Embed Size (px)

Citation preview

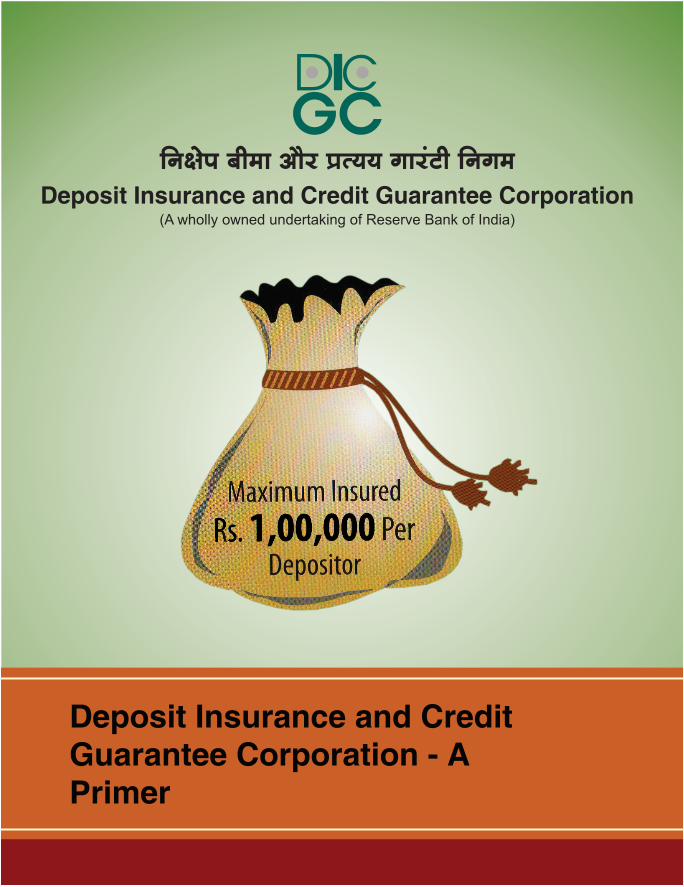

efve#esHe yeercee Deewj Òel³e³e ieejbìer efveieceDeposit Insurance and Credit Guarantee Corporation

(A wholly owned undertaking of Reserve Bank of India)

Deposit Insurance and CreditGuarantee Corporation – A

Primer

March 2017

efve#esHe yeercee Deewj Òel³e³e ieejbìer efveieceDeposit Insurance and Credit Guarantee Corporation

(A wholly owned undertaking of Reserve Bank of India)

efJepeve VISION

SkeÀ me#ece Deewj ÒeYeeJeer efve#esHe yeercee Òeoelee kesÀ ªHe ceW Hen®eeve yeveevee pees HeCeOeejkeÀeW keÀer DeeJeM³ekeÀleeDeeW kesÀ Òeefle mebJesoveMeerue nes ~

To be recognised as one of the most efficient and effective deposit

insurance providers, responsive to the needs of its stakeholders

efceMeve MISSION

ueIeg peceekeÀlee&DeeW keÀe efJeMes<e ªHe mes O³eeve jKeles ngS yeercee kesÀ ceeO³ece mes yeQefkebÀie ÒeCeeueer ceWpevelee keÀe efJeéeeme Deefpe&le keÀjkesÀ efJeÊeer³e efmLejlee ceW men³eesie osvee ~

To contribute to financial stability by securing public confidence in the banking system through provision of deposit insurance,

particularly for the benefit of the small depositors.

Disclaimer

The contents of this primer are for general information and guidance purpose only. The DICGC or Reserve Bank of India will not be liable for actions and / or decisions taken based on this primer. Readers are advised to refer to the specific provisions of the DICGC Act, 1961 and circulars issued by DICGC from time to time. While every effort has been made to ensure that the information set out in this document is accurate, the DICGC does not accept any liability for any action taken, or reliance placed on, any part, or all, of the information in this document or for any error in or omission from, this document.

Preface

The Deposit Insurance and Credit Guarantee Corporation (DICGC) has been in existence since 1961 and has been serving the role of safety net provider for the banks in the country. However, there is very low public awareness about DICGC.

