Embed Size (px)

Citation preview

Electronic authentication: validating and verifying customer identities and bank detailsPresented by: Stan Matthews & Scott Robertson13th November 2007

Making it easy for your customer

Streamlining business processes to improve customer interaction

Straight-through processingName and address capture

Electronic identity check

Credit check

Bank account validation

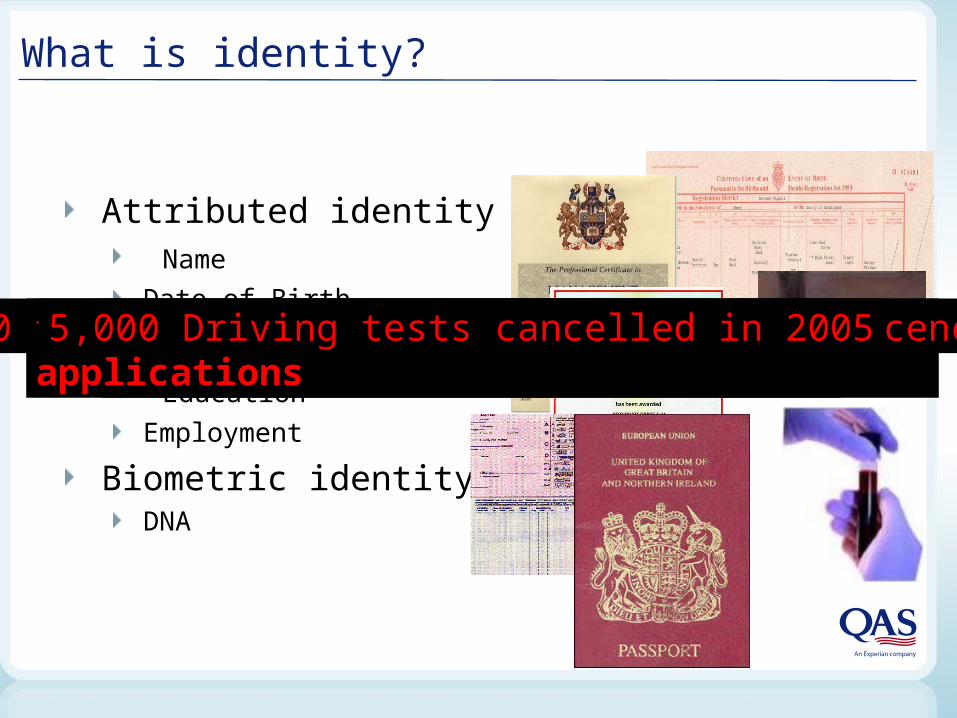

What is identity?

Attributed identity Name

Date of Birth

Collected identity Education

Employment

Biometric identityDNA

80,000 reported cases of Fraud 200680,000 reported cases of Fraud 2006UKPA had 16,500 known fraudulent applicationsUKPA had 16,500 known fraudulent applicationsUKPA issued 10,000 UKPA issued 10,000 2,500 fraudulent applications for Driving Licences2,500 fraudulent applications for Driving Licences5,000 Driving tests cancelled in 20055,000 Driving tests cancelled in 2005

Principles of eID Authentication

Electronic Identity Authentication

Proves your customers identity by comparing bio-graphical information given at point of

application against data held within authoritative databases……..

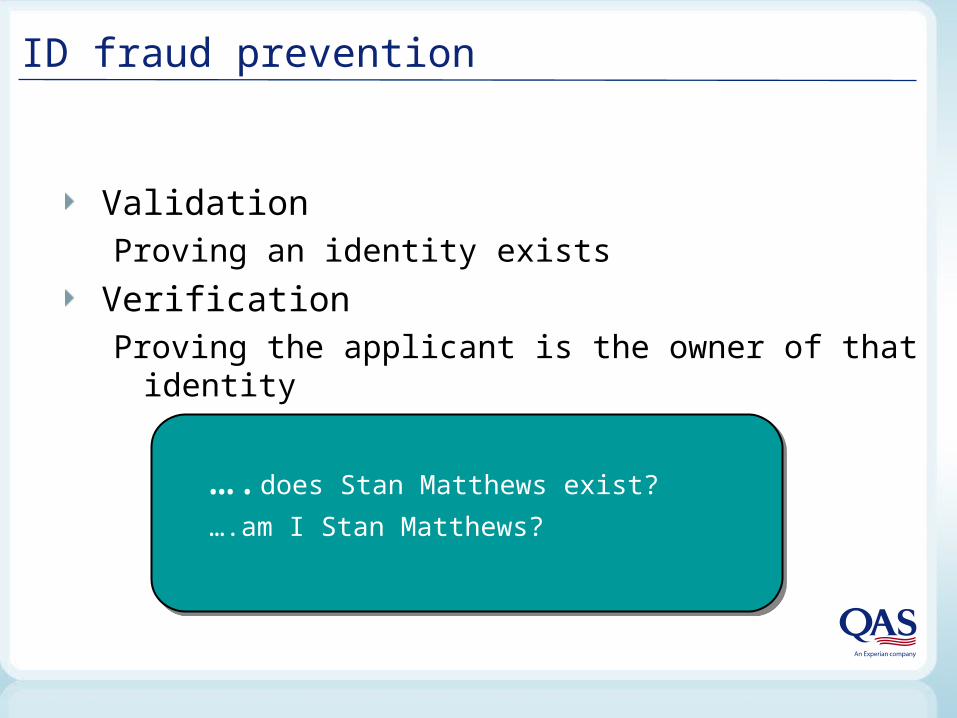

ID fraud prevention

ValidationProving an identity exists

VerificationProving the applicant is the owner of that identity

….does Stan Matthews exist?

….am I Stan Matthews?

