Embed Size (px)

Citation preview

Employer-Sponsored Health Insurance for Early Retirees:

Impacts on Retirement, Health and Health Care

Erin Strumpf, Ph.D.McGill University

AcademyHealth Health Economics Interest GroupJune 7, 2008

Funding from the National Institute on Aging, Grant Number T32-AG00186, is gratefully acknowledged.

Background

• Employer-sponsored health insurance is an important source of coverage for older Americans

• Rates of employer offer of retiree health insurance (RHI) have declined by 50%, from 66% of large firms in 1988 to 33% in 2005

• Based on these declining rates, we can expect that future cohorts of retirees will have much lower rates of RHI coverage

Research Question

• What implications can we expect among Americans ages 45-64?

• Measure the effect of RHI offer on:

– Retirement

– Health

– Health care spending

RHI Offer

Retirement

RHI Coverage

Health

How Does RHI Offer Affect Health?

Medical Care Useand Spending

Existing Literature• Effect of health insurance on retirement

– Strong evidence that health insurance affects retirement decisions, but generalizability is often limited

• Effect of health insurance on health

– Elderly (Medicare): no impact on mortality, some increase in utilization and improvement in self-reported health

– Non-elderly: some evidence of small positive effects for marginal populations, mostly no measurable effects

Madrian 1994, Gruber and Madrian 1995, 1996, Rust and Phelan 1997, Blau and Gilleskie 2001; McWilliams, et al. 2003, Levy and Meltzer 2004, Meara, et al. 2005, Finkelstein and McKnight 2005, Cutler and Vigdor 2005.

Data

• Health and Retirement Survey (HRS) 1992-2002

• A longitudinal study of older Americans with interviews every two years

• Sample restrictions:

– respondents aged 47-63 and report having employer-sponsored health insurance in 1992

– years when respondents are still under age 65

• RHI Offer: can continue current employer-sponsored coverage in retirement

IdentificationEmployer-sponsored coverage

RHI Offer No RHI Offer

Don’t RetireRetire Retire Don’t Retire

Health and Medical Spending

Health and Medical Spending

Need to show: • RHI offer is conditionally exogenous.• Conditional on offer status, there is no differential selection into retirement with respect to health.

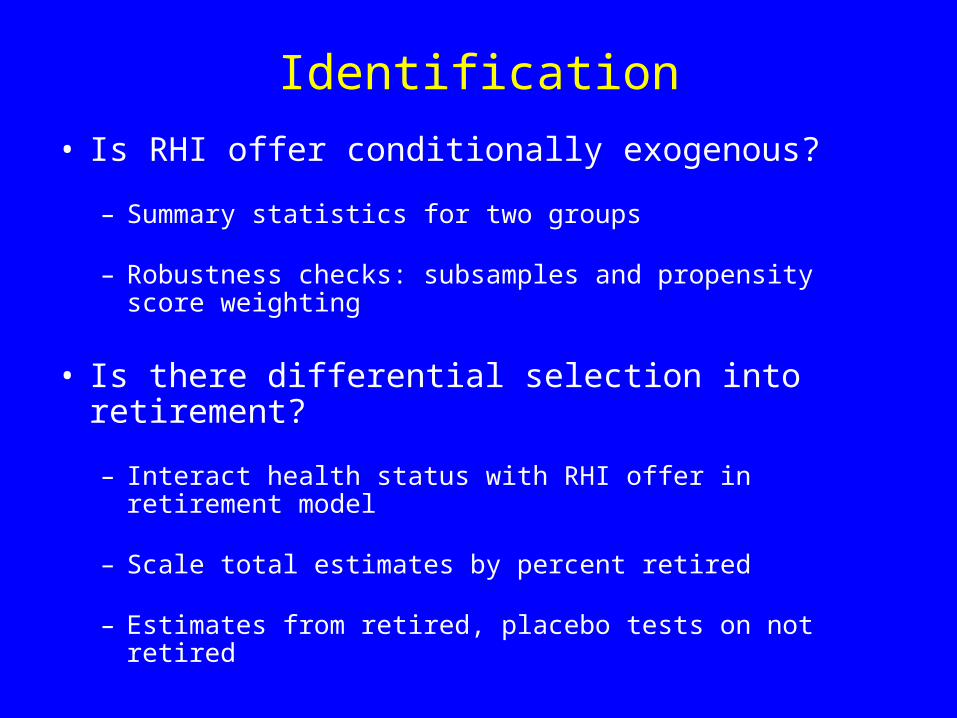

Identification

• Is RHI offer conditionally exogenous?

