Embed Size (px)

Citation preview

www.enbridgepartners.com

ENBRIDGE ENERGY PARTNERS, L.P.

1100 LOUISIANA, SUITE 3300

HOUSTON, TEXAS 77002

(713) 821-2000

ENBRIDGE ENERGY PARTNERS, L.P.

EN

BR

IDG

E E

NE

RG

YP

AR

TN

ER

S, L

.P.2

00

3 A

NN

UA

LR

EP

OR

T

2 0 0 3 A N N U A L R E P O R T

UnitholderInformation

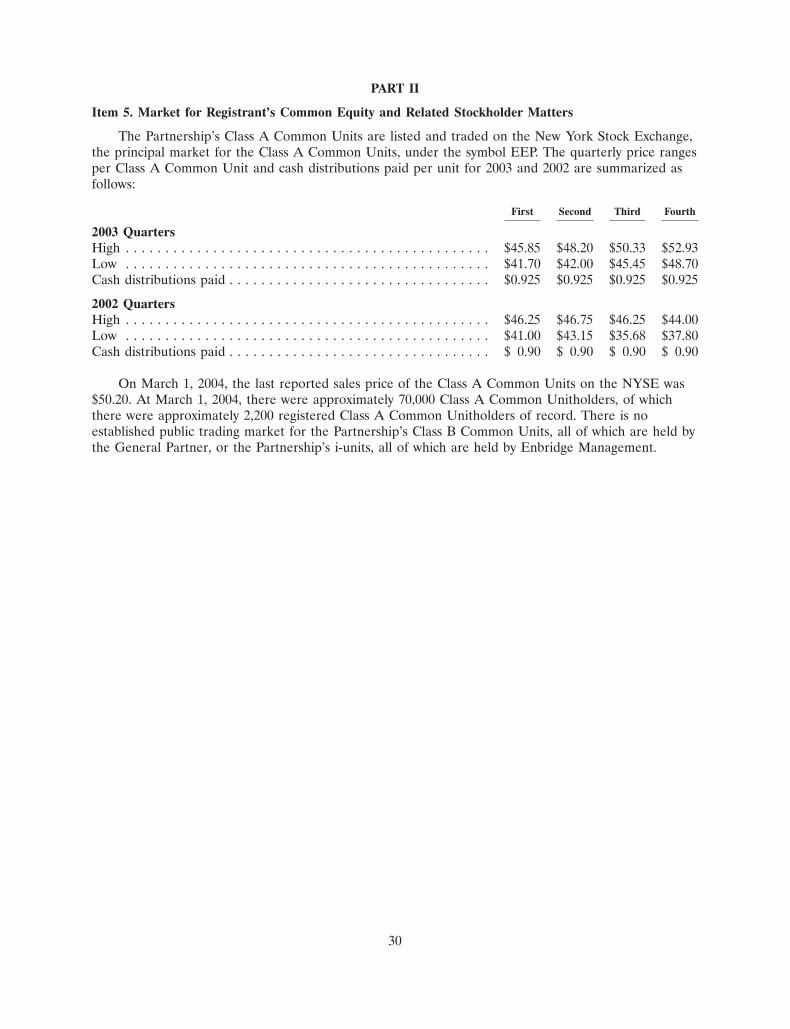

YEAR ENDED DECEMBER 31, 2003 2002

UNITS OUTSTANDING AT YEAR END (in thousands)

Class A Common 40,616 31,314Class B Common 3,913 3,913i-units 10,062 9,229

Approximate number of 70,000 48,000Unitholders at year end

CLASS A COMMON UNIT TRADING FOR YEAR

High $52.93 $46.75Low $41.70 $35.68Close $49.90 $42.15

The Partnership’s Class A Common Units are traded on the New YorkStock Exchange which is the principal market for the Partnership’sunits. All Class B Common Units are held by the General Partner andthere is no established trading market for these units. All i-units are heldby Enbridge Energy Management, L.L.C.

2004 PARTNERSHIP DISTRIBUTIONS INFORMATION

1ST Q 2ND Q 3RD Q 4TH Q

Declaration date Jan 22 Apr 26 Jul 22 Oct 22Ex-Dividend date Jan 29 May 3 Jul 29 Oct 28Record date Feb 2 May 5 Aug 2 Nov 1Payment date Feb 13 May 14 Aug 13 Nov 12

All dates are tentative until approved by the Board of Directors of theGeneral Partner.

To be entitled to a declared cash distribution, investors must havepurchased units at least one business day in advance of the Ex-Dividend date. Commencing on the Ex-Dividend date, units tradewithout entitlement to the recently declared cash distribution.

PARTNERSHIP CHARACTERISTICSEnbridge Energy Partners, L.P. is a publiclytraded master limited partnership. An invest-ment in a partnership differs in the followingsignificant ways from an investment in a corporation:

• A partner in a publicly traded partnership owns units of the partnership rather than shares of stock and receives cash distribu-tions rather than dividends. The cash dis-tributions are not taxable as long as the partner’s tax basis in the partnership exceeds zero.

• Generally, a corporation is subject to federal and state income taxes but a part-nership is not. All of the income, gains, losses and deductions of a partnership are passed through to its partners who are required to show their allocated share of these amounts on their personal incometax returns.

• In late February, unitholders (partners) are provided a tax package (Substitute Schedule K-1) required for preparation of their personal income tax returns. By comparison, a corporate stockholder typically receives a Form 1099 in late January detailing required tax data.

STOCK EXCHANGEThe Partnership’s Class A Common Unitsare traded on the New York Stock Exchangeusing ticker symbol EEP.

The shares of Enbridge Energy Manage-ment, L.L.C., exist one for one with thePartnership’s i-units and trade on the NewYork Stock Exchange, using ticker symbolEEQ.

TRANSFER AGENT AND REGISTRAREnbridge Energy Partners L.P.c/o Mellon Investor ServicesP.O. Box 3315So. Hackensack, NJ 07606Telephone: (888) 749-9483TDD:(800) 231-5469 (Hearing Assisted)

Internet:www.mellon-investor.com

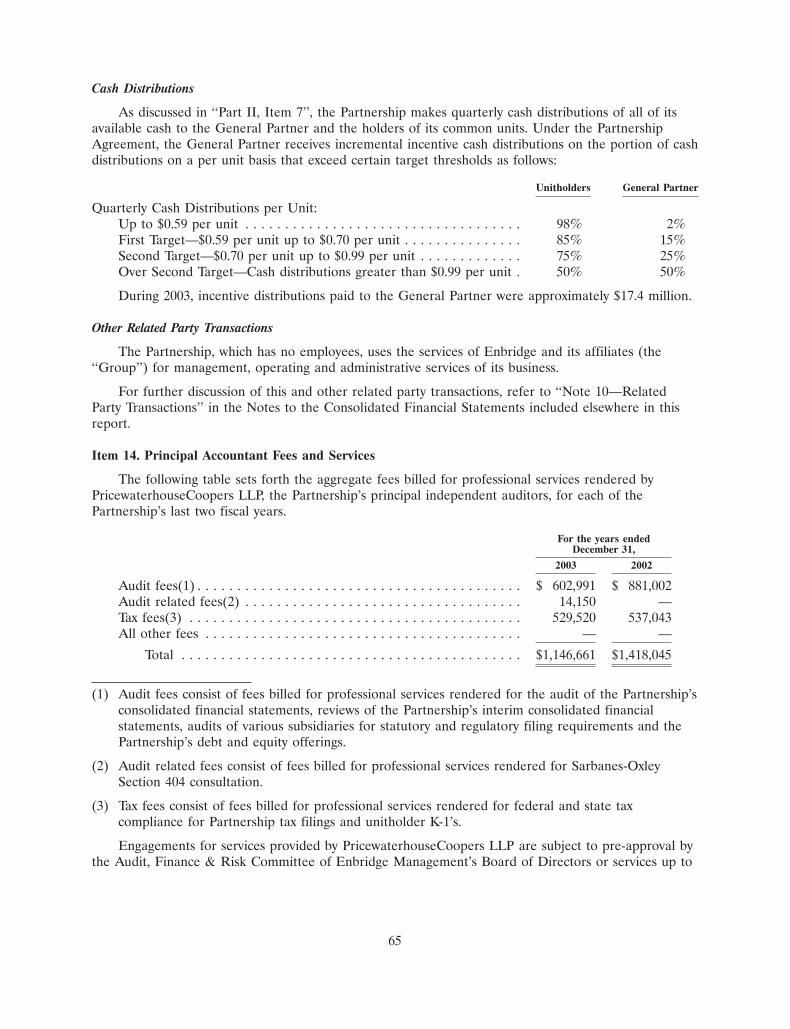

INDEPENDENT ACCOUNTANTSPricewaterhouseCoopers LLP1201 Louisiana, Ste. 2900Houston, Texas 77002

INFORMATIONInternetwww.enbridgepartners.com

Tax WebInvestor tax information (SubstituteSchedule K-1) is available via thePartnership Internet site.

Tax Call CenterToll Free: (800) 525-3999E-mail:[email protected]

Investor RelationsToll Free: (866) 337-4636

(866) EEP INFOFacsimile: (713) 821-2230E-mail:[email protected]

Media InquiriesTelephone: (713) 821-2253Facsimile: (713) 821-2230E-mail:[email protected]

E N B R I D G E E N E R G Y P A R T N E R S , L . P .2 0 0 3 A N N U A L R E P O R T

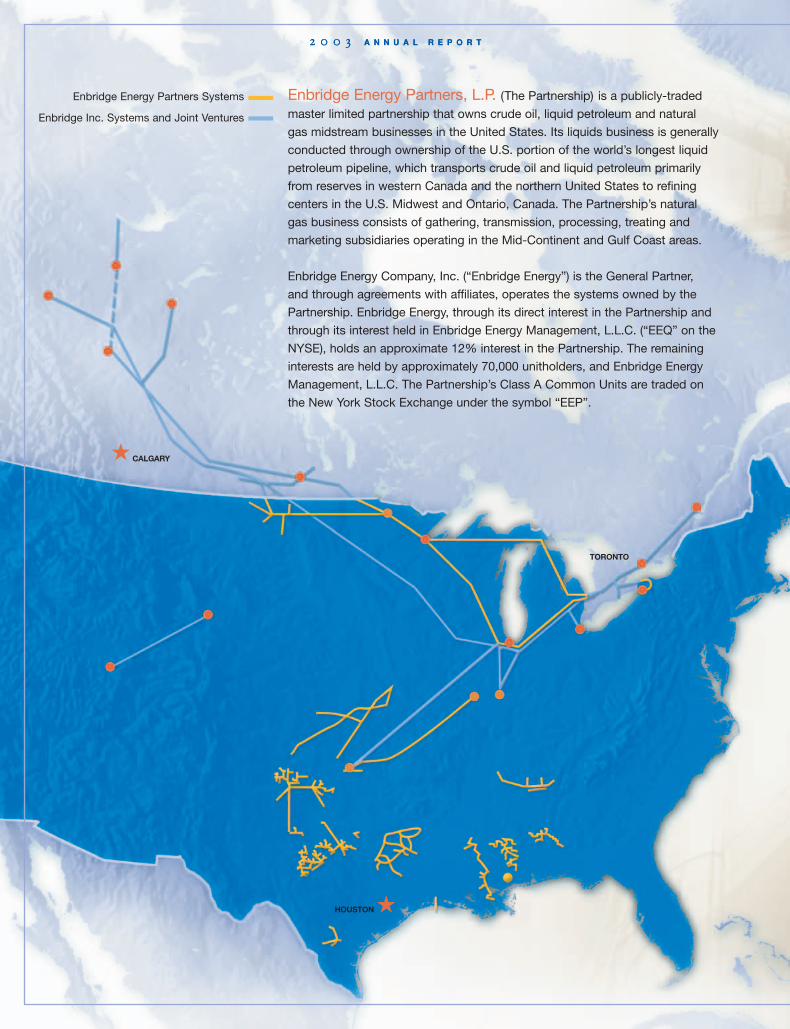

TORONTO

HOUSTON

CALGARY

Enbridge Energy Partners Systems

Enbridge Inc. Systems and Joint Ventures

Enbridge Energy Partners, L.P. (The Partnership) is a publicly-traded

master limited partnership that owns crude oil, liquid petroleum and natural

gas midstream businesses in the United States. Its liquids business is generally

conducted through ownership of the U.S. portion of the world’s longest liquid

petroleum pipeline, which transports crude oil and liquid petroleum primarily

from reserves in western Canada and the northern United States to refining

centers in the U.S. Midwest and Ontario, Canada. The Partnership’s natural

gas business consists of gathering, transmission, processing, treating and

marketing subsidiaries operating in the Mid-Continent and Gulf Coast areas.