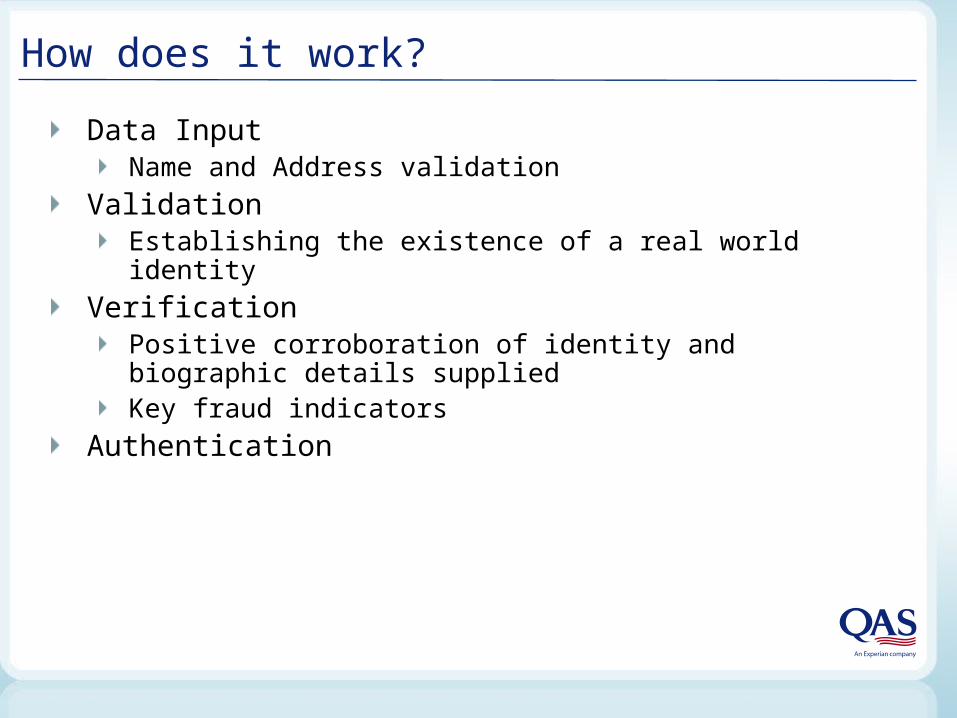

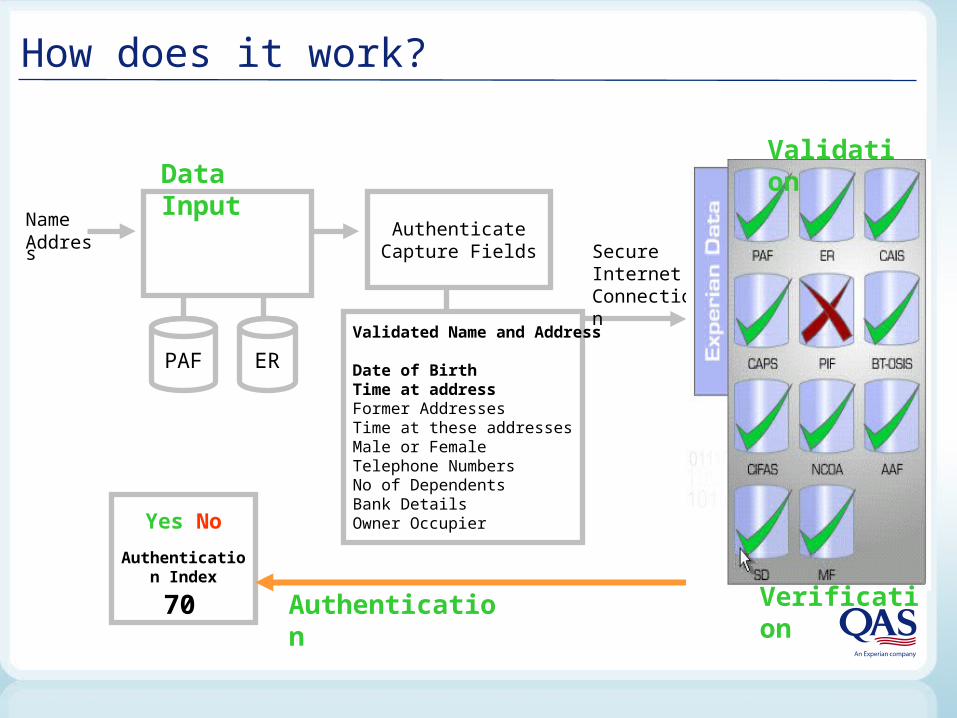

How does it work?

Data InputName and Address validation

ValidationEstablishing the existence of a real world identity

VerificationPositive corroboration of identity and biographic details suppliedKey fraud indicators

Authentication

How does it work?

AuthenticateCapture Fields

Validated Name and Address

Date of BirthTime at addressFormer AddressesTime at these addressesMale or FemaleTelephone NumbersNo of DependentsBank DetailsOwner Occupier

