Embed Size (px)

Citation preview

EL CIVICS BANKING

CASAS Civic Objective #1

Identify, evaluate, and compare financial service options in the community such as banks, credit unions, checkcashing

services and credit cards.

STUDENT’S WORKBOOK

NOCCCD SCE/ESL Program

1830 W. Romneya Drive Anaheim, CA 92801

By: Janet Cagley

Harinder Kahlon

FALL 2007

SECTION 1: BANKING – EL CIVICS OBJECTIVE #1

BANKING BASICS

5

BANKING TERMS:

Let’s get familiar with the world of banking

6

Vocabulary Words and Definitions – You will see the following words throughout the objective. Use the lines after each word to rewrite the definitions in your own words; then share with the class.

Balance The amount of money in an account, equal to the net of credits and debits at that point in time for that account. also called account balance. _________________________________________________________________

_________________________________________________________________

Bills – Paper money _________________________________________________________________

_________________________________________________________________

Borrow – To receive money on loan with the understanding that it will be repaid, usually with interest. _________________________________________________________________

_________________________________________________________________

Cash Currency and coins on hand _________________________________________________________________

_________________________________________________________________

Change – Coins such as pennies, nickels, dimes, quarters, or halfdollars _________________________________________________________________

_________________________________________________________________

Check A negotiable instrument drawn against deposited funds, to pay a specified amount of money to a specific person upon demand _________________________________________________________________

_________________________________________________________________

Checking Account An account which allows the holder to write checks against deposited funds _________________________________________________________________

_________________________________________________________________

Check Register An informal record of all deposits to and withdrawals from a given checking account. A checkbook register is used to perform bank reconciliation _________________________________________________________________

_________________________________________________________________

Coins – Pennies, nickels, dimes, quarters, halfdollars, or silver dollars _________________________________________________________________

_________________________________________________________________ 7

Deposit Money transferred into a customer's account at a financial institution. _________________________________________________________________

_________________________________________________________________

Deposit Slip A written notification accompanying a bank deposit, which specifies and categorizes the funds (such as checks, bills and coins) being deposited. _________________________________________________________________

_________________________________________________________________

Endorse/ Endorsement A signature used to legally transfer a negotiable instrument, such

as check

_________________________________________________________________

_________________________________________________________________

Interest The return earned on an investment. _________________________________________________________________

_________________________________________________________________

Joint Account Any account owned by two or more people _________________________________________________________________

_________________________________________________________________

Money Order Financial instrument, issued by a bank or other institution, allowing the

individual named on the order to receive a specified amount of cash on demand. Often used

by people who do not have checking accounts.

_________________________________________________________________

_________________________________________________________________

Monthly statement A report sent by a bank to each of its customers, providing details on

the previous month's transactions, dividends and interest, and the current account balance.

_________________________________________________________________

_________________________________________________________________

Overdraft The amount by which withdrawals exceed deposits, or the extension of credit by a lending institution to allow for such a situation. _________________________________________________________________

_________________________________________________________________

8

Personalized Check – A check that is preprinted with your personal information _________________________________________________________________

_________________________________________________________________

Savings Account A deposit account at a bank or savings and loan which pays interest, but cannot be withdrawn by check writing. _________________________________________________________________

_________________________________________________________________

Savings bond A registered, noncallable, nontransferable bond issued by the U.S. Government, and backed by its full faith and credit. _________________________________________________________________

_________________________________________________________________

Service Charge A fee charged for services rendered. _________________________________________________________________

_________________________________________________________________

Traveler’s check Check issued by a financial institution which functions as cash but is protected against loss or theft. _________________________________________________________________

_________________________________________________________________

Withdraw A removal of funds from an account.

_________________________________________________________________

_________________________________________________________________

Withdrawal Slip A written notification accompanying a bank withdrawal which specifies the amount being withdrawn. _________________________________________________________________

_________________________________________________________________

9

Introduction to Banking

In the past, when people wanted to save their money, they sometimes put it in a box and hid it under the bed or put it in a book. They thought the money was safe and nobody could find it. But times have changed, and now people have a better and safer place to keep their money. Now, many people take their money to a bank or a credit union. Keeping money in a bank or credit union is not only safe but also more convenient.

Discuss with your classmates:

1. Do you have a Bank account in the U.S.?

2. Did you have a Bank account in your country?

3. Do you remember the name of the Bank in your country?

4. Can you name a Bank in your neighborhood?

10

What is a Financial Institution? There are three types of financial institutions: Banks, Credit Unions, and Savings Institutions.

Bank A financial institution that is controlled by federal and state laws and regulations. Banks make loans, pay checks, accept deposits, and provide other financial services. Most banks are insured by the Federal Deposit Insurance Corporation or (FDIC). The FDIC insures a person’s money up to $100,000.

Credit Union A nonprofit financial institution owned by people who have something in common, for example, working in the same industry. You have to become a member of a credit union to keep your money there. Most credit unions are insured but the National Credit Union Administration (NCUA).

Savings Institution A savings bank or savings and loan association is similar to a bank. These companies were created to promote homeownership and must have a majority of their assets in housingrelated loans. Although many banks also make home loans, a savings institution’s main business is to make home loans.

11

What are some reasons people use banks and credit unions? • Banks and credit unions offer services to help you save and manage your

money. o A Savings Account is an account where you can deposit your

money and it will be safe. The bank pays you money, called Interest, when you save your money in one of their accounts.

o A Checking Account is an account where you can deposit your money when you will need to spend it soon. You can pay your bills with checks. The bank or credit union will take money from your account when they receive your check from a business or company.

o An Automated Teller Machine (ATM) lets you deposit or withdraw money from your savings or checking account at any time.

o An ATM/Debit Card is used to deposit or withdraw money from an ATM. It can also be used to pay at many stores or restaurants. § A PIN is necessary to use most ATM/Debit Cards. § A PIN is a Personal Identification Number. It is a special code

that identifies you as the owner of the card or account. o Loans are amounts of money that are provided by the bank or credit

union. This money is paid back over a period of time with interest. o Money Orders and Traveler’s Checks are

provided by banks and credit unions for a small fee or in some cases, for free, if you have an account.

o CheckCashing is provided as a free service if you have an account at a bank or credit union. Checkcashing businesses may charge 10% of the check or more.

12

Banking Services.

What can a Bank do for you?

Most banks offer these services to their customers or members. What services does your bank or credit union offer?

Checking Accounts Passbook Loans Savings Accounts Home Equity Loans Retirement Plans. Home Improvement Loans Money Market Accounts Home Mortgages. Term Deposit Accounts Construction Loans Direct Deposits. Bank online. Safe Deposit Account Notary Public Services New Car Loans Payroll Services Student Help Loans Travelers Checks All Purpose Loans 24 Hour Banking VISA Card Statements

13

Who will help me when I go to the bank?

Customer Service

Representative

Teller Loan Officer Store Manager

Helps you open your accounts

Accepts money for deposits

Reviews applications for loans

Makes sure that you get the help you need from the bank staff.

Explains services Cashes checks Answers questions about loans

Answers general questions

Answers questions

Provides written information explaining loan products

Provides written information explaining the bank’s products and services

Refers you to other people at the bank who can help you

Helps you fill out a loan application

Introduces you to others at the bank who can help you

What questions should I ask the customer service representative when I open an account? • Is there a minimum balance to open an account? • Am I required to keep a minimum balance in my account after I open it? • Are there any monthly service charges for my account? • How much will it cost to order personalized checks? • Is there a service charge each time I write a check? • What fees will I be charged if my checking account becomes overdrawn? • How much interest will my savings account earn? • Is my savings account connected to my checking account?

14

Choosing the Right Bank. There are many different banks. Not all are the same. They may differ in the services that they offer, or the interest that they pay. Look for some of these things when choosing a bank:

Choose a bank that pays a higher interest. Choose a bank that charges less for services. Choose a bank that is open on Saturdays. Choose a bank that is near your home or your job.

After you have compared and chosen a bank, you need to go inside and open an account. Here are some things that are important to know before you open an account.

Choosing A Checking Account A checking account is the most common type of banking account. Typical examples include:

The Minimum Balance Account The Regular Account The Special Account The Free Account.

Minimum Balance Account

Do you write a lot of checks? YES/NO

Do you have some extra money? YES/NO

If you answered YES to the above questions, then the minimum balance account may be good for you, but you need to remember to keep a certain amount of money in the account. This money is called the minimum balance. If you don’t have that certain amount in your account at all times, then your bank may charge you a fee.

Regular Checking Account

If you are unable to keep a minimum balance in your account then the regular checking account may be for you. It charges a monthly service fee, and the less money you have in the account, the more the service fee.

Special Checking Account

If you can’t keep a minimum balance in your account and you write a lot of checks, this may be the account for you. You can keep as much or as little money as you like in your special checking account, but each time you write a check you will have to pay a service charge.

Free Checking Account

With free checking you can keep any balance in your account, and write an unlimited number of checks

15

BL to Advanced:

A. Today is a busy day at the World Savings Bank. Look at the picture carefully and choose True or False.

1. There are two bank tellers working now. True / False. 2. Lea is putting her jewelry in the safedeposit box. True / False. 3. Al is in the bank to deposit money into his account. True / False. 4. Ann is the drivethru teller. True / False. 5. Marie is a bank officer. True / False. 6. Ali is a bank customer. True / False. 7. The 5 year CD rate is 1.2% today. True / False.

B. Look at the picture and fill in the blanks

1. Al is filling out a __________. 2. To take money out of the bank is called_________________________. 3. I can keep track of all my money by writing _____________________. 4. The 10 year CD rate is ____________ today. 5. You can withdraw cash from the _______ which is just outside the front door.

16

IL to Advanced

Directions: Use the picture and statements from the previous page to write one or two paragraphs describing some of the events and activities that are taking place in the World Savings Bank.

______________________________________________________________________

______________________________________________________________________

______________________________________________________________________

______________________________________________________________________

______________________________________________________________________

______________________________________________________________________

______________________________________________________________________

______________________________________________________________________

______________________________________________________________________

______________________________________________________________________

______________________________________________________________________

______________________________________________________________________

______________________________________________________________________

______________________________________________________________________

______________________________________________________________________

______________________________________________________________________

______________________________________________________________________

______________________________________________________________________

______________________________________________________________________ 17

Types of Accounts and Services

Directions: choose the kind of account and services that might be appropriate for you – in groups or as a class, discuss their advantages and disadvantages.

Checking Account – You put your money in this kind of account because you will need to spend it soon; for example, to pay your bills with checks or to withdraw cash for everyday spending. The bank will take the money from your account when they receive your check from whom you wrote it to.

Savings Account – In this kind of account you put money that you are not going to need right away, and you want to save it for later. The bank pays you interest for keeping it in one of their accounts.

Loans – Banks and credit unions can loan you money. You can pay back the loan a little at a time. They charge you interest for the loan.

ATM (Automated Teller Machine) – An ATM can be used for 4 things; withdraw money, deposit money, transfer money, or to check your balance. ATM’s are open 24 hours a day. You need a special card and a personal identification number from your bank to use the ATM.