Enbridge Energy Company, Inc. (“Enbridge Energy”) is the General Partner,

and through agreements with affiliates, operates the systems owned by the

Partnership. Enbridge Energy, through its direct interest in the Partnership and

through its interest held in Enbridge Energy Management, L.L.C. (“EEQ” on the

NYSE), holds an approximate 12% interest in the Partnership. The remaining

interests are held by approximately 70,000 unitholders, and Enbridge Energy

Management, L.L.C. The Partnership’s Class A Common Units are traded on

the New York Stock Exchange under the symbol “EEP”.

150.0

100.0

50.0

0 .02003 2002 2001 19992000

Net Income(dollars in millions)

4.00

3.80

3.60

3 .40

3 .20

3.002003 2002 2001 1999

Annual Distributions(per unit in dollars)

2000

1,500

1,400

1300

1,2002000 1999200120022003

1,600

1,500

1,400

1,300

1,2002003 2002 2001 19992000

Natural Gas Deliveries(Btu/d in billions)

Liquids Deliveries(bpd in thousands)

E N B R I D G E E N E R G Y P A R T N E R S , L . P .

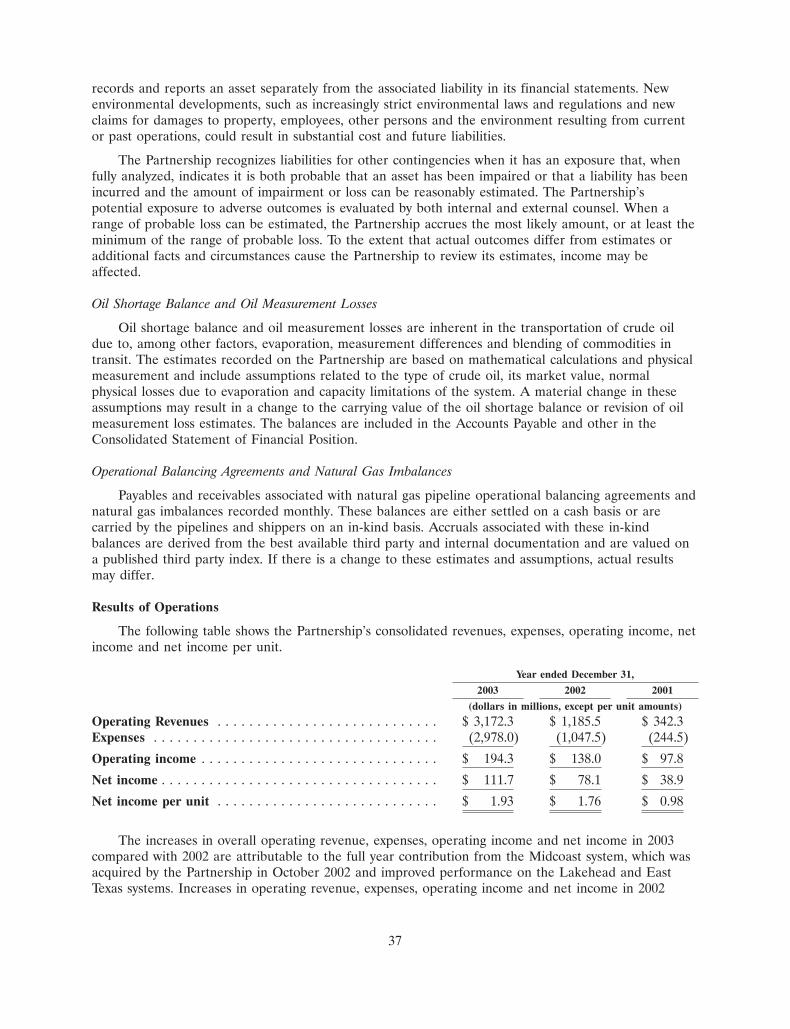

Year Ended December 31, 2003 2002 2001 2000 1999

Financial (dollars in millions)

Operating revenue $ 3,172.3 $ 1,185.5 $ 342.3 $ 307.0 $ 314.0Operating Income 194.3 138.0 97.8 117.9 131.7Net Income 111.7 78.1 38.9 60.2 78.7

Per Unit (in dollars)

Net Income 1.93 1.76 0.98 1.78 2.48Cash distributions 3.70 3.60 3.50 3.50 3.49

Operating

Deliveries Liquids Transportation (thousands of bpd)Lakehead System 1,354 1,302 1,315 1,338 1,369North Dakota System* 69 69 64 – –

1,423 1,371 1,379 1,338 1,369Deliveries Natural Gas Systems (MMBtu)

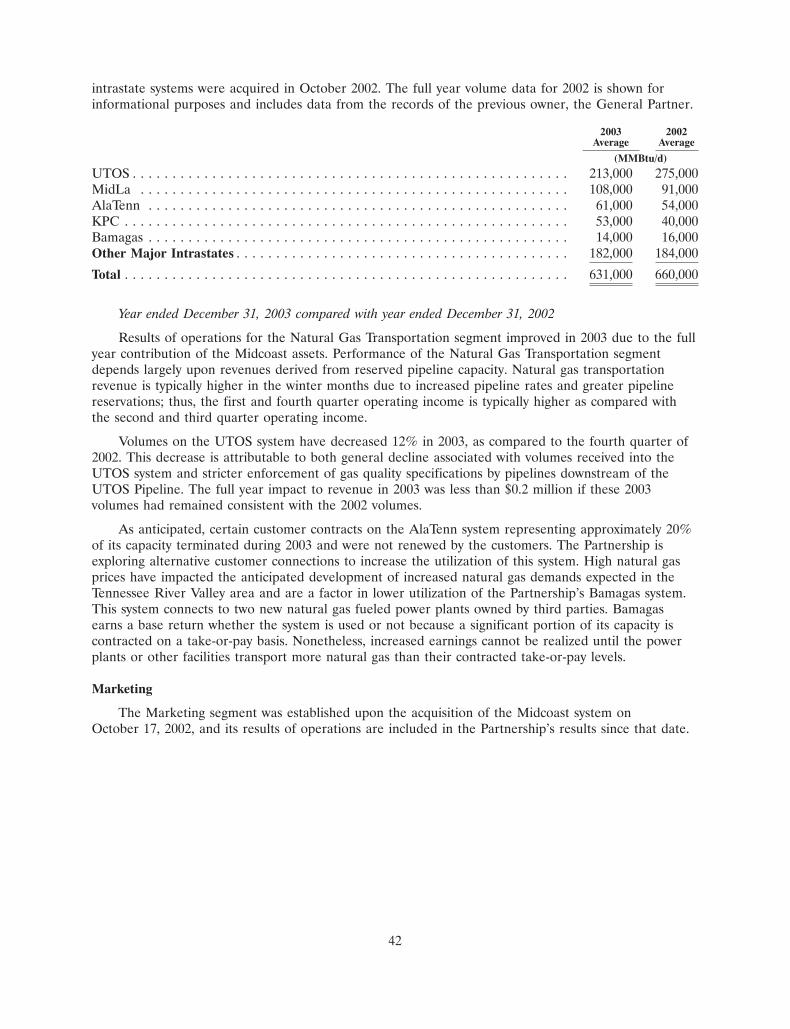

Major Transmission Systems 631 660** – – –Major Gathering Systems 873 767** – – –

1,504 1,427 – – –* Includes transmission system only

** The full year volume data for 2002 is shown for information purposes and includes data from the records of the previous owner, the General Partner.

Financial and Operating Highlights

1

FellowUnitholders

Our strategies served Enbridge Energy Partners, L.P. well during 2003.

Our disciplined growth strategy, steadfast focus on strong business funda-

mentals and our unwavering commitment to operational excellence and

corporate responsibility laid a foundation for 2004 and beyond to achieve

the long-term value you expect from your investment.

We have progressed by building on the strength of our core businesses — Liquids Transportation and Natural Gas Gathering, Processing andTransportation. During 2003, we:

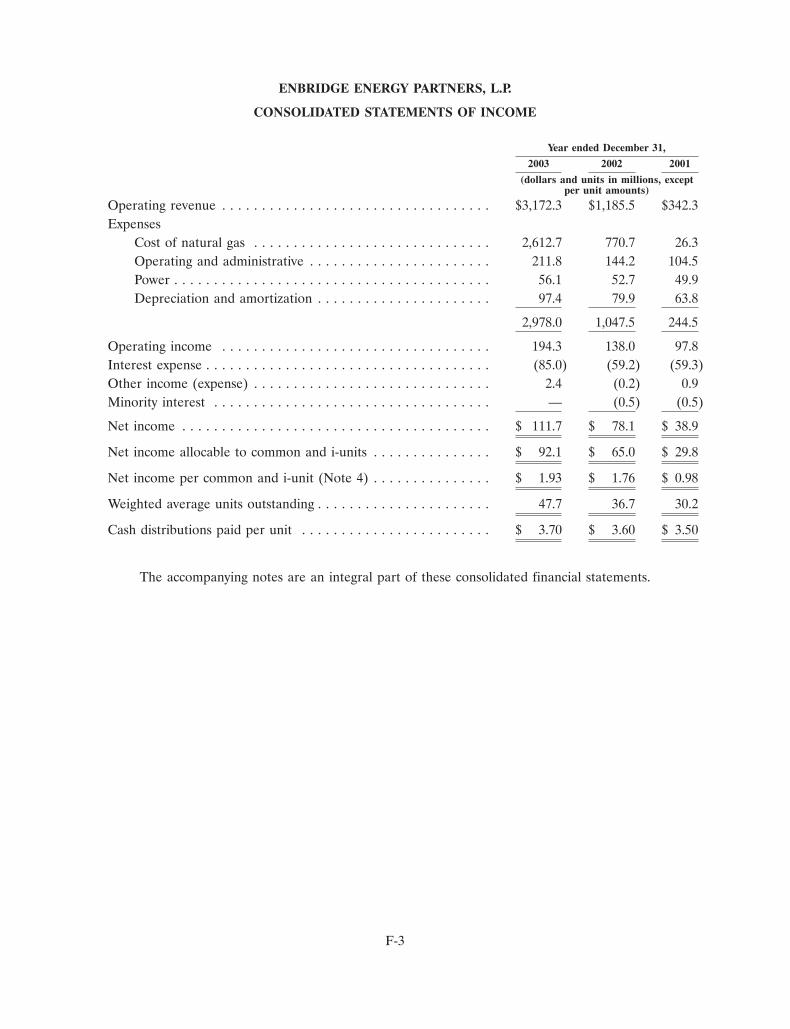

• Grew earnings per unit to $1.93 compared with $1.76 in 2002.