PAF ER

NameAddress

Data Input

Yes No

70

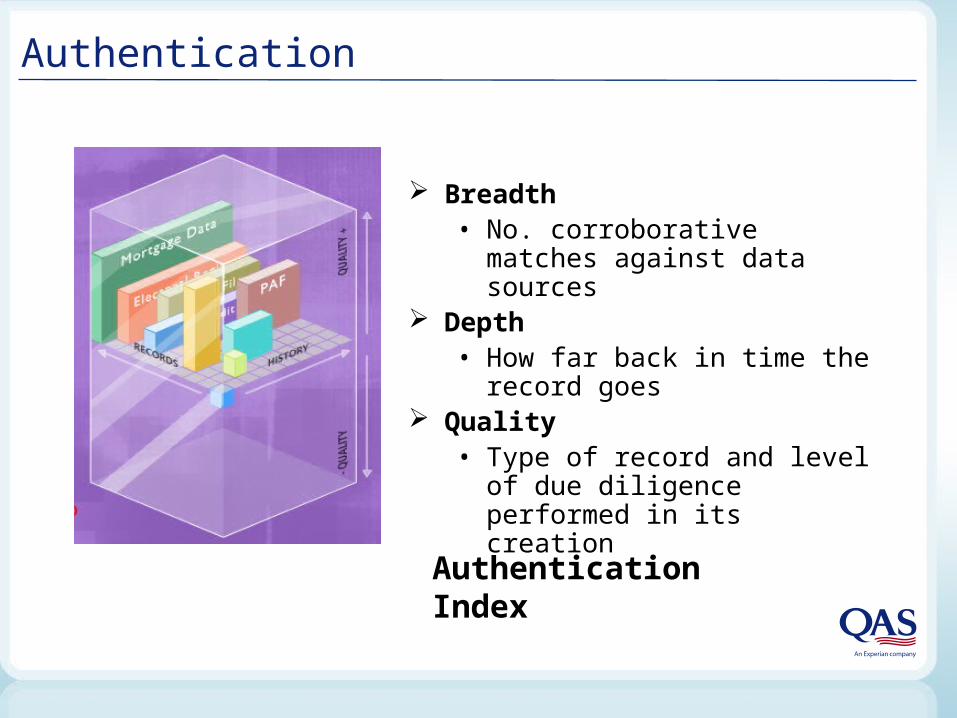

Authentication Index

Authentication

Secure Internet Connection

Validation

Verification

Authentication

Breadth• No. corroborative matches

against data sources Depth

• How far back in time the record goes

Quality• Type of record and level of due

diligence performed in its creation

Authentication Index

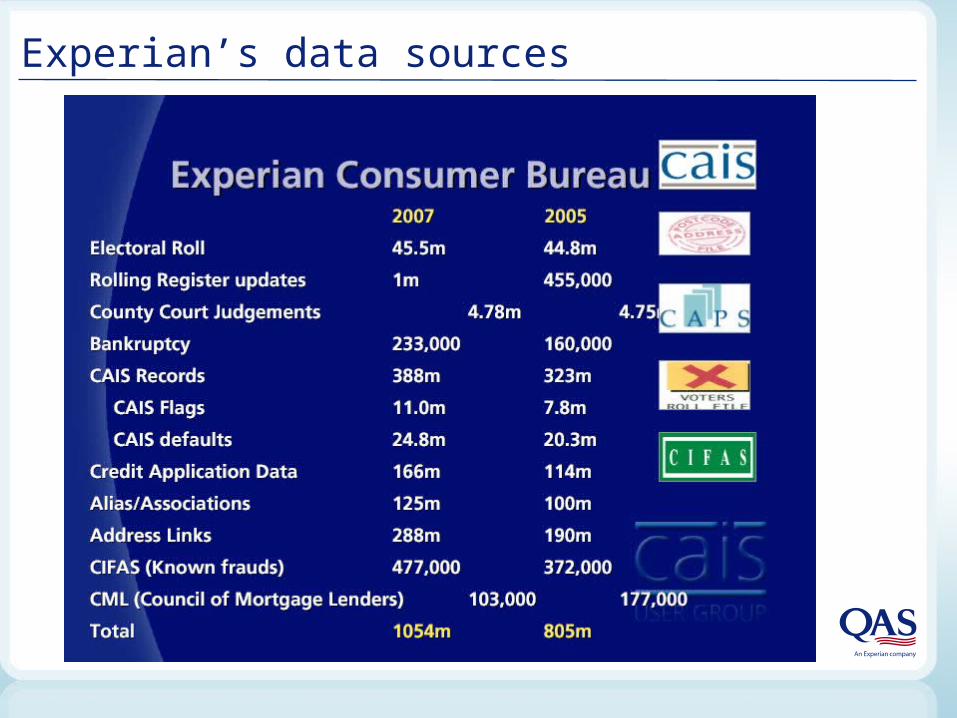

Experian’s data sources

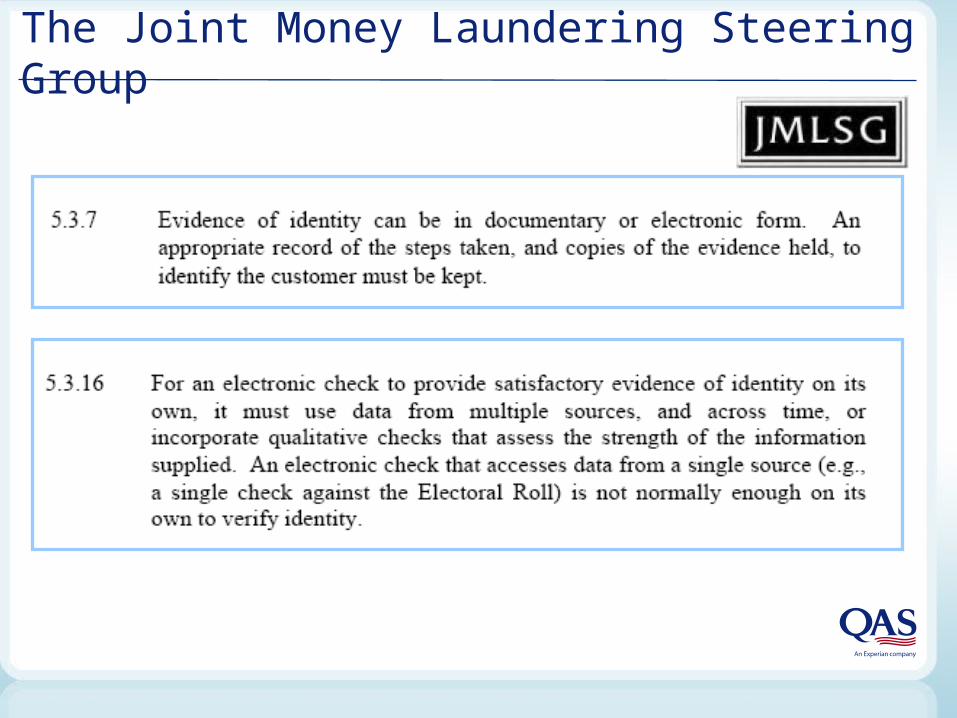

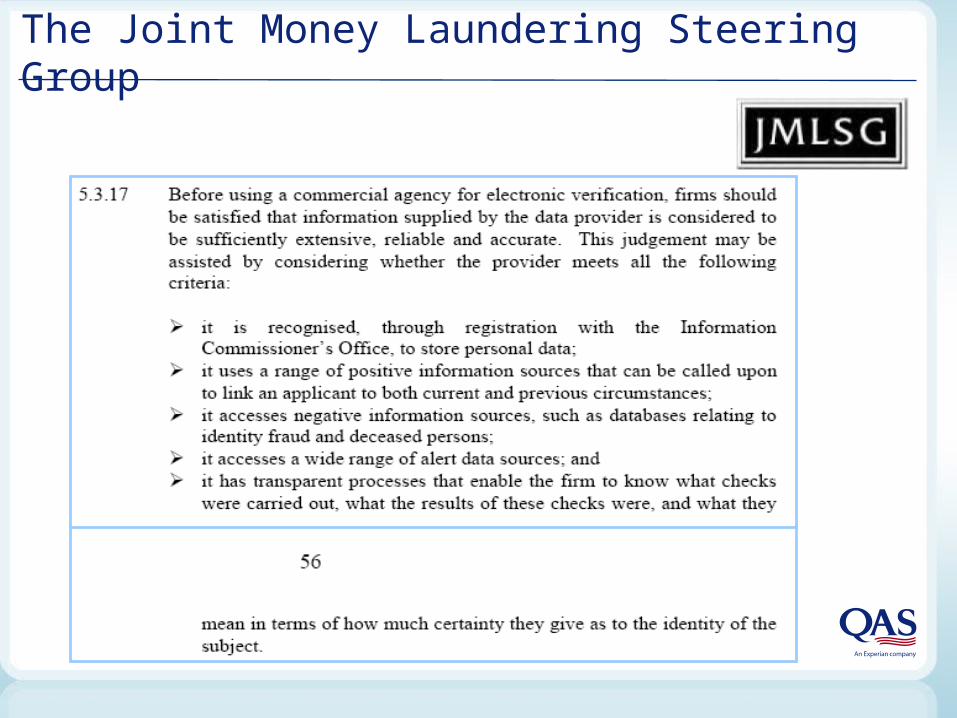

The Joint Money Laundering Steering Group

The Joint Money Laundering Steering Group

“Business drivers”

Straight through processing

Web

Call Centre

Post

Consistent AML strategy

Risk based approach

Improved operational efficiency

Compliant

Reduction in fraud