This primer is an attempt to improve public awareness about the institution and processes followed and also the future of DICGC in view of the ensuing Financial Resolution and Deposit Insurance (FRDI) Bill and formation of the Resolution Corporation (RC). The Primer has been written in the form of frequently asked questions to enable user-friendly presentation.DICGC would welcome suggestions to make this primer more user-friendly.

Smt Neti Sara Rajendra Kumar General Manager, DICGC,Reserve Bank of IndiaMarch 15, 2017

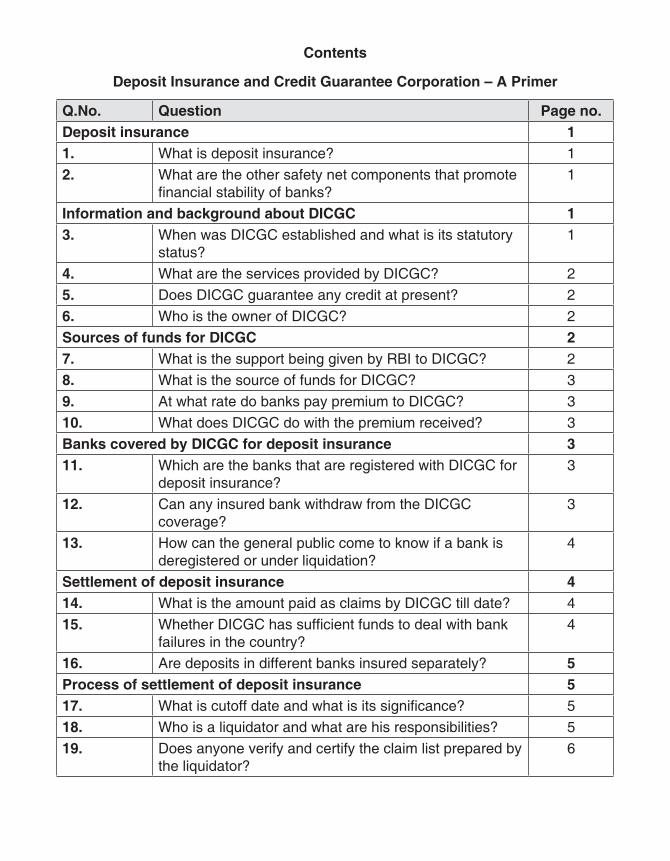

Contents

Deposit Insurance and Credit Guarantee Corporation – A Primer

Q.No. Question Page no.Deposit insurance 11. What is deposit insurance? 12. What are the other safety net components that promote

financial stability of banks?1

Information and background about DICGC 13. When was DICGC established and what is its statutory

status?1

4. What are the services provided by DICGC? 25. Does DICGC guarantee any credit at present? 26. Who is the owner of DICGC? 2Sources of funds for DICGC 27. What is the support being given by RBI to DICGC? 28. What is the source of funds for DICGC? 39. At what rate do banks pay premium to DICGC? 310. What does DICGC do with the premium received? 3Banks covered by DICGC for deposit insurance 311. Which are the banks that are registered with DICGC for

deposit insurance?3

12. Can any insured bank withdraw from the DICGC coverage?

3

13. How can the general public come to know if a bank is deregistered or under liquidation?

4

Settlement of deposit insurance 414. What is the amount paid as claims by DICGC till date? 415. Whether DICGC has sufficient funds to deal with bank

failures in the country?4

16. Are deposits in different banks insured separately? 5Process of settlement of deposit insurance 517. What is cutoff date and what is its significance? 518. Who is a liquidator and what are his responsibilities? 519. Does anyone verify and certify the claim list prepared by

