Embed Size (px)

Citation preview

Emerging Market Debt Environment

October 2014

2

EM Dollar Debt Posts Gains after Difficult 2013

3

EM vs. DM Growth Stabilizing at Lower Spread

Source: IMF, World Economic Outlook Update, April 2014

Real GDP Growth Rate Differential: Emerging Market Premium over Developed Markets

(2014 –2018 IMF Estimates)

‐1

0

1

2

3

4

5

6

7

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

Realized Average: 2.36%

4

‐4

‐3.5

‐3

‐2.5

‐2

‐1.5

‐1

‐0.5

0

0.5

1Brazil India Indonesia South Africa Turkey

Current Account Deficits have Stabilized

Source: FactSet, IMF

Average Current Account BalanceAs of July 31, 2014

Chan

ge in

Cur

rent

Acco

unt Y

oY(%

)

Fragile Five – YoY Change in Current AccountAs of June 30, 2014

Current account deficits from the Fragile Five have begun to improve, while balances in EM remain in surplus on aggregate.

Improving Current Account

Worsening Current Account

5

EM Currencies have Re‐Priced to Competitive Levels

Source: FactSet, IMF, JP Morgan

JP Morgan Emerging Market Currency IndexDecember 2012 – September 2014

Inde

x Level

Fragile Five – Currency Panic Subsiding December 2012 – September 2014

Pullback in U.S. interest rates and defensive central bank policies shore up Fragile Five currencies

70

75

80

85

90

95

100

105

110

Dec‐12 Jun‐13 Dec‐13 Jun‐14Local Currency vs. U

SD

Brazil

India

Indonesia

South Africa

Turkey

6

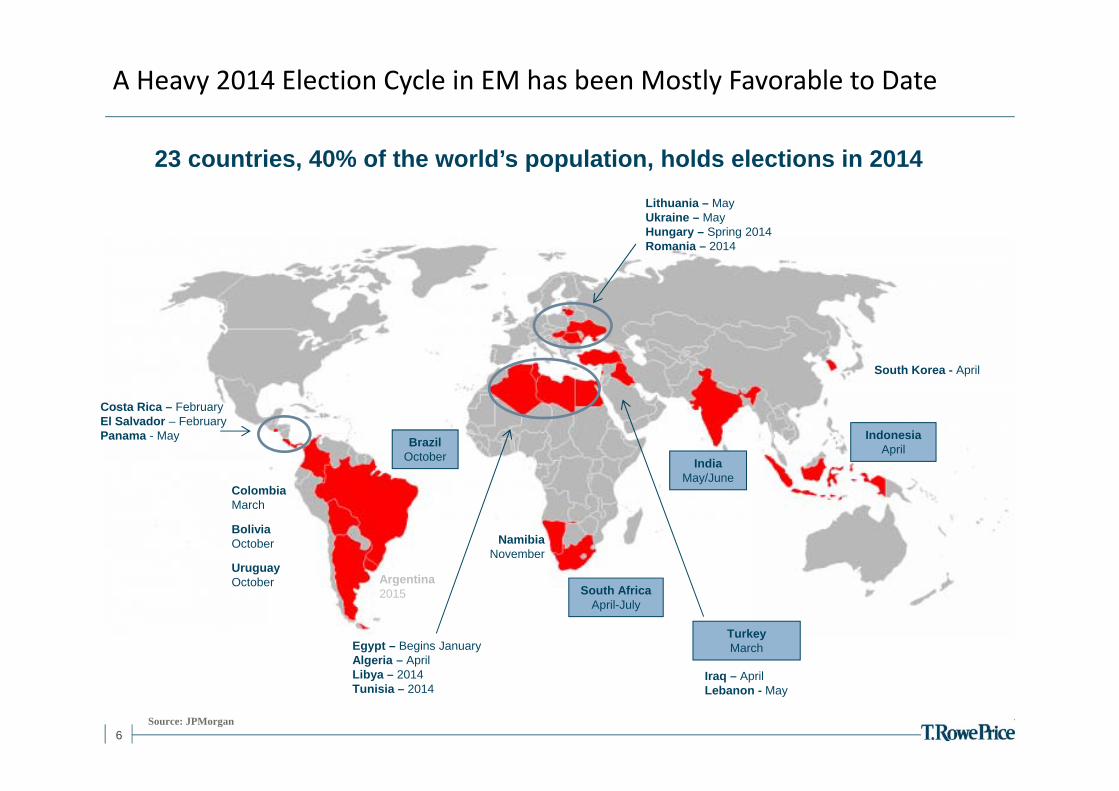

23 countries, 40% of the world’s population, holds elections in 2014

BrazilOctober India

May/June

Egypt – Begins JanuaryAlgeria – AprilLibya – 2014Tunisia – 2014

South AfricaApril-July

NamibiaNovember

South Korea - April

Iraq – AprilLebanon - May

IndonesiaApril

Lithuania – MayUkraine – MayHungary – Spring 2014Romania – 2014

Argentina2015

ColombiaMarch

BoliviaOctober

UruguayOctober

Turkey March

Costa Rica – FebruaryEl Salvador – FebruaryPanama - May

Source: JPMorgan

A Heavy 2014 Election Cycle in EM has been Mostly Favorable to Date

7Source: EPFR

Investors have Returned to EM Debt

(6)