Authenticate

Hosted, integrated or bespoke

Solution fast & easy to implement

Name & address verification on entry

Breadth & depth of Experian data

Data consistency and updates

Pre-configured authentication templates

Easy to use – improves business process

Scaleable Solution

Summary

Identity theft is growing problem

Paper based checks are flawed

Electronic checks are accredited

Ease of use and implementation

Integrated into existing applications

Electronic authentication: validating and verifying customer identities and bank details

Presented by: Stan Matthews & Scott Robertson

Getting payment processing right

Improve the customer experience

Reduce costs

Increase revenue

How many do you have?

What do you pay for by

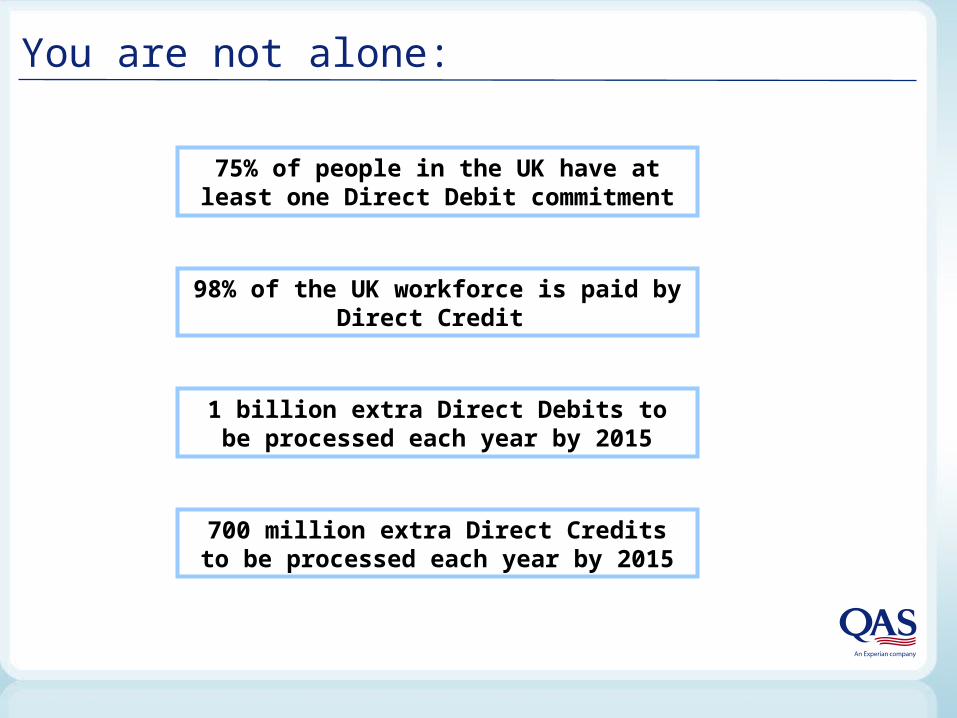

You are not alone:

