Embed Size (px)

Citation preview

Employee or Employee or Independent Independent Contractor?Contractor?

Making the Proper Making the Proper Determination in Determination in Your NonprofitYour Nonprofit

February 2, 2005February 2, 2005

Classification ChallengesClassification Challenges

Regulatory interpretations differ

Court decisions (trial and appellate) may give different view

No single definition; no single test

The nature of the Nonprofit World—time constraints, mission focus, lack of HR expertise

Statutory Definitions?

May be of little help:Title VII and the ADA-

Congress adopted a circular definition of “employee” — an employee is an “individual employed by an employer.”

What’s the difference?

Practical:Independent contractors require less of

an administrative burdenpayroll processing and taxesworkers’ compensationwhat else?

Flexibility is greater with contractors; no expectation of continuing relationship

What’s the difference?

Liability Risk:Liability risk is less

(e.g. federal anti-discrimination laws don’t apply)

Consequences of an Error

Key: choosing IC over employee statusback-taxes on wagesfinancial penalties and interestadditional wages due (e.g. FLSA)workers’ compensationliability for wrongful employment

practicesattorney’s fees

How does a Nonprofit Employer get caught?

Targeted investigation? Employee whistleblower Application for unemployment

benefits Harassment or discrimination

complaint with the EEOC IRS audit INS audit

Learning to distinguish employees from independent contractors

IRS 20-Factor Test

Labor Department’s Economic Reality Test

Common Law Control Test

IRS 20-Factor Test

No factor is determinative Document that your independent

contractors, consultants and free-lance workers meet these criteria

1. Control2. Responsible for hiring and

supervising others

IRS 20-Factor Test

3. Reimbursement4. Separate business address5. Work not typically performed by

employees6. Significant investment7. Other clients?8. Where will the work be performed?

IRS 20-Factor Test

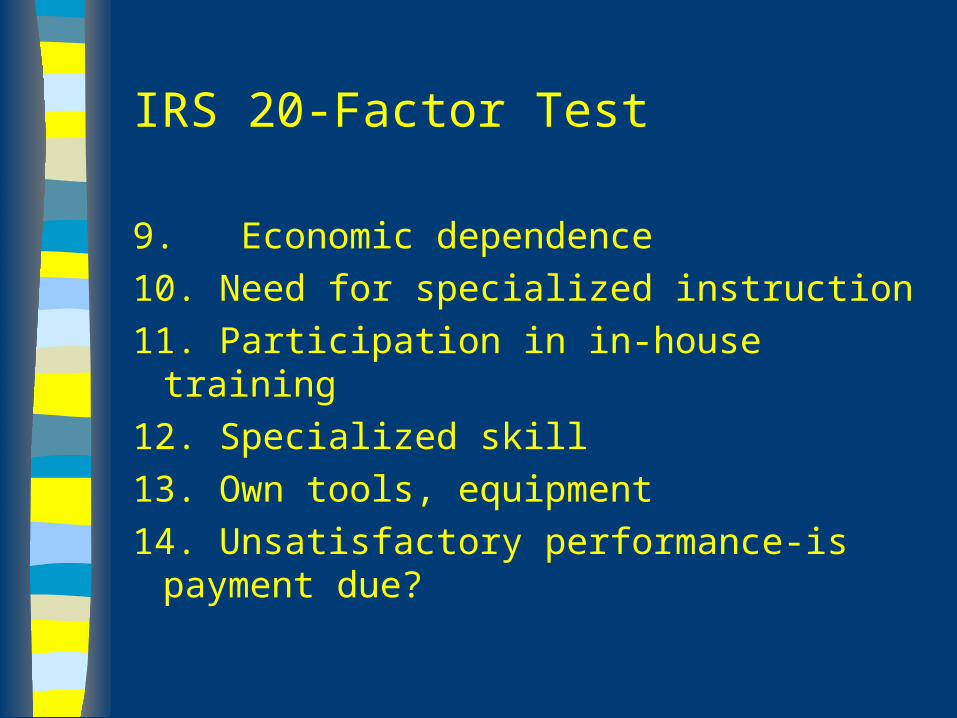

9. Economic dependence10. Need for specialized instruction11. Participation in in-house training12. Specialized skill13. Own tools, equipment14. Unsatisfactory performance-is

payment due?

