Embed Size (px)

Citation preview

DoingBusiness

in NicaraguaJanuary 2015

1

CONTENT

I. CENTRAL LAW ......................................................................................................................................................... 5

II. OVERVIEW OF NICARAGUA ................................................................................................................................... 5

1. Territory ........................................................................................................................................................ 5

2. Business Geography ...................................................................................................................................... 6

3. Government .................................................................................................................................................. 7

3.1. Executive Branch ........................................................................................................................................ 7

3.2. Legislative Branch ....................................................................................................................................... 7

3.3. Electoral Branch ......................................................................................................................................... 8

3.4. Judiciary Branch .......................................................................................................................................... 8

4. Population ..................................................................................................................................................... 9

5. Public Safety ................................................................................................................................................ 10

6. Foreign Direct Investment ........................................................................................................................... 11

7. Exports ......................................................................................................................................................... 14

8. Gross Domestic Product .............................................................................................................................. 15

9. Diplomatic Relations ................................................................................................................................... 16

10. Power Grid and Telecommunications ..................................................................................................... 18

11. Telecommunications ............................................................................................................................... 19

12. Labor Market ........................................................................................................................................... 20

III. WHY INVEST IN NICARAGUA .............................................................................................................................. 20

1. Stable Developing Economy ........................................................................................................................ 20

2. Solid and Harmonized Legal System ............................................................................................................ 21

2

3. Attractive Tax Incentives ............................................................................................................................. 22

3.1. Tax Benefits to Exports ........................................................................................................................ 22

3.2. Tax Benefits to Producers .................................................................................................................... 22

3.3. Tax Benefits to the Forestry Sector ..................................................................................................... 23

3.4. Temporary Admission Regime ............................................................................................................. 23

3.5. Benefits to Industrial Free Trade Zones .............................................................................................. 24

3.6. Benefits to Power Generation using Renewable Energy Sources ....................................................... 25

3.7. Benefits to the Mining Sector .............................................................................................................. 26

3.8. Benefits to Tourism ............................................................................................................................. 26

3.9. Benefits to Port Constructions ............................................................................................................ 27

3.10. Benefits to Social Housing Construction .......................................................................................... 27

3.11. Benefits to Fishing and Aquaculture ................................................................................................ 28

3.12. Non-‐Tax Incentives .......................................................................................................................... 28

3.13. Benefits to the Hydrocarbon Sector ................................................................................................ 28

4. Preferential introduction to international markets ..................................................................................... 29

5. Ease of Access To and From Nicaragua ....................................................................................................... 30

5.1. Land Connection .................................................................................................................................. 31

5.2. Customs Offices ................................................................................................................................... 31

IV. LEGAL FRAMEWORK OF INTEREST TO INVESTORS ............................................................................................. 32

1. Legislation promoting and protecting investments .................................................................................... 32

2. Social Security and Labor Laws .................................................................................................................... 33

2.1. Work Day ............................................................................................................................................. 34

2.2. Salaries ................................................................................................................................................ 34

2.3. Minimum Wage ................................................................................................................................... 35

2.4. Vacation ............................................................................................................................................... 36

2.5. Thirteenth Month ................................................................................................................................ 36

2.6. Termination of Employment ............................................................................................................... 37

2.7. Unions and Collective Agreements ..................................................................................................... 37

2.7.1. Collective Agreement .................................................................................................................. 38

2.8. Occupational Health and Safety .......................................................................................................... 38

2.9. Social Security ...................................................................................................................................... 39

3. Tax System ................................................................................................................................................... 39

3

3.1. Tax Year ............................................................................................................................................... 39

3.2. Income Tax .......................................................................................................................................... 40

a) Work Income ....................................................................................................................................... 40

b) Income from economic activities ........................................................................................................ 40

c) Capital revenue and capital profits and losses .................................................................................... 41

3.3. Value Added Tax .................................................................................................................................. 42

3.4. Selective Consumer Tax (ISC) .............................................................................................................. 42

3.5. Tax Stamps .......................................................................................................................................... 43

3.6. Municipal Income Tax ......................................................................................................................... 43

3.7. License Tax .......................................................................................................................................... 43

4. Intellectual Property Laws ........................................................................................................................... 43

4.1. Copyrights and Neighboring Rights ..................................................................................................... 44

4.2. Brands and Other Distinctive Signs ..................................................................................................... 45

4.3. Patents, Utility Models and Industrial Design ..................................................................................... 45

4.4. Protection of Programme-‐Carrying Satellite Signals ........................................................................... 46

5. Imports and Exports Standards ................................................................................................................... 47

5.1. Imports ................................................................................................................................................ 47

5.2. Exports ................................................................................................................................................. 47

6. Immigration Rules ....................................................................................................................................... 48

7. Consumer and User Rights .......................................................................................................................... 49

8. Mediation and Arbitration .......................................................................................................................... 49

V. EASE OF DOING BUSINESS ................................................................................................................................... 51

1. Types of Entities .......................................................................................................................................... 51

1.1. Individuals ........................................................................................................................................... 51

1.2. Collective or social ............................................................................................................................... 51

1.2.1. General Aspects ................................................................................................................................ 51

1.2.2. Types of Companies .......................................................................................................................... 52

a) Collective Liability Company ............................................................................................................ 52

b) Limited Partnership ......................................................................................................................... 53

c) Public Limited Liability Company ................................................................................................... 53

d) Partnership Limited by Shares ........................................................................................................ 54

2. Forming a Company .................................................................................................................................... 54

4

2.1. One-‐Stop Window ............................................................................................................................... 54

2.2. Processes at the One-‐Stop Business Service Window ......................................................................... 55

2.3. Clarifications on the DGI Process ......................................................................................................... 56

2.4. Fees from the Mayor’s Office in Managua .......................................................................................... 56

2.5. Processing at MIFIC ............................................................................................................................. 56

2.5.1. Foreign Investor Certificate ......................................................................................................... 56

VI. INSTITUTIONS PROMOTING INVESTMENT IN NICARAGUA ................................................................................ 57

1. PRONicaragua .............................................................................................................................................. 57

2. Ministry of Industry, Development and Trade (MIFIC) ................................................................................ 57

3. AMCHAM ..................................................................................................................................................... 57

4. CETREX ......................................................................................................................................................... 58

5

DOING BUSINESS IN NICARAGUA

I. CENTRAL LAW

CENTRAL LAW is a leading regional law firm advising clients on corporate law in Central America and the Caribbean. With 11 offices in the countries of Guatemala, El Salvador, Honduras, Nicaragua, Costa Rica, Panama and the Dominican Republic, CENTRAL LAW has helped develop domestic and foreign corporations as well as financial institutions in the countries where the offices of the firm are located. International directories such as Chambers & Partners, Legal 500, IFLR 1000, among others, have recognized the lawyers of CENTRAL LAW as prominent professionals in the fields of Corporate Commercial, Dispute Resolution, Corporate Finance and Corporate M&A law. The firm also ranks among the leading law firms in Latin America in the areas of Banking & Finance, Energy & Infrastructure, Energy and Natural Resources, Insurance, Intellectual Property, Labor & Employment, Real Estate and Tourism and Shipping.

II. OVERVIEW OF NICARAGUA

1. Territory Nicaragua is located in the center of the American continent. It has a territorial landmass of 130,373.4 Km2 and it is the largest country in Central America. Its geography includes approximately 800 Km of coastline in the Pacific Ocean and the Caribbean Sea, 28 volcanic formations, 22,000 Km2 of natural reserves, over 10,400 Km2 of lakes, lagoons and rivers and 7% of the world’s biodiversity. The country also has three Biosphere Reserves declared by the United Nations Educational, Scientific and Cultural Organization (UNESCO): Bosawás, Ometepe Island and San Juan River Biosphere Reserves1.

1 Biosphere Reserves Around the World, [online] [consulted on March 26, 2015], available at http://www.unesco.org

6

Geophysically, Nicaragua is divided into three large zones: the Pacific lowlands, north-central highlands, and the Caribbean lowlands. Administratively, it is divided into 15 departments, 2 autonomous regions in the Caribbean coast and 153 municipalities. Land borders are 1,146 Km long: 833 Km bordering Honduras to the north, and 312 Km bordering Costa Rica to the south. If measured in a straight line, Nicaragua has 350 Km of Pacific coastal line and 450 Km of Caribbean coastal line. In November 2012, the International Court of Justice (ICJ) ruled in favor of Nicaragua on the case versus Colombia in regards to the continental shelf pertaining to Nicaragua. ICJ recognized 200 nautical miles of territorial waters from the coast to the Atlantic Ocean as Nicaraguan territory. This sea territorial portion of Nicaragua represents an important investment opportunity due to its natural wealth.