the liquidator?6

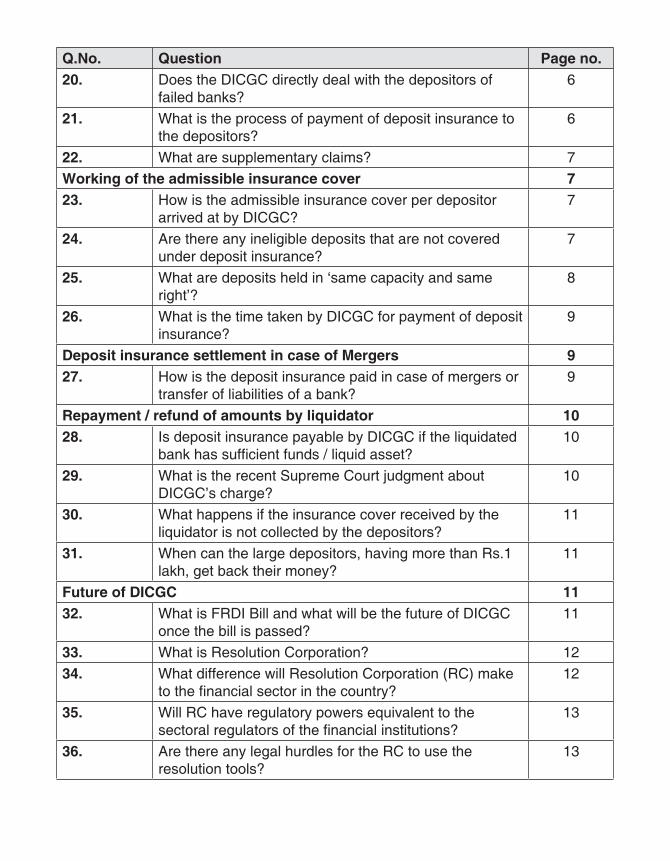

Q.No. Question Page no.20. Does the DICGC directly deal with the depositors of

failed banks?6

21. What is the process of payment of deposit insurance to the depositors?

6

22. What are supplementary claims? 7Working of the admissible insurance cover 723. How is the admissible insurance cover per depositor

arrived at by DICGC?7

24. Are there any ineligible deposits that are not covered under deposit insurance?

7

25. What are deposits held in ‘same capacity and same right’?

8

26. What is the time taken by DICGC for payment of deposit insurance?

9

Deposit insurance settlement in case of Mergers 927. How is the deposit insurance paid in case of mergers or

transfer of liabilities of a bank?9

Repayment / refund of amounts by liquidator 1028. Is deposit insurance payable by DICGC if the liquidated

