Embed Size (px)

Citation preview

NAT 73514-02.2013

Only use this ESS Annual Report to report ESS Interest for the 2010 financial year onwards.

For information about how to report electronically, phone us on 1800 072 681.

Instructions and form for Employee Share Scheme information

Employee Share Scheme (ESS) annual report How to complete the ESS annual report

© AUSTRALIAN TAXATION OFFICE FOR THE COMMONWEALTH OF AUSTRALIA, 2013

You are free to copy, adapt, modify, transmit and distribute this material as you wish (but not in any way that suggests the ATO or the Commonwealth endorses you or any of your services or products).

PUBLISHED BY

Australian Taxation Office Canberra February 2013 JS 26655

OUR COMMITMENT TO YOUWe are committed to providing you with accurate, consistent and clear information to help you understand your rights and entitlements and meet your obligations.

If you follow our information in this publication and it turns out to be incorrect, or it is misleading and you make a mistake as a result, we must still apply the law correctly. If that means you owe us money, we must ask you to pay it but we will not charge you a penalty. Also, if you acted reasonably and in good faith we will not charge you interest.

If you make an honest mistake in trying to follow our information in this publication and you owe us money as a result, we will not charge you a penalty. However, we will ask you to pay the money, and we may also charge you interest. If correcting the mistake means we owe you money, we will pay it to you. We will also pay you any interest you are entitled to.

If you feel that this publication does not fully cover your circumstances, or you are unsure how it applies to you, you can seek further assistance from us.

We regularly revise our publications to take account of any changes to the law, so make sure that you have the latest information. If you are unsure, you can check for more recent information on our website at www.ato.gov.au or contact us.

This publication was current at February 2013.

EmplOyEE SHArE SCHEmE (ESS) AnnuAl rEpOrT 1

WHO SHOulD COmplETE THE ESS AnnuAl rEpOrT?

Information can be reported to us electronically. We can supply you with the specifications necessary to use your own software.

Refer to our electronic publication How to lodge your employee share scheme annual report electronically at www.ato.gov.au/employeeshareschemes – ‘In detail’ – then select ‘Employer reporting requirements’.

To complete this form we recommend you refer to our electronic publications ESS – guide for employers and Employer reporting requirements for employee share schemes at www.ato.gov.au/employeeshareschemes

For ESS – guide for employers, go to ‘What you need to know’ – then select ‘Employers’.

For Employer reporting requirements for employee share schemes, go to ‘In detail’ – then select ‘Employer reporting requirements’.

The information you supply in this report will not update registration information held by the ATO and is used for identification and compliance purposes only.

To update name and address details, contact details and preferred correspondence methods, use our ‘change of registration details’ process. For information about this process, visit www.ato.gov.au

An employee share scheme (ESS) is a scheme in which ESS interests in a company are provided to employees (including past or prospective employees and their associates) in relation to the employee’s employment.

You should complete the Employee Share Scheme (ESS) annual report for the 2009–10 financial years onwards if you are a provider of ESS interests.

The ESS provider is the entity that provides an employee share scheme to employees.

An ESS provider may authorise an organisation to supply the ESS information on their behalf (known as the supplier).

It is the responsibility of the ESS provider to ensure that the ESS annual report is completed correctly and lodged with us by the due date.

An ESS annual report need only be lodged where the ESS provider is required to report in that year. An ESS provider is required to report for that year if an ESS taxing event occurred for at least one employee during that year.

A separate ESS annual report must be lodged for each provider and for each financial year.

You need to send your ESS annual report to the ATO by the 14 August each year.

If you require additional time to lodge your annual report phone 1800 072 681.

make sure you keep a copy for your records.

2 EmplOyEE SHArE SCHEmE (ESS) AnnuAl rEpOrT

HOW DO I COmplETE THE ESS AnnuAl rEpOrT?

Question 1 ESS provider’s Australian business number (ABN) or withholding payer number (WPN)provide the ESS provider’s current ABn or Wpn.

The ABn or Wpn reported must correspond to the ESS provider’s name at question 2.

place an ‘X’ in the box provided if the provider does not have an ABn or Wpn.