2. Business Geography Due to the geographical location and tropical climate of Nicaragua, the country has very fertile lands. Therefore, agriculture is one of the main economic activities. The main crops are cotton, sesame, bananas, coffee, cocoa, sugar cane, peanuts, beans and sorghum. Agriculture currently represents 60% of the total exports and bring approximately 300 million US dollars into the country. Nicaragua has around 800 kilometers of coastal line in the Pacific Ocean and the Caribbean Sea, 28 volcanic formations, more than 10,000 km2 of lakes, lagoons and rivers and it has the second largest lake of Latin America. This lake also has the largest island in a lake in the world. It has colonial cities with a rich culture, such as Granada - one of the oldest cities founded in the American continent-, and Leon, home to the last cathedral built in colonial times and which, due to its artistic, cultural and historical value, was declared a world heritage site by UNESCO in 20112. The combination of these characteristics along with the high citizen safety levels, make Nicaragua an attractive tourist destination. Therefore, the tourism industry is constantly progressing and it has become one of the most dynamic economic sectors in Nicaragua. It has become one of the first sources of hard currency in the country. According to the data provided by the Nicaraguan Institute of Tourism (INTUR), over 1.23 million tourists were recorded in Nicaragua in 2013, which represented a 4% growth. Tourism generated a revenue of $417 million US dollars.

2 List of World Heritage Sites, [online], [consulted on March 26, 2015], available at http://portal.unesco.org

7

In 2014, 1,329,600 tourists visited Nicaragua (data prior to December 2014). This figure represents approximately an 8.1% growth in the arrival of tourists. This is a significant increase in the main markets compared to 2013: United States 10%; Germany 15.9%; Spain 10.4% and England 47.1%. According to the Nicaraguan Institute of Tourism (INTUR), the sites preferred by tourists are: the colonial cities of Granada and Leon; Masaya City and Rivas City, and definitely the beach of San Juan del Sur, Ometepe Island, the Mombacho volcano, Corn Islands (Corn Island y Little Corn Island), and other destinations. Ecotourism and the growing interest in surfing also attract many tourists to the country. In the July 2014 edition of the Central American Forbes magazine, Gildan, a Canadian clothing manufacturer that expanded to Nicaragua in 2004, , commented on the value of the country’s strategic location, which facilitates a prompt response to the markets and also commented on the quality of the Nicaraguan workforce.

3. Government Nicaragua is a democratic republic. Democracy is exercised in a direct, participatory and representative manner. The functions delegated by the Sovereign Power are expressed through the Legislature, the Executive, the Judiciary and the Electoral Branch. Each Branch has specialized and separate functions. They collaborate harmonically with each other to achieve their goals.3

3.1. Executive Branch The President of the Republic is the Head of State and the Commander in Chief of the Defense and Security Forces of the Nation.4 The current President of the Republic is Mr. Daniel Ortega Saavedra, who was elected in November 2006 and re-elected in November 2011.

3.2. Legislative Branch It is exercised by the National Assembly and formed by 92 members elected by equal, direct and secret universal vote5 for a five-year term.

3 Article 7 Political Constitution with incorporated reforms. 4 Article 144 Political Constitution with incorporated reforms. 5 Article 132 and 133 Political Constitution with incorporated reforms.

8

3.3. Electoral Branch It is constituted by the Supreme Electoral Council and formed by Magistrates appointed by the National Assembly from separate lists proposed for each position by the President of the Republic and by the Members of the National Assembly in consultation with the relevant civil organizations,6 for a five-year term. This branch is exclusively in charge of the organization, management and vigilance of elections, plebiscites and referendums.

3.4. Judiciary Branch The Judiciary is formed by justice tribunals established by law, which upper-level body is the Supreme Court of Justice. This court is formed by sixteen magistrates appointed by the National Assembly, from separate lists proposed for each position by the President of the Republic and the Members of the National Assembly in consultation with the relevant civil organizations.7

Source: National Institute of Information Development (INIDE) The judiciary is a unitary system for the entire country and it is organized into specific divisions to resolve disputes according to the nature of each case, whether it is constitutional, civil, labor, criminal or administrative. It is also a system that permits alternative conflict resolution methods such as mediation, conciliation and arbitration, as established by the law of the matter. This helps reduce the number of judicial cases and expedites the administration of justice. 6 Article 138 item 8 Political Constitution with incorporated reforms. 7 Article 138 item 7 Political Constitution with reforms incorporated.

9

4. Population According to the National Institute of Information Development (INIDE in Spanish), the estimated population of Nicaragua for 2015 is 6.17 million, 51% female and 49% male. The following graph shows the population distribution per age group for 2015:

Department Population % of Total

Managua 1,480,270 24.00% Matagalpa 547,500 8.88% RAAN 476,298 7.72% Jinotega 438,412 7.11% Chinandega 419,753 6.81% León 399,879 6.48% RAAS 380,121 6.16% Masaya 361,914 5.87% Nueva Segovia 249,376 4.04% Estelí 223,356 3.62% Granada 201,993 3.28% Chontales 191,127 3.10% Carazo 186,438 3.02% Rivas 172,289 2.79% Boaco 160,711 2.61% Madriz 158,705 2.57% Río San Juan 119,095 1.93% Total 6,167,237 100.00% Source: National Institute of Information Development (INIDE).

10

Source: PRONicaragua. http://www.pronicaragua.org/es/por-que-invertir-en-nicaragua/excelente-calidad-de-vida Other important demographic indicators for 2010-2015 include:

§ Average annual growth: 1.22% § Life expectancy: 74.5 years § Gross birth rate: 23.2 per one thousand inhabitants § Gross mortality rate: 4.6 per one thousand inhabitants § Infant mortality rate: 18.1 per one thousand births § Overall fertility rate: 2.5 per woman

5. Public Safety Nicaragua is world known for the high level of public safety. In the last few years, it has become one of the safest countries in the western hemisphere. Homicide rates in Nicaragua in 2013 were 9 persons per 100,000 inhabitants.

Similarly, the Economist Intelligence Unit (EIU) confirms the high safety level of Nicaragua in its country risk evaluation, placing it as one of the safest countries in Central and Latin America. Indicators such as: armed conflicts, demonstrations, organized crime and kidnappings in different countries around the world are measured in the report.

11

Source: PRONicaragua. http://www.pronicaragua.org/es/por-que-invertir-en-nicaragua/excelente-calidad-de-vida

6. Foreign Direct Investment According to the Presidential Delegation for the Investment and Export Promotion Agency (PRONicaragua), revenue from foreign direct investment (FDI) was $1,388 million USD in 2013, which represented an 8 % increase compared to 2012. In 2004-2013, the FDI flow to Nicaragua recorded a 20% average growth rate annually, which reflects a safe and stable environment supported by a solid legal framework for investments. In 2013, FDI revenue was recorded in 11 economic sectors in the country. The top five sectors were: industry, mines, trade, financial services and telecommunications. These sectors represented 88% of the total foreign direct investment revenue. In the first semester of 2014, FDI in Nicaragua was more than $762 million USD, which represented a 8% growth compared to the same period in 2013. Over the last five years, Nicaragua has been at the top of the IEB/GDP index in Central America. This rate provides an objective measure of the FDI flow in relation to the size of the economy of every country. Specifically in 2013, Direct Foreign Investment/GDP in Nicaragua was 12.2%. The excellent business environment in the country has allowed not only an important growth in the FDI growth but also in local investment8.

8 Descubriendo Nicaragua, Economía [online] [consulted on March 12, 2015]. Available at www.pronicaragua.org

12

Source: MIFIC, BCN and PRONicaragua. *Estimated data. According to data from the Ministry of Industry, Development and Trade, the country has signed 19 Bilateral Investment Promotion and Protection Agreements, as part of the policy to encourage investment and ease the establishment of foreign investment in the country.

Name of legal document Place and date of signing

Agreement on investment guarantees between Nicaragua and the Republic of China (Taiwan). (1)

Managua, Nicaragua, July 29, 1992

Agreement for the mutual promotion and protection of investments between Nicaragua and the Kingdom of Spain

Managua, Nicaragua, March 16, 1994

Agreement on mutual promotion and protection of investments between Nicaragua and the United States of America.