• Increased operating income by approximately 40% to $194.3 million, from $138.0 million, in 2002.

• Announced two significant acquisitions, totaling approximately $365 million, which will contribute to unitholder value.

In conjunction with Enbridge Inc., we rolled outa multi-step plan that will greatly expand access by U.S. refineries to growing crude oil supplies produced in the Alberta oil sands. Our LakeheadSystem is a key link in the transportation path.

2003 Performance Continued to Deliver Value

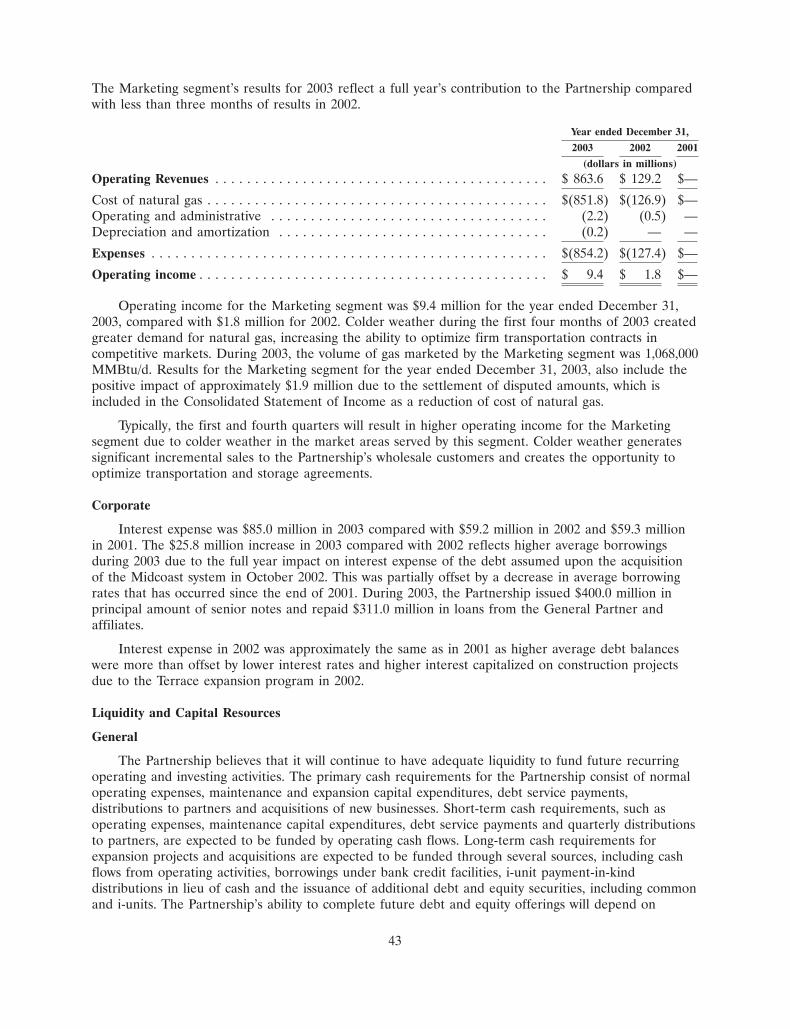

I am pleased with our progress during 2003.Enbridge Partners reported net income in 2003 of $111.7 million ($1.93 per unit) compared with $78.1 million ($1.76 per unit) in 2002. This improve-ment was largely attributable to a full year’s contribution from the natural gas systems acquiredfrom Enbridge Inc. in October 2002, as well asstronger performance on the Lakehead and EastTexas Systems.

The Partnership benefited from long-anticipatedincreases in throughput on the Lakehead System as production from Alberta’s oil sands expandedduring 2003. For the full year, deliveries averaged1.35 million barrels per day (bpd) compared to 1.30 million bpd during 2002. Lakehead deliv-eries averaged 1.46 million bpd during the fourth quarter of 2003, 9% higher than the 1.34 millionbpd recorded for the same period in 2002. This marked the first time since 1998 that averagequarterly deliveries exceeded the 1.4 million bpdthreshold; a strong positive indicator for futureLakehead System throughput.

During 2003, we successfully integrated andimproved performance of the Midcoast systems,which were acquired in October 2002. Natural gas volumes for the four largest gathering and pro-cessing systems (excluding the North TexasSystem acquired in December 2003) increasedapproximately 14% from an average of 767,000 million British thermal units (MMBtu) per day to873,000 MMBtu per day for 2003. A key contri-butor to volume growth was an increase in drillingactivity by natural gas producers due to higher natural gas prices. For the eleven major interstateand intrastate transmission pipeline systems, deliv-eries averaged 631,000 MMBtu per day for 2003 compared with 660,000 MMBtu per day for 2002.

2

E N B R I D G E E N E R G Y P A R T N E R S , L . P .

3

Competitive Strengths Support Positive Outlook

We have built a strong foundation to allow us tocapitalize on future growth opportunities.

The United States now imports nearly 63% of its total crude oil supply, with Canada the mostsecure source among the top four countries thatmeet this import demand. The Lakehead Systemdelivered approximately 64% of that Canadiancrude production to U.S. refineries. Canadianimports are expected to increase steadily in thefuture, principally due to the immense undevelopedoil reserves contained in the Alberta oil sands.

Our strategy to capitalize on this market positionis strengthened by the continued affiliation withEnbridge Inc. as demonstrated by our coordinatedefforts to expand access by U.S. refineries to growing Canadian crude oil supply. Specifically, in July 2003, Enbridge Inc. announced the acqui-sition of BP’s Cushing-to-Chicago pipeline, whichEnbridge plans to rename the “Spearhead System”.Planned reversal of this line in 2005 (subject to producer and regulatory approval) will attractincreased deliveries on the Lakehead System toChicago, the origination point of the SpearheadSystem. In October 2003, the Partnership announcedthe “Southern Access” expansion on the LakeheadSystem. This $550-$650 million pipeline is targetedfor completion in 2007 to further improve access to Canadian crude oil by refineries in America’sheartland.

A further step to expand and diversify thePartnership’s business was taken in December2003, when we announced the acquisition of crudeoil pipeline and terminal facilities from affiliates ofShell. This new “Mid-Continent System” suppliesMid-Continent area refineries with U.S. domesticand offshore crude, diversifying the Partnership’sliquids transportation cash flow beyond the histor-ical reliance on Canadian crude oil transportation.

We also implemented new commercial strategiesin the Mid-Continent and Gulf Coast to enhance theperformance of our natural gas gathering, process-ing and transportation assets. Mid-year 2003, weproposed construction of a 100-mile transmissionline in east Texas with capacity of up to 500 MMcfd.When complete in 2005, this new line will provideenhanced market access for our customers to theactive Carthage, Texas hub. On December 31, 2003,

we closed on the acquisition of the North TexasSystem, giving us an incremental 217 MMcfd ofprocessing capacity in the prolific Barnett Shaledevelopment, one of the most active onshore gasproducing regions in the United States.

I salute our employees for a job well done overthe past year. Through the efforts of our manage-ment team and exemplary workforce, we havesolidified our market presence in targeted regionsto meet energy transportation demand. Throughoperational excellence, we have delivered reliable,economical and safe service to our customers and the communities and environments where weoperate. These combined strengths will continue to deliver growth in unitholder value through core system expansions and complementary and profitable acquisitions.

We welcomed Martha Hesse as our newestboard member in March 2003. Ms. Hesse brings a great depth of industry, FERC and govern-ment experience to our Board and we appreciateher counsel.

We are excited about the opportunities aheadand are well positioned to generate superior totalreturns from a secure and growing asset base.

Dan C. Tutcher, PresidentEnbridge Energy Company, Inc.March 31, 2004

Defining the FutureThe Partnership’s broad geographic and commodity diversity positions us

to produce long-term value for our unitholders. At the end of 2003, we

owned more than 14,500 miles of crude oil, natural gas liquids, and natural

gas gathering and transmission pipelines. Our strong belief is that we

can succeed in growing the Partnership by pursuing a disciplined strategy

of profitable expansions and acquisitions that complement our asset

portfolio. Combined with committed leadership and a strong workforce,

these existing and new assets have laid a solid foundation for the Partnership

in 2003 and gives us a positive momentum in moving forward during 2004.

Disciplined Growth StrategyLast year, the Partnership focused on optimizing

existing assets and acquiring complementary sys-tems in the energy transportation sector. Today, weare securing new growth opportunities by:

• Meeting the demand of refineries in the Mid-Continent for increased access to growing Canadian crude oil supply;

• Diversifying the supply basins served by our liquids transportation business; and,

• Increasing our market presence in key natural gas production areas in Texas, including East Texas and the growing Barnett Shale development in the Fort Worth Basin.

Our core businesses include liquids transportationand natural gas assets in twenty states across theUnited States.

4

OperationalProfile

E N B R I D G E E N E R G Y P A R T N E R S , L . P .

Spanning approximately 1,900 miles across the United States, the Lakehead

System is operationally integrated with the pipeline system of Canadian

affiliate Enbridge Pipelines Inc.; and together they form the longest liquids

petroleum pipeline in the world. The combined mainline system has operated

since 1950 and spans more than 3,100 miles across North America. In 2003, the

Lakehead System transported approximately 64% of the crude oil exported

from Canada to the United States, feeding refineries in the Great Lakes region

and beyond.

The System extends to serve refineries in theProvince of Ontario through interconnects withEnbridge Pipelines at the Michigan-Canada border.The System re-enters the United States nearBuffalo, New York, and delivers crude oil throughinterconnecting pipelines to a Pennsylvania refinery.The Lakehead System has available tank storagecapacity of 14 million barrels and transported anaverage of 1.35 million barrels per day of crude oiland natural gas liquids in 2003.

In April 2003, the $195 million third phase of theTerrace expansion project was completed andincreased the Lakehead System’s delivery capacityby 140,000 bpd. In October 2003, a $41 million, 36-mile extension of one of the Chicago lines to theGriffith, Indiana terminal was completed; increasingthe Partnership’s delivery capability to Chicago-area refineries.

In October 2003, the Partnership announced further plans to expand the Lakehead System with a 630-mile pipeline from Superior, Wisconsinto Wood River, Illinois. Slated for startup in 2007, the approximate $600 million “Southern Access”

expansion project will increase capacity by 250,000to 400,000 bpd — meeting the demand of regionalrefineries for access to growing production fromAlberta’s vast oil sands reserves. The SouthernAccess project will extend the Lakehead Systembeyond Chicago, connect to Enbridge Inc.’sSpearhead System, and provide direct access to Canadian crude supplies for the large WoodRiver refinery center and beyond.

The North Dakota System consists of approx-imately 330 miles of crude oil gathering lines connected to 620 miles of transmission pipeline.During 2003, the North Dakota System trans-ported approximately 84,000 bpd of crude oil.Operational since the early 1960s, the NorthDakota System serves 36 crude oil fields in NorthDakota and Montana and has an interconnect with the affiliated Enbridge Saskatchewan Systemto transport western Canadian production. TheSystem serves the Mandan, North Dakota refineryand interconnects with the Lakehead System atClearbrook, Minnesota.