Question 2 ESS provider’s name provide the ESS provider’s name as it appears on the provider’s ABn or Wpn registration.

The ESS provider’s name must correspond to the provider’s ABn or Wpn at question 1. This should be the name that appears on the provider’s activity statements.

Question 3 ESS provider’s addressprovide the ESS provider’s postal address. This address will be used for any paper correspondence relating to this ESS annual report.

This form will not update registration information held by the ATO. To update name and address details, use our ‘change of registration details’ process. For information about this process, visit www.ato.gov.au

Question 4 Contact nameprovide the name and contact details for the person to be contacted if we need to discuss any information provided in the ESS annual report.

SECTION A: ESS PROVIDER DETAILSThe ESS provider is the entity that provides an employee share scheme to employees.

If you are supplying ESS information for more than one ESS provider you must lodge a separate ESS annual report for each provider.

You must complete only one Section A within your annual report.

Annual report for year ended 30 Juneprovide the financial year within which the ESS interests occurred. Report the year in which the financial year ends.

For example, if the ESS annual report is being lodged in August 2012 for ESS taxing events that occurred in the financial year 1 July 2011 to 30 June 2012, this field would be 2012.

You must complete a separate form for each financial year being reported.

The first report that you lodge with us for a financial year is referred to as your original report. Write ‘X’ in the ‘Original’ box if this is your first report that you lodge with us for the financial year.

If you need to amend details after the original ESS report has been lodged with us, refer to ‘How do I amend an ESS annual report that has been lodged?’ on page 8.

HOW DO I COmplETE THE ESS AnnuAl rEpOrT?

EmplOyEE SHArE SCHEmE (ESS) AnnuAl rEpOrT 3

TFN Code Description

444444444 Employee is a pensioner – where the employee is a recipient of a Centrelink or service pension or benefit (other than newstart, sickness allowance, special benefits or partner allowance) an exemption from quoting a TFn may be claimed. In this case the code 444444444 must be used.

987654321 Alphabetic characters in quoted TFn – where an employee has quoted a TFn with alpha characters, the code 987654321 must be used in place of the quoted TFn. This code must also be used where the TFn quoted cannot be contained in the TFN field.

