Embed Size (px)

Citation preview

A C l e A rwAt e r t M t t e A M r e p o rt

ENTERPRISE RESOURCEPLANNING REPORT 2013

Global presence,Global expertise

MUMBAI • SHANGHAI/BEIJING • MUNICH • ZURICH • TOKYO NEW YORK/CHICAGO • LONDON • MADRID • PARIS

Want proof? Our global technology team has completed over 100 deals in the last three years.

A CLEARWATER TMT TEAM REPORT 3

welCoMe

Given our reliance today on all things IT, you might be surprised to learn that the field ofEnterprise Resource Planning (ERP) traces its roots to the manufacturing sector whereMaterial Requirement Planning (MRP) systems first used computers to automate planning for components.

Over time such principles fed through to other business functions such as customerdatabases, sales orders, purchase orders and stock, such that today we have ended up with amulti-billion dollar ERP industry that just keeps on growing.

In today’s economic climate the value of ERP software has never been greater. With FDsfirmly in charge of budgets, the importance of having ready access to the numbers in abusiness, while also configuring software to a company’s needs to help drive efficiencies, is paramount.

Typical of the trend is the recent launch by the Access Group (profiled on page 12) of its ownCloud solution which allows FDs to instantly view key KPIs and up-to-date information on thefinancial position within the business.

Access has been one of the most active players in the M&A market and during the first halfof 2013 we have already seen a string of notable transactions which point to another year ofthought-provoking M&A in the sector. ACS’ acquisition of ERP operator CSH, which servesthe professional services market, is a particularly noteworthy deal, and one which turns whatwas originally a healthcare-focused buy-and-build into a serious ERP operator. Another is thereturn of Richard Beaton to the Tekton business he first sold to Sage five years ago (see page8) in an ISIS-backed buyout on which we were delighted to advise.

The consensus is that a lot of ERP businesses will come to market over the next few years,especially because so many of them remain under the control of owner managers nearingretirement. The key for many of these companies in this economic climate will be to getanother good year or two of trading behind them, and given the market dynamics this willsurely be achievable for many of them. Another key will also be continued collaboration withindustry giants such as Microsoft who have noticeably upped their game in the ERP arena inrecent years.

I hope you enjoy the report.

Carl Houghtonpartner

@CCFTech

/company/clearwater-corporate-finance

ContentsOVERVIEW 4State of the ERP market

TEKTON 8Richard Beaton talks exclusively about buying back the business

M&A REVIEW 10A look at the key ERP deals over the past year

CLOUD 12How players are stepping up their Cloud offering

MULTI-CHANNEL 14An analysis of the retail ERP space

PRIVATE EQUITY 16ERP remains attractive to PE players

CONSTELLATIONSOFTWARE 18An interview with the globalconsolidator

CLOUDEX 19ERP companies fare well in ourindex of global tech companies

COMPANY INDEX 20In-depth analysis of the world’stop ten largest ERP companies

This report is published by Clearwater InternationalEditor : Jim PendrillDesign: www.creative-bridge.comSubscription: [email protected] part of this publication may bereproduced or used in any form without prior permission of Clearwater International

ENTERPR I S E R E SOURCE P LANN ING4

In today’s economic climate ERP technology could providethe perfect solution.

MArket overview

To understand what’s driving the ERP market today,one need look no further than one of the standouttransactions of 2013 so far.

In March Advanced Computer Software Group, aprovider of healthcare and business managementsoftware and services, acquired Computer SoftwareHoldings (CSH) from HgCapital for £110m. CSH is aleading provider of accounting and back officesoftware to the UK professional services market aswell as of Customer Relationship Management (CRM)software for the Not-For-Profit (NFP) market.

Vin Murria, Chief Executive of Advanced, commentedat the time of the deal: “CSH has strong recurringrevenues and cash generation and proprietarysoftware IP. The addition of this business will enable usto widen our addressable markets and, in particular, togrow our back office solutions capabilities.”

As ever, Murria’s timing is impeccable. What startedout as a healthcare market buy-and-build is graduallymorphing into an ERP provider to be reckoned with in a market which is showing genuine signs of recovery.

Although TechMarketView* see growth in the UKEnterprise Software space slowing over the next fewyears, there are segments within the market that aremuch stronger and which are driving strongperformances from many of our mid-market focusedUK-based providers.

Data from Apps Run the World suggests that whilstthe market for ERP systems for enterprise customers(with more than 5,000 employees) will grow at aCAGR of just 2.4% between 2010 and 2015, theCAGR for the mid-market (or companies with

*UK Software and IT Services Market Trends & Forecast 2012

between 100 and 1,000 employees) is much higher at 5.6% and higher still for the SME segment.

The very latest views from Forrester also cite agrowing interest in ERP investment and a market thatis looking considerably more rosy than this time lastyear. Analyst China Martens commented: “Newinformation from clients today who are activelylooking for upgrades or who are looking to jump intoERP appears pretty healthy.”

To some extent it is no surprise that ERP technologyis having considerable resonance in a climate in whichboth businesses and governments across the westernworld continue to seek technological solutions toimprove their performance and efficiency. Indeed ERPtechnology provides exactly the kinds of metrics andreporting systems that companies want in today’seconomic climate.

As Martin Wygas at Lyceum Capital says: “If you aremaking operational improvements to your businessthen these can be measured very clearly via ERP

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

%

09/10 10/ 11 11/12 12/13 13/14 14/15

UK software market growth: 2009-2015

–– Software products n Productivity and Business Applications

Source: TechMarketView

A CLEARWATER TMT TEAM REPORT 5

systems. You can track their effect month on monthvery easily, you can see the numbers.”

But although ERP is certainly fit for purpose in today’s climate of austerity and efficiency, the oldmodel of an immense on-premise system is beingincreasingly challenged.

Unsurprisingly, the main challenge is expected tocome from the Cloud although so far the juryappears to still be out with take-up of Cloud systemsnot as widespread as some thought, whilst others seea new adoption cycle already underway. Forresterreports that although many customers are still notactively considering SaaS model ERP today, “they areat least looking at it”.

The stumbling block appears to be that customersgenerally don’t want to switch everything in theirbusiness over to a SaaS model in one go, oftenbecause one of the key strengths of ERP is the veryconfigurability of products to particular companiesand business functions.

Another are the costs involved. As Mark Thompson,Chief Executive of software solutions provider m-hance, adds: “The financial case behind the Cloudoffering has to be compelling. Most companies willupgrade either because of the return of investment(ROI) or because of efficiencies that come out ofhaving that new solution. As a provider you areconstantly looking to see if you can make a ROI on aparticular solution.”

Simon Weeks, Chief Executive at Maginus, sayschanging your ERP system is a little like changing yourhome boiler. “You know you could go out tomorrowand buy a more efficient system1 but you are unlikelyto do that unless the existing boiler packs upcompletely or is about to pack up. The reality today isthat a lot of companies are limping along at themoment because of the economy and so fewerpeople are changing systems.”

Weeks, whose firm specialises in software for multi-channel retailers, says a notable trend of recent timesis companies making more bite-sized investmentswhere they can see more instant results. “Buyers are

more canny these days. A few years ago if youreplaced an ERP system the traditional route was forthe seller to take you through a standard sales processwhich outlined all the solutions on offer. Then whenthe client was ready they would place an order for allthe software they needed in one big chunk.

“That certainly doesn’t happen now. What clientswant is the same selection process, but they thentend to only buy each part of the software as theyneed it. If you have a 12-month implementationprocess you don’t need all the software on day one.FDs are looking for more convenience.”

Against this backdrop Weeks says ERP providers have to act like service companies and ensure they don’t go over time or budget, commissioningwork upfront and then giving a fixed price forimplementation. Getting the budget right and not deviating from it has become key.

Analysts echo this sentiment with Forrester reportingthat “in general the pendulum is swinging to thecustomer having more choice”, and TechMarketViewseeing that “software is morphing into a series ofinterrelated platforms supporting mix-and-matchcomponent applications and services, where provisioncan be on or off premise, or a hybrid of the two”.

Thompson says the market today tends to split intothree distinct types of customer. “Firstly there are thesmaller businesses who say to themselves ‘why do I

0 50 100 150 200 250 300

Sage

ACS

Iris

Unit4

K3

Access

Principal players in UK mid-market ERP

Uk software revenue £m

Source: Clearwater; company accounts

“If you are making operational improvements to your business thenthese can be measured very clearly via ERP systems. You can track theireffect month on month very easily, you can see the numbers.”