WOOD RIVER

CUSHING

CHICAGO

SUPERIOR

CLEARBOOK

BUFFALO

5

Liquids Transportation Business

The Mid-Continent System is a new addition to the Partnership’s liquids transportation port-folio. The $115 million acquisition was announcedin December 2003 and closed on March 1, 2004.The System includes the 433-mile Ozark pipeline, 47-mile West Tulsa pipeline, 8.3 million barrelCushing tank storage terminal, and 1.2 million barrel El Dorado storage terminal. Interconnectingpipelines transport crude petroleum from produc-tion fields in Oklahoma and nearby states to thePartnership’s Mid-Continent System that connectsto the Wood River refinery market.

Liquids Transportation Future OutlookStrong growth in production from Alberta’s oil

sands region is expected to continue well into thenext decade. Production rose more than 100,000bpd during 2003 with the commissioning of sev-eral oil sands projects including the Athabasca OilSands Project (AOSP). Completion of this project istangible evidence that the long-awaited growth inWestern Canadian Sedimentary Basin production ismaterializing.

In an effort to better understand the potentialfrom western Canada’s oil sands resource, Enbridgeinitiated a comprehensive study of North Americanoil markets. The study is providing important insight

and information to help further the development ofmarkets for the vast oil sands resource and corre-sponding transportation infrastructure.

The market study concluded that there are several significant adjustments needed in the infrastructure to respond to declining U.S. domes-tic production, changes in the North American refinery market structure, and increases in westernCanadian crude oil supply.

Two critical components in the plan include thepump station expansion of the Superior-to-Chicagoline underway in 2004 and the Lakehead System’sSouthern Access expansion project targeted forcompletion in 2007. The visionary plan also includesEnbridge Inc.’s Spearhead Pipeline acquisition andreversal that will benefit the Partnership as increasedsupplies are delivered from the Lakehead System tothe interconnect with Spearhead near Chicago. TheLakehead System will benefit from the expansion of Enbridge Inc.’s Toledo Pipeline which receivesdeliveries off the Lakehead System at Stockbridge,Michigan. By implementing a market strategy thatextends transportation of western Canadian pro-duction into the Mid-Continent, Enbridge is driving a change in the energy transportation landscape inAmerica’s heartland and potentially beyond.

The Alberta Oil Sands is a world-scale resource, with reserves comparable to those of Saudi Arabia. The oil sands deposits contain about 14% of the known oil reserves in the world. Northern Alberta, Canada, contains three major oil sands regions covering some 30,000 square miles. While most of North America’s crude oil production regions are maturing, the Alberta oil sands is in its initial development with cumulative production to the end of 2002 of 3.8 billion barrels and remaining established reserves of over 174 billion barrels. During 2003, the oil sands produced nearly 800,000 bpd, accounting for approxi-mately 37% of western Canadian oil production. Based on Enbridge’s annual producer survey, finalized in early 2003, the Partnershipexpects that oil sands production will grow to more than 1.5 bpd by 2010 and comprise approximately 58% of western Canadianoil production.

What are oil sands?The Alberta oil sands are naturally occurring mixtures of sand, water,clay, and approximately 12% bitumen, a tar-like petroleum oil. Thesesands can be found at varying depths, even near the surface. Near-surface deposits are mined, and the oil is then extracted from thesands using a steam extraction process. Deposits deep under-ground can be recovered through several processes, which canrange from conventional vertical pumps to technologies wheresteam or solvents are used to assist the oil flow and enhance oilrecovery. Currently, about 75% of the bitumen is upgraded into lightersynthetic crudes prior to transportation to refining markets.

AL

BE

RT

A O

IL S

AN

DS

Western Canadian Oil Production

1997 1999 2001 2003 2005 2007 2009 2011 2013

Conventional Oil

Oil Sands

FORECASTACTUAL

BPD (000)

3,000

2,500

2,000

1,500

1,000

500

-

Year

6

E N B R I D G E E N E R G Y P A R T N E R S , L . P .

Natural Gas Business

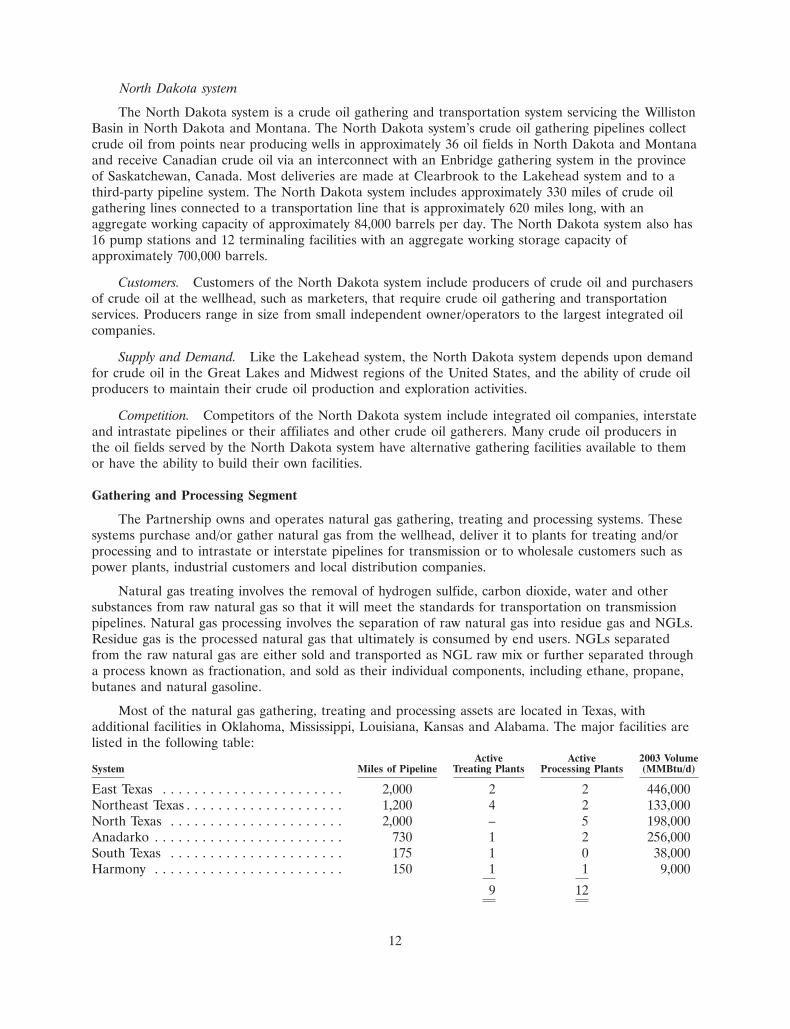

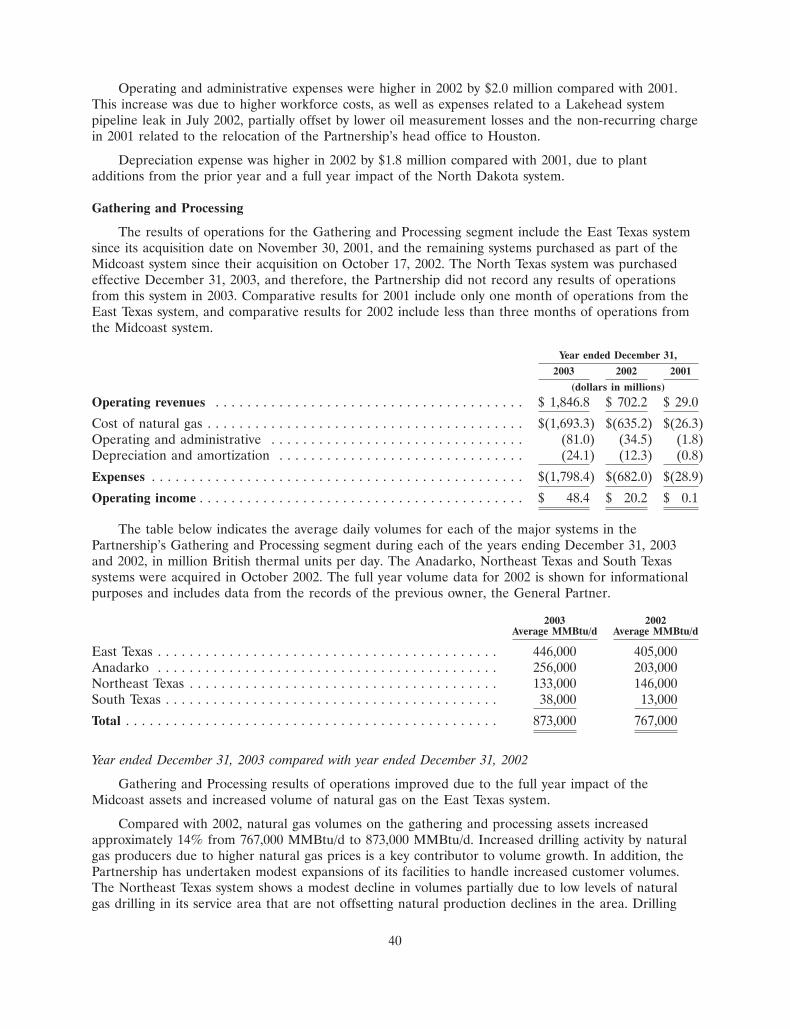

Natural Gas Gathering and Processing The Partnership’s five largest natural gas gather-

ing and processing systems include the EastTexas, Northeast Texas, Anadarko, South Texas andnewly acquired North Texas assets.

The 2,000-mile East Texas System provides natural gas gathering, treating and processing services and receives more than 446,000 MMBtuper day. The System includes two active treatingfacilities and two active processing plants. A pro-posed expansion to the East Texas System includesa new pipeline with capacity up to 500,000 MMcfper day supplementing the transportation con-nections to the active Carthage, Texas hub. Whencomplete in 2005, the pipeline will relieve trans-portation constraints now faced by shippers withproduction from regional natural gas developments.

Adjacent to the East Texas System is thePartnership’s 1,200 mile Northeast Texas System.The System currently handles approximately133,000 MMBtu of natural gas per day — a signif-icant portion of which contains hydrogen sulfideand/or carbon dioxide and is treated before trans-porting to downstream suppliers. The NortheastTexas System has four active treating plants andtwo active natural gas processing plants in Texas.

Further north, in the Texas Panhandle and western Oklahoma, is the Partnership’s 730-mileAnadarko System. The pipeline provides naturalgas gathering, treating and processing services andcurrently handles approximately 255,000 MMBtu ofnatural gas per day.

The South Texas System includes 175 miles ofnatural gas gathering pipelines and one treatingplant. During 2003, average delivery volumes were38,000 MMBtu per day.

Acquired in December 2003, the 2,000-mileNorth Texas System primarily serves the FortWorth Basin, including growing production from theBarnett Shale zone. Natural gas throughput on theSystem currently averages approximately 198,000MMBtu per day. The System includes five activeprocessing plants.

The Partnership also conducts natural gas liquid,crude oil and carbon dioxide trucking operationsthrough ownership of Dufour Petroleum, L.P.Approximately 100 trucks and trailers and 50 railcars transport natural gas liquids, crude oil and carbon dioxide, product treating and handlingequipment. Dufour also includes more than 400,000gallons of NGL storage facilities and a CO2 pro-cessing facility.

The Partnership offers value-added natural gas gathering, treating, processing

and transportation services to customers throughout the Mid-Continent and

Gulf Coast United States. The natural gas systems collectively comprise more

than 9,000 miles of gathering and transmission pipelines, 21 active treating and

processing plants, and the Dufour Petroleum trucking and rail operations.

Enbridge Energy Partners, L.P.