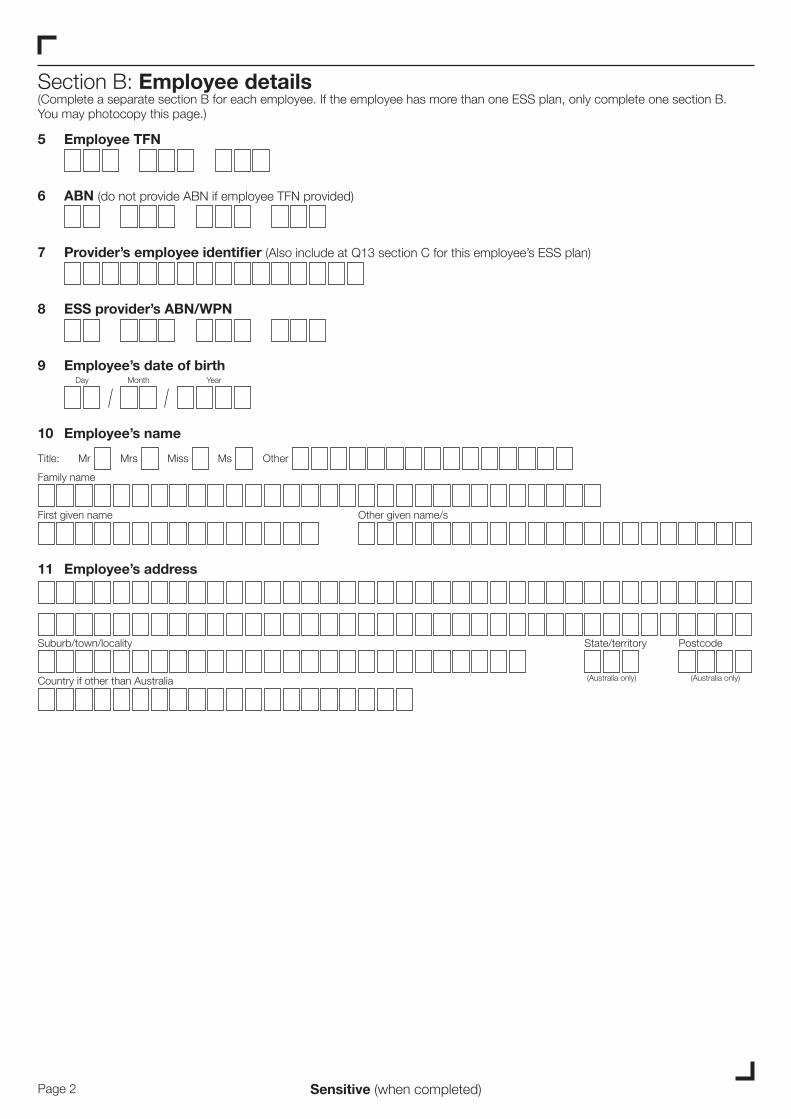

Question 6 ABNprovide the ABn of the employee (contractor) receiving the ESS interests. If you have provided the employee’s TFn then do not provide the employee’s (contractor’s) ABn.

The ABn reported must belong to the employee (contractor) named in this record.

Question 7 Provider’s employee identifier provide the employee identifier used to link the employee with the organisation. This identifier could be the employer’s employee number or any other unique identifier the ESS provider can use to identify the employee.

The employee identifier must be completed – it should not be left blank. The ESS provider must allocate unique employee identifiers to participants in the employee share scheme. The identifier can contain alpha or numeric characters or a combination of both.

SECTION B: EMPLOYEE DETAILS

you must complete a separate section B for each employee. you will need to photocopy the section B page of the form.

If the employee has more than one ESS plan, only complete one section B for that employee and a separate section C for each ESS plan.

Question 5 Employee tax file number (TFN)provide the TFn quoted by the employee. If the employee has not quoted a TFn, provide an appropriate TFn code from the table below.

The employer must withhold tax at the highest marginal rate plus the medicare levy if an employee or contractor has:n not quoted a TFn or an ABnn not claimed an exemption from quotingn been deemed by the ATO not to have quoted a TFn or an ABn.

If the employer has calculated an amount of TFn withholding from an employee’s assessable ESS interests, then the amount (in dollars and cents) should be completed at question 22.

TFN Code Description

000000000 no TFn quoted by the employee – the employee chooses not to quote a TFn or fails to provide one within 28 days

111111111 Employee applying for a TFn – if a summary is prepared for an employee who does not provide a TFn but indicates on the TFn declaration that one has been applied for, an interim code of 111111111 can be used by the employer.

This code would usually be updated with the employee’s TFn or with the no TFn quoted code (000000000) where an employee fails to provide the TFn to the employer within the 28 day period allowed, under legislation, to obtain and provide the TFn to the employer.

The ONLY time that the TFN code 111111111 would be reported to the ATO is when the employee commenced work in mid to late June and had not received notification of the TFN prior to the submission of the report to the ATO.

HOW DO I COmplETE THE ESS AnnuAl rEpOrT?

4 EmplOyEE SHArE SCHEmE (ESS) AnnuAl rEpOrT

Question 11 Employee’s addressprovide the employee’s residential address.

you must provide the employee’s address. Do not leave the employee address field blank.