Money Orders and Traveler’s Checks – Money orders and Traveler’s checks can be used when you do not want to use cash or regular checks. They may be free if you have an account with the bank.

Check Cashing – A paycheck or any other check can be cashed. This service is free at your bank or credit union. Other check cashing businesses may charge you a high fee, sometimes as high as 10% of your check.

A Safe Deposit Box – It is a long, metal box that is kept safely in the bank’s vault. You can put your important papers, jewelry, and other valuable items in the box, so they cannot be misplaced, stolen, or damaged in a fire or an earthquake.

18

Directions: Now that you are familiar with many banking terms, you can complete the exercise by writing the letter of the definition on the blank next to the correct word.

1. Balance _______

2. Bills _______

3. Borrow _______

4. Cash _______

5. Change _______

6. Check _______

7. Checking Account ______

8. Check Register _______

9. Coins _______

10. Deposit _______

11. Deposit Slip _______

12. Endorse/

Endorsement _______

13. Interest _______

14. Joint Account _______

15. Money Order _______

16. Monthly statement ______

17. Overdraft _______

18. Personalized

Check _______

19. Savings Account _______

20. Savings bond _______

21. Service Charge _______

22. Traveler’s check _______

23. Withdraw _______

24. Withdrawal Slip _______

A. A. A report providing details on the previous month's transactions.

B. Paper money C. Coins such as pennies, nickels, dimes, quarters, or

halfdollars D. A negotiable instrument drawn against deposited

funds, to pay a specified amount of money to a specific person upon demand

E. Currency and coins on hand F. The amount of money in an account, equal to the net

of credits and debits at that point in time for that account. Also called account balance.

G. An account which allows the holder to write checks against deposited funds

H. An informal record of all deposits to and withdrawals from a given checking account.

I. To receive money on loan with the understanding that it will be repaid, usually with interest.

J. A written notification accompanying a bank deposit, K. A signature used to legally transfer a negotiable

instrument, such as check L. Pennies, nickels, dimes, quarters, halfdollars M. The return earned on an investment. N. A deposit account at a bank or savings and loan

which pays interest, but cannot be withdrawn by check writing

O. Money transferred into a customer's account P. Any account owned by two or more people Q. The amount by which withdrawals exceed deposits R. A removal of funds from an account. S. A check that is preprinted with your personal

information T. A registered, noncallable, nontransferable bond

issued by the U.S. Government, and backed by its full faith and credit.

U. A written notification accompanying a bank withdrawal, which specifies the amount being withdrawn.

V. Check issued by a financial institution which functions as cash but is protected against loss or theft.

W. Often used by people who don’t have checking accounts.

X. A fee charged for services rendered

19

21

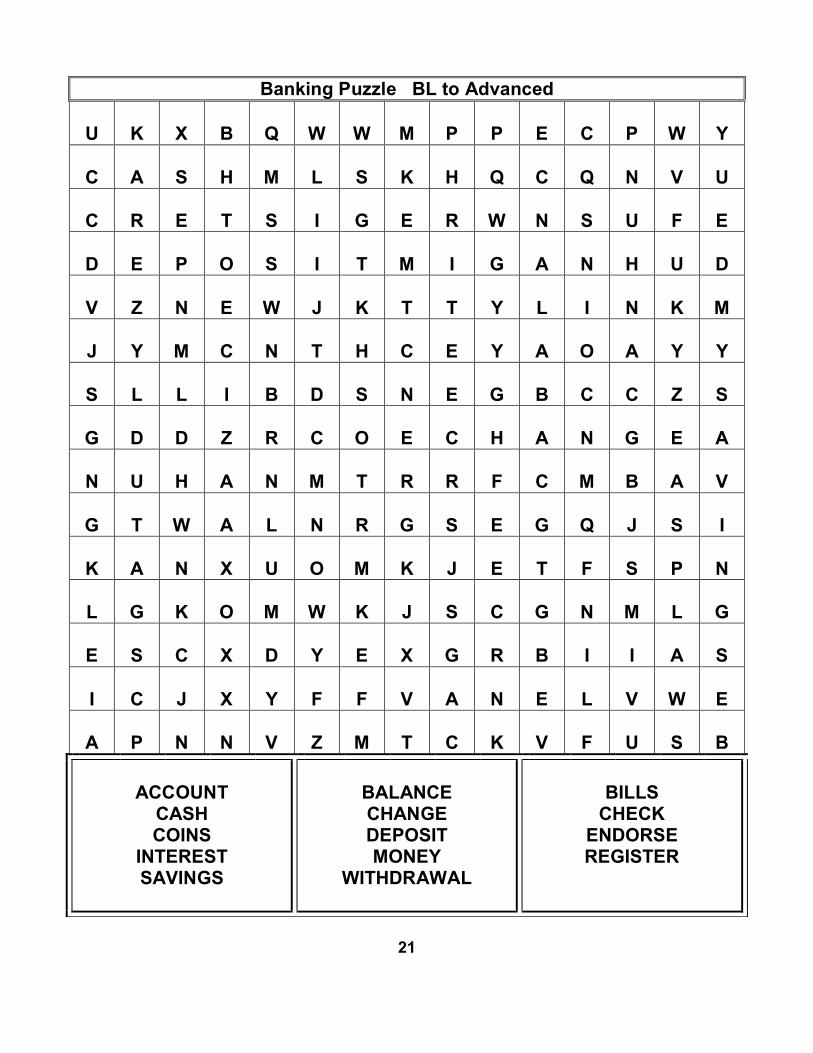

Banking Puzzle BL to Advanced

U K X B Q W W M P P E C P W Y

C A S H M L S K H Q C Q N V U

C R E T S I G E R W N S U F E

D E P O S I T M I G A N H U D

V Z N E W J K T T Y L I N K M

J Y M C N T H C E Y A O A Y Y

S L L I B D S N E G B C C Z S

G D D Z R C O E C H A N G E A

N U H A N M T R R F C M B A V

G T W A L N R G S E G Q J S I

K A N X U O M K J E T F S P N

L G K O M W K J S C G N M L G

E S C X D Y E X G R B I I A S

I C J X Y F F V A N E L V W E

A P N N V Z M T C K V F U S B

ACCOUNT CASH COINS

INTEREST SAVINGS

BALANCE CHANGE DEPOSIT MONEY

WITHDRAWAL

BILLS CHECK

ENDORSE REGISTER

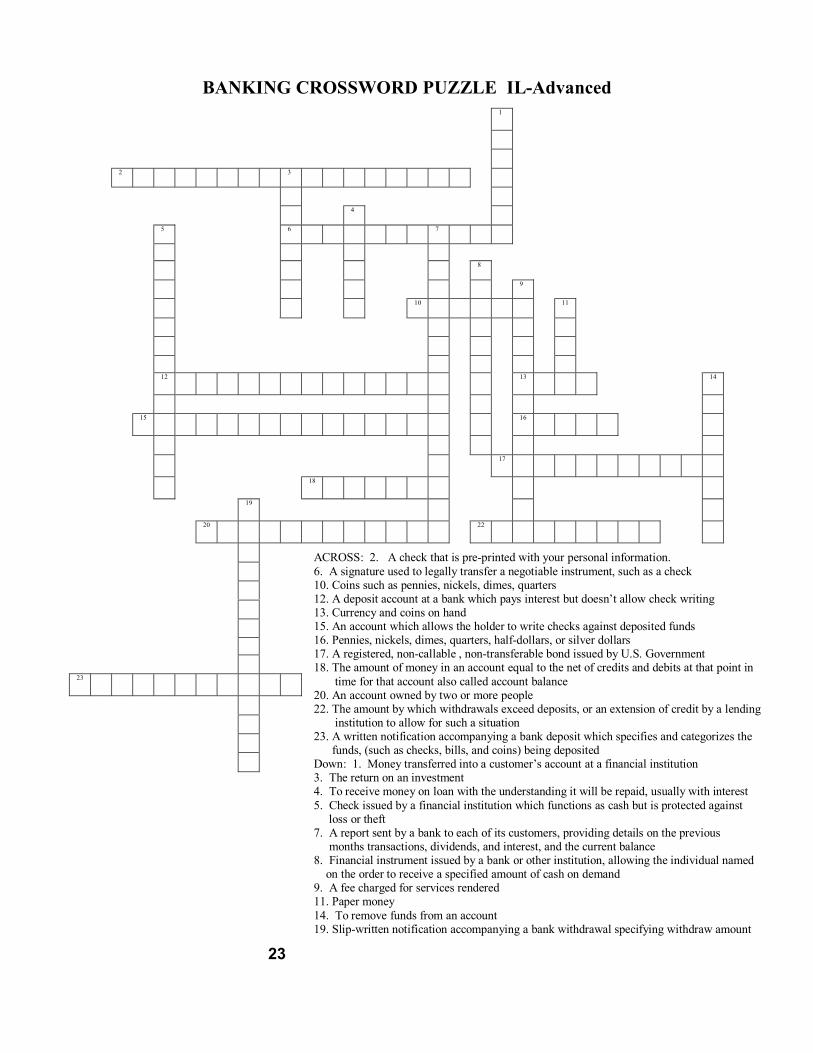

BANKING CROSSWORD PUZZLE ILAdvanced

23

1

2 3

4

5 6 7

8

9

10 11

12 13 14

15 16

17

18

19

20 22

23

ACROSS: 2. A check that is preprinted with your personal information. 6. A signature used to legally transfer a negotiable instrument, such as a check 10. Coins such as pennies, nickels, dimes, quarters 12. A deposit account at a bank which pays interest but doesn’t allow check writing 13. Currency and coins on hand 15. An account which allows the holder to write checks against deposited funds 16. Pennies, nickels, dimes, quarters, halfdollars, or silver dollars 17. A registered, noncallable , nontransferable bond issued by U.S. Government 18. The amount of money in an account equal to the net of credits and debits at that point in

time for that account also called account balance 20. An account owned by two or more people 22. The amount by which withdrawals exceed deposits, or an extension of credit by a lending

institution to allow for such a situation 23. A written notification accompanying a bank deposit which specifies and categorizes the

funds, (such as checks, bills, and coins) being deposited Down: 1. Money transferred into a customer’s account at a financial institution 3. The return on an investment 4. To receive money on loan with the understanding it will be repaid, usually with interest 5. Check issued by a financial institution which functions as cash but is protected against

loss or theft 7. A report sent by a bank to each of its customers, providing details on the previous

months transactions, dividends, and interest, and the current balance 8. Financial instrument issued by a bank or other institution, allowing the individual named on the order to receive a specified amount of cash on demand

9. A fee charged for services rendered 11. Paper money 14. To remove funds from an account 19. Slipwritten notification accompanying a bank withdrawal specifying withdraw amount

25

Across IL to ADVANCED 1 A bank account you use to pay everyday expenses.