South Texas

HOUSTONEast Texas

Northeast Texas

North Texas

Palo Duro

Anadarko

Kansas Pipeline

Harmony

Midla

UTOS MLGT

Dufour Petroleum, L.P.

Magnolia

BamaGas

AlaTenn

7

Natural Gas Transportation The following are the Partnership’s interstate

transmission pipeline systems regulated by theFederal Energy Regulatory Commission (FERC).

• The Midla System is a 405-mile pipeline that serves a number of large industrial markets and municipal customers.

• The UTOS System is a 30-mile, 42-inch offshore natural gas transmission pipeline.

• The AlaTenn System consists of 380 miles of pipeline serving industry users and local distri-bution companies in an eight county area in Alabama, Mississippi and Tennessee.

• The Kansas System includes a 1,100-mile gas pipeline that transports natural gas from Oklahoma and western Kansas to the metropol-itan Wichita and Kansas City markets.

The major intrastate transmission pipelinesinclude the Bamagas Pipeline, Mid-Louisiana GasTransmission Pipeline, and Magnolia Pipeline. Theintrastate systems are commercially regulated atthe state level, with some segments subject to lim-ited FERC jurisdiction.

These major interstate and intrastate trans-portation systems serve wholesale customers in theMid-Continent and Gulf Coast areas of the UnitedStates, including power plants, industrial facilities,local distribution companies, large consumersseeking an alternative to their local distribution

company and shippers of natural gas, such as producers and marketers.

Natural Gas Marketing The Partnership’s marketing affiliate provides

natural gas supply, transportation, balancing andsales services to producers and wholesale cus-tomers on the gathering, transmission and wholesalecustomer pipelines as well as interconnected third-party pipelines. Our Marketing affiliate manages its commodity risk by concurrently negotiating andexecuting gas purchase and sales agreements.

The Marketing affiliate was recognized inDecember 2003 in the reputable Mastio Natural GasStudy. In the survey, Enbridge Marketing ranked12th of 38 natural gas marketers in North Americafor quality service.

Natural Gas Future Outlook Natural gas use in the United States is expected

to continue growing by 1-2% per year, driven byenvironmental advantages of natural gas energy.

In recent years, growth in U.S. gas supply has not kept pace with growth in demand, result-ing in higher prices. Although stronger prices have stimulated drilling activities, conventional gas pro- duction in the lower 48 states continues to declinedue to the maturity of most onshore basins. Areaswhere supply growth is expected are the RockyMountain region, deepwater Gulf Coast offshore,liquefied natural gas (LNG) imports and, in the

Non-Conventional Gas SuppliesTight gas sands, gas shales and coalbed methane are all

classified as non-conventional gas sources, but the distinctionis diminishing as technology is allowing the economical pro-duction of these supply sources.

Gas shales are organic-rich rock with a major portion of thegas resource adsorbed on and within the organic matter in theshale. The shale reservoir is both the source rock and the reser-voir rock — typically covering a large geographical area.

Tight gas sands are low-permeability, gas-bearing reservoirsof a number of rock types that also tend to extend over largegeographic areas. Coalbed methane is typical of the reservesin the Rockies.

The Barnett Shale and Bossier Sand zones are two exam-ples of high-potential plays in gas shales and tight gas sands,

respectively. As one of the most active drilling plays in theUnited States with a trillion cubic feet of natural gas everyseven square miles, the Barnett Shale is the largest producing gas field in Texas and covers 15 counties in North Texas. Annualwell additions have grown four-fold in the last two years.

The Bossier Sand play has emerged as one of the premierbasins in the onshore United States. A flurry of drilling hasoccurred since 1997 as production increased from 530 to 1,800wells in 2003.

Drilling and completion techniques continue to improve, whichlead to decreased costs and increased efficiencies, causingshale gas resources to become a major factor in meeting theenergy demands of the next decade.

NA

TU

RA

L G

AS

E N B R I D G E E N E R G Y P A R T N E R S , L . P .

longer term, Alaskan gas supplies. The Partnershipwill carefully monitor developments in these areasto determine opportunities for growth that are suit-able to our risk profile.

Non-conventional gas reserves, such as coal- bed methane and shale gas, will also play a role in increasing the total available supply in the UnitedStates. The Partnership is well positioned to takeadvantage of the growth in these non-con-ventional natural gas developments. The BarnettShale, the Bossier Trend and the Granite Wash arethree of the fastest growing natural gas develop-ments in the United States and are served by thePartnership’s North Texas, East Texas and AnadarkoSystems, respectively.

With our recent acquisition of the North TexasSystem, the Partnership’s gathering and process-ing systems are virtually contiguous from theAnadarko basin in the Texas Panhandle to EastTexas. We are therefore solidly positioned to offerincreased delivery flexibility for our customers. Forexample, our proposed East Texas transmissionpipeline is initially designed to offer increasedaccess to the Carthage hub, for East Texas produc-tion. In addition, options to link North Texas andAnadarko to this delivery route will be actively pursued. The Carthage hub is expected to emergeas a premium market for producers as supply anddelivery patterns evolve in Texas.

Committed LeadershipWe have continued to do what we do best — own

and operate pipelines and other fee-for-serviceassets. The depth and breadth of our leadership isclearly evident as we continued to integrate andimprove performance of the natural gas businessesacquired initially by Enbridge Inc. in 2001 and rolledinto the Partnership in late 2002. With each newacquisition, we have further solidified our marketposition and added to distributable cash flow.

We enjoy an exemplary workforce that supports our growing business and reinforces our core valuesof Integrity, Accountability, Innovation and Flexibility,Value Creation and Corporate Responsibility. Ourcore values provide the framework for operational

excellence and reliable, competitive service to ourcustomers and contribute to long-term investorvalue. Our commitment to corporate responsibilitydefines how we relate to our stakeholders throughperformance in environment, health, safety, gover-nance, community investment and stakeholder relations. We joined Enbridge Inc. in issuing our sec-ond annual Environment Health and Safety report and are in the process of jointly issuing the renamed“Corporate Responsibility” report for 2003.

We are excited about the future we are defining forthe Partnership and the corresponding growth inlong-term value for you, our stakeholders.

Jeffrey A. Connelly,

Ernest C. Hambrook,

Patrick D. Daniel,

Dan C. Tutcher,

J. Richard Bird,

George K. Petty,

and Martha O. Hesse

The Enbridge Energy Company, Inc.

Board of Directors are: (left to right)

2 0 0 3 A N N U A L R E P O R T

UnitholderInformation

YEAR ENDED DECEMBER 31, 2003 2002

UNITS OUTSTANDING AT YEAR END (in thousands)

Class A Common 40,166 31,314Class B Common 3,913 3,913i-units 10,062 9,229

Approximate number of 70,000 48,000Unitholders at year end

CLASS A COMMON UNIT TRADING FOR YEAR

High $52.93 $46.75Low $41.70 $35.68Close $49.90 $42.15

The Partnership’s Class A Common Units are traded on the New YorkStock Exchange which is the principal market for the Partnership’sunits. All Class B Common Units are held by the General Partner andthere is no established trading market for these units. All i-units are heldby Enbridge Energy Management, L.L.C.

2004 PARTNERSHIP DISTRIBUTIONS INFORMATION

1ST Q 2ND Q 3RD Q 4TH Q

Declaration date Jan 22 Apr 26 Jul 22 Oct 22Ex-Dividend date Jan 29 May 3 Jul 29 Oct 28Record date Feb 2 May 5 Aug 2 Nov 1Payment date Feb 13 May 14 Aug 13 Nov 12

All dates are tentative until approved by the Board of Directors of theGeneral Partner.

To be entitled to a declared cash distribution, investors must havepurchased units at least one business day in advance of the Ex-Dividend date. Commencing on the Ex-Dividend date, units tradewithout entitlement to the recently declared cash distribution.

PARTNERSHIP CHARACTERISTICSEnbridge Energy Partners, L.P. is a publiclytraded master limited partnership. An invest-ment in a partnership differs in the followingsignificant ways from an investment in a corporation:

• A partner in a publicly traded partnership owns units of the partnership rather than shares of stock and receives cash distribu-tions rather than dividends. The cash dis-tributions are not taxable as long as the partner’s tax basis in the partnership exceeds zero.

• Generally, a corporation is subject to federal and state income taxes but a part-nership is not. All of the income, gains, losses and deductions of a partnership are passed through to its partners who are required to show their allocated share of these amounts on their personal incometax returns.

• In late February, unitholders (partners) are provided a tax package (Substitute Schedule K-1) required for preparation of their personal income tax returns. By comparison, a corporate stockholder typically receives a Form 1099 in late January detailing required tax data.

STOCK EXCHANGEThe Partnership’s Class A Common Unitsare traded on the New York Stock Exchangeusing ticker symbol EEP.

The shares of Enbridge Energy Manage-ment, L.L.C., exist one for one with thePartnership’s i-units and trade on the NewYork Stock Exchange, using ticker symbolEEQ.

TRANSFER AGENT AND REGISTRAREnbridge Energy Partners L.P.c/o Mellon Investor ServicesP.O. Box 3315So. Hackensack, NJ 07606Telephone: (888) 749-9483TDD:(800) 231-5469 (Hearing Assisted)

Internet:www.mellon-investor.com

INDEPENDENT ACCOUNTANTSPricewaterhouseCoopers LLP1201 Louisiana, Ste. 2900Houston, Texas 77002

INFORMATIONInternetwww.enbridgepartners.com

Tax WebInvestor tax information (SubstituteSchedule K-1) is available via thePartnership Internet site.

Tax Call CenterToll Free: (800) 525-3999E-mail:[email protected]

Investor RelationsToll Free: (866) 337-4636

(866) EEP INFOFacsimile: (713) 821-2230E-mail:[email protected]

Media InquiriesTelephone: (713) 821-2253Facsimile: (713) 821-2230E-mail:[email protected]

E N B R I D G E E N E R G Y P A R T N E R S , L . P .2 0 0 3 A N N U A L R E P O R T

TORONTO

HOUSTON

CALGARY

Enbridge Energy Partners Systems

Enbridge Inc. Systems and Joint Ventures

Enbridge Energy Partners, L.P. (The Partnership) is a publicly-traded

master limited partnership that owns crude oil, liquid petroleum and natural

gas midstream businesses in the United States. Its liquids business is generally

conducted through ownership of the U.S. portion of the world’s longest liquid

petroleum pipeline, which transports crude oil and liquid petroleum primarily

from reserves in western Canada and the northern United States to refining

centers in the U.S. Midwest and Ontario, Canada. The Partnership’s natural

gas business consists of gathering, transmission, processing, treating and

marketing subsidiaries operating in the Mid-Continent and Gulf Coast areas.

Enbridge Energy Company, Inc. (“Enbridge Energy”) is the General Partner,

and through agreements with affiliates, operates the systems owned by the

Partnership. Enbridge Energy, through its direct interest in the Partnership and

through its interest held in Enbridge Energy Management, L.L.C. (“EEQ” on the

NYSE), holds an approximate 12% interest in the Partnership. The remaining

interests are held by approximately 70,000 unitholders, and Enbridge Energy

Management, L.L.C. The Partnership’s Class A Common Units are traded on

the New York Stock Exchange under the symbol “EEP”.

www.enbridgepartners.com

ENBRIDGE ENERGY PARTNERS, L.P.

1100 LOUISIANA, SUITE 3300

HOUSTON, TEXAS 77002

(713) 821-2000

ENBRIDGE ENERGY PARTNERS, L.P.

