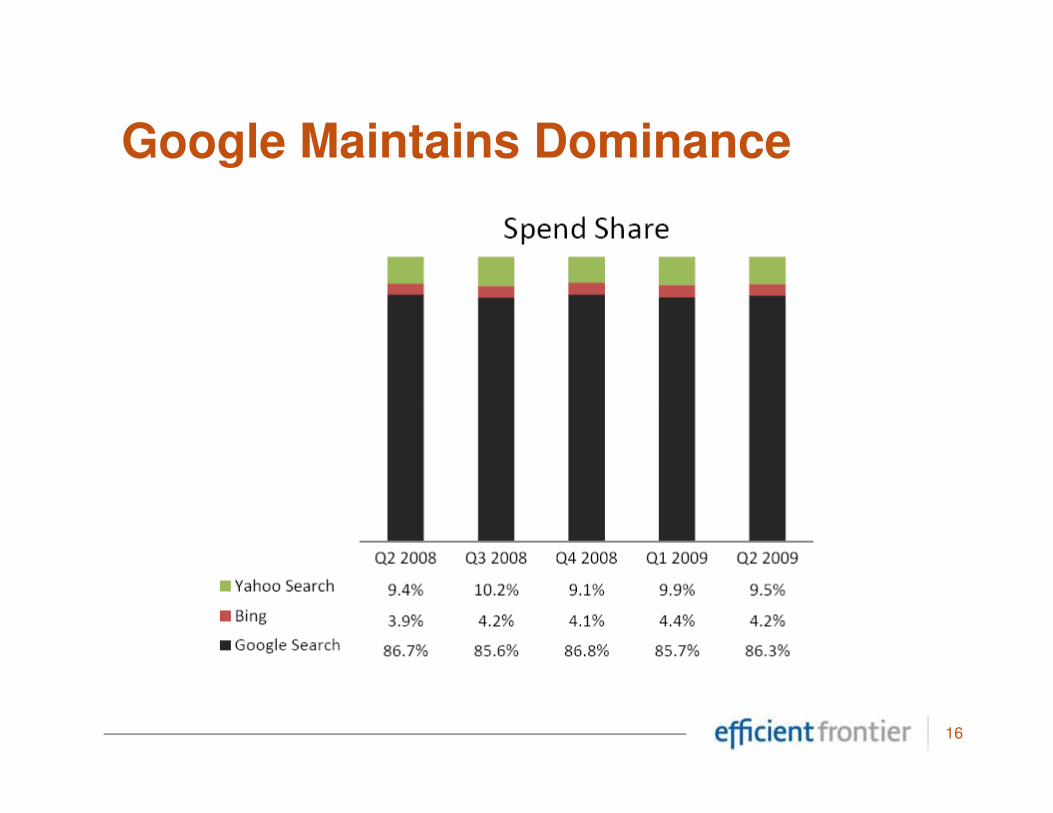

Google Maintains Dominance

16

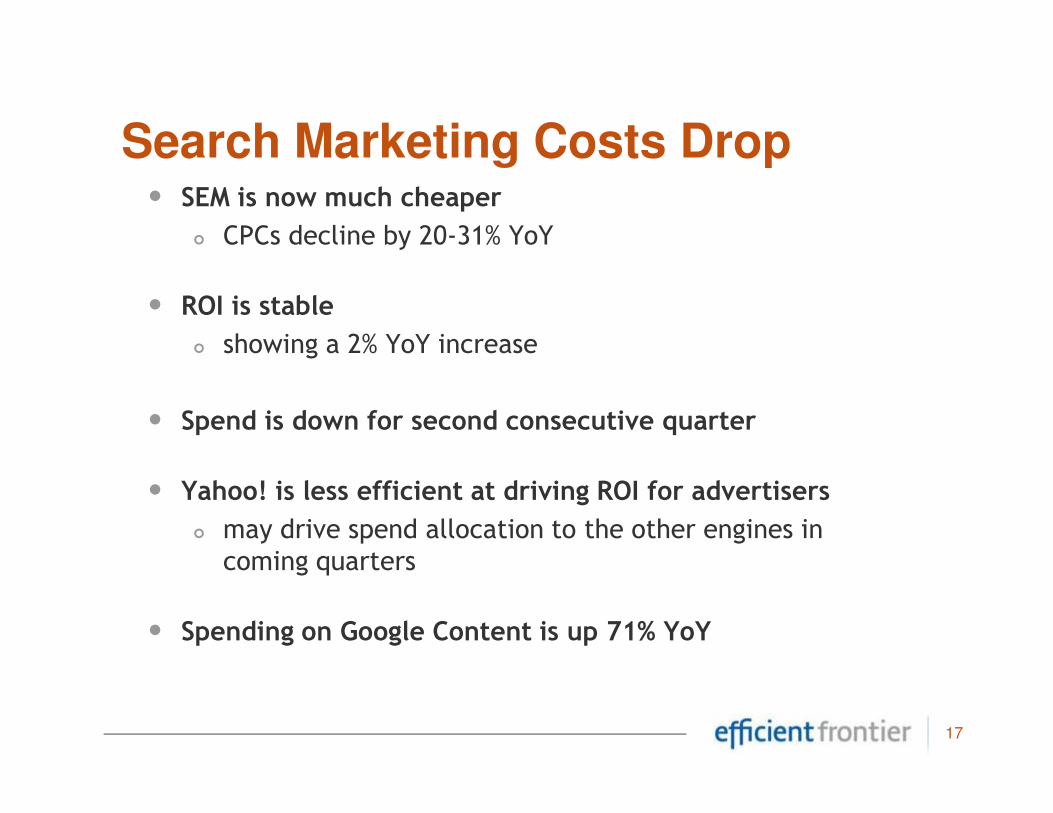

• SEM is now much cheaper

� CPCs decline by 20-31% YoY

• ROI is stable

� showing a 2% YoY increase

• Spend is down for second consecutive quarter

Search Marketing Costs Drop

• Spend is down for second consecutive quarter

• Yahoo! is less efficient at driving ROI for advertisers

� may drive spend allocation to the other engines in coming quarters

• Spending on Google Content is up 71% YoY

17

What does the future hold?

18

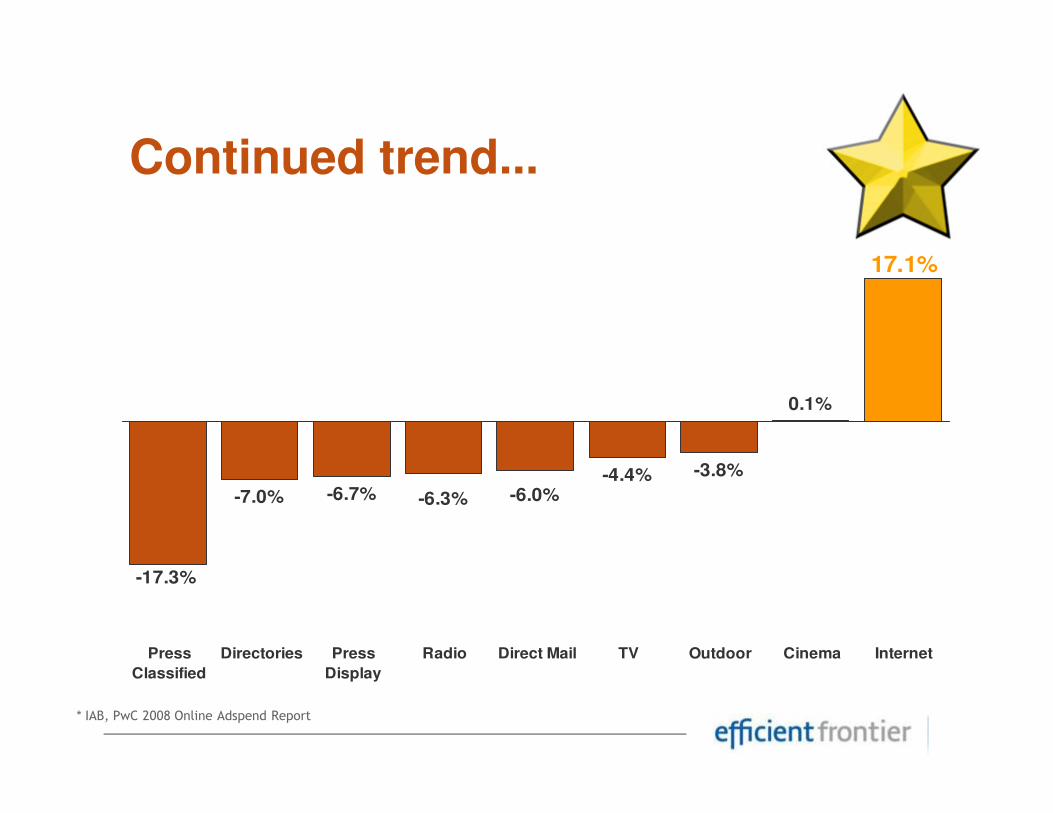

Continued trend...

0.1%

17.1%

-7.0%

-4.4% -3.8%

0.1%

-17.3%

-6.0%-6.3%-6.7%

Press

Classified

Directories Press

Display

Radio Direct Mail TV Outdoor Cinema Internet

* IAB, PwC 2008 Online Adspend Report

What does it mean....for Search?

“Search advertising remains among the most measurable media available to advertisers, which we suspect with continue to allow search to outperform other media.

Secondly, search advertising is what potential consumers tend to see Secondly, search advertising is what potential consumers tend to see in the final moments before purchase, making search marketing less discretionary than other forms of advertising. As a result of such characteristics, we believe search to be relatively well positioned heading into a recovery and we expect U.S. search advertising to increase 16% in 2010 and at a 13% CAGR for the next five years.”