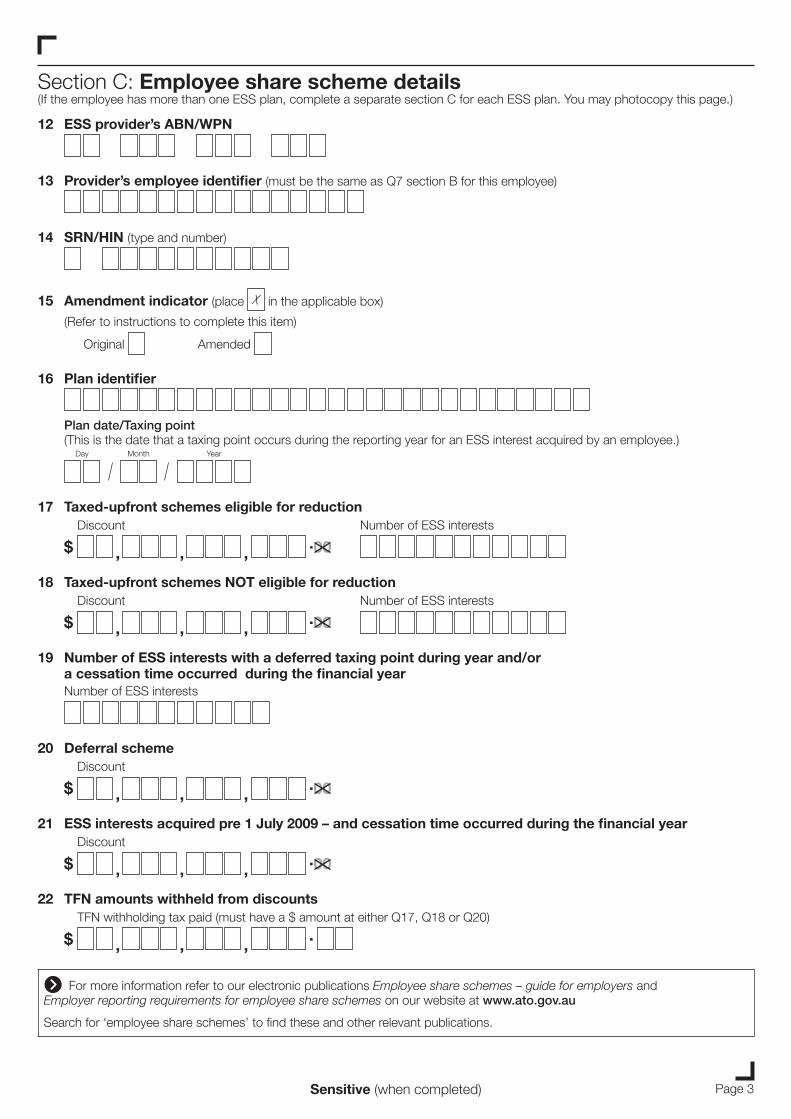

SECTION C: EMPLOYEE SHARE SCHEME DETAILS

If an employee has more than one ESS plan, then complete a separate Section C for each of the employee’s ESS plans. A separate Section C page is provided in the form for you to photocopy if necessary.

If you need more information to complete section C refer to our electronic publications ESS – guide for employers and Employer reporting requirements for employee share schemes at www.ato.gov.au/employeeshareschemes

For ESS – guide for employers, go to ‘What you need to know’ – then select ‘Employers’.

For Employer reporting requirements for employee share schemes, go to ‘In detail’ – then select ‘Employer reporting requirements’.

Question 12 Provider’s ABN/WPN For each Section C completed for an employee who has more than one ESS plan, provide the current ABn or Wpn for the employee’s ESS provider as in question 8 above. This information is provided again in case the separate Section C details become dislodged. If no ABn or Wpn, leave blank.

Question 13 Provider’s employee identifier For each section C completed for an employee who has more than one ESS plan, provide the employee identifier used to link the employee with the organisation as in question 7 above.

This information is provided again in case the separate section C details become dislodged.

Question 8 ESS provider’s ABN/WPN provide the current ABn or Wpn for the employee’s ESS provider. If no ABn or Wpn, leave blank.

This information is provided again in case the separate section B details become dislodged.

The ABn or Wpn reported must correspond to the ESS provider name at question 2 (Section A).

Question 9 Employee’s date of birthprovide the employees day, month and year of birth, if known. For example, if the employee’s date of birth is 19 June 1946 write 19 / 06 / 1946.

Write 0 in any part of the date of birth which is unknown. For example, if only the year of birth is known write zeros for the day and month of birth. So if the year of birth is 1956 write 00 / 00 / 1956.

Question 10 Employee’s nameprovide the employee’s full name.