EN

BR

IDG

E E

NE

RG

YP

AR

TN

ER

S, L

.P.2

00

3 A

NN

UA

LR

EP

OR

T

Check Out Tax Web

on

www.enbridgepartners.com

Don’t wait for your K-1 to arrive by the U.S. Postal Service! Access the tax information you need via our website as soon as it is available in lateFebruary of each year.

Here’s what you can do at this site:

• View your tax schedules for the current year• Print your tax package including instructions• Automatically transfer amounts from your Schedule K-1 to IRS forms filed by individuals• Download your K-1 information into the TurboTax software• Request changes to incorrect information

Save this card as a reminder to access your K-1 from our website.

UNITED STATESSECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

� ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THESECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended DECEMBER 31, 2003

OR

� TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THESECURITIES EXCHANGE ACT OF 1934

For the transition period from to

Commission File Number: 1-10934

ENBRIDGE ENERGY PARTNERS, L.P.(Exact name of Registrant as specified in its charter)

Delaware 39-1715850(State or other jurisdiction of (I.R.S. Employer Identification No.)incorporation or organization)

1100 LouisianaSuite 3300

Houston, Texas 77002(Address of principal executive offices and zip code)

(713) 821-2000(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

Title of each class Name of each exchange on which registeredClass A Common Units New York Stock Exchange

Securities registered pursuant to Section 12(g) of the Act: NONE

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed bySection 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for suchshorter period that the Registrant was required to file such reports), and (2) has been subject to such filingrequirements for the past 90 days. Yes � No �

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is notcontained herein, and will not be contained, to the best of the Registrant’s knowledge, in definitive proxy orinformation statements incorporated by reference in Part III of this Form 10-K or any amendment to thisForm 10-K. �

Indicate by check mark whether the registrant is an accelerated filer (as defined in Rule 12b-2 of theAct) Yes � No �

The aggregate market value of the Registrant’s Class A Common Units held by non-affiliates computedby reference to the price at which the common equity was last sold, or the average bid and asked price ofsuch common equity, as of June 30, 2003, was $1,683,394,439.

DOCUMENTS INCORPORATED BY REFERENCE: NONE

TABLE OF CONTENTS

Page

PART IItems 1. & 2. Business and Properties . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6Item 3. Legal Proceedings . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 29Item 4. Submission of Matters to a Vote of Security Holders . . . . . . . . . . . . . . . . . . . . 29

PART IIItem 5. Market for Registrant’s Common Equity and Related Stockholder Matters . . . . 30Item 6. Selected Financial Data . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 31Item 7. Management’s Discussion and Analysis of Financial Condition and Results of

Operations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 32Item 7A. Quantitative and Qualitative Disclosures About Market Risk . . . . . . . . . . . . . . 54Item 8. Financial Statements and Supplementary Data . . . . . . . . . . . . . . . . . . . . . . . . . 56Item 9. Changes in and Disagreements with Accountants on Accounting and Financial

Disclosure . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 56Item 9A. Controls and Procedures . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 56

PART IIIItem 10. Directors and Executive Officers of the Registrant . . . . . . . . . . . . . . . . . . . . . . 57Item 11. Executive Compensation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 60Item 12. Security Ownership of Certain Beneficial Owners and Management . . . . . . . . . 63Item 13. Certain Relationships and Related Transactions . . . . . . . . . . . . . . . . . . . . . . . . 64Item 14. Principal Accountant Fees and Services . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 65

PART IVItem 15. Exhibits, Financial Statement Schedules and Reports on Form 8-K . . . . . . . . . . 66Signatures . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 67Index to Consolidated Financial Statements . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F-1

This Annual Report on Form 10-K contains forward-looking statements. These forward-lookingstatements are identified as any statement that does not relate strictly to historical or current facts. They usewords such as ‘‘anticipate,’’ ‘‘believe,’’ ‘‘continue,’’ ‘‘estimate,’’ ‘‘expect,’’ ‘‘forecast,’’ ‘‘intend,’’ ‘‘may,’’‘‘plan,’’ ‘‘position,’’ ‘‘projection,’’ ‘‘strategy,’’ could,’’ ‘‘should,’’ or ‘‘will’’ or the negative of those terms orother variations of them or comparable terminology. In particular, statements, expressed or implied,concerning future actions, conditions or events or future operating results or the ability to generate revenue,income or cash flow are forward-looking statements. Forward-looking statements are not guarantees ofperformance. They involve risks, uncertainties and assumptions. Future actions, conditions or events andfuture results of operations may differ materially from those expressed in these forward-looking statements.Many of the factors that will determine these results are beyond the ability of the Partnership to control orpredict. For additional discussion of risks, uncertainties and assumptions, see ‘‘Items 1. & 2. Business andProperties—Risk Factors’’ included elsewhere in this Form 10-K.

2

Glossary

The following abbreviations, acronyms, or terms used in this Form 10-K are defined below:

Act . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Pipeline Safety ActAnadarko system . . . . . . . . . . . . . . . . . . . . . . . . Natural gas gathering and processing assets

located in western Oklahoma and the Texaspanhandle, which were acquired on October 17,2002

AOSP . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Athabasca Oil Sands ProjectBbl . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Barrel of liquids (approximately 42 U.S. gallons)Bpd . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Barrels per dayCAA . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Clean Air ActCAPP . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Canadian Association of Petroleum Producers, a

trade association representing a majority of theLakehead system’s customers

CERCLA . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Comprehensive Environmental Response,Compensation, and Liability Act

Cdn. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Amount denominated in Canadian dollarsCold Lake . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Oil sands reserves in the province of Alberta,

CanadaCWA . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Clean Water ActDOT . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Department of TransportationEast Texas system . . . . . . . . . . . . . . . . . . . . . . . . Natural gas gathering, treating and processing

assets in East Texas acquired on November 30,2001

Enbridge . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Enbridge Inc., of Calgary, Alberta, Canada, theultimate parent of the General Partner

Enbridge Management . . . . . . . . . . . . . . . . . . . . Enbridge Energy Management, L.L.C.Enbridge system . . . . . . . . . . . . . . . . . . . . . . . . . Canadian portion of the SystemEnbridge Pipelines . . . . . . . . . . . . . . . . . . . . . . . Enbridge Pipelines Inc.Enbridge U.S. . . . . . . . . . . . . . . . . . . . . . . . . . . Enbridge (U.S.) Inc.Energy Policy Act . . . . . . . . . . . . . . . . . . . . . . . . Energy Policy Act of 1992EES . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Enbridge Employee Services, Inc.EPA . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Environmental Protection AgencyEpu . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Earnings per unitExchange Act . . . . . . . . . . . . . . . . . . . . . . . . . . . Securities Exchange Act of 1934FASB . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Financial Accounting Standards BoardFERC . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Federal Energy Regulatory CommissionGeneral Partner . . . . . . . . . . . . . . . . . . . . . . . . . Enbridge Energy Company, Inc., general partner

of the PartnershipHCA . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . High consequence areaHinshaw pipeline . . . . . . . . . . . . . . . . . . . . . . . . An intrastate pipeline that receives gas in

interstate commerce at or within the boundariesof the state and is ultimately consumed withinthat state.

HLPSA . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Hazardous Liquid Pipeline Safety ActICA . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Interstate Commerce ActKPC . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Kansas Pipeline CompanyLakehead Partnership . . . . . . . . . . . . . . . . . . . . . Enbridge Energy, Limited Partnership, a

subsidiary of the Partnership

3

Lakehead system . . . . . . . . . . . . . . . . . . . . . . . . U.S. portion of the SystemLIBOR . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . London Interbank Offered Rate—British Bankers

Association’s average settlement rate for depositsin U.S. dollars

MMBtu/d . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Million British Thermal units per dayMMcf/d . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Million cubic feet per dayMidcoast system . . . . . . . . . . . . . . . . . . . . . . . . . Natural gas gathering, treating, processing,

transmission and marketing assets comprised ofthe Midcoast system, Northeast Texas System andSouth Texas System.

NEB . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . National Energy BoardNGA . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Natural Gas ActNGL or NGLs . . . . . . . . . . . . . . . . . . . . . . . . . . Natural gas liquidsNGPA . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Natural Gas Policy ActNorth Dakota system . . . . . . . . . . . . . . . . . . . . . Liquids petroleum pipeline system in the Upper

MidwestNortheast Texas system . . . . . . . . . . . . . . . . . . . . Natural gas gathering and processing assets

acquired on October 17, 2002North Texas system . . . . . . . . . . . . . . . . . . . . . . Natural gas gathering and processing assets

acquired on December 31, 2003NYMEX . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . The New York Mercantile Commodity Exchange

where natural gas futures, options contracts, andother energy futures are traded.

NYSE . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . New York Stock ExchangeOBA . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Operational balancing agreementOCSLA . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Outer Continental Shelf Lands ActOPA . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Oil Pollution ActOPS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Office of Pipeline SafetyOSHA . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Occupational Safety and Health AdministrationOTC . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Over-the-Counter derivatives are privately

negotiated contracts between two parties and arenot limited to restrictions of contracts traded onexchanges

PADD . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Petroleum Administration for Defense DistrictsPADD II . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Consists of Illinois, Indiana, Iowa, Kansas,

Kentucky, Michigan, Minnesota, Missouri,Nebraska, North Dakota, Ohio, Oklahoma, SouthDakota, Tennessee and Wisconsin

PADD III . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Consists of Alabama, Arkansas, Louisiana,Mississippi, New Mexico and Texas

PADD IV . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Consists of Idaho, Montana, Wyoming andColorado

PADD V . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Consists of Washington, Oregon, California,Arizona, Alaska, Hawaii and Nevada

Partnership Agreement . . . . . . . . . . . . . . . . . . . . Third Amended and Restated Agreement ofLimited Partnership of the Partnership

Partnership . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Enbridge Energy Partners, L.P. and subsidiariesPPIFG-1 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Producer Price Index for Finished Goods minus

1%PSA . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Pipeline Safety ActRCRA . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Resource Conservation and Recovery Act

4

RSPA . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Research and Special Programs AdministrationSAGD . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Steam Assisted Gravity DrainageSEC . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Securities and Exchange CommissionSEP II . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . System Expansion Program IISettlement Agreement . . . . . . . . . . . . . . . . . . . . A FERC approved settlement agreement, signed

October 1996SFAS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Statement of Financial Accounting StandardsSFPP . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Santa Fe Pacific Pipelines, L.P., an unrelated

companySPCC . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Spill Prevention, Control and CountermeasureSuncor . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Suncor Energy Inc., an unrelated companySyncrude . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Syncrude Canada Ltd., an unrelated companySystem . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . The combined liquid petroleum pipeline

operations of the Lakehead system and theEnbridge system

Tariff Agreement . . . . . . . . . . . . . . . . . . . . . . . . A 1998 offer of settlement filed with the FERCTerrace . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Terrace Expansion ProgramWCSB . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Western Canadian Sedimentary Basin

5

PART I

Items 1. & 2.—Business & Properties

OVERVIEW

The Partnership is a publicly traded Delaware limited partnership that owns and operates crude oiland liquid petroleum transportation assets and natural gas gathering, treating, processing, transmissionand marketing assets in the United States. The Class A common units of the Partnership are traded onthe NYSE under the symbol ‘‘EEP.’’

The Partnership was formed in 1991 by the General Partner to own and operate the Lakeheadsystem, which is the U.S. portion of a crude oil and liquid petroleum pipeline system extending fromwestern Canada through the upper and lower Great Lakes region of the United States to easternCanada. Since the Partnership’s initial public offering in 1991, it has increased its quarterly cashdistribution by 57% from $0.59 per unit to the current quarterly rate of $0.925 per unit.

