Embed Size (px)

DESCRIPTION

Report and Accounts of Elite Insurance Company Limited.

Citation preview

Report and Financial Statements

Proud sponsor ofNorthampton Saints

31 March 2014

Proud sponsor of Northampton Saints

No-one tackles risk like we do

Registered in Gibraltar: 91111

Elite Insurance Company Limited

Proud sponsor of Northampton Saints

Contents Page

Directors, Officers and Other Information 4

Directors’ Report 5

Independent Auditors’ Report to the Members 8

Statement of Comprehensive Income 10

Balance Sheet 11

Statement of Changes in Equity 12

Cash Flow Statement 13

Notes to the Financial Statements 14

3

Elite Insurance Company LimitedDIRECTORS, OFFICERS AND OTHER INFORMATION

Proud sponsor of Northampton Saints

4

Directors: P Lavender J Smart D Smith D Meadus S Panu R Smart I Prescott C Tattersall

Secretary: M Sene

Auditors: EY Limited Regal House Queensway Gibraltar

Registered office: 47/48 The Sails Queensway Quay Queensway Gibraltar

Elite Insurance Company LimitedDIRECTORS’ REPORT

Proud sponsor of Northampton Saints

5

The directors submit their report and the audited financial statements for the year ended 31 March 2014.

Principal activity

Elite Insurance Company Limited (“the Company”) was incorporated on 19 April 2004 and began trading in January 2006. The principal activity of the Company is that of an insurance underwriter. The Company is licensed by the Gibraltar Financial Services Commission, under the Financial Services (Insurance Companies) Act, to underwrite the following insurance classes:

1 Accident2 Sickness 3 Land vehicles 7 Goods in transit8 Fire and natural forces9 Damage to property10 Motor vehicle liability13 General Liability15 Suretyship 16 Miscellaneous financial loss17 Legal expenses

During the year the Company underwrote Legal expense business, Warranty, Property, Liability, Pet insurance, Professional Indemnity insurance, Performance Bonds and in July 2013, began writing motor insurance.

Review of business

The Company has performed strongly in the year ended 31 March 2014. Gross written premium has increased from £112,028,420 to £125,578,468 (12%). Underwriting profit (after operating expenses) has decreased from £11,325,139 to £7,863,658 (-31%) principally due to a decrease in ATE lines.

Changes to the After The Event (‘ATE’) insurance market following the introduction of the changes recommended in the Jackson Review (‘LASPO’), the Company has experienced a decrease in its gross written premium on ATE business of 71% to £15,721,237 (2013: £54,292,700). Although ATE business suffered a predicted decline following the LASPO changes, the General Insurance lines have seen large increases of 90% to £109,857,231 (2013: £57,735,720).

As at 31 March 2014, the Company’s cash and cash equivalents were £56,203,330 (2013: £26,998,830); gearing at both year ends was £nil. Net assets as at 31 March 2014 were £33,542,888 (2013: 27,215,480).

The Company’s investment policy continues to be conservative. With the exception of 3% of net assets held in property and intangibles, all investments are in cash or equivalent deposits with leading EU international clearing banks.

The Company has continued to increase its staffing resources, including senior appointments in the UK Branch, in finance, business development and underwriting. The Company has made significant progress in compliance with the requirements of Solvency II and expects to be fully compliant by the required date.

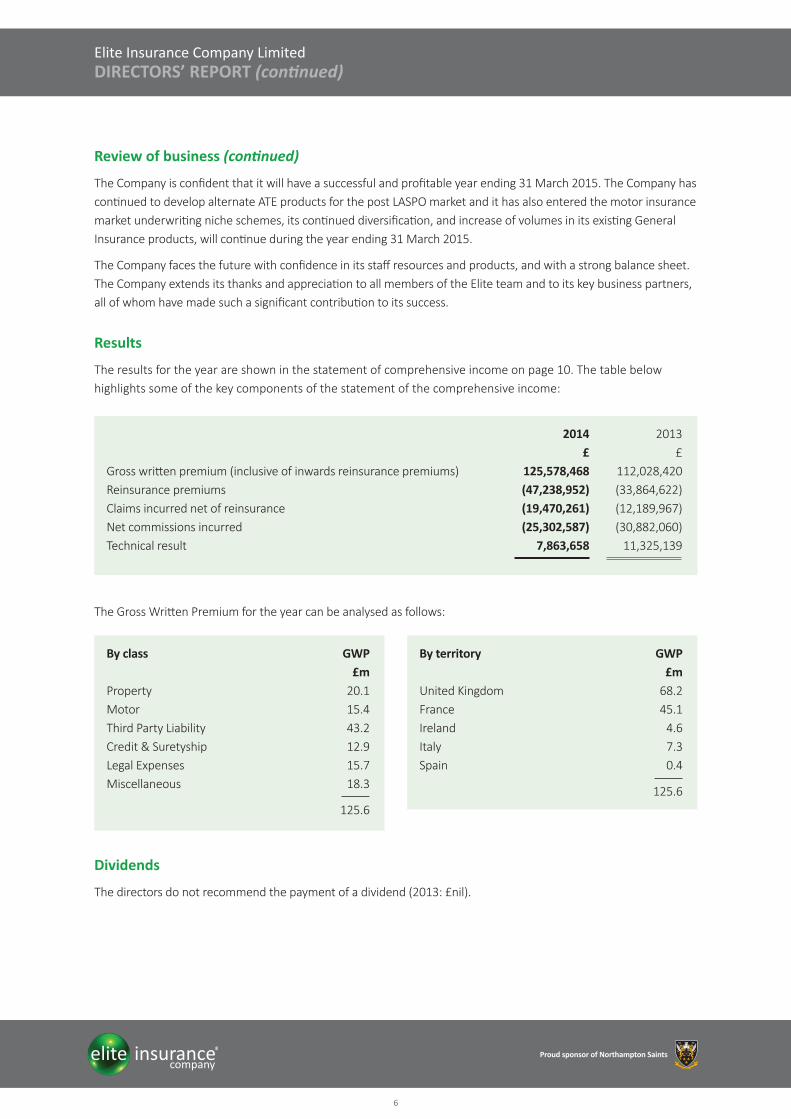

Review of business (continued)

The Company is confident that it will have a successful and profitable year ending 31 March 2015. The Company has continued to develop alternate ATE products for the post LASPO market and it has also entered the motor insurance market underwriting niche schemes, its continued diversification, and increase of volumes in its existing General Insurance products, will continue during the year ending 31 March 2015.

The Company faces the future with confidence in its staff resources and products, and with a strong balance sheet. The Company extends its thanks and appreciation to all members of the Elite team and to its key business partners, all of whom have made such a significant contribution to its success.

Results

The results for the year are shown in the statement of comprehensive income on page 10. The table below highlights some of the key components of the statement of the comprehensive income:

Dividends

The directors do not recommend the payment of a dividend (2013: £nil).

The Gross Written Premium for the year can be analysed as follows:

2014 2013 £ £Gross written premium (inclusive of inwards reinsurance premiums) 125,578,468 112,028,420Reinsurance premiums (47,238,952) (33,864,622)Claims incurred net of reinsurance (19,470,261) (12,189,967)Net commissions incurred (25,302,587) (30,882,060)Technical result 7,863,658 11,325,139

By class GWP £mProperty 20.1Motor 15.4Third Party Liability 43.2Credit & Suretyship 12.9Legal Expenses 15.7Miscellaneous 18.3

125.6

By territory GWP £mUnited Kingdom 68.2France 45.1Ireland 4.6Italy 7.3Spain 0.4

125.6

Elite Insurance Company LimitedDIRECTORS’ REPORT (continued)

Proud sponsor of Northampton Saints

6

DirectorsThe directors of the Company during the year were as stated on page 4.

Statement of Directors’ responsibilities

Company law requires the directors to prepare financial statements for each financial year, which give a true and fair view of the state of affairs of the Company and of the profit or loss for that period. In preparing those financial statements, the directors are required to:

• select suitable accounting policies and then apply them consistently;• make judgements and estimates that are reasonable and prudent;• state whether applicable accounting standards have been followed, subject to any material departures

disclosed and explained in the financial statements; and• prepare the financial statements on the going concern basis unless it is inappropriate to presume that the

Company will continue in business.

The directors are responsible for keeping proper accounting records which disclose with reasonable accuracy at any time the financial position of the Company and to enable them to ensure that the financial statements comply with the Gibraltar Companies Act and the Insurance Companies (Accounts Directive) Regulations 1997. They are also responsible for safeguarding the assets of the Company and hence for taking reasonable steps for the prevention and detection of fraud and other irregularities.

The maintenance and integrity of the Company’s website is the responsibility of the directors. The directors’ responsibility extends to the ongoing integrity of the financial statements contained therein.

Auditors

The retiring auditors are EY Limited who are eligible for reappointment.

Elite Insurance Company LimitedDIRECTORS’ REPORT (continued)

Proud sponsor of Northampton Saints

7

DirectorDerek Meadus24 October 2014

DirectorIan Prescott

Independent Auditors’ report to the members of Elite Insurance Company Limited

Proud sponsor of Northampton Saints

8

Report on the Financial Statements

We have audited the financial statements of Elite Insurance Company Limited for the year ended 31 March 2014 which comprise the Statement of Comprehensive Income, the Balance Sheet, the Statement of Changes in Equity, the Cash Flow Statement and the related notes. These financial statements have been prepared under the accounting policies set out therein.

This report, including the opinion, has been prepared for and only for the company’s members as a body in accordance with Section 182 of the Companies Act and for no other purpose. We do not, in giving these opinions, accept or assume responsibility for any other purpose or to any other person to whom this report is shown or into whose hands it may come save where expressly agreed by our prior consent in writing.

Directors’ responsibilities for the financial statements

The directors are responsible for the preparation and true and fair presentation of these financial statements in accordance with applicable law in Gibraltar and International Financial Reporting Standards as adopted for use in the European Union. This responsibility includes designing, implementing and maintaining internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error; selecting and applying appropriate accounting policies; and making accounting estimates that are reasonable in the circumstances.

Auditors’ responsibilities

Our responsibility is to express an opinion on these financial statements based on our audit. We conducted our audit in accordance with International Standards on Auditing. Those standards require that we comply with ethical requirements and plan and perform the audit to obtain reasonable assurance whether the financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditors’ judgement, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity’s preparation and true and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of accounting estimates made by management, as well as evaluating the overall presentation of the financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.

Independent Auditors’ report to the members of Elite Insurance Company Limited (continued)

Proud sponsor of Northampton Saints

9

Opinion

In our opinion, the financial statements:

• give a true and fair view, in accordance with International Financial Reporting Standards as adopted for use in the European Union, of the state of the Company’s affairs as at 31 March 2014 and of the Company’s profit and cash flows for the year then ended; and

• have been properly prepared in accordance with the Gibraltar Companies Act and the Insurance Companies (Accounts Directive) Regulations 1997 and other applicable legislation.

Opinion on other matter prescribed by the Companies Act

In our opinion the information given in the Directors’ Report for the financial year for which the financial statements are prepared is consistent with the financial statements.

Matters on which we are required to report by exception

We have nothing to report in respect of the following matters where the Companies Act requires us to report to you if, in our opinion:

• the company has not kept proper accounting records; or

• if information specified by law regarding directors’ remuneration and other transactions is not disclosed; or we have not received all the information and explanations we require for our audit.