(5)

(4)

(3)

(2)

(1)

0

1

2

3

Dec-12 Mar-13 May-13 Aug-13 Oct-13 Jan-14 Apr-14 Jun-14 Sep-14

U.S

. $, b

illio

ns

Weekly EM Fund and ETF Flows

EM Hard CurrencyEM LocalEM Blended Currency

Fed announces Tapering plans;‘Tourists’ leave the asset class

8

Reserve Accumulation of EM Countries*As of September 30, 2014

Many EM countries today have strong liquidity buffers, free-floating currency regimes, and relatively low debt burdens.

Emerging Markets vs. G7 Public Debt (% of GDP)IMF forecasts as of Apr 2014

EM’s Have Maintained Healthy Buffers to External Shocks

Source: Haver Analytics. *EM Countries include all constituents based on the JP Morgan GBI-EM Global Diversified Index

$mn

9Source: International Monetary Fund, World Economic Outlook Update, April 2014.

DM and EM Share of Global GDP (%)1982 – 2019 (Estimated)

EM Should not be Ignored Given its Rising Global Importance

10%

20%

30%

40%

50%

60%

70%

80%

90%

1982 1986 1990 1994 1998 2002 2006 2010 2014 2018

DM EM

(E) (E)

10

Although Idiosyncratic Events have Driven Disparate Returns

11

Source: JP MorganIndices: EMBI Global Diversified, CEMBI Broad Diversified, GBI-EM Global Diversified

Emerging Markets Hard Currency30 September 2011 – 30 September 2014

Today’s Absolute Valuations Are Fair…

5.31%

5.40%

Emerging Markets Corporate30 September 2011 – 30 September 2014

Emerging Markets Local Currency30 September 2011 – 30 September 2014

4

4.5

5

5.5

6

6.5

Sep‐11 Mar‐12 Sep‐12 Mar‐13 Sep‐13 Mar‐14 Sep‐14

Yield (%

)

JPM EMBI Glbl Div Average for period

4

4.5

5

5.5

6

6.5

7

7.5

Sep‐11 Mar‐12 Sep‐12 Mar‐13 Sep‐13 Mar‐14 Sep‐14

Yield (%

)

JPM CEMBI Broad Div Average for period

5.35%5.27%

5

5.5

6

6.5

7

7.5

Sep‐11 Mar‐12 Sep‐12 Mar‐13 Sep‐13 Mar‐14 Sep‐14

Yield (%

)