4 A bank employee.

5 Income before you pay taxes.

7 Take money out of the bank.

8 Borrowed money that you pay back at a regular interval.

10 Every month. 11 Put money in the bank.

12 Money borrowed on a credit card. (11)

15 An interest rate that changes with time.

17 Money that you borrow. 18 A bank's main interest rate. 19 Not pay a loan. 21 A bank account you use to

save money. 24 Money you pay to do

something. 25 Guarantee a loan for

somebody else. 28 The opposite of lend. 30 A monthly fee on borrowed

money.

31 What you have if you borrow money.

Down 1 The maximum you can borrow on your credit card.

2 Keep your money __ the bank.

3 A house loan.

4 Go __ the bank. 6 The opposite of save. 9 A cash machine. 12 VISA or MasterCard.

13 You are your own boss. 14 Yearly. 16 Work __ a bank. 20 Move money between bank

accounts. 22 Money that you earn.

23 Money that you withdrew from your account.

24 An interest rate that stays the same.

26 Your monthly wage.

27 Another word for money. 29 Income after you pay taxes.

BANKING BINGO Directions: Write one word in each square. Match each letter and word your teacher reads, or calls out. Cross off each letter and word pair until you have a complete line, horizontally, vertically, or diagonally.

B I N G O

FREE

27

Balance Bills Borrow Cash Change

Check Checking Account Coins Check Register Deposit Slip

Endorse Interest Joint Account Money Order Monthly statement

Overdraft Personalized Check Savings Account Savings Bond Service Charge

Traveler’s check Withdraw Withdrawal slip Deposit

SECTION 2A:

BANK APPLICATIONS, IDENTIFYING REQUIREMENT FOR OPENING AN ACCOUNT

LANGUAGE AND LITERACY OBJECTIVES #7

ADDITIONAL ASSESSMENT PLAN TASK #1

BEGINNING LOW TO BEGINNING HIGH

28

OPENING AN ACCOUNT (BLBH)

Any customer service representative at your bank or credit union can help you open a checking or savings account. You will need to decide whether you want to open a checking account, a savings account, or both.

Discussion Questions

BLBH: Do you have a checking account or a savings account? Are they joint accounts?

IA: What type of account is the best choice for you? Why?

When you open an account, you will need to fill out an application and provide personal information. You will need to provide your Social Security Number, address, phone number, date of birth, and occupation. You may have to provide additional information depending on which bank you choose.

You will need to decide whether or not you will open a Joint Account. A joint account is used by more than one person. For example, you and your husband or wife, can both write checks or make withdrawals from a joint account.

You will also need to decide whether or not you will name a beneficiary for your account. A beneficiary is the person who will receive the money in your account if you die.

You may also have to give your mother’s maiden name. This is your mother’s last name before she married. This fact is used for security purposes since it is a detail very few people would know about you.

29

Filling out an application to open a checking account, savings account or certificate of deposit.

PreWriting Fill in the blanks with your information.

First Name________________ Middle Initial_______ Last Name_________________

Street Address_______________________________ Apartment Number__________

City__________________________ State_________ Zip Code____________

Social Security Number_________________ Date of Birth (MM/DD/YY)____________

Email Address__________________________________________________

Home Telephone__________________ Work Telephone__________________

Occupation_______________________

Is this joint account? If yes, fill in the following information for the other person using the account. First Name_______________ Middle Initial_______ Last Name_________________

Street Address_______________________________ Apartment Number__________

City__________________________ State_________ Zip Code____________

Social Security Number_________________ Date of Birth (MM/DD/YY)___________

Email Address__________________________________________________

Home Telephone__________________ Work Telephone__________________

Occupation_______________________

30

Writing – Use the information on the previous page to fill out the sample account application below.

Application for Personal Checking Account Savings Account or Certificate of Deposit

To open one of the above accounts at Pacific Trust Bank, complete the following application. Please print or type your responses. All account applications are subject to approval.

For A Personal Checking Account What type of Checking Account do you wish to open? ____ Super Checking (interestbearing NOW account) ____ HighYield Checking (tiered rates, unlimited checks) ____ Basic Checking (totally free) ____ Money Market Checking (limited to 3 checks per month)

For A Personal Savings Account ____ Regular Savings ____ Christmas Club (not currently available) ____ Market Rate Account (tiered MMDA account) Money Market Deposit Account ____ Indexed Money Market Account

For Certificate of Deposit What type of Certificate of Deposit do you wish to open? ___3 month CD ___12 month CD ___18 month CD ___36 month CD

___6 month CD ___13 month CD ___21 month CD ___42 month CD

___7 month CD ___Flex 15 month CD ___24 month CD ___48 month CD

___9 month CD ___15 month CD ___30 month CD ___60 month CD

___Money Indexed AddOn 12month CD ___Savings Accumulation 36month CD

___Peace of Mind CD 36month adjustablerate

Will this be an individual or joint account? ___Individual ___Joint

Are you presently a customer of Pacific Trust Bank? ___Yes ___No Will there be a beneficiary on the account? ___Yes ___No

31

Account Ownership Information

Primary Applicant Information Name (First/ MI/ Last) ___________________________________________________

Social Security Number___________________________________________________

Date of Birth (Month/ Day/ Year)___________________________________________

Mother’s Maiden Name___________________________________________________

Primary Applicant Home Address:

Street_________________________________________________________________

City/Town__________________________ State___________ Zip Code___________

Mailing Address (if different)_______________________________________________

Home Telephone______________________ Work Telephone___________________

Email Address________________________ Occupation________________________

Joint Applicant Information (Complete only if joint account) Name (First/ MI/ Last)___________________________________________________

Social Security Number___________________________________________________

Date of Birth (Month/ Day/ Year)____________________________________________

Mother’s Maiden Name___________________________________________________

Primary Applicant Home Address:

Street_________________________________________________________________

City/Town__________________________ State___________ Zip Code___________

Mailing Address (if different)______________________________________________

Home Telephone______________________ Work Telephone___________________

Email Address________________________ Occupation________________________

Beneficiary (Complete only if there is a beneficiary) Name (First/ MI/ Last)___________________________________________________

Address_______________________________________________________________

Relationship____________________________________________________________

Date of Birth (Month/ Day/ Year)____________________________________________

Social Security Number __________________________________________________

Initial Deposit Information Initial Deposit (see account terms for minimum required initial deposit): $____________ If you are making your initial deposit via check, please make the check payable to Pacific Trust Bank for the account of “your name”. 32

Disclosures Government regulations require that we make the following disclosures available to you when you apply for an account with Pacific Trust Bank. You may print these disclosures for your records, if you wish. Links to these disclosures are available at http://www.pacifictrustbank.com/Handbook.html

Acknowledgements/ Certifications By my signature below, I acknowledge and certify the following:

• Each signatory authorizes the Bank to obtain consumer reports from any

consumer reporting agency, including but not limited to a check protection

service for use in connection with this account.

• I(we) certify that (1) that the number shown on this card is my, (our) correct

taxpayer identification number and (2) that I (we) are not subject to backup

withholding, either because I, (we) have not been notified of backup withholding

as a result of failure to report all interest or dividends, or the Internal Revenue

Service has notified me, (us), that I, (we), are no longer subject to backup

withholding. (Instruction to signer: If you have been notified by the IRS that you

are subject to backup withholding due to notified payee underreporting and you

have not been notified that the backup withholding is terminated you should

strike out the language in clause 2 above.)

• The Internal Revenue Service does not require your consent to any provision of

this document other than the certifications required to avoid back up withholding

I, (we) severally, agree to be bound by present or future bylaws, regulations or procedures of Pacific Trust Bank that are or may not become applicable to the Account.

Primary Applicant Signature _____________________________ Date_________

Joint Applicant Signature________________________________ Date_________

33

Web Quest Opening A Bank Account (All Levels)

Directions: Many banks will allow you to open an account online. You can practice opening a bank account in computer lab, a library, at home, or anywhere that access to the internet is available. Follow the directions to practice opening an account with Washington Mutual. (Note: This exercise is for practice only. You will not actually submit your information to the bank.)

1. Double click on the web browser icon on the computer desktop.

2. Type in the address: www.wamu.com

3. In the center of the page you will see the words “Open Online Now”

4. Click on the words “WaMu Free Checking”

5. Look for the words Special ONLINE ONLY offer available when you open a

WaMu Free Checking account & Online Savings together online! And click on the

blue words in the sentence. This will allow you to open a savings account and a

checking account at the same time.

6. Read the account information.

7. Select “No” to answer the question “Do you have an online ID?”

8. Click “Continue”

9. Enter your personal information including Name, Date of Birth, Mother’s Maiden

Name, Social Security Number, ID information, Email, Phone and Address. This is an

individual account application so you will not need to provide information for anyone

else.

10.Click “Continue”

11.Make sure your information is correct and read the disclosure information.

12.Click “Continue”

13.Choose the option “Make your deposit later” “Bring it in/ Mail it in”

14. DO NOT click “Continue” because you are not actually opening an account. 34

Review

BL – A Mark the following questions True or False:

1. Only one person can write checks on a joint checking account. True or False

2. Your mother’s maiden name is her last name after she got married. True or False

3. You are required to name a beneficiary for your bank accounts. True or False

4. Most banks will let you open your new account online. True or False

5. You can choose the type of account that is best for you. True or False

Fill in the Blank

ILA Choose the best word to complete each sentence.

1. Many applications will ask for your mother’s ____________ name.

2. I can open an account ________________.

3. When I open an account I will be asked for my ___________________.

4. I should write my name when the application asks for a _______________.

5. MI stands for _____________________.

6. My occupation is my _______________.

7. More that one person can use a ____________________.

8. I can name a ___________ to receive the money in my account if I die.

35

Word Bank

beneficiary middle initial social security number maiden

signature online job joint account

Discussion Questions: IL – Advanced

Answer each question with a complete sentence:

1. Who would you name as a beneficiary for your account? Why?

2. Why would the bank ask for your mother’s maiden name?

3. Would you open a joint account? Why or why not?

4. Why should you write your signature in handwriting instead of print?

36

Banking Conversation: Opening an Account (ALL Levels)

Bank Employee: A Customer: B

A: Welcome to Wells Fargo (BLUE). Can I help you?

B: I’d like to open an account.

A: What type of account do you want?

B: I would like a checking (RED) account.

A: Are there any special features you would like?

B: Yes, I would like an ATM / Check Card (GREEN) with my account.

A: Okay, how much of an initial deposit can you make today?

B: How about $50 (PURPLE)?

A: That’s fine. Let’s sit down over here and fillout the application.

B: Okay, thank you.

(BLUE) Institutions

(RED) Account Types

(GREEN) Special Features

(PURPLE) Initial Deposit

1. Wells Fargo 2. Bank of America 3. Washington Mutual 4. Banco Popular 5. CitiBank 6. Cathay Bank

1. Checking only 2. Savings only 3. Checking & Savings 4. Joint Checking 5. Interest Checking 6. Custodial Savings

1. ATM / Check Card 2. International Transfer 3. Free Online Banking 4. Online Access 5. No Monthly Fees 6. Overdraft Protection

1. $1 2. $5 3. $50 4. $100 5. $1,000 6. $10,000

Roll the four different colored dice to indicate which of the six variables you will use in the conversation.