75% of people in the UK have at least one Direct Debit commitment

98% of the UK workforce is paid by Direct Credit

1 billion extra Direct Debits to be processed each year by 2015

700 million extra Direct Credits to be processed each year by 2015

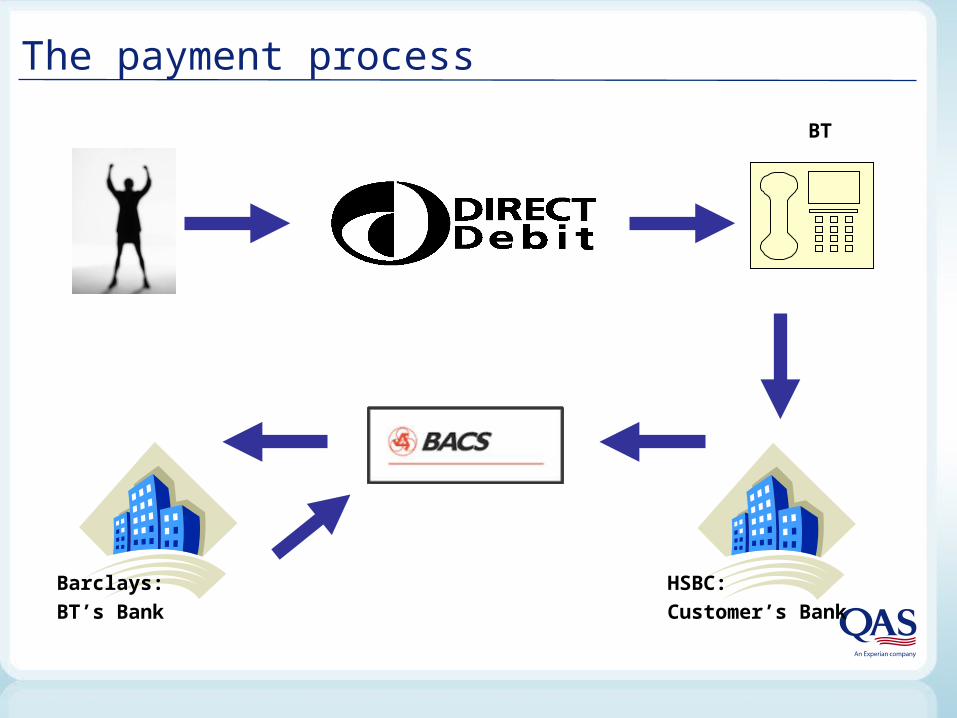

Barclays:

BT’s Bank

BT

HSBC:

Customer’s Bank

The payment process

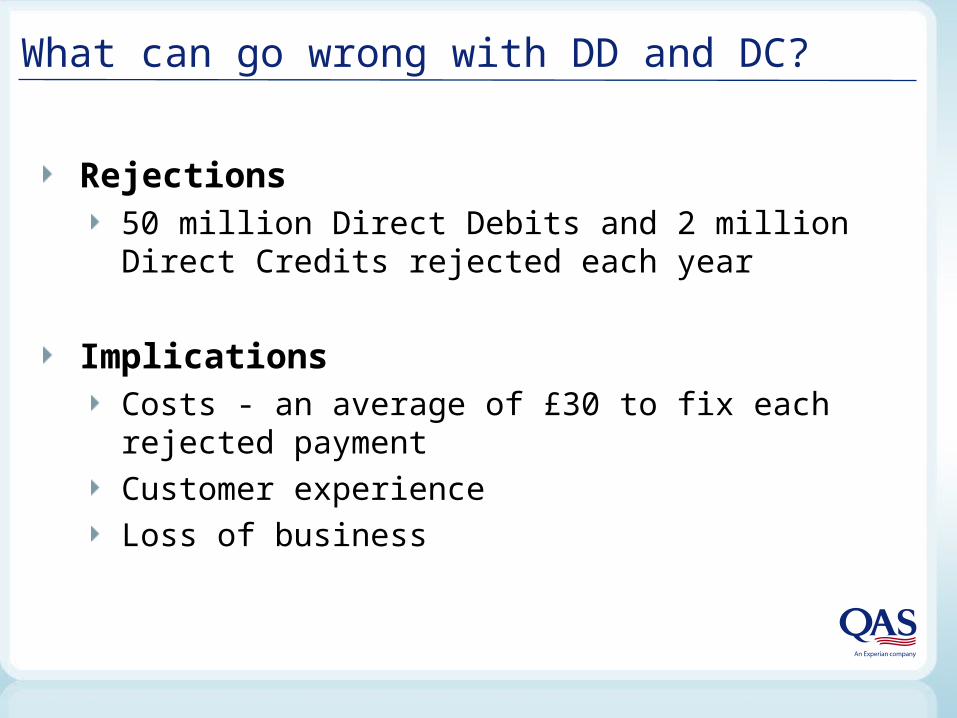

What can go wrong with DD and DC?

Rejections50 million Direct Debits and 2 million Direct Credits rejected each year

ImplicationsCosts - an average of £30 to fix each rejected payment

Customer experience

Loss of business

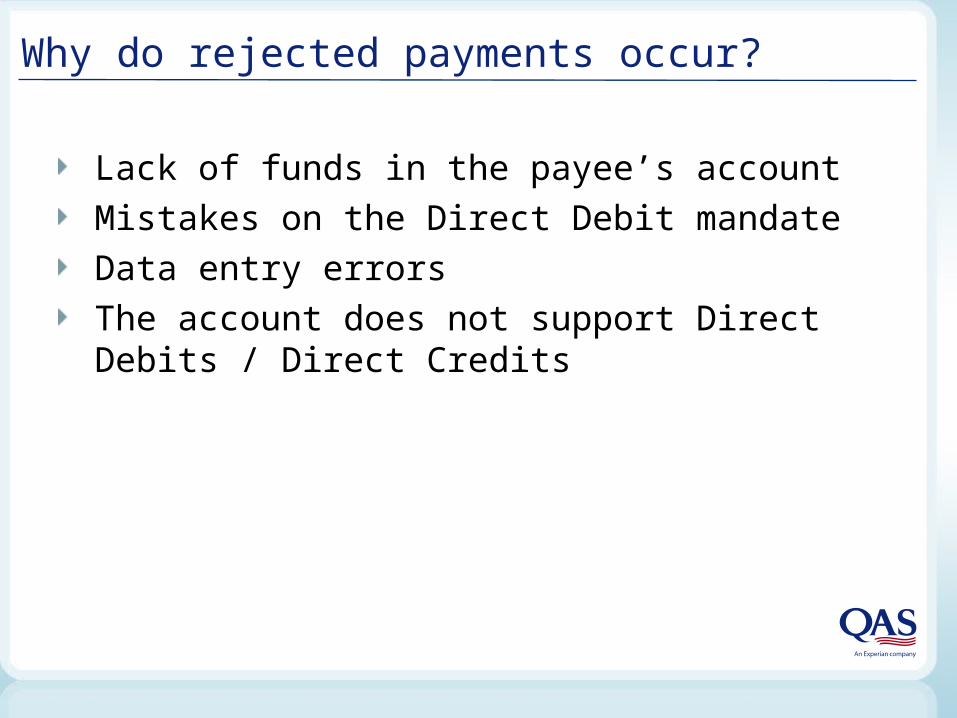

Lack of funds in the payee’s account

Mistakes on the Direct Debit mandate

Data entry errors

The account does not support Direct Debits / Direct Credits

Why do rejected payments occur?