The Partnership’s ownership is comprised of a 2% general partner interest and a 98% limitedpartner interest. The General Partner owns the 2% general partner interest and a 7.1% limited partnerinterest, in the form of 3,912,750 Class B common units in the Partnership. The remaining 90.9%limited partner interest is represented by a 72.7% ownership interest of 40,166,134 publicly tradedClass A common units and an 18.2% ownership interest of 10,062,170 i-units, which are wholly-ownedby Enbridge Management.

Enbridge Management is a Delaware limited liability company that was formed on May 14, 2002.Enbridge Management’s shares represent limited liability company interests and are traded on theNYSE under the symbol ‘‘EEQ.’’ Its principal asset is its 18.2% limited partnership interest in thePartnership through its ownership of i-units. Enbridge Management’s principal activity is managing thebusiness and affairs of the Partnership and its subsidiaries. Under a Delegation of Control Agreement,the General Partner delegated substantially all of its power and authority to manage the business andaffairs of the Partnership to Enbridge Management. The General Partner, through its direct ownershipof the voting shares of Enbridge Management, elects all of the directors of Enbridge Management.

Since May 2001, the Partnership has diversified its operations both geographically and by industry.The North Dakota system, acquired in May 2001, connects to the Partnership’s Lakehead system andaccessed a different crude oil supply basin in North Dakota and Montana. The East Texas system,acquired in November 2001, was the Partnership’s first entry into the natural gas gathering andprocessing business and diversified the geographic focus of the Partnership to include the southernUnited States. In October 2002, the Partnership continued its diversification through the acquisition ofthe Midcoast system, which included natural gas gathering, treating, processing, transmission andmarketing activities located in the southern United States. On December 31, 2003, the Partnershipacquired the North Texas system, a natural gas gathering and processing business in Texas.

AVAILABLE INFORMATION

The Partnership files annual, quarterly and other reports and information with the SEC under theExchange Act. You may read and copy any materials that the Partnership files with the SEC at theSEC’s Public Reference Room at 450 Fifth Street, NW, Washington, DC 20549. You may obtainadditional information about the Public Reference Room by calling the SEC at 1-800-SEC-0330. Inaddition, the SEC maintains an Internet site http://www.sec.gov that contains reports, proxy andinformation statements, and other information regarding issuers that file electronically with the SEC,including the Partnership.

The Partnership also makes available free of charge on or through its Internet websitehttp://www.enbridgepartners.com its Annual Report on Form 10-K, Quarterly Reports on Form 10-Q,Current Reports on Form 8-K and other information statements, and if applicable, amendments to

6

those reports filed or furnished pursuant to Section 13(a) of the Exchange Act as soon as reasonablypracticable after the Partnership electronically files such material with the SEC.

BUSINESS STRATEGY

The primary strategy of the Partnership is to grow cash distributions through the profitableexpansion of existing assets and through the development and acquisition of complementary businesseswith risk profiles similar to the Partnership’s current business.

A number of developments in 2003 strengthened the Partnership’s position as a crude oil carrierinto the U.S. Mid-Continent. The Partnership continues to expand the Lakehead system’s capacitythrough the construction of Terrace and the complementary expansion of pipeline facilities in theChicago area. CAPP had requested these expansions, in anticipation of future growth in crude oilproduction from the prolific Alberta oil sands. In September 2003, Enbridge purchased a crude oilpipeline that currently flows from Cushing, Oklahoma to Chicago, Illinois. Enbridge intends to reversethe direction of flow on this system, which should ultimately increase market access for Canadian crudeoil delivered on the Lakehead system. In December 2003, the Partnership announced the acquisition ofcrude oil pipeline and storage facilities in the U.S. Mid-Continent, which closed in the first quarter of2004. This acquisition is expected to be accretive to cash distributions while, at the same time,increasing the diversity of sources of crude oil, thereby reducing the Partnership’s dependence onwestern Canadian crude oil volumes.

The Partnership continues to grow its natural gas business with the acquisition of the North Texasgathering and processing system on December 31, 2003, adding to its presence in Texas. EffectiveOctober 2003, the Partnership made a decision to proceed with the construction of a pipeline toconnect its East Texas system to the Carthage, Texas hub. Carthage access is important to shippersbecause it offers a number of connections to interstate natural gas pipelines. These projects areallowing the Partnership to achieve a larger scale and geographic profile from its East Texas system toits Anadarko system in the Texas panhandle, where it can pursue commercial and operating synergiesthat will make it the operator of choice in Texas.

The Partnership will continue to analyze potential acquisitions, with a focus on crude oil, refinedproducts and natural gas pipelines, terminals and related facilities. Major energy companies have soldtheir non-strategic assets in recent years, continuing the trend of rationalization of the energyinfrastructure in the United States. The Partnership expects this trend to continue and believes it iswell positioned to participate in these opportunities. The Partnership will seek out opportunitiesthroughout the United States, particularly in the U.S. Gulf Coast area, where asset divestitures areanticipated in and around its existing natural gas gathering, processing and transportation businesses.

BUSINESS SEGMENTS

The Partnership conducts its business through four business segments: Liquids Transportation,Gathering and Processing, Natural Gas Transportation and Marketing.

• Liquids Transportation includes the operations of a common carrier pipeline and a feederpipeline, which transport crude oil and other liquid hydrocarbons.

• Gathering and Processing consists of natural gas gathering pipelines, treating plants andprocessing plants. This segment also includes the transportation of natural gas liquids, crude oiland carbon dioxide by rail and road.

• Natural Gas Transportation includes the operations of natural gas transmission pipeline systems.

• The Marketing segment provides natural gas supply, transmission and sales services forcustomers.

7

Liquid Transportation Segment

Lakehead system

The Lakehead system in the United States and the Enbridge system in Canada, which is owned byEnbridge Pipelines, a wholly-owned subsidiary of Enbridge, together form the System. The System,which spans 3,100 miles, is the longest liquid petroleum pipeline system in the world and transportscrude oil and other liquid petroleum products as a common carrier. The System is the primarytransporter of crude oil from western Canada to the United States and the only pipeline that transportscrude oil from western Canada to the province of Ontario in eastern Canada.

The System serves all the major refining centers in the Great Lakes and upper Midwest regions ofthe United States and the province of Ontario, and, through interconnects, the Patoka/Wood Riverpipeline hub located in southern Illinois. Deliveries of crude oil and NGLs from the Lakehead systemare made principally to refineries, either directly or through connecting pipelines of other companies,and serve as feedstocks for refineries and petrochemical plants.

The Lakehead system is a FERC regulated interstate common carrier pipeline system. TheLakehead system spans approximately 1,900 miles, and consists of approximately 3,300 miles of pipewith diameters ranging from 12 inches to 48 inches, 59 pump station locations with a total ofapproximately 752,000 installed horsepower and 60 crude oil storage tanks with an aggregate workingcapacity of approximately 14 million barrels. The System operates in a segregation, or batch mode. Thisoperating mode allows the Lakehead system to transport up to 45 different types of liquidhydrocarbons including light, medium and heavy crude oil (including bitumen, which is a naturallyoccurring tar-like mixture of hydrocarbons), condensate and NGLs. This flexibility increases utilizationof the system and enhances the Partnership’s ability to serve its customers.

Customers. The Lakehead system operates under month-to-month transportation arrangementswith its shippers. During 2003, 36 shippers tendered crude oil and liquid petroleum for delivery throughthe Lakehead system. These customers include integrated oil companies, major independent oilproducers, refiners and marketers.

Supply and Demand. The Lakehead system is well positioned as the primary transporter ofwestern Canadian crude oil and will benefit from the growing production of crude oil from the Albertaoil sands. As with U.S. domestic conventional crude oil production, western Canada’s conventionalcrude oil production is in decline. More than offsetting this decline is substantial growth in productionfrom Canada’s prolific oil sands resource from the WCSB.

The western Canadian oil sands are naturally occurring mixtures of sand, water, clay, andapproximately 12% bitumen. According to the Alberta Energy and Utilities Board, using existingtechnology, knowledge and economics, the remaining recoverable bitumen reserves in the province ofAlberta were estimated at the end of 2002 at approximately 174 billion barrels. This represents arecovery of approximately 10% of the initial volume in place (over 1.6 trillion barrels). The cumulativeproduction of bitumen to the end of 2002 stood at approximately 3.8 billion barrels. According toindustry sources, the economics of producing bitumen have improved substantially from the late 1970’swhen average production costs were nearly $23 per barrel (including extraction and upgrading costs).Bitumen production must be blended with lighter, less viscous materials to permit transportation viapipelines to refinery markets. Alternatively, bitumen can be upgraded into a synthetic crude oil to meetthe demand from a greater number of refineries. Recent industry estimates of the cost of producingupgraded crude oil from the bitumen deposits are $7 to $10 per barrel.

Firms involved in the development of heavy crude oil from the Alberta oil sands have investedapproximately $20.0 billion since 1995, with additional previously announced extraction or up-graderprojects valued in excess of approximately $30.0 billion over the next ten years. This could provide upto 1.5 million bpd of incremental crude oil production from western Canada. Based upon Enbridge’s

8

survey of producers, refiners and governments conducted in early 2003, the supply of western Canadiancrude oil and liquid petroleum is expected to be approximately 2.3 million bpd in 2004, 2.5 million bpdin 2005 and approximately 2.8 million bpd in 2010.

Although substantially all of the crude oil and liquid petroleum delivered through the Lakeheadsystem originates in oilfields in western Canada, the Lakehead system also receives approximately 5%of its receipts from domestic sources including:

• U.S. and Canadian production at Clearbrook, Minnesota through a connection with the NorthDakota system;

• U.S. production at Lewiston, Michigan; and

• both U.S. and offshore production in the Chicago area.

Supply from the WCSB, and hence future deliveries on the Lakehead system, is expected to growover 2003 levels. The near-term growth in supply comes from the completion of the Syncrude andSuncor oil sands expansions and full year production from the AOSP and Cold Lake expansions.Syncrude and Suncor were the original oil sands producers in northern Alberta, and AOSP and ColdLake expansions are separate producers and producing areas.

During the fourth quarter of 2003, Syncrude announced the completion of the second mining trainat its Aurora Mining site, which increases the bitumen mining capacity of the Syncrude project inpreparation for its Aurora Upgrader Expansion project. With the completion of this project, Syncrude’ssynthetic crude oil production capacity is expected to grow to approximately 350,000 bpd by 2005-2006from approximately 230,000 bpd in 2002.

Suncor began upgrading bitumen from the first phase of its Firebag in-situ oil sands developmentnear the end of 2003. Firebag phase one is expected to reach full production capacity of 35,000 bpd ofbitumen production in mid-2005. When complete, the first phase of Firebag and expanded upgraderfacilities are expected to bring Suncor’s production capacity to 260,000 bpd in 2005, compared with205,000 bpd in 2002.

The AOSP, owned by Shell Canada Limited (60%), Chevron Canada Limited (20%) and WesternOil Sands L.P. (20%) began commercial operation in June 2003. AOSP consists of oil sands mining andbitumen extraction operations in the Fort McMurray, Alberta region with transportation to the FortSaskatchewan, Alberta area for upgrading to sweet and heavy synthetic crude oil products. Productionfrom this operation averaged 122,500 bpd during initial operations in 2003. The project has a designcapacity to process 155,000 of bpd bitumen.

Imperial Oil Limited recently completed certain phases of its Cold Lake expansion project. Thisproject is expected to increase overall WCSB bitumen production by 30,000 bpd in 2004.