Conversation springboards: More advanced students may want to ask the customer why he or she wants certain features. This will lead to conversations beyond the scripted dialogue.

38

SECTION 2B:

BANK APPLICATIONS, IDENTIFYING REQUIREMENT FOR OPENING AN ACCOUNT

LANGUAGE AND LITERACY OBJECTIVES #15

ADDITIONAL ASSESSMENT PLAN TASK #1

INTERMEDIATE LOW TO ADVANCED

42

Loans

Most people cannot afford to buy large items, such as a house or a new car, with cash. In this situation, you can apply for a loan with your bank or credit union.

To get a loan, you must fill out an application and the bank or credit union will do a

credit evaluation or credit check to determine if you are a good credit risk. A credit

evaluation determines your income to debt ratio, or how much you owe versus how

much you earn. It’s better to owe very little. A credit evaluation also checks to see if

you make your loan payments on time, if you have ever defaulted on a loan or if you

have ever declared bankruptcy. If you default on a loan, this means that you did not keep your promise to pay back the money you borrowed. Bankruptcy is a legal

declaration that you are unable to pay your debts. If your credit evaluation shows that

you do not owe a lot of money to other people, that you have made payments for past

loans on time, and you have not declared bankruptcy in the past, you are considered to

be a good credit risk. If the bank determines you are a good credit risk, you may be eligible for a home loan also referred to as a mortgage.

43

Loans

If your credit evaluation shows that you are a bad credit risk, you may

not be able to get a loan or you may have to pay a higher interest rate.

The percentage of the total amount borrowed as a fee for using the money is an interest

rate. If you are a bad credit risk, you may have to get someone to cosign on your

loan. A cosigner is a person other than the borrower who signs the loan agreement

and promises to pay back the loan if you do not.

Other words you should know before you apply for a loan are:

• Debt – money owed that must be repaid.

• Creditor – a person or business that loans money to others. If you apply for a

loan with your bank or credit union, the financial institution is the creditor.

• Debtor – person who owes money

• Late fee – an extra charge if you do not make your payments on time.

What questions should I ask the loan officer before I agree to a loan?

• Will the bank add any fees to the amount I am borrowing?

• What is my interest rate?

• Is the interest rate fixed or variable? A fixed interest rate does not change after I

receive my loan. Interest rates on variable loans can change.

• What are my monthly payments?

• Will my interest rate increase if I make any late payments?

• Am I required to make a down payment? A down payment is the amount the

borrower is required to pay at the closing of the loan. The down payment

reduces the total amount you will need to pay back. If you are buying a house,

the down payment is often 20% of the house’s total value.

• Do I have to provide collateral? Collateral is an asset that you agree to give up

if you default on your loan. This is sometimes called a secured loan. 44

$ $ $ $ $ $

Loans

What information will I be asked to provide when I apply for a loan?

• In addition to the personal information you provided when you opened a checking

or savings account, you will be asked for more detailed financial information.

o Name

o Address

o Birth date

o Phone number

o Driver’s license number

o Social security number

o Number of dependents (a dependent is someone who depends on

you for financial support, such as your children)

o Do you own or rent your home? How long have you lived there?

o The name and address of your employer

o The amount of money you make each month

o Your current assets and debts

o Information on your current debts including creditor and amount

owed.

When you have the information listed above, you are ready to practice applying for a loan.

Fill in the following sample loan information. You do not have to use your real personal information if you don’t want to.

45

Pacific Trust Bank

Loan Application

TYPE OF CREDIT REQUESTED: (Check the appropriate loan)

___ Secured ___ Individual Credit (relying solely on my income or assets)

___ Unsecured

TYPE OF LOAN BEING APPLIED FOR: ___ Savings/ CD Secured ___ Personal Line of Credit

___ Term Unsecured Loan ___ Automobile Loan

___ RV/ Boat Loan INTEREST RATE PREFERRED:

___ Fixed Rate ___ Variable Rate AMOUNT REQUESTED: $____________ FOR HOW LONG? ___________ YEARS PAYMENT DATE DESIRED: __________ THIS LOAN WILL BE USED FOR: _____________

Section A – Individual Applicant Information

Name (Last, First, Middle) ________________________________________________ Birth Date _________ Telephone Number _______________________________ SSN ___________ Driver’s License No. ______________________________ Number of Dependents _________________ Ages of Dependents ______________

Address (Street, City, State, Zip Code):

______________________________________________________________________ County ______________ Do you ___ Own or ___ Rent? How Long? ______ Previous Address (Street, City, State, Zip Code): Complete if less that three years at your current address.

______________________________________________________________________ County ______________ Did you ___ Own or ___ Rent? How Long? ______ Employer: (company name and address) __________________________________ ________________________________________ How Long? ________________

Business Phone ____________ ext. ______ Position or Title __________________ Salary Per Month – Gross $ _____________

46

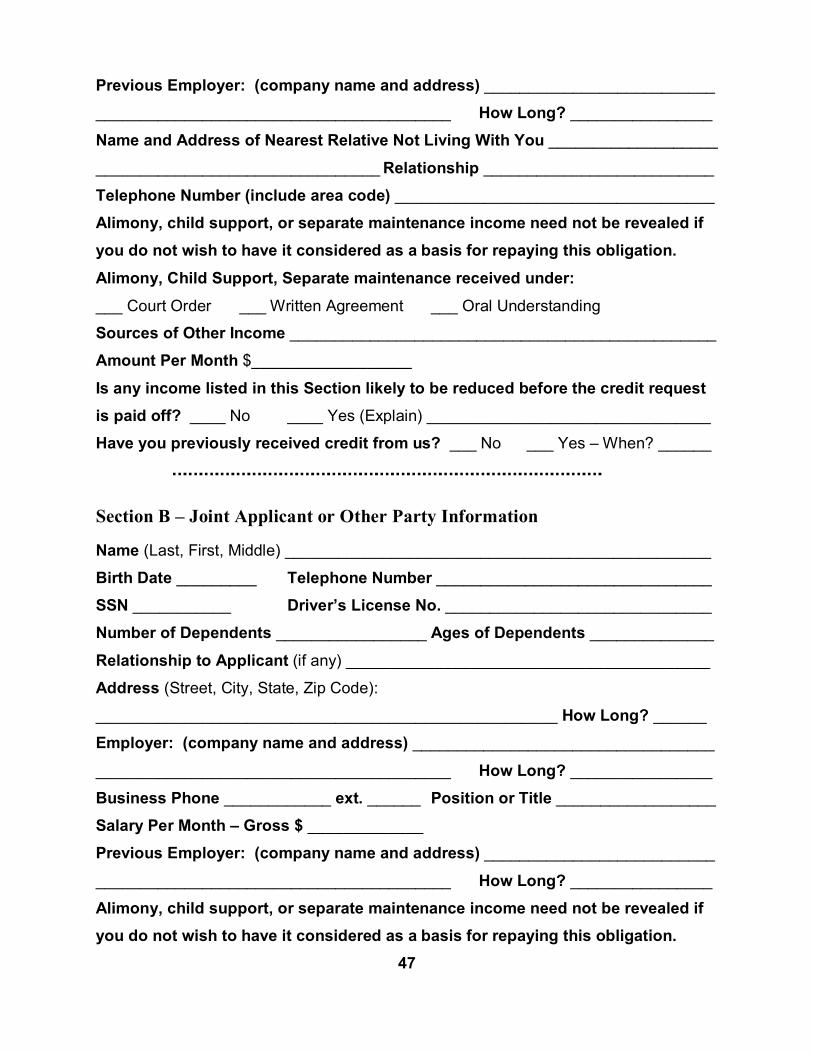

Previous Employer: (company name and address) __________________________ ________________________________________ How Long? ________________ Name and Address of Nearest Relative Not Living With You ___________________

________________________________Relationship __________________________ Telephone Number (include area code) ____________________________________ Alimony, child support, or separate maintenance income need not be revealed if you do not wish to have it considered as a basis for repaying this obligation.

Alimony, Child Support, Separate maintenance received under:

___ Court Order ___ Written Agreement ___ Oral Understanding Sources of Other Income ________________________________________________ Amount Per Month $__________________

Is any income listed in this Section likely to be reduced before the credit request is paid off? ____ No ____ Yes (Explain) ________________________________ Have you previously received credit from us? ___ No ___ Yes – When? ______

Section B – Joint Applicant or Other Party Information

Name (Last, First, Middle) ________________________________________________ Birth Date _________ Telephone Number _______________________________ SSN ___________ Driver’s License No. ______________________________ Number of Dependents _________________ Ages of Dependents ______________

Relationship to Applicant (if any) _________________________________________ Address (Street, City, State, Zip Code): ____________________________________________________ How Long? ______ Employer: (company name and address) __________________________________

________________________________________ How Long? ________________ Business Phone ____________ ext. ______ Position or Title __________________ Salary Per Month – Gross $ _____________ Previous Employer: (company name and address) __________________________

________________________________________ How Long? ________________ Alimony, child support, or separate maintenance income need not be revealed if you do not wish to have it considered as a basis for repaying this obligation.

47

Alimony, Child Support, Separate maintenance received under:

___ Court Order ___ Written Agreement ___ Oral Understanding Sources of Other Income ________________________________________________

Amount Per Month $__________________ Is any income listed in this Section likely to be reduced before the credit request is paid off? ____ No ____ Yes (Explain) ________________________________ Has joint applicant or other party ever received credit from us?

___ No ___ Yes – When? ______

Section C – Marital Status

Complete only if: for joint or secured credit, or applicant resides in a community property state

or is relying on property located in such a state as a basis for repayment of the credit requested.