Jose Julio Pisharello Statutory auditor for and on behalf of

EY LIMITED Registered auditors

Chartered Accountants Regal House Queensway Gibraltar

24 October 2014

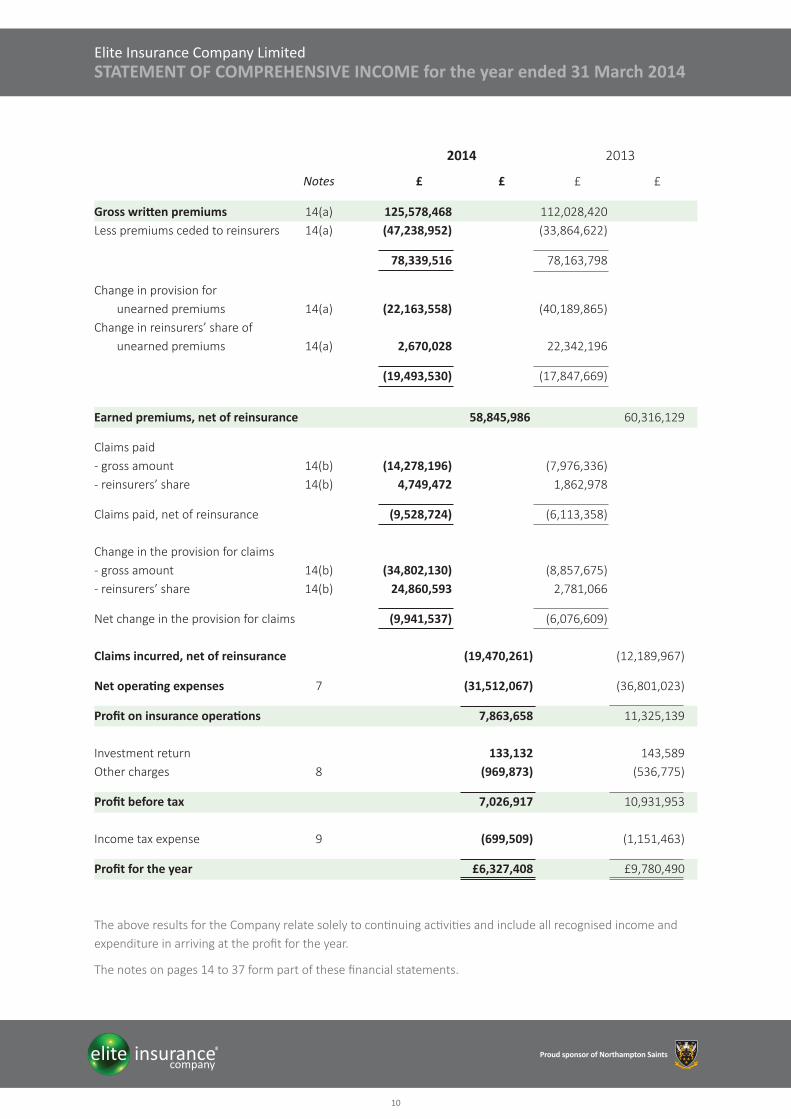

2014 2013 Notes £ £ £ £

Gross written premiums 14(a) 125,578,468 112,028,420Less premiums ceded to reinsurers 14(a) (47,238,952) (33,864,622)

78,339,516 78,163,798

Change in provision for unearned premiums 14(a) (22,163,558) (40,189,865)

Change in reinsurers’ share of unearned premiums 14(a) 2,670,028 22,342,196

(19,493,530) (17,847,669)

Earned premiums, net of reinsurance 58,845,986 60,316,129

Claims paid- gross amount 14(b) (14,278,196) (7,976,336)- reinsurers’ share 14(b) 4,749,472 1,862,978

Claims paid, net of reinsurance (9,528,724) (6,113,358) Change in the provision for claims- gross amount 14(b) (34,802,130) (8,857,675)- reinsurers’ share 14(b) 24,860,593 2,781,066

Net change in the provision for claims (9,941,537) (6,076,609) Claims incurred, net of reinsurance (19,470,261) (12,189,967)

Net operating expenses 7 (31,512,067) (36,801,023)

Profit on insurance operations 7,863,658 11,325,139

Investment return 133,132 143,589Other charges 8 (969,873) (536,775)

Profit before tax 7,026,917 10,931,953

Income tax expense 9 (699,509) (1,151,463)

Profit for the year £6,327,408 £9,780,490

The above results for the Company relate solely to continuing activities and include all recognised income and expenditure in arriving at the profit for the year.

The notes on pages 14 to 37 form part of these financial statements.

Elite Insurance Company LimitedSTATEMENT OF COMPREHENSIVE INCOME for the year ended 31 March 2014

Proud sponsor of Northampton Saints

10

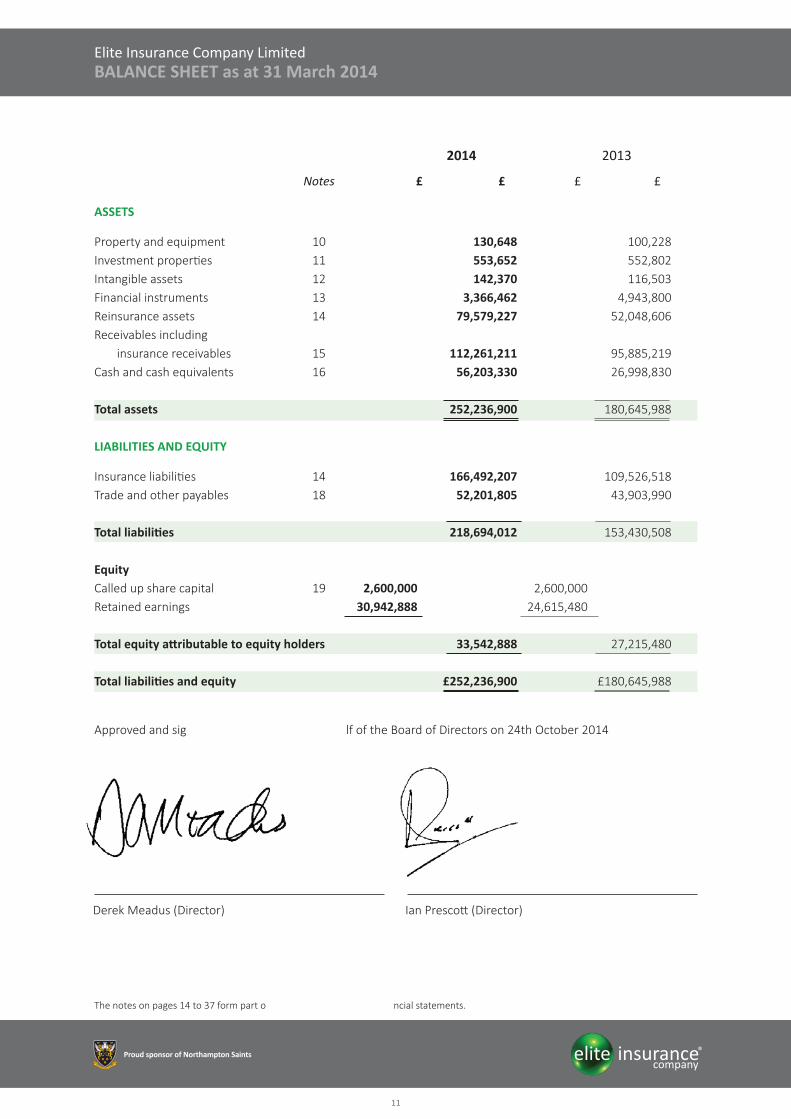

2014 2013 Notes £ £ £ £

ASSETS

Property and equipment 10 130,648 100,228Investment properties 11 553,652 552,802Intangible assets 12 142,370 116,503Financial instruments 13 3,366,462 4,943,800Reinsurance assets 14 79,579,227 52,048,606 Receivables including

insurance receivables 15 112,261,211 95,885,219Cash and cash equivalents 16 56,203,330 26,998,830 Total assets 252,236,900 180,645,988 LIABILITIES AND EQUITY

Insurance liabilities 14 166,492,207 109,526,518Trade and other payables 18 52,201,805 43,903,990 Total liabilities 218,694,012 153,430,508

EquityCalled up share capital 19 2,600,000 2,600,000Retained earnings 30,942,888 24,615,480 Total equity attributable to equity holders 33,542,888 27,215,480

Total liabilities and equity £252,236,900 £180,645,988

Approved and signed on behalf of the Board of Directors on 24th October 2014.

The notes on pages 14 to 37 form part of these financial statements.

Derek Meadus (Director) Ian Prescott (Director)

Elite Insurance Company LimitedBALANCE SHEET as at 31 March 2014

Proud sponsor of Northampton Saints

11

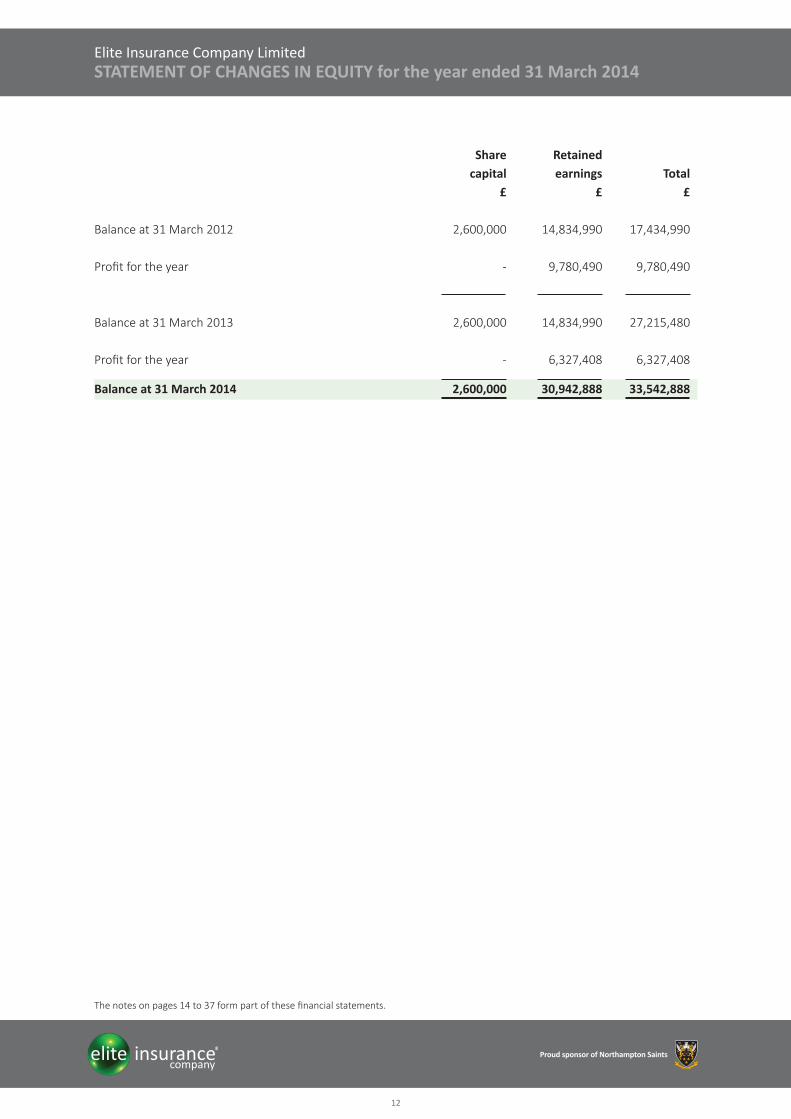

Share Retained capital earnings Total £ £ £ Balance at 31 March 2012 2,600,000 14,834,990 17,434,990

Profit for the year - 9,780,490 9,780,490 Balance at 31 March 2013 2,600,000 14,834,990 27,215,480 Profit for the year - 6,327,408 6,327,408

Balance at 31 March 2014 2,600,000 30,942,888 33,542,888

The notes on pages 14 to 37 form part of these financial statements.

Elite Insurance Company LimitedSTATEMENT OF CHANGES IN EQUITY for the year ended 31 March 2014

Proud sponsor of Northampton Saints

12

The notes on pages 14 to 37 form part of these financial statements.