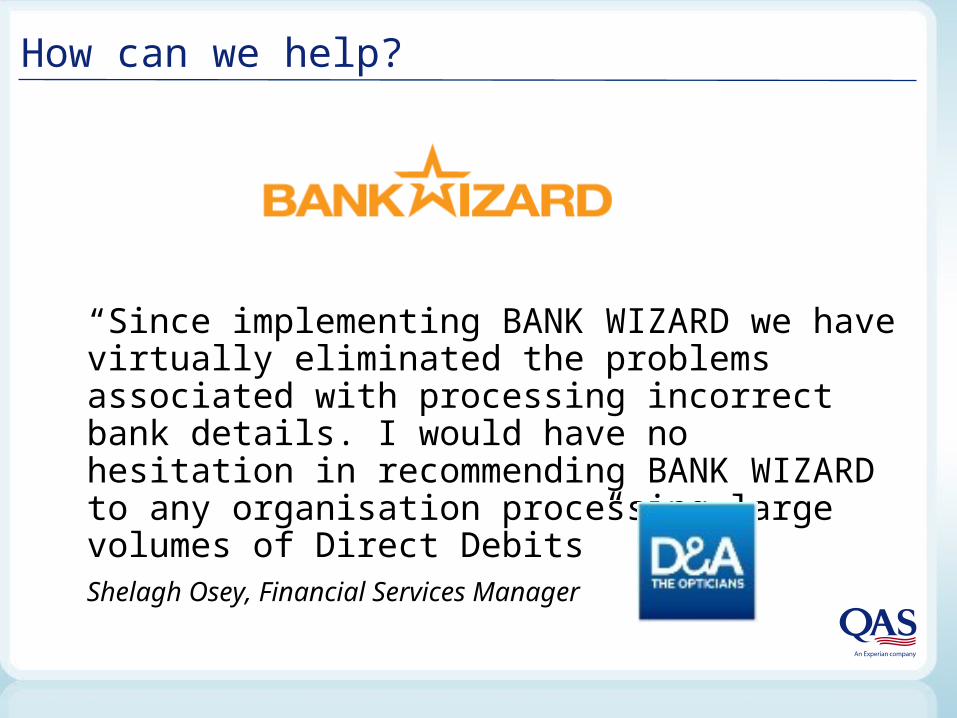

How can we help?

“Since implementing BANK WIZARD we have virtually eliminated the problems associated with processing incorrect bank details. I would have no hesitation in recommending BANK WIZARD to any organisation processing large volumes of Direct Debits” Shelagh Osey, Financial Services Manager