Applicant ___ Married ___ Legally Separated ___ Unmarried (including single, divorced and widowed

Other Party ___ Married ___ Legally Separated ___ Unmarried (including single, divorced and widowed

Section D – Asset & Debt Information If Section B has been completed, this Section should be completed about both the Applicant and Joint Applicant or Other Person. Please mark Applicantrelated information with an “A”. If Section B was not completed, only give information about the Applicant in this Section. Assets Owned (use separate sheet if necessary) Description of Assets Name in which the account is

carried Subject to debt? Value

Checking Account Number(s) (where)

$

Savings Account Number(s) (where) Certificate of Deposit(s) (where) Marketable Securities (issuer, type, no. of shares) Real Estate (location, date acquired) Life Insurance (issuer, face value) Automobiles (make, model, year) Other (list) 48

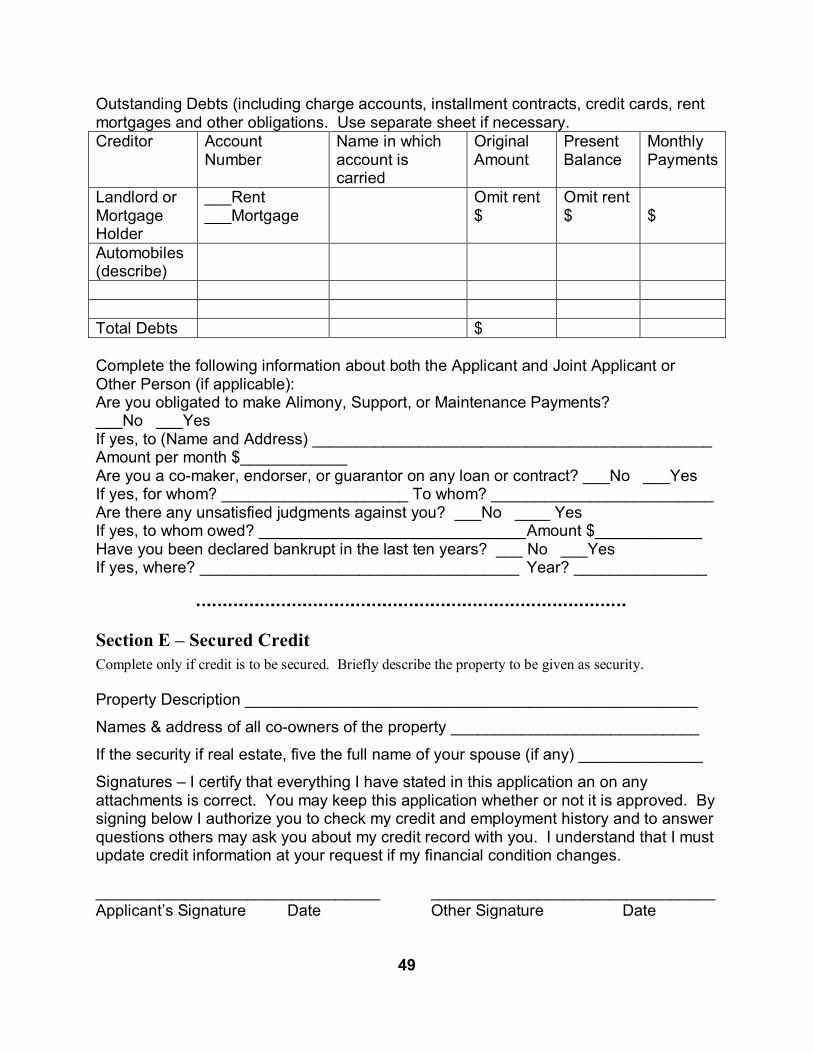

Outstanding Debts (including charge accounts, installment contracts, credit cards, rent mortgages and other obligations. Use separate sheet if necessary. Creditor Account

Number Name in which account is carried

Original Amount

Present Balance

Monthly Payments

Landlord or Mortgage Holder

___Rent ___Mortgage

Omit rent $

Omit rent $ $

Automobiles (describe)

Total Debts $

Complete the following information about both the Applicant and Joint Applicant or Other Person (if applicable): Are you obligated to make Alimony, Support, or Maintenance Payments? ___No ___Yes If yes, to (Name and Address) _____________________________________________ Amount per month $____________ Are you a comaker, endorser, or guarantor on any loan or contract? ___No ___Yes If yes, for whom? _____________________ To whom? _________________________ Are there any unsatisfied judgments against you? ___No ____ Yes If yes, to whom owed? ______________________________Amount $____________ Have you been declared bankrupt in the last ten years? ___ No ___Yes If yes, where? ____________________________________ Year? _______________

Section E – Secured Credit Complete only if credit is to be secured. Briefly describe the property to be given as security.

Property Description ___________________________________________________

Names & address of all coowners of the property ____________________________

If the security if real estate, five the full name of your spouse (if any) ______________

Signatures – I certify that everything I have stated in this application an on any attachments is correct. You may keep this application whether or not it is approved. By signing below I authorize you to check my credit and employment history and to answer questions others may ask you about my credit record with you. I understand that I must update credit information at your request if my financial condition changes.

________________________________ ________________________________ Applicant’s Signature Date Other Signature Date

49

Review

Directions: IL to Advanced Fill in the blank with the correct word from the word bank.

1. A ______ is money owed that must be repaid.

2. A ___________ is a person or business that loans money to others.

3. A person who owes money is a ____________.

4. An extra charge if you do not make your payments on time is a __________.

5. A house loan is called a_____________.

6. A ____________ determines your income to debt ratio.

7. If you _________ on a loan, this means that you did not keep your promise to pay

back the money you borrowed.

8. _______________ is a legal declaration that you are unable to pay your debts.

9. If your credit evaluation shows that you do not owe a lot of money to other people

then you are considered to be a __________________.

10. If your credit evaluation shows that you are a_______________, you may not be

able to get a loan.

11.The percentage of the total amount borrowed as a fee for using the money is an

________.

12.A _____________ is a person other than the borrower who signs the loan

agreement and promises to pay back the loan if you do not.

50

Word Bank

Credit Evaluation Bad Credit Risk Debt Debtor Late fee

Cosigner Default Mortgage Good Credit Risk Creditor

Bankruptcy Interest Rate

Review

IL to Advanced Answer the Questions:

1. What are three questions that you should ask the loan officer before agreeing to a loan?

2. What information will you probably be asked to provide on a loan application?

True or False

1. A house loan is called a mortgage. True False

2. Most people can afford to buy a home or car with cash. True False

3. If you default on a loan, you made all your payments on time. True False

4. When you apply for a loan, the bank will do a credit evaluation. True False

5. If you are a good credit risk, you will probably have to pay a high interest rate. True False

51

SECTION 3: READ AND FILL OUT A PERSONAL CHECK, A CHECK REGISTER AND/OR DEPOSIT AND WITHDRAWAL

SLIPS

LANGUAGE AND LITERACY OBJECTIVE #11

ADDITIONAL ASSESSMENT PLAN TASK #2 & #3

LEVEL: BLADVANCED

57

REVIEW CHECKING ACCOUNTS

BLAdvanced Levels

Directions: review the “Choosing a Checking Account” information on page 15. Read the following questions and circle the best answer.

1. A Minimum Balance Account is for you if

a. you write only 5 checks each month. b. you write a lot of checks. c. you don’t write any checks.

2. If you don’t keep the required minimum balance in your Minimum Balance Account, you

a. may have to transfer money. b. may have to open a new account. c. will be charged a fee.

3. A Regular Checking Account is good if you

a. can keep a minimum balance in your account. b. can’t keep a minimum balance in your account. c. have a lot of extra cash.

4. The service charge on a Regular Checking Account is based on

a. how much money you have in your account. b. your minimum balance. c. how many checks you write. .

59

REVIEW CHECKING ACCOUNTS

BLAdvanced Levels

Directions: review the “Choosing a Checking Account” information on page 15, then select the best word to fill in each blank.

Free Minimum Balance Special Regular

1. With a ______________ Checking Account, you pay a service charge each time you write a check.

2. A ______________ Checking Account allows you to keep any balance in your account and write an unlimited number of checks

3. A ______________ Checking Account is for people who can’t keep a minimum balance in their account.

4. _______________ Checking Account may be for you if you write a lot of checks and have some extra money.

61

Checks Checks are sometimes more convenient than cash. They are often used to pay bills because it is never a good idea to send cash in the mail.

Look at the sample check below to identify the parts of a check.

Date ______

Pay to the order of _____________________________________________ $ _________________

______________________________________________________________________________ Dollars

Bank’s Name Address City, State Zip Code

For ____________________ ______________________________________

012345678 00000281609 001001

1. Your personal information: Name

Address

City, State Zip Code

You can include your phone number if you want

2. The number of the check (1001, 1002, 1003, 1004, etc.) The number is also

printed on the last line.

3. Your banks information: Name

Address

City, State Zip Code

4. Your bank’s routing number. This number identifies the bank.

5. Your bank account number.

6. The check number (same as #2.)

63

Your Name Your Address City, State Zip Code

1001 1.

2.

3.

4. 5.

6.

Writing Checks

What to write Example 1. Write the date

August 6, 2007 or 8/6/07

2. Write the name of the person or Target

business that gets the check

3. Write the amount of the check in numbers $34.45

4. Write the amount of dollars in words thirtyfour

Write the amount of cents in numbers 45/100

Draw a line to the word dollars thirtyfour

and 45/100

5. Write a note to remember what school supplies

the check was for (this is not required but

can help when you balance your checkbook)

6. Sign your name Your Name

64

Your Name 1004 Your Address City, State Zip Code Date 1.___________

Pay to the order of _______________2.______________________________ Amount $___3.___________

_____4.____________________________________________________________________________ Dollars

Bank’s Name Address City, State Zip

For ___5.____________________ _______6___________________________________

1234567 0000000000160945456454 1004

Writing Numbers Review the spelling for numbers.

Dollar Amounts 1 one 2 two 3 three 4 four 5 five 6 six 7 seven 8 eight 9 nine 10 ten 11 eleven 12 twelve 13 thirteen 14 fourteen 15 fifteen 16 sixteen 17 seventeen 18 eighteen 19 nineteen 20 twenty 21 twentyone 22 twentytwo 23 twentythree 24 twentyfour 25 twentyfive 26 twentysix 27 twentyseven 28 twentyeight 29 twentynine 30 thirty 40 forty 50 fifty 60 sixty 70 seventy 80 eighty 90 ninety 100 one hundred

101 one hundred one 102 one hundred two 103 one hundred three 104 one hundred four 105 one hundred five 106 one hundred six 107 one hundred seven 108 one hundred eight 109 one hundred nine 110 one hundred ten 111 one hundred eleven 112 one hundred twelve 113 one hundred thirteen 114 one hundred fourteen 115 one hundred fifteen 116 one hundred sixteen 117 one hundred seventeen 118 one hundred eighteen 119 one hundred nineteen 120 one hundred twenty

Cents (¢) Amounts 0 ¢ 00/100 or no/100 1 ¢ 01/100 2 ¢ 02/100 3 ¢ 03/100 4 ¢ 04/100 5 ¢ 05/100 6 ¢ 06/100 7 ¢ 07/100 8 ¢ 08/100 9 ¢ 09/100 10 ¢ 10/100 11 ¢ 11/100 14 ¢ 14/100 20 ¢ 20/100 45 ¢ 45/100 56 ¢ 56/100 78 ¢ 78/100 81 ¢ 81/100 90 ¢ 90/100 99 ¢ 99/100 65

Practice Writing Numbers Write each amount in words.

1. 10 _________________________________

2. 35 _________________________________

3. 134 ________________________________

4. 67 _________________________________

5. 89 _________________________________

6. 2 __________________________________

7. 41 _________________________________

8. 256 ________________________________

9. 782 ________________________________

10.120 ________________________________

11.98 _________________________________

12.10/100 ______________________________

13.49/100 ______________________________

14.03/100 ______________________________

15.62/100 ______________________________

16. 99/100 ______________________________

17. 34/100 ______________________________

18.75/100 _______________________________

19.32/100_______________________________

20.81/100 _______________________________ Write each amount in number form

1. ninetyeight cents _____________________

2. thirtynine ___________________________

3. ninetyfour __________________________

4. fiftyseven cents ______________________

5. eleven _____________________________

6. seventeen __________________________

7. four cents __________________________

8. one hundred fourteen _________________

9. two hundred sixtyseven _______________

10. five hundred eighteen _________________ 66

Things to remember when you write a check

• Always write checks in ink.