Martin Wygas, Lyceum Capital

ENTERPR I S E R E SOURCE P LANN ING6

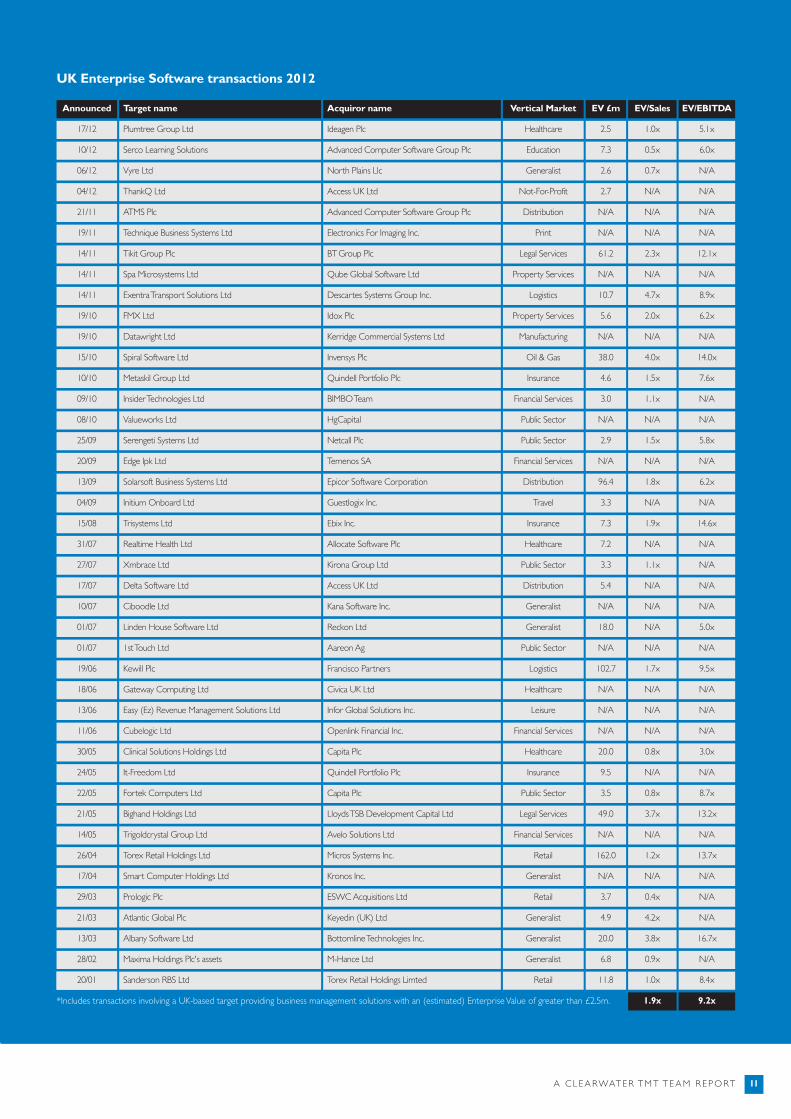

Announced

25/03

Acquiror name

Lloyds TSB Development Capital Ltd

Vertical market

Insurance

Target name

Validus-IVC Ltd

EV £m

12.0

EV/Sales

N/A

EV/EBITDA

N/A

N/A N/A N/A

N/A N/A N/A

110.0 1.8x 8.3x

N/A N/A N/A

N/A N/A N/A

N/A N/A N/A

73.9 3.1x 12.5x

9.3 5.1x 11.7x

N/A N/A N/A

25/03 Capita Plc Public SectorSTL Technologies Ltd

11/03 Concur Technologies Inc. GeneralistContgo Ltd

08/03 Advanced Computer Software Group Plc Professional ServicesComputer Software Holdings Ltd

06/03 Open Text Corporation GeneralistResonate KT Ltd

06/03 MBO team GeneralistSoftware (Europe) Ltd

25/02 Lefebvre Software SAS GeneralistCezanne Software Ltd

15/02 Pattington Ltd Financial ServicesFfastfill Plc

07/02 Wilmington Group Plc HealthcareNHiS Ltd

11/01 Wall Street Systems Services Corporation Fnancial ServicesIT2 Treasury Solutions Ltd

Uk Enterprise Software transactions, January - March 2013

even need to bother having a server anymore?’ and forwhom it is significantly cheaper and more reliable tooutsource. Then there are the really big companies forwhom the case is largely still the opposite. That leavesthe middle ground where there is definitely the mostactivity, change and opportunity for the likes of us.”

Meantime given the high barriers to entry in themarket, collaboration across the industry will remainkey. The point is no better illustrated than by thestrategy of Eque2 (see page 8), formerly the TektonGroup, which like many ERP companies sells the ERPsolutions of the likes of Microsoft and Sage and thenadds modules (or granules as the industry termsthem) which are more specific to their sub-sector.

As Eque2 Executive Chairman Richard Beaton says: “Inour sector which is construction, companies would notbuy the Microsoft product as it is, they would want tomake modifications to it which is where we come in.”

Beaton has worked in many different niche marketswithin the ERP sector and says every industry has itsown distinct peculiarities. “Whether it be distributors,electrical wholesalers, road hauliers, ad companies orconstruction companies, they all work in completelydifferent ways.”

The point is echoed by Thompson. “The challenge isto try and discern the particular issues that areaffecting specific sectors and see how those challengesare changing from year to year, and then adapting whatwe do accordingly. If you take a market like financialservices where we are strong, we are starting todevelop services which are much more tailored andfront-end like CRM, forecasting and security solutions.”

Better Capital-backed m-hance has been anotherparticularly notable player in the M&A market in recentyears following the acquisitions of Calyx Software, Trinity

Computer Services, sub-divisions of Touchstone Groupand Maxima Holdings. These acquistions, along withorganic growth, have helped sales increase 45% year onyear, and Thompson predicts the company will “double insize” over the next couple of years. “The question for usnow is working out what else is out there that will eitherbroaden our business or bring us new customers.”

Given the strong market dynamics of the sector it isno surprise that M&A in the world of ERP software -in the UK at least - remains lively with assets appealingto a broad range of buyers. Although Private Equity(PE) investment has been a key feature of the marketover the last few years, both in the UK and globally,2012 also saw some interesting strategic transactionsincluding established players beefing up their offeringgeographically, newer consolidators executing bolt-ondeals, and buyers from outside of the software spacerecognising the many attributes that business softwareplayers have to offer.

That said, PE interest in the market has remainedbuoyant with investors continuing to be attracted by thepotential for upturn in the market as well as strongmargins and recurring income. Investors also continuedto show a desire to back their existing teams leading toa number of PE-backed platform vehicles really rampingup activity during 2012, bolting on new products, dealerbases or vertical expertise to reshape the core offering.

Our data demonstrates a clear disparity in valuebetween the larger transactions (over £500m invalue) which have attracted strong double digitmultiples, and the mid-market transactions which havetended to land in the 8-9x EBITDA value range.However, in the SaaS world even the smallest playerscontinue to attract high values demonstrating thatmost expect the Cloud shift to happen in the ERPmarket, albeit we could have a bit longer to wait yet.

A CLEARWATER TMT TEAM REPORT 7

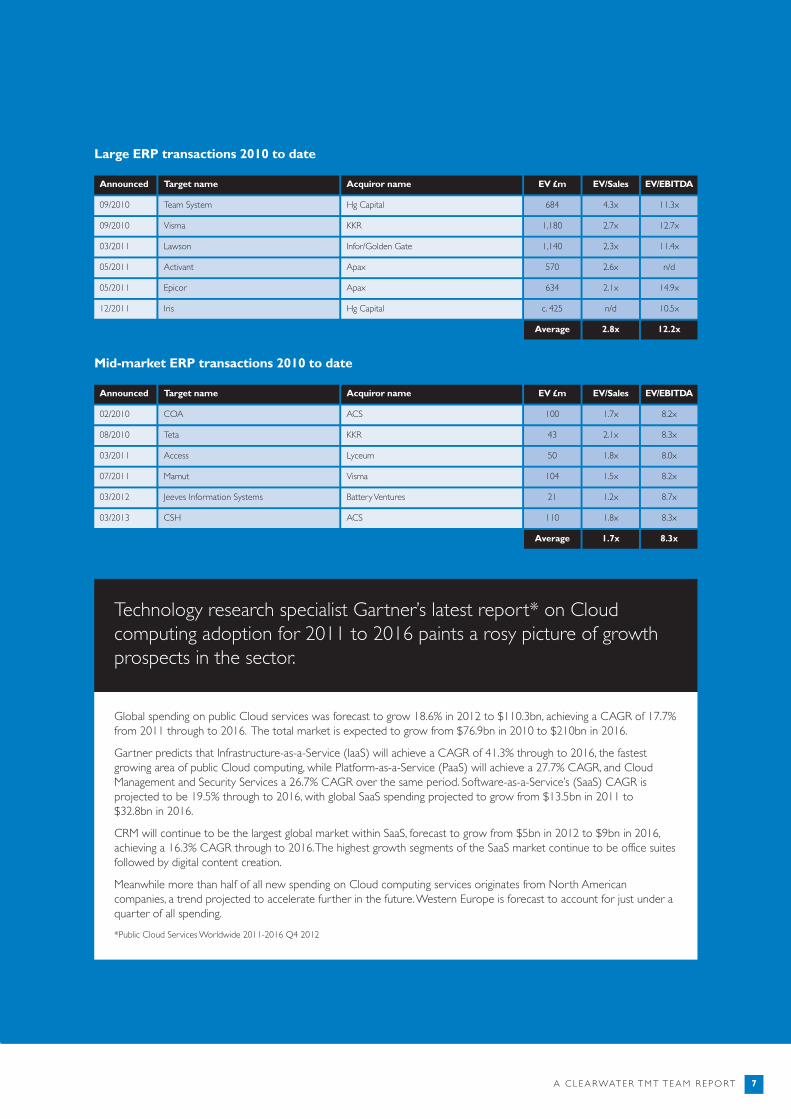

Announced

09/2010

Acquiror name

Team System

Target name

Hg Capital

EV £m

684

EV/Sales

4.3x

EV/EBITDA

11.3x

09/2010 Visma KKR 1,180 2.7x 12.7x

03/2011 Lawson Infor/Golden Gate 1,140 2.3x 11.4x

05/2011 Activant Apax 570 2.6x n/d

05/2011 Epicor Apax 634 2.1x 14.9x

12/2011 Iris Hg Capital c. 425 n/d 10.5x

Average 2.8x 12.2x

Large ERP transactions 2010 to date

Announced

02/2010

Acquiror name

COA

Target name

ACS

EV £m

100

EV/Sales

1.7x

EV/EBITDA

8.2x

08/2010 Teta KKR 43 2.1x 8.3x

03/2011 Access Lyceum 50 1.8x 8.0x

07/2011 Mamut Visma 104 1.5x 8.2x

03/2012 Jeeves Information Systems Battery Ventures 21 1.2x 8.7x

03/2013 CSH ACS 110 1.8x 8.3x

Average 1.7x 8.3x

Mid-market ERP transactions 2010 to date

Global spending on public Cloud services was forecast to grow 18.6% in 2012 to $110.3bn, achieving a CAGR of 17.7%from 2011 through to 2016. The total market is expected to grow from $76.9bn in 2010 to $210bn in 2016.