– Summary statistics for two groups

– Robustness checks: subsamples and propensity score weighting

• Is there differential selection into retirement?

– Interact health status with RHI offer in retirement model

– Scale total estimates by percent retired

– Estimates from retired, placebo tests on not retired

Summary Statistics 1992

Total ESI RHI offer No RHI offer

Age 55.2 0.051 55.4 0.061 54.8* 0.098

Education 12.9 0.033 13.0 0.039 12.7* 0.068

Fair/Poor Health 13% 0.004 13% 0.005 14% 0.008

OOP Health Spending 1,311 62 1,292 75 1,381 130

Mother Alive 45% 0.006 45% 0.008 44% 0.013

Married 83% 0.005 85% 0.006 77%* 0.011

Works Full-Time 65% 0.006 61% 0.008 73%* 0.011

Ages 47-63. Means and standard errors (adjusted for survey design and clustering at the individual level). * significantly different from RHI offer group at p<0.01.

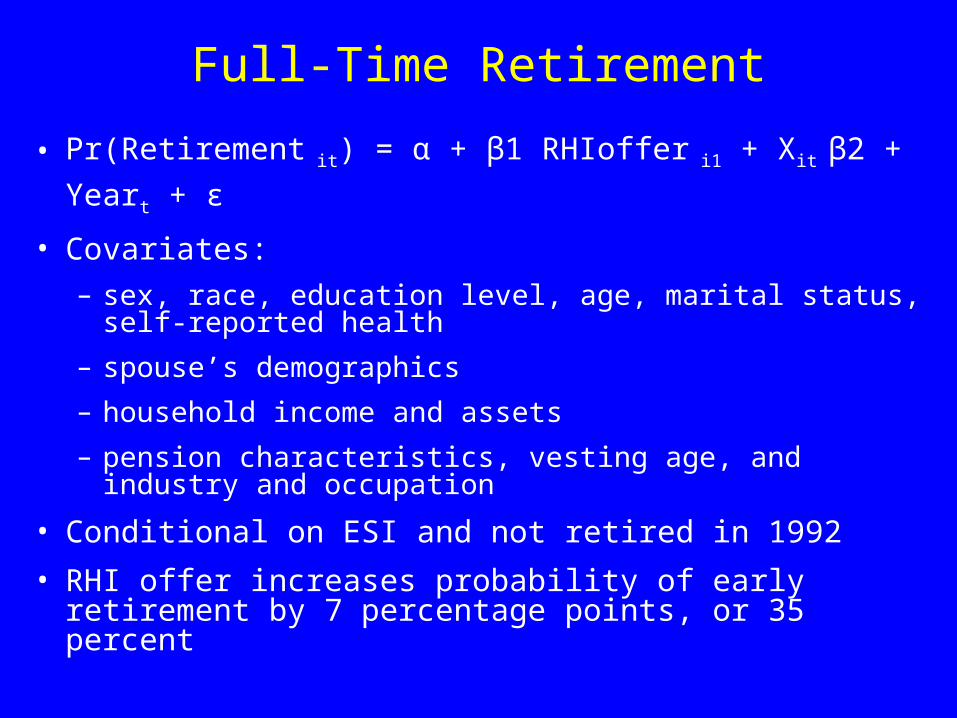

Full-Time Retirement

• Pr(Retirement it) = α + β1 RHIoffer i1 + Xit β2 + Yeart + ε

• Covariates:

– sex, race, education level, age, marital status, self-reported health

– spouse’s demographics

– household income and assets

– pension characteristics, vesting age, and industry and occupation

• Conditional on ESI and not retired in 1992

• RHI offer increases probability of early retirement by 7 percentage points, or 35 percent