• Fill in all of the amount line. If you have extra room, draw a line to fill in the extra

space.

• NEVER sign a blank check.

• Consider buying duplicate checks. This type of check is a little more expensive but

you always have a copy of your checks for your records.

• You don’t have to buy your checks at your bank. You just have to provide the bank’s

routing number and your account number to the check company and they can print

your checks.

Discussion 1. Why should you use ink to fill in your checks?

2. Why is it important to fill in the entire amount line on your check?

3. Why would it be a bad idea to sign a blank check?

68

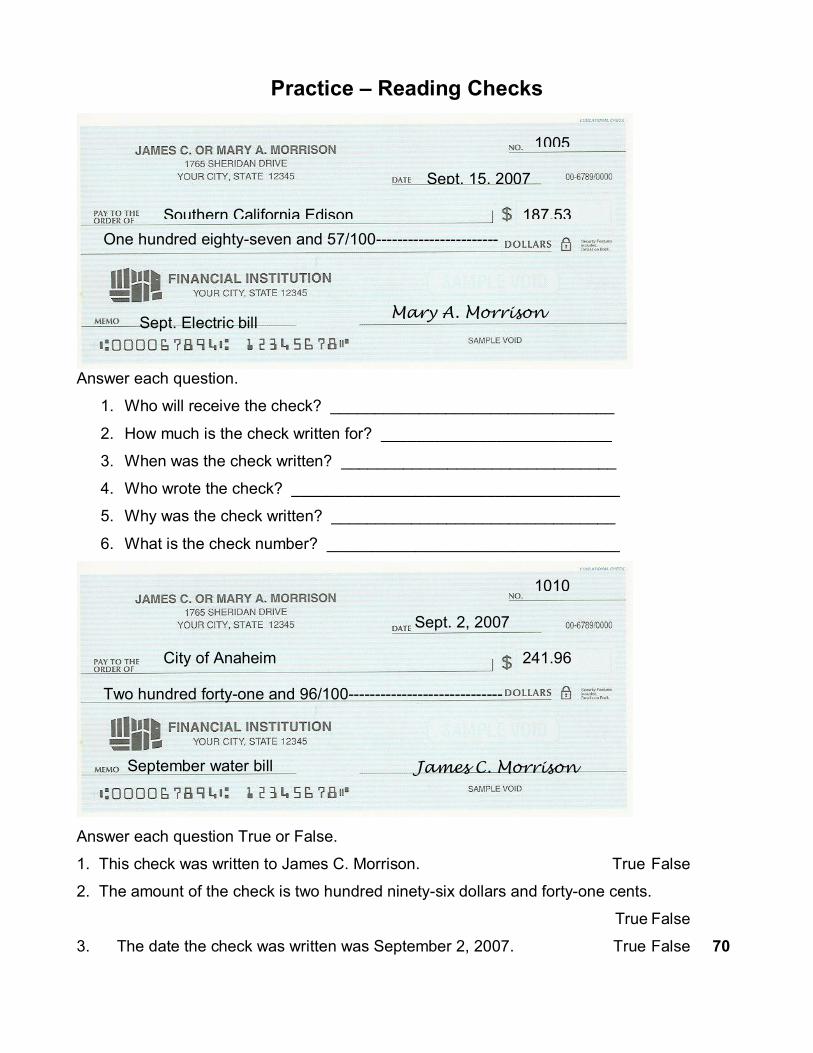

Practice – Reading Checks

Answer each question.

1. Who will receive the check? ________________________________

2. How much is the check written for? __________________________

3. When was the check written? _______________________________

4. Who wrote the check? _____________________________________

5. Why was the check written? ________________________________

6. What is the check number? _________________________________

Answer each question True or False.

1. This check was written to James C. Morrison. True False

2. The amount of the check is two hundred ninetysix dollars and fortyone cents.

True False

3. The date the check was written was September 2, 2007. True False 70

1005

Sept. 15, 2007

Southern California Edison 187.53 One hundred eightyseven and 57/100

Mary A. Morrison Sept. Electric bill

Sept. 2, 2007

1010

City of Anaheim 241.96

Two hundred fortyone and 96/100

James C. Morrison September water bill

Practice Writing Checks 1. You need to make a car payment to Ford Motor Finance on September 16, 2007 for two

hundred thirtytwo dollars and fourteen cents. Fill in the check below with the correct

information.

2. Today is September 22, 2007. You need to pay for groceries at Ralph’s. Your total is

sixtyseven dollars and eight cents.

72

Your Name 1005 Your Address City, State Zip Code Date ____________

Pay to the order of _________________________________________________ Amount $________________

___________________________________________________________________________________ Dollars

Bank’s Name Address City, State Zip

For ______________________ ____________________________________________

1234567 0000000000160945456454 1005

Your Name 1004 Your Address City, State Zip Code Date ____________

Pay to the order of _________________________________________________ Amount $________________

___________________________________________________________________________________ Dollars

Bank’s Name Address City, State Zip

For ______________________ ____________________________________________

1234567 0000000000160945456454 1004

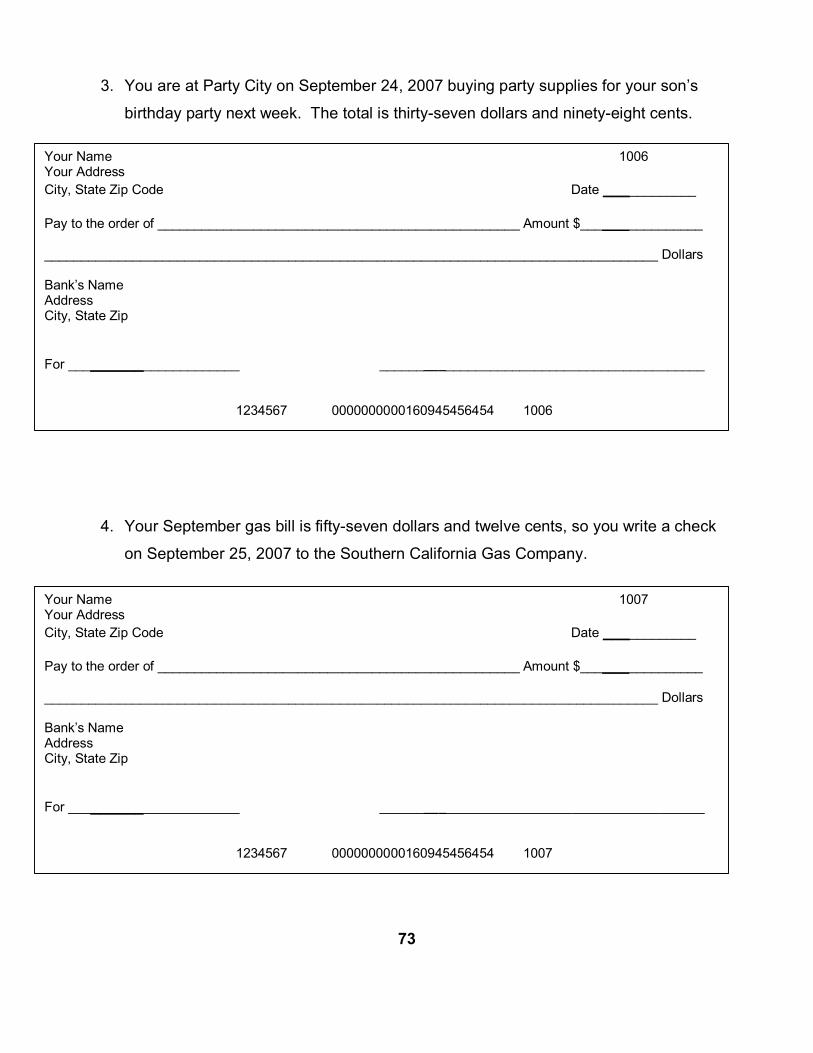

3. You are at Party City on September 24, 2007 buying party supplies for your son’s

birthday party next week. The total is thirtyseven dollars and ninetyeight cents.

4. Your September gas bill is fiftyseven dollars and twelve cents, so you write a check

on September 25, 2007 to the Southern California Gas Company.

73

Your Name 1006 Your Address City, State Zip Code Date ____________

Pay to the order of _________________________________________________ Amount $________________

___________________________________________________________________________________ Dollars

Bank’s Name Address City, State Zip

For ______________________ ____________________________________________

1234567 0000000000160945456454 1006

Your Name 1007 Your Address City, State Zip Code Date ____________

Pay to the order of _________________________________________________ Amount $________________

___________________________________________________________________________________ Dollars

Bank’s Name Address City, State Zip

For ______________________ ____________________________________________

1234567 0000000000160945456454 1007

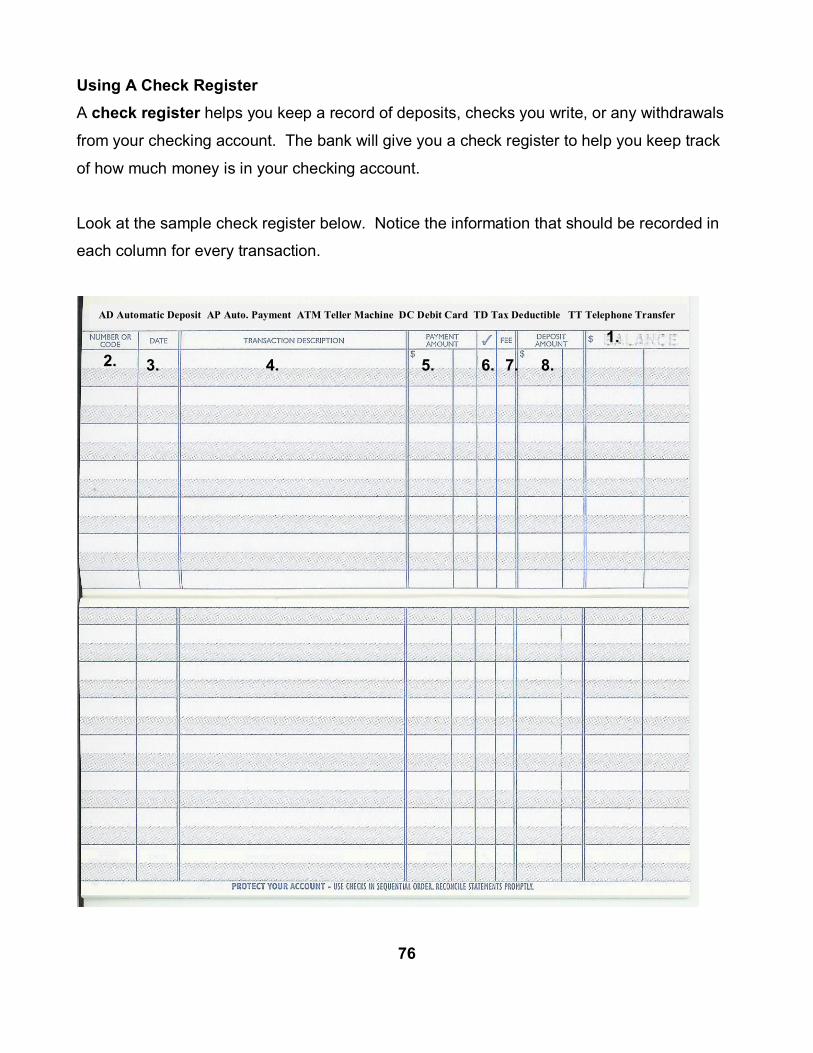

Using A Check Register A check register helps you keep a record of deposits, checks you write, or any withdrawals

from your checking account. The bank will give you a check register to help you keep track

of how much money is in your checking account.