Credit Suisse, US advertising Outlook, Sept 09

Efficient Frontier

U.S. Search Report

21

• Small shifts in spend trends QoQ

• Bing has increased its Market Share both by spend and clicks

• Increased ROI focus specially from small advertisers

• Travel is hurting

Insights from the US

• Automotive has seen slight recent improvement

• Finance has made a recovery

22

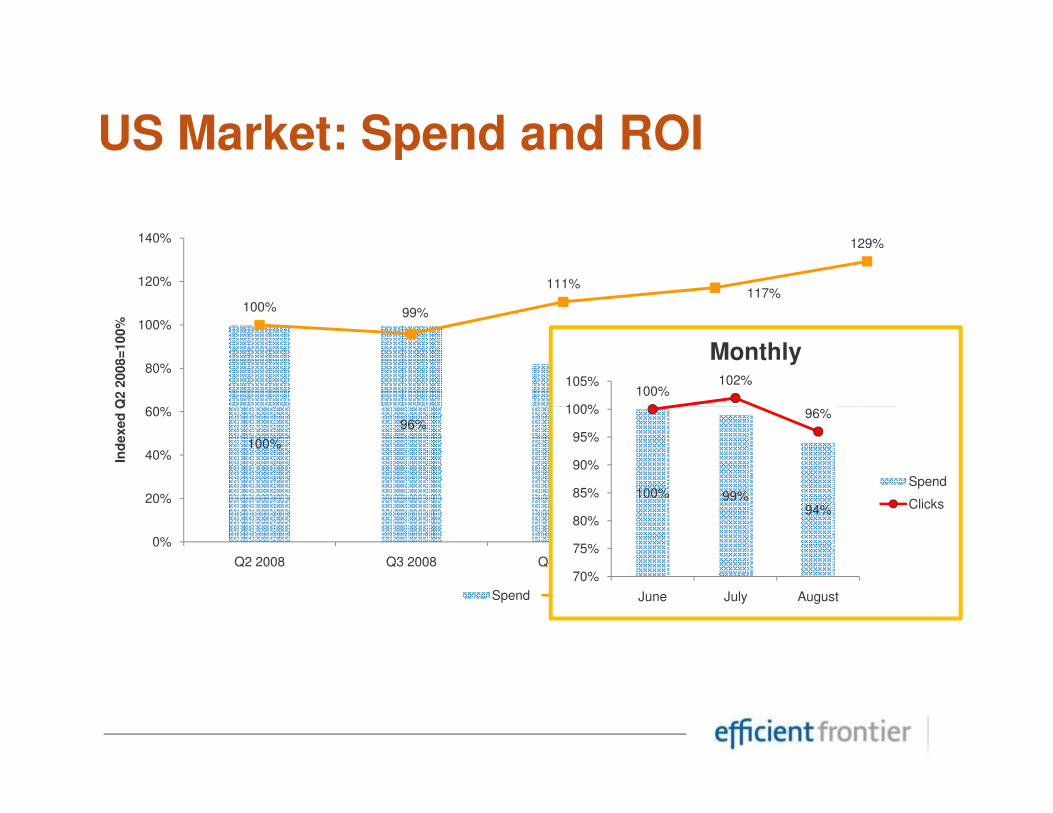

US Market: Spend and ROI

99%100%

111%117%

129%

60%

80%

100%

120%

140%

Q2 2

008=

100%

100%102%

96%100%

105%

Monthly

100%

82%

81%79%

96%

0%

20%

40%

60%

Q2 2008 Q3 2008 Q4 2008 Q1 2009 Q2 2009

Ind

exed

Q2

Spend ROI

100% 99%94%

96%

70%

75%

80%

85%

90%

95%

100%

June July August

Spend

Clicks

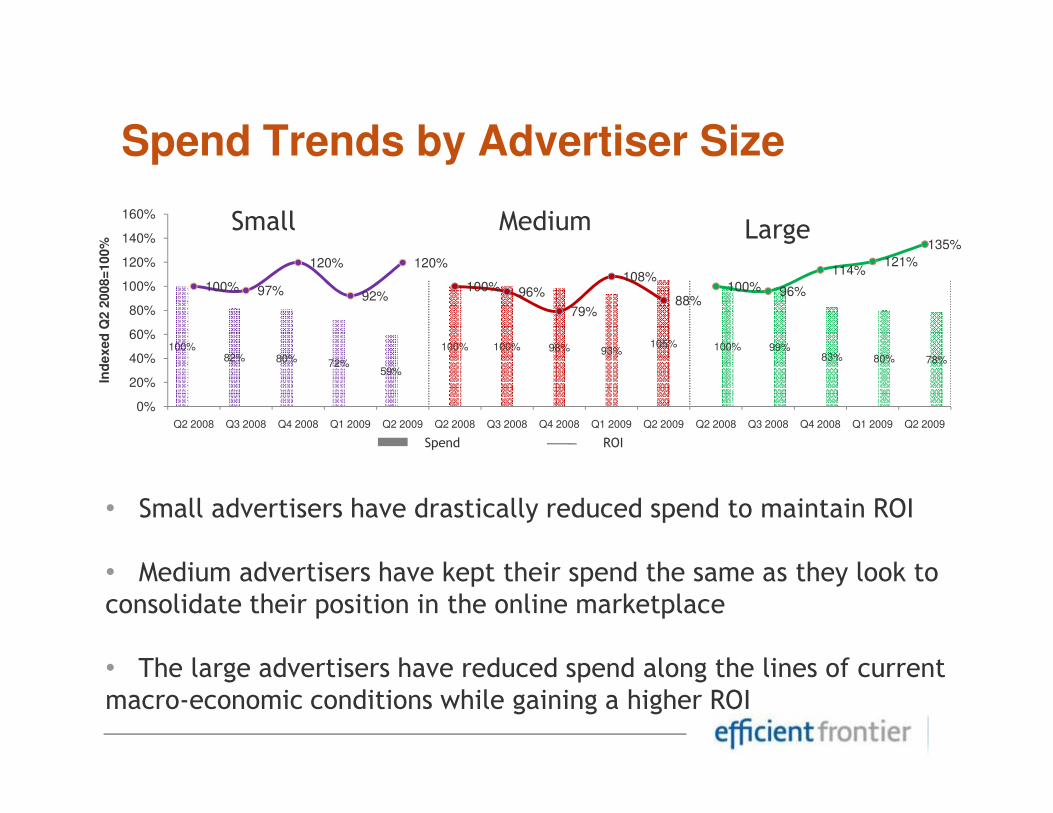

Spend Trends by Advertiser Size

100%82% 80% 72%

59%

100% 100% 98% 93%105% 100% 99%

83% 80% 78%

100% 97%

120%

92%

120%

100% 96%

79%

108%

88%100% 96%

114%121%

135%

0%

20%

40%

60%

80%

100%

120%

140%

160%

Ind

exed

Q2 2

008=

100%

Small Medium Large

• Small advertisers have drastically reduced spend to maintain ROI

• Medium advertisers have kept their spend the same as they look to consolidate their position in the online marketplace

• The large advertisers have reduced spend along the lines of current macro-economic conditions while gaining a higher ROI