Where the employee’s legal name is a single name only, include it in the ‘family name’ field rather than in the ‘first given name’ field. leave the other fields blank.

If the employee’s full first given name is not known, show their first initial.

you may leave the ‘Other given name/s’ field blank if the employee either has no other given name or it is unknown. use an initial in the field only if the employee’s full other given name is unknown.

Where an employee has more than two given names, do not provide the third and subsequent given names or initials.

HOW DO I COmplETE THE ESS AnnuAl rEpOrT?

EmplOyEE SHArE SCHEmE (ESS) AnnuAl rEpOrT 5

Question 16 Plan identifier and plan date/taxing pointprovide the identifier for the employee’s share scheme plan. The plan identifier is a reference that makes a plan unique within all plans run by the ESS provider.

provide the plan date/taxing point.

The plan date is the date that a taxing point happens (during the reporting year) to ESS interest acquired by an employee. For an upfront scheme this will be the acquisition date. For a deferred plan it will be the deferred taxing point.

Both the plan identifier and plan date fields must be completed even if the employer only offers a single plan to their employees.

If there are multiple taxing events (plan dates) attached to a plan, provide the earliest taxing event date (plan date).

Question 17 Taxed-upfront schemes eligible for reduction provide the amount of income assessable (discount amount) and the number of ESS interests acquired during the financial year not eligible for deferral but eligible for reduction.

you are only required to report these amounts in the year the ESS interests are acquired. They do not have to be reported again in a future year.

The discount amount for question 17 must be reported in whole dollars. If an amount includes cents, then disregard the cents.

For example, $10,000.57 would be reported as 10,000.

If you need more information to complete question 17 refer to our electronic publications ESS – guide for employers and Employer reporting requirements for employee share schemes at www.ato.gov.au/employeeshareschemes

For ESS – guide for employers, go to ‘What you need to know’ – then select ‘Employers’.

For Employer reporting requirements for employee share schemes, go to ‘In detail’ – then select ‘Employer reporting requirements’.

Question 14 Security holder reference number (SRN) and holder identification number (HIN)provide the ESS account holding type and number.

Include the Srn or HIn in this field that is relevant to the plan identifier.

Write the prefix for the SRN or HIN in the ‘type field’ followed by the number. For example, if a Srn write ‘I’ in the type field, if an HIn write ‘X’ in the type field.

Question 15 Amendment indicatorState whether the employee share scheme details contain original or amended information.

Complete this question by writing an ‘X’ in the applicable box.

Original information is information that is being reported for the first time.

Amended information is information that is correcting what has previously been reported.

If reporting amended information, be sure to provide the same financial year ended, employee identifier, and ESS plan identifier that was provided in the original report.

Refer to ’How do I amend an ESS annual report that has been lodged?’ on page 8.

HOW DO I COmplETE THE ESS AnnuAl rEpOrT?

6 EmplOyEE SHArE SCHEmE (ESS) AnnuAl rEpOrT

Question 20 Deferral schemeprovide the amount of income assessable (discount amount) where the deferred taxing point occurred during the financial year.

The discount amount in the ‘deferral schemes’ field will only be the amount relevant to the number of ESS interests with a ‘deferred taxing point arising during the year’.

The discount amount at question 20 must be reported in whole dollars. If an amount includes cents, then disregard the cents.

For example, $10,000.57 would be reported as 10,000.

Question 21 Discount on ESS interests acquired pre 1 July 2009 – and cessation time occurred during the financial year provide the amount of income from ESS interests acquired before 1 July 2009 for which a cessation time occurred during the financial year.

The discount amount for question 21 must be reported in whole dollars. If an amount includes cents, then disregard the cents.

For example, $10,000.57 would be reported as 10,000.

Question 22 TFN amounts withheld from discountsprovide the amount of TFn withholding tax paid in relation to the assessable discount from ESS interests for which a taxing point arose during the financial year where the employee has not provided a TFn or an ABn.

Question 22 must be reported in dollars and cents. For example, $86.42 would be reported as $86.42.