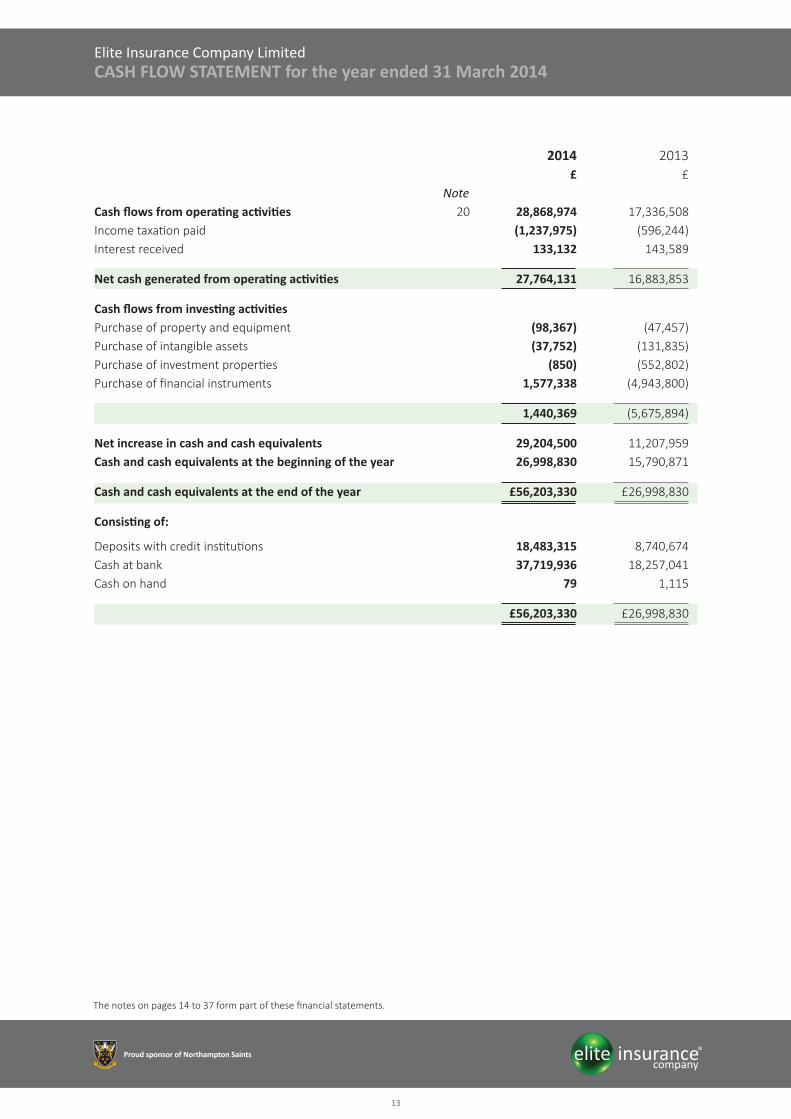

2014 2013 £ £ Note Cash flows from operating activities 20 28,868,974 17,336,508Income taxation paid (1,237,975) (596,244)Interest received 133,132 143,589

Net cash generated from operating activities 27,764,131 16,883,853

Cash flows from investing activitiesPurchase of property and equipment (98,367) (47,457)Purchase of intangible assets (37,752) (131,835)Purchase of investment properties (850) (552,802)Purchase of financial instruments 1,577,338 (4,943,800)

1,440,369 (5,675,894)

Net increase in cash and cash equivalents 29,204,500 11,207,959Cash and cash equivalents at the beginning of the year 26,998,830 15,790,871

Cash and cash equivalents at the end of the year £56,203,330 £26,998,830

Consisting of:

Deposits with credit institutions 18,483,315 8,740,674Cash at bank 37,719,936 18,257,041Cash on hand 79 1,115

£56,203,330 £26,998,830

Elite Insurance Company LimitedCASH FLOW STATEMENT for the year ended 31 March 2014

Proud sponsor of Northampton Saints

13

1. Significant accounting policies

The following accounting policies have been consistently applied in dealing with items which are considered material in relation to the Company’s financial statements.

Basis of accounting

These financial statements are prepared in accordance with International Financial Reporting Standards (“IFRS”) as defined by International Accounting Standards (“IAS”) 1, Presentation of Financial Statements. IFRS comprises standards issued by the International Accounting Standards Board (“IASB”) and interpretations issued by the International Financial Reporting Interpretations Committee (“IFRIC”) and as adopted by the European Union.

The financial statements have been prepared under the historical cost convention.

The preparation of financial statements in conformity with IFRS requires the use of certain critical accounting estimates. It also requires management to exercise its judgement in the process of applying accounting policies. The areas involving a higher degree of judgement or complexity, or areas where assumptions and estimates are significant to the financial statements are disclosed in Note 2.

New Accounting PronouncementsThere were no new standards or interpretations issued by the IASB or the IFRIC that were adopted by the Company in the current financial year that had a significant impact on its results or financial position.

There are a number of accounting and reporting changes issued under IFRS, including those still under development by the IASB, for years beginning on or after 1 January 2014 and subsequently.

The Company is currently assessing the impact on its financial statements of amendments related to the following pronouncements:

- IFRS 4, Insurance contracts - the final standard is not expected to be effective until at least 2015.

- IFRS 9, Financial Instruments - the standard is effective for annual periods beginning on or after 1 January 2015.

The following pronouncements do not have a significant impact on the Company’s financial statements.

- Amendments to IAS 32, Financial Instruments: Presentation - the amendments to IAS 32 are effective for periods beginning on or after 1 January 2013 and 1 January 2014 respectively.

- Amendments to IFRS 7, Financial Instruments: Disclosure - amendments become effective for annual periods beginning on or after 1 January 2013 and 1 January 2015 respectively.

- IAS 36, Impairment of Assets - amendments become effective for annual periods beginning on or after 1 January 2014.

- IAS 39, Financial Instruments: Recognition and Measurement - amendments become effective for annual periods beginning on or after 1 January 2014.

Elite Insurance Company LimitedNOTES TO THE FINANCIAL STATEMENTS

Proud sponsor of Northampton Saints

14

1. Significant accounting policies (continued)

Product classification

Insurance contracts are those contracts that transfer significant insurance risk at the inception of the contract. Insurance risk is transferred when an insurer agrees to compensate a policyholder if a specified uncertain future event adversely affects the policyholder. The significance of insurance risk is dependent on both the probability of an insured event and the magnitude of its potential effect. Once a contract has been classified as an insurance contract, it remains an insurance contract for the remainder of its lifetime, even if the insurance risk reduces significantly during this period.

All policies issued by the Company have been regarded as insurance contracts and have been accounted for in accordance with IFRS 4. The Company however entered into reinsurance arrangements whereby there was not a significant transfer of risk and so these have not been accounted for in accordance with IFRS 4.

Estimates and assumptions

Certain amounts recorded in the financial information include estimates and assumptions made by management, particularly about insurance liability reserves and other factors. Actual results may differ from the estimates made. For further information on the use of estimates and judgments, refer to Note 2.

Premiums

Premiums written are recorded from the inception date of the policy to which they relate. Premiums are disclosed gross of commission payable to intermediaries and exclude taxes based on premiums. Premiums written in the year are stated net of cancellations in respect of premiums incepted in prior periods and include a provision for expected cancellations on business incepting during the financial year.

Premiums are payable on inception of the policy other than for deferred policies where payment is due when the claim has been settled. The majority of legal expense business written by the Company is on a deferred premium basis where the premium is only received on the satisfactory settlement of cases. If the case fails, the amounts due from policyholders is written off as part of the claims cost.

Reinsurance

Contracts entered into by the Company with reinsurers under which the Company is compensated for losses on one or more contracts issued by the Company and that meet the classification requirements for insurance contracts are classified as reinsurance contracts held. Contracts that do not meet these classification requirements are classified as financial assets.

The benefits to which the Company is entitled under its reinsurance contracts held are recognised as reinsurance assets. These assets consist of short-term balances due from reinsurers, as well as longer term receivables that are dependent on the expected claims and benefits arising under the related reinsured insurance contracts. Amounts recoverable from or due to reinsurers are measured consistently with the amounts associated with the reinsured insurance contracts and in accordance with the terms of each reinsurance contract. Reinsurance liabilities are primarily premiums payable for reinsurance contracts and are recognised as an expense when due. The Company assesses its reinsurance assets for impairment on an ongoing basis.

Elite Insurance Company LimitedNOTES TO THE FINANCIAL STATEMENTS

Proud sponsor of Northampton Saints

15

1. Significant accounting policies (continued)

Unearned premiums reserve

The unearned premiums reserve comprises the proportion of gross premiums written which is to be earned in the following or subsequent financial years.

For policies with a defined period of insurance, the unearned premiums reserve is calculated by apportioning premiums over the period to which they relate on a pro rata basis adjusted to take account of the incidence of risk. In instances where the period of insurance is not finite, premiums are fully earned on the date of inception of the policy and an appropriate loss reserve is immediately created.

Investment return

Investment return comprises of interest income. Interest income is recognised using the effective interest method.

Claims incurred

Claims incurred comprise claims paid during the financial year together with the movement in the provision for outstanding claims, including claims incurred but not reported (“IBNR”). Claims paid include premiums written off on failed cases arising on legal expense business. Reinsurance recoveries are accounted for in the same accounting period as the claims for the related business being reinsured (see Note 2).

Acquisition costs and deferred acquisition costs

Acquisition costs comprise brokerage incurred on insurance contracts written during the financial year and are earned to match the related premiums.

Foreign currencies

(i) Functional and presentation currencyItems included in the financial statements are measured using the currency of the primary economic environment in which the entity operates (“the functional currency”). The Company’s financial statements are presented in Sterling, which is the Company’s presentation currency.

(ii) Transactions and balancesForeign currency transactions are translated into the functional currency using the exchange rates prevailing at the dates of the transactions. Foreign exchange gains and losses resulting from the settlement of such transactions and from the translation at year-end exchange rates of monetary assets and liabilities denominated in foreign currencies are recognised in the profit and loss account.

Post-retirement employee benefits

The Company operates a defined contribution stakeholder pension scheme and several other defined contribution schemes. It also makes payments into a number of personal money purchase pension plans. Contributions in respect of these schemes are charged to the statement of comprehensive income in the period to which they relate.

Elite Insurance Company LimitedNOTES TO THE FINANCIAL STATEMENTS

Proud sponsor of Northampton Saints

16

1. Significant accounting policies (continued)

Intangible assets - Computer software

Acquired computer software licences are capitalised on the basis of the costs incurred to acquire and bring into use the specific software. All computer software costs are treated as intangible finite life assets and amortised on a straight-line basis over their expected useful lives not exceeding a period of three years.

Property and equipment

Property and equipment are carried at cost, less accumulated depreciation and any impairment in value. Depreciation is calculated so as to write-off the cost over their estimated useful economic lives on a straight-line basis having regard to the residual value of each asset, as follows:

- Fixtures, fittings, tools and equipment - 33% per annum

The assets’ residual values, useful lives and method of depreciation are reviewed at each balance sheet date and adjusted if appropriate. An item of property and equipment is derecognised upon disposal or when no future economic benefits are expected to arise from the continued use of the asset. Gains and losses on the disposal of property and equipment are determined by comparing proceeds with the carrying amount of the asset and are included in the statement of comprehensive income. Costs for repairs and maintenance are expensed as incurred.

Investment properties

Investment properties are properties held to earn rentals and/or for capital appreciation (including property under construction for such purposes). Investment properties are measured initially at cost, including transaction costs. Subsequent to initial recognition, investment properties are measured at fair value. Gains and losses arising from changes in the fair value of investment properties are included in profit or loss in the period in which they arise.

An investment property is derecognised upon disposal or when the investment property is permanently withdrawn from use and no future economic benefits are expected from the disposal. Any gain or loss arising from derecognition of the property (calculated as the difference between the net disposal proceeds and the carrying amount of the asset) is included in profit or loss in the period in which the property is derecognised.

Financial instruments

Financial instruments include fixed term cash deposits with maturity of more than three months but less than six months at the date of placement or acquisition, free of encumbrances.

Cash and cash equivalents

Cash and cash equivalents include cash and short term deposits held with credit institutions and other short-term highly liquid investments with a maturity of three months or less at the date of placement or acquisition, free of encumbrances.

Elite Insurance Company LimitedNOTES TO THE FINANCIAL STATEMENTS

Proud sponsor of Northampton Saints

17

1. Significant accounting policies (continued)

Segmental reporting

A business segment is a group of assets and operations engaged in providing products or services that are subject to risks and returns that are different from those of other business segments. A geographical segment is engaged in providing products or services within a particular economic environment that are subject to risks and returns that are different from those of segments operating in other economic environments.

Trade and other receivables

Trade and other receivables are financial assets with fixed or determinable payments. Trade and other receivables are measured at amortised cost, using the effective interest method, less provision for impairment and provision for expected cancelations. A provision for impairment or cancelation of trade receivables is established when there is objective evidence that the Company will not be able to collect all amounts due according to their original terms. The provision for expected cancellations is established by reference to historic cancellation experience. Receivables arising from insurance and reinsurance contracts are also classified in this category and are reviewed for impairment as part of the impairment review of trade and other receivables.

Trade receivables arising from insurance contracts are stated net of commission payable as there is an implicit right of set off. Insurance contracts issued on a deferred premium basis will only become due and receivable once the claim is settled.

Share capital

Shares are classified as equity when there is no obligation to transfer cash or other assets. Incremental costs directly attributable to the issue of equity instruments are shown in equity as deduction from the proceeds.