Denver, Colorado, U.S.A., January 7, 1995

Agreement for the mutual promotion and protection of investments between Nicaragua and The Kingdom of Denmark

Copenhagen, Denmark, March 12, 1995

13

Treaty for the mutual promotion and protection of capital investments between Nicaragua and the Federal Republic of Germany

Managua, Nicaragua, May 6, 1996

Agreement for the mutual promotion and protection of investments between Nicaragua and United Kingdom of Great Britain

Managua, Nicaragua, December 4, 1996

Agreement for the mutual promotion and protection of investments between Nicaragua and France

Managua, Nicaragua, February 13, 1998

Agreement for the mutual promotion and protection of investments between Nicaragua and Argentina

Buenos Aires, Argentina, October 8, 1998

Agreement for the mutual promotion and protection of investments between Nicaragua and Chile

Santiago de Chile, November 8, 1998

Agreement for the mutual promotion and protection of investments between Nicaragua and the Swiss Confederation

Managua, Nicaragua, November 30, 1998

Agreement for the mutual promotion and protection of investments between Nicaragua and El Salvador

Managua, Nicaragua, January 23, 1999

Agreement for the mutual promotion and protection of investments between Nicaragua and the Kingdom of Sweden

Stockholm, Sweden, May 27, 1999

Agreement for the mutual promotion and protection of investments between Nicaragua and the Republic of Korea

Seoul, Korea, May 15, 2000

Agreement for the mutual promotion and Managua, Nicaragua, June 2, 2000

14

protection of investments Nicaragua and Ecuador (2)

Agreement on the mutual promotion and protection of investments between Nicaragua and the Kingdom of the Netherlands

Managua, Nicaragua, August 28, 2000

Agreement on the mutual promotion and protection of investments between Nicaragua and the Czech Republic

Managua, Nicaragua, April 2, 2002

Agreement on mutual promotion and protection of investments between Nicaragua and the Republic of Finland

Managua, Nicaragua, September 17, 2003

Agreement on promotion and protection of investments between Nicaragua and the Italian Republic

Managua, Nicaragua, April 20, 2004

Agreement on the promotion and protection of investments between Nicaragua the Belgium-Luxembourg

Luxembourg, May 27, 2005

Source: http://www.mific.gob.ni/INICIO/INVERSIONEXTRANJERA/ACUERDOSDEINVERSION

7. Exports In 2013, Nicaragua had a 2% growth in the volume of exports. In the third quarter of 2014, total exports grew almost 10%; and total trade grew almost 6% compared to the same period in 2013. The main FOB export products of Nicaragua in 2013 were: raw gold, beef, coffee, gold, sugar and peanuts, which represented approximately 64% of the total value. The main export destination countries in that year were the United States of America, Venezuela, Canada, El Salvador and Costa Rica. Within the same period and within the free-trade zones, the main exporting sectors were clothing and manufacturing, automotive harnesses, tobacco, agricultural industry and third-party services.9

9 Discover Nicaragua, Economy [online] [consulted on March 12, 2015]. Available at www.pronicaragua.org

15

Total exports in Nicaragua in 2014 were $5,125.7 million USD, out of which $4,273.5 million USD came from exports of the manufacturing industry (including agricultural industry, processing of fishing products, mining, tobacco, etc.). Sales in the international market of this International Standard Industrial Classification group had a 5 % growth in 2014 compared to 2013 where S$4,071.7 million USD were exported. In 2014, the main destinations of Nicaraguan exports were USA, including Puerto Rico and the USA Virgin Islands, (46.9%); Mexico (12.0%), Venezuela (7.6%), Canada (4.9%), El Salvador (4.5%), Honduras (3.0%), Costa Rica (3.0%). As economic regions, the European Union had a 6.3% participation, Central America (12.3%), and Asia (3.3%). The main destinations for Nicaraguan exports in 2014, and the most dynamic compared to 2013, were Italy, which increased imports from Nicaragua in 39.8%; China, 34.6%; Panama, 31.2%, Costa Rica, 21.9%; Spain, 18.1%; Honduras, 17.9%; USA, 15.7%; Taiwan, 10.8%; counterbalancing the drop in exports to Belgium (-0.3%), Germany (-6.8%), Dominican Rep. (-7.3%), France (-9.6%) and Canada (-23.4%)10.

Source: Banco Central de Nicaragua and the National Free-Trade Zone Committee. *Estimated data.

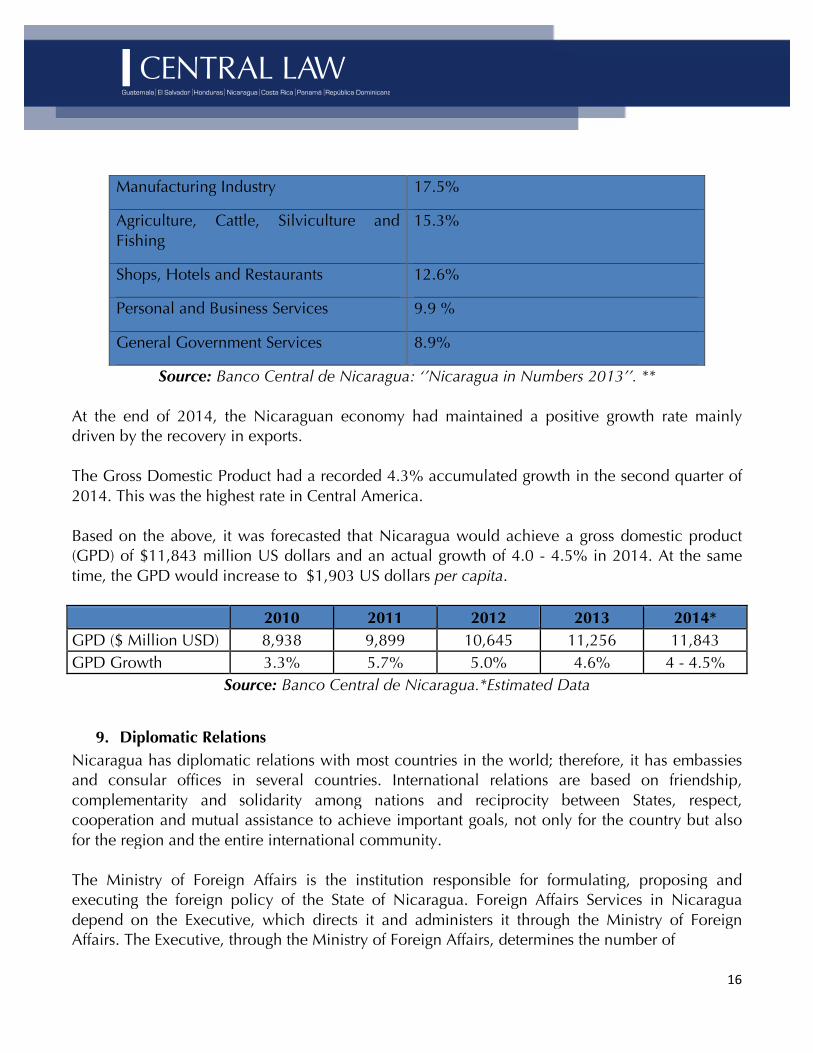

8. Gross Domestic Product In 2013, Nicaragua had a gross domestic product (GDP) of $11,255.6 million US dollars. This represents a 4.6% growth, above the 3.3% regional average and the highest in Central America in the last three years. At the same time, the per capita GDP increased to $1,831.3 USD, experiencing a 4.25% growth. The top five GDP sectors in Nicaragua in 2013 were:

10 Executive Report on Nicaragua Foreign Trade, 2014, MIFIC, [Online] [consulted on March 19, 2015]. Available at www.rpi.mific.gob.ni

16

Manufacturing Industry 17.5%

Agriculture, Cattle, Silviculture and Fishing

15.3%

Shops, Hotels and Restaurants 12.6%

Personal and Business Services 9.9 %

General Government Services 8.9%

Source: Banco Central de Nicaragua: ‘’Nicaragua in Numbers 2013’’. ** At the end of 2014, the Nicaraguan economy had maintained a positive growth rate mainly driven by the recovery in exports. The Gross Domestic Product had a recorded 4.3% accumulated growth in the second quarter of 2014. This was the highest rate in Central America. Based on the above, it was forecasted that Nicaragua would achieve a gross domestic product (GPD) of $11,843 million US dollars and an actual growth of 4.0 - 4.5% in 2014. At the same time, the GPD would increase to $1,903 US dollars per capita.

2010 2011 2012 2013 2014*

GPD ($ Million USD) 8,938 9,899 10,645 11,256 11,843 GPD Growth 3.3% 5.7% 5.0% 4.6% 4 - 4.5%

Source: Banco Central de Nicaragua.*Estimated Data

9. Diplomatic Relations Nicaragua has diplomatic relations with most countries in the world; therefore, it has embassies and consular offices in several countries. International relations are based on friendship, complementarity and solidarity among nations and reciprocity between States, respect, cooperation and mutual assistance to achieve important goals, not only for the country but also for the region and the entire international community. The Ministry of Foreign Affairs is the institution responsible for formulating, proposing and executing the foreign policy of the State of Nicaragua. Foreign Affairs Services in Nicaragua depend on the Executive, which directs it and administers it through the Ministry of Foreign Affairs. The Executive, through the Ministry of Foreign Affairs, determines the number of

17

Diplomatic Missions, Permanent Representations and Consular Offices as well as the position, rank and number of officials required to integrate the Foreign Affair Services, taking into consideration foreign policy objectives.