bank has sufficient funds / liquid asset?10

29. What is the recent Supreme Court judgment about DICGC’s charge?

10

30. What happens if the insurance cover received by the liquidator is not collected by the depositors?

11

31. When can the large depositors, having more than Rs.1 lakh, get back their money?

11

Future of DICGC 1132. What is FRDI Bill and what will be the future of DICGC

once the bill is passed?11

33. What is Resolution Corporation? 1234. What difference will Resolution Corporation (RC) make

to the financial sector in the country?12

35. Will RC have regulatory powers equivalent to the sectoral regulators of the financial institutions?

13

36. Are there any legal hurdles for the RC to use the resolution tools?

13

1

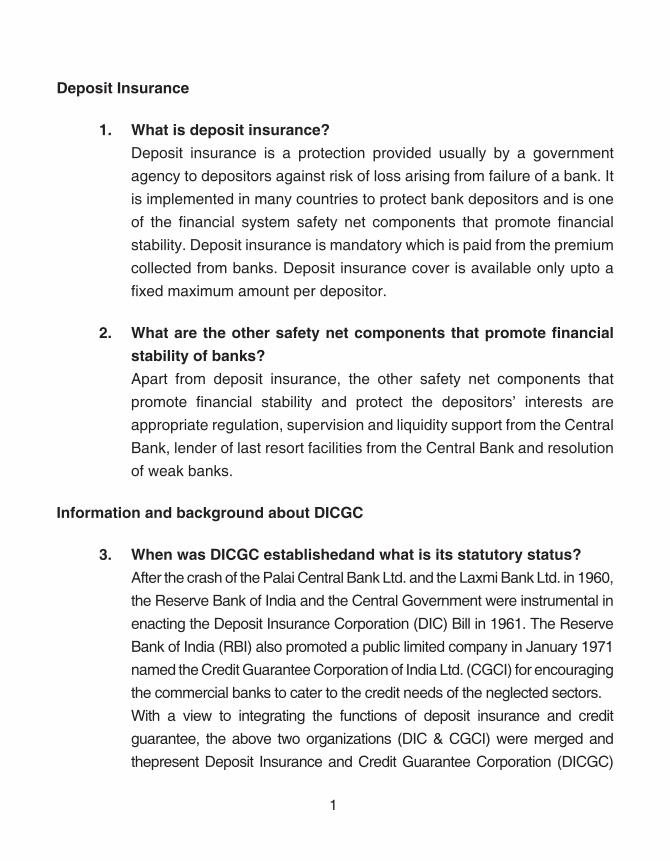

Deposit Insurance

1. What is deposit insurance? Deposit insurance is a protection provided usually by a government

agency to depositors against risk of loss arising from failure of a bank. It is implemented in many countries to protect bank depositors and is one of the financial system safety net components that promote financial stability. Deposit insurance is mandatory which is paid from the premium collected from banks. Deposit insurance cover is available only upto a fixed maximum amount per depositor.

2. Whataretheothersafetynetcomponentsthatpromotefinancialstabilityofbanks?

Apart from deposit insurance, the other safety net components that promote financial stability and protect the depositors’ interests are appropriate regulation, supervision and liquidity support from the Central Bank, lender of last resort facilities from the Central Bank and resolution of weak banks.

InformationandbackgroundaboutDICGC

3. WhenwasDICGCestablishedandwhatisitsstatutorystatus? After the crash of the Palai Central Bank Ltd. and the Laxmi Bank Ltd. in 1960,

the Reserve Bank of India and the Central Government were instrumental in enacting the Deposit Insurance Corporation (DIC) Bill in 1961. The Reserve Bank of India (RBI) also promoted a public limited company in January 1971 named the Credit Guarantee Corporation of India Ltd. (CGCI) for encouraging the commercial banks to cater to the credit needs of the neglected sectors.

With a view to integrating the functions of deposit insurance and credit guarantee, the above two organizations (DIC & CGCI) were merged and thepresent Deposit Insurance and Credit Guarantee Corporation (DICGC)

2

came into existence in July 1978. Consequently, the title of Deposit Insurance Act, 1961 was changed to ‘The Deposit Insurance and Credit Guarantee Corporation Act, 1961’. The DICGC Act applies to the whole of India.

4. WhataretheservicesprovidedbyDICGC? DICGC was established for providing insurance of deposits and

guaranteeing of credit facilities. At present, DICGC insures each depositor of a registered insured bank upto a maximum of Rs.1Lakh for all bank deposits, such as saving, fixed, current, recurring deposits.

5. DoesDICGCguaranteeanycreditatpresent? The credit guarantee scheme of DICGC is presently not operative as

the banks have opted out of the scheme due to availability of alternative guarantee schemes viz. Credit Guarantee Fund Trust for Micro and Small Enterprises (CGTMSE), Credit Guarantee Fund Scheme for Educational Loans (CGSEL), National Credit Guarantee Trustee Company (NCGTC), micro units development refinance agency (MUDRA), etc. The last claim settled under Credit Guarantee was for Rs.0.61 crore which was settled in 2003.

6. WhoistheownerofDICGC? DICGC is a wholly owned undertaking of the RBI. The RBI has invested

Rs.50 crore share capital of DICGC.

SourcesoffundsforDICGC

7. WhatisthesupportbeinggivenbyRBItoDICGC? As DICGC is a wholly owned undertaking of the RBI, it is considered

as one of the Departments of the RBI and staff from RBI is deputed to DICGC on the same pay and perquisites that the employees of RBI are entitled to. Further, DICGC is permitted to draw advances from the RBI

3

from time to time for deposit insurance purposes or credit guarantee purposes. However, DICGC has not availed of this facility till date.

8. WhatisthesourceoffundsforDICGC? The source of funds of DICGC is its capital, premium receipts from the

registered banks and income arising from the investments made by DICGC.

9. AtwhatratedobankspaypremiumtoDICGC? All registered insured banks are liable to pay to the DICGC deposit insurance

premium at the rate of 10 paise per annum for every deposit of Rs.100 (i.e 0.10%p.a) for the half year ending March and September on the total deposits of the bank as on the preceding half year.

10. WhatdoesDICGCdowiththepremiumreceived? As per the provisions of Section 25 of DICGC Act, 1961, the funds that

DICGC does not require for the time being, for settlement of claims, are invested in Central Government securities and deposits with the RBI. DICGC has a Treasury which takes care of the investments and liquidity requirements.