Related party transactions

Related party relationships exist when one party has the ability to control, directly, or indirectly through one or more of the intermediaries, the other party or exercise significant influence over the other party in making financial and operating decisions. Such relationships also exist between and/or among entities which are under common control with the reporting enterprise, or between and/or among the reporting enterprise and its key management personnel, directors, or its shareholder. Transactions between related parties are accounted for at arms’ length prices or on terms similar to those offered to non-related entities in an economically comparable market.

Current taxation

Current taxation is provided for on the basis of tax rates and tax laws that have been enacted or substantially enacted at the year-end date.

Elite Insurance Company LimitedNOTES TO THE FINANCIAL STATEMENTS

Proud sponsor of Northampton Saints

18

1. Significant accounting policies (continued)

Deferred taxation

Deferred tax is recognised in respect of all significant timing differences that have originated but not reversed at the balance sheet date where transactions or events that result in an obligation to pay more tax in the future or a right to pay less tax in the future have occurred at the balance sheet date. Timing differences are differences between the Company’s taxable profits and its results as stated in the financial statements that arise from the inclusion of gains and losses in tax assessments in periods different from those in which they are recognised in the financial statements.

Deferred tax is measured at the average tax rates that are expected to apply in the periods in which timing differences are expected to reverse, based on tax rates and laws that have been enacted or substantially enacted by the balance sheet date. Deferred tax is measured on a non-discounted basis.

Elite Insurance Company LimitedNOTES TO THE FINANCIAL STATEMENTS

Proud sponsor of Northampton Saints

19

2. Critical accounting estimates and judgments in applying accounting policies

The Company makes estimates and assumptions that affect the reported amounts of assets and liabilities. Estimates and judgements are continually evaluated and based on historical experience and other factors, including expectations of future events that are believed to be reasonable under the circumstances.

The ultimate liability arising from claims made under insurance

This is the Company’s most critical accounting estimate which includes a significant level of uncertainty. Claims incurred include all losses occurring during the year, whether reported or not.

In instances where the period of insurance is not finite, premiums are fully earned on the date of inception of the policy and an appropriate loss reserve is created at that date. The majority of this business is written on a deferred premium basis where the premium is only received on the satisfactory settlement of cases. If the case fails, the amounts due from policyholders is written off as part of the claims cost.

The provision for claims outstanding is made on an individual basis and is based on the ultimate cost of all claims not settled by the balance sheet date. The provision comprises of the estimated cost of IBNR at the balance sheet date which is based on statistical methods.

The estimation of IBNR is generally subject to a greater degree of uncertainty than the estimation of the cost of settling claims already notified to the Company, where more information about the claim event is generally available.

Where the IBNR proportion of the total reserve is high (as is the case), this will typically display greater variations between the initial estimates and the final outcomes because of the greater degree of difficulty of estimating those reserves. In calculating the estimated cost of unpaid claims the Company uses a variety of estimation techniques, generally based upon statistical analyses of historic experience, which assumes that the development pattern of the current claims will be consistent with past experience.

Overall the objectives of the estimates and judgments applied to claims provisions seek to state such provisions on a best estimate, undiscounted basis.

In respect of the recoverability of amounts due from reinsurers, provisions for bad debts are made specifically, based on the solvency of reinsurers, payment experience with them and any disputes of which the Company is aware. The carrying value at the balance sheet date of outstanding claims (claim reserves and IBNR) and the amount of reinsurance recoveries estimated at the balance sheet date were as set out in Note 14 to the accounts.

Elite Insurance Company LimitedNOTES TO THE FINANCIAL STATEMENTS

Proud sponsor of Northampton Saints

20

3. Risk management policies

The Company’s activities expose the business to a number of key risks which have the potential to affect its ability to achieve its business objectives. The following describes the Company’s financial and insurance risk management from a qualitative perspective. The Board is responsible for the Company’s systems of internal control and for reviewing their effectiveness. The systems of internal control are designed to manage rather than eliminate risk and aim to provide reasonable and not absolute assurance. Investment risk is managed in accordance with investment frameworks which are set by the board.

Financial Risk

Credit risk

This is the risk that one party to a financial arrangement will fail to discharge an obligation and cause the other party to incur a financial loss. The following is an overview of how the Company manages its significant credit risk exposures.

• Reinsurance - Reinsurance is placed in line with policy guidelines and concentration of risk is managed by reference to counterparties’ limits that are set each year and are subject to regular reviews. On a regular basis management performs assessments of creditworthiness of reinsurers to update reinsurance purchase strategy and to ascertain suitable allowance for impairment of reinsurance assets.

• Financial instruments and cash and cash equivalents - Credit risk relating to financial instruments and cash and cash equivalents is monitored daily. The Company’s investment guidelines specify the maximum percentage of the portfolios that can be invested in or with any single counterparty.

• Insurance receivables - The majority of legal expense business written by the Company is on a deferred premium basis where the premium is only received on the satisfactory settlement of cases. If the case fails, the amounts due from policyholders is written off as part of the claims cost. The Company’s credit risk is in respect of balances with both customers and intermediaries. The Company seeks to reduce its credit exposure to intermediaries through its active credit control procedures. Wherever possible, the Company includes premium payment warranties in its terms and conditions which gives it the right to cancel policies in the event of non-payment.

Liquidity Risk

The Company has defined liquidity risk as ‘the risk that the Company, although solvent, either does not have available sufficient financial resources to enable it to meet its obligations as they fall due, or can secure them only at excessive cost’. The major liquidity risk confronting the Company is the daily calls on its available cash resources in respect of claims arising from insurance contracts.

The Company manages this risk by maintaining sufficient liquid assets or assets that can be translated into liquid assets at short notice and without capital loss to meet the expected cash flow requirements.

A significant part of the total assets of the Company are in the form of deferred premium trade receivables that are not all expected to be received in the short term as there is no certainty as to when the underlying business will settle. Similarly, as at the year end commissions payable and reinsurance premiums that arise from the issuance of the insurance premiums, will not be due and payable until the respective deferred premiums have been received.

Elite Insurance Company LimitedNOTES TO THE FINANCIAL STATEMENTS

Proud sponsor of Northampton Saints

21

3. Risk management policies (continued)

Liquidity Risk (continued)

The nature of insurance is that the requirements of funding cannot be predicted with absolute certainty as the theory of probability is applied on insurance contracts to ascertain the likely provision and the time period when such liabilities will require settlement. The amounts and maturities in respect of insurance liabilities are thus based on management’s best estimate based on statistical techniques and past experience.

Market Risk

Market risk is the risk that the fair value or future cash flows of a financial instrument will fluctuate because of changes in market prices. Market risk comprises three types of risk: currency risk, interest rate risk and price risk.

• Market risk can be caused by factors specific to the individual instrument or its issuer or factors affecting all instruments traded in the market.

• Currency risk is mitigated by the Company mainly maintaining financial assets denominated in the same currencies as its liabilities which are principally in sterling.

• Interest rate risk is the risk that the value and future cash flows of a financial instrument will fluctuate because of changes in interest rates.

• Price risk is the risk that the value of investments decreases due to market factors. In order to manage interest rate and price risk the Company currently only invests in short term cash deposits.

Capital risk management

The Board is responsible for reviewing the capital structure on a regular basis such that the Company maximises the return to stakeholders through the optimisation of the debt and equity balance.

The Company is regulated by the Financial Services Commission (“FSC”) in Gibraltar which requires the Company to maintain the Required Minimum Margin (“RMM”) of solvency. The RMM, which takes into account the premiums written and outstanding reserves on a class of business basis, seeks to ensure that the Company has at least the minimum amount and type of capital to meet future expected claims obligations. The Company holds capital in excess of the FSC requirements in order to maintain a strong solvency position. All externally imposed capital requirements have been complied with during the year.

The Company is fully aware of current proposals for Solvency II which is expected to be implemented on 1st January 2016. The Company has embedded its capital management processes into its normal planning, reporting and decision making activities. The capital consequences of business developments at Company and class of business level are monitored regularly.

Elite Insurance Company LimitedNOTES TO THE FINANCIAL STATEMENTS

Proud sponsor of Northampton Saints

22

3. Risk management policies (continued)

Insurance risk

(i) Introduction

The risk under any one insurance contract is the possibility that the insured event occurs and the claim results. By the very nature of an insurance contract, risk is based on fortuity and is therefore unpredictable. The principal risks that the Company faces under its insurance contracts are that the business will be under-priced and/or under-reserved. Experience shows that the larger the portfolio of similar insurance contracts, the smaller the relative variability about the expected outcome will be. In addition, a more diversified portfolio is less likely to be affected across the board by a change in any subset of the portfolio.

The Company has developed its insurance underwriting strategy to diversify the type of insurance risks accepted to achieve a sufficiently large population of risks to reduce the variability of the expected outcome. The Company has developed underwriting guidelines, limits of authority and business plans which are binding upon all staff authorised to underwrite. These are detailed and specific to underwriters and classes of business as well as establishing more general principles and conditions.

(ii) Concentrations of risk

The Company underwrites contracts of insurance which cover risks located in the United Kingdom and other EU territories.

(iii) Reinsurance

The Company purchases reinsurance to limit its exposure to individual risks and aggregation of risks arising from individual large claims. The types of reinsurance purchased are as follows:

- Facultative reinsurance purchased to provide protection from specific claims.- Surplus treaty reinsurance purchased to provide protection from the aggregation of claims. - Quota Share treaty reinsurance purchased to provide protection against claims arising either from

individual large claims or aggregations.

In addition the Company participates in Excess of Loss treaties which are in effect on its reinsurance inwards business. The Company’s reinsurance strategy and all reinsurance contracts are approved by the Board.

Pricing Risk

In respect of Rate Based Legal Expense business, Elite Business Development Limited (“EBD”), an FSA regulated insurance intermediary, provides an individual risk assessment taking due concern of the specific risk, based on past experience and current market practice and provides a proposed pricing which is reviewed by a director of the Company before binding it in Gibraltar. Other risks may not require individual risk assessment and are bound under scheme rates agreed in advance by Company Directors.

Reserving Risk

Risk reserving is initially performed using past loss experience. The underwriting committee then reviews large unusual risks and sets individual loss reserves for these specific cases. The Directors review the reserves of the Company at each Board meeting and consider whether they are sufficient to secure the ongoing security of the Company.

Elite Insurance Company LimitedNOTES TO THE FINANCIAL STATEMENTS

Proud sponsor of Northampton Saints

23

Elite Insurance Company LimitedNOTES TO THE FINANCIAL STATEMENTS

Proud sponsor of Northampton Saints

24

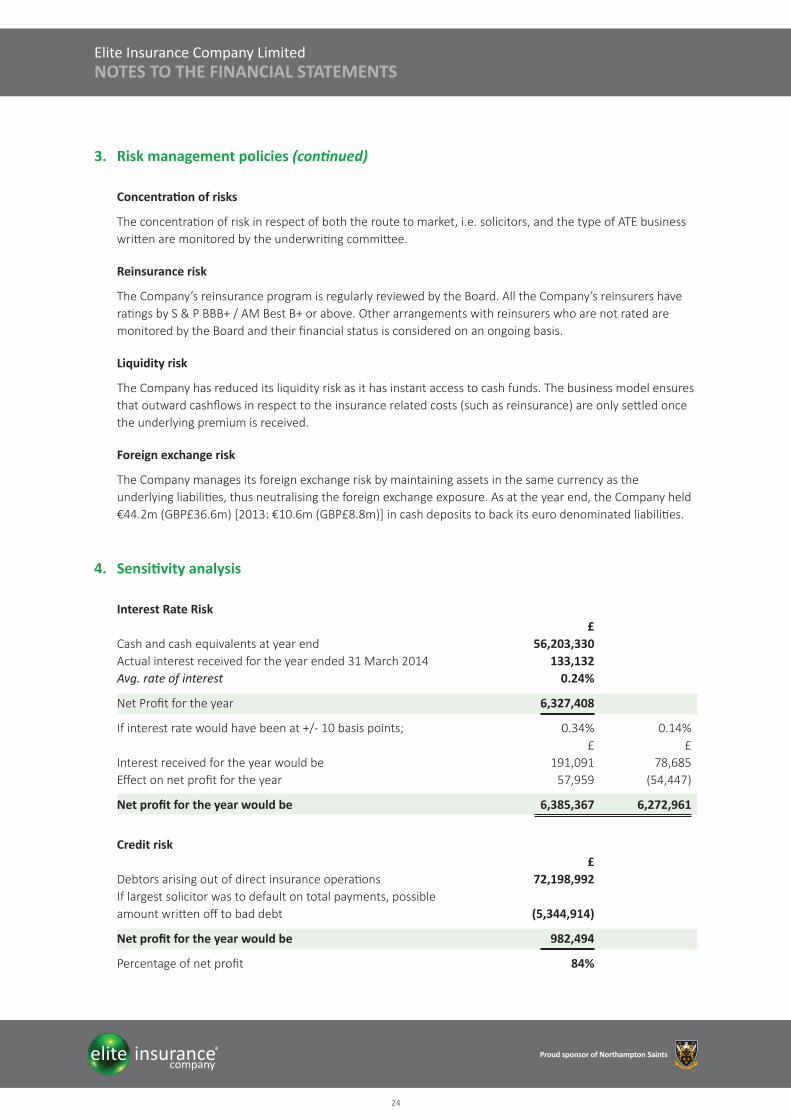

3. Risk management policies (continued)

Concentration of risks

The concentration of risk in respect of both the route to market, i.e. solicitors, and the type of ATE business written are monitored by the underwriting committee.