Embassies of Nicaragua in the World

EUROPE

GERMANY

AUSTRIA

BELGIUM

SPAIN

FINLAND

FRANCE

SWITZERLAND

NETHERLANDS

UNITED KINGDOM OF GREAT BRITAIN AND NORTHERN IRELAND

ITALY

PERMANENT MISSION UNESCO – FRANCE

RUSSIAN FEDERATION

SWEDEN

VATICAN

SOUTH AMERICA

ARGENTINA

BOLIVIA

BRAZIL

CHILE

COLOMBIA

ECUADOR

PERU

URUGUAY

VENEZUELA

CENTRAL AMERICA

BELICE

COSTA RICA

CUBA

EL SALVADOR

GUATEMALA

HONDURAS

JAMAICA

PANAMA

DOMINICAN REPUBLIC

NORTH AMERICA

MEXICO

UNITED STATES OF AMERICA

ASIA

KOREA

INDIA

IRAN

JAPAN

TAIWAN (CHINA)

AFRICA

EGYPT

SENEGAL

18

(HOLLY SEE)

Source: http://www.cancilleria.gob.ni/embajadas/

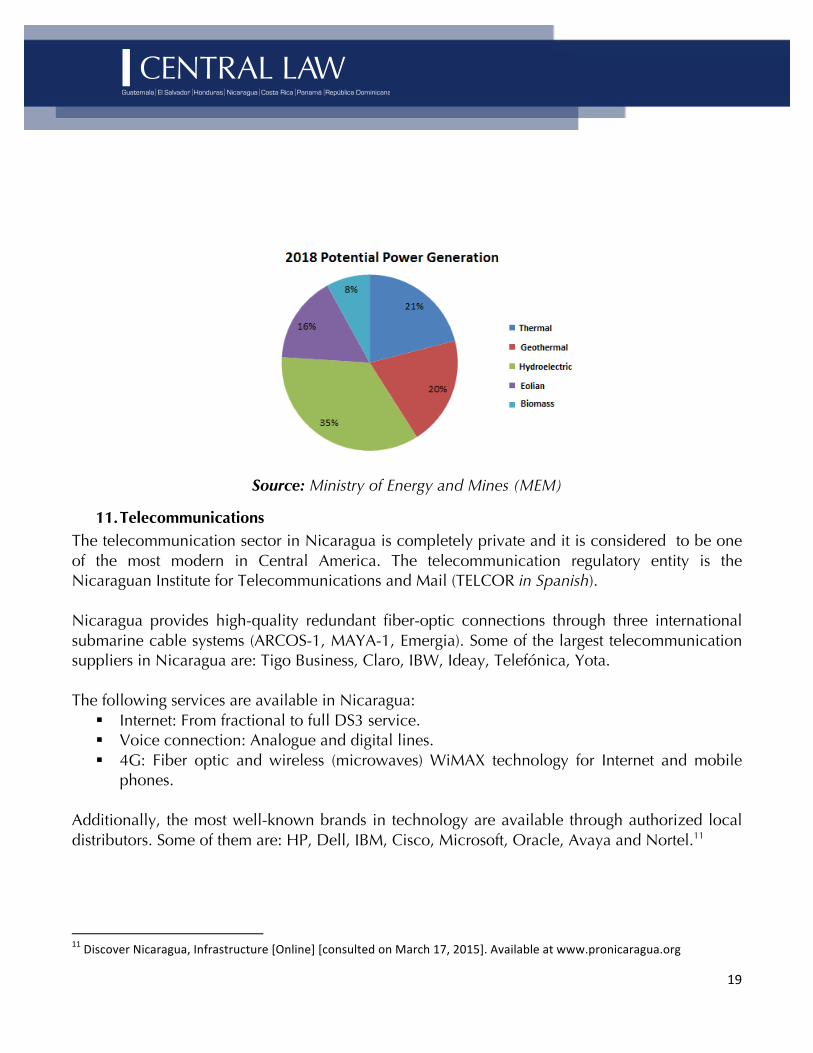

10. Power Grid and Telecommunications The energy sector in Nicaragua has been developing dynamically in the last five years with important public and private investments at a national level. As a result of these efforts, there has been an important improvement in the coverage of electrical services for the population and the capacity installed has increased. This has permitted to supply the national market demand and aim at exporting energy in the future via the Central American Electrical Interconnection System (SIEPAC) project.

Source: PRONicaragua http://www.pronicaragua.org/es/descubrenicaragua/infraestructura By June 2014, power generation in the country had a 5.7% accumulated growth. The renewable component was the main source of generation (53.0%) in the semester. At present, renewable sources are 51% of the matrix while they were 36% in 2007. The goal of the Nicaraguan Government for 2017 is to have 79% of the matrix in renewable power sources.

Source: Ministry of Energy and Mines (MEM)

2007 2008 2009 2010 2011 2012

Coverage 60.4% 63.4% 66.0% 70.0% 72.4% 75.0% Installed Capacity (MW) 832 891 982 1,073 1,109 1,286

19

Source: Ministry of Energy and Mines (MEM)

11. Telecommunications The telecommunication sector in Nicaragua is completely private and it is considered to be one of the most modern in Central America. The telecommunication regulatory entity is the Nicaraguan Institute for Telecommunications and Mail (TELCOR in Spanish). Nicaragua provides high-quality redundant fiber-optic connections through three international submarine cable systems (ARCOS-1, MAYA-1, Emergia). Some of the largest telecommunication suppliers in Nicaragua are: Tigo Business, Claro, IBW, Ideay, Telefónica, Yota. The following services are available in Nicaragua:

§ Internet: From fractional to full DS3 service. § Voice connection: Analogue and digital lines. § 4G: Fiber optic and wireless (microwaves) WiMAX technology for Internet and mobile

phones. Additionally, the most well-known brands in technology are available through authorized local distributors. Some of them are: HP, Dell, IBM, Cisco, Microsoft, Oracle, Avaya and Nortel.11

11 Discover Nicaragua, Infrastructure [Online] [consulted on March 17, 2015]. Available at www.pronicaragua.org

20

12. Labor Market Nicaraguan labor is young and dynamic. 76% of the population is younger than 39 and the workforce is 3.2 million people. It is known for being flexible and highly productive, with good work habits and the capacity to learn at a fast pace. These qualities have positioned Nicaragua as one of the most competitive and productive countries in the region in terms of human capital. According to statistics from the Nicaraguan Institute of Social Security (INSS in Spanish), in 2013, the economic activities that generated the most employment were community, social and personal services, manufacturing industry, retail, hotels and restaurants. The official unemployment figure for the third quarter of 2013 was 5.3%, while approximately 48.3% of the economically active population was underemployed. The number of active members insured by the INSS has substantially increased in the last few years. It has increased from 471,856 insured members in 2007 to 673,466 in 2013, which represented a 43% increase. In November 2014, 731,774 workers were recorded as being registered with social security, reaching a 5.6% average annual growth rate equivalent to 37,193 new members. By September 2014, some of the economic activities that created the most employment in the last twelve months were retail, services and industry with an employment rate of 43.2%, 24.1% and 8%, respectively. The average INSS salary was 8,335.6 Cordoba in September 2014.

III. WHY INVEST IN NICARAGUA

1. Stable Developing Economy Nicaragua has experienced a sustained economic growth as a result of the disciplined management of financial, tax, monetary and currency exchange policies. The excellent economic performance of Nicaragua has been recognized by the International Monetary Fund (IMF) through a series of reviews over the last few years. In 2013, the IMF stated that “The recent economic performance of Nicaragua has been favorable". It also indicated that "Prudent management of macroeconomic policies will turn into favorable short and long term prospects". In March 2015, during its latest visit, the IMF indicated that the economic policies implemented by the Government of Nicaragua are very positive and they should serve as an example to the

21

rest of the Latin American countries. It also indicated that the macroeconomic situation in the country is “fairly robust”, considering that the tax deficit is 1.6% (well below most countries in Latin America), while the total government debt decreased from 49 to 42% and foreign debt is 46%. This was assessed as being excellent. The constant and stable economic growth of Nicaragua was featured in the July 2014 edition of Forbes Central America, which recognized the country as “one of the big protagonists of the next decade.” According to the article, titled “The Nicaraguan Miracle”, the economic dynamism of Nicaragua increased five years ago with the increment of construction, energy and tourism projects driven by government investment promotion policies. Forbes also highlighted the high level of safety in the country, decrease in poverty, preferential access to markets, transformation of power matrix into renewable sources, and diversity of investment opportunities.12

2. Solid and Harmonized Legal System The Political Constitution is the fundamental norm of the Nicaraguan legal system and all other norms are subordinated to it. Therefore, the norms regulating the legal framework for investments in Nicaragua such as civil and commercial codes and other special laws, harmonically and appropriately complement each other to create a safe business environment of legal certainty. The Political Constitution expressly recognizes a group of rights that form the necessary fabric of an economic democracy, characterized by free enterprise, contractual freedom, respect for human rights and private property, prohibition of confiscation of goods and disruption of legal ownership and possession of any form of property recognized by the mixed economic model established in the Constitution. Principles such as the equality of companies before the law, tax legality and reserve of law to create taxes, protection of intellectual property and consensus among government, the private sector and workers, with the purpose of achieving productive stability and peace in business activities, constitute the fundamental basis of the social-economic order established in the Nicaraguan Political Constitution.