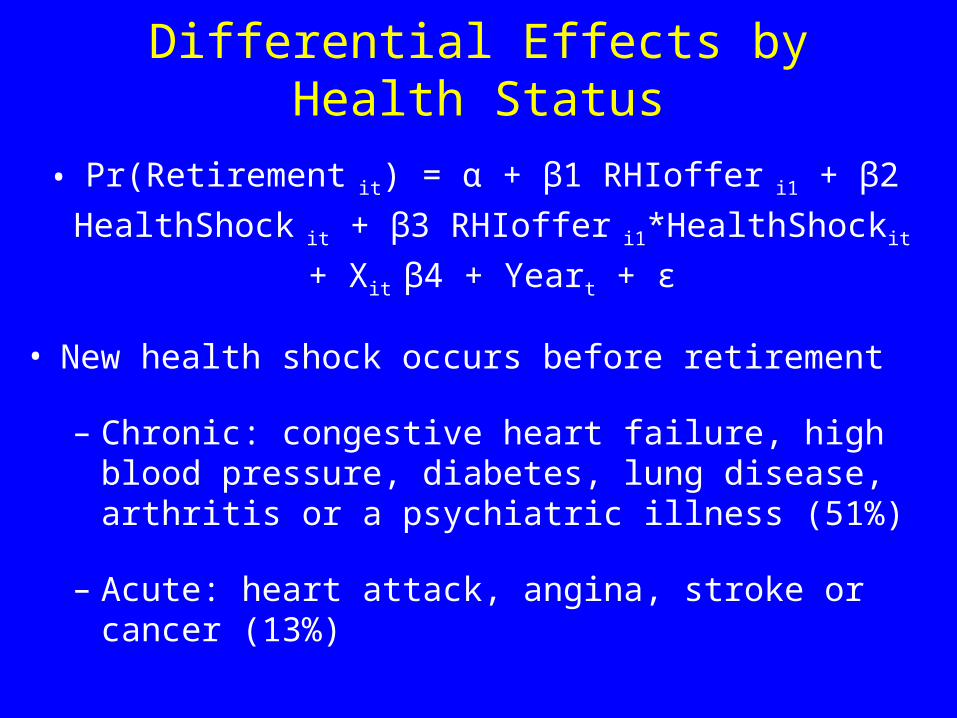

Differential Effects by Health Status

• Pr(Retirement it) = α + β1 RHIoffer i1 + β2 HealthShock it

+ β3 RHIoffer i1*HealthShockit + Xit β4 + Yeart + ε

• New health shock occurs before retirement

– Chronic: congestive heart failure, high blood pressure, diabetes, lung disease, arthritis or a psychiatric illness (51%)

– Acute: heart attack, angina, stroke or cancer (13%)

Differential Retirement by Health StatusFull-Time Retirement

Chronic Health Shock

Acute Health Shock

RHI offer 0.065*** 0.084*** 0.067*** 0.082***

[0.010] [0.014] [0.010] [0.013]

Health Shock -0.037** -0.039 0.056 0.057

[0.019] [0.023] [0.044] [0.055]

Offer*Shock 0.026 -0.018 -0.039 -0.080

[0.025] [0.029] [0.040] [0.046]

Lagged Shock (2 yrs)

0.032 0.156*

[0.025] [0.062]

Offer*Lagged Shock

-0.037 -0.067

[0.026] [0.050]

N 12,366 9,516 12,085 9,387

Marginal effects from probit models. Std errors adjusted for survey design and clustering at the individual level. *significant at 5%, ** 1%, *** 0.1%