Gartner predicts that Infrastructure-as-a-Service (IaaS) will achieve a CAGR of 41.3% through to 2016, the fastestgrowing area of public Cloud computing, while Platform-as-a-Service (PaaS) will achieve a 27.7% CAGR, and CloudManagement and Security Services a 26.7% CAGR over the same period. Software-as-a-Service’s (SaaS) CAGR isprojected to be 19.5% through to 2016, with global SaaS spending projected to grow from $13.5bn in 2011 to $32.8bn in 2016.

CRM will continue to be the largest global market within SaaS, forecast to grow from $5bn in 2012 to $9bn in 2016,achieving a 16.3% CAGR through to 2016. The highest growth segments of the SaaS market continue to be office suitesfollowed by digital content creation.

Meanwhile more than half of all new spending on Cloud computing services originates from North Americancompanies, a trend projected to accelerate further in the future. Western Europe is forecast to account for just under aquarter of all spending.

*Public Cloud Services Worldwide 2011-2016 Q4 2012

Technology research specialist Gartner’s latest report* on Cloudcomputing adoption for 2011 to 2016 paints a rosy picture of growthprospects in the sector.

ENTERPR I S E R E SOURCE P LANN ING8

Does Richard Beaton consider himself lucky? “You wouldn’t call it luck in the sense that I sold anexceptional business with a market-leading position ata time when Sage was looking for a market-leader inthe construction software space,” says the softwaretycoon. “What was lucky was the timing. No-oneexpected the downturn to last five years. It has beencolossal and everyone has had a tortuous time.”

The sale of the Tekton Group in early 2008 to SageGroup for £21m must rank as one of the most timelyexits in the software industry in recent times, not leastbecause the construction sector has been so crippledby the recession. As Beaton adds: “It has been a verydifficult time for the industry. Companies havecompletely redefined business models, completelyrestructured businesses, formed completely differentways of working.”

Against this economic backdrop it is little wonder thatSage had trouble making the deal work, but Beatonsays the company would be the first to admit that itfailed to deliver the strategy that it wanted to deliverfor Tekton. “At the time a lot of what Sage was tryingto do was to leverage the vertical market and takethe IP that existed within Tekton and move it intoSage products. The mistake they made was that forwhatever reason this just never happened.”

Fast forward to 2013 and Beaton says it is littlesurprise that Sage looked at their strategy and decidedit no longer wanted to pursue such vertical marketgrowth. “Ultimately Sage knows it can invest a certainamount in a horizontal market and get great coveragebecause of the reach of its customers. By the sametoken it knows it can invest the same amount in avertical market but get far less reach. They did thenumbers and asked where they were going to get the

maximum return to cement the long-term future ofthe business. It was really as simple as that. To behonest I’d probably agree with that as a strategy.”

With his unsurpassed network in the softwareindustry, forged from a string of notable M&A dealsstretching back the best part of 20 years, late last yearBeaton became aware of the way the tide wasturning and seized the moment, taking up an offerfrom within Sage itself of exploring a buyout to buythe business back.

As he explains: “Given all the investment that Sagehad made in the product since buying Tekton, it waskeen to sell to someone who really knew the productand really believed in it. I have a lot of admiration forSage because it did not let its heart rule its head. Itwas brave enough to say ‘this is not the way we aregoing to go’ and decided to return these customersto a home where they knew they would be lookedafter. They did not let emotion get in the way.”

After speaking with a number of PE houses Beatonput together a bid with ISIS Equity Partners, a housewith whom he had worked previously on investmentssuch as educational software business Micro LibrarianSystems, which was recently sold to Capita.

With the Tekton deal completing in Spring 2013 andhis feet now back under the table as ExecutiveChairman, Beaton admits it feels like groundhog dayat Tekton, now renamed Eque2. “It almost feels likethe last five years haven’t happened. The irony is thatwhen Sage bought the business we were midwaythrough making a few acquisitions. I have come backto my desk and it’s almost like ‘right, let’s carry onwhere we left off ’ in terms of doing deals.”

Five years after selling the business to Sage, Richard Beaton isback at the helm of construction specialist Tekton, now renamedEque2. We find out why he bought it back.

sAge retUrns

Beaton’s strategy for Eque2 is to now take a businesswith £10m sales and triple its turnover through acombination of strengthening its ties and winning newbusiness with Microsoft and Sage, while also acquiringits own IP businesses that will extend its licencingfootprint away from just back office functions.

“There is a huge market for us to go at coveringother software that construction companiesoutsource to reduce risk and increase efficiencies,”adds Beaton. “I genuinely think this is a business whichcan dominate its niche in contracting andconstruction. The key is to get the balance right interms of our own IP and third party sales, a mixwhich will make the business all the more valuablefurther down the line.”

The irony that Eque2 will further utilise Sage toexpand its reach, while also capitalising on thetechnological investment that Sage made in Tekton’sproducts, is not lost on Beaton. “Yes, over the last fiveyears Sage has invested a lot in rewriting products inthis space and writing big chunks of IP and we willbenefit from that. By the same token Microsoft’soffering and vision in this whole space has movedforward leaps and bounds over the last five years too.We will now build a stronger brand with Microsoft inthe upper mid-market and with Sage in the lowermid-market. Five years ago there were others whomight have given us a run for our money in this space,but I believe there won’t be now.”

Beaton says Eque2 will also benefit from widertechnological change. “Although I say it’s a bit likegroundhog day being back here, from a technologicalperspective the web has moved forward significantlyover the last five years. The very way in whichoperational staff can interact with core systems haschanged significantly, while there are all sorts of web-based applications that are making it easier forsystems to work together that were not around fiveyears ago.”

Beaton doesn’t dismiss looking at deals abroad,although stresses that bedding down the UK operationis paramount. “It is an option to look overseas wherethere is growth and where there is a common

language. For instance the US is coming back and thereare real opportunities in areas such as the Middle East.”

Back in the UK does he think we are over the worstof the downturn? And what about the constructionsector which is still languishing? Could this dampenthe Eque2 party?

“I would never want to call the upturn but there isdefinitely a lot of pent-up demand out there in oursector,” insists Beaton. “There are a lot of people whohave done nothing with their operational systems forfive or maybe even 10 years and who will have tomake that investment at some point in order toremain competitive and efficient. On the wider front,one of the key ways in which the UK economy isgoing to get moving again is through investing ininfrastructure and construction.”

The M&A market itself has been no less challenging inrecent times, but Beaton says that if you put sensibleprices on the table you can get sensible deals away. “I have bought an awful lot of companies over the last20 years and, like anything, if you do somethingenough you tend to get good at it while you alsolearn from the mistakes you make along the way.When it comes to a deal I know what I am lookingfor and have a reputation for sticking to the deal. You do not buy as many companies as I have boughtwithout putting a fair deal on the table and sticking toyour guns.”

A CLEARWATER TMT TEAM REPORT 9

As well as Eque2 Beaton is Executive Chairmanat a number of other software companies. Theseinclude information security software specialistDeep-Secure; Sleek Networks which specialisesin the design, construction and support of ITinfrastructure; and HR and payroll firm Selima. “Ilike the interaction that the Executive Chairmanrole gives me and I get involved in more detailand activity than a typical non-exec would,” says Beaton.

Beaton’s recipe

“I have a lot of admiration for Sage because it did not let its heart rule itshead. It was brave enough to say ‘this is not the way we are going to go’and decided to return these customers to a home where they knew theywould be looked after. They did not let emotion get in the way.”

Richard Beaton, Eque2

The ERP sector has already seen some notable deals in 2013,continuing the trend seen over the past year.

2013 has already seen a number of reallyinteresting transactions in the ERP marketpointing to another year of thought-provoking M&A.

Perhaps the most noteworthy deal so farthis year has been ACS’ acquisition ofHgCapital-owned ERP operator CSHwhich serves the professional servicesmarket. The deal is ACS’ largest transactionto date and really transforms the modelfrom what was originally a healthcare-focused buy-and-build into a serious ERPoperator. The transaction was executed atjust over 8x EBITDA, which adds to ACS’acquisitions last year of Serco LearningSolutions and ATMS, a warehousemanagement system.

Buy-and-build has certainly been the nameof the game for Lyceum Capital-backedAccess (see overleaf) which has been oneof the most prolific acquirers in the market,adding assets including Not-For-Profit(NFP) specialist ThankQ as well as DeltaSoftware, another warehouse managementspecialist. But other investees have also gotin on the act over recent months. NVM’sKerridge investment acquiredmanufacturing specialist Datawright; andBetter Capital-backed m-hance started theyear with the acquisition of some assetsfrom consolidator Maxima Holdings.

There were also a number of newinvestments into the wider businessmanagement space that caught the eye.Probably most notable was US houseFrancisco Partners’ acquisition of Kewill ina bidding war which saw it win out against

stiff competition from fellow US houseSymphony to clinch the deal at £102.7m,or 9.5x EBITDA. This was a higher pricethan most predicted for Kewill and anindicator of the level of interest in theenterprise software market globally.

Other transactions in recent months haveincluded HgCapital making its firstinvestment from its Technology mid-market Mercury fund into Valueworks, aprovider of procurement solutions topublic sector customers. The ever-activeLDC also invested in BigHand, a digitaldictation workflow software developer.

However it isn’t all about PE. Over thepast year US strategic players havecontinued to see the same opportunitiesin the market as the PE players, leading toa couple of interesting transactions by two of the leading global players in theERP industry.

In September Epicor announced theacquisition of Solarsoft, a provider of ERPsolutions to the distribution market, in adeal which provided an exit for Solarsoft’sCanadian investors Marlin Private Equity.The deal marked the first majoracquisition by one of the leading ERPplayers in the UK in a number of years,suggesting that the recent spate of PEinvestment into the market is sparking anew round of activity at mid-market level.

Epicor was acquired by Apax Partners in2011 in a $1bn deal which merged thegroup with fellow ERP operator Activant.

Infor, which itself merged with Lawson in adeal backed by Golden Gate Capital in2011, also announced a UK deal, picking upEasy (EZ) Revenue Management Solutions,a SaaS operator with a particular focus onthe hotel industry. Indeed the focus formost of the M&A activity of the major ERP operators globally has been on addingSaaS-model point solutions, whetherhorizontal or vertical, with the aim ofbuilding up their subscription revenueswithout compromising their core on-premise business.