12 Discover Nicaragua, Newsroom, Press Releases [Online] [consulted on March 18, 2015]. Available at www.pronicaragua.org

22

It is worth noting the pertinent recognition, also at a constitutional level, of the responsibility of the State to protect, foster and promote diverse forms of property and private economic and business management to guarantee social and economic democracy. It also safeguards and guarantees free competition, consumer rights, public-private national and foreign investments, and the leading role of the private initiative in order to contribute to the economic social development of the country. The foregoing is completed by specific valid standards that have been in force for over 15 years. These legal standards put into practice these constitutional precepts that constitute the pillars of the business climate in the country. They regulate matters such as: contracts, loans, incentives for investments and exports, banking, real estate, market actions and others.

3. Attractive Tax Incentives Through specific laws, Nicaragua offers generous tax incentives to a wide variety of sectors of great importance for investment, production and commercialization of goods and services, such as: production of national goods, free - trade zones, energy, tourism, agriculture, forestry sector, mining, fishing and agriculture, etc. That is why investors choose Nicaragua to conduct business and expand their opportunities. Tax incentives and legal background per sector are as follows: Law N° 822 “Tax Harmonization Law” and its reforms (LCT in Spanish), this legal standard establishes diverse tax benefits for certain economic production sectors with the objective of supporting their growth and development. Exemptions and exceptions awarded by this law are established without prejudice of those awarded by the legal provisions in article 287 of said law.

3.1. Tax Benefits to Exports In accordance with article 109, Law N°822, exports of national goods or services provided outside the country are applied a 0% Added Value Tax. Exports of goods are taxed at 0% of the Selective Consumer Tax and tax credits to advances or annual income tax with prior validation by the tax administration, at a figure equivalent to 1.5% of the FOB value of the exports (Art.151 and 273 Law N°822).

3.2. Tax Benefits to Producers Article 127 of Law N°822 establishes a transfer list exempted from carrying the Value Added Tax, some of them related to the agricultural sector. In addition, transfers of raw materials, intermediate products, capital assets, spare parts, parts and accessories for machinery and equipment for agricultural producers as well as producers from micro, small and medium

23

industrial and fishing companies are exempted from the Value Added Tax, Selective Consumption Tax and Import Duties through a taxation list (article 274 of said law).

3.3. Tax Benefits to the Forestry Sector Article 283 of Law N°822 extends the benefits to the forestry sector in Law N° 462, Forestry Conservation and Sustainable Development Law, until December 31, 2023. The benefits are the followings:

a) Exemption of payment of 50% of the Municipal Sales Tax and 50% on utilities used in those forestry plantations registered with the regulatory entity.

b) Exemption of payment of Real Estate Property Tax for the property areas where forestry plantations are established and the areas where forestry management is performed through a Forestry Management Plan.

c) Companies of any business nature investing in forestry plantations may claim 50% of the amount invested as expenses for income tax purposes.

d) Exemption of payment of import duties and taxes for companies of secondary and tertiary processing that import machinery, equipment and accessories that will improve their technological level in wood processing, excluding sawmills.

All individuals and corporations natural persons and legal entities may claim up to 100% of their income tax payment as long as it is to advancing reforestation or creating forestry plantations. For the purposes of such deduction, the taxpayer must submit the forestry initiative to the National Forestry Institute in advance. Furthermore, all State institutions must prioritize the acquisition of goods manufactured with wood in their contracting process. Such goods must carry the proper forestry certificate issued by the National Forestry Institute. They may identify up to a 5% pricing difference in the bid or tender.

3.4. Temporary Admission Regime Law N° 382, Law on Temporary Admission for and Facilitation of Exports establishes a temporary admission regime for active improvement. This is a Customs system that permits importing merchandise without any payment of fees, import duties or any other taxes on the condition that they need to be completed, that is, they need to undergo a subsequent process. This tax system allows goods to enter the national customs territory as well as purchasing them locally without payment of duties and taxes. Companies exporting directly or indirectly may avail themselves of this regime for at least 25% of their total sales and with a minimum exported value of $50,000 US dollars annually.

24

The merchandise that may be covered under this regime is the following:

a) Intermediate goods and raw material such as: consumable goods, semi-processed products, containers, packaging, any merchandise to be incorporated to the final product to be exported, samples, models and patterns required for production and staff training.

b) Capital goods directly involved in the production process, spare parts and accessories, such as: machinery, equipment, parts, molds, dies and utensils that complement such capital goods.

c) Materials and equipment that will become an integral and indispensable part of the facilities required for the production process.

3.5. Benefits to Industrial Free Trade Zones By Decree 46-91 on Industrial Free Trade Zones, Nicaragua offers important tax incentives to companies interested in setting up free trade zone operations to export from the textile and clothing manufacturing industries, the manufacturing and the agricultural industry. These benefits are awarded to all exports of international services under the free trade zone regime, such as Business Process Outsourcing (BPO), Knowledge Process Outsourcing (KPO), and Information and Technology Outsourcing (ITO), etc. Article 20 of the decree cited above, establishes the following tax benefits for Companies using Free Trade Zones:

a) 100% exemption during the first ten years and 60% from the eleventh year onwards from payment of taxes on the revenue generated by their operations in the Zone. This exemption does not include taxes on personal income, salary or remuneration paid to the Nicaraguan or foreign personnel working at the Company established in the Zone. However, it does include payment to non-resident foreign nationals for interests on loans, or for commissions, fees and remittances for legal services abroad or in Nicaragua, and promotion, marketing, consulting, payments from which those companies will not need to withhold any amounts.

b) Tax payment exemption on property transfers of real estate under any title including capital gain taxes, as applicable, provided that the company is closing operations in the Zone and the real estate asset remains attached to the Free Trade Zone.

c) Tax payment exemption for constitution, transformation, merger and change of the company, as well as the Stamp Duty.

d) Exemption from all consumer Customs duties and taxes related to the introduction into the country of raw materials, materials, equipment, machinery, dies, parts or spare parts, samples, molds and accessories destined to outfit the Company for operating in the Zone.

25

e) Exemption from Customs duties on transportation equipment, whether they are cargo, passenger or service vehicles, for the regular use of the Company in the Zone.

f) Full exemption from indirect taxes, sales or selective consumer taxes. g) Full exemption from municipal taxes. h) Full exemption from exports duties on products manufactured in the Zone.

3.6. Benefits to Power Generation using Renewable Energy Sources According to the provisions of Law N°532, Law on the Promotion of Electricity Generation from Renewable Sources, Nicaragua provides important tax and duty benefits to electrical power generation projects using renewable sources of energy performed by natural persons or legal entities with private, public or mixed investments. This is applicable to new projects and to those expanding the installed capacity. Article 7, Law N°532, outlines the following tax benefits:

a) Exemption of payment of Import Tax (DAI) for machinery, equipment, materials and consumables exclusively allocated to pre-investment work and construction work including construction of the sub transmission line required for transporting energy from the generation station to the National Interconnected System (SIN).

b) Exemption of payment of Value Added Tax on machinery, equipment, materials and consumables exclusively allocated to pre-investment work and construction work including construction of the sub transmission line required for transporting energy from the generation station to the National Interconnected System (SIN).

c) Exemption of payment of Income Tax and the minimum income tax payment for a maximum period of 7 years from the start of the Project commercial or business operation. Similarly, income from the sale of carbon credits will be exempted from payment of income tax during the same period.

d) Exemption from all existing municipal taxes on real estate property, sales, fees for the project build phase for a period of 10 years from the start of the project commercial operation, which will be applied as follows: 75% exemption during the first three years; 50% in the following five years and 25% in the last two years. Fixed investments on machinery, equipment and hydroelectric dams will be exempt of all taxes, charges, municipal rates, for a period of 10 years from the start of commercial operation.

e) Exemption from all taxes that may exist for the use of natural resources for a maximum period of 5 years after commencing operations.

f) Exemption from Stamp Tax (ITF)] that may result from the project construction, operation or expansion for a period of 10 years.

26

3.7. Benefits to the Mining Sector The exploration and exploitation of mineral resources is regulated by Law N° 387, Special Law on Mining Exploration and Exploitation and its Regulations, Decree 11-2001. Given the importance of the mining sector for the economic development of the country, the State of Nicaragua guarantees tax stability to national and foreign investment in this industry by applying the following benefits:

a) Temporary Admission Regime, in accordance with Law 382 Law of Temporary Admission for Active Improvement and Facilitation of Exports, permitting the entry of merchandise into the national Customs territory, the local purchase of goods or raw material without payment of any type of taxes or fees, provided that the merchandise is re-exported or exempted, as the case may be, after being subject to a process of transformation, preparation, repair or any other under applicable law.

b) According to this law, if it is not possible to suspend of duties and taxes in advance due to tax administration issues, the benefit will be applied as a subsequently as a return of taxes paid.

c) Tax payment exemption for real estate property within the perimeter of the mining concession.

d) 0% rate for exports, applicable to exports in general.