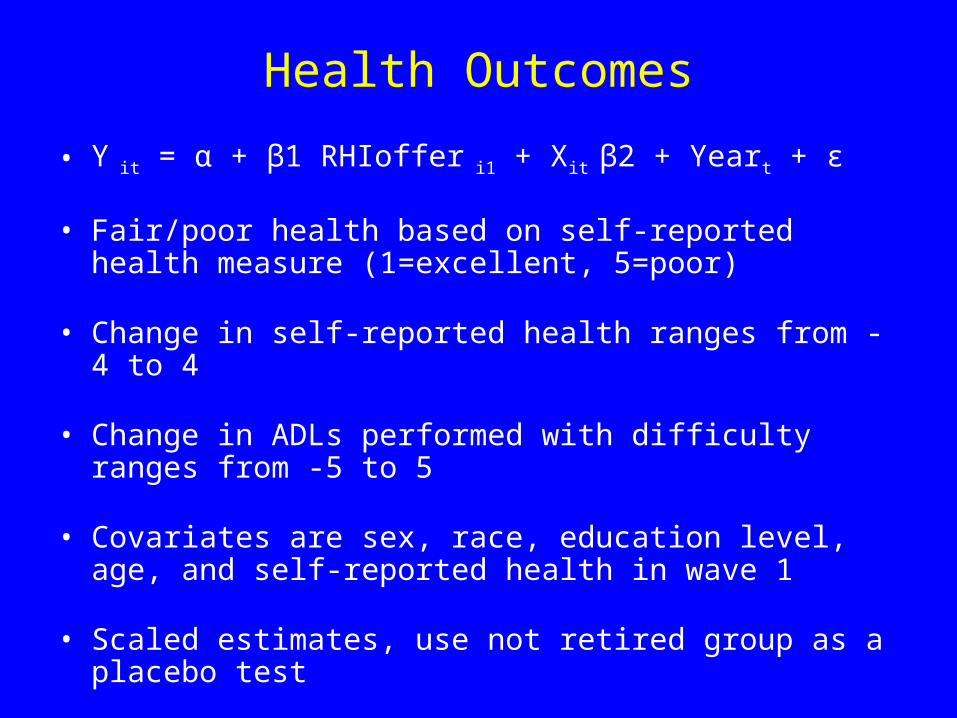

Health Outcomes

• Y it = α + β1 RHIoffer i1 + Xit β2 + Yeart + ε

• Fair/poor health based on self-reported health measure (1=excellent, 5=poor)

• Change in self-reported health ranges from -4 to 4

• Change in ADLs performed with difficulty ranges from -5 to 5

• Covariates are sex, race, education level, age, and self-reported health in wave 1

• Scaled estimates, use not retired group as a placebo test

Estimated Effect of RHI Offer on Health Status

Total Scaled Not Retired

Retired

Fair/Poor Self-Reported Health

RHI offer -0.008

3

-0.0366 -0.0089 -0.0308

[0.007] [0.007] [0.018]

Change in Self-Reported Health

RHI offer 0.0001

0.0002 -0.0038 -0.0038

[0.008] [0.009] [0.026]

Change in ADLs

RHI offer -0.003

0

-0.0124 0.0026 -0.0396

[0.005] [0.005] [0.022]

The fair/poor health regression is conditional on not being in fair/poor health at baseline.Std errors adjusted for survey design and clustering at the individual level. *significant at 5%, ** 1%, *** 0.1%