Reinsurance risk

The Company’s reinsurance program is regularly reviewed by the Board. All the Company’s reinsurers have ratings by S & P BBB+ / AM Best B+ or above. Other arrangements with reinsurers who are not rated are monitored by the Board and their financial status is considered on an ongoing basis.

Liquidity risk

The Company has reduced its liquidity risk as it has instant access to cash funds. The business model ensures that outward cashflows in respect to the insurance related costs (such as reinsurance) are only settled once the underlying premium is received.

Foreign exchange risk

The Company manages its foreign exchange risk by maintaining assets in the same currency as the underlying liabilities, thus neutralising the foreign exchange exposure. As at the year end, the Company held €44.2m (GBP£36.6m) [2013: €10.6m (GBP£8.8m)] in cash deposits to back its euro denominated liabilities.

4. Sensitivity analysis

Interest Rate Risk £Cash and cash equivalents at year end 56,203,330 Actual interest received for the year ended 31 March 2014 133,132 Avg. rate of interest 0.24%

Net Profit for the year 6,327,408

If interest rate would have been at +/- 10 basis points; 0.34% 0.14% £ £Interest received for the year would be 191,091 78,685Effect on net profit for the year 57,959 (54,447)

Net profit for the year would be 6,385,367 6,272,961

Credit risk £Debtors arising out of direct insurance operations 72,198,992If largest solicitor was to default on total payments, possible amount written off to bad debt (5,344,914)

Net profit for the year would be 982,494

Percentage of net profit 84%

Elite Insurance Company LimitedNOTES TO THE FINANCIAL STATEMENTS

Proud sponsor of Northampton Saints

25

The Company is insulated against fluctuations in the underlying reserves, on a net basis, primarily through the purchase of adequate reinsurance.

For the purpose of sensitivity analysis and based on the unlikely assumption that net ultimate claims, inception to date, were revised upwards by 20% from present levels management would estimate that the reduction in retained profit for the year would be approximately £13,200k.

2009 Ultimate gross claims and prior 2010 2011 2012 2013 2014 Total £000s £000s £000s £000s £000s £000s £000s

At end of the accident year 6,430 3,731 5,618 12,820 17,673 56,227 One year later 9,188 4,348 5,562 9,956 18,364 Two years later 9,791 5,473 6,691 6,827 Three years later 11,737 5,660 3,986 Four years later 13,359 5,623 Five years later 11,598 Six years and older 6,657 Cumulative claims incurred 11,390 5,623 3,986 6,827 18,364 56,227 102,417Claims paid (9,816) (4,605) (2,948) (4,211) (5,914) (8,677) (36,171)

Gross claims outstanding 1,574 1,018 1,038 2,616 12,450 47,550 66,246

Gross earned premiums 42,987 24,489 29,775 47,081 73,886 114,323 332,541

Claims incurred ratio % 26.5% 23.0% 13.4% 14.5% 24.9% 49.2% 30.8%

2009Ultimate net claims and prior 2010 2011 2012 2013 2014 Total £000s £000s £000s £000s £000s £000s £000s

At end of the accident year 4,449 2,058 3,968 11,036 14,171 27,878 One year later 5,892 2,495 3,976 8,215 12,305 Two years later 6,334 3,181 4,329 5,165 Three years later 7,710 3,309 2,195 Four years later 8,627 3,230 Five years later 7,505 Six years and older 4,852 Cumulative claims incurred 7,378 3,230 2,195 5,165 12,305 27,878 58,151Claims paid (6,474) (2,450) (1,346) (3,205) (4,152) (7,260) (24,887)

Net claims outstanding 904 780 849 1,960 8,153 20,618 33,264

Net earned premiums 36,759 19,689 26,017 41,969 62,120 69,425 255,979

Claims incurred ratio % 20.1% 16.4% 8.4% 12.3% 19.8% 40.2% 22.7%

5. Claims development and sensitivity analysis

Elite Insurance Company LimitedNOTES TO THE FINANCIAL STATEMENTS

Proud sponsor of Northampton Saints

26

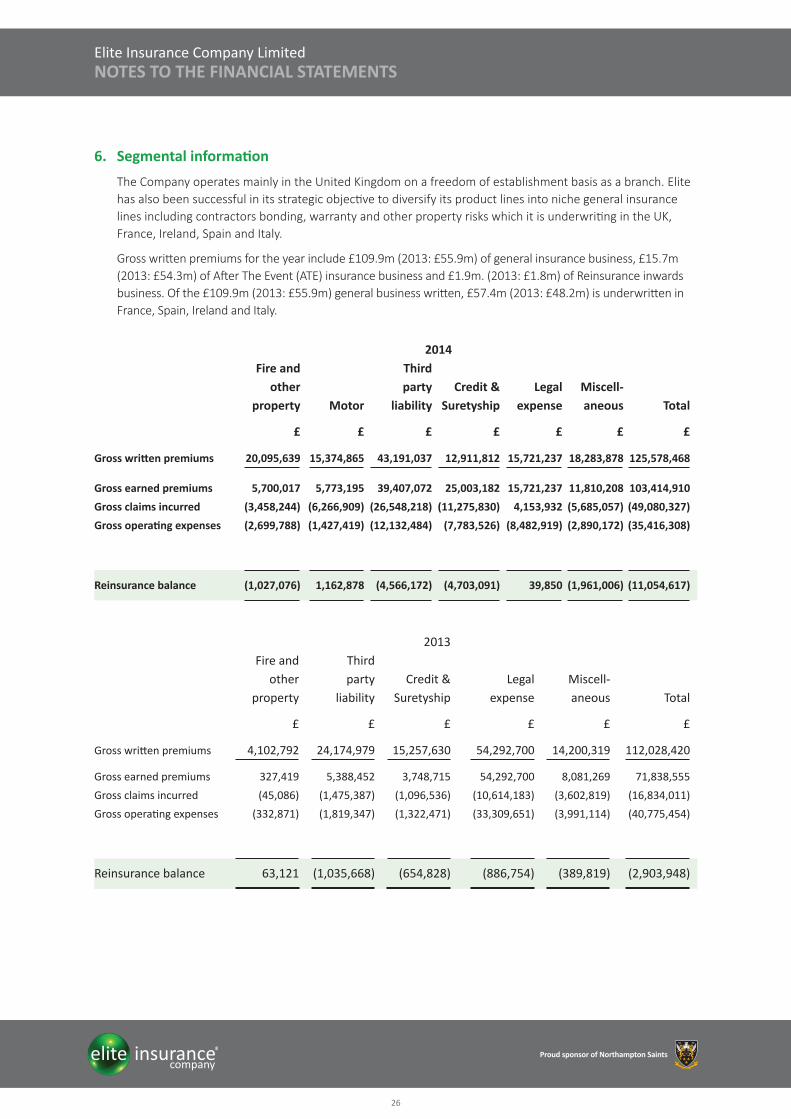

6. Segmental information

The Company operates mainly in the United Kingdom on a freedom of establishment basis as a branch. Elite has also been successful in its strategic objective to diversify its product lines into niche general insurance lines including contractors bonding, warranty and other property risks which it is underwriting in the UK, France, Ireland, Spain and Italy.

Gross written premiums for the year include £109.9m (2013: £55.9m) of general insurance business, £15.7m (2013: £54.3m) of After The Event (ATE) insurance business and £1.9m. (2013: £1.8m) of Reinsurance inwards business. Of the £109.9m (2013: £55.9m) general business written, £57.4m (2013: £48.2m) is underwritten in France, Spain, Ireland and Italy.

2013 Fire and Third other party Credit & Legal Miscell- property liability Suretyship expense aneous Total

£ £ £ £ £ £

Gross written premiums 4,102,792 24,174,979 15,257,630 54,292,700 14,200,319 112,028,420

Gross earned premiums 327,419 5,388,452 3,748,715 54,292,700 8,081,269 71,838,555

Gross claims incurred (45,086) (1,475,387) (1,096,536) (10,614,183) (3,602,819) (16,834,011)

Gross operating expenses (332,871) (1,819,347) (1,322,471) (33,309,651) (3,991,114) (40,775,454)

Reinsurance balance 63,121 (1,035,668) (654,828) (886,754) (389,819) (2,903,948)

2014 Fire and Third other party Credit & Legal Miscell- property Motor liability Suretyship expense aneous Total

£ £ £ £ £ £ £

Gross written premiums 20,095,639 15,374,865 43,191,037 12,911,812 15,721,237 18,283,878 125,578,468

Gross earned premiums 5,700,017 5,773,195 39,407,072 25,003,182 15,721,237 11,810,208 103,414,910

Gross claims incurred (3,458,244) (6,266,909) (26,548,218) (11,275,830) 4,153,932 (5,685,057) (49,080,327)

Gross operating expenses (2,699,788) (1,427,419) (12,132,484) (7,783,526) (8,482,919) (2,890,172) (35,416,308)

Reinsurance balance (1,027,076) 1,162,878 (4,566,172) (4,703,091) 39,850 (1,961,006) (11,054,617)

Elite Insurance Company LimitedNOTES TO THE FINANCIAL STATEMENTS

Proud sponsor of Northampton Saints

27

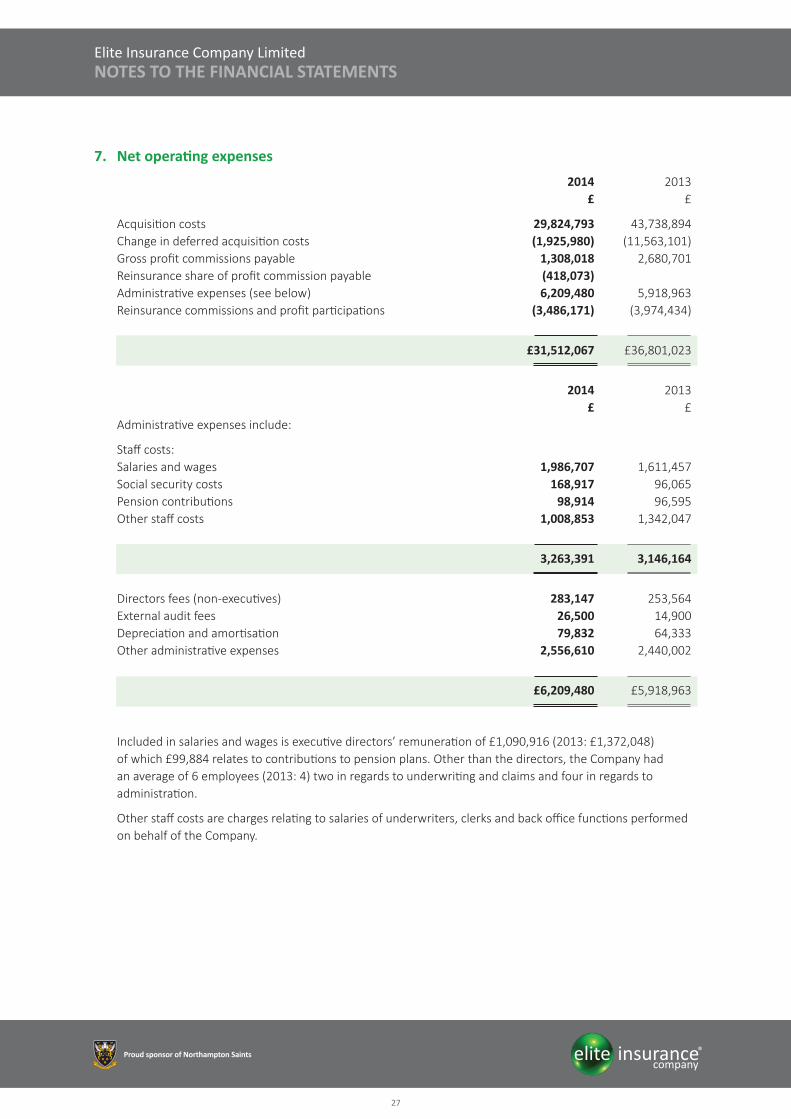

7. Net operating expenses

2014 2013 £ £

Acquisition costs 29,824,793 43,738,894Change in deferred acquisition costs (1,925,980) (11,563,101)Gross profit commissions payable 1,308,018 2,680,701Reinsurance share of profit commission payable (418,073)Administrative expenses (see below) 6,209,480 5,918,963Reinsurance commissions and profit participations (3,486,171) (3,974,434)

£31,512,067 £36,801,023

2014 2013 £ £Administrative expenses include:

Staff costs: Salaries and wages 1,986,707 1,611,457Social security costs 168,917 96,065Pension contributions 98,914 96,595Other staff costs 1,008,853 1,342,047

3,263,391 3,146,164

Directors fees (non-executives) 283,147 253,564External audit fees 26,500 14,900Depreciation and amortisation 79,832 64,333Other administrative expenses 2,556,610 2,440,002

£6,209,480 £5,918,963

Included in salaries and wages is executive directors’ remuneration of £1,090,916 (2013: £1,372,048) of which £99,884 relates to contributions to pension plans. Other than the directors, the Company had an average of 6 employees (2013: 4) two in regards to underwriting and claims and four in regards to administration.