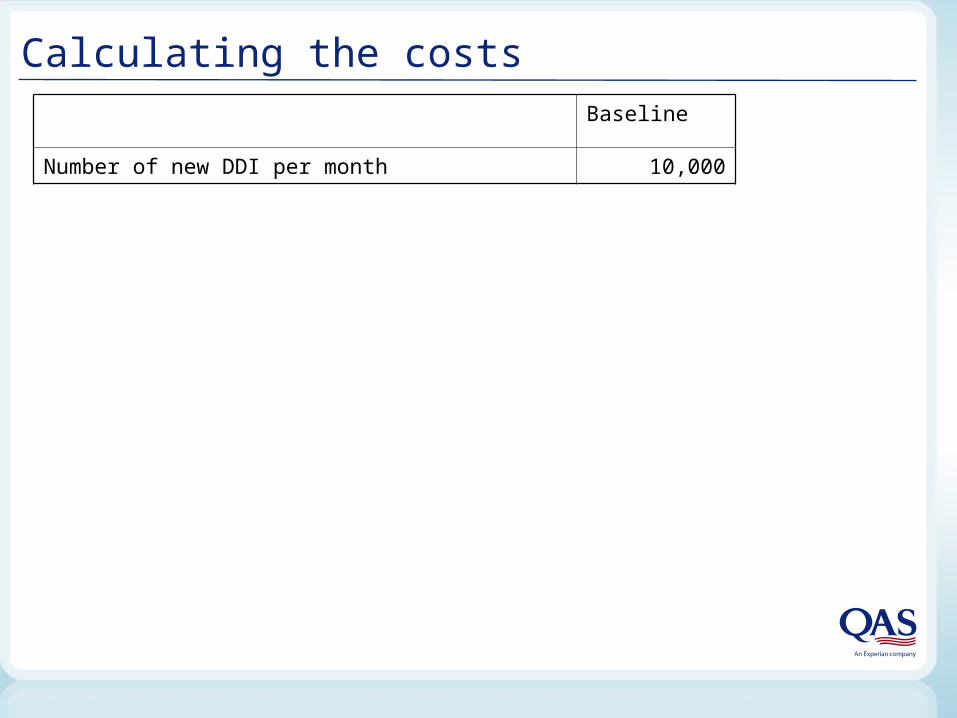

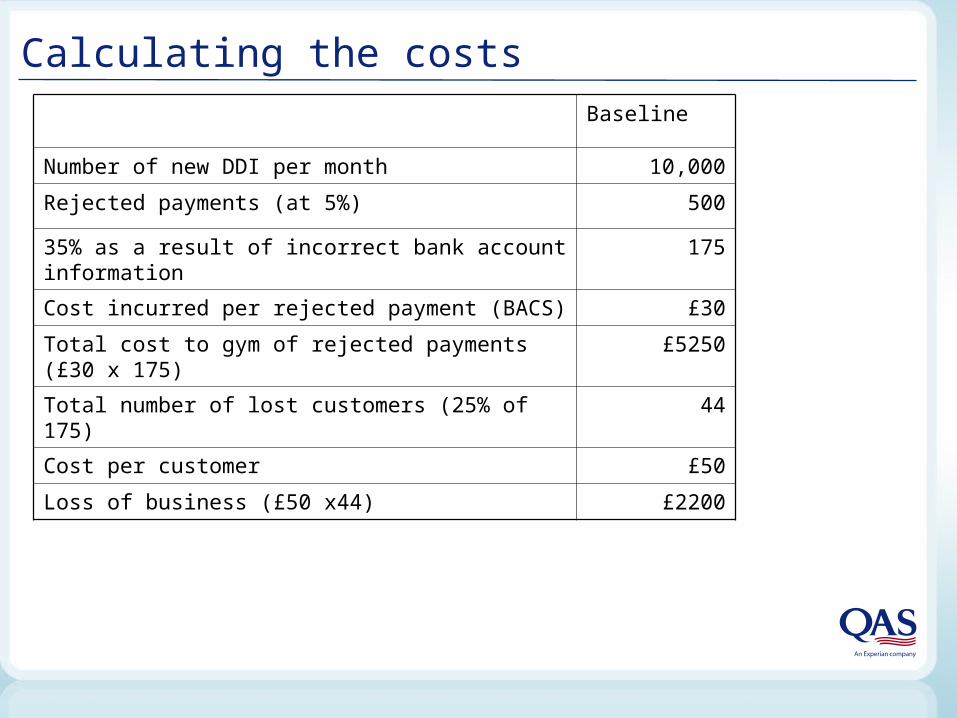

Calculating the costsBaseline

Number of new DDI per month 10,000

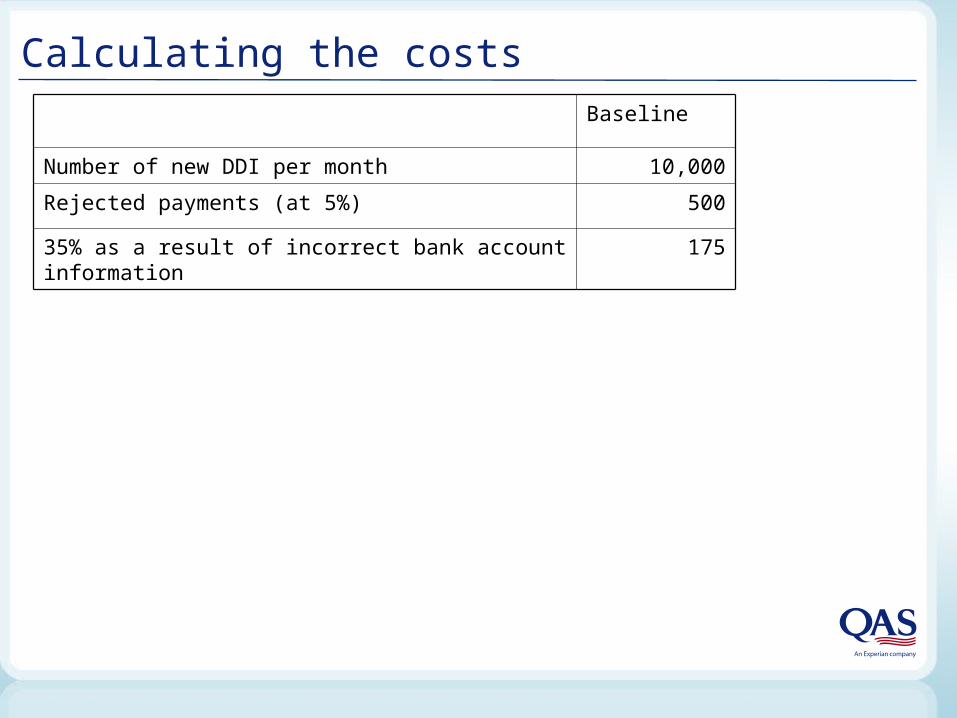

Calculating the costsBaseline

Number of new DDI per month 10,000

Rejected payments (at 5%) 500

35% as a result of incorrect bank account information 175

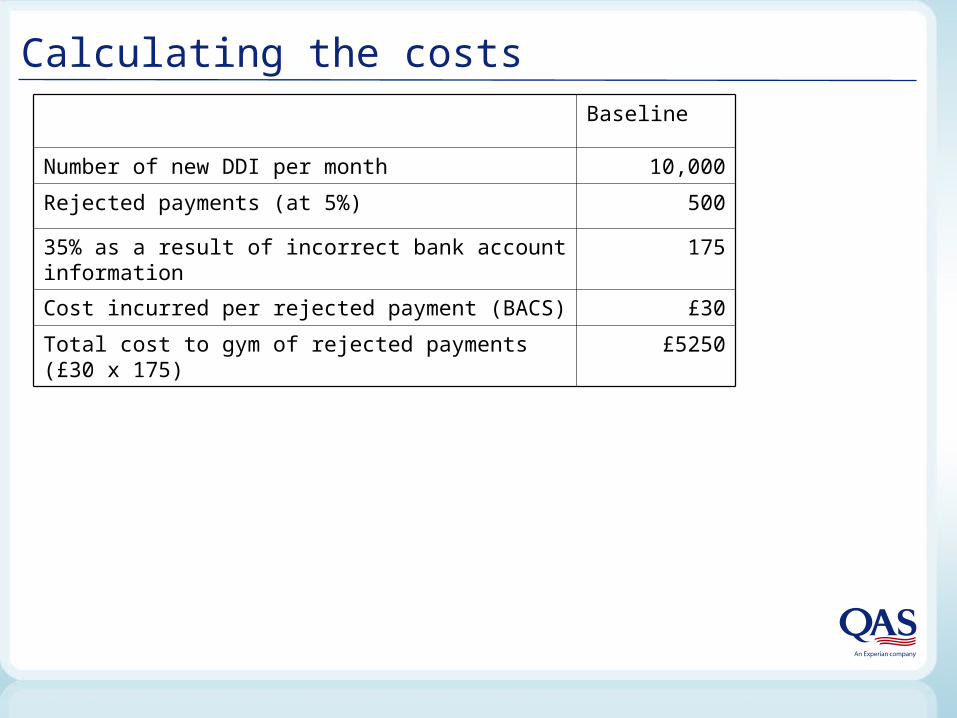

Calculating the costsBaseline

Number of new DDI per month 10,000

Rejected payments (at 5%) 500

35% as a result of incorrect bank account information 175

Cost incurred per rejected payment (BACS) £30

Total cost to gym of rejected payments (£30 x 175) £5250

Calculating the costsBaseline

Number of new DDI per month 10,000

Rejected payments (at 5%) 500

35% as a result of incorrect bank account information 175

Cost incurred per rejected payment (BACS) £30

Total cost to gym of rejected payments (£30 x 175) £5250

Total number of lost customers (25% of 175) 44