For an amount of TFN amounts withheld from discounts to be included at Question 22 you must have an amount at Question 17, 18 or 20.

Question 18 Taxed-upfront schemes NOT eligible for reductionprovide the amount of income assessable (discount amount) and the number of ESS interests acquired during the financial year nOT eligible for deferral or reduction.

you are only required to report these amounts in the year the ESS interests are acquired. They do not have to be reported again in a future year.

The discount amount for question 18 must be reported in whole dollars. If an amount includes cents, then disregard the cents.

For example, $10,000.57 would be reported as 10,000.

If you need more information to complete question 18 refer to our electronic publications ESS – guide for employers and Employer reporting requirements for employee share schemes at www.ato.gov.au/employeeshareschemes

For ESS – guide for employers, go to ‘What you need to know’ – then select ‘Employers’.

For Employer reporting requirements for employee share schemes, go to ‘In detail’ – then select ‘Employer reporting requirements’.

Question 19 Number of ESS interests with a deferred taxing point during the year and/or a cessation time occurred during the financial yearprovide the number of ESS interests with a deferred taxing point during the year, and/or, if known, the number of ESS interests acquired pre 1 July 2009 and a cessation time occurred during the financial year.

HOW DO I COmplETE THE ESS AnnuAl rEpOrT?

EmplOyEE SHArE SCHEmE (ESS) AnnuAl rEpOrT 7

SECTION D: DECLARATIONread the declaration. If all information you provided is true and correct, print your full name and then sign and date the declaration.

If an ESS supplier, such as an administrator or a tax agent, is completing the ESS annual report on behalf of the ESS provider, then complete the name of the supplier.

If the ESS provider is lodging the ESS on its own behalf, the name of the supplier does not need to be completed.

Send the completed ESS annual report to:Australian Taxation Office PO Box 2090 Chermside QLD 4032

Information can be reported to us electronically. We can supply you with the specifications necessary to use your own software. Phone our information line on 1800 072 681 for further details.

8 EmplOyEE SHArE SCHEmE (ESS) AnnuAl rEpOrT

HOW DO I AmEnD An ESS AnnuAl rEpOrT THAT HAS BEEn lODGED?

Section C: Employee share scheme details n Complete a new section C for amended ESS details. n All details and amounts relating to the amended ESS details

are to be reported exactly as they were reported in the original report except for the fields that require amendment.

n Amended employee details in section C are only required for errors to the following ESS details originally reported:– employee SRN/HIN number or type– employee amount(s)– employee number of ESS interest fields– plan identifier or plan date/taxing point (refer to ‘Amending

provider’s employee identifier and plan identifier’ on page 9).n Any amounts that were reported incorrectly on the original

report should be corrected on the amended report. For example if $200 was originally reported in the ‘discount from deferral schemes’ field but it should have been reported as $400, the amount of $400 should be reported for ‘discount from deferral schemes’ in the amended report.

Amended section C details must have an ‘X’ written in the ‘Amended’ box at question 15 ‘Amendment indicator’.

Employee or ESS details not included in original annual reportIf you have already lodged your original report and want to provide employee or ESS details that have not been sent to us, you can include the new Section B and Section C details within the amended annual report.

Original section C details contained in the amended report and not previously sent to us must have an ‘X’ written in the ‘Original’ box at question 15 ‘Amendment indicator’.

Section C lodged in errorIf you have lodged section C details for an employee in error and want those original details to be disregarded, prepare an amended ESS annual report for the same plan identifier and employee identifier and report zero amounts at all questions in Section C: Employee share scheme details.

The first report that you lodge with the ATO for a financial year is referred to as your original report.

Any employee details that you amend before sending your original report to the ATO should still be marked as original.

All Section C: Employee share scheme details sent to us for the first time for that financial year must have an ‘X’ written in the, ‘Original’ box at question 15 ‘Amendment indicator’.

AMENDING AN ESS ANNUAL REPORTIf you need to amend or include additional details after the original ESS report has been lodged with us, the corrected details should be reported in another annual report form for the same financial year. place an ‘X’ in the box marked ‘Amended’ on page 1.