BankscoveredbyDICGCfordepositinsurance

11. Which are the banks that are registeredwithDICGC for depositinsurance?

Deposit insurance is compulsory for all banks in the country. Therefore, all public sector banks, private sector banks, local area banks, regional rural banks, small finance banks, payments banks, branches of foreign banks functioning in India, all State, Central and Primary cooperative banks (Urban Cooperative Banks) are registered and insured by the DICGC. Presently, there are around 2,100 odd banks registered with DICGC.

4

12. CananyinsuredbankwithdrawfromtheDICGCcoverage? The deposit insurance scheme is compulsory and all banks need to get

registered with the DICGC and no bank can withdraw from the scheme. However, banks could be de-registered by DICGC on account of default in payment of premium for three consecutive periods. However, there is no such instance of de-registration on this account till date.

13. Howcanthegeneralpubliccometoknowifabankisderegisteredorunderliquidation?

The information on de-registered banks is available in the DICGC’s website, www.dicgc.org.in under For depositors > List of de-registered banks. Thede-registration could happen on account of cancellation of banking license or on account of the bank being migrated to a different type of bank. For Ex:- from Local Area bank to Small Finance Bank.

Settlementofdepositinsurance

14. WhatistheamountpaidasclaimsbyDICGCtilldate? As on March 31, 2016, the total amount of claims paid by DICGC since

inception were at Rs.50 billion.

15. WhetherDICGChassufficientfundstodealwithbankfailuresinthe country?

As on March 31, 2016, the insured deposits of all the banks in the country stood at Rs.28,264 billion and the amount in the deposit insurance fund (DIF) stood at Rs.603 billion yielding a Reserve Ratio (RR) (ratio of Deposit Insurance Fund to Insured Deposits) of 2.13 % which is comparable to the global scenario. The funds in DIF are more than 10 times of the claims paid till now by DICGC since its inception in 1961. DICGC also conducts periodic actuarial valuation of its liabilities, to ascertain if this fund is sufficient. It also has a backstop arrangement to borrow from the

5

RBI in a cash crunch. Further, going by the claims settled in the past, the funds available with DICGC are sufficient to handle normal rate of bank failures.

16. Aredepositsindifferentbanksinsuredseparately? Deposits of different banks are insured separately. The insurance cover

of Rs.1 lakh per depositor in the same right same capacity is for each bank separately. Therefore, even if two banks are closed / deregistered / cancelled on the same date, the same depositor will be eligible for a maximum insurance cover of Rs.1 lakh each in each bank.

Processofsettlementofdepositinsurance

17. Whatiscutoffdateandwhatisitssignificance The date of deregistration of a bank as an insured bank is the cutoff date

which is also the date of liquidation / cancellation of bank’s license or the date on which the scheme of amalgamation / merger / reconstruction comes into force. The claim amount (including interest) payable to each depositor, after set-off of loans and advances and clubbing of deposits, in the ‘same capacity and same right’, is arrived at, depositor-wise, as on the cutoff date.

18. Whoisaliquidatorandwhatarehisresponsibilities? On receipt of an order for liquidation of a bank or a scheme of

amalgamation/reconstruction for a bank approved by the Reserve Bank of India, the liquidator is appointed by the Registrar of Co-operative Societies of the respective State in case of Cooperative banks and Reserve Bank of India in case of commercial banks. On appointment of the liquidator, the DICGC sends detailed guidelines for compilation of the claim list and copies of the audited balance sheet, profit and loss accounts of the bank as on the date of cancellation of registration /

6

amalgamation /reconstruction, etc of the bank are called for, to verify the authenticity of the total deposits as given in the claim list. The liquidator is required to furnish the main claim list in the form and manner prescribed in the guidelines within 3 months from the date of his appointment. He is required to ensure that only eligible deposits are aggregated for each depositor in the ‘same capacity and same right’ and clubbed together after setting-off dues payable to the bank by the depositor. Further, only eligible insured depositors who are complying with the Know Your Customer (KYC)norms are required to be included in the Main Claim list in accordance with the Guidelines issued by DICGC.