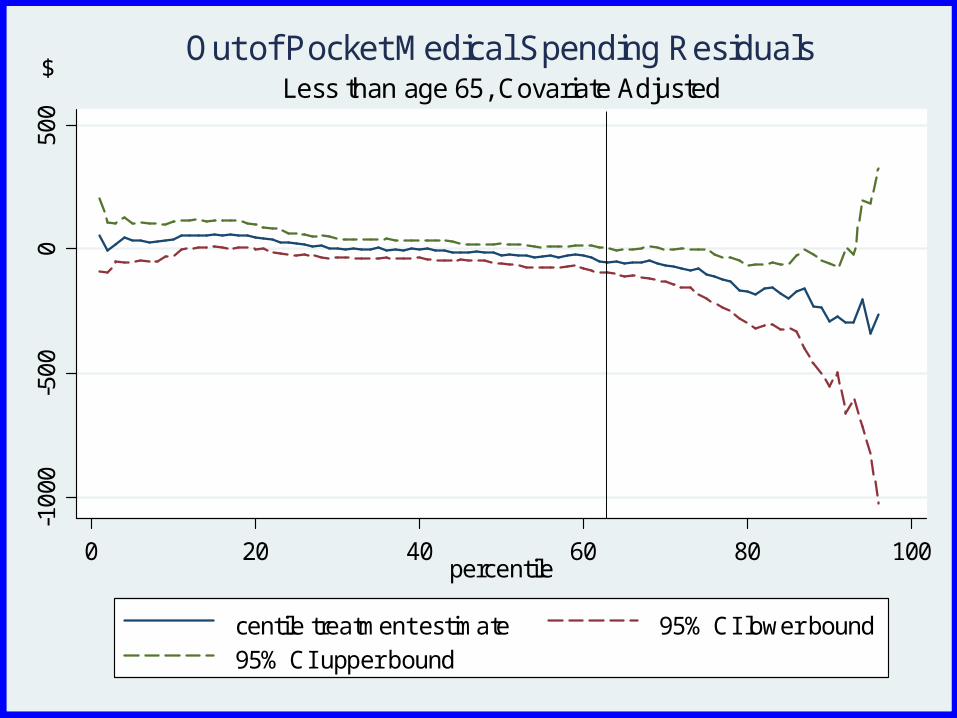

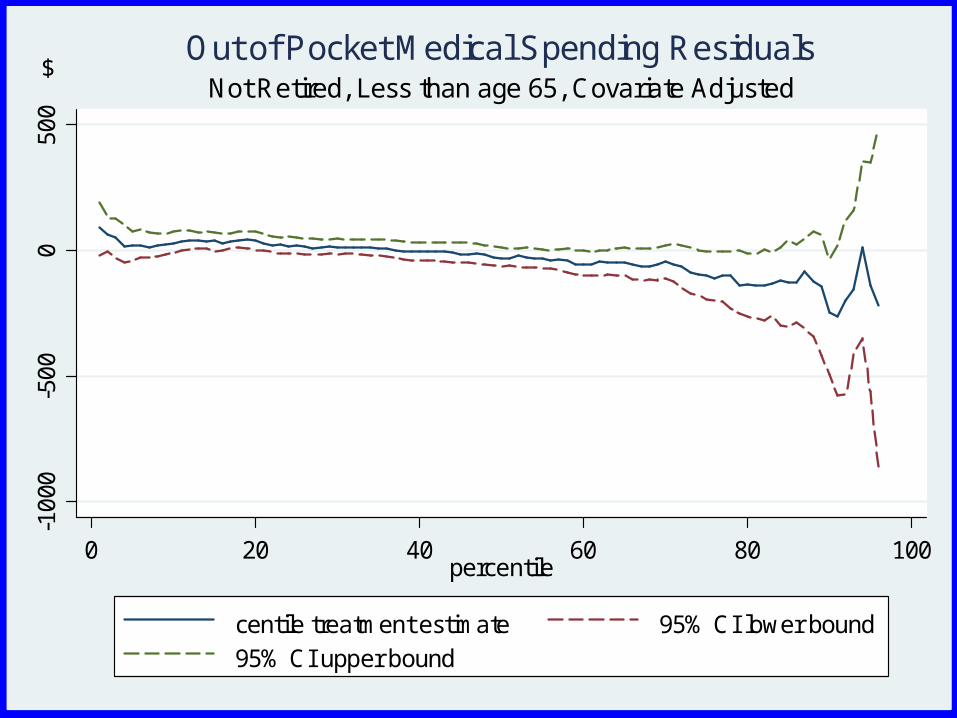

Out-of-Pocket Medical Care Spending

• Distribution of medical care spending significantly right-skewed

• Calculate residual out-of-pocket spending after controlling for age, sex, race, education, baseline health status and year

• Centile treatment effect:

Δ p = {resid spend p (offer = 1) – resid spend p (offer = 0)}

-100

0-5

000

500

0 20 40 60 80 100percentile

centile treatment estimate 95% CI lower bound 95% CI upper bound

Less than age 65, Covariate AdjustedOut of Pocket Medical Spending Residuals

$

-100

0-5

000

500

0 20 40 60 80 100percentile

centile treatment estimate 95% CI lower bound 95% CI upper bound

Not Retired, Less than age 65, Covariate AdjustedOut of Pocket Medical Spending Residuals