The usual suspects in terms of UKconsolidators have also been presentduring the year. Capita continued its reignas the most prolific acquirer of UKtechnology businesses adding assetsincluding Fortek, a provider of command,control and communication systems to theemergency service sector, as well asClinical Solutions which serves thehealthcare industry.

What was less predictable however, wasBT’s acquisition of Tikit, a provider ofsolutions to the legal services market for£62.4m, a racy12x EBITDA multiple, at theend of 2012. Tikit will sit within BTEnterprises which also includes businessessuch as retail technology specialists BTExpedite and Fresca, all of which operateon a standalone basis but which benefitfrom the BT brand and IT service capability.The transaction emphasises that enterprisesoftware remains a highly attractive marketwith positive drivers which appeal to arange of potential acquirers looking to buildsticky relationships with their customers.

M&A review

ENTERPR I S E R E SOURCE P LANN ING10

UK Enterprise Software transactions 2012

Announced

17/12

Target name

FMX Ltd

Acquiror name

Ideagen Plc

Vertical Market

Healthcare

Education

Generalist

Not-For-Profit

Distribution

Legal Services

Property Services

Property Services

Manufacturing

Oil & Gas

Insurance

Financial Services

Public Sector

Public Sector

Financial Services

Distribution

Travel

Insurance

Healthcare

Public Sector

Distribution

Generalist

Generalist

Public Sector

Logistics

Healthcare

Leisure

Financial Services

Healthcare

Insurance

Public Sector

Legal Services

Financial Services

Retail

Generalist

Retail

Generalist

EV £m

2.5

EV/Sales

1.0x

EV/EBITDA

5.1x

10/12

Datawright Ltd

Advanced Computer Software Group Plc 7.3 0.5x 6.0x

06/12

Spiral Software Ltd

North Plains Llc 2.6 0.7x N/A

04/12

Metaskil Group Ltd

Access UK Ltd 2.7 N/A N/A

21/11

Insider Technologies Ltd

Advanced Computer Software Group Plc N/A N/A N/A

19/11

Valueworks Ltd

Electronics For Imaging Inc. N/A N/A N/A

14/11

Serengeti Systems Ltd

BT Group Plc 61.2 2.3x 12.1x

14/11

Edge Ipk Ltd

Qube Global Software Ltd N/A N/A N/A

19/10

Solarsoft Business Systems Ltd

Idox Plc 5.6 2.0x 6.2x

19/10

Initium Onboard Ltd

Kerridge Commercial Systems Ltd N/A N/A N/A

15/10

Trisystems Ltd

Invensys Plc 38.0 4.0x 14.0x

10/10

Realtime Health Ltd

Quindell Portfolio Plc 4.6 1.5x 7.6x

09/10

Xmbrace Ltd

BIMBO Team 3.0 1.1x N/A

08/10

Delta Software Ltd

HgCapital N/A N/A N/A

25/09

Ciboodle Ltd

Netcall Plc 2.9 1.5x 5.8x

20/09

Linden House Software Ltd

Temenos SA N/A N/A N/A

04/09

1st Touch Ltd

Epicor Software Corporation 96.4 1.8x 6.2x

15/08

Kewill Plc

Guestlogix Inc. 3.3 N/A N/A

31/07

Gateway Computing Ltd

Ebix Inc. 7.3 1.9x 14.6x

27/07

Easy (Ez) Revenue Management Solutions Ltd

Allocate Software Plc 7.2 N/A N/A

17/07

Cubelogic Ltd

Kirona Group Ltd 3.3 1.1x N/A

10/07

Clinical Solutions Holdings Ltd

Access UK Ltd 5.4 N/A N/A

01/07

It-Freedom Ltd

Kana Software Inc. N/A N/A N/A

01/07

Fortek Computers Ltd

Reckon Ltd 18.0 N/A 5.0x

19/06

Bighand Holdings Ltd

Aareon Ag N/A N/A N/A

18/06

Trigoldcrystal Group Ltd

Francisco Partners 102.7 1.7x 9.5x

13/06

Torex Retail Holdings Ltd

Civica UK Ltd N/A N/A N/A

11/06

Smart Computer Holdings Ltd

Infor Global Solutions Inc. N/A N/A N/A

30/05

Prologic Plc

Openlink Financial Inc. N/A N/A N/A

24/05

Albany Software Ltd

Capita Plc 20.0 0.8x 3.0x

22/05

Quindell Portfolio Plc 9.5 N/A N/A

14/05

Lloyds TSB Development Capital Ltd 49.0 3.7x 13.2x

26/04

Avelo Solutions Ltd N/A N/A N/A

17/04

Micros Systems Inc. 162.0 1.2x 13.7x

29/03

Kronos Inc. N/A N/A N/A

13/03

ESWC Acquisitions Ltd 3.7 0.4x N/A

13/09

21/05

Bottomline Technologies Inc. 20.0 3.8x 16.7x

Maxima Holdings Plc's assets28/02 M-Hance Ltd Generalist 6.8 0.9x N/A

Atlantic Global Plc21/03 Keyedin (UK) Ltd Generalist 4.9 4.2x N/A

Exentra Transport Solutions Ltd14/11 Descartes Systems Group Inc. Logistics 10.7 4.7x 8.9x

Sanderson RBS Ltd20/01/2012 Torex Retail Holdings Limted Retail 11.8 1.0x 8.4x

1.9x 9.2x

Capita Plc 3.5 0.8x 8.7x

Plumtree Group Ltd

Serco Learning Solutions

Vyre Ltd

ThankQ Ltd

ATMS Plc

Technique Business Systems Ltd

Tikit Group Plc

Spa Microsystems Ltd

20/01

*Includes transactions involving a UK-based target providing business management solutions with an (estimated) Enterprise Value of greater than £2.5m.

A CLEARWATER TMT TEAM REPORT 11

ENTERPR I S E R E SOURCE P LANN ING12

ACCess All AreAs

With his passion for motor homes, Access’Commercial Director Chris Tossell confesses that oneday he dreams of travelling the globe in his pride andjoy. However his wanderlust may have to wait just alittle while yet given the growth of the softwareprovider since a buyout two years ago backed byLyceum Capital.

Tossell was one of the founders of Access more than20 years ago, but spent time out of the business towork abroad. A few years ago he was tempted backby Managing Director Alistair O’Reilly who thendecided he wanted to sell the business due to lifechanging circumstances. Tossell says: “From the startAlistair wanted to do a PE deal because he felt itwould give people the chance to roll over theirinvestment as the business grew.” In stepped Lyceumto fund a £50m buyout transaction backing new Chief Executive Chris Bayne.

Following that deal Access has embarked on anaggressive expansion strategy which has seen like forlike organic revenues grow by 14% per annum andthe successful execution of a buy-and-build plan,targeting sectors such as professional services,manufacturing and the Not-For-Profit (NFP) markets,as well as launching its own Cloud proposition AccessaCloud - a platform which includes applications forexpenses and document management with thestrapline “anytime, anywhere any device”.

aCloud is the start of the Cloud journey for Accesswhose core ERP product is an on-premise solutionprovided to around 4,500 clients, but which is tappinginto a market shift that could significantly impact thebusiness’ value on exit.

Tossell, who has headed the M&A drive within thebusiness, says: “We turned over £25m at the MBO, did £33m last year and are looking at £42m this year. The plan has always been to create a business worth£150m plus and given our momentum to date we arewell on the way to this. But with those aspirations weobviously need to keep asking ourselves how wemove that multiple needle.”

One of the obvious places to look for an example ofa successful Cloud ERP model is US pure playoperator NetSuite which recently reported a recordquarter, a profitable year and $190m cash in the bank.NetSuite’s break into profitability adds yet morecredence to the view that the concerns of companiesaround running their ERP systems in the Cloud arebeginning to ease. As businesses familiarise themselveswith Cloud applications in other categories such asCRM or Human Capital Management (HCM), theprospect of SaaS ERP looks less daunting and, in fact,has a range of benefits to outweigh the negativesincluding low investment cost, ease of managementand accounting compliance updates.

Gartner is predicting that SaaS-based ERP will growfrom 12% of the worldwide market in 2013 to 17%by 2016, growing at a CAGR of just under 14 percent and proving that the issues around configurabilityare no longer a deterrent for many. Indeed, althoughNetSuite has traditionally focused on a mid-marketcustomer base, recent wins have seen some majorcompanies such as Proctor & Gamble move toNetSuite technology and a Cloud model.

Although all of the major players have launched theirown Cloud solutions to the market - SAP’s BusinessBy Design and Oracle’s Fusion Apps for example -

On the back of a successful buy-and-build strategy the banks areknocking on the door of Access. Now the ERP software and servicesgroup has its sights set on the Cloud.

A CLEARWATER TMT TEAM REPORT 13

“The plan has always been to create a business worth £150m plus andgiven our momentum to date we are well on the way to this. But withthose aspirations we obviously need to keep asking ourselves how wemove that multiple needle.”

Chris Tossell, Access

most have had varying degrees of success, and issuesremain around the cannibalisation of their ownmodel. This conundrum has led to the market leadersmaking a string of large SaaS-model acquisitions -solutions which sit around the core ERP business,thereby increasing the level of subscription revenueswithin the business without launching a full scaleattack on the cash cow.

Transactions have included SAP’s $4.3bn acquisitionof e-procurement specialist Ariba, its $3.4bnacquisition of HCM vendor SuccessFactors, andOracle’s acquisition of Taleo, another HCM specialist,for $1.9bn.

Like its larger ERP rivals, Access has chosen the routeof establishing its own platform but also of acquiringSaaS point solutions to start its shift towards a Cloudmodel. Tossell adds: “We asked ourselves what morecan we put on our Cloud platform and what wouldwe need to acquire to achieve our wider goals.”