Other staff costs are charges relating to salaries of underwriters, clerks and back office functions performed on behalf of the Company.

Elite Insurance Company LimitedNOTES TO THE FINANCIAL STATEMENTS

Proud sponsor of Northampton Saints

28

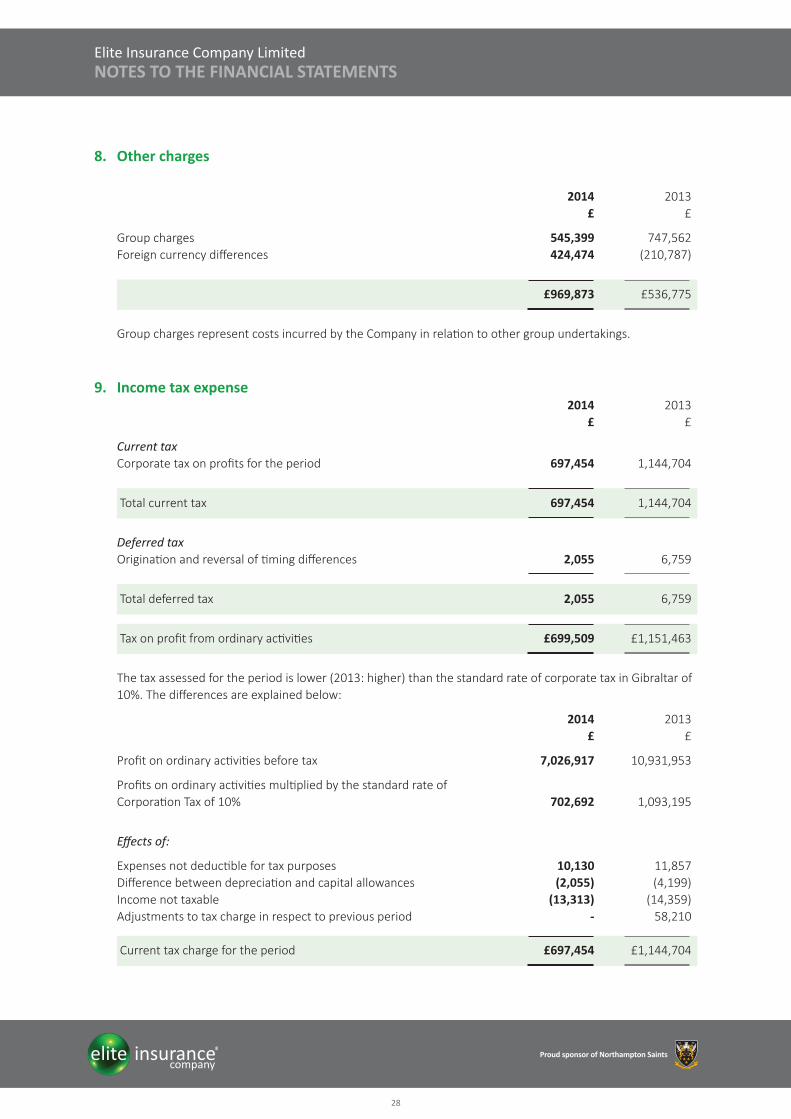

8. Other charges

2014 2013 £ £

Group charges 545,399 747,562Foreign currency differences 424,474 (210,787)

£969,873 £536,775

Group charges represent costs incurred by the Company in relation to other group undertakings.

9. Income tax expense 2014 2013 £ £

Current taxCorporate tax on profits for the period 697,454 1,144,704

Total current tax 697,454 1,144,704

Deferred tax Origination and reversal of timing differences 2,055 6,759

Total deferred tax 2,055 6,759

Tax on profit from ordinary activities £699,509 £1,151,463

The tax assessed for the period is lower (2013: higher) than the standard rate of corporate tax in Gibraltar of 10%. The differences are explained below:

2014 2013 £ £

Profit on ordinary activities before tax 7,026,917 10,931,953

Profits on ordinary activities multiplied by the standard rate of Corporation Tax of 10% 702,692 1,093,195

Effects of:

Expenses not deductible for tax purposes 10,130 11,857Difference between depreciation and capital allowances (2,055) (4,199)Income not taxable (13,313) (14,359)Adjustments to tax charge in respect to previous period - 58,210 Current tax charge for the period £697,454 £1,144,704

Elite Insurance Company LimitedNOTES TO THE FINANCIAL STATEMENTS

Proud sponsor of Northampton Saints

29

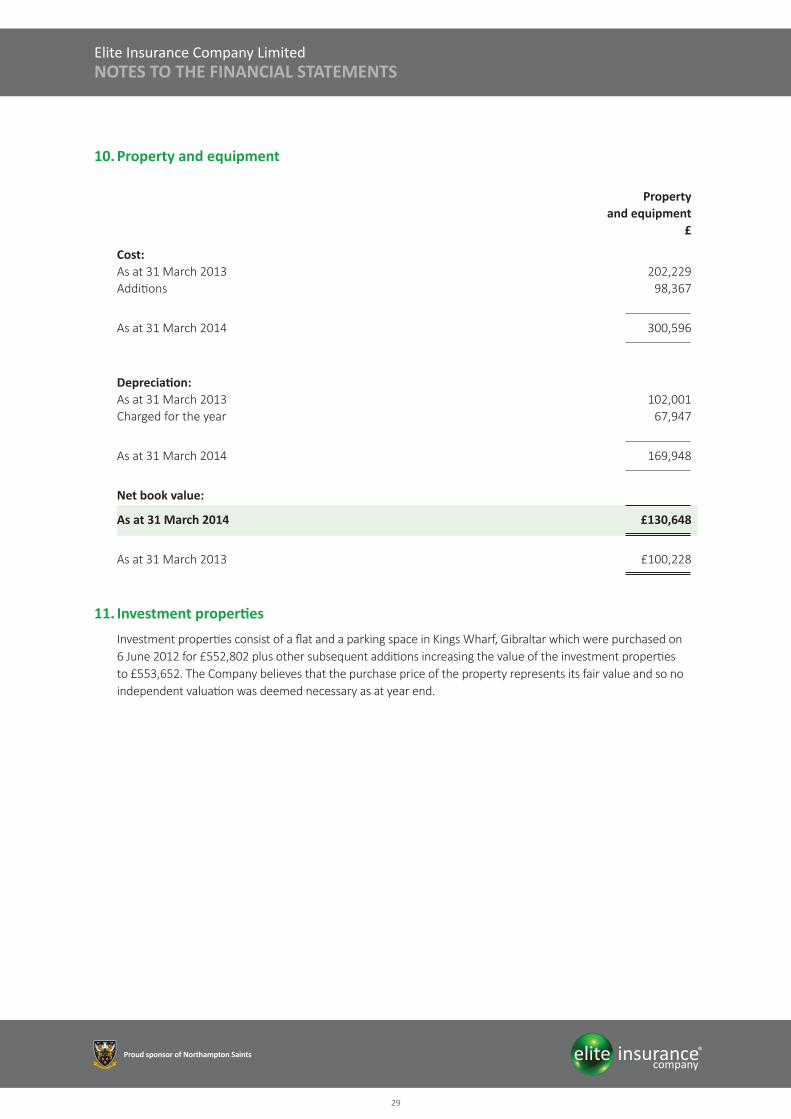

10. Property and equipment

Property and equipment £

Cost:As at 31 March 2013 202,229Additions 98,367

As at 31 March 2014 300,596

Depreciation: As at 31 March 2013 102,001Charged for the year 67,947

As at 31 March 2014 169,948

Net book value:

As at 31 March 2014 £130,648

As at 31 March 2013 £100,228

11. Investment properties

Investment properties consist of a flat and a parking space in Kings Wharf, Gibraltar which were purchased on 6 June 2012 for £552,802 plus other subsequent additions increasing the value of the investment properties to £553,652. The Company believes that the purchase price of the property represents its fair value and so no independent valuation was deemed necessary as at year end.

Elite Insurance Company LimitedNOTES TO THE FINANCIAL STATEMENTS

Proud sponsor of Northampton Saints

30

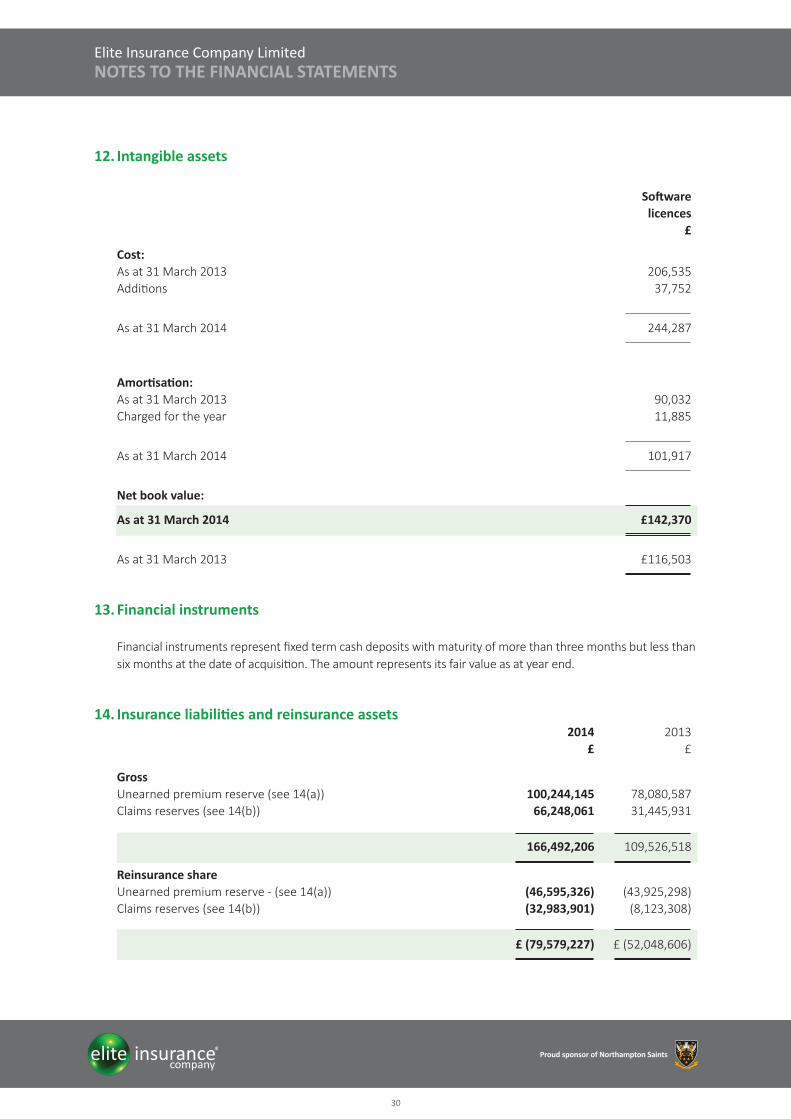

12. Intangible assets

Software licences £

Cost:As at 31 March 2013 206,535Additions 37,752

As at 31 March 2014 244,287

Amortisation: As at 31 March 2013 90,032Charged for the year 11,885

As at 31 March 2014 101,917

Net book value:

As at 31 March 2014 £142,370

As at 31 March 2013 £116,503

13. Financial instruments

Financial instruments represent fixed term cash deposits with maturity of more than three months but less than six months at the date of acquisition. The amount represents its fair value as at year end.