To lodge an amended annual report you need to complete and lodge the following sections:

Section A: ESS provider detailsn All details must be reported exactly as they were reported

in the original report.

Section B: Employee detailsn Complete a new Section B for an employee if they have

amended employee details or ESS details. Only one section B needs to be completed for each employee.

n All details relating to this employee are to be reported exactly as they were reported in the original report except for the fields that require amendment.

n Amended employee details in section B are only required for errors to the following employee details originally reported:− employee TFn or ABn or ESS provider’s ABn or Wpn− ESS provider employee identifier− employee date of birth− employee name.

you do not need to report amendments to a change of employee name (ie deed poll) or employee change of address.

HOW DO I AmEnD An ESS AnnuAl rEpOrT THAT HAS BEEn lODGED?

EmplOyEE SHArE SCHEmE (ESS) AnnuAl rEpOrT 9

Amending provider’s employee identifier and plan identifierIf you want to amend section B, question 7 ‘provider’s employee identifier’, or section C, question 16 ‘plan identifier and plan date/taxing point’, you must: n prepare amended Section C details for the original plan

identifier and employee identifier by writing ‘X’ in the ‘Amended’ box at question 15 ‘Amendment indicator’ and then report zero amounts at all questions in Section C: Employee share scheme details.

n prepare original section C details for the corrected plan identifier and employee identifier by writing ‘X’ in the ‘Original’ box at question 15 ‘Amendment indicator’ and then report the correct information at all questions in Section C: Employee share scheme details.

This is because we need the original employee identifier and plan identifier to find the details that require amending in our systems.

EXAMPLE

provider y lodges an ESS annual report for the 2011 financial year for an employee with plan identifier number ‘A123’ and an employee identifier number ‘r789’. The discount amount from taxed-upfront schemes eligible for reduction was reported as $50,000.

Y later finds that the discount amount of only $5,000 should have been reported for the employee. It seeks to amend the amount, but incorrectly reports the wrong plan identifier ‘A327’ with the corrected discount amount of $5,000.

We treat both of the ESS lodgments as original lodgments as they have different plan identifier numbers. We query the employee for having a larger amount of income to be assessed than indicated in their income tax return. The employee asks their provider, y, to amend the amount they have reported to the ATO.

y now needs to lodge two amended ESS forms for employee ‘r789’. The first is to amend the first ESS report it lodged by giving plan identifier ‘A123’ a discount amount from taxed-upfront schemes eligible for reduction amount of $5,000. The second is to amend the next ESS report it lodged to be disregarded, by giving plan identifier ‘A327’ a zero value for the discount amount.

Section D: Declaration n Complete a new section D.

When you prepare an amended ESS annual report, be sure to:n complete all sections (A to D) of the formn provide amended section B and section C details and

any additional original section B and section C details that were not reported in a prior annual report for the same financial year.

MORE INFORMATIONIf you need more information about the ESS annual report, you can:n visit www.ato.gov.au n phone 1800 072 681 between 8.00am and 5.00pm,

Monday to Fridayn write to the ATO at

Australian Taxation Office PO Box 2090 Chermside QLD 4032

If you do not speak English well and need help from the ATO, phone the Translating and Interpreting Service on 13 14 50.

If you are deaf, or have a hearing or speech impairment, phone the ATO through the national relay Service (nrS) on the numbers listed below:n TTY users, phone 13 36 77 and ask for the ATO number

you needn Speak and listen (speech-to-speech relay) users, phone

1300 555 727 and ask for the ATO number you needn Internet relay users, connect to the NRS on

www.relayservice.com.au and ask for the ATO number you need.

Employee share scheme (ESS) annual report

Page 1Sensitive (when completed)NAT 73514-02.2013

You should complete the Employee Share Scheme (ESS) annual report for the 2009–10 financial years onwards if you are an authorised supplier or provider of ESS information.

WHEN COMPLETING THIS FORMnUse the instructions to help you complete this report.nPrint clearly in BLOCK LETTERS using a black pen.nDo not use rubber stamps to show employer details.

nPlace X in all applicable boxes.

nDo not use whiteout or correction tape.