One such deal was its acquisition of French businessintelligence provider Prelytis, its first move into theSaaS market. Prelytis’ LiveDashBoard softwareprovides Access customers with a new dimension forviewing their management information on whateverplatform they choose - be it laptop, smartphone,tablet or desktop. Such real-time information is seen

as increasingly essential when it comes to runningbusinesses in today’s complex technical world,allowing managers to filter data easily to reviewtrends and act upon information.

On its own platform, the business has launchedaCloud Insight Finance which provides collaborativebusiness intelligence on the move from any device.The console was the first in a series of out-of-the-boxapplications for Access’ SaaS-based businessintelligence solutions. Adds Tossell: “It allows financeprofessionals to instantly view key KPIs and up-to-date information on the financial position within thebusiness. Having ready access to core KPIs is essentialto get to the heart of the numbers and makeinformed decisions.” Integration with other Accesssoftware solutions means that such data can bequickly turned into dashboards, graphs and charts too.

Tossell sees the SaaS suite of products as being key toAccess’ move into other new markets too. “Rightnow we are starting to look at markets such as multi-channel retail and e-commerce. This is a very excitingtime for us. We are not limited by funding, the banksare knocking on my door, and we will look at any sizedeal which is a great place to be. I can easily see ushitting £70m turnover with 10-15 per cent ofrevenues coming from SaaS.”

ENTERPR I S E R E SOURCE P LANN ING14

With its roots in supplying software to the UK retailsector these are, unsurprisingly, tough times for atleast one part of K3’s business. “Quite frankly highstreet retail is a pretty horrible place to be right now,”admits Chief Executive Andy Makeham. “But I wouldalso add that retail is the only space that is difficult forus right now. Everything else is flying. Take UKmanufacturing, that’s doing really well which mightcome as a surprise to some people.”

Makeham says retail is tough for the likes of K3 -which today has more than 3,000 customers in thesupply chain management industry, focused on themanufacturing, retail and distribution sectors -because when times are tough the FD is top of thedecision-making chain, rather than the sales director.“Right now it’s the FD that is saying ‘let’s see how nextmonth’s results come out’. We are finding it slow andthere is a lot of slippage in decisions.”

On the retail side of his business Makeham’s bigchallenge is to convince traditional retailers of theurgency and importance of moving to effective multi-channel ERP solutions right now, despite the hit on thebottom line. “Put simply they cannot afford not to doit. What you have to remember is that internet sellingonly really took off about five years ago, and in theearly days a lot of retailers quite often had a separatebrand online because they either didn’t trust orbelieve in the internet. Multi-channel only took off afew years ago once the technology caught up, and it isonly now that proper multi-channel retail systems aretruly becoming available.

“What we are providing is a complete retail system. In the old days companies would have many separateIT systems and trying to get them to join up andintegrate all the data was very difficult. That is the key to our products, they provide one database soyou can see a complete view of the business and the customer.”

Makeham says many retailers still struggle to take inthis “360 degree view” of the customer, somethingwhich technology can now enable them to do. “If you are buying something online the trick for theretailer is to know exactly what that customer hasalso been buying in their store and their entirespending history. That is the real holy grail forretailers, that’s their nirvana.”

To help deliver that view for customers K3 is nowsignificantly building upon its existing relationship withMicrosoft in a bid to become a true global player inthe multi-channel space. K3’s business model is basedon sales and maintenance of Microsoft, SYSPRO andSage software, with additional K3 IP tailoring theproduct to specific markets. K3 is already a partnerfor Microsoft’s Dynamic NAV ERP product for mid-sized businesses, a partnership that came aboutthrough K3’s acquisition of Pebblestone in 2010.

Microsoft has now launched a new enterprise solutionDynamics AX aimed at mid-sized to larger businesses,and K3 is working to unite Pebblestone’s wholesaleand K3’s retail solutions on AX, combining them in itsGemstone product which will be distributed globallyby Microsoft channels.

MUlti-CHAnnelsolUtions

In today’s market, companies have to get their multi-channel offering rightor it could cost them their business. We caught up with two leadingplayers in the retail ERP space to hear the challenges they face.

Makeham is spending £3m on the system which hasthe potential to turn K3 into a true global player. “AX is basically Microsoft’s new big shiny toy and thecompany has really changed the game by introducingthis new product at the top end of the market. We will effectively be Microsoft’s ‘go-to-market’partner. The big challenge right now is that AX is afairly new product and does not have many referencecustomers in retail so the absolute key for us is togain more customers. We have closed a few deals and it gets easier month by month, but it is still challenging.”

Makeham says existing K3 customers, typically turningover less than £50m, will have no need to changetheir systems from the NAV product. “AX is verymuch aimed at bigger players, those spending morethan £500,000 a year on IT. With Gemstone we willhave global coverage from day one as the product isrolled out.”

Meanwhile Makeham is equally excited about thecompany’s continued growth in its other markets suchas manufacturing. “UK manufacturing keeps on buyingmore from us. What is interesting is that as thesector has manufactured more abroad so it has hadto become more efficient at handling distributionchannels. Because manufacturers are increasinglymaking products offshore and doing the design anddevelopment work over here, we have had to change the way our products work to reflect thosechanges too.”

“Multi-channel only took off a few years ago once the technology caughtup, and it is only now that proper multi-channel retail systems are trulybecoming available.”

Andy Makeham, K3

A CLEARWATER TMT TEAM REPORT 15

MAginUsBefore the days of ‘multi-channel’ were born thevast majority of retailers had little need formultiple sales channels so the likes of ERPspecialist Maginus were serving a very nichemarket. Today, as chief executive Simon Weeksaffirms, it’s a very different story. “When westarted out there weren’t many doing what wedo. Now there are a lot of people trying to getinto our market.”

However Weeks says although every retailerwants to have a multi-channel proposition thesedays, there are not many single providers theycan go to which can provide both back officeand e-commerce solutions like Maginus. “Wehave all the practical experience here, and alsothe scars from having grown up with ourcustomers in delivering the technical solutionsthey have been asking for.”

Just like Makeham at K3, Weeks admits thoughthat times remain tough in retail. “Quite simplythere are fewer projects out there. We have agreat product but the reality is that fewcompanies in this climate have been changingtheir back office solutions wholesale. That said,retailers know that when it comes to onlinethere is still positive growth out there, and fortheir online offering to be up to scratch theyneed back office solutions that can cope.Companies know that they have got to get theirmulti-channel right or it might cost them theirbusiness full stop.”

Maginus has grown on the back of its own ERPsoftware, but like its main rivals it collaborates asnecessary with bigger players such as Microsoft. AsWeeks adds: “It’s a difficult place to be writing yourown software when you are competing with thelikes of Microsoft which can throw billions at it.”

That said, considerable R&D investment in itsown range of products continues to bear fruitfor Maginus. “Large companies tend to buyMicrosoft products but we have an existingcustomer base in the mid-market which willtend to buy our own product too.”

ENTERPR I S E R E SOURCE P LANN ING16

privAte plAyers

The attractions of the ERP sector are perfectlydemonstrated by Lyceum Capital’s investment twoyears ago in the Access Group (see page 12) sincewhen Lyceum has embarked on an aggressive buy-and-build strategy.

As Lyceum Investment Director Martin Wygasexplains: “For us the appeal of Access was very clear.It has large chunks of recurring revenues and there isa good annuity stream coming off it, so the business ishighly cash generative. In some software businesseschurn can be an issue but with Access the churn wasalready low when we bought it. The business also sitsat the lower end of the mid-market and we like thatspace as it is still quite fragmented, while anotherattraction was the company’s history. In the past it hadbeen run fairly conservatively and that was attractiveto us in terms of its growth potential.”

Wygas adds that there is significant mileage in termsof the customer base too. “Access has a client base ofaround 4,500 and not every single customer hasevery single product so there is a huge opportunityto exploit there. We ourselves at Lyceum are in many

ways a typical client for Access so when we took alook at the kit ourselves and really liked the products,that told us something. We wouldn’t claim to begreat software experts but you can tell when aproduct fits the bill.”

In terms of the wider ERP market Wygas believesthere is now a real opportunity for people who cansell well vertically. “The key for PE is to find a businessthat has not sold well vertically. ERP is a very analyticalindustry and if management teams are makingoperational improvements then these can bemeasured very clearly via ERP systems. You can tracktheir effect month on month very easily, you can seethe numbers. In this present market, where there is adegree of market uncertainty in many sectors,businesses like having a clear set of metrics and clearreporting systems in place.”

The point is echoed by Alex King, head of the TMTteam at HgCapital which has also been particularlyactive in the ERP space in recent years. Says King: “It’sa market which continues to be very attractive to us,not least because of the market penetration.

Company

Eque2

Iris Software Group

Access UK

M-hance

Kerridge Commercial Systems

Integrity Software

PE backer

ISIS Equity Partners

HgCapital

Lyceum Capital

Better Capital

NVM Private Equity

Graphite Capital

Date of investment

April 2013

December 2011

March 2011

September 2010

March 2010

July 2005

PE-backed ERP investments in the UK

Given the ERP sector’s strong revenue streams, recurringrevenues and market fragmentation, it remains a hotspot forPrivate Equity players.

A CLEARWATER TMT TEAM REPORT 17

“What we have to remember is that this is still a veryyoung industry and the extent to which software hastruly penetrated our lives remains limited.

“Although most companies use computers toorganise their business in some way, just how co-ordinated are those systems in practice? Even largecompanies will still have branch offices where theyprepare tax returns on a spreadsheet. So there isplenty of unit growth in the industry for some time tocome. Even the big companies can still see thatgrowth potential.”

King says another big attraction is the disruptive shiftfrom on-premise to software over the internet. “If youare a company only selling desktop software thenfrankly you have a problem. Customers aredemanding an increased amount of products to besold online and like subscription pricing models whichgive them clear numbers and no big upfront fees. Weexpect quite a bit of fallout in the market over thenext few years as anyone without subscription pricingmodels will really struggle. The largest players in ERP,SAP and Oracle, are hedging their bets today, havingmade very expensive acquisitions in the SaaS marketwhilst also continuing to enjoy large cashflows fromthe traditional client/server market.”