Look at the sample check register below. Notice the information that should be recorded in

each column for every transaction.

76

1. 2. 3. 4. 5. 6. 7. 8.

AD Automatic Deposit AP Auto. Payment ATM Teller Machine DC Debit Card TD Tax Deductible TT Telephone Transfer

1. Balance – this refers to the most recent balance which is carried over from the

previous page in your register

2. Number or Code – number refers to check number; code refers to the codes listed at

the top of the register to tell you what type of transaction is recorded. For example, if

your paycheck is automatically deposited each month, use the code AD. If you have

automatic payments scheduled to be withdrawn from your account regularly, the

amount should be coded AP. Any amounts deposited or withdrawn from an

automated teller machine, should be coded ATM. When you use your debit card to

make a purchase, use the code DC. If you transfer money from one account to

another over the phone, use the code TT for telephone transfer.

3. Date – record the date that the transaction took place.

4. Transaction Description – this area allows you to record whom you wrote the check

to or any other information that describes the transaction that took place.

5. Payment Amount – record amounts that will be taken out of your account.

6. a check off each item that appears on your monthly statement as you balance your

checkbook each month.

7. Fee record any fees associated with each transaction. For example, you may be

charged a small fee for using an ATM that is not part of your bank.

8. Deposit Amount record any transactions that will be added to your account balance.

77

Practice Reading A Check Register Use the sample check register to answer the following questions.

78

groceries AD 9/15

Cash withdrawal

Citibank

202 9/10 Ralph’s

47 .92 513 .42

Deposit paycheck

1206 .17 1719 .59

ATM 9/18 ATM

60 .00 1658 .09

203 Target school supplies

53 .17 1604 .92 9/19

204 9/28 credit card payment

128 .65 1476.27

AD Automatic Deposit AP Auto. Payment ATM Teller Machine DC Debit Card TD Tax Deductible TT Telephone Transfer

561 .34

1.50

Look at the sample check register on the previous page. Use the information to answer the following questions.

1. What check number was written on September 9 to Ralph’s? ______________

2. How much was the fee charged for the ATM withdrawal on September 18? _____

3. What was the reason for the check written to Citibank? ____________________

4. What was the amount of the check written to Target on September 19? _________

5. What was the balance of the account on September 18? ___________________

Answer each question True or False based on the sample check register.

1. Check number 203 was written to pay for school supplies. True False

2. The total amount taken from the account on September 18 was $60.

True False

3. The paycheck deposited on September 15 is coded as an Automatic Payment.

True False

4. Check 204 to Citibank was for the amount of $1,476.27. True False

5. Check 202 was written to Albertson’s. True False

79

Practice Recording Transactions In Your Check Register

Record each transaction in the sample check register below.

1. The current account balance is four hundred seventyone dollars and eightysix cents.

2. Your paycheck is automatically deposited on September 15 in the amount of two

thousand three hundred twelve dollars and fortysix cents.

3. You made a car payment to Ford Motor Finance on September 16, 2007 for two

hundred thirtytwo dollars and fourteen cents with check 1004.

4. On September 22, 2007, you paid for groceries at Ralph’s with check 1005. Your total

was sixtyseven dollars and eight cents.

5. You were at Party City on September 24, 2007 buying party supplies for your son’s

birthday party. The total was thirtyone dollars and ninetyseven cents. You wrote

check number 1006.

6. Your September gas bill was fiftyseven dollars and twelve cents, so you wrote check

1007 on September 25, 2007 to the Southern California Gas Company.

7. On September 26, you withdrew eighty dollars from your bank’s ATM.

81

Recording Transaction Practice

82

AD Automatic Deposit AP Auto. Payment ATM Teller Machine DC Debit Card TD Tax Deductible TT Telephone Transfer

Deposit and Withdrawal Slips

When you go to the bank to make a deposit or withdrawal from your account, you may be

asked to fill out a deposit or withdrawal slip. This is a written record of how much money you

are putting in or taking out of your account. Most of the time this is the same form.

Look at the sample deposit/ withdrawal slip below.

1. Enter the amount of cash you are depositing.

2. Enter the amount of each check you are depositing. (if you are depositing more than

two checks, you will need to use the worksheet on the back.)

3. Add the amount of cash and checks/

4. Write the amount of cash, if any, you would like back from the deposit amount.

5. Write the total amount you are depositing in your account.

6. If you are withdrawing money from your account, enter the amount and form of

currency you want to receive – cash, money order, or cashier’s check.

7. Add the amount of cash, money orders, or cashier’s check.

8. If you want to move money from this account to another account, enter the amount

you wish to transfer.

9. Add the total amount being withdrawn or transferred.

10.Sign your name. 84

1.

2.

3.

4.

5.

6.

7.

8.

9.

10.

If you are depositing more than two

checks, you will need to list the amount of

each check on the back and add to find the

total amount. This is the amount you will

write in the blank labeled “Total From

Reverse Side.”

85

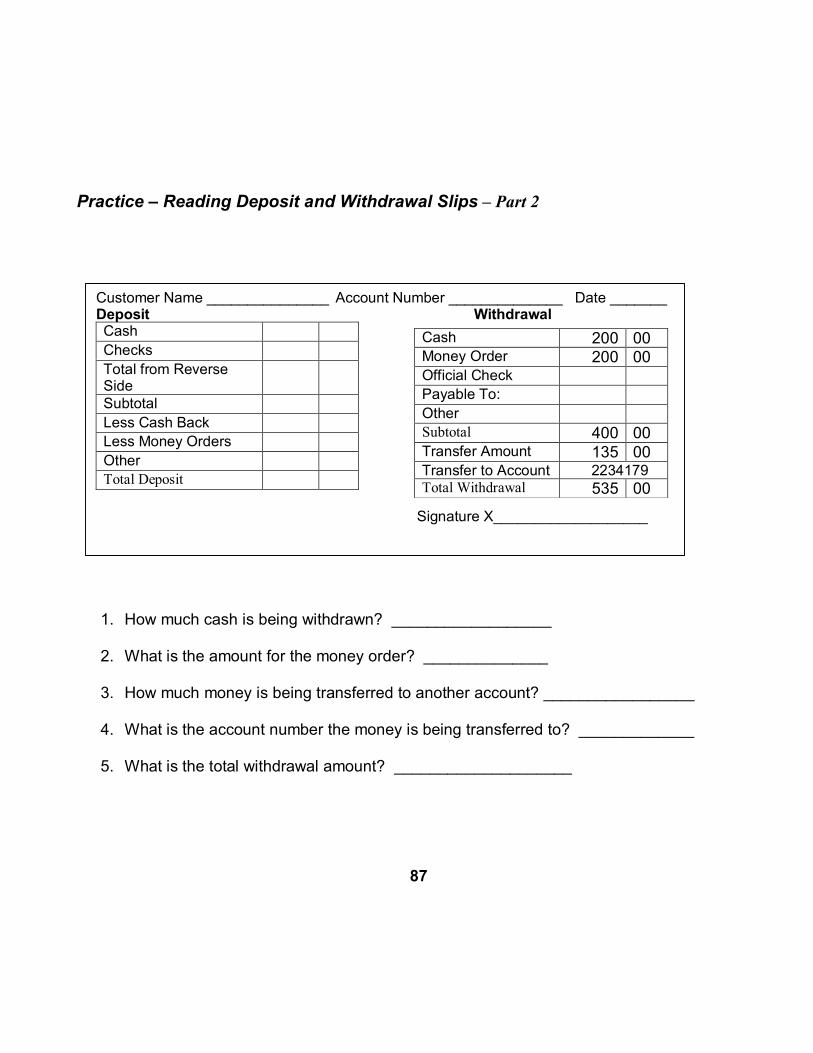

Practice – Reading Deposit and Withdrawal Slips

1. What is the total amount deposited? _______________________

2. How much cash is being deposited? _______________________

3. What is the amount of the check being deposited? ____________

4. Is any cash being taken out of the deposit? __________________

86

120 .00

Customer Name _______________ Account Number ______________ Date _______ Deposit Withdrawal

Signature X___________________

Cash 120 00 Checks 250 00 Total from Reverse Side Subtotal 370 00 Less Cash Back Less Money Orders Other Total Deposit 370 00

Cash Money Order Official Check Payable To: Other Subtotal Transfer Amount Transfer to Account Total Withdrawal

Practice – Reading Deposit and Withdrawal Slips – Part 2

1. How much cash is being withdrawn? __________________

2. What is the amount for the money order? ______________

3. How much money is being transferred to another account? _________________

4. What is the account number the money is being transferred to? _____________

5. What is the total withdrawal amount? ____________________

87

Customer Name _______________ Account Number ______________ Date _______ Deposit Withdrawal

Signature X___________________

Cash Checks Total from Reverse Side Subtotal Less Cash Back Less Money Orders Other Total Deposit

Cash 200 00 Money Order 200 00 Official Check Payable To: Other Subtotal 400 00 Transfer Amount 135 00 Transfer to Account 2234179 Total Withdrawal 535 00