19. Does anyone verify and certify the claim list prepared by theliquidator?

For certifying the main claim list prepared by the liquidator, a Chartered Accountant (CA) is appointed by the RBI who is required to check the deposits of the balance sheet, interest calculation and claim list for clubbing, set-off, KYC, etc and furnish a certificate with Annexures on admissible and inadmissible claims. Only after receipt of the certificate from the CA, the main claim is taken up for processing by DICGC.

20. DoestheDICGCdirectlydealwiththedepositorsoffailedbanks? In the event of a bank’s liquidation, the liquidator prepares depositor-wise

claim list and submits it to the DICGC for scrutiny and payment. The DICGC pays the money to the liquidator who is liable to pay to the depositors. In the case of amalgamation / merger of banks, the amount due to each depositor is paid to the transferee bank. Therefore, DICGC does not deal directly with the depositors. However, depositors are free to contact DICGC, in case of any grievance regarding deposit insurance of upto Rs.1 lakh.

7

21. What is the process of payment of deposit insurance to the depositors?

On scrutiny of the main Claim list submitted by the Liquidator and certificate furnished by the CA, admissible claim amount is arrived at by the DICGC and the admissible amount is sanctioned and disbursed to the liquidator or the liquidator is advised to settle the claim through adjustment through liquid funds available with the bank. On advice from DICGC, the liquidator pays the admissible amount to the depositors.

22. Whataresupplementaryclaims? During processing of main claims, DICGC may reject some claims due to

inadequate KYC verification by liquidator / CA, club certain claims which appear to be belonging to a same depositor, withhold some claims for want of additional information such as name of the firm, etc. Further, there are some claims that are parked as untraceable depositors which are called part B claims and certain claims refunded by the liquidator as undisbursed amounts. In respect of all the above and also in respect of additional claims which may have been missed during submission of main claim, the liquidator could submit supplementary claims with supporting documents as mentioned in the guidelines to the liquidators which are primarily KYC documents, legal heir certificate, etc.

Workingoftheadmissibleinsurancecover

23. HowistheadmissibleinsurancecoverperdepositorarrivedatbyDICGC?

When a bank goes into liquidation, the DICGC is liable to pay to each depositor through the liquidator, the admissible amount upto a maximum amount of Rs.1 lakh after exercising proper set-off of dues in respect of loans, advances and guarantees due to the bank and clubbing of deposits of the depositor in the ‘same capacity and same right’. The

8

net amount arrived, limited to the insurance cover of Rs.1 lakh, is the admissible amount due to the depositor from the DICGC.

24. Arethereanyineligibledepositsthatarenotcoveredunderdepositinsurance?

The DICGC insures all deposits such as savings, fixed, current, recurring, etc. and interest thereon, except deposits of foreign Governments, deposits of Central/State Governments, Inter-bank deposits, deposits of the State Land Development Banks with the State co-operative bank, any amount due on account of and deposit received outside India, amounts credited to the Depositor Education and Awareness Fund (DEAF) established by the Reserve Bank of India and any amount, which has been specifically exempted by the corporation with the previous approval of Reserve Bank of India. Further, deposits of any entity/individual banned as per the updated list by the UN Security Council (http://www.un.org/en/sc),deposits in respect of any of the terrorist organizations whose names have been notified under the Prevention of Terrorism Act, 2002 and deposits in respect of any of the 29 entities whose names are notified by the office of the custodian the Special Court, Department of Economic Affairs, Ministry of finance, Government of India in the Gazette of India Extra Ordinary Part III 4 -No.28 dated 17th June 1997, 273 dated 8th October 2001 and 302 dated 20th November 2001, will not be covered under the deposit insurance.

25. Whataredepositsheldin‘samecapacityandsameright’? If an individual has more than one deposit account in one or more branches

of a bank in his personal name, all these deposits are considered as accounts held in the ‘same capacity and in the same right’. Therefore, the balances in all these accounts are aggregated and set-off against the amounts due to the bank then the net amount is arrived at which is payable to the depositor upto a maximum of Rs.1 lakh. Further, the

9

deposits held in the name of a proprietary concern where a depositor is the sole proprietor and the amount of Deposit held in his individual capacity are aggregated to arrive at the admissible amount limited to the insurance cover of Rs.1 lakh.