14. Insurance liabilities and reinsurance assets 2014 2013 £ £

GrossUnearned premium reserve (see 14(a)) 100,244,145 78,080,587Claims reserves (see 14(b)) 66,248,061 31,445,931

166,492,206 109,526,518

Reinsurance share Unearned premium reserve - (see 14(a)) (46,595,326) (43,925,298)Claims reserves (see 14(b)) (32,983,901) (8,123,308)

£ (79,579,227) £ (52,048,606)

Elite Insurance Company LimitedNOTES TO THE FINANCIAL STATEMENTS

Proud sponsor of Northampton Saints

31

14. Insurance liabilities and reinsurance assets (continued)

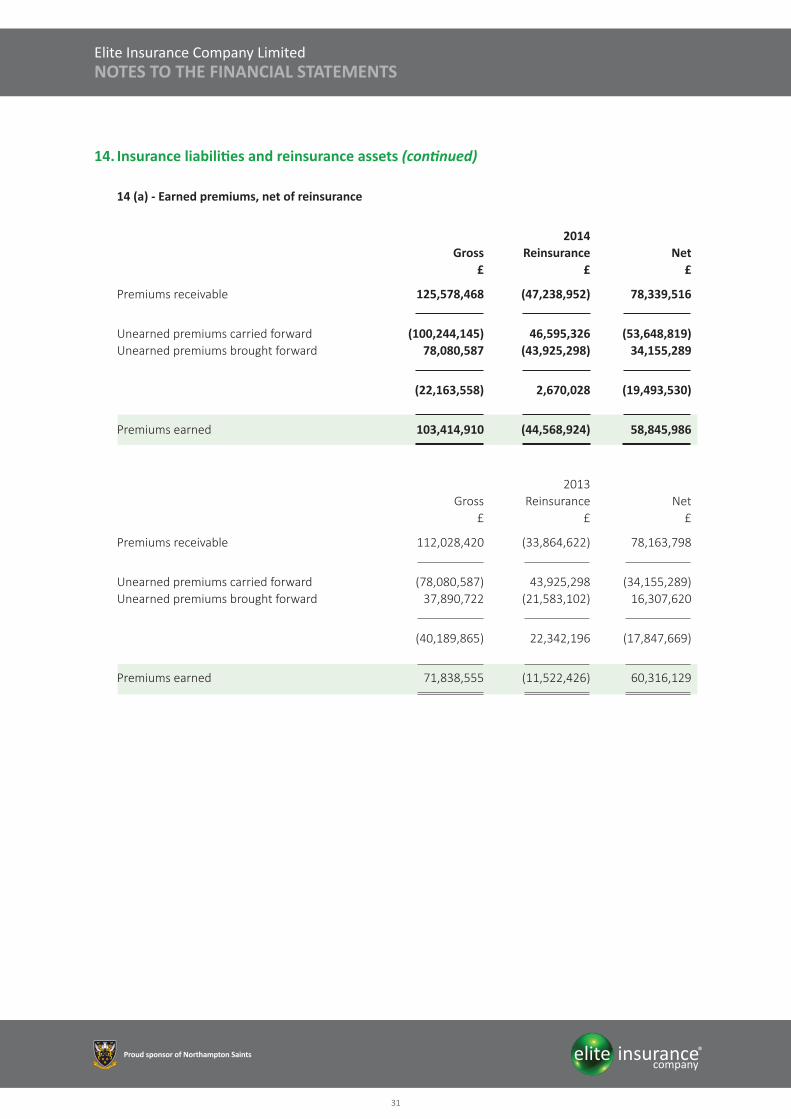

14 (a) - Earned premiums, net of reinsurance

2014 Gross Reinsurance Net £ £ £

Premiums receivable 125,578,468 (47,238,952) 78,339,516

Unearned premiums carried forward (100,244,145) 46,595,326 (53,648,819)Unearned premiums brought forward 78,080,587 (43,925,298) 34,155,289

(22,163,558) 2,670,028 (19,493,530)

Premiums earned 103,414,910 (44,568,924) 58,845,986

2013 Gross Reinsurance Net £ £ £

Premiums receivable 112,028,420 (33,864,622) 78,163,798

Unearned premiums carried forward (78,080,587) 43,925,298 (34,155,289)Unearned premiums brought forward 37,890,722 (21,583,102) 16,307,620

(40,189,865) 22,342,196 (17,847,669)

Premiums earned 71,838,555 (11,522,426) 60,316,129

Elite Insurance Company LimitedNOTES TO THE FINANCIAL STATEMENTS

Proud sponsor of Northampton Saints

32

14. Insurance liabilities and reinsurance assets (continued)

14(b) - Claims incurred, net of reinsurance 2014 Gross Reinsurance Net £ £ £

Claims paid 12,626,884 (4,388,352) 8,238,532Claims handling fees 1,651,312 (361,120) 1,290,192

14,278,196 (4,749,472) 9,528,724

Outstanding claims carried forward 66,248,061 (32,983,901) 33,264,160Outstanding claims brought forward (31,445,931) 8,123,308 (23,322,623)

34,802,130 (24,860,593) 9,941,537

Claims incurred 49,080,326 (29,610,065) 19,470,261

2013 Gross Reinsurance Net £ £ £

Claims paid 7,976,336 (1,862,978) 6,113,358

Outstanding claims carried forward 31,445,931 (8,123,308) 23,322,623 Outstanding claims brought forward (22,588,256) 5,342,242 (17,246,014)

8,857,675 (2,781,066) 6,076,609

Claims incurred 16,834,011 (4,644,044) 12,189,967

The above claims reserves are not all expected to be settled in the short term and there is considerable uncertainty as to the amounts at which they will be settled. Whilst the level of provision has been set by the Directors on the basis of information that is currently available, the ultimate liability will vary as a result of subsequent information and events and may result in significant adjustments to the amount provided.

14(b) - Claims incurred, net of reinsurance

Claims reserves have been set at directors’ valuation which is £3,177k lower gross, and £525k lower net than the suggested reserves from the actuaries in the latest actuarial review. The difference mainly relates to Solicitors PII, where the directors are of the opinion to use a lower reserve estimate more appropriately geared to the type of risks being written by the company, rather than the general market which the actuaries used. The directors are confident that claims reserves including IBNR are adequate without being excessive as at the balance sheet date.

Elite Insurance Company LimitedNOTES TO THE FINANCIAL STATEMENTS

Proud sponsor of Northampton Saints

33

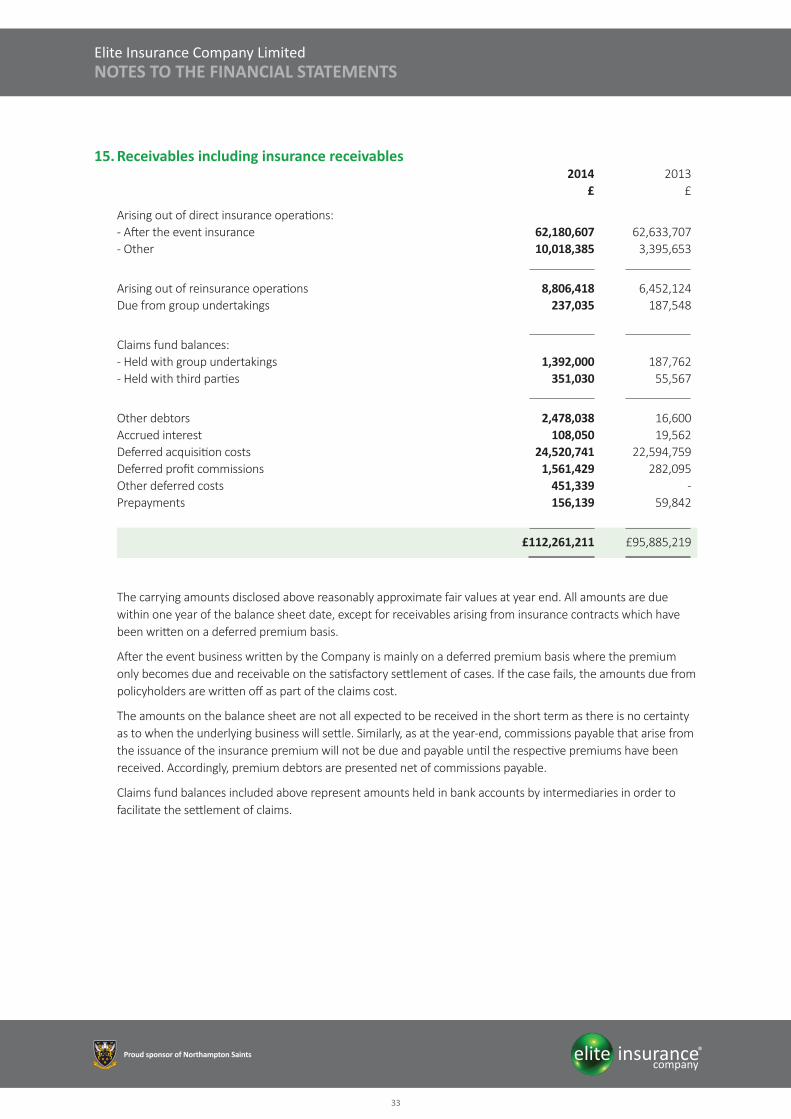

15. Receivables including insurance receivables 2014 2013 £ £

Arising out of direct insurance operations: - After the event insurance 62,180,607 62,633,707- Other 10,018,385 3,395,653

Arising out of reinsurance operations 8,806,418 6,452,124Due from group undertakings 237,035 187,548

Claims fund balances:- Held with group undertakings 1,392,000 187,762- Held with third parties 351,030 55,567

Other debtors 2,478,038 16,600Accrued interest 108,050 19,562Deferred acquisition costs 24,520,741 22,594,759Deferred profit commissions 1,561,429 282,095Other deferred costs 451,339 -Prepayments 156,139 59,842

£112,261,211 £95,885,219

The carrying amounts disclosed above reasonably approximate fair values at year end. All amounts are due within one year of the balance sheet date, except for receivables arising from insurance contracts which have been written on a deferred premium basis.

After the event business written by the Company is mainly on a deferred premium basis where the premium only becomes due and receivable on the satisfactory settlement of cases. If the case fails, the amounts due from policyholders are written off as part of the claims cost.

The amounts on the balance sheet are not all expected to be received in the short term as there is no certainty as to when the underlying business will settle. Similarly, as at the year-end, commissions payable that arise from the issuance of the insurance premium will not be due and payable until the respective premiums have been received. Accordingly, premium debtors are presented net of commissions payable.

Claims fund balances included above represent amounts held in bank accounts by intermediaries in order to facilitate the settlement of claims.