King adds that one of the characteristics of the ERPmarket at present is the big spectrum it encompasses.“You have some companies that have been around along time doing what they do and who have beenvery loathe to move to internet software models. Atthe other end you have new entrants who have onlydeveloped online services but who don't yet havemany customers. Although the market for raisingcapital is bullish for these new entrants, at some pointthey will have to show stronger revenues and that isstill some way off for a lot of these companies.”

Given the continued pressures on the UK and widerglobal economy, Wygas adds that take-up of Cloudsystems has not been as widespread as some thoughteither. “We actually like the Cloud and SaaS spacegiven its disruptive nature. But we are finding thatcustomers invariably don't want to switch everythingover to a SaaS model in one go. One of the keypoints about ERP is its ability to configure products to

the particular needs of a company to help driveefficiencies. Ultimately FDs and HR directors wantspecific things which they know can work for them.”

Hg itself was involved in one of the biggest UK ERPdeals of the year to date when it sold ComputerSoftware Holdings (CSH) to the Advanced ComputerSoftware Group, a leading provider of healthcare andbusiness management software and services, for£110m. CSH is a leading provider of accounting andback office software to the UK professional services,CRM and Not-For-Profit (NFP) markets.

HgCapital originally acquired CSH as part of itspurchase of the Iris Software Group in 2011 and hasnow succeeded in separating CSH out from Iris andselling it on to a strategic buyer. The sale wasHgCapital’s third successful exit in the TMT sector inthe last three years and followed successfulrealisations of Nordic SME software provider Visma in2010 and the sale of SiTel in 2011. HgCapital hadactually first invested in Iris back in 2004 and King saysthey reinvested in the company because of itscontinued growth. “The business continued to growto a point where the price worked for us as a buyer.”

Wygas believes that a lot of ERP businesses will cometo market over the next few years. “I think the key fora lot of companies at the moment in this economicclimate is to get another good year or two of tradingbehind them. Our own pipeline at Access iscontinuing to grow month on month, we have neverhad to turn the taps off. We still have a good level ofdemand in the business no matter what is happeningin the wider economy which must come down to thequality of the product. Customers can see thebenefits of embracing these solutions, they see thebenefits paying for themselves.

“For us the important thing is finding the business atthe right point in its trajectory. We are not aboutinvesting in start-ups but working with establishedbusinesses which, with extra investment, have thepotential to become market leaders.”

“If you are a company only selling desktop software then frankly you have aproblem. Customers are demanding an increased amount of products to besold online and like subscription pricing models which give them clearnumbers and no big upfront fees.”

Alex King, HgCapital

ENTERPR I S E R E SOURCE P LANN ING18

Even by Constellation’s standards, 2012was a particularly active year on the M&Afront. The Toronto-based business acquiredsome 35 companies during the year, takingits tally since 1995 to 170. As JohnBillowits, CEO of Constellation operatingcompany Vela Software, alludes: “Last yearwas a very good year for us, not only didwe acquire a number of owner-managedbusinesses but we also picked up a coupleof larger deals off corporates too.”

It is precisely these two types of vendors thathave fuelled Constellation’s voracious dealappetite. As Billowits continues: “We findboth types a particularly rich seam,” he says.“If you take owner managers then what wetypically find is that a lot of these businessesget to a certain size and then tend to plateauoften because their market is actually limited.Funding sources to get to that next stage canbe limited too. For instance they cannot reallyaccess the Private Equity (PE) marketbecause they don’t have the size and PEcannot put debt into the business.”

Billowits says he is more than happy towork with these companies and help themboth improve their operations and graspthe wider opportunities. “We understandtheir growth trajectory and also see themas attractive investments, especiallybecause customers are very loyal in thesebusinesses too. Once a customer finds anIT solution that works they tend to staywith you for a very long time. You can helpcustomers solve solutions.”

In terms of any sector approach, Billowits saysConstellation’s acquisition strategy is moreopportunistic. “We are interested in marketssuch as pharmaceuticals, financial services andinsurance, but we don’t tend to go out andsay we will specifically buy this or that.”

Billowits insists that the businesses are notacquired simply to make synergies. “People inthe companies we acquire are so specialistthat we see little benefit in consolidating whatthey do. You might save a bit of cost in theshort-term but you always risk losingcustomer relationships. What we do set outto do though is share business practices in awhole host of areas. We always pay cash andbecause of our track record these businessescan look around and understand what we dobefore doing the deal. They are often quiteconservative businesses seeing single digitgrowth, and in markets where customers arebuying large IT systems and are keeping themfor a long time, maybe 20 to 30 years.”

Billowits makes the point that for thesesorts of customers replacing their entiresystems with Cloud-based solutions issimply unrealistic. “It can be a lot easier toupgrade departmental solutions one at atime. However in my view the uptake ofCloud services for enterprise-widesolutions seems to be much less thanwhat people thought it would be.”

In terms of picking up investments fromcorporates, Billowits says this invariablyfollows on from businesses deciding theywant to focus on their core business. For

instance last year Constellation’s Volarisoperating division acquired SpecTec, anItalian company that offers remote assetmanagement solutions and other softwareprogrammes for the shipping industry.Although Volaris owns other assetmanagement and logistics businesses, itwas the company’s first foray into theshipping industry. “This was typical of thekind of deal we can pick up,” he adds.

Today around three quarters ofConstellation’s revenues come from NorthAmerica with the remainder from Europe.For instance the company has exposure inthe UK to the local authority leisure sectorand private fitness space, as well as to localauthority transport. Has it seen any impactfrom public sector cuts yet? “At the margin Iwould say we are seeing some impact,” saysBillowits. “However what we have also seenin the last couple of years is departmentsbuying software ahead of anticipated budgetscuts to come further down the line, so theywere closing procurement processes quickly.”

Billowits isn’t phased by further public sectorcuts. “As an IT provider you are ultimatelyhoping you can help the governmentachieve its aims by cost cutting and byproviding greater efficiencies in theirsystems.” However given the wider austerityprogrammes across Europe, Billowits admitsthat the North American market is currentlylooking stronger. “Right now the US feels abetter place to be than Europe. I don’t thinkthe US is on fire but there is more optimismand stability than in Europe.”

reACH for tHe stArs

Consolidation is nothing new in the ERP industry, but with 170 acquisitions under its belt Canadian software giant Constellation Software is a company that thinksparticularly big.

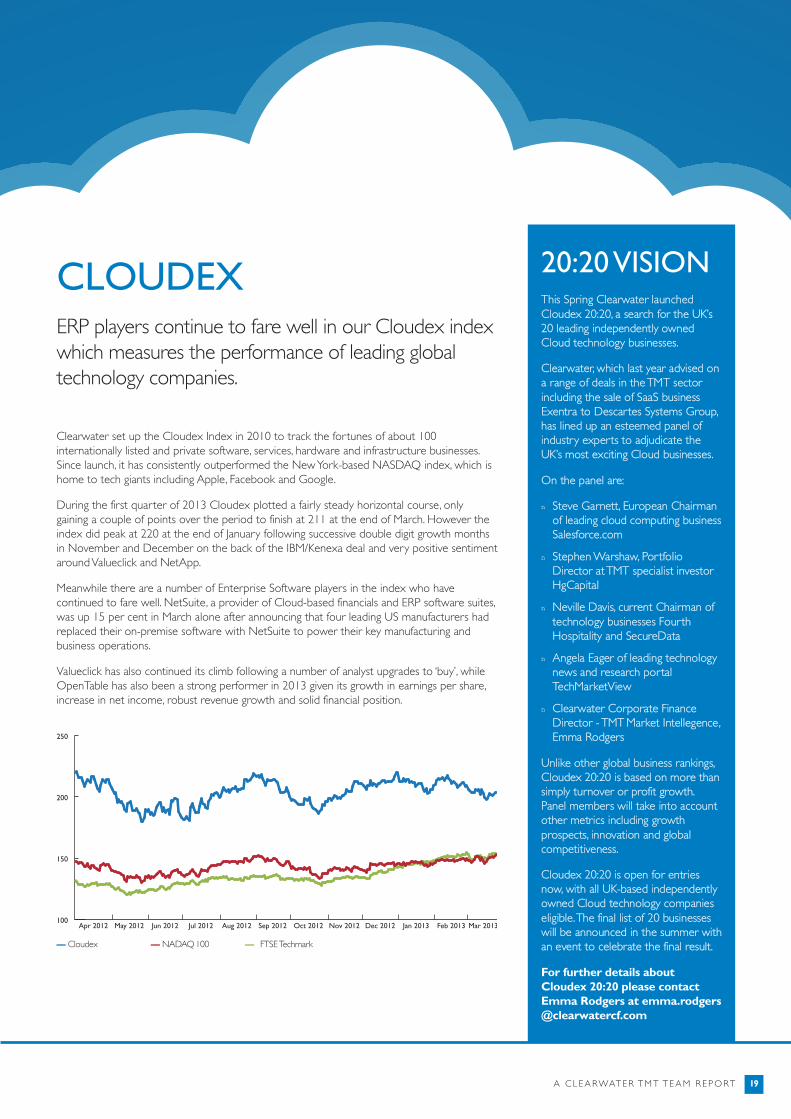

CloUdex

Clearwater set up the Cloudex Index in 2010 to track the fortunes of about 100internationally listed and private software, services, hardware and infrastructure businesses.Since launch, it has consistently outperformed the New York-based NASDAQ index, which ishome to tech giants including Apple, Facebook and Google.

During the first quarter of 2013 Cloudex plotted a fairly steady horizontal course, onlygaining a couple of points over the period to finish at 211 at the end of March. However theindex did peak at 220 at the end of January following successive double digit growth monthsin November and December on the back of the IBM/Kenexa deal and very positive sentimentaround Valueclick and NetApp.

Meanwhile there are a number of Enterprise Software players in the index who havecontinued to fare well. NetSuite, a provider of Cloud-based financials and ERP software suites,was up 15 per cent in March alone after announcing that four leading US manufacturers hadreplaced their on-premise software with NetSuite to power their key manufacturing andbusiness operations.