However, if a depositor also opens other deposit accounts in his capacity as a partner of a firm or guardian of a minor or director of a company or trustee of a trust or a joint account with another person, say his wife, then such accounts are considered as held in different capacity and different right. Accordingly, such deposits accounts will also enjoy the insurance cover upto Rs.1 lakh under each capacity and right.

26. WhatisthetimetakenbyDICGCforpaymentofdepositinsurance? The liquidator is required to submit the main claim list to DICGC in the

form and manner prescribed and DICGC is required to dispose the claim within 2 months from the date of receipt of the main claim list, and also after examining the CA certificate received on the main claim. DICGC either settles the claim or further clarifications are called for, relating to reconciliation or other discrepancies observed in the main claim list.

DepositinsurancesettlementincaseofMergers

27. Howisthedepositinsurancepaidincaseofmergersortransferofliabilitiesofabank?

The scheme of transfer is required to be approved by the regulator and will provide for the proportion of deposits of the transferor bank (merging bank), which will be taken over by the transferee bank (taking over bank). The deposit coverage ratio is arrived at, out of the ‘’readily realizable assets’’ of the transferor bank (merging bank) and from its own initial contribution. The deposit coverage ratio will depend on RBI’s / Chartered Accountant’s assessment of the financial position of the transferor bank (merging bank) based on the strength of the financials of

10

the transferor bank (merging bank). The ratio arrived at till now in case there is an assistance required by DICGC, has been that the liability of not less than 65 per cent of the deposits will be borne by the transferee bank (taking over bank) and the liability of not more than 35 per cent of the deposits will be borne by the DICGC. The claim list in these cases is prepared by the transferee bank (taking over bank) and all the assets and liabilities are normally absorbed by the bank. However, the merger cases were approved in the past based on an earlier circular issued by the regulatory departments. As of now, the relevant circular to address merger cases forthe present banks is yet to be issued by the regulatory departments.

Repayment/refundofamountsbyliquidator

28. IsdepositinsurancepayablebyDICGCiftheliquidatedbankhassufficientfunds/liquidassets?

As per the provisions of Section 21 of DICGC Act, 1961, the amount paid as deposit insurance is repayable by the liquidator. At the time of furnishing the main claim list and at quarterly intervals, the liquidator is required to furnish the ‘Liquid fund statement’ of the liquidated bank which indicates the liquid funds available with the liquidator, recoveries made during the half year and the estimated expenses for the next six months. As the deposit insurance paid by DICGC is repayable by the liquidator and to prevent mis-utilization of liquid funds available with the liquidator, DICGC tries to disburse the insurance cover / total admissible amount only to the extent of over and above the liquid funds available with the liquidator. The remaining amount that is adjusted from liquid funds towards insurance cover / total admissible amount is treated as payment made and repayment received by the DICGC.

11

29. WhatistherecentSupremeCourtjudgmentaboutDICGC’scharge? The Hon’ble Supreme Court in the case of DICGC v RagupathiRagavan(Civil

Appeal No. 1035 of 2008 & connected appeals) had vide its judgment dated July 1, 2015 settled the question of law on the priority of the claim of DICGC and held that there shall not be any other preferential creditor who would be getting any amount from the Liquidator till the amount repayableis paid to DICGC.

30. Whathappensiftheinsurancecoverreceivedbytheliquidatorisnotcollectedbythedepositors?

The admissible claim amount which has been settled by DICGC but not collected by the depositors is called the undisbursed amount. As indicated in DICGC circular dated April 27, 2012, this undisbursed amount should be refunded to DICGC without fail within 15 days after four months from the date of settlement of claim by DICGC. The amount should be refunded along with the list of the depositors and claim numbers against which the amount pertains. The refund of undisbursed amount to DICGC is required to ensure that the interests of the small depositors are protected and the amount is not utilized by the liquidator towards expenses or payment to large depositors. As and when the small depositors raise a claim with the liquidator, the same is settled by DICGC from the undisbursed amount refunded by the liquidator.

31. Whencan the largedepositors,havingmore thanRs.1 lakh,getbacktheirmoney?

The deposit insurance cover offered by DICGC is uptoRs. 1 lakh. The amount released by DICGC towards insurance cover and the undisbursed amount lying with the liquidator is required to be repaid / refunded to DICGC. Further, sufficient provision is required to be made for the untraceable depositors. Once the interests of small depositor’s is taken care, the liquidator could pay to the large depositors from the

12

recoveries made from the assets of the bank subject to approvals from his Registrar of Cooperative Societies.