Based on the above noted oil sands activity and its most recent survey of crude oil shippers, thePartnership estimates that deliveries on the Lakehead system will average approximately 1.45 millionbpd in 2004, an increase of approximately 100,000 bpd over 2003. The Partnership further believes thatthe outlook for increased crude oil production in western Canada continues to be positive and willyield additional volumes. In that event, the Partnership should expect increased earnings contributionsfrom the Lakehead system. As an example, an incremental 100,000 bpd of deliveries on the Lakeheadsystem to Chicago would increase operating income by approximately $10.0 million. The Partnershipexpects that increased capacity utilization on the Lakehead system should support a significantcomponent of its future earnings growth. The timing of growth in the supply of western Canadiancrude oil will depend upon the level of crude oil prices, oil drilling activity, the development of the oilsands resource, and access to compatible markets for Canadian oil sands production.

The Partnership’s ability to increase deliveries and to expand its Lakehead system in the future willultimately depend upon numerous factors. The investment levels and related development activities by

9

crude oil producers in conventional and oil sands production directly impacts the level of supply fromthe WCSB. Investment levels are influenced by crude oil producers’ expectations of crude oil andnatural gas prices. Higher crude oil production from the WCSB should result in higher deliveries onthe Lakehead system. Deliveries on the Lakehead system are also affected by periodic maintenance,turnarounds and other shutdowns at producing plants that supply crude oil to, or refineries that takedelivery from, the System.

The Partnership forecasts that demand for WCSB production will continue to increase in PADDII, which is the U.S. Government’s designation for the area that includes the Great Lakes and Midwestregions of the United States. PADD II refinery configurations and crude oil requirements continue tobe an attractive market for western Canadian supply. According to the U.S. Department of Energy’sEnergy Information Administration, demand for crude oil in PADD II increased from approximately2.75 million bpd in 1984 to approximately 3.2 million bpd in 2002. Over that same period, productionof crude oil within PADD II decreased from over 1.0 million bpd to approximately 450,000 bpd. ThePartnership expects this gap between PADD II demand and production will continue to widen,contributing to increased demand for imports of crude oil to PADD II.

The closure of Petro-Canada’s Oakville, Ontario refinery in late 2004, is expected to result in adecline in the volume of crude oil delivered by the Lakehead system to the province of Ontario and acorresponding increase in deliveries into the PADD II market. Following the announced refineryclosure, Lakehead system deliveries into Ontario are expected to remain relatively constant.

In anticipation of improving supply and demand fundamentals, a major expansion of the Systemwas commenced in 1999. This expansion, referred to as the Terrace expansion program, was undertakenat the request of CAPP and consists of a multi-phase expansion of both the Canadian and U.S.portions of the System. With the completion of the Terrace expansion program, as discussed below,approximately 350,000 bpd of incremental capacity has been added to the System.

• Phase I of the Terrace expansion program was completed in 1999 and included construction of anew 36-inch diameter pipeline facility from Kerrobert, Saskatchewan to Clearbrook, Minnesotathat added approximately 170,000 bpd of capacity to the System. The Partnership’s share of thecost of Phase I was approximately $140.0 million.

• Phase II of the Terrace expansion program was completed in early 2002. Although Phase II didnot involve construction on the Lakehead system, the approximate 40,000 bpd increase incapacity of the Enbridge system is expected to benefit the Partnership directly byaccommodating additional deliveries on the Lakehead system from the Alberta oil sands.

• Phase III of the Terrace expansion program was substantially complete in early 2003 and isdesigned primarily to increase heavy crude oil transportation capacity on the Lakehead systembetween Clearbrook and Superior, Wisconsin by approximately 140,000 bpd. The Partnership’scost of Phase III was approximately $195.0 million.

• Following Phase III of the Terrace expansion program, CAPP has also requested, and thePartnership has undertaken, the expansion of pipeline capacity into the Chicago market.Construction of additional facilities is underway and expected to be in service in 2004. ThePartnership’s cost is expected to be approximately $80.0 million.

Competition. As pipelines are the lowest cost method for intermediate and long haul movementof crude oil over land, the most significant existing competitors for the transportation of westernCanadian crude oil are other pipelines. In 2003, the Enbridge system transported approximately 67% oftotal western Canadian crude oil production; the remainder was either refined in the provinces ofAlberta, British Columbia or Saskatchewan, Canada or transported through other pipelines. Of thepipelines transporting western Canadian crude oil out of Canada, the System provides approximately77% of the total pipeline design capacity. The remaining 23% is shared among five other pipelines

10

transporting crude oil to British Columbia, Washington, Montana and other states in the northwesternUnited States.

To address growing demand in the PADD IV and Puget Sound Area of PADD V, severalexpansions of these competing pipeline systems have been announced. Competing pipelines are ownedby Terasen Inc. and transport crude oil from Alberta to British Columbia and Washington Statethrough the Trans Mountain pipeline and from Alberta to the PADD IV region of the U.S. through theExpress pipeline.

Terasen Inc. has stated that it plans to apply to the NEB for approval to increase the capacity ofits Trans Mountain pipeline from approximately 188,100 bpd to 214,500 bpd. It is anticipated that thisexpansion will be in service during the third quarter of 2004.

Terasen Inc. has also announced plans to proceed with the expansion of the Express pipelinesystem from current capacity of 172,000 bpd to 280,000 bpd. Terasen Inc. expects this expansion to bein service by April 2005.

Another competitor, Inter Pipeline Fund, has announced a commercial agreement with fourshippers to increase southbound capacity on its Bow River pipeline by 17,000 bpd. This systemtransports western Canadian crude to markets in Montana. Inter Pipeline Fund expects the newfacilities will be in place by May 1, 2004.

The pipeline expansions into PADD IV are in line with management expectations as the PADD IVregion indigenous supply continues to decline. Management expects the growing supply from WesternCanada to substantially exceed the impact requirements of the PADD IV region, leaving the balance tobe transported on the Lakehead system.

In the United States, the Lakehead system encounters competition from other liquid petroleumpipelines and other modes of transportation delivering crude oil and refined products to the refiningcenters of Minneapolis-St. Paul, Minnesota; Superior, Wisconsin; Chicago, Illinois; Detroit, Michigan;Toledo, Ohio; and the Patoka/Wood River area in southern Illinois.

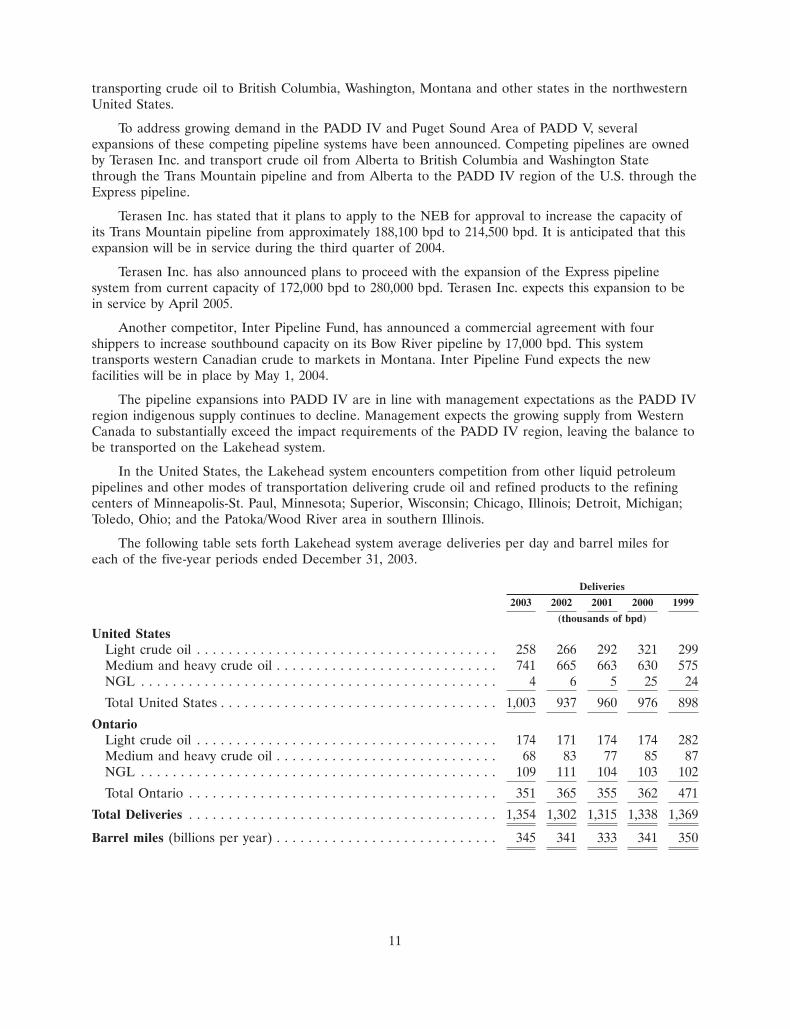

The following table sets forth Lakehead system average deliveries per day and barrel miles foreach of the five-year periods ended December 31, 2003.

Deliveries

2003 2002 2001 2000 1999

(thousands of bpd)

United StatesLight crude oil . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 258 266 292 321 299Medium and heavy crude oil . . . . . . . . . . . . . . . . . . . . . . . . . . . . 741 665 663 630 575NGL . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4 6 5 25 24

Total United States . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1,003 937 960 976 898

OntarioLight crude oil . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 174 171 174 174 282Medium and heavy crude oil . . . . . . . . . . . . . . . . . . . . . . . . . . . . 68 83 77 85 87NGL . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 109 111 104 103 102

Total Ontario . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 351 365 355 362 471

Total Deliveries . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1,354 1,302 1,315 1,338 1,369

Barrel miles (billions per year) . . . . . . . . . . . . . . . . . . . . . . . . . . . . 345 341 333 341 350

11

The North Dakota system is a crude oil gathering and transportation system servicing the WillistonBasin in North Dakota and Montana. The North Dakota system’s crude oil gathering pipelines collectcrude oil from points near producing wells in approximately 36 oil fields in North Dakota and Montanaand receive Canadian crude oil via an interconnect with an Enbridge gathering system in the provinceof Saskatchewan, Canada. Most deliveries are made at Clearbrook to the Lakehead system and to athird-party pipeline system. The North Dakota system includes approximately 330 miles of crude oilgathering lines connected to a transportation line that is approximately 620 miles long, with anaggregate working capacity of approximately 84,000 barrels per day. The North Dakota system also has16 pump stations and 12 terminaling facilities with an aggregate working storage capacity ofapproximately 700,000 barrels.

Customers. Customers of the North Dakota system include producers of crude oil and purchasersof crude oil at the wellhead, such as marketers, that require crude oil gathering and transportationservices. Producers range in size from small independent owner/operators to the largest integrated oilcompanies.

Supply and Demand. Like the Lakehead system, the North Dakota system depends upon demandfor crude oil in the Great Lakes and Midwest regions of the United States, and the ability of crude oilproducers to maintain their crude oil production and exploration activities.

Competition. Competitors of the North Dakota system include integrated oil companies, interstateand intrastate pipelines or their affiliates and other crude oil gatherers. Many crude oil producers inthe oil fields served by the North Dakota system have alternative gathering facilities available to themor have the ability to build their own facilities.

Gathering and Processing Segment

The Partnership owns and operates natural gas gathering, treating and processing systems. Thesesystems purchase and/or gather natural gas from the wellhead, deliver it to plants for treating and/orprocessing and to intrastate or interstate pipelines for transmission or to wholesale customers such aspower plants, industrial customers and local distribution companies.