Average for period JPM EM‐GBI Glbl Div

6.74%

6.27%

12 12

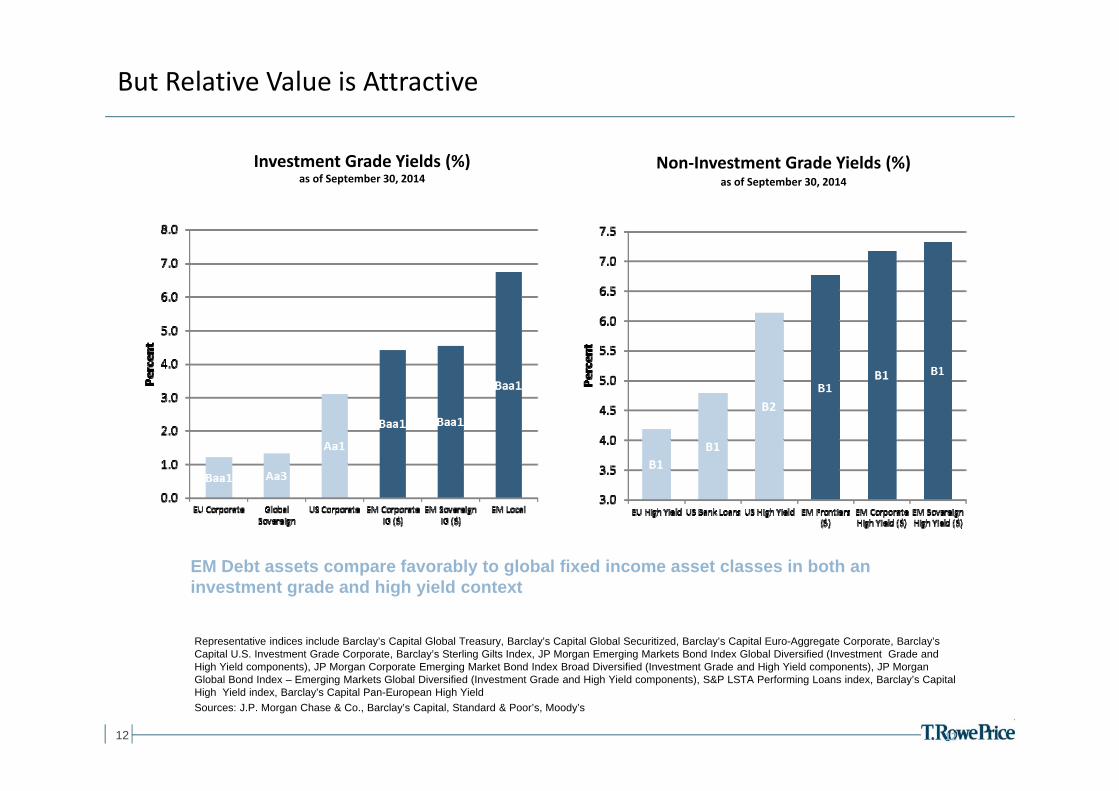

But Relative Value is Attractive

Representative indices include Barclay’s Capital Global Treasury, Barclay’s Capital Global Securitized, Barclay’s Capital Euro-Aggregate Corporate, Barclay’s Capital U.S. Investment Grade Corporate, Barclay’s Sterling Gilts Index, JP Morgan Emerging Markets Bond Index Global Diversified (Investment Grade and High Yield components), JP Morgan Corporate Emerging Market Bond Index Broad Diversified (Investment Grade and High Yield components), JP Morgan Global Bond Index – Emerging Markets Global Diversified (Investment Grade and High Yield components), S&P LSTA Performing Loans index, Barclay’s Capital High Yield index, Barclay’s Capital Pan-European High YieldSources: J.P. Morgan Chase & Co., Barclay’s Capital, Standard & Poor’s, Moody’s

EM Debt assets compare favorably to global fixed income asset classes in both an investment grade and high yield context

Investment Grade Yields (%) as of September 30, 2014

Non‐Investment Grade Yields (%) as of September 30, 2014

13

Sources: Barclays, JP Morgan, S&P/LSTA

J.P. Morgan indices: Emerging Markets Bond Index Global, Global High Yield, GBI-EM Global Diversified, CEMBI Broad Diversified; Barclays indices: U.S. Corporate Investment Grade, U.S. Aggregate Bond Index, Global Aggregate Bond Index, U.S. Treasury component of Barclays U.S. Agg; UK Sterling Aggregate, Swedish Krona Aggregate, Euro Corporate Investment Grade, Euro Aggregate

2H14 Returns Likely to be Driven by Carry versus Yield Compression

0

1

2

3

4

5

6

7

8

Global HY EM Local EM DollarSovereign

EM Corp U.S. IGCorp

UKSterling

Aggregate

SwedishKrona

Aggregate

Euro IGCorp

EuroAggregate

U.S.Aggregate

GlobalAggregate

U.S.Treasury

Average Coupon by Asset Class (%)as of September 30, 2014

14

Investor Allocations Continue to Rise from a Low Base

Sources: JP Morgan, Morningstar, Morgan Stanley

27%36%

36% 38% 37%

67%

57%

55%51% 52%

0

100

200

300

400

500

600

700

2010 2011 2012 2013 Sep‐2014

Corporate External Debt

External Debt

Local Debt

6%

7%

9%

12%11%

U.S

. $, b

illion

s

Dedicated EM Debt Investor Base**As of September 2014

As at 31 Dec 2012

15

Important Information

This document, including any statements, information, data and content contained therein and any materials, information, images, links, sounds, graphics or video provided in conjunction with this document (collectively “Materials”) are being furnished by T. Rowe Price for your general informational purposes only. The Materials are not intended for use by persons injurisdictions which prohibit or restrict the distribution of the Materials and in certain countries these Materials are only provided upon specific request. It is not intended for distribution to retail investors in any jurisdiction. Under no circumstances should the Materials, in whole or in part, be copied, redistributed or shown to any person without consent from T. Rowe Price. The Materials do not constitute a distribution, an offer, an invitation, recommendation or solicitation to sell or buy any securities in any jurisdiction. The Materials have not been reviewed by any regulatory authority in any jurisdiction. The Materials do not constitute investment advice and should not be relied upon. Investors should seek independent legal and financial advice, including advice as to tax consequences, before making any investment decision.

Issued in the EEA by T. Rowe Price International Limited (“TRPIL”), 60 Queen Victoria Street, London EC4N 4TZ which is authorised and regulated by the Financial Conduct Authority. For Qualified Investors only.

T. ROWE PRICE, INVEST WITH CONFIDENCE and the Bighorn Sheep design are, collectively and/or apart, trademarks or registered trademarks of T. Rowe Price Group, Inc. in the United States, European Union, and other countries. This material is intended for use only in select countries.

This material is provided for informational purposes only and is not intended to be investment advice or a recommendation to take any particular investment action. The views contained herein are as of September 2014, and may have changed since that time.

GL‐2014‐909