Annual report for year ending 30 June

Original Amended

Section A: ESS provider details

2 ESS provider’s name

3 ESS provider’s address

Country if other than Australia

Suburb/town/locality Postcode

(Australia only)

State/territory

(Australia only)

4 Contact name

Contact phone number

Contact email

1 ESS provider’s Australian business number (ABN) or withholding payer number (WPN)

Do not have an ABN/WPN

Page 2 Sensitive (when completed)

11 Employee’s address

Country if other than Australia

Suburb/town/locality Postcode

(Australia only)

State/territory

(Australia only)

Section B: Employee details (Complete a separate section B for each employee. If the employee has more than one ESS plan, only complete one section B. You may photocopy this page.)

5 Employee TFN

6 ABN (do not provide ABN if employee TFN provided)

7 Provider’semployeeidentifier(Also include at Q13 section C for this employee’s ESS plan)

8 ESS provider’s ABN/WPN

Day Month Year

9 Employee’s date of birth

10 Employee’s name

Family name

First given name Other given name/s

OtherTitle: Mrs Miss MsMr

Page 3Sensitive (when completed)

For more information refer to our electronic publications Employee share schemes – guide for employers and Employer reporting requirements for employee share schemes on our website at www.ato.gov.au

Search for ‘employee share schemes’ to find these and other relevant publications.

Section C: Employee share scheme details (If the employee has more than one ESS plan, complete a separate section C for each ESS plan. You may photocopy this page.)

12 ESS provider’s ABN/WPN

16 Planidentifier

Day Month Year

Plan date/Taxing point (This is the date that a taxing point occurs during the reporting year for an ESS interest acquired by an employee.)

14 SRN/HIN (type and number)

13 Provider’semployeeidentifier(must be the same as Q7 section B for this employee)

17 Taxed-upfront schemes eligible for reductionDiscount

.00$ , , ,

Number of ESS interests

18 Taxed-upfront schemes NOT eligible for reductionDiscount

.00$ , , ,

Number of ESS interests

20 Deferral schemeDiscount

.00$ , , ,

21 ESSinterestsacquiredpre1July2009–andcessationtimeoccurredduringthefinancialyearDiscount

.00$ , , ,

22 TFN amounts withheld from discounts

.$ , , ,

TFN withholding tax paid (must have a $ amount at either Q17, Q18 or Q20)

Original Amended

15 Amendment indicator (place X in the applicable box)

(Refer to instructions to complete this item)

19 Number of ESS interests with a deferred taxing point during year and/or acessationtimeoccurredduringthefinancialyearNumber of ESS interests

Page 4 Sensitive (when completed)

Section D: DeclarationThis section must be completed by an individual authorised by the provider.

Before you sign this reportCheck that you have provided accurate and complete information.

PENALTIESPenalties may be imposed for giving false or misleading information.

PrivacyWe are authorised by the Taxation Administration Act 1953 to ask for the information on this report. We need this information to help us administer the tax laws. Where authorised by law to do so, we may give this information to other government agencies which administer laws relevant to your particular situation. We may give this information to other government agencies as authorised in taxation law; for example, benefit payment agencies such as Centrelink and the Department of Education, Employment and Workplace Relations; law enforcement agencies such as state and federal police; and other government agencies such as Child Support Agency and the Australian Bureau of Statistics.

I declare that:n the current ESS provider has authorised this ESS annual report and the information in this ESS annual report is true and

correct and includes all ESS interest provided for each employee.n if the ESS annual report is being lodged by a supplier on the ESS provider’s behalf, that the information provided to

the supplier for the preparation of this ESS is true and correct, and the ESS provider authorised the supplier to lodge this ESS annual report.

ESS provider’s ABN/WPN

Name of supplier (if other than the ESS provider)

Name of signatory

On behalf of (ESS provider’s name)

Signature

DateDay Month Year

Lodging your reportRemove the instructions from the front of this report. Keep a copy for your records and return the completed original by 14 August to:Australian Taxation Office PO Box 2090 Chermside QLD 4032