FutureofDICGC

32. WhatisFRDIBillandwhatwillbethefutureofDICGConcethebillis passed?

The Union Finance Minister, in his Budget Speech 2016-17, announced that a comprehensive ‘Code on Resolution of Financial Firms’ will be introduced as a Financial Resolution and Deposit Insurance (FRDI) Bill in the Parliament during 2016-17. The Code will provide a specialized resolution mechanism to deal with bankruptcy situations in banks, insurance companies and other financial sector entities apart from dealing with deposit insurance for banks.

On passing of the FRDI Bill, Resolution Corporation (RC) will be established and DICGC will be subsumed in the RC. Deposit insurance for banks will continue to be handled by RC as presently done by DICGC.

33. WhatisResolutionCorporation? At present, DICGC performs the ‘pay box’ function in terms of settlement

of claims up to Rs.1 lakh to the depositors of failed banks. It also provides financial support to the depositors of a bank in case of compromise arrangement or reconstruction or amalgamation. However, DICGC does not have the resolution powers under the existing legal framework. In this backdrop, various committees constituted by the Reserve Bank of India and Government of India in the past recommended an enhanced role for DICGC from being a mere ‘pay box’ entity to ‘pay box plus’ entity with resolution powers.

In this backdrop, the formation of Resolution Corporation in the country is envisaged for resolving the financial institutions

a) without causing severe systemic disruption,

13

b) without exposing taxpayers to loss, c) while protecting vital economic functions, d) make it possible for shareholders and unsecured and uninsured

creditors to absorb losses in a manner that respects the hierarchy of claims in liquidation.

34. What difference will Resolution Corporation (RC) make to thefinancialsectorinthecountry?

A greater role is envisaged for the proposed RC vis-a-vis DICGC in terms of application of various resolution tools for orderly resolution of entities under its purview in contrast to the ‘pay box’ function i.e., reimbursement of insured amount to the depositors of failed banks currently handled by DICGC.The proposed RC intends to cover all the financial sector entities viz., banks, insurance companies, non-bank finance companies, holding companies, systemically important financial institutions (SIFIs) and any other entity which may be notified by the Central Government for the purpose of resolution, while confining the deposit insurance only to banks. The RC would help the country on resolution of financial firms by addressing all the gaps in the current resolution mechanism in India in terms of legal framework, resolution tools, liquidation, coverage of entities, cross border cooperation, oversight framework etc. To resolve weak financial entities, RC would use resolution tools such as, transfer or acquire assets and liabilities, create a temporary bridge institution (till suitable buyer is found), bail-in (shareholders and creditorsbear the loss of failure), liquidate, merge or amalgamate, etc.

35. WillRChaveregulatorypowersequivalenttothesectoralregulatorsofthefinancialinstitutions?

In case of weak financial institutions, some of the regulatory powers now being exercised by the respective financial sector regulator will be vested with the RC. With such powers, the RC will be in a position to use the

14

resolutions tools for resolving the financial entity to merge, amalgamate, transfer of assets and liabilities, create a bridge institution, bail-in the creditors and shareholders to share the loss relating to failure of the institution, liquidate,etc which were hitherto used by the regulators.

36. ArethereanylegalhurdlesfortheRCtousetheresolutiontools? As Primary cooperative banks (Urban Cooperative Banks) are governed

by the respective State Cooperative Acts or The Multi-State Cooperative Act, certain amendments to the existing Acts would be required to enable the RC to exercise some of the regulatory powers instead of the powers presently being

exercised by the Registrar of Cooperative Societies of the States (RCS) or Central Registrar of Cooperative Societies (CRCS). For the purpose, a two year transition for amendments to the Acts is envisaged to enable the RC to acquire the regulatory powers over the cooperative banks and start resolving the weak cooperative banks. During the transition, the RBI, in consultation with RCS and the CRCS, would continue to exercise their powers to resolve the cooperative banks. However, the Deposit insurance for banks, including cooperative banks, will be handled by RC.