3.8. Benefits to Tourism

Law N° 306, the Law on Tourism Incentives of Nicaragua, provides a series of tax incentives to investments in this sector and it is considered to be the most generous and competitive in the region. This law provides incentives to investments on accommodation, food and beverages, travel agencies, tourism transportation, airlines, among others:

a) Exemption from import duty and the Value Added Tax on the local purchase of construction materials and permanent building fittings.

b) Exemption from import duties and taxes and/or the Value Added Tax on the local purchase of fittings, furniture, equipment, buildings, automotive vehicles of 12 passengers or more, cargo vehicles, that have been declared by INTUR as necessary for establishing and operating the tourist activity, and in the purchase of equipment that contributes to saving water and energy, and those required for project security for a term of 10 years from the date when INTUR declares that such company has started operations.

c) Exemption from Property Tax (IBI in Spanish) for a ten-year term from the date when INTUR declares that the tourist activity has initiated operations.

d) Value Added Tax Exemption applicable to design/engineering and construction services.

27

e) Partial exemption of 80% Income tax for a ten-year term from the date when INTUR declares that such Company has commenced operations. The exemption is 90% should the project be situated in a Special Tourist Planning and Development Zone. If the project qualifies and it is also approved under the Inn Program, the exemption will be 100%. For three years, the Company will have the option of annually deferring the implementation and application of the ten-year exemption on such tax.

f) Within the exemption period awarded, should the Company decide to expand and/or substantially renew the project, the exemption period will be extended for another 10 years from the date when INTUR declares that the company has completed such investment and expansion.

g) Income tax exemption on profit from a tourist activity authorized by INTUR or a lease to a third party of refurbished properties in the Historical Properties, for 10 years from the date when INTUR certifies that the work has been completed and project conditions and standards have been met.

3.9. Benefits to Port Constructions In May 2013, Nicaragua approved Law N°838, General Law of Ports among others with the purpose of providing an incentive to the construction of new ports in the country. According to article 128 of this law: “Investment projects approved, during the port construction, improvement expansion or development of infrastructure, will be considered as exempted from import taxes and duties, local purchases and municipal taxes and will enjoy the following tax benefit on the following: imports of machinery, equipment, materials, spare parts and tools required for port construction, improvement, expansion or development of infrastructures, of state, public-use ports and terminals, under public administration or through concessions, outfitted for internal and external trade”.

3.10. Benefits to Social Housing Construction The Government of Nicaragua has had the goal of fostering and promoting the construction of housing, with emphasis on social housing; therefore, the approval of Law N° 428, Urban and Rural Housing Organic Law granted the Government the powers to set rules and standards to facilitate and encourage maximizing investment on housing and building lands. Furthermore, article 39 of this Law provides for direct incentives to people investing in building social housing. The incentives for this type of investment are the following:

a) Exemption of tax payment for operations, acts, construction permits, formalization and registration of acts, contracts, deeds, processing and authorization of drawings.

b) Exemption of all tax payments for the purchase of construction materials, tools and minor equipment related to social housing and residential civil works, qualified and approved by INVUR.

28

Certification to access these benefits will be issued by INVUR and the Ministry of Finance and Public Credit and they may be used for Added Value tax exemptions on the purchase of construction materials, tools and minor equipment.

3.11. Benefits to Fishing and Aquaculture In addition to the benefits in the Tax Harmonization Law, Law N° 489, Law on Fisheries and Aquaculture grants the right of advance cancellation of taxes on diesel for fishing and industrial aquaculture for individuals or corporate entities, when such consumable is used in capturing products for the domestic and exports market. Similarly, this law stipulates that in the case of traditional aquaculture and fishing, taxes on diesel and gasoline may be suspended when such supplies are used for catching products for exports. It also considers that aquaculture and fishing fees may be offset by the tax credits in favor of aquaculture and fishing taxpayers.

3.12. Non-Tax Incentives Should the results of scientific fishing justify the use of the researched species, preference will be given to the individual or corporate entity, whether private or public, national or foreign, that caught it to have the right to use the hydro biological resource.

3.13. Benefits to the Hydrocarbon Sector Companies in a line of business related to Hydrocarbons enjoy tax benefits with respect exports and the tax system, as a result of the major social-economic impact that Hydrocarbons have on the country. Law N° 277, Hydrocarbon Supply Law, establishes a special tax regime for this type of companies. First, it stipulates an exception of Import Duties (DAI) and the Temporary Protection Duties (ATP), which are governed by the Convention on the Central American tariff and Customs Regime. These duties are the highest for importing products. Imports exemptions apply to crude, refined or reconstituted oil and by-products. In Nicaragua, there is a Specific Fuel Tax (IECC). The specific purpose of this tax is to have a single tax applicable to crude, partially refined or reconstituted oil, and by-products. This tax is regulated by Title IV of Law N° 822 on the specific fuel tax. The IECC taxes the transfer, import or admission of oil by-products . Law 822 prohibits any other type of taxation on them, including any regional, local or municipal taxes.

29

4. Preferential introduction to international markets Nicaragua is a country that continues to seek opportunities to successfully position itself in the international trade and global economy. For this purpose, it has signed several Free Trade Agreements and bilateral, regional agreements or agreements as part of the Central American Common Market (CACM). These have opened economic growth opportunities for Nicaragua through trade exchanges under preferential conditions by eliminating obstacles to trade and facilitating the circulation of products across borders; as well as establishing standards that promote fair competition and will contribute to a higher flow of investments. These agreements are the following:

Agreements Countries

Free Trade Agreements U.S.A, Mexico, Panama, Taiwan, Dominican Republic, Chile & the European Union

Central American Common Market

Nicaragua, Guatemala, El Salvador, Honduras & Costa Rica. In addition, free movement of capital, services and human resources among CA-4 countries.

Preferential Access Agreements

Japan (SGP), Norway (SGP), Canada (SGP), Russia (SGP), Switzerland (SGP) and ALADI

Solidarity Union Agreements (ALBA)

Venezuela, Ecuador, Bolivia, Cuba, Antigua & Barbuda, Dominica & St. Vincent and the Grenadines

Recent Agreements ALADI (Argentina, Bolivia, Brazil, Chile, Colombia, Ecuador, Mexico, Paraguay, Peru, Uruguay, Venezuela and Cuba)

Agreements under negotiation

Canada, CARICOM

Source: Ministry of Development, Industry and Trade Some of the products exported in 2014 to destinations where Nicaragua has preferential duties were the following:

a) Electrical conductors (harnesses) with exports around $562.1 million US dollars in 2014. They are produced in Free Trade Zones and they are mainly exported to Mexico and USA.

b) Beef with a volume increase from 88,683.9 MT in 2013 to 94,364.9 MT in 2014; that is, 6.4%; while value increased in 16.7%, from $383.8 million USD to $448.0 million USD. The main destinations were USA, Venezuela, Central America and Taiwan. Outside the Free Trade Zone regime, beef was the main export product.

c) Coffee had an exported value of $395.5 million US dollars in 2014, exceeding $349.5 million US dollars in 2013 by 13.2%. This was the result of higher export volumes, which

30

increased by 15.8%, from 97,173.8 T.M. in 2013 to 112,483.0 T.M. in 2014; coffee exports were 7.7% in 2014, and they were primarily sent to USA, Venezuela and the European Union.

d) Gold exports generated $387.0 million US dollars in 2014. The main buyers of Nicaraguan gold are Canada and USA.

e) Shrimp exports had a 29.6% increase in value during 2014 with respect to 2013. This was determined by a 32.0% growth in exports volumes. Exported volumes of shrimp went from $171.2 million US dollars in 2013 to $221.8 million US dollars in 2014, and volumes from 26,144.1 MT to 34,514.7 MT. It was exported to markets such as Mexico, the European Union, USA, Taiwan, Japan, among others.

f) On the other hand, sugar exports grew from $186.8 million US dollars in 2013 to $220.9 million US dollars in 2014. This represented an 18.3% increase; while exported volumes increased from 388,157.2 MT to 496,077.3 MT, i.e. 27.8%. It is worth mentioning that sugar is one of our most diversified goods in terms of destination markets. In 2014, the main buyers were Venezuela, USA, Ghana, Taiwan, Spain, Chile, Canada and Haiti.

In 2014, the main destinations of Nicaraguan exports were USA, including Puerto Rico and the USA Virgin Islands, (46.9%); Mexico (12.0%), Venezuela (7.6%), Canada (4.9%), El Salvador (4.5%), Honduras (3.0%), Costa Rica (3.0%). In terms of economic regions, the European Union had a participation of 6.3%, Central America (12.3%), Asia (3.3%)13.