0%

Q2 2008 Q3 2008 Q4 2008 Q1 2009 Q2 2009 Q2 2008 Q3 2008 Q4 2008 Q1 2009 Q2 2009 Q2 2008 Q3 2008 Q4 2008 Q1 2009 Q2 2009

Small Adv. Med Adv. Large Adv. Small ROI Med ROI Large ROISpend ROI

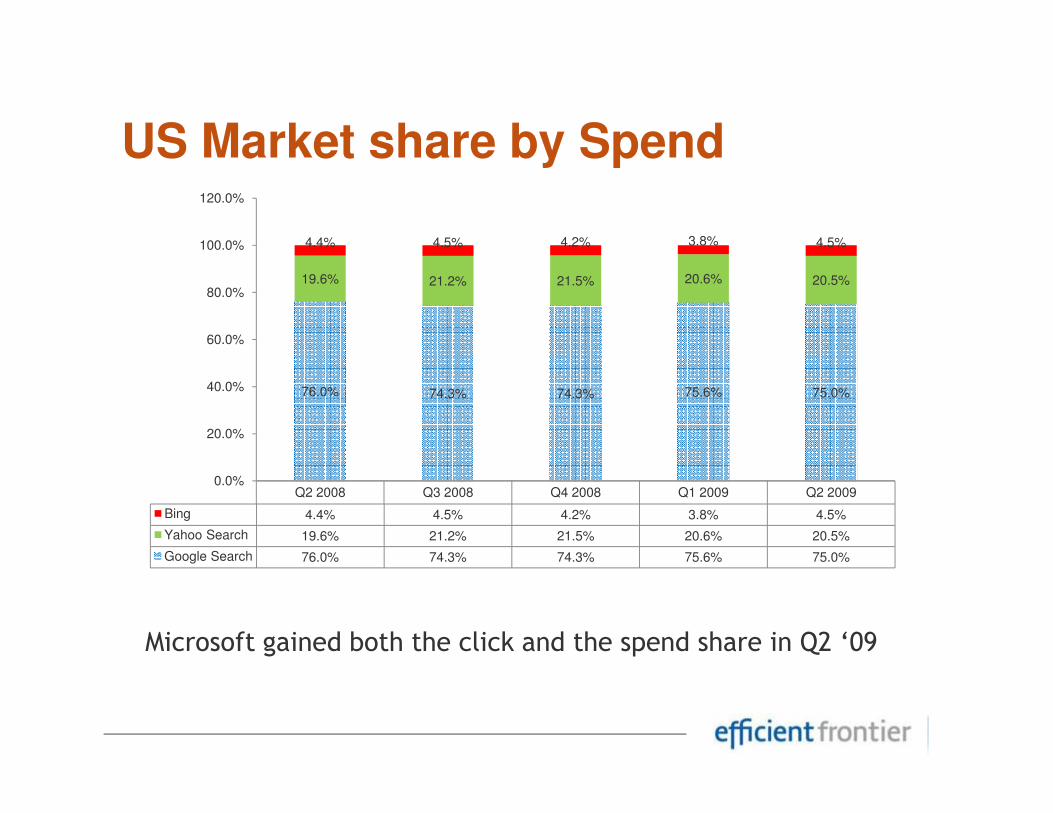

US Market share by Spend

76.0% 74.3% 74.3% 75.6% 75.0%

19.6% 21.2% 21.5% 20.6% 20.5%

4.4% 4.5% 4.2% 3.8% 4.5%

40.0%

60.0%

80.0%

100.0%

120.0%

Q2 2008 Q3 2008 Q4 2008 Q1 2009 Q2 2009

Bing 4.4% 4.5% 4.2% 3.8% 4.5%

Yahoo Search 19.6% 21.2% 21.5% 20.6% 20.5%

Google Search 76.0% 74.3% 74.3% 75.6% 75.0%

0.0%

20.0%