$

-800

0-6

000

-400

0-2

000

0

0 20 40 60 80 100percentile

centile treatment estimate 95% CI lower bound 95% CI upper bound

Retired, Less than age 65, Covariate AdjustedOut of Pocket Medical Spending Residuals

$

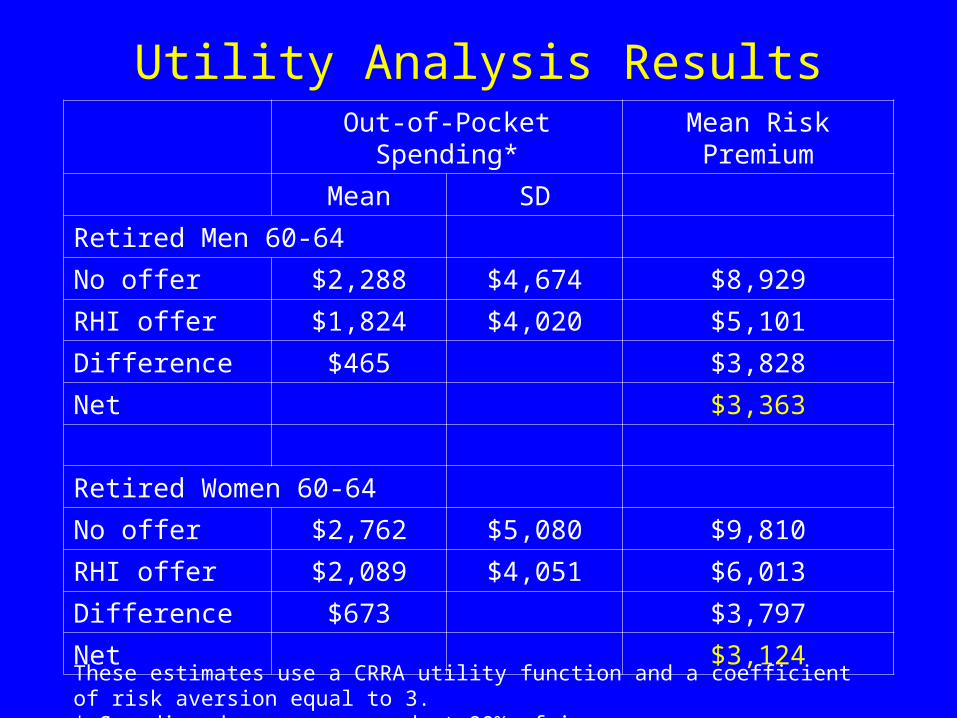

Insurance Value of RHI

• U (household income – out-of-pocket medical spending)

• Subject each individual to random draws from the empirical distribution of spending in the offered and not offered groups

• Calculate risk premia based on expected utility

Utility Analysis ResultsOut-of-Pocket Spending* Mean Risk

Premium

Mean SD

Retired Men 60-64

No offer $2,288 $4,674 $8,929

RHI offer $1,824 $4,020 $5,101

Difference $465 $3,828

Net $3,363

Retired Women 60-64

No offer $2,762 $5,080 $9,810

RHI offer $2,089 $4,051 $6,013

Difference $673 $3,797

Net $3,124These estimates use a CRRA utility function and a coefficient of risk aversion equal to 3.* Spending draws are capped at 90% of income.

Summary of Findings

• RHI offer increases the probability of early retirement by 35%

• RHI offer has no significant effects on health status

• RHI offer provides significant risk protection, decreasing out-of-pocket medical spending by 20% in the top 40% of the spending distribution among retirees

• Retired men aged 60-64 value RHI at about $3,400; women $3,100

Policy Implications

• Lower early retirement rates and delayed retirement

• Decreased financial risk protection: changes to individual insurance market and/or public programs

• Decline of employer-sponsored health insurance more broadly