Valueclick has also continued its climb following a number of analyst upgrades to ‘buy’, whileOpenTable has also been a strong performer in 2013 given its growth in earnings per share,increase in net income, robust revenue growth and solid financial position.

ERP players continue to fare well in our Cloudex indexwhich measures the performance of leading globaltechnology companies.

A CLEARWATER TMT TEAM REPORT 19

20:20 visionThis Spring Clearwater launchedCloudex 20:20, a search for the UK’s20 leading independently ownedCloud technology businesses.

Clearwater, which last year advised ona range of deals in the TMT sectorincluding the sale of SaaS businessExentra to Descartes Systems Group,has lined up an esteemed panel ofindustry experts to adjudicate theUK’s most exciting Cloud businesses.

On the panel are:

n Steve Garnett, European Chairmanof leading cloud computing businessSalesforce.com

n Stephen Warshaw, PortfolioDirector at TMT specialist investorHgCapital

n Neville Davis, current Chairman oftechnology businesses FourthHospitality and SecureData

n Angela Eager of leading technologynews and research portalTechMarketView

n Clearwater Corporate FinanceDirector - TMT Market Intellegence,Emma Rodgers

Unlike other global business rankings,Cloudex 20:20 is based on more thansimply turnover or profit growth.Panel members will take into accountother metrics including growthprospects, innovation and globalcompetitiveness.

Cloudex 20:20 is open for entriesnow, with all UK-based independentlyowned Cloud technology companieseligible. The final list of 20 businesseswill be announced in the summer withan event to celebrate the final result.

For further details aboutCloudex 20:20 please contactEmma Rodgers at [email protected]

100

150

200

250

Apr 2012 May 2012 Jun 2012 Jul 2012 Aug 2012 Sep 2012 Oct 2012 Nov 2012 Dec 2012 Jan 2013 Feb 2013 Mar 2013

–– Cloudex –– NADAQ 100 –– FTSE Techmark

CoMpAny indexA guide to the top 10 global ERP companies

Location: Germany

Revenue £m2012 13,5912011 12,1912010 11,215

Revenue CAGR (2010-2012) 7%

EBIT £m2012 3,2032011 4,084

EBIT CAGR (2010-2012) -8%

Number of employees: 61,344

Principle areas of business: Enterprise Software & Computer Services

Segmental revenue breakdown (2012)Software and Software related services 81%Professional and other services 19%

Geographical revenue breakdown (2012)Germany 16%Japan 5% USA 26% Asia Pacific 11% Other Americas 10% Other 32%

Company description: SAP is an enterprise application softwaredeveloper which has the aim of helpingcompanies run better. From back office toboardroom, warehouse to storefront,desktop to mobile device, SAP software isgeared towards helping people andorganisations work together more efficiently.

It operates in more than 120 countries andhas in excess of 190,000 customers.

Recent M&A activity: Acquired Datango AG, an elearning softwaredeveloper in February 2012.

Acquired Syclo LLC, a US mobile enterpriseplatform and application developer in June 2012.

Sold its stake in Tea Leaf Technology Inc, aweb application software developer, in June2012.

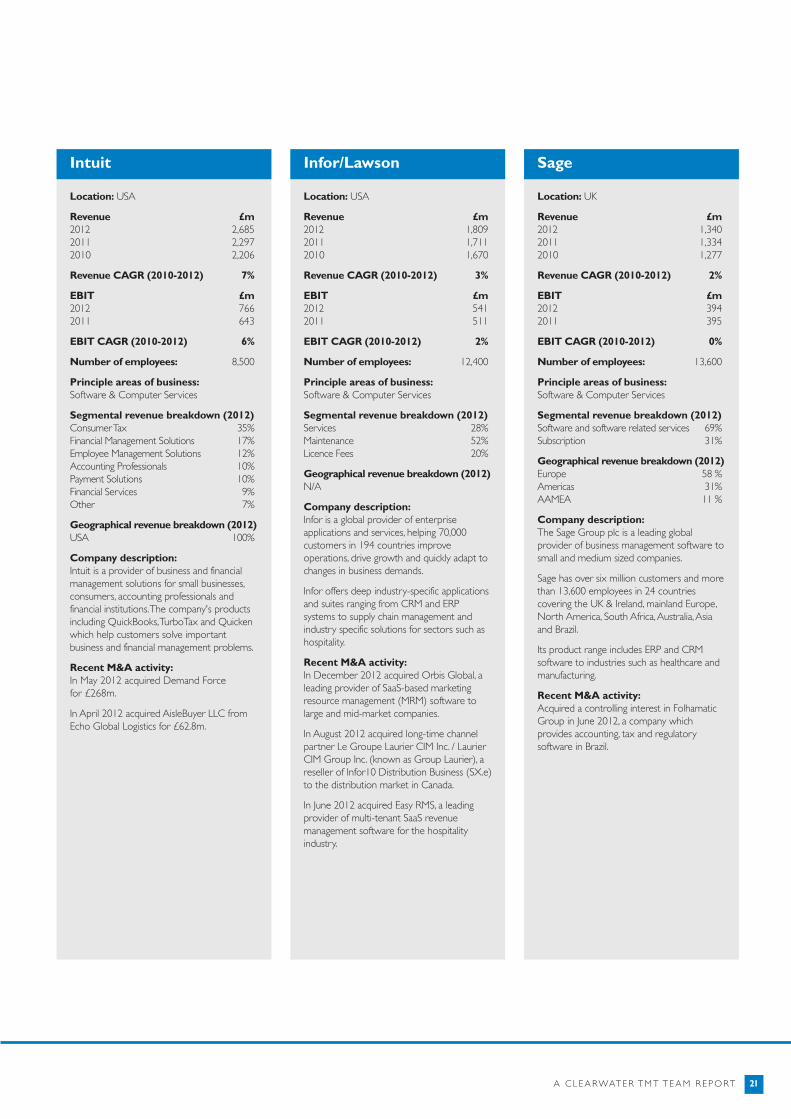

SAP

Location: USA

Revenue £m2012 24,0172011 23,0472010 17,352

Revenue CAGR (2010-2012) 11%

EBIT £m2012 10,7782011 9,055

EBIT CAGR (2010-2012) 6%

Number of employees: 115,000

Principle areas of business: Software & Computer Services

Segmental revenue breakdown (2012)Software Licence Updates and Support 43%New Software Licences 27%Services Business 13%Hardware Products 10%Hardware Support 7%

Geographical revenue breakdown (2012)USA 42%UK 6%Japan 5%Germany 4%Canada 3%Australia 3%France 3% Other 34%

Company description: Oracle is a provider of enterprise software and computer hardware products and services.

Recent M&A activity: In December 2012 acquired DataRaker, aprovider of a Cloud-based analytics platform.

In November 2012 acquired Instantis, aprovider of Cloud-based and on-premiseproject portfolio management solutions.

In July 2012 acquired Skire, a provider ofcapital programme management and facilitiesmanagement applications.

Oracle

ENTERPR I S E R E SOURCE P LANN ING20

Location: USA

Revenue £m2012 45,5972011 45,3332010 40,388

Revenue CAGR (2010-2012) 4%

EBIT £m2012 13,4602011 13,176

EBIT CAGR (2010-2012) 1%

Number of employees: 94,000

Principle areas of business: Software & Computer Services

Segmental revenue breakdown (2012)Microsoft Business Division 32%Windows and Windows Live Division 25%Server and Tools 25%Entertainment and Devices Division 13%Online Services Business 5%

Geographical revenue breakdown (2012)United States 53%Other 47%

Company description: Microsoft is involved in developing, licensingand supporting a range of software productsas well as designing and selling hardware.

The company is divided into five businesssegments: Windows division; Server andTools; Online services; Microsoft BusinessDivision; and Entertainment and DevicesDivision.

It is the world's largest software maker by revenues.

Recent M&A activity: In July 2012 acquired Edgewater Fullscope'sProcess Industries software and IP as well asYammer Inc.

In October 2012 acquired Phone Factor Inc.

Microsoft

A CLEARWATER TMT TEAM REPORT 21

Location: UK

Revenue £m2012 1,3402011 1,3342010 1,277

Revenue CAGR (2010-2012) 2%

EBIT £m2012 3942011 395

EBIT CAGR (2010-2012) 0%

Number of employees: 13,600

Principle areas of business: Software & Computer Services

Segmental revenue breakdown (2012)Software and software related services 69%Subscription 31%

Geographical revenue breakdown (2012)Europe 58 %Americas 31%AAMEA 11 %

Company description: The Sage Group plc is a leading globalprovider of business management software tosmall and medium sized companies.

Sage has over six million customers and morethan 13,600 employees in 24 countriescovering the UK & Ireland, mainland Europe,North America, South Africa, Australia, Asiaand Brazil.

Its product range includes ERP and CRMsoftware to industries such as healthcare andmanufacturing.

Recent M&A activity: Acquired a controlling interest in FolhamaticGroup in June 2012, a company whichprovides accounting, tax and regulatorysoftware in Brazil.

Sage

Location: USA

Revenue £m2012 1,8092011 1,7112010 1,670

Revenue CAGR (2010-2012) 3%

EBIT £m2012 5412011 511

EBIT CAGR (2010-2012) 2%

Number of employees: 12,400

Principle areas of business: Software & Computer Services

Segmental revenue breakdown (2012)Services 28%Maintenance 52%Licence Fees 20%

Geographical revenue breakdown (2012)N/A

Company description: Infor is a global provider of enterpriseapplications and services, helping 70,000customers in 194 countries improveoperations, drive growth and quickly adapt tochanges in business demands.

Infor offers deep industry-specific applicationsand suites ranging from CRM and ERPsystems to supply chain management andindustry specific solutions for sectors such ashospitality.

Recent M&A activity: In December 2012 acquired Orbis Global, aleading provider of SaaS-based marketingresource management (MRM) software tolarge and mid-market companies.

In August 2012 acquired long-time channelpartner Le Groupe Laurier CIM Inc. / LaurierCIM Group Inc. (known as Group Laurier), areseller of Infor10 Distribution Business (SX.e)to the distribution market in Canada.