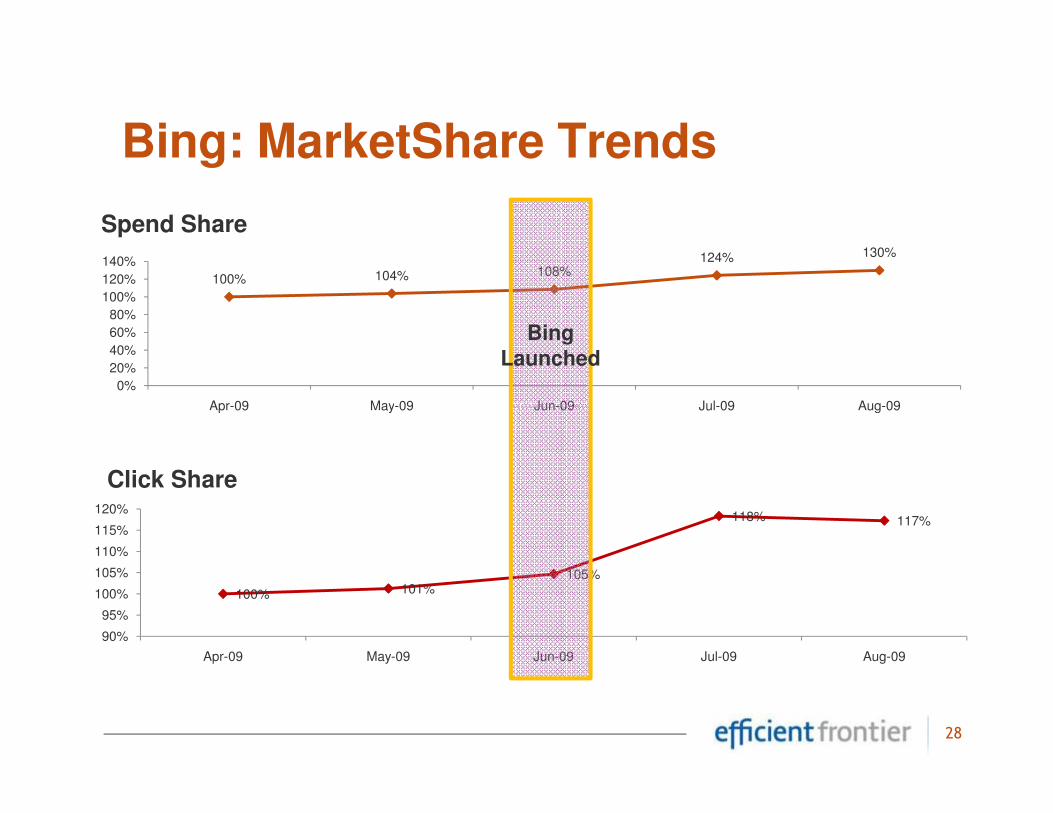

Microsoft gained both the click and the spend share in Q2 ‘09

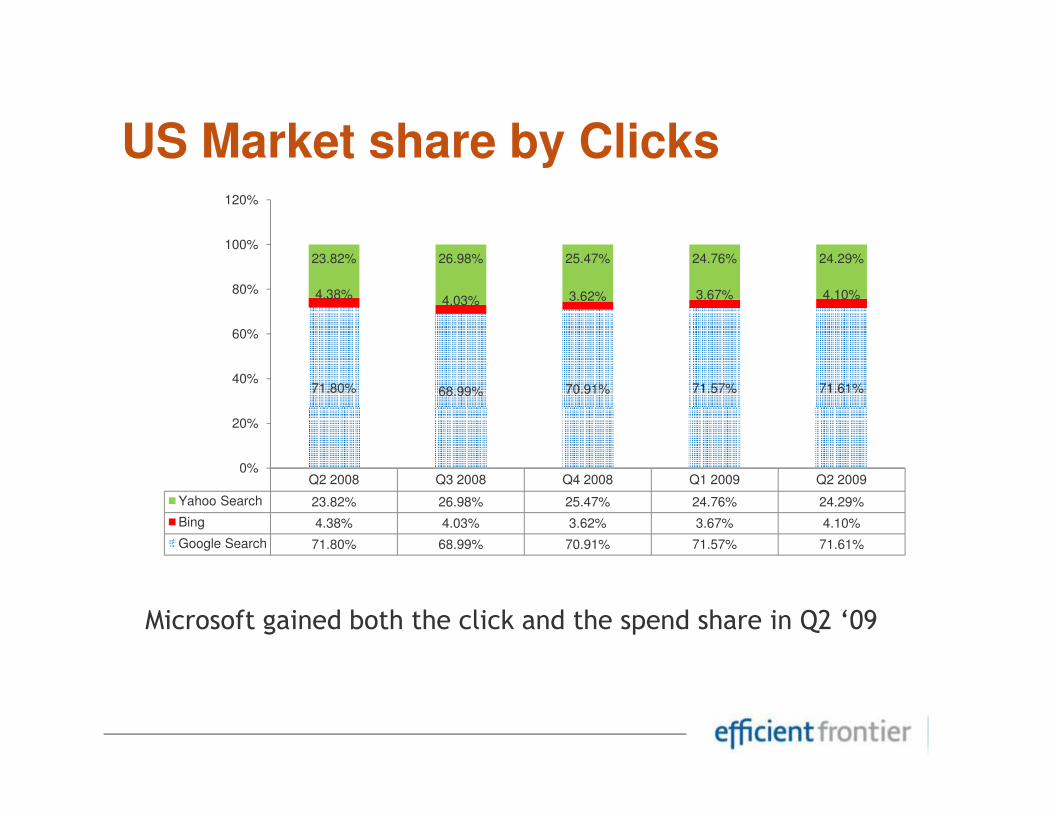

US Market share by Clicks

71.80% 68.99% 70.91% 71.57% 71.61%

4.38% 4.03% 3.62% 3.67% 4.10%

23.82% 26.98% 25.47% 24.76% 24.29%

40%

60%

80%

100%

120%

Q2 2008 Q3 2008 Q4 2008 Q1 2009 Q2 2009

Yahoo Search 23.82% 26.98% 25.47% 24.76% 24.29%

Bing 4.38% 4.03% 3.62% 3.67% 4.10%

Google Search 71.80% 68.99% 70.91% 71.57% 71.61%

0%

20%

Microsoft gained both the click and the spend share in Q2 ‘09

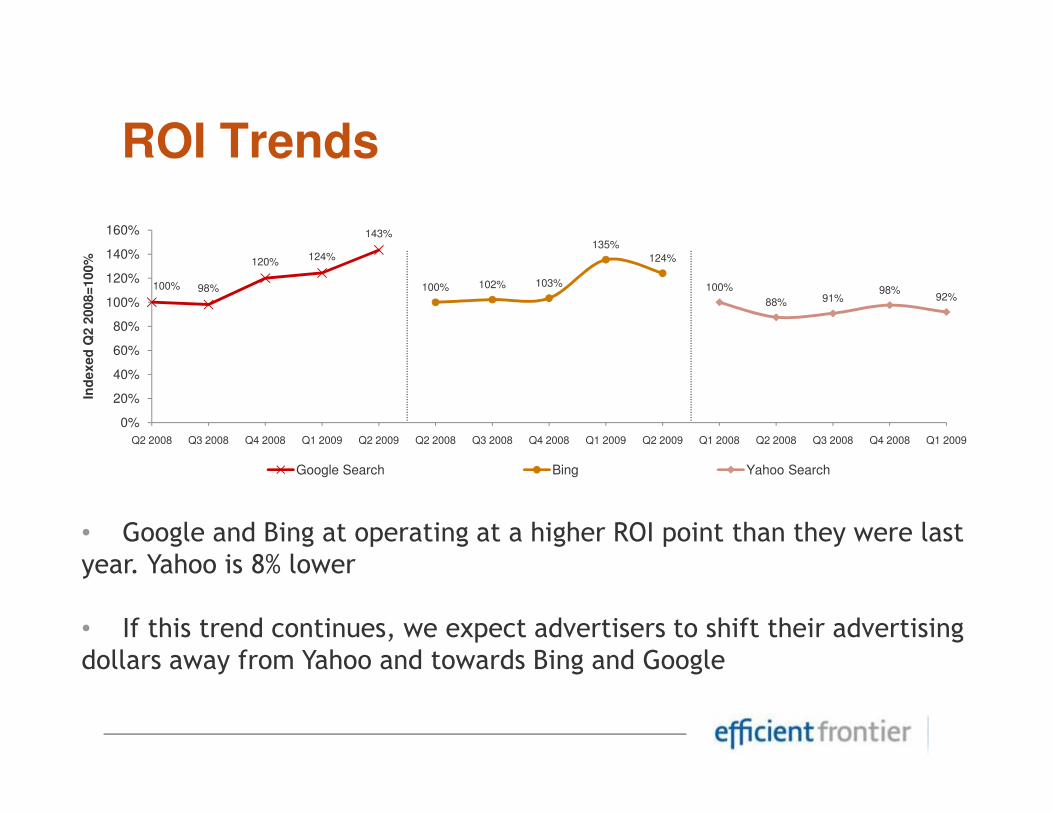

ROI Trends

100% 98%

120%124%

143%

100% 102% 103%

135%

124%

100%

88% 91%98%

92%

20%

40%

60%

80%

100%

120%

140%

160%

Ind

exed

Q2 2

008=

100%

0%

Q2 2008 Q3 2008 Q4 2008 Q1 2009 Q2 2009 Q2 2008 Q3 2008 Q4 2008 Q1 2009 Q2 2009 Q1 2008 Q2 2008 Q3 2008 Q4 2008 Q1 2009

Google Search Bing Yahoo Search

• Google and Bing at operating at a higher ROI point than they were last year. Yahoo is 8% lower

• If this trend continues, we expect advertisers to shift their advertising dollars away from Yahoo and towards Bing and Google