5. Ease of Access To and From Nicaragua Nicaragua has an international airport located in the capital city, Managua, and three national airports located in Bluefields, Puerto Cabezas and Corn Island. There are also rural airports in Nueva Guinea, San Carlos, Siuna, Waspan, Rosita and Bonanza. The International Airport Augusto C. Sandino was classified as one of the safest in Latin America. Airlines flying to Nicaragua have connections to destinations in the North, Central and South America, as well as Asia and Europe. The airport serves the following international Airlines: American Airlines, United Airlines, Delta, Spirit, Copa and AVIANCA. There are direct flights from Nicaragua to 9 destinations, 4 of them to cities in the United States of America.

13 Executive Report on Nicaraguan Foreign Trade, 2014, MIFIC, [Online] [consulted on March 19, 2015]. Available at www.rpi.mific.gob.ni

31

DIRECT FLIGHTS FROM NICARAGUA TO CITIES IN THE UNITED STATES OF AMERICA

City Duration Airline Atlanta, USA 3 h

40 m Delta Airlines

Fort Lauderdale, USA

2 h 25 m

Spirit Airlines Houston, USA 3 h

25 m United Airlines

Miami, USA 2 h 35 m

American Airlines, AVIANCA TO CITIES IN CENTRAL AMERICA

Guatemala 1 h 15 m

Copa Airlines Panama 1 h

35 m Copa Airlines

San Jose, Costa Rica 1 h 5 m

Copa Airlines, Lacsa, Nature Air San Salvador, El

Salvador 1 h 0

m AVIANCA and Lacsa

Tegucigalpa, Honduras

1 h 0 m

La Costeña The International Airport Augusto C. Sandino also has a cargo terminal that provides services to four cargo carrier airlines. Cargo airlines handle and transport cargo from and to North, Central and South America and Europe. They have their own warehouses to store the cargo they transport. Air cargo transport services are provided by American Airlines Cargo, Copa Airlines Cargo, Avianca Cargo, UPS Air Cargo and Arrow Air.

5.1. Land Connection Nicaragua can be reached by land in approximately 9 hours: from Tegucigalpa (Honduras) or San Salvador, El Salvador in the North and from San Jose (Costa Rica) in the South. International Land Transport Companies are: KING-QUALITY, NICABUS INTERNACIONAL, TICABUS and TRANSNICA.

5.2. Customs Offices Nicaragua has several land and maritime customs offices throughout the national territory. The main customs offices in the country are outlined below:

Office location Observation International Airport Managua, Managua Air Terminal Guasaule Somotillo, Chinandega Border with Honduras El Espino Somoto, Madriz Border with Honduras Las Manos Ocotal, Nueva Segovia Border with Honduras Peñas Blancas Sapoá, Rivas Border with Costa Rica Puerto Corinto Corinto, Chinandega Exit to the Pacific Ocean Puerto Arlen Siú El Rama, RAAS Exit to the Atlantic Ocean

32

IV. LEGAL FRAMEWORK OF INTEREST TO INVESTORS

1. Legislation promoting and protecting investments The Constitution of Nicaragua guarantees the principle of legality, legal safety, constitutional supremacy, publicity of norms, non-retroactive laws and interdiction of public powers. In this sense, it established that: Every person has the right to have legal capacity and personality, the law is not retroactive, except in penal matters when it favors the accused; no position awards the person performing it, other functions than those conferred by the Constitution and the laws; the administration of justice guarantees the principle of legality and access to justice through the implementation of the law in pertinent matters or processes; the Political Constitution is the fundamental charter of the Republic, all other laws are subordinated to it; and no Power of the State, government body or official will have other opportunities, powers or jurisdiction than those conferred by the Political Constitution and the laws of the Republic. Nicaragua has achieved a proper socio-economic climate for investments as a result of the opening and globalization of markets, standards and laws consistent with the Constitution that provide legal certainty to the foreign investor. In this line of action, Law N° 344 on Foreign Investment was approved. It is based on the Political Constitution, article 100 that establishes the obligation of the State of Nicaragua to approve foreign investment laws. The purpose of this law is to establish standards that will generate trust and credibility for the investment climate, will eliminate discretionary powers and will simplify and expedite processes to benefit the investor’s legal certainty. Similarly, this Law establishes that foreign investors will have the same rights and means to exercise those rights under conditions equal to those of national investors. It also recognizes that foreign investors have full rights to enjoy, use and own the property related to their investment without any other limitations than those established by the Political Constitution. They may have free access to purchase and sell available foreign currency and free Currency; that is, there are no restrictions with respect to conversion or transfer of funds related to investments. There is freedom of transfer of profits, dividends, and revenue, with prior payment of taxes and freedom to pay and send overseas payment for debts contracted abroad, interests: royalties; income and technical assistance.

33

Foreign investment interested in the benefits contained in such law, must be registered at the Foreign Investment Registry managed by the Ministry of Industry, Development and Trade for such purpose. For another part, institutions involved in investment development have the applicable administrative resources for affected parties to file claims and enforce their rights. Similarly, there is an Appeal for Legal Protection as a constitutional control mechanism established in the Political Constitution which may be used by any national citizen or foreign national who perceives a deterioration or detriment of his constitutional rights as a result of an act, resolution, order, action or omission of a public administration agent or official. In addition, Nicaragua is positioned in the world market through several bodies of which it is a member such as the World Trade Organization (WTO), the Central America Integration System (SICA), institution of which Nicaragua is a member and its Council of Ministers of Economy and Trade of Central America (COMIECO), the Secretariat for Central American Economic Integration (SIECA), the Executive Committee of Economic Integration (CEIE) and the Central American Bank for Economic Integration (BCIE). It is also part of the International Centre for Settlement of Investment Disputes (ICSID), Multilateral Investment Guarantee Agency (MIGA), the Overseas Private Investment Corporation (OPIC), the United Nations Commission on International Trade Law (UNCITRAL), of the New York Convention and the Inter-American Convention on International Commercial Arbitration, and agreements signed with the Multilateral Investment Guarantee Agency of the World Bank (MIGA). This ample international set of standards regulates the commercial relations of Nicaragua with the world, becoming a favorable destination for investment and economic development.

2. Social Security and Labor Laws Labor and social security laws are an important part of Nicaraguan legal structure since they are based on the Political Constitution. The Constitution establishes working rights and conditions to ensure: the participation of workers in Company management; equal salaries in identical conditions; physical integrity, health, safety and decrease of professional risks; eight-hour work day, work stability in accordance with the law; and social security for special protection. Labor relations are regulated by Law N°185 Labor Code, which is a public policy legal instrument establishing the minimum rights and obligations of employers and workers.

34

2.1. Work Day A work day is the time during which a worker is at the disposal of the employer, fulfilling his labor obligations. A work day may be: a day shift, to be performed during the day from six o’clock in the morning to eight o’clock at night on the same day; a night shift, to be performed from eight o’clock at night to six o’clock in the morning the next day; and mixed shift, to be performed in a period of time that is partially during the day and partially at night. Notwithstanding the foregoing, a work day will be considered a night shift and not a mixed shift when more than three and a half hours are worked at night. The effective day shift is 8 hours per day and 48 hours a week; an effective regular night shift is 7 hours a day and 42 hours a week; and a regular mixed shift is 7 hours and a half a day and 45 hours a week. Work performed outside regular work shifts constitutes overtime. Overtime will be paid as 100% more than what the employee receives for a regular work day. The maximum time is 3 hours a day in addition to regular hours and it cannot exceed 9 hours a week.

2.2. Salaries Salaries will be paid in the legal currency, on a work day, at the place where the service is provided within the term and amount set in the contract arising from the working relation. Default in payment of salaries within the time agreed or ordered by law, as the case may be, forces the employer to pay the worker for the following two working weeks, a tenth above the due amount for each week of default, except in case the default is due to Force Majeure or an Act of God. The seventh day will be remunerated; if the salary is paid bi-weekly, it is understood that they are included in the remuneration. All legal deductions will be made from the salary.