Elite Insurance Company LimitedNOTES TO THE FINANCIAL STATEMENTS

Proud sponsor of Northampton Saints

34

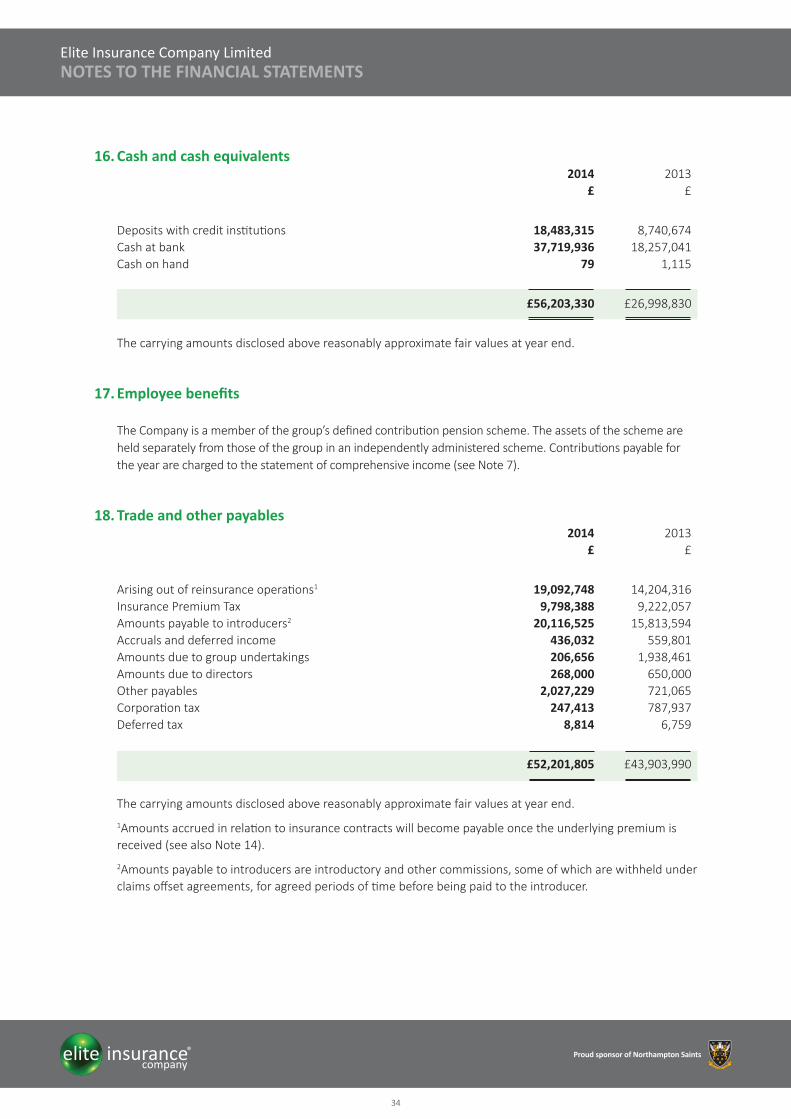

16. Cash and cash equivalents 2014 2013 £ £

Deposits with credit institutions 18,483,315 8,740,674Cash at bank 37,719,936 18,257,041Cash on hand 79 1,115

£56,203,330 £26,998,830

The carrying amounts disclosed above reasonably approximate fair values at year end.

17. Employee benefits

The Company is a member of the group’s defined contribution pension scheme. The assets of the scheme are held separately from those of the group in an independently administered scheme. Contributions payable for the year are charged to the statement of comprehensive income (see Note 7).

18. Trade and other payables 2014 2013 £ £

Arising out of reinsurance operations1 19,092,748 14,204,316Insurance Premium Tax 9,798,388 9,222,057Amounts payable to introducers2 20,116,525 15,813,594Accruals and deferred income 436,032 559,801Amounts due to group undertakings 206,656 1,938,461Amounts due to directors 268,000 650,000Other payables 2,027,229 721,065Corporation tax 247,413 787,937Deferred tax 8,814 6,759

£52,201,805 £43,903,990

The carrying amounts disclosed above reasonably approximate fair values at year end.

1Amounts accrued in relation to insurance contracts will become payable once the underlying premium is received (see also Note 14).

2Amounts payable to introducers are introductory and other commissions, some of which are withheld under claims offset agreements, for agreed periods of time before being paid to the introducer.

Elite Insurance Company LimitedNOTES TO THE FINANCIAL STATEMENTS

Proud sponsor of Northampton Saints

35

19. Called up share capital 2014 2013 £ £

Authorised:

10,000,000 Ordinary shares of £1 each 10,000,000 10,000,000

2014 2013 £ £

Share capital allotted, called up and fully paid:

2,600,000 Ordinary shares of £1 each 2,600,000 2,600,000

20. Cash flows from operating activities 2014 2013 £ £

Profit on ordinary activities before tax 7,026,917 10,931,953Depreciation of property and equipment 67,947 34,452Amortisation of intangible assets 11,885 29,881Interest income (133,132) (143,589)

Changes in working capital: Receivables including insurance receivables (16,375,994) (30,212,373)Insurance and reinsurance contracts 29,435,067 23,924,278Trade and other payables 8,836,284 12,771,906

Net cash flow from operating activities £28,868,974 £17,336,508

Elite Insurance Company LimitedNOTES TO THE FINANCIAL STATEMENTS

Proud sponsor of Northampton Saints

36

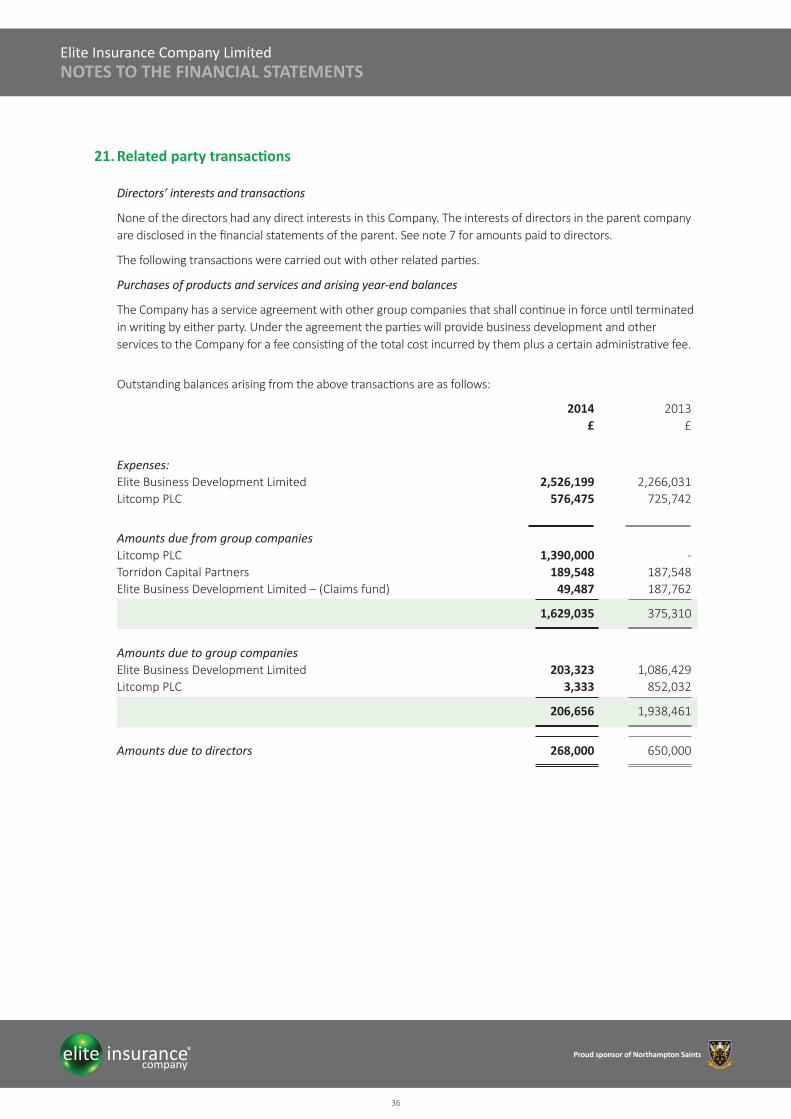

21. Related party transactions

Directors’ interests and transactions

None of the directors had any direct interests in this Company. The interests of directors in the parent company are disclosed in the financial statements of the parent. See note 7 for amounts paid to directors.

The following transactions were carried out with other related parties.

Purchases of products and services and arising year-end balances

The Company has a service agreement with other group companies that shall continue in force until terminated in writing by either party. Under the agreement the parties will provide business development and other services to the Company for a fee consisting of the total cost incurred by them plus a certain administrative fee.

Outstanding balances arising from the above transactions are as follows:

2014 2013 £ £

Expenses:Elite Business Development Limited 2,526,199 2,266,031Litcomp PLC 576,475 725,742

Amounts due from group companiesLitcomp PLC 1,390,000 -Torridon Capital Partners 189,548 187,548Elite Business Development Limited – (Claims fund) 49,487 187,762

1,629,035 375,310

Amounts due to group companiesElite Business Development Limited 203,323 1,086,429Litcomp PLC 3,333 852,032

206,656 1,938,461

Amounts due to directors 268,000 650,000

Elite Insurance Company LimitedNOTES TO THE FINANCIAL STATEMENTS

Proud sponsor of Northampton Saints

37

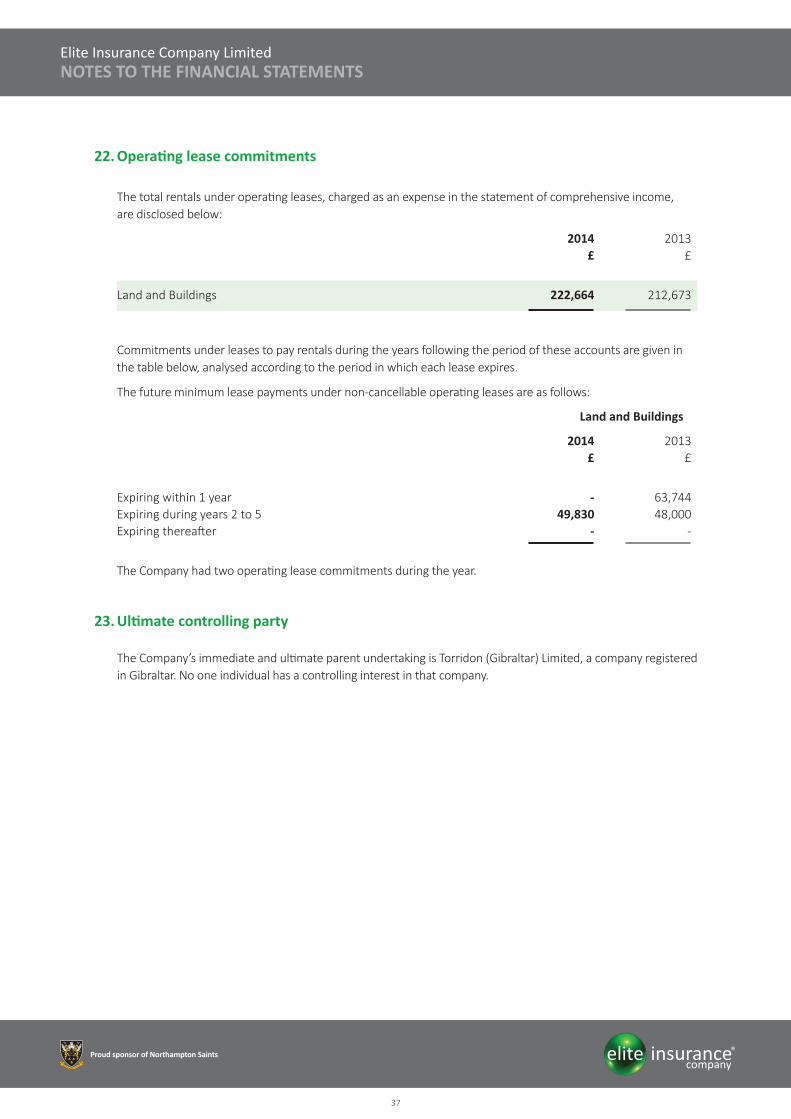

22. Operating lease commitments

The total rentals under operating leases, charged as an expense in the statement of comprehensive income, are disclosed below:

2014 2013 £ £

Land and Buildings 222,664 212,673

Commitments under leases to pay rentals during the years following the period of these accounts are given in the table below, analysed according to the period in which each lease expires.

The future minimum lease payments under non-cancellable operating leases are as follows:

Land and Buildings

2014 2013 £ £

Expiring within 1 year - 63,744Expiring during years 2 to 5 49,830 48,000Expiring thereafter - -

The Company had two operating lease commitments during the year.

23. Ultimate controlling party

The Company’s immediate and ultimate parent undertaking is Torridon (Gibraltar) Limited, a company registered in Gibraltar. No one individual has a controlling interest in that company.

Elite Insurance Company Limited

Proud sponsor of Northampton Saints

38

Notes

Elite Insurance Company Limited

Proud sponsor of Northampton Saints

39

Notes

T: 0845 601 1221 F: 01476 563 600 E: [email protected], Grantham, London, Madrid, Milan, Paris, Warrington

www.elite-insurance.co.uk

Elite Insurance Company Limited. Registered in Gibraltar. Company No. 91111. Registered Office Address: 47-48 The Sails, Queensway Quay, Queensway, Gibraltar GX11 1AA