Bing: MarketShare Trends

100% 104% 108%124% 130%

0%

20%

40%

60%

80%

100%

120%

140%

Apr-09 May-09 Jun-09 Jul-09 Aug-09

Spend Share

Bing Launched

28

Apr-09 May-09 Jun-09 Jul-09 Aug-09

100% 101%105%

118% 117%

90%

95%

100%

105%

110%

115%

120%

Apr-09 May-09 Jun-09 Jul-09 Aug-09

Click Share

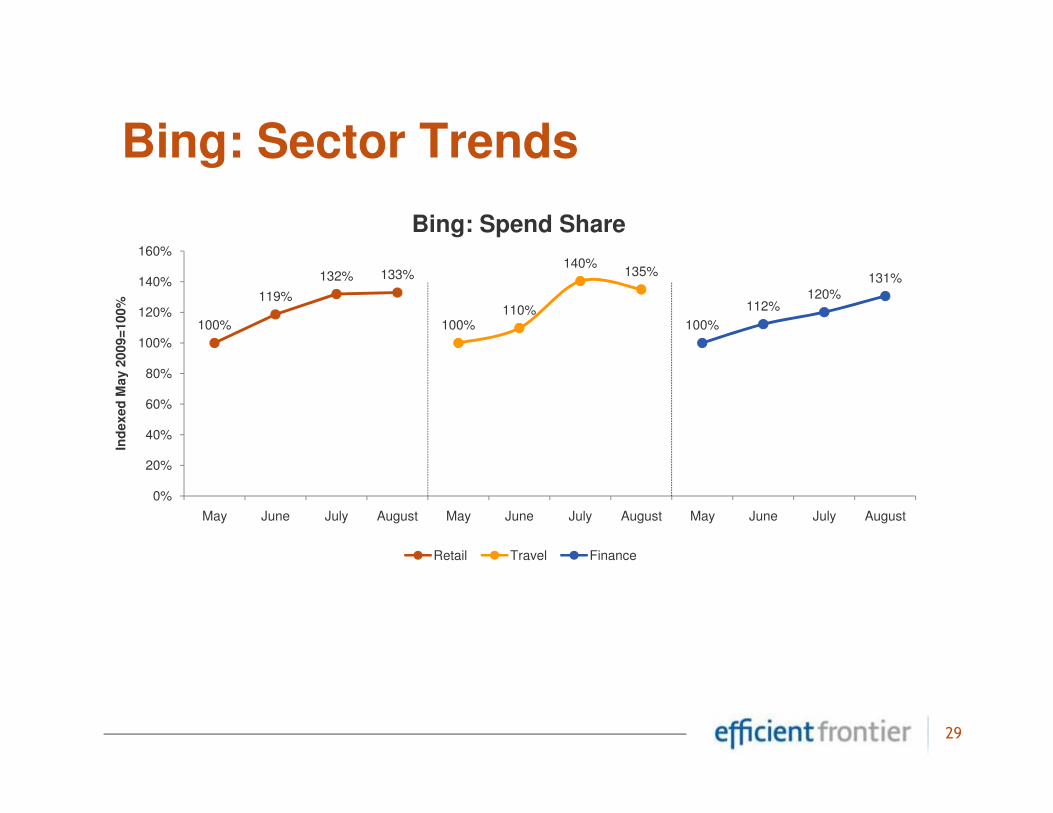

Bing: Sector Trends

100%

119%

132% 133%

100%110%

140%135%

100%

112%120%

131%

60%

80%

100%

120%

140%

160%

Ind

exed

May 2

009=

100%

Bing: Spend Share

29

0%

20%

40%

60%

May June July August May June July August May June July August

Ind

exed

May 2

009=

100%

Retail Travel Finance

US CPC Trends

100%110% 114%

107% 102%96% 100%

90% 87% 89% 91% 94% 97% 94%85%

100% 98% 94% 95% 94%104% 109%

79% 74%82% 83% 85% 85%

79% 79%

40%

80%

0%

40%

80%

120%

Ind

exed

Ju

n 2

008=

100%

30

100% 100%

78%

62% 63%55% 52% 52% 50% 52%

58% 57% 59%67% 63%

100%107% 107% 105%

96% 91% 90% 87%92% 88% 85% 84% 84%

76% 78%

0%

40%

80%

0%

40%

80%

0%

Apr-08 Jun-08 Jul-08 Sep-08 Oct-08 Dec-08 Feb-09 Mar-09 May-09 Jul-09 Aug-09

Ind

exed

Ju

n 2

008=

100%

Finance Travel Automotive Retail

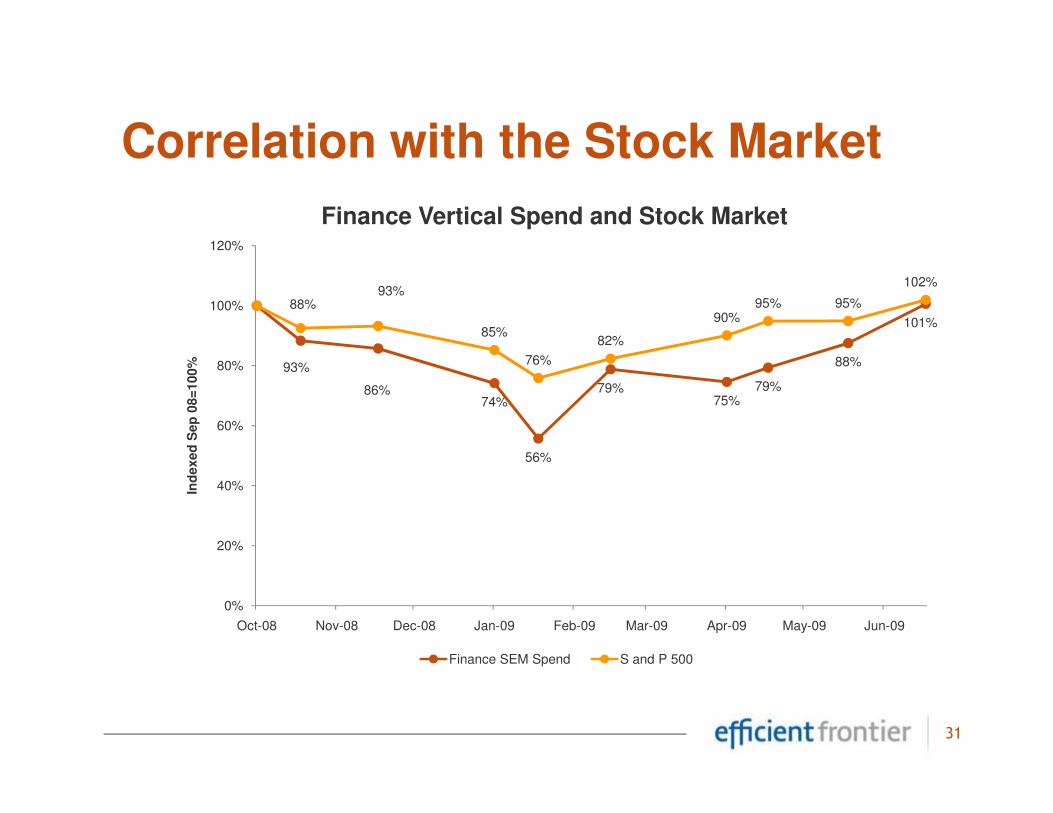