IRS 20-Factor Test

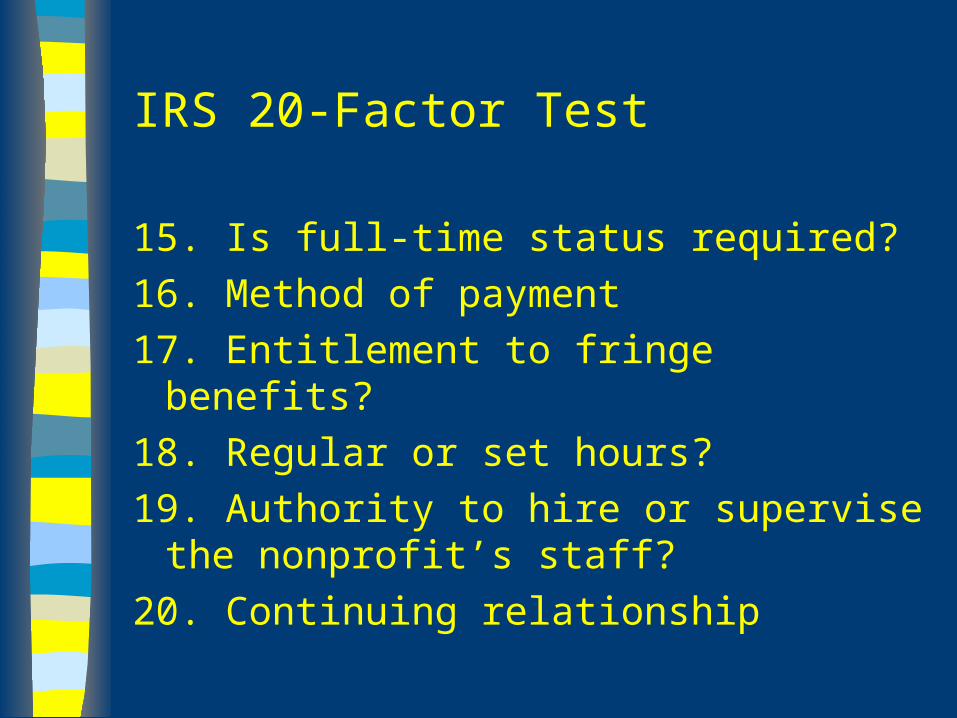

15. Is full-time status required?16. Method of payment17. Entitlement to fringe benefits?18. Regular or set hours?19. Authority to hire or supervise the