In June 2012 acquired Easy RMS, a leadingprovider of multi-tenant SaaS revenuemanagement software for the hospitalityindustry.

Infor/Lawson

Location: USA

Revenue £m2012 2,6852011 2,2972010 2,206

Revenue CAGR (2010-2012) 7%

EBIT £m2012 7662011 643

EBIT CAGR (2010-2012) 6%

Number of employees: 8,500

Principle areas of business: Software & Computer Services

Segmental revenue breakdown (2012)Consumer Tax 35%Financial Management Solutions 17%Employee Management Solutions 12%Accounting Professionals 10%Payment Solutions 10%Financial Services 9%Other 7%

Geographical revenue breakdown (2012)USA 100%

Company description: Intuit is a provider of business and financialmanagement solutions for small businesses,consumers, accounting professionals andfinancial institutions. The company's productsincluding QuickBooks, TurboTax and Quickenwhich help customers solve importantbusiness and financial management problems.

Recent M&A activity: In May 2012 acquired Demand Force for £268m.

In April 2012 acquired AisleBuyer LLC fromEcho Global Logistics for £62.8m.

Intuit

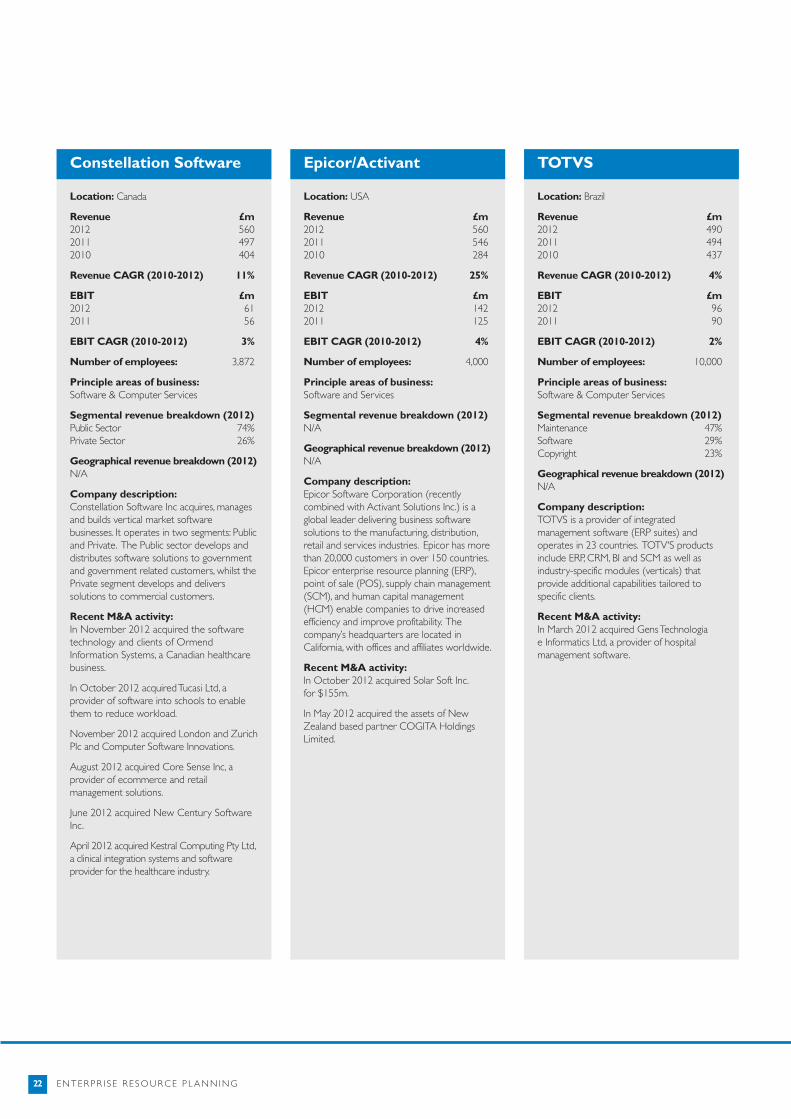

Location: Canada

Revenue £m2012 5602011 4972010 404

Revenue CAGR (2010-2012) 11%

EBIT £m2012 612011 56

EBIT CAGR (2010-2012) 3%

Number of employees: 3,872

Principle areas of business: Software & Computer Services

Segmental revenue breakdown (2012)Public Sector 74%Private Sector 26%

Geographical revenue breakdown (2012)N/A

Company description: Constellation Software Inc acquires, managesand builds vertical market softwarebusinesses. It operates in two segments: Publicand Private. The Public sector develops anddistributes software solutions to governmentand government related customers, whilst thePrivate segment develops and deliverssolutions to commercial customers.

Recent M&A activity: In November 2012 acquired the softwaretechnology and clients of OrmendInformation Systems, a Canadian healthcarebusiness.

In October 2012 acquired Tucasi Ltd, aprovider of software into schools to enablethem to reduce workload.

November 2012 acquired London and ZurichPlc and Computer Software Innovations.

August 2012 acquired Core Sense Inc, aprovider of ecommerce and retailmanagement solutions.

June 2012 acquired New Century SoftwareInc.

April 2012 acquired Kestral Computing Pty Ltd,a clinical integration systems and softwareprovider for the healthcare industry.

Constellation Software

Location: Brazil

Revenue £m2012 4902011 4942010 437

Revenue CAGR (2010-2012) 4%

EBIT £m2012 962011 90

EBIT CAGR (2010-2012) 2%

Number of employees: 10,000

Principle areas of business: Software & Computer Services

Segmental revenue breakdown (2012)Maintenance 47%Software 29%Copyright 23%

Geographical revenue breakdown (2012)N/A

Company description: TOTVS is a provider of integratedmanagement software (ERP suites) andoperates in 23 countries. TOTV'S productsinclude ERP, CRM, BI and SCM as well asindustry-specific modules (verticals) thatprovide additional capabilities tailored tospecific clients.

Recent M&A activity: In March 2012 acquired Gens Technologia e Informatics Ltd, a provider of hospitalmanagement software.

TOTVS

ENTERPR I S E R E SOURCE P LANN ING22

Location: USA

Revenue £m2012 5602011 5462010 284

Revenue CAGR (2010-2012) 25%

EBIT £m2012 1422011 125

EBIT CAGR (2010-2012) 4%

Number of employees: 4,000

Principle areas of business: Software and Services

Segmental revenue breakdown (2012)N/A

Geographical revenue breakdown (2012)N/A

Company description: Epicor Software Corporation (recentlycombined with Activant Solutions Inc.) is aglobal leader delivering business softwaresolutions to the manufacturing, distribution,retail and services industries. Epicor has morethan 20,000 customers in over 150 countries.Epicor enterprise resource planning (ERP),point of sale (POS), supply chain management(SCM), and human capital management(HCM) enable companies to drive increasedefficiency and improve profitability. Thecompany’s headquarters are located inCalifornia, with offices and affiliates worldwide.

Recent M&A activity: In October 2012 acquired Solar Soft Inc. for $155m.

In May 2012 acquired the assets of NewZealand based partner COGITA HoldingsLimited.

Epicor/Activant

A CLEARWATER TM T TEAM RE PORT 23

Location:Netherlands

Revenue £m2012 3932011 3812010 378

Revenue CAGR (2010-2012) 1%

EBIT £m2012 242011 42

EBIT CAGR (2010-2012) N/A

Number of employees: 4,090

Principle areas of business: Software & Computer Services

Segmental revenue breakdown (2012)N/A

Geographical revenue breakdown (2012)Netherlands 30%UK 17%Sweden 15%Poland 7%Norway 9%Spain 7%Germany 3%USA 5%Belgium 3%Other 4%

Company description: Unit 4 is a Netherlands based provider ofintegrated business management softwareand related services. The businessspecialisations include ERP for service basedorganisations, human capital management,financial management and expert softwareservices. Its key markets globally includegovernments, non-profit organisations, financialand professional services companies.

Recent M&A activity: In November 2012 it acquired MontananSoftware, an accountancy software developer.

Unit 4

9 Colmore RowBirmingham B3 2BJ

Tel: +44 845 052 0360Fax: +44 845 052 0361

62-65 Chandos PlaceLondon WC2N 4HG

Tel: +44 845 052 0300Fax: +44 845 052 0303

50 Brown StreetManchester M2 2JT

Tel: +44 845 052 0340Fax: +44 845 052 0341

16 The RopewalkNottingham NG1 5DT

Tel: +44 845 052 0380Fax: +44 845 052 0381

ECI Partners

Acquisition of a SaaS provider to thehospitality industry

Clearwater Corporate Finance advisedECI and assisted with negotiations

Fourth Hospitality

Descartes Systems Group, Inc

Disposal of a SaaS model provider ofdriver compliance solutions

Clearwater Corporate Finance advisedthe vendors

Exentra Transport Solutions

WebTrends Corporation

Disposal of a provider of a real-timeweb analytics system

IMAP advised the vendor

Reinvigorate

LDC Private Equity

Acquisition of a leading B2B mobileapplication software developer

Clearwater Corporate Finance advisedthe shareholders

Kirona Solutions

LDC Private Equity

Investment in wireless and fibreinternet service provider

Clearwater Corporate Finance advisedthe shareholders

Metronet

Aures Technologies

Disposal of a supplier of touchscreenelectronic point of sale terminals and systems

Clearwater Corporate Finance advisedthe vendors

J2 Retail

Royal Imtech NV

Acquisition of integrated control andreal-time IT solutions provider

Clearwater Corporate Finance advisedthe purchaser

Capula

CompuGain, Inc.

Acquisition of a provider of decisioningsupport software solutions

IMAP advised the purchaser

Overture Technologies

ISIS Private Equity

MBO of a provider of ERP solutions tothe construction sector from SageGroup plc

Clearwater Corporate Finance advisedthe management team

Eque2

w w w. C l e A rwAt e r i n t e r n At i o n A l . C o M