Cost per customer £50

Loss of business (£50 x44) £2200

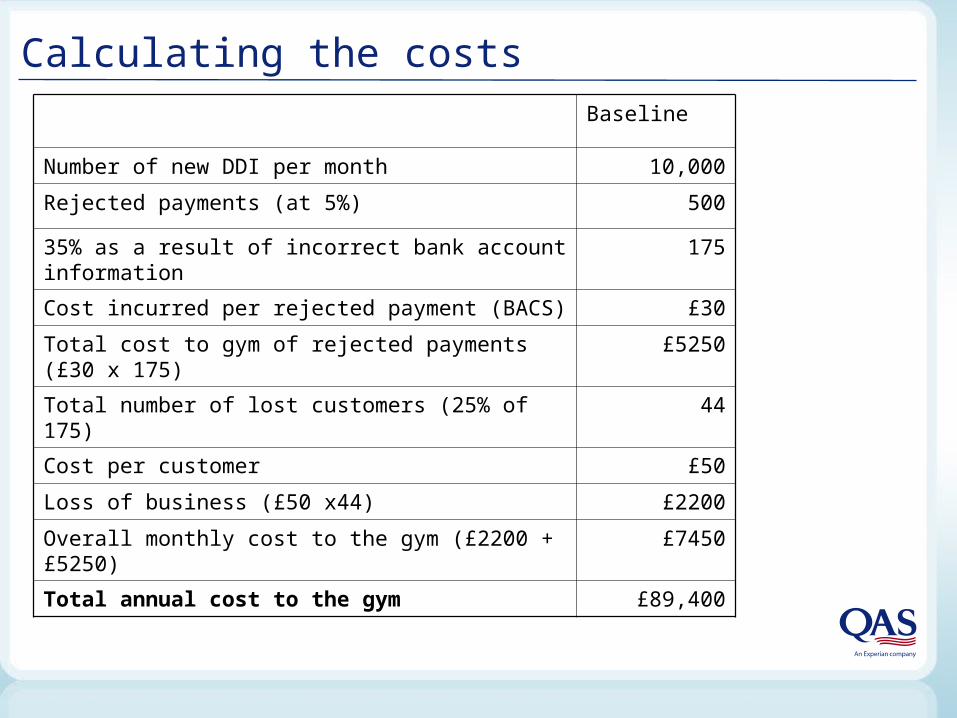

Calculating the costsBaseline

Number of new DDI per month 10,000

Rejected payments (at 5%) 500

35% as a result of incorrect bank account information 175

Cost incurred per rejected payment (BACS) £30

Total cost to gym of rejected payments (£30 x 175) £5250

Total number of lost customers (25% of 175) 44

Cost per customer £50

Loss of business (£50 x44) £2200

Overall monthly cost to the gym (£2200 + £5250) £7450

Total annual cost to the gym £89,400

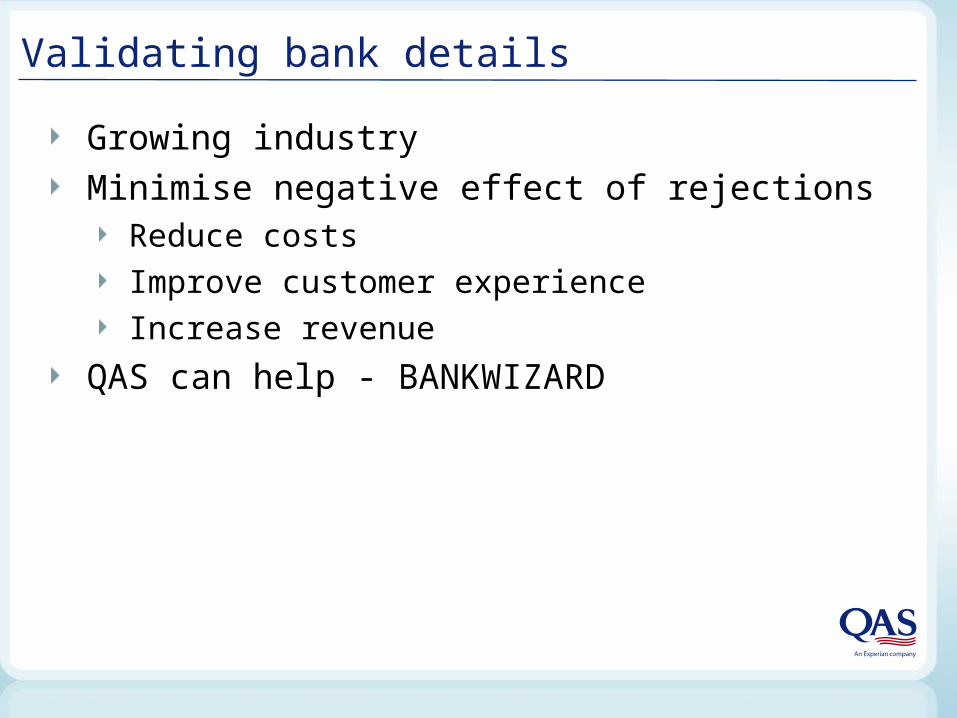

Validating bank details

Growing industry

Minimise negative effect of rejectionsReduce costs

Improve customer experience

Increase revenue

QAS can help - BANKWIZARD

Thank you for listening

Any Questions?

Thank you for listening

Presented by: Stan Matthews & Scott Robertson Date: 13th November 2007

www.qas.co.uk