nonprofit’s staff?20. Continuing relationship

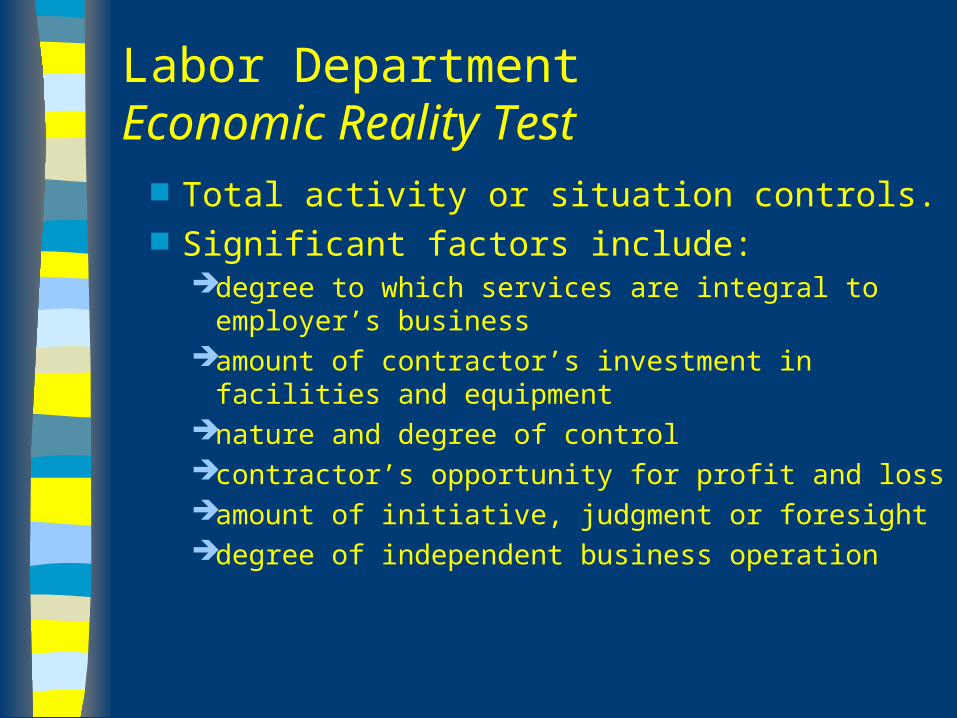

Labor DepartmentEconomic Reality Test

Total activity or situation controls. Significant factors include:

degree to which services are integral to employer’s business

amount of contractor’s investment in facilities and equipment

nature and degree of controlcontractor’s opportunity for profit and lossamount of initiative, judgment or foresight degree of independent business operation

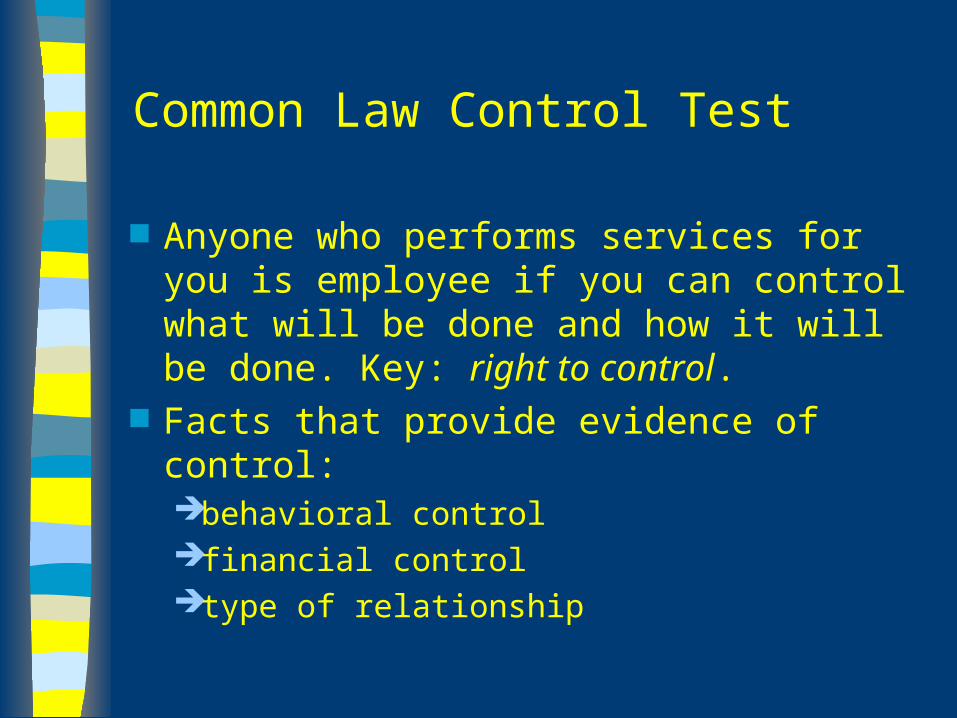

Common Law Control Test

Anyone who performs services for you is employee if you can control what will be done and how it will be done. Key: right to control.

Facts that provide evidence of control:behavioral controlfinancial controltype of relationship

Proceeding with care

Examine duties and position in light of 20-factors.

When employing contractors, seek most qualified for the job and established business

Always negotiate a written contract before the work begins

Never use employees and contractors to perform the same task.

Independent Contractor Cases

Lerohl v. Friends of Minnesota Sinfonia

Appellate Court ruling:independent contractor may be

required to work to exacting specifications of the hiring party

persuasive evidence? Musicians could choose whether or not to perform at concerts sponsored by the Sinfonia

Independent Contractor Cases

Woolf v. Mary Kay Cosmetics Insurance agency manager case Compassion versus deviating

from policy and practice Classify with care Punitive damages: company

acted with “oppression or malice”

Nonprofit Risk Management Center

Please call or email for free technical assistance

(202) 785-3891 [email protected]

Check out the resources on our web site: www.nonprofitrisk.org