Correlation with the Stock Market

88%

86%74%

79%75%

79%

88%

101%

93%

93%

85%

76%

82%

90%95% 95%

102%

80%

100%

120%

Ind

exed

Sep

08=

100%

Finance Vertical Spend and Stock Market

31

74%

56%

75%

0%

20%

40%

60%

Oct-08 Nov-08 Dec-08 Jan-09 Feb-09 Mar-09 Apr-09 May-09 Jun-09

Ind

exed

Sep

08=

100%

Finance SEM Spend S and P 500

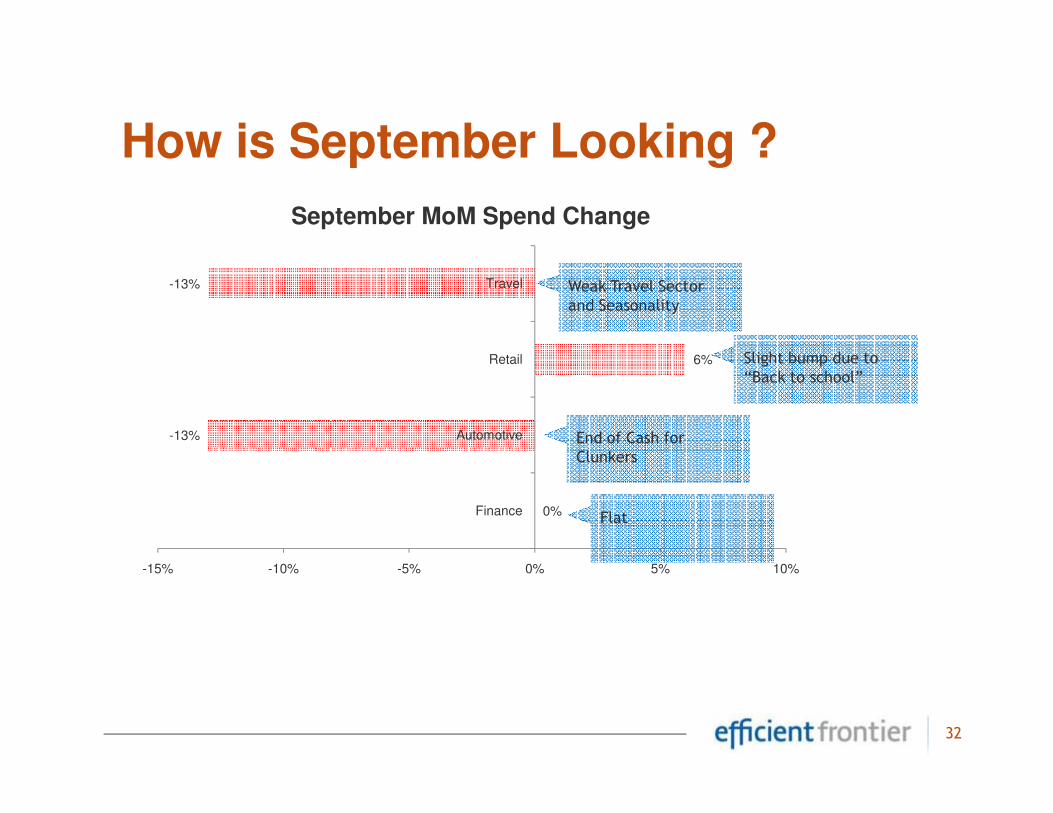

How is September Looking ?

6%

-13%

Retail

Travel

September MoM Spend Change

Weak Travel Sector and Seasonality

Slight bump due to “Back to school”

32

0%

-13%

-15% -10% -5% 0% 5% 10%

Finance

Automotive End of Cash for Clunkers

Flat

What does it mean for the UK?

33

• Bing represents an under levered opportunity for advertisers

• Advertisers will take a harder look at ROI and will increasingly optimize to harder metrics

• Travel will continue to hurt while finance will be closely tied

Takeaways

• Travel will continue to hurt while finance will be closely tied to the state of the financial markets

34

Efficient Frontier Q3 SE Report- published mid October

Join our mailing list!

35

Merinda Peppard

European Marketing Manager

Blog: blog.efrontier.com

Twitter: efrontier