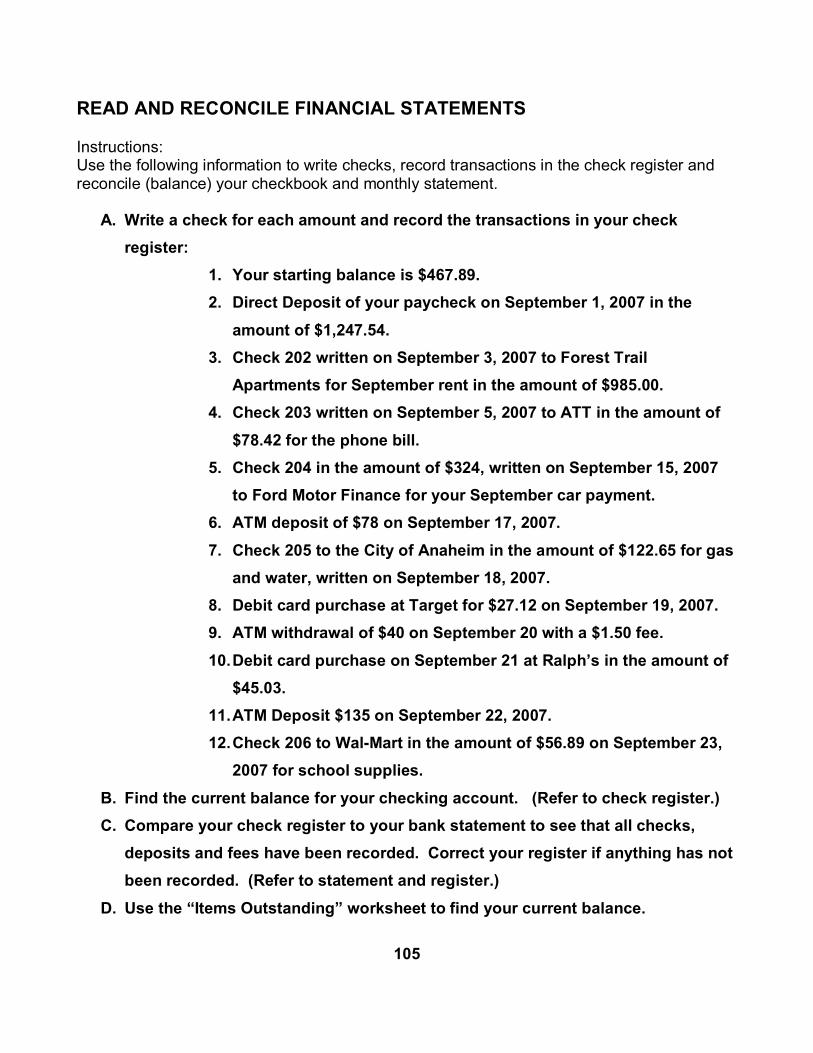

SECTION 4: READ AND RECONCILE FINANCIAL STATEMENTS

Language and Literacy Objective #1 Read and reconcile financial statements

Additional Assessment Plan Task #4 Reconcile a bank statement: given a bank statement, completed check register, and

reconciliation form, student will reconcile the bank statement

LEVEL: ILADVANCED

94

Credit Cards and Bank Statements

Vocabulary

Credit – borrowing money now and paying later.

Credit Cards – cards that you use to buy goods and pay for them later

Credit Rating – tells the lender whether you will be able to pay back the borrowed money.

Debt – the money that you have borrowed from a person or business.

Application – a written form you fill out to apply for a credit card.

Due Date – the date that the company must receive your payment.

Minimum Payment – the least amount of money you should pay.

We don’t always have cash on hand to buy all the things that we need in our everyday lives. For example suppose you need new tires for your car – they are really old and worn out. You cannot wait too long, because it’s not safe to drive around with worn out tires. When you get an estimate, you find it will cost $600.00 to replace the front tires. If you save $50 from your paycheck each month, how long will it take before you have saved up enough to buy the tires? Can you wait that long? Is it safe to wait that long? Probably not, so you might need access to a credit card so you can buy the tires as soon as possible.

What is Credit?

When you don’t have cash, credit allows you to buy things and pay for them later. It’s borrowing money from companies, stores, or banks. They charge you interest for allowing you to use the credit.

What is a Credit Card?

A Credit Card looks like any other plastic card. The name and the logo of the company along with numbers and your name is printed on it. It also has the expiration date on it. A Credit Card allows you to make purchases for which you pay at a later date.

95

Types of Credit Cards

There are different types of Credit Cards issued by different companies, stores or banks. Store Cards are issued by large stores; for example Nordstrom, Sears, JCPenny and other stores. The store cards can be used only in the different branches of the same store. Major Cards are issued by banks. Bank cards can be used in many places, for example; in restaurants, grocery stores, gas stations, motels, and many other places.

Why should I have A Credit Card?

It’s useful to have a credit card, but remember you have to pay interest on the purchases. Let’s look at some advantages and disadvantages of it.

Advantages Of A Credit Card.

1. A Credit Card is easier to carry then a bundle of money in your pocket. 2. A Credit Card is easier to carry when you are traveling. 3. You have only one bill to pay at the end of the month rather than

mailing payments to several different stores. 4. You build a good credit rating by using your credit card and paying the bill

on time.

Disadvantages Of A Credit Card.

1. Using your card to buy more than you can afford. 2. Many companies charge a very high interest. 3. It is easy to overspend when using a credit card. 4. You can very easily get into debt with credit cards.

How Can I Apply for A Credit Card?

If you are at least 18 years old, you can apply for a credit card. All you have to do is fill out a credit card application, mail it and then wait a few days. The company will process your application and inform you by mail. You can also go online and apply for it.

96

Some Important Things To Remember:

• Use Credit Cards only to buy things you can afford. • Pay the full amount by the due date. • If you cannot pay the full amount, pay the minimum payment. • Don’t be late on your payments. • You will be charged interest on the unpaid amount. • Always check your monthly statement and compare it with your

purchases. • Call the company if you see a mistake on the monthly statement. • It is easy to get into debt with credit cards. • Don’t be tempted. Use the credit cards wisely. • Don’t carry too many cards with you. • Keep your cards in a safe place.

What If The Credit Card Is Lost Or Stolen?

If your credit is lost or stolen report it immediately or as soon as you find it. Call the credit company or the bank. Tell the representative that your card has been lost or stolen. He will ask you for your account number. To stop the thief from using your card they will close your account and cancel your card. In this way your card cannot be misused. The company or the bank will issue you a new card with a new account number.

97

CREDIT CARD EXERCISE:

Matching:

______ 1. The date that the payment must be a. application received by the company is the __________.

______ 2. If you cannot pay all of your credit b. interest card bill, the credit card company will charge you high ___________.

______ 3. If you use your credit card to buy c. minimum more than you can afford, payment

you will have _________.

______ 4.The least amount you can pay is the ________________. d. due date

______ 5.A written form you fill out to apply e. credit rating for credit is called an __________________.

______ 6.Cards that let you buy things now and f. debt and pay for them later are called __________________.

______ 7.If you always pay your bills on time you are g. credit cards building a good _________________.

98

Directions: Fill out the form, and review the credit card terminology on the next page.

100

Credit Card Application Form

Individual Applicant Information

Name (Last, First, Middle)

BIRTHDATE TELEPHONE NO. DRIVER’S LICENSE NO. SOCIAL SECURITY NO. NO. DEPENDENTS

ADDRESS (Street, City, State and Zip) COUNTY Do You:

OWN RENT

How Long

ADDRESS (Street, City, State and Zip) (Complete if less than 3 years at present address) COUNTY Do You:

OWN RENT

How Long

Employment Information

EMPLOYER (Company Name and Address) How Long

BUSINESS PHONE Ext. POSITION OR TITLE SALARY PER MONTH

GROSS $ PREVIOUS EMPLOYER (Company Name & Address) How Long

NAME & ADDRESS OF NEAREST RELATIVE RELATIONSHIP TELEPHONE NO. (include area code) NOT LIVING WITH YOU

By submitting this application, I certify that I have read, met and agreed to all of the terms, conditions and disclosures related to this application.

Signed: __________________________________________________________ Date: ________________________

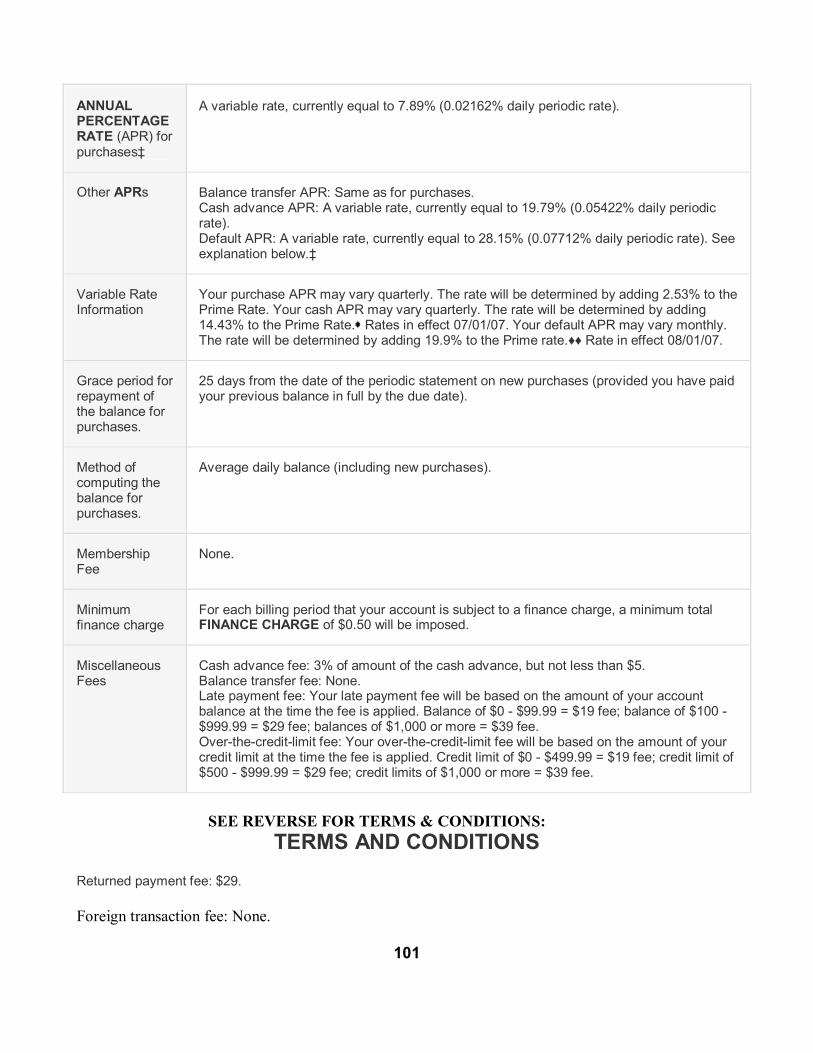

SEE REVERSE FOR TERMS & CONDITIONS: TERMS AND CONDITIONS

Returned payment fee: $29.

Foreign transaction fee: None.

101

ANNUAL PERCENTAGE RATE (APR) for purchases‡

A variable rate, currently equal to 7.89% (0.02162% daily periodic rate).

Other APRs Balance transfer APR: Same as for purchases. Cash advance APR: A variable rate, currently equal to 19.79% (0.05422% daily periodic rate). Default APR: A variable rate, currently equal to 28.15% (0.07712% daily periodic rate). See explanation below.‡

Variable Rate Information

Your purchase APR may vary quarterly. The rate will be determined by adding 2.53% to the Prime Rate. Your cash APR may vary quarterly. The rate will be determined by adding 14.43% to the Prime Rate. Rates in effect 07/01/07. Your default APR may vary monthly. The rate will be determined by adding 19.9% to the Prime rate.♦♦ Rate in effect 08/01/07.

Grace period for repayment of the balance for purchases.

25 days from the date of the periodic statement on new purchases (provided you have paid your previous balance in full by the due date).

Method of computing the balance for purchases.

Average daily balance (including new purchases).