35

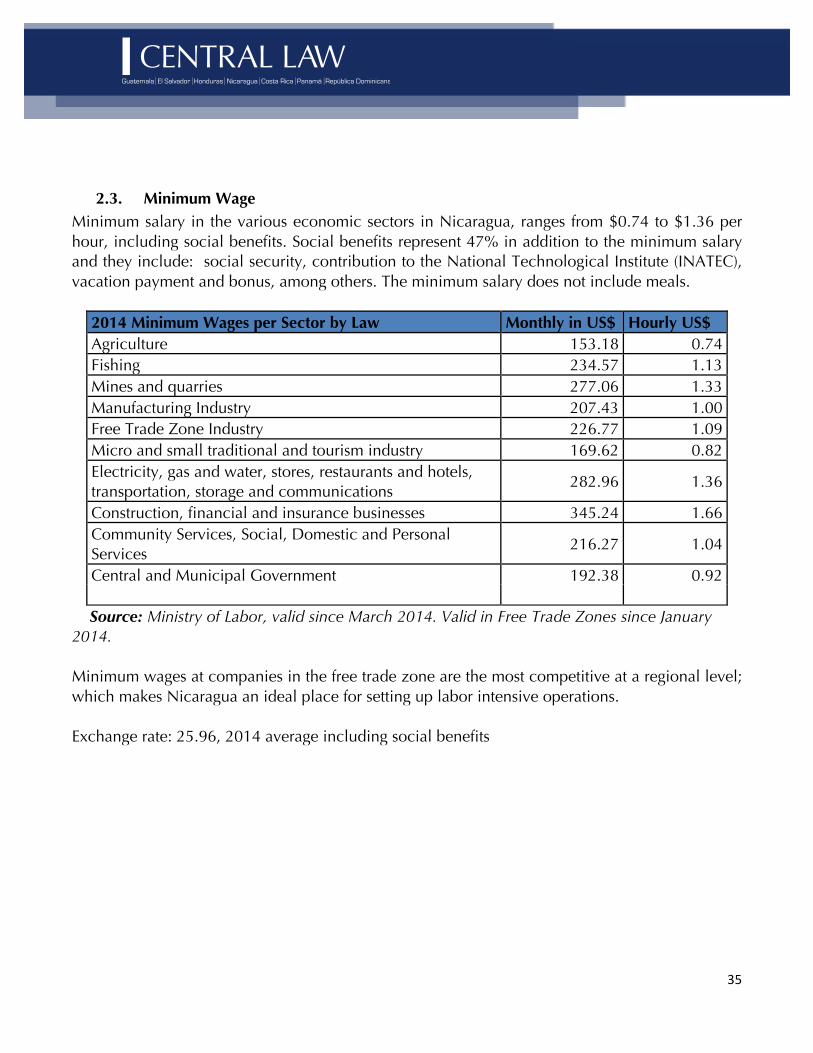

2.3. Minimum Wage Minimum salary in the various economic sectors in Nicaragua, ranges from $0.74 to $1.36 per hour, including social benefits. Social benefits represent 47% in addition to the minimum salary and they include: social security, contribution to the National Technological Institute (INATEC), vacation payment and bonus, among others. The minimum salary does not include meals.

2014 Minimum Wages per Sector by Law Monthly in US$ Hourly US$ Agriculture 153.18 0.74 Fishing 234.57 1.13 Mines and quarries 277.06 1.33 Manufacturing Industry 207.43 1.00 Free Trade Zone Industry 226.77 1.09 Micro and small traditional and tourism industry 169.62 0.82 Electricity, gas and water, stores, restaurants and hotels, transportation, storage and communications

282.96 1.36

Construction, financial and insurance businesses 345.24 1.66 Community Services, Social, Domestic and Personal Services

216.27 1.04

Central and Municipal Government 192.38 0.92

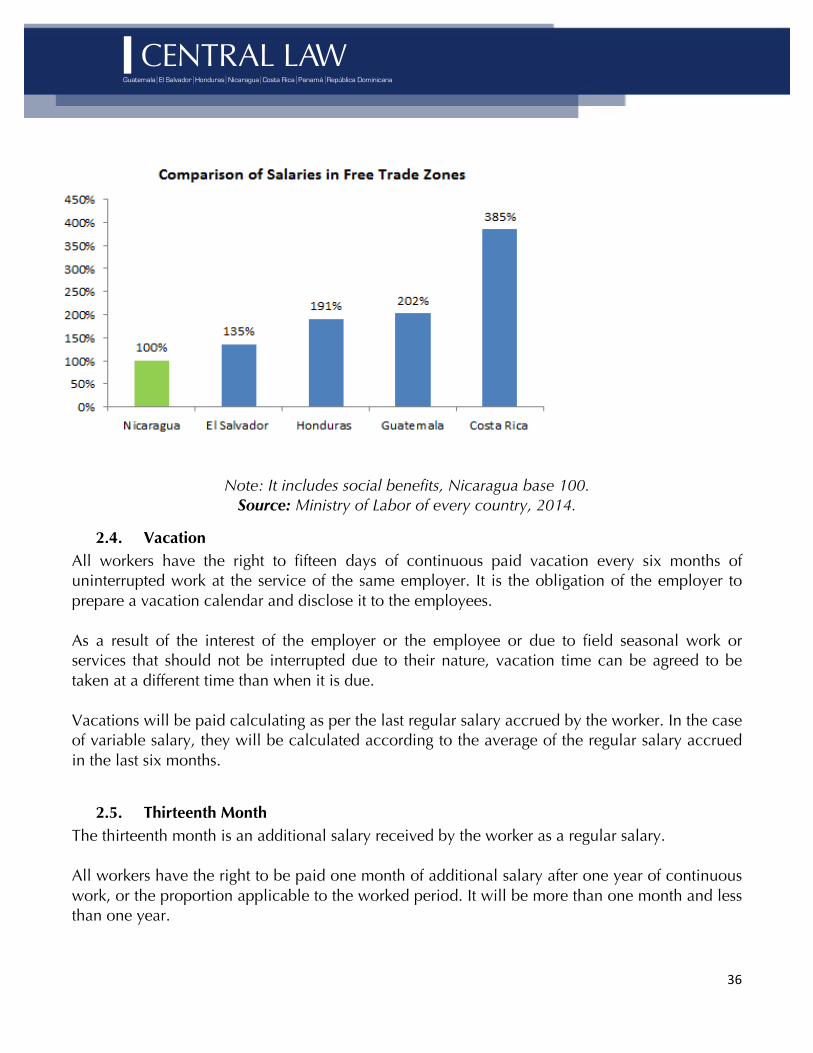

Source: Ministry of Labor, valid since March 2014. Valid in Free Trade Zones since January 2014. Minimum wages at companies in the free trade zone are the most competitive at a regional level; which makes Nicaragua an ideal place for setting up labor intensive operations. Exchange rate: 25.96, 2014 average including social benefits

36

Note: It includes social benefits, Nicaragua base 100.

Source: Ministry of Labor of every country, 2014.

2.4. Vacation All workers have the right to fifteen days of continuous paid vacation every six months of uninterrupted work at the service of the same employer. It is the obligation of the employer to prepare a vacation calendar and disclose it to the employees. As a result of the interest of the employer or the employee or due to field seasonal work or services that should not be interrupted due to their nature, vacation time can be agreed to be taken at a different time than when it is due. Vacations will be paid calculating as per the last regular salary accrued by the worker. In the case of variable salary, they will be calculated according to the average of the regular salary accrued in the last six months.

2.5. Thirteenth Month The thirteenth month is an additional salary received by the worker as a regular salary. All workers have the right to be paid one month of additional salary after one year of continuous work, or the proportion applicable to the worked period. It will be more than one month and less than one year.

37

The thirteenth month will be paid according to the last salary received, except when a different salary has been accrued through a different model. In that case, it will be paid according to the highest salary received during the last six months. The thirteenth month shall be paid within the first ten days of December of each year, or within the first ten days upon completion of the work contract. Should the employer fail to do so, it will pay the worker compensation equivalent to the value of one working day for every day of delay.

2.6. Termination of Employment Individual work contracts may be for a limited or unlimited period of time. The work contract or relationship will be for an unlimited period of time when there is no set term or when the contract for a limited period of time has expired and the worker continues to provide services for another thirty days or, when the term of the second contract extension has expired and the worker continues working or when it is extended again. The individual contract or working relation may end:

a) Due to the expiry of the agreed term or completion of the work or service that originated the contract; in case of death or permanent incapacitation of the employer that specifically results in the termination of the company; or due to the death or permanent incapacitation of the employee; due to conviction or incarceration of the employee; cessation of industry, store or service for economic reasons; by firm legal ruling that entails the final disappearance of the company; by termination of contract according to the law; due the retirement of the employee; due to Force Majeure or an Act of God that precisely results in closing the company.

b) Regardless the cause of the work contract termination, the employer is obligated to pay the employee, or to whom it may concern, the proportional part of benefits such as: vacations and the thirteenth month.

c) Where the contract is for an indefinite period of time, the worker may terminate it by notifying the employer verbally or in writing fifteen days in advance.

d) Should the work contract for an indefinite period of time be rescinded by the employer without justification, the employer shall pay the worker compensation equivalent to: one month of wages for each of the first three years of work; twenty days of salary for every year of work from the fourth year onward. In no case the compensation will be less than a month or more than five months. Fractions of years worked will be settled proportionally.

2.7. Unions and Collective Agreements Unions are formed in accordance with the Labor Code. For the purposes of obtaining legal personality, they must be registered in the Registration Book of Trade Union Organizations of the

38